30.10.2012 key challenges and opportunities for continued growth and investment into mongolia,...

TRANSCRIPT

RACE TO THE FUTURE

Key Challenges and Opportunities for Continued Growth and Investment in Mongolia

Mongolia 2012 Investment Summit October 30, 2012

Randolph S. KoppaPresident,

Trade and Development Bank of Mongolia

SIGNIFICANT HISTORICAL EVENTS

Khunnu Empire

Chinggis Khan forms

modern Mongolian

state

Mongolian sovereign

state

Mongolian democratic

republic

Exports coking coal

to China

OT investment agreement with

Ivanhoe Mines and Rio Tinto

HKSE IPOsMMC- $749 SGE- $395

WINSWAY- $512

189 B.C. 1921 2005

1206 1990

2009

2010

MSE volume up 277% to $251 mln

$1.2 bln Debt Issuance

so far

TDB issues first

Mongolian bond $75 mln

2007

TDB’s second bond issue$ 150 mln

October 2010

April2012

2011

TDB’s third bond issue $ 300 mln

September 2012

• Coal and iron exports ramp up during 2009

• OT Agreement signed October 2009

At the first Mongolian Investment Summit here two years ago, these were represented in the pictures…

OF HUGE HISTORICAL SIGNIFICANCE

MONGOLIA

• What is the progress the country has made in

addressing the aspiration and needs of the

people and the development of the

infrastructure to handle the needs of a growing

economy?

• What needs attention?

• What are the opportunities?

WHAT HAS HAPPENED SINCE?

• Socio-economic landscape

• Obstacles to growth

• Economic Performance

• Priorities

• Key drivers for foreign investment

• Opportunities for investors

• Summary of progress

TOPICS

• Population growing

• Life expectancy increasing

• Urbanisation increasing

• GDP per capita increasing

• Education supported

• Medical services lagging

HUMAN DEVELOPMENT

THE MONGOLIANS

Source: UNDP

IMPROVING HUMAN DEVELOPMENT INDEX

Source: UNDP

OUTPACING OTHER ASIAN NEIGHBORS

Source: UNDP

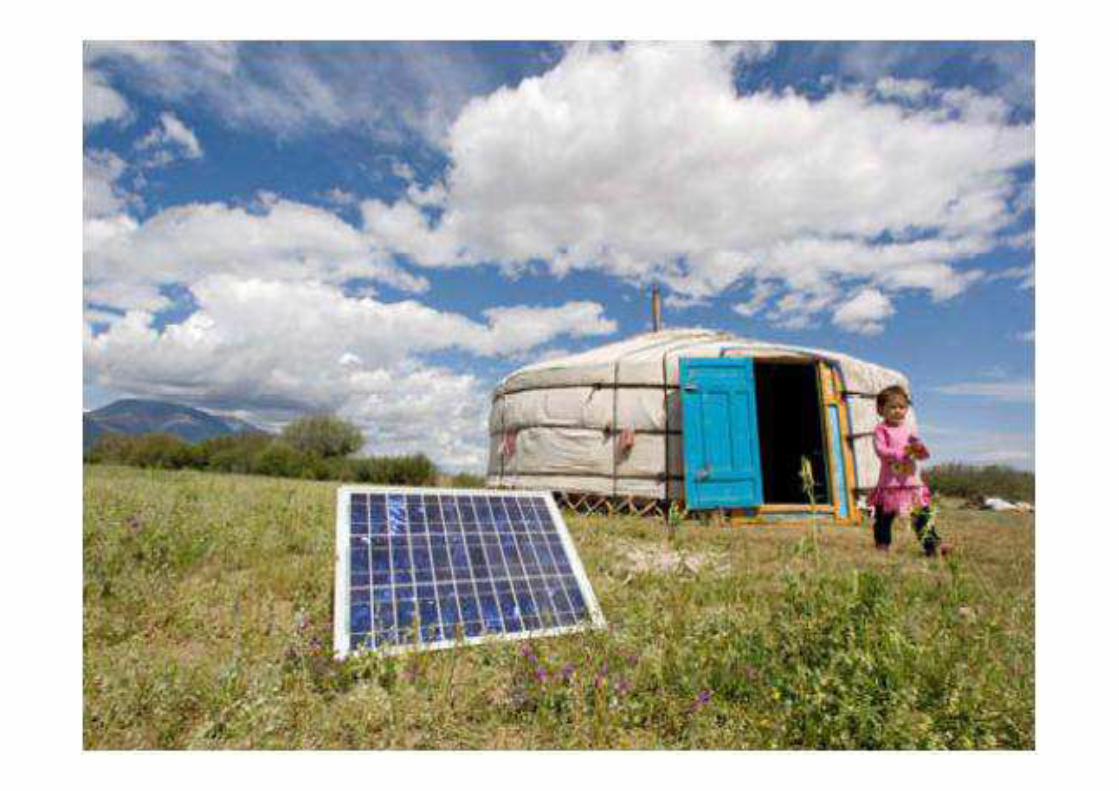

THE SUN POWERS THE COUNTRYSIDE

• Over 100,000 herder gers use solar power

• 500,000 people affected

• 65% of nomadic residents

• 18% of total population

• Subsidy funding of less than USD 10 million

• World Bank, Netherlands Government, GoM

Source: Ministry of Mineral resources and Energy, Mongolia

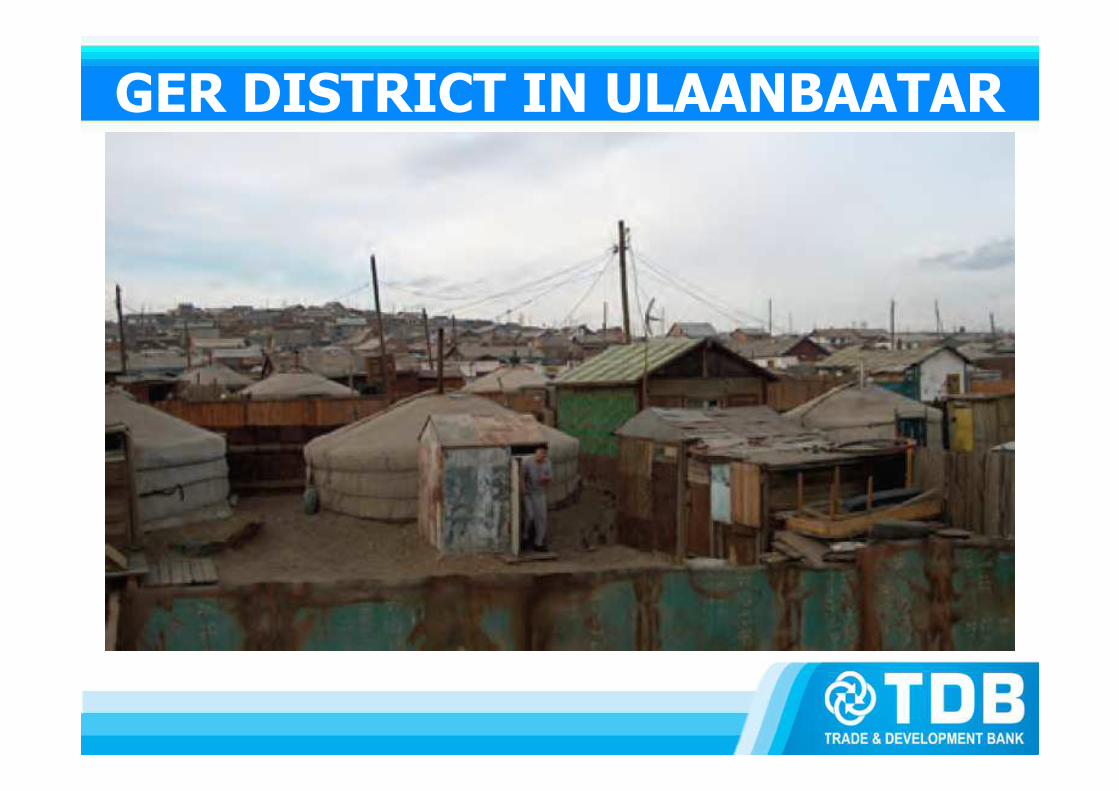

GER DISTRICT IN ULAANBAATAR

CLEANER BURNING MEANS CLEANER AIR

• 170,000 ger households in UB

• 65% of total urban households in UB

• 100,000 now have clean burn stoves which reduce emissions of particulate matter 90%

• “The air is cleaner going out than coming in.”

• Others can use clean burn briquettes

• Funding from Millenium Challenge Fund and others plus micro finance loans

TRANSFER PAYMENTS

• MNT 21,000 a month per person for 18 months or USD750 million

• Partly to fulfill old campaign promises

• Partly to share in advance the awaited financial benefits of new mining projects such as OT and TT

• Transfer payments now curtailed and limited to students, elderly and needy

• Risk of Dutch Disease

STILL SCEPTICAL

PUBLIC OPINION

• Recent surveys of population show:

• 76% of respondents believe the government should have majority control of large scale mining projects

• Main reasons, 84%, are to protect Mongolian interests, assure Mongolia control, to be run efficiently and for national security. Only 8% chose the reason to create revenue

Source: Sant Marat Foundation

HOW TO FINANCE GOVERNMENT INVESTMENT IN MINES

• 12% : it should come for free

• 20% : from government savings

• 16 % : from foregoing dividends

• 19% : from the international capital market borrowing by the government for its equity participation

CLEARLY, there are some challenging views

Source: Sant Marat Foundation

QUALITIES OF FOREIGN INVESTORS

• Respect of local culture and law

• Transparency

• International reputation

• Scale of operations

Source: Sant Marat Foundation

WHY?

• The scars from mining activity, the strain on the ecosystem and way of life as roads and soon rail, interrupt nomadic patterns for people, livestock and wild animals, are seen as harmful and somehow have been equated with foreign influence.

• Political seasons tend to heighten these issues

• Very high expectations have been created

• Old patterns take time to change

• More knowledge and better information needed.

A METAPHOR

• To understand some of the these issues

Consider this metaphor:

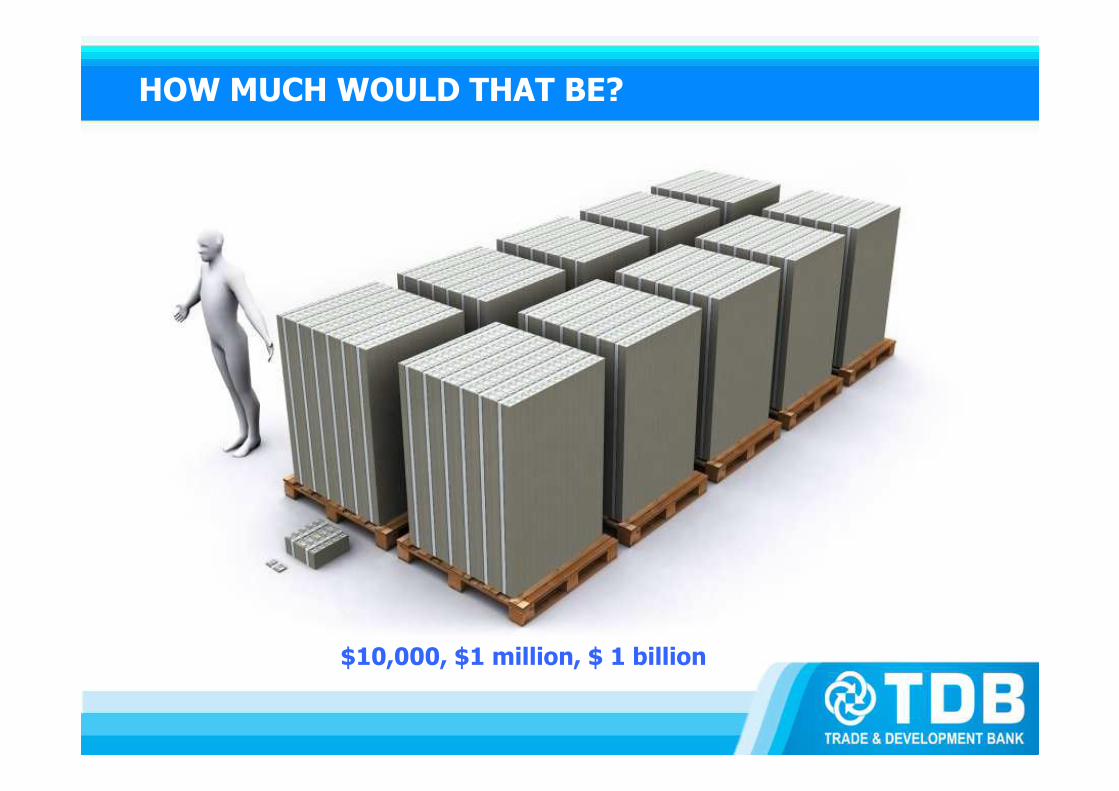

The recent mining boom is as if Mongolia has been awarded by the world an A380 placed on the Gobi Desert

THE PLANE IS LOADED WITH USD 100 BILLS

HOW MUCH WOULD THAT BE?

$10,000, $1 million, $ 1 billion

ONE BILLION DOLLARS LOOKS LIKE THIS

HOW MUCH CAN AN A380 HOLD?

• In the passenger luggage hold, USD 2 billion

• As a cargo plane, USD 15 billion, which weighs almost 150 tons which represents the plane’s maximum payload.

THERE IS ONE CONDITION

You have to get the plane to fly!

Then the money can be showered down

for the Mongolian people to collect.

LEARN TO FLY AND BUILD THE RUNAWAY

• At present, the plane is taxiing and has turned onto the runaway for take off

• The run away is still being built

• 2.8 million Mongolians are watching

• Will the runaway be completed in time?

WHAT HAPPENS NEXT?

WILL IT BE THIS?

OR WILL THIS FOIL THE TAKE OFF?

MEANING OF THE METAPHOR

• Mining investment and developmenthave been advancing at a faster pacethan the underlying infrastructuresnecessary to handle the growth

Mln Mt/brl 2010 2011 2012 3Q

COAL 16.7 21.1 14.3 +3.4% YoY

COPPER .56 .57 .43 +12.5% YoY

IRON ORE 3.6 5.8 4.6 +12% YoY

CRUDE OIL 2.1 2.5 2.4 +38.6% YoY

EXPORTS VOLUMES BOOM DESPITE LAGGING INFRASTRUCTURE

Source: NSO

EXPORTS REVENUES EASE AS MARKET SOFTENS

VALUE 2010 2011 2012 3Q

EXPORTS+ 54%

USD 2.9 bln + 66%

USD 4.8 bln -4.7%*

USD 3.2 bln

COKING COAL Up 188% Up 155% Down 6.8%

IRON ORE Up 186% Up 72% Up 27.2%

COPPER CONCENTRATE

Up 54% Up 25% Down 15.9%

CRUDE OIL Up 34% Up 63% Up 33.3%

Source: NSO* On top 4 minerals only

MONGOLIAN COAL EXPORTS

Source: NSO & TDBC

• Average price in 2011 $110 per ton• Average price in 2012 $100 per ton

2.5 3.3 4.27.1

16.7 21.1

14.3

22*

52

6570

0

10

20

30

40

50

60

70

80

2006 2007 2008 2009 2010 2011 Sep,2012 2013 2014 2015

Mt

ACTUAL FORECAST

* Revised forecast by TDB

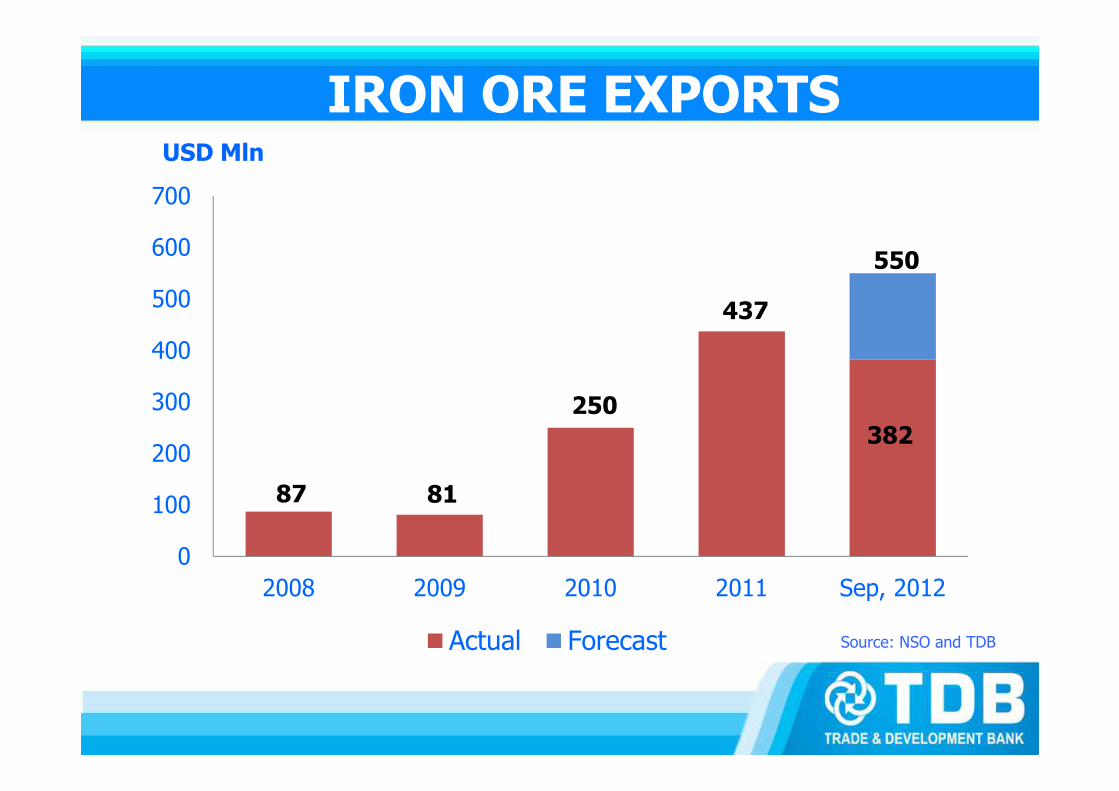

IRON ORE EXPORTS

87 81

250

437

382

550

0

100

200

300

400

500

600

700

2008 2009 2010 2011 Sep, 2012

Actual Forecast

USD Mln

Source: NSO and TDB

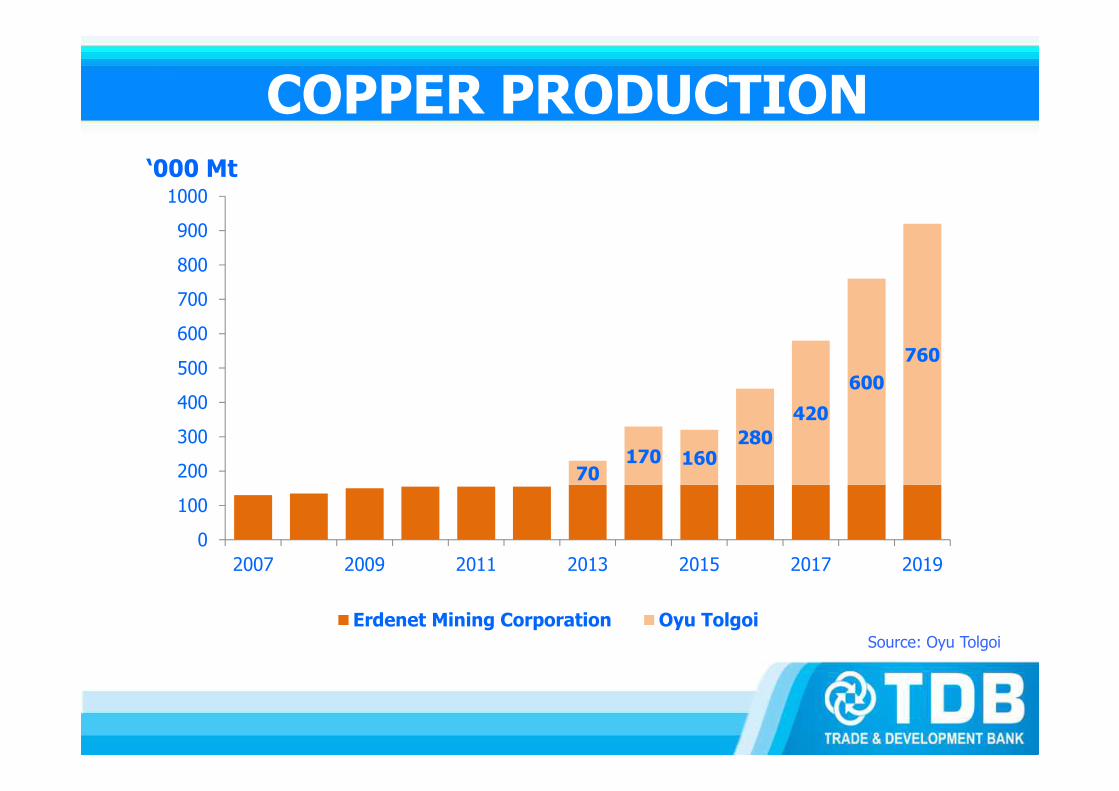

COPPER PRODUCTION

70170 160

280

420

600

760

0

100

200

300

400

500

600

700

800

900

1000

2007 2009 2011 2013 2015 2017 2019

Erdenet Mining Corporation Oyu TolgoiSource: Oyu Tolgoi

‘000 Mt

10.9

14.6

18.0

20.9

25.5

29.6

-5.0

0.0

5.0

10.0

15.0

20.0

-

5.00

10.00

15.00

20.00

25.00

30.00

35.00

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Actual Forecast Real GDP growth rate Source: IMF & NSO

USD bln %

NOMINAL ANNUAL GDP AND REAL GDP GROWTH

INFLATION PREDICTION

Source: IMF and NSO

8.2

26.8

6.3

10.2

9.5

13.6

12.5

9.78.2 7.6 7.0

0

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012E 2013E 2014E 2015E 2016E 2017E

CPI (%) Y-O-Y

September 2012 YoY 14.8%; Ulaanbaatar city 13.4%

60 123 102

-296 -329

2

-391 -486 -300-1000

0

1000

2000

3000

4000

5000

6000

7000

8000

2005 2006 2007 2008 2009 2010 2011 2012E* 2013

Preliminary

Revenue Expenditure Budget Balance

BUDGET INDICATORS

PRIORITY ISSUES

• Fiscal control

• Inflation reduction

• Infrastructure

• Management of expectations

• Foreign investment law clarity

• Enforcement of laws

• Consistency and transparency

INFRASTRUCTURE

• Power: Mongolia facing a 4oo MW shortage

• Rail: Needed to maintain price advantages and to reduce negative environmental impact of trucking

• Road: For mine supplying and to borders

• Water: Need to resolve supply and use questions in the South Gobi and elsewhere

TRANSPORTATION NETWORK

Source: MRTCUD

RECENT PROGRESS

• MMC commencing 250 km rail to border

• DBM funding for east line to Sainshand

• 50MW Salkhit wind farm turbines up

• CHP 5 450 MW USD 1.4 bn power plant in UB negotiating concession agreement with Mongolia/International consortium

• Other power initiatives in process as tariffs have been raised to underpin financing

BREAKTHROUGH

• Mongolia sovereign bond to be launched

• USD 1.5 bn

• Aimed to finance needed infrastructure to support exports

• Leverage funds through PPP

• Not for budget shortfalls

• Key: resource nationalism rhetoric to be toned down

OTHER DEVELOPMENTS

• Construction

• Cement

• Steel

• Animal and agri value added processing

• Import substitution

• Consumer goods

• Financial services

DUTCH DISEASE

• Not a great threat to traditional exports of cashmere hair and bulk meat

• Movements towards higher value potentially brand-able exports has begun

• Import substitution, services and further processing could face labor shortages but can provide buffer to imports

• Inflation always threatens

• Green movement helps

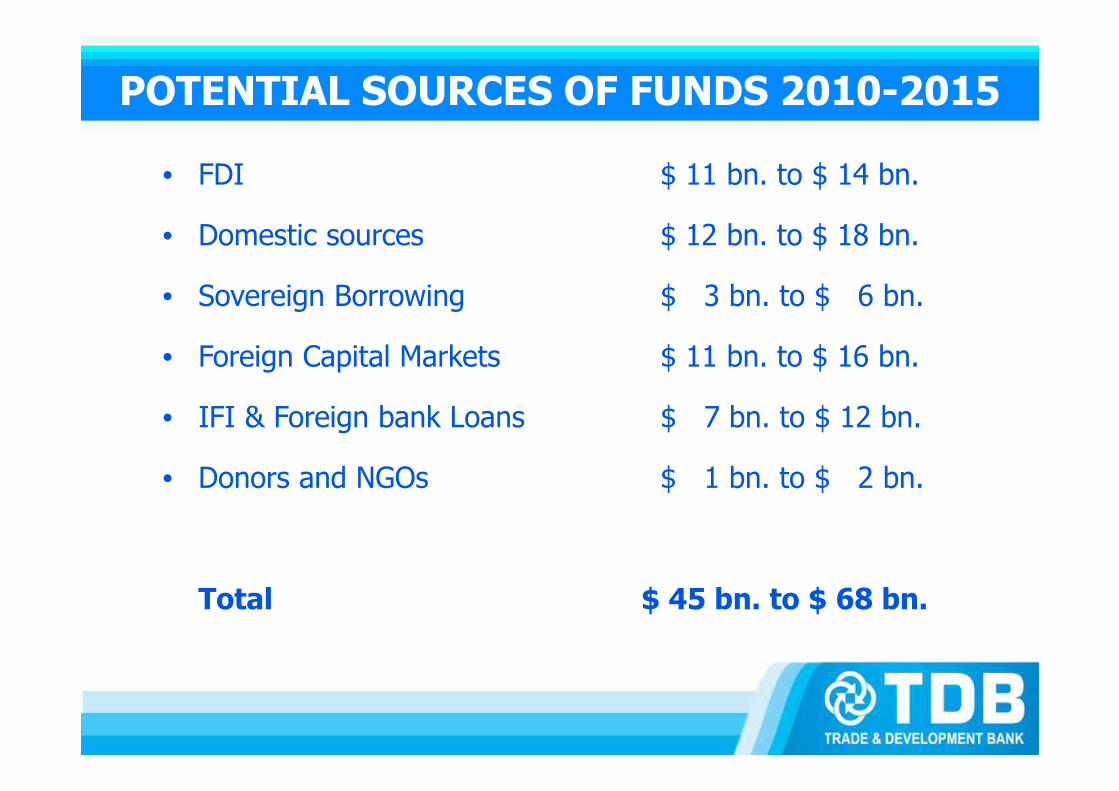

TOTAL FINANCING AND INVESTMENT NEEDS ANDOPPORTUNITIES 2010 TO 2015

• Mine Development $ 12 bn. to $ 20 bn.

• Infrastructure $ 8 bn. to $ 12 bn.

• Urban development $ 6 bn. to $ 8 bn.

• Agriculture $ 1 bn. to $ 2 bn.

• Industry and Commerce $ 15 bn. to $ 20 bn.

• Environment $ 1 bn. to $ 2 bn.

• Social $ 1 bn. to $ 2 bn.

• Financial Sector $ 1 bn. to $ 2 bn.

Totals: $ 45 bn. to $ 68 bn.

POTENTIAL SOURCES OF FUNDS 2010-2015

• FDI $ 11 bn. to $ 14 bn.

• Domestic sources $ 12 bn. to $ 18 bn.

• Sovereign Borrowing $ 3 bn. to $ 6 bn.

• Foreign Capital Markets $ 11 bn. to $ 16 bn.

• IFI & Foreign bank Loans $ 7 bn. to $ 12 bn.

• Donors and NGOs $ 1 bn. to $ 2 bn.

Total $ 45 bn. to $ 68 bn.

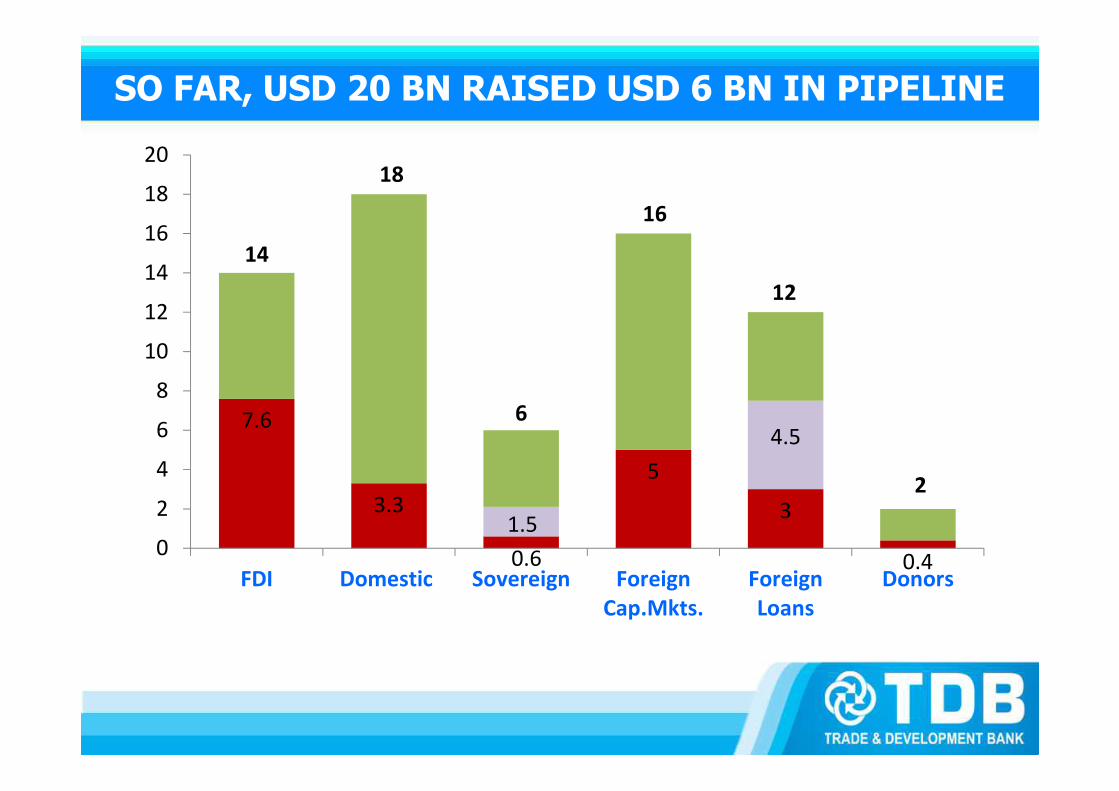

7.6

3.3

0.6

5

3

0.4

1.5

4.5

14

18

6

16

12

2

0

2

4

6

8

10

12

14

16

18

20

FDI Domestic Sovereign Foreign

Cap.Mkts.

Foreign

Loans

Donors

SO FAR, USD 20 BN RAISED USD 6 BN IN PIPELINE

FOREIGN INVESTMENT

0.5 0.7 0.8

1.3

4.8

1.6

2,2

2.8

3.65

4.6

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014 2015

USD bln

Actual Projected based on 30% annual CGR 2004 to 2010

Source: World bank and FIFTA

FOREIGN INVESTMENT KEYS

• Clear and consistent legal and regulatory environment

• Fiscal discipline

• Focused infrastructure investment

• Information and education

– Public – importance of foreign investment

– Government – FDI requirements and interest in welcoming foreign investment

– Investors – Mongolia’s enduring strategic advantage in serving China’s needs

CONCLUSIONS

• Mongolia still adjusting to market economy

• Pace and staging of developments has impacted foreign opinion

• Democracy prompts speaking out

• New foreign investment law needs clarifying or changing

• Infrastructure is in focus

• Move to sovereign bond soon signals understanding of conditions necessary for a successful issue

RECOMMENDATIONS

• Engage

- Here

- In Mongolia

- Communicate with all constituents

Come and see us!

Remember, There are more than USD 40 billion of opportunities in the next few years

JUST THREE FULLY LOADED

OR, SKIP THE PLANE CHARTER

Simply wire the funds through TDB

Thank you for your attention!

Juulchin Street - 7

Baga Toiruu - 12

Ulaanbaatar, Mongolia

Tel: 976-11-31 99 43

Fax: 976-11-31 24 18

Email: [email protected]

http://www.tdbm.mn

http://www.bankcard.mn

http://www.mongolianbusinessguide.com

TDB Presentation

Company Overview

Corporate Banking International Banking Treasury Retail and SME Banking

ATMInternet

Bank

Unrivalled Relationships with International FIs

•Maintains 38 nostro accounts in 14 currencies at 27 top rated foreign banks in 16 different countries

•Direct correspondent relationships with >150 foreign financial institutions

•Clean trade finance lines from 32 large foreign institutions

Wide Scope of Products and Services Provided

•44 branches, 107 ATMs, 1170 merchants, 1773 point of sale terminals

•Most advanced virtual banking services, such as Internet Banking service, Mobile Banking Service, E-Billing

•Ability to process payments under Visa, MasterCard, JCB/Discover and Diners

TDB30.8%

Other69.2%

3Q2012, Corporate Loans market share

36.6%

21.3%

29.3%

0%

10%

20%

30%

40%

Goldmarket

Moneymarket

FXmarket

3Q2012, Treasury market share

Company Highlights

■ Profitable and efficient corporate bank uniquely positioned to benefit from Mongolia’s growth potential

■ The “International Face of Mongolia”

■ Increasingly sizeable retail banking platform driven by selectively targeting high income customers

■ Efficient asset and liability management to ensure high liquidity

■ Leadership in profitability and efficiency throughout business cycles

■Market leader in risk management and strong corporate governance

■ Experienced management team with proven track record

2009 2010 2011 2012.09

Total Asset 578.8 1,065.0 1,498.8 1935.4

Total Loans (net) 290.2 369.5 805.5 1110.3

Total Deposits 479.0 912.2 941.1 1540.6

Total Equity 48.0 70.2 100.0 197.4

Net Profit 10.7 16.5 30.2 35.8

Capital Adequacy 13.0% 15.9% 12.7% 14.1%

ROAA 2.1% 2.3% 2.6% 3.1%

ROAE 22.6% 26.9% 39.8% 35.7%

MNT/USD = 1394.47 * Including bonds

Financial Results (mln.USD)*Financial Results (mln.USD)*

Bank Ratings by Moody’sBank Ratings by Moody’s

• Senior Unsecured EMTN (foreign currency) B1• LT/ST Bank Deposits (foreign currency) B2/NP• LT/ST Bank Deposits (domestic currency) B1/NP• LT/ST Issuer Rating B1• Subordinated foreign currency issue B2• Local currency bank deposit B1• Outlook Stable

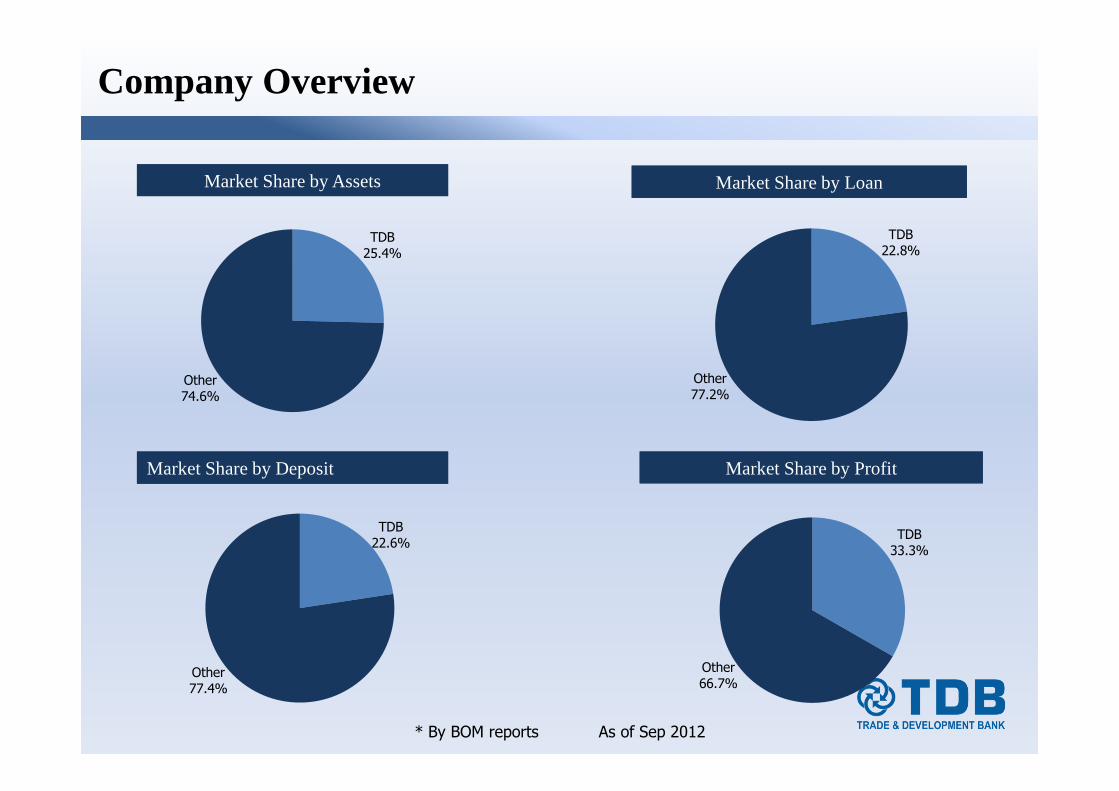

Company Overview

Market Share by AssetsMarket Share by Assets

Market Share by DepositMarket Share by Deposit

Market Share by LoanMarket Share by Loan

Market Share by ProfitMarket Share by Profit

* By BOM reports As of Sep 2012

TDB25.4%

Other74.6%

TDB22.8%

Other77.2%

TDB22.6%

Other77.4%

TDB33.3%

Other66.7%

US Global Investment LLC

Globull Investment & Development SCA

Individual Shareholders

Goldman Sachs Mongolia Investments Limited

Mr. Erdenebileg Doljin

Central Asia Mining LLC The Goldman Sachs Group, Inc

Treasury Stock

50%

100%

50% 100%

100%

65.8%

7.3% 3.8% 4.8% 18.3%

Strive to internationalize and diversify shareholder base demonstrated by Goldman Sachs Group’s recent equity investment

Ownership Structure

Organizational Structure

AccomplishmentsContinuously at the Forefront of Innovation

1990 19921993 1996

2001 20042006 2007

2008 20102011 2012

First state-owned commercial bank

in Mongolia

First Mongolian Bank to adopt International Financial Reporting

Standard

First to Introduce modern banking

technology to Mongolia

First deliver cash services of AMEX, VISA,

MasterCard, JCB and Traveler’s cheque

First to become a member of SWIFT

network

First Mongolian Bank to offer ATM services

First Mongolian Bank to commence gold exports into foreign

markets

First Mongolian Bank to participate

in international syndicated loan

transaction

ADB and IFC injected US$11 mm capital into

TDB - First bilateral investment made into

the Mongolian banking sector

First Mongolian Commercial Bank to be rated by Moody’s and

with credit ratings above the country

ceiling

First Mongolian company to issue in

the international capital markets –US$75 mm senior unsecured bond off

a US$150 mm EMTN Programme

First Mongolian bank to launch international

Martercard and issue Euro MasterCard

First Mongolian company to be a

repeat issuer in the international bond market (US$150 mm senior notes)

Introduced EMV chip card in credit

cards

First Mongolian bank to establish an investment

banking subsidiary which obtained underwriting and brokerage licenses from Mongolia FRC

“Best Trade Finance Bank

in Mongolia” in both 2011 and 2012 by GTR

journal

GS Mongolia Investments Ltd., a subsidiary of The

Goldman Schs Group invested 4.78% in

TDB

First bank to launch

Mongolian T brand card

“Best Bank of Mongolia” by FinanceAsia

FMO provided US$20 mm loan

to TDB

Introduced “Most Money”, an advanced, up to date and high-tech electronic bankingservice

StrategyClear Strategy to Maintain Leadership in Corporate Banking and Selectively Expand into Retail and SME Banking

Company HighlightsProfitable & Efficient Corporate Bank Uniquely Positioned to Benefit from Mongolia’s Growth Potential

… with Steady Rise of Number of Corporate Customers… with Steady Rise of Number of Corporate Customers Diversified Loan ExposureDiversified Loan Exposure

Consistent Growth in Lowest Cost Corporate DepositConsistent Growth in Lowest Cost Corporate Deposit

Agriculture 1.8%

Mining 19.6%

Manufacture 13.3%

Petroleum import 5.9%

Retail and wholesale trading

18.3%

Construction 10.7%

Travel 2.1%

Transportation 2.4%

Mortgage 12.2%

Consumer 12.2%

Other 1.5%

3Q2012 Total Loans Mix by Industry

15,51517,421

19,99122,071

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 3Q2012

No. of Corporate Customers

252 267 562 718

Total Corporate

Loans(US$ mm)

207.4341.9 406.2

607.1

0

200

400

600

800

2009 2010 2011 3Q2012

Corporate Deposits

Company HighlightsThe “International Face of Mongolia”

Top Trade Finance Bank in MongoliaTop Trade Finance Bank in Mongolia

TDB49%

Other52%

FY2011 Market Share of Mongolian Trade Finance Transaction

■Maintains 40 nostro accounts in 14 currencies at 29 top rated foreign banks in 16 different countries.

■ Direct correspondent relationship with >150 foreign financial institutions.

■Only Mongolian Bank which has arranged syndicated club deals with foreign banks for MNT58 bln and > USD170 mm since 2005.

■ Clean trade finance lines from 32 large foreign institutions with amount of US$267.57 mm as of Sep 2012.

■ US$35 mm trade finance line

■ US$30 mm trade finance line

■ EUR 21 mm trade finance line

■ US$15 mm trade finance line

■ EUR11 mm trade finance line

29.4

70.3

94.6

2010 2011 1H2012

Leading Bank by Borrowings from Foreign Institutions

(US$ mm)

Company HighlightsThe “International Face of Mongolia”

Only Mongolian Repeat Issuer with Proven Track Record of Debt Repayment in the International Market

Only Mongolian Repeat Issuer with Proven Track Record of Debt Repayment in the International Market

2007

US$75 mm

3-yr Senior Notes

Fully Repaid in 2010

2010

US$150 mm

3-yr Senior Notes

2010

US$25 mm

5-yr Subordinated

Notes

First Mongolian issuer in the international capital market

2012

�US$ 300million 8.5% Unsecured Senior Notes�Under US$ 700 million EMNT Program

Banks

and

Others

15%

Asset

Manag

ers,

60%

Private

Banks,

25%

Investor profile

Asia ,

60%

Europe

, 35%

Offshor

e US,

5%

Geographic demand

Joint Arrangers / Joint Book Runners /Joint Lead Managers

Listing Stock Exchange Rated by

Company HighlightsEfficient Asset and Liability Management to Ensure High Liquidity

Diversified and Strong Funding BaseDiversified and Strong Funding Base

519

881

1368

1935

0

500

1000

1500

2000

2500

2009 2010 2011 3Q2012

Sources of Funding

Consistently High Contribution of Low Cost Deposit

Consistently High Contribution of Low Cost Deposit

Diversified funding base as a result of strong lending relationships with international banks and price leadership in deposit funding

Deposits from customers 54.9%

Interbank deposits and

borrowings FIS 9.8%

Debt securities issued 22.8%

Equity, included subordinated debt 10.2%

Other liabilities 2.3%

41.4% 37.3% 41.2% 43.2%

12.9%12.2%

16.1% 14.9%

44.8% 49.1%41.7% 40.8%

0.8% 1.3% 1.0% 1.1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012.09.30

Other Time Savings Current account

Company HighlightsEfficient Asset and Liability Management to Ensure High Liquidity

Well Balanced Asset Composition Well Balanced Asset Composition Asset/ Loan growth exceeds sector’s medianAsset/ Loan growth exceeds sector’s median

Comparison of Assets and Loans to Banking SectorComparison of Assets and Loans to Banking Sector

� TDB Asset Growth 22.9% 65.2% 56.1% 29.1%

� Mongolian Banking Sector Asset Growth 21.1% 41.2% 50.1% 17.0%

2009 2010 2011 2012.09

� TDB Loan Growth (7.7%) 14.3% 141.9% 37.8%

� Mongolian Banking Sector Loan Growth 0.4% 21.5% 72.3% 22.2%

Cash 2.1%Interbank

Deposits 3.9%

Investment Securities 7.5%

Net loan 57.4%

Others 29.1%

66.8%

50.1%

34.7%

53.7%57.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

500

1000

1500

2000

2500

2008 2009 2010 2011 2012.09

USD

mill

ions

Gross Loans Total Assets Loan/Assets

14.20%13.00%

15.90%

12.40%

14.50%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

2008 2009 2010 2011 3Q2012

Company HighlightsEfficient Asset and Liability Management to Ensure High Liquidity

Decreasing NPLDecreasing NPL

5.30%4.10%

2.50%1.30%

17.10%

11.30%

6%4.80%

2009 2010 2011 3Q2012

TDB NPL Ratio Industry NPL Ratio

Substantial Improvement in Capital BaseSubstantial Improvement in Capital Base

BoMminimum required

level 12.0%

… while Maintaining High Proportion of Liquid Assets Mitigating Liquidity Risk

… while Maintaining High Proportion of Liquid Assets Mitigating Liquidity Risk

47%

67%

43%37%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2009 2010 2011 3Q2012

Minimum Liquidity Ratio set by BOM

>25%

Highest Credit Quality Across Peers (As of Sep 2012)Highest Credit Quality Across Peers (As of Sep 2012)

1.3% 1.3% 1.3%2.3%

0.7%

2.0% 2.3%

1.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

TDB Khan Xac bank Golomt

Loan in arrears NPL ratio

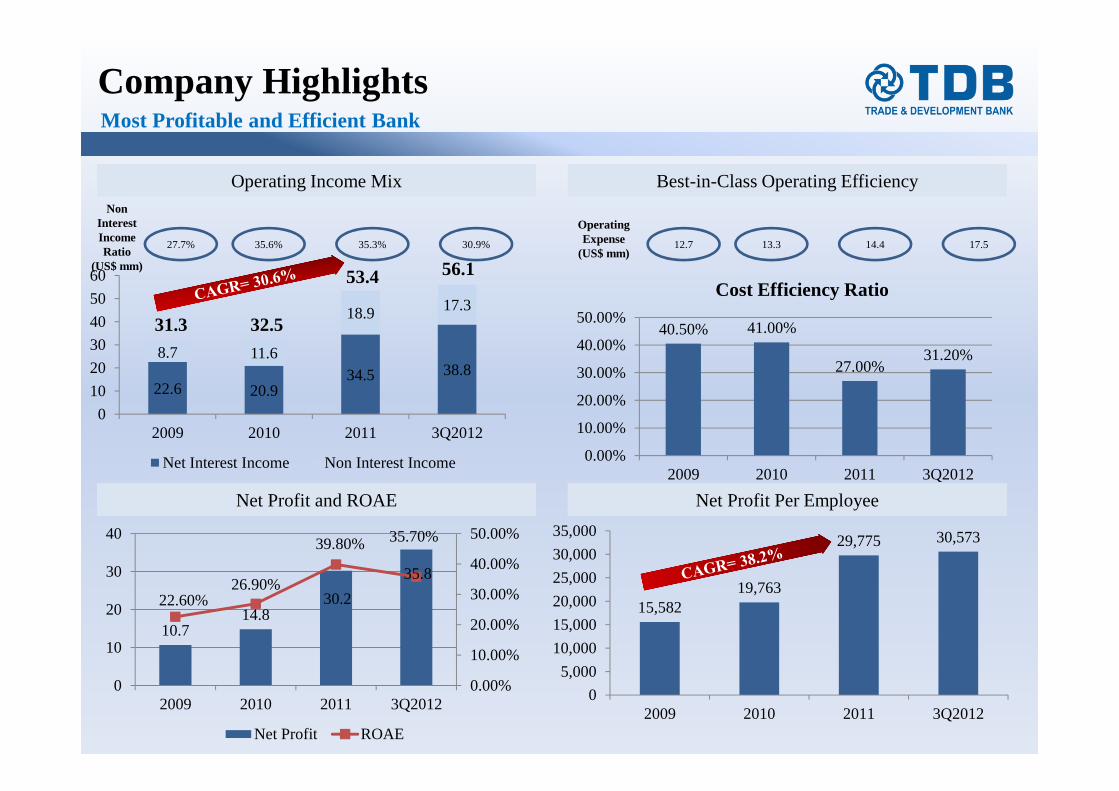

Company HighlightsMost Profitable and Efficient Bank

Operating Income MixOperating Income Mix

22.6 20.934.5 38.8

8.7 11.6

18.9 17.3

0

10

20

30

40

50

60

2009 2010 2011 3Q2012

Net Interest Income Non Interest Income

Non Interest Income Ratio

(US$ mm)

27.7% 35.6% 35.3% 30.9%

31.3 32.5

53.4 56.1

Best-in-Class Operating Efficiency Best-in-Class Operating Efficiency

40.50% 41.00%

27.00%31.20%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

2009 2010 2011 3Q2012

Cost Efficiency Ratio

Operating Expense

(US$ mm)12.7 13.3 14.4 17.5

Net Profit and ROAE Net Profit and ROAE Net Profit Per EmployeeNet Profit Per Employee

10.714.8

30.2

35.8

22.60%26.90%

39.80% 35.70%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

0

10

20

30

40

2009 2010 2011 3Q2012

Net Profit ROAE

15,58219,763

29,775 30,573

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2009 2010 2011 3Q2012

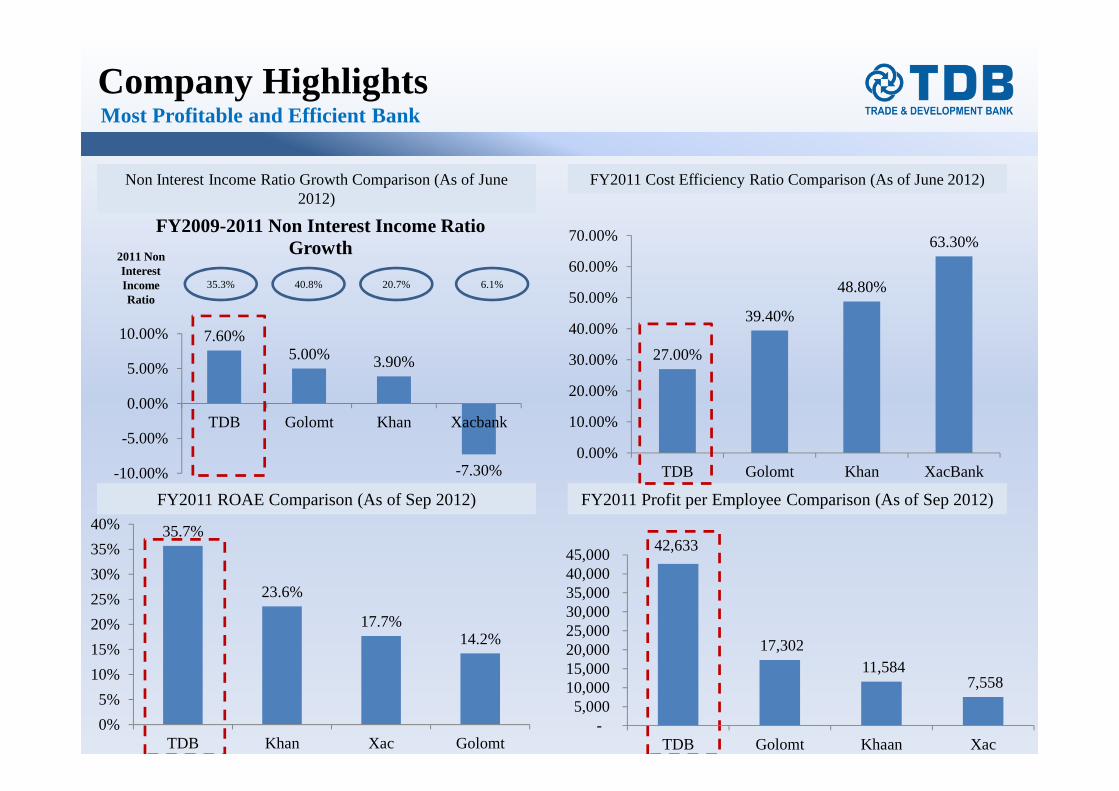

Company HighlightsMost Profitable and Efficient Bank

Non Interest Income Ratio Growth Comparison (As of June 2012)

Non Interest Income Ratio Growth Comparison (As of June 2012)

FY2011 Cost Efficiency Ratio Comparison (As of June 2012)FY2011 Cost Efficiency Ratio Comparison (As of June 2012)

FY2011 ROAE Comparison (As of Sep 2012)FY2011 ROAE Comparison (As of Sep 2012) FY2011 Profit per Employee Comparison (As of Sep 2012)FY2011 Profit per Employee Comparison (As of Sep 2012)

7.60%5.00% 3.90%

-7.30%-10.00%

-5.00%

0.00%

5.00%

10.00%

TDB Golomt Khan Xacbank

FY2009-2011 Non Interest Income Ratio Growth2011 Non

Interest Income Ratio

35.3% 40.8% 20.7% 6.1%

27.00%

39.40%

48.80%

63.30%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

TDB Golomt Khan XacBank

35.7%

23.6%

17.7%14.2%

0%

5%

10%

15%

20%

25%

30%

35%

40%

TDB Khan Xac Golomt

42,633

17,302 11,584

7,558

- 5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

TDB Golomt Khaan Xac

Company HighlightsEfficient Asset and Liability Management to Ensure High Liquidity

Risk Governance FrameworkRisk Governance Framework

Industry leading risk management framework and strong corporate governance to fully control key risks

“Excellent Quality of Straight Through Processing Award

2008” by Germany Commerzbank AG

2009 “Best Spread Bank" by Thomson Reuters

Agency

2007 “VISA Outstanding New Product Designing” (Visa

International)

2006 “Best business entity for its social responsibility” Mongolian National Chamber of Commerce

2006 “Quality Recognition Award” (Citibank, USA)

2005 “Best Bank of the Year” (The Bank of Mongolia)

2001, 2002 Best Bank in Mongolia

(“The Banker”)

2011 “The Best Bank”

“Top – 5 Banks of Mongolia”

2012, 2011 “Best Trade Finance Bank in Mongolia”

(Global Trade Review)

2011 “Investment Envoy”

(Foreign Investment & Foreign Trade Agency of Mongolia)

2012 “Best Bank of Mongolia”

FINANCE ASIA

External Recognition

Contact us

Director of International Banking Department

Ms. Erkhembayar BaltsukhTel: +976 11 319943 ext. 1408 Fax: +976 11 312418 Email: [email protected]

TDBJuulchin Street - 7, Baga Toiruu - 12Ulaanbaatar, MongoliaSwift: TDBMMNUBWebsite: www.tdbm.mn