actuary education in hitotsubashi university

TRANSCRIPT

Actuary Examination in Japan Actuary Education in Hitotsubashi University

.

.

. ..

.

.

Actuary Education in Hitotsubashi University

Takahiko Fujita

Hitotsubashi University

Aug. 8, 2009

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Contents

.

. .1 Actuary Examination in Japan

Mathematics

Life Insurance Mathematics

Nonlife Insurance Mathmatics

Pension Mathematics

Accounting· Economics·Investment Theory

.

. .

2 Actuary Education in Hitotsubashi University

Actuary Education in Hitotsubashi University

Math.Test Example

Life Insurance mathematics Problem (Example)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

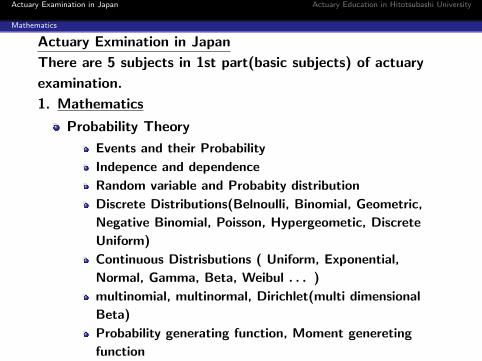

Mathematics

Actuary Exmination in Japan

There are 5 subjects in 1st part(basic subjects) of actuary

examination.

1. Mathematics

Probability Theory

Events and their Probability

Indepence and dependence

Random variable and Probabity distribution

Discrete Distributions(Belnoulli, Binomial, Geometric,

Negative Binomial, Poisson, Hypergeometic, Discrete

Uniform)

Continuous Distrisbutions ( Uniform, Exponential,

Normal, Gamma, Beta, Weibul . . . )

multinomial, multinormal, Dirichlet(multi dimensional

Beta)

Probability generating function, Moment genereting

function

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Accounting´ Economics´Investment Theory

Conditional probability, conditional Expectation

Statistics

Estimation(Interval, Point, Maximum likelihood,

Cramer-Rao)

Hypothesis Testing

orderstatistics

F, t, χ distribution

Modeling

Regression

Time Series(Stationary process, AR(p), MA(q), ARMA)

Stochastic Process( Markov, Random Walk, Poisson

Process, Brownian motion, Martingale)

Simulation(Inverse function method, Composition

method, rejection method)

Linear Programming

2. Life Insurance Mathematics

3. Nonlife Insurance Mathematics

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Mathematics

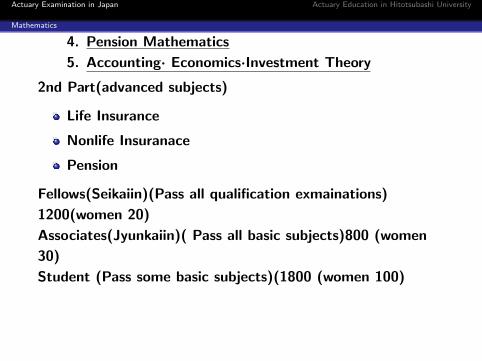

4. Pension Mathematics

5. Accounting· Economics·Investment Theory

2nd Part(advanced subjects)

Life Insurance

Nonlife Insuranace

Pension

Fellows(Seikaiin)(Pass all qualification exmainations)

1200(women 20)

Associates(Jyunkaiin)( Pass all basic subjects)800 (women

30)

Student (Pass some basic subjects)(1800 (women 100)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Mathematics

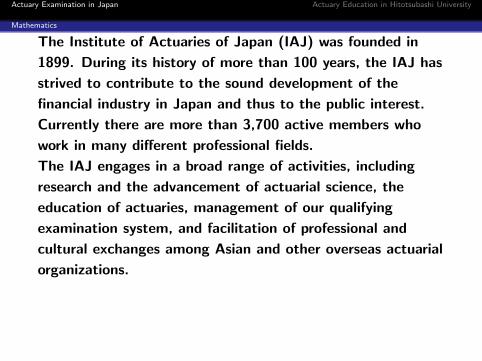

The Institute of Actuaries of Japan (IAJ) was founded in

1899. During its history of more than 100 years, the IAJ has

strived to contribute to the sound development of the

financial industry in Japan and thus to the public interest.

Currently there are more than 3,700 active members who

work in many different professional fields.

The IAJ engages in a broad range of activities, including

research and the advancement of actuarial science, the

education of actuaries, management of our qualifying

examination system, and facilitation of professional and

cultural exchanges among Asian and other overseas actuarial

organizations.

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Actuary Education in Hitotsubashi University

Actuary Education in Hitotsubashi University

In the last ten years, there are about thirty acturies or

actuary candiates who graduated Hitotsubashi University and

Graduate School. First they studied ”Mathematics ” , ”Life

Insurance Mathematics”, ”Nonlife Insurance Mathemtics”. I

gave lots of mathematical problem to them. Once a week,

they solve these problems and check answers. For another

one day in week, they study Life Insurance Mathematics or

Nonlife Insurance Mathematics in the seminar.

Here we show examples for mathematical exercises.

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

2009 actuary math test(example)

.

..

1 ある交差点の交通事故の起こる間隔は独立で パラメータ – の指数分布(平均 1λ)である。時刻 0 から時刻

t までに起こった事故の回数 = Nt (N0 = 0) とし 1 回の事故で払われる保険金は平均 1µの指数分

布で独立とする。また時刻 0 から時刻 t までに払った保険金の総額 = Yt とする。以下を求めよ。

(1) E (Nt ) (2) V (Nt ) (3) E (Nt (Nt ` 1) (Nt ` 2) ) (4) E (N3t ) (5) E (Nt jNt > 0 )

(6) E (Yt ) (7) V (Yt ) (8)E (N2t jNt ) (9)E“(N2t)

2jNt

”

.

.

.

2 Wt; W′t を独立な(標準)ブラウン運動とするとき、以下を求めよ。

(10) E ( jWt j3 ) (11) E ( jWt +W ′t j3 ) (12) E ( jWt +W2t j3 )

(13) fW2t|Wt(x j y ) (14) fW2t|W ′

t(x j y ) (15) fWt|W2t

(x j y )

(16) E (W22t jWt = y ) (17) E (W2

2t jW ′t = y ) (18) E (W2

t jW2t = y )

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

.

.

.

3 確率密度関数 f(x ´ „) =

((1 + „)xθ 0 < x < 1

0 その他 を分布に持つ母集団から

大きさ n の標本 x1; x2; ´ ´ ´ ; xn にもとづく Q の最尤推定量を求めよ。(19)

.

. .4 密度関数 fX(x) =

(6x (1` x) 0 < x < 1

0 その他 を分布に持つ母集団から大きさ 45 の標本が

とられた。標本平均を X とするとき、次を求めよ。

(20) X の分布を求めよ。(正規近似を用いよ)(21) P (X < 0:55) の近似値を求めよ。

ただし P (N (0; 1) < u (") ) = " となる u(") の逆関数 u−1(") を用いてよい。

.

.

.

5 X ‰ Fs (p1) (i:e:P (X = k) = p1(1` p1)k−1 (k = 1; 2; ´ ´ ´ )) Y ‰Fs (p2) X;Y は独立とする。また R = X

Yとする。次を求めよ。

(22) C を自然数とするとき E ( min (C;X) ) (23) E (Y min (Y;X) )

(24) r =n

m(m;n は互いに素な自然数) とするとき P (R = r)

.

.

.

6 事象 A1; A2; ´ ´ ´ ; An; ´ ´ ´ は独立で P (An) = 1` 1nである。

N = min fn jAn が起こる g (つまり A1; A2; ´ ´ ´ ; An の中で最初に起こる番号) とする。このとき

(25) k 2 N [ f0g として P (N > k) (26) P (N = k) (27) gN (t) = E (tN )

(28) E (N) (29) V (N)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

.

.

.

7 白玉 a 個 黒玉 b 個入れたつぼがある。一球ずつ取り出すことを、全て同じ色の玉がつぼの中に残るまで続ける。つぼの中に残る玉が白である確率を求めよ。(30)

.

..

8 X ‰ Y ‰ U(0; 1) は独立でまた、 X = x という条件のもとで Z ‰ U(0; x2) である。 以下を求めよ。(32) flog X(x) (33) fmin (X,Y )(x) (34) fmax (3X,4Y )(x) (35) E(max(3X; 4Y ))

(36) fZ|X(zjx) (37) fZ(z) (38) E(ZjX = x) (39) E(Z) (40) V (Z)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

第7回解答

1: (1) ポアソン過程の性質より Ntは パラメータ(強度)–のポアソン過程 ) Nt ‰Po (–t) ) E (Nt) = –t

(2) V (Nt) = V (Po (–t)) = –t

(3) E (¸Nt ) = E (¸P o(λt)) =

e−λt(1−α) ¸で 3 回微分して E“Nt (Nt ` 1) (Nt ` 2)¸(Nt−3)

”=

(–t)3e−λt(1−α)

) ¸ = 1 を代入して E (Nt (Nt ` 1) (Nt ` 2) ) = (–t)3

(4) x3 = x(x` 1)(x` 2) + 3x(x` 1) + x より E (N3

t ) = E (Nt (Nt ` 1) (Nt ` 2) ) + 3E (Nt (Nt ` 1) ) + E (Nt) =

(–t)3 + 3(–t)2 + –t

(5) P (Nt > 0) = 1` P (Nt = 0) = 1` e−λt E (Nt; Nt > 0) =P∞

k=1 k(λt)k

k!e−λt =

P∞l=0

(λt)l+1

l!e−λt = –t

) E (Nt jNt > 0) =E (Nt,Nt>0)

P (Nt>0)= λt

1−e−λt

(6) X1; X2; ´ ´ ´ ; Xi; ´ ´ ´は独立で Xi ‰ Exp (—) とすると定義より Yt =PNt

i=1Xi

よって E (Yt jNt = n) = E`Pn

i=1Xi jNt = n´= E

`Pni=1Xi

´=Pn

i=1 E (Xi) = nµ

(* X1; X2; ´ ´ ´ ; Xi; ´ ´ ´と Ntは独立)

) E (Yt jNt) =Ntµ

) E (Yt) = E (E (Yt jNt)) = E“

Ntµ

”= λt

µ

(7) V (Yt jNt = n) = V`Pn

i=1Xi jNt = n´= V

`Pni=1Xi

´= nV (Xi) =

nµ2 ) V (Yt jNt) =

Ntµ2

) V (Yt) = E (V (Yt jNt)) + V (E (Yt jNt)) = E

„Ntµ2

«+ V

“Ntµ

”=

λtµ2 + 1

µ2 V (Nt) = 2λtµ2

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

(8) E (N2t jNt) = E (Nt +N2t `Nt jNt)

= Nt + E (N2t `Nt jNt)

= Nt + E (N2t `Nt) (* 独立増分性)

= Nt + E (gNt) = Nt + –t

(9) E“(N2t)

2 jNt

”

= E“(Nt +N2t `Nt)

2 jNt

”= E

“N

2t + 2Nt(N2t `Nt) + (N2t `Nt)

2 jNt

”

= N2t + 2Nt E (N2t `Nt jNt) + E

“(N2t `Nt)

2jNt

”

= N2t + 2NtE (N2t `Nt) + E

“(N2t `Nt)

2”

(* 独立増分性)

= N2t + 2Nt(–t) + –t+ (–t)2

2: (10) Wt ‰ N (0; t) ‰ ptN (0; 1) ) E (jWt j3) = (pt)3E ( jN (0; 1) j3 )

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

E ( jN (0; 1) j3 ) =1p

2ı

Z ∞

−∞jxj3 e− 1

2x2dx =

2p

2ı

Z ∞

0x3e

− 12

x2dx

=2p

2ı

Z ∞

0(p

2u)3e−up

21

2u

− 12 du (x =

p2u)

=2p

2ı´ 2Z ∞

0ue−udu

= 2 ´s

2

ı` (2) = 2

s2

ı

) E (jWt j3) = (pt)32

s2

ı

(11) 正規分布の再生性より Wt +W ′t ‰ N (0; t) +N (0; t)

| {z }互いに独立

‰ N (0; 2t) ‰

p2tN (0; 1)

) E ( jWt +W ′t j3 ) = E

“(p

2t)3 jN (0; 1) j3”

= (p

2t)32q

2π

= 8

pt3√π

(12) Wt +W2t = 2Wt +W2t `Wt ‰ 2N (0; t) +N (0; t)| {z }

互いに独立

‰

N (0; 4t) +N (0; t)| {z }

互いに独立

‰ N (0; 5t) ‰ p5tN (0; 1)

(* 正規分布の再生性) ) E ( jWt +W2t j3 ) = (p

5t)3E“jN (0; 1) j3

”=

(p

5t)32q

2π

(13) f(Wt,W2t)(y; x ) = 1√

2πte

− y2

2t 1√2πt

e− (y−x)2

2t

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

) fW2t|Wt(x j y ) =

f(Wt,W2t)(y,x )

fWt(y)=

1√2πt

e− y2

2t 1√2πt

e− (x−y)2

2t

1√2πt

e− y2

2t

=

1√2πt

e− (x−y)2

2t

(14) Wtと W2tは独立より fW2t|W ′t

(x j y ) = fW2t(x) = 1√

2π2te

− x2

2·2t

(15) fWt|W2t(x j y ) =

f(Wt,W2t)(x,y)

fW2t(y)

=

1√2πt

e− x2

2t 1√2πt

e− (x−y)2

2t

1√2π2t

e− y2

2·2t

=1pıte

− x2

2t− (x−y)2

2t+

y2

4t

=1pıte

− 14t

(2x2+2(x2−2xy+y2)−y2)=

1pıte

− 14t

(y−2x)2

(注 W2t = y のもとで Wt ‰ N„y

2;t

2

«)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example(16)E (W2

2t jWt = y )

= E“(Wt +W2t `Wt)

2 jWt = y”

= E“( y +W2t `Wt )

2 jWt = y”

= E“y2

+ 2y(W2t `Wt) + (W2t `Wt)2”

(* Wtと W2t `Wtは独立)

= y2

+ 2yE (W2t `Wt) + E“(W2t `Wt)

2”

= y2

+ 0 + t = y2

+ t

(17) W2tと W′tは独立より E (W2

2t jW ′t = y ) = E

“(W2t)

2”

= V (W2t) =

2t (* E(W2t) = 0)

(18)E (W2t jW2t = y )

= E

„„N

„y

2;t

2

««2 «

(* (15) の注)

= V

„N

„y

2;t

2

««+

„E

„N

„y

2;t

2

«««2=t

2+y2

4

(19) 尤度関数は L (x1; x2; ´ ´ ´ ; xn j „) = (1 + „)n(x1; x2; ´ ´ ´ ; xn)θ

) logL = n log(1 + „) + „ log(x1; x2; ´ ´ ´ ; xn)

0 = ∂ log L∂θ

= n1+θ

+ log(x1; x2; ´ ´ ´ ; xn) ) „ = ` nlog(x1,x2,··· ,xn)

` 1

4: (20) E (X) = 12; V (X) = 1

20) E (X) = 1

2V (X) = 1

45´ 2

20= 1

900

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

) 中心極限定理より X− 12q

1900

‰ N (0; 1) ) Y の分布 + N ( 12; 1900

)

(21) P (X < 0:55) = P

X− 1

2130

<0.55− 1

2130

!=

P (N (0; 1) < 1:5 ) つまり求める確率 u−1(1:5)

(22) E ( min (C;X) ) =PC

k=1 kP (X = k) +PN

k=C+1 CP (X = k) =PC

k=1 kp1(1` p1)k−1 + CP∞

k=C+1 p1(1` p1)k−1

ここで S =PC

k=1 k(1` p1)k−1 とおくと

S = 1 + 2(1` p1) + ´ ´ ´ + C(1` p1)C−1

(1` p1)S = (1` p1) + ´ ´ ´

+ (C ` 1)(1` p1)C−1

+ C(1` p1)C

p1S = 1 + (1` p1) + ´ ´ ´ + (1` p1)C−1 ` C(1` p1)

C

=1` (1` p1)C

1` (1` p1)` C(1` p1)

C

E ( min (C;X) ) =1−(1−p1)C

p1` C(1` p1)C + C(1` p1)C =

1−(1−p1)C

p1(C = 0; 1 などで検算)

(23) E (Y min (Y;X) jY = C) = CE ( min (C;X) jY = C) =

CE ( min (C;X) ) = C ´ 1−(1−p1)C

p1

E (Y min (Y;X) jY ) = Yp1` 1

p1Y (1` p1)Y

E (Y min (Y;X) ) = E (E (Y min (Y;X) jY )) =1

p1E (Y )` 1

p1E“Y (1` p1)Y

”

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

ここでE (Y ) = 1p2

また E (tY ) =p2t

1−(1−p2)t

) E (Y tY −1) =p2( 1−(1−p2)t)−( −(1−p2))p2t

( 1−(1−p2)t)2=

p2( 1−(1−p2)t)2

) E (Y tY ) =p2t

( 1−(1−p2)t)2) E

“Y (1` p1)Y

”=

p2(1−p1)

( 1−(1−p1)(1−p2))2

) E (Y min (Y;X) ) = 1p1p2

` 1p1ˆ p2(1−p1)

( 1−(1−p1)(1−p2))2

(24) P (R =n

m) =

∞X

k=1

P (X = nk \ Y = mk)

=∞X

k=1

P (X = nk)P (Y = mk)

=∞X

k=1

p1(1` p1)nk−1p2(1` p2)

mk−1

=p1p2(1` p1)n−1(1` p2)m−1

1` (1` p1)n(1` p2)m

(25) P (N > k) = P (A1; A2; ´ ´ ´ ; Akはすべて起こらない) =

P (Ac1)P (Ac

2) ´ ´ ´ P (Ack) = 1

1ˆ 1

2ˆ ´ ´ ´ ˆ 1

k= 1

k!

(26) P (N = k) = P (N > k` 1)` P (N > k) =1

(k` 1)!` 1

k!(k = 1; 2; ´ ´ ´ )

(27) gN (t) =∞X

k=1

tk

1

(k` 1)!` 1

k!

!= t

∞X

l=0

tl

l!`

∞X

k=0

tk

k!= te

t`(et`1) = 1+(t`1)e

t

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

(28) g′N (t) = et

+ (t` 1)et ) E (N) = g′N (1) = e

(29) g′′N (t) = et + et + (t` 1)et ) g′′

N (1) = 2e ) V (N) =

g′′N (1) + g′

N (1)` ` g′N (1)

´2 = 2e+ e` e2 = 3e` e2

7: (30) 取り出し方を逆に見ても (逆に完了という考え方) 同じことなので最初に白球を選ぶ確率に等しい

よって a

a+ b

8. (32) P (X < 0) = 1 に注意して x < 0 に対して Flog X(x) = P (logX < x) = P (X < ex) = ex 微分して flog X(x) = ex(x < 0)

(33) 0 < P (min (X; Y ) < 1) = 1 に注意して 0 < x < 1 に対して、Fmin (X,Y )(x) = P (min (X;Y ) < x) = 1`P (min (X; Y ) > x) = 1`(1`x)2 = 2x`x2,

微分して fmin (X,Y )(x) = 2(1` x) (0 < x < 1)

(34)0 < P (min (X;Y ) < 4) = 1 に注意して 3 < x < 4 に対して、 Fmax (3X,4Y )(x) =

P (max (3X; 4Y ) < x) = P (3X < x)P (4Y < x) = P (X < x3)P (Y < x

4) = x

4, また、

0 < x < 3 に対して、 Fmax (3X,4Y (x) = P (max (3X; 4Y < x) = P (3X < x)P (4Y <

x) = P (X < x3)P (Y < x

4) = x2

12微分して fmin (X,Y )(x) =

(x6

(0 < x < 3)14

(3 < x < 4)

(35)E(max(3X; 4Y )) =R 30

x2

6dx+

R 43

x4dx = 19

8

(36) fZ|X(zjx) = 1x2 (0 < z < x2) (37)

f(Z,X)(z; x) = fZ|X(zjx)fX(x) = 1x2 (0 < z < x2 < 1; x > 0) よって 0 < z < 1 とし

て、 fZ(z) =R 1√

z1

x2 dx =1−√

z√z

(38)0 < x < 1 として、 E(ZjX = x) = E(U(0; x2)) = x2

2(39)

E(Z) = E(E(ZjX)) = E( X2

2) = 1

6

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Math.Test Example

(40)V (ZjX = x) = V (U(0; x2)) = x4

12よって

V (Z) = E(V (ZjX)) + V (E(ZjX)) = E( X4

12) + V ( X2

2) = 7

180

(注意 もちろん fZ(z) ができているのでそれを用いて計算してもよい。)

Actuary Examination in Japan Actuary Education in Hitotsubashi University

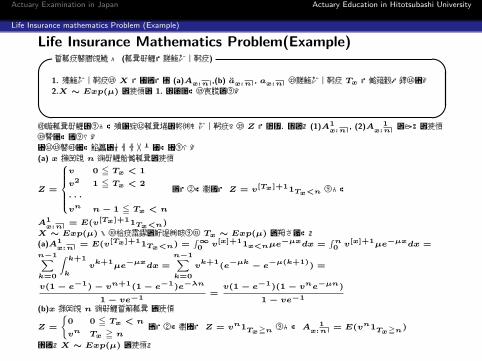

Life Insurance mathematics Problem (Example)

Life Insurance Mathematics Problem(Example)生保数理超入門 � (保険契約と余命確率変数)¶ ³

1. 寿命確率変数を X としたとき (a)Ax:n ,(b) ax:n , ax:n を余命確率変数 Tx と期待値で表わせ。2.X ‰ Exp(—) の場合に 1. のすべてを計算せよ。

µ ´解説保険契約によって受け取る保険金の現価(確率変数)を Z とおく. まず,(1)A1

x:n, (2)A 1

x:nの2つの場合

を調べてみよう。それを理解して問題にチャレンジしてみよう。(a) x 才加入 n 年契約定期保険の場合

Z =

8>>>><>>>>:

v 0 5 Tx < 1

v2 1 5 Tx < 2

´ ´ ´vn n` 1 5 Tx < n

まとめて書くと Z = v[Tx]+11Tx<n よって

A1x:n

= E(v[Tx]+11Tx<n)

X ‰ Exp(—) なら指数分布の無記憶性より Tx ‰ Exp(—) に注意して,(a)A1

x:n= E(v[Tx]+11Tx<n) =

R∞0 v[x]+11x<n—e

−µxdx =Rn0 v[x]+1—e−µxdx =

n−1X

k=0

Z k+1

kv

k+1—e

−µxdx =

n−1X

k=0

vk+1

(e−µk ` e−µ(k+1)

) =

v(1` e−1)` vn+1(1` e−1)e−λn

1` ve−1=v(1` e−1)(1` vne−µn)

1` ve−1

(b)x 才加入 n 年契約生存保険 の場合

Z =

(0 0 5 Tx < n

vn Tx = nまとめて書くと Z = vn1Tx=n よって A 1

x:n= E(vn1Tx=n)

また,X ‰ Exp(—) の場合,

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Life Insurance mathematics Problem (Example)

A 1x:n

= E(vn1Tx=n) =R∞0 vn1u=n—e

−µudu = vn R∞n —e−µudu = vne−µn

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Life Insurance mathematics Problem (Example)

Answer

(a) x 才加入 n 年契約期始払い生命年金の場合 Z =

8>>>><>>>>:

1 Tx = 0

v Tx = 1

´ ´ ´vn−1 Tx = n` 1

つまり,Z =

8<:

1 + v + ´ ´ ´+ vTx =1−vTx+1

1−vTx 5 n` 1

1 + v + ´ ´ ´+ vn−1 =1−vn

1−vTx = n

まとめると Z =1−vmin(Tx+1,n)

1−vよって ax:n = E(Z) = E(

1−vmin(Tx+1,n)

1−v)

(b)x 才加入 n 年契約期ま末払い生命年金の場合

Z =

8>>>><>>>>:

v Tx = 1

v2 Tx = 2

´ ´ ´vn Tx = n

つまり,Z =

8><>:v + v2 + ´ ´ ´+ vTx =

v−vTx+1

1−vTx 5 n

1 + v + ´ ´ ´+ vn−1 =v−vn+1

1−vTx = n

まとめると Z =v−vmin(Tx+1,n+1)

1−vよって ax:n = E(Z) = E(

v−vmin(Tx+1,n+1)

1−v)

2. X ‰ Exp(—) なら指数分布の無記憶性より Tx ‰ Exp(—) である。よって

(a)ax:n = E(Z) = E(1−vmin(Tx+1,n)

1−v) ここで

E(vmin(Tx+1,n)) =R∞0 vmin(x+1,n)—e−µxdx =

Rn−10 vn—e−µxdx+

R∞n−1 v

x+1—e−µxdx = vn + vne−µ(n−1) log vµ−log v

よって

ax:n = 11−v

` 11−v

(vn + vne−µ(n−1) log vµ−log v

=1−vn

1−v` vn

1−ve−µ(n−1) log v

µ−log v

(b)ax:n = E(v−vmin(Tx+1,n+1)

1−v) = v

1−v` 1

1−vE(vmin(Tx+1,n+1)) =

Actuary Examination in Japan Actuary Education in Hitotsubashi University

Life Insurance mathematics Problem (Example)

v1−v

` 11−v

(vn+1 + vn+1e−µn log vµ−log v

=v−vn+1

1−v` vn+1

1−ve−µn log v

µ−log v