april 17, 2007d. brothwell, cpslo 1 revenue management program past, present and future financial...

Post on 19-Dec-2015

216 views

TRANSCRIPT

April 17, 2007 D. Brothwell, CPSLO 1

Revenue Management Program

Past, Present and FutureFinancial Officers Association

Annual Conference - April 2007

D. Brothwell, CPSLO 2April 17, 2007

The Past

D. Brothwell, CPSLO 3April 17, 2007

The way it used to be In general, the CSU has funded the

support of instruction from two sources 70% from state support30% from student fee revenue

The state funds $.70 on the dollar and students fund $.30 on the dollarCampuses collected the $.30 from the

students Campuses remitted the .$.30 to the state The state then allocated $1.00 back to the campus to spend ALL expenditures had to be processed thru the State Controller

D. Brothwell, CPSLO 4April 17, 2007

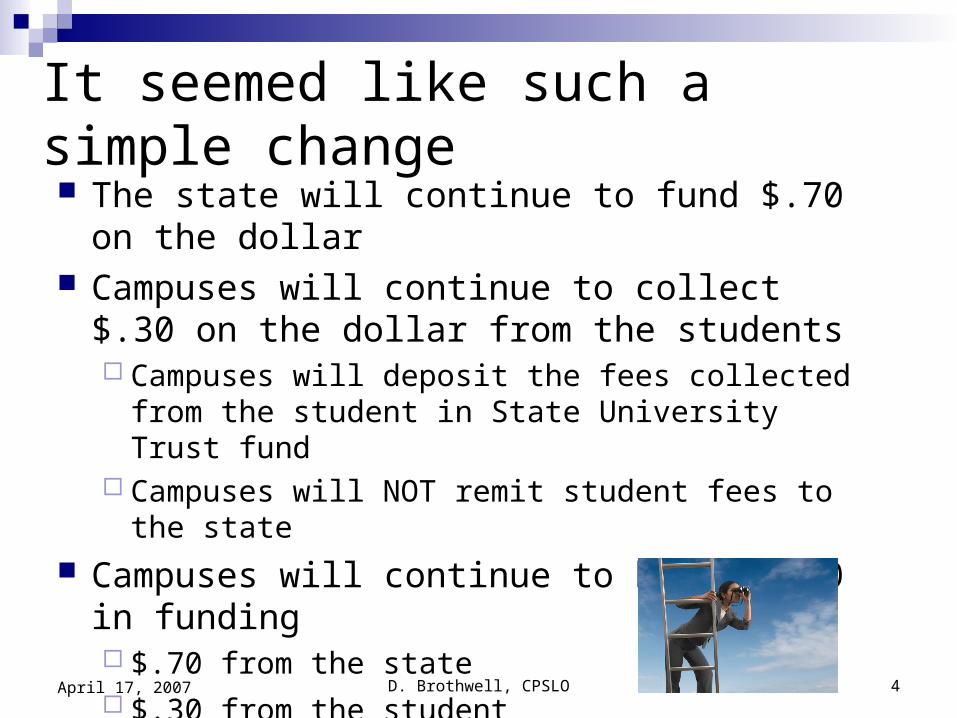

It seemed like such a simple change The state will continue to fund $.70 on the

dollar Campuses will continue to collect $.30 on the

dollar from the students Campuses will deposit the fees collected from the

student in State University Trust fund Campuses will NOT remit student fees to the state

Campuses will continue to have $1.00 in funding $.70 from the state $.30 from the student

D. Brothwell, CPSLO 5April 17, 2007

Original Vision of SB 1802

Improve Financial ManagementDemonstrate to rating agencies that the

CSU has control of its finances – deposit and investment of fee revenue

CSU Central Bank

Bring the state’s treatment of student fee revenue in line with other 4-yr Universities nationwide

D. Brothwell, CPSLO 6April 17, 2007

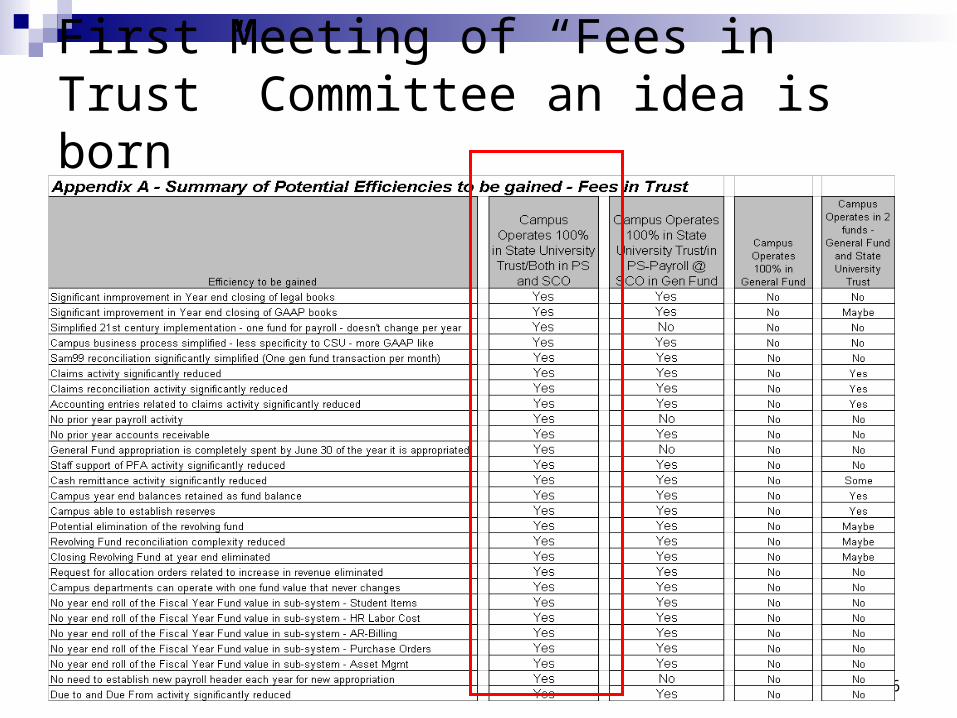

First Meeting of “Fees in Trust” Committee an idea is born

D. Brothwell, CPSLO 7April 17, 2007

Evolving ConceptInitial• Allow fees to be deposited into Trust• Operate from General Fund and Trust Fund Revised

• Allow fees to be deposited into Trust• Operate from one Fund

D. Brothwell, CPSLO 8April 17, 2007

Now we’re all on the same page

Deposit Student Fees in Trust Implement CSU Central Bank

Control of our finances Improve bond ratings

Operate within the State University Trust Fund

So we just have to do a few things

D. Brothwell, CPSLO 9April 17, 2007

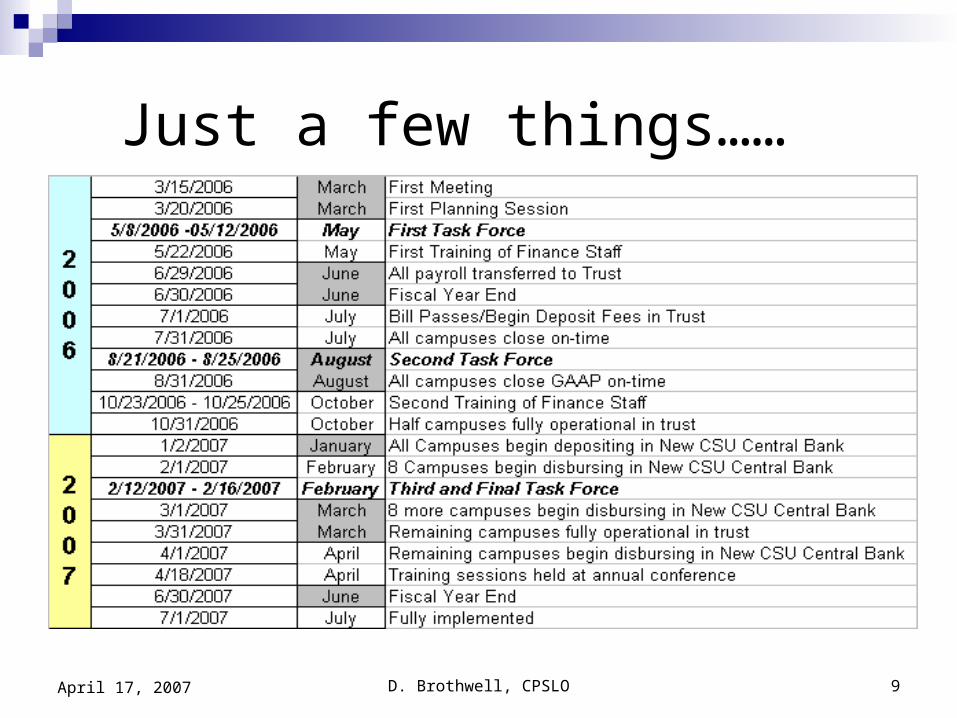

Just a few things……

D. Brothwell, CPSLO 10April 17, 2007

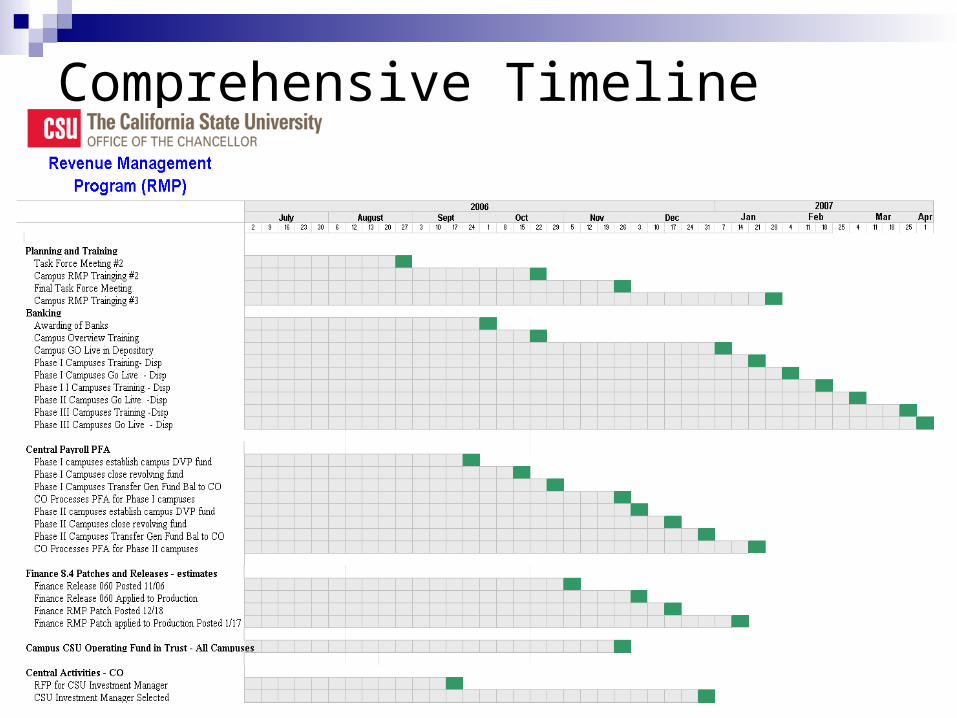

Comprehensive Timeline

D. Brothwell, CPSLO 11April 17, 2007

As of today – April 17, 2007

The RMP Task Force: Met for one week in May 2006 Met for one week in August 2006 Met for one week in February 2007

Approx 300 campus finance staff Attended one day training May 22, 2006 Attended 3 day training October 23 – 25, 2006

CSU contracted with Wells Fargo for all CSU Banking activity CSU has contracted with 2 investment managers

Wachovia US Bank

Custodian Bank CSU has a new approved Plan of Financial Adjustment – (March 28, 2007) Interim guidelines issued March 19, 2007 addressing topics in need of

immediate operating guidance

D. Brothwell, CPSLO 12April 17, 2007

As of today – April 17, 2007

All payroll is being processed within the State University Trust Fund

23 campuses have closed the general fund revolving fund Modified all PeopleSoft claims set up accordingly Modified all revolving fund business processes accordingly

23 campuses are fully operational within the CSU Central Bank – Wells Fargo Modified all PeopleSoft Banking set up accordingly Modified all banking business processes accordingly

23 campuses are fully operational within the State University Trust Fund

D. Brothwell, CPSLO 13April 17, 2007

In Summary

The Past was really busy We changed almost everything we do It’s been a little crazy Oh yea, and year end is just around the

corner

D. Brothwell, CPSLO 14April 17, 2007

The Present

D. Brothwell, CPSLO 15April 17, 2007

New Procedures and/or Processes

Revenue Payroll Accounting Banking Cash and Investments Budget CSU Fund 499 New FIRMS Object Codes New Acronyms

D. Brothwell, CPSLO 16April 17, 2007

Budget Trailer Bill 1802 – Passed effective July 1, 2006Amended Ed Code 89721 – “The Chief Fiscal

Officer of each campus of the CSU shall deposit and maintain in local trust accounts….. “

(L) Moneys collected as higher education fees and income from students of any campus of the CSU and from other persons pursuant to Section 89700”Allows the CSU to deposit revenue from student fees into the State University Trust Fund

What is Revenue Management Program?

D. Brothwell, CPSLO 17April 17, 2007

Revenue referred to in AB1802

“Money’s collected in the Higher Education Fees and Income Fund” SCO Fund 0498 CSU deposited approximately $1.2B in SCO Fund

498 in 2005-2006 as of June 30, 2006 However, campuses were not all depositing the same fee

revenue Need to establish consistent base

CSU will continue to pay the state back for lost interest earnings on these specific fees

Budget Act Item 6610-402

D. Brothwell, CPSLO 18April 17, 2007

Budget Act Item – “Fiscal Neutrality”

D. Brothwell, CPSLO 19April 17, 2007

The Problem – How do we define the $1.2B?

D. Brothwell, CPSLO 20April 17, 2007

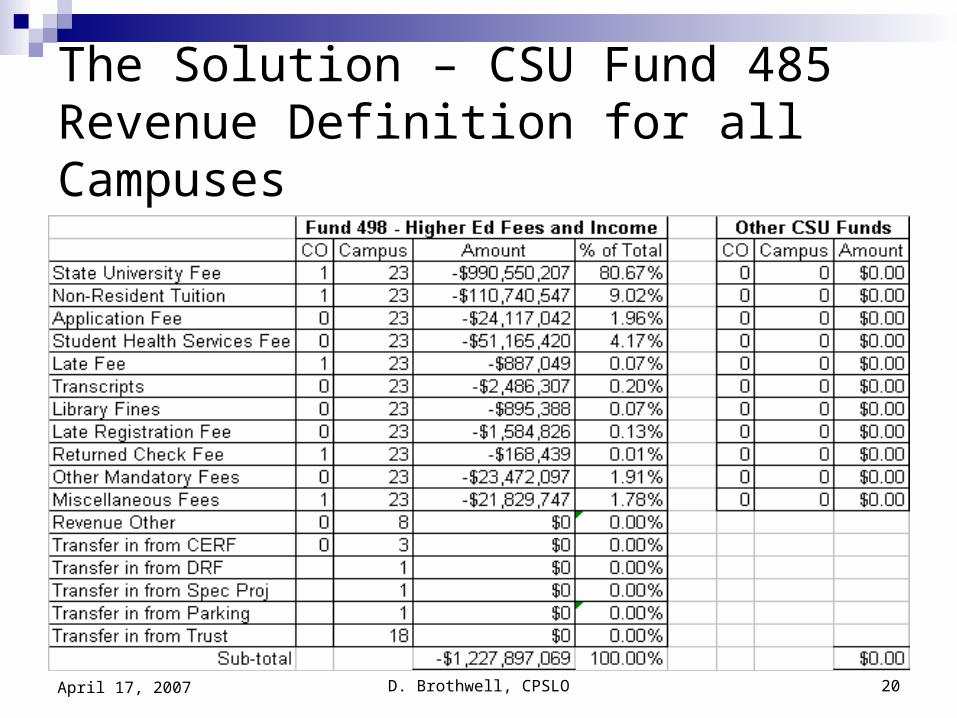

The Solution – CSU Fund 485 Revenue Definition for all Campuses

D. Brothwell, CPSLO 21April 17, 2007

Transfers In to CSU Fund 485 – CSU Operating Fund Campuses can continue to record transfer

in activity as appropriate with CSU fund 485These transfers would meet the following

criteria The funds are for state support of instruction and

related programs Can not identify a specific expenditure

EX: Cost Recovery Income

D. Brothwell, CPSLO 22April 17, 2007

The following fee revenue shall be reported within CSU Fund 485 effective FY 2006-2007

D. Brothwell, CPSLO 23April 17, 2007

Implementation Issues

Health Service Fee Campuses may continue to operate as self-support

Establish a unique PeopleSoft Fund within CSU Fund 485 Can change FNAT but MUST create a new fund in the old CSU

Fund and journal the appropriate equity amounts and transfer in/out to avoid FIRMS reject errors

Program Code classification for this activity will be “0507 – Student Health Services” within CSU Fund 485

Was previously classified as “2001 – Auxiliary Enterprise” within the Health Service CSU Fund

Reported as CSU Fund 485, Accounted for separately

D. Brothwell, CPSLO 24April 17, 2007

Payroll Accounting Changes Payroll originates by the SCO within the State

University Trust Fund CO Processes an expenditure transfer for the

estimated payroll between the campus General Fund (SCO Fund 0001) and the campus State University Trust Fund (SCO Fund 0948 Can be processed as AD-NOAT, CPO or Both Campus are to record the expenditure adjustment in

FIRMS Object Code 690003 within both SCO Fund 0001 and SCO Fund 0948

D. Brothwell, CPSLO 25April 17, 2007

Payroll Accounting Changes

Payroll posts at the campus in the appropriate fund

Campus processes a PFA to adjust the SCO Funds to reflect payroll within the correct SCO Fund. This PFA DOES NOT include an adjustment to the SCO Fund 0001 – General Fund All activity posted within the SCO Fund 0001 –

General Fund is initiated by the Chancellor’s Office NOT the campus

D. Brothwell, CPSLO 26April 17, 2007

Payroll Accounting Changes

The CO initiated PFA for the estimated payroll amount is referred to as Central Payroll Activity (CPA)

This process assists the CSU in fully expending (depleting) the General Fund appropriation each year on or before the month of May.

D. Brothwell, CPSLO 27April 17, 2007

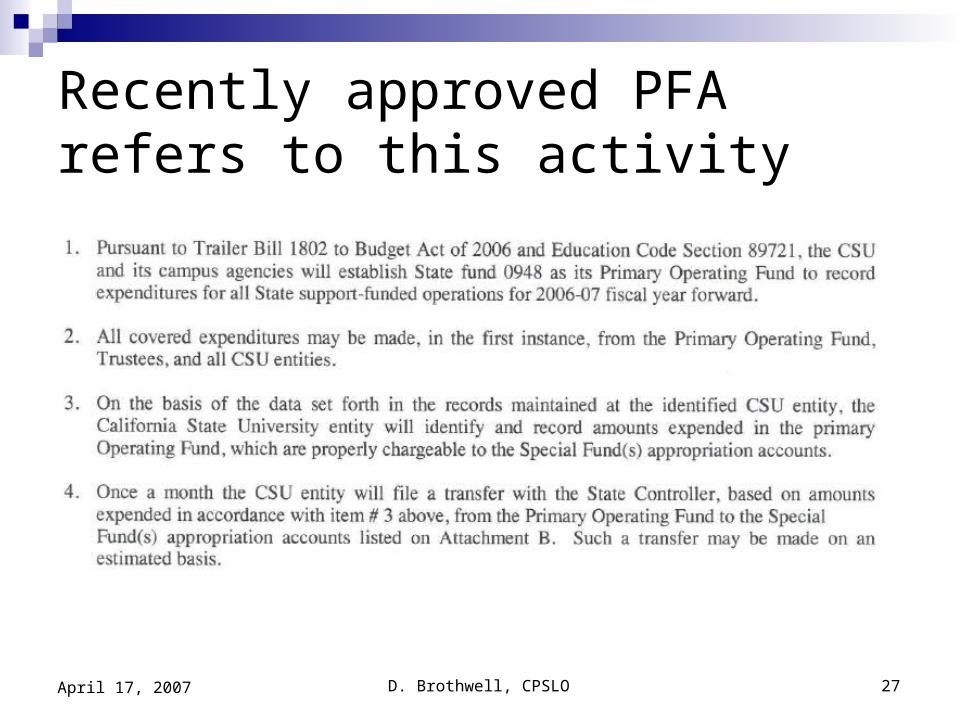

Recently approved PFA refers to this activity

D. Brothwell, CPSLO 28April 17, 2007

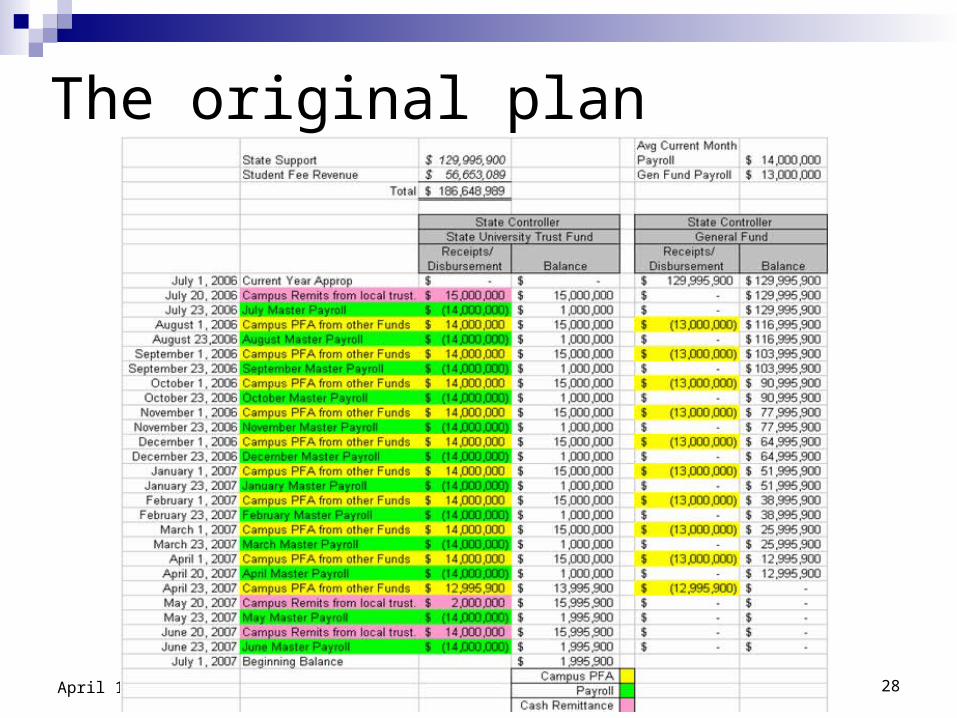

The original plan

D. Brothwell, CPSLO 29April 17, 2007

Payroll Accounting Changes - Cont

As per the interim guidelines issue March 19, 2007, Section 2 of 9 Positive Payroll for the June pay period may be

posted to July 2007 – no accruals Effective with FY 2007-2008 – 12 months of positive

payroll activity will be posted, June thru May Fiscal year 2006-2007 will have savings as a result of this

change This change will assist with a more timely year end close

NO payroll accruals for faculty payroll for the July and August pay-periods are to be accrued

D. Brothwell, CPSLO 30April 17, 2007

Banking

State Treasurer ActivityFIRMS Object Code – 101001 Cash

Wells Fargo ActivityFIRMS Object Code – 108090 Investments

Other

D. Brothwell, CPSLO 31April 17, 2007

State Treasury Activity - 101001

All University Union Fees received by campuses with “senior debt” must transferred to the state treasury Until August 2007

Chico, Northridge, Fullerton, San Diego, San Francisco Until November 2007

San Luis Obispo Principal and Interest payments for revenue

bonds payable to the Dorm Revenue Interest and Redemption Fund 15 days prior to due date Procedures in development

D. Brothwell, CPSLO 32April 17, 2007

State Treasury - 101001

Documents used to process transaction with State Treasury and SCO AccountsState Treasury Deposit SlipRemittance AdviceLocal Bank set up to ZBA to the State

Treasury

D. Brothwell, CPSLO 33April 17, 2007

Wells Fargo - 108090 All fees and income not required to be transferred to the

state treasury remain in Wells Fargo Currently, the CMO office is manually transferring cash

from Wells Fargo to Wachovia Campuses receive a Cash Posting Order (CPO)

Campuses need to notify the CO Cash Management Office (CMO) regarding any “large” deposits or withdrawals as it effects the daily investment activity $200,000 or more, especially wire transfers (ACH in or out)

D. Brothwell, CPSLO 34April 17, 2007

Implementation Issues

Campuses were originally advised to record banking activity within Wells Fargo in FIRMS Object Code 101006

Campuses are now required to record all banking activity within Wells in FIRMS Object Code 108090 (Investments) No year end accrual required to adjust negative cash Reflects accurately that campus is fully invested Cleared by KPMG

D. Brothwell, CPSLO 35April 17, 2007

FIRMS Object Code – 108090

Campus implementation optionsModify all sub-system codes and open

documents to reflect account 108090 Reconcile 101006 to Wells – journal to 108090

Re-map campus account 101006 to FIRMS Object code 108090 for the interim

Modify all sub-system codes and open documents - later

D. Brothwell, CPSLO 36April 17, 2007

Cash and InvestmentActivity

All banking activity recorded within the CSU Central Bank (Wells Fargo) is to be recorded in FIRMS Object Code – 108090

Currently, the CMO office is manually transferring cash from Wells Fargo to Wachovia Campuses receive a Cash Posting Order (CPO)

Some campuses are recording the CPO Credit Cash Debit Investments – other

Need to revisit as both of these accounts should now be mapping to 108090

D. Brothwell, CPSLO 37April 17, 2007

Cash and Investment Activity

All campuses are to record all their allocated investment income for SCO fund 0948 in CSU Fund 499 – FIRMS Object Code 508001 FIRMS Object Code 508001 is only to be used in

CSU Fund 499 within SCO Fund 0948 Campuses may re-allocate investment income to

other CSU Funds using the following new FIRMS Object Codes

680051 Transfer out – investment income 506051 Transfer in – investment income

D. Brothwell, CPSLO 38April 17, 2007

Implementation Issues Campus investment earnings (508001) for SCO

Fund 0948 to date have been recorded in various CSU Funds Need to be corrected by 6-30-2007

Investment Income for 0948 is to be posted to CSU Fund 499 (508001)

Investment Income allocation by the campus to various CSU funds within 0948 is to be recorded using Transfer out (680 051) in CSU 499 and Transfer in (506051) in the receiving CSU Fund

CSU Fund 485 should only receive interest earnings if they are needed to cover planned expenditures within the year (506051)

D. Brothwell, CPSLO 39April 17, 2007

Budget

Campus financial management of CSU Operating FundBBA vs Fund Equity

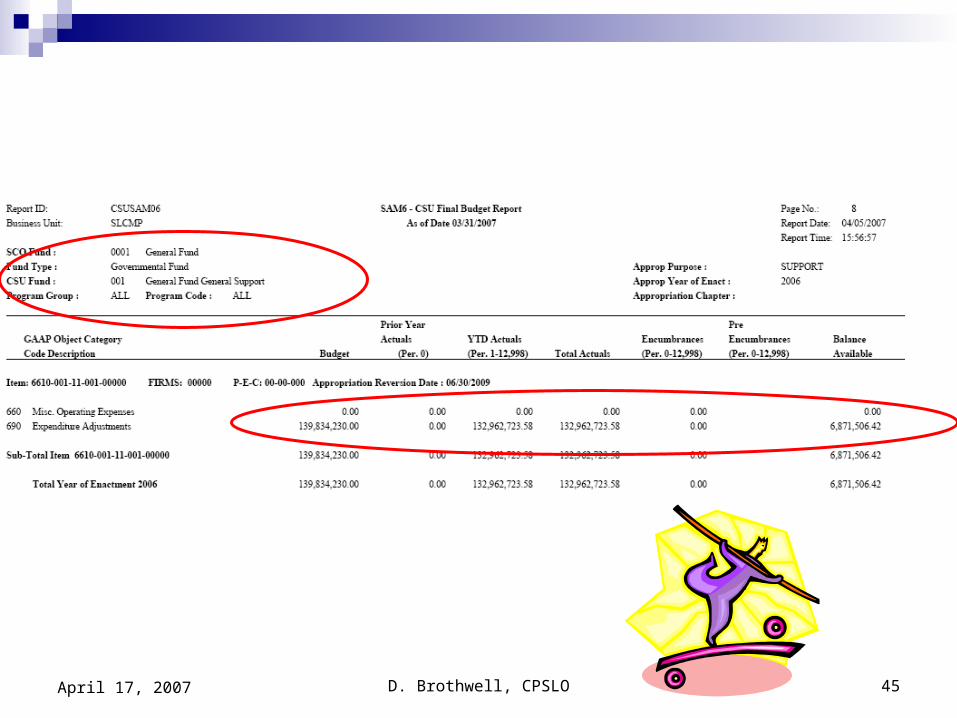

SWAT Transaction Sweep balances vs roll forward Managing Contingencies SAM 6 – Managing the campus current

year plan

D. Brothwell, CPSLO 40April 17, 2007

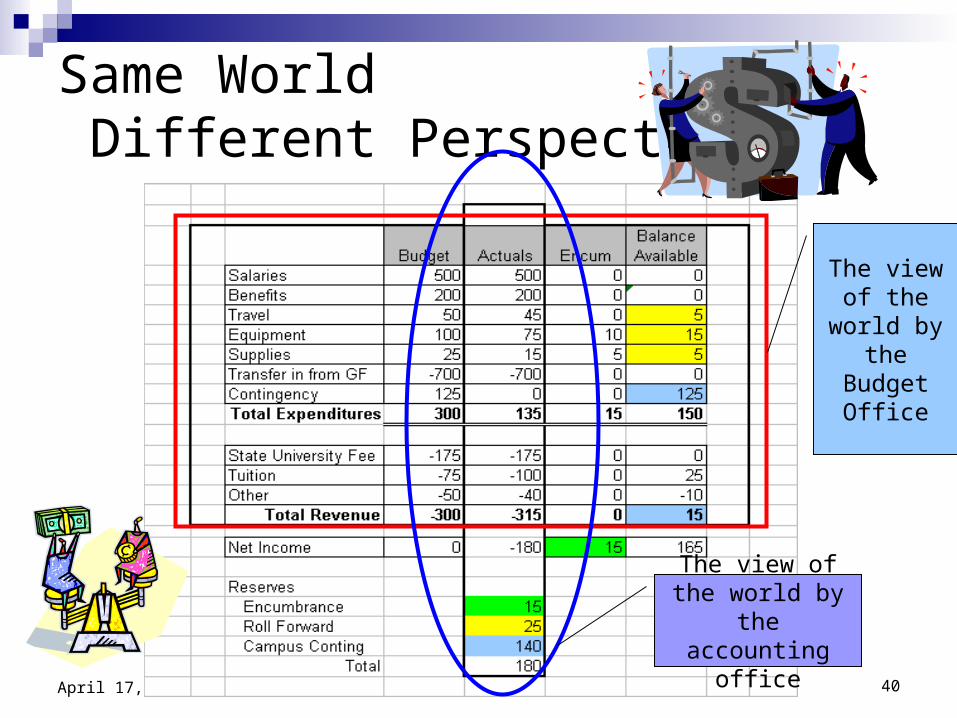

Same World Different Perspective

The view of the world

by the Budget Office

The view of the world by the

accounting office

D. Brothwell, CPSLO 41April 17, 2007

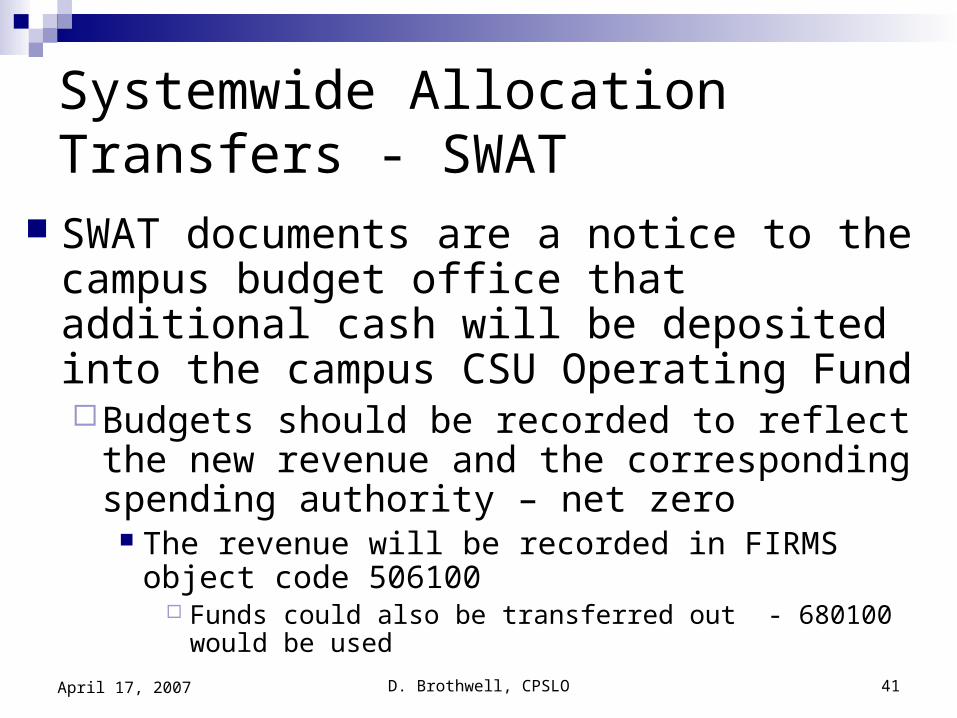

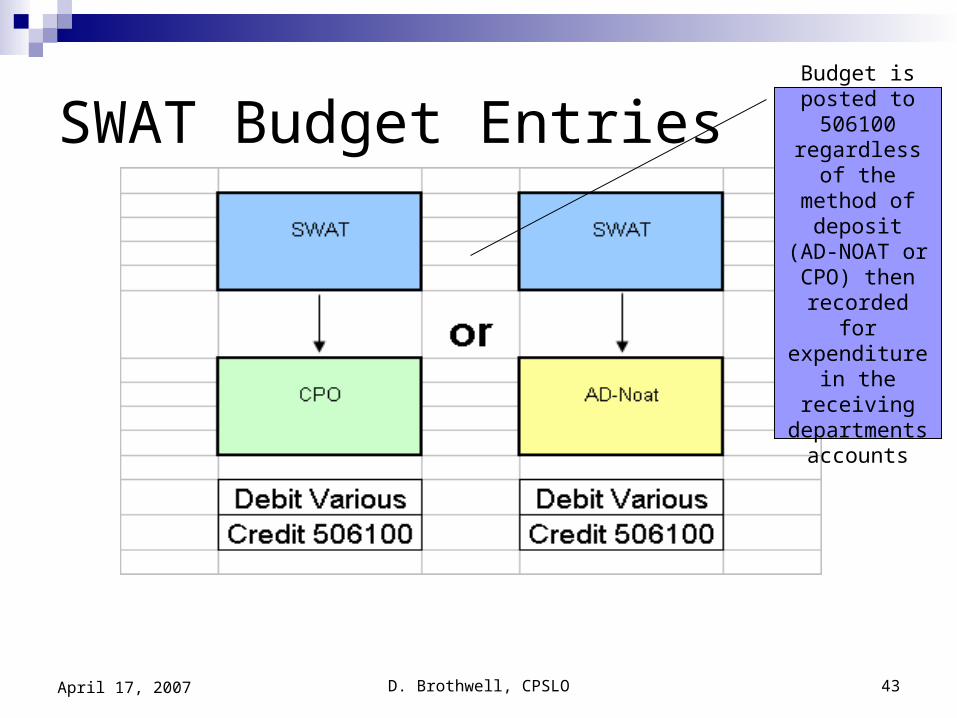

Systemwide Allocation Transfers - SWAT

SWAT documents are a notice to the campus budget office that additional cash will be deposited into the campus CSU Operating FundBudgets should be recorded to reflect the new

revenue and the corresponding spending authority – net zero

The revenue will be recorded in FIRMS object code 506100

Funds could also be transferred out - 680100 would be used

D. Brothwell, CPSLO 42April 17, 2007

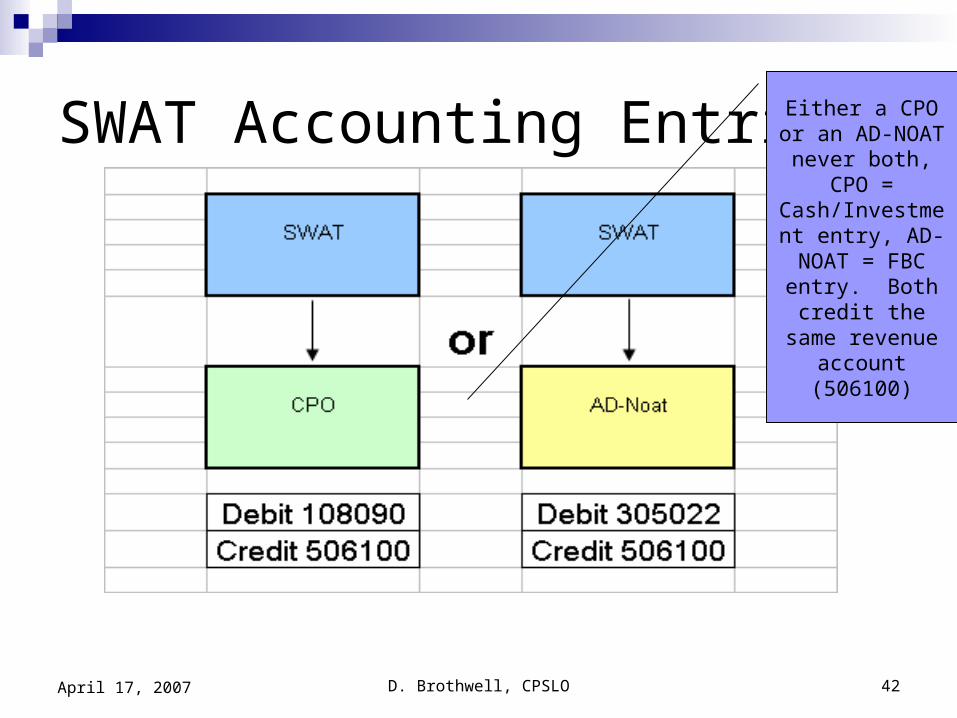

SWAT Accounting Entries Either a CPO or an AD-NOAT

never both, CPO =

Cash/Investment entry, AD-NOAT

= FBC entry. Both credit the same revenue

account (506100)

D. Brothwell, CPSLO 43April 17, 2007

SWAT Budget Entries Budget is posted to 506100

regardless of the method of deposit (AD-

NOAT or CPO) then recorded for expenditure in the receiving

departments accounts

D. Brothwell, CPSLO 44April 17, 2007

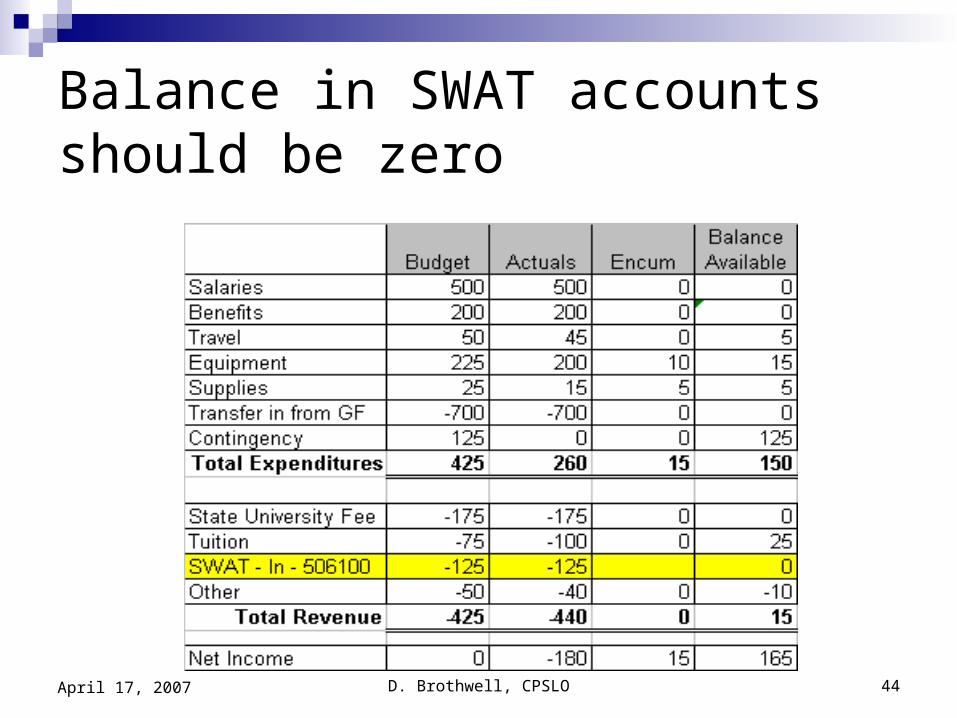

Balance in SWAT accounts should be zero

D. Brothwell, CPSLO 45April 17, 2007

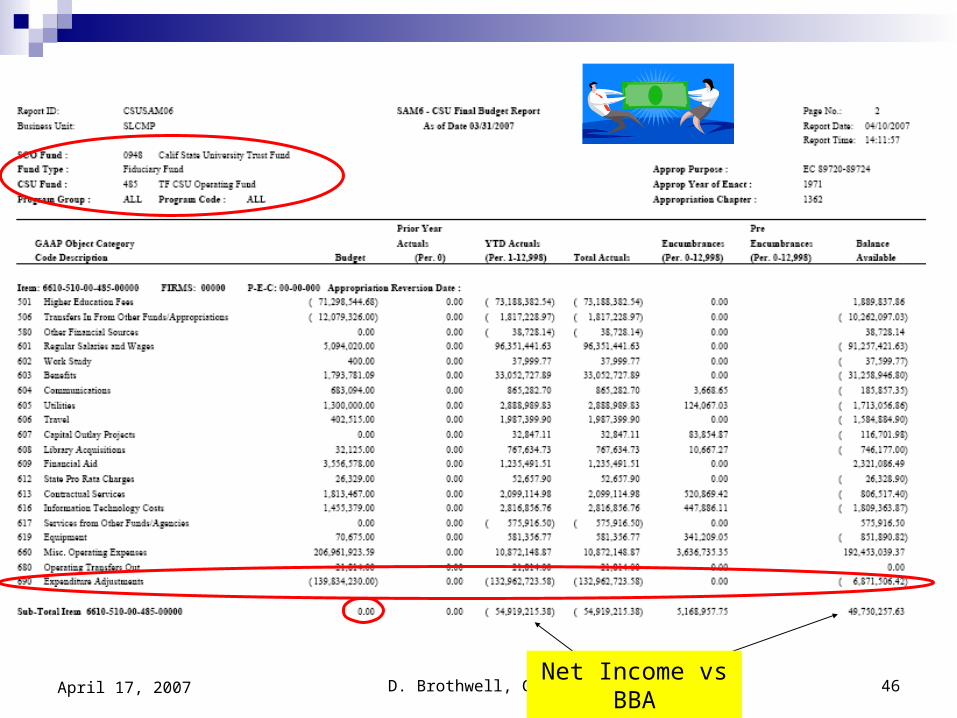

D. Brothwell, CPSLO 46April 17, 2007Net Income vs

BBA

D. Brothwell, CPSLO 47April 17, 2007

Budget Considerations

Does your campus sweep budget balances (BBA) to contingency or roll them forward to the departmentPeopleSoft Fund does not change from year

to year so any differences between what was accrued and what is paid in the subsequent year will be processed within the users account

D. Brothwell, CPSLO 48April 17, 2007

Budget Considerations Managing Contingencies

Campuses historically manage contingencies thru the budget process.

Prior year savings will be a reserve amount in fund equity

Budget offices will more than likely establish a budget for this in order to manage the allocations and the transfers to departments in the subsequent year

This budget will not be recorded in the reserve account

Pre-closing reserve entries per “Interim Guidelines”

D. Brothwell, CPSLO 49April 17, 2007

CSU Fund 499 – Internal Service Fund All investment earnings for SCO Fund

0948 – State University Trust will be recorded in this fund

Direct vendor pay activity will be recorded in this fundCSU Fund 499 is capitalized by CSU Fund

485

D. Brothwell, CPSLO 50April 17, 2007

NEW FIRMS Object Codes and/or new uses 680100 – SWAT Transfer Out 506100 – SWAT Transfer In 506051 – Transfer in Invest Earnings 680051 – Transfer out Invest Earnings 690003 – Transfer in General Fund Exp 108090 – Investment - other

D. Brothwell, CPSLO 51April 17, 2007

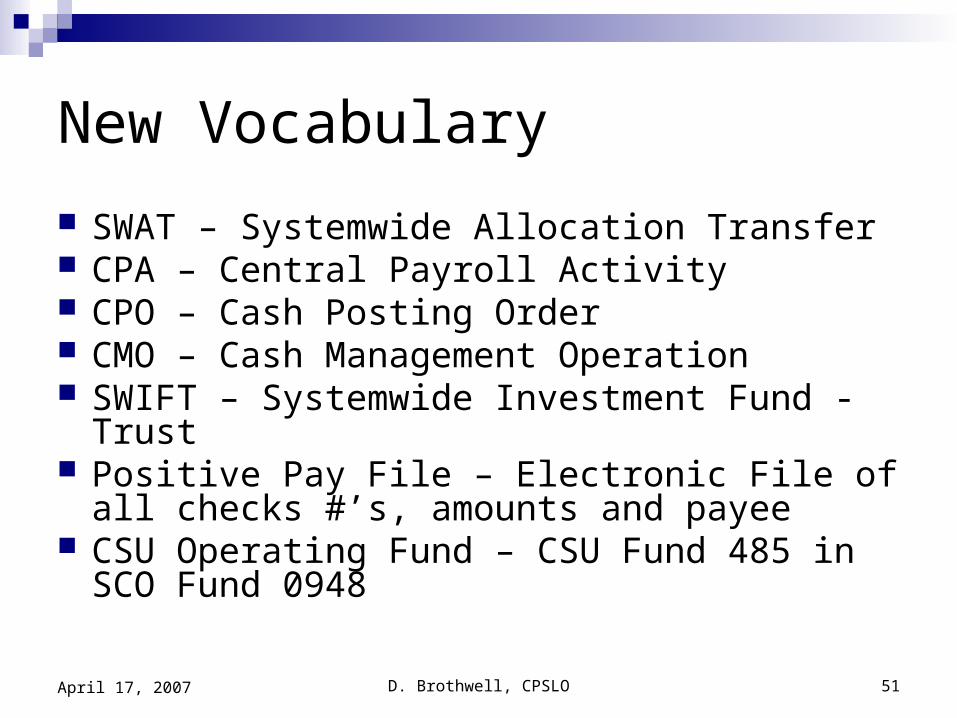

New Vocabulary

SWAT – Systemwide Allocation Transfer CPA – Central Payroll Activity CPO – Cash Posting Order CMO – Cash Management Operation SWIFT – Systemwide Investment Fund - Trust Positive Pay File – Electronic File of all checks

#’s, amounts and payee CSU Operating Fund – CSU Fund 485 in SCO

Fund 0948

D. Brothwell, CPSLO 52April 17, 2007

The Future

D. Brothwell, CPSLO 53April 17, 2007

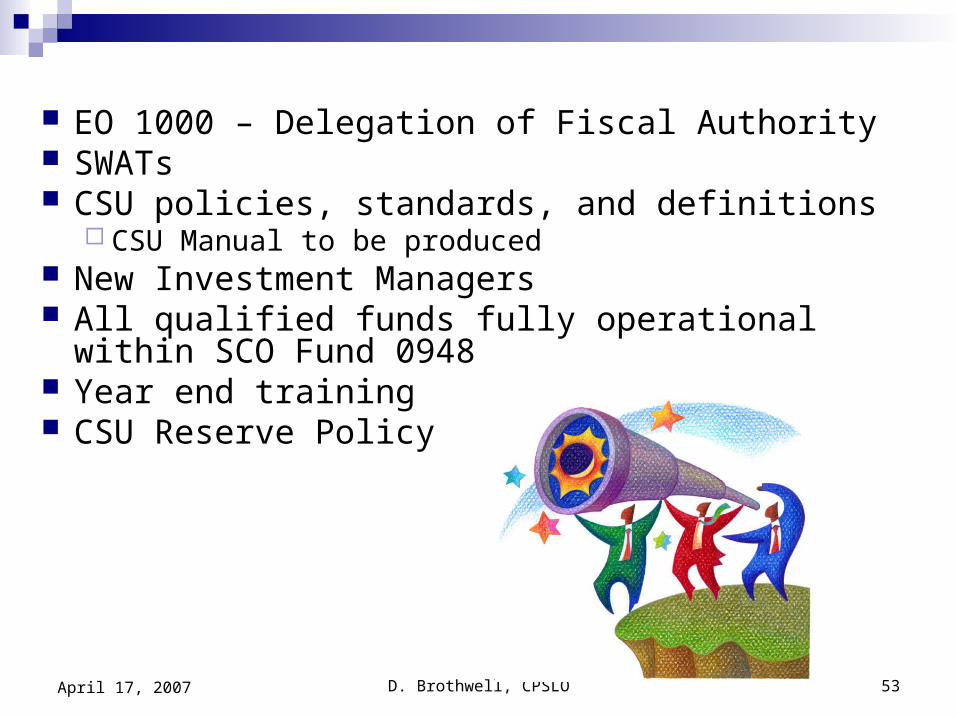

EO 1000 – Delegation of Fiscal Authority SWATs CSU policies, standards, and definitions

CSU Manual to be produced New Investment Managers All qualified funds fully operational within SCO

Fund 0948 Year end training CSU Reserve Policy

D. Brothwell, CPSLO 54April 17, 2007

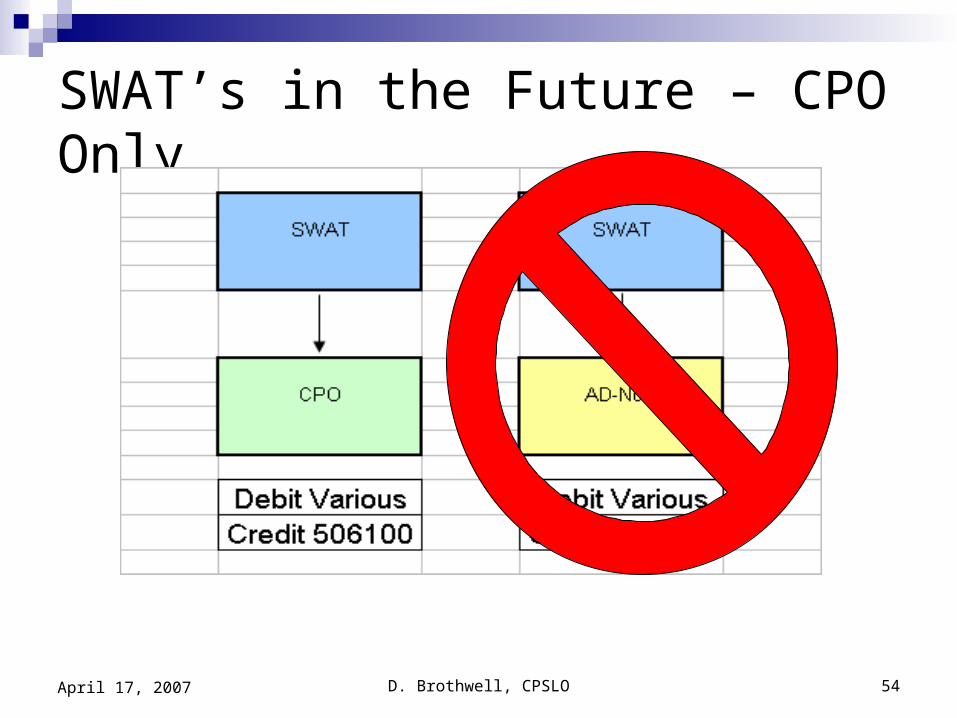

SWAT’s in the Future – CPO Only

D. Brothwell, CPSLO 55April 17, 2007

EO 1000 – CSU Delegation of Fiscal Authority Overall approach

Create a framework that supports the development of CSU accounting definitions and standards (principle based). Create a delegation of authority based on “textbook” governmental accounting definition of funds – sustainability for the CSU.

This EO acknowledges, defines and guides the CSU, as it now operates within two succinct set of accounting records.

D. Brothwell, CPSLO 56April 17, 2007

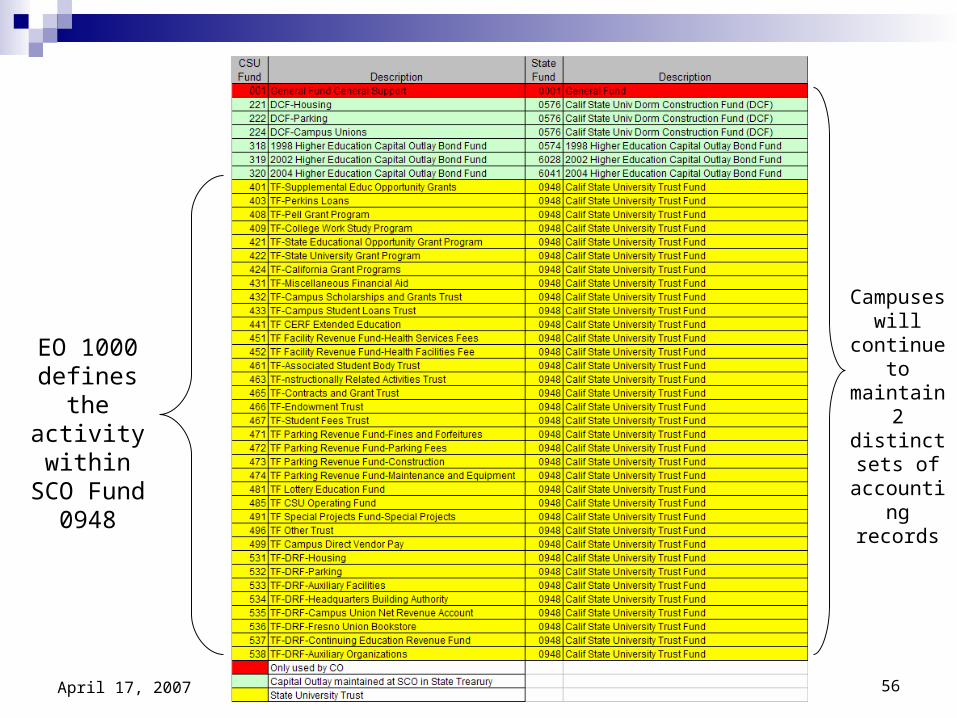

EO 1000 defines the

activity within SCO Fund 0948

Campuses will

continue to maintain 2

distinct sets of

accounting records

D. Brothwell, CPSLO 57April 17, 2007

New CSU “Manual”

“CSU policies, standards, and definitions” refers to a unified system of CSU policies, standards, and definitions pertaining to the administration and safe-keeping of university assets, budgetary accounting and classification, financial accounting and classification, and financial reporting, and is inclusive of financial transactions between the campus and recognized Auxiliary Organizations.

D. Brothwell, CPSLO 58April 17, 2007

New Investment Managers US Bank (custodian) and Wachovia Effective with the implementation of the

new investment activity (daily sweeping of balanced) campuses will NO LONGER receive CPO documents for investment activityDaily sweep activity can be seen on-line in the

Wells CEO

D. Brothwell, CPSLO 59April 17, 2007

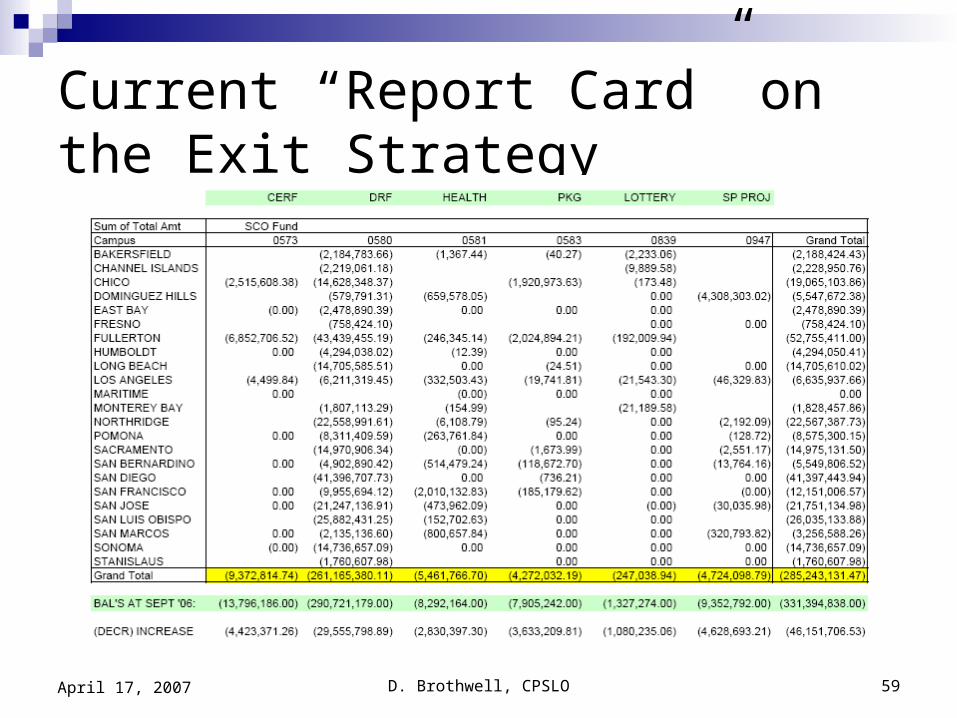

Current “Report Card” on the Exit Strategy

D. Brothwell, CPSLO 60April 17, 2007

Year end training considerations

Fund Roll Forward rules Combo Edit Changes Year end close rules

CSU Fund 485 closes to 305002 NOT 305022 No activity in 101006 Health Services Fund should be closed

D. Brothwell, CPSLO 61April 17, 2007

Important Documents

Interim Guidelines Memo – March 19, 2007From Dennis Hordyk to Vice Presidents

EO 1000 – Delegation of Fiscal Authority Current Approved PFA – March 28, 2007 This presentation Year end training materials

D. Brothwell, CPSLO 62April 17, 2007

Planning for 2007-2008