a world leading natural rubber player -...

TRANSCRIPT

Do not refresh this file

Opportunity Day Presentation 20 May 2013

A World Leading Natural Rubber Player

Do not refresh this file

2

Do not refresh this file

2

Disclaimer

Certain forward looking statements may be made in the course of the presentation. These forward-

looking statements generally can be identified by use of statements that include words or phrases

such as STA or We or our management “believe”, “expect”, “anticipate”, ”intend”, ”plan”, ”foresee”,

”project”, ”may”, “will”, “shall”, or other similar words or phrases. Similarly, statements that describe

STA’s objectives, plans or goals also are forward-looking statements. These statements involve

known and unknown uncertainties and risks that could differ materially from actual results,

performance or events.

The forward-looking statements contained in the slides are not and should not be constructed as

representations of the future performance of STA and that such statements are an expression of the

Company’s reviews based on its current view and certain assumptions including, but not limited to,

prevailing economic and market conditions and currently available information. The reader or the

listener is cautioned to not unduly rely on these forward-looking statements. We do not undertake

any duty to publish any update or revision of any forward-looking statements.

628363-027

Do not refresh this file

3

Do not refresh this file

3

Our Executive Directors

Dr. Viyavood Sincharoenkul

Chairman & Managing Director

Kitichai Sincharoenkul

Executive Director

Paul Sumade Lee

Executive Director

Founding member of Sri Trang and

appointed as Chairman in 2010

26 years of experience in the natural

rubber industry

Joined Sri Trang in 1988 and has

served as a Director since 1995

23 years of experience in the natural

rubber industry

Joined Sri Trang in 2004 and

appointed as a Director in 2010

8 years of experience in the natural

rubber industry

628363-027

Chaiyos Sincharoenkul

Executive Director

Prasit Panidkul

Executive Director

A Director since our inception

43 yrs of experience in natural rubber

industry

A Director since our inception

26 yrs of experience in natural rubber

industry

628363-027

I. Sri Trang Business Highlights

II. Natural Rubber Industry Snapshot

III. Financial Highlights

IV. Growth Strategy

AGENDA

Do not refresh this file

5

Do not refresh this file

5

9% world market

share contributed

by STA

Fully Integrated and Globally Natural Rubber Supply Chain

Upstream Midstream

Finished Products Plantation Procurement Processing

628363-027

31% of natural

rubber production

come from Thailand

Sales & Distribution

RSS

TSR

Con. Latex

Unsmoked

sheets

Fresh

Latex

Cup Lump

Hydraulic Hoses

Examination gloves

Downstream

Thailand is the

world largest

natural rubber

supplier

Thailand and Indonesia control more

than half of world supply

China is world largest

natural rubber

consuming country

Produced from

Thailand and

distributed worldwide

57% of world

supply come from

Thailand and

Indonesia

13% market share

of China import

contributed by STA

4th ranked of

world largest glove

manufacturing

Escalator Handrail

Do not refresh this file

6

Do not refresh this file

6

(By tonnage) (‘000 tons)

(By tonnage)

Sri Trang9%

Rest of the world91%

Sri Trang 18%

Rest of Thailand

82%

795

913

932

955

976

3,015

3,522

0 2000 4000

PRC (#6)

India (#5)

Malaysia (#4)

Vietnam (#3)

Sri Trang

Indonesia (#2)

Thailand (#1)

Sri Trang 13%

Others 87%

Sri Trang - Dominant Natural Rubber Processors

Global NR market share Sri Trang vs. leading natural rubber producing

countries

Thailand NR production share China NR imports 2012

(By tonnage)

Do not refresh this file

7

Do not refresh this file

7

World Largest Midstream Natural Rubber Producer

628363-027

Concentrated

Latex

Ribbed Smoked

Sheet (RSS)

Technically

Specified Rubber (TSR)

Existing plants

Plants under construction

23 factories, 21 in

Thailand and 2 in Indonesia

1.2 million tons per annum for production capacity

61 procurement units, 40 in Thailand and 21 in Indonesia

Do not refresh this file

8

Do not refresh this file

8

Our Midstream Business Strategy

628363-027

TSR RSS Con. Latex

Full range of natural rubber products

• Serve all downstream businesses & capture all

possible market segments

• Create production efficiency

• Excellent diversification

• More than sufficient raw material to secure from

world largest Natural Rubber producing

countries

• Well-balanced seasonal management

Thailand Indonesia

Strategic Production base

Type of

Product

No. of plant Total production

capacity

TSR 12 828,850

RSS 5 206,392

LTX 6 191,488

Total 23 1,226,730

Do not refresh this file

9

Do not refresh this file

9

Thailand as our focus for upstream

Strategic Expansion to Upstream Business

> 4,700 hectare rubber plantation in Thailand

> 60% with an

average gestation period of 2 years

Will mature for first commercial tapping from

2016 Tapping

Under gestation

Land development

Chiang Mai Chiang Rai

Lampang

Utaradit Sukhothai

Pitsanulok Pichit Sakon Nakhorn

Surat Thani

Krabi Songkhla

Petchaboon

Sakaeo

Prae

Chumporn

Do not refresh this file

10

Do not refresh this file

10

Income Diversification through Investment in Downstream Business

Latex / nitrile examination gloves for medical and industrial purposes

Operated through 40.2% owned associate SSC

World top four and Thailand largest glove manufacturer

Production capacity of 14 billion pieces per annum

Operated through 42.5%-owned associate in Thailand and 50%-owned associate in PRC

Largest hydraulic hoses producer in Thailand

Production capacity of 42.5 million meter per annum

10%-owned entity in PRC

Production capacity of 1.4 million meter per annum

Examination Gloves High-pressure

hydraulic hoses Escalator handrails

Do not refresh this file

11

Do not refresh this file

11

Plantation

Procurement

Processing

Finished products

Sale & Distributio

n

Gain direct access to supply

information

Ability to control the quality of

supply

Reduce purchasing volumes to

transact with intermediaries

Minimise operating cost

Ability to control the quality of

supply

First-hand

understanding of

customer

requirements

Quick access to

reliable market

information

Be flexible to any market

conditions and able to manage

production and position

efficiently

Distinctive Advantage - Capture Value throughout the Supply Chain

628363-027

I. Sri Trang Business Highlights

II. Natural Rubber Industry Snapshot

III. Financial Highlights

IV. Growth Strategy

AGENDA

Do not refresh this file

13

Do not refresh this file

13

Natural Rubber Industry Supply Chain

NR supply by type of plantation

Estates 22%

Small Holdings

78%

Source: IRSG,

NR demand by end use

Latex

13%

Other

uses

17%

Tyre

70%

Replacement market

70%

Original equipped market 30%

Market Segmentation

Do not refresh this file

14

Do not refresh this file

14

World Major NR Producing and Consuming Countries

628363-027

7.6 7.9

8.7 9.2

9.7 10.2 10.2

9.3

10.8 11.0

10.9 11.6

7.3 8.0

8.7 8.9 9.8 9.9

10.1 9.7 10.4

11.0 11.4 11.8

(0.25) 0.07 0.03 (0.30) 0.14 (0.29) (0.05) 0.36 (0.38) 0.05 0.46 0.18

(2.0)

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2002 2004 2006 2008 2010 2012

Demand Supply Supply surplus/(deficit)

Indonesia 26%

Thailand 31%

China 7%

Malaysia 8%

Vietnam 8%

India 8%

Others 12%

China 34%

North America

10% Europe

10%

India 9%

Japan 7%

Thailand 5%

Others 25%

Unit : million tons

(by tonnage) (by tonnage)

25%

35%

45%

55%

65%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Advanced¹ Emerging

Overall NR demand and supply Demand trend moves to emerging market

Source: IRSG and LMC 1 Advanced markets include USA, Canada, Western Europe and East Asia

Major suppliers of Natural Rubber Major consumers of Natural Rubber

Do not refresh this file

15

Do not refresh this file

15

Supply Limited in Equator Countries

628363-027

1,274

795

913

932

955

3,015

3,522

Others

China

India

Malaysia

Vietnam

Indonesia

Thailand

0 1,000 2,000 3,000 4,000

2,814

2,000

640 607 506 504 55 101

670

785

434 470 405 255

225 27

3,484

2,785

1,074 1,077 911 759

280 128

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000 Immature area (Hectares)

Tapped area (Hectares)

Yield per hectare (Kg.)

Unit : ‘000 tons

0

1,000

2,000

3,000

4,000

5,000

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Malaysia Indonesia Thailand India

PRC Vietnam Other

Unit : ‘000 tons

Rubber tree grows well in tropical area Thailand - the world largest NR supplier

Area for rubber plantation Global natural rubber production by country

Do not refresh this file

16

Do not refresh this file

16

-15%

-10%

-5%

0%

5%

10%

15%USA

EU

Brazil

China

Japan

IndonesiaRussia

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

-1%

0%

1%

2%

3%

4%

5%

6% GDP (LHS) NR consumption (RHS)

0%

2%

4%

6%

8%

0

500

1,000

1,500

PC LCV

M/HCV PC (% growth)

LCV (% growth) M/HCV (% growth)

2,789

502

740

1,001

1,058

1,092

3,765

Others

Thailand

Japan

India

Europe

America

China

0 1,000 2,000 3,000 4,000

China – world largest NR consumer

Forecasted growth of NR demand by country

NR Demand mainly driven by world activities

Global vehicle growth trend (Million units)

Demand Driven by Tyre Industry

Unit : ‘000 tons

Do not refresh this file

17

Do not refresh this file

17

Consistent Demand for Natural Rubber

Source: IRSG

20

30

40

50

60

Jan

-07

Ap

r-0

7Jul-

07

Oct-

07

Jan

-08

Ap

r-0

8Jul-

08

Oct-

08

Jan

-09

Ap

r-0

9Jul-

09

Oct-

09

Jan

-10

Apr-

10

Jul-

10

Oct-

10

Jan

-11

Ap

r-1

1Jul-

11

Oct-

11

Jan

-12

Ap

r-1

2Jul-

12

Oct-

12

Share of natural rubber in rubber consumption (%)

39-49%

Synthetic Rubber

Natural Rubber

Heat

resistance Elasticity

Resilient demand for natural rubber

-100%

-50%

0%

50%

100%

150%

200%Brent Crude oil Butadiene-Rubber Natural Rubber

Price movement

• Natural rubber and synthetic rubber are substitute and

complimentary products

• The substitution between synthetic rubber and natural

rubber is limited (less than 10%)

Do not refresh this file

18

Do not refresh this file

18

Natural Rubber Price Interaction

628363-027

(400)

(200)

0

200

400

0

2,000

4,000

6,000

Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Jul-09

Oct-

09

Ja

n-1

0

Apr-

10

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Supply surplus / (deficit) (RHS) SICOM price (TSR20) (LHS)

0

1,000

2,000

3,000

0

2,000

4,000

6,000

Ja

n-0

7

Ap

r-0

7

Ju

l-0

7

Oct-

07

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Jul-09

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

Oct-

11

Ja

n-1

2

Apr-

12

Ju

l-1

2

Oct-

12

Total stock (RHS) SICOM price (TSR20) (LHS)

(US

D p

er

ton

s)

NR price VS. fundamental demand/supply

(Un

it : ‘00

0 to

ns)

NR price VS. global stock

(US

D p

er

ton

s) (U

nit : ‘0

00

ton

s)

628363-027

I. Sri Trang Business Highlights

II. Natural Rubber Industry Snapshot

III. Financial Highlights

IV. Growth Strategy

AGENDA

Do not refresh this file

20

Do not refresh this file

20

628363-027

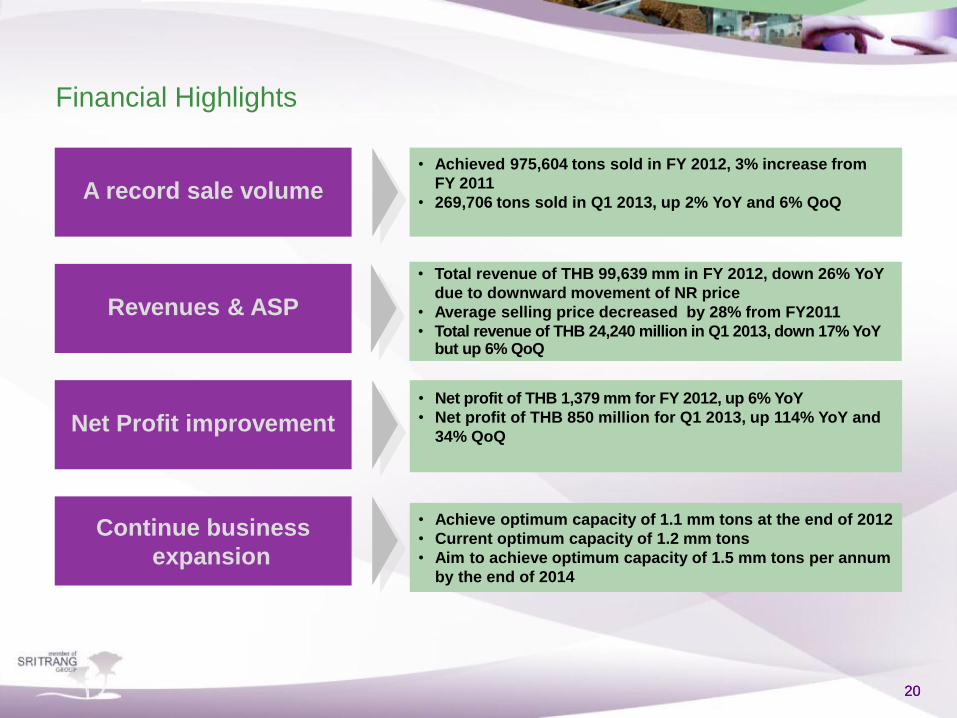

Financial Highlights

A record sale volume

Revenues & ASP

Net Profit improvement

Continue business

expansion

• Achieved 975,604 tons sold in FY 2012, 3% increase from

FY 2011

• 269,706 tons sold in Q1 2013, up 2% YoY and 6% QoQ

• Total revenue of THB 99,639 mm in FY 2012, down 26% YoY

due to downward movement of NR price

• Average selling price decreased by 28% from FY2011

• Total revenue of THB 24,240 million in Q1 2013, down 17% YoY but up 6% QoQ

• Net profit of THB 1,379 mm for FY 2012, up 6% YoY

• Net profit of THB 850 million for Q1 2013, up 114% YoY and

34% QoQ

• Achieve optimum capacity of 1.1 mm tons at the end of 2012

• Current optimum capacity of 1.2 mm tons

• Aim to achieve optimum capacity of 1.5 mm tons per annum

by the end of 2014

Do not refresh this file

21

Do not refresh this file

21

Revenue Breakdown by Product

Yearly (THB mm) Quarterly (THB mm)

628363-027

-17.2% +6.3%

-25.5%

13,591

77,500

6,436

2,386

2,112

24,943

96,139

10,236

133,704

99,639

FY 2011 FY 2012

RSS TSR Con. Latex Others

2,750

18,070

1,4621,568

517598 512

3,6672,6003,3314,909

21,940

19,23618,254

18,299

1,5081,534

1,932

706

485

29,266

24,61822,960

24,24022,794

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

RSS TSR Con. Latex Others

Do not refresh this file

22

Do not refresh this file

22

Revenue Breakdown by Geography

Yearly (THB mm) Quarterly (THB mm)

628363-027

-17.2% +6.3%

-25.5%

10,720 9,057 9,809 11,851 12,355

12,309 10,999 9,033

7,865 8,396

3,882

2,636 2,337 1,744

2,020

2,222

1,781

1,699 1,282 1,370

133

145

82 53 99

29,266

24,618 22,960 22,794

24,240

Q1 2012 Q2 2012 Q3 3012 Q4 2012 Q1 2013

PRC ASIA (Ex. PRC) USA Europe Others

Do not refresh this file

23

Do not refresh this file

23

Adjusted GP and GPM*

Margin % THB mm Margin % THB mm

628363-027

+109.4% +11.3% -39.5%

* GP and GPM after adjusting for (reversal) allowance of inventory and realised forex gains / losses

4,318

7,139

4.3%

5.3%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY 2011 FY 2012

0%

2%

4%

6%

8%

10%

763

1,168

950

1,436

1,598

4.1%

4.7%

2.6%

6.6%

6.3%

0

200

400

600

800

1,000

1,200

1,400

1,600

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

0%

1%

2%

3%

4%

5%

6%

7%

Yearly (THB mm) Quarterly (THB mm)

Do not refresh this file

24

Do not refresh this file

24

SICOM Price and F/X

628363-027

TH

B/U

SD

Mo

ve

me

nt

SIC

OM

Pri

ce

Mo

ve

me

nt

297

275

386

370

359

330

310

288 316

296

RSS TSR

Avg.

price

29.0706

Avg. = 29.5710

(US cent /

Kg.)

Do not refresh this file

25

Do not refresh this file

25

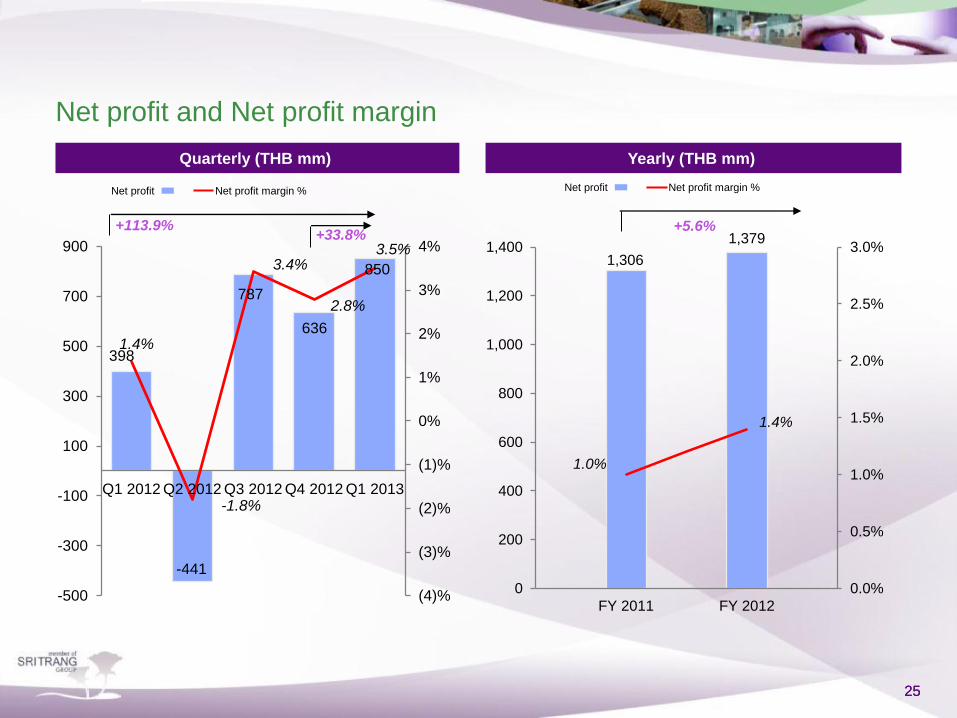

Net profit and Net profit margin

Quarterly (THB mm) Yearly (THB mm)

Net profit Net profit margin %

628363-027

+5.6%

Net profit Net profit margin %

+113.9% +33.8%

1,306

1,379

1.0%

1.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

0

200

400

600

800

1,000

1,200

1,400

FY 2011 FY 2012

398

-441

787

636

850

1.4%

-1.8%

3.4%

2.8%

3.5%

(4)%

(3)%

(2)%

(1)%

0%

1%

2%

3%

4%

-500

-300

-100

100

300

500

700

900

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013

Do not refresh this file

26

Do not refresh this file

26

Return on Assets and Return on Equity

ROA ROE

628363-027

EBITDA (THB mm)

3,883

5,579

3,311 2,840

FY 2009 FY 2010 FY 2011 FY 2012

EBITDA margin

8.4%

6.7%

2.5% 2.9%

FY2009 FY2010 FY2011 FY 2012

11.74% 12.59%

3.36% 3.59%

FY2009 FY2010 FY2011 FY 2012

36.08%

43.21%

9.19% 7.46%

FY2009 FY2010 FY2011 FY 2012

Do not refresh this file

27

Do not refresh this file

27

Healthy leverage and coverage ratios

Debt / equity Net debt / equity

2.16

2.62

1.22 0.94

FY2009 FY2010 FY2011 FY2012

2.03

2.45

1.10 0.86

FY2009 FY2010 FY2011 FY2012

628363-027

Debt = Total liabilities

Equity = Total equity

Assets = Total assets

Net debt = debt – cash

Cash = cash and cash equivalents + fixed deposits at financial institutions

Interest Coverage = EBITDA/finance costs

Interest Coverage

18.85

10.90

3.74 4.00

FY2009 FY2010 FY2011 FY2012

628363-027

I. Sri Trang Business Highlights

II. Natural Rubber Industry Snapshot

III. Financial Highlights

IV. Growth Strategy

AGENDA

Do not refresh this file

29

Do not refresh this file

29

2013 Target & Future Growth Strategy

2013 2014 2015

Rubber plantation: Achieve 50,000 rai

(approx. 8,000 hectares)

Midstream business: Achieve production

capacity of more than 1.5

million tons per year

Target

Capacity : 1.2 mil tons

Sale volume : 1.15 mil tons

Gross profit : 5-7%

Net profit : 2-3%

Dividend

policy :

30% of net

profit

Do not refresh this file

30

Do not refresh this file

30

Upstream strategy update

628363-027

Enhance profitability

and reduce volatility in

earning

Create procurement

networks for potential

raw material from

neighboring area

Pinpoint strategic

locations for

midstream factories in

the future

Ability to procure raw

material at appropriate

price

10,600

17,300

29,385

50,000

Mar'11 Mar'12 Mar'13 Dec'14 (f)

Land development Gestation Tapping area

Achieve 50,000 rai of rubber plantation

• Balance location mix for long-term management

• Ensure sufficiency of saplings from both suppliers

and in-house development

• Synergise across natural rubber value chain

Unit :Rai

Do not refresh this file

31

Do not refresh this file

31

Midstream strategy update

628363-027

Capacity expansion to increase market share

tons p.a.

• Thailand & Indonesia are primary countries for expansion

with focus on diversification to new territories

• Explore new potential country to establish footprints of crumb

rubber plant

• Seek for M&A opportunity for a leap-frog growth at

reasonable cost & return

4%

6%

8%

10%

12%

14%

-

300,000

600,000

900,000

1,200,000

1,500,000

1,800,000

2005

2006

2007

2008

2009

2010

2011

2012

2013f

2014f

2015f

RSS Latex TSR Market share

Increase profitability

Maintain world largest

fully-integrated

Natural Rubber

processor position

Benefit from

economies of scale

Balance the

bargaining power with

suppliers and

customers

Enhance accessibility

to different sources of

fund to support our

operation and

expansion

Do not refresh this file

32

Do not refresh this file

32

Sale & Marketing Strategy

628363-027

Well-balanced portfolio of customers worldwide

Japan

France

USA

Germany

Italy Korea

Taiwan

China

Finland

India

Goodyear Tire & Rubber Co.

Coopper Tire & Rubber Co.

Group Michelin

Nokian

Tyres

P.L.C

Pirelli & C.S.p.A

Continental A.G.

Hangzhou Zhongce Rubber Co. Ltd.

Double Coin Holdings Ltd.

Shandong Linglong Rubber Co. Ltd.

JK Tyres

MRF Ltd.

Apollo Tyres Ltd.

Giti Tire Co. Ltd.

Hankook Tire Co. Ltd.

Kumho Tire Co. Ltd.

Toyo Tire & Rubber Co. Ltd.

Bridgestone Corp.

Sumitomo Rubber Industries Ltd.

Yokohama Rubber Co. Ltd.

Maxxis International /

Cheng Shin Rubber

Singapore

0%2%4%6%8%10%12%14%16%

0

2,000

4,000

2005 2006 2007 2008 2009 2010 2011 2012

NR Import by China (LHS)

• Increase sales team to capture demand growth.

• Create “Sri Trang” standard to meet all

requirements from customers

• Maintain and further improve the reputation of

“most trusted” partner with all tyre makers

Increase coverage of customers in China

• Cover all classes of more than 250 customers to

serve all demand from every corner of the word.

• No single customer accounts for more than 6% of our

total sales.

• Get direct access to end-users to gain demand flow

and market sentiment.

Contribution of STA on China NR Import

Do not refresh this file

33

Do not refresh this file

33

Our Vision

628363-027

Green Rubber Product

Green Company

Green Supply

Green Factory

Passionately, we drive

possibilities

>> the green rubber company >>

Do not refresh this file

34

Do not refresh this file

34

Q&A

628363-027