africa’s leading independent oil...

TRANSCRIPT

First Energy Global Energy Conference 2015 Tullow Oil plc

Angus McCoss – Exploration Director First Energy Global Energy Conference– 22nd September 2015

AFRICA’S LEADING INDEPENDENT OIL COMPANY

First Energy Global Energy Conference 2015

This presentation contains certain forward-looking statements that are subject to the usual risk factors and uncertainties associated with the oil and gas exploration and production business.

Whilst Tullow believes the expectations reflected herein to be reasonable in light of the information available to them at this time, the actual outcome may be materially different owing to factors beyond the Group’s control or within the Group’s control where, for example, the Group decides on a change of plan or strategy.

The Group undertakes no obligation to revise any such forward-looking statements to reflect any changes in the Group’s expectations or any change in circumstances, events or the Group’s plans and strategy. Accordingly no reliance may be placed on the figures contained in such forward looking statements.

Disclaimer

Slide 2

First Energy Global Energy Conference 2015

FIRST ENERGY GLOBAL ENERGY CONFERENCE 2015

First Energy Global Energy Conference 2015

Business re-set for $50 oil price environment

Slide 4

1H 2015 financials in line with expectations

Funding in place with significant liquidity & headroom

Growing high margin cash flow underpinned by hedging

Major projects on schedule and on budget

Major cost cutting completed

First Energy Global Energy Conference 2015

FIRST ENERGY GLOBAL ENERGY CONFERENCE 2015

First Energy Global Energy Conference 2015

Financing Strategy

Slide 6

• Proactive measures already taken to manage business in a low oil price environment

• Quality assets and hedging programmes have allowed us financial flexibility and headroom;

• Financial strategy going forwards to significantly deleverage company beyond benefit from TEN production:

- Continued focus on high margin production and active hedging, cost and capital management

- Active portfolio management and farmdown activity

- Management of East Africa development capex

- Target Net Debt / EBITDAX <2X

De-leveraging will create capacity to reinstate the dividend and increase exploration capital expenditure up to $400 million per annum

First Energy Global Energy Conference 2015

2015 capital expenditure

Slide 7

$1.9 billion capex for full year 2015

• Ghana: Jubilee & TEN developments - $1,210m

• Other West Africa: Non-op production - $190m

• Europe: Maintaining mature production - $25m

• Uganda and Kenya: Pre-development activities

supporting FID - $225m

• Kenya: Exploration & appraisal drilling - $100m

• New Ventures exploration activities - $150m

1H 2015 capital split:

$521m

West Africa

$186m

East Africa

$76m

New Ventures

Notes: i) 2013 Capital Expenditure excludes the Spring acquisition expenditure ii) 2013, 2014 & 2015 Exploration expenditure is net of Norwegian tax refund

0 500 1,000 1,500 2,000 2,500

2012

2013

2014

2015

$2,020m

$1,800m

$1,870m

Development & Operations Exploration & Appraisal

$1,900m

1H 2015 $783m

$250m $1,650m

$800m $1,220m

$990m $810m

$1,060m $810m

2016 Capex guidance: $1.2 to $1.4 billion

First Energy Global Energy Conference 2015

$m Commitment size Maturity

RBL 3,700 Oct 2019

Corporate Facility 1,000 Apr 2017

6% Senior Notes 650 Nov 2020

6¼% Senior Notes 650 Apr 2022

EFF 1 ~280 Dec 2018

(1) Norwegian Exploration Finance Facility, NOK2.25bn (2) Final maturity; RBL amortises linearly from October 2016 – 2019

$m 30 June 2015 31 Dec 2014

Cash and cash equivalents 488 319

Debt outstanding

RBL Facilities 2,634 1,987

EFF 1 164 135

Corporate Facility - -

Senior Notes 1,300 1,300

Total debt 4,098 3,422

Net debt 3,610 3,103

Facility headroom plus free cash 2,348 2,381

Debt maturity profile Key metrics

EFF1

$m

1H 2015 Financing Initiatives

• Liquidity: $450m increase in bank facilities

• RBL: draw capacity maintained

• Financial covenant: relaxed

164

2,634

650 650 1,000

0

1,000

2,000

3,000

4,000

2017 2018 2019 2020 2021 2022

Strong liquidity position through TEN first oil

Slide 8

~$2.3bn of facility headroom plus free cash end 1H 2015; Expect ~$1bn debt facility headroom mid-2016

Senior Notes

RBL2 3,700

Corporate Facility Senior

Notes

Facility headroom

Drawings

First Energy Global Energy Conference 2015

Hedge strategy • Hedge strategy is approved by the Board and reviewed quarterly

• Hedges are executed rateably on a three year forward rolling basis

• Hedge by purchasing a mix of Dated Brent options (puts, collars, 3-way collars)

Current Portfolio • Approximately 60% of 2015 oil entitlement volumes is hedged at ~$86/bbl

• MTM as at 30 June ~$0.3bn

Oil Hedging

Hedge Position (as at 30 June 2015) 2H 2015 2016 2017 2018

Oil Volume (bopd) 34,500 31,257 19,500 5,000

Average floor price protected ($/bbl) 85.98 79.29 76.68 68.04

MTM value at 30 June 2015 ($m)* 111.0 130.1 57.7 -1.2

The hedging programme has helped to significantly mitigate the impact of lower oil prices; $146m benefit to 1H 2015 revenues with ~$300m mark-to-market value looking forwards

Slide 9

*Net of hedge premium

First Energy Global Energy Conference 2015

FIRST ENERGY GLOBAL ENERGY CONFERENCE 2015

First Energy Global Energy Conference 2015

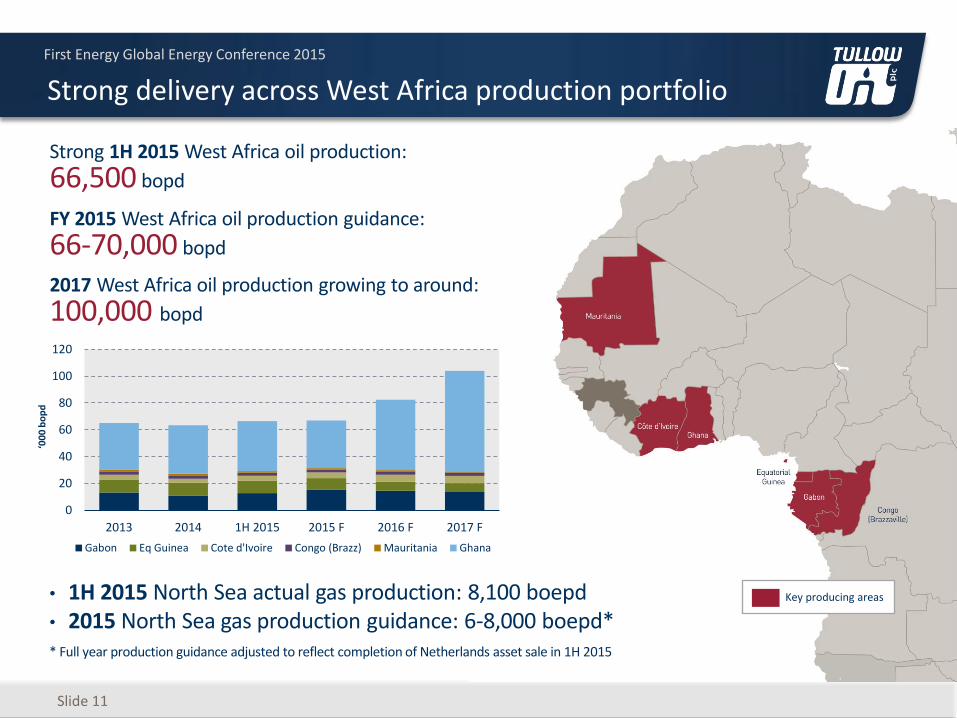

Strong delivery across West Africa production portfolio

Slide 11

• 1H 2015 North Sea actual gas production: 8,100 boepd • 2015 North Sea gas production guidance: 6-8,000 boepd* * Full year production guidance adjusted to reflect completion of Netherlands asset sale in 1H 2015

‘00

0 b

op

d

0

20

40

60

80

100

120

2013 2014 1H 2015 2015 F 2016 F 2017 F

Gabon Eq Guinea Cote d'Ivoire Congo (Brazz) Mauritania Ghana

Strong 1H 2015 West Africa oil production:

66,500 bopd

FY 2015 West Africa oil production guidance:

66-70,000 bopd

Key producing areas

2017 West Africa oil production growing to around:

100,000 bopd

First Energy Global Energy Conference 2015

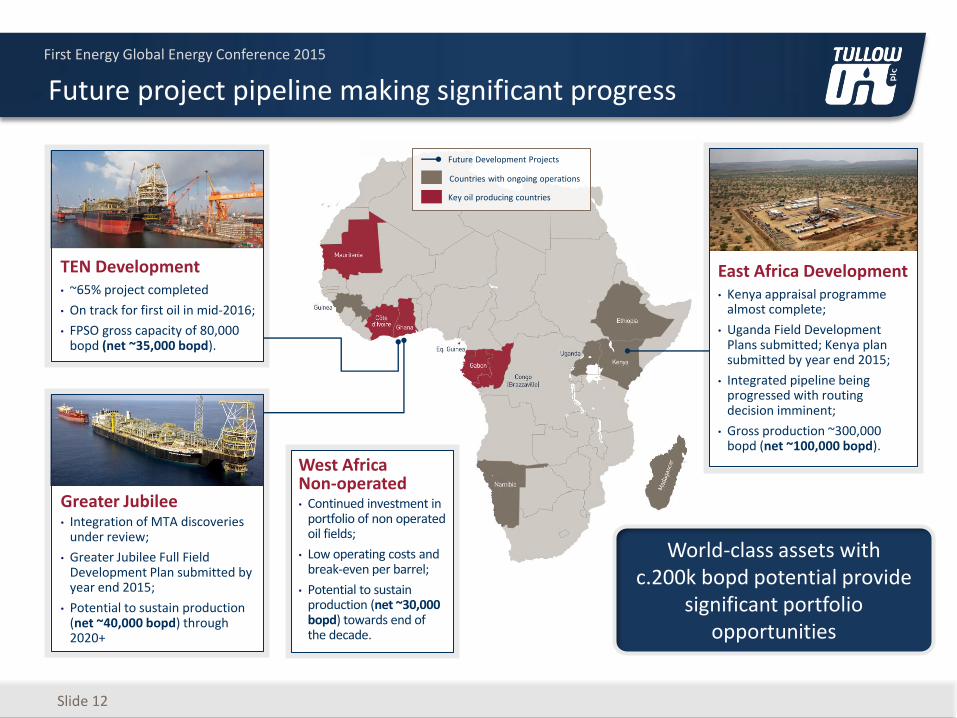

Future project pipeline making significant progress

Slide 12

Countries with ongoing operations

Key oil producing countries

Future Development Projects

World-class assets with c.200k bopd potential provide

significant portfolio opportunities

East Africa Development • Kenya appraisal programme

almost complete;

• Uganda Field Development Plans submitted; Kenya plan submitted by year end 2015;

• Integrated pipeline being progressed with routing decision imminent;

• Gross production ~300,000 bopd (net ~100,000 bopd).

TEN Development • ~65% project completed

• On track for first oil in mid-2016;

• FPSO gross capacity of 80,000 bopd (net ~35,000 bopd).

Greater Jubilee • Integration of MTA discoveries

under review;

• Greater Jubilee Full Field Development Plan submitted by year end 2015;

• Potential to sustain production (net ~40,000 bopd) through 2020+

West Africa Non-operated • Continued investment in

portfolio of non operated oil fields;

• Low operating costs and break-even per barrel;

• Potential to sustain production (net ~30,000 bopd) towards end of the decade.

First Energy Global Energy Conference 2015

Slide 13

Strong Jubilee performance year-to-date • 1H15 average gross production: 105 kbopd

• FY15 guidance: 100 kbopd; impacted by short term gas compression issue

• Gas export averaging c.80mmscfd since commissioning

• Reduced gas injection allowing FPSO capacity to rise to ~115kbopd

Strong focus on cost management • 1H15 opex per barrel: $10.9/bbl

• On-track to meet FY15 target: <$10/bbl

• TEN provides opportunity to further reduce Ghana opex/bbl

Future investment opportunities • Additional infill well being drilled this year in JUA

• Greater Jubilee Development Plan submission by end 2015

- Optimal integration of MTA discoveries under review

- Long term infill drilling plans to extend production plateau

- Reviewing options to expand FPSO capacity

Jubilee development options present growth opportunities

First Energy Global Energy Conference 2015

TEN project on schedule and on budget for first oil mid-2016

Slide 14

DRILLING

Project c.65% complete

• FPSO Conversion (92%)

- All major installation work complete

- On track for sailaway around year-end

- Field installation completion 2Q15

• Subsea Fabrication (95%) & Installation (45%)

- All major fabrication complete

- Subsea installation campaign underway

- Optimisation of program to first oil underway

• Drilling (100%) and Completions (25%)

- All eleven start-up wells drilled

- 2 of 10 well completions installed, third underway

Plateau production targeted early 2017

TEN Gross Development Capex US$bn

-

0.5

1.0

1.5

2.0

2013 2014 2015 2016 2017 2018 2019

First Energy Global Energy Conference 2015

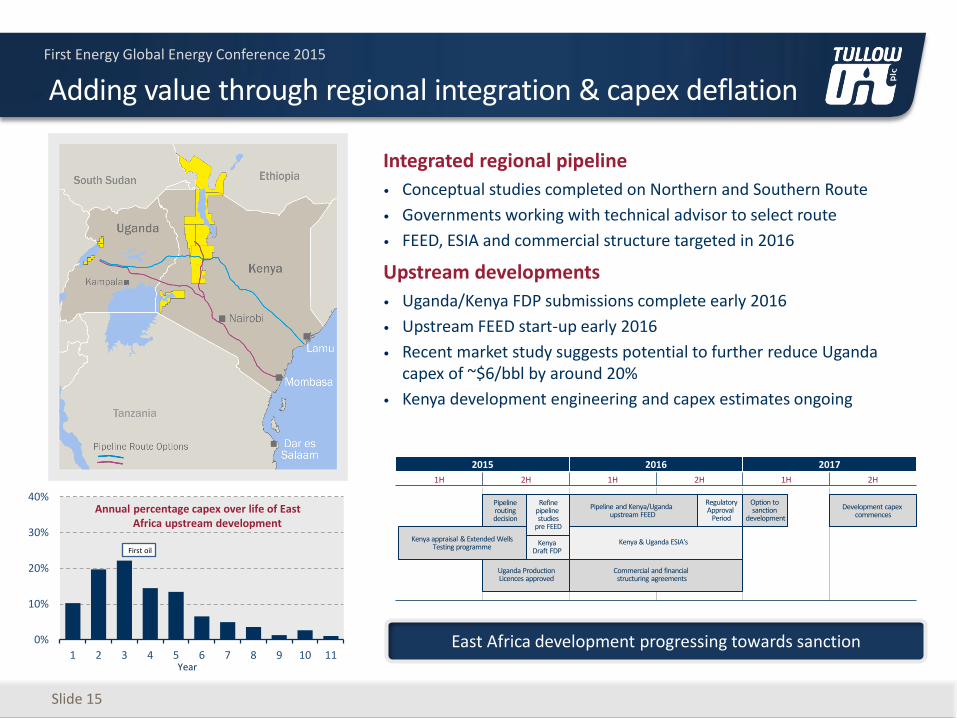

Integrated regional pipeline

• Conceptual studies completed on Northern and Southern Route

• Governments working with technical advisor to select route

• FEED, ESIA and commercial structure targeted in 2016

Upstream developments

• Uganda/Kenya FDP submissions complete early 2016

• Upstream FEED start-up early 2016

• Recent market study suggests potential to further reduce Uganda capex of ~$6/bbl by around 20%

• Kenya development engineering and capex estimates ongoing

0%

10%

20%

30%

40%

1 2 3 4 5 6 7 8 9 10 11

First oil

Slide 15

Adding value through regional integration & capex deflation

Annual percentage capex over life of East Africa upstream development

Year

2015 2016 2017

1H 2H 1H 2H 1H 2H

Pipeline routing decision

Refine pipeline studies

pre FEED

Pipeline and Kenya/Uganda upstream FEED

Regulatory Approval

Period

Option to sanction

development

Development capex commences

Kenya appraisal & Extended Wells Testing programme

Kenya Draft FDP

Uganda Production Licences approved

Commercial and financial structuring agreements

East Africa development progressing towards sanction

Kenya & Uganda ESIA's

First Energy Global Energy Conference 2015

FIRST ENERGY CAPITAL CONFERENCE 2015

First Energy Global Energy Conference 2015

Adapting our E&A strategy to current environment

Slide 17

Adapted to mitigate risks & expense • Reduce cost exposure: Farm-out early to spread risk & earn carries

• Revised risk screening: High-grade exploration programmes to tougher decision thresholds

• Avoid complex wells: Target normally pressured oil plays in onshore & simple offshore settings

• Focused human resources: Deploy Geoscientists to portfolio rejuvenation & oil field development

Consistent long-term focus on high-impact exploration portfolio

• Conventional Light Oil: materially-valuable ‘core play’ campaigns using cost-effective technologies

• Africa & Atlantic: in-house geological experience & strong above-ground relationships

• Infrastructure-led exploration: building on our West Africa & East Africa hubs

• Finding the next hub: frontier new ventures to open new plays or basins

Investing for our future: drill high-graded ‘trigger wells’ & replenish portfolio with new ventures

First Energy Global Energy Conference 2015

Finding oil onshore East Africa

Slide 18

Location Activity

Uganda

Lake Albert Basin

• 17+ oil fields discovered (90% success)

• 1.7 billion barrels of oil discovered

Kenya

South Lokichar Basin

• 9/11 wildcat oil discoveries

• + 2 technical discoveries (tight oil plays)

• Discovered 600 mmbo resources (Pmean)

• New plays & prospects to be tested

Kerio Basin • Basin margin play unsuccessful at Kodos-1

• Epir-1 established a working petroleum system

• Independent plays in main basin untested

North Turkana Basin

• Basin margin play unsuccessful at Engomo-1

• Independent plays away from basin margin untested

Ethiopia

Omo Basin • Working petroleum system seen (oil shows)

Chew Bahir Basin

• Dry hole – Reviewing potential away from volcanics

Exciting basin & new play testing wildcats

Several undrilled basins being tested Q3 2015 to end 2016 • Cheptuket (Kerio Valley Basin), Tausi (North Lokichar Basin)

First Energy Global Energy Conference 2015

Q&A FIRST ENERGY GLOBAL ENERGY CONFERENCE 2015

First Energy Global Energy Conference 2015

Tullow Oil plc 9 Chiswick Park

566 Chiswick High Road London, W4 5XT United Kingdom

Tel: +44 (0)20 3249 9000 Fax: +44 (0)20 3249 8801

Email: [email protected]

Follow Tullow on: