accounting standards accounts 9 ... - live.icai.org

TRANSCRIPT

LIVE COACHING CLASSESBOARD OF STUDIES(A), ICAI

CA FINALPAPER 8: INDIRECT TAX LAWSTOPIC: REFUND UNDER GST

Faculty: CA Gella Praveenkumar

© The Institute of Chartered Accountants of India

Date: 20th January 2022

Coverage:▪ Overview of Refund provisions

▪ Specific terms & their importance

▪ Analysis of Refund provisions

▪ Examples for practise

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 2

Overview of Refund provisions▪ Refund of tax or any other amount paid erroneously

▪ Refund of taxes in the regular course of supply

▪ Refund of IGST paid by tourist

▪ Refund in certain cases

▪ Process of filing & verification

▪ Stages of Refund processing – various forms

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 3

Relevant Definitions:▪ Explanation to Section 54 – Refund

“refund” includes refund of tax paid on zero-rated supplies of goods or services or both

or on inputs or input services used in making such zero-rated supplies, or refund of tax

on the supply of goods regarded as deemed exports, or refund of unutilised input tax

credit as provided under section 54(3)

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 4

Relevant Definitions:▪ Explanation to Section 15 of IGST Act – Tourist

“tourist” means a person not normally resident in India, who enters India for a stay of

not more than six months for legitimate non-immigrant purposes.

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 5

Refund scenarios

I. Zero-rated supply with payment of IGST

II. Refund of unutilized Input tax credit – Zero-rated supply without payment of IGST

or Inverted Duty structure

III. Refund of tax paid on supply of goods regarded as Deemed Exports

IV. Refund of balance in Electronic Cash Ledger

V. Refund on account of a supply which is not provided, either wholly or partly

VI. Refund of tax wrongly collected & paid – u/s 77

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 6

Refund scenarios

VII. Refund of IGST paid by Tourist leaving India on any goods taken out of India

VIII.Tax becomes refundable on account of a Judgement, Decree, Order or direction of

Appellate authority, Tribunal or a Court

IX. On finalization of a provisional assessment

X. Refund of taxes on purchases made by UN Bodies or Embassies etc.,

XI. Refund of taxes to the retail outlets established in Departure area of Intnl. Airport

XII. Refund of Advance tax paid by CTP/NRTP

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 7

Refund of Tax paid on Export of goods

▪ Export of goods with Payment of IGST

▪ No Refund application required

▪ Shipping bill filed by the Exporter is deemed to be the refund application

▪ Details of GSTR1 for Export of goods shall be validated with details available on

ICEGATE portal on the basis of Shipping Bill

▪ All the reconciled transactions – payment shall be made automatically by concerned

authority for refund of IGST paid into the Bank A/c of the Registered person

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 8

TL for filing Refund application

▪ Any person claiming refund of

▪ any tax and interest, if any,

▪ paid on such tax or any other amount paid by him,

▪ may make an application

▪ before the expiry of two years from the relevant date

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 9

TL for filing Refund application

(a) in the case of goods exported out of India:

▪ (i) if the goods are exported by sea or air, the date on which the ship or the aircraft in

which such goods are loaded, leaves India; or

▪ (ii) if the goods are exported by land, the date on which such goods pass the frontier;

or

▪ (iii) if the goods are exported by post, the date of despatch of goods by the Post Office

concerned to a place outside India;

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 10

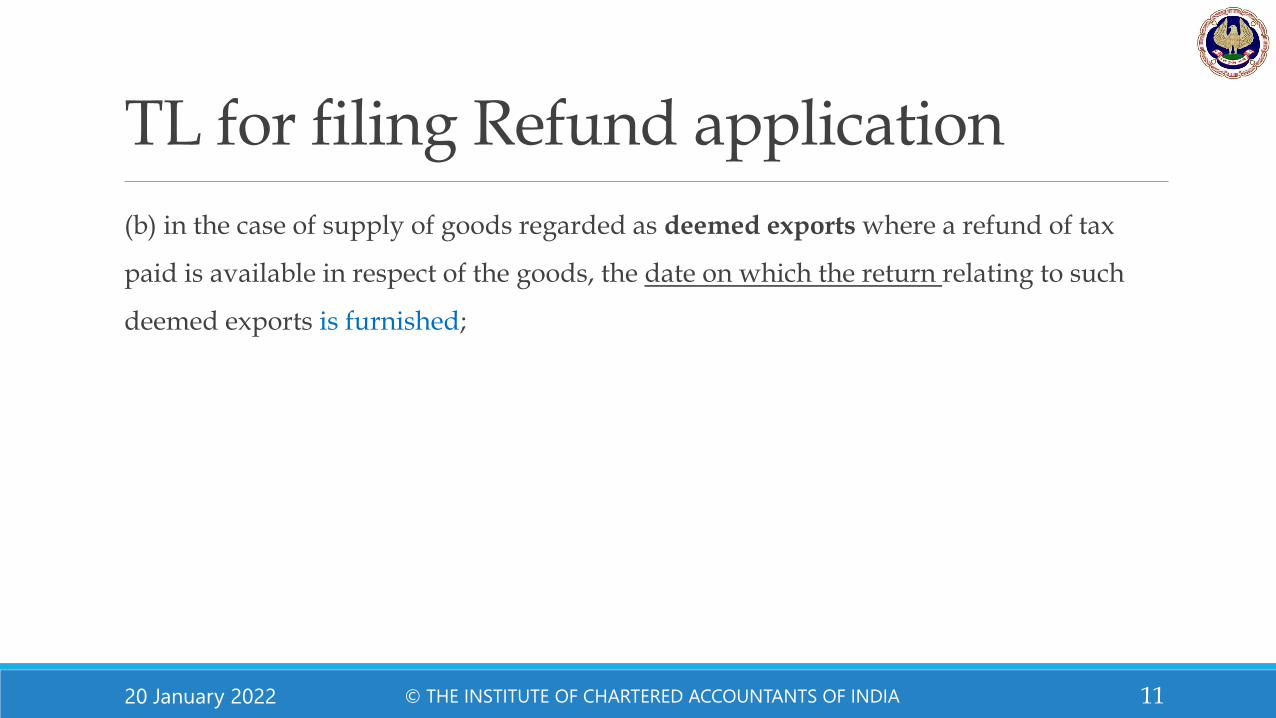

TL for filing Refund application

(b) in the case of supply of goods regarded as deemed exports where a refund of tax

paid is available in respect of the goods, the date on which the return relating to such

deemed exports is furnished;

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 11

TL for filing Refund application

(c) in the case of services exported out of India the date of:–

(i) receipt of payment in convertible foreign exchange or in Indian rupees wherever

permitted by the Reserve Bank of India, where the supply of services had been

completed prior to the receipt of such payment; or

(ii) issue of invoice, where payment for the services had been received in advance prior

to the date of issue of the invoice;

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 12

TL for filing Refund application

(d) in case where the tax becomes refundable as a consequence of judgment, decree,

order or direction of the Appellate Authority, Appellate Tribunal or any court, the date

of communication of such judgment, decree, order or direction;

(e) in the case of refund of unutilised input tax credit under clause (ii) of the first proviso

to sub-section (3)[inverted duty structure], the due date for furnishing of return under

section 39 for the period in which such claim for refund arises

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 13

TL for filing Refund application

(f) in the case where tax is paid provisionally under this Act or the rules made

thereunder, the date of adjustment of tax after the final assessment thereof;

(g) in the case of a person, other than the supplier, the date of receipt of goods or

services or both by such person; and

(h) in any other case, the date of payment of tax.

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 14

Procedure on receipt of Refund claim

1) Acknowledgement for Refund claim

a) Claim relates to refund from electronic cash ledger

b) Other Claims

▪ Application shall be forwarded to proper officer

▪ Proper officer within 15days of filing the said application, scrutinise the application for its

completeness

▪ Where application is found to be complete, an acknowledgement in prescribed form shall be issued

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 15

Procedure on receipt of Refund claim

2) Deficiencies in Refund claim – deficiency memo

a) Where any deficiencies are noticed, the same shall be communicated to the applicant

b) A fresh application has to be filed by the applicant rectifying the stated deficiencies

c) Deficiency communicated under SGST are deemed to be communicated under this act

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 16

Procedure on receipt of Refund claim

3) Grant of Provisional Refund

a) Act provides for Provisional grant of 90% of the total refund

b) In the case of Refund application pertains to Zero-rated supply

c) The above amount shall be paid within 7 days after giving the acknowledgement

d) The balance amount shall be paid after due scrutiny of the documents furnished

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 17

Issuance of SCN and rejection of Refund

Rule 92- Order Sanctioning Refund

▪ In case the Proper officer is not satisfied with the application received for Refund

▪ He shall issue a SCN, stating the ground of rejection

▪ Applicant has to respond within 15days from the date of receipt of SCN

▪ After providing an opportunity of being heard to the applicant, the Proper officer shall pass an

Order either for Refund in whole or part or rejecting the said refund claim

▪ TL for issuance of Refund Order is 60days from the date of filing application as mentioned in Ack.

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 18

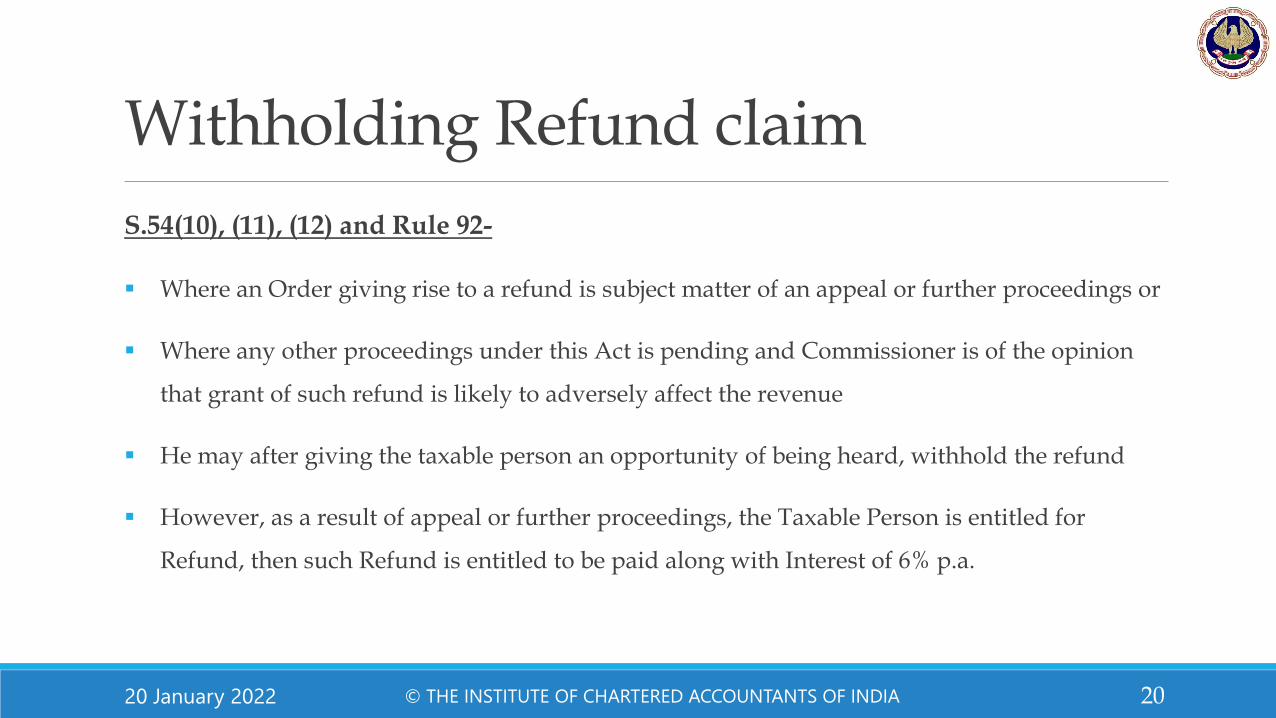

Withholding Refund claim

S.54(10), (11), (12) and Rule 92-

▪ Where any refund of untilised ITC is due in case of Zero-rated supply or Inverted duty

structure, to a Registered person who has defaulted in furnishing any return or who is

required to pay any tax, interest or penalty

▪ Which is not stayed by any court, tribunal or appellate authority with the date specified

▪ The proper officer may withhold payment of refund due until the said person has furnished

the return or paid the tax, interest or penalty as the case may be

▪ Deduct from the refund due of any tax, interest or penalty which remains unpaid

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 19

Withholding Refund claim

S.54(10), (11), (12) and Rule 92-

▪ Where an Order giving rise to a refund is subject matter of an appeal or further proceedings or

▪ Where any other proceedings under this Act is pending and Commissioner is of the opinion

that grant of such refund is likely to adversely affect the revenue

▪ He may after giving the taxable person an opportunity of being heard, withhold the refund

▪ However, as a result of appeal or further proceedings, the Taxable Person is entitled for

Refund, then such Refund is entitled to be paid along with Interest of 6% p.a.

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 20

Recredit of rejected Refund claim

Rule 93- Credit of rejected refund claim

▪ Where any deficiency in Refund claim have been communicated, the amount earlier debited

while filing Refund application shall be re-credited to the electronic credit ledger

▪ Where any Refund amount claimed is rejected, either fully or partly, the amount debited to the

extent of rejection shall be re-credited to the electronic credit ledger

▪ A Refund shall be deemed to be rejected if the appeal if finally rejected or if the applicant gives

an undertaking in writing to the Proper officer that he shall not file an Appeal

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 21

Refund of unutilized ITC

Section 54(3):

▪ Input tax credit gets accumulated in Books of Accounts on account of:

a. Zero-rated supplies

b. Inverted duty structure

▪ Not all Registered persons are entitled for Refund under Inverted Duty structure

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 22

Refund of unutilized ITC

Section 54(3) read with R.89(4) – amount to be claimed as Refund:

▪ For Zero-rated supply:

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 23

Refund Amount

(Turnover of Zero-rated supply of Goods + Turnover of Zero-rated supply of Services)

Adjusted Total Turnover

Net ITC

Refund of unutilized ITC

Section 54(3) read with R.89(4) – relevance of Terminology:

▪ Net ITC - means input tax credit availed on inputs and input services during the

relevant period other than the input tax credit availed for which refund is claimed

under sub-rules (4A) or (4B) or both;

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 24

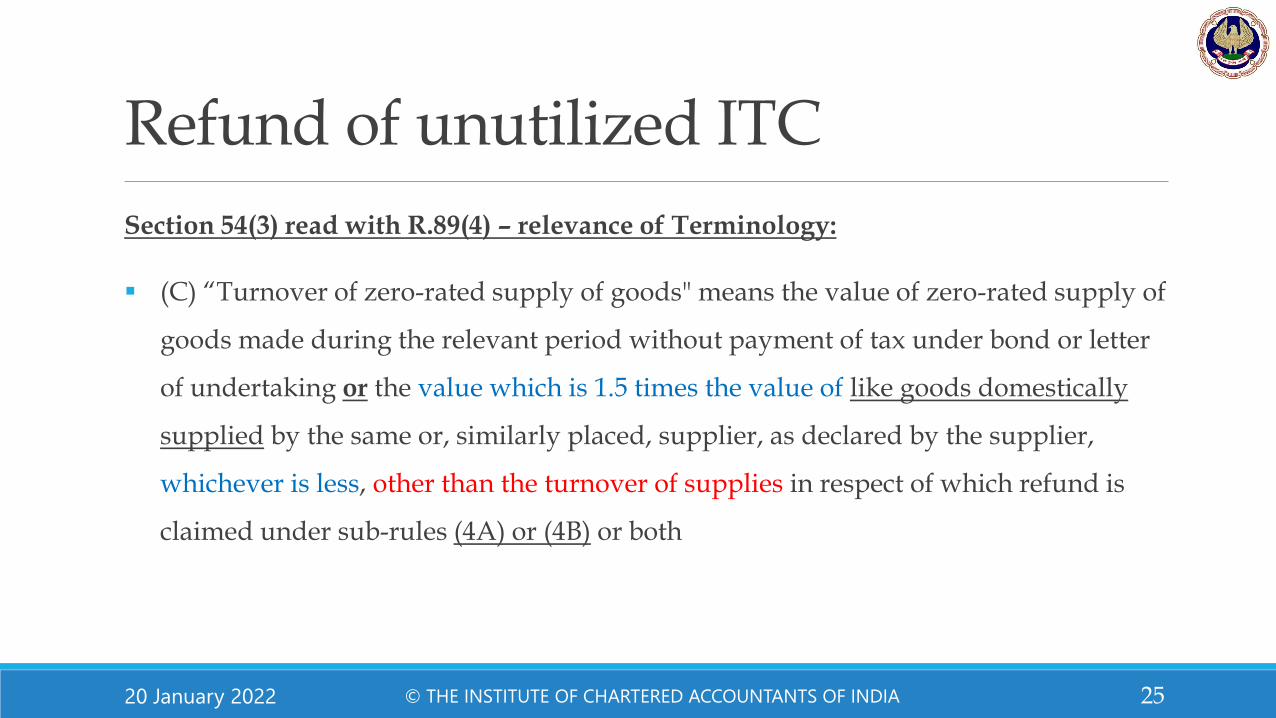

Refund of unutilized ITC

Section 54(3) read with R.89(4) – relevance of Terminology:

▪ (C) “Turnover of zero-rated supply of goods" means the value of zero-rated supply of

goods made during the relevant period without payment of tax under bond or letter

of undertaking or the value which is 1.5 times the value of like goods domestically

supplied by the same or, similarly placed, supplier, as declared by the supplier,

whichever is less, other than the turnover of supplies in respect of which refund is

claimed under sub-rules (4A) or (4B) or both

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 25

Refund of unutilized ITC

Section 54(3) read with R.89(4) – relevance of Terminology:

▪ (D) "Turnover of zero-rated supply of services" means the value of zero-rated supply

of services made without payment of tax under bond or letter of undertaking,

calculated in the following manner, namely:-

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 26

Aggregate of the payments received during the relevant period for zero-rated supply of services

zero-rated supply of services where supply has been completed for which payment had been received in advance in any period prior to the relevant period advances received for zero-rated supply of services for which the supply of services has not been completed during the relevant period

Refund of unutilized ITC

Section 54(3) read with R.89(4) – relevance of Terminology:

▪ (E) “Adjusted Total Turnover” means the sum total of the value of-

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 27

(a) the turnover in a State or a Union territory, as defined under section 2 (112), excluding the turnover of services;

(b) the turnover of zero-rated supply of services determined in terms of clause (D) above and non-zero-rated supply of services,

(i) the value of exempt supplies other than zero-rated supplies;

(ii) the turnover of supplies in respect of which refund is claimed under sub-rule (4A) or sub-rule (4B) or both, if any,

Refund of unutilized ITC

Section 54(3) read with R.89(4A) – Deemed Exports

▪ Stipulates that in case of supplies received

▪ On which supplier has availed the benefit of Deemed Exports

▪ Refund of ITC, availed in respect of Other Inputs/ Input Services used in making

Zero-rated supply of goods or services or both

▪ Shall be granted

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 28

Refund of unutilized ITC

Section 54(3) read with R.89(4B) – Merchant Exports

▪ Stipulates that where person claiming refund of Unutilised ITC on account of Zero-

rated supply w/o payment of tax has –

a) Received supplies on which the supplier has availed the benefit of supply of goods to

merchant exporter at the concession rate of 0.1% or

b) Availed the benefit of exemption from IGST & Cess in respect of goods imported by EOU or

Advance authorisation/EPCG,

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 29

Contd…

Refund of unutilized ITC

Section 54(3) read with R.89(4B) – Merchant Exports

▪ Stipulates that where person claiming refund of Unutilised ITC on account of Zero-

rated supply w/o payment of tax has –

▪ the refund of input tax credit, availed in respect of inputs received under the said

notifications for export of goods and the input tax credit availed in respect of other

inputs or input services to the extent used in making such export of goods, shall be

granted.

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 30

Refund of unutilized ITC

Section 54(3) read with R.89(5) – Inverted Duty Structure

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 31

Maximum Refund Amount

Turnover of inverted rated supply of goods and services

Adjusted Total Turnover

Net ITC

Tax payable on such inverted rated supply of goods and services

Refund of unutilized ITC

Section 54(3) read with R.89(5) – Inverted Duty Structure

▪ (a) Net ITC shall mean input tax credit availed on inputs during the relevant period

other than the input tax credit availed for which refund is claimed under sub-rules

(4A) or (4B) or both; and

▪ (b) "Adjusted Total turnover” and “relevant period" shall have the same meaning as

assigned to them in sub-rule (4)

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 32

Refund of unutilized ITC

Permissible ITC -

1) Maximum refund amount as per above formulae in R.89(4) or (5)

2) Balance in electronic credit ledger of the applicant at the end of tax period for which

the refund claim is being filed

3) Balance in electronic credit ledger of the applicant at the time of filing the refund

application

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 33

Refund of unutilized ITC

Permissible ITC – Order of Debit for Refund

Amount quantified for eligibility as per above shall first be

1) Debited in IGST A/c to the balance available

2) CGST & SGST in equal proportion

3) If there is a part amount diff in CGST/SGST, respective other account can be debited

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 34

Restriction of ITC refund

Amount of ITC is not allowed:

1) Refund not allowed if the goods exported are subjected to export duty

2) If the supplier avails the drawback in respect of CGST or claims refund of IGST paid

on such supplies

Supplier availing drawback of only basic customs duty shall be eligible for refund

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 35

Minimum refund claim

Reference to S.54(14):

1) No refund shall be paid to applicant, if the amount is less than Rs.1,000

2) Above limit is applicable to each tax head separately and not cumulative

3) However, no such restriction for balance available in Electronic cash ledger

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 36

Export of Goods/ Service with payment of tax

Rule 96A – restrictions for Person claiming refund of IGST paid on Goods/Services

exported should not have:

1) Received supplies on which the benefit of Deemed exports, except so far it relates to

EPCG has been availed or benefit of supply of goods to merchant exporter at

concessional rate of 0.1% has been availed

2) Availed the benefit of exemption from IGSST & Cess in respect of goods imported

by EOU or goods imported under Advance Authorisation

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 37

Interest on Delayed Refund

Interest on Refund under normal circumstances:

1) If any tax ordered to be refunded under section 54(5)

2) to any applicant is not refunded within sixty days from the date of receipt of

application,

3) interest at such rate not exceeding six per cent. shall be payable in respect of such

refund from the date immediately after the expiry of sixty days from the date of

receipt of application till the date of refund of such tax

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 38

Interest on Delayed Refund

Interest on Refund in consequence to Order passed in Appeal or Further proceedings:

1) any claim of refund arises from an order passed by an adjudicating authority or

Appellate Authority or Appellate Tribunal or court which has attained finality and

2) the same is not refunded within sixty days from the date of receipt of application

filed consequent to such order,

3) interest at such rate not exceeding nine per cent. shall be payable in respect of such

refund from the date immediately after the expiry of sixty days from the date of

receipt of application till the date of refund

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 39

20 January 2022 © THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA 40

THANK YOU