2014 state of manufacturing- pollster's powerpoint

TRANSCRIPT

Helping Manufacturing Enterprises Grow Profitably

Presents

On behalf of Enterprise Minnesota, Public Opinion

Strategies is pleased to present the key findings from the

sixth annual survey of manufacturing executives in

Minnesota.

The survey was conducted February 28-March 13, 2014,

among 400 manufacturing executives; it has a margin of

error of +4.9%. Respondent titles included owners, CEOs,

CFOs, COOs, presidents, vice presidents, and managing

officers.

Rob Autry is a Partner of Public Opinion Strategies, a

national political and public affairs survey research firm

based in Alexandria, VA.

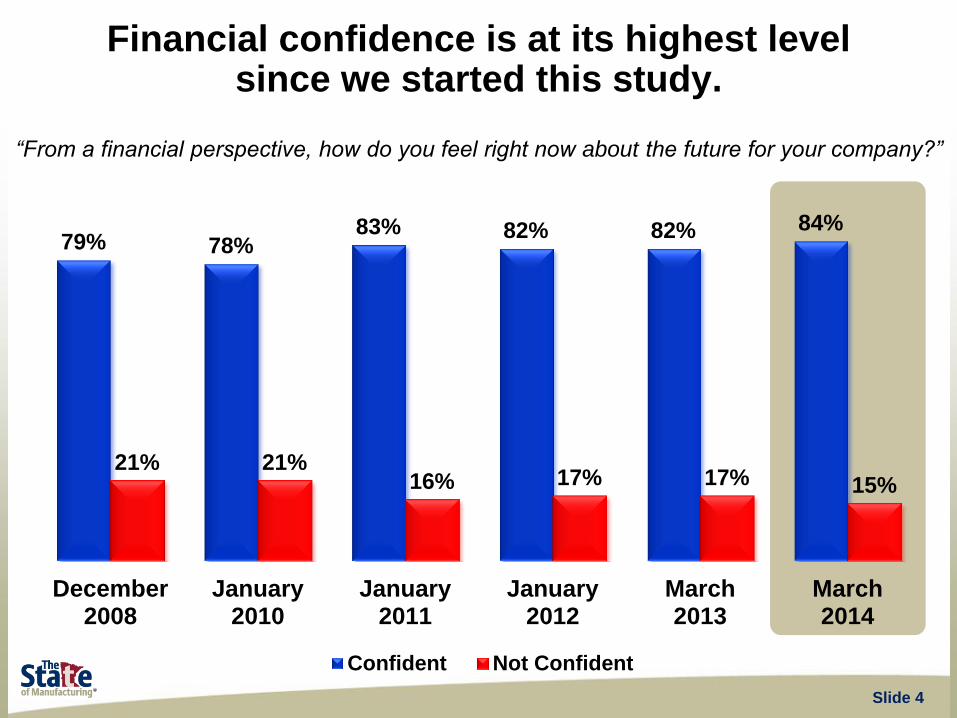

79% 78% 83% 82% 82% 84%

21% 21% 16% 17% 17% 15%

December2008

January2010

January2011

January2012

March2013

March2014

Confident Not Confident

“From a financial perspective, how do you feel right now about the future for your company?”

Slide 4

Financial confidence is at its highest level since we started this study.

8%

26%

40%

32% 34% 37%

34%

53% 49%

55%

46%

54% 56%

19%

9% 10% 15%

7%

December2008

January2010

January2011

January2012

March2013

March2014

Economic Expansion Flat Economy Recession

“Thinking about the upcoming year, in 2014, do you anticipate economic expansion,

a flat economy, or a recession?”

Slide 5

Manufacturing executives are more economically hopeful than in previous years; recessionary

concerns are at their lowest.

30% 33%

41% 40% 39% 41%

55% 54%

47% 47% 49% 51%

December2008

January2010

January2011

January2012

March2013

March2014

Right Direction Wrong Track

“Generally speaking, in regard to being a competitive business location, would you say that things in

Minnesota are going in the right direction, or have they pretty seriously gotten on the wrong track?”

Those who say the state’s business climate is on the wrong track is at its highest level since 2010.

Slide 6

23%

17% 19%

44%

36%

24%

51%

39%

32%

47%

31%

27%

41%

32%

28%

45%

35%

27%

Gross Revenues Profitability Capital Expenditures

2008 2010 2011 2012 2013 2014

Percent Expecting Increases Per Year

Slide 7

We also see a slight uptick in expected gross revenues and profitability for 2014, but not with capital expenditures.

We asked manufacturing executives to rate how concerned

they were about a series of factors affecting companies

like theirs. In total, we had them rate 7 different factors.

“Now, I would like to read you a list of

factors that some companies are

concerned about. For each one, please

rate how concerned your firm is about

that particular factor using a scale

from 1 to 10, where one means that

your firm is NOT AT ALL CONCERNED

about it and where ten means your firm

is VERY CONCERNED about it.”

1 2

3

4 5

80

90

100

110

6 7

8

9 10

Slide 9

59%

55%

34%

31%

18%

16%

11%

Concerns Ranked By % Concern (8-10)

Slide 10

The costs of health care coverage

Government policies and regulations

The ability to attract and

retain qualified workers

Economic and global uncertainty

Costs of employee salaries and

benefits, not including health insurance

Increased competition from

foreign sources

Managing supply chain relationships

Health care costs and government policies and regulations top the list of concerns.

48%

31%

31%

29%

21%

“What would you say are the one or two biggest challenges your firm is facing that

might negatively impact future growth?” (Ranked By % Combined Choice)

Slide 11

Unfavorable business climate,

such as taxes, regulations,

and policy uncertainties

Rising health care and

insurance costs

Weak economy and lower

sales for your products

Rising costs of energy and

materials for your products

Attracting and retaining a

qualified workforce

The business climate and government policies are seen as the biggest obstacle to growth.

2010 2011 2012 2013 2014

The costs of health care coverage 68% 71% 68% 67% 59%

Government policies and regulations 57% 61% 56% 58% 55%

The ability to attract and retain

qualified workers 19% 14% 31% 30% 34%

Economic and global uncertainty n/a n/a n/a n/a 31%

Costs of employee salaries and

benefits, not including health

insurance

16% 15% 13% 19% 18%

Increased competition from foreign

sources 27% 20% 21% 17% 16%

Managing supply chain relationships n/a n/a 15% 10% 11%

Slide 13

Concerns Among Manufacturing Executives (% Concern 8-10)

We have seen a consistent rise in concern about finding and keeping qualified workers.

We asked manufacturing executives to rate how important a

series of factors were in helping them to attract and recruit

new employees to their firm.

“Changing the focus somewhat to

attracting and recruiting new employees

to your firm...I am going to read a series

of factors and, after I read each one,

please tell me how important that

particular factor is to your firm in

attracting workers, using a one to ten

scale where one means that factor is

NOT IMPORTANT AT ALL and where ten

means that factor is VERY IMPORTANT.”

1 2

3

4 5

80

90

100

110

6 7

8

9 10

Slide 14

55%

40% 45%

58% 60%

67%

43%

55% 50%

39% 36%

32%

December2008

January2010

January2011

January2012

March2013

March2014

Difficult Not Difficult

“How difficult is it to attract qualified candidates for your firm’s vacancies?”

Slide 15

Two-thirds now say it is difficult to attract new workers, the highest margin in six years.

54%

61% 55%

75%

43% 37%

43%

25%

December 2008 March 2014 December 2008 March 2014

Difficult Not Difficult

“How difficult is it to attract qualified candidates for your firm’s vacancies?”

Slide 16

Difficulty in filling vacancies has noticeably soared with non-Metro area manufacturers.

Metro Firms Non-Metro Firms

20%

19%

49%

6%

22%

21%

47%

6% 2013 Data 2014 Data

“When looking to hire new employees, where is your need greatest?”

Slide 17

Entry-level employees

Employees with

technical training

Employees with technical

training and experience

Employees with four-year

college degrees

Nearly half of all manufacturers say they’re looking for employees with training and experience.

27% 22% 23%

16% 16% 14%

56% 60% 62%

January 2012 March 2013 March 2014

Grow Shrink About The Same

“Looking back on the last 12 months, did your company’s workforce grow,

shrink, or stay about the same?”

Slide 18

Sixty-two percent of firms say their workforce has stayed about the same in the past year.

29% 25%

30%

2% 5%

2%

68% 69% 67%

January 2012 March 2013 March 2014

Grow Shrink About The Same

“In the next 12 months, does your company expect to grow or shrink the size

of its workforce, or will it stay about the same?”

Slide 19

And, two-thirds expect their workforces to stay about the same for the next year, too.

2013 2014

Metro Firms 25% 30%

Non-Metro Firms 26% 30%

Less than $1 million in revenue 20% 21%

$1-5 million in revenue 31% 33%

Over $5 million in revenue 33% 41%

50 or fewer employees 23% 27%

Over 50 employees 39% 42%

Been in operation 1-15 years 25% 27%

Been in operation over 15 years 25% 31%

Slide 20

Percent Expect Their Firm To Grow In Next 12 Months

We are starting to see some interesting differences on workforce growth by firm type.

66%

48%

41% 43% 43%

54%

6%

13% 14% 9% 10%

5%

27%

38%

44% 46% 44% 39%

December2008

January2010

January2011

January2012

March2013

March2014

Increased Decreased Stayed About the Same

“On average, over the last two years, have your firm’s wages increased,

decreased, or stayed about the same?”

Slide 22

A majority of executives report increasing wages for the first time since the recession.

41% 45%

53% 54%

48%

62%

7% 4% 2% 2% 4% 2%

51% 49% 44% 43%

46%

35%

December2008

January2010

January2011

January2012

March2013

March2014

Increase Decrease Stay About the Same

“Do you expect the average wages to increase or decrease over

the next two years, or will they stay about the same?”

Slide 23

The highest percentage since 2008 expect wages to rise over the next two years.

2008 2010 2011 2012 2013 2014

Affordable Health Care 39% 39% 45% 50% 54% 51%

Salary and Wage Expectations 43% 38% 29% 22% 25% 32%

Competitive Benefits Package 35% 32% 31% 22% 27% 25%

Flexible Work Schedules 32% 30% 20% 14% 12% 13%

The Need to Accommodate

Part-Time Workers n/a n/a n/a n/a n/a 7%

Top Recruitment Factors Ranked By Importance (8-10)

Slide 24

And, we have also seen a significant rise in salary and wage expectations since 2012.

16% 19% 18% 17% 18%

25%

13% 10% 8% 8%

12% 7%

69% 67% 71% 72%

68% 67%

December2008

January2010

January2011

January2012

March2013

March2014

Will Invest More Will Invest Less Will Stay the Same

“Generally speaking, would you say that as a percentage of payroll your company will

invest MORE in employee development or LESS next year compared to 2013,

or will it stay about the same?”

Slide 25

And, now a quarter of firms predict investing more in employee development in the coming year.

Yes No

Metro Firms 34% 65%

Non-Metro Firms 27% 71%

Less than $1 million in revenue 8% 90%

$1-5 million in revenue 36% 63%

Over $5 million in revenue 55% 44%

50 or fewer employees 24% 76%

Over 50 employees 62% 34%

Been in operation 1-15 years 23% 76%

Been in operation over 15 years 33% 66%

Slide 26

“Does your company have an employee development and retention program

for your less-experienced employees?”

Larger firms are more likely to have employee development and retention programs.

Yes No

Metro Firms 27% 72%

Non-Metro Firms 32% 68%

Less than $1 million in revenue 11% 89%

$1-5 million in revenue 26% 74%

Over $5 million in revenue 57% 41%

50 or fewer employees 20% 79%

Over 50 employees 66% 33%

Been in operation 1-15 years 18% 82%

Been in operation over 15 years 32% 68%

Slide 27

“Does your firm have a recruiting relationship with one or more vocational,

technical, or community colleges or universities?”

Non-Metro firms and firms that expect to grow are forming relationships with educational institutions.

“How much of your product did you ship internationally in the last year?”

2008 2010 2011 2012 2013 2014

None 58% 58% 56% 52% 56% 51%

10% or Less 31% 29% 28% 29% 29% 23%

11% - 25% 5% 7% 8% 9% 8% 14%

26% - 50% 4% 4% 6% 7% 4% 4%

51% or More 1% 1% 2% 2% 2% 5%

Slide 29

We see a bump up in the percentage of firms that ship more than 11% of their product aboard.

11% or More 10% 12% 16% 18% 14% 23%

24%

66%

"Home Sourcing"

Yes No

Slide 30

“Have you gained new business because of ‘home sourcing’

(or re-shoring) by your OEM customers?”

About one fourth of firms have gained new business due to “home sourcing.”

Yes

Metro Area Firms 23%

Non-Metro Firms 26%

Less than $1 million revenue 12%

$1-5 million in revenue 35%

Over $5 million revenue 34%

50 or fewer employees 23%

Over 50 employees 32%

Been in operation 1-15 years 19%

Been in operation over 15 yrs 26%

Slide 31

Shorter lead times and costs are the main reasons why supply chain relationships have changed.

AMONG THOSE WHO GAINED NEW BUSINESS: “And, what would you say is

the main reason why your supply chain relationships changed?”

31%

26%

18%

12%

11%

Shorter lead times

Total costs vs. only

product costs

Closer relationships/regional

suppliers

Better inventory management

Don’t know/Not sure

87%

56%

44%

81%

33% 27%

Confident In Firm'sFinancial Future

Expect Increase In GrossRevenues

Expect Increase InProfitability

Have Formal Planning Process Do NOT

Slide 32

Firms with formal planning processes are more likely to expect increases in gross revenues and

profitability for the coming year.

87%

60%

46%

82%

31% 26%

Confident In Firm'sFinancial Future

Expect Increase In GrossRevenues

Expect Increase InProfitability

Have Formal Marketing Process Do NOT

Slide 33

And, we find the same differences exist between firms that have formal marketing processes

and those that don’t.

50% 48%

37%

48% 52%

62%

Formal PlanningProcess

Formal MarketingProcess

Formal QualityManagement System

Yes No

Slide 34

Half of firms have marketing and planning processes in place, and two thirds do not have

ISO or a similar quality standard. “Does your firm have a formal

planning process?”

“Does your company have a

formal quality management

system, such as ISO?”

“Does your firm have a formal

marketing process?”

I. Health care remains the most important issue facing

manufacturers for the fifth year in a row.

II. We are seeing a rise in concern about finding, recruiting and

retaining qualified and experienced workers.

III. And, concern is soaring with firms that are located outside of

the metro area.

IV. While confidence in the financial future is at its highest level

yet and recessionary fears are at their lowest, a majority still

believe the state’s business climate is on the wrong track.

V. Firms that have strategic planning processes in place are

noticeably more optimistic about their future growth and

prosperity.

Helping Manufacturing Enterprises Grow Profitably

The 2014 State of Manufacturing Poll was sponsored by:

Full results can be viewed at

www.enterpriseminnesota.org