akuntansi keuangan lanjutan 1 2018 - spa feb ui · akuntansi keuangan lanjutan 1 2018 . chapter 4:...

TRANSCRIPT

AKUNTANSI KEUANGAN LANJUTAN

1 2018

CHAPTER 4: CONSOLIDATION OF WHOLLY-OWNED SUBSIDIARIES ACQUIRED AT

MORE THAN BOOK VALUE

Targaryen Corporation acquired 100 percent ownership of Baratheon Company on January 1, 20X8,

for $128,000. At that date, the fair value of Baratheon Co.’s building and equipment was $20,000

more than book value. Buildings and equipment are depreciated on a 10-year basis. Although

goodwill is not amortized, the management of Targaryen Corp. concluded on December 31, 20X8

that goodwill involved in its acquisition of Baratheon Co. shares has impaired and the correct

carrying value was $2,500. No additional impairment occured in 20X9. Trial balance data for

Targaryen Corp. and Baratheon Co. on December 31, 20X9, are as follows:

Required

a. Give all eliminating entries needed to prepare a three-part consolidation worksheet as of

December 31, 20X9.

b. Prepare a three-part consolidation worksheet for 20X9 in a good form.

Debit Credit Debit Credit

Cash 45,500 32,000

Accounts Receivable 85,000 14,000

Inventory 97,000 24,000

Land 50,000 25,000

Buildings and Equipment 350,000 150,000

Investment in Baratheon Co. Stock 142,500

Cost of Goods Sold 145,000 114,000

Wage Expense 35,000 20,000

Depreciation Expense 25,000 10,000

Interest Expense 12,000 4,000

Other Expenses 23,000 16,000

Dividends Declared 30,000 20,000

Accumulated Depreciation 170,000 50,000

Accounts Payable 51,000 15,000

Wages Payable 14,000 6,000

Notes Payable 150,000 50,000

Common Stock 200,000 60,000

Retained Earnings 131,000 48,000

Sales 290,000 200,000

Income from Subsidiary 34,000

TOTAL 1,040,000 1,040,000 429,000 429,000

ItemTargaryen Corporation Baratheon Company

JAWABAN:

a)

Record Targaryen Corp.’s 100% share of Baratheon Co.’s 20X9 income:

Investment in Baratheon Co. Stock 36,000

Cash 36,000

Record Targaryen Corp.’s 100% share of Baratheon Co.’s 20X9 dividend:

Cash 20,000

Investment in Baratheon Co. Stock 20,000

Record amortization of excess acquisition price:

Income from Subsidiary 2,000

Investment in Baratheon Co. Stock 2,000

Book Value Calculation Total BV C/S R/E

Original BV 108,000 60,000 48,000

+ Net Income 36,000 36,000

- Dividend (20,000) (20,000)

Ending Book Value 124,000 60,000 64,000

Excess Value (Differential)

Calculation

Total BV B&E Acc. Depr. Goodwill

Original BV 20,500 20,000 (2,000) 2,500

Changes (2,000) (2,000)

Ending BV 18,500 20,000 (4,000) 2,500

ELIMINATING ENTRIES

Basic Elimination Entry:

C/S 60,000

R/E 48,000

Income from Subs 36,000

Dividend Declared 20,000

Investment in Baratheon 124,000

Amortized excess value reclassification entry:

Depreciation Exp 2,000

Income from Subs 2,000

Excess value (differential) reclassification entry:

Building & Equipment 20,000

Goodwill 2,500

Acc Depr 4,000

Investment in Baratheon 18,500

b)

Targaryen

Corp.

Baratheon

Co.

Elimination Entries Consolidated

DR CR

Income Statement

Sales 290.000 200.000 490.000

Less: COGS -145.000 -114.000 -259.000

Less: Wage Expense -35.000 -20.000 -55.000

Less: Depreciation Expense -25.000 -10.000 2.000 -37.000

Less: Interest Expense -12.000 -4.000 -16.000

Less: Other Expenses -23.000 -16.000 -39.000

Income from Subsidiary 34.000 36.000 2.000 0

Net Income 84.000 36.000 84.000

Statement of Retained

Earnings

Beginning Balance 131.000 48.000 48.000 131.000

Net Income 84.000 36.000 84.000

Less: Dividends Declared -30.000 -20.000 20.000 -30.000

Ending Balance 185.000 64.000 185.000

Balance Sheet

Cash 45.500 32.000 77.500

Accounts Receivable 85.000 14.000 99.000

Inventory 97.000 24.000 121.000

Land 50.000 25.000 75.000

Buildings & Equipment 350.000 150.000 20.000 520.000

Less: Accumulated

Depreciation -170.000 -50.000 4.000 -224.000

Investment in Baratheon Co. 142.500 124.000

18.500 0

Goodwill 2.500 2.500

Total Assets 600.000 195.000 671.000

Accounts Payable 51.000 15.000 66.000

Wages Payable 14.000 6.000 20.000

Notes Payable 150.000 50.000 200.000

Common Stock 200.000 60.000 60.000 200.000

Retained Earnings 185.000 64.000 185.000

Total Liabilities & Equity 600.000 195.000 168.500 168.500 671.000

CHAPTER 5: CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

ACQUIRED AT MORE THAN BOOK VALUE

Hartanto Corporation acquired 70 percent of Palupi Corporation’s common stock on December

31, 20X4, for $102,200. At that date, the fair value of the non-controlling interest was $43,800.

Data from the balance sheets of the two companies included the following amounts as of the date

of acquisition:

Item Hartanto Corporation Palupi Corporation

Cash $ 50,300 $ 21,000

Accounts Receivable 90,000 44,000

Inventory 130,000 75,000

Land 60,000 30,000

Buildings & Equipment 410,000 250,000

Less: Accumulated Depreciation (150,000) (80,000)

Investment in Palupi Corporation Stock 102,200

Total Assets $692,500 $340,000

Accounts Payable $152,500 $ 35,000

Mortgage Payable 250,000 180,000

Common Stock 80,000 40,000

Retained Earnings 210,000 85,000

Total Liabilities & Stockholders’ Equity $692,500 $340,000

At the date of the business combination, the book values of Palupi’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $81,000, and buildings

and equipment, which had a fair value of $185,000. At December 31, 20X4, Hartanto reported

accounts payable of $12,500 to Palupi, which reported an equal amount in its accounts receivable.

Required

(1). Give the elimination entry or entries needed to prepare a consolidated balance sheet

immediately following the business combination.

(2). Prepare a consolidated balance sheet worksheet.

JAWABAN:

(1)

a. Equity Method Entries on Hartanto Corp.’s Books:

Investment in Palupi Corp. 102,200

Cash 102,200

b. Book Value Calculations

NCI 30% + Hartanto Corp. 70% = Common Stock + Retained Earnings

Ending book value 37,500 87,500 40,000 85,000

c. Basic Elimination Entry:

Common Stock 40,000

Retained Earnings 85,000

Investment in Palupi Corp. 87,500

NCI in NA of Palupi Corp. 37,500

d.

NCI 30% + Hartanto Corp. 70% = Inventory + Buildings & Equipment

Ending book value 6,300 14,700 6,000 15,000

Excess value (differential) reclassification entry:

Inventory 6,000

Buildings & Equipment 15,000

Investment in Palupi Corp. 14,700

NCI in NA of Palupi Corp. 6,300

e. Eliminate intercompany accounts:

Accounts Payable 12,500

Accounts Receivable 12,500

Accumulated Depreciation 80,000

Building & Equipment 80,000

(2). . Elimination Entries

Hartanto Corp. Palupi Corp. DR CR Consolidated

Balance Sheet

Cash 50,300 21,000 86,000

Accounts Receivable 90,000 44,000 12,500 121,500

Inventory 130,000 75,000 6,000 211,000

Land 60,000 30,000 90,000

Buildings & Equipment 410,000 250,000 15,000 80,000 595,000

Less: Acc. Depreciation (150,000) (80,000) 80,000 (150,000)

Investment in Palupi Corp. 102,200 87,500 0

14,700

Total Assets 692,500 340,000 101,000 194,700 938,800

Accounts Payable 152,500 35,000 12,500 175,000

Mortgage Payable 250,000 180,000 430,000

Common Stock 80,000 40,000 40,000 80,000

Retained Earnings 210,000 85,000 85,000 210,000

NCI in NA of Palupi Corp. 37,500 43,800

6,300

Total Liabilities & Equity 692,500 340,000 137,500 43,800 938,800

CHAPTER 6: INTERCOMPANY TRANSACTIONS

Tamaria Corporation holds 60 percent ownership of Anggara Company. Each year, Anggara

purchases large quantities of a gnarl root used in producing health drinks. Anggara purchased

$150,000 of roots in 20X7 and sold $40,000 of these purchases to Tamaria for $60,000. By the

end of 20X7, Tamaria had resold all but $15,000 of its purchase from Anggara. Tamaria

generated $90,000 on the sale of roots to various health stores during the year.

Required:

a. Give the journal entries recorded by Tamaria and Anggara during 20X7 relating to the initial

purchase, intercorporate sale, and resale of gnarl roots.

b. Give the worksheet elimination entries needed as of December 31, 20X7, to remove all

effects of the intercompany transfer in preparing the 20X7 consolidated financial statements.

JAWABAN:

a.

Journal entries recorded by Anggara Company:

(1) Inventory 150,000

Cash (Accounts Payable) 150,000

Record purchases from nonaffiliated.

(2) Cash (Accounts Receivable) 60,000

Sales 60,000

Record sale to Tamaria Corporation.

(3) Cost of Goods Sold 40,000

Inventory 40,000

Record cost of goods sold to Tamaria Corporation.

Journal entries recorded by Tamaria Corporation:

(1) Inventory 60,000

Cash (Accounts Payable) 60,000

Record purchases from Anggara Company.

(2) Cash (Accounts Receivable) 90,000

Sales 90,000

Record sale of items to nonaffiliated.

(3) Cost of Goods Sold 45,000

Inventory 45,000

Record cost of goods sold.

(4) Income from Tamaria 5,000

Investment in Tamaria 5,000

Eliminate unrealized gross profit on inventory purchases from Tamaria.

b. Eliminating entry:

Total = Re-sold + Ending Inventory

Sales 60,000 45,000 15,000

COGS 40,000 30,000 10,000

Gross Profit 20,000 15,000 5,000

Gross Profit % 33.33%

Sales 60,000

Cost of Goods Sold 55,000

Inventory 5,000

Eliminate intercompany sale of inventory.

Debit Credit Debit Credit

Cash 15,850$ 58,000$

Accounts Receivable 65,000$ 70,000$

Interest & Other Receivables 30,000$ 10,000$

Inventory 150,000$ 180,000$

Land 80,000$ 60,000$

Building & Equipment 315,000$ 240,000$

Bond Discount 15,000$

Investment in Salad's Stock 157,630$

COGS 375,000$ 110,000$

Depretiation Expense 25,000$ 10,000$

Interest Expense 24,000$ 33,000$

Other Expense 28,000$ 17,000$

Dividends Declared 30,000$ 5,000$

Accumulated Depretiation 120,000$ 60,000$

Accounts Payable 61,000$ 28,000$

Other Payable 30,000$ 20,000$

Bonds Payable 250,000$ 300,000$

Common Stock 150,000$ 100,000$

APIC 30,000$

Retained Earnings 165,240$ 100,000$

Sales 450,000$ 190,400$

Other Income 28,250$

Gain on sale of equipment 9,600$

Income from Salad 10,990$

Total 1,295,480$ 1,295,480$ 808,000$ 808,000$

SaladPaprika

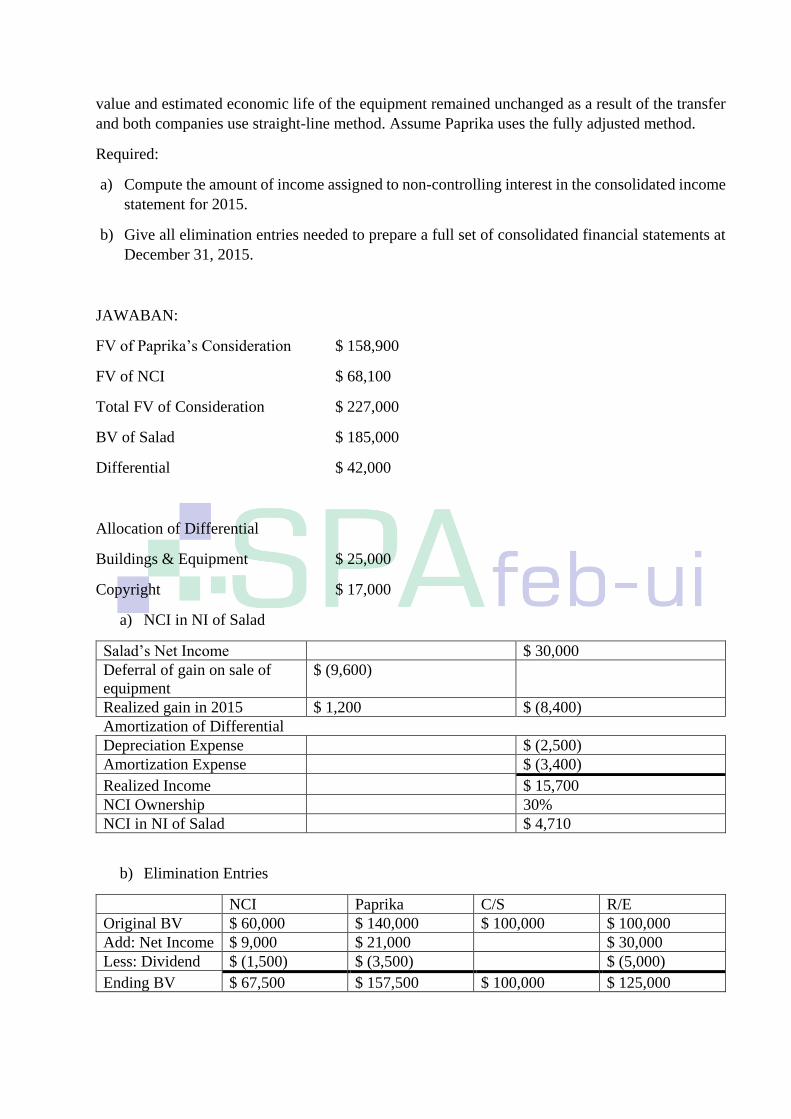

CHAPTER 7: INTERCOMPANY TRANSFER OF NONCURRENT ASSETS & SERVICES

Paprika Corp. acquired 70% of Salad Inc. voting common stock on January 1, 2013, for $158,900.

Salad reported common stock outstanding of $100,000 and retained earnings of $85,000. The fair

value of NCI was $68,100 at the date of acquisition. Buildings and equipment held by Salad had

a fair value $25,000 higher than book value. The remainder of the differential was assigned to a

copyright held by Salad. Buildings and equipment had a 10-year remaining life and copyright had

a 5-year life at the date of acquisition.

Trial balance for Paprika and Salad on December 31, 2015 are as follows:

Paprika sold land it had purchased for $21,000 to Salad on September 20, 2014 for $32,000. Salad

plans to use the land for future plant expansion. On January 1, 2015, Salad sold equipment to

Paprika for $91,600. Salad purchased the equipment on January 1, 2013 for $100,000 and

depreciated it on a 10-year basis, including an estimated residual value of $10,000. The residual

value and estimated economic life of the equipment remained unchanged as a result of the transfer

and both companies use straight-line method. Assume Paprika uses the fully adjusted method.

Required:

a) Compute the amount of income assigned to non-controlling interest in the consolidated income

statement for 2015.

b) Give all elimination entries needed to prepare a full set of consolidated financial statements at

December 31, 2015.

JAWABAN:

FV of Paprika’s Consideration $ 158,900

FV of NCI $ 68,100

Total FV of Consideration $ 227,000

BV of Salad $ 185,000

Differential $ 42,000

Allocation of Differential

Buildings & Equipment $ 25,000

Copyright $ 17,000

a) NCI in NI of Salad

Salad’s Net Income $ 30,000

Deferral of gain on sale of

equipment

$ (9,600)

Realized gain in 2015 $ 1,200 $ (8,400)

Amortization of Differential

Depreciation Expense $ (2,500)

Amortization Expense $ (3,400)

Realized Income $ 15,700

NCI Ownership 30%

NCI in NI of Salad $ 4,710

b) Elimination Entries

NCI Paprika C/S R/E

Original BV $ 60,000 $ 140,000 $ 100,000 $ 100,000

Add: Net Income $ 9,000 $ 21,000 $ 30,000

Less: Dividend $ (1,500) $ (3,500) $ (5,000)

Ending BV $ 67,500 $ 157,500 $ 100,000 $ 125,000

Deferred Gain Calculation

Total Paprika NCI

Upstream sale of asset $ (9.600) $ (6.720) $ (2.880)

Extra Depretiation $ 1.200 $ 840 $ 360

Total $ (8.400) $ (5.880) $ (2.520)

Basic Elimination Entry

C/S $ 100,000

R/E $ 100,000

Income from Salad $ 15,120

NCI in NI of Salad $ 6,480

Dividends Declared $ 5,000

Investment in Salad $ 151,620

NCI in NA of Salad $ 64,980

Differential Calculation

NCI Paprika

Buildings &

Equipment Copyright Acc. Depr

01-Jan-13 $ 12.600 $ 29.400 $ 25.000 $ 17.000

Changes $ (1.770) $ (4.130) $ (3.400) $ (2.500)

01-Jan-14 $ 10.830 $ 25.270 $ 25.000 $ 13.600 $ (2.500)

Changes $ (1.770) $ (4.130) $ (3.400) $ (2.500)

01-Jan-15 $ 9.060 $ 21.140 $ 25.000 $ 10.200 $ (5.000)

Changes $ (1.770) $ (4.130) $ (3.400) $ (2.500)

31-Des-15 $ 7.290 $ 17.010 $ 25.000 $ 6.800 $ (7.500)

Excess Value Reclassification

Buildings & Equipment $ 25,000

Copyright $ 6,800

Acc Depr $ 7,500

Investment in Salad $ 17,010

NCI in NA of Salad $ 7,290

Amortized Excess Value Reclassification

Depreciation Exp $ 2,500

Amortization Exp $ 3,400

Income from Salad $ 4.130

NCI in NI of Salad $ 1,770

Eliminate Gain on Sale of Land

Investment in Salad $ 11,000

Land $11,000

Eliminate Gain on Sale of Equipment

Accumulated Depreciation $ 1,200

Depreciation Expense $ 1,200

Equipment $ 8,400

Gain on Sale of Equipment $ 9,600

Acc Depr $ 18,000