annual report - eximghana.com · mr. dwumah started his career with sinapi aba trust (sat), now...

TRANSCRIPT

2015

ANNUAL REPORTAND FINANCIAL STATEMENTS

EXIMGUARANTY COMPANY GHANA LTDGUARANTEEING CREDIT FOR ECONOMIC GROWTH

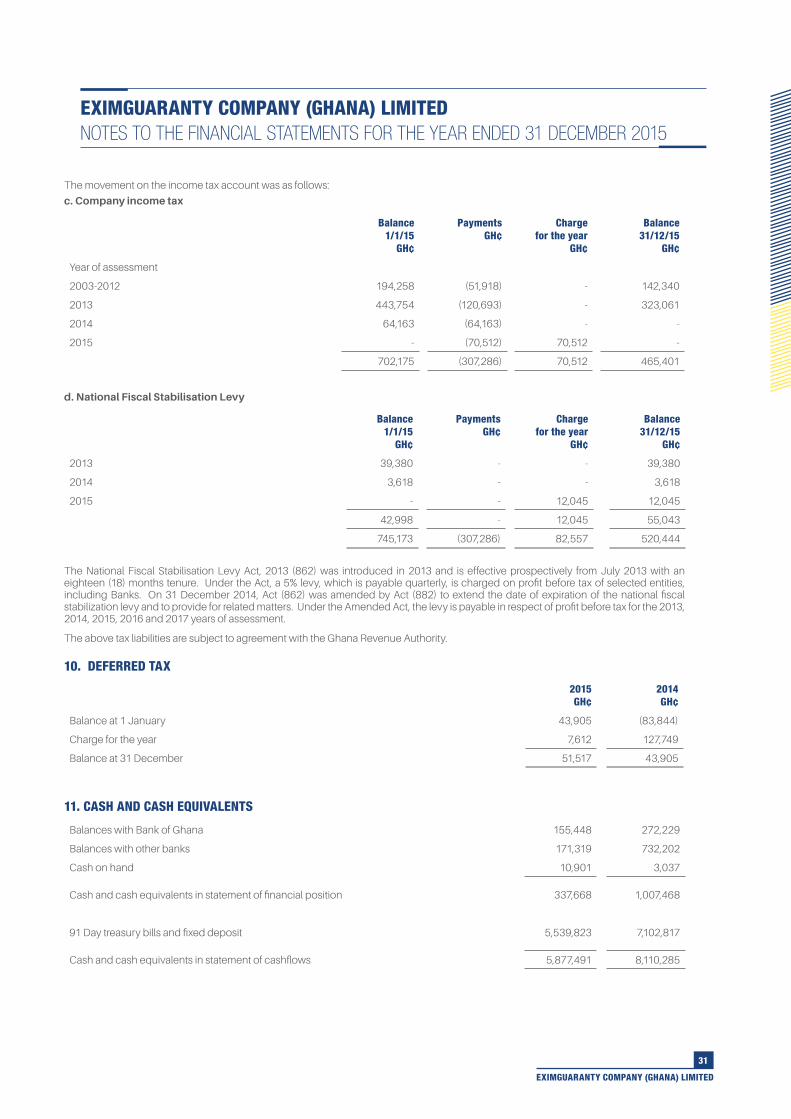

EXIMGUARANTY COMPANY (GHANA) LIMITED

4

EXIMGUARANTY COMPANY (GHANA) LIMITED BOARD OF DIRECTORS, OFFICIALS, AUDITORS AND REGISTERED OFFICE

DIRECTORS Mr. Felix Ntrakwah - Chairman

Mr. Andrew Boye-Doe

Ms Yvonne Quansah

Mr. George Mensah-Asante

Mr Isaac Owusu-Hemeng

Mr. Peter Hayibor

Mr. Richard Amo -Tachie

Mr. Zac Bentum - Managing Director

SECRETARY Mrs. Priscilla Budu

AUDITORS KPMG

13 Yiyiwa Drive, Abelenkpe

PO Box GP242

Accra

SOLICITORS Peasah-Boadu & Co.

P. O. Box CT 3523

Cantonment, Accra

BANKERS Bank of Ghana

Ecobank Ghana Limited

First Atlantic Bank Limited

REGISTERED OFFICE No. 27, Noi Fetreke Street

Roman Ridge Ambassadorial

Estate Extension Accra

www.eximghana.com

CORPORATE INFORMATION

EXIMGUARANTY COMPANY (GHANA) LIMITED

5

CONTENT

4 Corporate Infomation

6 Profile of Directors

9 Profile of Executives

10 Chairman’s Statement

12 Managing Director’s Statement

14 Directors’ Report

16 Report of the Auditors

17 Statement of Comprehensive Income

18 Statement of Financial Position

19 Statement of Changes in Equity

20 Statement of Cash Flows

21 Notes to the Financial Statements

39 Proxy

EXIMGUARANTY COMPANY (GHANA) LIMITED

6

NOTICE OF ANNUAL GENERAL MEETING

NOTICE IS HEREBY GIVEN that the 17th Annual General Meeting of EXIMGUARANTY COMPANY (GHANA) LIMITED will be held at the BOARDROOM OF THE COMPANY, 27 NOI FETREKE STREET, ROMAN RIDGE AMBASSADORIAL ESTATES EXTENSION, ACCRA on Thursday 23rd June 2016 at 11.00am to transact the following business:

1. To receive and consider the Audited Financial Statements for the year ended 31st December 2015 together with the Reports of the Directors and Auditors thereon.

2. To authorise the Directors to determine the remuneration of the Auditors.

3. To approve of the fees of the Directors.

Dated this 18th day of May 2016

BY ORDER OF THE BOARD

PRISCILLA BUDU (MRS)

SECRETARY

NOTE

A member of the company entitled to attend and vote is entitled to appoint a Proxy to attend and vote instead of him/her. A Proxy form is attached.

EXIMGUARANTY COMPANY (GHANA) LIMITED

7

PROFILE OF DIRECTORS

MR. FELIX NTRAKWAH, CHAIRMAN

Mr Felix Ntrakwah is a senior member of the Ghana Bar Association with specialization in corporate commercial law practice. He was for years a director of GCB Limited and the Chairman of its Audit and Finance Committee. He brings unto the board, a wealth of knowledge and experience in corporate governance and corporate finance.

He is the founder of the Corporate Law Institute, Ghana and a member of the Chartered Institute of Arbitrators (UK). Mr Ntrakwah is a member of the International Chamber Of Commerce Court of International Commercial Arbitration in Paris. He is also a fellow of the Litigation Counsel of America.

He was a member of the Committee of Experts who drafted a new Companies Bill for Ghana. Mr Ntrakwah is the chairman of Financial Investment Trust. He also chairs the Royal Senchi Limited and serves on other boards

ANDREW BOYE-DOE

Andrew is a lawyer by profession, specializing in international banking and finance. He is a Director and Head of the Legal Department (General Counsel) at the Bank of Ghana. He is a Director of Export Finance Company, a member of the Board of Trustees of the Financial Investment Trust (FIT). He also serves on the Board of the Financial Intelligence Centre. He is a fellow of the Society for Advanced Legal Studies, London and the Chairman of the Legal and Institutional Issues Committee of the West African Monetary Zone (WAMZ). He is a Research Fellow at the Centre for International Documentation on Organized and Economic Crimes and a Resource Person of the Cambridge International Symposium, UK. Mr. Boye-Doe is also a visiting lecturer in Banking and Finance Law, Commercial Law, International Economic Law and Law and Practice of International Finance in both local and foreign universities.

MS. YVONNE QUANSAH

Yvonne is an economist with good understanding of contemporary macroeconomic, financial sector issues with extensive experience in aid and public debt management having headed the Aid and Debt Management and Financial Sector Divisions of the Ministry. She is a Chief Economics Officer and Director of the External Resources Mobilisation – Bilateral Division at the Ministry of Finance. She has also served as a facilitator/resource person as well as conducted and /or participated in a number of studies and reviews, both locally and internationally.

GEORGE MENSAH-ASANTE

George heads Ecobank Ghana’s Domestic Banking business which covers Local Corporates, SME’s, Public Sector and Retail banking and is also the Cluster Head for Domestic Banking for the West African Monetary Zone (WAMZ) of the Ecobank Group. Mr. Mensah-Asante is also a member of the Board of Directors of Ecobank Ghana.

He is an accomplished banker with over 20 years in treasury management and sales/relationship development. Prior to his appointment as Executive Director of Ecobank, he was the Head, Retail Banking for Ecobank Ghana and was instrumental in growing the bank’s branch network and deposit base. He also worked as Deputy Country Treasurer. George holds a BSc in Administration (Accounting) and an Executive MBA in (Finance) from the University of Ghana, Legon.

ISAAC OWUSU –HEMENG

Isaac is a former Managing Director of The Trust Bank Limited (now part of Ecobank Ltd). He is a fellow of the Chartered Institute of Bankers, Ghana, and a member of the West African Nobles Forum with over 37 years banking and finance exposure. He served for two terms as President of the Chartered Institute of Bankers between 2006 and 2010. In 2014 he was honoured with a Lifetime Achievement award at the Banking Awards by the CIG. He has a vast wealth of experience in risk management and corporate banking and rejoined the Exim Board in September 2012 after serving on the board for 9 years from 2000 to 2009.

EXIMGUARANTY COMPANY (GHANA) LIMITED

8

PROFILE OF DIRECTORS

MR. PETER HAYIBOR

Peter is a Legal Practitioner with over twenty years experience at the Ghana Bar. He is currently the General Manager/General Counsel of the Social Security and National Insurance Trust. He has immense experience in Finance Law, Policy Formulation, Human Resource Management, Litigation, Arbitration, Negotiating and Drafting Commercial Agreements, Mergers and Acquisitions and Pensions Administration. He is member of the Ghana Bar Association, the International Bar Association, Institute of Professional Financial Managers, the Ghana Institute of Directors and the Faculty of Chartered Administrators and Secretaries. Mr. Hayibor is also on the Board of a number of institutions and these include the Global Impact Foundation, Ghana Agro-Food Company Limited (GAFCO) and the Odwen Anoma Rural Bank Limited.

MR. RICHARD AMO-TACHIE

Richard joined the Board of Eximguaranty Company Limited in August 2014. He heads National Investment Bank’s Audit & Bank Inspection Department. He is a Chartered Accountant and a member of the Institute of Chartered Accountants. He holds an ICA (Gh) Professional Certificate and a certificate from the Chartered Institute of Taxation (CIT) Ghana.

MR. ZAC BENTUM, MANAGING DIRECTOR

Zac is a fellow of ACCA and a FCIB. He is a Council Member of the Chartered Institute of Bankers, and a former Council Member of the Association of Chartered Certified Accountants.

Mr. Bentum sits on the Guarantee Fund for Private Investment in West Africa (GARI), Lome, Togo as an Independent Expert and is the West Africa (Alternate) Representative on the Executive Committee of the Association of African Development Finance Institutions (AADFI) based in Cote D’Ivoire. Zac, before joining Exim, worked with Ashanti Goldfields Company Ltd, now Anglogold Ashanti.

Zac currently is a member of the World Bank Taskforce on: Design, Implementation and Evaluation of Public Credit Guarantees for SMEs in Emerging Markets and Developing Economies. He is also a Member of the Presidential Taskforce for the establishment of Ghana Exim Bank.

EXIMGUARANTY COMPANY (GHANA) LIMITED

9

PROFILE OF EXECUTIVE COMMITTEE

ANTHONY K. DWUMAH Head Of Operations

Anthony Kofi Dwumah is an International Certified Expert in SME Lending (from Frankfurt School of Finance and Management), SME/Microfinance Practitioner and Development Analyst and holds a Master of Science (M. Sc.) in Development Policy and Planning and BSc. Agriculture (Economics Option) from the Kwame Nkrumah University of Science and Technology (KNUST), Kumasi. He has over a decade experience in SME finance and microfinance operations.

Before joining Exim, Mr. Dwumah consulted as a Senior Business Advisor for Medical Credit Fund, a Netherland NGO involved in the provision of credit guarantees to private healthcare facilities. He was responsible for credit underwriting and business plan development for SMEs

He also worked as the Head of Operations at HFC Boafo Microfinance Services Ltd from 2009 to 2012 where he facilitated the expansion of branch network from nine to seventeen.

Mr. Dwumah started his career with Sinapi Aba Trust (SAT), now Sinapi Aba Savings and Loans as a credit officer and rose through the ranks to become Operations Manager. He spearheaded the creation of the deposit, SME lending and remittances departments at Sinapi Aba.

MRS. PRISCILLA BUDUHead, Legal/Admin./Company Secretariat

Priscilla holds a LLB (Hons) degree from the University of Ghana and a BL Law from the Ghana School of Law as well as an Executive MBA in Human Resource Management from the

University of Ghana. She has over fifteen years of experience as a lawyer. Her strengths include drafting, industrial relations and good management practices. Prior to joining Eximguaranty, she

was Head of the Legal Department and Secretary to the Board of Directors at ProCredit Savings and Loans Co. Ltd. She is a member of the Ghana Bar Association.

ESTHER KENYENSO Head of Finance

Esther Kenyenso is a member of ICA (Ghana). She has an MBA from the University of Hertfordshire in the United Kingdom and a Bachelor of Science degree in Business Administration from the University of Ghana.

Esther has over 15 years experience in Financial Management, Accounting and Auditing. Prior to joining Exim she worked with Viasat Ghana and Starwin Products as Financial Controller and Head of Finance respectively; having previously worked with KPMG Ghana.

MR. ZAC BENTUM Managing Director

Zac is a fellow of ACCA and a FCIB. He is a Council Member of the Chartered Institute of Bankers, and a former Council Member of the Association of Chartered Certified Accountants.

Mr. Bentum sits on the Guarantee Fund for Private Investment in West Africa (GARI), Lome, Togo as an Independent Expert and is the West Africa (Alternate) Representative on the Executive Committee of the Association of African Development Finance Institutions (AADFI) based in Cote D’Ivoire. Zac, before joining Exim, worked with Ashanti Goldfields Company Ltd, now Anglogold Ashanti.

Zac currently is a member of the World Bank Taskforce on: Design, Implementation and Evaluation of Public Credit Guarantees for SMEs in Emerging Markets and Developing Economies. He is also a Member of the Presidential Taskforce for the establishment of Ghana Exim Bank.

EXIMGUARANTY COMPANY (GHANA) LIMITED

10

BOARD CHAIRMAN’S ADDRESS Distinguished Shareholders and Board Members of Exim, permit me to warmly welcome you all to this very important business – our 2016 Annual General Meeting.

In 2015, our Company, like several other businesses in Ghana, had to deal with very challenging socio-economic headwinds which adversely affected business operations. However, with our strong systems in place and a firm commitment of leadership, we were able to grow our revenue and profit compared to our 2014 outturn.

GLOBAL ECONOMIC PERSPECTIVESReports from the World Bank January 2016 Global Economic Prospects indicate once again a disappointing performance in global growth. Global growth slowed down to 2.4% in 2015 and is expected to recover at a slower pace. Growth is projected to reach 2.9% in 2016 as advanced economies continue to recover modestly and economic activity stabilizes among major commodity exporters. The normalization of US monetary policy is also expected to tighten global financial conditions.

Sub- Saharan African economies are facing a challenging near-term outlook as commodity prices are expected to stabilize but remain low through 2017. Although governments in Sub- Saharan Africa are taking steps to resolve power issues, erratic electricity supply is expected to persist. These factors point to a weaker recovery in 2016. After slowing to 3.4% in 2015, activity is expected to pick up to 4.2% in 2016 and 4.7% in 2017-18 in emerging and developing economies. (World Economic Outlook, October 2015)

Ghana’s GDP growth for 2015 was estimated at 3.9% and projected to hit 4% in 2016. In real numbers our GDP for 2015 declined by 4% from GHC 38.5 billion in 2014 to GHC 37 billion in 2015. Interest rate keeps soaring with end of year monetary policy rate being 26% and inflation at17.7% in 2015. Our per capital income also reduced from USD 1, 426 in 2014 to USD 1, 339 in 2015.

Ghana’s banking sector for the first time in decades also suffered a reduction in total revenue growth from 34.9% in 2014 to negative 5.4% in December 2015. Similarly, the Industry’s net profit after tax also contracted by 10.5% in December 2015 according to the Bank of Ghana.

OPERATIONAL AND FINANCIAL HIGHLIGHTSLadies and Gentlemen, the myriad of challenges that confronted SMEs and Financing Institutions like ours in 2015 had a direct impact on our performance. Total value of guarantees issued in 2015 declined by 59% and total guarantee fees amounting to GHC 1,448,264 represents a decline of almost 4%.

Our overall revenue inched up by 10% from GHC 6,203,527 in 2014 to GHC 6,828,648.

Our performance in respect of guarantees issued, fees and revenue could have been better but for Ghana Cocobod’s decision not to accept guarantees from Non -Bank Financial Institutions.

Total investment income grew by 14% from GHC 3,547,535 in 2014 to GHC 4,047,244

Total net assets was GHC 16,319,794, a 15.48% drop from GHC 19,310,355 recorded in the previous year.

Profit after tax was GHC 150,732, representing a 384% increase over 2014 performance.

KEY BOARD DECISIONS

The commitment and insightful contributions of the Board, Ladies and Gentlemen, impacted strongly in the adoption of effective policies, systems and strategies that strengthened our overall operational performance and corporate governance.

BOARD CHAIRMAN’S ADDRESS

EXIMGUARANTY COMPANY (GHANA) LIMITED

11

In line with our Mandate, the Board in 2015 reviewed and approved the following:

• The Eximguaranty/FinGap Agreement

• Revised Corporate Policies for Departments and Units

• Consideration of a new Product for SMEs- Letter of Intent

• Directive to Management to reduce Office space in Takoradi Agency Office

Ladies and Gentlemen, the Board continues to maintain an oversight role in the following key areas:

• Obtaining assurances that the Company’s risk is reasonable and that the risk portfolio is well covered and managed.

• Establishing an efficient enterprise risk management system and

• Monitoring corporate performance against targets

The Board has also instituted the “ Chairman’s Day” programme as a refresher for Directors to discuss emerging corporate governance issues.

STRATEGYIn the light of our unique mandate to provide financing guarantees to SMEs in Ghana, Exim continues to deepen its engagement with key stakeholders particularly those in the financial services industry, EDAIF, USAID/FinGAP, and Contract Awarding agencies. We believe that our continuous engagement will enable us to not only serve our Clients better but also maintain our leadership position in the market.

On the external front, we also took steps to activate key protocols, with our external partners. We did this with the clear objective of strengthening our relationship with GARI and AADFI to best support our SME clients.

Continuous improvement of Staff knowledge and competence in the areas of product innovation, risks and credit guarantee business will receive the needed attention to drive our strategic orientation and performance in the future.

OUTLOOK FOR 2016Economic forecasts for this year appear positive. Ghana’s GDP is projected to inch past 4% with much better fiscal discipline under the IMF programme. Government’s investment in the power sector is beginning to pay off and most SMEs are now able to plan and execute their business agenda. The Cedi is relatively stable against the US Dollar.

Cost of doing business is still high with Bank of Ghana’s monetary policy rate at 26%; interest rate at over 30% and inflation now over 18%.

Despite all of this, we are hopeful of a better outlook this year. The Government of Ghana’s plan of maintaining tight fiscal discipline, despite being an election year, coupled with AGI’s renewed confidence in the economy as well as the IMF’s current positive rating of the economy after latest review of its extended credit facility with Ghana makes us hopeful.

ESTABLISHMENT OF GHANA EXIM BANKLadies and Gentlemen, the Government of Ghana’s plan of setting up a Ghana Exim Bank to help address the challenge of long term credit for exporters and also accelerate Ghana’s drive towards achieving a more diversified economy has become a reality with the passing of the Ghana Export-Import Bank Act, 2016 ( Act 911) by Parliament.

The integration process of our Company with EDAIF and Export Finance Company into the new Ghana Exim Bank has begun in earnest. A Technical/Transition Committee is already working on integration modalities for smooth implementation and we are reliably informed the Exim Bank Board has been constituted and we await the announcement soon.

Currently, as a Board, we are also doing our best to meet all the legal requirements expected to facilitate this integration process.

ACKNOWLEDGEMENTOn behalf of my fellow Board Members, I wish to thank our distinguished Shareholders for the support and confidence reposed in us in protecting the Guarantee Fund.

To all our business partners and key Stakeholders who continue to support us in various ways to grow our business, we say a BIG thank you as we forge ahead.

I also wish to express my heartfelt appreciation to the Management and Staff of Exim for their loyalty and dedication to duty.

Thank you.

EXIMGUARANTY COMPANY (GHANA) LIMITED

12

Dear Shareholders, I take this opportunity to welcome you to today’s Annual General Meeting. The year under review (2015) was quite challenging for most businesses in Ghana, particularly for both financing institutions and SMEs. Despite this, your Company maintained its dominance as the preferred Credit Guarantee Company in the Ghanaian market.

We took steps to deepen our relationship with key international partners like Guarantee Fund for Private Investments in West Africa( GARI) and Association of African Development Finance Institutions (AADFI )and through that strengthened our corporate image and brand positioning in the 2015 AADFI - PSGRS rankings for Africa. Out of the 46 development finance Institutions that participated in Africa, Exim Ghana was placed joint 10th scoring A+.

Our business in 2015 was adversely affected by the decision of the Ghana Cocoa Board not to accept our Guarantees due to the size of the Fund. Consequently, the total value of Guarantees issued in 2015 declined significantly by 59% to GHC 28,051,762 from previous year’s GHC 47, 479,138. We have stepped up efforts to address this major challenge by diversifying our products portfolio while we continue to engage COCOBOD on the way forward.

ECONOMYThe Ghanaian economy in 2015 experienced some major challenges that impacted negatively on most businesses and ours was not excluded. The energy crisis affected overall productivity. GDP declined by 4% to GHC 37 billion from GHC 38.5 billion in 2014. Annual inflation also rose to 17.7% from 17% in 2014 (Source: Ghana Statistical Service).

GDP growth for 2015 is estimated at 3.9%. The services sector contributed about 54.4% to overall GDP with industry doing 25.3%. General cost of doing business continues to soar higher as Bank of Ghana’s monetary policy rate ended the year at 26%. Average lending rate for most businesses was about 32% or more. The 91-day and 182-day Treasury bill rate as at December 2015 was 22.6% and 24.4% respectively.

Developments on the foreign exchange market during the 2015 year, indicated that the Cedi depreciated by about 18% against the US Dollar.

FINANCIAL PERFORMANCEThe decision of Ghana Cocobod not to accept guarantees from Non Bank Financial Institutions, including Exim, impacted negatively on our results particularly in the road construction sector. Total gurantees issued dropped by 59%. However, this was compensated for by a 10% growth in total revenue of GHC 6,828,648 as against GHC 6,203,527 in 2014.

Total Guarantee fees declined marginally by 3.85% from the 2014 figure of GHC 1,506,347 to GHC 1,448,264.

Total investment income for 2015 was GHC 4,047,244, an appreciable growth of 14% on 2014 figure of GHC 3,547,535.

Operating profit before tax went up significantly by 333% to GHC 240,901 when compared to 2014 recorded figure of GHC 72,355.

Total profit after tax for 2015 was GHC 150,732, another significant growth of 384% over 2014 out turn of GHC 39,233.

Total net assets declined by 15.48% from GHC 19,310,355 to GHC 16,319,794 as a result of net claims on the Guarantee Fund.

AGENCY OFFICESGeneral business activities in our Agency Offices in Takoradi and Kumasi have been relatively low, a true reflection of the economic slowdown in the Country. It is also worthy to mentioning that majority of our Financing partners and SME decision makers are in Accra and so naturally most business referrals are executed in Accra. Our Operations and Marketing Officers have intensified efforts including media campaigns to generate more businesses for our agency offices. Plans are also far advanced to pilot the introduction of our new SME driven product –“Letter of Intent” at both the Kumasi and Takoradi Offices to drive business activity there.

MANAGING DIRECTOR’S ADDRESS

EXIMGUARANTY COMPANY (GHANA) LIMITED

13

PRODUCTS AND SERVICESExim continues to work with Financing Institutions and Contract Awarding Agencies to offer needed guarantee covers to facilitate SME’s growth and development in the productive sectors of the economy.

In 2015, 47% of our total guarantees issued were from ‘Advanced Mobilisation/Payment Guarantee. This was followed by Credit Guarantees and Bid Security products.

During the year, in order to stay competitive in the Industry, we undertook a Customer Satisfaction Survey and used the findings to improve our processes, turnaround time and overall services delivery. We will continue to invest in research and customer services to strengthen our overall market share and revenue.

CORPORATE SOCIAL RESPONSIBILITYAs a responsible corporate citizen, our passion to touch lives and improve the well being of the communities in which we do business underpin the focus of our Corporate Social Responsibility. We activated most of our Corporate Social Responsibility projects through either sponsorships or partnering with other credible organizations to affect lives and businesses.

During the period, we sponsored the Miss Ghana Foundation, organisers of the 2015 Miss Ghana Blood donation exercise, to promote blood donation attitude among Ghanaians and to also restock the Korle Bu Blood bank. We also responded to an appeal made by the Village of Hope Orphanage to pay the medical bill of a young girl diagnosed of Cancer at the Korle Bu Teaching Hospital.

As a Company interested in promoting Agribusiness, we donated both cash and agric products to support the National Farmers Day event organized by the Ministry of Food and Agriculture.

In partnership with the Organiser’s of the Ghana Banking Awards, we also sponsored the Award of Best Bank in Agribusiness.

STAFF DEVELOPMENTYour Company continues to invest in developing the capacity of its Staff to reposition our brand leadership on the market and manage our risks portfolio more efficiently and prudently. In pursuance to this objective, some staff members were sponsored by the Company to upgrade their skills in various specialists courses on short term basis during 2015.

2016 OUTLOOKThis year’s outlook appears bullish with government’s investment in the energy sector yielding positive results for businesses. The unfortunate nightmare ritual of power rationing usually called ‘Dumsor’ is beginning to give way for SMEs to utilize their full capacities for business development. General business confidence in the economy is improving as projected GDP is expected to grow to almost 4%. The Government of Ghana’s decision to reduce the budget deficit to less than 10% should free up some space for the private sector to grow.

Being an election year, we expect a disciplined approach to spending in Infrastructual development to drive the economy and as a business concern, Exim will take full advantage through various initiatives to improve our bottom line.

With Government’s desire to work to bring down inflation and reduce the cost of doing business, we anticipate an improved performance in 2016.

Mr. Chairman, we are very much aware of the Government’s decision to set up an Exim Bank to accelerate the development of an export led economy. The Ghana Exim Bank bill has been passed by Parliament and plans are far advanced to merge our Company with EDAIF and Export Finance Company to form the new Exim Bank. A technical/ transition Committee has been established to work on the modalities for the smooth implementation of this strategic policy of Government.

ACKNOWLEDGEMENT I must thank the Board, Management and Staff for their support and commitment they showed in deepening the focus of our business despite a challenging 2015.

I wish to also express our appreciation to all our Stakeholders particularly financing institutions, contract awarding agencies, the Ministry of Finance, our loyal Clients and the media for their support.

To our valued Shareholders, I wish to assure you of our collective resolve to not only grow our portfolio but also protect the Guarantee Fund in the interest of our economy.

Thank you.

EXIMGUARANTY COMPANY (GHANA) LIMITED

14

The Directors present their report and the financial statements of the Company for the year ended 31 December 2015.

DIRECTORS’ RESPONSIBILITY STATEMENTThe Directors are responsible for the preparation of financial statements that give a true and fair view of Eximguaranty Company (Ghana) Limited, comprising the statement of financial position at 31 December 2015 and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and notes to the financial statements which include a summary of significant accounting policies and other explanatory notes, in accordance with International Financial Reporting Standards and in the manner required by the Companies Act, 1963 (Act 179) and the Non-Bank Financial Institutions Act, 2008 (Act 774). In addition, the Directors are responsible for the preparation of the Directors’ report.

The Directors are also responsible for such internal control as the Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error, and for maintaining adequate accounting records and an effective system of risk management.

The Directors have made an assessment of the ability of the Company to continue as a going concern and have no reason to believe that the business will not be a going concern in the year ahead.

The auditor is responsible for reporting on whether the financial statements give a true and fair view in accordance with the applicable financial reporting framework.

NATURE OF BUSINESSThe principal activities of the Company is to provide credit guarantee cover to financial institutions and other credit awarding agencies to assist them in extending credit facilities to borrowers who may have inadequate or no collateral. The Company is licensed by the Bank of Ghana as a non-bank financial institution under the Non-Bank Financial Institutions Act, 2008, (Act 774). There was no change in the nature of business of the Company during the year.

FINANCIAL STATEMENTS AND DIVIDENDThe results for the year are as set out in the attached financials, highlights of which are as follows:

2015GH¢

2014GH¢

Profit for the year (attributable to equity holders) 150,732 35,539

to which is added the balance brought forward

on retained earnings of 130,574 691,587

281,306 727,126

out of which is transferred to the mandatory reserve fund, in accordance with the Non-Bank Financial Institutions Act an amount of

(75,366) (17,770)

and transfers from/(to) credit risk reserve of 114,949 (495,399)

giving a total of 320,889 213,957

less: Interest on preference shares (30,000) (30,000)

Resulting in a balance of 290,889 183,957

less: prior year’s dividend paid - (53,383)

290,889 130,574

less: transfer to Guarantee Fund (58,178) -

leaves a balance to be carried forward on retained earnings of 232,711 130,574

No dividend was declared in the current year (2014: Nil).

The Directors confirm that to the best of their knowledge:

• the financial statements, prepared in accordance with applicable laws and the Company’s financial reporting framework, give a true and fair view of the Company’s financial position, performance and cash flows; and

• the state of the Company’s affairs is satisfactory.

APPROVAL OF THE FINANCIAL STATEMENTSThe financial statements of Eximguaranty Company (Ghana) Limited, as identified in the first paragraph, were approved by the Board of Directors on 18th May 2016 and signed on their behalf by

……………………...……………. ...…….…………………………...

DIRECTOR DIRECTOR

REPORT OF THE DIRECTORS TO THE MEMBERS OFEXIMGUARANTY COMPANY (GHANA) LIMITED

EXIMGUARANTY COMPANY (GHANA) LIMITED

15

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OFEXIMGUARANTY COMPANY (GHANA) LIMITED We have audited the financial statements of Eximguaranty Company (Ghana) Limited, which comprise the statement of financial position at 31 December 2015, and the statements of comprehensive income, changes in equity and cash flows for the year then ended, and the notes to the financial statements which include a summary of significant accounting policies and other explanatory notes, as set out on pages 16 to 37.

DIRECTORS’ RESPONSIBILITY FOR THE FINANCIAL STATEMENTSThe Directors are responsible for the preparation of financial statements that give a true and fair view in accordance with International Financial Reporting Standards and in the manner required by the Companies Act, 1963 (Act 179) and the Non-Bank Financial Institutions Act, 2008 (Act 774), and for such internal control as the Directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

AUDITOR’S RESPONSIBILITYOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation of financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OPINIONIn our opinion, these financial statements give a true and fair view of the financial position of Eximguaranty Company (Ghana) Limited at 31 December 2015 and of its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards and in the manner required by the Companies Act, 1963 (Act 179) and the Non-Bank Financial Institutions Act, 2008 (Act 774).

REPORT ON OTHER LEGAL AND REGULATORY REQUIREMENTSCompliance with the requirements of Section 133 of the Companies Act, 1963 (Act 179)

We have obtained all the information and explanations which, to the best of our knowledge and belief were necessary for the purpose of our audit.

In our opinion, proper books of account have been kept, and the statements of financial position and comprehensive income are in agreement with the books of account.

18th May 2016

SIGNED BY: FREDERICK NYAN DENNIS (ICAG/P/1426)FOR AND ON BEHALF OF:KPMG: (ICAG/F/2016/038)CHARTERED ACCOUNTANTS13 YIYIWA DRIVE, ABELENKPEP O BOX GP 242ACCRA

EXIMGUARANTY COMPANY (GHANA) LIMITED

16

EXIMGUARANTY COMPANY (GHANA) LIMITEDSTATEMENT OF FINANCIAL POSITION AT 31 DECEMBER 2015

2015GH¢

2014GH¢

Note

ASSETS

Property, plant and equipment 14 781,133 822,417

Non-current assets 781,133 822,417

Short term investments 12 16,276,010 16,687,219

Accounts receivable 13 487,249 643,352

Cash and cash equivalents 11 337,668 1,007,468

Current assets 17,100,927 18,338,039

Total assets 17,882,060 19,160,456

EQUITY

Stated capital 17 3,062,900 3,062,900

Preference shares 18 3,000,000 3,000,000

Mandatory reserve fund 19 1,511,108 1,435,742

Retained earnings 22 232,711 130,574

Credit risk reserve 23 583,294 698,243

Total equity 8,390,013 8,327,459

LIABILITIES

Deferred income 21 575,560 943,084

Guarantee fund 20 8,036,879 8,879,944

Deferred tax liability 10 51,517 43,905

Non-current liabilities 8,663,956 9,866,933

Income tax liability 9(c,d) 520,444 745,173

Accounts payable 15 233,980 177,224

Interest payable on preference shares 16 73,667 43,667

Current liabilities 828,091 966,064

Total liabilities 9,492,047 10,832,997

Total liabilities and equity 17,882,060 19,160,456

…………………………… ……………………………

DIRECTOR DIRECTOR

The notes on pages 20 to 37 are an integral part of this Annual report.

EXIMGUARANTY COMPANY (GHANA) LIMITED

17

IEXIMGUARANTY COMPANY (GHANA) LIMITED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER 2015

Note2015GH¢

2014GH¢

Guarantee and agency fees 5 1,448,264 1,506,347

Investment income 6 4,047,244 3,547,535

Other Income 7 43,671 44,915

Release from guarantee fund 20 1,289,469 980,495

Total revenue 6,828,648 6,079,292

Administrative expenses 8 5,298,278 5,026,442

Claims incurred 20 1,289,469 980,495

Total expenses 6,587,747 6,006,937

Operating profit before taxation 240,901 72,355

Income tax expense 9(a) (90,169) (36,816)

Profit for the year and total comprehensive

income 150,732 35,539

The notes on pages 20 to 37 are an integral part of this Annual report.

EXIMGUARANTY COMPANY (GHANA) LIMITED

18

Statedcapital

GH¢

Preferenceshares

GH¢

Mandatoryreserve

GH¢

Retained earnings

GH¢

Credit riskreserve

GH¢TotalGH¢

Balance at 1 January 2015 3,062,900 3,000,000 1,435,742 130,574 698,243 8,327,459

Total comprehensive income for the year

Profit for the year - - - 150,732 - 150,732

Total comprehensive income for the year - - - 150,732 - 150,732

Transactions with equity holders

Interest on preference shares - - - (30,000) - (30,000)

Total transactions with equity holders - - - (30,000) - (30,000)

Regulatory and other reserves

Transfer to mandatory reserve fund - - 75,366 (75,366) - -

Transfer from credit risk reserve - - - 114,949 (114,949) -

Total net movements in reserves - - 75,366 39,583 (114,949) -

Transfer to guarantee fund (58,178) (58,178)

Balance at 31 December 2015 3,062,900 3,000,000 1,511,108 232,711 583,294 8,390,013

Statedcapital

GH¢

Preferenceshares

GH¢

Mandatoryreserve

GH¢

Retained earnings

GH¢

Credit riskreserve

GH¢TotalGH¢

Balance at 1 January 2014 3,062,900 3,000,000 1,417,972 206,633 202,844 7,890,349

Adjustment - - - 484,954 - 484,954

3,062,900 3,000,000 1,417,972 691,587 202,844 8,375,303

Total comprehensive income for the year

Profit for the year - - - 35,539 - 35,539

Total comprehensive income for the year - - - 35,539 - 35,539

Transactions with equity holders

Dividend on ordinary dividend - - - (53,383) - (53,383)

Interest on preference shares - - - (30,000) - (30,000)

Total transactions with equity holders - - - (83,383) - (83,383)

Regulatory and other reserves

Transfer to credit risk reserve - - - (495,399) 495,399 -

Transfer to mandatory reserve fund - - 17,770 (17,770) - -

Net transfer to reserves - - 17,770 (513,169) 495,399 -

Balance at 31 December 2014 3,062,900 3,000,000 1,435,742 130,574 698,243 8,327,459

The notes on pages 20 to 37 are an integral part of this Annual report.

EXIMGUARANTY COMPANY (GHANA) LIMITEDSTATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2015

EXIMGUARANTY COMPANY (GHANA) LIMITED

19

EXIMGUARANTY COMPANY (GHANA) LIMITEDSTATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 2015

Note2015GH¢

2014GH¢

Net cashflow from operating activities

Profit after taxation 150,732 35,539

Adjustments:

Depreciation 14 265,804 219,678

Profit on sale of property and equipment 14 (5,086) (2,036)

Tax expense 9(a) 90,169 36,816

Interest income 6 (4,047,244) (3,547,535)

Unrealised exchange difference on cash (1,542) (8,737)

(3,547,167) (3,266,275)

Changes in:

Accounts receivables 156,103 760,979

Accounts payables 56,756 (356,702)

Deferred income (367,524) 266,023

Cash used in operations (3,701,832) (2,595,975)

Tax paid 9(c) (307,286) (35,355)

Claims paid 20 (1,289,469) (980,495)

Claims recovered 20 388,226 231,709

Net cash flow used in operating activities (4,910,361) (3,380,116)

Cashflows from investing activities

Purchase of property, plant & equipment 14 (224,521) (288,854)

Proceeds from sale of property and equipment 14 5,086 18,060

Interest received 3,861,987 3,550,875

Increase in medium term investments (966,527) 2,199,083

Net cashflow from investing activities 2,676,025 5,479,164

Cashflows used in financing activities

Dividend paid 22 - (83,383)

Net cashflow used in financing activities - (83,383)

Net decrease/(increase) in cash and cash equivalents (2,234,336) 2,015,665

Cash and cash equivalents at 1 January 8,110,285 6,085,883

Effect of exchange rate fluctuations on cash held 1,542 8,737

Cash and cash equivalents at 31 December 5,877,491 8,110,285

The notes on pages 20 to 37 are an integral part of this Annual report.

EXIMGUARANTY COMPANY (GHANA) LIMITED

20

1. REPORTING ENTITYEximguaranty Company (Ghana) Limited is domiciled in Ghana. The Company’s registered office is at No. 27 Noi Fetreke, Roman Ridge, Ambassadorial Estate Extensions Accra.

The Company is involved in the provision of credit guarantee cover to financial institutions and other credit awarding agencies to assist them in extending credit facilities to borrowers who may have inadequate or no collateral. The financial statements at and for the year ended 31 December 2015 comprise the individual financial statements of the Company.

2. BASIS OF PREPARATION

(a) Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRSs) and in a manner required by the Companies Act 1963, (Act 179), and the Non-Bank Financial Institutions Act, 2008 (Act 774).

(b) Basis of measurement

The financial statements are prepared on the historical cost basis.

(c) Functional and presentation currency

The financial statements are presented in Ghana Cedis (GH¢) which is the Company’s functional and presentation currency. All financial information presented in Ghana Cedis have been rounded to the nearest Cedi, except where otherwise indicated.

(d) Use of estimates and judgment

The preparation of financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. Estimates and underlying assumptions are based on historical experience and other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods.

In particular, information about significant areas of estimation, uncertainty and critical judgments in applying accounting policies that have the most significant effect on amounts recognised in the financial statements is included in the following notes:

o Note 3(e) – determination of fair values

o Note 4 – financial instruments – fair values and risk management.

3. SIGNIFICANT ACCOUNTING POLICIESThe accounting policies set out below have been applied consistently to all periods presented in these financial statements.

(a) Foreign currency

(i) Foreign currency transactions

Transactions denominated in foreign currency are translated into the functional currency using exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

denominated in foreign currencies are recognised in the income statement. Non-monetary assets and liabilities are translated at historical exchange rates if held at historical cost, or at exchange rates ruling at the date that fair value was determined if held at fair value, with the resulting exchange gain or loss recognised in the income statement or shareholders’ equity as appropriate. Foreign currency differences arising on retranslation are generally recognized in profit or loss in other income or administrative expenses depending on whether foreign currency movements are in a net gain or loss position.

(b) Property, plant and equipment

(i) Recognition and measurement

Items of property, plant and equipment (PPE) are measured at acquisition or construction cost less accumulated depreciation and any accumulated impairment losses.

Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labour, and any other costs directly attributable to bringing the asset to a working condition for its intended use. Purchased software that is integral to the functionality of the related equipment is capitalised as part of that equipment.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components).

(ii) Subsequent expenditure

The cost of replacing part of an item of property, plant or equipment is recognised in the carrying amount of the item if it is probable that future economic benefits embodied within the part will flow to the Company and its cost can be measured reliably. The costs of the day-to-day maintenance, repair and servicing expenditures incurred on property, plant and equipment are recognised in income statement.

(iii)Depreciation

Depreciation is recognised in the income statement on a straight-line basis over the estimated useful lives of each part of an item of property, plant and equipment. Leased assets are depreciated over the shorter of the lease term and their useful lives.

(iii) Depreciation (cont’d)

The estimated useful lives of major classes of depreciable property, plant and equipment are:

Office Building - 50 years

Plant and Machinery - 10 years

Motor Vehicles - 4 years

Office Equipment - 4 years

Furniture and Fittings - 4 years

Depreciation methods, useful lives and carrying amount are reassessed at each reporting date. The carrying amounts of property, plant and equipment are assessed whether they are recoverable in the form of future economic benefits. If the recoverable amount of a PPE has declined below its carrying amount, an impairment loss is recognised to reduce the value of the asset to its recoverable amount. In determining the recoverable amount of the asset, expected cash flows are discounted to their present value.

Gains and losses on disposal of property, plant and equipment are determined by comparing proceeds from disposal with the carrying amounts of property, plant and equipment and are recognised in the income statement as other income.

EXIMGUARANTY COMPANY (GHANA) LIMITED

21

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

(iv) Derecognition

Property, plant and equipment are derecognised upon disposal or when no future economic benefits are expected to flow to the Company from either their use or disposal.

(c) Intangible assets

Software

Software acquired by the Company is stated at cost less accumulated amortisation and accumulated impairment losses.

Subsequent expenditure on software assets is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is expensed as incurred.

Amortisation is recognised in the income statement on a straight-line basis over the estimated useful life of the software from the date that it is available for use.

Intangible assets are derecognised upon disposal or when no future economic benefits are expected to flow to the Company from either their use or disposal. Gains or losses on derecognition of an intangible asset are determined by comparing the proceeds from disposal, if applicable, with the carrying amount of the intangible asset and are recognised directly in profit or loss.

(d) Financial instruments

(i)Non-derivative financial instruments

Non-derivative financial instruments comprise account receivables, cash and cash equivalents, short term investments and account payables.

Recognition and derecognition of a non-derivative financial instrument

The Company classifies its financial liabilities other than financial guarantees and loan commitments as financial liabilities measured at amortised cost.

(i) Non-derivative financial instruments - (cont’d)

The Company initially recognises loans and receivables on the date when they are originated. Financial assets are derecognised when the contractual rights to the cash flows from the assets expire, or it transfers the right to receive the contractual cash flows in a transaction in which substantially all of the risks and rewards of ownership are transferred or it neither transfers nor retains substantially all of the risks and rewards of ownership and does not retain control over the transferred asset. Any interest in such derecognised financial assets that is created or retained by the Company is recognised as a separate asset or liability.

Financial liabilities are initially recognised on the trade date when the entity becomes a party to the contractual provisions of the instrument. The Company derecognises a financial liability when its contractual obligations are discharged or cancelled or expire.

Non-derivative financial instruments are categorised as follows:

• Loans and receivables – these are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. Loans and receivables are subsequently recognised at amortised cost using effective interest method less appropriate allowances for doubtful receivables. Allowances for doubtful receivables represents the Company’s estimate of incurred losses arising from the failure or inability of customers to make payments when due. These estimates are based on aging of customer’s balances, specific credit circumstances and the Company’s receivables historical experience. Loans and receivables comprise cash and cash equivalents and account receivables.

Cash and cash equivalents - Cash and cash equivalents comprise cash balances and call deposits with maturities of three months or less from the acquisition date that are subject to an insignificant risk of changes in fair value and are used by the Company in the management of its short-term commitments.

• Held-to-maturity – these are non-derivative assets with fixed or determinable payments and fixed maturity that the Company has the positive intent and ability to hold to maturity and which are not designated at fair value through profit or loss or available-for-sale. Held to maturity assets are initially measured at fair value plus incremental direct transaction costs and subsequently measured at amortized cost using the effective interest method. Any sale or reclassification of a significant amount of held to maturity asset not close to their maturity would result in the reclassification of all held to maturity assets as available-for-sale, and would prevent the Company from classifying investment securities as held-to-maturity for the current and the following two financial years. Differences between the carrying amount (amortized cost) and the fair value on the date of the reclassification are recognized in other comprehensive income.

The Company classifies short term investments as held-to-maturity.

• Financial liabilities measured at amortised cost - this relates to all other liabilities that are not designated at fair value through profit or loss. The Company classifies non-derivative financial liabilities into the other liabilities category.

Other financial liabilities comprise account payables.

(ii) Share capital

Ordinary shares

Proceeds from the issue of ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares are recognised as a deduction from equity, net of any tax effects.

(e) Determination of fair values

Some of the Company’s accounting policies and disclosures require the determination of fair value, for both financial and non-financial assets and liabilities. The Company regularly reviews significant unobservable inputs and valuation adjustments. When measuring the fair value of an asset or liability, the Company uses market observable data as far as possible.

Fair values are categorised into different levels in the fair value hierarchy based on the inputs used in the valuation techniques as follows:

o Level 1: quoted prices (unadjusted) in active markets for identical assets or liabilities.

o Level 2: inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices).

o Level 3: inputs for the asset and liability that are not based on observable market data (unobservable inputs).

If inputs used to measure the fair value of an asset or a liability might be categorised in different levels of the fair value hierarchy, then the fair value measurement is categorised in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement.

Further information about the assumptions made in determining fair values is included in Note 4, financial instruments – fair value and risk management.

EXIMGUARANTY COMPANY (GHANA) LIMITED

22

(f) Impairment

(i) Financial assets

A financial asset is considered impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset.

An impairment loss in respect of a financial asset measured at amortised cost is calculated as the difference between its carrying amount and the present value of the estimated future cash flows discounted at the original effective interest rate.

Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in groups that share similar credit risk characteristics.

All impairment losses are recognised in the income statement. An impairment loss is reversed if the reversal can be related objectively to an event occurring after the impairment loss was recognised.

(ii) Non-financial assets

The carrying amounts of the Company’s non-financial assets other than deferred tax assets are reviewed at each reporting date to determine whether there is an indication of impairment. If any such indication exists then the asset’s recoverable amount is estimated.

(ii) Non-financial assets (cont’d)

The recoverable amount of an asset or cash generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflect current market assessments of the time value of money and the risk specific to the asset.

An impairment loss is recognised if the carrying amount of an asset or its cash generating unit exceeds its recoverable amount. Impairment losses are recognised in the income statement.

A previously recognised impairment loss is reversed where there has been a change in circumstances or in the basis of estimation used to determine the recoverable value, but only to the extent that the asset’s net carrying amount does not exceed the carrying amount of the asset, after provisions and depreciation, which would have been determined if no impairment loss had been recognised.

(g) Mandatory reserve fund

In accordance with the industry’s legal and regulatory frameworks, a mandatory reserve is established and maintained, to cover the risk of bankruptcy. This is measured at 50% of the net profits after tax, but before dividend and such amount shall accumulate until it reaches the minimum paid-up capital, after which time the applicable percentage reduces to a minimum of 15%.

(h) Interest income and expense

Interest income and expense are recognized in profit or loss using the effective interest method.

When calculating the effective interest rate, the Company estimates future cash flows considering all contractual terms of the financial instrument, but not future credit losses. The calculation includes all transaction costs, fees and points paid or received that are an integral part of the effective interest rate. Transaction costs include incremental costs that are directly attributable to the acquisition or issue of a financial asset or liability.

Once a financial asset or a group of similar financial assets have been written down as a result of an impairment loss, interest income is recognized using the rate of interest used to discount future cash flows for the purpose of measuring the impairment loss.

(i) Guarantee and agency fees

Guarantee and agency fees are generally recognised on an accrual basis when services have been rendered, it is probable that future economic benefits of the transaction will flow to the entity, the revenue can be measured reliably and the costs are identifiable and can be measured reliably.

If the guarantees issued under a single arrangement are rendered over different reporting periods, then the guarantee fees are deferred on a straight line basis between the different reporting periods.

(j) Employment benefits

(i) Defined contribution plans

A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions to a separate entity and will have no legal or constructive obligation to pay future amounts. Obligations for contributions to defined contribution schemes are recognised as an expense in the statement of comprehensive income in the periods during which services are rendered by employees.

(ii) Short-term employee benefits

Short-term employee benefit obligations are measured on an undiscounted basis and are expensed as the related service is provided. A provision is recognised for the amount expected to be paid under short-term cash bonus or profit-sharing plans if the Company has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee and the obligation can be estimated reliably.

(iii) Provident fund

The Company has a provident fund scheme for all employees who have completed their probation period with the Company.

Employees contribute 5.5% of their basic salary to the Fund whilst the Company contributes 13%. Obligations under the plan are limited to the relevant contributions, which are settled on due dates to the Fund Manager.

(k) Taxation

Income tax expense comprises current and deferred tax. The Company provides for income taxes at the current tax rates on the taxable profits of the Company.

Income tax is recognised in the income statement except to the extent that it relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable on taxable income for the year using tax rates enacted or substantially enacted at the reporting date, and any adjustment to tax payable in respect of previous years.

Deferred tax is provided using the balance sheet method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the corresponding amounts used for taxation purposes.

Deferred tax is measured at tax rates that are expected to be applied to temporary differences when they reverse, based on laws that have been enacted or substantively enacted by the reporting date.

A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available against which the asset can be utilised. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

EXIMGUARANTY COMPANY (GHANA) LIMITED

23

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

(l) Provisions

A provision is recognised when the Company has a present legal or constructive obligation as a result of a past event, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at pre-tax rates that reflect current market assessments of the time value of money and where appropriate, risks specific to the liability.

(m) Dividend

Dividend payable is recognised as a liability in the period in which they are declared. Dividend proposed which is yet to be approved by the shareholders, is disclosed by way of notes.

(n) Financial guarantee contracts

Financial guarantee contracts are contracts that require the Company to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due, in accordance with the terms of the debt instrument.

Financial guarantees are initially recognised at fair value and amortised over the useful life of the financial guarantee. The liability is subsequently carried at the higher of the amortised amount and the present value of any expected payments to settle the liability, when payment becomes probable.

(o) Grant in support of guarantee fund

Grants are received from Export Development and Agricultural Investment Fund (EDAIF) to augment the guarantee fund to further enhance activities in support of the export sector. This grant is accounted for as deferred income and are released to the income statement to offset claims incurred.

(p) Subsequent events

Events subsequent to the reporting date are reflected in the financial statements only to the extent that they relate to the year under consideration and the effect is material.

(q) Comparatives

Except when a standard or an international interpretation permits or requires otherwise, all amounts are reported or disclosed with comparative information. Where considered necessary, comparative figures have been adjusted to conform to changes in presentation in the current year.

(r) New standards and interpretations not yet adopted

There are new or revised Accounting Standards and Interpretations in issue that are not yet effective. These include the following Standards and Interpretations that are applicable to the business of the entity and may have an impact on future financial statements:

Standard/Interpretation Date issued by

LASB

Effective date Periods beginning

on or after

IFRS 9 Financial Instruments

July 2014 1 January 2018

IFRS 15 Revenue from contracts with customers

May 2014 1 January 2018

• IFRS 9 Financial Instruments

IFRS 9 published in July 2014, replaces the existing guidance in IAS 39 Financial Instruments: Recognition and Measurement. IFRS 9 includes revised guidance on the classification and

measurement of financial instruments, including a new expected credit loss model for calculating impairment on financial assets and the new general hedge accounting requirements. It also carries forward the guidance on recognition and derecognition of financial instruments from IAS 39.

IFRS 9 is effective for annual reporting periods beginning on or after 1 January 2018 with retrospective application, with early adoption permitted.

The Company is assessing the potential impact on its financial statements resulting from the application of IFRS 9. Given the nature of the Company’s operations, this standard is expected to have a significant impact on the Company’s financial statements. In particular, calculation of impairment of financial instruments on an expected credit loss basis is expected to result in an increase in the overall level of impairment allowances.

• IFRS 15 Revenue from Contracts with Customers

IFRS 15 establishes a comprehensive framework for determining whether, how much and when revenue is recognized. It replaces existing revenue recognition guidance, including IAS 18 Revenue, IAS 11 Construction Contracts and IFRIC 13 Customer Loyalty Programmes.

IFRS 15 is effective for annual reporting periods beginning on or after 1 January 2018, with early adoption permitted.

The Company is assessing the potential impact on its financial statements resulting from the application of IFRS 15, therefore the impact is currently unknown.

The following new or amended standards are not expected to have a significant impact on the Company’s financial statements.

• Defined Benefit Plans: Employee Contributions (Amendments to IAS 19).

• Annual Improvements to IFRSs 2010 – 2012 Cycle.

• Annual Improvements to IFRSs 2011 – 2013 Cycle.

• IFRS 14 Regulatory Deferral Accounts.

• Accounting for Acquisitions of Interests in Joint Operations (Amendments to IFRS 11).

• Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to IAS 16 and IAS 38).

• Agriculture: Bearer Plants (Amendments to IAS 16 and IAS 41).

• Equity Method in Separate Financial Statements (Amendments to IAS 27).

• Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments to IFRS 10 and IAS 28).

• Annual Improvements to IFRSs 2012 – 2014 Cycle – various standards.

4. FINANCIAL INSTRUMENTS – FAIR VALUES AND RISK

MANAGEMENT

(a) Accounting classification and fair values

The following table shows the carrying amounts and fair values of financial assets and financial liabilities, including their levels in the fair value hierarchy.

It does not include fair value information for financial assets and financial liabilities not measured at fair value if the carrying amount is a reasonable approximation of fair value.

EXIMGUARANTY COMPANY (GHANA) LIMITED

24

Loans & Receivables

GH¢

Held-to-maturity

GH¢

Other financial

liabilities GH¢

Total GH¢

December 2015

Financial assets not measured at fair value

Cash and cash equivalents 337,668 - - 337,668

Short term investments - 16,276,010 - 16,276,010

Accounts receivables 145,388 - - 145,388

483,056 16,276,010 - 16,759,066

Financial liabilities not measured at fair value

Accounts payable - - 182,083 182,083

December 2014

Financial assets not measured at fair value

Cash and cash equivalents 1,007,468 - - 1,007,468

Short term investments - 16,687,219 - 16,687,219

Accounts receivables 387,418 - - 387,418

1,394,886 16,687,219 - 18,082,105

Financial liabilities not measured at fair value

Accounts payable - - 161,284 161,284

(b) Financial risk management

(i) Overview

The Company has exposure to the following risks from its use of financial instruments:

o credit risk

o liquidity risk

o market risks

o operational risk

This note presents information about the Company’s exposure to each of the above risks, the Company’s objectives, policies and processes for measuring and managing risk, and the Company’s management of capital.

(ii) Risk management framework

The Board of Directors has the overall responsibility for the establishment and oversight of the Company’s risk management framework. The responsibilities of the Board of Directors include: setting out the Company’s overall risk appetite/tolerance limit, ensuring that the Company’s overall risk exposure is maintained at prudent levels and consistent with available capital. They also include; ensuring that executive management as well as individuals responsible for risk management possess sound expertise and knowledge to accomplish the risk management function and ensuring that appropriate policies and procedures for risk management are in place.

The Board of Directors, credit committee and the management team oversee implementation of the broad risk management policies and objectives of the Company.

The most important components of this financial risk are interest rate risk, equity risk, currency risk, credit risk and liquidity risk.

These risks arise from open positions in interest rates which are exposed to general and specific market movements. The risk that the Company primarily faces due to the nature of its investments and liabilities is interest rate risk.

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

EXIMGUARANTY COMPANY (GHANA) LIMITED

25

(iii) Credit risk

Credit risk stems from outright default due to inability or unwillingness of a client or counterpart to meet commitments in relation to guarantees issued. Resultant losses are written off in the statement of comprehensive income.

The credit committee is responsible for implementation of the guarantee risk policy and monitoring credit risk on transactional basis to ensure compliance with guarantee limits approved by the Board. The credit committee is a separate function from the operations department and this ensures credibility and discipline in the guarantee delivery value chain.

Managing problem guarantees

Monitoring and Recovery department manages delinquent facilities including outright recoveries or nursing of such problem guarantees back to health.

At delinquent stage and 360 days past due, where recovery efforts are unsuccessful, the Monitoring and Recovery Department refers the client to the Company’s contractual external solicitors.

Provisioning for guarantees

In conformity with Bank of Ghana‘s directives, the minimum provision that are held are as follows:

Guarantee risk rating minimum provision

Required - %

Advanced mobilization 1.0

Credit guarantee 1.0

Mobilisation guarantee 1.5

Advance payment guarantee 1.0

Guarantee risk rating minimum provision

Required - %

Bid bon 0.5

Bid security 0.5

Performance bond/performance security 1.0

Seed fund guarantee 1.0

Syndication guarantee 1.0

Exposure to credit risks

The carrying amount of financial assets represents the maximum credit risk exposure. The maximum exposure at the reporting date was:

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

EXIMGUARANTY COMPANY (GHANA) LIMITED

26

2015 GH¢

2014 GH¢

Accounts receivable 145,388 387,418

Short-term investments 16,276,010 16,687,219

Bank balances 326,767 1,004,431

16,748,165 18,079,068

Off-balance sheet items:

Unexpired guarantees outstanding 47,375,085 59,123,006

Concentration by location within Ghana

Accounts receivable 145,388 387,418

Short-term investments 16,276,010 16,687,219

Bank balances 326,767 1,004,431

16,748,165 18,079,068

Off Balance sheet items:

Unexpired guarantees outstanding 47,375,085 59,123,006

Concentration by location outside Ghana - -

iv) Liquidity Risk

Liquidity risk is the risk that the Company either does not have sufficient financial resources available to meet all its obligations and commitments as they fall due, or can access them only at excessive cost. The Company’s approach to managing liquidity is to ensure that it will maintain adequate liquidity to meet its liabilities when due.

The following are contractual maturities of financial liabilities:

Amount GH¢

6mths or less GH¢

12mthsGH¢

December 2015

Non-derivative financial liabilities

Accounts payable 182,083 182,083 -

December 2014

Non-derivative financial liabilities

Accounts payable 161,284 161,284 -

(v) Market risk

Market risk is the risk that changes in market prices, such as foreign exchange rates, interest rates and equity prices will affect the Company’s income or the value of its holding of financial instruments. The objective of market risk management is to manage and control market risk exposures within acceptable parameters, whilst optimizing the return.

(a) Currency risk

The Company is exposed to currency risk in terms of balances denominated in currencies other than the functional currency.

The Company’s exposure to foreign currency risk was as follows based on notional amounts.

2015 US$ Euro GB£

Assets

Cash and bank balances 15,139 135 27

Net exposure 15,139 135 27

2014

Assets

Cash and bank balances 1,758 135 27

Net exposure 1,758 135 27

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

EXIMGUARANTY COMPANY (GHANA) LIMITED

27

EXIMGUARANTY COMPANY (GHANA) LIMITEDNOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2015

(a) Currency risk (cont’d)

The following significant exchange rates applied during the year:

Average rate Reporting rate

2015 2014 2015 2014

US$ 1 3.76 3.04 3.80 3.20

Euro 1 4.16 4.03 4.13 3.90

GBP 1 5.75 5.00 5.62 4.98

(b) Sensitivity analysis on currency risks

The following table shows the effect of a strengthening or weakening of GH¢ against all other currencies on equity and profit or loss. This sensitivity analysis indicates the potential impact on equity and profit or loss based upon the foreign currency exposures recorded at 31 December. (See “currency risk” above) and it does not represent actual or future gains or losses. The sensitivity analysis is based on the percentage difference between the closing exchange rate and the average exchange rate per currency recorded in the course of the respective financial year.

A strengthening/weakening of the GH¢, by the rates shown in the table, against the following currencies at 31 December would have increased/decreased equity and profit or loss by the amounts shown below:

This analysis assumes that all other variables, in particular interest rates, remain constant.

2015 2014

At 31 December %

Change

Proft or loss/equity impact Strengthening

GH¢

Proft or loss/equity impact

Weakening GH¢

%

Change

Proft or loss/equity impact Strengthening

GH¢

Proft or loss/equity impact Weakening

GH¢

Euro ±10% 56 (56) ±10% 53 (53)

USD ±10% 5,748 (5,748) ±10% 563 (563)

GBP ±10% 15 (15) ±10% 13 (13)

(c) Interest rate risk

Changes in market interest rates have a direct effect on the contractually determined cash flows associated with floating rate instruments. Interest rate risk relates to the Company’s investments in floating or fixed rate deposits and treasury bills. At the reporting date, the interest rate profile of the Company‘s interest-bearing financial instruments was:

Carrying amounts

2015 2014

GH¢ GH¢

Fixed rate instruments

Fixed deposit 11,823,142 11,334,535

Treasury bills 4,452,868 5,352,684

16,276,010 16,687,219

EXIMGUARANTY COMPANY (GHANA) LIMITED

28

(c) Interest rate risk (cont’d)

The Company does not account for any fixed rate financial instruments at fair value through profit or loss therefore a change in interest rates at the reporting date would not affect profit or loss. No interest rate sensitivity analysis has thus been disclosed.

The Company does not have variable-rate instruments.

(vi) Operational risk

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. It is the risk of loss arising from the potential that inadequate information systems, breaches of internal controls, fraud, technological failure and unforeseen catastrophes may result in unexpected loss or reputational problems.

The Company has developed a thorough and consistent framework and policies to control and actively manage its operational risk.

(vii) Compliance and regulatory risk

In order to strengthen the Company’s compliance with regulatory requirements, the Company organizes series of dedicated training on a regular basis to equip staff with compliance and regulatory issues in order to minimize risk emanating there from.

(viii) Legal risk

The Company is not dependent on any patent or any industrial, commercial or financial contract. The Company’s activities are undertaken in a manner which adequately reduces the risks which may arise out of material litigation to be initiated against it (the Company).

(ix) Reputational risk

The Company conducts its business in a responsible, professional and transparent way. By offering simplified products and following the necessary legal and regulatory processes, the Company safeguards the interest of its clients as well as its reputation. Furthermore, the Company maintains close ties with the communities in which it operates by supporting them in various ways. This is aimed at demonstrating our commitment and fostering a long term relationship with our clients and the public at large.

(x) Capital management

(a) Capital definition

The Company’s capital, ordinarily referred to as shareholders fund comprises ordinary share capital raised through direct investment, retained earnings including current year profit and various reserves the Company is statutorily required to maintain. As a non-bank financial institution, the Company also has regulatory capital as defined below.

The primary objectives of the Company’s capital management are to ensure that the Company complies with the requirement of Bank of Ghana and healthy capital ratios in order to support its business and to maximise shareholders value.

(a) Capital definition (cont’d)