an ebiquity company interim presentation six months to october 2008

Post on 20-Dec-2015

216 views

TRANSCRIPT

an Ebiquity company

Interim Presentation

Six Months to October 2008

2

A company newly positioned to meet the needs of a new age

Welcome to Ebiquity!

1. A new name signals our commitment to data analytics2. A new on-line interface that brings our technology tools and services together into one powerful

program3. An upgraded advertising monitoring service - Billetts Media Monitoring4. A new ‘state of the art’ editorial monitoring service - Newslive 2.05. A unique go to market strategy ‘Marketing Investment Management’ that combines the strength of

our analytics business with the power of our database

Our strategic goals have been met:

3

The CEO perspective

A view from the Boardroom

“Marketing, once seen as an expensive luxury, must now become a hygiene factor

for my organisation

The Marketing Director waxes lyrical about the intangible asset of the brand…but we

all have to clearly demonstrate what that investment produces in terms of building

value in the business.

Marketing have constantly hidden behind a fog of measures that are based purely on

tactical marketing activity, rather than solid financial metrics..

Our focus must be to develop a standard set of auditable metrics that both the

Marketing Director and I understand. Without these, Marketing should realise that I

will continue to challenge their budgets”

‘Marketing in 3D’ - Deloitte

4

A view from the agencies

Looking into the future

"Clients won't move in the future unless they get quantitative justification for what they do. We may not like it - creative departments of ad agencies certainly

don't - but that's the way the world's going."

Martin Sorrell

5

Perfectly positioned to help companies address the challenges of the new communications landscape

6

...a very different recession with a mountain of debt

Challenge 1

7

Dynamic and complex media landscapeChallenge 2

Consumers and their journeys have become more complex and less stereotyped Marketing and media planning has been slow to change

8

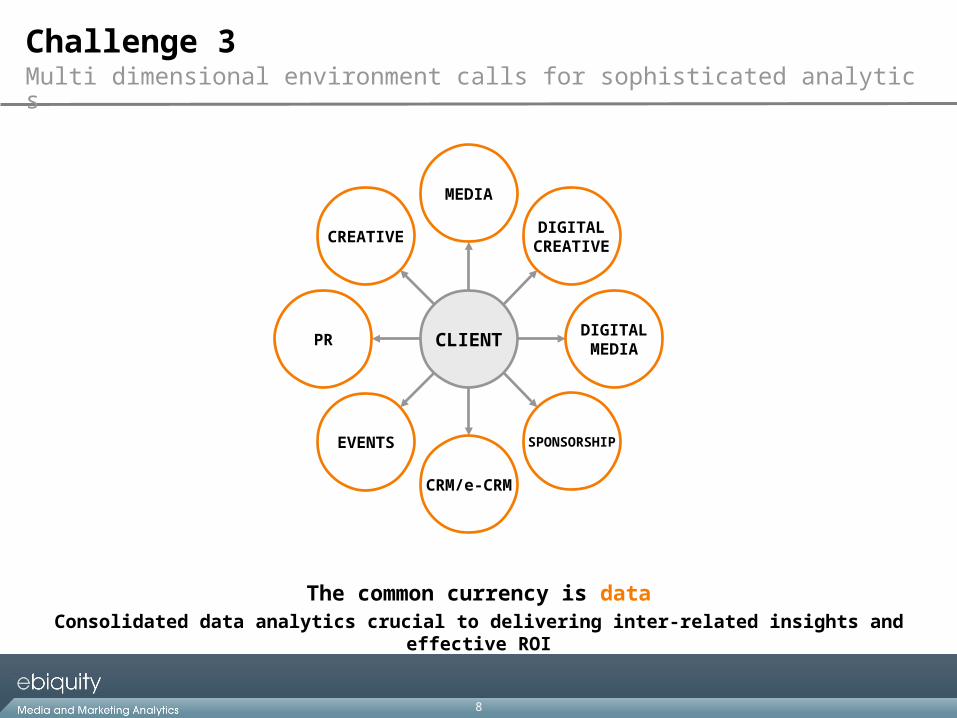

Multi dimensional environment calls for sophisticated analytics

The common currency is dataConsolidated data analytics crucial to delivering inter-related insights and effective ROI

Challenge 3

CREATIVE

PR

EVENTS

CRM/e-CRM

SPONSORSHIP

DIGITALMEDIA

DIGITALCREATIVE

MEDIA

CLIENT

9

How can I deliver more for less?

ROI just became a lot tougherEnsuring that every last penny is maximised is a pre-requisite

Challenge 4

10

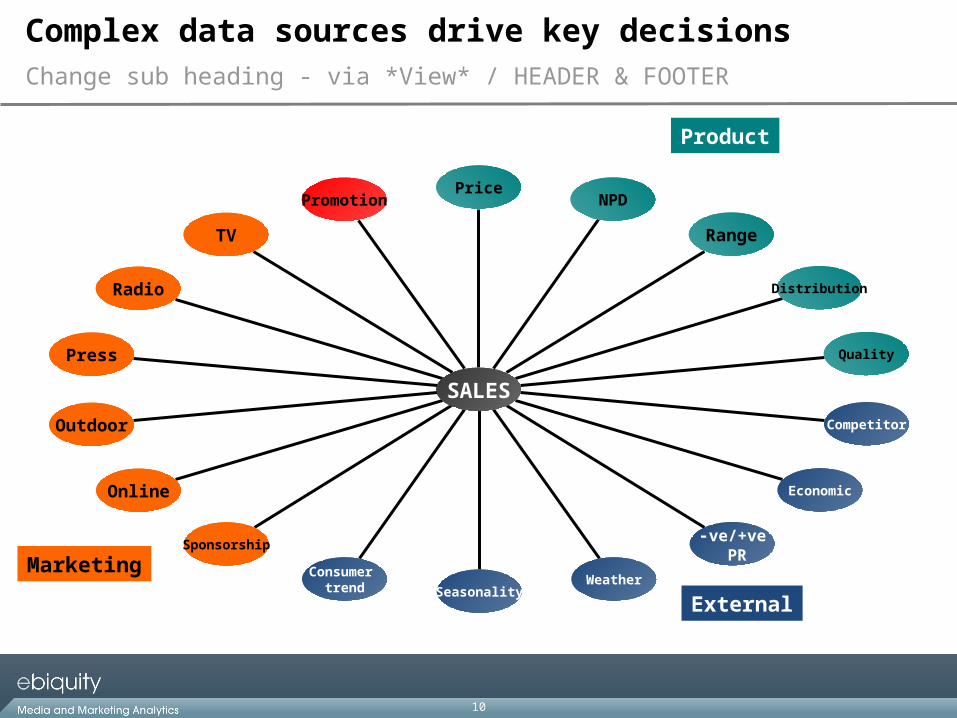

Change sub heading - via *View* / HEADER & FOOTER

Promotion

TV

Radio

Press

Outdoor

Online

Sponsorship

Consumer trend Seasonality

Weather

-ve/+ve PR

Economic

Competitor

Quality

Distribution

Range

NPDPrice

SALES

Product

Marketing

External

Complex data sources drive key decisions

11

Change sub heading - via *View* / HEADER & FOOTER

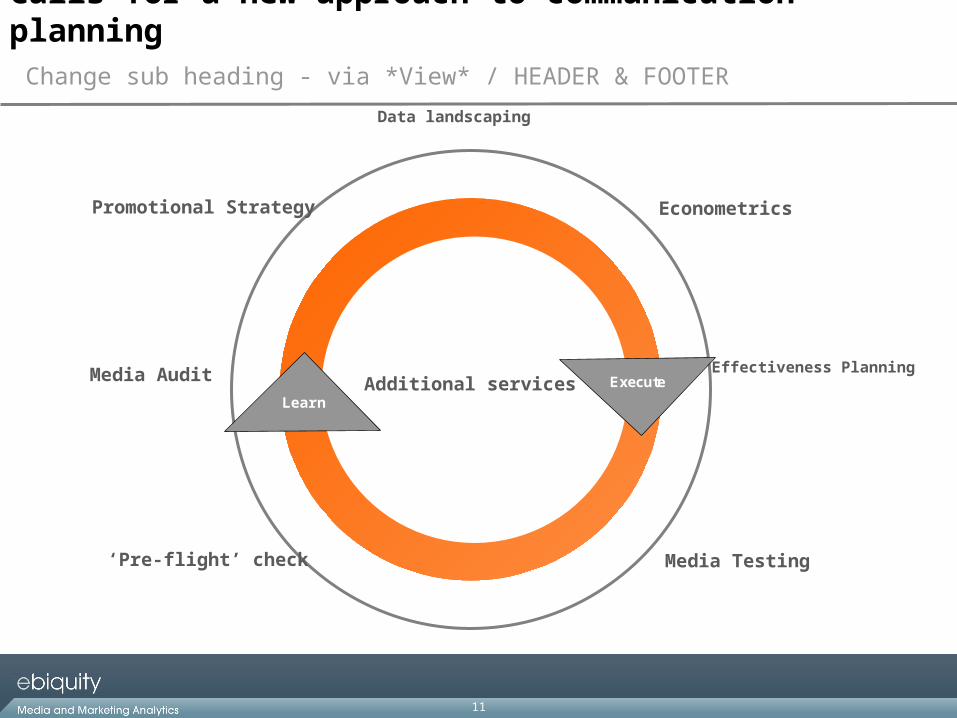

Data landscaping

Calls for a new approach to communication planning

Econometrics

Effectiveness Planning

Media Testing‘Pre-flight’ check

Media Audit

LearnExecute

Promotional Strategy

LearnAdditional services

12

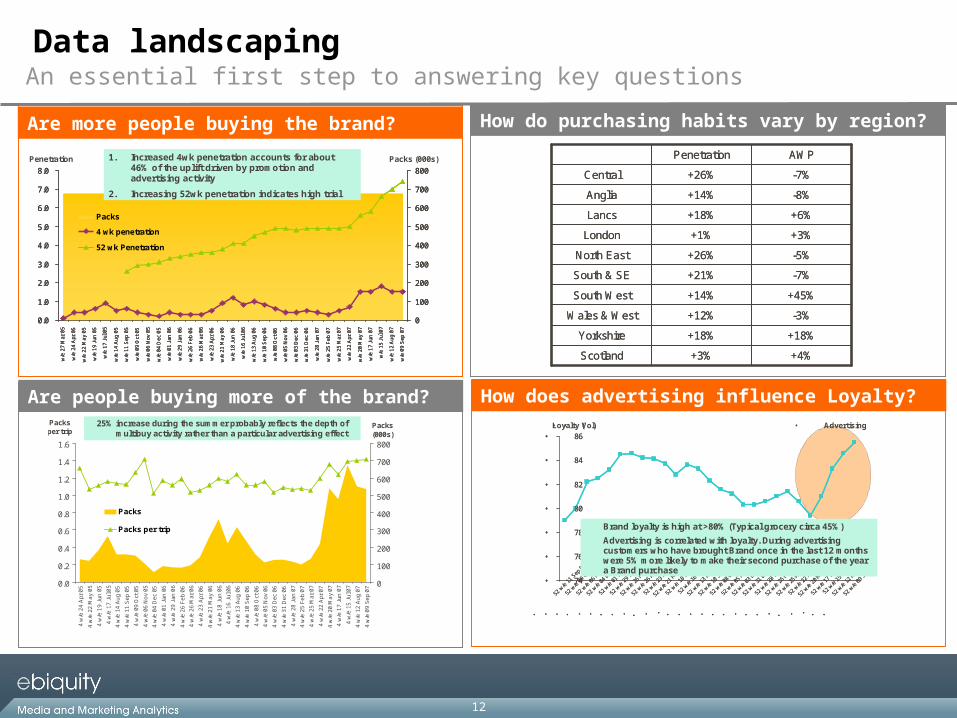

An essential first step to answering key questions

©copyright billetts 2008

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

w/e

27

Mar

05

w/e

24

Apr

05

w/e

22

Ma

y 0

5

w/e

19

Jun

05

w/e

17

Jul

05

w/e

14

Au

g 0

5

w/e

11

Sep

05

w/e

09

Oct

05

w/e

06

No

v 0

5

w/e

04

Dec

05

w/e

01

Jan

06

w/e

29

Jan

06

w/e

26

Feb

06

w/e

26

Mar

06

w/e

23

Apr

06

w/e

21

Ma

y 0

6

w/e

18

Jun

06

w/e

16

Jul

06

w/e

13

Au

g 0

6

w/e

10

Sep

06

w/e

08

Oct

06

w/e

05

No

v 0

6

w/e

03

Dec

06

w/e

31

Dec

06

w/e

28

Jan

07

w/e

25

Feb

07

w/e

25

Mar

07

w/e

22

Apr

07

w/e

20

Ma

y 0

7

w/e

17

Jun

07

w/e

15

Jul

07

w/e

12

Au

g 0

7

w/e

09

Sep

07

0

100

200

300

400

500

600

700

800

Packs

4 wk penetration

52 wk Penetration

Penetration Packs (000s)1. Increased 4wk penetration accounts for about 46% of the uplift driven by promotion and advertising activity

2. Increasing 52wk penetration indicates high trial

©copyright billetts 2008

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

w/e

27

Mar

05

w/e

24

Apr

05

w/e

22

Ma

y 0

5

w/e

19

Jun

05

w/e

17

Jul

05

w/e

14

Au

g 0

5

w/e

11

Sep

05

w/e

09

Oct

05

w/e

06

No

v 0

5

w/e

04

Dec

05

w/e

01

Jan

06

w/e

29

Jan

06

w/e

26

Feb

06

w/e

26

Mar

06

w/e

23

Apr

06

w/e

21

Ma

y 0

6

w/e

18

Jun

06

w/e

16

Jul

06

w/e

13

Au

g 0

6

w/e

10

Sep

06

w/e

08

Oct

06

w/e

05

No

v 0

6

w/e

03

Dec

06

w/e

31

Dec

06

w/e

28

Jan

07

w/e

25

Feb

07

w/e

25

Mar

07

w/e

22

Apr

07

w/e

20

Ma

y 0

7

w/e

17

Jun

07

w/e

15

Jul

07

w/e

12

Au

g 0

7

w/e

09

Sep

07

0

100

200

300

400

500

600

700

800

Packs

4 wk penetration

52 wk Penetration

Penetration Packs (000s)1. Increased 4wk penetration accounts for about 46% of the uplift driven by promotion and advertising activity

2. Increasing 52wk penetration indicates high trial

©copyright billetts 2008

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

w/e

27

Mar

05

w/e

24

Apr

05

w/e

22

Ma

y 0

5

w/e

19

Jun

05

w/e

17

Jul

05

w/e

14

Au

g 0

5

w/e

11

Sep

05

w/e

09

Oct

05

w/e

06

No

v 0

5

w/e

04

Dec

05

w/e

01

Jan

06

w/e

29

Jan

06

w/e

26

Feb

06

w/e

26

Mar

06

w/e

23

Apr

06

w/e

21

Ma

y 0

6

w/e

18

Jun

06

w/e

16

Jul

06

w/e

13

Au

g 0

6

w/e

10

Sep

06

w/e

08

Oct

06

w/e

05

No

v 0

6

w/e

03

Dec

06

w/e

31

Dec

06

w/e

28

Jan

07

w/e

25

Feb

07

w/e

25

Mar

07

w/e

22

Apr

07

w/e

20

Ma

y 0

7

w/e

17

Jun

07

w/e

15

Jul

07

w/e

12

Au

g 0

7

w/e

09

Sep

07

0

100

200

300

400

500

600

700

800

Packs

4 wk penetration

52 wk Penetration

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

w/e

27

Mar

05

w/e

24

Apr

05

w/e

22

Ma

y 0

5

w/e

19

Jun

05

w/e

17

Jul

05

w/e

14

Au

g 0

5

w/e

11

Sep

05

w/e

09

Oct

05

w/e

06

No

v 0

5

w/e

04

Dec

05

w/e

01

Jan

06

w/e

29

Jan

06

w/e

26

Feb

06

w/e

26

Mar

06

w/e

23

Apr

06

w/e

21

Ma

y 0

6

w/e

18

Jun

06

w/e

16

Jul

06

w/e

13

Au

g 0

6

w/e

10

Sep

06

w/e

08

Oct

06

w/e

05

No

v 0

6

w/e

03

Dec

06

w/e

31

Dec

06

w/e

28

Jan

07

w/e

25

Feb

07

w/e

25

Mar

07

w/e

22

Apr

07

w/e

20

Ma

y 0

7

w/e

17

Jun

07

w/e

15

Jul

07

w/e

12

Au

g 0

7

w/e

09

Sep

07

0

100

200

300

400

500

600

700

800

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

w/e

27

Mar

05

w/e

24

Apr

05

w/e

22

Ma

y 0

5

w/e

19

Jun

05

w/e

17

Jul

05

w/e

14

Au

g 0

5

w/e

11

Sep

05

w/e

09

Oct

05

w/e

06

No

v 0

5

w/e

04

Dec

05

w/e

01

Jan

06

w/e

29

Jan

06

w/e

26

Feb

06

w/e

26

Mar

06

w/e

23

Apr

06

w/e

21

Ma

y 0

6

w/e

18

Jun

06

w/e

16

Jul

06

w/e

13

Au

g 0

6

w/e

10

Sep

06

w/e

08

Oct

06

w/e

05

No

v 0

6

w/e

03

Dec

06

w/e

31

Dec

06

w/e

28

Jan

07

w/e

25

Feb

07

w/e

25

Mar

07

w/e

22

Apr

07

w/e

20

Ma

y 0

7

w/e

17

Jun

07

w/e

15

Jul

07

w/e

12

Au

g 0

7

w/e

09

Sep

07

0

100

200

300

400

500

600

700

800

Packs

4 wk penetration

52 wk Penetration

Penetration Packs (000s)1. Increased 4wk penetration accounts for about 46% of the uplift driven by promotion and advertising activity

2. Increasing 52wk penetration indicates high trial

Are more people buying the brand? How do purchasing habits vary by region?

Are people buying more of the brand? How does advertising influence Loyalty?

Data landscaping

©copyright billetts 2008

4 wk packs per trip – Total market

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

4 w

/e 2

4 A

pr

05

4 w

/e 2

2 M

ay 0

5

4 w

/e 1

9 Ju

n 0

5

4 w

/e 1

7 Ju

l 05

4 w

/e 1

4 A

ug

05

4 w

/e 1

1 S

ep 0

5

4 w

/e 0

9 O

ct 0

5

4 w

/e 0

6 N

ov

05

4 w

/e 0

4 D

ec

05

4 w

/e 0

1 Ja

n 0

6

4 w

/e 2

9 J

an

06

4 w

/e 2

6 F

eb

06

4 w

/e 2

6 M

ar 0

6

4 w

/e 2

3 A

pr 0

6

4 w

/e 2

1 M

ay 0

6

4 w

/e 1

8 J

un

06

4 w

/e 1

6 J

ul 0

6

4 w

/e 1

3 A

ug

06

4 w

/e 1

0 S

ep 0

6

4 w

/e 0

8 O

ct 0

6

4 w

/e 0

5 N

ov

06

4 w

/e 0

3 D

ec

06

4 w

/e 3

1 D

ec

06

4 w

/e 2

8 Ja

n 0

7

4 w

/e 2

5 F

eb

07

4 w

/e 2

5 M

ar

07

4 w

/e 2

2 A

pr

07

4 w

/e 2

0 M

ay

07

4 w

/e 1

7 J

un

07

4 w

/e 1

5 Ju

l 07

4 w

/e 1

2 A

ug 0

7

4 w

/e 0

9 S

ep

07

0

100

200

300

400

500

600

700

800

Packs

Packs per trip

Packs per trip

25% increase during the summer probably reflects the depth of multibuy activity rather than a particular advertising effect

Packs (000s)

+45%+14%South West

-7%+21%South & SE

-5%+26%North East

+3%+1%London

+6%+18%Lancs

-8%+14%Anglia

-3%+12%Wales & West

-7%+26%Central

+4%+3%Scotland

+18%+18%Yorkshire

AWPPenetration

+45%+14%South West

-7%+21%South & SE

-5%+26%North East

+3%+1%London

+6%+18%Lancs

-8%+14%Anglia

-3%+12%Wales & West

-7%+26%Central

+4%+3%Scotland

+18%+18%Yorkshire

AWPPenetration

• ©• copyright billetts 2008

• 74

• 76

• 78

• 80

• 82

• 84

• 86

•

52 w

/e11

Sep

05

•

52 w

/e09

Oct

05

•

52 w

/e06

Nov

05

•

52 w

/e04

Dec

05

•

52 w

/e01

Jan

06

•

52 w

/e29

Jan

06

•

52 w

/e26

Feb

06

•

52 w

/e26

Mar

06

•

52 w

/e23

Apr

06

•

52 w

/e21

May

06

•

52 w

/e18

Jun

06

•

52 w

/e16

Jul 0

6

•

52 w

/e13

Aug

06

•

52 w

/e10

Sep

06

•

52 w

/e08

Oct

06

•

52 w

/e05

Nov

06

•

52 w

/e03

Dec

06

•

52 w

/e31

Dec

06

•

52 w

/e28

Jan

07

•

52 w

/e25

Feb

07

•

52 w

/e25

Mar

07

•

52 w

/e22

Apr

07

•

52 w

/e20

May

07

•

52 w

/e17

Jun

07

•

52 w

/e15

Jul 0

7

•

52 w

/e12

Aug

07

•

52 w

/e09

Sep

07

• Loyalty (• Vol• )

Brand loyalty is high at >80% (Typical grocery circa 45%)

Advertising is correlated with loyalty. During advertising customers who have brought Brand once in the last 12 months were 5% more likely to make their second purchase of the year a Brand purchase

• Advertising

• ©• copyright billetts 2008

• 74

• 76

• 78

• 80

• 82

• 84

• 86

•

52 w

/e11

Sep

05

•

52 w

/e09

Oct

05

•

52 w

/e06

Nov

05

•

52 w

/e04

Dec

05

•

52 w

/e01

Jan

06

•

52 w

/e29

Jan

06

•

52 w

/e26

Feb

06

•

52 w

/e26

Mar

06

•

52 w

/e23

Apr

06

•

52 w

/e21

May

06

•

52 w

/e18

Jun

06

•

52 w

/e16

Jul 0

6

•

52 w

/e13

Aug

06

•

52 w

/e10

Sep

06

•

52 w

/e08

Oct

06

•

52 w

/e05

Nov

06

•

52 w

/e03

Dec

06

•

52 w

/e31

Dec

06

•

52 w

/e28

Jan

07

•

52 w

/e25

Feb

07

•

52 w

/e25

Mar

07

•

52 w

/e22

Apr

07

•

52 w

/e20

May

07

•

52 w

/e17

Jun

07

•

52 w

/e15

Jul 0

7

•

52 w

/e12

Aug

07

•

52 w

/e09

Sep

07

• 74

• 76

• 78

• 80

• 82

• 84

• 86

•

52 w

/e11

Sep

05

•

52 w

/e09

Oct

05

•

52 w

/e06

Nov

05

•

52 w

/e04

Dec

05

•

52 w

/e01

Jan

06

•

52 w

/e29

Jan

06

•

52 w

/e26

Feb

06

•

52 w

/e26

Mar

06

•

52 w

/e23

Apr

06

•

52 w

/e21

May

06

•

52 w

/e18

Jun

06

•

52 w

/e16

Jul 0

6

•

52 w

/e13

Aug

06

•

52 w

/e10

Sep

06

•

52 w

/e08

Oct

06

•

52 w

/e05

Nov

06

•

52 w

/e03

Dec

06

•

52 w

/e31

Dec

06

•

52 w

/e28

Jan

07

•

52 w

/e25

Feb

07

•

52 w

/e25

Mar

07

•

52 w

/e22

Apr

07

•

52 w

/e20

May

07

•

52 w

/e17

Jun

07

•

52 w

/e15

Jul 0

7

•

52 w

/e12

Aug

07

•

52 w

/e09

Sep

07

• Loyalty (• Vol• )

Brand loyalty is high at >80% (Typical grocery circa 45%)

Advertising is correlated with loyalty. During advertising customers who have brought Brand once in the last 12 months were 5% more likely to make their second purchase of the year a Brand purchase

• Advertising

13

Proprietory tools to support better decision makingOnline tools

14

LOWER QUALITY HIGHER QUALITYNORM

Track your own - and competitors’ - activity in real-time

Online toolsBilletts Media Monitoring

15

Desktop access to international results all in one placeDashboard delivery

16

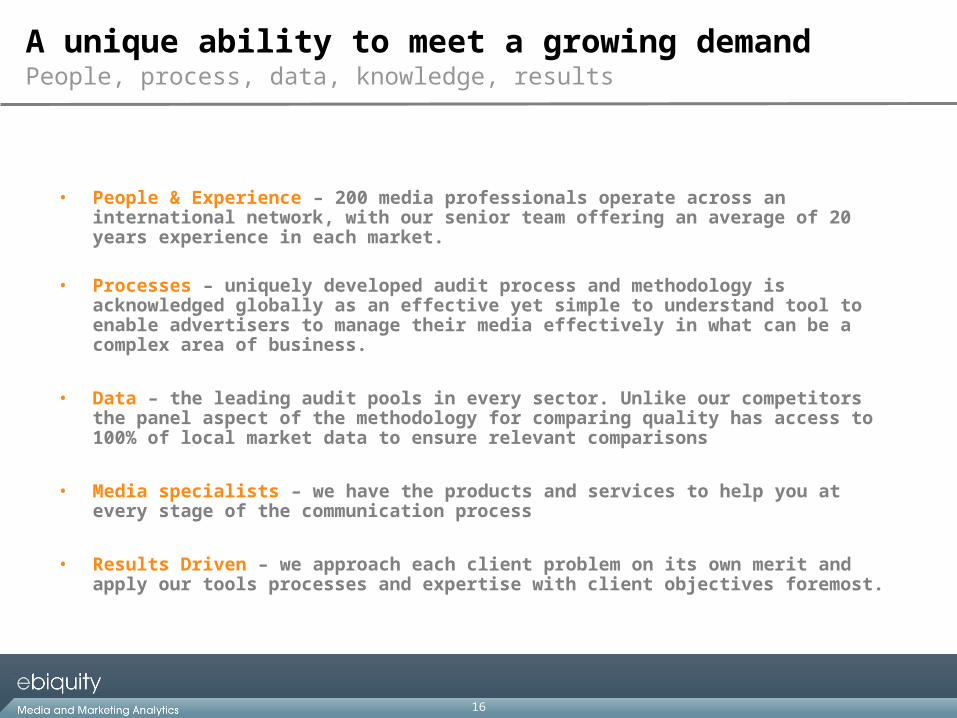

People, process, data, knowledge, results

• People & Experience – 200 media professionals operate across an international network, with our senior team offering an average of 20 years experience in each market.

• Processes – uniquely developed audit process and methodology is acknowledged globally as an effective yet simple to understand tool to enable advertisers to manage their media effectively in what can be a complex area of business.

• Data – the leading audit pools in every sector. Unlike our competitors the panel aspect of the methodology for comparing quality has access to 100% of local market data to ensure relevant comparisons

• Media specialists – we have the products and services to help you at every stage of the communication process

• Results Driven – we approach each client problem on its own merit and apply our tools processes and expertise with client objectives foremost.

A unique ability to meet a growing demand

an Ebiquity company

The story so far…..

18

Two complementary divisions

What we do

Analytics Division

Platform Division

•Media Auditing and Optimisation•Marketing Effectiveness

•Ad Monitoring•News Monitoring•Publisher Services

19

...but weak economy has a silver lining!

A story of two parts

Analytics Division

Platform Division

Strong growth in a market in which ROI and value are‘mission critical’

Weaker sales from those companiesfor whom Ad Monitoring is not ‘mission critical’. Newslive is work in progress but early signs are promising

20

Strong growth with limited competition

Analytics Division

• Billetts ‘Marketing Investment Management’ provides ‘best practice’ approach to media and marketing investment

• Billetts name - strongest sector specialist

• Largest media data base with proprietary analytics

• Continuing significant growth from international companies

• Limited competition

• US office growing in strength and reputation

• Germany, Spain and Nordics will strengthen international offering

21

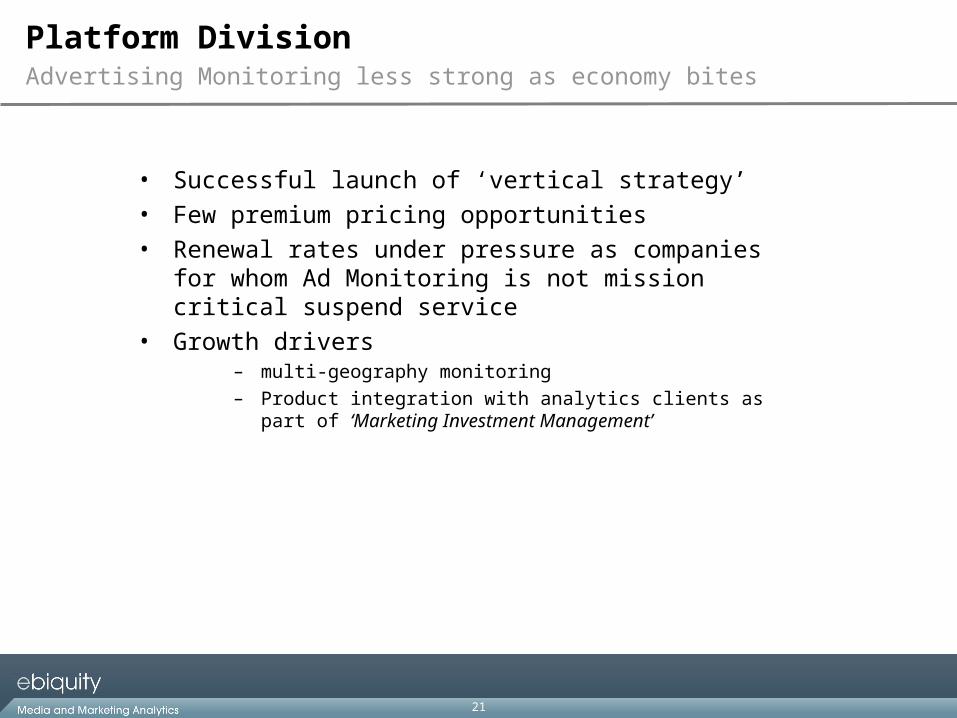

Advertising Monitoring less strong as economy bites

Platform Division

• Successful launch of ‘vertical strategy’

• Few premium pricing opportunities

• Renewal rates under pressure as companies for whom Ad Monitoring is not mission critical suspend service

• Growth drivers – multi-geography monitoring– Product integration with analytics clients as part of ‘Marketing

Investment Management’

22

Newslive - work in progress but good start

Platform Division

• Weak economy means reputation monitoring increasingly mission critical

• But more price competitive than before

• Successful launch of ‘best in class’ platform - September

• Trials phase successfully completed

• Loss making in 2008/9

• Full impact in 2009/10

23

Six months to October 2008

Financials

Financial Summary

24

Change sub heading - via *View* / HEADER & FOOTER

Revenue

Oct 08 Oct 07 YOY Apr 08

All numbers in £’000s 6m 6m % 12m

Analytics 5,717 5,467 5% 11,310

Platform 2,875 2,935 (2%) 5,910

Total 8,592 8,402 2% 17,220

25

Change sub heading - via *View* / HEADER & FOOTER

Gross Margin

Oct 08 Oct 07 YOY Apr 08

6m 6m % 12m

Gross profit

Analytics 2,892 2,646 9% 5,541

Platform 1,520 1,738 (13%) 3,418

Total 4,412 4,384 1% 8,959

Gross margin

Analytics 51% 48% 6% 49%

Platform 53% 59% (10%) 58%

Total 51% 52% (2%) 52%

26

Change sub heading - via *View* / HEADER & FOOTER

Underlying Operating Profit

Oct 08 Oct 07 YOY Apr 08

6m 6m % 12m

Analytics 1,204 836 44% 1,857

Platform (228) 295 (177%) 419

Central (55) (69) (20%) (259)

Underlying operating profit 921 1,063 (13%) 2,017

Highlighted items - non cash (333) (1,690) 83% (1,835)

- cash (161) (463) 65% (1,305)

Reporting operating profit 427 (1,090) 139% (1,123)

27

Change sub heading - via *View* / HEADER & FOOTER

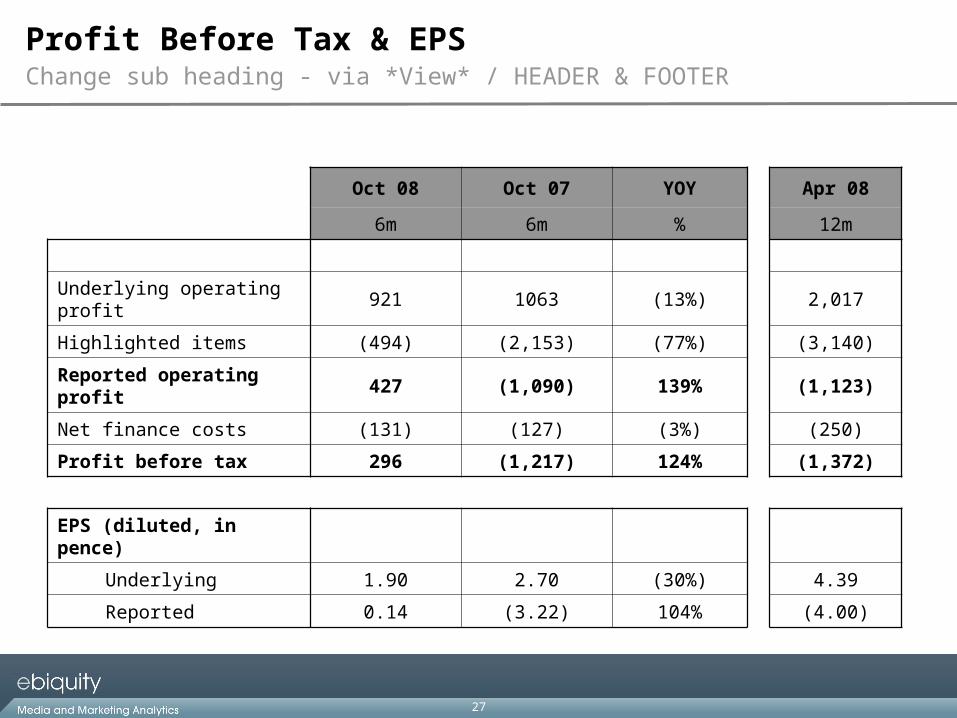

Profit Before Tax & EPS

Oct 08 Oct 07 YOY Apr 08

6m 6m % 12m

Underlying operating profit 921 1063 (13%) 2,017

Highlighted items (494) (2,153) (77%) (3,140)

Reported operating profit 427 (1,090) 139% (1,123)

Net finance costs (131) (127) (3%) (250)

Profit before tax 296 (1,217) 124% (1,372)

EPS (diluted, in pence)

Underlying 1.90 2.70 (30%) 4.39

Reported 0.14 (3.22) 104% (4.00)

28

Change sub heading - via *View* / HEADER & FOOTER

Net Debt

Oct 08 Oct 07 Apr 08

Cash 1,277 1,286 1,687

Gross debt 4,000 4,038 3,751

Net debt 2,723 2,752 2,064

Unutilised cash facility 1,000 4,100 4,100

29

A unique offering in a growing market

Outlook

• Media and Marketing analytics key driver of growth

• International growth likely to continue to accelerate with strong pipeline

• Advertising Monitoring likely to continue to show some weakness

• Growing impact of Newslive as revenues begin to scale although loss making in year one

• Continue to be confident that the Company is well positioned for future growth

30

The Future Looks Bright

• We help our clients to save money, make them more efficient and help them to make better informed decisions

• Our services are even more valid during economic uncertainty

• We see big international opportunities with limited credible competition

• We are at the beginning of our journey – our strategy is set, and we have delivered our promises

• We are conservatively financed

• We control our costs tightly

• We are in a position to look at well priced acquisition opportunities

an Ebiquity company

The Registry

Royal Mint Court

London

EC3N 4QN

Tel. +44 (0) 20 7650 9600

Fax. +44 (0) 20 7650 9650

www.ebiquity.com

an Ebiquity company

Financial Appendices

33

Highlighted items

Oct 08 Oct 07 Apr 08

6m 6m 12m

Recurring

Share based expenses 152 45 99

Amortisation of purchased intangibles 181 188 369

333 233 468

Non recurring

Write down of development asset - 1,457 1,457

Property costs - 246 458

Management restructuring 161 127 521

Other - 90 236

161 1,920 2,672

Total 494 2,153 3,140

34

Balance sheet

Oct 08 Oct 07 Apr 08

Non current assets 13,841 13,284 13,606

Current assets Trade debtors 3,194 3,496 3,052

Accrued income 2,083 1,698 1,904

Cash 1,277 1,286 1,687

Other 853 466 797

7,407 6,946 7,440

Current liabilities Loans 2,400 2,038 1,951

Deferred income 2,927 2,562 2,830

Other 4,400 3,375 4,528

9,727 7,975 9,309

Non current liabilities Loans 1,600 2,000 1,800

Deferred tax 615 720 667

Other 39 124 65

2,254 2,844 2,532

Net assets 9,267 9,411 9,205

35

Cashflow

Oct 08 Oct 07

6m 6m

Cash generated from operations 376 430

Finance expense (147) (164)

Income taxes paid (118) 167

Net cash from operating activities 111 433

Investing activities

Purchase of PPE (341) (140)

Capitalised development costs (454) (211)

Finance income 16 30

(779) (321)

Financing activities

New borrowings 500 62

Loan repayments (251) (1,019)

249 (957)

Net decrease in cash (419) (845)