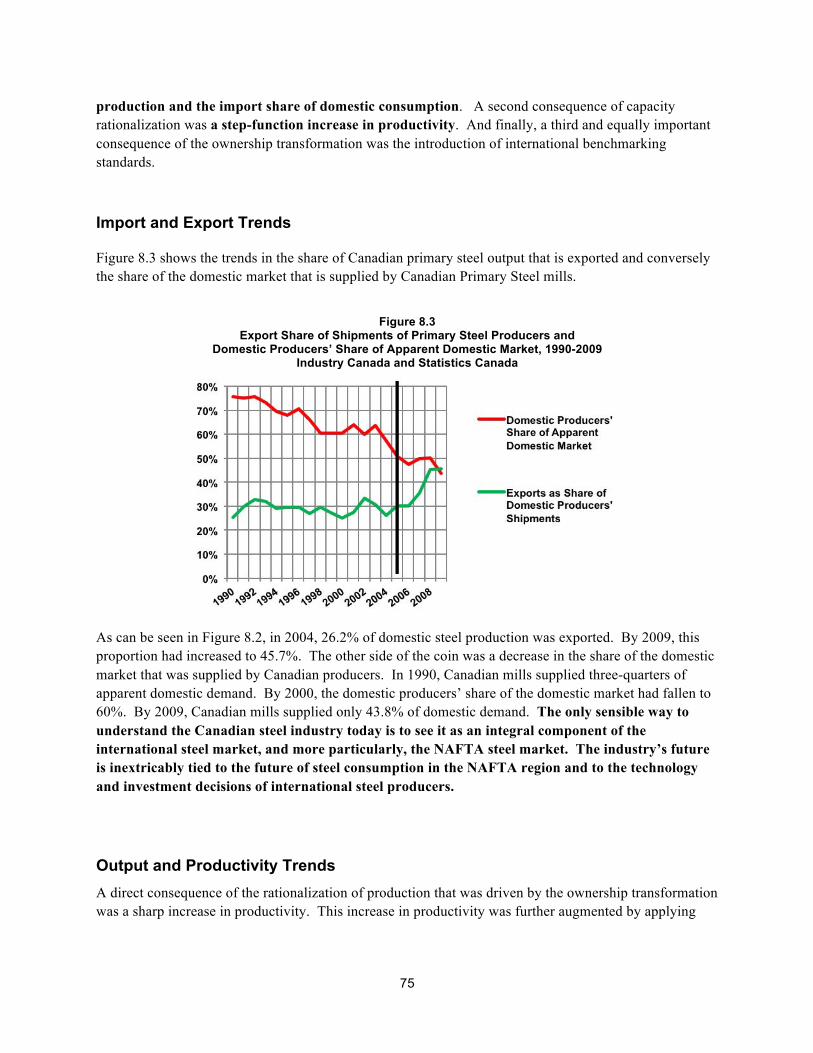

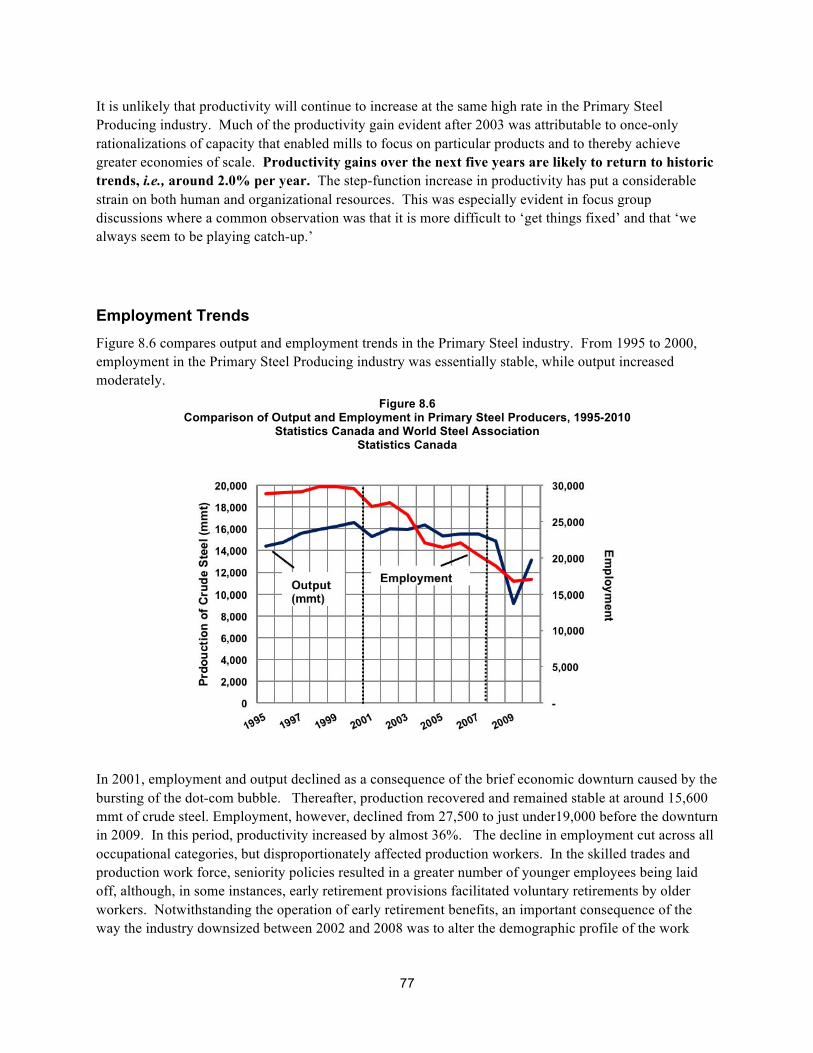

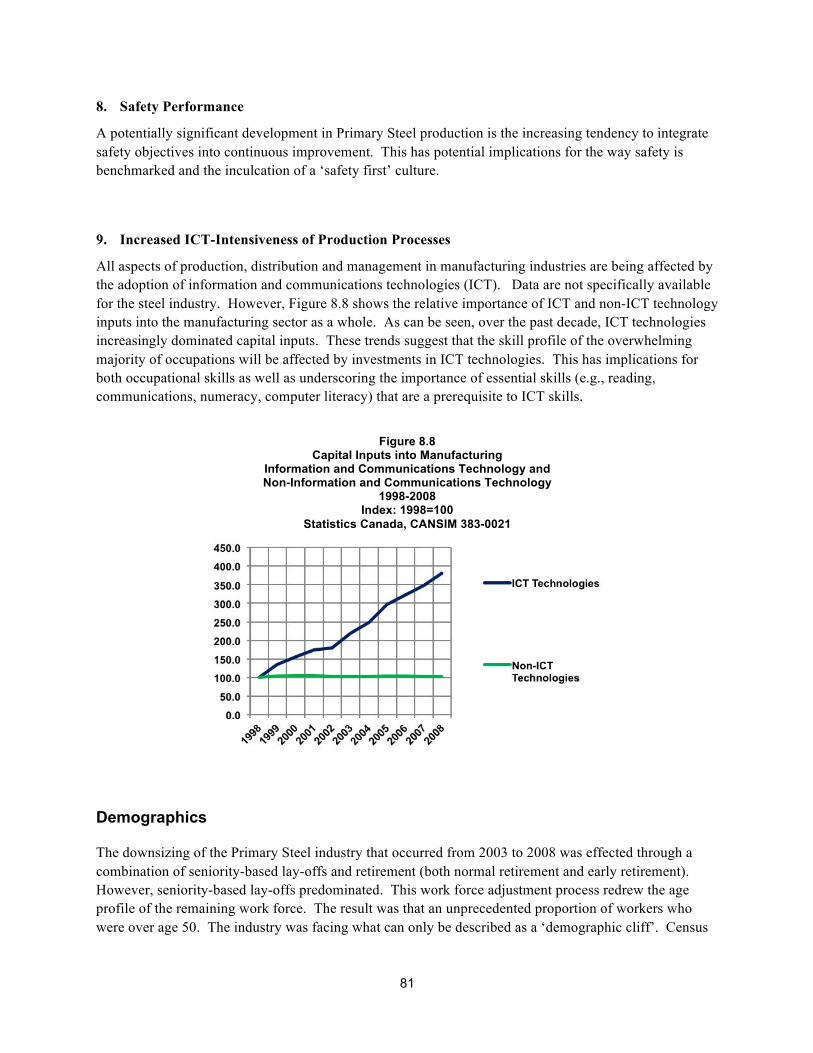

2010 sector study_report_english

DESCRIPTION

TRANSCRIPT

http://www.cstec.ca

Human Resources in the Canadian Steel Sector Final Report March 2011

Human Resources in the Canadian Steel Sector

Final Report

March 2011

Prism Economics and Analysis

Prism Economics and Analysis Suite 404

160 Eglinton Avenue East Toronto, ON

M4P 3B5 Tel: (416)-484-6996 Fax: (416)-484-4147

website: www.prismeconomics.com

John O’Grady Partner, Prism Economics and Analysis

Direct Phone: (416)-652-0456 Direct Fax: (416)-652-3083

Email: [email protected] website: www.ogrady.on.ca

Peter Warrian Associate, Prism Economics and Analysis

Direct Phone: (416)-946-8934 Email: [email protected]

1

2

Human Resources in the Canadian Steel Sector Final Report

Table of Contents

Executive Summary 4

Chapter One: Introduction 12

Chapter Two: Overview of the Broader Steel Sector 14

Chapter Three: Drivers of Change in the Broader Steel Sector 21

Chapter Four: Employment Projections 34

Chapter Five: Human Resources Managers Survey 47

Chapter Six: Local Union Leaders Survey 52

Chapter Seven: What We Heard 59

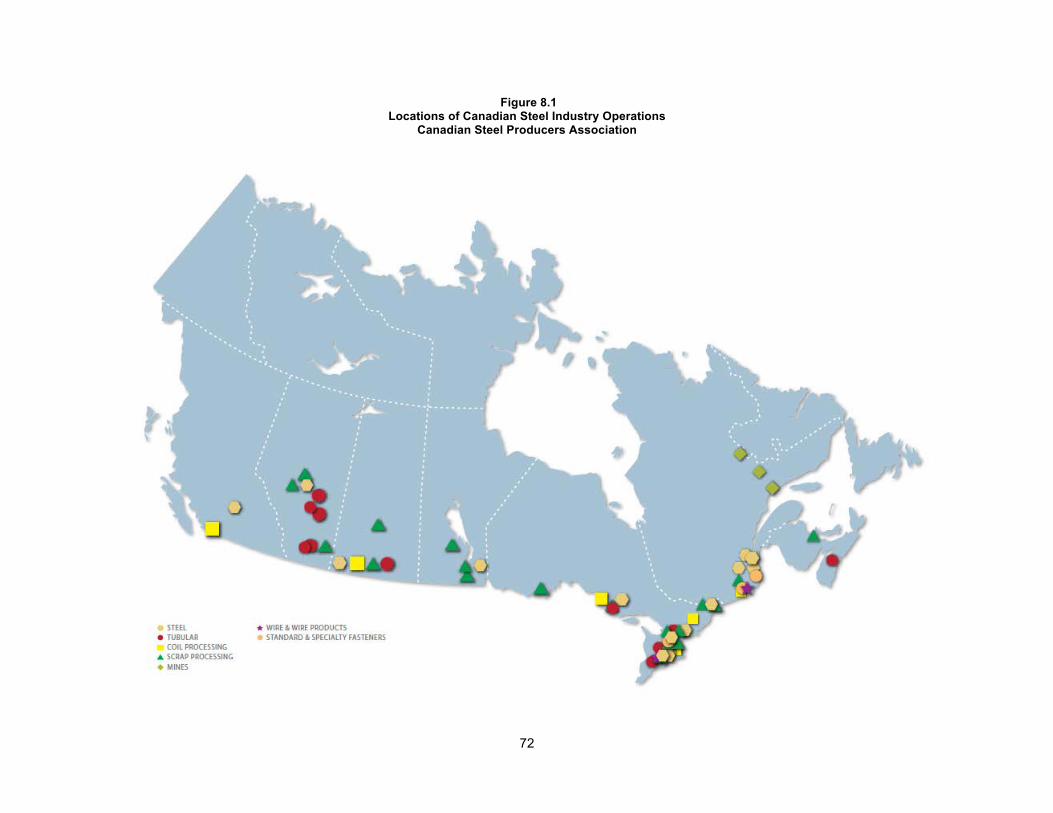

Chapter Eight: Primary Steel Producers 71

Chapter Nine: Foundries 92

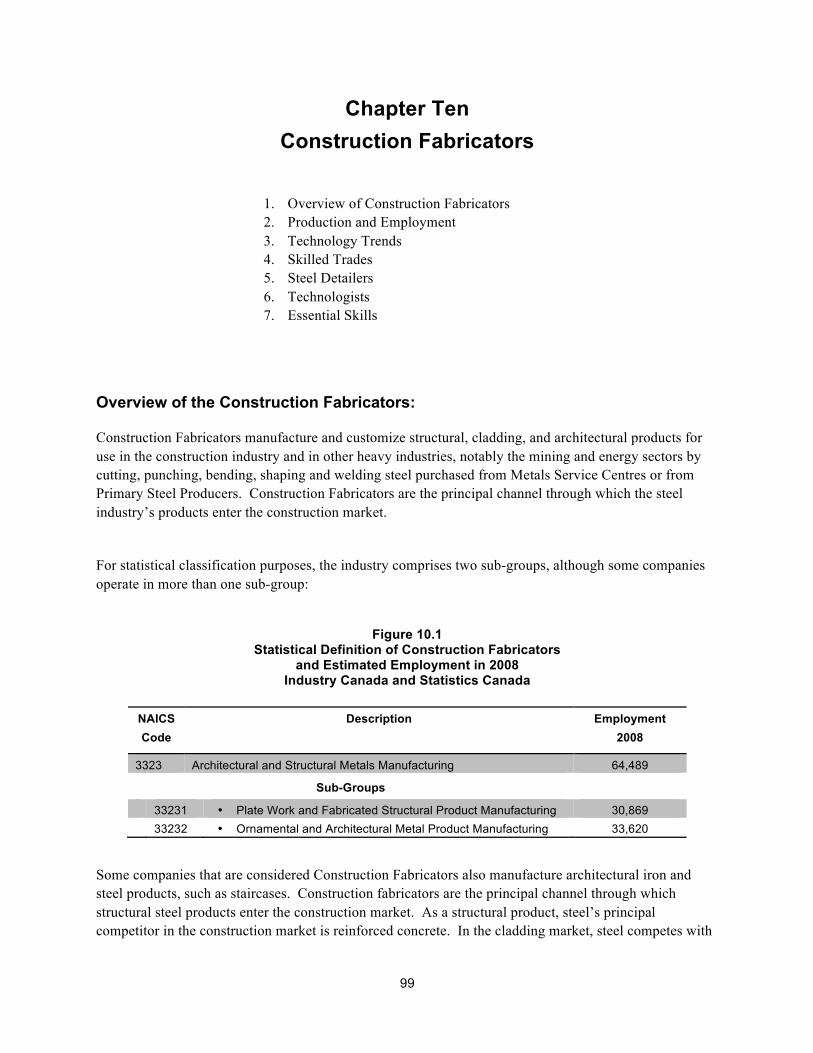

Chapter Ten: Construction Fabricators 99

Chapter Eleven: Metals Service Centres 106

Chapter Twelve: Recommendations 115

Appendices 127

Appendix A: Steering Committee 128

Appendix B: Interviews and Focus Groups 130

Appendix C: Local Union Leader Survey 135

Appendix D: Human Resources Manager Survey 138

3

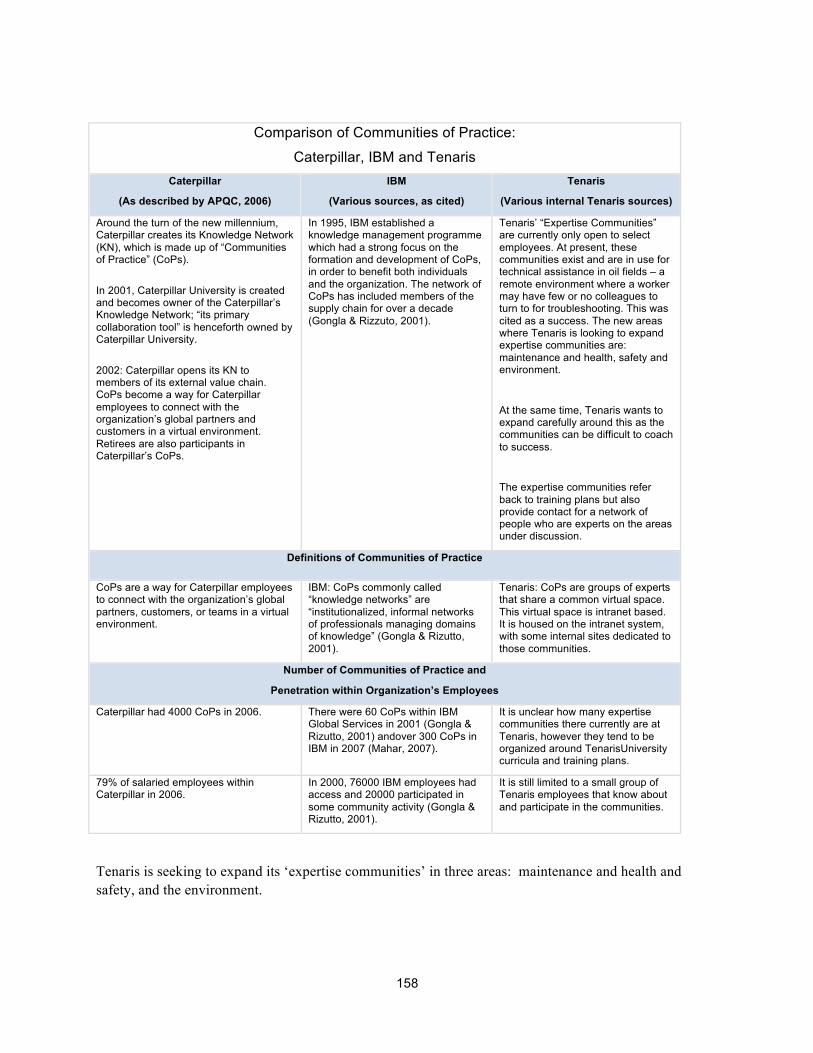

Appendix E: Global Benchmarking Report 141

Part 1: ArcelorMittal Ghent and TenarisDalmine 142

Part 2: Knowledge Management and Knowledge Transfer 148

Part 3: TenarisUniversity 150

References: Human Resources Manager Survey 161

Annex: Human Resources Manager Survey 164

4

Executive Summary Central Message of the Report:

• Leaders in the Steel Sector identify five long-term business and human resources goals: 1. Zero accidents, 2. Zero product defects, 3. 100% reliability for on-time delivery, 4. Ongoing productivity gains, and 5. Supporting more well-paid jobs by securing new and existing markets

based on new products and a reputation for quality and delivery.

• The central finding of this report is that achieving these objectives requires bolstering human resources planning at the sector level and building a stronger training culture in the workplace.

Strengthening Human Resources Planning at the Sector Level:

• Over the next five years, the Broader Steel Sector will need to hire between 19,000 and 29,000 workers. To meet these human resources requirements will require strategies:

(1) to train and recruit between 5,000 and 10,800 skilled tradespersons,

(2) to expand the sector’s involvement in co-op and internship programs for technicians and technologists, and

(3) to deliver career information which attracts the best and most motivated job-seekers

• While employers can meet some of these strategic needs through steps at the company level, it is imperative that industry stakeholders also develop carefully focused sector-based strategies to support company-level human resources planning.

Skilled Trades:

• The most urgent and pressing challenge facing the Steel Sector will be replacing skilled tradespersons who retire. Over the next five years the Broader Steel Sector will need to hire between 5,000 and 10,800 skilled tradespersons.

• There are at least three dimensions to this challenge that need to be taken into account:

First, the Steel Sector cannot count on meeting its future need for skilled tradespersons through ad hoc recruitment or recalling workers who were laid off during the recent

5

downturn. There is a strong likelihood of a systemic shortage of skilled tradespersons in the Canadian economy. The Steel Sector will be in competition with other industries. In many cases, the wage premium which the Steel Sector offered has narrowed such that the Steel Sector’s competitive position in the labour market is not as favourable as it was in previous decades.

Second, as a consequence of the increased competition for the skilled tradespersons, the Steel Sector will need to ramp up its investment in apprenticeship. A successful sector strategy will be central to realizing this investment.

Third, the skill needs of the Steel Sector are evolving as production technology becomes more technologically sophisticated. The historic boundary between technicians/ technologists and skilled tradespersons is blurring. For the Steel Sector this means that there has been and will continue to be an increase in the technology skills required of skilled tradespersons. This implies a need for specialized training that goes beyond established skill standards for tradespersons. Again, this challenge can more effectively be tackled with a sector strategy.

• The Steel Sector, of course, is not alone in facing a growing need to replace retiring skilled tradespersons. Other industries face equally serious challenges. A Steel Sector strategy, therefore, will be far more effective if it is implemented in the context of a national strategy to address the looming shortage of skilled tradespersons.

Technicians and Technologists: Trained for the Steel Sector

• There is no systemic shortage of technicians and technologists. However, companies in the Steel Sector need technicians and technologists who have training and experience in the Steel Sector. As we move forward, there will be a shortage of technicians and technologists with industry training and industry experience that is specific to steel. Only the Steel Sector can solve that problem.

• The key to bridging the gap between college training and industry-specific training and experience is to augment the Steel Sector’s investment in co-op placements and internships. To attract the highest calibre students the Steel Sector must offer an expanded co-op placement program. This requires a sector-based strategy.

Attracting the Best and Most Motivated

• The Steel Sector will be competing with other industries, many of which have already developed sophisticated strategies to support their recruitment efforts.

• The Steel Sector urgently needs to develop a recruitment and career strategy to meet is human resources needs in a labour market that will be significantly more competitive, especially for hiring skilled tradespersons and technicians and technologists with relevant industry experience.

6

• The effectiveness of company recruitment strategies will be significantly leveraged if there is a carefully designed and concurrent sector strategy to deliver career information for targeted occupations.

Strengthening Training Culture in the Workplace

• The Steel Sector needs to strengthen its training culture in the workplace. This was a recommendation from the 2005 sector study. While there has been progress, it has been limited. Changes in the industry since the 2005 study have made it more urgent to strengthen workplace training culture. This report recommends two specific measures to strengthen training culture: benchmarking and joint advisory committees.

• Benchmarking: The Primary Steel Producing industry already has a well-developed strategy for benchmarking production performance. The same strategy can contribute to strengthening training culture. It should be a high priority for CSTEC to implement a benchmarking survey which provides workplaces with the information they need on where they stand in relation to other workplaces, how much (or how little) progress they have made, and how they can strengthen their performance. This benchmarking survey should be the core of CSTEC’s efforts to strengthen its capacity to provide relevant Labour Market Information.

• Joint Advisory Committees: When there is a will to move forward, consultative committees in the workplace can lead to improved performance. In many workplaces, this has been the case for occupational health and safety where joint committees have played a key role in improving health and safety performance. Survey data indicate that consultations on training are common in the Steel Sector, though not universal and are often informal. To strengthen training culture in the Steel Sector, CSTEC should work with stakeholders to establish joint workplace advisory committees on training and development or, if appropriate, to broaden the mandate of existing consultative structures to include training and development.

Building on Human Resources Capacity:

• Knowledge Transfer: Knowledge transfer has emerged as a new challenge for the Steel Sector, primarily in the Primary Steel Producing industry. Knowledge transfer is the transmission of undocumented or tacit workplace knowledge from experienced workers to new hires. There is a significant risk that the retirement wave that is taking place in the Primary Steel Producing industry will remove experience-based knowledge before new employees are hired or fully integrated. A strategy to document and transfer tacit workplace knowledge is essential to ensure that productivity gains achieved in the last five years are not eroded.

• Essential Skills: CSTEC and the Steel Sector need to update their understanding of essential skills to better align with new and emerging workplace realities. The conventional understanding of essential skills encompasses basic reading, verbal communications, and computational skills. In light of the high proportion of the workforce that has not completed high school, essential skills, in the conventional sense, are, and will continue to be a challenge for the Steel Sector. However, new essential skills needs are emerging. These include: supporting apprentices in their classroom training

7

and accelerating the integration of recent immigrants ho have strong technical training, but inadequate language skills.

• The successful implementation of continuous improvement and total productive maintenance also will require new attention to essential skills weaknesses. Gaps in essential skills will impair the sector’s ability to achieve zero accidents and zero defects.

A Call to Action:

• The Steel Sector plays a key role in the Canadian economy. The sector supports over 100,000 direct jobs in Canada and many more jobs which supply the companies that make up the Steel Sector. In many communities, the steel industry is both the lynchpin and the driver of economic development. It is in the interests of every stakeholder in the Steel Sector – companies, workers, communities, and governments – to see a strong and competitive steel industry. Human resources planning and training culture will not achieve that goal on their own. However, a strong and competitive steel industry will not be achieved without bolstering human resources planning at the sector level and a strengthening training culture in the workplace.

• The Steel Sector is changing rapidly under the pressure of globalization and the high Canadian dollar. The Sector does not have the luxury to wait for another five years to take action on human resource planning and strengthening its training culture.

• It is a matter of urgency for the primary stakeholders in the Steel Sector – companies and unions – to focus on the need to bolster their sector-level human resources planning and to concurrently strengthen their workplace training culture. This report documents the changes that make those goals important and proposes a path for achieving them.

Recommendations

Recommendation No. 1 Benchmarking Training and Development

(a) CSTEC should implement an annual benchmarking survey of employers, unions and workers

that tracks indicators of training and professional development. Individual companies should not be identifiable from the survey results. The initial Training and Development Benchmarking Survey should generate base-line data that can be used in assessing subsequent performance.

(b) The annual Training and Development Benchmarking Survey should be at the core of CSTEC’s Labour Market Information services. Survey results should be presented to stakeholders through a webinar and a written report.

8

Recommendation No. 2

Workplace Advisory Committees on Training and Development

CSTEC should work with stakeholders to establish joint workplace-level, advisory committees on training and development or, if appropriate, to broaden the mandate of existing consultative structures to include training and development. In support of this initiative, CSTEC should develop support materials for the workplace parties to assist them in identifying needs and possible resources. Among the training needs that should be considered are:

• essential skills, • apprenticeship, • skilled trades upgrading, and • the skills required to successfully implement continuous improvement and

total productive maintenance.

Recommendation No. 3 Implementing a Career Information Strategy

In collaboration with other partners in the Steel Sector, including the Canadian Steel Producers Association, the Canadian Institute of Steel Construction, the Canadian Foundry Association, and the Canadian Division of the Metal Service Centre Institute, CSTEC should develop:

(a) web-based, career information targeted to students and to young workers who are considering an apprenticeable trade or a career as a technician or technologist,

(b) career information focused on non-traditional sources, including young women, technically trained recent immigrants, aboriginal Canadians and workers who are members of visible minorities.

(c) a social media strategy to reach a broader range of potential steel sector employees and to draw attention to the opportunities in the steel sector

Recommendation No. 4

National Skilled Trades Strategy

(a) CSTEC should continue to develop a National Skilled Trades Strategy, based in part on the success of its pilot program in Hamilton. The strategy should be expanded to include all industries in the Broader Steel Sector. In some regions, to achieve critical mass, the strategy may need to involve other manufacturing industries.

9

(b) The focus of the National Skilled Trades Strategy should be to create regional consortia that will manage the regional design and implementation of the national strategy. Administrative support would be provided by CSTEC through its regional staff. The CMSO should lead the design and implementation of the strategy in Quebec.

(c) CSTEC should develop supplementary curriculum material to strengthen the training of apprentices in their understanding of metallurgy and related topics.

(d) CSTEC’s National Skilled Trades Strategy should cover the full range of skilled trades needed by the Steel Sector. Among the trades which should be included are:

• Industrial Electricians • Industrial Mechanics / Millwrights • Pipefitters • Stationary Engineers1 • Crane Operators • Welders • Other Metal-Working Trades2

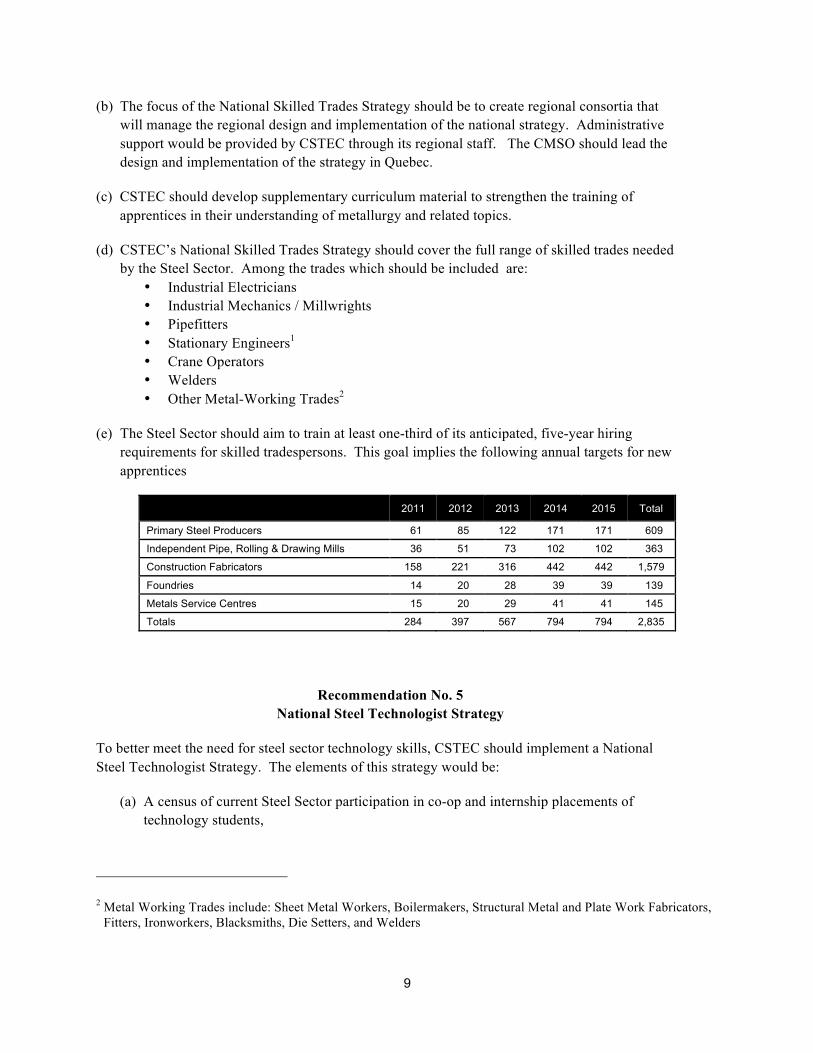

(e) The Steel Sector should aim to train at least one-third of its anticipated, five-year hiring requirements for skilled tradespersons. This goal implies the following annual targets for new apprentices

2011 2012 2013 2014 2015 Total

Primary Steel Producers 61 85 122 171 171 609

Independent Pipe, Rolling & Drawing Mills 36 51 73 102 102 363

Construction Fabricators 158 221 316 442 442 1,579

Foundries 14 20 28 39 39 139

Metals Service Centres 15 20 29 41 41 145

Totals 284 397 567 794 794 2,835

Recommendation No. 5

National Steel Technologist Strategy

To better meet the need for steel sector technology skills, CSTEC should implement a National Steel Technologist Strategy. The elements of this strategy would be:

(a) A census of current Steel Sector participation in co-op and internship placements of technology students,

2 Metal Working Trades include: Sheet Metal Workers, Boilermakers, Structural Metal and Plate Work Fabricators,

Fitters, Ironworkers, Blacksmiths, Die Setters, and Welders

10

(b) A national target to increase the number of co-op and internship placements of technology students,

(c) Development of an occupational standard for a Steel Technologist,

(d) Partnerships with colleges and CEGEPs to deliver training to meet the Steel Technologist standard.

Recommendation No. 6

Steel Detailers

CSTEC should support CISC in developing a national occupational standard for Steel Detailers and making Steel Detailing an apprenticeable Red Seal trade or a certifiable occupation in all provinces.

Recommendation No. 7 Knowledge Transfer

CSTEC should produce a best practices guide on how companies in the steel industry and in other industries are tackling the knowledge transfer challenge.

CSTEC also should develop a strategy to link the documentation of experience-based skills and knowledge to essential skills training.

Recommendation No. 8

Essential Skills

CSTEC needs to broaden its essential skills training strategy to include:

• Supporting apprentices, • Bridging the language skills gaps of recent immigrants, • Linking essential skills to the implementation of continuous improvement and total

productive maintenance, • Linking essential skills training to documenting tacit knowledge and skills and thereby

supporting knowledge transfer, • Health and safety.

Recommendation No. 9 Energy Conservation in Production and Maintenance

CSTEC should develop a training program to support companies in the steel sector that are seeking to achieve operational excellence in the use of energy through the adoption of best practices on the part of operators and maintenance workers.

11

●

12

Chapter One Introduction

This report as commissioned by the Canadian Steel Trade and Employment Congress (CSTEC) with support from Human Resources and Skills Development Canada (HRSDC).

CSTEC was established by the United Steelworkers and leading employers in the steel industry. From its inception, CSTEC has served as a forum where employers and representatives of workers can identify common human resources challenges and pursue joint initiatives to address those challenges. Over its more than 25 years of operation, CSTEC has implemented a range of innovative training and labour adjustment programs. In recent years, these have included: new approaches to apprenticeship recruitment and training, essential skills training, career awareness programs, youth employment services, and the development of training courses for the steel industry.

The purpose of this report is to review trends and developments in the Broader Steel Sector and to identify the implications of these trends for human resources planning. The Broader Steel Sector comprises the Primary Steel Producers and steel-using industries that have historically had a close relationship to the Primary Steel industry. These include: Independent Pipe Mills, Rolling Mills and Drawing Mills, Foundries, Construction Fabricators and Metals Service Centres.

A previous review of trends in the Broader Steel Sector was published by CSTEC in 2005.3 Since 2005, there have been significant changes in the Broader Steel Sector. In the Primary Steel industry, there has been a complete transformation of ownership structures, a rationalization of production capacity and an acceleration of integration into the NAFTA market. These trends have also affected Independent Pipe Mills, Rolling Mills and Drawing Mills. In the Foundry industry, there has been a significant decline in employment and a re-orientation of production as low value production moved off-shore in response to the appreciation of the Canadian dollar. Construction Fabricators are experiencing major technological innovations that are changing both production processes and the design process. Metal Service Centres have taken on ‘finishing functions’ that were previously performed by Primary Steel Producers. As well, changes in the composition and nature of the metals manufacturing sector (also a consequence of the higher dollar) are changing the customer base of Service Centres. Adjusting to changing work force demographic trends is a challenge across the Broader Steel Sector. All of these trends and changes in the Steel Sector have implications for human resources.

The findings and recommendations of this study are based on

• a review of scholarly and trade literature on the Broader Steel Sector, • an analysis of statistical indicators, • a custom forecast of output and employment trends in the Broader Steel Sector by

the Conference Board,

3 CSTEC, Human Resources Study of the Broader Canadian Steel Industry: Final Report (2005). This study is

available at: www.cstec.ca/Sector_Study.asp

13

• the Construction Sector Council’s forecast of trends in non-residential construction,

• interviews with senior executives in the Broader Steel Sector and with Local Union leaders,

• focus groups with workers, • a Survey of Human Resources Managers, and • a Survey of Local Union Leaders.

Chapter Two provides an overview of trends in the Broader Steel Sector.

Chapter Three examines the drivers of change that are altering human resources needs.

Chapter Four summarizes the results of forecasts of human resources needs by major occupational groups, based on alternative productivity scenarios. This chapter sets out key findings, in particular, for the Broader Steel Sector’s needs for skilled tradespersons.

Chapter Five summarizes the results of the Survey of Human Resources Managers.

Chapter Six reports the results of the Survey of Local Union Leaders. These two surveys show that training is a high priority for both employers and Local Union Leaders. However, and not surprisingly, they have different perspectives on training culture in the Steel Sector and training needs.

Chapter Seven summarizes salient comments derived from interviews with senior executives, Local Union Leaders and workers who participated in focus groups.

Chapters Eight through Eleven present detailed profiles of human resources trends in each of the industries that comprise the Broader Steel Sector. These chapters note progress that has been made and identify gaps and challenges that will be important over the next decade.

Chapter Twelve presents recommendations based on the analysis set out in the previous chapters.

The central conclusion of this report is that the skills profile of the ‘Steelworker of the Future’ will be different from the skills profile of the ‘Steelworker of Today’. This is not to say that ten years from now the Steel Sector will be unrecognizable to the current work force. However, the change in production processes and in skill needs will be significant. The overriding goal of this study is to assist stakeholders in the Broader Steel Sector to understand what the ‘Steelworker of the Future’ will look like, what skills those Steelworkers will need, and how employers, Local Unions, and CSTEC can contribute to building a strong and competitive steel industry that generates more secure and well-paid jobs.

CSTEC wishes to thank the members of the Steering Committee who provided advice and direction for this study. We also acknowledge and thank those who contributed their time through participating in interviews, focus groups and surveys. A list of Steering Committee members, interviews and focus groups can be found in the Appendices to this study. Finally, CSTEC wishes to acknowledge and thank Human Resources and Skills Development Canada for financial support for this study through the Sector Councils Program.

●

14

Chapter Two Overview of the Broader Steel Sector

1. Defining the Broader Steel Sector 2. Employment Trends in the Broader Steel Sector 3. Steel in the Canadian Economy 4. Human Resources Challenges

1. Defining the Broader Steel Sector4

The Broader Steel Sector employs approximately 100,000 Canadians. The sector comprises the Primary Steel Producers (NAICS 3311), together with mills that produce pipe and tube or roll and draw iron and steel (NAICS 3312)5, and three industries that historically have been linked closely to Primary Steel Producers:

• Iron and Steel Foundries (NAICS 33151), • Construction Fabricators (sub-components of NAICS 3323), and • Metals Service Centres (NAICS 4162)

Primary Steel Producers manufacture the basic steel shapes: slabs, billets and blooms. Two manufacturing processes predominate in primary steel production. The first is blast furnace technology, which is also known as oxygen blown converter (OBC) technology. Producers using OBC technology convert raw materials (iron ore, coking coal, and limestone) into the basic steel shapes. These mills are often referred to as ‘integrated mills’. The second type of steel-making technology uses electric arc furnaces (EAF). Producers using EAF technology convert scrap metal into the basic steel shapes.

The basic steel shapes – slabs, billets and blooms – are further processed into semi-finished steel products. Slabs are converted into hot and cold strip steel, steel plate, and coiled sheet steel. Billets are further processed into various shapes of bars, rods and tubes. Blooms are made into structural shapes for

4 For statistical purposes, industries are classified using the North American Industry Classification System

(NAICS). Statistical classification is based on the dominant activity of an ‘establishment’, not on the dominant activity of a company. Companies that have multiple facilities may have those establishments classified differently based on the dominant activity at each site. Conversely a company that has multiple industrial activities within one establishment will be classified as being in only one industry, based on the activity that is deemed dominant.

5 Some pipe mills, rolling mills and drawing mills are owned and operated by Primary Steel Producers. Other mills

are independently operated. Mills that are operated by Primary Steel Producers are included in NAICSZ 3311. Mills that are operated independently are included in NAICS 3312. Human resources issues are the same, regardless of ownership and statistical classification.

15

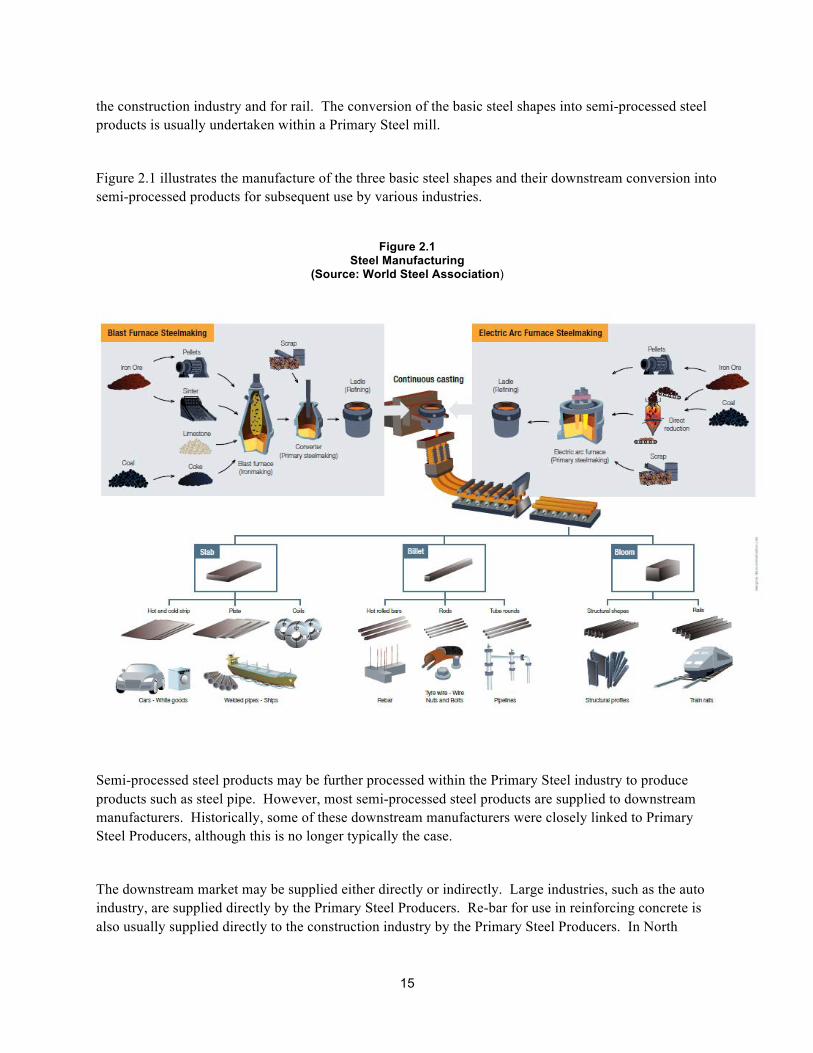

the construction industry and for rail. The conversion of the basic steel shapes into semi-processed steel products is usually undertaken within a Primary Steel mill.

Figure 2.1 illustrates the manufacture of the three basic steel shapes and their downstream conversion into semi-processed products for subsequent use by various industries.

Figure 2.1

Steel Manufacturing (Source: World Steel Association)

Semi-processed steel products may be further processed within the Primary Steel industry to produce products such as steel pipe. However, most semi-processed steel products are supplied to downstream manufacturers. Historically, some of these downstream manufacturers were closely linked to Primary Steel Producers, although this is no longer typically the case.

The downstream market may be supplied either directly or indirectly. Large industries, such as the auto industry, are supplied directly by the Primary Steel Producers. Re-bar for use in reinforcing concrete is also usually supplied directly to the construction industry by the Primary Steel Producers. In North

16

America, companies in other industries are generally supplied through Metals Service Centres which are wholesale distributors of semi-processed steel products (and other metals). Outside of North America, Metals Service Centres are often affiliated to Primary Steel Producers and distribute mainly or exclusively the output of their parent firm.

Metals Service Centres inventory and distribute semi-processed steel products to downstream users of these products in the manufacturing and construction industries. Over the past two decades many Metals Service Centres have also taken on ‘finishing functions’ which were previously carried out by the Primary Steel Producers. Examples of ‘finishing functions’ are: sawing, shearing or cutting basic steel shapes into standard sizes, rolling basic steel shapes to produce angle products, drilling, threading, slotting, and painting. Metals Service Centres obtain steel from domestic producers, other NAFTA region producers and from off-shore sources. For many steel-using companies, their primary contact with the steel industry is through Metals Service Centres. Many Metals Service Centres also supply non-ferrous metal products.

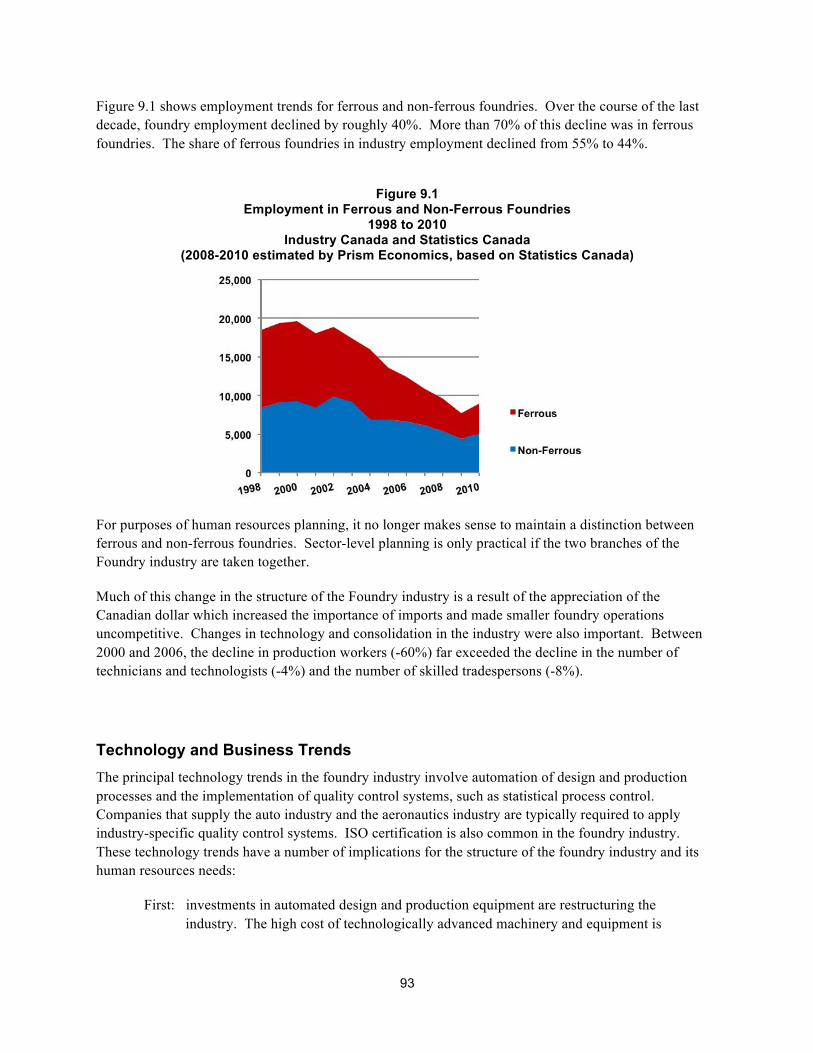

Foundries re-melt steel, cast the molten steel into specific shapes and further finish the cast product by grinding, sanding, drilling, etc. Historically, many foundry operations were owned by Primary Steel Producers, though this is no longer the case in North America. While some foundries work solely with iron and steel, it is increasingly common for foundries to cast other metals, especially aluminium. Some foundries make their own moulds for casting, while others purchase moulds from specialized mould-making shops. Over the past decade, the majority of ferrous foundry operations in Canada have closed or moved offshore.

Construction Fabricators comprise plants that fabricate plate work and structural products by cutting, punching, bending, shaping and welding steel for use in the construction industry and in other heavy industries, notably the mining and energy sectors. Some companies that are considered Construction Fabricators also manufacture architectural iron and steel products, such as staircases. Construction fabricators are the principal channel through which structural steel products enter the construction market. As a structural product, steel’s principal competitor in the construction market is reinforced concrete.

There is an approximate, but not a precise, correspondence between the industries defined in the NAICS system and the scope of the various industry associations in the Broader Steel Sector. Figure 2.2 shows the approximate mapping of statistically defined industries into industry associations. Some companies, however, operate in more than one industry. Companies also may belong to more than one industry association.

17

Figure 2.2 Relationship between Industry Associations and

the Statistical Definition of Industries in the Broader Steel Sector

NAICS Descriptor Industry Association

3311 Primary Steel Producers Canadian Steel Producers Association (CPSA)

33121 Pipe and Tube Corrugated Steel Pipe Institute (CSPI)

33122 Rolling and Drawing No specific association in Canada

33151 Iron & Steel Foundries Canadian Foundries Association (CFA)

3323 Construction Fabricators Canadian Institute of Steel Construction (CISC) Canadian Steel Sheet Building Institute (CSSBI) Steel Framing Alliance (SFA)

4162 Metals Service Centres Metals Service Center Institute (MSCI) – Canadian Section

2. Employment Trends in the Broader Steel Sector

Figure 2.3 shows employment trends in the industries that comprise the Broader Steel Sector. Figure 2.3

Employment in the Broader Steel Sector, 1991 -20106 Statistics Canada, CANSIM 281-0024

6 Data for 2010 are preliminary, based on the average monthly employment for January to October. Data for

foundries include both ferrous and non-ferrous foundries. Data for Independent Pipe & Tube, Drawing and Rolling Mills are NAICS 3312). Data for Construction Fabricators are for all ‘Architectural and Structural Metals Manufacturing’ (NAICS 3323). This includes re-bar manufacturers and manufacturers of metal doors and windows. Separate annual data are not available for Construction Fabricators. Construction Fabricators are approximately 75% of NAICS 3323.

18

Industry NAICS Code

2010 Employment

Primary Steel Producers 3311 16,957 Independent Pipe, Rolling and Drawing Mills 3312 7,564 Construction Fabricators 3323 52,956 Foundries (Ferrous & Non-Ferrous) 3315 8,495 Metals Service Centres 4162 17,016 Total 102,988

Prior to the downturn at the end of 2008, the principal sources of employment growth were Construction Fabricators and Metals Service Centres. From 2000 to 2008 (i.e., prior to the downturn in 2008), employment in Construction Fabricators increased by 15%. In Metals Service Centres, employment increased by approximately 5%.

Employment in Primary Steel Producers and in Pipe, Rolling and Drawing Mills was relatively stable in the 1990s. However, in the most recent decade, employment fell by approximately 44%. Roughly three-quarters of this decline was driven by changes in business organization and technology. Over the past decade, employment in Foundries fell by roughly 55%. Almost two-thirds of this decline preceded the downturn in 2008. An important factor in this decline was the appreciation of Canadian dollar which forced domestic producers to either cease operations or relocate offshore.

3. Steel in the Canadian Economy Throughout its history, the Canadian steel industry has developed alongside Canadian manufacturing. We would not have one without the other. The economic and business histories of the steel industry and the manufacturing sector as a whole are bound up with one another. This relationship is described in a 2010 study supported by CSTEC, the Canadian Steel Producers Association, and the United Steelworkers.7 Among the findings in this study are:

• The steel sector supports over 100,000 direct jobs in Canada and many more jobs which supply the companies in the steel sector.

• The steel industry produces a versatile material that is essential to other key industries, to the quality of our life, to our transportation systems, and to our physical infrastructure.

• Steel will continue to play a key role in our energy and environmental future, including the products and technologies of a ‘greener’ economy.

• Steel generates $7 billion per year in exports.

• Steel will be one of the critical underpinnings of a sustainable manufacturing sector in the Canadian economy of the future.

7 Peter Warrian, “The Importance of Steel Manufacturing to Canada – A Research Study”, Canadian Steel Producers

Association (May 2010) www.canadiansteel.ca/media/2010/cspa-warrian-report.pdf

19

Transportation costs create a natural clustering of steel producers and their customers both in the Broader Steel Sector and in manufacturing. Owing to the high cost of transporting basic steel shapes and semi-processed steel products, many steel using companies locate near the mills. A second factor which reinforces this trend is the need to draw on a common pool of skills. These include trade skills, technology and engineering skills, and industry management and marketing skills. The lesson is that the steel mill is a hub. Steel companies also generate demands from suppliers of goods and services in the local economy. These include skill-intensive, professional services. Many of the businesses and professional practices that supply these goods and services to the steel industry subsequently become regional exporters, in their own right.

Canada has developed a significant steel industry. This industry has evolved in a close relationship with both its suppliers and its customers. The steel supply chain has generated good jobs for suppliers as well as customers, as well as benefits for the communities in which the steel industry is located. If our steel industry were to contract, it is not only the steel industry and steel communities that would decline. Many other companies that make up the steel supply chain – customers, as well as suppliers – also would migrate. For example, if Canada were unable to supply the metallurgical needs of the auto industry and its parts suppliers, transportation costs would lead many of these companies to relocate closer to where that supply capacity could be found. Other links are more subtle. Steel products and steel-making inputs are the largest user of the St. Lawrence Seaway. Without the volumes represented by steel, communities from the mine to the mill to downstream manufacturers would be pushed into an inexorable decline.

4. Human Resources Challenges

In 2005, the Canadian Steel Trade and Employment Congress published the final report of the Human Resources Study of the Broader Canadian Steel Industry.8 The 2005 report identified two primary drivers of change in the broader steel sector. The first of these was rationalization of production in response to competitive pressures and a higher Canadian dollar. The report saw rationalization leading to further downsizing in the industry as well as to changing skill needs. The second driver of change was the aging of the work force, especially in the skilled trades. Even with only 50% of retiring skilled tradespersons being replaced, the 2005 report forecast serious recruitment and training challenges for the broader steel sector, and especially for the Primary Steel Producers.

The 2005 report recommended sector-based strategies to address a number of emerging human resources issues. These included:

• increasing the number of apprenticeships,

• developing sector-based recruitment strategies,

8 Available from the CSTEC web site: http://www.cstec.ca/Sector_Study.asp

20

• designing a strategy to address the essential skills deficit,

• strengthening the sector’s training culture and increasing employee involvement in identifying training priorities,

• increasing the utilization of CSTEC’s skills upgrading courses,

• building stronger relationships with community colleges and CEGEPs, and

• continuing active labour adjustment programs to support workers who will be adversely affected by downsizing.

In 2011, some of the challenges identified in 2005 continue to be important. The need to ensure a supply of qualified tradespersons is as important in 2011 as it was in 2005. So also is the need to strengthen the sector’s training culture. Addressing the essential skills deficit also will continue to be a challenge for the sector. However, much has changed in the broader steel sector since 2005. The overarching challenge is to understand the impact of globalized supply chains on human resources and then to identify sector-based strategies that will support improved human resources development and human resources management at the company level. Central to globalization is a restructuring of supply chains. Labour-intensive, lower value-added processes will continue to be moved offshore. The appreciation of the Canadian dollar will accelerate this process. What remains is the more skill-intensive, higher value-added processes. There is nothing automatic about these production processes being located in Canada. Canada necessarily competes with other OECD and economies such as China, India and Brazil. In this competition for high value-added production, a key determinant of national success will be the quality of human resources. The key questions, therefore, are (1) what are the skills and practices that will be needed by the steel industry of the future? and (2) how can CSTEC promote and support the development of these skills and practices?

●

21

Chapter Three Drivers of Change in the Broader Steel Sector

1. Globalization, 2. Demographic trends, 3. Technology and work organization, 4. Economic trends and the demand for steel 5. Energy costs and green manufacturing

Human resources needs in the Broader Steel Sector are being transformed by five over-arching trends. These are (1) globalization, (2) the aging of the work force, (3) changes in technology, including how work is organized, (4) broad macro-economic trends, especially in the NAFTA region, and (5) trends in the demand for steel and steel products. It would be a serious error, however, to interpret these drivers of change as having the same impact across Primary Steel Producers, Foundries, Fabricators, and Metals Service Centres. There is no single ‘human resources story’ in the Canadian steel sector. Rather there are four distinct narratives that overlap at some points, but diverge at others.

1. Globalization

Three phenomena are at the heart of globalization. The first is the internationalization of ownership structures. This is most evident in Primary Steel Production where, over the past several years, there has been a change of ownership in every steel producing operation. With only one exception, this change in ownership involved a shift from domestic control to international control.

A direct consequence of the transformation of ownership structures is significantly increased international flows of capital, technology, managerial norms and talent. While attention most often focuses on capital and technology, the adoption of international managerial norms and the international flows of talent may have the most far-reaching impact on human resources. These international managerial norms include productivity benchmarking, new approaches to work organization, and distinct strategies related for training and human resources development.

The second phenomenon that defines globalization is the accelerated integration of international markets. The signature development that marks this integration is a sharp increase in both exports and imports of steel products. Figure 3.1 illustrates this acceleration during the most recent decade.

22

Figure 3.1 Canadian Trade (Imports + Export) in Steel Mill Products

Showing Compound Annual Growth Rate (CAGR) (Customs Basis)

1986 – 2010 Statistics Canada, Labour CANSM

Prior to 1992, Canadian trade in steel mill products (imports + exports) grew only marginally. Indeed, if price effects are taken into account, there may not have been any real growth in terms of tonnage. From 1992 to 2003, the dollar volume of trade in steel mill products increased by around 7.2% annually. After 2003, and until the onset of the recession in 2009, the compound annual growth rate (CAGR) almost doubled, averaging 15.2% over the period 2003 to 2008. As Figure 3.2 shows, during the period 2003 to 2008, trade in steel products grew at 3 times the rate of trade in manufactured products as a whole.

Figure 3.2 Canadian Trade in Steel Mill Products

Compared to Trade in All Manufactured Goods (Excluding Food Products) 1986 – 2010

Statistics Canada, Labour CANSM

23

The increased trade flows shown in Figure 3.2 are predominantly a NAFTA phenomenon. Roughly two-thirds of Canadian imports are from the United States or Mexico, while over 90% of Canadian exports flow in that direction.

A significant rationalization of production underpinned the increased export orientation of the Primary Steel industry. This rationalization of capacity drove a step-function increase in productivity that reduced overall employment and is also reshaping the skill needs of the steelworker of the future. Although globalization led to a increase in the Primary Steel industry’s export orientation, it would be a serious error to discount the continuing importance of the domestic market. Even with exports taking an increased share of output, the domestic market still accounts for at least half of industry shipments. As discussed later in this chapter, the Primary Steel industry is still vulnerable to unfair trade practices, such as ‘dumping’.

The third phenomenon at the heart of globalization is a marked increase in the scope and reach of international supply chains. The logic driving the globalization of supply chains is the competitive advantage that derives from achieving an approximate symmetry between labour intensiveness and skill availability on the one hand and labour cost on the other. The migration of low-skill, labour intensive production processes to lower cost jurisdictions is not a new story. What is new is the increase in the scope and reach of international supply chains to include production processes that were much less vulnerable to offshoring prior to this decade. The change is being driven by the rapid appreciation of the Canadian dollar. This is most evident in the Foundries industry where labour accounts for approximately 34% of production costs.9 Prior to the economic downturn in 2009, the total real value of shipments from ferrous foundries had fallen by more than 30% since 1999. Most of this decline reflected the movement of commodity production to lower cost jurisdictions. By contrast, in the Primary Steel industry, labour accounts for only 15% of production costs. Consequently, the Primary Steel industry is less vulnerable to the pressure to relocate production to offshore locations. The Primary Steel industry is also more skill intensive and will become even more so in the future.

The impact of globalization has differed significantly across the four industries that comprise the Broader Steel Sector:

• In Primary Steel Production, the impact of globalization is most evident in the internationalization of ownership, the rationalization of production and the adoption of international performance benchmarking. These developments have fundamentally altered productivity conditions over the past five years and will reshape human resources requirements in the Primary Steel industry. Owing to the relatively low share of labour in total production costs (approximately 15%), the Primary Steel industry is much less vulnerable to pressure to relocate production to low-cost jurisdictions. However, the internationalization of production has increased the intensity of competition for investment and technology within global companies.

9 Statistics Canada, CANSIM, Table 301-0006

24

Another critical aspect of the globalization of the steel industry is the explosive growth in world demand for steel. The principal driver in this growth is the rapid expansion of China, India, Brazil and other emerging economies. China, in particular, is a singular factor in the growth of world demand, rising from a relatively minor share of global production and consumption in 2000 to almost one half in 2010. (See Figure No. 3.5 in Chapter Three.) China’s steel-making capacity has increased faster than its domestic consumption, with the result that China’s share of world exports to all countries, including Canada, has grown significantly.

• For Construction Fabricators, the ramification of globalization is chiefly the way that the increased importance of export markets, together with the opening of the domestic market to low-cost producers, has forced the industry to supply higher value-added products and services. This ratcheting up of the industry’s value-added trajectory is driving new human resources needs and changing the profile of the industry’s work force. Important consequences of this trend are the widespread adoption of international quality certification systems, such as ISO, and the adoption of more advanced production and imaging technology. This includes high definition plasma cutting on the production side, three-dimensional imaging technologies on the design side, and Building Information Modelling (BIM) on the project management side.

• For Foundry operations, the principal impact of globalization has been to off-shore the majority of ferrous foundry operations. The foundries that remain in Canada are predominantly non-ferrous or mixed ferrous and non-ferrous. As commodity production has moved off-shore, the remaining foundries have focused on higher value-added metallurgical products. This, in turn, is increasing the strategic importance of metallurgical technology skills and the ability to cast complex and precision designs.

• In contrast with the other industries in the steel sector, Metals Service Centres are predominantly focused on the domestic market, although some Service Centres have cross-border operations. There has thus far been no significant internationalization of ownership. However, two consequences of broader globalization trends are evident. The first is that the rationalization of production in primary steel production has led the Primary Producers to withdraw from finishing functions in those lines of production which they no longer undertake. This, in turn, has resulted in those specific finishing functions (and the related skill needs) migrating to service centres. The second impact of globalization is the introduction into North America of the European and Asian business model whereby Primary Producers operate wholly owned service centres and utilize this distribution channel to disseminate technical support to downstream steel users. While this trend has not yet taken root in Canada, there may be changes in the future.

25

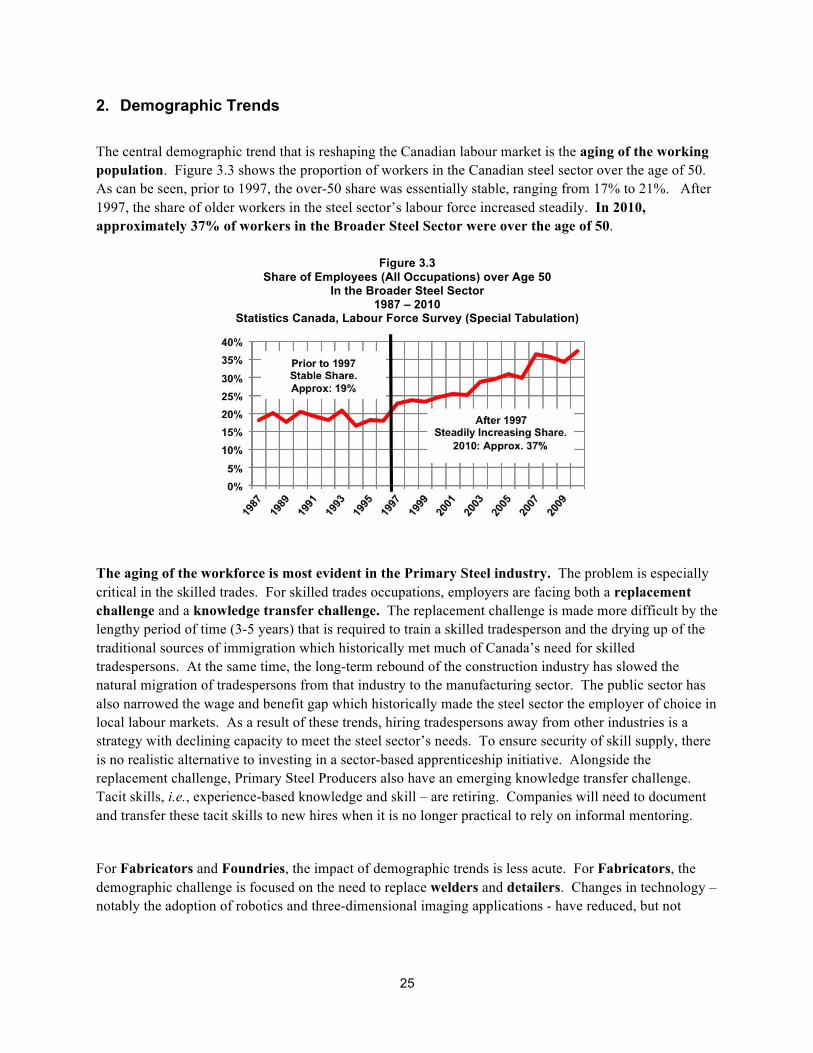

2. Demographic Trends

The central demographic trend that is reshaping the Canadian labour market is the aging of the working population. Figure 3.3 shows the proportion of workers in the Canadian steel sector over the age of 50. As can be seen, prior to 1997, the over-50 share was essentially stable, ranging from 17% to 21%. After 1997, the share of older workers in the steel sector’s labour force increased steadily. In 2010, approximately 37% of workers in the Broader Steel Sector were over the age of 50.

Figure 3.3

Share of Employees (All Occupations) over Age 50 In the Broader Steel Sector

1987 – 2010 Statistics Canada, Labour Force Survey (Special Tabulation)

The aging of the workforce is most evident in the Primary Steel industry. The problem is especially critical in the skilled trades. For skilled trades occupations, employers are facing both a replacement challenge and a knowledge transfer challenge. The replacement challenge is made more difficult by the lengthy period of time (3-5 years) that is required to train a skilled tradesperson and the drying up of the traditional sources of immigration which historically met much of Canada’s need for skilled tradespersons. At the same time, the long-term rebound of the construction industry has slowed the natural migration of tradespersons from that industry to the manufacturing sector. The public sector has also narrowed the wage and benefit gap which historically made the steel sector the employer of choice in local labour markets. As a result of these trends, hiring tradespersons away from other industries is a strategy with declining capacity to meet the steel sector’s needs. To ensure security of skill supply, there is no realistic alternative to investing in a sector-based apprenticeship initiative. Alongside the replacement challenge, Primary Steel Producers also have an emerging knowledge transfer challenge. Tacit skills, i.e., experience-based knowledge and skill – are retiring. Companies will need to document and transfer these tacit skills to new hires when it is no longer practical to rely on informal mentoring.

For Fabricators and Foundries, the impact of demographic trends is less acute. For Fabricators, the demographic challenge is focused on the need to replace welders and detailers. Changes in technology – notably the adoption of robotics and three-dimensional imaging applications - have reduced, but not

26

eliminated the replacement challenge. Metals Service Centres, on the whole, do not confront any serious demographic challenges.

3. Technology Trends and Human Resources Management

There are two broad technology trends in the broader steel sector:

(1) increased capital/labour ratios, and

(2) an increase in the use of information technologies in design and production processes.

These trends have had five consequences:

First: labour productivity gains have steadily reduced the number of production workers and materials handlers as well as their share in the Primary Steel Producers’ work force. Automation will continue to eliminate these types of jobs. In Foundries, Fabricators and Service Centres, automation will also eliminate some metal-working jobs, notably welding and machining;

Second: the need to maintain production equipment has led to an increase in the relative share, though not the absolute number, of skilled tradespersons in the steel sector. Larger establishments will generally prefer to provide their own maintenance using direct employees. Smaller establishments may prefer to contract for maintenance services;

Third: the technology intensiveness of production and design equipment – especially the application of information technologies to product and design processes – has increased both the number of technicians and technologists employed in the steel sector and their share in the sector’s work force;

Fourth: a further consequence of the increased application of information technologies to production processes has been an increased need for skilled tradespersons to have technology skills; and

Fifth: in the absence of technology breakthroughs, which are inherently unpredictable, the principal sources of productivity gains over the next five years will be (a) continued automation of labour processes, (b) the implementation of continuous improvement strategies, and (c) the adoption of total productive maintenance strategies.

27

4. Economic Outlook:

Recovery:

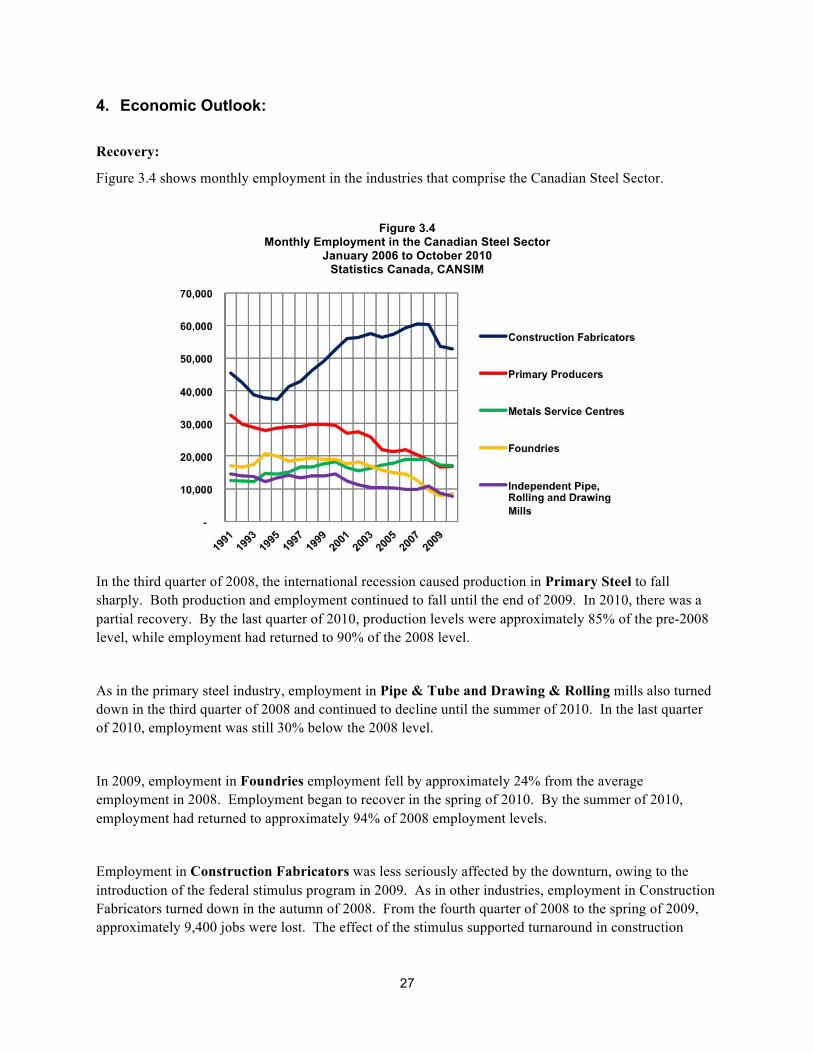

Figure 3.4 shows monthly employment in the industries that comprise the Canadian Steel Sector.

Figure 3.4

Monthly Employment in the Canadian Steel Sector January 2006 to October 2010

Statistics Canada, CANSIM

In the third quarter of 2008, the international recession caused production in Primary Steel to fall sharply. Both production and employment continued to fall until the end of 2009. In 2010, there was a partial recovery. By the last quarter of 2010, production levels were approximately 85% of the pre-2008 level, while employment had returned to 90% of the 2008 level.

As in the primary steel industry, employment in Pipe & Tube and Drawing & Rolling mills also turned down in the third quarter of 2008 and continued to decline until the summer of 2010. In the last quarter of 2010, employment was still 30% below the 2008 level.

In 2009, employment in Foundries employment fell by approximately 24% from the average employment in 2008. Employment began to recover in the spring of 2010. By the summer of 2010, employment had returned to approximately 94% of 2008 employment levels.

Employment in Construction Fabricators was less seriously affected by the downturn, owing to the introduction of the federal stimulus program in 2009. As in other industries, employment in Construction Fabricators turned down in the autumn of 2008. From the fourth quarter of 2008 to the spring of 2009, approximately 9,400 jobs were lost. The effect of the stimulus supported turnaround in construction

28

restored approximately 40% of these jobs. In the fourth quarter of 2010, employment in the industry was approximately 92% of the pre-downturn level. The challenge for the industry will be whether sufficient private investment in new construction occurs to compensate for the winding down of stimulus spending.

The downturn in Metals Service Centre employment, though severe, was not as acute as in Primary Steel and Foundries. In part, this was because construction demand offset the decline in demand from manufacturers of steel products. During 2009 and through to the beginning of 2010, employment fell by approximately 12% from 2008 levels. By the last quarter of 2010, employment had returned to 90% of 2008 levels.

The NAFTA Region:

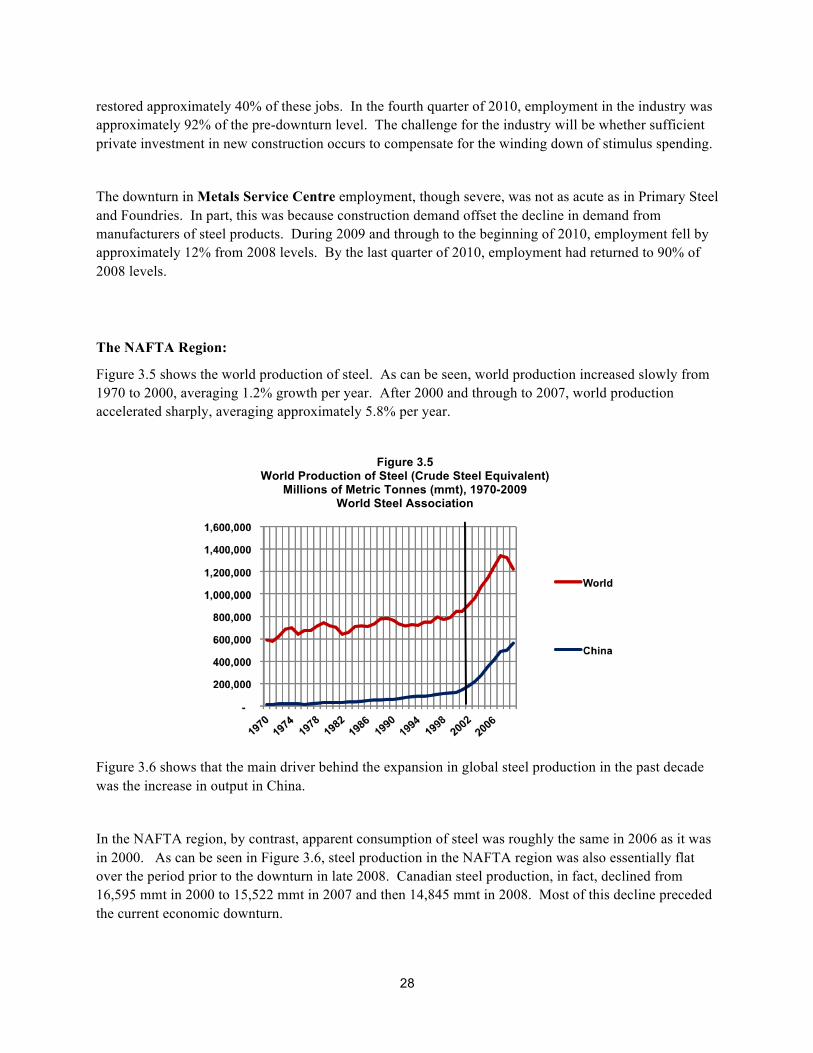

Figure 3.5 shows the world production of steel. As can be seen, world production increased slowly from 1970 to 2000, averaging 1.2% growth per year. After 2000 and through to 2007, world production accelerated sharply, averaging approximately 5.8% per year.

Figure 3.5 World Production of Steel (Crude Steel Equivalent)

Millions of Metric Tonnes (mmt), 1970-2009 World Steel Association

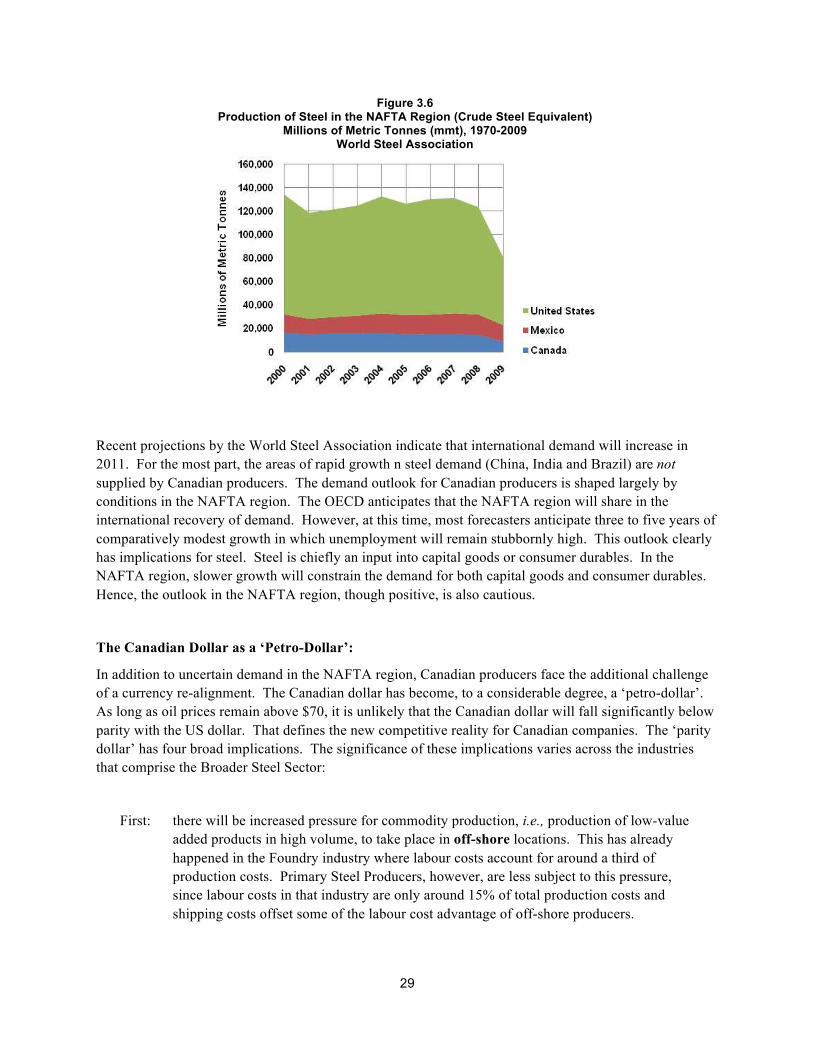

Figure 3.6 shows that the main driver behind the expansion in global steel production in the past decade was the increase in output in China.

In the NAFTA region, by contrast, apparent consumption of steel was roughly the same in 2006 as it was in 2000. As can be seen in Figure 3.6, steel production in the NAFTA region was also essentially flat over the period prior to the downturn in late 2008. Canadian steel production, in fact, declined from 16,595 mmt in 2000 to 15,522 mmt in 2007 and then 14,845 mmt in 2008. Most of this decline preceded the current economic downturn.

29

Figure 3.6 Production of Steel in the NAFTA Region (Crude Steel Equivalent)

Millions of Metric Tonnes (mmt), 1970-2009 World Steel Association

Recent projections by the World Steel Association indicate that international demand will increase in 2011. For the most part, the areas of rapid growth n steel demand (China, India and Brazil) are not supplied by Canadian producers. The demand outlook for Canadian producers is shaped largely by conditions in the NAFTA region. The OECD anticipates that the NAFTA region will share in the international recovery of demand. However, at this time, most forecasters anticipate three to five years of comparatively modest growth in which unemployment will remain stubbornly high. This outlook clearly has implications for steel. Steel is chiefly an input into capital goods or consumer durables. In the NAFTA region, slower growth will constrain the demand for both capital goods and consumer durables. Hence, the outlook in the NAFTA region, though positive, is also cautious.

The Canadian Dollar as a ‘Petro-Dollar’:

In addition to uncertain demand in the NAFTA region, Canadian producers face the additional challenge of a currency re-alignment. The Canadian dollar has become, to a considerable degree, a ‘petro-dollar’. As long as oil prices remain above $70, it is unlikely that the Canadian dollar will fall significantly below parity with the US dollar. That defines the new competitive reality for Canadian companies. The ‘parity dollar’ has four broad implications. The significance of these implications varies across the industries that comprise the Broader Steel Sector:

First: there will be increased pressure for commodity production, i.e., production of low-value added products in high volume, to take place in off-shore locations. This has already happened in the Foundry industry where labour costs account for around a third of production costs. Primary Steel Producers, however, are less subject to this pressure, since labour costs in that industry are only around 15% of total production costs and shipping costs offset some of the labour cost advantage of off-shore producers.

30

Second: higher value-added production will continue to be viable in Canada. However, this continued viability will require increases in productivity, i.e., increases in value-added per worker. There are three principal ways these increases in value added per employee can be achieved: (1) more efficient operations that reduce or eliminate down-time and defects, (2) investment in new technology that automates labour processes, and (3) investment which enables Canadian operations to supply more sophisticated alloys, advanced coatings, and complex designs. The imperative to increases value-added per worker clearly has implications for skill requirements and human resources planning. The new investments in technology that will be required may be beyond the reach of some small companies, notably in the foundry, construction fabricator, and service centre segments of the Broader Steel Sector. Rationalization has already taken place in the primary producer industry. The rationalization trend will spread to foundries, fabricators and service centres. This rationalization will be associated with an increase in average establishment size;

Third: the high dollar will accelerate rationalization and the move to off-shore locations among manufacturers of some fabricated steel products (i.e., the customer base). This may reduce domestic demand for steel or slow the growth of demand; and

Fourth: the shift to higher value-added production will drive a change in both skill requirements and in the occupational composition of the work force in the steel sector.

5. The Potential for Growth10

The growth potential of the Broader Steel Sector differs across the industries that comprise the sector.

• Primary Steel Producers can look to four markets to drive a growth in output and consequent growth in employment. The first of these is the auto industry which is projected to recover from its cyclical downturn and capacity restructuring. The pace of this recovery may be slower that previous upturns, owing to the general trend of households to reduce their debt burden. However, in virtually every scenario for the NAFTA region, there will be a significant ramping up of auto production. The second market that will drive growth is oil and gas, chiefly oil sands development and pipeline construction. Third, power generation and distribution will generate a need for steel products. And finally, the industry has the potential to capture an increased share of the construction market by adapting high strength and coated products developed for the manufacturing sector.11

10 Detailed employment projections are provided in Chapter Four. 11 The ‘growth story’ is set out more fully in Peter Warrian, “The Importance of Steel Manufacturing to Canada – A

Research Study”, Canadian Steel Producers Association (May 2010)

31

• The Foundries industry does not share the same potential for growth as the Primary Steel Producers. Over the next five years, the ‘commodity’ production that remains in Canada will be at increased risk of moving off-shore or losing market to off-shore suppliers. Higher-value casting work will increase, but will be limited by the overall growth in sophisticate durable products and machinery. While there is scope for metal casting replacing other materials (notably plastics and polymer compounds), that scope is limited.

• Growth of Construction Fabricators is tied to the construction industry’s outlook, especially non-residential building construction and to the steel share of the construction market. Over the next five years, demand is unlikely to exceed the levels seen in the period prior to 2008, though steel may capture an increased share of the structural and cladding market if prices remain competitive with other materials.

• The customer base for Metal Service Centres is chiefly metals using manufacturers, excluding the auto assemblers. In most regions of Canada, there has been a structural change which has seen a significant fraction of metals using manufacturers close or transfer operations to off-shore locations. While the remaining customer base will experience growth, in tandem with the overall recovery in the goods producing sector, the decline in the size of the customer base will offset much of that growth.

6. Anti-Competitive Trade Practices of Off-Shore Producers

The Primary Steel industry has historically been the focus of anti-competitive policies and unfair or illegal practices by offshore producers seeking to protect their domestic market or give their exporters an unfair advantage. It is a common practice for off-shore suppliers to engage in ‘dumping’, i.e., selling surplus product at less than the average cost of production12. As well, many of these offshore producers enjoy hidden subsidies from their governments. These anti-competitive practices are contrary to the international rules of trade. However, it can be both difficult and costly to police these anti-competitive practices. The secular decline in international shipping costs has put North American-based producers at increased risk of dumping.

Primary Steel Producers in many developing countries – especially China – receive direct and indirect state support. This support may take various forms, including below-market costs for capital, regulatory impedance of imports, and above-market prices for products (which allows dumping of surplus product).

12 All industries in which fixed costs constitute the lion’s share of production costs are vulnerable to dumping. A

simplified model illustrates the economics of dumping. A batch of output can be divided into two categories – A and B. The price charged for category A output covers the total fixed costs (i.e., amortization of the capital stock) of producing both A and B plus the variable cost (labour, materials, energy, and shipping) of producing A. The price charged for category B output, therefore, only needs to cover the variable costs, since the fixed costs were covered by the proceeds from the sale of category A output. If fixed costs are a high proportion of total costs, as they are in the Primary Steel Industry, a price which covers only variable costs will be substantially less than a price which covers both variable and fixed costs. If a producer has already covered its fixed costs from the proceeds of category A output, then any price above the variable cost for category B output will add to its profit.

32

Governments in the NAFTA region will need to increase their vigilance in enforcing trade rules the prevent off-shore producers from ‘dumping’ product in the NAFTA market.

7. Energy Costs

Energy looms large as a production cost. Figure 3.7 compares the approximate share of labour and energy and water in production costs. For Primary Steel Producers, energy costs almost the same as labour costs. An important implication for Primary Steel Producers is that increased efficiency in energy utilization is on par with increased labour productivity as a source of overall improvement in productive efficiency.

Figure 3.7 ‘Labour Share’ and ‘Energy and Water Share’ in Production Costs

Average 2004 – 20078 Statistics Canada, CANSIM

●

33

Chapter Four Employment Projections

1. Macroeconomic parameters 2. Technology impacts 3. Retirements and Quits 4. Primary Steel Producers 5. Construction Fabricators 6. Foundries 7. Metals Service Centres

The forecast scenarios set out in this chapter are based on four sources:

• a special forecast commissioned for this study from the Conference Board, • the Construction Sector Council’s forecast for the construction industry, • the Survey of Human Resources Managers undertaken for this study, and • occupational estimates developed by Prism Economics.

A forecast should be interpreted as a scenario that is based on expectations that are judged reasonable when the forecast is developed. For purposes of human resources planning, a forecast is helpful in identifying likely trends in employment if the macro-economic and technology assumptions on which the forecast rests are substantially borne out over the forecast period.

Macroeconomic Parameters

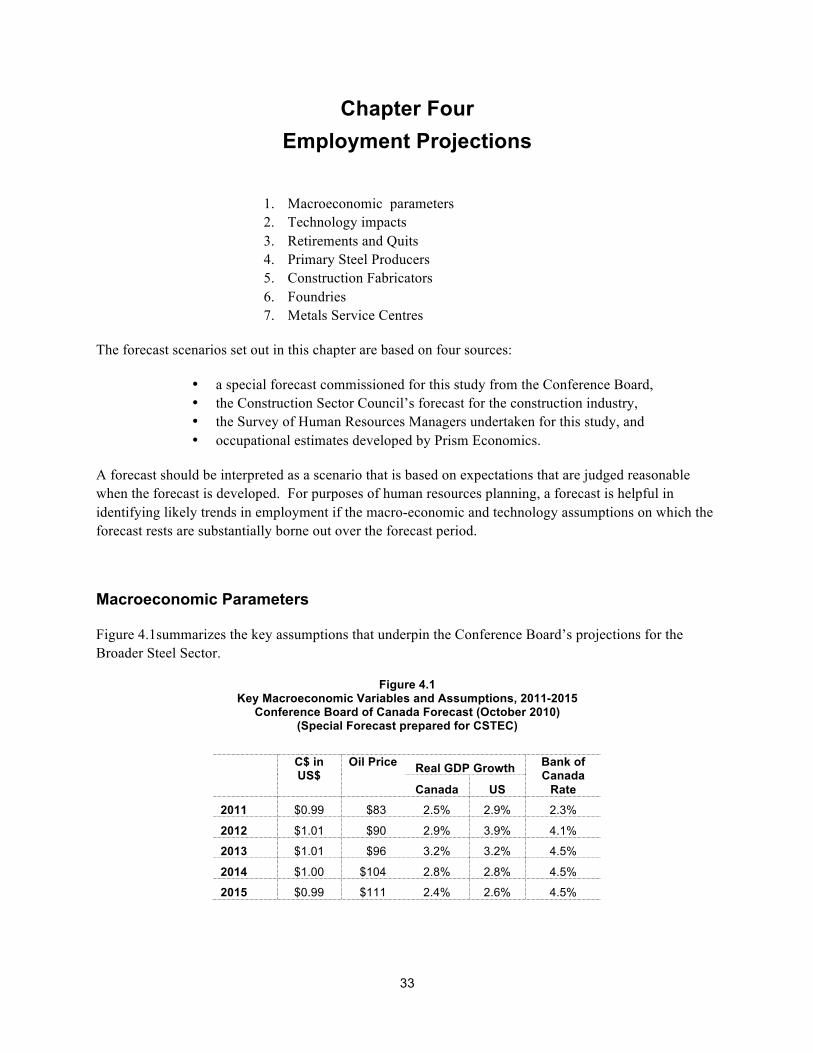

Figure 4.1summarizes the key assumptions that underpin the Conference Board’s projections for the Broader Steel Sector.

Figure 4.1 Key Macroeconomic Variables and Assumptions, 2011-2015

Conference Board of Canada Forecast (October 2010) (Special Forecast prepared for CSTEC)

C$ in US$

Oil Price Real GDP Growth Bank of Canada

Rate Canada US 2011 $0.99 $83 2.5% 2.9% 2.3%

2012 $1.01 $90 2.9% 3.9% 4.1%

2013 $1.01 $96 3.2% 3.2% 4.5%

2014 $1.00 $104 2.8% 2.8% 4.5%

2015 $0.99 $111 2.4% 2.6% 4.5%

34

These macroeconomic assumptions and expectations are broadly comparable to those of other forecasters:

Technology Impacts

From a human resources perspective, the principal impacts of changes in technology are on the occupational composition of the work force and on productivity trends. The principal drivers of productivity growth are changes in work organization (‘soft technologies’) and capital investment (‘hard technologies’). It is difficult to sustain productivity gains of more than 0.5% annually based solely on improvements in work organization, such as continuous improvement (kaizen) or total productive maintenance (TPM) strategies. To consistently achieve an average annual productivity growth of 1.0%, and especially 2.0% (or more), requires ongoing and significant increases in investment in new machinery and equipment. Some companies may pursue this strategy. However, in the medium-term, this is likely to be the exception, rather than the norm. In the main, the weak economic recovery will lead most companies to be exceedingly cautious about major investments in new technology. This implies that productivity growth will be slower than prior to the economic downturn, i.e. in the range of 0.5% to 1.0% per year.

The employment forecasts that are set out in the balance of this chapter present estimates based on 0.5%, 1.0% and 2.0% productivity growth, relative to pre-downturn levels of productivity. For human resources planning purposes, the 1.0% assumption reflects the most likely trend.

Retirements, Voluntary Quits and Permanent Lay-Offs

An exit rate, composed of projected retirements, voluntary quits, and permanent lay-offs has been estimated, based on responses to the Survey of Human Resources Managers. Different exit rates have been calculated for each of the four industries that comprise the Broader Steel Sector and for different occupational groups within these industries.

Primary Steel Producers

Figure 4.2 shows actual employment for 2008 to 2010, based on Statistics Canada’s Survey of Employment, Payroll and Hours and projections for employment over the period 2011 to 2015. The employment projections are based on alternative productivity assumptions and the Conference Board’s output forecast. In these scenarios productivity growth and employment growth are inversely related rather than directly related. That is to say, higher productivity growth reduces total labour requirements while lower productivity growth implies greater overall labour requirements.13

13 This should not be interpreted as a policy preference for lower productivity growth. In the longer run, low

productivity growth implies higher costs and reduced competitiveness – both of which call into question the

35

Figure 4.2 Primary Steel Producers (NAICS 3311)

Actual Employment: 2008- 2010 (Statistics Canada, CANSIM) Projected Employment: 2011-2015 based on Alternative

Productivity Assumptions and Projected Industry Output Conference Board of Canada Forecast (October 2010)

(Special Forecast prepared for CSTEC)

Under none of the productivity assumptions does employment in 2015 return to the 2008 level.

Figure 4.3 summarizes expected employment in the Primary Steel Producers by major occupational group, based on alternative productivity scenarios. The main impact of higher productivity growth is deemed to fall on workers in ‘production and materials handling’ occupations. Higher productivity growth is also expected to entail some degree of substitution of engineering and technology workers for tradespersons and production workers. Consequently, in the high productivity growth scenario, there is an increase in both the number and the share of engineering and technology workers.

Figure 4.3 Primary Steel Producers (NAICS 3311)

Projected Employment by Major Occupational Group (Prism Economics and Analysis)

2010 2015

(Alternative Productivity Scenarios) Low

(0.5%) Moderate

(1.0%) High

(2.0%) Trades 6,895 7,585 7,274 6,702 Production and Materials Handlers 5,155 5,475 5,325 4,970 Engineering and Technology 1,632 1,795 1,746 1,723 Administration 1,686 1,855 1,787 1,669 Management 832 905 882 816 Sales 526 572 552 516 Other 231 251 242 226 Total 16,957 18,438 17,808 16,622

continued viability of a manufacturing operation. Higher productivity growth is also the ultimate economic foundation of higher wages and salaries.

36

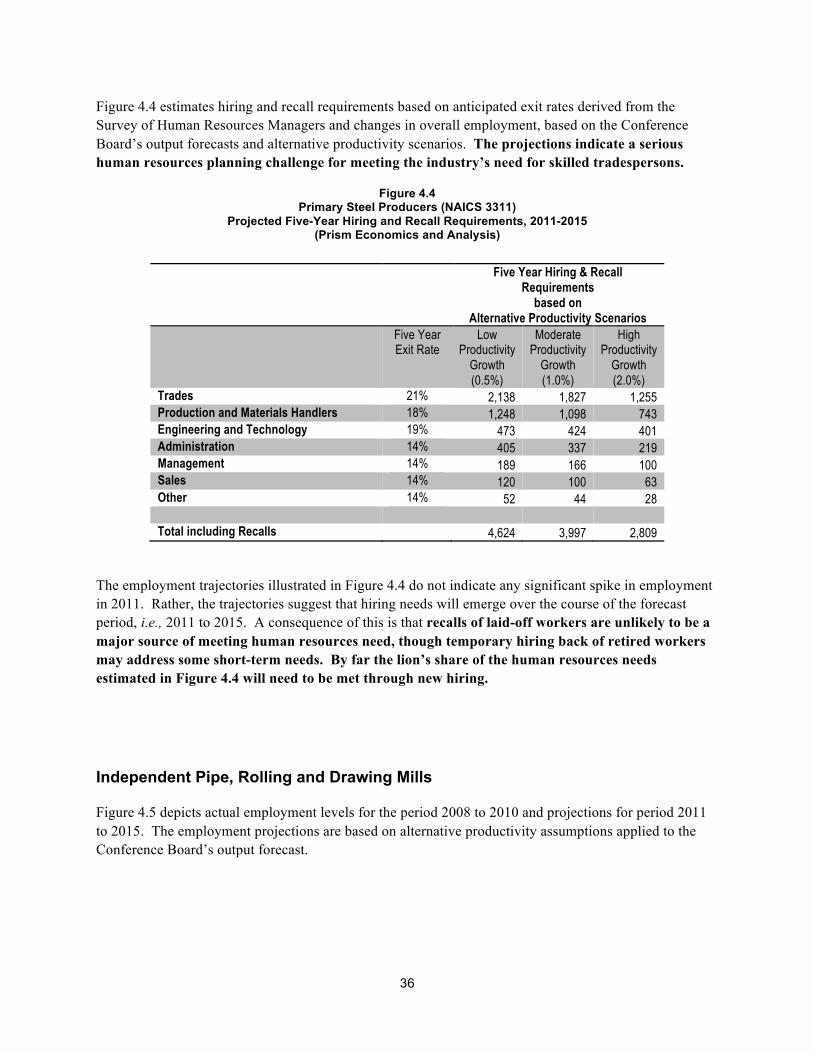

Figure 4.4 estimates hiring and recall requirements based on anticipated exit rates derived from the Survey of Human Resources Managers and changes in overall employment, based on the Conference Board’s output forecasts and alternative productivity scenarios. The projections indicate a serious human resources planning challenge for meeting the industry’s need for skilled tradespersons.

Figure 4.4 Primary Steel Producers (NAICS 3311)

Projected Five-Year Hiring and Recall Requirements, 2011-2015 (Prism Economics and Analysis)

Five Year Hiring & Recall Requirements

based on Alternative Productivity Scenarios

Five Year Exit Rate

Low Productivity

Growth (0.5%)

Moderate Productivity

Growth (1.0%)

High Productivity

Growth (2.0%)

Trades 21% 2,138 1,827 1,255 Production and Materials Handlers 18% 1,248 1,098 743 Engineering and Technology 19% 473 424 401 Administration 14% 405 337 219 Management 14% 189 166 100 Sales 14% 120 100 63 Other 14% 52 44 28

Total including Recalls 4,624 3,997 2,809

The employment trajectories illustrated in Figure 4.4 do not indicate any significant spike in employment in 2011. Rather, the trajectories suggest that hiring needs will emerge over the course of the forecast period, i.e., 2011 to 2015. A consequence of this is that recalls of laid-off workers are unlikely to be a major source of meeting human resources need, though temporary hiring back of retired workers may address some short-term needs. By far the lion’s share of the human resources needs estimated in Figure 4.4 will need to be met through new hiring.

Independent Pipe, Rolling and Drawing Mills

Figure 4.5 depicts actual employment levels for the period 2008 to 2010 and projections for period 2011 to 2015. The employment projections are based on alternative productivity assumptions applied to the Conference Board’s output forecast.

37

Figure 4.5 Independent Pipe, Rolling and Drawing Mills (NAICS 3312)

Actual Employment: 2008- 2010 (Statistics Canada, CANSIM) Projected Employment: 2011-2015 based on Alternative

Productivity Assumptions and Projected Industry Output Conference Board of Canada Forecast (October 2010)

(Special Forecast prepared for CSTEC)

The first and most important inference from the projections is that, under none of the productivity assumptions, is employment in 2015 projected to return to the 2008 level. Compared to 2008, industry output in 2015 is projected by the Conference Board to be down by approximately 4.6%. Employment levels in 2015 are forecast to be 8% to 17% lower than 2008. Relative to 2010, however, both employment and output are projected to increase. Roughly two-thirds of the projected increase in employment after 2010 is expected to occur in 2011 as the industry experiences a recovery that is approximately in line with the rest of the manufacturing sector. An important implication of this employment path is that a large fraction of the projected five-year hiring and recall requirement may be met through recalling laid off workers.

Figure 4.6 summarizes expected employment in pipe, rolling and drawing mills by major occupational group. The main impact of higher productivity growth is deemed to fall on workers in ‘production and materials handling’ occupations. Higher productivity growth is also expected to entail some degree of substitution of engineering and technology workers for tradespersons and production workers. Consequently, in the high productivity growth scenario, there is an increase in both the number and the share of engineering and technology workers.

38

Figure 4.6 Independent Pipe, Rolling and Drawing Mills (NAICS 3312)

Projected Employment by Major Occupational Group (Prism Economics and Analysis)

2010 2015

(Alternative Productivity Scenarios) Low

(0.5%) Moderate

(1.0%) High

(2.0%) Trades 2,792 3,679 3,490 3,125 Production and Materials Handlers 2,454 3,234 3,044 2,733 Engineering and Technology 544 717 771 827 Administration 949 1,250 1,240 1,230 Management 557 734 728 716 Sales 268 353 353 353

Total 7,564 9,967 9,626 8,984

Figure 4.7 estimates hiring and recall requirements based on anticipated exit rates derived from the Survey of Human Resources Managers and changes in overall employment, based on the Conference Board’s output forecasts and alternative productivity scenarios.

Figure 4.7 Independent Pipe, Rolling and Drawing Mills (NAICS 3312)

Projected Five-Year Hiring and Recall Requirements, 2011-2015 (Prism Economics and Analysis)

Five Year Hiring & Recall Requirements

based on Alternative Productivity Scenarios

Five Year Exit Rate

Low Productivity

Growth (0.5%)

Moderate Productivity

Growth (1.0%)

High Productivity

Growth (2.0%)

Trades 14% 1,277 1,089 724 Production and Materials Handlers 12% 1,074 884 573 Engineering and Technology 10% 227 281 337 Administration 10% 396 386 376 Management 8% 222 215 203 Sales 8% 107 106 106

Total Hiring and Recall Requirements 3,303 2,961 2,319

As noted earlier, most of the increase in employment over 2010 is expected to occur in 2011. This implies that a substantial portion of the estimated hiring and recall requirements will be met by recalling workers who were laid off during the downturn. Actual recruitment challenges are likely to be around 35%-45% of the estimates set out Figure 4.7. For skilled trades, this would imply five-year recruitment needs in the range of 290 to 510 persons.

39

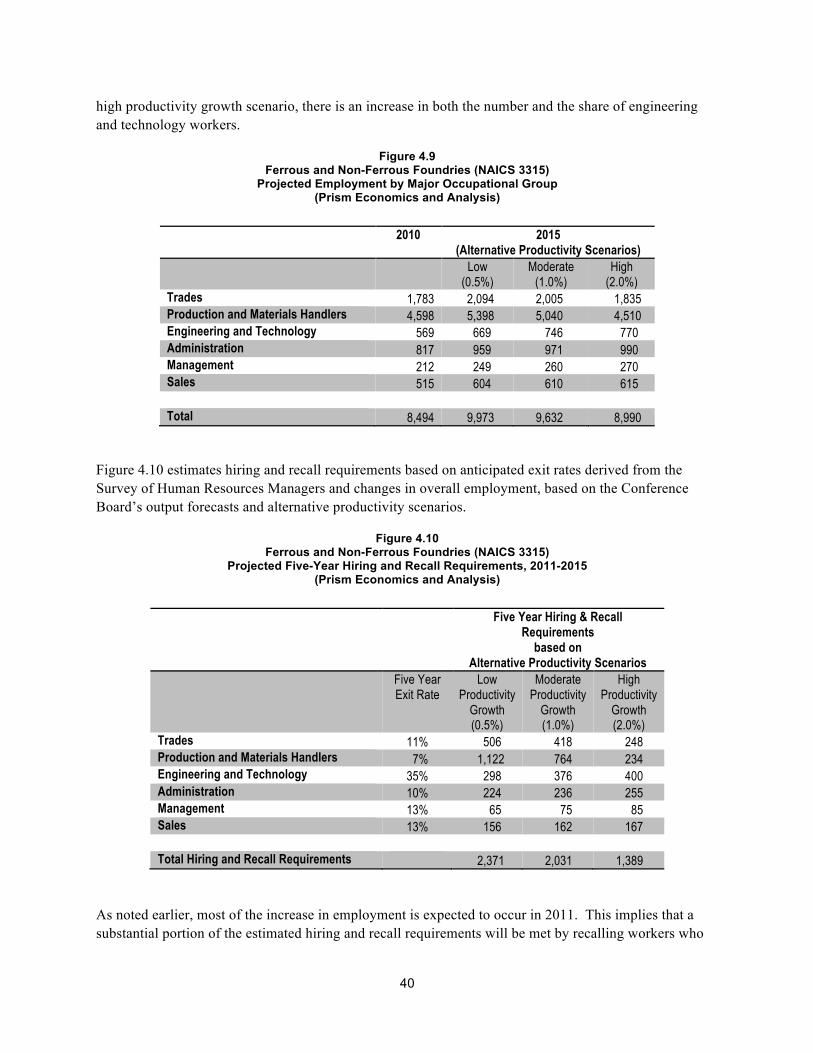

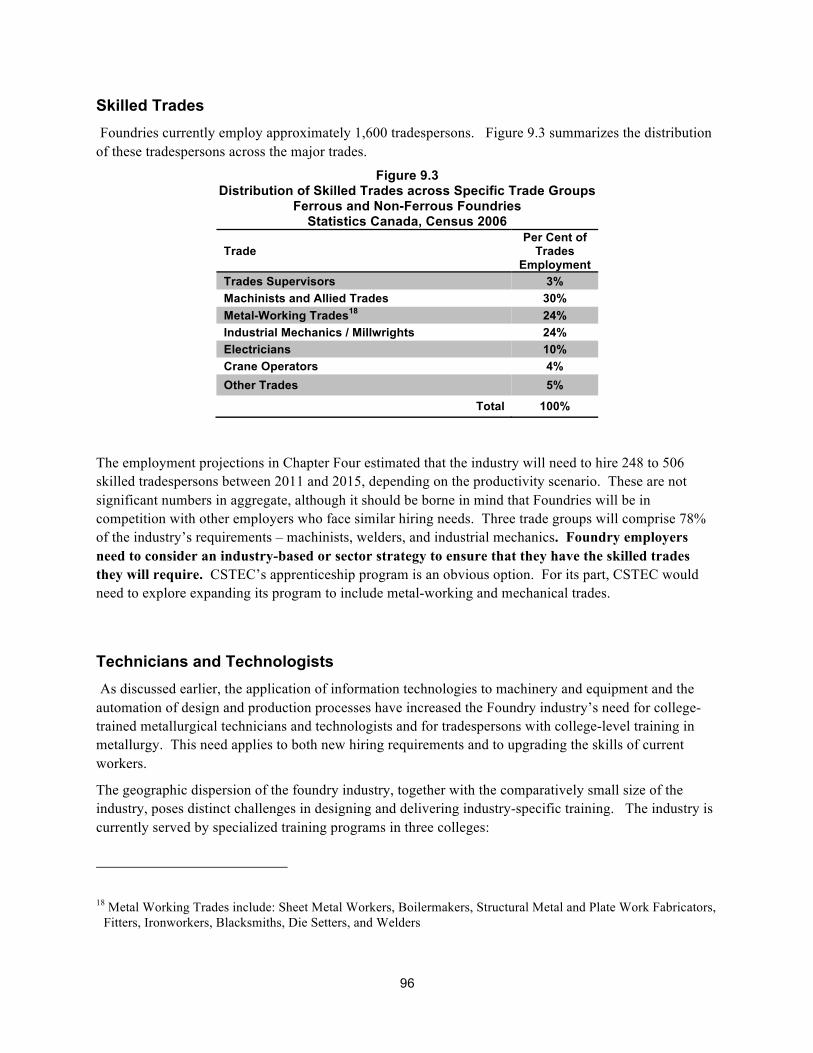

Foundries

Figure 4.8 shows the actual employment in 2008 to 2010 and projections for period 2011 to 2015. The data refer to both Ferrous and Non-Ferrous Foundries. The employment projections are based on alternative productivity assumptions applied to the Conference Board’s output forecast.

Figure 4.8 Ferrous and Non-Ferrous Foundries (NAICS 3315)

Actual Employment: 2008- 2010 (Statistics Canada, CANSIM) Projected Employment: 2011-2015 based on Alternative

Productivity Assumptions and Projected Industry Output Conference Board of Canada Forecast (October 2010)

(Special Forecast prepared for CSTEC)

The Conference Board anticipates that by 2015 output in the Foundries industry will be approximately 7.4% higher than in 2008. This projection is based on an expected recovery in the North American auto sector. Employment levels in the foundry industry depend on productivity and investment assumptions.