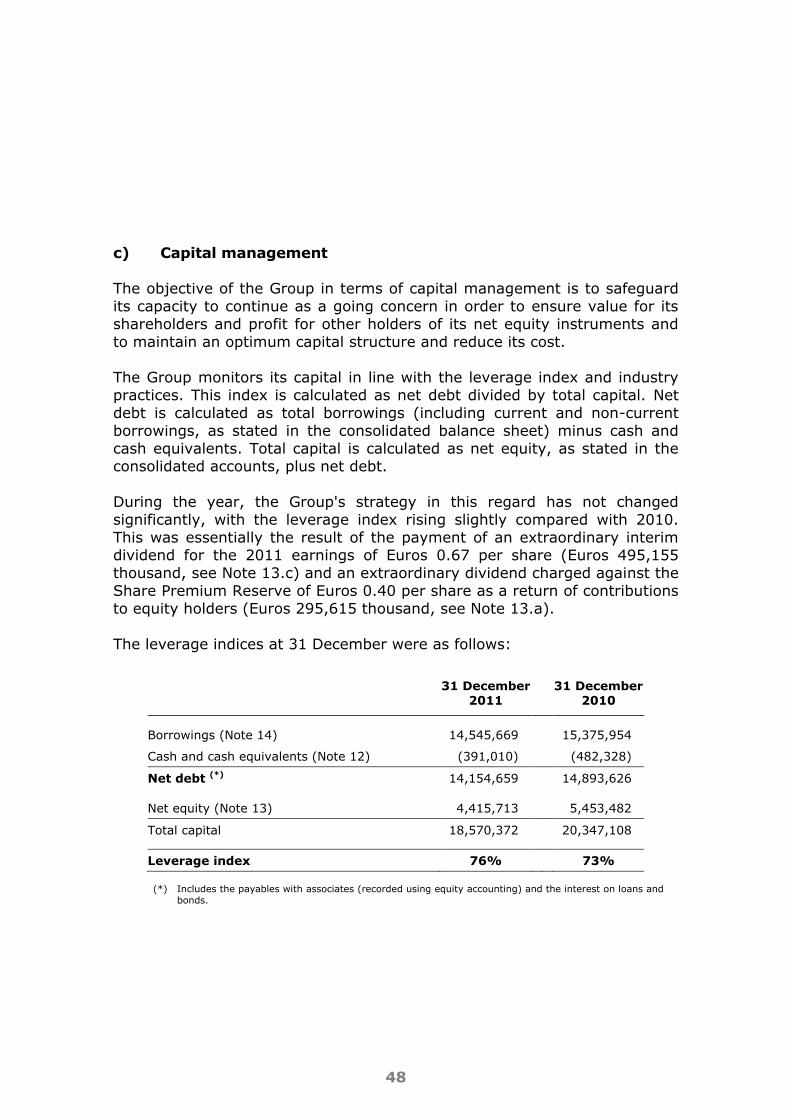

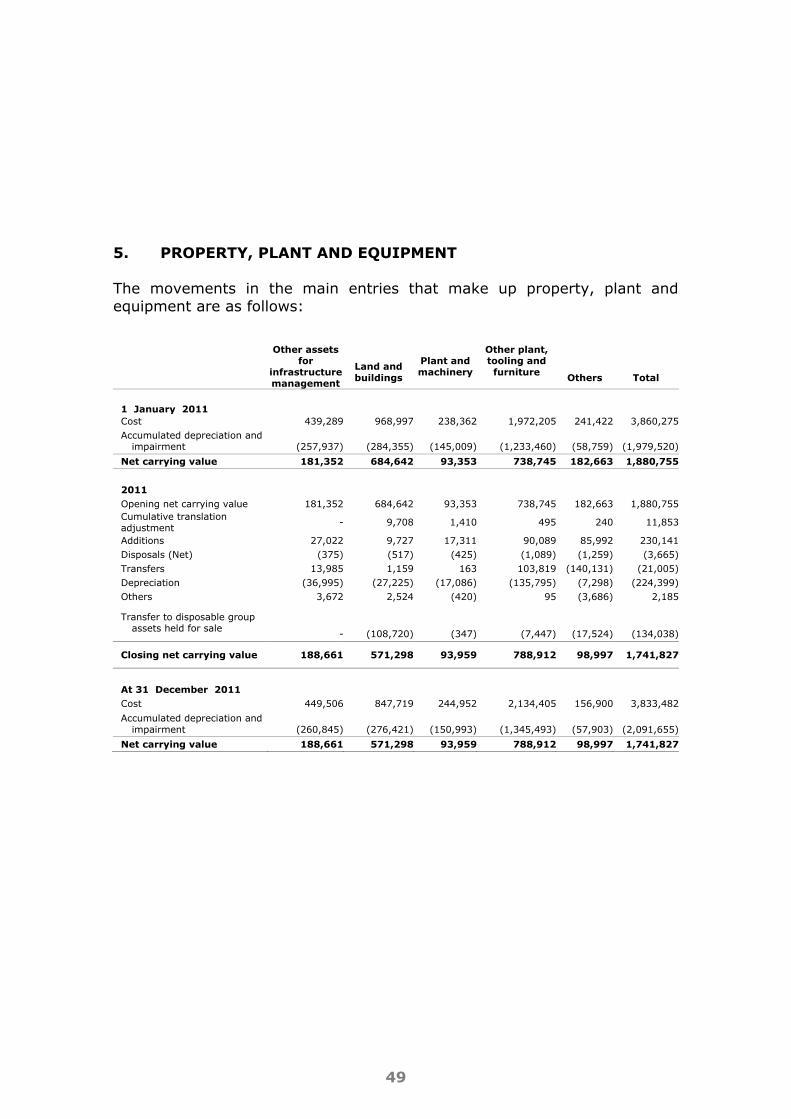

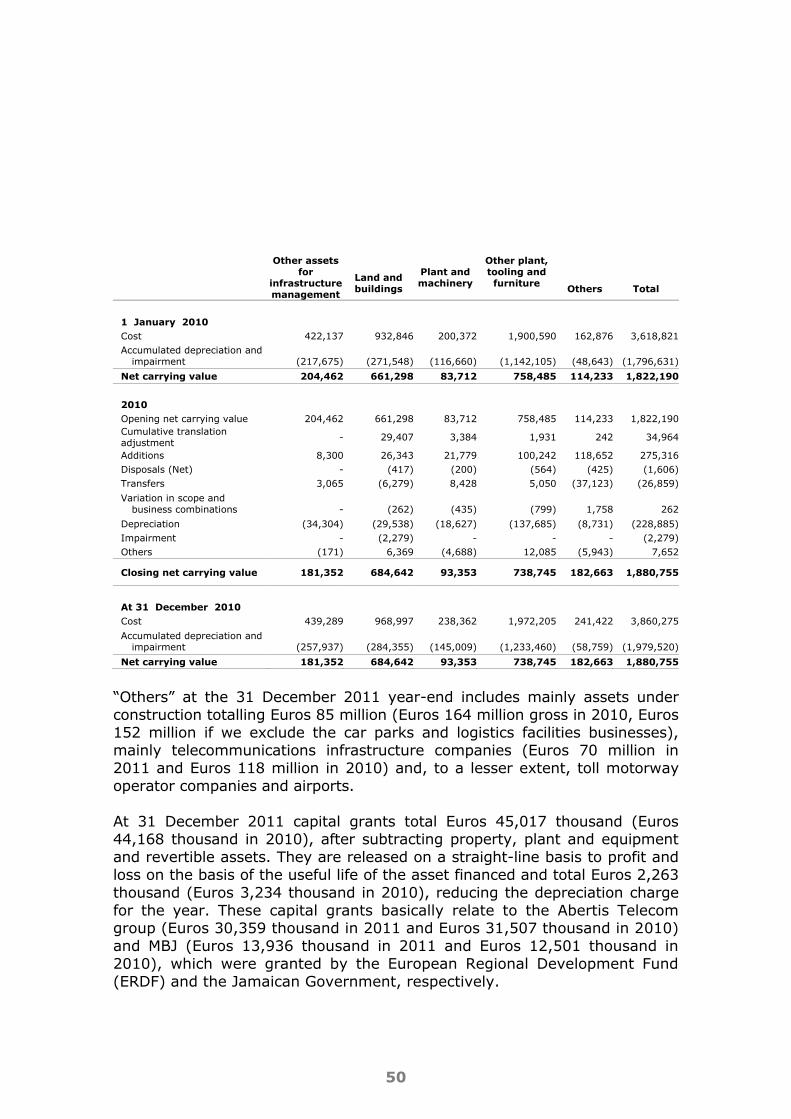

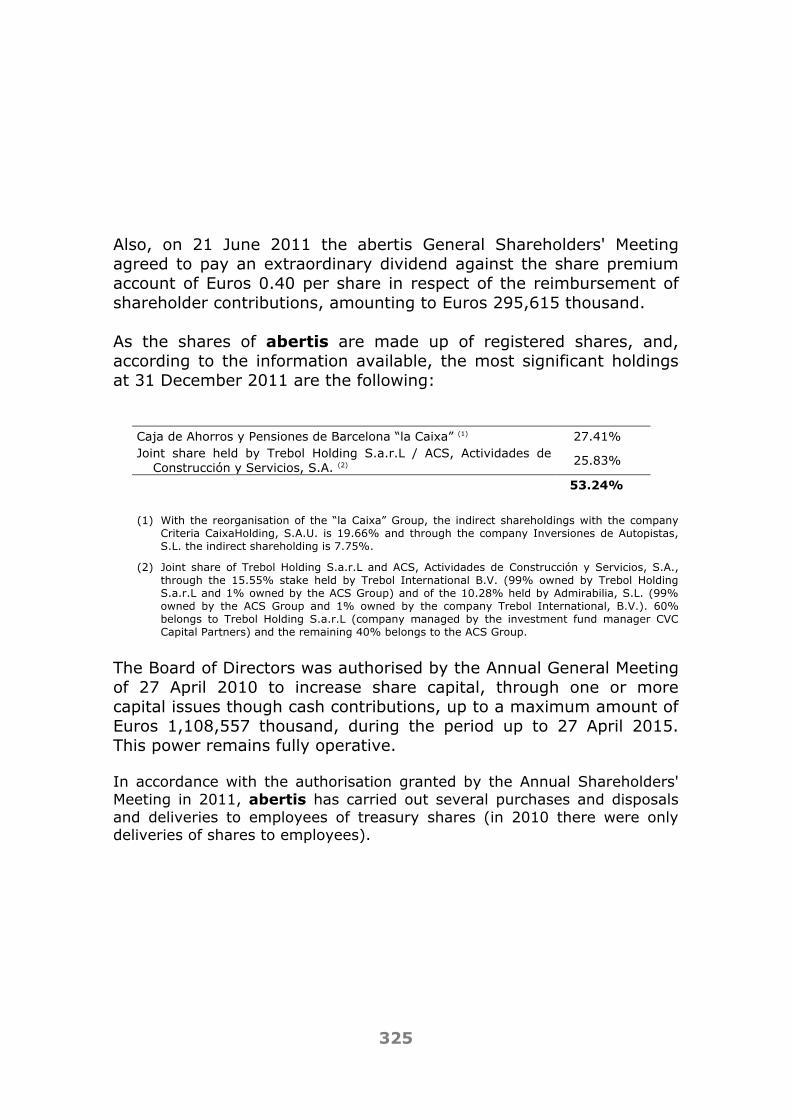

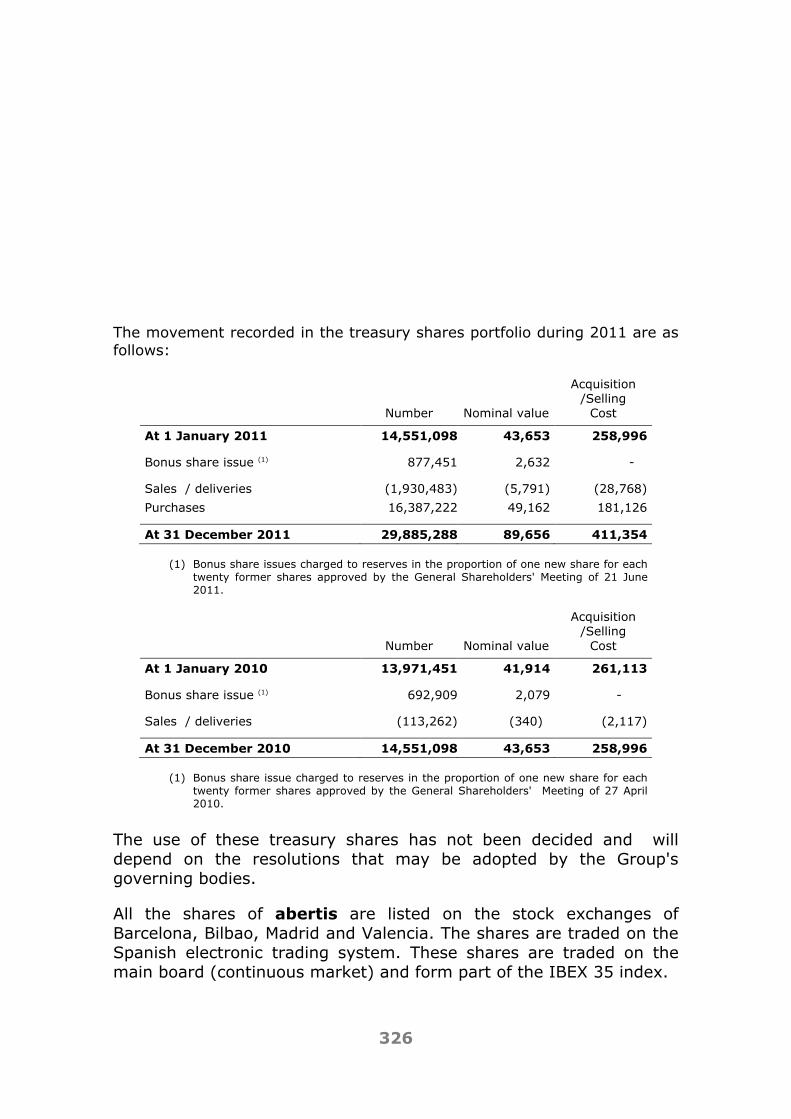

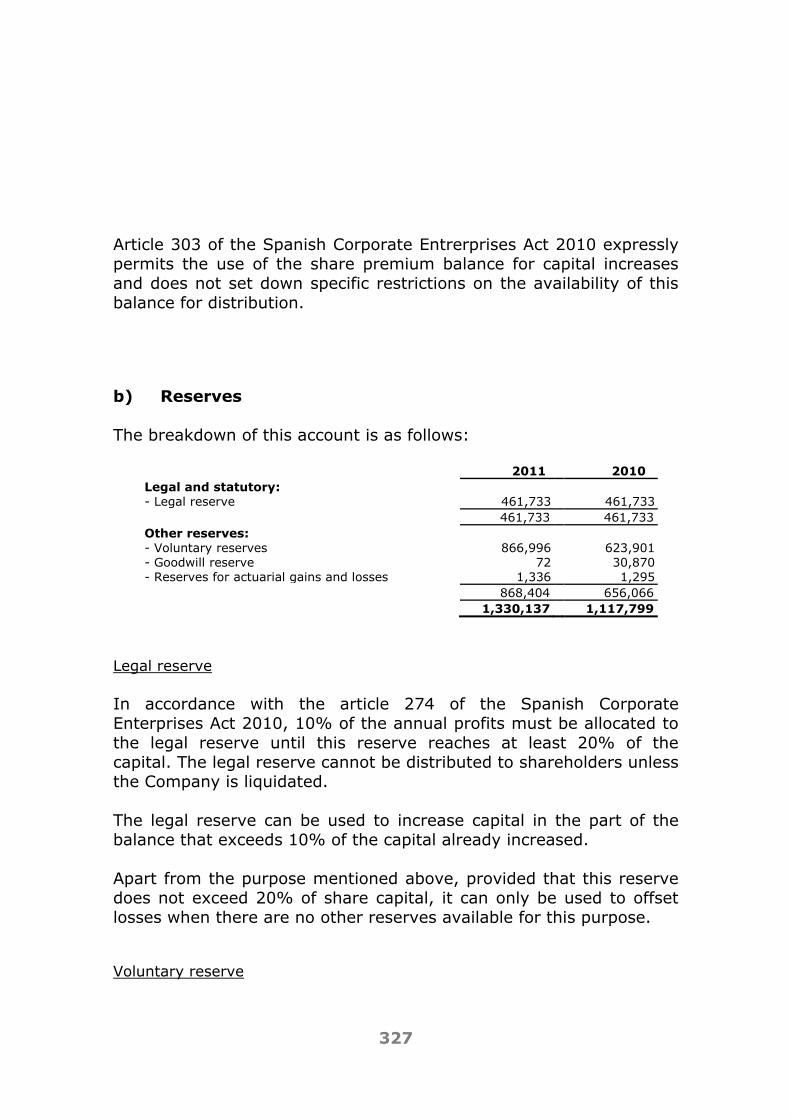

annual accounts 2012 abertis

DESCRIPTION

TRANSCRIPT

1

ABERTIS INFRAESTRUCTURAS, S.A.

AND SUBSIDIARY COMPANIES

Consolidated Annual Accounts and Consolidated Directors’ Report

Year Ended 31 December 2011 (prepared under International Financial Reporting Standards)

2

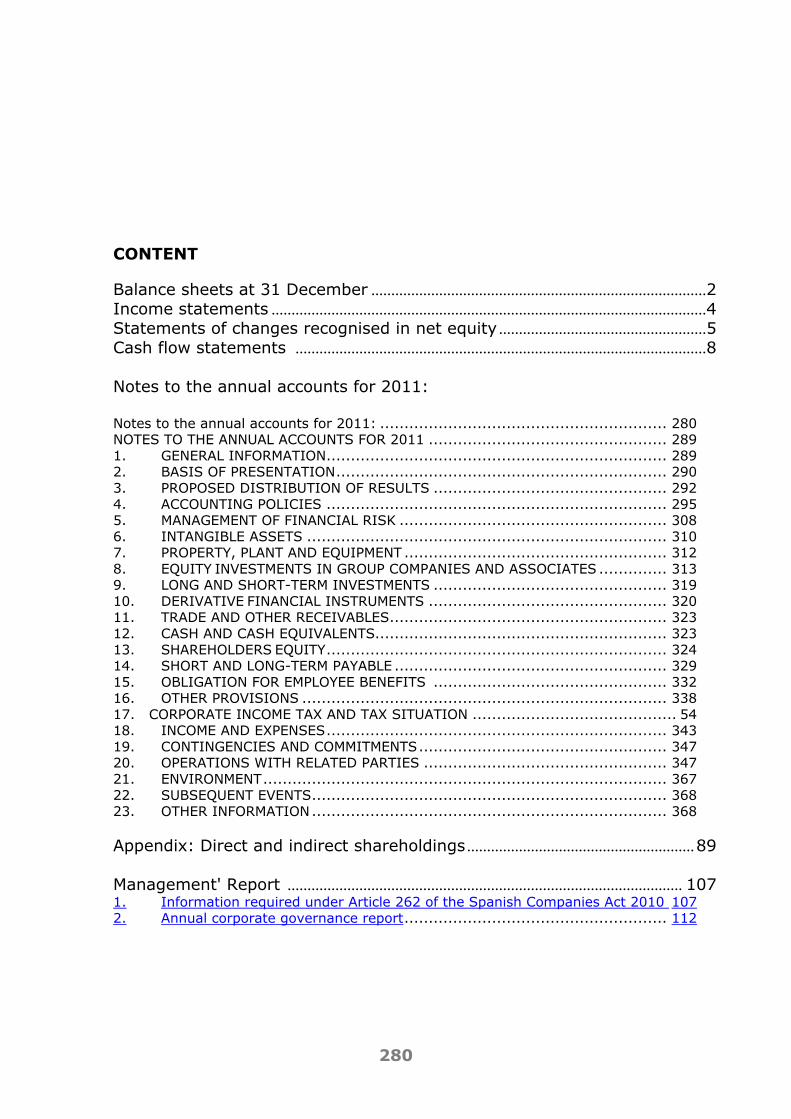

INDEX

Consolidated Balance Sheets at 31 December ....................................................... 3 Consolidated Income Statements at 31 December ................................................. 5 Consolidated Statements of Comprehensive Income at 31 December ....................... 6 Statement of Changes in Consolidated Net Equity ................................................. 7 Consolidated Cash Flow Statements .................................................................... 8

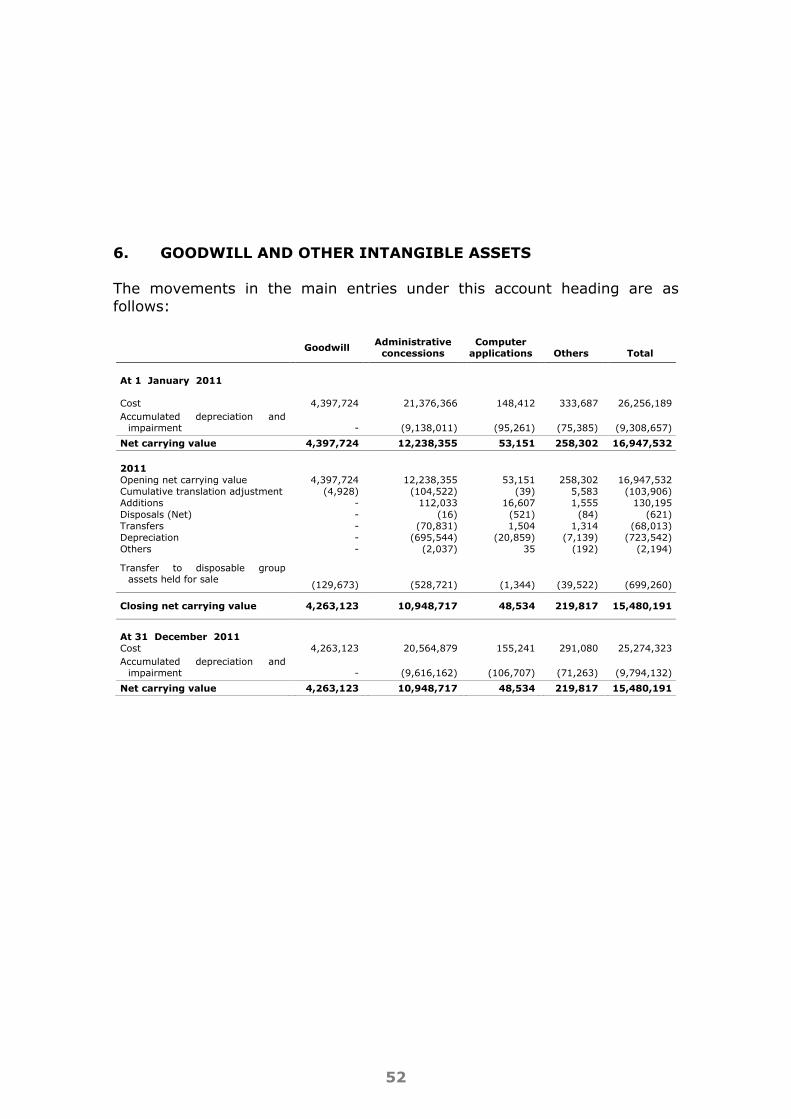

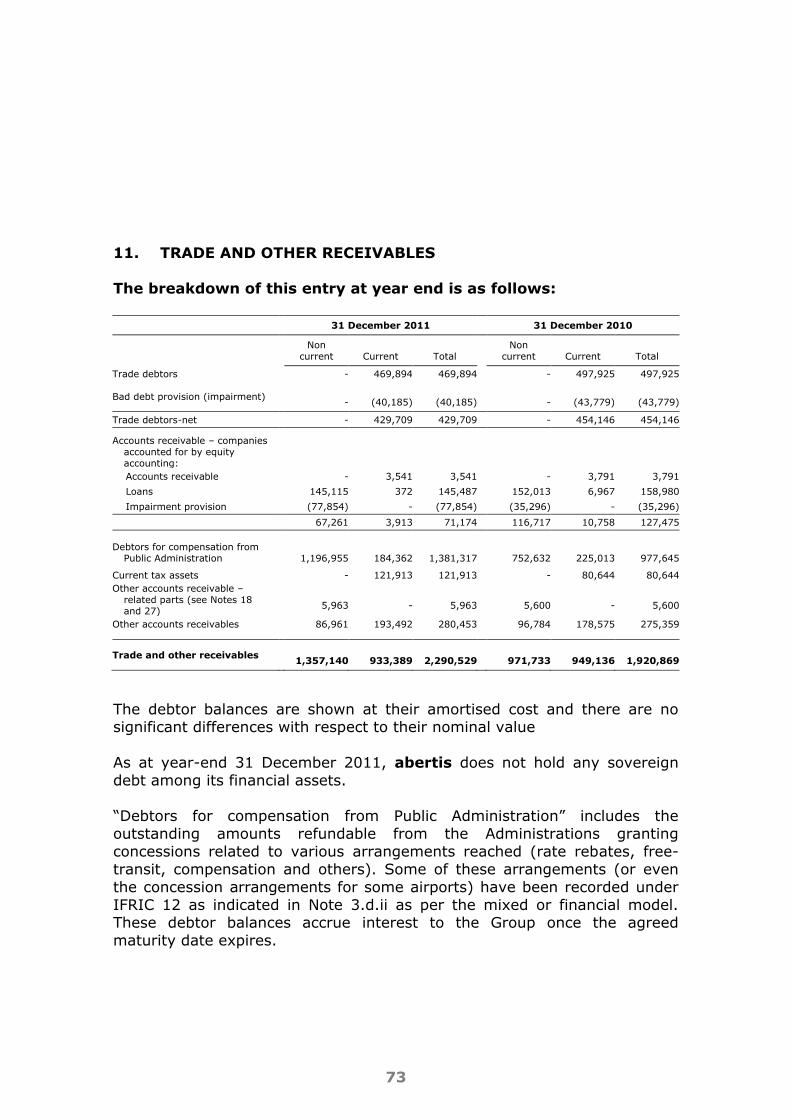

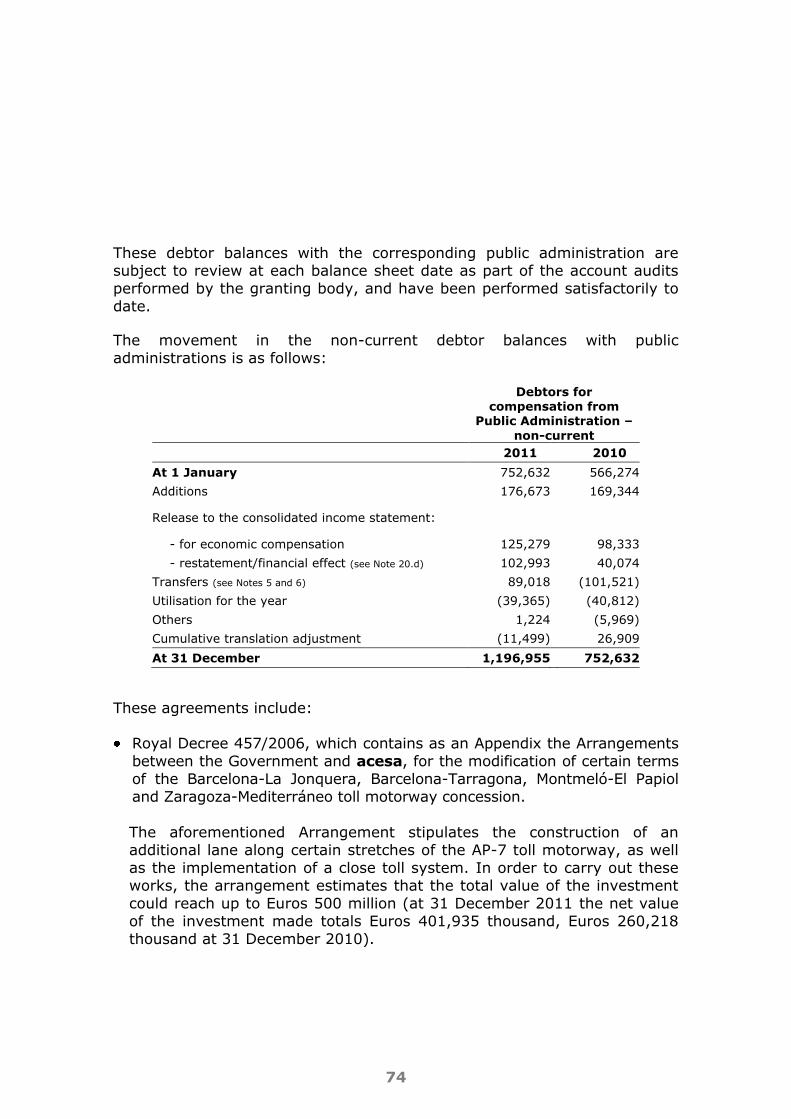

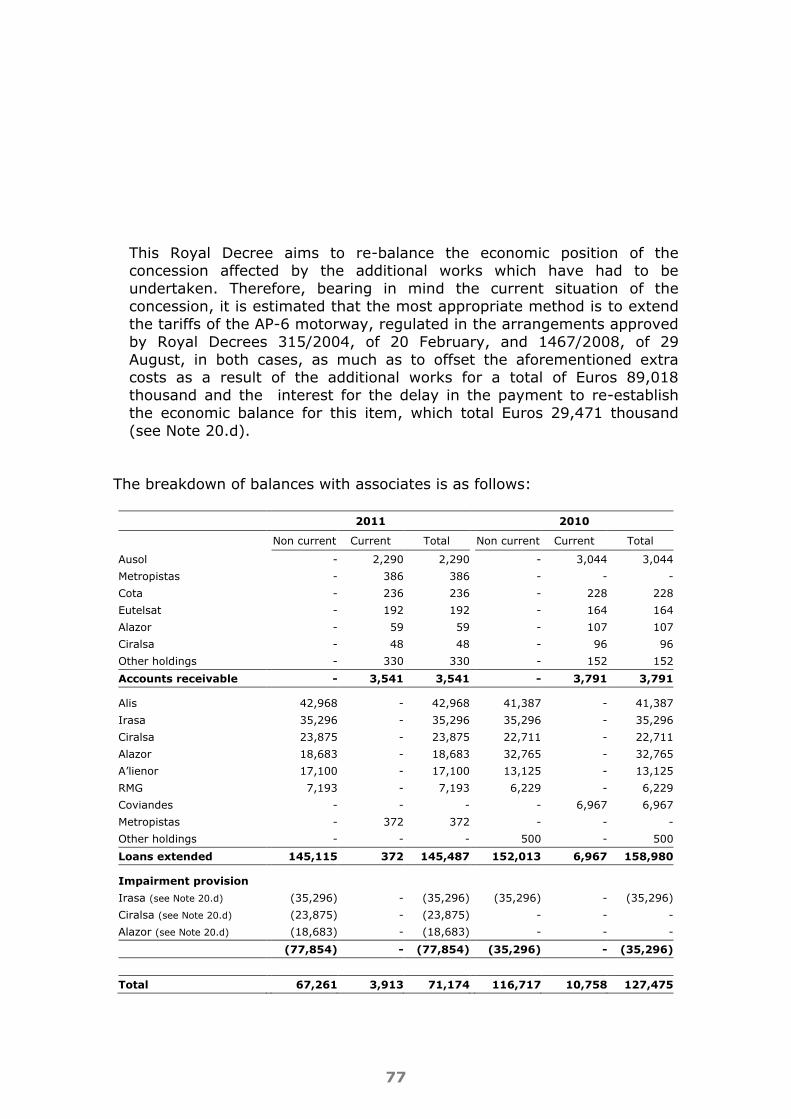

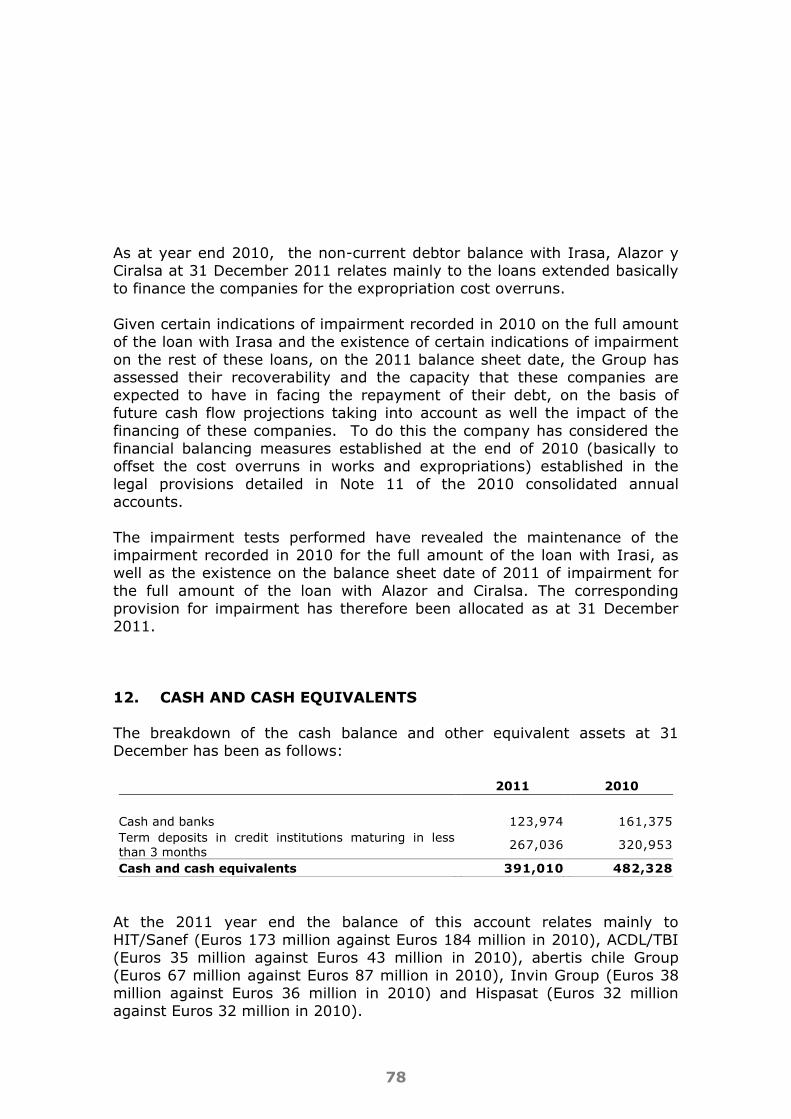

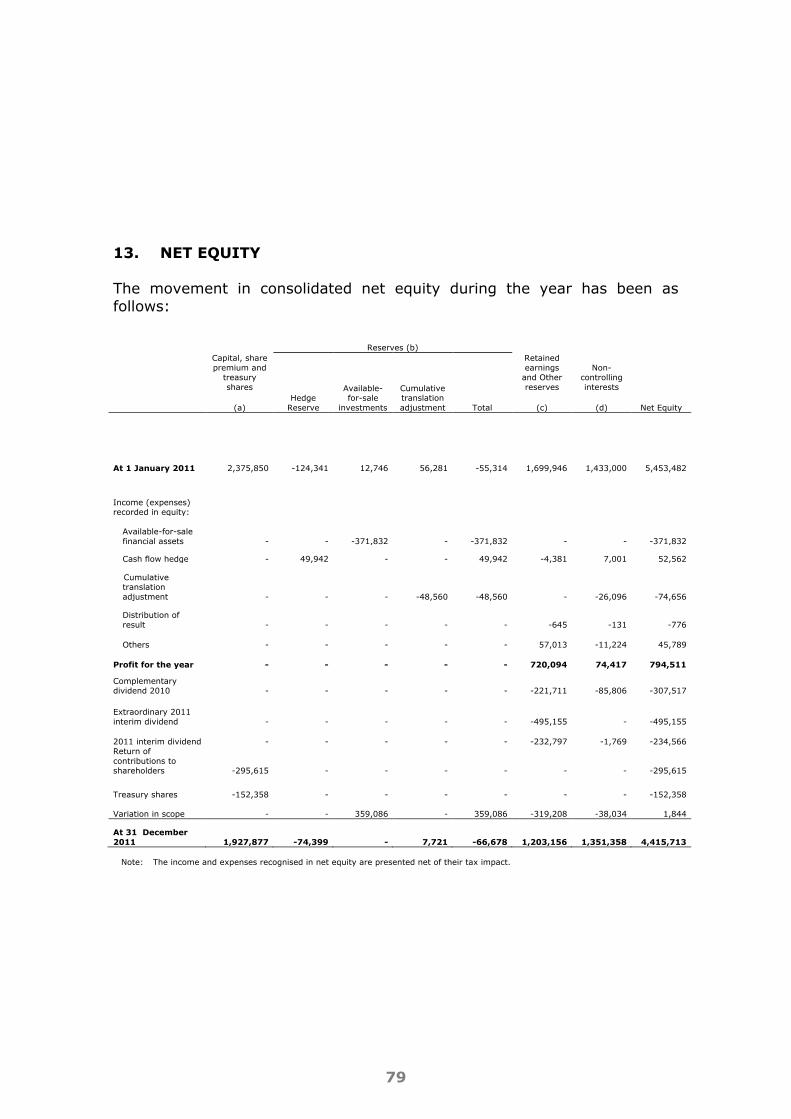

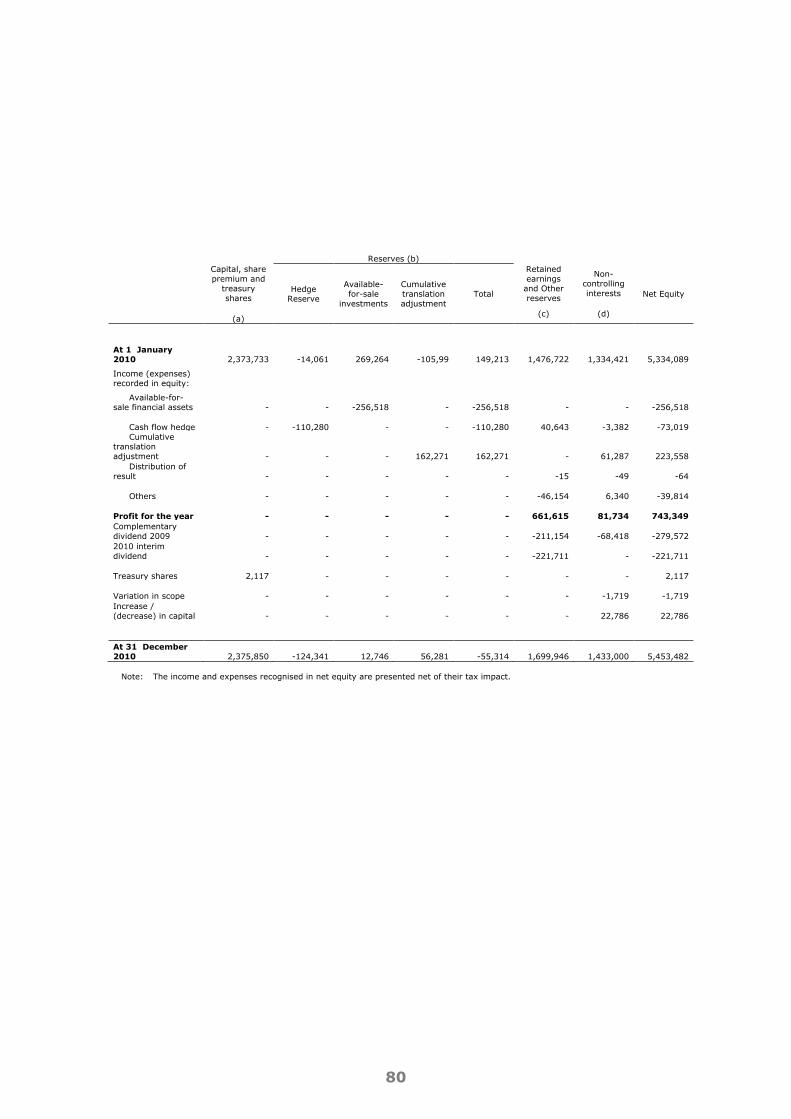

NOTES TO THE 2011 CONSOLIDATED ANNUAL ACCOUNTS ................................... 10 1. General information .............................................................................. 10 2. Basis of presentation ............................................................................. 11 3. Accounting policies ............................................................................... 23 4. Management of financial risk and capital .................................................. 43 5. Property, plant and equipment ............................................................... 49 5. Property, plant and equipment ............................................................... 49 6. Goodwill and other intangible assets ........................................................ 52 7. Investment property ............................................................................. 61 8. Investments in associates ...................................................................... 62 9. Available-for-sale financial assets ........................................................... 68 10. Derivative financial instruments .............................................................. 69 11. Trade and other receivables ................................................................... 73 12. Cash and cash equivalents ..................................................................... 78 13. Net equity ........................................................................................... 79 14. Borrowings .......................................................................................... 94 15. Deferred income ................................................................................... 98 16. Trade and other payables ...................................................................... 99 17. Corporate income tax .......................................................................... 100 18. Obligations for employee benefits ......................................................... 105 19. Provisions and other liabilities .............................................................. 110 20. Income and expenses ......................................................................... 112 21. Contingencies and commitments ........................................................... 115 22. Business combinations ........................................................................ 116 23. Shareholdings in multigroup companies ................................................. 117 24. Environment ...................................................................................... 118 25. Segment reporting .............................................................................. 119 26. Discontinued operations and assets and liabilities held for sale .................. 123 27. Related parties ................................................................................... 128 28. Share-based payments ........................................................................ 140 29. Other information ............................................................................... 144 30. Subsequent events ............................................................................. 149

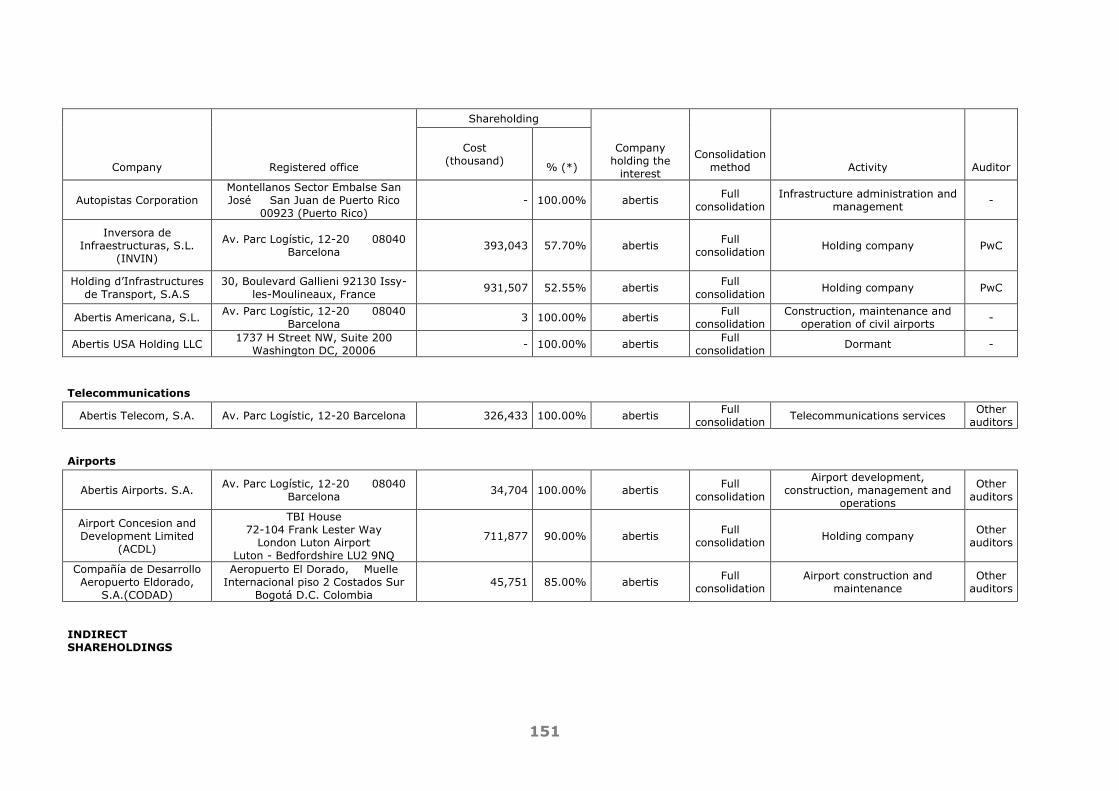

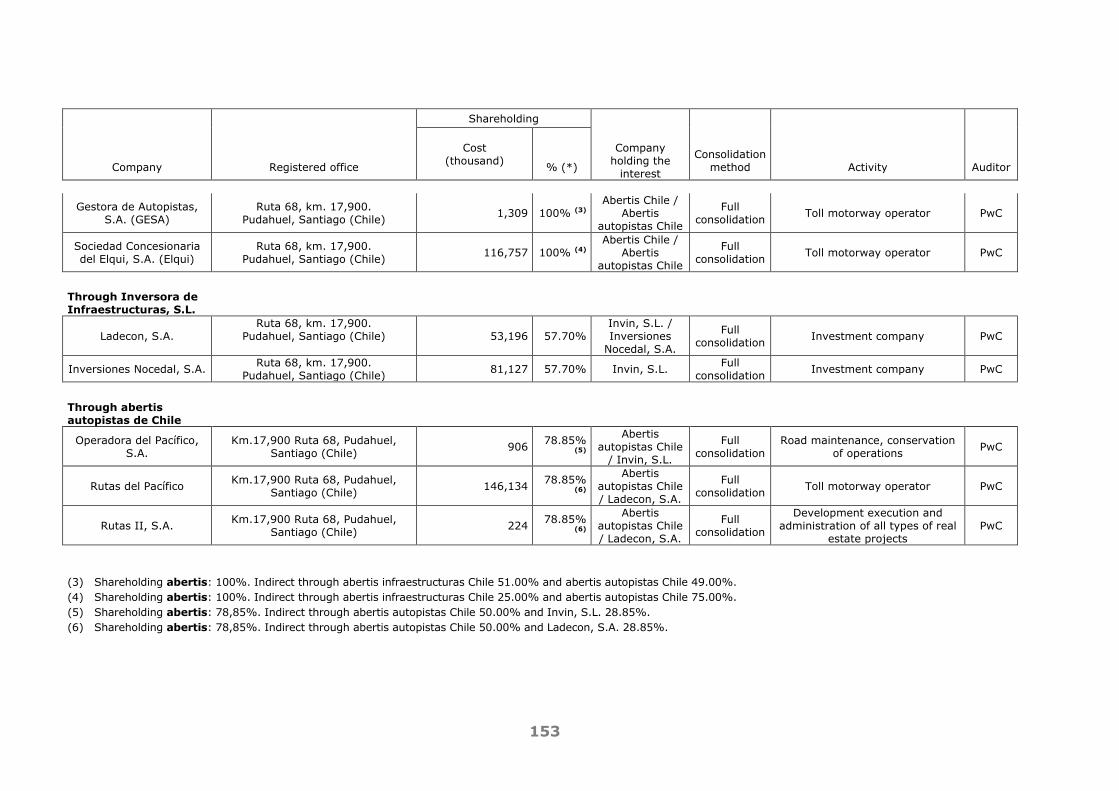

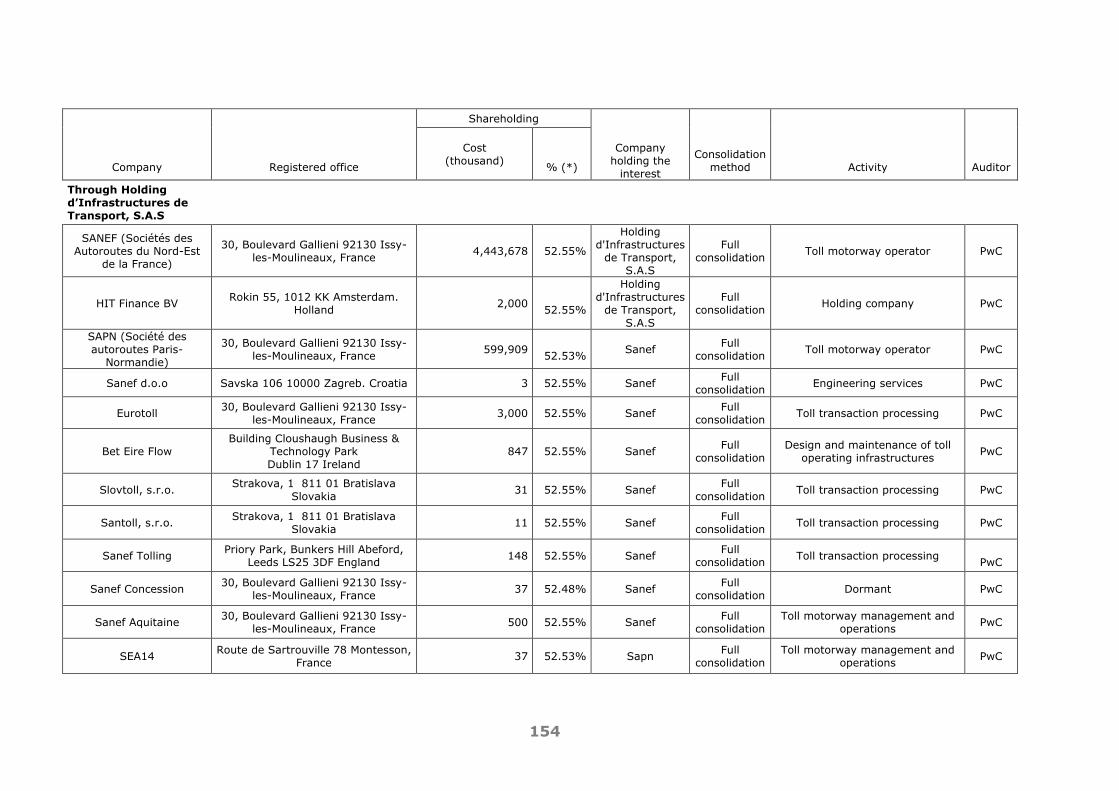

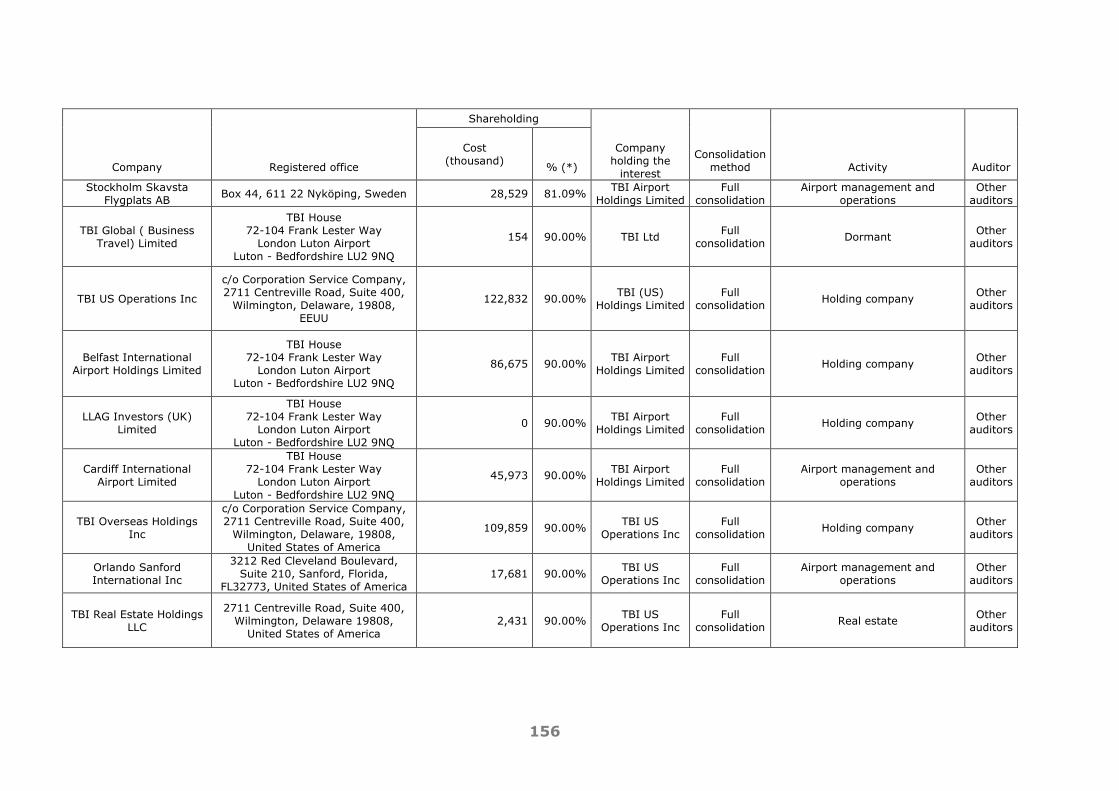

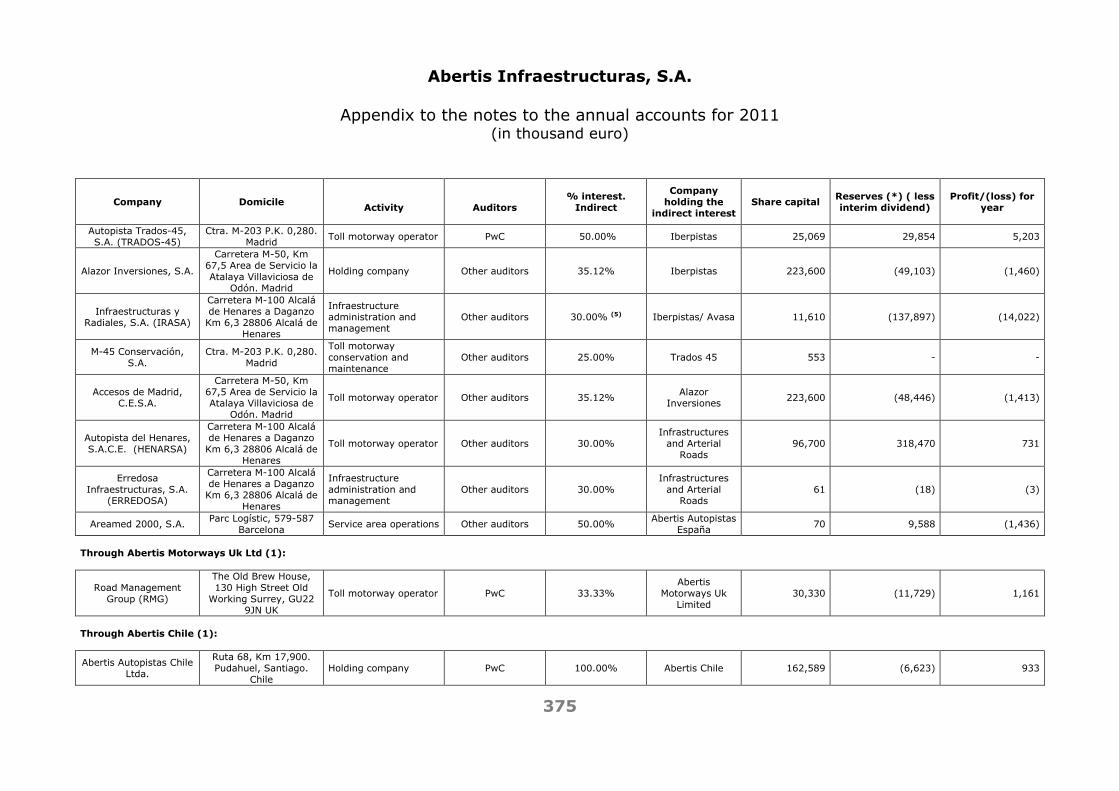

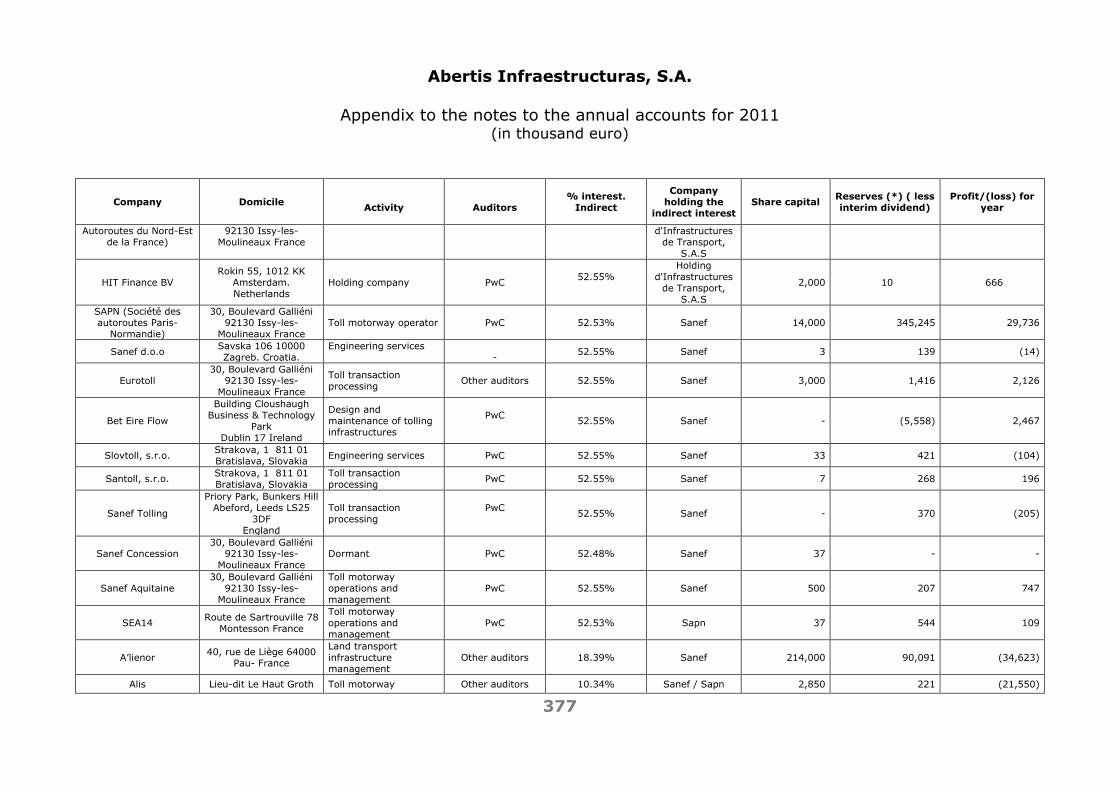

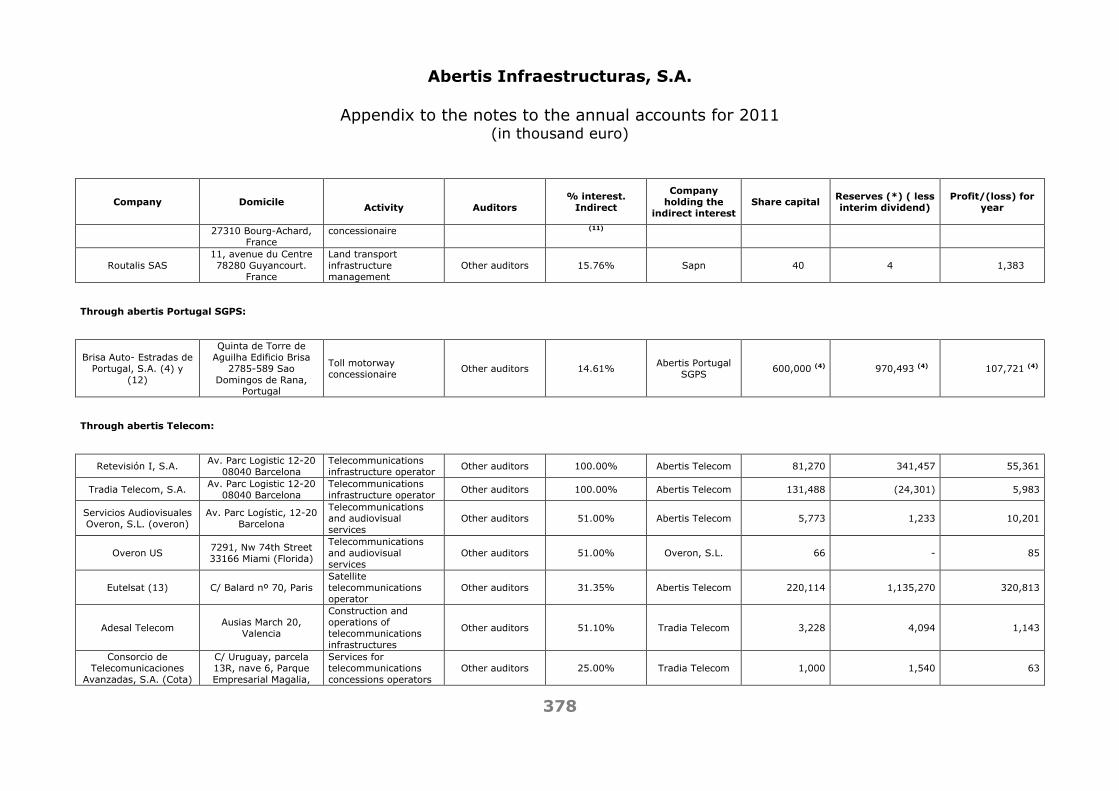

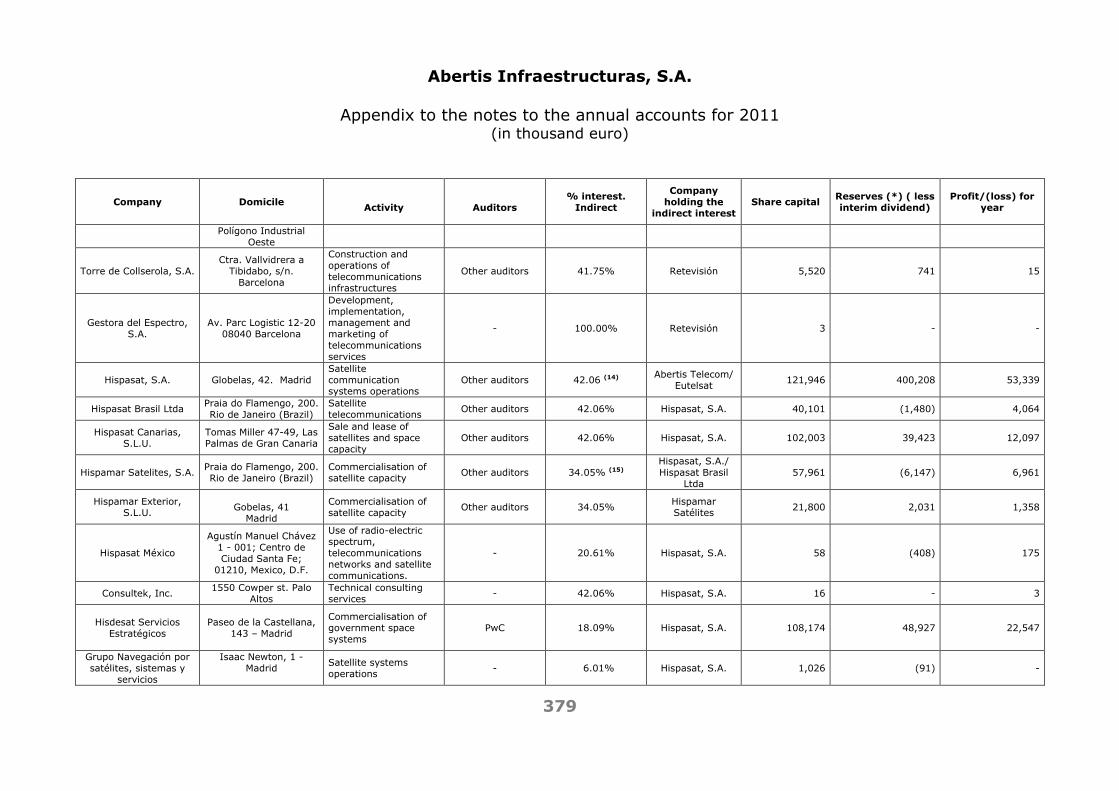

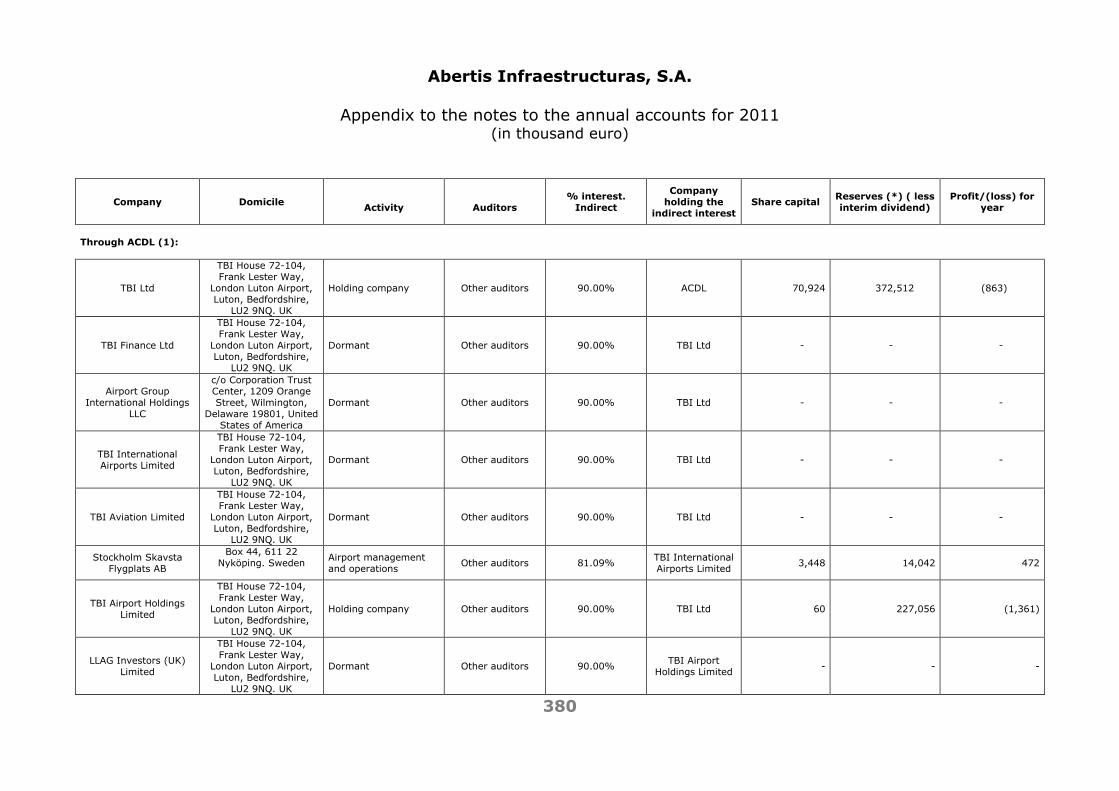

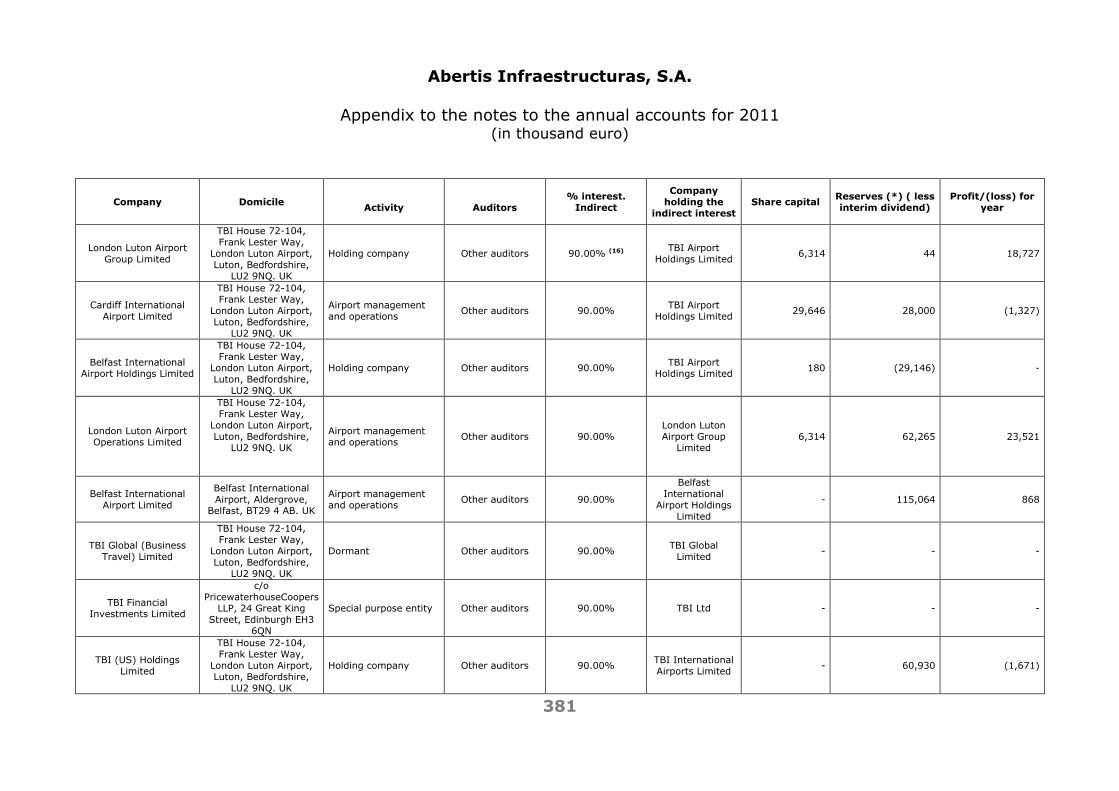

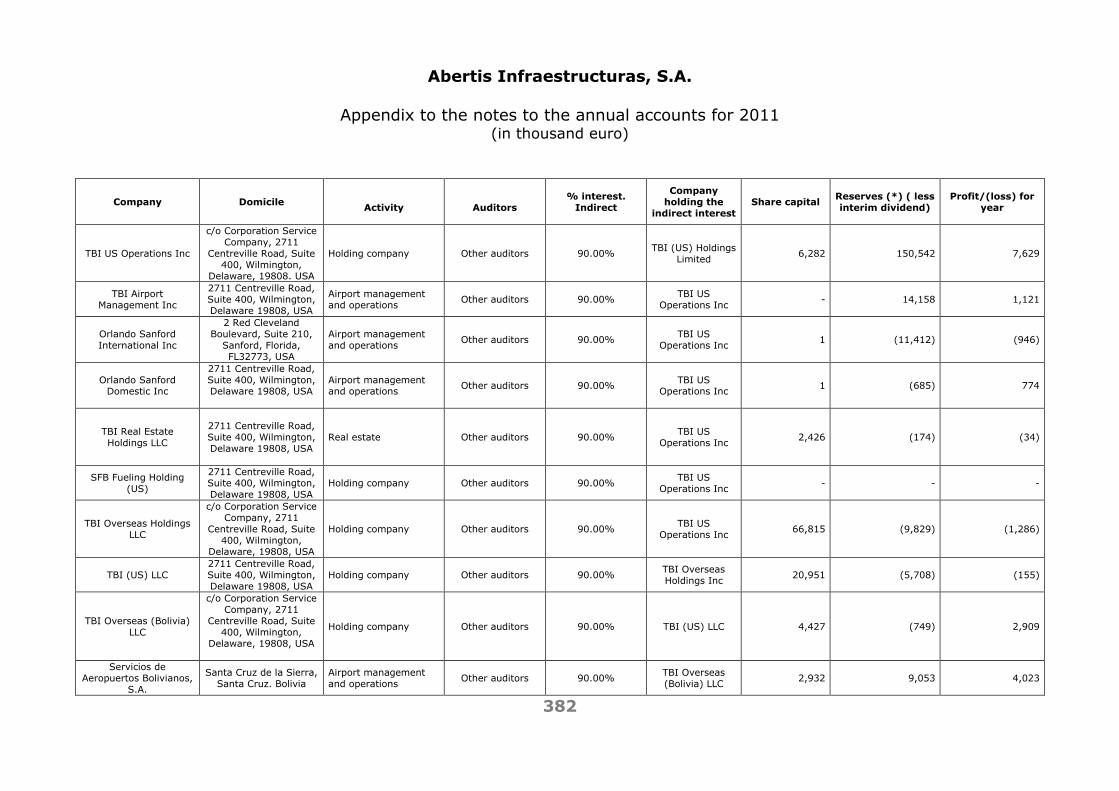

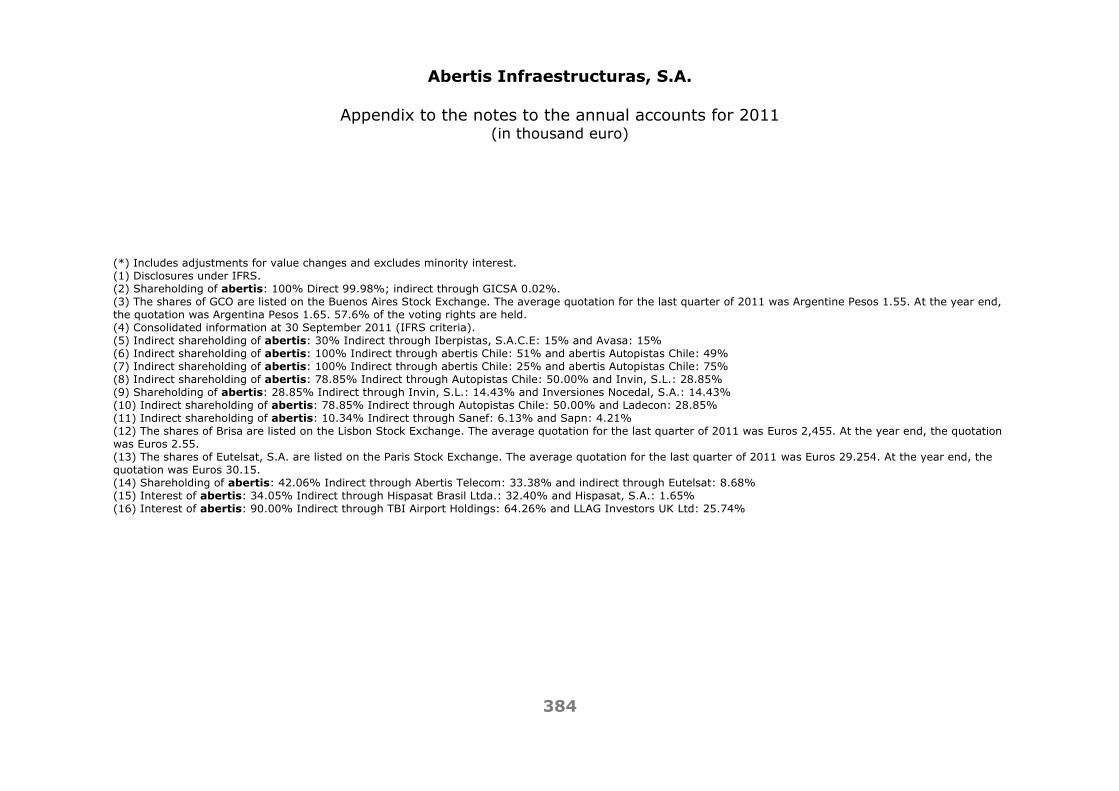

APPENDIX I. Subsidiaries in the consolidation scope ......................................... 150 APPENDIX II. Multi-group companies in the consolidation scope .......................... 159 APPENDIX III. Associates in the consolidation scope ........................................... 161 CONSOLIDATED MANAGEMENT REPORT FOR 2011 ............................................ 164 1. Information required under the provisions of article 262 of the corporate

enterprises act ................................................................................... 164 2. Annual corporate governance report ...................................................... 173

ABERTIS INFRAESTRUCTURAS, S.A. Y SOCIEDADES DEPENDIENTES

3

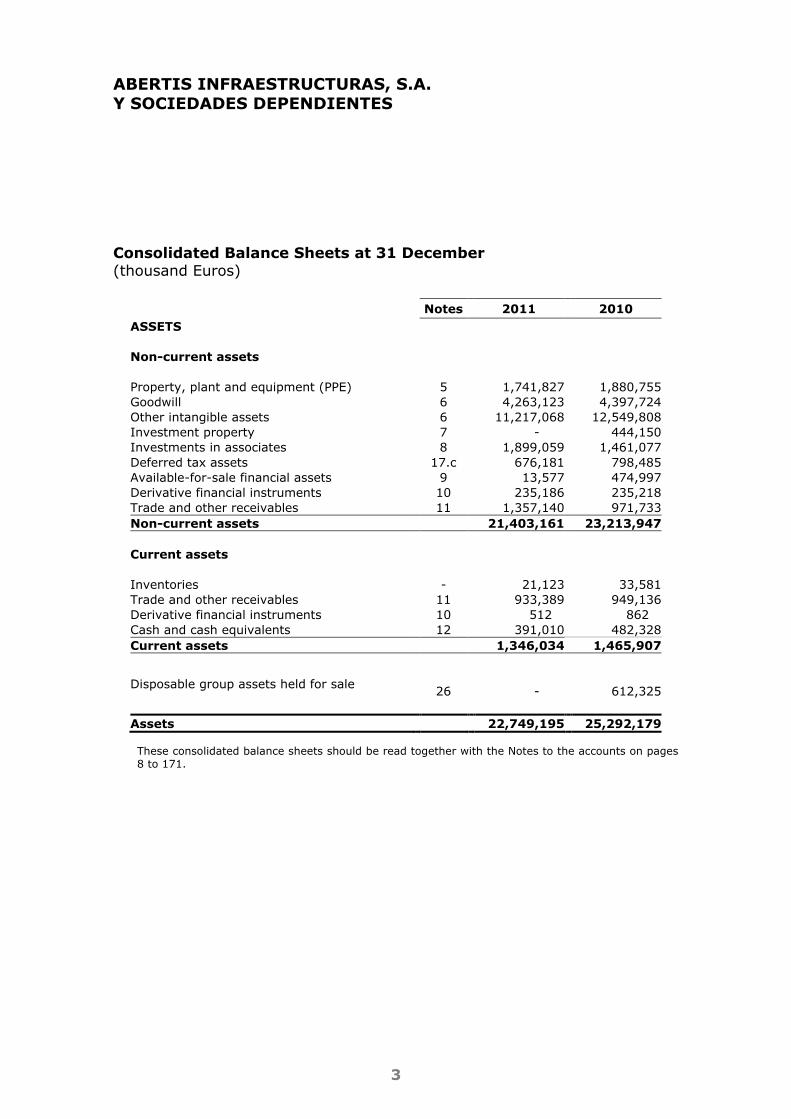

Consolidated Balance Sheets at 31 December (thousand Euros)

Notes 2011 2010

ASSETS

Non-current assets

Property, plant and equipment (PPE) 5 1,741,827 1,880,755

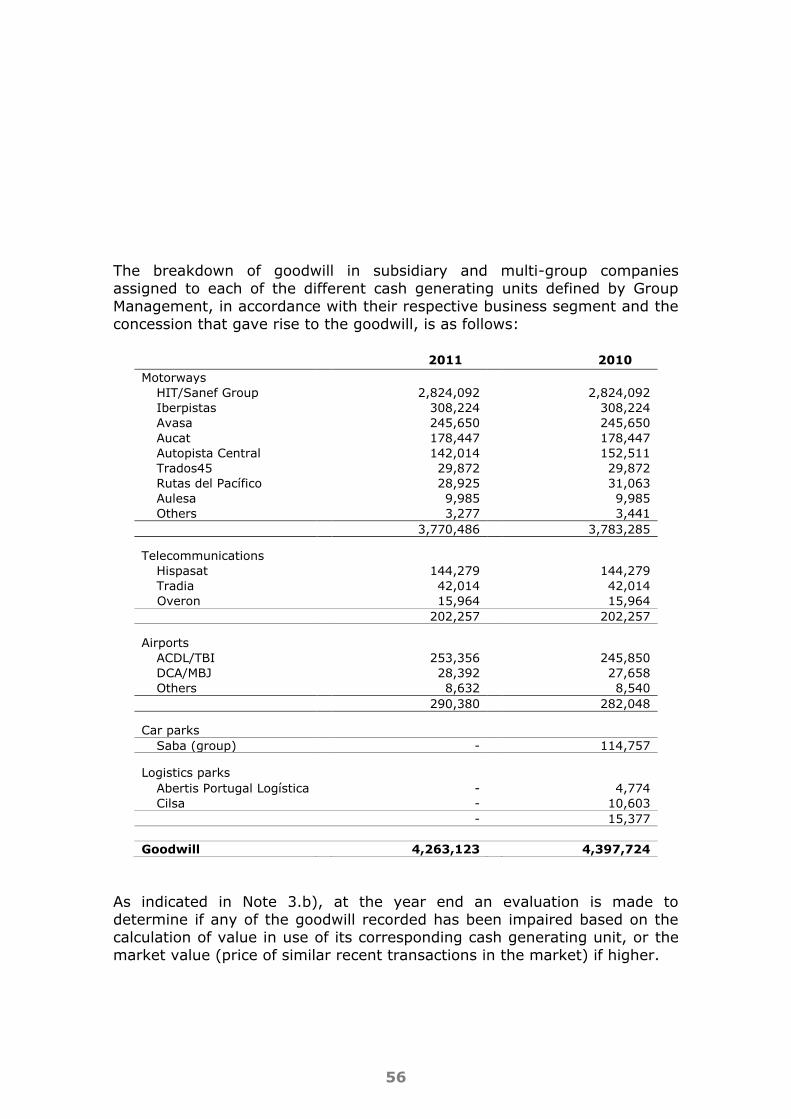

Goodwill 6 4,263,123 4,397,724

Other intangible assets 6 11,217,068 12,549,808

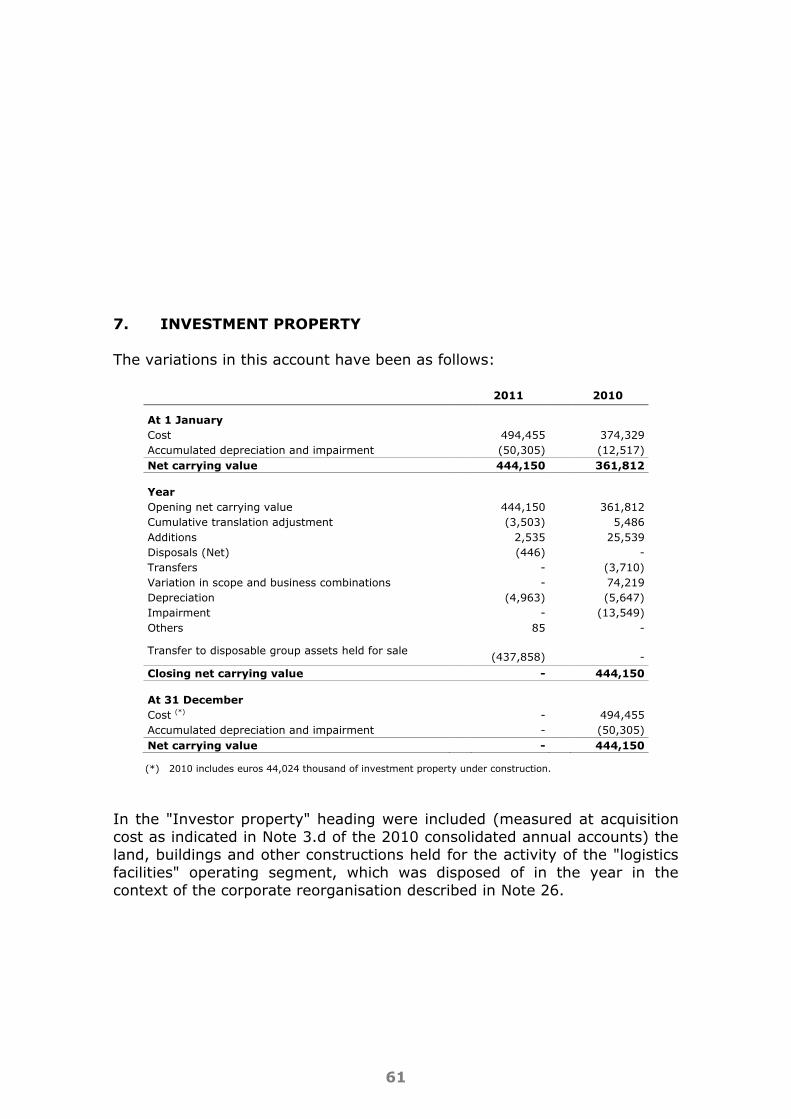

Investment property 7 - 444,150

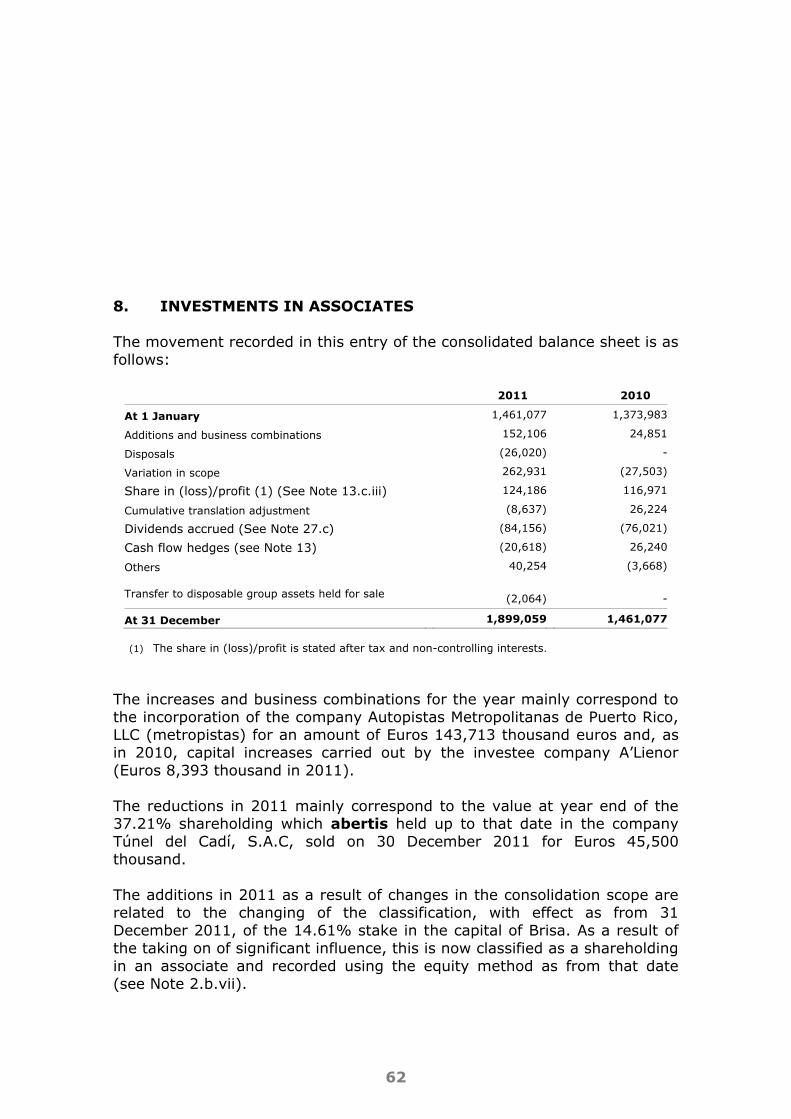

Investments in associates 8 1,899,059 1,461,077

Deferred tax assets 17.c 676,181 798,485

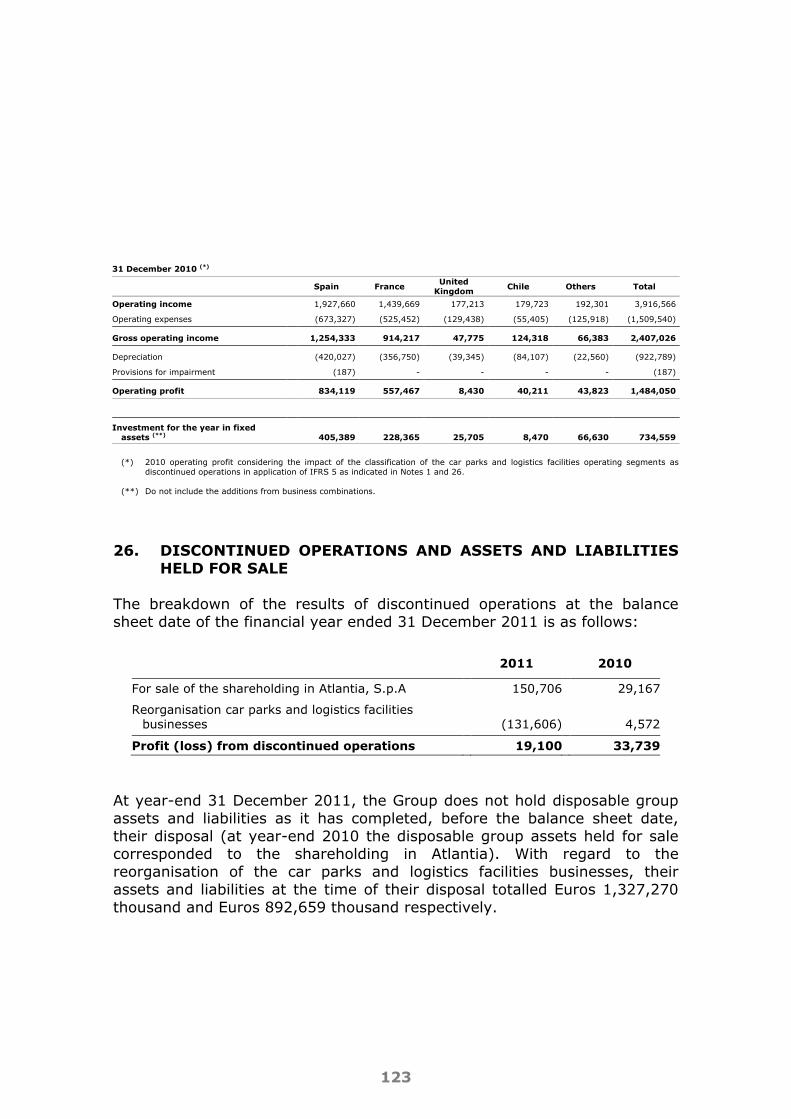

Available-for-sale financial assets 9 13,577 474,997

Derivative financial instruments 10 235,186 235,218

Trade and other receivables 11 1,357,140 971,733

Non-current assets 21,403,161 23,213,947

Current assets

Inventories - 21,123 33,581

Trade and other receivables 11 933,389 949,136

Derivative financial instruments 10 512 862

Cash and cash equivalents 12 391,010 482,328

Current assets 1,346,034 1,465,907

Disposable group assets held for sale

26

-

612,325

Assets 22,749,195 25,292,179

These consolidated balance sheets should be read together with the Notes to the accounts on pages

8 to 171.

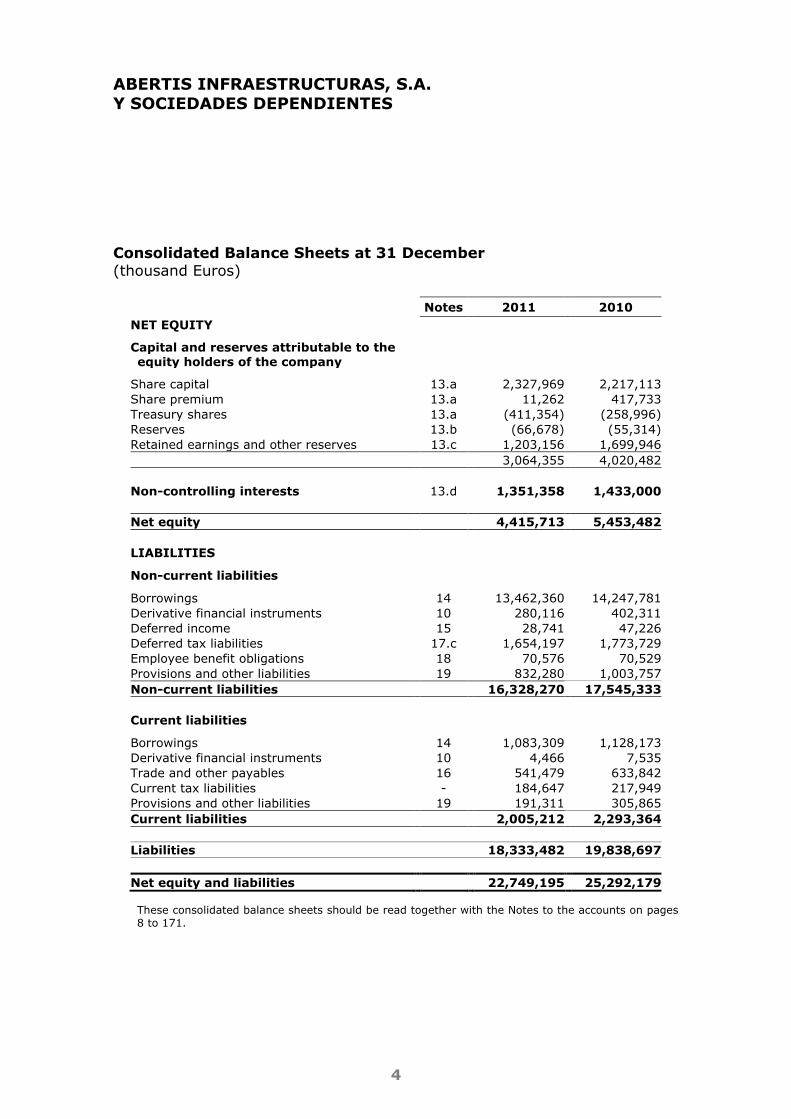

ABERTIS INFRAESTRUCTURAS, S.A. Y SOCIEDADES DEPENDIENTES

4

Consolidated Balance Sheets at 31 December (thousand Euros)

Notes 2011 2010

NET EQUITY

Capital and reserves attributable to the equity holders of the company

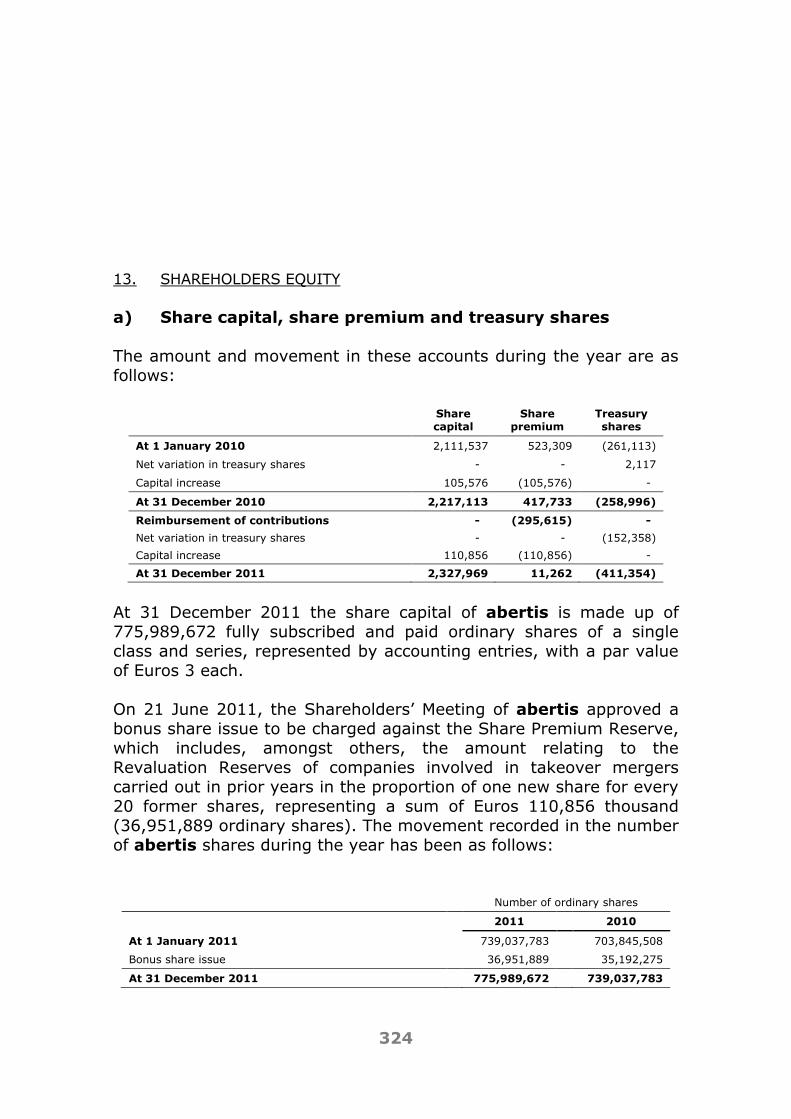

Share capital 13.a 2,327,969 2,217,113

Share premium 13.a 11,262 417,733

Treasury shares 13.a (411,354) (258,996)

Reserves 13.b (66,678) (55,314)

Retained earnings and other reserves 13.c 1,203,156 1,699,946

3,064,355 4,020,482

Non-controlling interests 13.d 1,351,358 1,433,000

Net equity 4,415,713 5,453,482

LIABILITIES

Non-current liabilities

Borrowings 14 13,462,360 14,247,781

Derivative financial instruments 10 280,116 402,311

Deferred income 15 28,741 47,226

Deferred tax liabilities 17.c 1,654,197 1,773,729

Employee benefit obligations 18 70,576 70,529

Provisions and other liabilities 19 832,280 1,003,757

Non-current liabilities 16,328,270 17,545,333

Current liabilities

Borrowings 14 1,083,309 1,128,173

Derivative financial instruments 10 4,466 7,535

Trade and other payables 16 541,479 633,842

Current tax liabilities - 184,647 217,949

Provisions and other liabilities 19 191,311 305,865

Current liabilities 2,005,212 2,293,364

Liabilities 18,333,482 19,838,697

Net equity and liabilities 22,749,195 25,292,179

These consolidated balance sheets should be read together with the Notes to the accounts on pages

8 to 171.

ABERTIS INFRAESTRUCTURAS, S.A. Y SOCIEDADES DEPENDIENTES

5

Consolidated Income Statements at 31 December (thousand Euros)

Notes 2011 2010 (*)

Rendering of services 20.a 3,810,683 3,802,345

Other operating income 20.b 85,467 89,836

Own work capitalised - 14,112 16,864

Other income 20.b 4,527 7,521

Operating income 3,914,789 3,916,566

Income for upgrades to infrastruture - 265,239 337,200

Other operating income 4,180,028 4,253,766

Personnel expenses 20.c (615,334) (572,332)

Other operating expenses - (832,523) (926,017)

Variation in trade provisions - (12,184) (8,343)

Variation in provisions for impairment of assets 9 (1,678) (187)

Amortisation and depreciation 5/6/7/26 (934,710) (922,789)

Other expenses - (1,002) (2,848)

Operating expenses (2,397,431) (2,432,516)

Expenses for upgrades to infrastructures - (265,239) (337,200)

Other operating expenses (2,662,670) (2,769,716)

Operating profit 1,517,358 1,484,050

Variation in valuation of hedging instruments 20.d (4,213) (1,076)

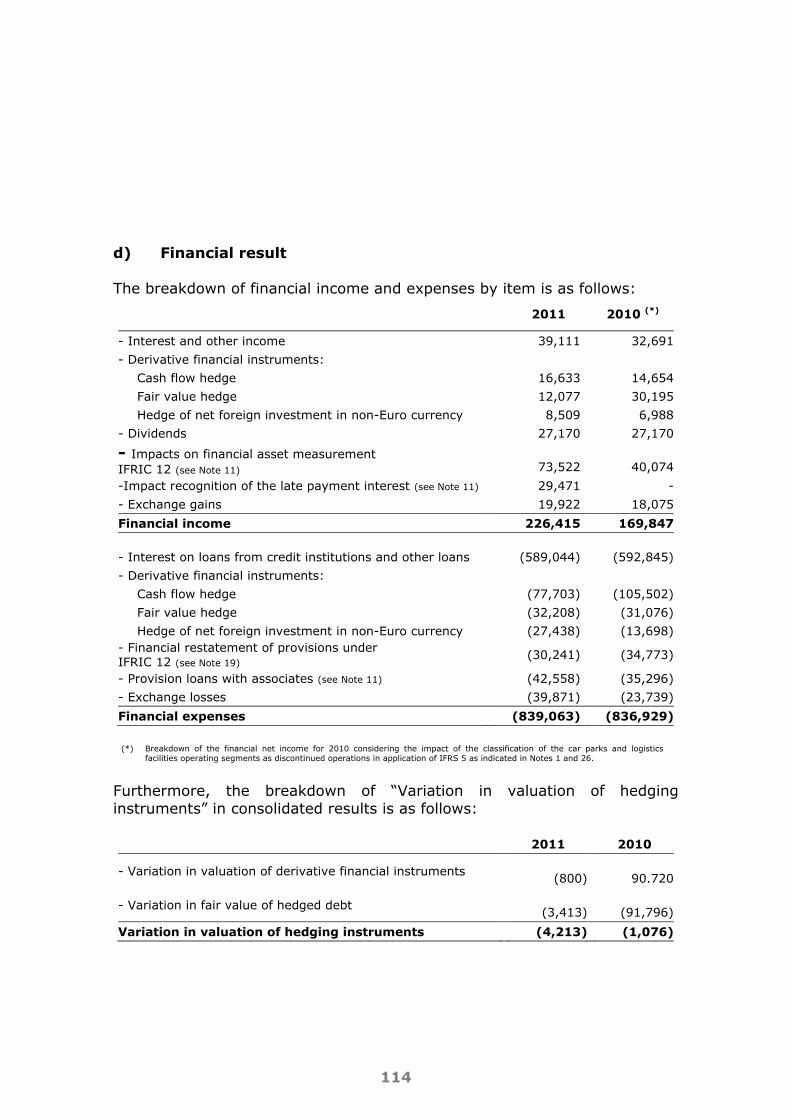

Financial income 20.d 226,415 169,847

Financial expenses 20.d (839,063) (836,929)

Net financial result (616,861) (668,158)

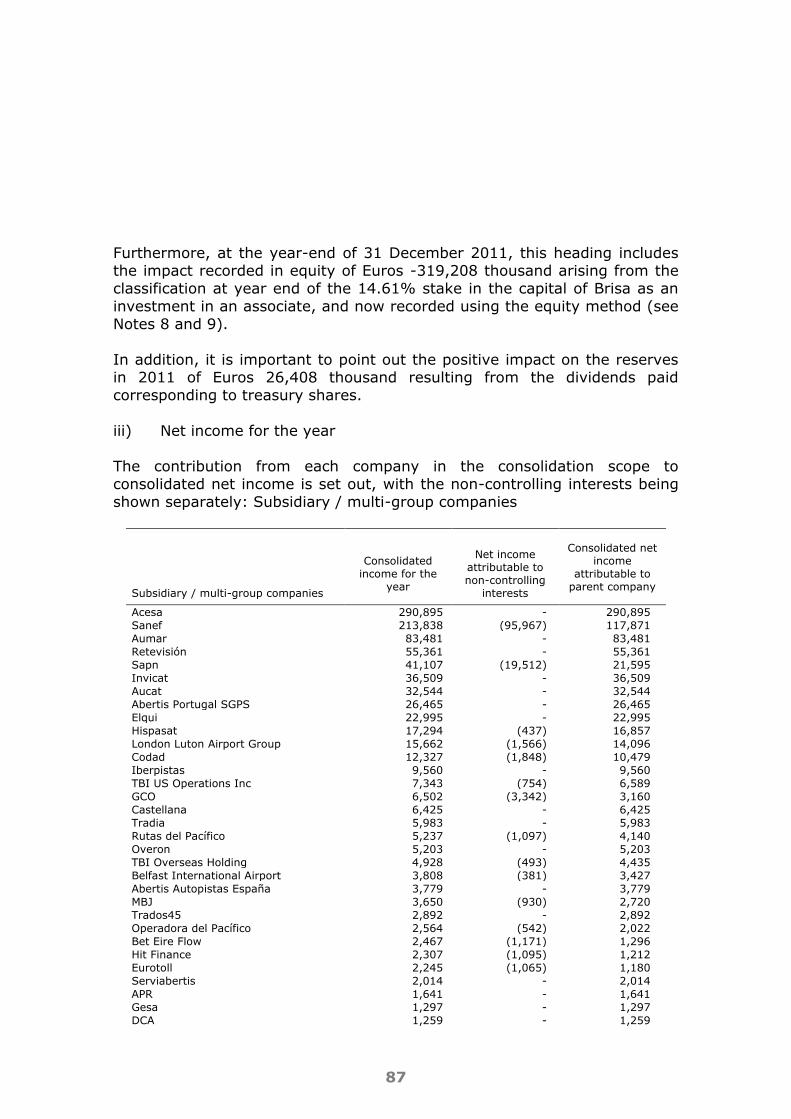

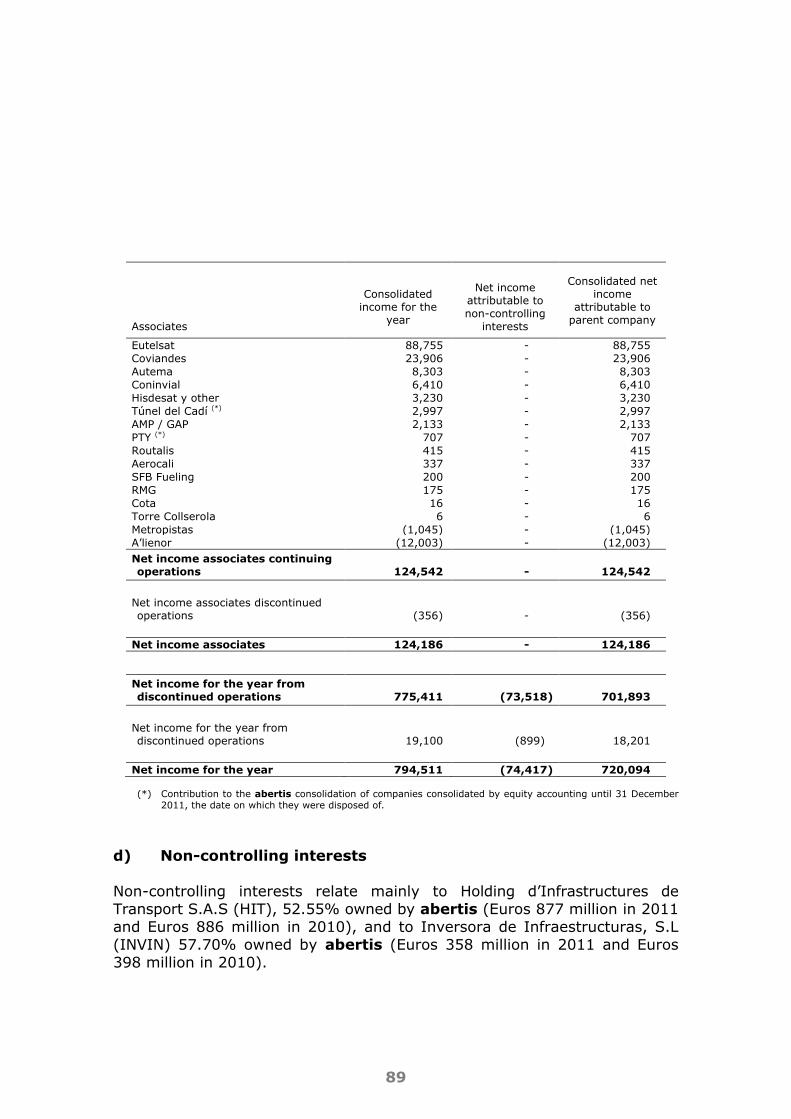

Results of companies accounted for by equity accounting

8/13.c.iii/26

124,542

116,919

Profit before tax 1,025,039 932,811

Corporate Income tax 17.b (249,628) (223,201)

Profit from continuing operations 775,411 709,610

Profit (loss) from discontinued operations 26 19,100 33,739

Profit for the year 794,511 743,349

Attributable to non-controlling holdings 13.c.iii 74,417 81,734

Attributable to the equity holders of the Company 720,094 661,615

Profit per share for continuing and discontinued

operations (€ per share)

- basic of continuing operations 13.f 0.93 0.83

- basic of discontinued operations - 0.02 0.04

- diluted of continuing operations 13.f 0.93 0.83

- diluted of disconiued operations - 0.02 0.04

These consolidated balance sheets should be read together with the Notes to the accounts on pages 8 to 170. (*) 2010 income statement includes the impact of the classification of discontinued operations in application of

IFRS 5 as indicated in Note 1 and 26 and expressing income and expenses for improvements in infrastructure as shown in detail in Note 1.

ABERTIS INFRAESTRUCTURAS, S.A. Y SOCIEDADES DEPENDIENTES

6

Consolidated Statements of Comprehensive Income at 31 December (thousand Euros)

Notes 2011 2010

Profit for the year 794,511 743,349

Net income and expenses charged directly to net equity:

Net fair value gains/(losses) of available-for-sale financial assets

(gross of tax)

9/13

(234,359)

(171,870)

Net fair value gains/(losses) of held-for-sale assets (gross of tax)

26.a

13,233

(84,648)

Cash flow hedges in parent, fully and proportionally consolidated

companies

10

21,229

(96,527)

Net foreign investment hedges in parent, fully and proportionally

consolidated companies

10

22,868

(148,969)

Cash flow hedges / net foreign investment companies accounted for

by equity accounting

13

(13,970)

26,240

Currency translation differences 13 (74,656) 223,558

Others 13.c 9,936 (30,290)

Actuarial gain and loss 18 (1,078) (89)

Tax on items taken directly to or transferred from net equity

17.c

4,385

69,816

(252,412) (212,779)

Releases to the income statement:

Cash flow hedges in fully and proportionally consolidated

companies

20.d/10

61,070

90,848

Cash flow hedges / net foreign investment in fully and

proportionally consolidated companies

20.d/10

18,929

6,710

Gain on sale of Atlantia, S.p.A 26.a (150,706) -

Tax effect 17.c (25,794) (30,636)

(96,501) 66,922

Other comprehensive income (348,913) (145,857)

Total comprehensive income 445,598 597,492

Attributible to:

The Company’s equity holders:

for continuing operations 519,664 420,681

for discontinued operations (118,033) 30,881

401,631 451,562

Non-controlling interests 43,967 145,930

445,598 597,492

These consolidated balance sheets should be read together with the Notes to the accounts on pages 8 to 171.

7

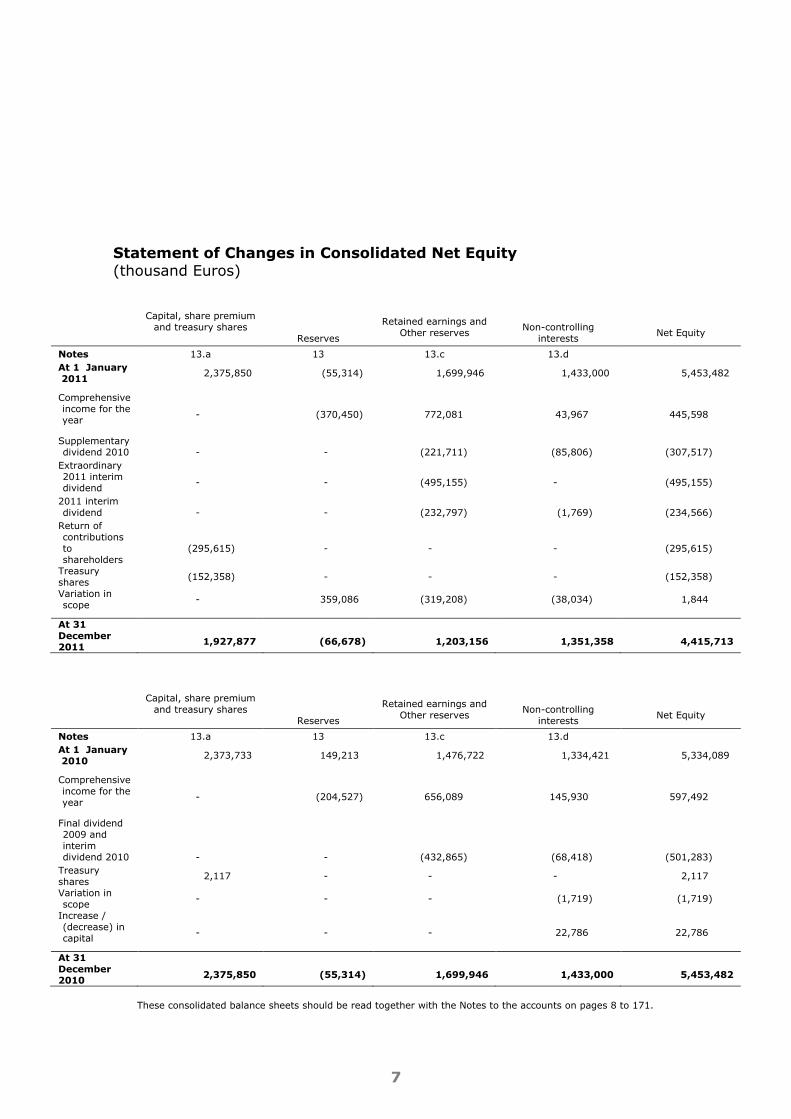

Statement of Changes in Consolidated Net Equity (thousand Euros)

Capital, share premium

and treasury shares

Reserves

Retained earnings and

Other reserves

Non-controlling interests

Net Equity

Notes 13.a 13 13.c 13.d

At 1 January 2011 2,375,850 (55,314) 1,699,946 1,433,000 5,453,482

Comprehensive income for the year

-

(370,450)

772,081

43,967

445,598

Supplementary dividend 2010

-

-

(221,711)

(85,806)

(307,517)

Extraordinary 2011 interim dividend

-

-

(495,155)

-

(495,155)

2011 interim dividend

-

-

(232,797)

(1,769)

(234,566)

Return of contributions to shareholders

(295,615)

-

-

-

(295,615)

Treasury shares (152,358) - - - (152,358)

Variation in scope - 359,086 (319,208) (38,034) 1,844

At 31 December 2011

1,927,877

(66,678)

1,203,156

1,351,358

4,415,713

Capital, share premium

and treasury shares

Reserves

Retained earnings and

Other reserves

Non-controlling interests

Net Equity

Notes 13.a 13 13.c 13.d

At 1 January 2010 2,373,733 149,213 1,476,722 1,334,421 5,334,089

Comprehensive income for the year

-

(204,527)

656,089

145,930

597,492

Final dividend 2009 and interim dividend 2010

-

-

(432,865)

(68,418)

(501,283)

Treasury

shares 2,117 - - - 2,117

Variation in scope - - - (1,719) (1,719)

Increase / (decrease) in capital

-

-

-

22,786

22,786

At 31 December 2010

2,375,850

(55,314)

1,699,946

1,433,000

5,453,482

These consolidated balance sheets should be read together with the Notes to the accounts on pages 8 to 171.

8

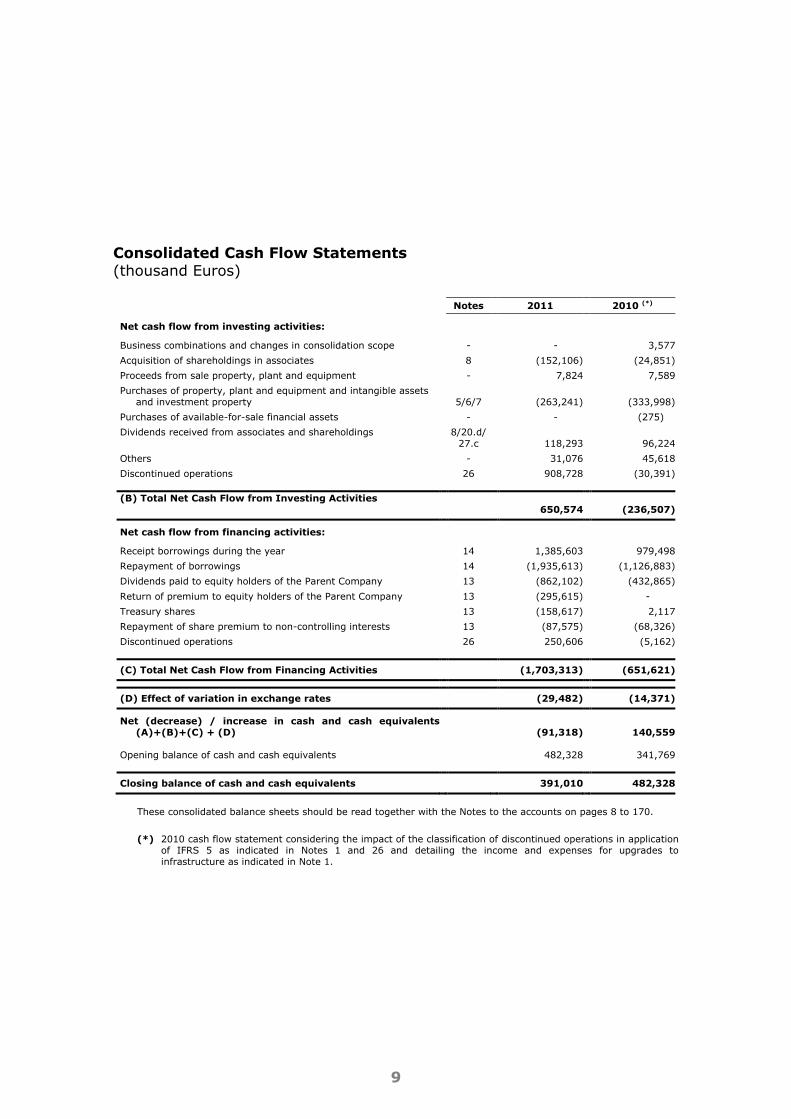

Consolidated Cash Flow Statements (thousand Euros)

Notes 2011 2010 (*)

Net cash flow from operating activities:

Profit for the year from continuing operations 775,411 709,610

Adjustments to:

Taxes 17.b 249,628 223,201

Depreciation and amortisation for the year 5/6/7 934,710 922,789

Variation in asset impairment provision 9 1,678 187

(Profit)/loss, net, on sale of property, plant and equipment and intangible assets and other assets

-

(3,525)

(4,673)

(Profit)/loss on hedging instruments 20.d 4,213 1,076

Variation in post-employment provisions 18 16,353 15,298

Variation in provisions for IFRIC 12 and other provisions 19 68,681 72,369

Dividend income 20.d (27,170) (27,170)

Interest income 20.d (199,245) (142,677)

Interest expense 20.d 839,063 836,929

Release of deferred income to profit and loss 15 (2,716) (5,462)

Income from upgrade to infrastructure (265,239) (337,200)

Other adjustments to net income 11 (125,279) (98,333)

Share in results of associates accounted for by equity accounting 13.c.iii

(124,542)

(116,919)

2,142,021 2,049,025

Variation in current assets/liabilities:

Inventories - (5,439) 5,235

Trade and other receivables - (50,448) (71,694)

Derivative financial instruments - (2,608) (3,751)

Trade and other payables - (52,473) 26,487

Other current liabilities - (73,900) 60,267

(184,868) 16,544

Cash flow generated from operations 1,957,153 2,065,569

Corporate income tax paid - (249,284) (254,421)

Interest and settlement of hedges paid - (730,585) (776,637)

Interest and settlement of hedges received - 96,077 101,241

Utilisation of provisions for post-employment benefits 18 (15,686) (12,531)

Utilisation of provisions for IFRIC 12 and other provisions 19 (120,478) (70,266)

Other payables 19 17,051 31

Receipt / refund of grants and other deferred income 15 2,415 811

Non-current debtors and other receivables - 24,367 (54,127)

Discontinued operations 26 9,873 43,388

(A) Total Net Cash Flow from Operations 990,903

1,043,058

These consolidated balance sheets should be read together with the Notes to the accounts on pages 8 to 171.

(*) 2010 cash flow statement considering the impact of the classification of discontinued operations in application

of IFRS 5 as indicated in Notes 1 and 26 and detailing the income and expenses for upgrades to infrastructure as indicated in Note 1.

9

Consolidated Cash Flow Statements (thousand Euros)

Notes 2011 2010 (*)

Net cash flow from investing activities:

Business combinations and changes in consolidation scope - - 3,577

Acquisition of shareholdings in associates 8 (152,106) (24,851)

Proceeds from sale property, plant and equipment - 7,824 7,589

Purchases of property, plant and equipment and intangible assets and investment property

5/6/7

(263,241)

(333,998)

Purchases of available-for-sale financial assets - - (275)

Dividends received from associates and shareholdings 8/20.d/ 27.c

118,293

96,224

Others - 31,076 45,618

Discontinued operations 26 908,728 (30,391)

(B) Total Net Cash Flow from Investing Activities

650,574

(236,507)

Net cash flow from financing activities:

Receipt borrowings during the year 14 1,385,603 979,498

Repayment of borrowings 14 (1,935,613) (1,126,883)

Dividends paid to equity holders of the Parent Company 13 (862,102) (432,865)

Return of premium to equity holders of the Parent Company 13 (295,615) -

Treasury shares 13 (158,617) 2,117

Repayment of share premium to non-controlling interests 13 (87,575) (68,326)

Discontinued operations 26 250,606 (5,162)

(C) Total Net Cash Flow from Financing Activities (1,703,313) (651,621)

(D) Effect of variation in exchange rates (29,482) (14,371)

Net (decrease) / increase in cash and cash equivalents

(A)+(B)+(C) + (D)

(91,318)

140,559

Opening balance of cash and cash equivalents 482,328 341,769

Closing balance of cash and cash equivalents 391,010 482,328

These consolidated balance sheets should be read together with the Notes to the accounts on pages 8 to 170.

(*) 2010 cash flow statement considering the impact of the classification of discontinued operations in application

of IFRS 5 as indicated in Notes 1 and 26 and detailing the income and expenses for upgrades to infrastructure as indicated in Note 1.

10

NOTES TO THE 2011 CONSOLIDATED ANNUAL ACCOUNTS

1. GENERAL INFORMATION

Abertis Infraestructuras, S.A. (hereinafter abertis or the Parent Company)

was incorporated in Barcelona on 24 February 1967. The Company’s

registered office is in Avenida del Parc Logistic nº 12-20, Barcelona. On 30

May 2003 the Company’s name was changed from Acesa Infraestructuras, S.A. to its current name.

abertis is the parent company of a group of companies mainly engaged in

the management of mobility and communications infrastructures operating

in three sectors: motorway concessions, telecommunications and airports.

As shown in Note 26, the Group sold the car parks and logistics facilities sectors over the year. Therefore, their resources are classified as

discontinued operations in accordance with IFRS 5 "Non-current assets held

for sale and discontinued operations".

Its business purposes include the construction, maintenance and operation of motorways under concession; the management of motorway concessions

in Spain and internationally; the construction of roads; ancillary

construction activities, maintenance and operation of motorways, including

service stations, integrated logistics and/or transport centres and/or car

parks, as well as any other activity related to transport infrastructures and communications and/or telecommunications for the mobility and transport

of people, goods and information, under the necessary authorisation, as the

case may be.

The Company can undertake its business purposes, especially its concessionary activity, directly or indirectly through its shareholding in

other companies, subject, in this respect, to the legal provisions in force at

any time.

Note 29.c includes information on the Group’s concession contracts.

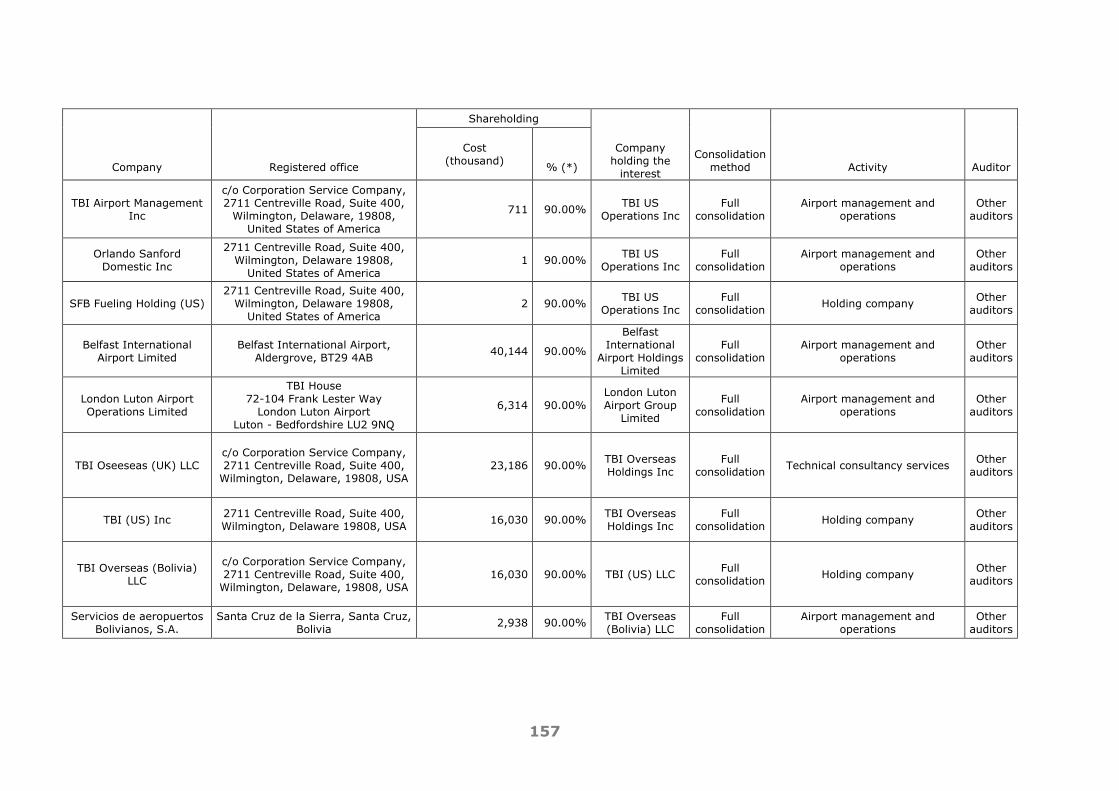

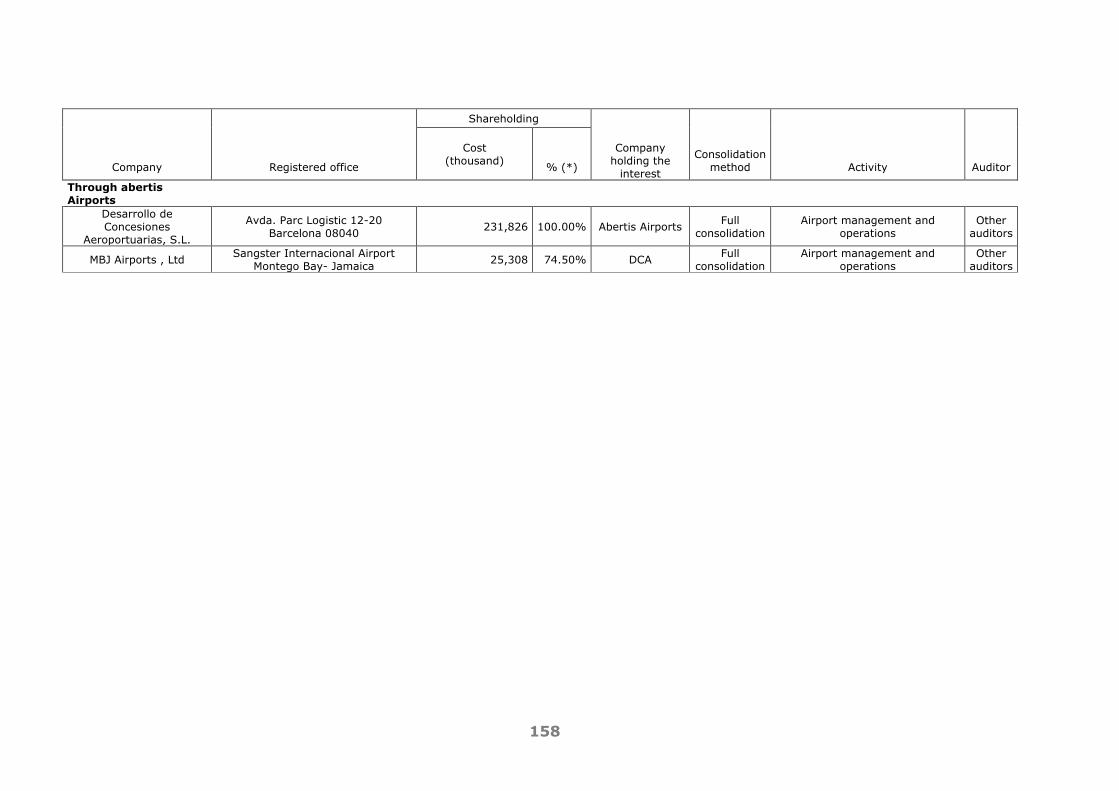

The lists of the subsidiary and multi-group companies of abertis, which

together with the parent Company make up the consolidated group

(hereinafter, the Group) at 31 December 2011 are set out in Appendix I

and Appendix II, respectively.

11

The aggregates contained in all the financial statements that form part of the consolidated annual accounts (consolidated balance sheet, consolidated

income statement, consolidated statement of comprehensive income,

consolidated statement of changes in net equity, consolidated cash flow

statement) and the notes to the consolidated annual accounts are

expressed in thousand Euros, unless explicitly stated in million Euros.

2. BASIS OF PRESENTATION

a) Basis of presentation

These consolidated annual accounts have been prepared in accordance with

the International Financial Reporting Standards adopted by the European

Union under Regulation (EC) No. 1606/2002 of the European Parliament

and the Council on 19 July 2002 and others in force at 31 December 2011 (hereinafter, IFRS). In addition, the obligation to present consolidated

annual accounts under EU approved IFRS is governed by the final eleventh

provision of the Tax, Administrative and Corporate Measures Act, Law

62/2003/30 December (Official State Gazette (BOE) of 31 December 2004).

These consolidated annual accounts prepared under IFRS have been formulated by the Directors of abertis in order to provide a true and fair

view of its consolidated equity, financial situation for the year ended 31

December 2011, consolidated results from its operations, the changes in

consolidated net equity and consolidated cash flows in accordance with the

above-mentioned legislation in force.

The first consolidated annual accounts to be presented under IFRS were

those for the year ended 31 December 2005. Consequently, IFRS-1, “First-

time Adoption of the International Financial Reporting Standards” was

applied at the transition date of 1 January 2004.

12

As required by IFRS, these 2011 consolidated annual accounts include the figures corresponding for the previous year for comparative purposes.

These figures have been duly restated as result of the following concepts:

In accordance with IFRS 5 "Non-Assets held for sale and discontinued

operations" and, mainly as a result of the disposal of the car parks

and logistics facilities businesses in October 2011 (see details in Note 26), the 2010 income and expenses corresponding to these

businesses have been classified as discontinued operations in line

with the figures for 2011.

In accordance with the criteria indicated in Note 3.0, construction activities and upgrades in infrastructure carried out by the Group in

2010 (Euros 337 million) have been recorded as income and

expenses. These figures were mentioned in Note 30 of the 2010

consolidated annual accounts, although they were not broken down in

the income statement.

As stated in Note 3.q, at the date of preparation of these consolidated

annual accounts, there are standards and interpretations which during 2011

were revised and being studied by the corresponding international

regulatory bodies. In any case, the application of these will be considered

by the Group once they are approved by the European Union, as the case

may be. The preparation of the consolidated annual accounts under IFRS requires

Management to make certain accounting estimates and certain judgements.

These are continuously evaluated and are based on the historical experience

and other factors, including the expectations of future events, which are

considered reasonable under the circumstances. Whilst the estimations have been made based on the best information available at the time of preparing

these consolidated annual accounts, in accordance with IAS-8, any

modification in the future of these estimations would be applied from that

point on, recognising the impact of the change in the estimates made in the

consolidated income statement for the year in question.

13

The main estimates and judgements considered in preparing the consolidated annual accounts are the following:

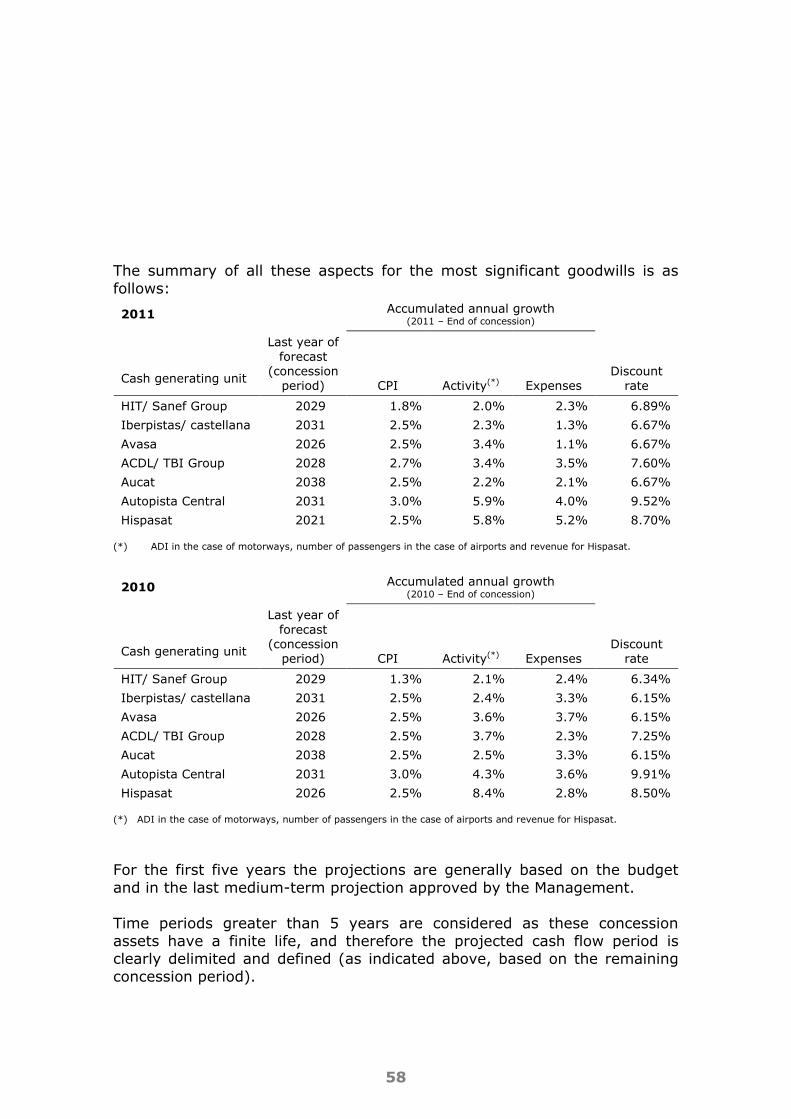

Assumptions used in the impairment test to determine the

recoverability of goodwill and other non-financial (see Notes 3.c, 6 and

7) and financial assets (see Notes 3.d and 11) assets.

Fair value of derivatives and other financial instruments (see Notes 3.e and 10).

Estimates of the intervention cycles in determining the provisions

under IFRIC 12 (see Notes 3.n and 19).

Fair value of assets and liabilities in business combinations (see Note

22).

Financial investments available sale (see Notes 3.d.i, 3.h and 9).

Changes in the consolidation scope (see Notes 8 and 9).

Actuarial hypotheses used in determining the liabilities for post-

employment obligations and other commitments with employees (see

Notes 3.l and 18).

Corporate income tax (see Notes 3.k and 17).

The consolidated annual accounts have been prepared on the basis of

historical cost, except in the cases specifically mentioned in these Notes, such

as those items measured at fair value, which are mentioned in Note 4.b. The consolidated annual accounts have been prepared on the basis of

uniformity in recognition and measurement. If new standards modifying the

existing valuation principles become applicable, they will be applied in

accordance with the transition criteria set down in said standards. Certain amounts in the consolidated income statement and the consolidated

balance sheet have been grouped together for clarity, with their breakdown

being shown in the Notes to the consolidated annual accounts.

The distinction presented in the consolidated balance sheet between current and non-current entries has been made on the basis of whether the assets

and liabilities fall due within one year or more.

Additionally, the consolidated annual accounts include all the information that

is considered necessary for their correct presentation under company law in force in Spain.

14

The consolidated annual accounts of abertis together with the parent Company’s annual accounts and the accounts of subsidiary companies will

be presented at their respective Shareholders’ General Meetings in due

time. The Directors of abertis expect these accounts to be approved

without significant changes.

b) Consolidation principles

i) Consolidation methods Subsidiary Companies

Subsidiary Companies are all those entities in which abertis directly or

indirectly controls the financial and operating policies. This normally occurs

when more than half of the voting rights are held. Additionally, in order to evaluate whether abertis controls another entity, the existence and effect

of potential voting rights that are can be exercised or convertible at this

time are also considered. Subsidiary companies are consolidated as from

the date on which control passes to abertis, and they are de-consolidated

on the date that control ceases to exist. Subsidiary companies are fully consolidated.

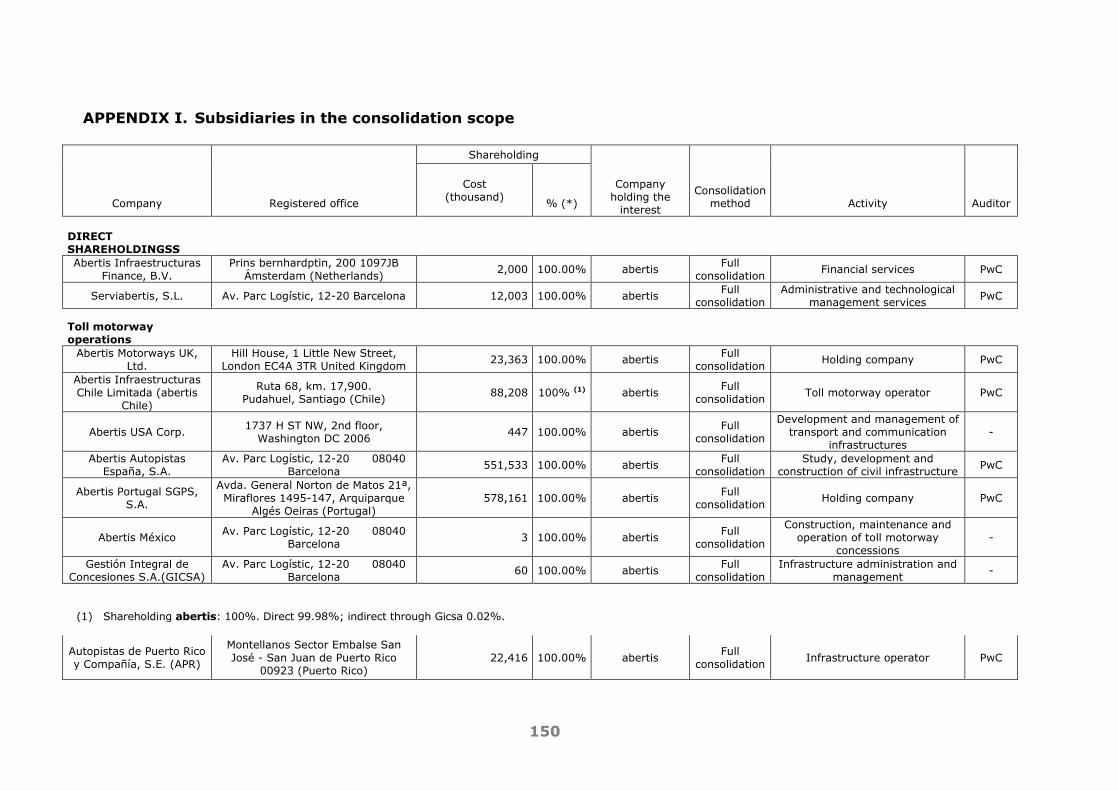

Appendix I to these Notes provides a breakdown of critical information on

all the subsidiary companies included in the consolidation scope at 31

December 2011.

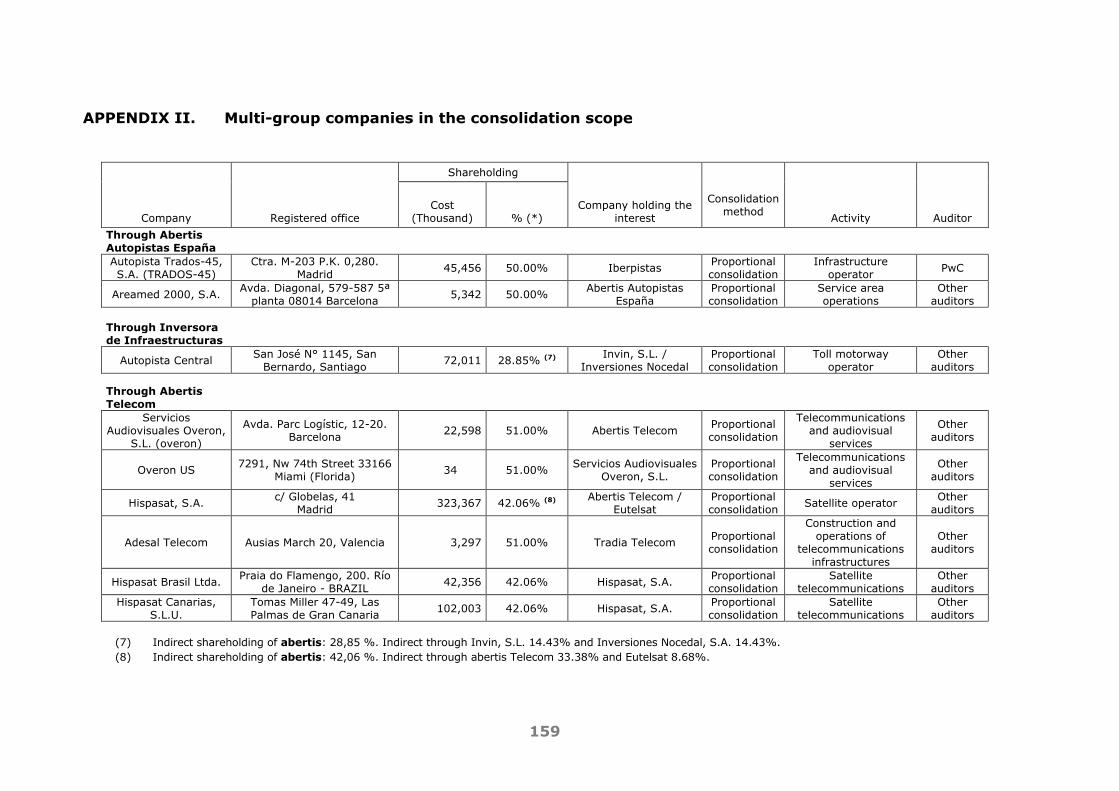

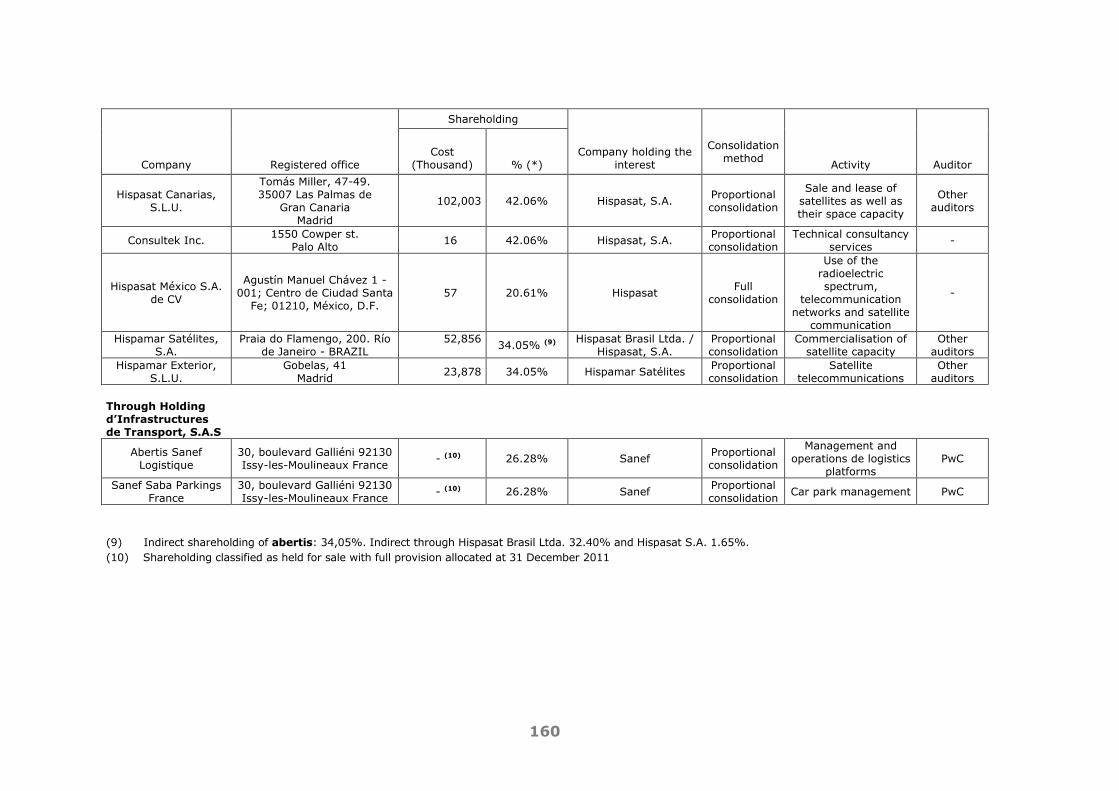

Multigroup Companies (Joint Ventures)

These are companies that have a contractual arrangement with a third party to share control of their activity and where the strategic financial and

operating decisions related thereto require the unanimous arrangement of all

the parties that share control.

The interests of the Group in joint ventures are accounted for under the proportional consolidation method.

Appendix II to these Notes gives information on the multigroup companies

included in consolidation scope at 31 December 2011.

15

Associates

Associates are companies in which abertis has significant influence and a

long-term relationship that fosters and influences its business in spite of a

small representation in the management and control bodies. This is

generally accompanied by a shareholding of between 20% and 50% of the

voting rights unless it can be clearly demonstrated that no such influence exists or when abertis holds less than 20% and it can be clearly

demonstrated that said influence does exist.

Investments in associates are accounted for by equity accounting and

initially stated at acquisition cost. The shareholding of abertis in associates includes, as per IAS 28, goodwill (net of any loss or accumulated

impairment) identified in the acquisition and recorded under “Investments

in associates” in the consolidated balance sheet.

In the case of associates acquired in stages, IAS 28 does not specifically define how to determine the cost of the acquisitions. Therefore, the Group

interprets that the cost of a shareholding in an associate acquired in stages

is the sum of the amounts paid in each acquisition plus the share of the

profits and other changes in shareholders' equity less any impairment which

may have occurred.

Thereafter, the share of abertis in the earnings and reserves of associates is

recognised in the consolidated income statement and as consolidation

reserves (other comprehensive income), respectively, with the value of the

shareholding as the balancing entry in both cases. Dividend receipts and/or

accrual after acquisition are adjusted against the value of the shareholding.

In the event that the Group’s share in the losses of an associate is equal to or

greater than the financial value of its shareholding, including any other

unsecured outstanding accounts receivable, additional losses will not be

recognised unless obligations have been incurred or payments made in the name of the associate.

Appendix III to these Notes provides the particulars of the associates

included in the consolidation scope under equity accounting at 31 December

2011.

16

ii) Standardisation of timing and valuation

Except for Eutelsat Communications, S.A. which year end is 30 June, all the

companies included in the consolidation scope close their financial year on

31 December and for the purposes of the consolidation process the

respective financial statements prepared under IFRS principles have been

used. In accordance with current legislation, these companies present individual annual accounts in accordance with the standards applicable in

their country of origin.

In the specific case of Eutelsat Communications, S.A. the respective timing

standardisation has been undertaken and for the purposes of the consolidation process the respective financial statements prepared under

IFRS principles for the year ended 31 December have been used.

The standards of valuation applied by the Group companies largely coincide.

However, whenever necessary the corresponding adjustments are made to standardise valuation to ensure uniformity of the accounting policies of the

companies included in the consolidation scope with the policies adopted by

the Group.

iii) Differences on first consolidation

The Group uses the acquisition method to account for the acquisition of

subsidiary companies in accordance with the revised IFRS 3. The acquisition

cost is the fair value of the assets, the equity and the liabilities on

acquisition date, plus any asset or liability resulting from the contingent consideration. The costs directly attributed to the acquisition are recognised

directly in the consolidated income statement for the year in which it takes

place.

The identifiable assets acquired, the liabilities and contingencies assumed in a business combination are initially valued at their fair value on acquisition

date, including the non-controlling interests. For each business combination,

the Group can elect to recognise any non-controlling interest in the acquired

company at fair value or for the proportional part of the non-controlling

interest of the net identifiable assets of the acquired entity.

The excess of the acquisition cost over the fair value of the net assets

identified in the transaction is accounted for as consolidation goodwill, which

is assigned to the respective cash generating unit.

17

On the contrary, if the acquisition cost is less than the fair value of the net assets of the company acquired, if the purchase is made under

advantageous conditions, the difference is recognised directly in the

statement of comprehensive income.

Consolidation goodwill is not written off on a straight-line basis and is

subject to an annual impairment test, as indicated in Note 3.c.

In the case of step-acquisitions, when control is obtained, the fair value of

the assets and liabilities of the business acquired must be determined by

including the part already owned. The differences that arise between the

assets and liabilities already recognised must be recognised in the income statement.

In case of step-acquisitions of associates, goodwill is calculated in each

acquisition based on the cost and the share of the fair value of the acquired

net assets on each acquisition date.

As indicated in Note 2.b.i, the goodwill related to acquisitions of associates

is included as part of the respective shareholding, and is valuated in

accordance with the procedures set out in Note 3.b.iv.

iv) Elimination of internal operations

The balances and intercompany transactions between companies of the

Group are eliminated, as are the unrealised profits from third parties

generated by transactions between Group companies. Unrealised losses are also eliminated, unless the transaction provides evidence of a loss due to

the impairment of the transferred asset.

In transactions with joint ventures (multigroup companies) the share in the

profit or loss from operations with Group companies is only recorded in the

part corresponding to other participants.

The profit and loss from transactions between the Group and its associates

is recorded in the Group's financial statements only to the extent that they

correspond to the shareholdings of other investors in the associates which

are not linked to the investor.

18

v) Translation of financial statements in foreign currencies

The financial statements of foreign companies, none of which operate in

hyperinflationary economies, prepared in a functional currency (that of the

main economic area in which the entity operates) distinct from the

presentation currency of the consolidated annual accounts (Euros) are

translated into Euros using the year end exchange rate, whereby:

Net equity is translated at historical exchange rates.

Entries in the income statement are translated using the average

exchange rate for the period as an approximation of the exchange rate at the transaction date.

The other balance sheet entries are translated at the year end

exchange rate.

As a result of using this method, the currency translation differences

generated are included under “Reserves – Cumulative translation

adjustments” in net equity on the consolidated balance sheet.

vi) Others

The currency translation differences that arise from the translation of net

investment in foreign companies, and from loans and other instruments in

non-Euro currencies designated as hedges on these investments, are

recorded against net equity. When they are sold, said cumulative translation adjustments are recognised in the income statement as part of the

consolidated gain or loss on the sale.

The adjustments to goodwill and the fair value that arise from the

acquisition of a foreign entity are considered as assets and liabilities of the foreign entity and are translated using the year end exchange rate.

vii) Variations in the consolidation scope The most significant changes in the consolidation scope and in the

companies falling under said scope in 2011 have been as follows:

On 11 April 2011 incorporation of the company Saba

Infraestructuras, S.A. fully owned by Abertis Infraestructuras, S.A.

This company has been fully consolidated.

19

Within the framework of the reorganisation of the structure of abertis businesses as detailed in Note 26, on 18 May 2011 the car

parks and logistics facilities businesses have been provided to this

company through contribution of all the shares held by Abertis

Infraestructuras, S.A. in Saba Aparcamientos, S.A. and Abertis

Logística, S.A. through a non-monetary capital increase.

In June 2011, the General Meeting of Shareholders of abertis approved the payment of an extraordinary interim dividend for the

profits of the year of Euros 0.67 per share which may be optionally

exchanged for shares in Saba Infraestructuras, S.A. (see Note 13.c

and 26). Following this payment, abertis then held 78.06% of the

aforementioned company.

Finally, on 26 October 2011, Abertis Infraestructuras, S.A. sold its

entire shareholding which on the aforementioned date it held in Saba

Infraestructuras, S.A. This sale was carried out in accordance with

the share purchase contract which abertis held with Criteria

CaixaHolding, S.A.U. (and other third parties), see Note 26.

With effect on 31 December 2011, the classification of the 14.61%

holding in the capital of Brisa has changed from an available-for-sale

financial asset to a shareholding in an associate and now recorded

using equity accounting (See Note 8 and 9).

Other changes having a minor impact have been as follows:

On 18 May 2011 incorporation of the company Gestora del Espectro,

S.L., fully owned by Retevisión I, S.A. This company has been fully

consolidated.

Incorporation of the company Autopistas Metropolitanas de Puerto Rico, LLC (metropistas), 45% owned by abertis are recorded using

equity accounting. In September 2011 this company was awarded

the concession for managing the PR-22 and PR-5 motorways in

Puerto Rico (see Note 8).

Increase, with effect on 1 April 2011, of sanef’s shareholding in

Sanef Tolling, Ltd from 70% to 100%.

Increase, with effect on 1 January 2011, of sanef’s shareholding in

Bet Eire Flow from 80% to 100%.

On 30 December 2011 sale of the company Túnel del Cadí, S.A.C., recorded at that time using equity accounting, in which abertis had

an indirect shareholding of 37.21% (see Note 8).

20

On 20 December 2011 sale of the company Pt Operational Services Limited (PTY), recorded at that time using equity accounting, in which

abertis had a shareholding of 33.30%.

Exit from the consolidation scope in May 2011 of the company Acesa

Italia, S.r.L., in which abertis had an indirect shareholding of 100% as a result of its liquidation, following the sale of the 6.68%

shareholding in Atlantia.

Exit from the consolidation scope in June 2011 of the companies

Aldergrove International Airport Limited, Aldergrove Airport Limited and Aldergrove Car Parks, in which abertis had an indirect

shareholding of 90%, as a result of their liquidation.

Exit from the consolidation scope in August 2011 of the company

MB121 Limited, in which abertis had an indirect shareholding of 90%, as a result of its liquidation.

Exit from the consolidation scope in November 2011 of the company

TBI Global Limited, in which abertis had an indirect shareholding of

90%, as a result of its liquidation.

Takeover merger of companies of ACDL Group TBI Cargo Inc and TBI

(US) Holdings Limited, the latter 90% owned abertis (through acdl).

In addition, with effect on 21 December 2011 Abertis Infraestructuras, S.A. sold to Abertis Autopistas España, S.A. (with no impact on these

consolidated annual accounts as both companies belong to the consolidation

scope) the shareholdings of the companies Autopistas Concesionaria

Española, S.A. (acesa), Infraestructures Viàries de Catalunya, S.A.

(invicat), Autopistas Aumar Concesionaria Española, S.A. (aumar) and

Iberpistas, Concesionaria Española, S.A. (iberpistas), with the aim of grouping together all the operator companies of Spanish motorways under

one single company responsible for joint management of all of those

companies.

Additionally, in 2010 there were no changes with a significant impact on the consolidation scope or on the companies making up the scope although the

following changes with a lesser impact on the corresponding consolidated

accounts were recorded:

On 3 June 2010, the associate Centro Intermodal de Logística, S.A. (cilsa) sold its entire stake in the Group subsidiary Consorcio de

Plataformas Logísticas, S.A. (cpl), and reduced the indirect

shareholding of abertis as at that date from 66,68% to 51%.

21

On 30 December 2010 the shareholding of abertis (through the subsidiary Abertis Logística, S.A.) in Consorcio de Plataformas

Logísticas, S.A. (cpl), a fully consolidated company, rose from the

aforementioned 51% to 64.5%, through the capital increase that the

latter performed, which was subscribed by Abertis Logística, S.A. through a non-cash contribution of the 32% stake it held in Centro

Intermodal de Logística, S.A. (cilsa).

As a result of the non-cash contribution made by the other

shareholder of Consorcio de Plataformas Logísticas, S.A. (cpl) in

order to subscribe the aforementioned capital increase, cpl has come

to own 44% of Centro Intermodal de Logística, S.A. (cilsa), and, accordingly, this company, in light of the new shareholder

arrangements as from that date, has gone from being accounted for

by equity accounting to proportional consolidation effective 30

December 2010. Consequently, the indirect shareholding of abertis

of cilsa was 28.38%.

The shareholding operations at 30 December 2010 did not have a

significant impact on equity.

Increase in the shareholding of abertis in Saba Aparcamientos, S.A.

(saba), from 99.46% a un 99.48%.

Increase in the shareholding of Saba Aparcamientos, S.A. in Parcheggi Pisa, S.r.L. from 70% to 80%, and, accordingly, the

indirect shareholding of abertis amounted to 79.58%.

Increase in the shareholding of Saba Aparcamientos, S.A. in Saba

Aparcament de Santa Caterina, S.L. from 92% to 100%, and,

accordingly, the indirect shareholding of abertis amounted to

99.48%.

Increase in the shareholding of abertis in Autopistas de Puerto Rico

and Compañía, S.E. (APR) from 75% to 100%.

Sale in September 2010 of Rabat Parking, S.A. in which abertis had

an indirect shareholding of 50.72%.

Teledifusión de Madrid, S.A., in which abertis had an indirect shareholding of 80%, left the consolidation scope in June 2010.

Takeover merger of the Group companies Saba Campo San Giacomo

S.r.L. and Saba Italia S.p.A., that latter of which is 99.48% owned by

abertis (through Saba Aparcamientos, S.A.).

22

Incorporation of the company Overon US, Inc., fully owned by Servicios Audiovisuales Overon, S.L. (overon), proportionally

consolidated by the Group by virtue of current shareholders’

arrangements (abertis holds an indirect 51% stake).

Incorporation of the company Impulso Aeroportuario del Pacífico, S.A. de C.V., 99.9% owned by the associate Aeropuertos Mexicanos del

Pacífico, S.A. de C.V. (AMP), consolidated by equity accounting

(abertis holds an indirect stake of 33.33%).

Incorporation of the company Parcheggio Largo Bellini S.r.L 80% owned by Saba Italia S.p.A and fully consolidated. Through Saba

Aparcamientos, S.A. abertis holds an indirect stake of 79.58%.

Incorporation of the company Constructura de Infraestructura Vial

SAS, 40% owned by abertis. This company has been consolidated by equity accounting.

Incorporation of the company Consorci de Parcs Logístics del

Penedés, S.L., fully owned by Abertis Logística, S.A. This company

has been fully consolidated.

Incorporation of the company Consorci de Parcs Logístics Toulouse,

fully owned by Consorcio de Plataformas Logísticas, S.A. (cpl). This

company has been fully consolidated.

viii) Transactions with non-controlling interests

Under IAS 27 revised, transactions with non-controlling interests are

recorded as transactions with the owners of Group equity. Accordingly, in

the purchases of non-controlling interests, the difference between the consideration paid and the respective proportion of the book value of the

net assets of the subsidiary impacts net equity. Likewise, the gains or loss

from the sale of non-controlling interests are also recognized in the net

equity of the Group.

23

In the event that significant influence or control is lost, the remaining interest is stated once again at fair value, and the difference in relation to

the investment previously recorded is recognized in the consolidated income

statement for the year. Additionally, any amount previously recognized in

other comprehensive income in relation to this entity is recorded as if the

Group had directly sold all the related assets and liabilities, which would

mean, as the case may be, that the amounts previously recognized in other comprehensive income would be reclassified to the consolidated income

statement for the year. If the decrease in the shareholding in an associate

does not imply a loss of significant influence, the proportional part formerly

recognized under Other comprehensive income would be reclassified to the

income statement.

3. ACCOUNTING POLICIES

The most significant accounting policies applied in the preparation of these

consolidated annual accounts are as follows:

a) Property, plant and equipment (PPE)

Property, plant and equipment are accounted for at cost of acquisition less depreciation and the accumulated amount of any loss in value. Property,

plant and equipment includes the legal revaluations applied in years prior to

1 January 2004 allowed under local accounting standards, which value has

been taken as cost of acquisition as permitted under IFRS-1 “First-time

Adoption of International Financial Reporting Standards”.

Capital grants received reduce the cost of acquisition of property, plant and

equipment and are recorded when the requirements are met in order to

demand payment of the grant. Grants are released to profit and loss on a

straight-line basis depending on the useful life of the asset financed reducing the depreciation charge for the year.

Personnel costs and other expenses, as well as net financing costs directly

related to property, plant and equipment, are capitalised as part of the

investment until brought into use.

Costs of refurbishment, extension or improvement of property, plant and

equipment are capitalised only when they increase the capacity,

productivity or extend the useful life of the asset, provided that it is possible

to know or estimate the net carrying value of the assets which are written

off when replaced.

24

The costs of repairs and maintenance are charged to the consolidated

income statement in the year in which they are incurred.

The investment in infrastructure recorded by the operator companies under

PPE includes the assets over which the Grantor holds no control (not owned

by Grantor given that it does not control the residual value of the assets at the end of the concession), although they are necessary for the operation

and management of the infrastructure. These assets mainly comprise the

buildings used in operations, the toll facilities and material, video-

surveillance, etc. The depreciation of property, plant and equipment is calculated on a

straight line basis using the estimated useful life of the assets, taking into

consideration wear and tear derived from normal use.

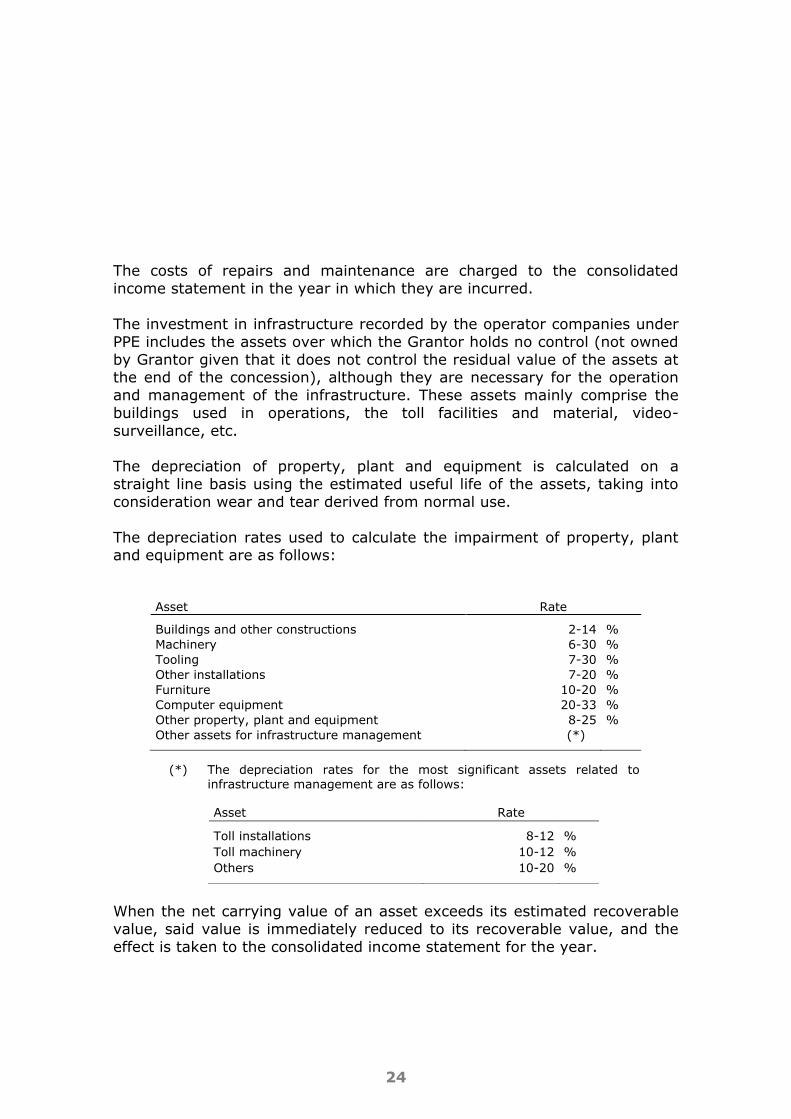

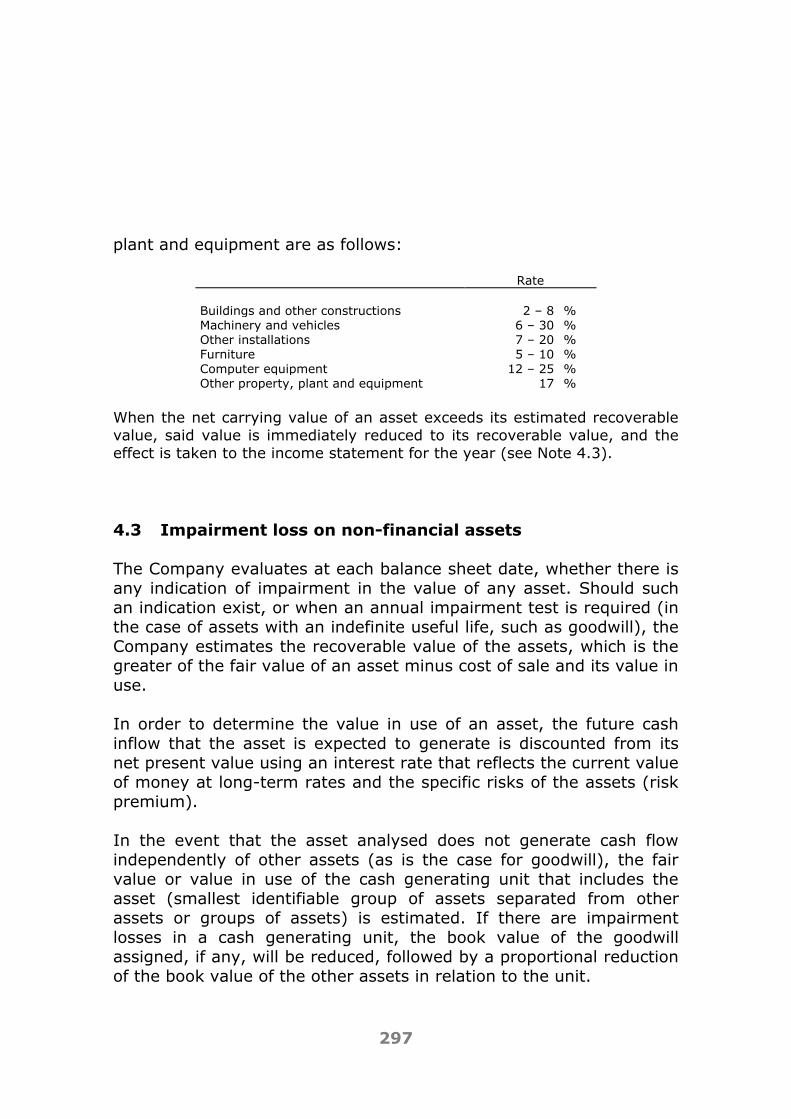

The depreciation rates used to calculate the impairment of property, plant and equipment are as follows:

Asset Rate Buildings and other constructions 2-14 %

Machinery 6-30 %

Tooling 7-30 %

Other installations 7-20 %

Furniture 10-20 %

Computer equipment 20-33 %

Other property, plant and equipment 8-25 %

Other assets for infrastructure management (*)

(*) The depreciation rates for the most significant assets related to infrastructure management are as follows:

Asset Rate Toll installations 8-12 %

Toll machinery 10-12 %

Others 10-20 %

When the net carrying value of an asset exceeds its estimated recoverable

value, said value is immediately reduced to its recoverable value, and the

effect is taken to the consolidated income statement for the year.

25

b) Goodwill and other intangible assets

The intangible assets indicated below are recorded at acquisition cost less

the accumulated amortisation and any loss due to impairment, useful life

being evaluated on the basis of a prudent estimate. Capital grants received

reduce the cost of acquisition of the intangible asset and are recorded when the requirements are met in order to demand payment of the grant. Grants

are released to profit and loss on a straight-line basis depending on the

useful life of the asset financed reducing the amortisation charge for the

year. The net carrying value of intangible assets is reviewed for possible

impairment when certain events or changes indicate that their net carrying

value may not be recoverable.

i) Research and development expenses

Research costs are expensed as they are incurred, whilst the expenses on

development incurred in a project are capitalised if the project is feasible

from a technical and commercial perspective, if there are sufficient technical

and financial resources to complete the project, if the costs incurred can be determined in a reliable manner as established by the international

standard, and the generation of future profits is probable. These are

recorded at their cost of acquisition.

The amortisation is made on the basis of the estimated useful life for each project (between 3 and 5 years).

ii) Computer applications Refers principally to the amounts paid for access to ownership or for the right

to use computer programs, only when usage is expected to cover several

years.

The computer applications are stated at their acquisition cost and amortised on the basis of their useful life (between 3 and 5 years). Maintenance

expenses on these computer applications are charged to the income

statement in the year in which they are incurred.

26

iii) Administrative concessions

Administrative concessions are listed as assets valued at the total amount of

the payments made to obtain them.

IFRIC 12 regulates the treatment of public-to-private service concession arrangements when:

The Grantor controls or regulates which services the operator must

provide with the infrastructure, to whom these services must be

rendered, and, at what price, and

The Grantor controls the entire significant residual interest in the

infrastructure at the end of the arrangement.

Under these concession arrangements, the operator acts as a service

provider, specifically, on the one hand, construction services or infrastructure enhancement, and, on the other hand, operational and

maintenance service during the term of the arrangement. The consideration

received for these services is recorded bearing in mind the type of

contractual right received:

In cases in which the right is granted to charge a price to users for the user of the public service, and the latter is not unconditional but

depends on the fact that the users actually use the service, the

consideration for the construction or enhancement service is recorded

as an intangible asset under “Other intangible assets – administrative concessions” in application of the intangible asset model, in which the

risk of demand is borne by the operator. This model is applicable to

most concessionary companies.

If an unconditional right is granted by the Grantor (or on its account)

to receive cash or other financial assets, and the Grantor has little or no capacity to avoid the payment, the consideration for the

construction or enhancement service is recorded as a financial asset

under “Debtors and other receivables – public administration debtors”

(see section d.ii of this Note) in application of the financial model, in

which the operator bears no risk of demand (payment is made even if the infrastructure is not used since the Grantor guarantees payment

to the Operator of a fixed or specifiable amount or of the deficit, if

any). This model is residually applicable for the Group to the odd

airport.

27

The amounts which appear under the heading "Administrative concessions"

mostly result from the transition to the application of IFRIC 12 with effect

from 1 January 2009, which are the result of their reclassification from the

heading of "property, plant and equipment" and for the same carrying

amount which appear on said date, in line with the provisions in paragraph

30 of the transition of IFRIC 12.

The administrative concessions have a finite useful life and their cost if

recorded as an intangible asset, is expensed, through their amortisation, over

the term of the concession on a straight-line basis. In the case of administrative concessions acquired through business

combinations after 1 January 2004 (IFRS transition date), these, as per IFRS-

3, are stated at fair value (on the basis of valuations based on discounted

cash flow analyses at their current value at the acquisition date) and

amortised on a straight-line basis over the concession period.

iv) Goodwill

Goodwill generated in different business combinations, represents the surplus

of the acquisition cost over the fair or market value of the identifiable net assets of all the company acquired at acquisition date.

The possible impairment of goodwills recognised separately (those of

subsidiary and jointly-controlled companies) is tested annually for

impairment to determine whether its value has declined to a level below the carrying value at the aforementioned transition date, and, as the case may

be, the necessary charge is made against the consolidated income statement

for the year (see Notes 3.c and 6). The losses for impairment of goodwill are

not subsequently reversed. The impairment of the goodwills included in the carrying value of the equity

investment in associates is not tested separately. However, under IAS 36,

the total carrying value of the investment is tested for impairment by

comparing the recoverable amount (the greater of value in use and fair

value, minus cost of sale) to carrying value, provided that there are indications that the value of the investment may have been impaired.

The loss or gain obtained from the sale of an entity includes the carrying

value of the goodwill of the entity sold.

28

In view of the fact that the goodwill is considered an asset of the acquired

company (except the goodwills generated prior to 1 January 2004, which

under IFRS-1 were considered assets of the acquiring company), a subsidiary

using a functional currency other than the Euro valuated in the functional

currency of the subsidiary, and the translation into Euros, is made at the exchange rate on the balance sheet date, as indicated in Note 2.b.vi.

v) Other intangible assets

Primarily includes licences for the management of airport infrastructures, which are carried as assets in the consolidated balance sheet at fair value at

acquisition moment, obtained on the basis of valuations based on the

analysis of discounted cash flows at their current value at the acquisition date

as per IFRS-3. These are expensed using the straight line amortisation

method.

c) Impairment losses on non-financial assets

The Group evaluates, at each balance sheet date, whether there is any

indication of impairment in the value of any asset. Should such an indication exist, or when an annual impairment test is required (in the case of

goodwill), the Group estimates the recoverable value of the assets, which is

the greater of the fair value of an asset minus cost of sale and its value in

use. In order to determine the value in use of an asset, the future cash

inflow that the asset is expected to generate is discounted from its net present value using an interest rate that reflects, amongst other, the

current value of money at long-term rates and the specific risks of the

assets (risk premium). See Note 6.

In the event that the asset analysed does not generate cash flow independently of other assets (as is the case for goodwill), the fair value or

value in use of the cash generating unit that includes the asset (smallest

identifiable group of assets separated from other assets or groups of assets)

is estimated. If there are impairment losses in a cash generating unit, the

book value of the goodwill assigned, if any, will be reduced, followed by a

proportional reduction of the book value of the other assets in relation to the unit.

29

Losses for impairment (surplus of the asset’s book value over the recoverable value) are recognised in the consolidated income statement for

the year.

With the exception of goodwill, where impairment losses are irreversible, if

the Group has recognised losses for impairment of assets at the end of each

financial year, an evaluation will be made to determine whether the

indications of impairment have disappeared or lessened, and the recoverable value of the impaired asset, if applicable, will be estimated.

A loss due to impairment recognised in prior years will only be reversed if

there is a change in the estimates used to determine the recoverable value

of the asset as from the time the last loss due to impairment was recognised. If this is the case, the book value of the asset would increase to

its recoverable value, which cannot exceed the book value that would have

been recorded, net of amortisation, had the impairment loss on the asset in

prior years not been recorded. This reversal would be recorded in the

consolidated income statement for the year.

d) Investments and other financial assets (excluding derivative

financial instruments)

The Group determines the classification of its financial assets when they are initially recognised. At the close of 31 December 2011 the financial assets

have been classified under the following categories:

i) Available-for-sale financial assets This entry in the consolidated balance sheet includes those investments in

which the Group does not exert any significant influence or control (see

Note 9). These are classified as non current assets unless there is an

intention to dispose of the investment in the twelve months as from the

consolidated balance sheet date, in which case they are classified as current assets.

These investments are stated at fair value, and gains or losses arising from

changes in value are part of the other comprehensive result until the

investment is sold or suffers losses due to impairment.

The Group evaluates, at each balance sheet date, whether there is any

effective indication of impairment, among others, taking into account

whether there has been a significant or prolonged decrease in the fair value

of the securities below cost price. If there are any indications of this type,

the accumulated loss previously recorded in net equity under “Reserves –

30

investments available-for-sale” would be transferred to profit and loss as gains or losses on the respective financial assets.

For the purposes of identifying indications of impairment, the Group first

uses Spanish accounting standards (Spanish General Chart of Accounts)

which indicate that an available-for-sale financial asset will be assumed to

have suffered impairment after a fall of one and a half years and forty percent of its price without their being a recovery in its value. At any event,

and where necessary, a specific analysis is conducted on those figures of

the instrument which are deemed essential for confirming or rejecting the

need, or not, to record deterioration of the capital instrument.

The fair value of the investments that are actively traded on official stock

exchanges is taken as the trading price at the close of the market at the

balance sheet date. In the case of investments where there is not an active

market, the fair value is determined using valuation methods, such as

projections of discounted cash flows. If their market value cannot be determined in a reliable manner, they will be valued at cost or at a lower

amount if there is evidence of impairment.

Dividend income arising from available-for-sale financial assets are recorded

under “Financial income” (see Note 20.d) in the consolidated income

statement when the right of the Group to receive them is established.

ii) Trade and other receivables

This entry corresponds primarily to:

Loans granted to associates or related entities which are valued at

amortised cost using the effective interest method. This value is

decreased, as the case may be, by the respective provision for impairment of the asset.

Deposits and guarantee deposits recorded at their nominal value.

Trade accounts receivable, which are stated at their nominal

value, which is similar to initial fair value. Said value is reduced, if necessary, by the corresponding provision for bad debts (loss for

impairment of asset) whenever there is objective evidence that

the amount owed will not be partially or fully collected, charged

against the consolidated income statement for the year.

31

Accounts receivable resulting from the application of the financial model in recording certain concession arrangements subject to

IFRIC 12 (see section b.iii of this Note). This right is stated initially

at fair value and subsequently at amortised cost, and at the

balance sheet date financial income is booked that has been calculated using an effective interest rate, during the term of the

concession arrangement.

e) Derivative financial instruments The Group uses derivative financial instruments to manage its financial risk

arising principally from fluctuations in interest rates and exchange rates

(see Note 4). These derivative financial instruments, whether or not they

have been classified as hedges, have been recorded at fair value, which is

the year end market value of listed instruments, or valuations based on the analysis of discounted cash flows using assumptions that are mainly based

on the market conditions at the balance sheet date for unlisted derivative

instruments.

At the beginning of the transaction the Group documents the relationship between the hedging instruments and the assets they cover, as well as the

risk management objectives and the strategy for its hedging transactions.

The Group also documents their evaluation, both at the beginning and

continuously, as to whether the derivatives that are used in the hedging

transactions are highly effective for offsetting the changes in fair value or cash flows of the items hedged.

The fair value of derivative financial instruments used for hedging purposes

is set out in Note 10, and the variation in the hedging reserve recorded

under consolidated net equity is set out in Note 13.

Classification on the balance sheet as current or non-current will depend on

whether the maturity of the hedge at the year end is less or more than one

year. Non-hedge derivatives will be classified in any case as current.

32

The criteria used to account for these instruments are as follows:

i) Fair value hedges

The changes in the fair value of the designated derivatives that meet the

conditions to be classified as hedging operations of the fair value of assets

or liabilities are recorded in the income statement for the year under

“Variation in valuation of hedging instruments”, together with any change in the fair value of the asset or liability covered by the hedge attributable to

the risk hedged. This corresponds mainly to those derivative financial

instruments contracted by the Group companies to convert fixed interest

debt into floating rate debt.

ii) Cash flow hedges

The positive or negative changes in the valuation of the derivatives

classified as cash flow hedges are charged, in the effective portion, net of

any tax impact, to consolidated equity under the entry “Reserves – Hedge reserve”, until the hedged item impacts the result for the year (or when the

hedged item matures or is sold or if it is no longer probable that the

transaction will take place), at which point the retained earnings or losses in

net equity are transferred to the consolidated income statement for the

year.

The positive or negative differences in the valuation of the derivatives

corresponding to the ineffective portion, if they exist, are recorded directly

in the consolidated income statement for the year under “Variation in

valuation of hedging instruments”.

This type of hedge corresponds primarily to those derivatives contracted by

the Group companies that convert floating rate debt to fixed rate debt.

iii) Hedging net foreign investment in non-euro currency

In certain cases abertis finances its activities in the same functional

currency in which the foreign investments are held so as to reduce the

exchange rate risk. This is done by raising finance in the corresponding

currency or by contracting cross currency interest rate swaps.

33

The hedging of net foreign investments is accounted for in a way that is

similar to the cash flow hedge. The gains or losses on the hedging

instrument for the effective portion are recorded under net equity and the

gains or losses related to the ineffective portion are recognised immediately in the consolidated income statement for the year.

Accumulated gains or losses in net equity are carried in the income

statement when the foreign transaction is concluded.

iv) Derivatives not qualified as accounting hedges

In case there are derivatives that do not meet the criteria established to be

qualified as hedges, the positive or negative variation arising from recalculating the fair value of these derivatives is taken directly to

consolidated profit and loss for the year.

f) Inventories Inventories consist primarily of spare parts for property, plant and equipment

and are valued at cost, calculated using the weighted average price method,

making the necessary valuation adjustments and raising the corresponding

impairment.

g) Cash and cash equivalents

Cash and cash equivalents include cash on hand, demand deposits in banks

and short-term investments in highly liquid instruments maturing in three months or less.

h) Non current assets held for sale Non current assets are classified as held for sale when their value will be

recovered mainly through sale, provided that said sale is highly likely. These

assets are stated at the lesser of their book value or fair value, less the costs

of sale.

34

i) Treasury shares

In the event that any Group entity or the Parent Company acquires shares of

abertis, these are recorded under “Treasury shares” in the consolidated balance sheet and consolidated net equity is reduced. The shares are stated

at acquisition cost, without recording any provisions.

When these shares are sold, any amount received, net of any additional

directly attributable transaction costs and the corresponding effect of the tax on the profit generated, and are included in the net equity attributable to

equity holders of the parent Company.

j) Borrowings

Borrowings are initially recorded at fair value, including the costs incurred in

raising the debt. In subsequent periods they are valued at amortised cost and

the difference between the funds obtained (net of the costs involved in

raising the funds) and the repayment value, as the case may be, and if it is

significant, is recorded in the income statement over the life of the debt using the effective interest method.

Borrowings at a fixed interest rate hedged using derivatives that modify this

interest rate from fixed to floating are stated at fair value for the hedged

component, and these variations are taken to profit and loss, thus offsetting the impact on results of the variation in the fair value of the derivative

instrument.

k) Income tax

The tax expense (or, where appropriate, income) on profits is the total

amount accrued for this purpose during the year, representing both current

and deferred tax. Both the current tax expense (or, where appropriate, income) and deferred

tax expense are recorded in the consolidated income statement for the year.

However, the tax effect relating to items recorded directly in other

comprehensive income or net equity is recorded under other comprehensive

income or net equity.

35

The deferred tax is calculated using the liabilities method based on the

balance sheet, on the temporary differences that arise between taxable

income of the assets and liabilities and their accounting amounts in the

consolidated annual accounts, under the regulations and using tax rates in force, or pending approval, on the balance sheet date and which are

expected to be used when the corresponding deferred tax asset is realised or

the deferred tax liability is settled.

Deferred tax liabilities that arise from temporary differences with subsidiary, multi-group companies and/or associates are always recorded, except in

those cases in which the Group can control the date on which the temporary

differences will reverse and it is probable that they will not reverse in the

foreseeable future.

The deferred income tax assets are recognised if it is probable that future tax

profit will arise with which to offset the deductible temporary differences or

the losses or unused fiscal credits. In the case of deferred tax assets that

could arise due to temporary differences with subsidiary and multigroup

companies and/or associates, these are recognised if additionally it is

possible that they will reverse in the foreseeable future.

The recoverability of deferred tax assets is evaluated when they are

generated, and at each year end, depending on the evolution of results

expected from the companies according to their respective business plans.

l) Employee benefits

Under the respective collective bargaining arrangements, various companies

in the Group have the following commitments with their employees:

i) Post-employment obligations:

Defined contributions to employee welfare instruments (employee

pension plans and collective insurance policies).

Defined benefits, in the form of bonuses or payments for retirement from the company and temporary and /or life-time annuities.

36

In defined contribution employee welfare, the Company makes predefined

contributions to an external entity and does not have a legal or real

obligation to make additional contributions in the event that this entity does

not have sufficient assets to cover the employee payments that related to the services provided in the current year and previous years. The annual expense

recorded is the corresponding contribution made in the year.

In the defined benefit commitments, where the Company assumes certain

actuarial and investment risks, the liability recorded on the balance sheet is the present value of the obligations at the balance sheet date less the fair

value of the possible assets for this commitment on said date, plus or minus

any unrealised actuarial gain or loss, less any amount arising from the cost of

past services not yet recognised.

The actuarial valuation of the defined benefit commitments is made annually

by independent actuaries using the projected credit unit method to determine

both the current value of the obligations and the cost of the services provided

in the current and previous years. The actuarial gains and losses arising from

changes in the actuarial assumptions are recognised in the year in which they

occur. They are not included in the consolidated income statement, but presented in the statement of comprehensive income.

Costs for past services are recognised as an expense, and are allocated on a

straight-line basis over the average period remaining until the right to receive

the benefits has finally vested. Nevertheless, when the benefits are immediately irrevocable after the introduction of a defined benefits plan, or

following any change in the plan, the costs for past services are recognised

immediately.

The hedging of commitments by making contributions to an insurance policy, where the legal or implied obligation to meet the agreed benefits remains, is

always treated as a defined benefit.

ii) Other long-term benefits, related to the length-of-service of the employee in the company.

In respect of long-term commitments for the length of service of employees

in the company, the liability recognised on the balance sheet coincides with

the current value of the obligations at the balance sheet date, if there are no

other assets related to them.

37

The projected credit unit method is used to determine both the current value

of the obligations at the balance sheet date and the cost of the services

rendered during the current year and previous years. The actuarial gains and

losses that arise from changes in the actuarial assumptions are recognized, unlike the post-employment obligations, in the year in which they are

generated, in the consolidated income statement for the year.

iii) Share-based payments.

As indicated in Note 28, the group has a Management compensation plan

consisting in the distribution of options in abertis stock that can only be

settled in shares.

This plan is valuated at its fair value, at the date it is initially distributed,

using a generally accepted financial calculation method, which, amongst

others, takes into account the option exercise price, volatility, exercise term,

expected dividends and the risk-free interest rate.

The cost of the plan is charged to the consolidated income statement as a personnel expense as it accrues during the period of time required for the

employee to remain in the company in order to exercise the option, while a

counter-entry is made in consolidated net equity, without a re-estimate of its

initial valuation, as per IFRS-2. However, at the year end the Group reviews

its original estimates of the number of options expected to be exercisable (affected, inter alia, by the impact of any bonus share issue) and recognizes,

as the case may be, the impact of its review on the income statements by

making the respective adjustment to consolidated net equity as it accrues

during the period of time remaining until the end of the period of time

required for the employee to remain in the company in order to exercise the option.

m) Transactions in foreign currencies Transactions in foreign currencies are translated into the presentation

currency of the Group (Euro) using the exchange rates in force on the

transaction date. The gains and losses on foreign currencies that arise from

the settlement of these transactions and from the translation of monetary

assets and liabilities held in foreign currency at the year end exchange rates

are recorded in the consolidated income statement, unless they are

38

deferred in net equity as in the case of cash flow hedges and hedges on net investments, as noted in section e) of this Note.

n) Provisions

Provisions are recorded when the Group has a present legal or implied

obligation, as the result of past events where it is probable that a disbursement must be made to settle the obligation and when the amount

can be reliably estimated.

In cases in which the effect of the time value of money is significant, the

amount of the provision is calculated as the present value of the future cash flows that are estimated to be required to settle the existing obligation.