6.5 ratio analysis - shodhganga : a reservoir of indian...

TRANSCRIPT

223

6.5 Ratio Analysis

Ratio 1; Inventory Turnover Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 6.991 5.892 4.571 3.391 4.713 4.257 3.835 2.194 2.250 3.140 3.616 4.326 2 ABB 4.543 5.011 6.762 7.154 6.554 7.184 7.884 7.794 7.386 7.714 8.928 10.125 3 Batliboi 4.631 4.742 0.00 9.418 6.410 7.001 6.477 6.451 6.089 6.642 7.880 4.556 4 Bosch Re 3.016 3.735 3.969 5.633 4.820 3.636 3.310 3.109 4.460 4.581 4.328 4.482 5 Blue Star 6.022 5.900 5.574 7.013 7.654 6.579 6.191 6.172 6.849 7.082 7.328 7.200 6 Banco Products 3.789 4.845 4.258 4.434 4.978 4.739 6.405 7.667 7.356 7.095 5.786 5.790 7 Elecon 2.901 1.942 2.229 2.870 3.818 4.336 4.100 4.460 5.520 4.728 3.772 3.165 8 Eimco Elecon 2.887 3.317 1.582 2.663 4.294 4.234 3.489 2.686 3.196 3.139 2.912 2.852 9 FAGBearing 1.942 2.226 2.239 2.670 2.837 3.269 3.439 4.105 4.373 3.945 4.146 4.761

10 GMM 2.505 2.674 2.685 2.876 3.066 3.697 2.830 3.024 3.164 2.798 2.747 2.532 11 Gujarat Apollo 3.226 3.582 5.580 5.905 6.458 6.969 5.543 5.262 6.009 7.489 7.757 6.390 12 HindustanDorr Oliver 22.611 21.348 32.400 47.516 37.924 36.607 22.986 25.703 33.312 14.585 25.929 18.580 13 Hitachi Home &Life 7.340 8.918 6.100 8.943 12.103 7.989 8.640 7.009 5.411 5.299 6.572 3.909 14 Ingersoll Rand 3.736 3.906 3.543 3.496 3.325 3.434 3.829 5.885 NA NA 4.172 NA 15 Jyoti 2.432 2.723 3.119 3.107 3.047 3.289 4.810 6.213 6.477 5.301 5.249 2.567 16 Jord Engg. 4.796 2.641 5.605 5.587 7.186 10.920 4.207 3.056 3.517 2.638 2.898 1.933 17 Kabra Extrusion 6.085 7.533 6.340 6.658 7.554 5.614 2.701 2.974 3.176 4.092 4.966 4.796 18 Kilburn Engg. 2.896 2.425 2.892 3.600 2.500 2.164 2.492 3.784 4.868 3.947 3.536 4.243 19 Mipco Seamless 5.599 5.232 4.930 4.076 3.767 4.882 5.156 4.274 3.957 3.990 2.755 3.618 20 Stovec Industries 4.194 3.167 3.523 3.801 3.712 3.519 3.614 3.073 3.607 5.114 5.473 6.843 21 Windsor Machines 2.617 2.729 1.912 2.112 1.394 3.083 1.747 2.046 1.548 1.803 1.993 1.550

224

Ratio 1

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 4.098 1.383 0.399 3.017 5.179 ABB 12 7.253 1.510 0.436 6.073 8.434 Batliboi 11 6.391 1.453 0.438 5.181 7.600 Bosch Re 12 4.090 0.773 0.223 3.486 4.694 Blue Star 12 6.630 0.653 0.188 6.120 7.141 Banco Products 12 5.595 1.295 0.374 4.583 6.608 Elecon 12 3.654 1.061 0.306 2.824 4.483 Eimco Elecon 12 3.104 0.722 0.208 2.540 3.668 FAGBearing 12 3.329 0.944 0.273 2.591 4.068 GMM 12 2.883 0.326 0.094 2.628 3.138 Gujarat Apollo 12 5.847 1.375 0.397 4.772 6.923 HindustanDorr Oliver 12 28.292 9.423 2.720 20.925 35.659 Hitachi Home &Life 12 7.353 2.169 0.626 5.657 9.049 Ingersoll Rand 9 3.925 0.781 0.260 3.165 4.685 Jyoti 12 4.028 1.479 0.427 2.872 5.184 Jord Engg. 12 4.582 2.524 0.729 2.609 6.555 Kabra Extrusion 12 5.207 1.709 0.493 3.872 6.543 Kilburn Engg. 12 3.279 0.843 0.243 2.620 3.938 Mipco Seamless 12 4.353 0.820 0.237 3.712 4.994 Stovec Industries 12 4.137 1.118 0.323 3.263 5.011 Windsor Machines 12 2.044 0.519 0.150 1.639 2.450

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 6919.340 20 345.967 58.683 0.000 1.617Within Groups 1338.279 227 5.896 Total 8257.619 247

Mean inventory turnover ratio of ABB is highest (7.253) among all the companies. GMM Pfaudler has mean ratio of 2.883 which is least among all companies. The ANOVA test is applied to compare the mean inventory turnover ratio for all the companies. F value is 58.683 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Sales turnover ratio has been higher in case of Asea Brown Boveri, and Blue Star. ABB and Blue Star are the professionally managed companies. HDO’s performance on this count is ignored, since it is concentrating on fabrication work which are basically labour jobs.

In case of all the companies covered under study, there was an increasing trend of sales from 1991 to 1996. After 1996, in majority of companies, the sales turnover and business activity has shown declining trend, till 2002. The work in process, old non-standard items and unused raw materials have been slow moving items.

225

Ratio 2; Return on Net Assets

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.385 0.366 0.289 0.181 0.175 0.161 0.169 0.090 NA 0.100 0.159 0.023 2 ABB 0.262 0.297 0.414 0.327 0.340 0.485 0.202 0.126 0.147 0.194 0.221 0.284 3 Batliboi 0.207 0.192 NA 0.297 0.279 0.202 0.107 0.167 0.266 NA NA NA 4 Bosch Re 0.225 0.222 0.221 0.213 NA 0.171 0.157 0.063 0.079 0.189 0.257 0.229 5 Blue Star 0.163 0.123 0.159 0.175 0.257 0.392 0.220 0.147 0.149 0.191 0.205 0.266 6 Banco Products 0.722 0.278 0.106 0.082 0.061 0.218 0.302 0.253 0.225 0.322 0.161 0.188 7 Elecon 0.191 0.180 0.214 0.198 0.237 0.206 0.168 0.148 0.205 0.090 0.058 0.053 8 Eimco Elecon 0.271 0.310 0.260 0.265 0.322 0.354 0.288 0.196 0.232 0.205 0.220 0.189 9 FAGBearing 0.267 0.148 0.161 0.112 0.214 0.358 0.244 0.152 0.128 0.173 0.192 0.210

10 GMM 0.394 0.424 0.379 0.467 0.317 0.365 0.247 0.139 0.129 0.072 0.055 0.035 11 Gujarat Apollo NA 0.089 0.204 0.219 0.232 0.220 0.228 0.211 0.185 0.182 0.165 0.150 12 HindustanDorr Oliver 0.266 0.230 0.265 0.209 0.166 0.260 0.134 0.238 0.089 NA 0.162 0.150 13 Hitachi Home &Life 0.059 0.075 0.059 0.122 0.124 0.183 0.157 0.132 NA 0.119 NA NA 14 Ingersoll Rand 0.266 0.409 0.375 0.363 0.515 1.103 0.237 0.301 0.245 0.239 0.210 NA 15 Jyoti 0.196 0.173 0.208 0.192 0.182 0.158 0.167 0.168 0.172 0.189 0.139 0.044 16 Jord Engg. NA 0.117 0.137 0.150 0.180 0.159 0.109 0.093 NA NA NA NA 17 Kabra Extrusion 0.192 0.215 0.267 0.300 0.217 0.285 0.136 0.085 0.090 0.124 0.161 0.184 18 Kilburn Engg. 0.252 0.255 0.225 0.151 0.176 0.162 0.192 0.077 NA NA NA 0.186 19 Mipco Seamless 0.252 0.280 0.207 0.160 0.057 0.140 0.206 0.057 NA 0.024 0.001 NA 20 Stovec Industries 0.205 0.100 0.129 0.132 0.089 0.129 0.007 NA 0.061 0.189 0.198 0.170 21 Windsor Machines 0.273 0.227 0.093 0.097 0.260 0.198 0.091 0.122 NA 0.047 0.050 NA

226

Ratio 2

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 11 0.191 0.113 0.034 0.097 0.285 ABB 12 0.275 0.106 0.031 0.192 0.358 Batliboi 8 0.215 0.063 0.022 0.146 0.283 Bosch Re 11 0.184 0.063 0.019 0.132 0.236 Blue Star 12 0.204 0.074 0.021 0.146 0.262 Banco Products 12 0.243 0.173 0.050 0.108 0.378 Elecon 12 0.162 0.062 0.018 0.114 0.211 Eimco Elecon 12 0.259 0.053 0.015 0.218 0.301 FAGBearing 12 0.197 0.069 0.020 0.143 0.250 GMM 12 0.252 0.158 0.046 0.128 0.376 Gujarat Apollo 11 0.190 0.043 0.013 0.154 0.225 HindustanDorr Oliver 11 0.197 0.060 0.018 0.147 0.247 Hitachi Home &Life 9 0.114 0.043 0.014 0.073 0.156 Ingersoll Rand 11 0.387 0.255 0.077 0.175 0.599 Jyoti 12 0.166 0.043 0.012 0.132 0.199 Jord Engg. 7 0.135 0.031 0.012 0.098 0.172 Kabra Extrusion 12 0.188 0.072 0.021 0.131 0.245 Kilburn Engg. 9 0.186 0.055 0.018 0.132 0.240 Mipco Seamless 10 0.138 0.099 0.031 0.050 0.227 Stovec Industries 11 0.128 0.061 0.019 0.077 0.179 Windsor Machines 10 0.146 0.086 0.027 0.069 0.223

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 0.812 20 0.041 3.933 0.000 1.622Within Groups 2.126 206 0.010 Total 2.938 226

Mean return on capital employed of Ingersoll Rand is highest (38.70) among all the companies. Hitachi Home & Life has mean ratio of 11.40 which is least among all companies. The ANOVA test is applied to compare the mean return on capital employed for all the companies. F value is 3.933 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Analysis of EBIT compared to net assets has been found highest in case of Ingersoll Rand, ABB and GMM Pfaudler. It is very high in case of Ingersoll Rand.

Return on Capital Employed (EBIT/Net Assets) has been found going down in good companies also, particularly after 1996. ROCE has been down because of reduced fixed assets turnover ratio, increased operating costs and increase in fixed assets not accompanied by turn over.

227

Ratio 3; Fixed Assets Turnover Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 2.828 3.900 3.644 2.399 3.098 1.819 1.650 1.133 1.092 1.636 2.234 1.503 2 ABB 6.373 6.594 7.682 6.922 8.974 9.117 5.640 4.668 5.627 5.600 6.668 8.174 3 Batliboi 7.147 7.525 NA 10.867 5.987 6.815 5.770 5.267 4.609 NA 2.306 1.396 4 Bosch Re 3.864 4.283 4.290 4.551 5.454 NA 2.829 2.709 3.401 3.966 4.381 5.202 5 Blue Star 7.553 8.510 8.829 10.131 8.954 10.352 11.175 6.432 5.360 5.315 6.227 9.091 6 Banco Products 8.542 8.272 8.899 6.365 5.096 4.903 4.181 4.444 4.060 4.507 5.576 4.625 7 Elecon Engg. 5.025 4.702 5.280 7.631 7.689 4.828 3.602 2.948 4.211 2.814 2.566 2.811 8 Eimco Elecon 7.716 9.246 11.771 6.275 6.048 4.817 3.872 3.471 4.549 3.708 4.076 3.062 9 FAGBearing 2.762 2.676 2.333 1.847 2.106 2.478 1.979 1.885 NA 2.069 2.405 2.535

10 GMM 4.320 4.778 5.465 5.595 3.328 2.545 2.521 1.857 2.335 1.910 2.177 2.072 11 Gujarat Apollo NA 3.403 5.410 4.373 4.215 NA NA NA 5.594 7.365 6.930 5.120 12 HindustanDorr Oliver 22.000 15.726 19.837 21.192 18.375 2.044 1.440 1.669 1.469 0.816 1.092 1.263 13 Hitachi Home &Life 3.189 3.802 4.012 7.285 12.103 NA NA 6.624 5.412 6.372 11.732 7.325 14 Ingersoll Rand 11.394 14.980 14.175 8.590 7.198 6.853 6.091 7.704 6.700 7.753 7.382 NA 15 Jyoti Ltd. 2.267 2.868 3.325 3.321 4.109 5.210 7.754 6.889 47.957 6.883 6.655 3.593 16 Jord Engg. NA 2.931 2.470 3.012 1.794 2.076 3.125 2.088 NA 1.413 1.663 0.746 17 Kabra Extrusion 12.077 13.780 13.737 12.000 8.323 2.933 2.218 2.662 2.595 2.920 3.760 3.755 18 Kilburn Engg. 6.200 4.655 4.917 1.934 1.472 1.774 2.439 3.218 2.577 0.902 0.634 0.900 19 Mipco Seamless 2.213 2.908 3.263 2.076 0.855 1.297 1.700 1.047 0.789 1.302 1.276 1.652 20 Stovec Industries 3.125 2.931 3.162 2.795 1.271 1.449 NA 1.673 1.904 2.512 2.908 2.985 21 Windsor Machines 8.818 7.490 4.565 4.241 5.063 4.940 2.758 3.119 2.486 3.053 3.512 2.977

228

Ratio 3

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 2.245 0.944 0.273 1.506 2.983 ABB 12 6.837 1.405 0.406 5.738 7.935 Batliboi 10 5.769 2.684 0.849 3.367 8.171 Bosch Re 11 4.084 0.867 0.261 3.363 4.806 Blue Star 12 8.161 1.974 0.570 6.617 9.704 Banco Products 12 5.789 1.795 0.518 4.386 7.193 Elecon 12 4.509 1.751 0.506 3.140 5.878 Eimco Elecon 12 5.718 2.662 0.768 3.637 7.799 FAGBearing 11 2.280 0.319 0.096 2.014 2.546 GMM 12 3.242 1.415 0.409 2.135 4.348 Gujarat Apollo 8 5.301 1.346 0.476 3.855 6.747 HindustanDorr Oliver 12 8.910 9.407 2.716 1.555 16.265 Hitachi Home &Life 10 6.786 3.071 0.971 4.037 9.535 Ingersoll Rand 11 8.984 3.097 0.934 6.404 11.563 Jyoti 12 8.403 12.592 3.635 -1.443 18.248 Jord Engg. 10 2.132 0.767 0.242 1.446 2.818 Kabra Extrusion 12 6.730 4.846 1.399 2.941 10.519 Kilburn Engg. 12 2.635 1.783 0.515 1.241 4.029 Mipco Seamless 12 1.698 0.785 0.227 1.084 2.312 Stovec Industries 11 2.429 0.714 0.215 1.834 3.024 Windsor Machines 12 4.418 1.965 0.567 2.882 5.955

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 1321.232 20 66.062 4.003 0.000 1.619Within Groups 3581.044 217 16.503 Total 4902.276 237

Mean assets turnover ratio of Ingersoll Rand is highest (8.984) among

all the companies. Mipco Seamless has mean ratio of 1.698 which is least among all companies. The ANOVA test is applied to compare the mean assets turnover for all the companies. F value is 4.003 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Asset utilization has been found highest in case of Ingersoll Rand, Jyoti Ltd. and Blue Star.

In most of the companies covered by the study, the fixed assets utilization increased 1991 onwards till 1996. In few companies the increasing trend was till 1997. However, in all the cases, there was a drastic down trend after 1997, till 2002. In very few companies like ABB, Blue Star, Hindustan Dorr Oliver, Ingersoll Rand and Kabra Extrusion, the fixed assets utilization has been found very high as compared to other companies.

229

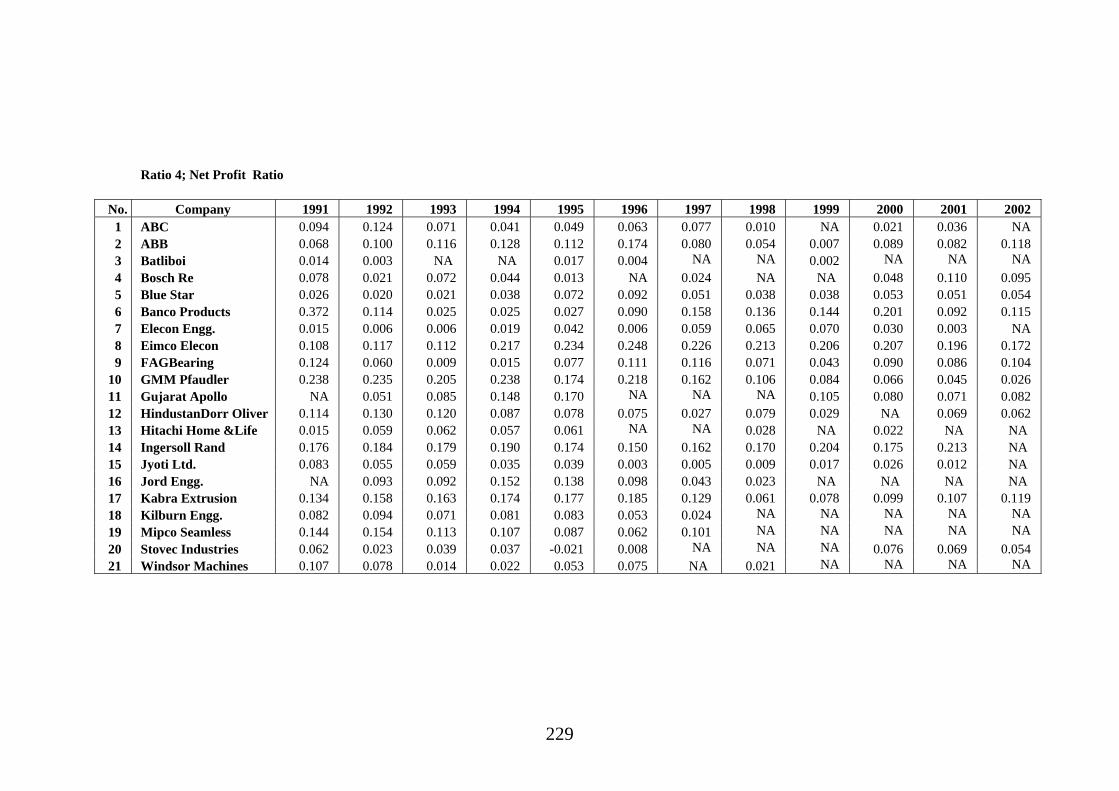

Ratio 4; Net Profit Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.094 0.124 0.071 0.041 0.049 0.063 0.077 0.010 NA 0.021 0.036 NA 2 ABB 0.068 0.100 0.116 0.128 0.112 0.174 0.080 0.054 0.007 0.089 0.082 0.118 3 Batliboi 0.014 0.003 NA NA 0.017 0.004 NA NA 0.002 NA NA NA 4 Bosch Re 0.078 0.021 0.072 0.044 0.013 NA 0.024 NA NA 0.048 0.110 0.095 5 Blue Star 0.026 0.020 0.021 0.038 0.072 0.092 0.051 0.038 0.038 0.053 0.051 0.054 6 Banco Products 0.372 0.114 0.025 0.025 0.027 0.090 0.158 0.136 0.144 0.201 0.092 0.115 7 Elecon Engg. 0.015 0.006 0.006 0.019 0.042 0.006 0.059 0.065 0.070 0.030 0.003 NA 8 Eimco Elecon 0.108 0.117 0.112 0.217 0.234 0.248 0.226 0.213 0.206 0.207 0.196 0.172 9 FAGBearing 0.124 0.060 0.009 0.015 0.077 0.111 0.116 0.071 0.043 0.090 0.086 0.104

10 GMM Pfaudler 0.238 0.235 0.205 0.238 0.174 0.218 0.162 0.106 0.084 0.066 0.045 0.026 11 Gujarat Apollo NA 0.051 0.085 0.148 0.170 NA NA NA 0.105 0.080 0.071 0.082 12 HindustanDorr Oliver 0.114 0.130 0.120 0.087 0.078 0.075 0.027 0.079 0.029 NA 0.069 0.062 13 Hitachi Home &Life 0.015 0.059 0.062 0.057 0.061 NA NA 0.028 NA 0.022 NA NA 14 Ingersoll Rand 0.176 0.184 0.179 0.190 0.174 0.150 0.162 0.170 0.204 0.175 0.213 NA 15 Jyoti Ltd. 0.083 0.055 0.059 0.035 0.039 0.003 0.005 0.009 0.017 0.026 0.012 NA 16 Jord Engg. NA 0.093 0.092 0.152 0.138 0.098 0.043 0.023 NA NA NA NA 17 Kabra Extrusion 0.134 0.158 0.163 0.174 0.177 0.185 0.129 0.061 0.078 0.099 0.107 0.119 18 Kilburn Engg. 0.082 0.094 0.071 0.081 0.083 0.053 0.024 NA NA NA NA NA 19 Mipco Seamless 0.144 0.154 0.113 0.107 0.087 0.062 0.101 NA NA NA NA NA 20 Stovec Industries 0.062 0.023 0.039 0.037 -0.021 0.008 NA NA NA 0.076 0.069 0.054 21 Windsor Machines 0.107 0.078 0.014 0.022 0.053 0.075 NA 0.021 NA NA NA NA

230

Ratio 4 C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper BoundABC 10 0.059 0.034 0.011 0.028 0.089 ABB 12 0.094 0.042 0.012 0.061 0.127 Batliboi 5 0.008 0.007 0.003 -0.004 0.020 Bosch Re 9 0.056 0.034 0.011 0.023 0.090 Blue Star 12 0.046 0.021 0.006 0.030 0.063 Banco Products 12 0.125 0.096 0.028 0.050 0.200 Elecon 11 0.029 0.026 0.008 0.008 0.051 Eimco Elecon 12 0.188 0.049 0.014 0.149 0.227 FAGBearing 12 0.075 0.038 0.011 0.046 0.105 GMM 12 0.150 0.080 0.023 0.087 0.212 Gujarat Apollo 8 0.099 0.040 0.014 0.056 0.142 HindustanDorr Oliver 11 0.079 0.033 0.010 0.051 0.107 Hitachi Home &Life 7 0.043 0.021 0.008 0.018 0.068 Ingersoll Rand 11 0.180 0.018 0.005 0.165 0.194 Jyoti 11 0.031 0.026 0.008 0.010 0.053 Jord Engg. 7 0.091 0.047 0.018 0.035 0.148 Kabra Extrusion 12 0.132 0.040 0.012 0.101 0.164 Kilburn Engg. 7 0.069 0.024 0.009 0.041 0.098 Mipco Seamless 7 0.109 0.032 0.012 0.071 0.148 Stovec Industries 9 0.039 0.031 0.010 0.008 0.069 Windsor Machines 7 0.053 0.035 0.013 0.010 0.096

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 0.496 20 0.025 12.766 0.000 1.628Within Groups 0.356 183 0.002 Total 0.852 203

Mean net profit ratio of Eimco Elecon is highest (18.80) among all the companies. Batliboi has mean ratio of 0.80 which is least among all companies. The ANOVA test is applied to compare the mean net profit ratio for all the companies. F value is 12.766 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 0.01, it is concluded that this difference is significant at less than 1% level of significance.

Ingersoll Rand, Eimco Elecon and Kabra Extrusion have been found to have very high profitability. Batliboi and Jyoti Ltd. had least net profit ratio during the period of study, i.e. 1991 to 2002.

In majority of the companies, increase in net profit (profit after tax) has been observed till 1996. After 1996, there is a fall in the amount and rate of net profit earned by the engineering companies till 2002. This shows general slow down of economy after 1996.

In case of two companies, Blue Star and Ingersoll Rand, which are professionally managed companies, the profit level was down after 1996. However, only these two companies were able to restore the level of satisfactory profitability by 2002. In other cases there was a down trend after 1996 till 2002.

231

Ratio 5; Return on Equity

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.862 1.034 0.643 0.442 0.466 0.218 0.219 0.021 NA 0.064 0.090 0.000 2 ABB 0.159 0.220 0.186 0.227 0.229 0.384 0.146 0.082 0.101 0.136 0.131 0.190 3 Batliboi 0.089 0.021 NA NA 0.108 0.038 NA NA 0.023 NA NA 0.000 4 Bosch Re 0.221 0.072 0.137 0.139 0.084 NA 0.077 0.071 0.053 NA NA 0.090 5 Blue Star 0.132 0.107 0.112 0.122 0.266 0.256 0.144 0.144 0.144 0.186 0.214 0.246 6 Banco Products 1.343 0.341 0.079 0.003 0.067 0.204 0.242 0.203 0.190 0.240 0.117 0.137 7 Elecon 0.011 0.019 0.021 0.034 0.169 0.210 0.151 0.141 0.120 0.046 0.005 0.000 8 Eimco Elecon 0.245 0.203 0.130 0.201 0.231 0.295 0.184 0.133 0.146 0.141 0.131 0.121 9 FAGBearing 0.195 0.160 0.018 0.038 0.145 0.138 0.178 0.145 0.065 0.147 0.169 0.193

10 GMM 0.298 0.276 0.275 0.340 0.242 0.344 0.238 0.119 0.066 0.043 0.041 0.025 11 Gujarat Apollo NA 0.198 0.269 0.250 0.259 NA NA NA 0.216 0.161 0.150 0.147 12 HindustanDorr Oliver 0.092 0.094 0.072 0.059 0.082 0.076 0.009 0.050 0.015 NA 0.052 0.045 13 Hitachi H & L NA 0.133 0.138 0.218 0.266 NA NA 0.120 NA 0.100 NA 0.000 14 Ingersoll Rand 0.241 0.261 0.254 0.243 0.221 0.220 0.237 0.292 0.265 0.228 0.203 NA 15 Jyoti 0.198 0.153 0.203 0.005 0.010 0.007 0.009 0.007 0.053 0.098 0.036 0.000 16 Jord Engg. NA 0.073 0.077 0.167 0.207 0.176 0.093 0.058 NA NA NA NA 17 Kabra Extrusion 0.214 0.256 0.272 0.293 0.162 0.224 0.114 0.068 0.076 0.117 0.135 0.115 18 Kilburn Engg. 0.251 0.202 0.199 0.110 0.125 0.114 0.067 NA NA NA NA NA 19 Mipco Seamless 0.341 0.259 0.143 0.153 0.155 0.146 0.164 NA NA NA NA NA 20 Stovec Industries 0.224 0.047 0.075 0.072 0.021 0.019 NA NA NA 0.207 0.183 0.105 21 Windsor Machines 0.351 0.170 0.032 0.053 0.107 0.183 0.196 NA 0.060 NA NA 0.000

232

Ratio 5

C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 11 0.369 0.353 0.107 0.075 0.663

ABB 12 0.183 0.080 0.023 0.120 0.245

Batliboi 6 0.047 0.043 0.017 -0.014 0.107

Bosch Re 9 0.105 0.053 0.018 0.054 0.156

Blue Star 12 0.173 0.058 0.017 0.127 0.219

Banco Products 12 0.264 0.352 0.102 -0.012 0.539

Elecon 12 0.077 0.075 0.022 0.018 0.136

Eimco Elecon 12 0.180 0.056 0.016 0.136 0.224

FAGBearing 12 0.133 0.060 0.017 0.086 0.179

GMM 12 0.192 0.124 0.036 0.095 0.289

Gujarat Apollo 8 0.206 0.050 0.018 0.152 0.260

HindustanDorr Oliver 11 0.059 0.028 0.009 0.035 0.082

Hitachi Home &Life 7 0.139 0.085 0.032 0.036 0.243

Ingersoll Rand 11 0.242 0.025 0.008 0.222 0.263

Jyoti 12 0.065 0.078 0.023 0.004 0.126

Jord Engg. 7 0.122 0.060 0.023 0.049 0.194

Kabra Extrusion 12 0.171 0.078 0.023 0.109 0.232

Kilburn Engg. 7 0.152 0.065 0.025 0.073 0.231

Mipco Seamless 7 0.194 0.076 0.029 0.102 0.287

Stovec Industries 9 0.106 0.079 0.026 0.029 0.183

Windsor Machines 9 0.128 0.109 0.036 0.022 0.234

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 1.202 20 0.060 3.252 0.000 1.626

Within Groups 3.493 189 0.018

Total 4.695 209

233

Mean return on equity of Antifriction Bearing Corporation is highest (36.90) among all the companies. Batliboi has mean ratio of 4.70 which is least among all companies. The ANOVA test is applied to compare the mean return on equity for all the companies. F value is 3.252 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Return on equity has been found higher in case of ABC Bearings, Banco Products and Ingersoll Rand.

It is evident that between 1991 to 1996, the share capital of majority of companies has gone up. After 1996 till 2002, there were no major share capital issues by the companies. This is because of the fact that after 1991, on account of Harshad Mehta factor since the stock market was booming, new share issues were a common phenomena. Harshad Mehta's scam came out in 1992, because of which investors were very cautious. Another reason being after 1996, there was a down trend in general economic activity and recessionary trend which did not warrant new fixed investments in different industries.

Earning on shareholders' funds also shown improvement year by year from 1991 till 1996. This has gone down after 1996, and resultant effect on dividends declared on equity shares. Ingersoll Rand has maintained very healthy trend of net profit to net worth throughout the period of study, i. e. 1991 to 2002. In case of some of the companies like Elecon Engineering, FAG Bearings and GMM Pfaudler, this profitability has substantially gone down after 1996. In certain other cases, there have been losses after 1996.

The analysis of return on investment (ROI) of all the companies reveal that ROI rate has gone up year by year after 1991 till 1996. In all the cases, except Ingersoll Rand, ROI has gone down after 1996. The rate of ROI which was in 1996 has not been reached till 2002. Ingersoll Rand has maintained good ROI, being a well managed professional business enterprise in the field of engineering.

234

Ratio 6; Dividend Pay Out Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.266 0.299 0.301 0.306 0.299 0.350 0.349 0.100 NA NA NA NA 2 ABB 0.280 0.300 0.300 0.350 0.400 0.787 0.500 0.500 0.500 0.500 0.500 0.600 3 Batliboi 0.200 0.150 NA NA 0.093 0.107 NA NA NA NA NA NA 4 Bosch Re 0.200 0.142 0.153 0.270 0.293 0.100 NA NA NA NA NA NA 5 Blue Star 0.339 0.180 0.230 0.250 0.349 0.350 0.350 0.350 0.350 0.500 0.550 0.650 6 Banco Products 0.200 0.253 0.122 0.178 0.133 0.180 0.200 0.300 0.350 0.300 0.300 0.400 7 Elecon 0.060 NA 0.080 0.100 0.160 0.160 0.159 0.181 0.200 0.181 NA NA 8 Eimco Elecon 0.202 0.394 0.142 0.250 0.249 0.270 0.270 0.270 0.270 0.270 0.300 0.329 9 FAGBearing 0.200 0.200 0.100 0.120 0.150 0.200 0.200 0.200 0.270 0.350 0.350 0.400

10 GMM 0.550 0.653 0.750 1.100 1.150 1.151 1.151 1.151 1.151 0.748 0.503 0.252 11 Gujarat Apollo NA 0.077 0.136 0.184 0.297 NA NA NA 0.400 0.251 0.200 0.114 12 HindustanDorr Oliver 0.299 0.299 0.299 0.299 0.349 0.600 0.101 0.202 0.101 0.152 0.152 0.120 13 Hitachi H & L 0.100 0.094 0.106 0.139 0.186 NA NA 0.149 NA 0.100 NA NA 14 Ingersoll Rand 0.350 0.450 0.250 0.300 0.350 0.400 0.450 0.650 0.700 0.800 0.800 NA 15 Jyoti NA NA NA NA 0.120 NA NA NA NA NA NA NA 16 Jord Engg. NA 0.068 0.114 0.224 0.237 0.250 NA NA NA NA NA NA 17 Kabra Extrusion 0.150 0.180 0.251 0.281 0.306 0.399 0.399 0.300 0.200 0.200 0.240 0.350 18 Kilburn Engg. 0.120 0.200 0.200 0.186 0.225 0.200 0.101 NA NA NA NA NA 19 Mipco Seamless 0.120 0.150 0.150 0.150 0.150 0.201 0.200 0.075 NA NA NA NA 20 Stovec Industries 0.270 0.261 0.269 0.263 0.100 0.100 NA NA NA 0.254 0.301 0.239 21 Windsor Machines 0.200 0.169 0.100 0.100 0.179 0.240 0.100 0.100 NA NA NA NA

235

Ratio 6

C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 8 0.284 0.079 0.028 0.199 0.369

ABB 12 0.460 0.146 0.042 0.346 0.574

Batliboi 4 0.137 0.048 0.024 0.022 0.253

Bosch Re 6 0.193 0.076 0.031 0.086 0.301

Blue Star 12 0.371 0.135 0.039 0.265 0.476

Banco Products 12 0.243 0.088 0.025 0.174 0.312

Elecon 9 0.142 0.050 0.017 0.094 0.190

Eimco Elecon 12 0.268 0.061 0.018 0.220 0.316

FAGBearing 12 0.228 0.095 0.027 0.154 0.303

GMM 12 0.859 0.322 0.093 0.607 1.111

Gujarat Apollo 8 0.208 0.106 0.037 0.094 0.321

HindustanDorr Oliver 12 0.248 0.143 0.041 0.136 0.360

Hitachi Home &Life 7 0.125 0.034 0.013 0.083 0.167

Ingersoll Rand 11 0.500 0.201 0.061 0.332 0.668

Jyoti 1 0.120

Jord Engg. 5 0.179 0.082 0.037 0.035 0.322

Kabra Extrusion 12 0.271 0.083 0.024 0.206 0.336

Kilburn Engg. 7 0.176 0.047 0.018 0.119 0.232

Mipco Seamless 8 0.150 0.041 0.014 0.106 0.193

Stovec Industries 9 0.229 0.075 0.025 0.156 0.301

Windsor Machines 8 0.148 0.056 0.020 0.088 0.208

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 6.019 20 0.301 17.777 0.000 1.634

Within Groups 2.810 166 0.017

Total 8.830 186

236

Mean dividend payout ratio of GMM Pfaudler is highest (85.90)

among all the companies. Batliboi has mean ratio of 13.70 which is

least among all the companies. The ANOVA test is applied to

compare the mean dividend payout ratiofor all the companies. F value

is 17.777 with the corresponding P value 0.000. As P value is less

than 0.01, it is concluded that this difference is significant at less than

1 % level of significance.

During the period of 1991 to 2002, dividend payout was very high

in case of GMM Pfaudler, Ingersoll Rand and ABB.

Increasing trend has been observed in the rate of dividend declared

by majority of companies from 1991 to 1996. This is on account of

more earnings on equity till 1996. After 1996, the rate of dividend

declared/paid by different companies has fallen down year by year

on account of lesser business and resultant reduced profit before

tax as well as profit after tax. Only in case of two companies,

Ingersoll Rand and Blue Star there was increase of dividend

declared after 1996, on account of their ability to sustain business

operations, cost control and good profitability during that period.

Some of the companies like Bosch Rexroth, Elecon Engineering,

Jord Engineering, Kilburn Engineering and Windsor Machines

incurred losses after 1996 till 2002. This is due to reduced

business, absence of cost control and lower profitability on account

of operations at lower level of activity (Sales), and having heavy

pressure of fixed overheads.

237

Ratio 7; Earnings Per Share

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 8.916 14.831 9.221 6.338 5.882 NA 13.426 1.263 NA 1.870 2.857 NA 2 ABB 10.061 16.907 14.879 16.347 20.129 49.871 15.653 9.112 8.982 13.040 15.415 22.928 3 Batliboi 10.577 2.476 NA NA 10.528 2.545 NA NA 0.939 NA NA NA 4 Bosch Re 6.933 1.511 3.667 3.867 2.333 NA 1.644 NA NA 4.302 8.396 9.189 5 Blue Star 11.962 5.207 5.798 6.071 16.302 9.293 5.454 5.724 6.004 8.577 11.585 14.223 6 Banco Products 48.267 4.000 2.434 3.467 2.219 13.284 20.089 20.237 22.278 17.056 8.935 10.917 7 Elecon 0.638 1.116 1.222 2.036 11.829 18.187 15.105 16.088 15.257 6.018 0.602 NA 8 Eimco Elecon 17.374 17.879 6.411 11.901 17.039 15.407 13.432 10.693 13.293 14.437 14.818 14.558 9 FAGBearing 8.160 5.138 0.840 1.713 4.908 5.122 7.354 6.205 4.326 7.750 9.037 11.895

10 GMM 14.645 16.279 19.547 30.987 25.393 42.929 35.072 19.359 10.999 9.436 9.077 5.795 11 Gujarat Apollo NA 2.950 5.182 7.160 7.143 NA NA NA 10.686 8.943 NA 9.543 12 HindustanDorr Oliver 5.453 5.789 6.695 5.621 8.232 11.411 1.389 7.642 2.253 NA 7.432 6.716 13 Hitachi H & L 0.322 1.582 2.012 3.548 5.865 NA NA 3.663 NA 2.652 NA NA 14 Ingersoll Rand 8.971 11.537 6.665 7.463 7.745 8.715 11.163 15.497 17.188 16.593 16.171 NA 15 Jyoti 15.230 8.907 8.237 3.594 4.503 0.424 0.248 0.197 2.142 3.135 1.200 NA 16 Jord Engg. NA 1.429 1.382 6.272 6.484 8.273 3.636 2.398 NA NA NA NA 17 Kabra Extrusion 3.371 4.794 6.255 8.427 8.980 14.810 7.551 4.781 5.510 8.834 11.079 10.292 18 Kilburn Engg. 3.392 2.910 3.085 2.889 3.422 3.215 1.956 NA NA NA NA NA 19 Mipco Seamless 5.437 5.037 3.002 3.502 3.936 3.983 4.930 NA NA NA NA NA 20 Stovec Industries 19.820 3.866 6.723 7.177 2.010 1.770 NA NA NA 12.919 13.254 6.938 21 Windsor Machines 9.633 6.353 1.203 1.917 4.663 9.018 NA 1.863 NA NA NA NA

238

Ratio 7

C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 9 7.178 4.861 1.620 2.450 11.907

ABB 12 17.777 10.945 3.160 9.219 26.335

Batliboi 5 5.413 4.735 2.118 -2.863 13.689

Bosch Re 9 4.649 2.868 0.956 1.859 7.439

Blue Star 12 8.850 3.832 1.106 5.854 11.846

Banco Products 12 14.432 12.951 3.739 4.306 24.557

Elecon 11 8.009 7.272 2.192 1.953 14.065

Eimco Elecon 12 13.937 3.198 0.923 11.436 16.437

FAGBearing 12 6.037 3.076 0.888 3.632 8.442

GMM 12 19.960 11.519 3.325 10.954 28.966

Gujarat Apollo 7 7.372 2.665 1.007 4.143 10.602

HindustanDorr Oliver 11 6.239 2.741 0.827 3.956 8.522

Hitachi Home &Life 7 2.806 1.778 0.672 0.651 4.961

Ingersoll Rand 11 11.610 4.050 1.221 8.237 14.983

Jyoti 11 4.347 4.697 1.416 0.435 8.259

Jord Engg. 7 4.268 2.746 1.038 0.939 7.596

Kabra Extrusion 12 7.890 3.224 0.931 5.370 10.411

Kilburn Engg. 7 2.981 0.499 0.189 2.376 3.586

Mipco Seamless 7 4.261 0.892 0.337 3.180 5.342

Stovec Industries 9 8.275 5.980 1.993 2.458 14.092

Windsor Machines 7 4.950 3.495 1.321 0.714 9.186

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 4776.203 20 238.810 6.246 0.000 1.629Within Groups 6920.274 181 38.234 Total 11696.477 201

239

Mean earnings per share of GMM Pfaudler is highest (199.60)

among all the companies. Kilburn Engineering has mean ratio of

29.81 which is least among all the companies. The ANOVA test is

applied to compare the mean earnings per share for all the

companies. F value is 6.246 with the corresponding P value 0.000.

As P value is less than 0.01 %, it is concluded that this difference

is significant at less than 1 % level of significance.

EPS has been found very high in case of GMM Pfaudler, ABB and

Banco Products. It was very low for Kilburn Engineering and Jord

Engineering.

In most of the cases, the EPS has moderately increased from 1991

to 1996. After 1996 there is a down trend in many companies. In

case of some companies, it has been found that their EPS in 2002

was lower than 1991, on account of recessionary pressures, lower

business, increasing administrative expenses and no control on

overheads. When the EPS of 2002 is compared with EPS of 1991,

it is evident that it has gone up by 127 % for ABB, 20 % for Blue

Star and 90 % for Ingersoll Rand. In case of ABB, the earning per

share in 1996 was at peak, i. e. five times, an increase of 495 %

after 1991. In case of GMM Pfaudler also in 1996 this was four

times compared to 1991 and increase of 300 percent compared to

1991. However, this can be considered an exceptional cases.

Overall, in majority of the cases, the EPS has gone down on

account of general recession in the economy after 1996, lesser

business and pressures on the cost structure.

240

Ratio 8; Tax Provision to Profit Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

1 ABC 0.513 0.387 0.374 NA 0.160 0.021 0.148 0.110 NA 0.036 0.096 NA 2 ABB 0.418 0.047 0.419 0.036 0.376 0.238 0.255 0.244 0.030 0.023 0.002 0.029 3 Batliboi NA NA NA NA NA NA NA NA NA NA NA NA 4 Bosch Re 0.350 0.382 0.493 NA NA NA 0.295 NA NA 0.066 0.378 0.409 5 Blue Star 0.096 0.119 0.088 0.350 0.259 0.290 0.378 0.146 0.101 0.078 0.008 0.006 6 Banco Products 0.044 0.247 0.140 0.959 1.497 0.187 0.299 0.290 0.278 0.312 0.318 0.277 7 Elecon 0.825 NA 0.169 0.661 0.150 0.171 0.128 0.134 0.375 0.320 0.128 NA 8 Eimco Elecon 0.526 0.606 0.538 0.453 0.402 0.373 0.383 0.376 0.364 0.365 0.402 0.248 9 FAGBearing 0.456 NA 0.026 NA 0.222 0.517 0.436 0.269 0.077 0.301 0.225 0.198

10 GMM 0.375 0.481 0.467 0.453 0.459 0.423 0.333 0.256 0.463 0.303 0.256 0.204 11 Gujarat Apollo NA NA 0.245 0.304 0.265 NA NA NA 0.213 0.039 0.333 0.303 12 HindustanDorr Oliver 0.535 0.521 0.453 0.494 0.236 0.304 0.705 0.442 0.483 NA 0.066 0.243 13 Hitachi H & L NA 0.289 0.040 NA NA NA NA NA NA 0.048 NA NA 14 Ingersoll Rand 0.375 0.412 0.408 0.403 0.344 0.341 0.321 0.315 0.313 0.311 0.291 NA 15 Jyoti NA NA NA NA NA 0.556 0.662 0.850 0.040 0.239 0.393 NA 16 Jord Engg. NA NA NA 0.009 NA NA 0.031 0.024 NA NA NA NA 17 Kabra Extrusion 0.143 0.285 0.345 0.375 0.375 0.191 0.220 0.109 0.156 0.165 0.269 0.235 18 Kilburn Engg. 0.296 0.453 0.435 0.278 0.091 0.172 0.138 NA NA NA NA NA 19 Mipco Seamless NA 0.274 0.411 0.205 NA NA 0.372 NA NA NA NA NA 20 Stovec Industries NA 0.352 0.448 NA NA NA NA NA NA 0.115 0.086 0.076 21 Windsor Machines 0.227 0.269 NA 0.051 0.153 0.120 NA 0.107 NA NA NA NA

241

Ratio 8

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 9 0.205 0.175 0.058 0.035 0.375

ABB 12 0.177 0.167 0.048 0.046 0.307

Batliboi 0

Bosch Re 7 0.339 0.135 0.051 0.176 0.502

Blue Star 12 0.160 0.127 0.037 0.060 0.259

Banco Products 12 0.404 0.410 0.118 0.084 0.724

Elecon 10 0.306 0.248 0.079 0.084 0.528

Eimco Elecon 12 0.420 0.097 0.028 0.344 0.495

FAGBearing 10 0.273 0.160 0.051 0.130 0.416

GMM 12 0.373 0.099 0.029 0.296 0.450

Gujarat Apollo 7 0.243 0.099 0.037 0.123 0.363 HindustanDorr Oliver 11 0.408 0.178 0.054 0.259 0.556

Hitachi Home &Life 3 0.125 0.142 0.082 -0.497 0.748

Ingersoll Rand 11 0.349 0.044 0.013 0.312 0.385

Jyoti 6 0.457 0.294 0.120 0.041 0.872

Jord Engg. 3 0.021 0.012 0.007 -0.029 0.072

Kabra Extrusion 12 0.239 0.092 0.026 0.167 0.311

Kilburn Engg. 7 0.266 0.142 0.054 0.094 0.438

Mipco Seamless 4 0.315 0.094 0.047 0.090 0.541

Stovec Industries 5 0.215 0.173 0.077 -0.087 0.517

Windsor Machines 6 0.154 0.081 0.033 0.040 0.269

ANOVA Source of Variation SS Df MSS F-Calc P-value F crit

Between Groups 1.730 19 0.091 2.785 0.000 1.656Within Groups 4.937 151 0.033 Total 6.667 170

242

Mean tax provision to PBT ratio of Jyoti Ltd. is highest (45.70)

among all the companies. Blue Star has mean ratio of 16.00 which

is least among all the companies (Jord Engineering & Hitachi

ignored, since they are loss making companies). The ANOVA test

is applied to compare the mean tax provision to PBT ratio for all

the companies. F value is 2.785 with the corresponding P value

0.000. As P value is less than 0.01, it is concluded that this

difference is significant at less than 1 % level of significance.

It has been observed that among all the companies, Blue Star,

ABB, and FAG Bearings have been doing best tax planning,

whereby they pay least income tax. Their average tax provision

made in books is least among all the companies. Jyoti Ltd.,

Hindustan Dorr Oliver and Banco Products have very weak tax

planning.

Effective Tax planning has not been observed in majority of the

cases. Only professionally managed companies like ABB, Blue

Star and Ingersoll Rand have paid lesser corporation tax than the

rate of effective tax on profit before tax earned by them. To some

extent, companies like Elecon Engineering, Banco products and

Kabra Extrusion are found to practice systemic tax planning, by

making lower tax provision and least possible tax payment. Tax

planning leads to saving of money and its plough back in the

business. This can increase the financial strength of the company.

This has not been observed in case of other companies.

243

Ratio 9; Sales to Admn. and General Expenses Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.015 0.014 0.018 0.032 0.024 0.024 0.045 0.065 0.047 0.046 0.047 0.068 2 ABB 0.116 0.105 0.098 0.111 0.108 0.091 0.109 0.143 0.123 0.116 0.110 0.107 3 Batliboi 0.062 0.066 NA 0.050 0.062 0.070 0.086 0.099 0.116 NA 0.169 0.265 4 Bosch Re 0.134 0.160 0.108 0.175 0.156 0.147 0.136 0.142 0.113 0.115 0.100 0.104 5 Blue Star 0.101 0.082 0.093 0.085 0.084 0.098 0.091 0.085 0.088 0.089 0.086 0.090 6 Banco Products 0.056 0.061 0.067 0.067 0.059 0.065 0.071 0.086 0.094 0.091 0.101 0.091 7 Elecon 0.082 0.089 0.062 0.044 0.054 0.065 0.078 0.085 0.074 0.089 0.100 0.121 8 Eimco Elecon 0.104 0.110 0.098 0.109 0.103 0.126 0.132 0.170 0.154 0.141 0.125 0.129 9 FAGBearing 0.182 0.137 0.151 0.175 0.182 0.116 0.130 0.123 0.115 0.134 0.131 0.144

10 GMM 0.093 0.124 0.148 0.103 0.110 0.125 0.120 0.206 0.158 0.142 0.163 0.151 11 Gujarat Apollo NA 0.074 0.088 0.103 0.102 NA NA NA 0.099 0.083 0.079 0.066 12 HindustanDorr Oliver 0.040 0.050 0.096 0.090 0.108 0.104 0.110 0.118 0.121 0.256 0.191 0.162 13 Hitachi H & L 0.005 0.011 0.046 0.059 0.082 NA NA 0.142 0.148 0.171 0.157 0.148 14 Ingersoll Rand 0.110 0.095 0.122 0.115 0.111 NA 0.087 0.103 0.182 0.213 0.246 NA 15 Jyoti 0.088 0.069 0.074 0.071 0.056 0.068 0.071 0.098 0.117 0.114 0.070 0.087 16 Jord Engg. NA 0.047 0.056 0.038 0.035 0.038 0.067 0.035 NA 0.032 0.021 0.033 17 Kabra Extrusion 0.089 0.055 0.074 0.056 0.058 0.094 0.128 0.126 0.144 0.121 0.134 0.121 18 Kilburn Engg. 0.198 0.265 0.161 0.125 0.166 0.149 0.156 0.170 0.236 1.006 0.440 0.250 19 Mipco Seamless 0.020 0.033 0.035 0.038 0.031 0.025 0.034 0.028 0.073 0.030 0.035 0.061 20 Stovec Industries 0.138 0.117 0.115 0.106 0.124 0.125 NA 0.111 0.126 0.156 0.147 0.122 21 Windsor Machines 0.054 0.055 0.080 0.074 0.064 0.086 0.121 0.131 0.190 0.142 0.134 0.156

244

Ratio 9

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 0.037 0.019 0.005 0.022 0.052 ABB 12 0.111 0.013 0.004 0.101 0.122 Batliboi 10 0.105 0.067 0.021 0.045 0.164 Bosch Re 12 0.133 0.024 0.007 0.113 0.152 Blue Star 12 0.089 0.006 0.002 0.085 0.094 Banco Products 12 0.076 0.016 0.005 0.063 0.088 Elecon 12 0.079 0.021 0.006 0.062 0.095 Eimco Elecon 12 0.125 0.022 0.006 0.108 0.142 FAGBearing 12 0.143 0.024 0.007 0.124 0.162 GMM 12 0.137 0.031 0.009 0.113 0.161 Gujarat Apollo 8 0.087 0.014 0.005 0.072 0.101 HindustanDorr Oliver 12 0.121 0.059 0.017 0.074 0.167 Hitachi Home &Life 10 0.097 0.064 0.020 0.040 0.154 Ingersoll Rand 10 0.138 0.055 0.017 0.089 0.188 Jyoti 12 0.082 0.019 0.006 0.067 0.097 Jord Engg. 10 0.040 0.013 0.004 0.028 0.052 Kabra Extrusion 12 0.100 0.033 0.010 0.074 0.126 Kilburn Engg. 12 0.277 0.245 0.071 0.085 0.468 Mipco Seamless 12 0.037 0.015 0.004 0.025 0.049 Stovec Industries 11 0.126 0.015 0.005 0.113 0.139 Windsor Machines 12 0.107 0.044 0.013 0.072 0.142

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 0.600 20 0.030 7.365 0.000 1.619Within Groups 0.888 218 0.004 Total 1.488 238

Mean general expenses to sales ratio of Kilburn Engineering is highest

(27.70) among all the companies. Mipco Seamless has mean ratio of

3.70 which is least among all the companies. The ANOVA test is

applied to compare the mean general expenses to sales ratio for all the

companies. F value is 7.365 with the corresponding P value 0.000. As

P value is less than 0.01, it is concluded that this difference is

significant at less than 1 % level of significance.

Kilburn Engineering, FAG Bearings and Ingersoll Rand are having

very heavy administration, sales and general expenses in their cost

structure.

245

Ratio 10; Gross Profit Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.572 0.589 0.581 0.599 0.592 0.405 0.353 0.281 0.456 0.376 0.467 0.425 2 ABB 0.299 0.342 0.296 0.327 0.308 0.294 0.290 0.326 0.273 0.277 0.271 0.272 3 Batliboi 0.882 0.319 NA 0.181 0.185 0.161 0.224 0.205 0.252 NA 0.259 0.351 4 Bosch Re 0.424 0.432 0.420 0.446 0.392 0.173 0.315 0.399 0.237 0.318 0.274 0.476 5 Blue Star 0.214 0.193 0.196 0.213 0.209 0.224 0.216 0.210 0.221 0.234 0.208 0.218 6 Banco Products 0.515 0.208 0.092 0.133 0.049 0.112 0.159 0.158 0.150 0.196 0.122 0.143 7 Elecon 0.370 0.427 0.409 0.302 0.342 0.392 0.449 0.581 0.288 0.241 0.237 0.190 8 Eimco Elecon 0.410 0.439 0.434 0.523 0.510 0.430 0.409 0.431 0.406 0.414 0.363 0.400 9 FAGBearing 0.251 0.274 0.269 0.487 0.507 0.675 0.545 0.520 0.513 0.539 0.543 0.544

10 GMM 0.626 0.648 0.626 0.642 0.564 0.610 0.573 0.622 0.596 0.599 0.571 0.585 11 Gujarat Apollo NA 0.112 0.128 0.168 0.187 NA NA NA 0.116 0.087 0.079 0.094 12 HindustanDorr Oliver 0.276 0.312 0.314 0.276 0.289 0.194 0.180 0.270 0.211 0.217 0.366 0.272 13 Hitachi H & L 0.055 0.101 0.094 0.091 0.086 NA NA 0.043 NA 0.038 0.000 0.000 14 Ingersoll Rand NA 0.159 0.153 0.167 0.157 NA 0.364 0.392 0.392 0.371 0.028 NA 15 Jyoti 0.402 0.377 0.391 0.406 0.381 0.346 0.392 0.385 0.298 0.304 0.310 0.276 16 Jord Engg. NA 0.712 0.249 0.199 0.362 0.204 0.119 0.114 NA 0.053 0.068 0.000 17 Kabra Extrusion 0.424 0.374 0.347 0.344 0.376 0.263 0.341 0.201 0.222 0.272 0.279 0.367 18 Kilburn Engg. 0.461 0.542 0.509 0.461 0.609 0.536 0.481 0.357 0.369 0.366 0.302 0.361 19 Mipco Seamless 0.232 0.234 0.194 0.181 0.193 0.302 0.419 0.361 0.190 0.147 0.338 0.381 20 Stovec Industries 0.549 0.521 0.529 0.524 0.607 0.299 NA 0.261 0.399 0.360 0.329 0.419 21 Windsor Machines 0.293 0.327 0.322 0.302 0.308 0.260 0.400 0.456 0.355 0.444 0.394 0.201

246

Ratio 10 C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper BoundABC 12 0.475 0.110 0.032 0.389 0.561 ABB 12 0.298 0.024 0.007 0.279 0.316 Batliboi 10 0.302 0.213 0.067 0.112 0.492 Bosch Re 12 0.359 0.094 0.027 0.285 0.432 Blue Star 12 0.213 0.011 0.003 0.204 0.222 Banco Products 12 0.170 0.117 0.034 0.078 0.261 Elecon 12 0.352 0.109 0.031 0.267 0.438 Eimco Elecon 12 0.431 0.045 0.013 0.396 0.466 FAGBearing 12 0.472 0.134 0.039 0.368 0.577 GMM 12 0.605 0.028 0.008 0.583 0.627 Gujarat Apollo 8 0.121 0.039 0.014 0.080 0.163 HindustanDorr Oliver 12 0.265 0.055 0.016 0.222 0.308 Hitachi Home &Life 9 0.057 0.039 0.013 0.018 0.095 Ingersoll Rand 9 0.243 0.137 0.046 0.109 0.376 Jyoti 12 0.356 0.046 0.013 0.319 0.392 Jord Engg. 10 0.208 0.206 0.065 0.023 0.393 Kabra Extrusion 12 0.318 0.069 0.020 0.264 0.371 Kilburn Engg. 12 0.446 0.094 0.027 0.372 0.520 Mipco Seamless 12 0.264 0.091 0.026 0.193 0.336 Stovec Industries 11 0.436 0.116 0.035 0.340 0.532 Windsor Machines 12 0.338 0.075 0.022 0.280 0.397

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 3.670 20 0.184 17.993 0.000 1.619Within Groups 2.203 216 0.010

Mean gross profit ratio of GMM Pfaudler is highest (60.50) among all the companies. Hitachi Home and Life Solutions has mean ratio of 5.70 which is least among all the companies. The ANOVA test is applied to compare the mean gross profit ratio for all the companies. F value is 17.993 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

As per the data reflected by the financial statements, GMM Pfaudler, Antifriction Bearings and FAG Bearings are having highest gross profit earning capacity. Hitachi Home and Life solutions and Gujarat Apollo are having very low gross profit ratio, and hence heavy material consumption cost and labour cost.

During this period of study fro 1991 to 2002, it is observed that gross profit has gown down in case of all the companies, except Ingersoll Rand after 1996. This is on account of increasing material cost and other direct manufacturing costs. In case of Ingersoll Rand, gross profit ratio has gone up on account of better inventory management and control of direct manufacturing costs.

247

Ratio 11; Earning on Equity Capital Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 1.830 2.418 1.473 0.634 0.701 1.149 1.576 0.142 NA 0.194 0.316 NA 2 ABB 1.729 3.202 2.560 2.536 3.229 6.549 2.035 1.139 1.908 1.813 1.444 3.275 3 Batliboi 1.057 0.247 NA 0.000 0.748 0.255 NA NA 0.094 NA NA NA 4 Bosch Re 1.067 0.244 0.723 0.653 0.156 0.080 0.233 NA NA 0.460 1.349 1.432 5 Blue Star 1.324 0.590 0.637 0.934 2.199 1.308 0.820 0.630 0.668 0.929 1.257 1.415 6 Banco Products 5.740 2.373 0.455 0.436 0.423 1.633 2.864 2.852 3.086 2.479 1.311 1.550 7 Elecon 3.971 0.112 0.147 0.600 1.389 1.850 1.761 1.837 2.441 0.885 0.069 NA 8 Eimco Elecon 3.667 4.535 1.386 2.177 2.849 2.456 2.179 1.714 2.092 2.276 2.478 2.256 9 FAGBearing 1.499 0.509 0.086 0.171 0.631 1.061 1.302 0.870 0.274 0.486 1.109 1.528

10 GMM 2.346 3.138 3.667 5.667 4.698 7.434 5.258 2.453 1.672 1.354 1.000 0.554 11 Gujarat Apollo NA 0.268 0.604 0.734 0.950 NA NA NA 1.357 1.466 1.266 1.463 12 HindustanDorr Oliver 0.545 0.579 0.802 0.562 0.823 1.640 0.472 1.371 0.436 NA 0.796 0.781 13 Hitachi H & L 1.200 0.223 0.210 0.355 0.586 NA NA 0.328 NA 0.271 NA NA 14 Ingersoll Rand 1.436 1.962 1.126 1.250 1.181 1.322 1.643 2.262 2.503 2.407 2.282 NA 15 Jyoti 1.522 0.891 0.824 0.359 0.450 0.028 0.073 0.131 0.318 0.412 0.198 NA 16 Jord Engg. NA 0.076 0.221 0.321 0.648 0.827 0.375 0.246 NA NA NA NA 17 Kabra Extrusion 0.393 0.670 0.955 1.348 1.437 1.831 0.968 0.536 0.653 1.058 1.516 1.741 18 Kilburn Engg. 0.481 0.531 0.546 0.400 0.376 0.344 0.215 NA NA NA NA NA 19 Mipco Seamless 0.543 0.693 0.503 0.440 0.393 0.399 0.788 NA NA NA NA NA 20 Stovec Industries NA 0.395 1.176 1.679 3.397 0.177 NA NA NA 1.459 1.450 1.139 21 Windsor Machines 1.246 0.869 0.120 0.202 0.551 1.025 NA 0.209 NA NA NA NA

248

Ratio 11 C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper BoundABC 10 1.043 0.770 0.243 0.354 1.732 ABB 12 2.618 1.429 0.412 1.501 3.735 Batliboi 6 0.400 0.412 0.168 -0.183 0.983 Bosch Re 10 0.640 0.497 0.157 0.195 1.084 Blue Star 12 1.059 0.469 0.135 0.692 1.426 Banco Products 12 2.100 1.508 0.435 0.921 3.279 Elecon 11 1.369 1.188 0.358 0.380 2.359 Eimco Elecon 12 2.505 0.851 0.246 1.840 3.171 FAGBearing 12 0.794 0.507 0.146 0.397 1.191 GMM 12 3.270 2.122 0.613 1.611 4.929 Gujarat Apollo 8 1.013 0.446 0.158 0.534 1.493 HindustanDorr Oliver 11 0.801 0.380 0.115 0.484 1.117 Hitachi Home &Life 7 0.453 0.353 0.133 0.026 0.881 Ingersoll Rand 11 1.761 0.533 0.161 1.317 2.205 Jyoti 11 0.473 0.446 0.134 0.102 0.845 Jord Engg. 7 0.388 0.262 0.099 0.071 0.705 Kabra Extrusion 12 1.092 0.480 0.139 0.717 1.468 Kilburn Engg. 7 0.413 0.117 0.044 0.272 0.555 Mipco Seamless 7 0.537 0.151 0.057 0.354 0.721 Stovec Industries 8 1.359 0.977 0.345 0.310 2.408 Windsor Machines 7 0.603 0.450 0.170 0.058 1.148

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 143.851 20 7.193 8.694 0.000 1.628Within Groups 152.232 184 0.827 Total 296.082 204

Mean return on equity capital of GMM Pfaudler is highest (327)

among all the companies. Kilburn Engineering has mean ratio of

41.30 which is least among all the companies. The ANOVA test is

applied to compare the mean return on equity for all the companies. F

value is 8.694 with the corresponding P value 0.000. As P value is less

than 0.01, it is concluded that this difference is significant at less than

1 % level of significance.

249

GMM Pfaudler, ABB and Eimco Elecon are having very high EPS

ratio.

The comparison of profit before tax with equity capital has shown

erratic behaviour throughout the period of 1991 to 2002. However

this has been found in the year 1995 and 1996. After 1996, this

ratio has gone down till 2002.This was 743 percent in case of

GMM Pfaudler, which is the highest among all the companies

during the period of study. This is on account of higher margin

orders, monopolistic position and highest amount of sales turnover

of the concerned company during the period of study. This has

been reflected in the highest ever declaration of dividend of 115 %

for the Accounting year 1995-96 in case of GMM Pfaudler Ltd.

However, in case of this company, this ratio has gone down

drastically after 1996, on account of heavy fall in operations and

lower sales year after year, after 1996 till 2002. Only in case of one

company, Ingersoll Rand India Ltd. There was no down trend in

this ratio, i. e. profit before tax to equity capital, even after 1996.

On the contrary, this is increasing. This is even when after 1996,

the sales was down in the year 1999 and 2001. Otherwise also, this

company has very healthy working with professional management,

because of which with reference to different parameters, as

discussed earlier, the performance is found to be best among all

other companies covered by this study. This is praiseworthy, since

the results are showing better performance even during bad

economic and business environment.

250

Ratio 12; Salaries & Wages to Sales Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.010 0.010 0.010 0.010 0.010 0.094 0.087 0.153 0.175 0.160 0.148 0.160 2 ABB 0.111 0.105 0.085 0.092 0.086 0.078 0.095 0.125 0.135 0.128 0.108 0.102 3 Batliboi 0.068 0.066 NA 0.082 0.075 0.076 0.099 0.113 0.169 NA 0.270 0.266 4 Bosch Re 0.090 0.083 0.085 0.103 0.095 0.115 0.142 0.134 0.135 0.138 0.111 0.125 5 Blue Star 0.104 0.096 0.104 0.103 0.091 0.097 0.100 0.106 0.103 0.115 0.100 0.106 6 Banco Products 0.195 0.119 0.095 0.067 0.040 0.083 0.078 0.096 0.087 0.085 0.108 0.081 7 Elecon 0.082 0.113 0.098 0.075 0.090 0.100 0.098 0.113 0.104 0.149 0.104 0.103 8 Eimco Elecon 0.026 0.027 0.025 0.032 0.032 0.032 0.036 0.044 0.045 0.037 0.034 0.050 9 FAGBearing 0.127 0.108 0.111 0.105 0.130 0.135 0.099 0.106 0.102 0.122 0.119 0.114

10 GMM 0.216 0.230 0.113 0.098 0.176 0.161 0.164 0.150 0.165 0.172 0.151 0.160 11 Gujarat Apollo NA 0.018 0.015 0.020 0.019 NA NA NA 0.028 0.024 0.025 0.031 12 HindustanDorr Oliver 0.075 0.080 0.075 0.069 0.075 0.061 0.059 0.077 0.078 0.096 0.175 0.167 13 Hitachi H & L 0.014 0.018 0.022 0.018 0.020 0.040 0.040 0.061 0.071 0.064 0.067 0.073 14 Ingersoll Rand 0.090 0.077 0.074 0.092 0.103 0.093 0.100 0.102 NA 0.090 0.124 NA 15 Jyoti 0.218 0.208 0.209 0.230 0.242 0.248 0.185 0.194 0.168 0.153 0.147 0.244 16 Jord Engg. NA 0.030 0.018 0.015 0.015 0.016 0.013 0.013 NA 0.018 0.012 0.022 17 Kabra Extrusion 0.064 0.051 0.046 0.042 0.037 0.037 0.058 0.052 0.065 0.066 0.063 0.076 18 Kilburn Engg. 0.145 0.157 0.130 0.121 0.145 0.143 0.119 0.094 0.167 0.340 0.345 0.204 19 Mipco Seamless 0.040 0.046 0.049 0.060 0.060 0.090 0.095 0.157 0.208 0.133 0.144 0.121 20 Stovec Industries 0.097 0.125 0.119 0.122 0.135 0.132 0.150 0.140 0.121 0.097 0.090 0.098 21 Windsor Machines 0.074 0.075 0.107 0.111 0.093 0.121 0.155 0.139 0.194 0.168 0.151 0.174

251

Ratio 12

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 0.086 0.071 0.021 0.030 0.141 ABB 12 0.104 0.018 0.005 0.090 0.118 Batliboi 10 0.128 0.080 0.025 0.057 0.200 Bosch Re 12 0.113 0.022 0.006 0.096 0.130 Blue Star 12 0.102 0.006 0.002 0.097 0.107 Banco Products 12 0.095 0.037 0.011 0.065 0.124 Elecon 12 0.102 0.018 0.005 0.088 0.117 Eimco Elecon 12 0.035 0.008 0.002 0.029 0.041 FAGBearing 12 0.115 0.012 0.003 0.106 0.124 GMM 12 0.163 0.036 0.011 0.134 0.191 Gujarat Apollo 8 0.023 0.005 0.002 0.017 0.028 HindustanDorr Oliver 12 0.091 0.039 0.011 0.060 0.121 Hitachi Home &Life 12 0.042 0.023 0.007 0.024 0.061 Ingersoll Rand 10 0.095 0.014 0.004 0.082 0.107 Jyoti 12 0.204 0.035 0.010 0.177 0.231 Jord Engg. 10 0.017 0.005 0.002 0.012 0.022 Kabra Extrusion 12 0.055 0.012 0.004 0.045 0.065 Kilburn Engg. 12 0.176 0.082 0.024 0.111 0.240 Mipco Seamless 12 0.100 0.053 0.015 0.059 0.142 Stovec Industries 12 0.119 0.020 0.006 0.104 0.134 Windsor Machines 12 0.130 0.039 0.011 0.099 0.161

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 0.509 20 0.025 17.299 0.000 1.618Within Groups 0.325 221 0.001 Total 0.835 241

Mean salaries & wages to Sales ratio of Jyoti Ltd. is highest (20.40)

among all the companies. Eimco Elecon has mean ratio of 3.50 which is

least among all the companies (Jord Engineering ignored). The ANOVA

test is applied to compare the mean Salaries to Sales ratio for all the

companies. F value is 17.299 with the corresponding P value 0.000. As P

value is less than 0.01, it is concluded that this difference is significant at

less than 1 % level of significance.

252

Jyoti Ltd., Kilburn Engineering and GMM are having heavy load

of salaries and wages in their cost structure. This is very low in

case of Eimco Elecon, Hitachi H & L and Antifriction Bearing

Corporation.

By and large, all the companies were able to maintain salaries and

wages cost compared to sales income during the period of study.

This component of cost, in terms of its load on overall activity, has

been found to be constant. Only in case of three companies, HDO,

Kilburn Engineering and Windsor Machines, there is increasing

trend even when there is growth in sales year after year. The fact

that HDO and Kilburn Engineering are the companies engaged in

fabrication business, there is heavy involvement of labour force in

the manufacturing activities of these companies. In case of other

companies, this cost has been under control on account of benefit

of Voluntary Retirement Scheme availed by majority of the

companies.

The ratio of sales and General Administrative expenses has shown

that this block of expenses as a major expenses for engineering

companies. With the increase in activities, i.e., Sales, the

proportion of this type of expenses should come down. However,

in certain companies like Ingersoll Rand, Elecon and GMM

Pfaudler, these expenses proportion has gone up. This shows a link

of this type of expenses with their activities.

253

Ratio 13; Interest Coverage Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 1.176 1.057 0.557 0.498 0.632 0.786 0.826 0.077 NA 0.251 0.313 NA 2 ABB 0.925 1.226 3.368 2.982 5.700 8.991 5.917 3.871 6.078 6.539 5.342 16.469 3 Batliboi 0.435 0.065 NA -0.619 0.323 0.094 NA -0.002 0.028 NA NA NA 4 Bosch Re 0.658 0.122 0.362 0.237 0.143 NA 0.123 -0.517 NA 0.534 1.395 1.685 5 Blue Star 0.979 0.660 0.671 1.047 3.237 6.343 2.998 2.790 1.650 2.436 2.709 4.911 6 Banco Products 3.017 0.256 0.235 0.574 0.815 1.321 2.248 3.288 3.519 6.904 5.441 11.015 7 Elecon 0.042 0.059 0.057 0.137 0.850 1.262 1.200 1.373 1.019 0.553 0.047 NA 8 Eimco Elecon 0.887 0.617 0.572 2.611 4.686 5.051 3.202 3.809 4.309 4.339 3.563 5.714 9 FAGBearing 1.017 0.461 0.050 0.119 0.749 0.772 0.773 0.683 0.551 1.100 1.534 2.841

10 GMM 23.300 NA NA NA 20.200 10.044 2.876 1.890 0.956 1.484 2.360 2.055 11 Gujarat Apollo NA 5.288 5.483 16.688 24.438 16.938 1.138 6.981 1.202 NA 2.434 1.715 12 HindustanDorr Oliver 54.462 37.163 20.627 21.225 13.892 10.342 14.622 24.832 34.119 20.224 23.100 NA 13 Hitachi H & L 15.111 7.952 17.652 3.662 3.089 0.138 0.060 0.054 0.473 0.828 0.132 NA 14 Ingersoll Rand NA 0.055 0.222 1.147 2.247 2.158 0.848 1.187 NA NA NA NA 15 Jyoti 0.169 0.233 0.279 0.336 0.498 0.668 0.363 0.257 0.355 0.420 0.488 0.372 16 Jord Engg. NA 4.667 2.039 3.900 0.729 0.189 0.106 NA NA NA NA NA 17 Kabra Extrusion 6.037 5.593 3.333 4.375 11.800 4.613 4.214 NA NA NA NA NA 18 Kilburn Engg. 4.400 0.708 0.762 2.000 0.192 0.076 NA NA NA 0.263 0.272 0.123 19 Mipco Seamless 21.146 15.721 4.741 8.160 13.818 6.959 NA 1.328 NA NA NA NA 20 Stovec Industries 0.050 0.158 0.329 0.615 0.761 0.671 0.708 1.126 NA 2.399 NA NA 21 Windsor Machines NA 0.093 0.207 0.381 0.597 0.162 0.198 0.267 0.268 0.216 0.377 0.406

254

Ratio 13

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 10 0.617 0.352 0.111 0.302 0.932 ABB 12 5.617 4.120 1.189 2.396 8.839 Batliboi 7 0.047 0.336 0.127 -0.360 0.453 Bosch Re 10 0.474 0.646 0.204 -0.104 1.053 Blue Star 12 2.536 1.742 0.503 1.174 3.897 Banco Products 12 3.219 3.225 0.931 0.698 5.741 Elecon 11 0.600 0.553 0.167 0.139 1.060 Eimco Elecon 12 3.280 1.763 0.509 1.902 4.658 FAGBearing 12 0.888 0.737 0.213 0.312 1.463 GMM 9 7.241 8.694 2.898 -1.217 15.699 Gujarat Apollo 10 8.230 8.189 2.590 0.901 15.559 HindustanDorr Oliver 11 24.965 12.668 3.820 14.414 35.515 Hitachi Home &Life 11 4.468 6.383 1.925 -0.848 9.785 Ingersoll Rand 7 1.123 0.853 0.322 0.089 2.157 Jyoti 12 0.370 0.136 0.039 0.264 0.476 Jord Engg. 6 1.938 1.959 0.800 -0.833 4.709 Kabra Extrusion 7 5.709 2.831 1.070 2.278 9.140 Kilburn Engg. 9 0.977 1.416 0.472 -0.400 2.355 Mipco Seamless 7 10.268 6.911 2.612 1.892 18.643 Stovec Industries 9 0.757 0.699 0.233 0.078 1.437 Windsor Machines 11 0.289 0.142 0.043 0.171 0.406

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 6638.081 20 331.904 15.502 0.000 1.627Within Groups 3982.389 186 21.411 Total 10620.471 206

Mean interest coverage ratio of Hindustan Dorr Oliver is highest (249)

among all the companies. Batliboi has mean ratio of 4.70 which is

least among all the companies. The ANOVA test is applied to

compare the mean interest coverage ratio for all the companies. F

value is 15.502 with the corresponding P value 0.000. As p value is

less than 0.01, it is concluded that this difference is significant at less

than 1 % level of significance.

255

Hindustan Dorr Oliver, Mipco Seamless Rings and Gujarat Apollo

are having very healthy interest coverage ratio. This is very weak

in case of Batliboi, Windsor Machines and Elecon Engineering.

There has been marked mixed performance of different companies

about interest coverage ratio. Some of the companies interest

coverage has improved after 1991 till 2002. But this improvement

is marginal on account of heavy burden of interest cost. It was

highest in case of GMM Pfaudler in initial years (1991 to 1996)

since it was earning interest income on account of heavy liquidity

of funds. However, this company's interest coverage ratio gone

down by eleven times in 2002. This was on account of reduced

profitability and increasing interest cost. In a peculiar situation, the

interest coverage ratio of Ingersoll Rand has gown down after

1991.

256

Ratio 14; Retained Earning to PAT Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.660 0.609 0.913 0.615 0.441 0.323 0.740 0.137 NA 1.000 0.997 NA 2 ABB 0.722 0.822 0.798 0.786 0.801 0.840 0.649 0.396 0.120 0.526 0.648 0.740 3 Batliboi 0.809 0.386 NA -0.329 0.006 1.551 NA NA NA NA NA NA 4 Bosch Re 0.481 1.471 0.073 0.345 0.143 NA 0.986 NA NA 1.000 0.969 1.002 5 Blue Star 0.734 0.651 0.602 0.588 0.786 0.678 0.294 0.328 0.344 0.504 NA 0.087 6 Banco Products 0.959 0.367 0.500 0.487 0.400 2.134 0.895 0.800 0.792 0.429 0.591 0.251 7 Elecon 5.194 1.000 0.348 0.504 0.864 0.912 0.912 0.877 0.817 0.565 1.000 NA 8 Eimco Elecon 0.872 0.650 0.705 0.744 0.777 0.467 0.778 0.695 0.789 0.772 0.745 0.486 9 FAGBearing 0.755 0.778 0.000 0.297 0.695 0.609 0.910 0.678 1.008 2.102 0.075 0.690

10 GMM 0.622 0.602 0.617 0.645 0.547 0.731 0.674 0.347 0.063 0.076 0.458 0.717 11 Gujarat Apollo NA 0.145 0.255 0.449 0.409 0.253 2.742 0.656 2.037 NA NA NA 12 HindustanDorr Oliver 0.083 0.073 0.083 0.053 0.092 0.046 0.001 0.061 0.064 NA 0.024 NA 13 Hitachi H & L NA NA 0.062 0.201 0.321 3.854 NA 7.842 1.618 0.657 NA NA 14 Ingersoll Rand NA 58.474 15.471 3.549 1.887 1.626 3.408 6.980 NA NA NA NA 15 Jyoti 4.533 2.609 2.431 1.102 0.744 0.024 0.093 0.049 0.741 0.795 0.282 NA 16 Jord Engg. NA 0.102 0.144 1.308 1.818 3.014 4.303 NA NA NA NA NA 17 Kabra Extrusion 0.307 0.530 1.111 1.429 1.720 2.587 0.825 NA NA NA NA NA 18 Kilburn Engg. 0.336 0.652 0.463 0.467 1.881 1.541 NA NA NA NA NA NA 19 Mipco Seamless 0.146 0.157 0.352 0.294 0.120 0.060 NA NA NA NA NA NA 20 Stovec Industries 15.833 0.429 0.495 0.556 NA 0.007 NA NA NA 0.559 NA NA 21 Windsor Machines NA 8.407 NA NA 1.420 3.780 NA NA NA NA NA NA

257

Ratio 14

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 10 0.643 0.286 0.090 0.387 0.899 ABB 12 0.654 0.214 0.062 0.487 0.821 Batliboi 5 0.485 0.732 0.327 -0.795 1.764 Bosch Re 9 0.719 0.475 0.158 0.257 1.181 Blue Star 11 0.509 0.218 0.066 0.327 0.690 Banco Products 12 0.717 0.500 0.144 0.326 1.108 Elecon 11 1.181 1.348 0.406 0.058 2.304 Eimco Elecon 12 0.707 0.121 0.035 0.612 0.801 FAGBearing 12 0.717 0.536 0.155 0.297 1.136 GMM 12 0.508 0.231 0.067 0.328 0.689 Gujarat Apollo 8 0.868 0.970 0.343 -0.173 1.910 HindustanDorr Oliver 10 0.058 0.028 0.009 0.033 0.083 Hitachi Home &Life 7 2.079 2.866 1.083 -1.395 5.553 Ingersoll Rand 7 13.057 20.593 7.783 -11.901 38.014 Jyoti 11 1.218 1.414 0.426 0.041 2.396 Jord Engg. 6 1.782 1.649 0.673 -0.552 4.115 Kabra Extrusion 7 1.216 0.779 0.294 0.271 2.160 Kilburn Engg. 6 0.890 0.653 0.266 -0.034 1.813 Mipco Seamless 6 0.188 0.111 0.045 0.031 0.345 Stovec Industries 6 2.980 6.300 2.572 -5.933 11.893 Windsor Machines 3 4.536 3.554 2.052 -11.058 20.130

ANOVA Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 1087.483 20 54.374 3.044 0.000 1.636Within Groups 2893.874 162 17.863 Total 3981.357 182

Mean retained earnings ratio of Ingersoll Rand is highest (130.5) among all the companies. Hindustan Dorr Oliver has mean ratio of 5.80 which is least among all the companies. The ANOVA test is applied to compare the mean retained earnings ratio for all the companies. F value is 3.044 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Ingersoll Rand, Windsor Machines and Stovec Industries are having very healthy retained earnings ratio. This is very low for Hindustan Dorr Oliver, Mipco Seamless Rings and Batliboi Ltd.

The retained earnings to net profit ratio has shown down trend after 1996 in case of all the companies. The retained earnings have gone down evev in case of good companies like ABB and Blue Star. This is on account of reduced earnings after 1996.

258

Ratio 15; Net Fixed Assets to Net Worth Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 2.347 4.094 3.750 3.966 4.389 1.944 2.011 1.992 2.640 1.917 1.226 1.799 2 ABB 0.626 0.725 0.358 0.399 0.493 0.419 0.409 0.459 0.374 0.357 0.349 0.281 3 Batliboi 0.869 0.958 NA 1.654 1.508 1.358 2.005 2.090 2.090 NA 1.615 1.606 4 Bosch Re 1.128 1.263 0.875 1.172 1.161 0.870 1.089 0.998 1.074 0.787 0.722 0.604 5 Blue Star 0.744 0.722 0.666 0.485 0.555 0.416 0.666 0.831 0.833 0.745 0.734 0.536 6 Banco Products 0.423 0.482 0.414 0.534 0.614 0.584 0.532 2.290 0.456 0.389 0.338 0.370 7 Elecon 0.870 0.663 0.761 0.710 0.717 0.764 0.826 0.925 0.650 0.813 0.788 0.785 8 Eimco Elecon 0.617 0.474 0.214 0.270 0.274 0.332 0.345 0.290 0.247 0.290 0.274 0.357 9 FAGBearing 1.923 3.115 1.774 1.333 1.129 0.965 1.413 1.340 1.132 1.173 1.077 0.967

10 GMM 0.400 0.474 0.460 0.463 0.772 0.983 0.812 0.751 0.653 0.500 0.464 0.480 11 Gujarat Apollo NA 0.116 0.074 0.087 0.100 0.070 0.088 0.099 0.111 0.126 0.146 0.174 12 HindustanDorr Oliver 6.469 0.501 0.367 0.334 0.373 1.863 1.907 1.730 1.336 1.182 2.379 NA 13 Hitachi H & L 0.042 0.053 0.049 0.042 0.044 0.068 0.077 0.098 0.123 0.123 0.121 NA 14 Ingersoll Rand 0.550 1.100 0.908 1.111 1.237 1.511 1.954 2.017 2.063 1.835 1.643 NA 15 Jyoti NA 8.077 1.879 1.033 0.591 0.487 0.254 0.277 NA 0.420 NA NA 16 Jord Engg. 0.362 0.346 1.003 0.971 1.509 1.981 1.985 3.532 3.503 4.094 3.630 3.445 17 Kabra Extrusion 0.905 0.864 0.901 0.268 0.472 0.607 0.591 0.724 NA NA NA NA 18 Kilburn Engg. 0.669 0.704 0.838 2.513 2.917 2.696 1.317 2.571 5.103 11.756 NA NA 19 Mipco Seamless 0.519 0.481 0.386 0.285 0.805 0.905 1.133 1.549 1.485 1.457 1.091 0.761 20 Stovec Industries 0.457 0.261 0.299 0.375 0.553 0.494 0.437 0.309 0.431 0.519 0.534 3.320 21 Windsor Machines NA 5.346 4.658 3.217 2.771 3.276 3.149 2.782 2.388 1.967 1.647 1.461

259

Ratio 15

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 2.673 1.077 0.311 1.831 3.515 ABB 12 0.437 0.126 0.036 0.339 0.535 Batliboi 10 1.575 0.429 0.136 1.191 1.959 Bosch Re 12 0.979 0.205 0.059 0.819 1.139 Blue Star 12 0.661 0.135 0.039 0.556 0.767 Banco Products 12 0.619 0.533 0.154 0.202 1.036 Elecon 12 0.773 0.081 0.023 0.709 0.836 Eimco Elecon 12 0.332 0.112 0.032 0.244 0.419 FAGBearing 12 1.445 0.604 0.174 0.973 1.918 GMM 12 0.601 0.187 0.054 0.455 0.747 Gujarat Apollo 11 0.108 0.031 0.009 0.082 0.134 HindustanDorr Oliver 11 1.677 1.747 0.527 0.222 3.131 Hitachi Home &Life 11 0.076 0.034 0.010 0.048 0.105 Ingersoll Rand 11 1.448 0.503 0.152 1.029 1.867 Jyoti 8 1.627 2.661 0.941 -1.230 4.485 Jord Engg. 12 2.197 1.381 0.399 1.117 3.277 Kabra Extrusion 8 0.667 0.227 0.080 0.423 0.910 Kilburn Engg. 10 3.108 3.328 1.052 0.130 6.087 Mipco Seamless 12 0.905 0.443 0.128 0.559 1.251 Stovec Industries 12 0.666 0.841 0.243 0.008 1.324 Windsor Machines 11 2.969 1.189 0.358 1.979 3.959

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 179.956 20 8.998 7.680 0.000 1.620Within Groups 250.714 214 1.172 Total 430.670 234

Mean fixed assets to net worth ratio of Kilburn Engineering is highest

(310.80) among all companies. Hitachi Home and Life Solutions has mean ratio of 0.076 which is least among all the companies. The ANOVA test is applied to compare the mean fixed assets to net worth ratio for all the companies. F value is 7.680 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1% level of significance.

Majority of fixed assets are financed by shareholders’ funds in case of Gujarat Apollo, Eimco Elecon and ABB.

Financing of fixed assets through shareholders' funds is also studied covering the period of 1991 to 2002.lt has been observed in all the companies throughout this period, that fixed assets are fully financed through shareholders' funds, and balance amount of shareholders' funds has been invested in other current assets.

260

Ratio 16; Equity to Total Assets Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 0.136 0.135 0.124 0.129 0.126 0.261 0.263 0.269 0.208 0.256 0.339 0.246 2 ABB 0.263 0.211 0.413 0.377 0.352 0.446 0.498 0.538 0.503 0.507 0.477 0.457 3 Batliboi 0.251 0.199 NA 0.149 0.179 0.178 0.130 0.136 0.144 NA 0.245 0.230 4 Bosch Re 0.251 0.205 0.261 0.216 0.151 0.212 0.252 0.284 0.259 0.344 0.326 0.386 5 Blue Star 0.282 0.276 0.250 0.350 0.371 0.443 0.399 0.347 0.336 0.387 0.358 0.366 6 Banco Products 0.294 0.295 0.320 0.404 0.415 0.423 0.541 0.601 0.612 0.699 0.702 0.716 7 Elecon 0.265 0.276 0.223 0.229 0.230 0.321 0.341 0.344 0.417 0.433 0.413 0.356 8 Eimco Elecon 0.270 0.305 0.445 0.604 0.652 0.691 0.690 0.686 0.753 0.701 0.742 0.780 9 FAGBearing 0.261 0.171 0.310 0.376 0.411 0.477 0.312 0.284 0.391 0.380 0.406 0.441

10 GMM 0.428 0.434 0.417 0.460 0.394 0.404 0.338 0.358 0.394 0.612 0.641 0.649 11 Gujarat Apollo 0.495 0.515 0.599 0.600 0.515 0.715 0.829 0.841 0.756 0.933 0.793 0.892 12 HindustanDorr Oliver 0.037 0.222 0.302 0.312 0.281 0.481 0.351 0.352 0.365 0.318 0.141 NA 13 Hitachi H & L 0.518 0.526 0.549 0.565 0.543 0.524 0.591 0.679 0.770 0.874 0.727 NA 14 Ingersoll Rand 0.316 0.149 0.210 0.287 0.296 0.341 0.335 0.312 0.242 0.238 0.067 0.159 15 Jyoti NA 0.427 0.742 0.632 0.542 0.256 0.346 0.296 NA 0.211 NA NA 16 Jord Engg. 0.456 0.464 0.542 0.549 0.832 0.685 0.713 0.759 0.759 0.713 0.755 0.686 17 Kabra Extrusion 0.283 0.248 0.194 0.511 0.367 0.247 0.215 0.189 NA NA NA NA 18 Kilburn Engg. 0.541 0.642 0.717 0.600 0.327 0.313 0.373 0.342 0.183 0.063 NA NA 19 Mipco Seamless 0.347 0.319 0.236 0.478 0.303 0.300 0.280 0.279 0.350 0.296 0.353 0.399 20 Stovec Industries 0.312 0.387 0.384 0.364 0.424 0.356 0.318 0.308 0.212 0.169 0.151 0.029 21 Windsor Machines NA 0.341 0.334 0.264 0.515 0.516 0.436 0.411 0.428 0.432 0.405 0.371

261

Ratio 16

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 0.208 0.075 0.022 0.149 0.266 ABB 12 0.420 0.102 0.029 0.340 0.500 Batliboi 10 0.184 0.045 0.014 0.143 0.225 Bosch Re 12 0.262 0.065 0.019 0.211 0.313 Blue Star 12 0.347 0.055 0.016 0.304 0.390 Banco Products 12 0.502 0.162 0.047 0.375 0.629 Elecon 12 0.321 0.076 0.022 0.261 0.380 Eimco Elecon 12 0.610 0.174 0.050 0.474 0.746 FAGBearing 12 0.352 0.086 0.025 0.284 0.419 GMM 12 0.461 0.110 0.032 0.375 0.547 Gujarat Apollo 12 0.707 0.157 0.045 0.584 0.829 HindustanDorr Oliver 11 0.287 0.119 0.036 0.188 0.387 Hitachi Home &Life 11 0.624 0.120 0.036 0.524 0.724 Ingersoll Rand 12 0.246 0.086 0.025 0.179 0.313 Jyoti 8 0.431 0.191 0.067 0.227 0.636 Jord Engg. 12 0.659 0.125 0.036 0.562 0.757 Kabra Extrusion 8 0.282 0.109 0.038 0.165 0.399 Kilburn Engg. 10 0.410 0.210 0.066 0.222 0.598 Mipco Seamless 12 0.328 0.064 0.018 0.278 0.378 Stovec Industries 12 0.285 0.119 0.034 0.192 0.377 Windsor Machines 11 0.405 0.076 0.023 0.342 0.468

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 5.235 20 0.262 19.006 0.000 1.619Within Groups 2.975 216 0.014 Total 8.210 236

Mean proprietary ratio of Jord Engineering is highest (65.90) among all the companies. Batliboi has mean ratio of 18.40 which is least among all the companies. The ANOVA test is applied to compare the mean proprietary ratio for all the companies. F value is 19.006 with the corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Gujarat Apollo, Jord Engineering and Hitachi H & L have very healthy proprietory ratio. This is found to be very weak in case of Batliboi, Antifriction Bearing Corp. and Kabra Extrusion.

The proprietary ratio has very moderately increased during 1991 to 2002 for all the companies. This shows much dependant on debt. Only in case of Ingersoll Rand, it has gone down in 2002 compared to 1991.

262

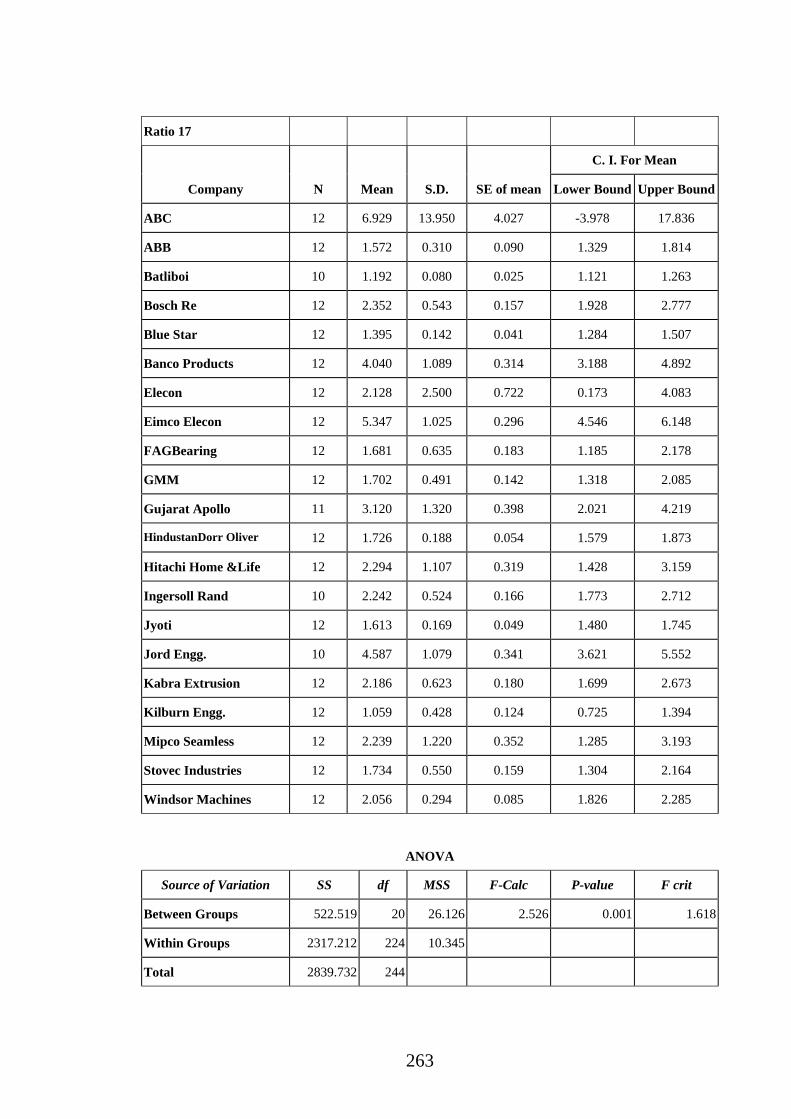

Ratio 17; Current Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 2.748 51.211 3.665 2.618 2.808 2.425 2.387 3.230 2.760 2.850 3.092 3.351 2 ABB 1.354 1.191 1.506 1.377 1.265 1.445 2.377 1.620 1.774 1.692 1.640 1.622 3 Batliboi 1.142 1.158 NA 1.148 1.034 1.305 1.221 1.248 1.291 NA 1.178 1.194 4 Bosch Re 2.149 1.551 2.081 2.040 1.889 2.301 3.605 2.998 2.455 2.401 2.085 2.673 5 Blue Star 1.214 1.237 1.294 1.422 1.378 1.517 1.385 1.247 1.659 1.592 1.461 1.338 6 Banco Products 6.977 3.394 3.431 3.598 2.629 3.974 4.339 4.259 4.813 4.072 3.746 3.248 7 Elecon 1.332 1.290 1.258 1.239 1.382 0.013 1.386 1.142 1.980 2.412 9.823 2.275 8 Eimco Elecon 3.605 4.121 5.491 5.215 4.175 5.600 5.183 5.947 5.679 6.247 5.502 7.398 9 FAGBearing 0.706 0.975 1.699 1.872 1.622 1.541 1.066 1.217 2.881 2.439 2.094 2.063

10 GMM 1.319 1.345 1.458 1.558 1.320 1.611 1.118 1.749 1.606 2.462 2.698 2.173 11 Gujarat Apollo NA 3.092 2.866 6.822 2.998 3.720 2.812 2.604 2.614 1.946 2.034 2.817 12 HindustanDorr Oliver 1.619 1.942 1.664 1.943 2.000 1.515 1.545 1.583 1.622 1.980 1.545 1.753 13 Hitachi H & L 4.696 2.417 4.166 2.493 2.495 2.233 1.847 1.684 1.594 1.433 1.370 1.094 14 Ingersoll Rand 2.093 1.951 2.106 1.974 1.869 1.745 1.911 2.481 NA 2.930 3.361 NA 15 Jyoti 1.195 1.848 1.585 1.736 1.727 1.597 1.492 1.779 1.543 1.602 1.558 1.691 16 Jord Engg. NA 3.417 3.941 5.685 5.250 3.950 4.604 4.824 NA 5.538 5.994 2.663 17 Kabra Extrusion 1.428 1.689 1.441 1.561 1.806 1.862 3.190 2.814 2.828 2.447 2.742 2.422 18 Kilburn Engg. 1.222 1.128 1.239 1.000 1.422 1.457 1.232 1.388 1.459 0.442 0.304 0.421 19 Mipco Seamless 3.820 4.121 4.039 2.413 3.014 1.208 1.829 1.448 0.929 0.926 1.215 1.900 20 Stovec Industries 2.061 2.325 2.168 0.246 2.061 2.030 2.077 1.558 1.494 1.589 1.536 1.659 21 Windsor Machines 1.859 1.976 2.190 2.015 2.070 2.519 2.477 2.393 1.982 1.847 1.800 1.541

263

Ratio 17

C. I. For Mean

Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 12 6.929 13.950 4.027 -3.978 17.836

ABB 12 1.572 0.310 0.090 1.329 1.814

Batliboi 10 1.192 0.080 0.025 1.121 1.263

Bosch Re 12 2.352 0.543 0.157 1.928 2.777

Blue Star 12 1.395 0.142 0.041 1.284 1.507

Banco Products 12 4.040 1.089 0.314 3.188 4.892

Elecon 12 2.128 2.500 0.722 0.173 4.083

Eimco Elecon 12 5.347 1.025 0.296 4.546 6.148

FAGBearing 12 1.681 0.635 0.183 1.185 2.178

GMM 12 1.702 0.491 0.142 1.318 2.085

Gujarat Apollo 11 3.120 1.320 0.398 2.021 4.219

HindustanDorr Oliver 12 1.726 0.188 0.054 1.579 1.873

Hitachi Home &Life 12 2.294 1.107 0.319 1.428 3.159

Ingersoll Rand 10 2.242 0.524 0.166 1.773 2.712

Jyoti 12 1.613 0.169 0.049 1.480 1.745

Jord Engg. 10 4.587 1.079 0.341 3.621 5.552

Kabra Extrusion 12 2.186 0.623 0.180 1.699 2.673

Kilburn Engg. 12 1.059 0.428 0.124 0.725 1.394

Mipco Seamless 12 2.239 1.220 0.352 1.285 3.193

Stovec Industries 12 1.734 0.550 0.159 1.304 2.164

Windsor Machines 12 2.056 0.294 0.085 1.826 2.285

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit

Between Groups 522.519 20 26.126 2.526 0.001 1.618

Within Groups 2317.212 224 10.345

Total 2839.732 244

264

Mean current ratio of Antifriction Bearing Corp. is highest (6.92)

among all the companies. Kilburn Engineering has mean ratio of

1.059 which is least among all the companies. The ANOVA test is

applied to compare the mean current ratio for all the companies. F

value is 2.526 with corresponding P value 0.001. As P value is less

than 0.01, it is concluded that this difference is significant at less

than 1% level of significance.

It is found that Antifriction Bearing Corp., Eimco Elecon and Jord

Engineering were having very healthy current ratio. This was weak

in case of Batliboi, Kilburn Engineering and Blue Star.

Study of current assets and current liabilities during this period has

shown that there is no much improvement in the current ratio

within twelve years' period of 1991 to 2002. Twelve years period is

a very long period, even then there is no improvement. This shows

(a) that the majority of period was a disturbing period for the

manufacturing industries all over the world, and particularly in

India, and (b) the components of current assets and current

liabilities are, to some extent, not controllable by the management

of the business enterprise. In the ultimate analysis, the current ratio

has not become healthy after 1991 in case of all the companies

covered by the study.

265

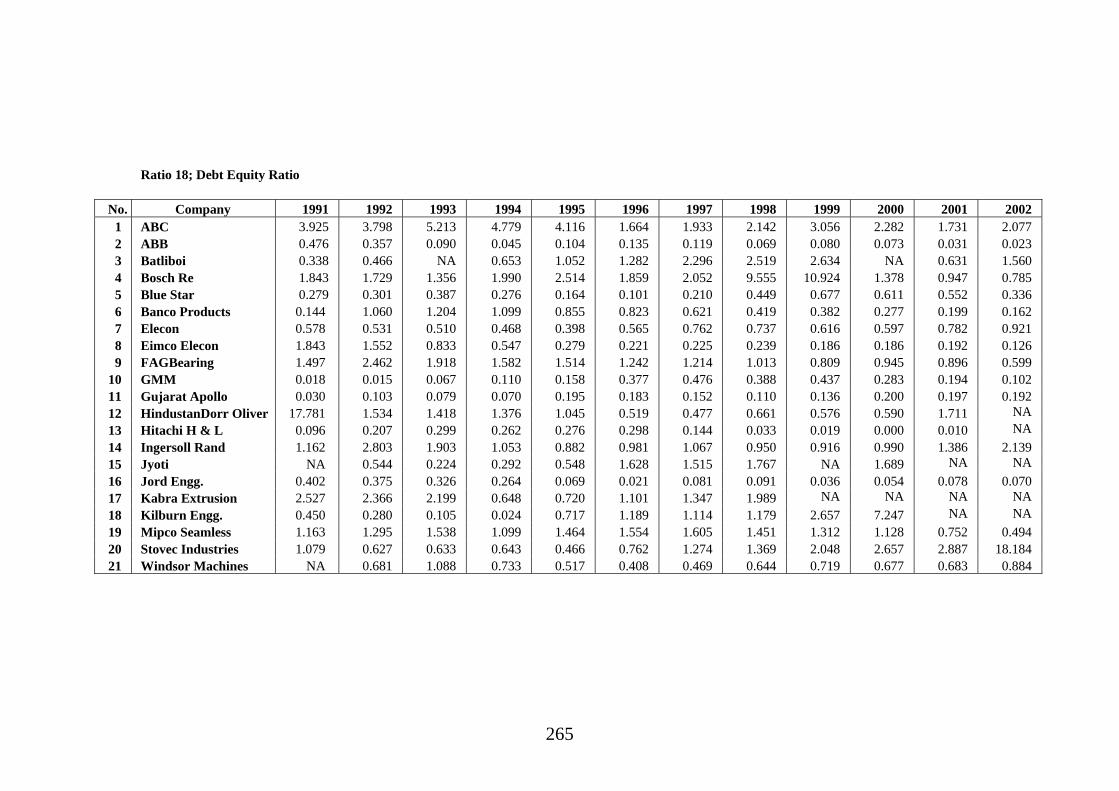

Ratio 18; Debt Equity Ratio

No. Company 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 1 ABC 3.925 3.798 5.213 4.779 4.116 1.664 1.933 2.142 3.056 2.282 1.731 2.077 2 ABB 0.476 0.357 0.090 0.045 0.104 0.135 0.119 0.069 0.080 0.073 0.031 0.023 3 Batliboi 0.338 0.466 NA 0.653 1.052 1.282 2.296 2.519 2.634 NA 0.631 1.560 4 Bosch Re 1.843 1.729 1.356 1.990 2.514 1.859 2.052 9.555 10.924 1.378 0.947 0.785 5 Blue Star 0.279 0.301 0.387 0.276 0.164 0.101 0.210 0.449 0.677 0.611 0.552 0.336 6 Banco Products 0.144 1.060 1.204 1.099 0.855 0.823 0.621 0.419 0.382 0.277 0.199 0.162 7 Elecon 0.578 0.531 0.510 0.468 0.398 0.565 0.762 0.737 0.616 0.597 0.782 0.921 8 Eimco Elecon 1.843 1.552 0.833 0.547 0.279 0.221 0.225 0.239 0.186 0.186 0.192 0.126 9 FAGBearing 1.497 2.462 1.918 1.582 1.514 1.242 1.214 1.013 0.809 0.945 0.896 0.599

10 GMM 0.018 0.015 0.067 0.110 0.158 0.377 0.476 0.388 0.437 0.283 0.194 0.102 11 Gujarat Apollo 0.030 0.103 0.079 0.070 0.195 0.183 0.152 0.110 0.136 0.200 0.197 0.192 12 HindustanDorr Oliver 17.781 1.534 1.418 1.376 1.045 0.519 0.477 0.661 0.576 0.590 1.711 NA 13 Hitachi H & L 0.096 0.207 0.299 0.262 0.276 0.298 0.144 0.033 0.019 0.000 0.010 NA 14 Ingersoll Rand 1.162 2.803 1.903 1.053 0.882 0.981 1.067 0.950 0.916 0.990 1.386 2.139 15 Jyoti NA 0.544 0.224 0.292 0.548 1.628 1.515 1.767 NA 1.689 NA NA 16 Jord Engg. 0.402 0.375 0.326 0.264 0.069 0.021 0.081 0.091 0.036 0.054 0.078 0.070 17 Kabra Extrusion 2.527 2.366 2.199 0.648 0.720 1.101 1.347 1.989 NA NA NA NA 18 Kilburn Engg. 0.450 0.280 0.105 0.024 0.717 1.189 1.114 1.179 2.657 7.247 NA NA 19 Mipco Seamless 1.163 1.295 1.538 1.099 1.464 1.554 1.605 1.451 1.312 1.128 0.752 0.494 20 Stovec Industries 1.079 0.627 0.633 0.643 0.466 0.762 1.274 1.369 2.048 2.657 2.887 18.184 21 Windsor Machines NA 0.681 1.088 0.733 0.517 0.408 0.469 0.644 0.719 0.677 0.683 0.884

266

Ratio 18

C. I. For Mean Company N Mean S.D. SE of mean Lower Bound Upper Bound

ABC 11 2.981 1.288 0.388 1.908 4.053 ABB 11 0.102 0.092 0.028 0.026 0.179 Batliboi 9 1.455 0.847 0.282 0.631 2.278 Bosch Re 11 3.190 3.534 1.066 0.247 6.133 Blue Star 11 0.369 0.186 0.056 0.214 0.524 Banco Products 11 0.646 0.381 0.115 0.328 0.963 Elecon 11 0.626 0.157 0.047 0.495 0.757 Eimco Elecon 11 0.417 0.430 0.130 0.059 0.775 FAGBearing 11 1.290 0.545 0.164 0.836 1.744 GMM 11 0.237 0.162 0.049 0.102 0.372 Gujarat Apollo 11 0.147 0.050 0.015 0.105 0.188 HindustanDorr Oliver 10 0.991 0.480 0.152 0.561 1.421 Hitachi Home &Life 10 0.155 0.128 0.041 0.040 0.270 Ingersoll Rand 11 1.370 0.636 0.192 0.841 1.899 Jyoti 8 1.026 0.680 0.240 0.296 1.756 Jord Engg. 11 0.133 0.125 0.038 0.029 0.237 Kabra Extrusion 7 1.481 0.706 0.267 0.625 2.337 Kilburn Engg. 9 1.612 2.259 0.753 -0.585 3.810 Mipco Seamless 11 1.245 0.353 0.107 0.950 1.539 Stovec Industries 11 2.868 5.150 1.553 -1.421 7.158 Windsor Machines 11 0.682 0.190 0.057 0.524 0.840

ANOVA

Source of Variation SS df MSS F-Calc P-value F crit Between Groups 193.440 20 9.672 4.013 0.000 1.624Within Groups 474.771 197 2.410 Total 668.210 217

Mean debt equity ratio of Bosch Rexroth is highest (3.190) among all

the companies. ABB has mean ratio of 0.102 which is least among all the companies. The ANOVA test is applied to compare the mean debt equity ratio for all the companies. F value is 4.013 with corresponding P value 0.000. As P value is less than 0.01, it is concluded that this difference is significant at less than 1 % level of significance.

Bosch Rexroth, Antifriction Bearing Corporation and Stovec Industries were having very high debt equity ratio, which is not a healthy phenomena. The companies having comfortable debt equity ratio are Jord Engineering, Gujarat Apollo and Hitachi H & L.

During the period of study, the reliance on debt has gone down in all cases. This has gone up after 1996 only in case of Elecon Engineering, Ingersoll Rand and Stovec Industries, which have used debt finance for requirement for their increased activities.

267

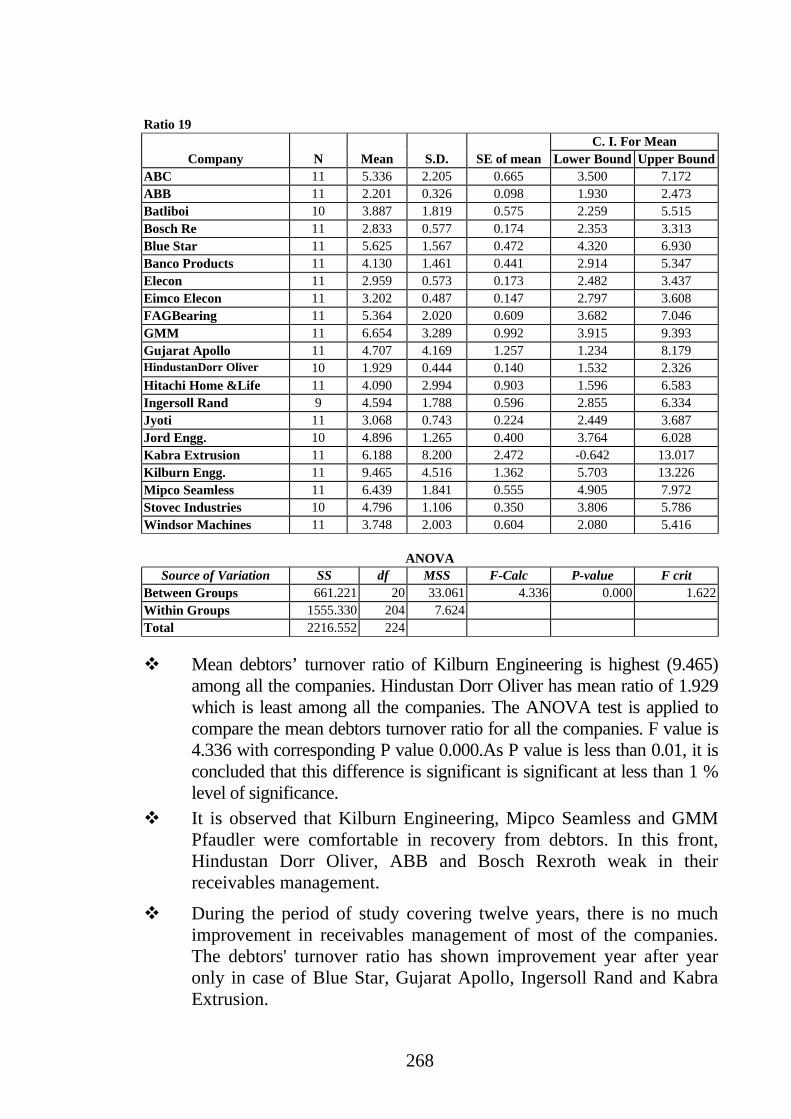

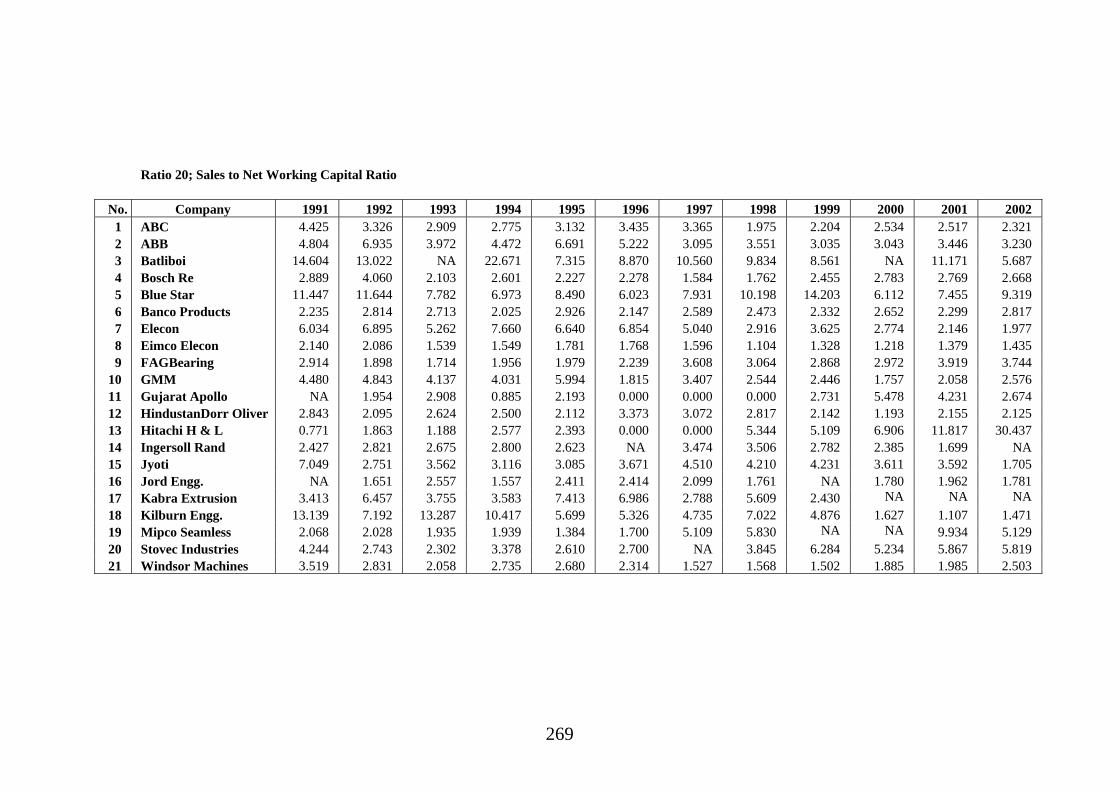

Ratio 19; Debtors Turnover Ratio