2012 summary of california land sales …€¦ · 2012 summary of california land sales ......

TRANSCRIPT

2012 SUMMARY OF CALIFORNIA LAND SALES

23rd Annual LA/OC Market Trends Seminar

Appraisal Institute – Southern California ChapterThursday, January 28, 2016 – 10:15 a.m.

Garden Grove, CA

Presenter:

Tom Reimers

President – CA Division

Land Advisors Organization

2015/2016 Land Market Update

135 121 85 79

$1.51

$1.40

$0.71

$1.05

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

Q1-2015 Q2-2015 Q3-2015 Q4-2015

0

20

40

60

80

100

120

140

160

Bill

ion

s o

f $

in S

ales

Nu

mb

er o

f Tr

ansa

ctio

ns

# of Deals Total Consideration

2015 Headline NumbersCALIFORNIA LAND SALES

Source: Land Advisors Organization research

420 Total Transactions (-27.6%)

$4.66B Total Sales (-8.5%)

$11.1M Avg. SP (+26.3%)

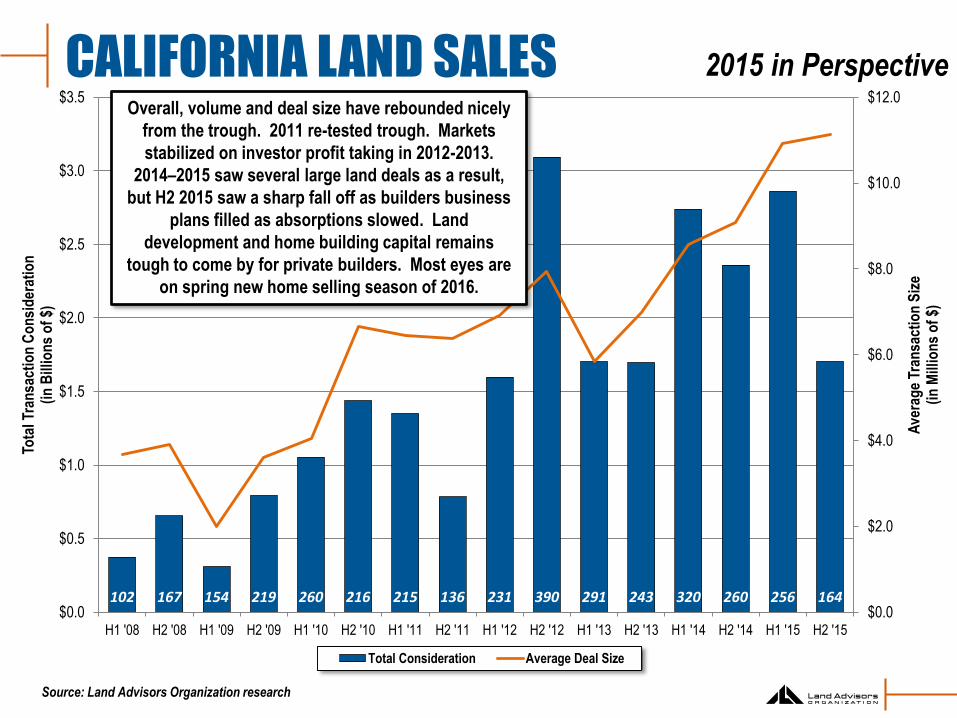

102 167 154 219 260 216 215 136 231 390 291 243 320 260 256 164$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

H1 '08 H2 '08 H1 '09 H2 '09 H1 '10 H2 '10 H1 '11 H2 '11 H1 '12 H2 '12 H1 '13 H2 '13 H1 '14 H2 '14 H1 '15 H2 '15

Ave

rag

e Tr

ansa

ctio

n S

ize

(in

Mill

ion

s o

f $)

Tota

l Tra

nsa

ctio

n C

on

sid

erat

ion

(in

Bill

ion

s o

f $)

Total Consideration Average Deal Size

Overall, volume and deal size have rebounded nicely

from the trough. 2011 re-tested trough. Markets

stabilized on investor profit taking in 2012-2013.

2014–2015 saw several large land deals as a result,

but H2 2015 saw a sharp fall off as builders business

plans filled as absorptions slowed. Land

development and home building capital remains

tough to come by for private builders. Most eyes are

on spring new home selling season of 2016.

CALIFORNIA LAND SALES

Source: Land Advisors Organization research

2015 in Perspective

S. CALIFORNIA LOT VALUES

Source: Land Advisors Organization research

2015 in Perspective

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%Q

1 2

00

4

Q2

20

04

Q3

20

04

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

Q3

20

06

Q4

20

06

Q1

20

07

Q2

20

07

Q3

20

07

Q4

20

07

Q1

20

08

Q2

20

08

Q3

20

08

Q4

20

08

Q1

20

09

Q2

20

09

Q3

20

09

Q4

20

09

Q1

20

10

Q2

20

10

Q3

20

10

Q4

20

10

Q1

20

11

Q2

20

11

Q3

20

11

Q4

20

11

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

12

Q1

20

13

Q2

20

13

Q3

20

13

Q4

20

13

Q1

20

14

Q2

20

14

Q3

20

14

Q4

20

14

Q1

20

15

Q2

20

15

Q3

20

15

Q4

20

15

Fin

ish

ed L

ot

Val

ue

YO

Y C

han

ge

W. Riv. Co San Bern. High Des.

San Bern. Basin Coachella Valley

L.A. Co. - Ant. Valley L.A. Co. - Santa Clarita

Ventura Co. San Diego

Avg. Value Peak-> Trough-> Current as Year-Over-Year Lot Value Change

AREA Q4 '15 Peak Trough Trough Current % of Peak Q4 ‘14 Q1 ‘15 Q2 ‘15 Q3 ‘15 Q4 ’15

NORTHERN CENTRAL VALLEY

(14 Markets)$132,917 $236,250 $55,000 (76.8%) 113.4% 47.6% 13.3% 12.3% 10.8% 16.4% 14.7%

BAY AREA

(15 Markets)$486,563 -- $185,000 -- 188.4% -- 12.6% 11.7% 13.1% 20.8% 16.7%

LOWER CENTRAL VALLEY

(10 Markets)$71,000 $115,000 $44,850 (58.6%) 56.9% 67.0% 11.6% 0.0% 0.0% 0.0% 0.0%

VENTURA CO.

(8 Markets)$235,625 $544,000 $189,000 (64.4%) 36.9% 48.5% 4.5% 6.0% 6.4% 4.8% 4.8%

LOS ANGELES – ANTELOPE VALLEY

(4 Markets)$77,500 $165,000 $45,000 (72.7%) 71.5% 46.7% (6.2%) (4.9%) 1.4% 1.4% 1.4%

LOS ANGELES – SANTA CLARITA

(4 Markets)$243,750 $313,750 $130,000 (57.7%) 73.8% 72.9% 0.6% (1.7%) 2.4% 4.1% 4.5%

SAN BERNARDINO – HIGH DESERT

(4 Markets)$72,250 $128,750 $41,250 (68.0%) 75.6% 56.1% 0.0% 4.6% 7.6% 2.9% 10.2%

SAN BERNARDINO – BASIN

(11 Markets)$208,182 $282,727 $111,932 (60.5%) 82.1% 71.6% (6.0%) (5.3%) (3.5%) (1.8%) 6.7%

RIVERSIDE – WESTERN

(17 Markets)$140,250 $206,553 $72,395 (65.2%) 92.2% 66.3% (6.1%) (6.2%) (4.1%) (3.1%) 3.3%

RIVERSIDE – COACHELLA

(12 Markets)$168,000 $217,917 $81,708 (64.7%) 105.9% 71.9% 0.0% (1.8%) (2.0%) (2.9%) (4.6%)

SAN DIEGO

(9 Markets)$422,778 -- -- -- -- -- 3.2% 5.8% 6.9% 8.4% 9.1%

CALIFORNIA STATEWIDE

(107 Markets)$223,655 $257,930 $104,746 (63.4%) 89.8% 64.1% 3.2% 3.8% 4.9% 6.3% 7.0%

CALIFORNIA FINISHED LOT VALUE METRICS

Source: Land Advisors Organization research

Selected Regions – 2003 through 2015

0%

10%

20%

30%

40%

50%

60%

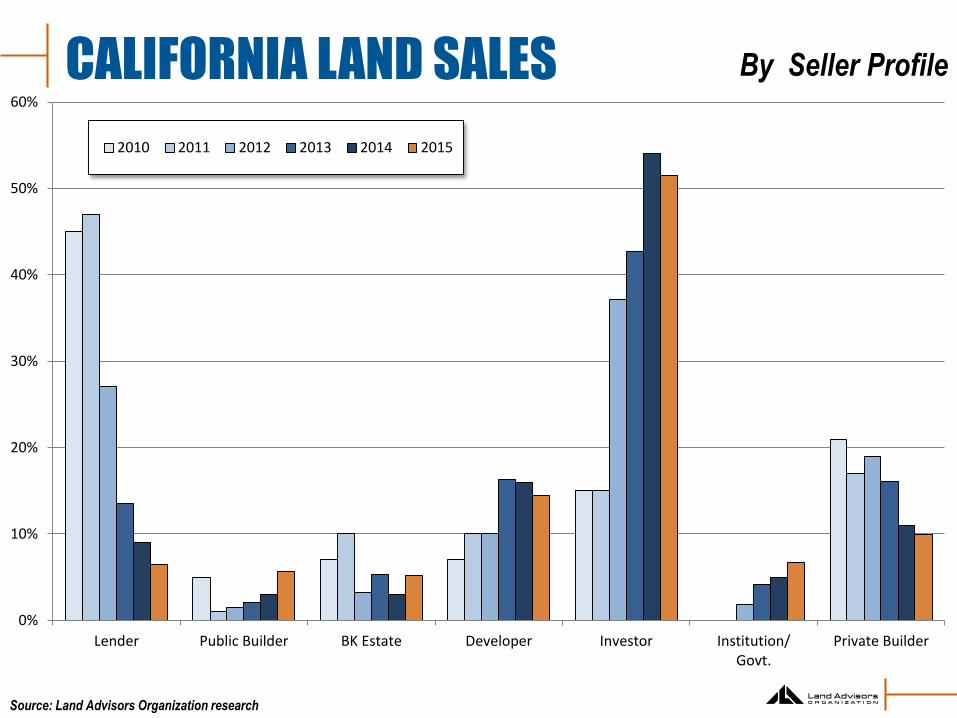

Lender Public Builder BK Estate Developer Investor Institution/Govt.

Private Builder

2010 2011 2012 2013 2014 2015

By Seller ProfileCALIFORNIA LAND SALES

Source: Land Advisors Organization research

0%

10%

20%

30%

40%

50%

60%

Public Builder Institution/Govt.

Investor Private Builder Developer

2010 2011 2012 2013 2014 2015

By Buyer ProfileCALIFORNIA LAND SALES

Source: Land Advisors Organization research

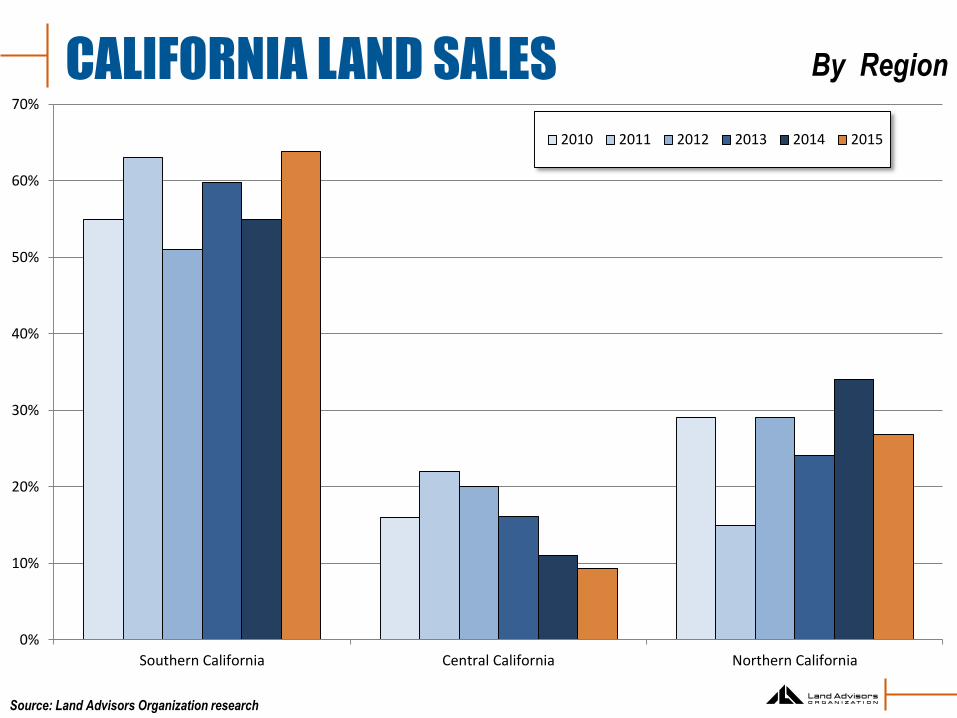

By RegionCALIFORNIA LAND SALES

Source: Land Advisors Organization research

0%

10%

20%

30%

40%

50%

60%

70%

Southern California Central California Northern California

2010 2011 2012 2013 2014 2015

By Site ConditionCALIFORNIA LAND SALES

Source: Land Advisors Organization research

0%

10%

20%

30%

40%

50%

60%

70%

80%

Unimproved Partially Improved Finished

2010 2011 2012 2013 2014 2015

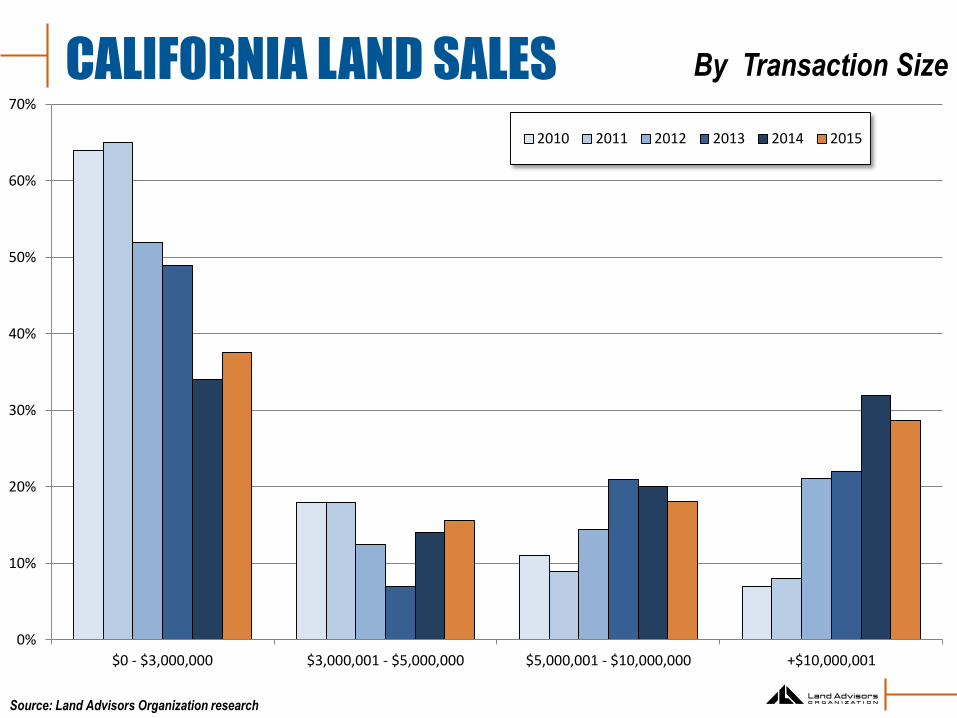

By Transaction SizeCALIFORNIA LAND SALES

Source: Land Advisors Organization research

0%

10%

20%

30%

40%

50%

60%

70%

$0 - $3,000,000 $3,000,001 - $5,000,000 $5,000,001 - $10,000,000 +$10,000,001

2010 2011 2012 2013 2014 2015

CALIFORNIA BUILDING PERMITS

Source: Census & Land Advisors Organization research

Region

2015 Current Current % Current %

Annualized

@ 12/1/ 2015 % of Total Peak of Peak Trough of Trough

Bay Area 18,002 20.1% 35,855 50.2% 5,161 348.8%

Central Coast 2,258 2.5% 7,481 30.2% 814 277.4%

Central Valley 7,101 7.9% 39,897 17.8% 4,119 172.4%

Northern California 2,464 2.8% 6,866 35.9% 457 539.2%

Sacramento Region 6,286 7.0% 23,236 27.1% 2,055 305.9%

Southern California 53,255 59.6% 117,541 45.3% 16,441 323.9%

Totals/Averages 89,366 100.0% 230,876 38.7% 29,047 307.7%

PERMIT SCENARIOS THRU 2020

POPULATION GROWTH OF 1,500,000

487,013 New Households

220,234 Units Built 2009-2015

266,779 Remainder 2016-2020

53,355

Average Permits Needed Per Year(2013 = 35,563)

(2014 = 44,277)

(2015 = 53,084)

POPULATION GROWTH OF 2,000,000

649,351 New Households

220,234 Units Built 2009-2015

429,117 Remainder 2016-2020

85,823

Average Permits Needed Per Year(2013 = 35,563)

(2014 = 44,277)

(2015 = 53,084)

POPULATION GROWTH OF 2,500,000

811,688 New Households

220,234 Units Built 2009-2015

591,454 Remainder 2016-2020

118,290

Average Permits Needed Per Year(2013 = 35,563)

(2014 = 44,277)

(2015 = 53,084)

Southern California – Single-Family & Multi-Family Combined

Source: SCAG, SANDAG, Land Advisors Organization research

26,0

50

29,2

19

36,6

66

38,9

79 4

4,5

93

43,5

63

47,2

91

53,9

92

62,1

57

69,8

55

69,6

87

51,9

27

28,8

22

12,7

36

10,2

74

11,5

65

9,7

20

11,6

31

15,0

87

18,0

09

18,9

38

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15P

Recession

S. CALIFORNIA SINGLE-FAMILY PERMITSRecession

Southern California includes Los Angeles, Orange, San Bernardino, Riverside, and San Diego counties

Source: U.S. Census, Land Advisors Organization research, through November 2015

1995-1999

175,507(35,101/year)

2010-2015p

84,667(14,111/year)

2000-2009

450,304(45,030/year)

5,8

96

6,5

99

10,2

37

10,8

50

17,1

56

20,7

60

20,2

95

18,5

70

24,9

44

29,3

83

22,3

96

25,9

18

22,8

49

15,4

06

5,4

79 7

,623

13,8

73

17,4

31

20,4

76

25,9

82

34,1

45

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15P

Recession Recession

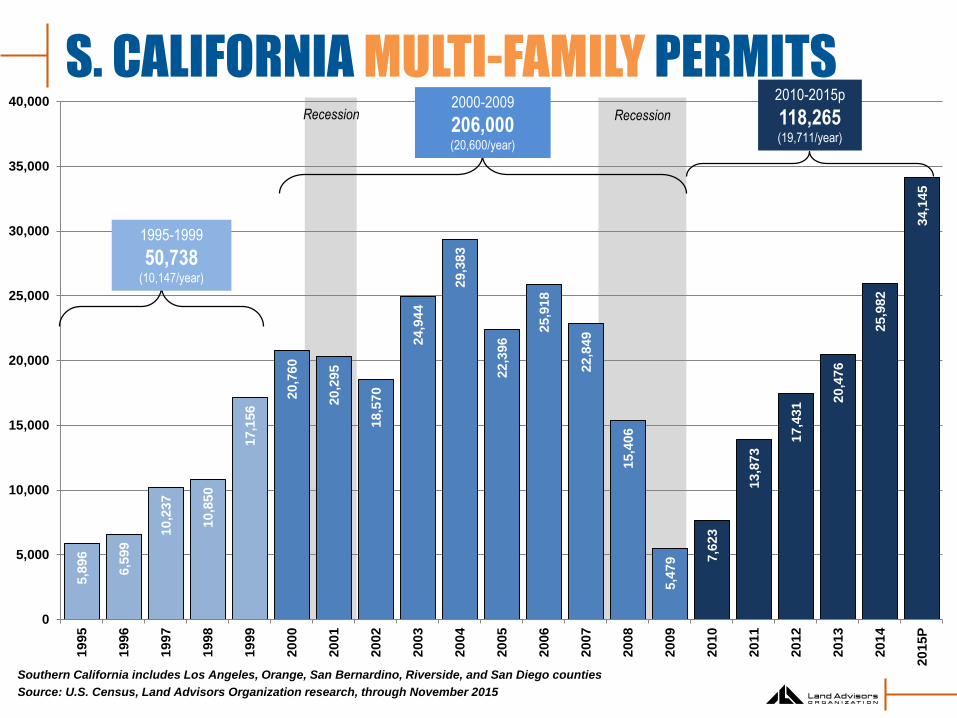

S. CALIFORNIA MULTI-FAMILY PERMITS

1995-1999

50,738(10,147/year)

2000-2009

206,000(20,600/year)

2010-2015p

118,265(19,711/year)

Southern California includes Los Angeles, Orange, San Bernardino, Riverside, and San Diego counties

Source: U.S. Census, Land Advisors Organization research, through November 2015

31,9

46

35,8

18

46,9

03

49,8

29

61,7

49

64,3

23

67,5

86

72,5

62

87,1

01

99,2

38

92,0

83

77,8

45

51,6

71

28,1

42

15,7

53

19,1

88

23,5

93

29,0

62 35,5

63 4

3,9

91

53,0

84

0

20,000

40,000

60,000

80,000

100,000

120,0001

99

5

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15P

Recession Recession

S. CALIFORNIA TOTAL BUILDING PERMITS

1995-1999

226,245(45,249/year)

2000-2009

656,304(65,630/year)

2010-2015p

202,933(33,822/year)

Southern California includes Los Angeles, Orange, San Bernardino, Riverside, and San Diego counties

Source: U.S. Census, Land Advisors Organization research, through November 2015 but annualized

2012 SUMMARY OF CALIFORNIA LAND SALES

Thank you for the opportunity to present today!

Presenter:

Tom Reimers

President – CA Division

Land Advisors Organization

2015/2016 Land Market Update