an introduction for cpas

TRANSCRIPT

Blockchain:

An Introduction for CPAs

Publication Date: March 2020

Blockchain: An Introduction for CPAs

Copyright © 2020 by

DeltaCPE LLC

All rights reserved. No part of this course may be reproduced in any form or by any means, without

permission in writing from the publisher.

The author is not engaged by this text or any accompanying lecture or electronic media in the

rendering of legal, tax, accounting, or similar professional services. While the legal, tax, and accounting

issues discussed in this material have been reviewed with sources believed to be reliable, concepts

discussed can be affected by changes in the law or in the interpretation of such laws since this text

was printed. For that reason, the accuracy and completeness of this information and the author's

opinions based thereon cannot be guaranteed. In addition, state or local tax laws and procedural rules

may have a material impact on the general discussion. As a result, the strategies suggested may not

be suitable for every individual. Before taking any action, all references and citations should be

checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the subject

matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal,

accounting, or other professional services. If legal advice or other expert advice is required, the services

of a competent professional person should be sought.

—-From a Declaration of Principles jointly adopted by a committee of the American Bar Association

and a Committee of Publishers and Associations.

Course Description

Blockchain is essentially an accounting technology, and it enables the collaborative creation of a

universal ledger with capabilities going beyond traditional book-keeping systems. The emergence of

blockchain signals a fundamental change in how data, information, and assets can be authorized,

recorded, processed, reported and stored. With the growing adoption of this world-changing

technology, accountants and auditors with a strong knowledge of blockchains are already increasingly

in demand, as an intricate understanding of the technology and its impact is required to provide

appropriate guidance.

The focus of this course is to explain blockchain technology, specifically, how it could transform

methods to secure information, accounting processes, and auditing procedures. This course offers a

detailed examination of the blockchain technology model including blockchain features, consensus

models, smart contracts, and types of blockchains. To truly appreciate the value of this technology, we

need to understand the current accounting and auditing landscape and hurdles, which are addressed

in the second part of this course. Finally, it discusses the implications of blockchains to the accounting

and auditing profession.

Field of Study Accounting Level of Knowledge Overview Prerequisite None Advanced Preparation None

Table of Contents Introduction 1

Learning Objectives 1

I. What is Blockchain Technology? 2

The Language of Blockchain 2

A World without Middlemen 5

DLT: Distributed Architecture 5

Blockchain: A Self-Regulating Ecosystem 7

The Future of Record-Keeping 9

Triple-Entry Accounting 9

Tamper-Proof Record 10

Self-Executing Agreement 20

Illustration: Crypto Transactions on a Blockchain 22

Review Questions - Section 1 23

Types of Blockchains 25

Public Blockchains 27

Private Blockchains 29

Hybrid Blockchains 34

Whether to Deploy Blockchain Solutions 35

Review Questions - Section 2 37

II. How Blockchain will Enhance the Accounting and Auditing Professions 38

Foundation of Accounting Principles 38

The Value of Accounting 38

The Development of Accounting Discipline 39

The Role of Auditor 42

The Functions of Intermediaries 44

Review Questions - Section 3 46

Obstacles of the Current Practice 48

A Burden on Business 48

Inherent Limitations of Financial Audits 50

Erosion of Confidence: Audit Deficiencies 57

The Potential Impact on the Accounting and Auditing Professions 61

Enhancement of Book-Keeping Systems 61

Transformation of Auditing Practices 63

Review Questions - Section 4 72

Appendix A: Blockchain Decision Tree 74

Appendix B: Blockchain’s Impacts on Auditing Practices 75

Answers to Review Questions 76

Review Questions - Section 1 76

Review Questions - Section 2 80

Review Questions - Section 3 82

Review Questions - Section 4 84

Glossary 88

Index 89

1

Introduction The creation of blockchain technology opens the door to revolutionary possibilities. It combines the

power of the Internet with the security of cryptography to offer, for example, cheaper and faster

payment options than those offered by traditional financial services businesses, without a trusted third

party. It is important to first understand how blockchains work before it becomes clear what they can

offer to accounting and auditing. As adoption becomes more widespread, accountants and auditors

should be getting on board. This course goes into well researched and newbie-friendly reflections

about the most important blockchain concepts by addressing the following frequently asked

questions:

• How does a distributed ledger differ from traditional databases?

• What are the components of a blockchain ecosystem?

• How does blockchain work?

• What does trustless mean in blockchain technology?

• What are the benefits of blockchain technology?

• How does triple-entry accounting work?

• What is a blockchain wallet?

• How is consensus reached in a blockchain?

• What is a 51% attack?

• What are blockchain forks?

• What are smart contracts?

• What are the different types of blockchains?

• How can block chains reshape accounting and auditing practices?

This course provides guidance to these, and many more, questions connected to this topic. It explains

block chain fundamentals and how this technology will enhance many of the core businesses of the

accounting and auditing profession.

Learning Objectives After completing this course, you will be able to:

• Recognize the technical terms associated with blockchain

• Identify the key components of blockchain technology and how they function

• Identify different types of blockchains

• Recall basic accounting and auditing principles

• Recognize how blockchains could reshape accounting and auditing practices

2

I. What is Blockchain Technology? As you will learn, Blockchains can function as constantly growing distributed ledgers where companies

record their transactions directly into activity registers. Distributed ledger technology (DLT) has many

advantages, including increased security in trustless environments, and has been successfully

implemented in a variety of industries. The Big 4 accounting firms are developing skills required to

understand and audit blockchain technology as clients start switching portions of their business onto

blockchain-based infrastructure.

This chapter defines the high-level components of a blockchain network architecture, including

distributed ledgers, cryptography, and consensus protocols. It also explains how blockchains have

profoundly changed the current organizational and technological infrastructure required to create

trust and revolutionize record-keeping systems.

The Language of Blockchain

Blockchains facilitate the digital transformation of business and social ecosystems. The growing

popularity and prevalence of technology is clear. Worldwide spending on blockchain solutions is

projected to grow from $1.5 billion in 2018 to $11.7 billion by 20221. Spending by the U.S., the largest

regional spender on blockchain solutions, is expected to reach $4.2 billion by 2020.2

The world of blockchain introduces many technical terms. Newcomers might be baffled by crypto

jargon. Knowing the vocabulary is essential to understanding. To help ease you into this landscape, we

created this section to introduce common terms and phrases relevant to blockchain technology.

Address: An address is basically a destination where a user sends and receives digital currency. It is

similar to a bank account. An address usually includes a long series of letters and numbers.

Algorithm: A process or set of rules to be followed in calculations or other problem-solving operations.

Altcoins: Altcoin is a blended word, derived from “alternative” and “coin”, and refers to any digital

currency that is not bitcoin.

Bitcoin: Bitcoin is both a concept (technology or movement) and a currency. As a concept, Bitcoin is

capitalized. The unit of the currency, bitcoin, is lowercase.

1 Blockchain statistics are from “Blockchain - Statistics & Facts,” statista, with values as accessed on December 22, 2019. 2 Blockchain statistics are from “Worldwide spending on blockchain solutions,” statista, with values as accessed on December 26, 2019.

3

Blockchain: A blockchain is a digital, decentralized ledger, consisting of a series of blocks. A block is

simply a group of cryptocurrency transactions that have been verified. Blockchain technology is used

for recording transactions made with cryptocurrencies, such as bitcoin, and has many other

applications.

Consensus Mechanism: A method to authenticate and validate a set of values or a transaction without

the need to trust or rely on a centralized authority. It allows each participant to trust the network as

they know each transaction will follow rules they ratified when the network launched. For example,

when a transaction is made, if all nodes on the network agree that it is valid on a blockchain, they have

a consensus.

Cryptocurrency: A cryptocurrency is a digital currency that relies on cryptography. Bitcoin, for

example, leverages cryptography in order to verify transactions.

Cryptography: Cryptography, the process of encoding and decoding information, is used to verify and

secure transactions on a blockchain.

Digital Signature: Digital signature provides validation and authentication in the same way signatures

do, in digital form; ensuring the security and integrity of the data recorded onto a blockchain.

Distributed Ledger: A distributed ledger is a system of independent computers (peer-to-peer) that are

simultaneously recording data. Identical copies of the recording are kept by each computer. Blockchain

is a distributed ledger that was originally created to keep track of all bitcoin transactions.

Double-Spending: Double-spending is the attempt to send cryptocurrency to two separate locations

at the same time. For example, this could happen if a cryptocurrency user tries to purchase something

with a coin she or he has already spent. Bitcoin was the first to implement a solution that protects

against double-spending by verifying each transaction added to a blockchain to ensure that the coins

for the transaction had not previously been spent.

Hashing: Hashing involves taking plain-text and converting it to a hash value of fixed size by a hash

function. This process ensures the integrity of the message as the hash value on both the sender’s and

receiver’s side should match if the message is unaltered.

Mining: Mining is the computer process of validating information, creating a new block and recording

that information into a blockchain.

Node: Blockchain is spread over network computers. Each user actively on the network is a node.

Peer-to-Peer: A connection between two or more computers without using a centralized third party

as an intermediary. Most cryptocurrencies operate on a peer-to-peer network.

4

PoA: Acronym for “proof of authority”, a reputation-based consensus algorithm, leveraging the value

of identity rather than staking digital assets. The principle behind this reputation mechanism is the

certainty of a pre-approved validator’s identity.

PoS: Acronym for "proof of stake”. A consensus mechanism, used to validate transactions recorded

on certain blockchains, is based upon a user’s proof of stake (how many units they have) in a

blockchain. Proof of stake is a common alternative to a proof of work protocol.

PoW: Acronym for "proof of work”. A consensus mechanism is used to validate transactions recorded

on certain blockchains. It generally requires the production of proof of complex cryptographic

computations and large amounts of computing power in order to validate transactions.

Private Key: Similar to a password to access one’s account, a private key is a string of letters and

numbers known only by the owner that allows them to spend their cryptocurrency. Thus, private keys

must never be revealed to anyone but the owner.

Public Key: A string of letters and numbers that allows cryptocurrency to be received.

Wallet (Virtual Wallet): Electronic device or online service that allows a user to receive

cryptocurrencies, store them, and send them to others.

5

A World without Middlemen

DLT: Distributed Architecture

“Distributed ledger technology is one such innovation that has been cited as a means of transforming

payment, clearing, and settlement (PCS) processes, including how funds are transferred and how

securities, commodities, and derivatives are cleared and settled.”

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs

Federal Reserve Board, Washington, D.C.

While blockchain technology was initially a means to create bitcoin, a global cryptocurrency, it is also

the foundation of most modern cryptocurrencies. The most popular and widely used cryptocurrency

is bitcoin; however, there are more than 2,300 cryptocurrencies in circulation3.

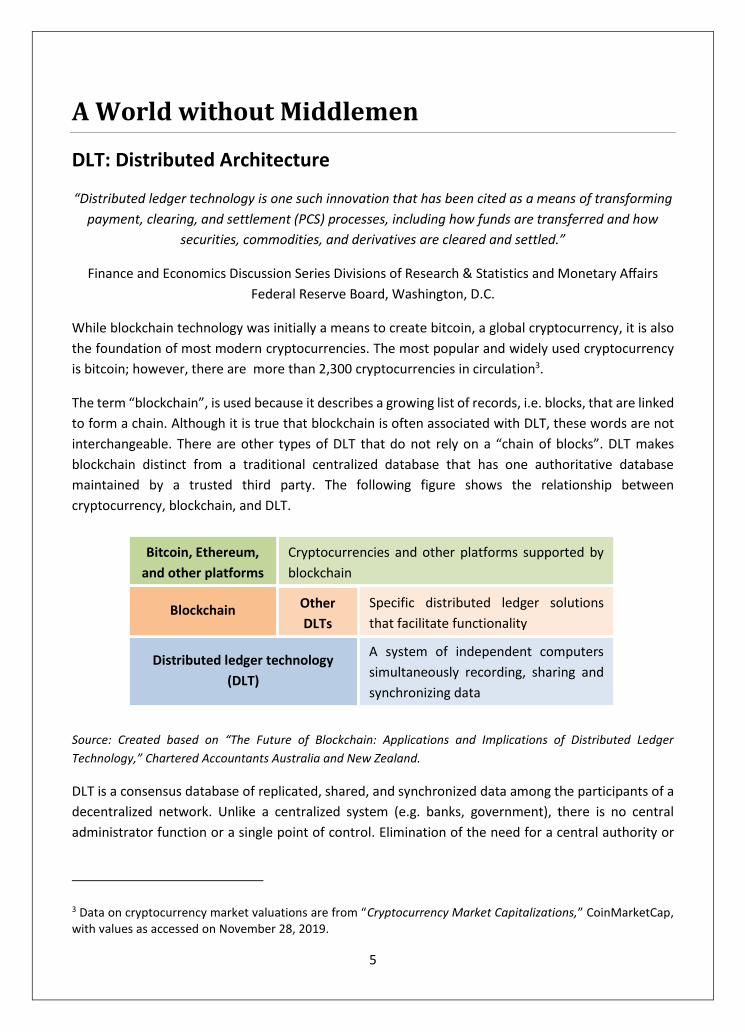

The term “blockchain”, is used because it describes a growing list of records, i.e. blocks, that are linked

to form a chain. Although it is true that blockchain is often associated with DLT, these words are not

interchangeable. There are other types of DLT that do not rely on a “chain of blocks”. DLT makes

blockchain distinct from a traditional centralized database that has one authoritative database

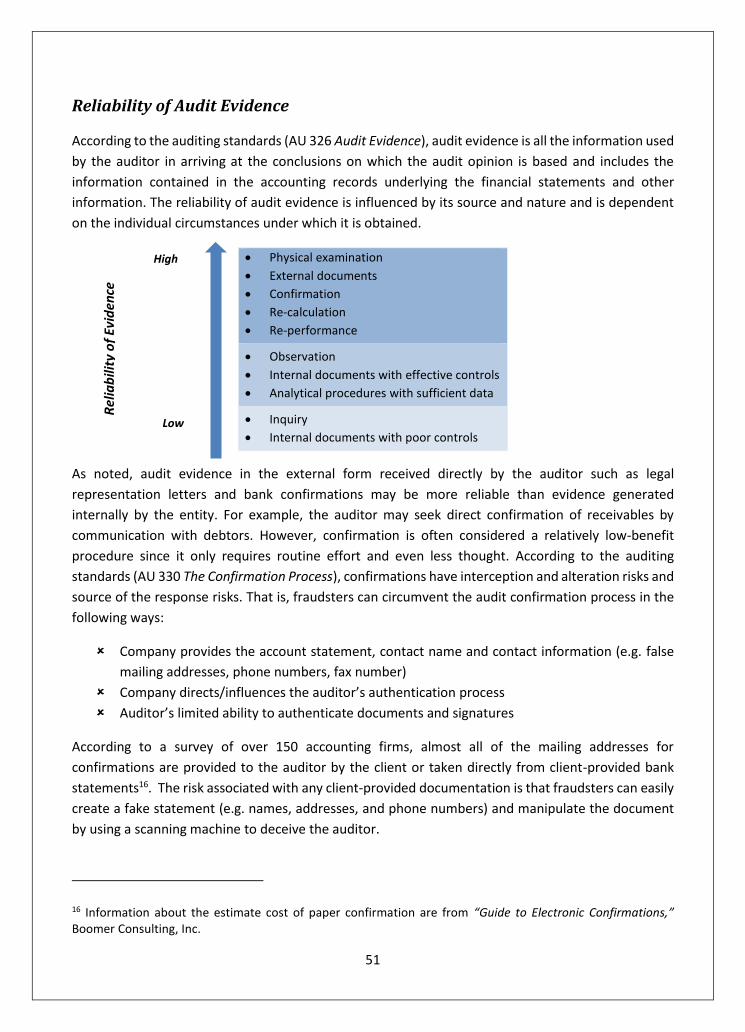

maintained by a trusted third party. The following figure shows the relationship between

cryptocurrency, blockchain, and DLT.

Source: Created based on “The Future of Blockchain: Applications and Implications of Distributed Ledger

Technology,” Chartered Accountants Australia and New Zealand.

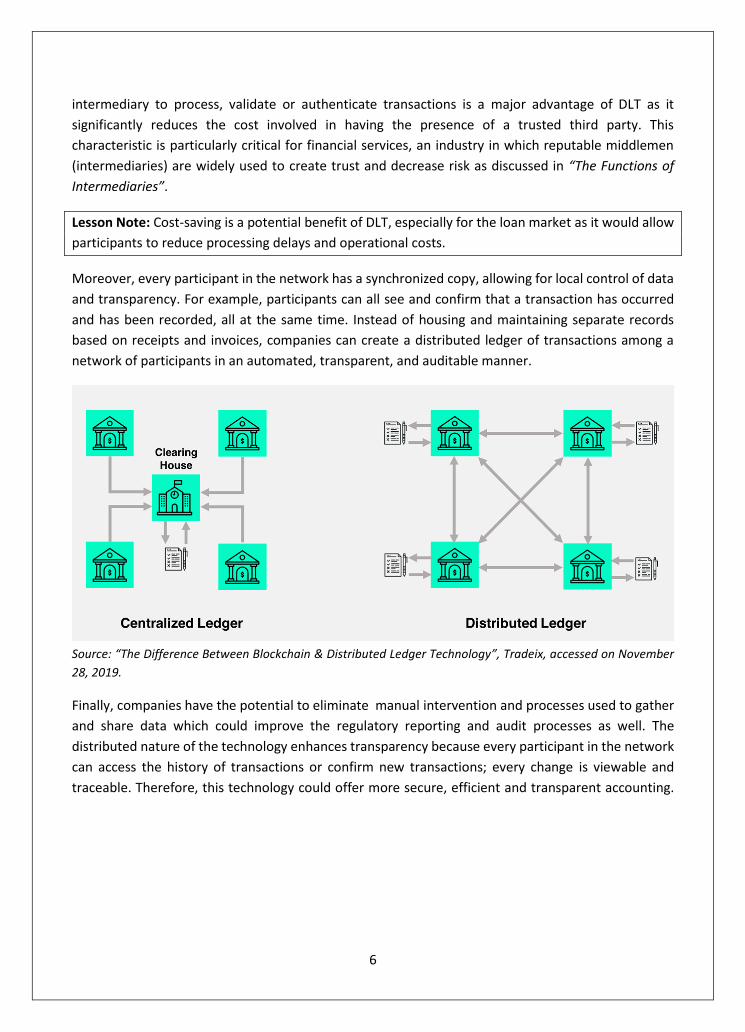

DLT is a consensus database of replicated, shared, and synchronized data among the participants of a

decentralized network. Unlike a centralized system (e.g. banks, government), there is no central

administrator function or a single point of control. Elimination of the need for a central authority or

3 Data on cryptocurrency market valuations are from “Cryptocurrency Market Capitalizations,” CoinMarketCap, with values as accessed on November 28, 2019.

Distributed ledger technology

(DLT)

A system of independent computers

simultaneously recording, sharing and

synchronizing data

Blockchain Specific distributed ledger solutions

that facilitate functionality

Other

DLTs

Cryptocurrencies and other platforms supported by

blockchain

Bitcoin, Ethereum,

and other platforms

6

intermediary to process, validate or authenticate transactions is a major advantage of DLT as it

significantly reduces the cost involved in having the presence of a trusted third party. This

characteristic is particularly critical for financial services, an industry in which reputable middlemen

(intermediaries) are widely used to create trust and decrease risk as discussed in “The Functions of

Intermediaries”.

Lesson Note: Cost-saving is a potential benefit of DLT, especially for the loan market as it would allow

participants to reduce processing delays and operational costs.

Moreover, every participant in the network has a synchronized copy, allowing for local control of data

and transparency. For example, participants can all see and confirm that a transaction has occurred

and has been recorded, all at the same time. Instead of housing and maintaining separate records

based on receipts and invoices, companies can create a distributed ledger of transactions among a

network of participants in an automated, transparent, and auditable manner.

Source: “The Difference Between Blockchain & Distributed Ledger Technology”, Tradeix, accessed on November

28, 2019.

Finally, companies have the potential to eliminate manual intervention and processes used to gather

and share data which could improve the regulatory reporting and audit processes as well. The

distributed nature of the technology enhances transparency because every participant in the network

can access the history of transactions or confirm new transactions; every change is viewable and

traceable. Therefore, this technology could offer more secure, efficient and transparent accounting.

7

Companies have the following common motivations behind efforts to develop and deploy DLT

arrangements4:

✓ Reduce complexity (especially in multiparty, cross-border transactions)

✓ Improve end-to-end processing speed and availability of assets and funds

✓ Decrease need for reconciliation across multiple record-keeping infrastructures

✓ Increase transparency and immutability in transaction record-keeping

✓ Improve network resiliency through distributed data management

✓ Reduce operational and financial risks

The following table identifies the major differences of a distributed ledger and centralized ledger.

Distributed Ledger Centralized Ledger

• Consensus on data

• Immutable

• Distributed

• Decentralized

• Peer-to-Peer

• Cryptographic validation

• Cryptographic authentication and authorization

• Resiliency and availability increase with node

count

• Internal and external reconciliation required

• No restrictions

• Single point of failure

• Single point of control

• Unnecessary gateways and middlemen

• Cryptographic must be added as afterthought

• Actions are done on behalf of others

• Backup must be set up manually

Source: International Research Journal of Engineering and Technology (IRJET), “BlockChain Technology

Centralised Ledger to Distributed Ledger,” Volume: 04 Issue: 03 | Mar -2017.

Blockchain: A Self-Regulating Ecosystem

Blockchain is a type of distributed ledger that creates a peer-to-peer network, which establishes a

means for transacting and enables recording, transferring, tracking, authenticating, and storing of

digital assets. Blockchain is often referred to as a “trustless” system because it provides a secure and

decentralized ledger of all transactions across a network without the need for trusted intermediaries

by using three principal technologies, which is a significant innovation in traditional record-keeping:

1. Distributed Ledger enables a decentralized exchange of trusted data

2. Cryptography enforces the authentication and confidentiality of transactions

3. Consensus mechanism ensures correct sequencing of transactions on a blockchain

Each technology is explained in “The Future of Record-Keeping”.

4 Information collected through interviews with industry stakeholders is from “Distributed ledger technology in payments, clearing, and settlement,” Finance and Economics Discussion Series 2016-095. Washington: Board of Governors of the Federal Reserve System.

8

Lesson Note: To gain control over a peer network, a person attempts to gain a disproportionately large

influence by creating a large number of nodes or accounts. The technical term for this is a “Sybil”

attack.

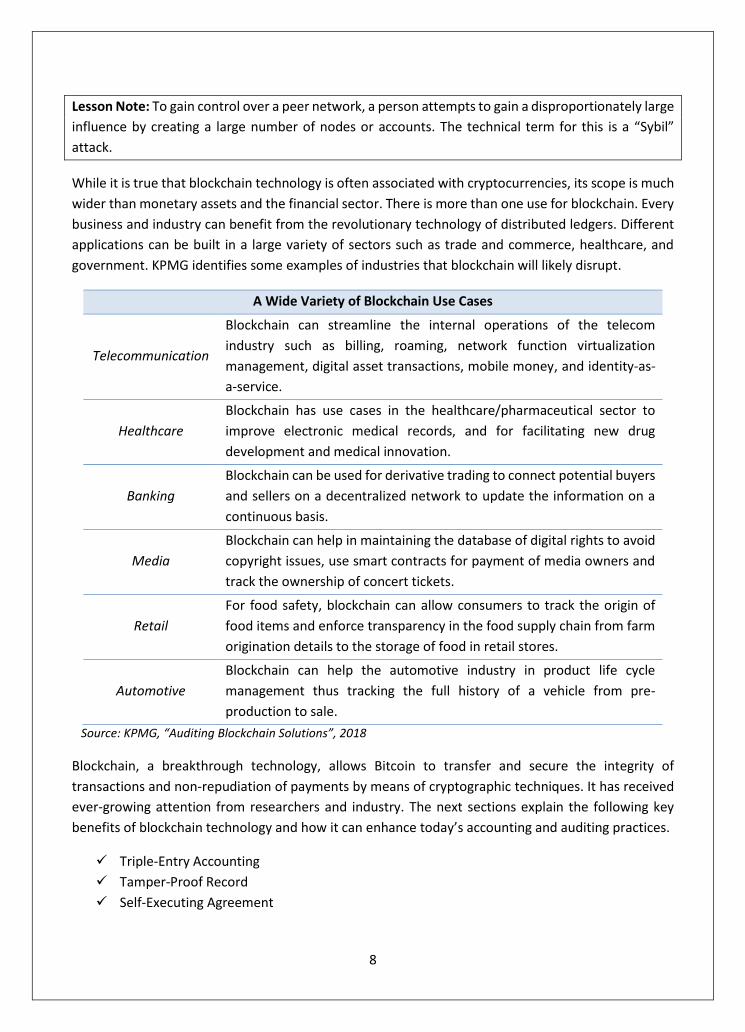

While it is true that blockchain technology is often associated with cryptocurrencies, its scope is much

wider than monetary assets and the financial sector. There is more than one use for blockchain. Every

business and industry can benefit from the revolutionary technology of distributed ledgers. Different

applications can be built in a large variety of sectors such as trade and commerce, healthcare, and

government. KPMG identifies some examples of industries that blockchain will likely disrupt.

A Wide Variety of Blockchain Use Cases

Telecommunication

Blockchain can streamline the internal operations of the telecom

industry such as billing, roaming, network function virtualization

management, digital asset transactions, mobile money, and identity-as-

a-service.

Healthcare

Blockchain has use cases in the healthcare/pharmaceutical sector to

improve electronic medical records, and for facilitating new drug

development and medical innovation.

Banking

Blockchain can be used for derivative trading to connect potential buyers

and sellers on a decentralized network to update the information on a

continuous basis.

Media

Blockchain can help in maintaining the database of digital rights to avoid

copyright issues, use smart contracts for payment of media owners and

track the ownership of concert tickets.

Retail

For food safety, blockchain can allow consumers to track the origin of

food items and enforce transparency in the food supply chain from farm

origination details to the storage of food in retail stores.

Automotive

Blockchain can help the automotive industry in product life cycle

management thus tracking the full history of a vehicle from pre-

production to sale.

Source: KPMG, “Auditing Blockchain Solutions”, 2018

Blockchain, a breakthrough technology, allows Bitcoin to transfer and secure the integrity of

transactions and non-repudiation of payments by means of cryptographic techniques. It has received

ever-growing attention from researchers and industry. The next sections explain the following key

benefits of blockchain technology and how it can enhance today’s accounting and auditing practices.

✓ Triple-Entry Accounting

✓ Tamper-Proof Record

✓ Self-Executing Agreement

9

Lesson Note: The term "Triple-Entry Accounting" refers to a system proposed by Ian Grigg, financial

cryptographer, and described in his paper “Triple Entry Accounting” published in 2005.

The Future of Record-Keeping

Many industries have used blockchain to secure all types of records; from land transactions to financial

information. The most common types of records kept on blockchain include:

✓ Public records (e.g. property register)

✓ Financial information

✓ Business transactions

✓ Medical records

✓ Identity management

✓ Management activities

✓ Contracts

Blockchain does not only apply to documents. It can be used with any kind of digital asset, such as

video files, images, and email backups. This course focuses on the accounting and auditing aspects.

Triple-Entry Accounting

Companies have relied on double-entry accounting to gather information and maintain control over

their operations. This accounting method and the audited financial statements serve as valuable tools

for management, shareholders, governments and tax authorities. However, in its current state,

double-entry accounting has its limitations and can be circumvented. Although many proposed

solutions exist, one widely discussed alternative method is triple-entry accounting, an extension of the

double-entry system, enhanced by adding a third blockchain layer, a distributed ledger. Triple-entry

accounting improves the traditional double-entry accounting system by having all accounting entries

involving third parties cryptographically secured by a third entry.

A triple-entry accounting system is similar to the double-entry system except that there is a third layer,

using blockchain technology, embedded onto it. Triple-entry accounting has the potential to increase

the transparency, traceability, and efficiency of the process of accounting for transactions. Every

transaction would have a corresponding third entry that was verified by a blockchain. As parties create

transactions, the blockchain technology will use a consensus process to validate each new transaction,

create a third entry, and then post it to a shared (public) ledger. The following figure shows an example

of how blockchain creates a third entry linked to participants.

10

Company A’s Books Company B’s Books

Debits Credits Debits Credits

500 500

2,000 2,000

Blockchain Technology:

Distributed (Public) Ledger

Company A Company B

-500 500

-2,000 2,000

For example, if Company A records debits of $500 and $2,000 to account for cash received from

Company B for previous sales on account, Company B also records credits of $500 and $2,000 to

account for cash paid to Company A. When payments are made to Company A, new blocks are created

which are linked to all previous blocks in the chain, maintaining transaction history. Since the blocks

are visible to Company A and B in the public ledger, both companies are able to immediately see the

update. Therefore, both companies can confirm transactions without a need for a trusted party since

the public ledger (the third entry) ensures a match between payable and receivable.

In summary, Blockchain, a distributed ledger, allows companies to record their transactions directly

into a shared register as demonstrated in the diagram. Blockchain offers the possibility to use it to

generate trust, security, and transparency among people and entities that do not necessarily know

each other and to provide more business opportunities in areas where governing authority and

intermediaries exist. The next section explains how blockchain technology takes over the functions

performed by a trusted party.

Tamper-Proof Record

Tamper-proof, or immutability, is the ability for a blockchain ledger to create and store a permanent,

immutable, signed, and time-stamped record of identity, ownership, transactions or contractual

commitments. Although there have been a few incidents of hacking of digital currencies that rely on

blockchain technology, the unique way in which the information is stored and updated makes it very

secure as shown below.

CryptographyHashing Process

Consensus Mechanism

Tamper-Proof

11

Lesson Note: Although most publications on blockchain technology consider blockchain ledgers to be

immutable, there are situations in which a blockchain can be compromised. This is known as a 51%

attack and is discussed in detail later.

Consensus Mechanism

Blocks contain records of transactions or other data, which together form a blockchain. Each block is

cryptographically connected using a complex mathematical algorithm, known as a consensus

mechanism. Consensus mechanisms require a majority of nodes to agree on whether:

1. A new block is valid and appropriate for inclusion in the ledger; and

2. The ledger and its history is correct based on the consensus rules

Consensus mechanisms authenticate and validate a set of values or a transaction without the need to

rely on a centralized authority. The calculation results in an alphanumeric string that is put on the next

block. The process is then repeated for each bundle of transactions that are aggregated together; the

number of blocks will increase, and the chain will continue to grow over time.

In simple words, a block is a group of transactions on blockchain that have been verified. If a

transaction violates one of the rules the network agreed on (consensus), the transaction will be

considered invalid. Consensus helps keep inaccurate or potentially fraudulent transactions out of the

database and ensures a correct sequencing of transactions on a blockchain. For instance,

cryptocurrencies are secured via a consensus mechanism to prevent “double-spending”; spending the

same money twice. Two concensus-based validation processes must be carried out:

1. Ownership of the cryptocurrency; and

2. Sufficiency of cryptocurrency in the spender’s account

As defined, the spender of the cryptocurrency needs to prove the ownership of the private key in order

to initiate a transaction. To ensure that the spender has a sufficient balance in his/her account, every

transaction is verified against the spender’s account (“public key”) in the public ledger. Although no

personal information is shared, the transaction is validated and recorded via this consensus protocol.

There are different kinds of consensus mechanism algorithms which work on different principles.

Following is a brief discussion of the most commonly used mechanisms in the context of

cryptocurrencies.

1. Proof of Work

2. Proof of Stake

3. Proof of Authority

12

Proof of Work

Proof of Work (PoW) is a consensus protocol used to validate transactions recorded on blockchains

and generally requires the production of proof of complex cryptographic computations. It is a function

used to confirm transactions before they can be accepted by network participants. Mining, the process

of validating (confirming) transactions and adding them (a new block) to a blockchain, limits the

possibility of malicious entities manipulating a blockchain and falsifying transactions by:

✓ Verifying the legitimacy of a transaction by solving a mathematical puzzle, which is called a

hash function (discussed in the next section).

To include a transaction in the next block, a miner needs to know the cryptographic hash value

of the last recorded block. This hash value must be referenced to create/add a new block.

✓ Releasing newly-created cryptocurrencies (e.g. bitcoin) to reward the first miner who

generates a new block as “block reward”.

A successful miner is the one who beats everyone else in this game and solves this

mathematical puzzle. After finding the hash of the last recorded block, a miner announces it to

the network for the other nodes to verify and creates a new block with the transactions.

Bitcoin is the most well-known crypto with a PoW consensus-building algorithm. Other examples

include Litecoin, Bitcoin Cash, and Monero. Mining requires a special program, which helps miners

compete with their peers in solving massive mathematical puzzles as the input of each block becomes

larger over time (a more complex calculation). It also requires large amounts of computing power in

order to solve the puzzles (validating transactions) and earn rewards.

Lesson Note: As of November 28, 2019, the Bitcoin network accounts for roughly 0.21% of global

electricity use. Over the course of a year this is equal to around 69.59 TWh or terawatt-hours of energy

consumption5. The closest comparison for electricity consumption is the country Austria.

Mining pools are groups of collaborating miners who agree to share block rewards according to their

contributed mining hash power. There are various bitcoin mining pools across the globe and they

compete to be the next to find a valid block hash. In 2019, China mined the most bitcoins. With bitcoin,

the reward for mining a block is now 12.5 bitcoins. To keep bitcoin's inflation in check, every 4 years

on average (210,000 blocks), the reward granted to bitcoin miners is cut in half. This process is referred

to as a “halving”.

As explained, mining requires a vast amount of computing resources, which consume a significant

amount of electricity. Thus, PoW makes it extremely challenging to alter any aspect of the chain

because such an alteration would require re-mining all subsequent blocks. However, there are

5 Bitcoin energy consumption statistics are from the Cambridge Bitcoin Electricity Consumption Index (CBECI), with values as accessed on November 28, 2019.

13

different ways a blockchain can be attacked. A 51% attack, commonly known as majority attack, refers

to an attack on a blockchain where a single entity or group of organizations control more than 50% of

the mining power (hash rate). As a result, the attacker is able to interfere with the validation process

and manipulate the public ledger by:

Invalidating ongoing transactions (denial-of-service)

Intentionally omitting an event

Preventing other miners from mining (selfish mining)

Changing the sequence of transactions

Reversing transaction history (double-spend)

In May 2018, a group of malicious miners controlled 51% of the hash rate in Bitcoin Gold to falsify the

currency’s ledger and defraud (double-spending) at least $18 million worth of cryptocurrency from

online exchanges. A selfish mining attack (block withholding attack) is also an attack on the integrity

of the blockchain network. It is a strategy used by miners to increase their rewards by intentionally

withholding a validated block from being released to the network. They attempt to mislead other

miners to continue mining already validated transactions, reducing the number of miners doing real

mining work.

The following table summarizes the characteristics of PoW.

Goal Advantages Disadvantages

To provide a barrier to

publishing blocks in the form

of a computationally difficult

puzzle to solve to enable

transactions between

untrusted participants.

• Difficult to perform denial

of service by flooding

network with bad blocks.

• Open to anyone with

hardware to solve the

puzzle.

Computationally intensive

(by design), power

consumption, hardware

arms race.

Potential for 51 % attack

by obtaining enough

computational power.

Source: National Institute of Standards and Technology, “NISTIR 8202 Blockchain Technology Overview,”

accessed on November 24, 2019.

Proof of Stake

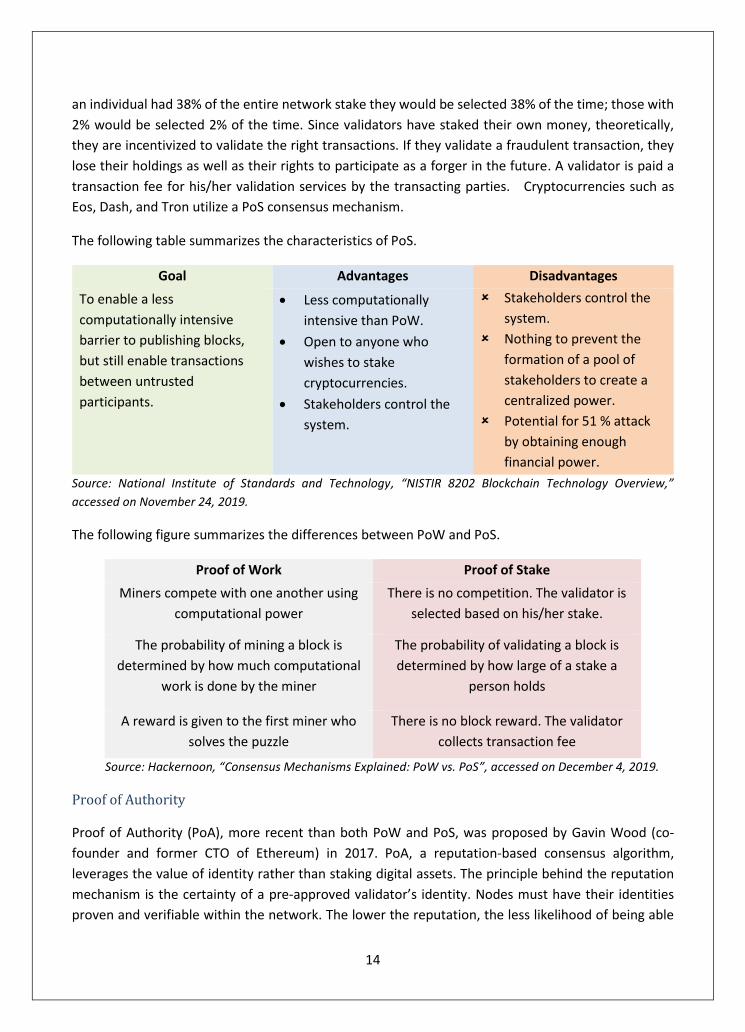

Proof of Stake (PoS) is another consensus protocol used to validate transactions on blockchains based

on a user’s stake. PoS evolved as a low-cost, low-energy consuming alternative to PoW algorithm. In

a PoS system, the act of validating transactions and creating new blocks is called “forging”. A validator

(forger) validates block transactions based on his or her stake by proving ownership of a certain asset

(e.g. a certain number of cryptocurrency units). In other words, validators must first put their own

assets at stake in order to take part in the forging process.

When selecting validators, the blockchain network usually looks at all participants and chooses

amongst them based on their ratio of stake to the overall amount of cryptocurrency staked. Thus, if

14

an individual had 38% of the entire network stake they would be selected 38% of the time; those with

2% would be selected 2% of the time. Since validators have staked their own money, theoretically,

they are incentivized to validate the right transactions. If they validate a fraudulent transaction, they

lose their holdings as well as their rights to participate as a forger in the future. A validator is paid a

transaction fee for his/her validation services by the transacting parties. Cryptocurrencies such as

Eos, Dash, and Tron utilize a PoS consensus mechanism.

The following table summarizes the characteristics of PoS.

Goal Advantages Disadvantages

To enable a less

computationally intensive

barrier to publishing blocks,

but still enable transactions

between untrusted

participants.

• Less computationally

intensive than PoW.

• Open to anyone who

wishes to stake

cryptocurrencies.

• Stakeholders control the

system.

Stakeholders control the

system.

Nothing to prevent the

formation of a pool of

stakeholders to create a

centralized power.

Potential for 51 % attack

by obtaining enough

financial power.

Source: National Institute of Standards and Technology, “NISTIR 8202 Blockchain Technology Overview,”

accessed on November 24, 2019.

The following figure summarizes the differences between PoW and PoS.

Proof of Work Proof of Stake

Miners compete with one another using

computational power

There is no competition. The validator is

selected based on his/her stake.

The probability of mining a block is

determined by how much computational

work is done by the miner

The probability of validating a block is

determined by how large of a stake a

person holds

A reward is given to the first miner who

solves the puzzle

There is no block reward. The validator

collects transaction fee

Source: Hackernoon, “Consensus Mechanisms Explained: PoW vs. PoS”, accessed on December 4, 2019.

Proof of Authority

Proof of Authority (PoA), more recent than both PoW and PoS, was proposed by Gavin Wood (co-

founder and former CTO of Ethereum) in 2017. PoA, a reputation-based consensus algorithm,

leverages the value of identity rather than staking digital assets. The principle behind the reputation

mechanism is the certainty of a pre-approved validator’s identity. Nodes must have their identities

proven and verifiable within the network. The lower the reputation, the less likelihood of being able

15

to validate a block. In order to ensure the efficiency and security of the network, the group of validators

usually remains fairly small (25 or less). Although the conditions may vary from system to system,

there are three basic requirements to become a validator:

1. The identity must be formally confirmed with the ability to cross-reference such information

(e.g. address, phone number) in a public domain (public notary database)

2. The process of becoming a validator must be difficult to reduce the risks of selecting

questionable validators and incentivize the position and long-term commitment

3. The validator approval process must be consistent (standard) to ensure that all candidates

have an equal chance

Since PoA is designed to be less computationally intensive than PoW and has a limited number of

validators, it has the following advantages:

✓ The computational resources required for solving complex mathematical tasks (validating a

block) is far lower than PoW and PoS. Thus, a PoA network has a low requirement of

computational power, requiring significantly less power consumption.

✓ PoA has a high transaction rate as its transaction time is significantly faster than the

transaction time of PoW-based networks. Hence, it provides better performance.

✓ The interval of time it takes to validate blocks is predictable, unlike PoW and PoS consensuses

where this time varies.

The following figure summarizes the main pros and cons of PoA.

Pros Cons

Using PoA eliminates the possibility of an

attack since the validators are checked at the

stage of obtaining authority and are reliable.

With the use of PoA, decentralization is not

possible since a limited circle of people can

participate in block validation

It is an energy-efficient solution compared to

other consensus mechanisms

Although PoA can be used in public

blockchains, it is usually applied in private

blockchains requiring permission

Fast transaction processing Reputation cannot always keep participants

from malicious actions. If the reward for

fraud is more valuable than the authority, a

participant can harm the system

A new block is created in just 5 seconds, the

fees are extremely low, and network scaling

can occur horizontally, combining several

networks into one

16

Source: Changelly, “A Complete Guide to the Proof of Authority (PoA) Algorithm”, accessed on December 26,

2019.

The Concept of Forking

Changes to a blockchain network’s protocol and data structures are called forks. As a result of a fork,

a blockchain diverges into two potential paths forward, either with regards to a new rule (e.g.

validating transactions) or a transaction’s history. Reasons for effecting such a change/fork can occur

for various reasons, including:

• Add new functionality (e.g. making improvements)

• Correct security issues (e.g. addressing security risks)

• Reverse transactions (e.g. malicious transactions)

Forks are divided into two categories:

1. Hard forks

2. Soft forks

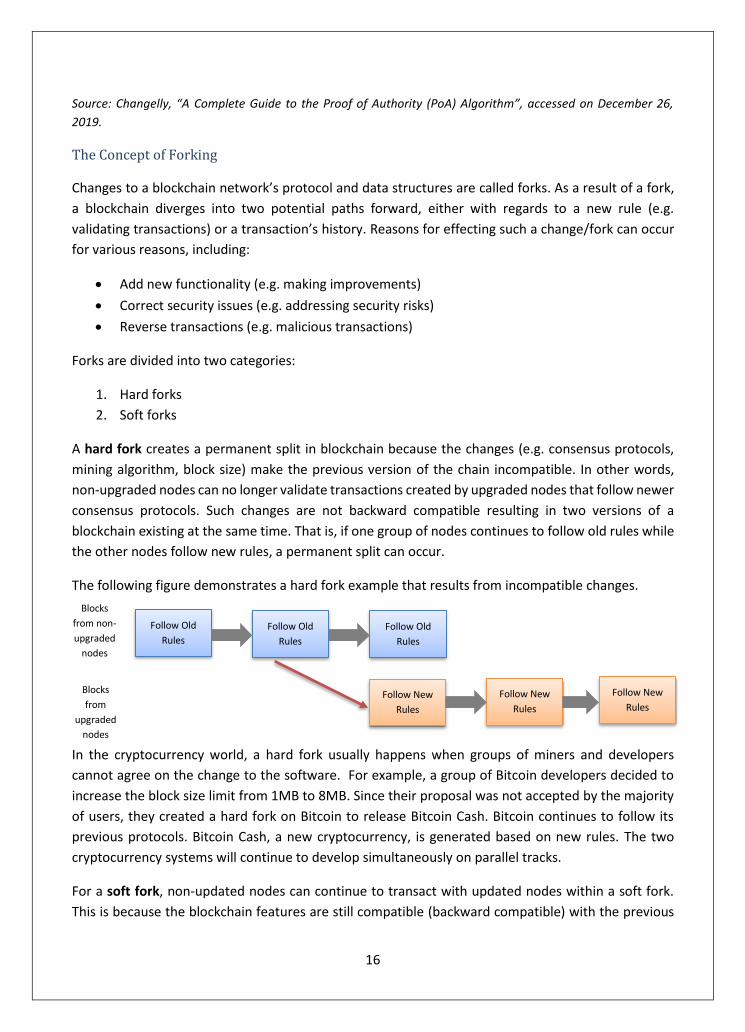

A hard fork creates a permanent split in blockchain because the changes (e.g. consensus protocols,

mining algorithm, block size) make the previous version of the chain incompatible. In other words,

non-upgraded nodes can no longer validate transactions created by upgraded nodes that follow newer

consensus protocols. Such changes are not backward compatible resulting in two versions of a

blockchain existing at the same time. That is, if one group of nodes continues to follow old rules while

the other nodes follow new rules, a permanent split can occur.

The following figure demonstrates a hard fork example that results from incompatible changes.

In the cryptocurrency world, a hard fork usually happens when groups of miners and developers

cannot agree on the change to the software. For example, a group of Bitcoin developers decided to

increase the block size limit from 1MB to 8MB. Since their proposal was not accepted by the majority

of users, they created a hard fork on Bitcoin to release Bitcoin Cash. Bitcoin continues to follow its

previous protocols. Bitcoin Cash, a new cryptocurrency, is generated based on new rules. The two

cryptocurrency systems will continue to develop simultaneously on parallel tracks.

For a soft fork, non-updated nodes can continue to transact with updated nodes within a soft fork.

This is because the blockchain features are still compatible (backward compatible) with the previous

Follow Old

Rules

Follow Old

Rules

Follow Old

Rules

Follow New

Rules

Follow New

Rules

Follow New

Rules

Blocks

from non-

upgraded

nodes

Blocks

from

upgraded

nodes

17

version of the chain which does not result in a duplication of the blockchain. For example, Segregated

Witness (SegWit), a Bitcoin protocol upgrade, is a soft fork designed to increase block capacity by

removing (“segregating”) digital signature (“witness”) data from transactions.

Hashing Process

Hashing is a process that converts an input of letters and numbers into an encrypted output of a fixed

length. The main use of a hash function is to verify the authenticity of a piece of data. A hash, a unique

fixed-length 32-byte identifier for every block, is the backbone of the blockchain network. It is

generated based on the information present in the block header. The use of a fixed-length output

drastically enhances the security of the data. If a hacker attempts to decrypt the hash, he or she cannot

tell how long or short the input is simply by looking at the length of the output.

Each block includes a timestamp and a link to a previous block through its hash, creating a literal

blockchain going back to the very beginning. In other words, the chain is “unbreakable” because the

hashing process of a new block always includes meta-data from the previous block’s hash output.

Therefore, it is nearly impossible to tamper with the stored information after it has been validated and

connected to a blockchain. If attempted, the subsequent blocks in the chain would reject the

attempted modification since their hashes would not be valid.

As blockchain uses the hashing process to link data items to each other, this technology makes it

challenging to tamper with a single record since a hacker would need to change the block containing

that record as well as those linked to it to avoid detection. The following graphic demonstrates how

the hash value is carried over to the next block in the chain to make the blockchain network generally

immutable.

Source: National Institute of Standards and Technology, “NISTIR 8202 Blockchain Technology Overview,”

accessed on November 24, 2019.

Cryptography

The records on a blockchain are secured through cryptography, the process of enforcing

authentication, data confidentiality, and data integrity, as opposed to those systems where the

transactions are channeled through a centralized trusted entity. Cryptography is the technique of

disguising and revealing, otherwise known as encryption and decryption, data through complex

18

mathematics. Thus, the information can only be viewed by the intended recipients. This cryptographic

technique allows each block to be broadcast to participants in the network in an encrypted form so

that the transaction details are not made public.

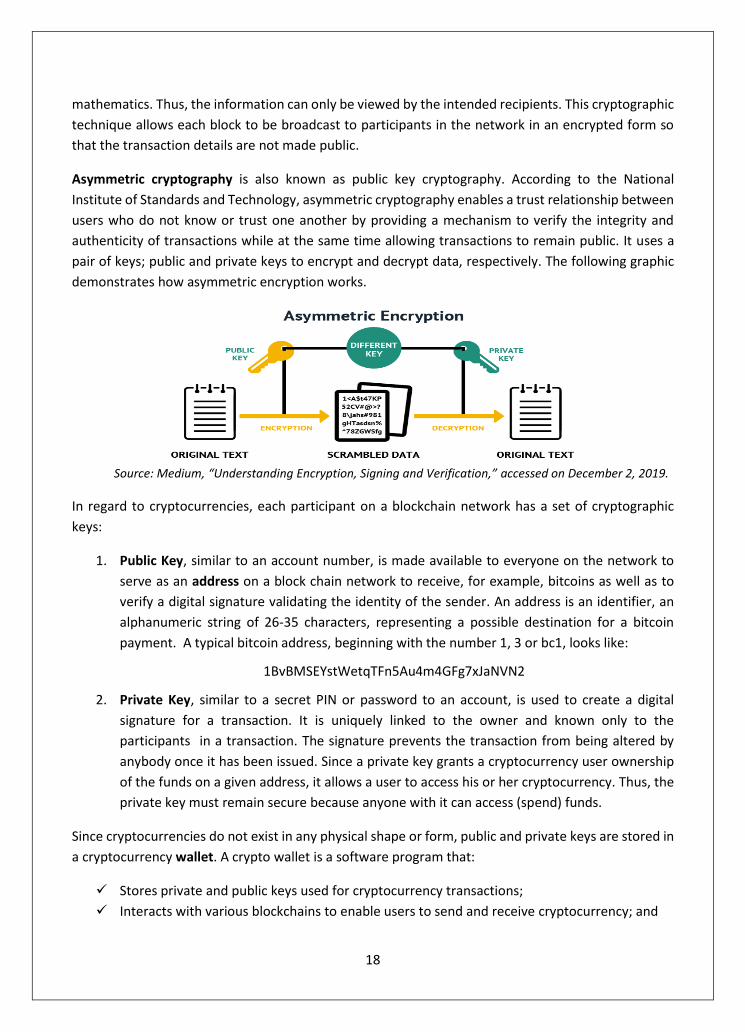

Asymmetric cryptography is also known as public key cryptography. According to the National

Institute of Standards and Technology, asymmetric cryptography enables a trust relationship between

users who do not know or trust one another by providing a mechanism to verify the integrity and

authenticity of transactions while at the same time allowing transactions to remain public. It uses a

pair of keys; public and private keys to encrypt and decrypt data, respectively. The following graphic

demonstrates how asymmetric encryption works.

Source: Medium, “Understanding Encryption, Signing and Verification,” accessed on December 2, 2019.

In regard to cryptocurrencies, each participant on a blockchain network has a set of cryptographic

keys:

1. Public Key, similar to an account number, is made available to everyone on the network to

serve as an address on a block chain network to receive, for example, bitcoins as well as to

verify a digital signature validating the identity of the sender. An address is an identifier, an

alphanumeric string of 26-35 characters, representing a possible destination for a bitcoin

payment. A typical bitcoin address, beginning with the number 1, 3 or bc1, looks like:

1BvBMSEYstWetqTFn5Au4m4GFg7xJaNVN2

2. Private Key, similar to a secret PIN or password to an account, is used to create a digital

signature for a transaction. It is uniquely linked to the owner and known only to the

participants in a transaction. The signature prevents the transaction from being altered by

anybody once it has been issued. Since a private key grants a cryptocurrency user ownership

of the funds on a given address, it allows a user to access his or her cryptocurrency. Thus, the

private key must remain secure because anyone with it can access (spend) funds.

Since cryptocurrencies do not exist in any physical shape or form, public and private keys are stored in

a cryptocurrency wallet. A crypto wallet is a software program that:

✓ Stores private and public keys used for cryptocurrency transactions;

✓ Interacts with various blockchains to enable users to send and receive cryptocurrency; and

19

✓ Monitors users’ balances in each cryptocurrency resulting from various transactions.

There are two types of cryptocurrency wallets:

1. Hot wallet is located in a device connected to the Internet (whether hosted or entity-

controlled). It allows users to send cryptocurrency to another address and to obtain an up-to-

date snapshot of all the entity’s recent cryptocurrency transactions and balances.

2. Cold wallet (cold storage) means generating and storing the private keys in an offline

environment (away from the Internet) since the online environment is very vulnerable to

hacking.

The basic distinction between the two is that hot wallets are connected to the Internet, while cold

wallets are kept offline. Since funds stored in a hot wallet are more accessible in comparison to funds

in a cold wallet, they are more vulnerable to hacking and phishing. In other words, cold wallets usually

maintain higher levels of security than hot wallets. There are different choices of cold wallets, such as

a hardware wallet or a paper wallet.

• Hardware wallets are located on a USB or other device. The entity’s private and public keys

are generated in the device when it is offline by using a random number generator.

• Paper wallets are a paper record of the entity’s private keys and related information. When

the entity’s computer or other devices and printer are offline, software is used to generate a

set of private and public keys and related addresses for its cold wallet.

In the asymmetric method, anyone can encrypt messages using the public key, but only the holder of

the paired private key can decrypt. That is, a person can encrypt a message using the receiver’s public

key, but it can be decrypted only by the receiver's private key. Security relies on the secrecy of the

private key. Each transaction is protected through a digital signature. The sender and the recipient

interact directly with each other and there is no need for verification by a trusted third-party.

Identifying information is also encrypted. If a record is altered, the signature will become invalid and

the peer network will know right away that something has happened. Early notification is critical to

preventing further damage.

The private key must be backed up and protected from accidental loss. Private keys are like physical

dollar bills. If they are lost, they cannot be recovered; the funds are forever lost, too. The holders,

unfortunately, lose the ability to sell or transfer the crypto funds attached to those keys.

20

Self-Executing Agreement

“A smart contract is a computerized transaction protocol that executes the terms of a contract. The

general objectives are to satisfy common contractual conditions.”

Nick Szabo, Cryptographer

Another important benefit of certain blockchains is that they can create “smart contracts”. Although

the concept of a smart contract was first introduced in 1994 by Nick Szabo, it was only with blockchain

technology that smart contracts were able to facilitate and verify the performance of a contract.

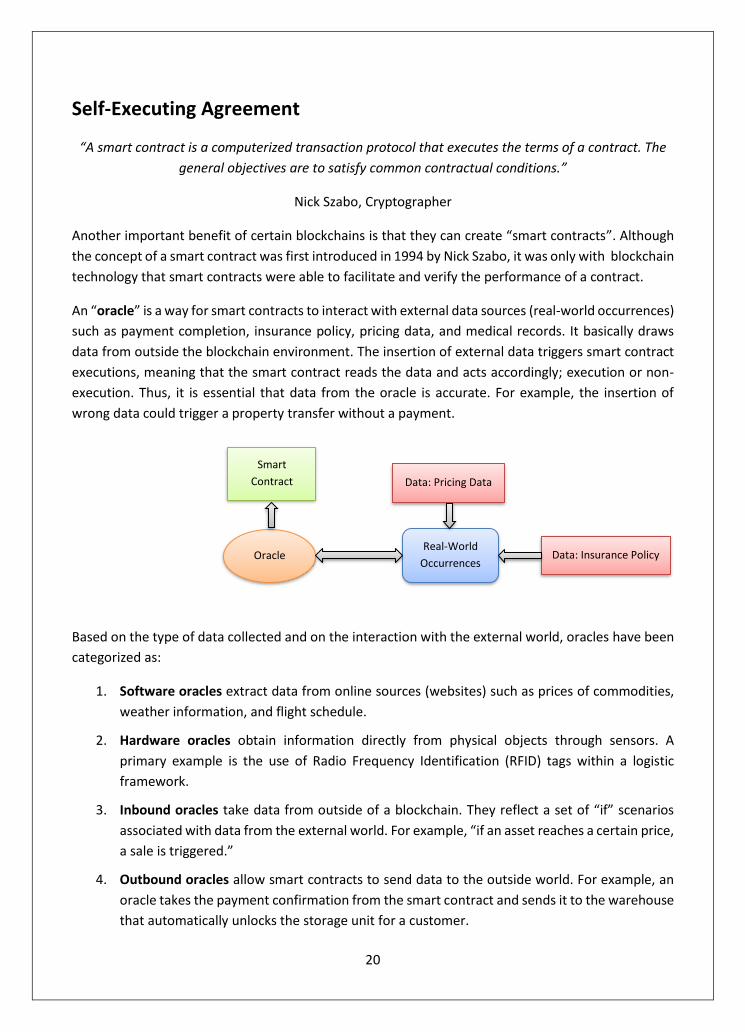

An “oracle” is a way for smart contracts to interact with external data sources (real-world occurrences)

such as payment completion, insurance policy, pricing data, and medical records. It basically draws

data from outside the blockchain environment. The insertion of external data triggers smart contract

executions, meaning that the smart contract reads the data and acts accordingly; execution or non-

execution. Thus, it is essential that data from the oracle is accurate. For example, the insertion of

wrong data could trigger a property transfer without a payment.

Based on the type of data collected and on the interaction with the external world, oracles have been

categorized as:

1. Software oracles extract data from online sources (websites) such as prices of commodities,

weather information, and flight schedule.

2. Hardware oracles obtain information directly from physical objects through sensors. A

primary example is the use of Radio Frequency Identification (RFID) tags within a logistic

framework.

3. Inbound oracles take data from outside of a blockchain. They reflect a set of “if” scenarios

associated with data from the external world. For example, “if an asset reaches a certain price,

a sale is triggered.”

4. Outbound oracles allow smart contracts to send data to the outside world. For example, an

oracle takes the payment confirmation from the smart contract and sends it to the warehouse

that automatically unlocks the storage unit for a customer.

Smart

Contract

Oracle Real-World

Occurrences

Data: Pricing Data

Data: Insurance Policy

21

Smart contracts are self-executing because they constitute lines of codes (e.g. pre-defined rules)

around an agreement that automate the contracting process and enable monitoring and enforcement

of contractual promises. Transactions are self-verifiable and tamper-proof. Therefore, unlike a

traditional contract where parties need remedial action through the legal system, self-executed smart

contracts eliminate the need for middlemen and keep the system conflict-free. For example, money

can only be sent from Alice to Bob if the conditions of an agreement are met: 1) date equals “January

1, 2020”, and 2) “Bob’s balance is less than 10 bitcoin”. If these conditions are met, the smart contract

executes itself to produce the output.

Since smart contracts enable decentralized automation by facilitating, verifying or enforcing the

negotiation or performance of a contract, they allow people to exchange anything of value, such as

money, shares, or property in a transparent manner. The Real Estate industry has experienced many

notable advantages of smart contracts. For example, the act of buying and transferring ownership of

property remains a tedious and lengthy process. These transfers typically need to be reviewed and

confirmed by multiple third parties such as escrow agents, lawyers, and governmental bodies.

Ethereum, a decentralized platform, utilizes smart contracts and as a result, it could be used to

automatically transfer homeownership to a buyer, and the funds to a seller, after a deal is agreed upon

without needing a third party to execute it on their behalf. Because the process is simplified, both the

buyer and the seller can save money and time.

Lesson Note: Management is responsible for establishing controls to ensure that the smart contract

source code is consistent with the intended business logic. An auditor should consider management’s

controls over the smart contract code.

Smart contracts are also beneficial in the cases of manual operations and lack of automation. For

instance, claim processing usually takes a significant amount of resources and time in insurance

administration. The use of smart contracts simplifies and streamlines processes by automatically

triggering payments for claims when certain agreed upon conditions between the company and the

customer are met.

The following table summarizes the differences between traditional contracts and smart contracts.

Traditional Contracts Smart Contracts

• 1-3 Days

• Manual remittance

• Escrow necessary

• Expensive

• Physical presence (wet signature)

• Lawyers necessary

• Minutes

• Automatic remittance

• Escrow may not be necessary

• Fraction of the cost

• Virtual presence (digital signature)

• Lawyers may not be necessary Source: PwC, “How Smart Contracts Automate Digital Business?”, 2016

22

Illustration: Crypto Transactions on a Blockchain

The following example demonstrates how blockchain technology allows for payments to move from

one party to another without going through a central or commercial bank.

Both Alice and Bob use a bitcoin wallet to make transactions. A wallet is specialized software that

calculates the balance of the user by keeping track of all incoming and outgoing payments.

All transactions are verified by network nodes through cryptography and recorded in a public

distributed ledger. Anyone with bitcoin can participate in the network, send and receive bitcoin, and

even hold a copy of this ledger. A bitcoin or a transaction cannot generally be changed, erased, copied,

or forged as everybody would know.

When Alice clicks ‘send’ in her wallet, the transaction gets propagated across the network. That is, she

broadcasts a message with the transaction that she wants to make to all the miners in the network as:

“Alice owns one bitcoin that lives at this address (insert bitcoin address). Alice wishes to send this

bitcoin to Bob at this address (BTC address)”.

While Alice publicly announces her intention, she must also securely send Bob the private key that

enables Bob to unlock the transaction and prove he is now the rightful owner. While the Bitcoin

network can always see the public address, it can never see the private key.

Within seconds most of the network knows about this transaction and Bob sees a new pending

transaction. In that transaction, Alice provides the miners with Bob's address and the number of

bitcoins she would like to send, along with a digital signature and her public key. The signature is made

with Alice's private key and the miners can validate that Alice, in fact, is the owner of those coins. Once

miners validate the transaction via the consensus mechanism protocol, they add the transaction to

the blockchain (hashing process). Now Bob will see in his wallet that the transaction is confirmed. It

means that by now it is recorded in the blockchain and cannot be reversed.

If Alice or Bob wanted to falsify a transaction, they would have to compromise the majority of

participants. This is much harder than compromising a single participant. Alice cannot claim that she

never sent a bitcoin/digital token to Bob because her ledger would not agree with everyone else’s.

Bob cannot claim that Alice gave him two bitcoins/tokens as his ledger would be out of sync.

23

Review Questions - Section 1

1. What is a basic feature of a blockchain platform?

A. A need for middlemen

B. Single point of control

C. Peer-to-peer network

D. Use of symmetric cryptography

2. Which of the following describes a potential attack on a peer network, where a person attempts

to gain control over the network by creating a large number of accounts?

A. Botnets

B. Sybil attack

C. Distributed denial-of-service

D. IP spoofing

3. What is the method that prevents “double-spending” in cryptocurrency exchanges?

A. Encryption

B. Block reward

C. Halving

D. Consensus algorithm

4. What is Proof of Work (PoW)?

A. A process of encoding and decoding information

B. A destination where a user sends and receives digital currency

C. A software program used to store private and public keys

D. A consensus protocol used to confirm transactions and produce new blocks to the chain

5. All of the following conditions must be satisfied in order to become validators in PoA EXCEPT:

A. Their identities need to be confirmed

B. High performance computer hardware is required

C. Eligibility is difficult to obtain

D. The selection process is standard

24

6. What is the term that describes a permanent split in a blockchain resulting from a change in

protocol and data structures?

A. 51% attack

B. Double-spending

C. Selfish mining

D. Hard fork

7. What is a change to blockchain protocol that is backward-compatible?

A. Soft fork

B. Hashing

C. Mining

D. Hard fork

8. What is the method that secures blockchain transactions by assuring the authentication and

confidentiality?

A. Hot wallet

B. Firewall

C. Cold storage

D. Cryptography

9. What does asymmetric encryption use?

A. Public keys only

B. Private keys only

C. Proof of Work

D. Public and Private keys

10. Which of the following describes an alphanumeric string of 26-35 characters that represents a

possible destination for a bitcoin payment?

A. Hash

B. Address

C. Wallet

D. Digital Signature

11. Which of the following techniques enables automation of the contracting process by facilitating,

verifying or enforcing the negotiation or performance of a contract?

A. Proof of Work

B. Smart contract

C. A stealth address

D. Hashing algorithm

25

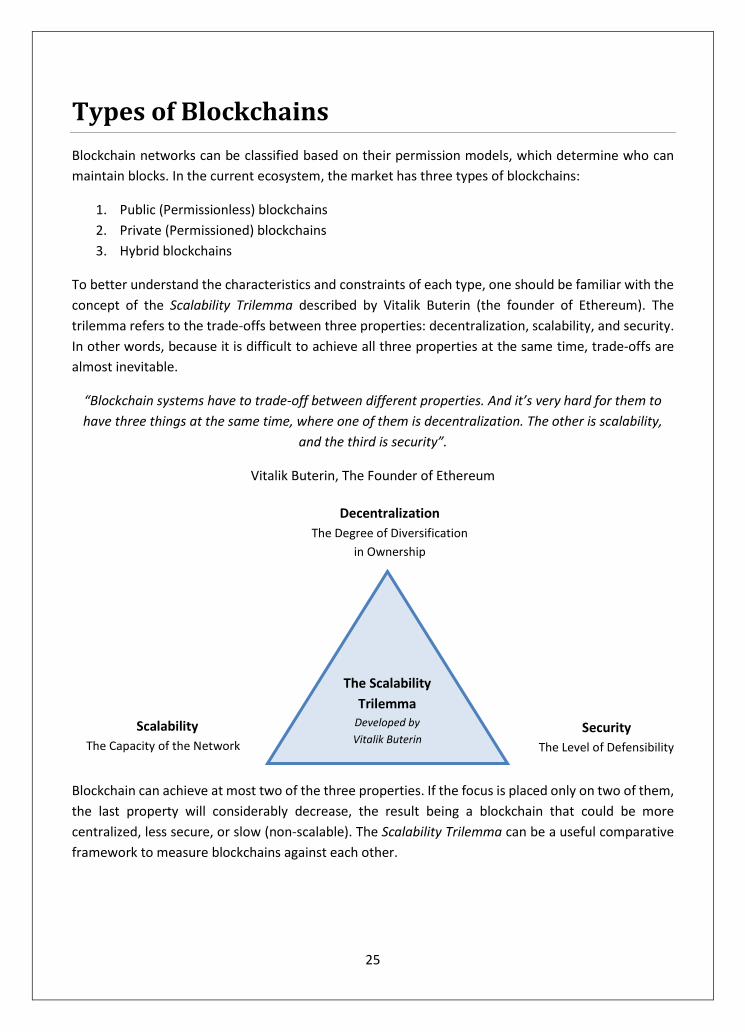

Types of Blockchains

Blockchain networks can be classified based on their permission models, which determine who can

maintain blocks. In the current ecosystem, the market has three types of blockchains:

1. Public (Permissionless) blockchains

2. Private (Permissioned) blockchains

3. Hybrid blockchains

To better understand the characteristics and constraints of each type, one should be familiar with the

concept of the Scalability Trilemma described by Vitalik Buterin (the founder of Ethereum). The

trilemma refers to the trade-offs between three properties: decentralization, scalability, and security.

In other words, because it is difficult to achieve all three properties at the same time, trade-offs are

almost inevitable.

“Blockchain systems have to trade-off between different properties. And it’s very hard for them to

have three things at the same time, where one of them is decentralization. The other is scalability,

and the third is security”.

Vitalik Buterin, The Founder of Ethereum

Blockchain can achieve at most two of the three properties. If the focus is placed only on two of them,

the last property will considerably decrease, the result being a blockchain that could be more

centralized, less secure, or slow (non-scalable). The Scalability Trilemma can be a useful comparative

framework to measure blockchains against each other.

The Scalability

Trilemma Developed by

Vitalik Buterin

Decentralization

The Degree of Diversification

in Ownership

Scalability

The Capacity of the Network

Security

The Level of Defensibility

26

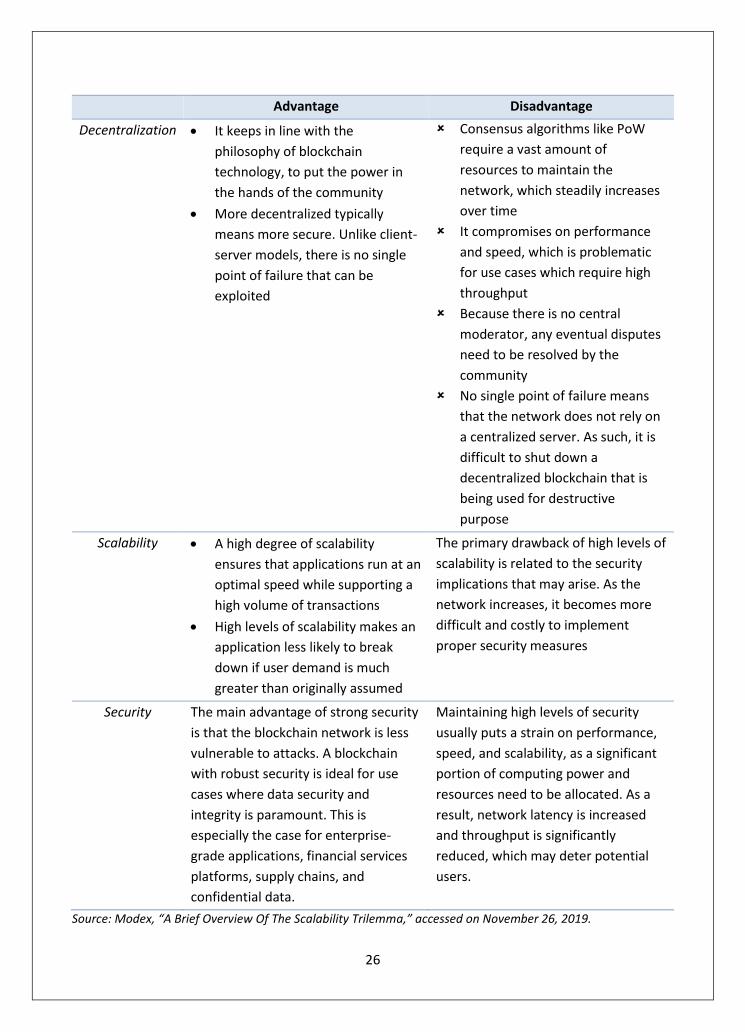

Advantage Disadvantage

Decentralization • It keeps in line with the

philosophy of blockchain

technology, to put the power in

the hands of the community

• More decentralized typically

means more secure. Unlike client-

server models, there is no single

point of failure that can be

exploited

Consensus algorithms like PoW

require a vast amount of

resources to maintain the

network, which steadily increases

over time

It compromises on performance

and speed, which is problematic

for use cases which require high

throughput

Because there is no central

moderator, any eventual disputes

need to be resolved by the

community

No single point of failure means

that the network does not rely on

a centralized server. As such, it is

difficult to shut down a

decentralized blockchain that is

being used for destructive

purpose

Scalability • A high degree of scalability

ensures that applications run at an

optimal speed while supporting a

high volume of transactions

• High levels of scalability makes an

application less likely to break

down if user demand is much

greater than originally assumed

The primary drawback of high levels of

scalability is related to the security

implications that may arise. As the

network increases, it becomes more

difficult and costly to implement

proper security measures

Security The main advantage of strong security

is that the blockchain network is less

vulnerable to attacks. A blockchain

with robust security is ideal for use

cases where data security and

integrity is paramount. This is

especially the case for enterprise-

grade applications, financial services

platforms, supply chains, and

confidential data.

Maintaining high levels of security

usually puts a strain on performance,

speed, and scalability, as a significant

portion of computing power and

resources need to be allocated. As a

result, network latency is increased

and throughput is significantly

reduced, which may deter potential

users.

Source: Modex, “A Brief Overview Of The Scalability Trilemma,” accessed on November 26, 2019.

27

Public Blockchains

Public (permissionless) blockchain networks allow every participant to submit transactions and add

entries to the ledger as no permission is required to join the network. The operation is like the public

internet, where anyone can participate. In other words, any participants can read and write to the

ledger. Thus, to prevent manipulation and protect the integrity of data, blockchain applies consensus-

based validation mechanisms (e.g. proof of work).

Although no personal information is shared and identifying data is encrypted, each participant has a

public address that theoretically could be traced back to an IP address or exchange account (through

proper network analysis). For this reason, transactions are not entirely anonymous, but they are

pseudonymous. The vast majority of cryptocurrencies currently in circulation are based on public

blockchains (e.g. Bitcoin, Bitcoin Cash, Ethereum, and Litecoin). However, public blockchains have

limited applications in the financial industry due to the public nature of transactions and limited

functionality support at a protocol level.

Public blockchains have no single owner. They are far more decentralized than a private

(permissioned) system because anyone can join the network. However, scalability is the trade-off,

meaning that public blockchains are usually slower than private blockchains. This is because of the

computational power required to maintain public blockchains and assure consensus. Consequently, as

the volume of transactions and the number of individuals joining the network increases, the longer it

takes to process these transactions (e.g. validation), especially during peak hours.

Bitcoin, in its current form, can process approximately seven transactions per second. Ethereum can

handle 20 transactions per second. Comparable traditional centralized payment systems, such as VISA,

MasterCard, and PayPal, offer significantly higher transactions per second. For instance, VISA handles

150 million transactions per day, averaging roughly 1,700 transactions per second6. PayPal currently

processes 193 transactions per second. Finally, the costs of processing a transaction usually increase

as the network’s usage rises7.

6 Data on Bitcoin and VISA transactions speed statistics are from “Bitcoin vs. Bitcoin Cash: What is the Difference?,” Investopedia, with values accessed on November 26, 2019. 7 Data on Ethereum and PayPal are from “Transactions Speeds: How Do Cryptocurrencies Stack Up To VISA or PayPal?”, howmuch.net, with values as accessed on December 26, 2019.

28

Real-World Case: A Peer-to-Peer Electronic Cash System

“What is needed is an electronic payment system based on cryptographic proof instead of trust,

allowing any two willing parties to transact directly with each other without the need for a trusted

third party. Transactions that are computationally impractical to reverse would protect sellers from

fraud…. The system is secure as long as honest nodes collectively control more CPU power than any

cooperating group of attacker nodes.”

Satoshi Nakamoto, The Founder of Bitcoin

Bitcoin, the first permissionless blockchain, is public and open to all. It permits the transfer of currency

online, directly, and independent of central control. Bitcoin, an example of convertible virtual

currency, is used for retail purchases and investments. For example, it can be digitally traded between

users and can be purchased for, or exchanged into, U.S. dollars, Euros, and other real or virtual

currencies. Many merchants (e.g. Internet, real-world places) accept bitcoin as payment today

including:

✓ Overstock.com is the first major online retailer to accept bitcoin

✓ Microsoft accepts bitcoin payments for a variety of digital content

✓ Dell allows customers to buy computers and hardware with bitcoin

✓ DISH Network, the first subscription model pay-TV provider to accept bitcoin, added Bitcoin Cash

as a payment option

✓ Expedia accepts bitcoin for hotel bookings

Bitcoin remains the most well-known and widely used cryptocurrency, accounting for 72% of the

market8. This is the only type of virtual currency that has the potential to compete with traditional

currency.

In late 2019, there were about 18 million bitcoins in circulation. This number changes about every 10

minutes when new blocks are mined. Currently, each new block adds 12.5 bitcoins into circulation,

and 144 blocks per day are mined on average. So, the average amount of new bitcoins mined per day

is 1,800 (12.5 x 144) 9.

8 Data on cryptocurrency market valuations are from “Cryptocurrency Market Capitalizations,” CoinMarketCap, with values as accessed on September 20, 2019. 9 Data on bitcoin statistics are from “How Many Bitcoins Are There?,” Buy Bitcoins Worldwide, with values as accessed on December 26, 2019.

29

Private Blockchains

Private (permissioned) blockchains restrict access regarding who can perform different activities on

the network. The system operates similarly to a privately maintained database that is controlled by

giving read privileges to outsiders. For example, the owner (a single authority or an organization) of a

private blockchain has the ability to dictate who can and cannot become part of its network. That is,

only authorized participants are allowed write and read privileges.

Transaction processing and extension of the blockchain is performed by a set of known and accepted

nodes. Each participant of a private network knows the identity of the counterparty on the other side

of a transaction. This feature is critical to financial services due to anti-money laundering and know-

your-customer (“KYC”) considerations. Private blockchains also use consensus models (e.g. proof-of-

stake) for publishing blocks.

Since the participation is limited and controlled, private blockchains have a number of advantages over

public networks such as greater scalability, lower transaction costs, increased privacy, and less

vulnerability to malicious attacks. A private blockchain typically can process much higher transaction

volumes at higher speeds because, unlike public blockchains, it does not require significant

computational resources. For example, XRP is the cryptocurrency used by the Ripple payment

network. Built for enterprise use, XRP aims to be a fast, cost-efficient cryptocurrency for cross-border

payments. The Ripple platform is designed to allow fast and cheap transactions.

Private blockchains can also be for internal enterprise use, such as auditing and database

management. There are also some applications in the public sector, such as government budget or

government-industry statistics, which are usually managed by the government but can be made

available for the public to view.

Private blockchains may also be used by organizations that need to more tightly control and protect

their information. For instance, certain private blockchains require all members to be authorized to

send and receive transactions. In this case, members are not anonymous or pseudo-anonymous. This

feature discourages fraudsters since they can be identified. Thus, private blockchains can be beneficial

when transaction-processing nodes need to be known to comply with regulations. Other examples of

private blockchains include asset management. The most known examples of private blockchains are

Hyperledger Fabric and R3 Corda.

The following table summarizes the differences between the public and private blockchains.

30

Characteristics Public (Permissionless) Private (Permissioned)

Access Open and Transparent Access Authorized Members Only

Read Open to Anyone Authorized Members Only

Write Anyone Authorized Operators Only

Performance Slower Faster

Scalability Limited Scalability Highly Scalable

*Consensus Proof-of-Work (Mining) or

Proof-of-Stake

Proof-of-Stake or

Pre-approved participation

Transaction Cost Higher Low

Access Control Same Access Level for All

Participants

Full Control over Members

Access

Identify Anonymous or Pseudo

Anonymous Known

*: The concept of consensus is explained in “A Self-Regulating Ecosystem”.

Source: Business Blockchain HQ, “Blockchain Fundamentals,” accessed on November 12, 2019.

The following table identifies a list of opportunities and challenges auditors face in permissionless and

permissioned blockchains.

Opportunities Challenges

Permissionless • Examine transaction record on

blockchain;

• Develop novel audit process on

blockchain transactions;

• Verify the consistency between

items on blockchain and in the

physical world.

No reversal of erroneous

transactions;

No centralized authority to verify

the existence, ownership, and

measurement of items recorded

on blockchain;

Data retrieval due to clients’ loss of

private key;

No centralized authority to report

cyberattacks.

Need to be proficient in various

blockchain technologies;

Difficult to reach consensus rules

among all participants, when

acting as an organizational agent;

Audit transaction linked to a side

agreement that is ‘‘off-chain’’;

Tackle the situation when central

authority has the power to

Permissioned • Develop guidelines for blockchain

implementation;

• Leverage industry knowledge and

experience to offer advice for best

practices for blockchain consensus

protocols;

• Leverage business networks to

form permissioned blockchain

based on market demand;

31

• Act as planner and coordinator of

potential participants of a

blockchain;

• Leverage their expertise on IT

auditing to audit internal control of

blockchain, including data integrity

and security;

• Offer independent rating services

to a specific blockchain;

• Act as administrator of blockchain.

override information on

blockchain;

Cope with change of consensus

protocol in a blockchain.

Source: American Accounting Association, “How Will Blockchain Technology Impact Auditing and Accounting:

Permissionless versus Permissioned Blockchain”, Current Issues in Auditing Vol. 13, No. 2 Fall 2019.

Real-World Case: Blockchain for the Financial Industry

Quorum is an enterprise-focused, open-source version of Ethereum created by J.P. Morgan. Quorum

is designed to address specific challenges to blockchain technology adoption within the financial

industry and supports blockchain transactions amongst a permissioned group of known participants

J.P. Morgan

Quorum, developed by J.P. Morgan, offers an enterprise-focused and permitted blockchain. It will

become the first distributed ledger platform available through Azure Blockchain Service, allowing J.P.

Morgan and Microsoft customers to build and scale blockchain networks in the cloud. The principle of

Quorum is to apply cryptography to prevent all except those parties to the transaction from seeing

sensitive data. The solution involves a single shared blockchain and a combination of smart contract

software architecture and modifications to Ethereum. Quorum Whitepaper provides a high-level

overview of the Quorum blockchain platform:

Built on Ethereum

• First mover advantage. In production since July 2015

• 50,000 + unit tests, Security Audits, Bounty Program

• Largest Ecosystem of Developers, Tools DApp’s

• Public Ethereum blockchain protect over $1B + Ether

Simple Privacy Design

• Supports both private and public transactions and smart contracts

Single Blockchain Architecture

32

• All public and private smart contracts and state derived from a single, common, complete

blockchain of transactions validated by every node in the network

• Private smart contract state validated by parties to contract only

• Best of both worlds…every node validating the list of transactions while only exposing details of

private transactions and contracts to relevant parties

High Performance

• Able to process dozens to hundreds of transactions per second, depending on system

configuration; enough to support institutional volumes