affordable care act update rev 10/07/2013 your presenter: jerry rhinehart, cic, clu, chfc, rhu...

TRANSCRIPT

Affordable Care Act Update

Rev 10/07/2013Rev 10/07/2013

Your Presenter:Your Presenter:

Jerry Rhinehart, CIC, CLU, ChFC, RHUPanama City, FL

93 TOTAL provisions will be enacted over the 10 year time span that will impact: every US citizen, health

insurance coverage, health insurance companies, pharmaceutical

companies, employers, Medicare, Medicaid, taxes (21 major),

substantial regulations for hospital & physicians, … and even required

posting of nutritional content at your favorite fast food restaurant.

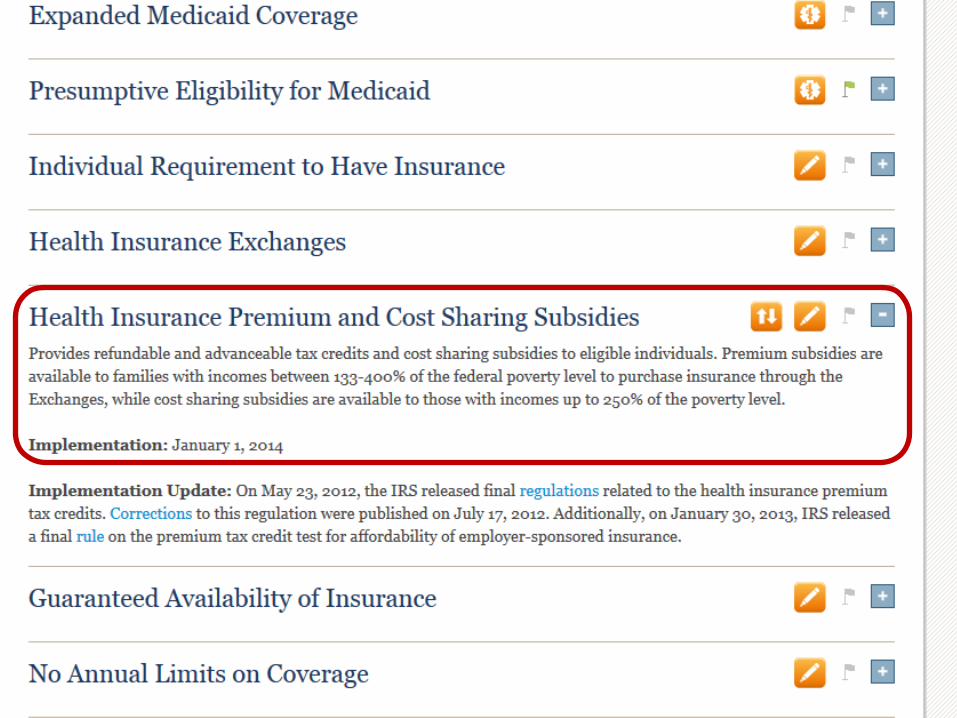

Provides refundable and advanceable tax credits and cost sharing subsidies to eligible individuals. Premium subsidies are available to families with incomes between 133-400% of the federal poverty level (FPL) to purchase insurance through the Exchanges, while cost sharing subsidies are available to those with incomes up to 250% of the poverty level.

Health Insurance Premiums and Cost-Sharing Subsidies (2014)

Understanding Health Insurance Subsidies (2014)

2013: CMS

400% FPL _

250% FPL _

133% FPL _ _133% FPL

_250% FPL

_400% FPL

_100% FPL 100% FPL _

Required to show proof of a QHP- but no financial assistance of any form

Required to show proof of a QHP- and eligible for advanced premium tax credits

Required to show proof of a QHP- and eligible for advanced premium tax credits and cost-sharing reductions

Eligible for Medicaid – little or no cost

Those Having (and Not Having) Health Insurance

US (%) Type Coverage & Where NC (%)49 ER’ Provided Coverage 475 Individual Coverage 4

16 Medicaid 1713 Medicare 131 Other Public 2

16 Uninsured 17307,890,000 9,376,800

2011: KFF.org – State Health Facts

MLR (Medical Loss Ratio – 80% Small Group and

Individual – 85% Large Group) (eff 01-01-2011)

NOTE: The MLR requirement does NOT apply to ERISA plans - fully or

partially self-funded.

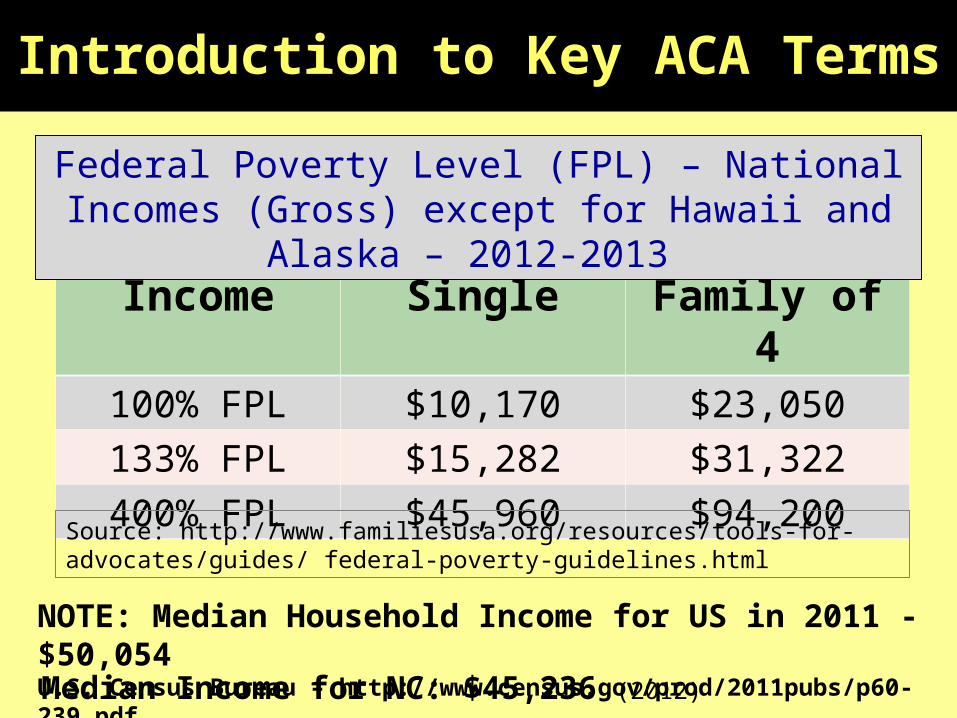

Introduction to Key ACA Terms

MLR (Medical Loss Ratio – 80% Small Group and

Individual – 85% Large Group) (eff 01-01-2011)

FPL (Federal Poverty Level – 133% - 400%) (eff 01-

01-2014) (NOTE: Box #1 on the Employees W-2)

Introduction to Key ACA Terms

Income Single Family of 4100% FPL $10,170 $23,050133% FPL $15,282 $31,322400% FPL $45,960 $94,200

Federal Poverty Level (FPL) – National Incomes (Gross) except for Hawaii and Alaska – 2012-2013

Source: http://www.familiesusa.org/resources/tools-for-advocates/guides/ federal-poverty-guidelines.html

Introduction to Key ACA Terms

NOTE: Median Household Income for US in 2011 - $50,054U.S. Census Bureau – http://www.census.gov/prod/2011pubs/p60-239.pdf

Median Income for NC: $45,236 (2012)

Health Reform Implementation Timeline

Insurance Reforms (CO-OP; enhanced use of e-filing)

Employer Notice Requirements – (03-01-13) Requires employers to provide written notice informing employees about the Exchange and potential eligibility for premium credits. (Released 06/2013 – one for coverage / one for no coverage)

2013

Search: Jones Day aca exchange notification

Search: Jones Day aca exchange notification

Health Reform Implementation Timeline

Insurance Reforms (CO-OP; enhanced use of e-filing)

Employer Notice Requirements – (03-01-13) Requires employers to provide written notice informing employees about the Exchange and potential eligibility for premium credits. (Released 06/2013 – one for coverage / one for no coverage)

Tax Change

2013

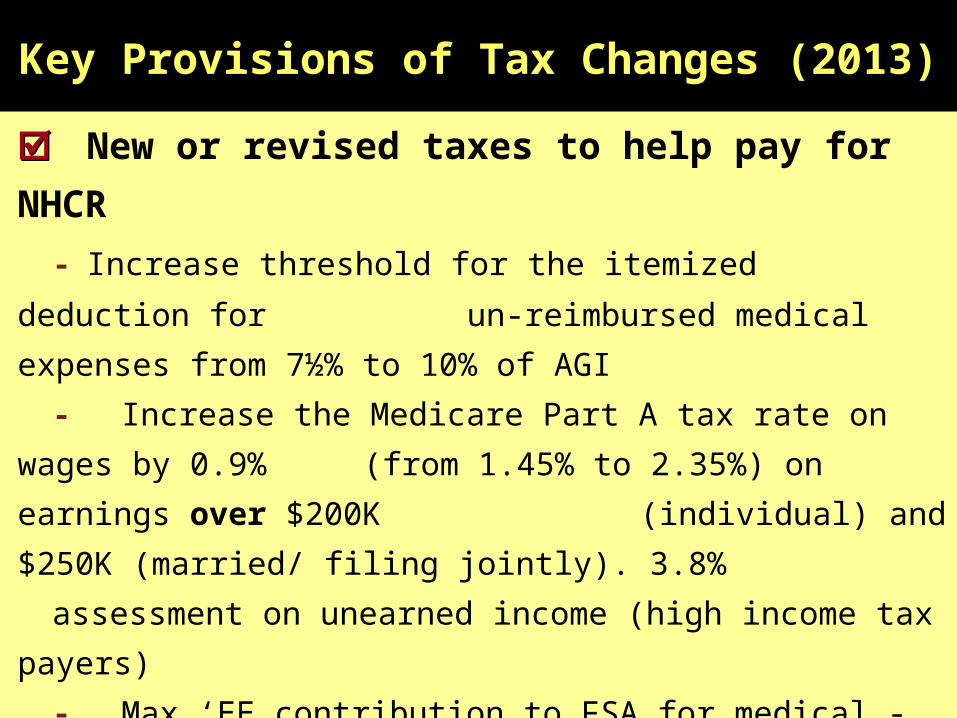

Key Provisions of Tax Changes (2013)

New or revised taxes to help pay for NHCR

- Increase threshold for the itemized deduction for

un-reimbursed medical expenses from 7½% to 10% of AGI

- Increase the Medicare Part A tax rate on wages by 0.9%

(from 1.45% to 2.35%) on earnings over $200K

(individual) and $250K (married/ filing jointly). 3.8%

assessment on unearned income (high income tax

payers)

- Max ‘EE contribution to FSA for medical - $2,500 per year

- Excise tax (2.3%) on medical devices (hip replacement, x-

ray machine, etc. – numerous exceptions exists)

- Eliminated ‘ER deduction for retiree Medicare Part D

Health Reform Implementation Timeline

Individual and Employer Requirements

2014

Individual and Employer Requirements (2014)

Require U.S. citizens and legal immigrants to have

qualified health coverage

- For Individuals: Phased-in tax penalty

- For Large Employers: Possible penalties to “Large ‘ER”

(50 or more FTEs – 30 hrs)

- Complex rules and variables exist

This was the “individual mandate”

litigation ruled upon by the SCOTUS

in June of 2012

Those who fall under the “requirement” but fail to carry at least the “Bronze” plans will be subject to a penalty: (the greater of…) - $95 per year in 2014, $325 in 2015, $695 in 2016 (half that amount for children under age 18), up to maximum of three times those penalty amounts per family, OR,

- 1% of income above the tax filing threshold in 2014, 2% in 2015, and 2½% in 2016

Individual Non-Compliance - ACA (2014)

Income 2014 2015 2016

$100,000

Income

$285 $975 $2,085

$1,000 (1%) $2,000 (2%) $2,500 (2½%)

The penalty is the greater of the two calculations

- Family of Four (includes 2 children under age 18) $100K Taxable -

What are the Potential Financial Penalties to Individuals who do NOT carry insurance?

Individual Non-Compliance - ACA (2014)

Employer Responsibility / Penalties (2014)

Large Employer (50+ EEs) (* Delayed until 2015)

- Full time employees (30 hrs)

- Part time employees

Small Employer (1 to 49 EEs)

Employer Responsibility / Penalties (2014)

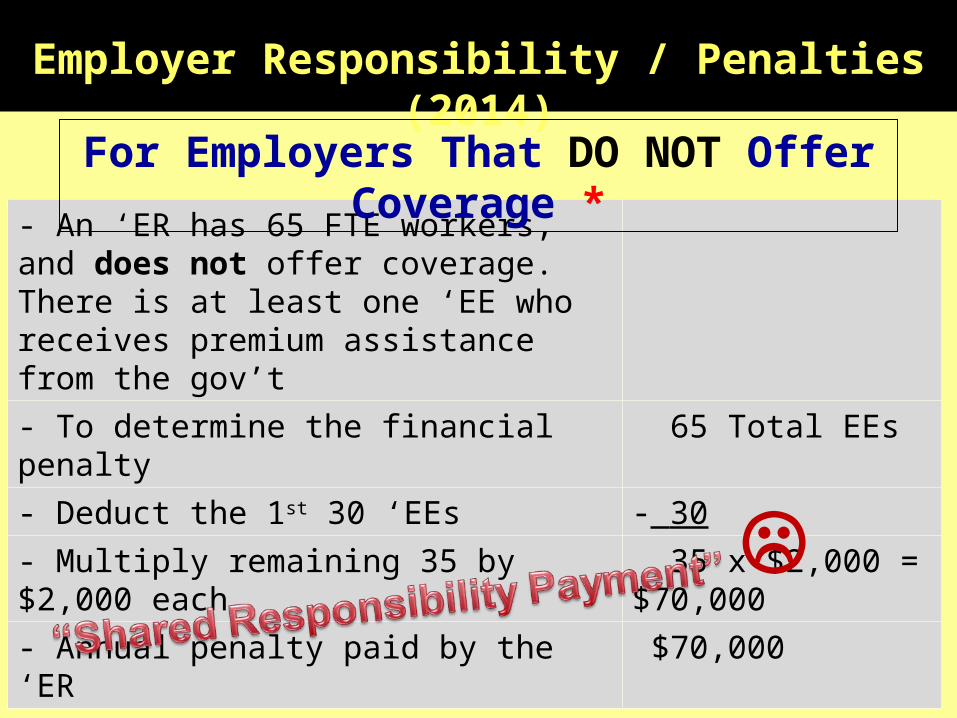

Possible financial penalties for an ‘ERs that DOES NOT

offer coverage *

- If ANY FTE receives premium assistance (due to FPL) from

the government (and through the Exchange) the ‘ER will

face an annual fee of $2,000 imposed on every full-time

‘EE (excluding the 1st 30 ‘EEs). Penalties are pro-rated

monthly.

- EXAMPLE …

Employer Responsibility / Penalties (2014)

- An ‘ER has 65 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t- To determine the financial penalty 65 Total EEs- Deduct the 1st 30 ‘EEs - 30- Multiply remaining 35 by $2,000 each 35 x $2,000 = $70,000 - Annual penalty paid by the ‘ER $70,000

For Employers That DO NOT Offer Coverage *

Employer Responsibility / Penalties (2014)

Possible financial penalties for an ‘ERs that DOES offer

coverage *

- If ANY FTE receives premium assistance (due to FPL) from

the government (and through the Exchange) the ‘ER will

face an annual fee of the lesser of $2,000 imposed on every

full-time ‘EE (excluding the 1st 30 ‘EEs), OR $3,000 for each

FTE that receives a premium subsidy. Penalties are pro-

rated monthly.

- EXAMPLE …

Employer Responsibility / Penalties (2014)

- An ‘ER has 65 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government- To determine the financial penalty 65 Total EEs- Deduct the 1st 30 ‘EEs - 30- Multiply remaining 35 ‘EEs by $2,000 each 35 x $2,000 = $70,000 - Penalty paid by the ‘ER $70,000 - OR - 15 ‘EEs receiving premium asst x $3,000 $45,000 - ‘ER assessed penalty – lesser of the two $45,000

For Employers That DO Offer Coverage *

Employer Responsibility / Penalties (2014)

Joe’s Burgers & Shakes *- 3 locations

- 40 FTEs

- 20 PTEs

20 PTEs at 24 hrs per week (1920 hrs / month)

1920 ÷ 120 = 16 PTEs + 40 FTEs =

- Joe is now considered a “LARGE EMPLOYER”

20 PTE x 24 hrs x 4 = 1920 hrs / 120 (minimum FTE work hrs in

a calendar month) = 16 EEs

56

Employer Responsibility / Penalties (2014)

- ‘ER has 40 FTE workers, and does not offer coverage. There is at least one ‘EE who receives premium assistance from the gov’t- To determine the financial penalty 40 Total EEs- Deduct the 1st 30 ‘EEs - 30- Multiply remaining 10 by $2,000 each 10 x $2,000 = $20,000 - Annual penalty paid by the ‘ER $20,000

Joe’s Burgers & Shakes – Coverage NOT Offered

Employer Responsibility / Penalties (2014)

- ‘ER has 40 FTE workers, and does offer coverage. There are 15 ‘EE who receives premium assistance from the government- To determine the financial penalty 40 Total EEs- Deduct the 1st 30 ‘EEs - 30- Multiply remaining 10 ‘EEs by $2,000 each 10 x $2,000 = $20,000 - Penalty paid by the ‘ER $20,000 - OR - 15 ‘EEs receiving premium asst x $3,000 $45,000 - ‘ER assessed penalty – lesser of the two $20,000

Joe’s Burgers & Shakes – Coverage IS Offered

Employer Responsibility / Penalties (2014)

How Do Employers Determine Full-Time Status?

Google: Towers Watson health care bulletin 7943

- Guidance on Safe-Harbor methods to

determine Full-Time Employee status

- Variable-Hour employees

- Seasonal Employees

Employer Responsibility / Penalties (2014)

Consider this Potential Scenario for the Uninformed Business Owner in 2014 (Delayed until 2015)

Mountain Top Resort - Golf Course, Lodge & Spa

- 49 FETs

- Provides NO Qualified Health Plan to its EEs

- So … it pays no ACA “shared responsibility payment”

- But business improves … so, they hire a new FTE (#50)

for the entire year. Look what it will cost as

mandated by the ACA if only ONE FTE receives a

subsidy:

- $2,000 x 20 (50 – 30) = $40,000

Employer Responsibility / Penalties (2014)

FPL and how it will work in 2014 (and later)

- Premium assistance for those individuals earning less

than 400% of FPL. Currently (2013 numbers), this is

income at $45,980 for an individual and $94,200 for a

family of four.

- The premium assistance will INCREASE to eligible

individuals / families as the percentage of FPL goes

DOWN.

The CBO’s estimates of the average individual subsidy: 05/2010 was $3,970; 10/2012 was revised to $4,780;

02/2013 was revised to now be $5,510

Employer Responsibility / Penalties (2014)

In terms of calculating potential penalties, part-time

employees (and their hours) are only used to see if an

employer is a “large employer”.

- Penalties (if any) are ONLY calculated on FTEs

- No penalties on part-time employee, even if that part-time

employee received Premium Assistance.

- If no FTE receives Premium Assistance (only part-time)

the employer will have no possibility of a penalty.

Employer Responsibility / Penalties (2014)

In 2014, Employers (50 + FTE) must decide … *

- Whether to offer medical coverage or potentially face a

financial penalty;

- If coverage is provided to employees … is it considered

“affordable” enough to avoid a potential financial penalty?

NOTE: The FPL issue is actually a multiple part question / test: 1) Is the ‘EE under 400% FPL?; 2) Does

the ‘ER provide a plan that pays least 60% of the health expenses (for the typical population); 3) Is the ‘EEs required premium contribution “unaffordable” -

meaning …does it exceed 9.5%* of the employee’s income for self-only coverage?

QHP Premium Paid by the Employee – Is It Affordable?- Sarah’s annual salary is $40,000. Her husband’s salary with

another ‘ER is also $40,000. They have two children under age 18. They would be eligible for premium assistance

due to the FPL rule. Sarah’s ‘ER provides her a QHP. - Sarah’s QHP covers all family members. The annual cost of

the self-only portion is $4,800 annually ($400 per month).

- The ‘ER pays 90% of Sarah’s premium ($360 per month) and Sarah pays the remaining 10% ($40 per month). She pays 100% of the family member’s premium.

- 9.5% of Sarah’s annual income (40,000 x 9.5%) is $3,800. That works out to be $316.66 per month. Thus the ‘EE

required premium is considered “affordable”. Sarah is NOT eligible for any premium assistance.

Employer Responsibility / Penalties (2014)

Percent of Federal Poverty Level in 2012

Maximum Premium As a % of Income in 2014

133% 2.00%133.01% 3.00%

150% 4.00%200% 6.30%250% 8.05%300% 9.50%400% 9.50%

Maximum Premium Payment Under ACA

Jimmy – Bartender for Beach Grill (has 15 EEs)

Jimmy is single - his W-2 shows $34,000 (@300% FPL)

Scenario #1 - Beach Grill provides NO QHP Jimmy can go to the Marketplace and apply for a subsidy and select the plan he desires. He will pay the balance of the un-subsidized premium. Beach Grill will have no ACA penalty placed on them for not providing a QHP.

Jimmy – Bartender for Beach Grill (has 15 EEs)

Jimmy is single - his W-2 shows $34,000 (@300% FPL)

Scenario #2 - Beach Grill provides a plan of health that is classified as a ‘Mini-Med’

($50,000 annual limits) This plan of insurance is NOT a QHP. Jimmy can go to the Marketplace and apply for a subsidy and select the plan he desires. He will pay the balance of the un-subsidized premium. Beach Grill will have no ACA penalty placed on them for not providing a QHP.

Jimmy – Bartender for Beach Grill (has 15 EEs)

Jimmy is single - his W-2 shows $34,000 (@300% FPL)

Scenario #3 – ER provides a Bronze Plan (QHP) and pays 70% of Jimmy’s premium. What Jimmy has to pay works to be 15% of his income. Jimmy’s premium is ‘unaffordable’. He can go to the Marketplace and apply for a subsidy and select the plan he desires. He will pay the balance of the un-subsidized premium. Beach Grill will have no ACA penalty placed on them when Jimmy receives a subsidy.

Jimmy – Bartender for Beach Grill (has 15 EEs)

Jimmy is single - his W-2 shows $34,000 (@300% FPL)

Scenario #4 – Beach Grill provides a Bronze Plan (QHP) and pays 90% of Jimmy’s premium. What Jimmy has to pay works to be 8% of his income. But Jimmy wants a Gold plan… one that will pay more of covered claims.

The premium is considered ‘affordable’. Jimmy is NOT eligible for a subsidy since the employer’s plan is both a QHP and is ‘affordable’. If he wants a broader plan he will pay the FULL cost. Beach Grill will have no ACA penalty - even if they were to have 50+ EEs.

Health Reform Implementation Timeline

Individual and Employer Requirements

Insurance Reforms

2014

Key Provisions of Insurance Reform (2014)

Create state-based Health Benefit Exchanges

(Marketplace) & SHOP

QUESTIONS:

What is an Exchange?

Who will operate it?

What will it physically look like?

What if a state says “NO”? (which 27 states – including North Carolina – have done so)

States Health Insurance Marketplace Decisions, May 10, 2013

Partnership Marketplace (7 states)

State-based Marketplace (16 states and DC)

Federally-facilitated Marketplace (27 states)

WA

OR

WY

UT*

TX

SD

OK

ND

NM

NV NE

MT

LA

KS

ID

HI

CO CA

ARAZ

AK

WI

WV VA

TN SC

OH

NCMO

MS

MN

MI

KY

IA

IN IL

GA

FL

AL

VT

PA

NY

NJ

NHMA

ME

CT

DE

RI

MD

DC

* In Utah, the federal government will run the marketplace for individuals while the state will run the small business, or SHOP, marketplace.

Health Insurance Marketplace (2014)

Goal of PPACA: 1) provide health care to millions of

uninsured Americans, and, 2) making that coverage

more affordable.

- Introduce managed retail competition into the

marketplace and encourage better pricing and

quality coverage

- Easier “comparison” shopping

- Offer choices in standard benefit plans and levels of

coverage

- Clear communication regarding plans and rates

PPACA – Four Levels (“Tiers”) of Coverage:Plan Level Percent of Average

Medical Cost CoveredConsumer Cost-

Sharing

Platinum 90% 10%

Gold 80% 20%

Silver 70% 30%

Bronze 60% 40%

Note: Insurance carriers can sell in or out of the Marketplace. The PPACA will allow states the option to require additional “state specific mandates”. Additionally, insurance carriers (and agents) may find a niche sales area in the FSA, supplemental accident, critical illness, or similar products.

Health Insurance Marketplace (2014)

http://www.zanebenefits.com/blog/bid/315824/North-Carolina-Health-Insurance-Exchange-Update-Health-Plan-Rates-Preview

Only three insurance carriers, Blue Cross Blue Shield, Coventry and FirstCarolinaCare Insurance Co. in Pinehurst, will participate in the individual exchange for 2014.

http://www.forbes.com/sites/theapothecary/2013/09/25/double-down-obamacare-will-increase-avg-individual-market-insurance-premiums-by-99-for-men-62-for-women/

Tax “Dumpster” (Subsidy)

Exchange / Marketplace(State or Federal)

Application (on-line or paper)

Social Security

Homeland Security

Internal Rev Service

After Approval – Selects Ins Company and Medal Plan

Subsidy $$ Goes to

Insurance Company

Applicant Pays

Balance of Premium

USA Today family glitch

Applying For, Renewals and Making Changes - ACA

Applying for and Renewal – including new and revised

subsidy- Oct 1st and then for approximately three month

each year

What about changes during the calendar year?- Only for special events:

M - MarriageA - AdoptionD - Death

M - MaternityD - Divorce

Health Insurance Marketplace (2014)

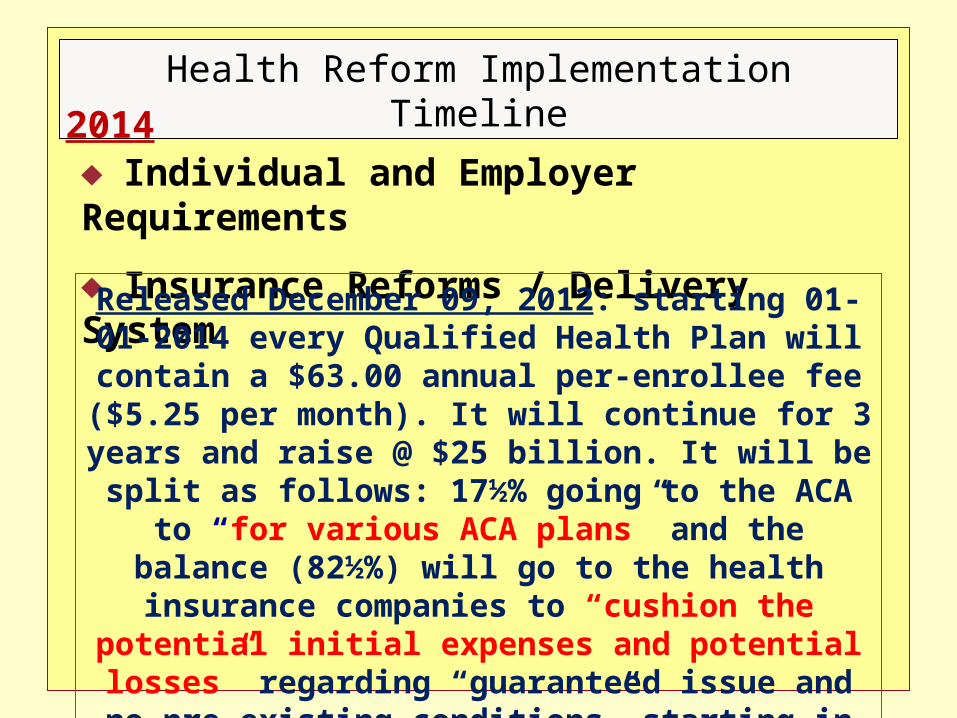

Health Reform Implementation Timeline

Individual and Employer Requirements

Insurance Reforms / Delivery System

2014

Released December 09, 2012: starting 01-01-2014 every Qualified Health Plan will contain a $63.00 annual per-enrollee fee ($5.25 per month). It will

continue for 3 years and raise @ $25 billion. It will be split as follows: 17½% going to the ACA to “for various ACA plans” and the balance (82½%) will go to the health insurance companies to “cushion the

potential initial expenses and potential losses” regarding “guaranteed issue and no-pre-existing

conditions” starting in 2014.

Google: PPACA transitional reinsurance fee crawford

The 2014 Transitional Reinsurance Fee in Action …- 176 ‘EEs (‘ER currently pay 80% of premium for ‘EE only)- 164 Individuals covered- 103 Spouses- 109 Dependents- 476 Total covered “heads” (2.7 “covered heads” per ‘EE)- 11 COBRA QB & 9 retirees = 496 total “heads”- $63 x 496 = $31,248

- $31,000 … plus renewal premium that everyone feels will increase in 2014 over 2013 levels!

Key Provisions of Insurance Reform (2014)

Create state-based Health Benefit Marketplaces

Require Guaranteed Issue and Guaranteed Renewable

plans in the individual, small groups and Marketplaces

- Premiums / rates must follow required thresholds

concerning ages (3 to 1 limit), rating area, family

composition and tobacco use * (max ratio: 1.5 to 1).

Note: No FPL subsidy is allowed for the tobacco surcharge portion on individual plans. Nor is it eligible for a group coverage participation UNLESS they enroll in a “smoking / tobacco cessation program”.

How Might Tobacco Use Impact Your Health Insurance Premiums and Potential Subsidy in 2014 and Beyond? *

- Consider this possibility: (assuming Nat Avg Prem - @$14,000)

- Husband & wife (no dependants) / $100,000 annual

income … thus, NOT eligible for a premium subsidy

- Both are tobacco users and their health insurance

carrier uses the maximum allowable surcharge (1.5)

- $14,000 x 1.5 = $21,000

- Options: 1) Pay the premium; 2) Shop the Marketplace

for a better deal; 3) forgo the insurance and pay the

annual penalty ($1,000) – But They Risk Bankruptcy!

The ACA and Tobacco Rating*

The tobacco surcharge rating can be “state-specific” (Meaning: YES; NO; Percentage less than 1.5) A carrier may charge less than 1.5 – some have announced there will be no tobacco rating Tobacco usage is defined in terms of regular usage and time last used: average of 4+ in a week / within the last 6 months An interesting fact: there are no provisions, questions

nor surcharge regarding the usage of marijuana, cocaine, etc.

“Coverage Requirements” (2014)

… will be included in ALL PLANS …- various government-sponsored programs- eligible employer-sponsored plans - plans in the individual market- grandfathered group health plans- others (as recognized by HHS)

So… who has to comply with the ACA? All for-profits companies, all non-profits (churches, universities, schools, etc.), governmental entities (state, local, municipalities, etc.), and, of course, individuals. Basically, NO one is exempt!

“Coverage Requirements” (2014)

Coverage must include benefits for: 1)Ambulatory patient services; 2)emergency services; 3)hospitalization; 4)maternity and newborn care; 5)mental health and substance use disorder services, including behavioral health treatment;6)prescription drugs; 7)rehabilitative services and devices; 8)laboratory services; 9)preventive/ wellness/ disease management; 10)pediatric services, including oral and vision care.

“Coverage Requirements” (2014) Coverage will be required to be maintained by all individuals, with EXCEPTION:

- religious objections, - financial hardships, - undocumented immigrants, - American Indians, - those incarcerated, - citizens not residing in the U.S., - people earning under the tax-filing threshold, and,--

those with short gaps in coverage

“Coverage Requirements” (2014)

Recently announced by HHS: If an Employer provides a QHP for its employees, it must also make available:

… but the employer is NOT required to make any contribution toward the dependant coverage

Health Reform Implementation Timeline

Individual and Employer Requirements

Insurance Reforms

Premium Subsidies

2014

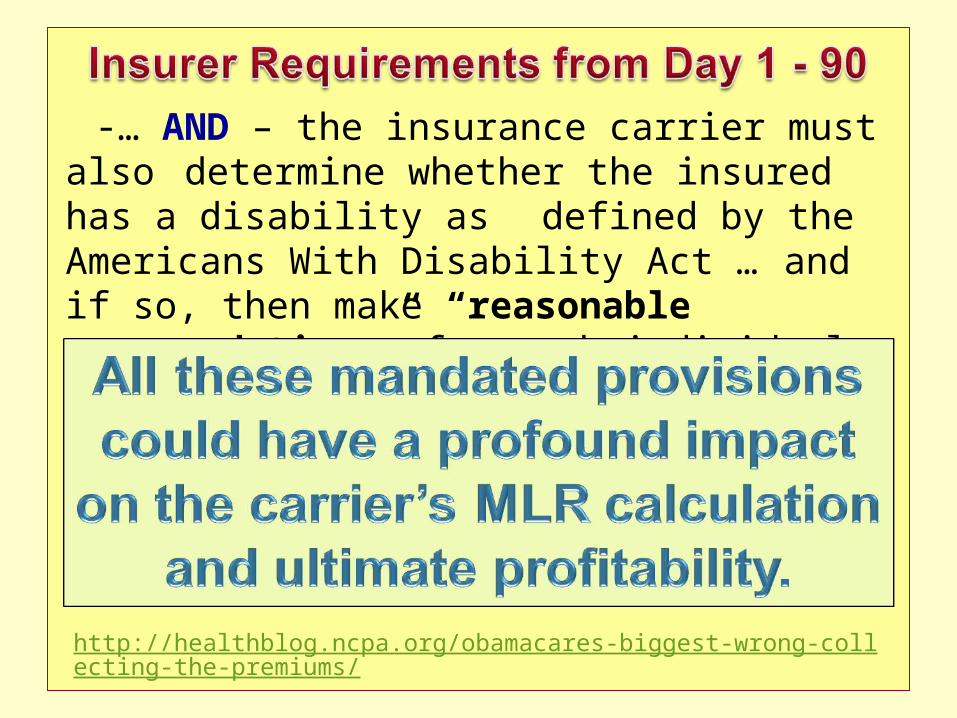

NOTE: As of January 1, 2014 … an individual / family that receive an ACA subsidy (Exchange) will have a 90 DAY grace period for premium payments! For non-subsidy contracts, it will be 30 days.

-Continue coverage – Insurer covers for 1st 30

- Notify HHS of non-payment

-Notify providers of the possibility of denied claims during 2nd and 3rd months (providers on the hook!)

-Notify the insured he / she is delinquent

- Continue to collect the advanced tax credit on behalf of the policyholder (in case they catch-up premiums!)

-Return the tax credit for the 2nd and 3rd month to the Treasury Department (if insured fails to pay)

-Issue a termination notice at end of grace period

-… AND – the insurance carrier must also determine whether the insured has a

disability as defined by the Americans With Disability Act … and if so, then make “reasonable accommodations” for such individuals.

http://healthblog.ncpa.org/obamacares-biggest-wrong-collecting-the-premiums/

Mom & Dad, Inc. – 60 ‘EEs in 2013

Mom, Inc – 30 ‘EEs in 2014

Dad, Inc – 30 ‘EEs in 2014

Be VERY Careful! Potential HEAVY penalties under ACA!!

Employer Responsibility / Penalties (2014)

So … Let’s Review – Potential Employer Penalty

Under 50 FTEs 50+ FTEs - No QHP 50+ FTEs – Provides QHP- No chance of ANY penalty- Chance of a tax credit for certain size groups

- One FTE receives FPL subsidy through the Marketplace and ‘ER will have a $2,000 annual penalty on ALL FTEs, excluding the first 30 ‘EEs. Penalty pro-rated monthly. *

- Same rule as to the left, but penalty is the lesser of:-1) Did ‘EE receive FPL subsidy? 2) Is the plan broad enough (60%)? 3) Is ‘EEs required portion of premium for QHP deemed “unafford-able”? If fail on any*, $3,000 for EACH qualifying ‘EE. *

EXAMPLE: 100 ‘EEs. 30 qualifies. 30 x 3,000 = $90,000 (or lesser of table to left).* - Exceptions apply

EXAMPLE: 100 ‘EEs. One ‘EE receives a subsidy. 100 – 30 = 70 x $2,000 = $140,000 (“Shared Responsibility Payment” … which is not deductible)

Employer Incentives / Penalties (2014)

In 2014 will be a critical year for Employers as it relates

to National Health Care Reform

- Certain tax incentives will be in place for a business that

has 25 or fewer FTEs (tax incentives will vary depending

on “average income”)

- Potential penalties will exist for a business that has 50 or

more FTEs

- At present there are no tax incentives nor potential

penalties for a business that has 26 to 49 FTEs

Are Changes Ahead for the ACA?

Various components of the ACA has been challenged in several courts. SCOTUS ruled

(June 28, 2012) that the “individual mandate” is constitutional. There are still a few

challenges in the courts regarding various components of the law. But the Presidential election has settled the issue regarding the

law’s implementation.

- Affordable Care Act Update-

THANK YOU FOR YOUR THANK YOU FOR YOUR ATTENDANCEATTENDANCE

Jerry Rhinehart, CIC, CLU, ChFC, RHUJerry Rhinehart, CIC, CLU, ChFC, RHUPanama City, FLPanama City, FL