2011 fy financial results presentation · aciaria gusa nordeste brazil 1.2m tpy long products 2011...

TRANSCRIPT

2011 FY Financial Results Presentation April, 2012

Disclaimer

2

The materials contained in this document (together, the “Presentation”) has been prepared by OJSC KOKS (the “Company”) and are given in

conjunction with a live presentation and should not be taken out of context.

Some of the information in this Presentation may contain projections or other forward-looking statements regarding future events or the future financial

performance of the Company. You can identify forward looking statements by terms such as "expect", "believe", "anticipate", "estimate", "intend", "will",

"could," "may" or "might" the negative of such terms or other similar expressions. The Company wishes to caution you that these statements are only

predictions and that actual events or results may differ materially. The Company does not intend to update these statements to reflect events and

circumstances occurring after the date hereof or to reflect the occurrence of unanticipated events. Many factors could cause the actual results to differ

materially from those contained in projections or forward-looking statements of the Company, including, among others, general economic conditions, the

competitive environment, risks associated with operating in Russia, rapid technological and market change in the industries the Company operates in, as

well as many other risks specifically related to the Company and its operations.

Neither this Presentation nor any copy of it may be taken or transmitted, directly or indirectly, into the United States, Australia, Canada, Japan or the

Russian Federation. This Presentation does not constitute or form part of any offer or invitation to sell, or any solicitation of any offer to purchase or

subscribe nor shall it (or any part of it) or the fact of its distribution, form the basis of, or be relied on in connection with, any contract therefor. The offer

and the distribution of these materials and other information in connection with the listing and offer in certain jurisdictions may be restricted by law and

persons into whose possession any document or other information referred to herein comes should inform themselves about and observe any such

restriction. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such jurisdiction.

This Presentation is not an offer for sale of any securities in the United States. Securities may not be offered or sold in the United States or to, or for the

account or benefit of, U.S. person (as defined in Regulation S under the Securities Act of 1933) absent registration or an exemption from registration

under the U.S. Securities Act of 1933. The Company has not registered and does not intend to register any portion of any offering in the United States or

to conduct a public offering of any securities in the United States.

The Presentation is only addressed to and directed at persons in member states of the European Economic Area who are “qualified investors” within the

meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC) (“Qualified Investors”). In addition, in the United Kingdom, the Presentation

is being distributed only to, and is directed only at, Qualified Investors (i) who have professional experience in matters relating to investments falling

within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) and Qualified Investors falling within

Article 49(2)(a) to (d) of the Order, and (ii) to whom it may otherwise lawfully be communicated (all such persons together being referred to as “Relevant

Persons”). The Presentation must not be acted on or relied on (i) in the United Kingdom, by persons who are not Relevant Persons, and (ii) in any

member state of the European Economic Area other than the United Kingdom, by persons who are not Qualified Investors.

44,259

9,159

3,027 4,216

55,589

8,283

1,227

6,762

0

10 000

20 000

30 000

40 000

50 000

60 000

Revenue EBITDA Net income Capex

2010

2011

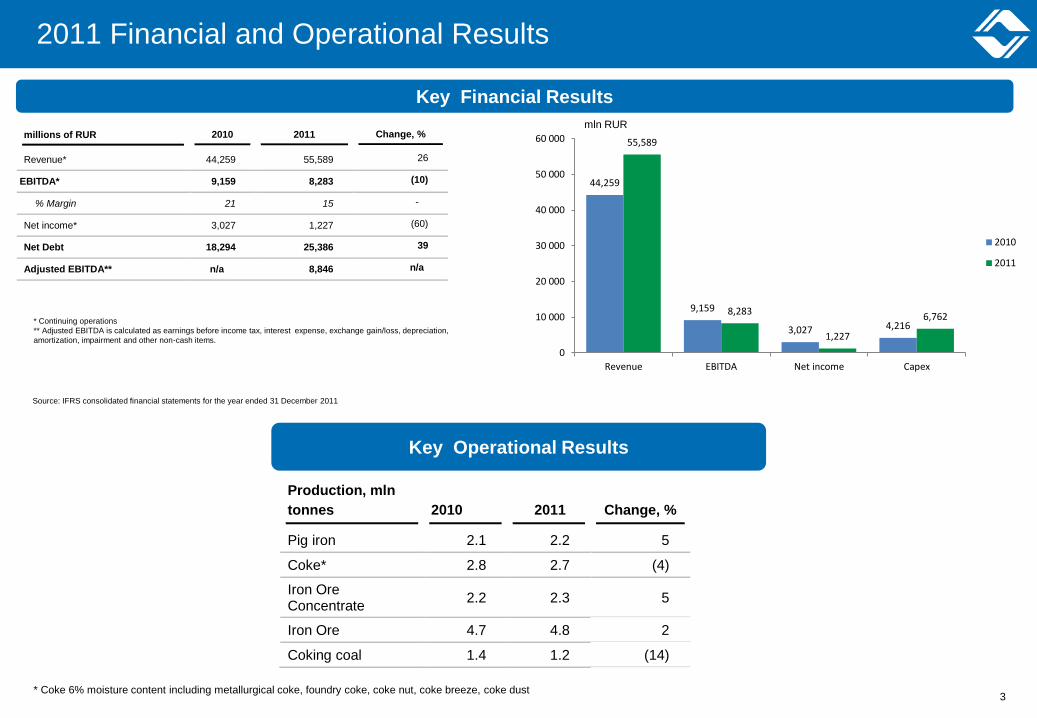

millions of RUR 2010 2011 Change, %

Revenue* 44,259 55,589 26

EBITDA* 9,159 8,283 (10)

% Margin 21 15 -

Net income* 3,027 1,227 (60)

Net Debt 18,294 25,386 39

Adjusted EBITDA** n/a 8,846 n/a

2011 Financial and Operational Results

Key Financial Results

mln RUR

Key Operational Results

Production, mln

tonnes

2010

2011

Change, %

Pig iron 2.1 2.2 5

Coke* 2.8 2.7 (4)

Iron Ore Concentrate

2.2 2.3 5

Iron Ore 4.7 4.8 2

Coking coal 1.4 1.2 (14)

* Continuing operations

** Adjusted EBITDA is calculated as earnings before income tax, interest expense, exchange gain/loss, depreciation,

amortization, impairment and other non-cash items.

* Coke 6% moisture content including metallurgical coke, foundry coke, coke nut, coke breeze, coke dust 3

Source: IFRS consolidated financial statements for the year ended 31 December 2011

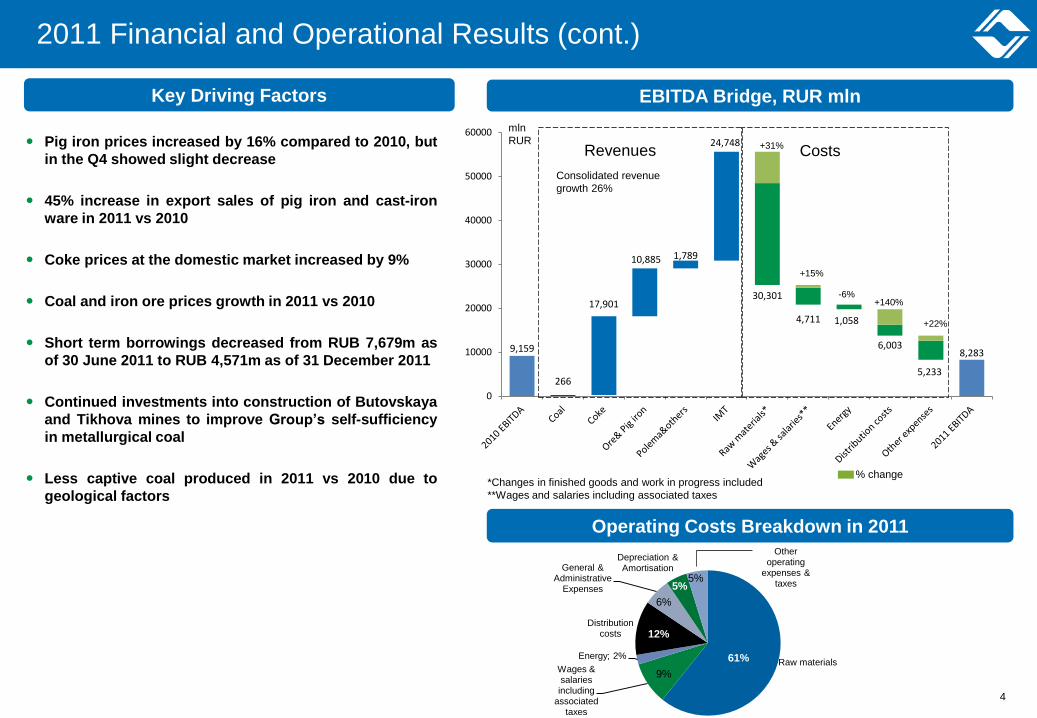

9,159 8,283

266

17,901

10,885 1,789

24,748

30,301

4,711 1,058

6,003

5,233

0

10000

20000

30000

40000

50000

60000 Pig iron prices increased by 16% compared to 2010, but

in the Q4 showed slight decrease

45% increase in export sales of pig iron and cast-iron

ware in 2011 vs 2010

Coke prices at the domestic market increased by 9%

Coal and iron ore prices growth in 2011 vs 2010

Short term borrowings decreased from RUB 7,679m as

of 30 June 2011 to RUB 4,571m as of 31 December 2011

Continued investments into construction of Butovskaya

and Tikhova mines to improve Group’s self-sufficiency

in metallurgical coal

Less captive coal produced in 2011 vs 2010 due to

geological factors

2011 Financial and Operational Results (cont.)

4

Key Driving Factors

Consolidated revenue

growth 26%

EBITDA Bridge, RUR mln

Operating Costs Breakdown in 2011

*Changes in finished goods and work in progress included

**Wages and salaries including associated taxes

Revenues Costs

% change

+31%

+15%

+140%

+22%

-6%

mln

RUR

4

Raw materials Wages & salaries including

associated taxes

Energy; 2%

Distribution costs

General & Administrative

Expenses

Depreciation & Amortisation

Other operating

expenses & taxes

61%

5% 5%

6%

12%

9%

Segmental Overview

External revenue, % EBITDA by segments

2011 total: RUR 8,283 mln

2010 total: RUR 9,159 mln

EBITDA margin, %

2011 total:

55,589

2010 total:

44,259

5

32% 38%

20%

55%

4%

4%

44%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2010

IMT

Polema & other

Ore & Pig iron

Coke22%

31%

44%

-1%

4%

-20

0

20

40

60

80

100

120

2011

Coal Coke Ore & Pig Iron Polema & other IMT

9.8%

50.8%

36.7%

2.7%

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2010

Coal Coke Ore & Pig Iron Polema, IMT, & other

17

7

12 10

1 0

2

4

6

8

10

12

14

16

18

Coal Coke Ore & Pig Iron Polema IMT

0

20

40

60

80

100

120

2011 2010

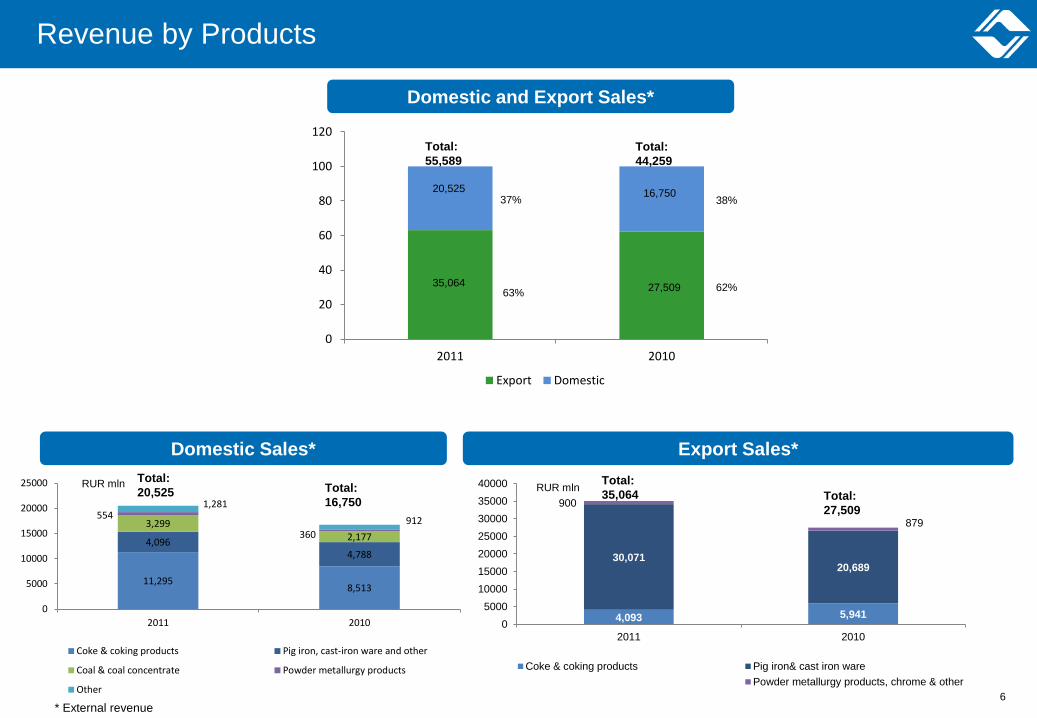

Export Domestic

4,093 5,941

30,071 20,689

900

879

0

5000

10000

15000

20000

25000

30000

35000

40000

2011 2010

Coke & coking products Pig iron& cast iron ware

#REF! Powder metallurgy products, chrome & other

11,295 8,513

4,096 4,788

3,299

2,177

554

360

1,281

912

0

5000

10000

15000

20000

25000

2011 2010

Coke & coking products Pig iron, cast-iron ware and other

Coal & coal concentrate Powder metallurgy products

Other

Revenue by Products

Domestic Sales* Export Sales*

RUR mln RUR mln

Domestic and Export Sales*

* External revenue

35,064 27,509

20,525 16,750 37%

63%

38%

62%

Total:

55,589

Total:

44,259

Total:

35,064 Total:

27,509

Total:

20,525 Total:

16,750

6

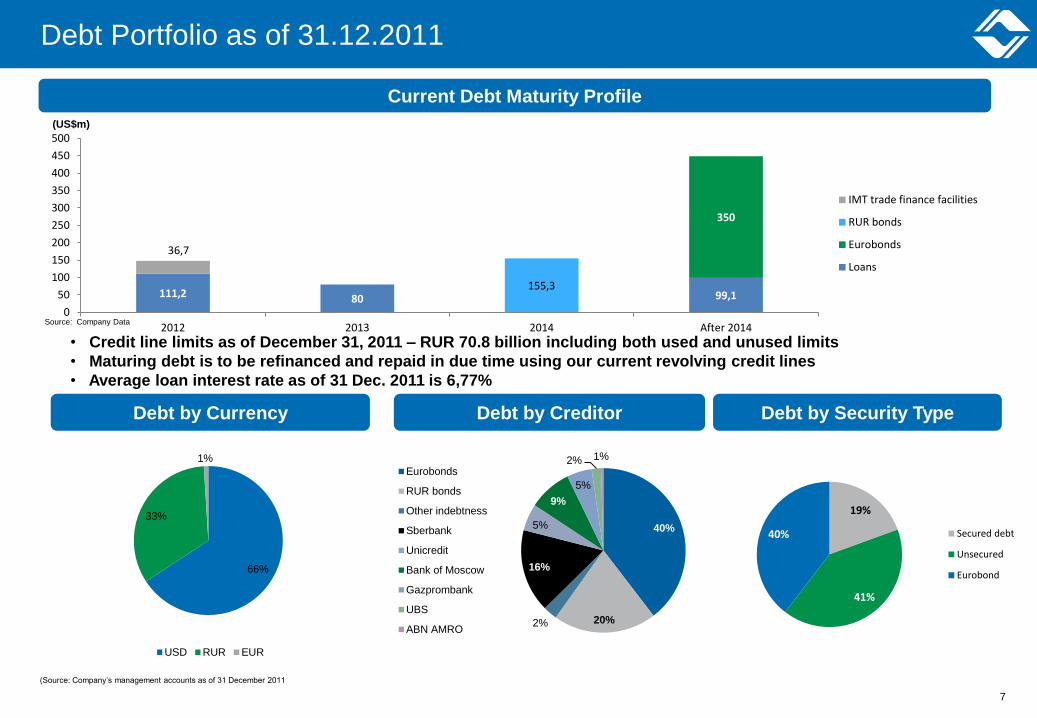

111,2 80 99,1

350

155,3

36,7

0

50

100

150

200

250

300

350

400

450

500

2012 2013 2014 After 2014

IMT trade finance facilities

RUR bonds

Eurobonds

Loans

Debt Portfolio as of 31.12.2011

Current Debt Maturity Profile

Debt by Currency

(Source: Company’s management accounts as of 31 December 2011

(US$m)

Source: Company Data

Debt by Creditor

• Credit line limits as of December 31, 2011 – RUR 70.8 billion including both used and unused limits

• Maturing debt is to be refinanced and repaid in due time using our current revolving credit lines

• Average loan interest rate as of 31 Dec. 2011 is 6,77%

66%

33%

1%

USD RUR EUR

40%

20% 2%

16%

5%

9%

5%

2% 1%

Eurobonds

RUR bonds

Other indebtness

Sberbank

Unicredit

Bank of Moscow

Gazprombank

UBS

ABN AMRO

Debt by Security Type

19%

41%

40% Secured debt

Unsecured

Eurobond

7

Overview of Key Financials

Income Statement Highlights Balance Sheet Highlights

millions of RUR 2010 2011

Revenue* 44,259 55,589

Cost of sales* (32,065) (39,570)

Gross profit* 12,194 16,019

Gross profit margin

28% 29%

Operating profit* 6,394 5,743

Operating profit margin

14% 10%

Net Income * 3,027 1,227

Adjusted EBITDA n/a 8,846

millions of RUR

December 31,

2010

December 31,

2011

Total Assets 52,022 56,618

Total Liabilities 31,974 35,033

Total Equity 20,048 21,585

Property Plant & Equipment 24,299 28,337

Total Debt 21,245 25,566

Cash & Cash Equivalents** 2,951 180

Net Debt 18,294 25,386

** Cash & cash equivalents including restricted cash

* Continuing operations

Cash Flow Highlights

millions of RUR 2010 2011

Profit before income tax 3,891 1,728

Operating cash flows before working capital changes

9,251 8,488

Net cash from operating activities of continuing operations

7,915 4,856

Net cash (used from)/ in investment activities

680 (6,251)

Net cash used in financing activities

(6,378) (1,623)

8

Source: IFRS consolidated financial statements for the year ended 31 December 2011

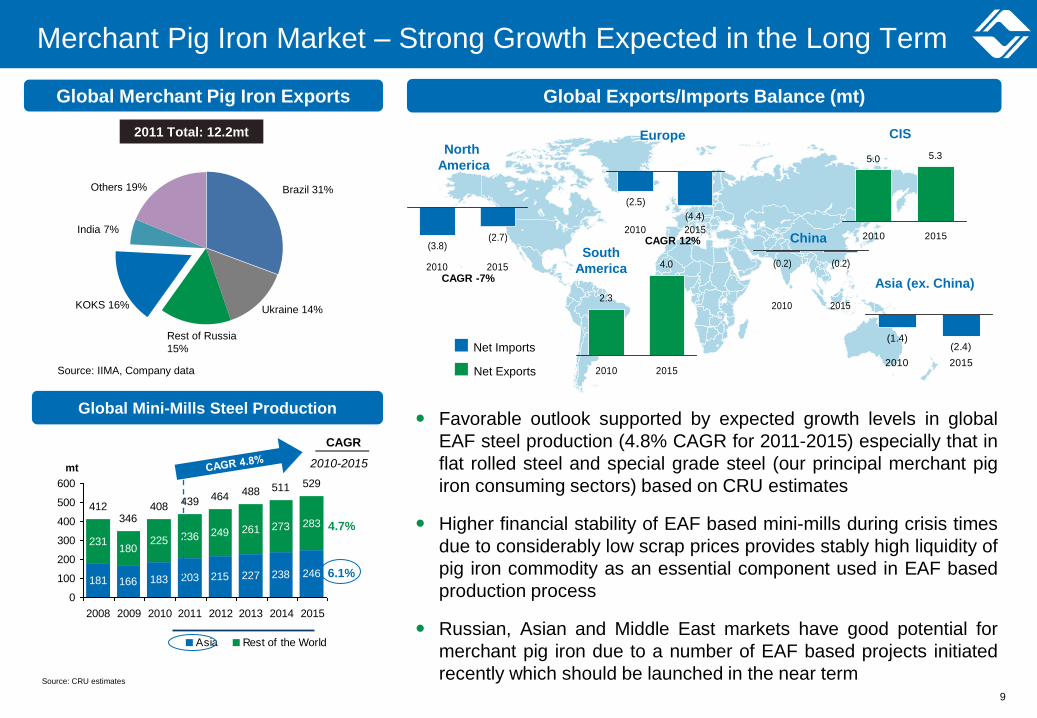

Source: CRU estimates

China (3.8)

(2.7)

2010 2015

2.3

4.0

2010 2015

5.0 5.3

2010 2015

(1.4)(2.4)

2010 2015

Europe

(2.5)

(4.4)

2010 2015

(0.2) (0.2)

2010 2015

Net Imports

Net Exports

South

America

CIS North

America

Asia (ex. China)

Favorable outlook supported by expected growth levels in global

EAF steel production (4.8% CAGR for 2011-2015) especially that in

flat rolled steel and special grade steel (our principal merchant pig

iron consuming sectors) based on CRU estimates

Higher financial stability of EAF based mini-mills during crisis times

due to considerably low scrap prices provides stably high liquidity of

pig iron commodity as an essential component used in EAF based

production process

Russian, Asian and Middle East markets have good potential for

merchant pig iron due to a number of EAF based projects initiated

recently which should be launched in the near term

CAGR -7%

CAGR 12%

Merchant Pig Iron Market – Strong Growth Expected in the Long Term

Global Exports/Imports Balance (mt)

181 166 183 203 215 227 238 246

231180

225 236 249 261 273 283

412346

408 439 464 488 511 529

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015

Asia Rest of the World

4.7%

6.1%

CAGR

2010-2015

Global Mini-Mills Steel Production

mt

Global Merchant Pig Iron Exports

2011 Total: 12.2mt

KOKS 16% Ukraine 14%

Brazil 31% Others 19%

India 7%

Rest of Russia

15%

Source: IIMA, Company data

9

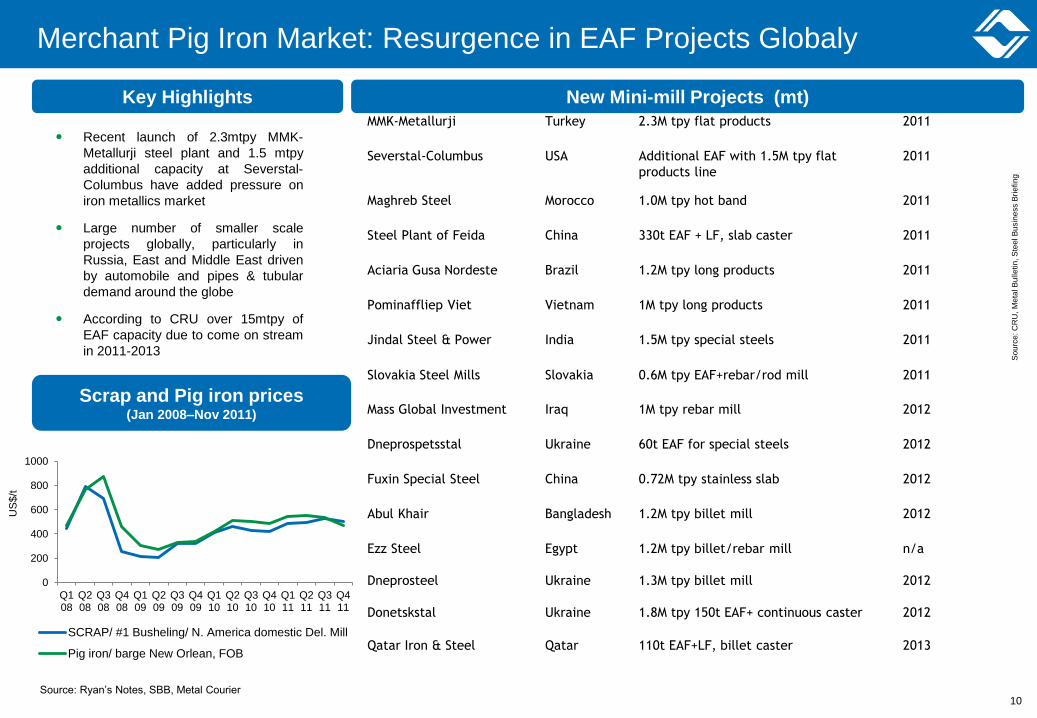

Steelmaker Location Main details Start-up

MMK-Metallurji Turkey 2.3M tpy flat products 2011

Severstal-Columbus USA Additional EAF with 1.5M tpy flat

products line

2011

Maghreb Steel Morocco 1.0M tpy hot band 2011

Steel Plant of Feida China 330t EAF + LF, slab caster 2011

Aciaria Gusa Nordeste Brazil 1.2M tpy long products 2011

Pominaffliep Viet Vietnam 1M tpy long products 2011

Jindal Steel & Power India 1.5M tpy special steels 2011

Slovakia Steel Mills Slovakia 0.6M tpy EAF+rebar/rod mill 2011

Mass Global Investment Iraq 1M tpy rebar mill 2012

Dneprospetsstal Ukraine 60t EAF for special steels 2012

Fuxin Special Steel China 0.72M tpy stainless slab 2012

Abul Khair Bangladesh 1.2M tpy billet mill 2012

Ezz Steel

Dneprosteel

Donetskstal

Egypt

Ukraine

Ukraine

1.2M tpy billet/rebar mill

1.3M tpy billet mill

1.8M tpy 150t EAF+ continuous caster

n/a

2012

2012

Qatar Iron & Steel

Qatar

110t EAF+LF, billet caster

2013

So

urc

e: C

RU

, M

eta

l B

ulle

tin

, S

tee

l B

usin

ess B

rie

fin

g

Recent launch of 2.3mtpy MMK-

Metallurji steel plant and 1.5 mtpy

additional capacity at Severstal-

Columbus have added pressure on

iron metallics market

Large number of smaller scale

projects globally, particularly in

Russia, East and Middle East driven

by automobile and pipes & tubular

demand around the globe

According to CRU over 15mtpy of

EAF capacity due to come on stream

in 2011-2013

Merchant Pig Iron Market: Resurgence in EAF Projects Globaly

New Mini-mill Projects (mt) Key Highlights

Scrap and Pig iron prices (Jan 2008–Nov 2011)

0

200

400

600

800

1000

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

SCRAP/ #1 Busheling/ N. America domestic Del. Mill

Pig iron/ barge New Orlean, FOB

US

$/t

Source: Ryan’s Notes, SBB, Metal Courier 10

So

urc

e: S

tee

l B

usin

ess B

rie

fin

g

Merchant Pig Iron Market: Resurgence in EAF Projects in Russia

Company/

Investor

Project

Region

EAF size; capacity

Main

products

Geographic

markets

Start‐up/ Status

Volga Electro-

metallurgical

Plant (VEMZ)

Volga

Electrometallurgi-

cal Plant (VEMZ)

Ivanovo 300,000 t/y Rebar Central federal

district

Q2 2012/ Under

Construction

NLMK Kaluga mini‐mill Kaluga 120t;

1.5m t/y

Rebar, light

sections

Central federal

district

2012/ Nearing

Completion

Ural Mining

and Metals (UGMK)

Tyumen

mill

Tyumen 70t;

0,55m t/y

Bars,

light sections

Regions of

Urals federal District

Early 2013/

Well Advanced

Severstal Balakovo

mini‐mill

Balakovo,

Saratov

120t; 1.1m

t/y

Rebar, light

sections

Volga + Central

federal districts

2013/

Construction ongoing

TMK Taganrog

Steel

Plant (Tagmet)

Taganrog,

Rostov

135t; 1m t/y Tube

rounds

Russia +

abroad

Q2 2013/

Construction ongoing

Novorosmetall Abinsk

Electrometallur-

gical Plant

Abinsk,

Krasnodar

territory

130t; 1.3m

t/y

Rebar Southern federal

district

Q4 2013/

Construction ongoing

Trabikum Ltd

(successor to

Maxi‐invest)

Tatstal Leninogorsk,

Tatarstan

120t; 1m t/y Rebar,

light sections

Tatarstan +

surrounding

regions

2014/

Construction underway

Investor unknown

(used to be Maxi‐

Invest)

Kovrov

plant

Kovrov,

Vladimir

120t;

1.2m t/y

Rebar, light

sections

Central + NW

federal districts

2014/ Construction yet

to begin

Ruspolymet Micro‐mill

Kulebaki,

Nizhny Novgorod

40t;

350,000 t/y

Rebar

Nizhny Novgorod

+ surrounds

Undecided

Stavropol

Steel

(Stavstal)

Rebar

rolling mill

Stavropol 350,000t/y Rebar, wire

rod

Southern +

North Caucasian

federal districts

Stage 1,

Q3 2012 //

500,000 t/y EAF

planned for stage 2

Moscow

government

Casting-rolling

plant

Yartsevo,

Smolensk

40t;

210,000 t/y

Rebar Regions of Central

federal district

Undecided

OMK Vyksa Steel Works Vyksa,Nizhny

Novgorod

160t; 1.5m

t/y

Thin slab for pipe

feed

All across Russia Undecided

Metallurgical Investment

Co

OHF replacement Chusovoy, Perm

territory

0.9‐1m t/y Spring steel All Russia Undecided

11

Source: Company data, RZhD statistics

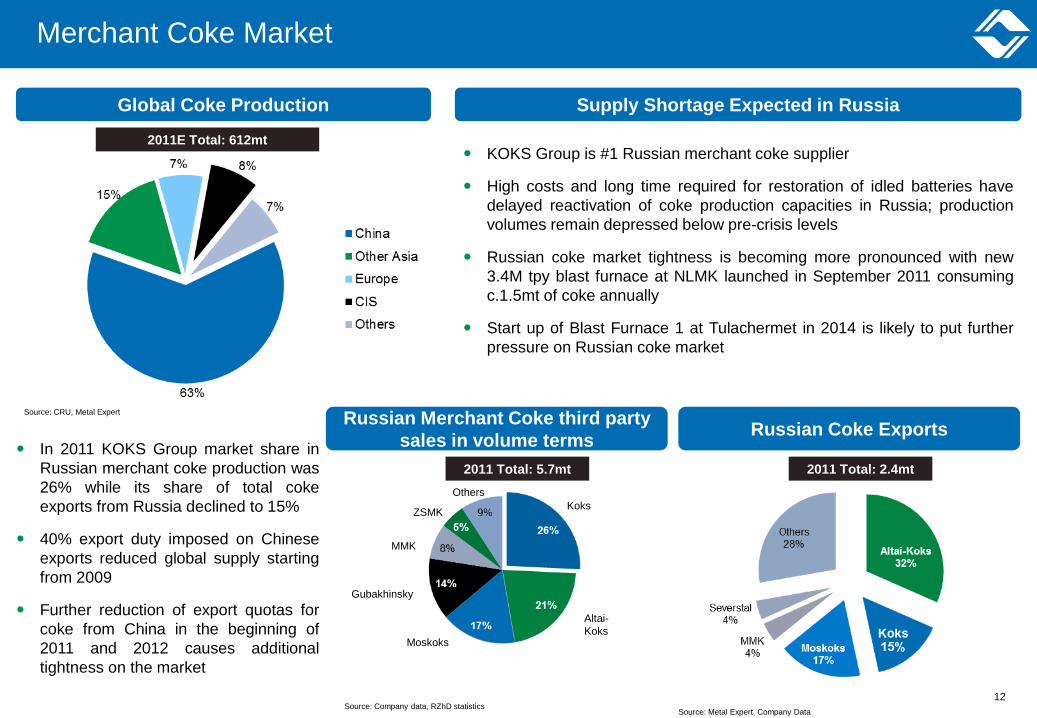

Merchant Coke Market

In 2011 KOKS Group market share in

Russian merchant coke production was

26% while its share of total coke

exports from Russia declined to 15%

40% export duty imposed on Chinese

exports reduced global supply starting

from 2009

Further reduction of export quotas for

coke from China in the beginning of

2011 and 2012 causes additional

tightness on the market

Russian Merchant Coke third party

sales in volume terms Russian Coke Exports

2011 Total: 5.7mt 2011 Total: 2.4mt

Source: CRU, Metal Expert

Global Coke Production

2011E Total: 612mt KOKS Group is #1 Russian merchant coke supplier

High costs and long time required for restoration of idled batteries have

delayed reactivation of coke production capacities in Russia; production

volumes remain depressed below pre-crisis levels

Russian coke market tightness is becoming more pronounced with new

3.4M tpy blast furnace at NLMK launched in September 2011 consuming

c.1.5mt of coke annually

Start up of Blast Furnace 1 at Tulachermet in 2014 is likely to put further

pressure on Russian coke market

Supply Shortage Expected in Russia

Koks

Gubakhinsky

Altai-

Koks

Others

Moskoks

MMK

Source: Metal Expert, Company Data

12

ZSMK

Цена

концентрата

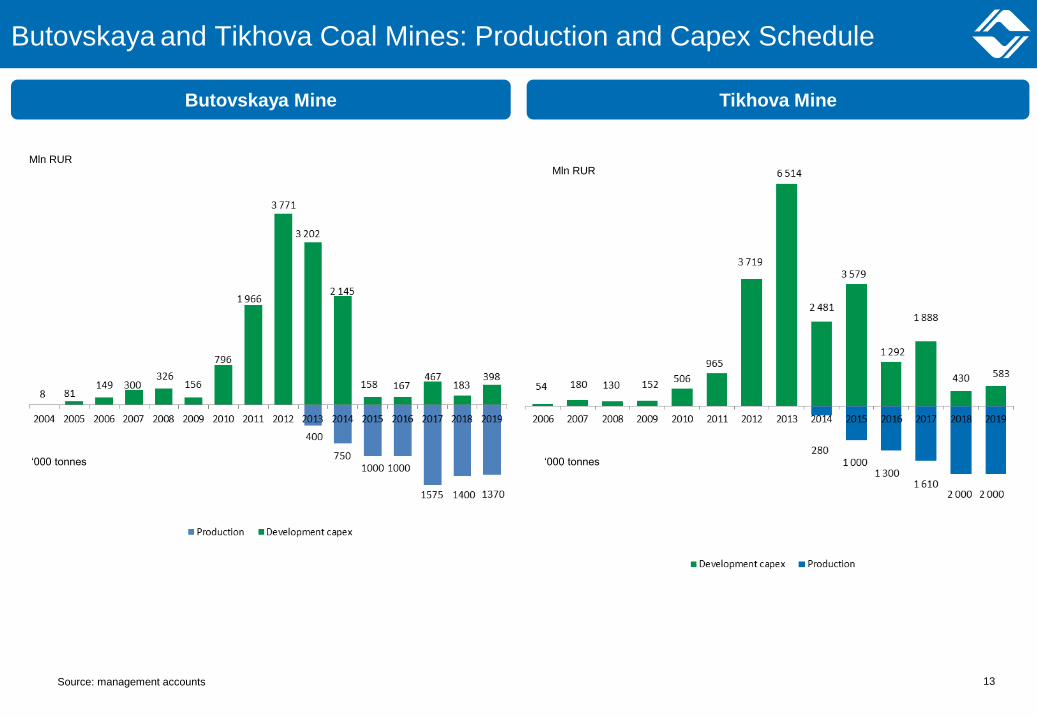

Butovskaya and Tikhova Coal Mines: Production and Capex Schedule

Mln RUR

‘000 tonnes

Butovskaya Mine Tikhova Mine

Mln RUR

‘000 tonnes

Source: management accounts 13

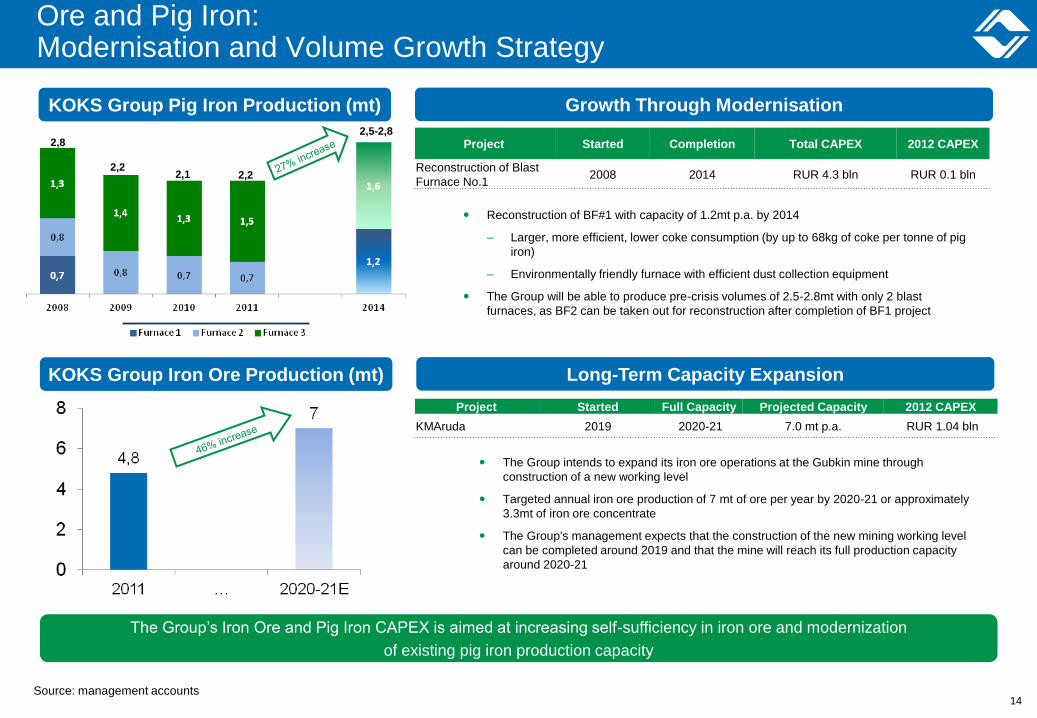

Ore and Pig Iron: Modernisation and Volume Growth Strategy

Growth Through Modernisation KOKS Group Pig Iron Production (mt)

Long-Term Capacity Expansion KOKS Group Iron Ore Production (mt)

The Group’s Iron Ore and Pig Iron CAPEX is aimed at increasing self-sufficiency in iron ore and modernization

of existing pig iron production capacity

Project Started Completion Total CAPEX 2012 CAPEX

Reconstruction of Blast

Furnace No.1 2008 2014 RUR 4.3 bln RUR 0.1 bln

Project Started Full Capacity Projected Capacity 2012 CAPEX

KMAruda 2019 2020-21 7.0 mt p.a. RUR 1.04 bln

14 Source: management accounts

2,5-2,8

2,2 2,2

2,1

2,8

Reconstruction of BF#1 with capacity of 1.2mt p.a. by 2014

– Larger, more efficient, lower coke consumption (by up to 68kg of coke per tonne of pig

iron)

– Environmentally friendly furnace with efficient dust collection equipment

The Group will be able to produce pre-crisis volumes of 2.5-2.8mt with only 2 blast

furnaces, as BF2 can be taken out for reconstruction after completion of BF1 project

The Group intends to expand its iron ore operations at the Gubkin mine through

construction of a new working level

Targeted annual iron ore production of 7 mt of ore per year by 2020-21 or approximately

3.3mt of iron ore concentrate

The Group's management expects that the construction of the new mining working level

can be completed around 2019 and that the mine will reach its full production capacity

around 2020-21

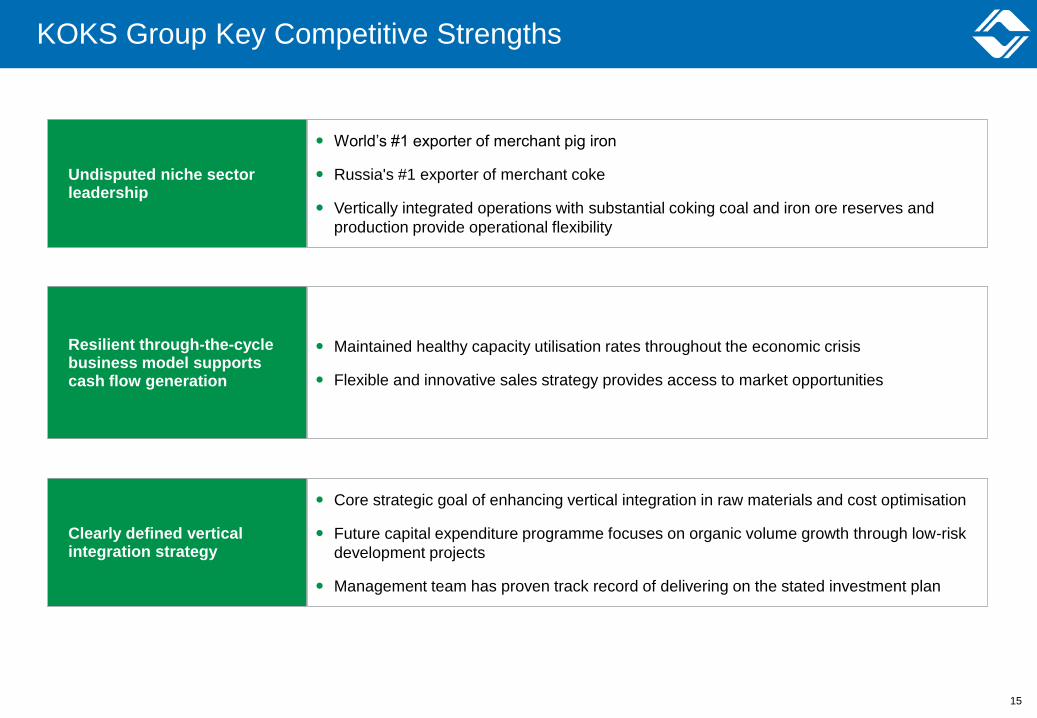

World’s #1 exporter of merchant pig iron

Russia's #1 exporter of merchant coke

Vertically integrated operations with substantial coking coal and iron ore reserves and

production provide operational flexibility

Undisputed niche sector leadership

Maintained healthy capacity utilisation rates throughout the economic crisis

Flexible and innovative sales strategy provides access to market opportunities

Resilient through-the-cycle business model supports cash flow generation

Core strategic goal of enhancing vertical integration in raw materials and cost optimisation

Future capital expenditure programme focuses on organic volume growth through low-risk

development projects

Management team has proven track record of delivering on the stated investment plan

Clearly defined vertical integration strategy

KOKS Group Key Competitive Strengths

15