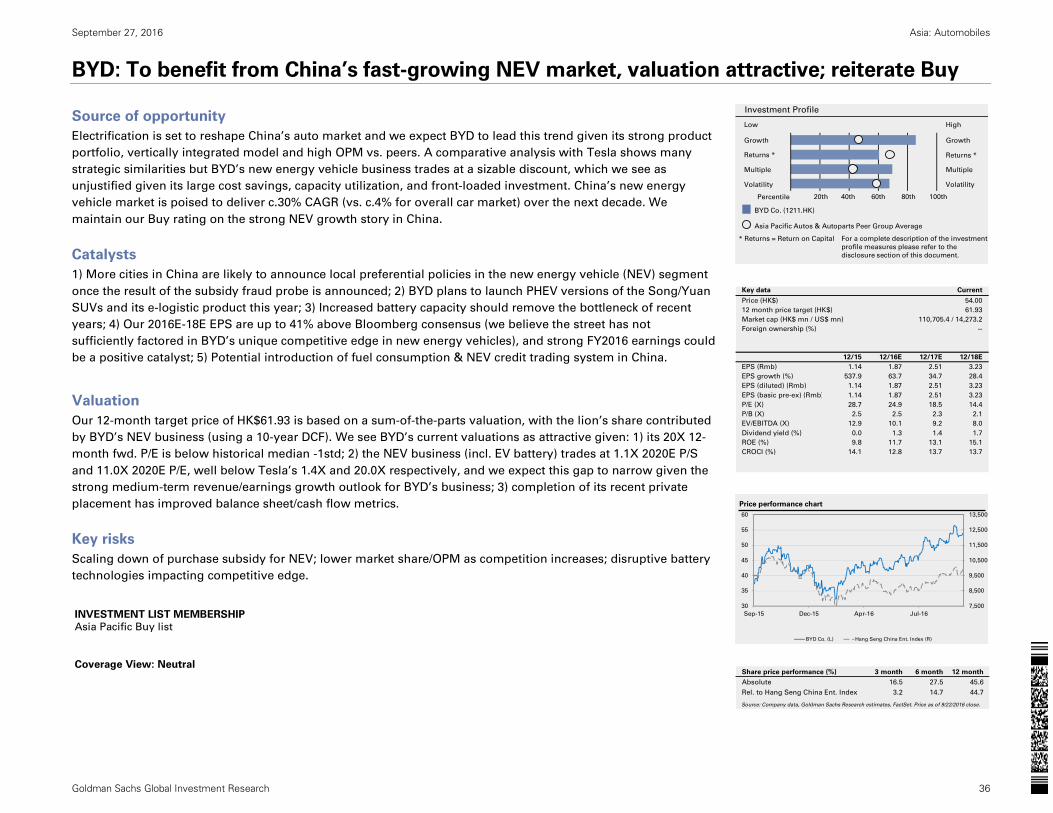

asia: automobiles — charging the future: asia leads … · september 27, 2016 asia: automobiles...

TRANSCRIPT

September 27, 2016

Asia: Automobiles

Charging the future: Asia leads drive to

next-generation EV battery market Equity Research

Pushing the limits of lithium-ion batteries and investing in all-solid-state batteries

Battery market to grow 6X by 2025E

We believe the rapid adoption of electric vehicles

and hybrids over the next decade will spur an

enormous increase in the market for EV batteries

and heightened demand for advances in battery

technology. We forecast a six-fold increase in the

market for EV batteries to US$24 billion by 2025,

fueled by increases in energy density to lower

prices. In this report, we outline where we see

Asian companies leading this growth and

pioneering efforts to find the next-generation

battery technology to replace lithium-ion.

Powering the transition to EVs

Our battery market forecasts rest on our

expectations for a 30% CAGR in sales of electric

vehicles (EVs) to 2025, along with a 36% CAGR in

sales of plug-in hybrid electric vehicles (PHEVs) to

reduce CO2 emissions. We expect that over that

span, the gravimetric energy density of EV

batteries will climb to over 500 Wh/kg from 200

Wh/kg in 2015, likely requiring transition to a

post-lithium technology.

Investing with eye to lithium’s limits

Our approach is to look for companies that will

benefit from expansion and innovation in the

lithium-ion battery (LIB) market, as well as those

invested in the development of potential

successor technologies. We believe the post-

lithium transition could start from 2020. Among a

range of alternatives we focus on all-solid-state

batteries that would do away with the liquid

electrolyte found in most lithium-ion batteries and

offer advantages in size and cost.

Asian at heart of battery ecosystem

LG Chem (CL-Buy), Korea’s leading battery

manufacturer, has supply contracts with multiple

automakers, and in our view has an edge over

rivals from both a technical and cost perspective

BYD (Buy), China’s leading EV manufacturer, is

mass-producing its own inexpensive batteries. In

addition, we highly value Toyota’s long-term

strategy to focus on all-solid-state batteries, but

remain Neutral due to US auto slowdown

concerns in the near term.

Kota Yuzawa

+81(3)6437-9863 [email protected] Goldman Sachs Japan Co., Ltd.

Yipeng Yang

+86(10)6627-3189 [email protected] Beijing Gao Hua Securities Company Limited

Nikhil Bhandari

+65-6889-2867 [email protected] Goldman Sachs (Singapore) Pte

Masaru Sugiyama

+81(3)6437-4691 [email protected] Goldman Sachs Japan Co., Ltd.

Shuhei Nakamura

+81(3)6437-9932 [email protected] Goldman Sachs Japan Co., Ltd.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

The Goldman Sachs Group, Inc. Global Investment Research

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 2

Table of contents Our thesis in four charts: Battery market to grow 6X by 2025E

Executive summary: Battery race starting to rev up in Asia

10 Asian beneficiaries of LIB growth, development of post-lithium technology

Key industry themes

Battery race accelerating with energy density likely to double, market up 6X by 2025E

Up the technology curve: Next-generation LIBs, then all-solid-state batteries

EV and PHEV penetration set to accelerate through 2025E

Stocks in focus

LG Chem: Strong and diversified EV battery client base; reiterate CL-Buy

BYD: To benefit from China’s fast-growing NEV market, valuation attractive; reiterate Buy

Panasonic Corp: Leading LIB supplier globally, but Neutral on tough market outlook

Toyota: Leading all-solid-state battery development, but Neutral on stiff competition

Toray: No. 2 supplier of LiB separators globally, further expansion underway; Neutral

Samsung SDI: Shifting focus from mobile to EV, but challenges ahead; Neutral

Other beneficiaries

Appendix

Disclosure Appendix

Prices are as of September 21 close for Japanese companies and September 22 close for non-Japanese companies. The Future in

numbers

The drive for better EV batteries sits at the nexus of multiple trends. See our theme pages for related work on Cars 2025, The Low Carbon Economy and The Great Battery Race.

Lighter, Faster, Cheaper, Apr 7, 2016

Disruption in China’s new car market, Feb 29, 2016

BYD (1211.HK) Buy: Electrifying the world’s largest new car market; reinstate at Buy, Aug 31, 2016

The Low Carbon Economy, Nov 30, 2015

Electric Vehicles – customer acceptance & continued scaling; check, Apr 7, 2016

The Great Battery Race, Oct 18, 2015

China Energy Storage: Charged up and ready to grow, Jun 8, 2016

LG Chem (051910.KS) Buy: Right chemistry and charged batteries; initiate at Buy (on CL), Jan 22, 2016

Get a 2-minute audio summary from author Kota Yuzawa. Listen here

4

5

6

9

10

14

25

33

34

36

38

40

42

44

47

50

56

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 3

Charging The Future in numbersSATISFYING THIRST FOR RANGEBATTERY BOOM ON THE WAY

GREATER DEMAND, GREATER DENSITYCOST TO COME DOWN

THE LARGEST MARKET - CHINAASIA TAKING THE LEAD

Increase in lithium-ion battery (LiB) demand expected between 2015 and 2025, rising from 58 GWh to 387 GWh. Demand for automotive batteries is slated to rise from 15 GWhto 279 GWh during the same period. (p. 12)

6x

2x Increase in energy density expected between 2015 and 2025, from 200 Wh/kg to 550 Wh/kg. (p. 10)

60 kWhBattery capacity needed to achieve a driving distance comparable with that of a gasoline-powered vehicle (around 300 km/200 miles). (p. 11)

US$272 to US$100 per kWhCost for auto batteries from 2015 to 2025E. Improvement in energy density should help drive this decline. (p. 10)

300,000 New Energy Vehicle sales (excluding hybrids) in China (2015). (p. 29)Percentage of global output from Asian battery makers. (p. 6) 50%+

3,000+ Patents for all-solid-state batteries filed in 2002-2011, far higher than other post-LiB technologies. 71% of these applications were filed by Japan, Korea and China. (p. 19)

The All-Solid-State Batteries Future

What is an all-solid-state battery?An orthodox LiB has a separator and liquid electrolyte between the cathode and the anode. An all-solid-state battery, on the other hand, has only a solid electrolyte between the cathode and the anode, and contains no liquid. There is no need for a separator, as the solid electrolyte also takes on that function. These batteries are known as all-solid-state batteries as they contain absolutely no liquid.

Why are all-solid-state batteries needed?All-solid-state batteries have advantages in terms of safety, and they also offer stable performance through a wide range of temperatures, which is why they are being developed for automotive applications. As they eliminate the need for liquid electrolytes and separators, all-solid-state batteries could in theory have much higher energy density. Competition to develop solid electrolytes will be the key.

Is the production method different?A mass production technique for all-solid-state batteries has yet to be established. However, in many cases the production of relatively large-capacity all-solid-state batteries for automotive applications involves a pressurized process, which means that facilities will differ from those used to make conventional LiBs. Solid electrolytes are generally less conductive than liquid electrolytes, but a number of companies, including Toyota, are vying with each other to develop solid electrolytes that have ionic conductivity on a par with, or even exceeding, that of liquid electrolytes.

Negative current collector Positive current collector

Separator

Li+

Li-

Li-

Li-

Li-

Li-

Li+

Li+Li+

Li+

Li+

Anode CathodeLiquid

Negative current collector Positive current collector

Li+

Li-

Li-

Li-

Li-

Li-

Li+

Li+Li+

Li+

Li+

Anode CathodeSolid

Lithium-ion battery All-solid-state battery

Source: Goldman Sachs Global Investment Research.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 4

Our thesis in four charts: Battery market to grow 6X by 2025E

Exhibit 1: Bullish on demand outlook for EVs, PHEVs Outlook for EV/PHEV sales, 2015-2025E CAGR

Exhibit 2: Forecast rapid increase in energy density, battery costs halving Outlook for energy density, battery costs

Note: Excluding low speed EV in China.

Source: IHS, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

Exhibit 3: At battery cost of US$100 per kWh, EVs could represent cheapest

solution for reducing CO2 Additional cost to reduce CO2 by 1g

Exhibit 4: We project six-fold growth in automotive battery market LIB market outlook, by application

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

(Thous.) 2015 2020E 2025E CAGR

PHEV 397 1,272 2,787 22%

China 60 518 1,339 36%

Non-China 337 753 1,448 16%

EV 251 1,322 4,014 32%

China 140 864 1,890 30%

Non-China 111 458 2,123 34%

PHEV+EV 648 2,594 6,801 27%

Global auto demand 88,384 101,730 111,494 2%

683

272

197

100150

200

300

500

0

100

200

300

400

500

600

700

0

100

200

300

400

500

600

700

Cost(USD/Wh, RHS)

Energy density(Wh/kg, LHS)

Current LIB

Next generation LIB

Post LIB(All-solid-state battery)

Needtechnologicalbreakthrough

Li-ion battery All-solid-state battery

2010 2015 2020E 2025-2030E

10 9 7 215 1517

9 113

86

302710 17

4

279

49

0

50

100

150

200

250

300

Mobile phone PC Tablet Machine tool Automotive Others

2015 2020 2025

(GWh)

2015$ 4bn

2025$ 24bn

Automotivebattery market (USD)

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 5

Executive summary: Battery race starting to rev up in Asia

PHEV, EV penetration set to pick up pace; EVs key to CO2 reduction Almost two decades have passed since Toyota launched the world’s first mass-produced hybrid vehicle (HV) in 1997. By 2015, the

hybrid vehicle market had grown to 2 mn units, making an enormous contribution to CO2 reduction. Over the coming 10 years, we

think electric vehicles (EVs) and plug-in hybrid vehicles (PHEVs) will demonstrate remarkable growth. In recent years, environmental

regulations have been strengthened and tightened, forcing automakers to review their powertrain strategies. In addition, we see

significant support for EV growth from stepped-up new energy vehicle (NEV) subsidies in China. Moreover, advances in lithium-ion

battery (LIB) technology (huge leaps in energy density) could result in an increase in battery capacity per vehicle. We see the EV

market expanding from 250,000 units in 2015 to 4.01 mn units in 2025 (CAGR of 30%) and look for PHEV sales to rise from 400,000

units to 2.78 mn units (CAGR of 36%). Over the same period, we expect the HV market to grow from 2.16 mn units to 13.94 mn units

(CAGR of 20%).

The lower the cost for batteries, the more sense it will make to adopt an EV-based business model. We calculate that in PHEVs, the

additional cost to lower CO2 by 1 gram is US$139. Based on a battery cost of US$272 per kWh in 2015, we calculate that in EVs, the

additional cost to lower CO2 by 1 gram would be US$124, similar to that for PHEVs. That cost would shrink to US$31, though, in the

case of a battery cost as low as US$100 per kWh. This would make EVs an inexpensive solution for reducing CO2 emissions, on a

par with vehicle light weighting and downsizing turbo engines. From the automakers’ perspective, we see grounds to continue

investing heavily in EVs through 2030.

Turning point ahead for batteries; six-fold growth in automotive battery market by 2025E We look for the automotive battery market to expand considerably, in tandem with growth in the EV and PHEV markets. We expect a

roughly six-fold increase in LIB demand between 2015 and 2025, from 58 GWh to 387 GWh, with demand for automotive batteries

rising from 15 GWh to 279 GWh over the same period. Thus far, mobile phones and PCs have been the main source of demand for

LIBs, but over the next decade we think rapid growth in automotive applications will bring battery operations to a major turning

point. Even allowing for an average annual decrease of about 5% in battery prices—to encourage greater uptake—we think the

market for automotive LIBs could grow sharply in size between 2015 and 2025, from US$4 bn to a massive US$24 bn. For further

details on LIB demand, see our October 18, 2015 report Global: Clean Energy: The Great Battery Race.

Rapid improvement in energy density; focus on all-solid-state batteries The history of automotive LIBs is one of unstinting efforts to improve energy density (gravimetric or volumetric). In 2007–08, Nissan

announced plans for large-scale investment in pouch-type batteries with manganese spinel as the cathode material, going on to

launch the Leaf EV. At the time, we estimate that gravimetric energy density was 100-150 Wh/kg, but by 2015, batteries with ternary

cathode materials were achieving gravimetric energy density of over 200 Wh/kg. Looking ahead, further technical advances will

likely lift this figure to 300 Wh/kg by 2020, and over 500 Wh/kg in 2025 and beyond. Similarly, the aim is to boost volumetric energy

density from 500 Wh/l in 2015 to 700 Wh/l in 2020 and 1,100 Wh/l in 2025 and beyond. We note this will likely require a transition to

so-called “post-lithium ion” technology. Among the many next-generation battery technologies, we focus on all-solid-state batteries.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 6

10 Asian beneficiaries of LIB growth, development of post-lithium technology

While innovation in battery technologies is proceeding at a rapid pace worldwide, battery development is booming in Asia in

particular. Asian battery makers currently have around 50 GWh of production capacity, equivalent to 50% or more of global output

(consumer electronics/automotive battery capacity combined), and have monopolistic shares of 50%-80% of core component

materials, such as cathode materials and separators. Asian producers have also taken the lead in the development of next-

generation batteries. Japan accounted for 53% of patent applications filed in 2002-2011, followed by the US at 13%, Europe at 12%,

Korea at 10% and China at 8%. We reiterate our Buy ratings on LG Chem (CL) and BYD on the back of rapid LIB business expansion.

We remain Neutral on Toyota over short-term US auto market slowdown concerns, but highly value its long term strategy to focus

on all-solid-state batteries. We also spotlight seven other battery and related product makers from among the many Asian names in

this space.

• LG Chem (battery manufacturer, Korea, CL-Buy): A major battery manufacturer with total production capacity of 13 GWh

(our estimate, consumer electronics/automotive battery capacity combined), for a 13% share of the global market. It has well-

established automotive battery supply agreements with Hyundai, General Motors, Ford, and other major automakers. LG Chem

also has an edge in terms of technological development, having successfully developed ternary (nickel, cobalt, manganese

composite) batteries with energy density of more than 200 Wh/kg.

• BYD (automaker, China, Buy): Sales have been growing rapidly on the back of China’s NEV policies. BYD currently mass

produces batteries using lithium ferrophosphate as a cathode material, but also plans to develop batteries with improved

energy density, mainly through the use of ternary (nickel, cobalt, manganese composite) technologies. We see advantages in

terms of cost competitiveness for automakers producing batteries in-house under a vertically integrated business model.

• Toyota (automaker, Japan, Neutral): Toyota is the world’s largest producer of nickel-metal hydride batteries for hybrid

vehicles, but has made no major investments in LIBs. We believe the company considers all-solid-state batteries essential to

growth in EV uptake. We see appeal in Toyota’s accumulating expertise in the field of all-solid-state batteries, including the

development of (solid) electrolytes with high ionic conductivity, but think any real-world applications are unlikely to become a

reality before 2020.

• Panasonic (battery manufacturer, Japan, Neutral): A major battery manufacturer with total production capacity of 10 GWh

(our estimate, consumer electronics/automotive battery capacity combined), for a 10% share of the global market. Sales of

automotive batteries in FY3/16 stood at around ¥150 bn, but we expect this figure to rise sharply to ¥350 bn by FY3/19.

Panasonic is also responsible for supplying nickel cobalt aluminum batteries to Tesla, and has decided to invest around ¥150-

¥200 bn in the US automaker’s Gigafactory project.

• Toray Industries (separator maker, Japan, Neutral): A hybrid chemical maker that makes wet separators, with a 20% market

share in separators, second to Asahi Kasei, which has a 45% share (including its Celgard acquisition). Despite the fact that the

separator business accounts for only 1.2% of sales, the company is planning aggressive capacity additions in coming years.

• Samsung SDI (battery manufacturer, Korea, Neutral): SDI has built a solid track record with increasing market shares in

consumer/mobile battery business. However, we do not expect SDI’s success in mobile battery will directly translate into EV

battery industry given diverging industry dynamics and customer base. We foresee three major challenges for SDI’s EV battery

business including limited customer base, slower cost reduction, and regulation risks in China.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 7

• Asahi Kasei (separator maker, Japan, Not Covered): The only maker of both dry and wet separators, the company has a

dominant, 45% separator market share (Asahi Kasei acquired rival Celgard, which makes dry separators, in 2015). The

separator business accounts for 6% of sales. According to Asahi Kasei, the business is expected to make ¥2.5 bn in operating

losses in 2016 due to goodwill amortization from the Celgard acquisition.

• Tanaka Chemical (cathode materials maker, Japan, Not Covered): A pure play that mainly makes positive electrode

precursors. On August 31, 2016, Tanaka Chemical announced plans to raise capital by issuing new shares via a private

placement to Sumitomo Chemical. This would take Sumitomo Chemical’s stake in Tanaka Chemical to 50.1%. The two have

been collaborating already on development of next-generation nickel-cobalt-manganese (NCM) cathode materials with a nickel

weighting as high as 90%, which should contribute to further increasing batteries’ energy density.

• W-Scope (separator maker, Japan, Not Covered): A wet separator pure play, with a 5% separator market share. It currently

has a 65% consumer electronics separator weighting and a 35% automotive separator weighting, but is targeting market share

growth in automotive separators with the shift from wet to dry separators. Its head offices are in Japan, and it is listed in Japan,

but all of its production bases are in Korea.

• Hitachi Zosen (all-solid-state battery maker, Japan, Not Covered): A machinery maker engaged in the ship engine and

environmental plant businesses that is devoting energy to the development of all-solid-state batteries that make use of

machine stamping technology. With all-solid-state batteries, the process of applying pressure is important in order to boost

electrolyte and positive/negative electrode conductivity, and Hitachi Zosen’s press technology is used for this. The company

has already succeeded in 200 Wh/kg aluminum laminate trial production.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 8

Exhibit 5: Stock selection premised on rapid increase in demand for automotive batteries Valuations for related stocks

Note: NC=Not Covered. All target prices are on a 12-month timeframe. Shares shown above in terms of sales (based on FY2015 company data).

Source: Datastream, Goldman Sachs Global Investment Research.

Mkt cap Price TP Return(mn USD) (local) (local) Potential FY17 FY16E FY17E FY17 FY16E FY17E FY17 FY16E FY17E

OEMsToyota 203,469 Neutral ¥ 6,144 6,400 4% 12.0 11.0 10.1 1.1 1.0 0.9 8.8% 9.0% 9.1%BYD (H) 6,370 Buy HK$ 54.00 61.93 15% 24.9 18.5 14.4 2.9 2.7 2.4 11.8% 14.5% 16.6%Battery makersLG Chem 14,326 Buy CL ₩ 238,500 335,000 40% 11.1 10.3 9.8 1.2 1.1 1.0 11.1% 11.1% 10.6%Panasonic 25,603 Neutral ¥ 1,052 1,100 5% 18.1 13.0 11.5 1.4 1.3 1.2 7.5% 9.7% 10.2%Toray 15,961 Neutral ¥ 986 1,000 1% 16.2 14.9 14.1 1.5 1.4 1.3 9.5% 9.6% 9.4%Samsung SDI 6,202 Neutral ₩ 99,500 105,000 6% 19.7 24.3 15.3 0.6 0.6 0.6 3.2% 2.6% 3.9%Asahi Kasei 11,377 NC ¥ 818 - - 13.0 11.9 11.1 1.0 1.0 0.9 8.0% 8.2% 8.3%Tanaka Chemical 171 NC ¥ 1,161 - - - - - - - - - - -W-Scope 667 NC ¥ 2,154 - - 22.6 17.1 13.0 3.6 3.0 2.4 16.0% 17.4% 18.4%Hitachi Zosen 888 NC ¥ 526 - - 11.8 9.8 8.8 0.7 0.6 0.6 6.3% 6.6% 6.5%

(Valuation) ROERating P/E P/BCurrency

EV battery, 7%

Consumer

battery, 37%

Non-Battery, 56%

Samsung SDI

EV battery,

2%

Consumer

battery, 1%

Non-Battery,

97%

PanasonicBattery, <1%

Non-Battery,

99%

ToyotaBattery,

1%

Non-Battery,

99%

Toray

Battery, 16%

Non-Battery, 84%

LG ChemBattery, 7%

Non-Battery, 93%

BYD

EV battery,

32%

Consumer battery,

50%

Non-Battery,

18%

Tanaka ChemicalBattery, 6%

Non-Battery, 94%

Asahi Kasei

EV battery,

35%

Consumer battery,

65%

W-scopeBattery, <1%

Non-Battery,

99%

Hitachi Zosen

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 9

Key industry themes

Key industry themes

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 10

Battery race accelerating with energy density likely to double, market up 6X by 2025E

Battery history one of tackling energy density

The history of automotive LIBs is one of unstinting efforts to improve energy density (by gravimetric or volumetric). In 2007–08,

Nissan announced plans for large-scale investment in pouch-type batteries with manganese spinel as the cathode material, going

on to launch the Leaf EV. At the time, we estimate that gravimetric energy density was 100-150 Wh/kg, but by 2015, batteries with

ternary cathode materials were achieving gravimetric energy density of over 200 Wh/kg. Looking ahead, further technical advances

likely will lift this figure to 300 Wh/kg by 2020, and over 500 Wh/kg in 2025 and beyond. Similarly, the aim is to boost volumetric

energy density from 500 Wh/l in 2015 to 700 Wh/l in 2020 and 1,100 Wh/l in 2025 and beyond.

Improvement in energy density to reduce battery cost

Improving energy density on per unit gravimetric /volumetric basis is expected to contribute significantly to the reduction in battery

costs. We estimate the cost of automotive batteries was around US$272 per kWh in 2015, and we forecast it will decline to US$197

per kWh by 2020 and US$100 per kWh by 2025. This is because the improvement in energy density should not only reduce materials

costs but also increase economies of scale through greater automotive battery penetration. We note, though, that achieving a

twofold increase in gravimetric/volumetric energy density by 2025 likely will require a transition to so-called “post-lithium ion”

technology. Among the many next-generation battery technologies, we focus in particular on all-solid-state batteries.

Exhibit 6: Energy density likely to take off over the next 10 years Energy efficiency per unit weight and volume forecasts

Exhibit 7: Battery costs could halve kWh cost forecasts (US$)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

500

800

1,100

200

350

550

0

200

400

600

800

1,000

1,200

2010 2015 2020E 2025E 2030-E

Current Wh/L

Future(All solid) Wh/L

Current Wh/kg

Future(All solid) Wh/kg

LiB All Solid Battery etc.

683

272

197

100

0

100

200

300

400

500

600

700

2010 2015 2020E 2025E 2030-E

Current LiB

Future LiB

Post-LiB

LiB All Solid Battery etc.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 11

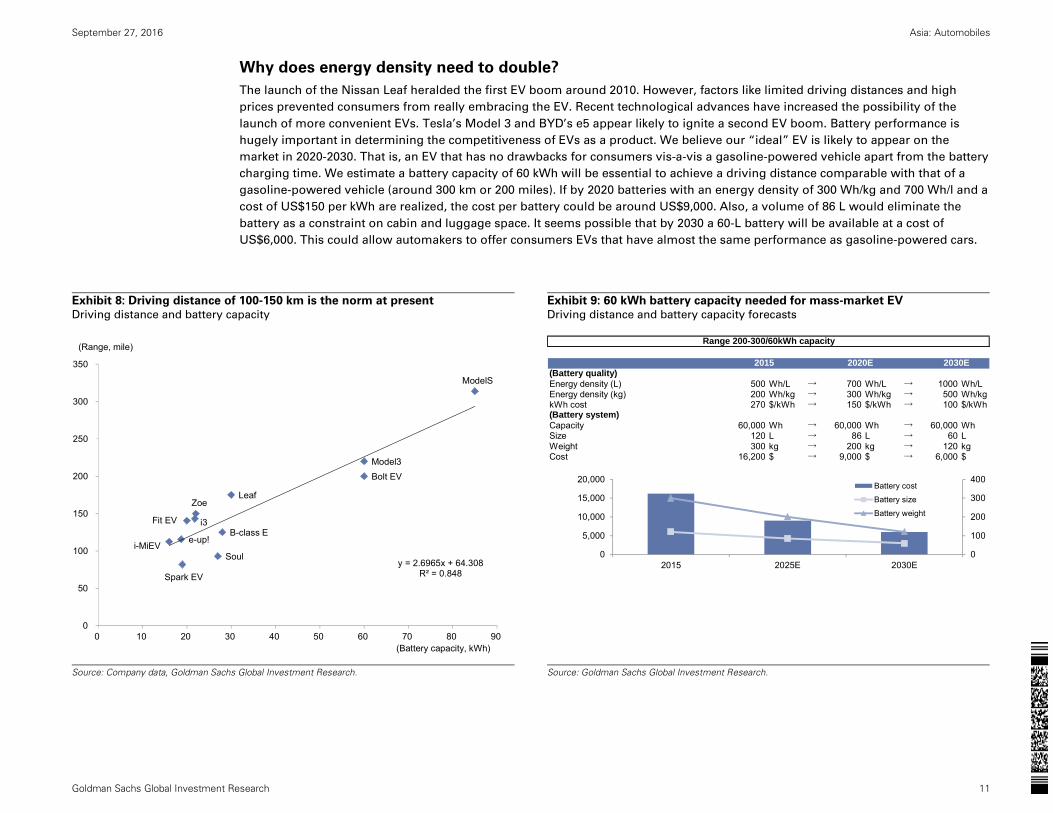

Why does energy density need to double?

The launch of the Nissan Leaf heralded the first EV boom around 2010. However, factors like limited driving distances and high

prices prevented consumers from really embracing the EV. Recent technological advances have increased the possibility of the

launch of more convenient EVs. Tesla’s Model 3 and BYD’s e5 appear likely to ignite a second EV boom. Battery performance is

hugely important in determining the competitiveness of EVs as a product. We believe our “ideal” EV is likely to appear on the

market in 2020-2030. That is, an EV that has no drawbacks for consumers vis-a-vis a gasoline-powered vehicle apart from the battery

charging time. We estimate a battery capacity of 60 kWh will be essential to achieve a driving distance comparable with that of a

gasoline-powered vehicle (around 300 km or 200 miles). If by 2020 batteries with an energy density of 300 Wh/kg and 700 Wh/l and a

cost of US$150 per kWh are realized, the cost per battery could be around US$9,000. Also, a volume of 86 L would eliminate the

battery as a constraint on cabin and luggage space. It seems possible that by 2030 a 60-L battery will be available at a cost of

US$6,000. This could allow automakers to offer consumers EVs that have almost the same performance as gasoline-powered cars.

Exhibit 8: Driving distance of 100-150 km is the norm at present

Driving distance and battery capacity

Exhibit 9: 60 kWh battery capacity needed for mass-market EV

Driving distance and battery capacity forecasts

Source: Company data, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

ModelS

Model3

Leaf

i-MiEV

Zoe

Spark EV

e-up!

i3

Soul

Fit EVB-class E

Bolt EV

y = 2.6965x + 64.308R² = 0.848

0

50

100

150

200

250

300

350

0 10 20 30 40 50 60 70 80 90

(Range, mile)

(Battery capacity, kWh)

(Battery quality) Energy density (L) 500 Wh/L → 700 Wh/L → 1000 Wh/LEnergy density (kg) 200 Wh/kg → 300 Wh/kg → 500 Wh/kgkWh cost 270 $/kWh → 150 $/kWh → 100 $/kWh(Battery system)Capacity 60,000 Wh → 60,000 Wh → 60,000 WhSize 120 L → 86 L → 60 LWeight 300 kg → 200 kg → 120 kg Cost 16,200 $ → 9,000 $ → 6,000 $

Range 200-300/60kWh capacity

2020E2015 2030E

0

100

200

300

400

0

5,000

10,000

15,000

20,000

2015 2025E 2030E

Battery cost

Battery size

Battery weight

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 12

Improving energy efficiency to expand the EV and PHEV markets over next decade

Almost two decades have passed since Toyota launched the world’s first mass-produced HV in 1997. The market for HVs had grown

to 2 mn units by 2015 and contributed significantly to improved fuel economy. Over the coming 10 years, we think EVs and PHEVs

also will demonstrate remarkable growth. We think advances in LIB technology (huge leaps in energy density) could result in an

increase in battery capacity per vehicle. We see the EV market expanding from 250,000 units in 2015 to 4.01 mn units in 2025 (CAGR

of 30%) and look for PHEV sales to rise from 400,000 units to 2.78 mn units (CAGR of 36%). Over the same period, we expect the HV

market to grow from 2.16 mn units to 13.94 mn units (CAGR of 20%).

EV market growth could lead to a six-fold increase in the automotive battery market to US$24 bn

We look for the automotive battery market to expand considerably, in tandem with growth in the EV and PHEV markets. We expect a

roughly six-fold increase in LIB demand between 2015 and 2025, from 58 GWh to 387 GWh, with demand for automotive batteries

rising from 15 GWh to 279 GWh over the same period. Thus far, mobile phones and PCs have been the main source of demand for

LIBs, but over the next decade we think rapid growth in automotive applications will bring battery operations to a major turning

point. Even allowing for an average annual decrease of about 5% in battery prices—to encourage greater uptake—we think the

market for automotive LIBs could grow sharply between 2015 and 2025, from US$4 bn to a massive US$24 bn.

Exhibit 10: We expect strong EV and PHEV demand EV and PHEV volume forecasts (K units)

Exhibit 11: Automotive battery market could grow six-fold over the next 10

years LIB market forecasts

Source: IHS, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

20%

52%

27%

35%

27%

38%

18%

22%

10%

19%

0%

10%

20%

30%

40%

50%

60%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

EV PHEV YoY

10 9 7 215 1517 9 11

3

81

302710 17

4

279

49

0

50

100

150

200

250

300

Mobile phone PC Tablet Machine tool Automotive Others

2015 2020 2025

(GWh)

2015$ 4bn

2025$ 24bn

Automotivebattery market (USD)

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 13

LIB capacity utilization is currently low; we estimate US$25bn investment by 2025

LIB makers appear to have surplus capacity. Global production capacity is 100 GWh (combined consumer electronics and

automotive battery capacity). In 2014, actual production was 45 GWh, equating to a capacity utilization of just 45%. Capacity

utilization rates at major battery makers are also around 70%. Thus, even excluding start-up battery makers in China, factories are

not particularly busy. We believe many battery makers are still not able to fully use the excess capacity built during the first EV

boom. The appetite for battery-related investment is rising, however, with an eye on 2020-2025, and we believe some major

investment announcements are likely over the next few years. Tesla’s Gigafactory is scheduled to commence operations at the end

of 2016 and aims to increase output to 50 GWh by 2020. The total investment is US$5 bn (including a US$1-2 bn investment by

Panasonic in a cell production line). Tesla has received more than 300,000 advance orders for the Model 3 (orders based on the

refundable deposit of US$1,000), and the astonishing demand prompted it to bring forward the start of Gigafactory production. Also,

in response to emission testing irregularities, Volkswagen announced it would invest to increase battery production capacity to 150

GWh by 2026. VW is revising its diesel strategy and accelerating investment in EVs and PHEVs. In China, meanwhile, with the

government offering generous subsidies for new energy vehicles (NEV), BYD and many other battery makers are announcing large

investments. Based on Tesla’s Gigafactory, 1 GWh of capacity requires capex of US$100 mn. On this basis, we calculate a total

investment of more than US$25 bn will be needed to realize battery demand of 279 GWh by 2025.

Exhibit 12: Surplus battery capacity LIB maker capacity and utilization

Exhibit 13: 1 GWh of production capacity requires investment of US$100 mn Examples of LIB factory investments

Source: Avicenne, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

5

10

15

20

25

30

35

40

45

50

Samsung LG Panasonic SONY Lishen ATL BYD Others

Production(2014)(GWh)Capacity(GWh)Operation ratio

Capacity(GWh)

CAPEX(mn$)

CAPEX/Capacity

SAFT 2008/1 0.6 150 250

LG Chem 2010/7 1.2 300 250

A123 2010/9 1.4 700 500

Loitech 2011/12 1.5 450 300

Nissan AESC 2012/12 5.0 1,000 200

BYD 2016 6.0 900 150

Tesla 2017~ 50.0 5,000 100

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 14

Up the technology curve: Next-generation LIBs, then all-solid-state batteries

Innovation for next-generation LIBs

Gravimetric energy density was just 30-50 Wh/kg when lead-acid batteries debuted in 1859, but this increased to 90-100 Wh/kg with

nickel-hydride batteries in 1990, and LIBs developed in 1991 achieved 200-250 Wh/kg while trying a variety of different materials.

Main LIB components include (1) cathode materials, (2) anode materials, (3) separators, and (4) liquid electrolytes. However, we

expect cathode materials and separators to change significantly in automotive batteries by 2020. Ternary materials (NCM) are

already the mainstream for cathode materials, but we expect the nickel ratio to rise to 80-90% from the current 30%. We also think

separators will change from dry-type separators to the wet-type separators widely used in consumer products. Each step is a

technological innovation to achieve even higher energy density.

Transition to post-LIB from 2020; all-solid-state in focus

We believe transition to post-LIBs could start from 2020 because the theoretical limits of LIBs are coming into view. We provide

further details later in this report, but think all-solid-state batteries are promising candidates for automotive batteries. All-solid-state

batteries replace liquid electrolytes with solid electrolytes to substantially increase energy density and make it easier to enhance

heat resistance and ensure safety. These batteries have properties that Toyota and other automakers regard as well-suited for

automotive batteries.

Battery and component makers also face changes

Nissan’s potential sale of its battery subsidiary Automotive Energy Supply Corporation (AESC; Nissan owns 51%, NEC owns 49%),

reported by the Nikkei on August 5, underscores the difficulty in establishing a business strategy in battery development amid rapid

technological innovation. Over the past 10-15 years, the positive electrode materials used in automobiles have evolved from iron

phosphate (mainly preferred by Chinese automakers) to manganese (used by Nissan), nickel acid (mainly Tesla), and ternary

materials (the current mainstream). With ternary materials set to become more nickel rich over 2017-18, we expect a further rise in

energy density. The accuracy of the Nikkei report is unknown, but we believe the competitiveness of the manganese materials that

Nissan has opted is gradually starting to wane. Both battery makers and component makers are struggling with the trends and pace

of technological innovation.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 15

Exhibit 14: Major changes in battery materials Technological trends for the main four components of LIBs

Source: Goldman Sachs Global Investment Research.

Exhibit 15: Many components and materials makers are Japanese and Korean at present

Market shares for four main components and materials makers (2014)

Source: Company data, Goldman Sachs Global Investment Research.

2010s 2015-2020 2025 -

Cathode

$2.5bn

Anode

0.8bn

Separator

1.15bn

Electrolyte

0.68bn

LFP, LMO, NCA NCM(Nickel rich) LiCO

Graphite Graphite/Si Graphite/LTO

Dry Wet None

EC(Ethylene Carbonate) EC/PC (Propylenecarbonate) LGPS - Solid

Cathode Anode Separator Electrolyte

Nichia, 20%

L&F Material, 15%

Umicore, 15%

Toda Industrial, 10%

Nippon Chem,

5%

Tanaka Chem,

5%

Mitsubishi Chem,

5%

Nippon Denko,

3%Others,

22%Hitachi Chem, 30%

BTR, 20%

Mitsubishi

Chem, 15%

JFE Chem, 10%

Tokai Carbon,

10%

Nippon Carbon,

5%

Showa Denko,

5%

Kureha, 3%

Others, 2%

Asahi Kasei, 30%

Toray, 20%Celgard

, 15%

SK Innovation, 10%

Ube Industries, 5%

Sumitomo

Chem, 5%

Mitsubishi

Chem, 5%

Teijin, 3%

Others, 7%

Ube Industries, 20%

Mitsubishi

Chem, 20%

Panax, 15%

Chell Industries, 15%

LG Chem, 10%

Fuji Chem, 10%

Central Glass,

8%

Others, 2%

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 16

Rapid technological changes for cathode materials, cause for reluctance in large investments

Companies are competing hard to develop cathode materials in particular because these contribute directly to raising energy

density. The competitive environment is severe, and some industry reorganization has taken place during the past year, including

Toda Kogyo selling its entire cathode material business and Sumitomo Chemical increasing investment in Tanaka Chemical. For

automotive applications, LFP (iron phosphate) is the safest and lowest priced, and is being increasingly used by Chinese makers.

Despite the drawback of low energy density, we expect localized penetration to increase its presence to 15% in 2025, from 10% in

2014. LMO (manganese-based) is not well-suited for high energy density in automotive applications, as indicated by the reported

sale of AESC. We expect its presence to decrease to 9% in 2025, from 20% in 2014. Consequently, we expect NCA (nickel acid

lithium) material (used by Tesla) to expand with the Gigafactory startup, rising in presence to 14% in 2025, from 9% in 2014. We

expect NCM (ternary) to achieve high growth on a shift to nickel-rich material. However, we expect NCM adoption to gather pace in

the Chinese market amid efforts to increase energy density, resulting in a faster shift in demand to NCM from LFP.

Exhibit 16: NCA and NCM are main cathode materials, but LFP rising in China

Cathode material mix

Exhibit 17: Cathode makers have specialty areas

Cathode material market shares by manufacturer

Source: Avicenne, Goldman Sachs Global Investment Research.

Source: Avicenne, Goldman Sachs Global Investment Research.

36%26%

25%36%

9%14%

20% 9%

10%15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2014 2025E

LFPLMONCANCMLCO

LCO:Lithium cobalt oxide. Mainlyfor consumer electronic components.

LFP: Using phosphoric acid iron. Low energy density. Adopted by Chinese battery makers and we expect high volume growth.

LMO: Using manganese. Low energy density and expecting low volume growth.

NCA: Using Lithum nickelate. Adopted by Tesla and Panasonic in their 18,650 type battery.

NCM: Ternary system battery (cobalt, nickel, manganese). Aiming to improve energy density by increasing nickel composition from current 30% to 80-90% in the future.

CY2014 LCO CY2014 LMONichia 13% JGC 16%Umicore 17% Chinese local 26%B&M 7% Nippon Denko 8%Easpring 6% ShanShan 9%Reshine 11% Reshine 8%L&F 16% Nichia 7%Other China 14% Others 26%Others 16% CY2014 LFPCY2014 NCM Internal 29%Nichia 15% Cleriant 8%Umicore 31% Aleees 10%L&F 8% STL 11%ShanShan 11% Pulead 13%Reshine 4% Zhuoneng 6%Other China 8% BTR 2%Others 23% Others 21%CY2014 NCASumitomo Metal Mining 57%Toda 14%Nihon Kagaku Sangyo 13%Ecopro 5%Others 11%

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 17

Innovations in separators

Battery separators create a barrier between the positive (anode) and negative (cathode) electrodes to prevent electrical short-circuits

between internal battery components. While ionic conductivity is essential, separators also require a porous structure with

exceptional mechanical strength. A particularly important role of the separator is the so-called shutdown function. This function will

close (fill in) the pores on multilayer separators to prevent ionic transfer if the battery temperature rises abnormally for any reason

(overheats). We estimate that the automotive separator market was worth around US$600 mn in 2015 and totaled 0.5 bn m2 on a

surface-area basis. Separator usage is typically around 15-30 m2 per kWh, so as auto batteries rapidly increase to 279 GWh in 2025E

from 15 GWh in 2015, we expect the separator market to rapidly grow to 7 bn m2. Over the longer term, however, there is risk of the

market shrinking as separators would become unnecessary if all solid-state batteries emerge as the successor to lithium ion

batteries. Among major battery makers, Asahi Kasei has a global separator share of 30%, Celgard 15%, Toray Industries 20%, and

Sumitomo Chemical 5%.

Wet type separators may become a mainstream for auto

Separators come in two types: wet separators and dry separators. Wet separators have become the most widely used type in

consumer electronics applications, but dry separators remain the mainstream in automotive applications. Wet separators have the

advantage of being stronger than dry separators, which means they can be thinner. The main obstacle to the broader adoption of

EVs and PHEVs is range, and increasing the energy density of batteries has become a pressing issue. Dry separators generally

comprise three layers of polypropylene/polyethylene, but wet separators can be made using a single layer, which in theory means

thickness of just 6-7 microns is possible (compared with 16 microns for a dry separator). The disadvantages of wet separators are a

more expensive manufacturing process and greater difficulty in ensuring safety. Wet separator manufacturing production costs are

structurally higher because additional facilities are needed due to the use of solvents. That said, the price differential versus dry

separators has now shrunk to around 10%-20%, thanks to the increasing size of production lines and volume efficiencies. On the

safety front, there are issues associated with the use of high-nickel cathode materials. However, technology has now been

developed to increase heat resistance by adding a special ceramic coating to wet separators, and we expect to see an increase in the

number of manufacturers using wet separators for automotive applications.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 18

Exhibit 18: Separator market is growing rapidly Separator demand by total surface area (1,000m2) and market scale (¥ mn)

Exhibit 19: We see greater uptake of wet type separators Estimated demand for wet and dry type separators for automotive application

(1,000m2)

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Cutting costs while improving energy density

We would expect higher energy density to reduce battery costs. As of 2015, we estimate cell costs at US$250 per kWh, pack costs at

US$140, and total costs at US$390. By 2025, however, we think costs could be reduced to US$164 for cells, US$25 for packs, and

US$189 overall. We expect the four main components noted above to see annual cost reductions of 3-5%, and also expect decreases

in R&D costs and depreciation based on mass production benefits. Packs have a high ratio of fixed costs, making them likely to

benefit from mass production. At present, Tesla has the most aggressive outlook for battery price declines, and seeks to reduce total

costs to US$100 by 2020. Our estimate is generally near the market consensus, and we expect no fundamental cost breakthrough

until the mass production of all-solid-state batteries.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Auto

Non-auto

Market size

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Wt Dry

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 19

Exhibit 20: We expect battery unit prices to decrease by half…

LIB cost breakdown (US$)

Exhibit 21: …with Tesla having the most optimistic cost outlook kWh unit price outlook (US$)

Source: Avicenne, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

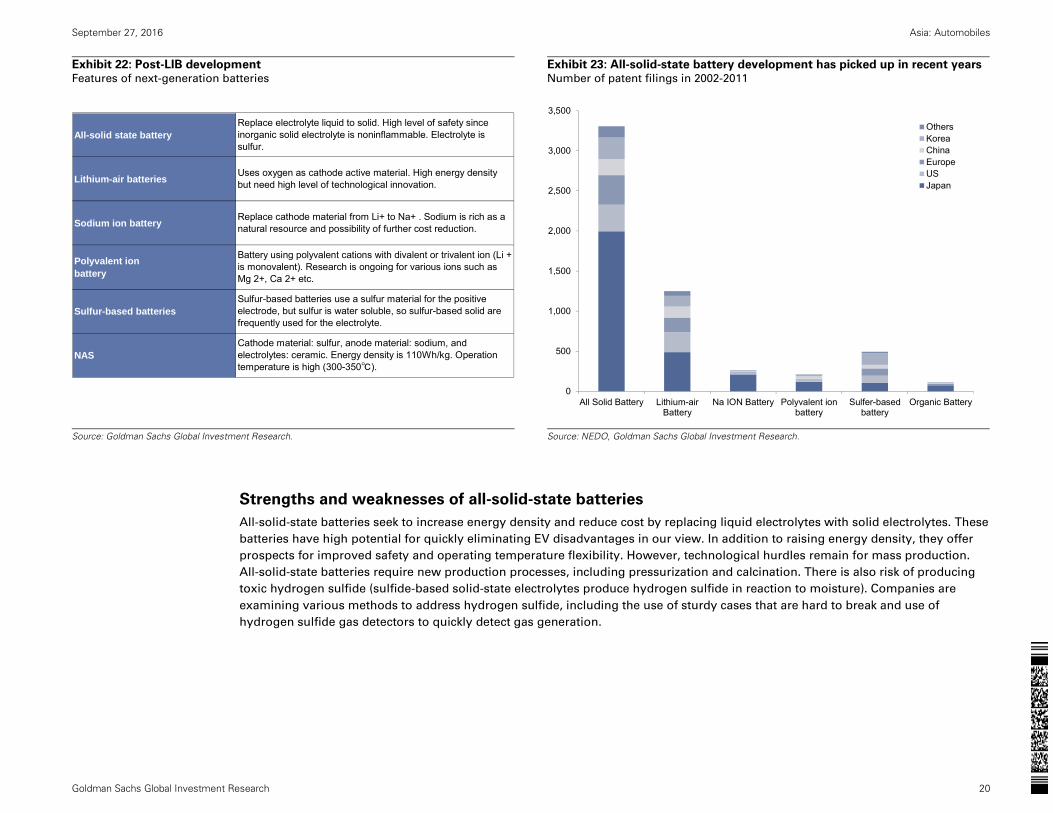

Search for suitable post-LIB technology: All-solid-state batteries in the lead

Post-LIB development competition is growing more severe as LIBs approach their theoretical limits. All-solid-state battery

technology has advanced noticeably in the past 5-10 years amid intensifying development competition with lithium-air batteries,

multivalent ion batteries, and sulfur-based batteries. More than 3,000 patents for all-solid-state batteries were filed in 2002-2011, far

higher than other post-LIB technologies. Toyota/Tokyo Institute of Technology, Hitachi Zosen, Ohara, and other companies have

announced technological innovations for all-solid-state batteries in 2016.

0

50

100

150

200

250

300

350

400

450

2015 2020E 2025E

Pack costCathodeAnodeElectrolyteSeparatorOthersDepreciationDirect laborEnergyR&DSales&AdmMargin

0

50

100

150

200

250

300

350

400

450

2015 2016E 2017E 2018E 2019E 2020E

High estimate Low estimate (Tesla)

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 20

Exhibit 22: Post-LIB development Features of next-generation batteries

Exhibit 23: All-solid-state battery development has picked up in recent years Number of patent filings in 2002-2011

Source: Goldman Sachs Global Investment Research.

Source: NEDO, Goldman Sachs Global Investment Research.

Strengths and weaknesses of all-solid-state batteries

All-solid-state batteries seek to increase energy density and reduce cost by replacing liquid electrolytes with solid electrolytes. These

batteries have high potential for quickly eliminating EV disadvantages in our view. In addition to raising energy density, they offer

prospects for improved safety and operating temperature flexibility. However, technological hurdles remain for mass production.

All-solid-state batteries require new production processes, including pressurization and calcination. There is also risk of producing

toxic hydrogen sulfide (sulfide-based solid-state electrolytes produce hydrogen sulfide in reaction to moisture). Companies are

examining various methods to address hydrogen sulfide, including the use of sturdy cases that are hard to break and use of

hydrogen sulfide gas detectors to quickly detect gas generation.

All-solid state battery

Lithium-air batteries

Sodium ion battery

Polyvalent ionbattery

Sulfur-based batteries

NAS

Battery using polyvalent cations with divalent or trivalent ion (Li +is monovalent). Research is ongoing for various ions such asMg 2+, Ca 2+ etc.

Replace electrolyte liquid to solid. High level of safety sinceinorganic solid electrolyte is noninflammable. Electrolyte issulfur.

Cathode material: sulfur, anode material: sodium, andelectrolytes: ceramic. Energy density is 110Wh/kg. Operationtemperature is high (300-350℃).

Uses oxygen as cathode active material. High energy densitybut need high level of technological innovation.

Replace cathode material from Li+ to Na+ . Sodium is rich as anatural resource and possibility of further cost reduction.

Sulfur-based batteries use a sulfur material for the positiveelectrode, but sulfur is water soluble, so sulfur-based solid arefrequently used for the electrolyte.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

All Solid Battery Lithium-airBattery

Na ION Battery Polyvalent ionbattery

Sulfer-basedbattery

Organic Battery

OthersKoreaChinaEuropeUSJapan

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 21

Exhibit 24: All-solid-state batteries feature greater energy density and safety; need to overcome mass production challenges Advantages and disadvantages of all-solid-state batteries

Source: Goldman Sachs Global Investment Research.

Exhibit 25: LIB using liquid electrolyte between cathode and anode LIB diagram

Exhibit 26: All-solid-state battery using solid electrolytes rather than liquid

electrolytes All-solid-state battery diagram

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

Merits

SafeWide range of operating temp. High energy densityHigh volume energy densityDemerits

Low productivityLow power densityUnknown accidents

→ Conductivity of solid electrolyte is not very high.→ Some research warn against a generation of hydrogen sulfide.

→ Less risk of fire due to no liquid electrolyte.→ Especially in low temperature.→ It is possible by using sulfur for electrode material.→ Easy to form a layered structure.

→ Need pressurization or calcination to form a solid electrolyte.

Negative current collector Positive current collector

Separator

Lithium ion battery

Li+

Li-

Li-

Li-

Li-

Li-

Li+

Li+Li+

Li+

Li+

Anode CathodeLiquid

Negative current collector Positive current collector

All-solid-state battery

Li+

Li-

Li-

Li-

Li-

Li-

Li+

Li+Li+

Li+

Li+

Anode CathodeSolid

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 22

Multiple players in all-solid-state battery development

Toyota, Sekisui Chemical, and Hitachi Zosen are targeting mass production of all-solid-state batteries in 2020-2025. Samsung Elec.,

Daimler, and Sony have also announced R&D initiatives, but their mass production timeframes are unknown. BYD has launched a

special team and is conducting research into all-solid-state batteries. Leading auto parts maker Bosch acquired the all-solid-state

battery venture company Seeo. Consumer electronics maker Dyson also entered the battery business by acquiring Skit3. We think

expectations are rising for using all-solid-state batteries not only for automotive applications, but for consumer products as well.

All-solid-state battery production processes differ greatly from current LIBs

The production of all-solid-state batteries can be broadly separated into three main methods. (1) Hitachi Zosen and Toyota use a

powder pressing process that applies pressure to sulfide-based solid electrolytes and the cathode/anode. This method increases

ionic conductivity by making the contact state more adhesive through component interface movement. Ensuring ionic conductivity

within the solid state is the primary hurdle for replacing liquid electrolytes with solid electrolytes. (2) Bosch and Sekisui Chemical

are developing a coating-based process that performs roll-to-roll layering. Electrolytic materials often use semi-solid materials. (3)

Dyson and Applied Materials are developing a semiconductor process, but expansion to high-capacity automotive batteries is

difficult. We would expect this to be used mainly for consumer products.

Exhibit 27: Growing interest in all-solid-state batteries for both automobiles and consumer products

Leading manufacturers and technological features

Source: Nikkei Elec, Goldman Sachs Global Investment Research.

Powder and pressure Coating Semiconductor

Mass production Hitachi Zosen established a massproduction method.

Mass production is possible by roll-to-rollprocess. Under development

Energy densityHigh value from the research done byHigh Tokyo University and TokyoInstitute of Technology.

Average High theoretical value but unsuitable formass production.

Power densityHigh value from the the research doneby High Tokyo University and TokyoInstitute of Technology.

Average Challenge is how to make a separatorthinner.

Safety Risk: generation of hydrogen sulfidefrom sulfide-based electrolyte.

Sekisui Chemical is confident in thesafety of the battery. High level of safety

Toyota Sekisui Chemical (acquired Enax) Dyson (acquired Sakit3)Hitachi Zosen Bosch (acquired Seeo) Applied MaterialsSamsung Zeptor

Battery makers

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 23

Exhibit 28: All-solid-state batteries use special pressing process Comparison of production processes for all-solid-state batteries and LIBs

All-solid-state battery production process

LIB production process

Source: Goldman Sachs Global Investment Research.

Anode

Cathode

Separator

Coating Insert electrolyteLaminateDry

Liquid Electrolyte

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 24

Case study: Samsung’s exploding mobile phone batteries

1) What is happening inside the batteries?

At a press briefing on September 2, 2016, Samsung Electronics (SEC) announced that it will recall all Galaxy Note 7 (Note 7) that have been shipped, around 2.5mn units globally. SEC indicated that the problem stems from issues with the battery cell, while it declined to mention the supplier of the batteries that caused these problems. SEC explained that it mainly uses batteries from two different suppliers, and that an error in the manufacturing process at one supplier caused the cathode and anode of the battery to contact each other which resulted in the battery exploding.

2) Automotive batteries differ from consumer electronics ones, but further safety measures are inevitable

In the case of Note 7 explosion, the battery used is polymer-type while Samsung SDI supplies can-type for EV batteries. So they are different types of batteries, but the risk here is that there could be reputational risk as OEMs will be reluctant to use battery produced by a company that has seen problems even if that was for another application. Another potential implication is increase in entry barriers for EV battery suppliers given OEMs will likely raise safety measures for batteries.

3) Learning from past incidents of battery overheating

There have been several incidences of LIBs overheating in addition to the recent cases involving Samsung. We think there are generally two causes for such overheating (exact cause still unclear for Samsung). The first is a problem with the separator between the positive and negative electrodes. The battery’s safety becomes compromised if the separator is not strong enough or it is damaged by the presence of foreign materials. The second is the possibility of a problem in the battery pack. The battery includes a mechanism (known as a battery management system) that acts as a block when there is a large outflow of electric current. If this battery management system does not function properly for some reason, then it can become impossible to control a thermal runaway in the battery.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 25

EV and PHEV penetration set to accelerate through 2025E

PHEVs could take off by 2020, followed by EVs thereafter

We forecast vehicles with an electric powertrain system will account for 25% of global auto sales in 2025, up from 5% in 2015. While

we expect hybrids to be the main type of electrified vehicle, electrification is gaining traction, driven by the aggressive adoption of

car purchase subsidies in Europe and China. In California and nine other US states, electrification is likely to accelerate from 2018,

spurred by zero-emission vehicle (ZEV) regulations (requiring the sale of a certain volume of PHEVs, EVs, and FCVs, according to

annual sales volume). We forecast global demand for EVs and PHEVs combined will increase sharply to 6.8 mn vehicles in 2025,

from 650,000 vehicles in 2015. In our view, PHEVs will lead the way through 2020 due to battery performance constraints, with the

EV market entering a sharp expansionary phase from 2020.

Even stricter CO2 environmental regulations, moves toward RDE

Fuel economy standards could tighten intermittently between 2020 and 2025, mainly in the US and Europe. The US corporate

average fuel economy (CAFE) target of 54.5 mpg for the 2025 model year and the possible European CO2 emission targets of 95

g/km by 2020 and of 72 g/km by 2025 (not officially decided yet) represent very challenging hurdles for automakers. China has

decided to tighten fuel efficiency standards in response to increasing environmental problems, a heavy reliance on overseas energy

(already more than 50%), and urban traffic congestion. We expect the VW emissions scandal that surfaced in October 2015 to have a

significant impact on emission/fuel economy regulations. In Europe, discussions are progressing ahead of the adoption of Euro 6c

emission standards in 2017, and automakers will need to pay increased attention to the difference between real-world and test-

mode fuel economy.

CO2 emissions: The Euro 6c CO2 emission measurements use the Worldwide harmonized Light vehicles Test Procedures (WLTP),

the unified testing mode for Japan, the US, and Europe. The difference between test-mode and real-world fuel economy is

calculated by comparing real driving emissions (RDE) conditions with WLTP results. New models tested from September 2017 will

need to conform to a permitted difference of 2.1x or less between RDE fuel economy and certified (catalog) fuel economy.

Discussions are also under way on narrowing this difference to 1.5x.

NOx and PN standards: The New European Driving Cycle (NEDC) is currently used to assess emission levels, but under Euro 6C

RDE tests will be adopted as the uniform testing method in Europe. RDE test procedure details are currently under discussion, with

technical adjustments being made to testing environments (test course, latitude, altitude, etc.).

ZEV regulations prompting action; hybrid vehicles to be excluded from ZEV category from 2018

Automakers are rushing to launch EVs and PHEVs in part because of the ZEV regulations announced by the state of California, US.

Major automakers need to generate ZEV credits equivalent to 4.5% of the vehicles they sell in California from 2018, but hybrid

vehicles will no longer be included in the ZEV category. Mid-tier automakers must also generate ZEV credits, like major automakers,

five years later, from 2023. As such, we think electrification is inevitable even at Mazda Motor and Fuji Heavy Industries.

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 26

Exhibit 29: Electrification set to continue Demand estimates by powertrain

Exhibit 30: CO2 emissions need to be cut by over 20% Reductions called for in CO2 emission standards in major countries

Source: IHS, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research

EVs becoming a reasonable solution

Automakers need to move forward with electrification at some point in order to meet stricter standards. Establishing EV business

models is a matter of urgency for all automakers. EVs and PHEVs do not differ significantly in terms of well-to-wheels CO2

emissions, with both being around 60-80 g/km (these figures naturally change depending on the method of electric power

generation). On the cost side, however, the more battery prices decline, the more likely that an EV business model may make sense.

We estimate that with PHEVs the additional cost of reducing CO2 emissions by 1 gram is US$139 and that with EVs the cost of a 1-

gram reduction is nearly the same, at US$124, based on 2015 per-kWh battery prices. A drop in per-kWh battery prices to around

US$100, however, would bring the cost of a 1-gram reduction down to US$31, which would make EVs an inexpensive CO2 reduction

solution, rivaling auto lightweighting and downsizing turbo engines. From automakers’ perspective, we see grounds to continue

investing heavily in EVs through 2030.

0

20,000

40,000

60,000

80,000

100,000

120,00020

12

2013

2014

2015

2016

E

2017

E

2018

E

2019

E

2020

E

2021

E

2022

E

2023

E

2024

E

2025

E

FCV

EV

PHEV

HV

Internal combustion engines

Using ICE96%

Using battery20%

Using fuel cell0.5%

(K units)

153 156

120

165

89

116

72

118

0

20

40

60

80

100

120

140

160

180

200

US CAFE Japan Europe China

2014

2025E

(g/km)

-42% -26%

-40%

-28%

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 27

Exhibit 31: EV and PHEV CO2 emissions do not differ significantly on a well-

to-wheels basis

CO2 emissions by powertrain (g/km)

Exhibit 32: EVs could become an inexpensive CO2 emissions reduction

solution in 2030

Estimated additional cost of a 1-gram reduction in CO2 emissions (US$)

Source: NEDO.

Source: Goldman Sachs Global Investment Research.

Price and driving range are the keys to EV penetration

The high price of EVs is the main obstacle to their penetration, as reflected in price concerns being cited by 50% of consumers who

participated in a 2016 Ministry of Economy, Trade and Industry survey in Japan. The next largest issues are driving range (cited by

13%) and a lack of charging facilities at home (10%). Improvements in energy density should dispel at least two of consumers’ major

concerns. Around 53% of the respondents said they would be satisfied with a driving range of 300 km/200 miles, and 80% said that

given a driving range of 500 km/300 miles, this factor would not be an obstacle to buying an EV. This is why we see 60 kWh as the

ideal battery capacity for EVs.

21.1

40.1

67.4

0 20 40 60 80 100 120 140 160

GasolineVehicle

PHEV

EV Well to TankTank to Wheel

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 28

Exhibit 33: Price is the main issue with EVs, followed by driving range Impediments to buying an EV (2016 survey)

Exhibit 34: Around 50% of consumers would be satisfied with a driving range

of 300 km

EV driving range survey, 2016

Source: METI.

Source:METI.

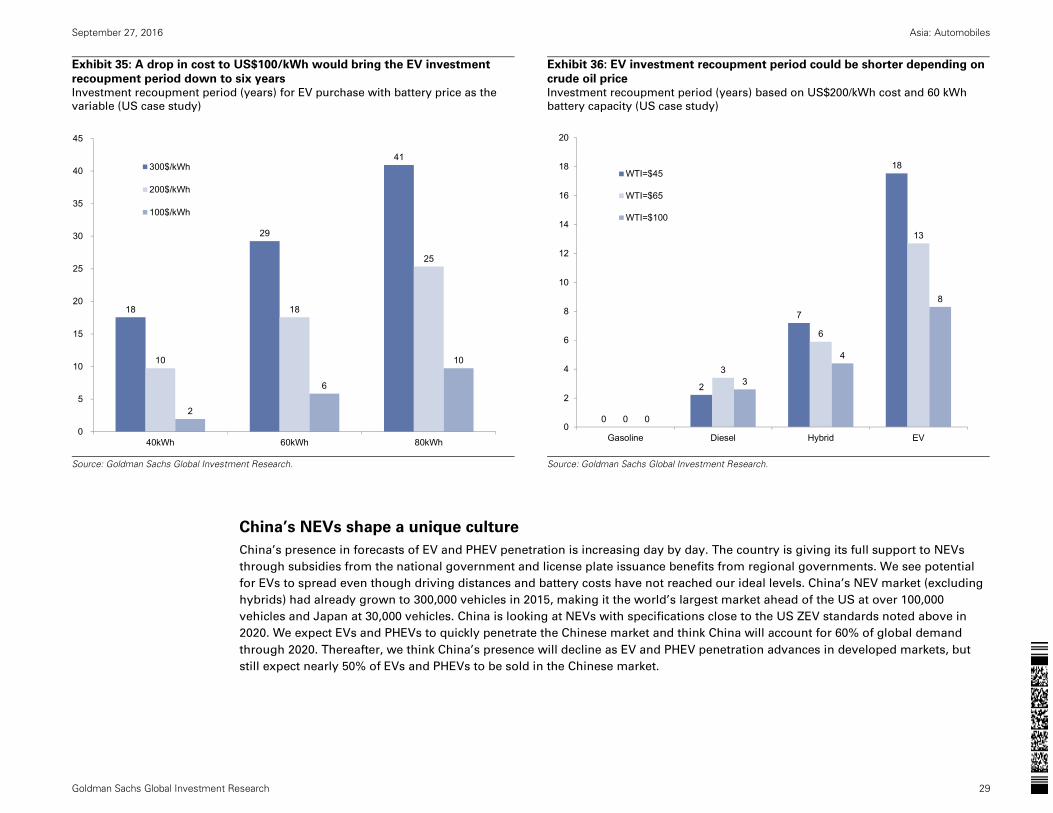

Investment recoupment period growing shorter every year

With price being the greatest concern when considering purchase of an EV, we see US$100 per kWh as a reasonable battery cost

target, based on lifecycle cost for the entire ownership period. Based on battery capacity of 60 kWh, car owners would recoup the

higher cost of purchasing an EV in six years. If we additionally factor in a rise in crude oil prices, the recoupment period would be

significantly reduced even if we assume a battery cost of US$200 per kWh in 2020. Assuming a WTI price of US$100/bbl, the

recoupment period for EVs would be eight years in 2020. We estimate that the recoupment period in the first half of 2000s was

around five years, and that this drove the sharp growth in hybrid cars then.

0% 10% 20% 30% 40% 50% 60%

Expensive

Short running distance

No EV charging facility at home

Few EV charging station

Spending long time for charging

Worse automobile performance

Not attractive

16% 15% 18% 20%

28% 26%27% 27%

44%41%

40% 36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015

80km160km320km480km640km

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 29

Exhibit 35: A drop in cost to US$100/kWh would bring the EV investment

recoupment period down to six years Investment recoupment period (years) for EV purchase with battery price as the

variable (US case study)

Exhibit 36: EV investment recoupment period could be shorter depending on

crude oil price Investment recoupment period (years) based on US$200/kWh cost and 60 kWh

battery capacity (US case study)

Source: Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

China’s NEVs shape a unique culture

China’s presence in forecasts of EV and PHEV penetration is increasing day by day. The country is giving its full support to NEVs

through subsidies from the national government and license plate issuance benefits from regional governments. We see potential

for EVs to spread even though driving distances and battery costs have not reached our ideal levels. China’s NEV market (excluding

hybrids) had already grown to 300,000 vehicles in 2015, making it the world’s largest market ahead of the US at over 100,000

vehicles and Japan at 30,000 vehicles. China is looking at NEVs with specifications close to the US ZEV standards noted above in

2020. We expect EVs and PHEVs to quickly penetrate the Chinese market and think China will account for 60% of global demand

through 2020. Thereafter, we think China’s presence will decline as EV and PHEV penetration advances in developed markets, but

still expect nearly 50% of EVs and PHEVs to be sold in the Chinese market.

18

29

41

10

18

25

2

6

10

0

5

10

15

20

25

30

35

40

45

40kWh 60kWh 80kWh

300$/kWh

200$/kWh

100$/kWh

0

2

7

18

0

3

6

13

0

3

4

8

0

2

4

6

8

10

12

14

16

18

20

Gasoline Diesel Hybrid EV

WTI=$45

WTI=$65

WTI=$100

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 30

Exhibit 37: China is already the world’s largest NEV market HV, PHEV, and EV sales in Japan, US, and China (Thous.)

Exhibit 38: Expect China to account for majority of global NEVs in 2020 China’s NEV market outlook (excluding commercial vehicles, K units)

Source: CAAM, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

NEVs are supported by robust subsidies

NEV policies have been established with robust support from the Chinese government. China relies on overseas supplies for over

60% of its crude oil, making NEV policies increasingly important from the standpoint of energy security. Our China analyst Yipeng

Yang estimates that the NEV business of BYD, which sells the most NEVs in China, had an operating margin above 15% in 2015.

However, excluding subsidies, it may have had a negative operating margin in excess of 10% in real terms (this real profit margin is

roughly equal to Tesla). Automakers involved in NEVs in China have been able to save cash for reinvestment amid the worst period

for earnings due to business startup. However, the government has indicated that it intends to eliminate NEV purchase subsidies

from 2020. It will likely no longer be possible for all NEV makers to reap excess returns on an ongoing basis. We expect both Tesla

and BYD to achieve positive operating profits in real terms in 2018-2019 on lower battery costs and mass production benefits.

45

247

77 7617 17

30

84

48 53

13 13

189 209

857

1,013

0

200

400

600

800

1,000

1,200

CY2014 CY2015 CY2014 CY2015 FY2013 FY2014

HEVPHEVEV

China US Japan0%

10%

20%

30%

40%

50%

60%

70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

EV

PHEV

EV/China

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 31

Exhibit 39: Top NEV makers have double-digit (%) op. margins after subsidiesComparison of margins at BYD and Tesla

Exhibit 40: China plans to annually reduce NEV purchase subsidies Overview of subsidies (Thous. RMB, R:ranges)

Note: Comparable OPM excludes subsidies.

Source: Company data, Goldman Sachs Global Investment Research.

Source: CAAM, Goldman Sachs Global Investment Research.

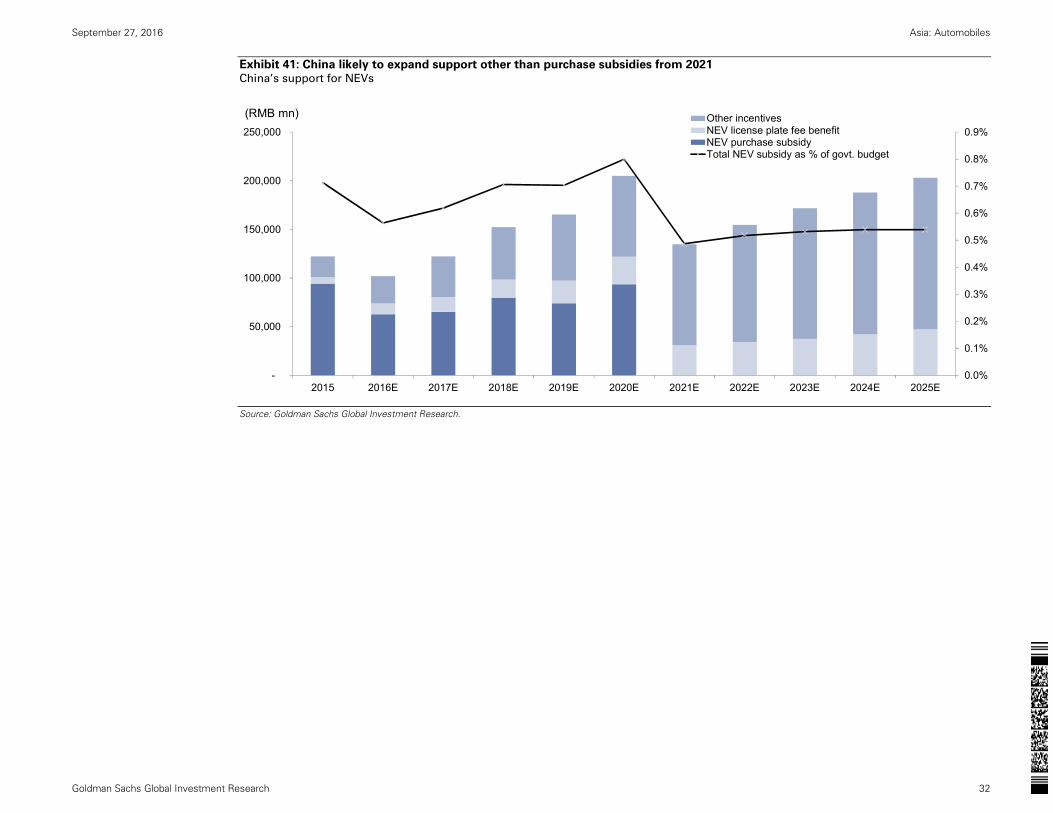

China to reduce purchase subsidies, but lays groundwork for NEVs to expand

Even if China eliminates NEV purchase subsidies in 2020, we believe it will still have policies to support NEV penetration. In

particular, many more cities are considering the adoption of license plate issuance regulations in response to more severe air

pollution and traffic congestion. Special measures for NEVs that are unique to China, such as the preferential issuance of license

plates and absence of travel restrictions, could support EV and PHEV penetration from 2020. We expect the government’s NEV-

related costs to stabilize at around 0.5% of national expenditures from 2020 vs. around 0.7% in 2015.

-4.0%

9.6%

16.5%

12.6%

-11.1%

8.8%

-12.6%

6.3%

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

2015 2016E 2017E 2018E 2019E 2020E

BYD-NEV OPM

Tesla OPM

BYD-NEV comparable OPM

Tesla comparable OPM

0

10

20

30

40

50

60

70

2013 2014 2015 2016E 2017E 2018E 2019E 2020E

EV 80≤R<150 (100≤R<150 from 2016)EVEV 150≤R<250EV R≥250PHEV R≥50

(K Rmb)

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 32

Exhibit 41: China likely to expand support other than purchase subsidies from 2021 China’s support for NEVs

Source: Goldman Sachs Global Investment Research.

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

0.8%

0.9%

-

50,000

100,000

150,000

200,000

250,000

2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E 2024E 2025E

Other incentivesNEV license plate fee benefitNEV purchase subsidyTotal NEV subsidy as % of govt. budget

(RMB mn)

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 33

Stocks in focus

Stocks in focus

September 27, 2016 Asia: Automobiles

Goldman Sachs Global Investment Research 34

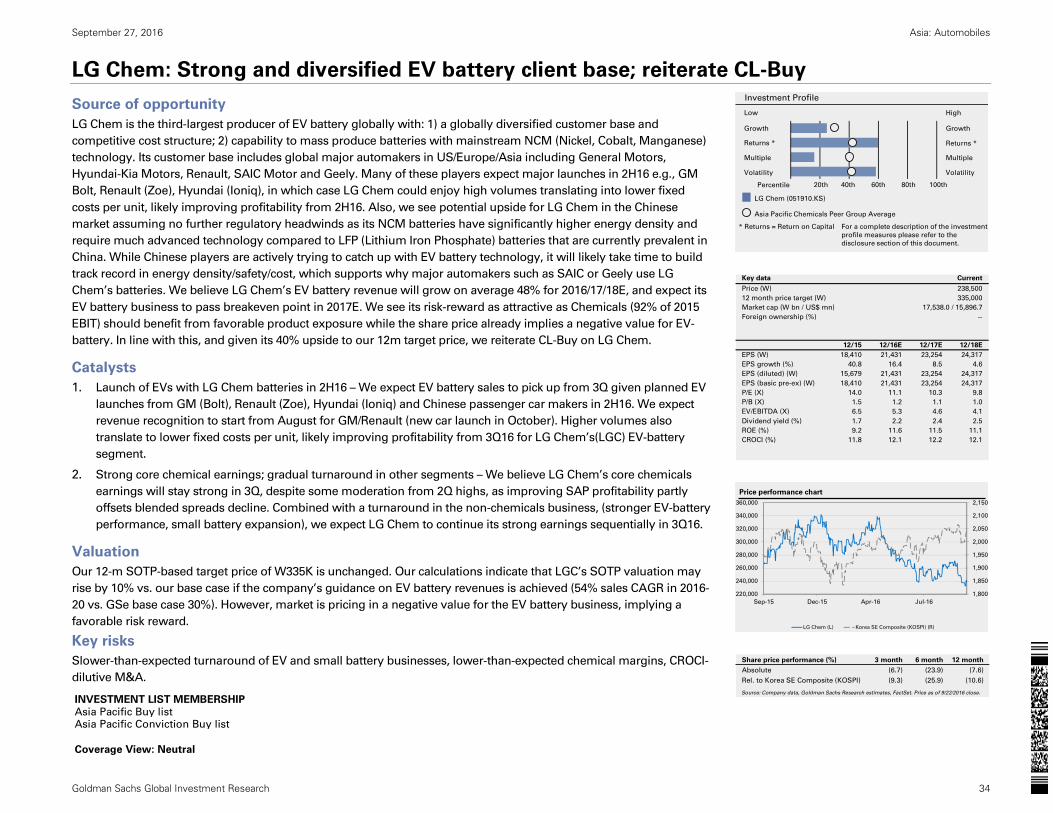

LG Chem: Strong and diversified EV battery client base; reiterate CL-Buy

Source of opportunity

LG Chem is the third-largest producer of EV battery globally with: 1) a globally diversified customer base and

competitive cost structure; 2) capability to mass produce batteries with mainstream NCM (Nickel, Cobalt, Manganese)

technology. Its customer base includes global major automakers in US/Europe/Asia including General Motors,

Hyundai-Kia Motors, Renault, SAIC Motor and Geely. Many of these players expect major launches in 2H16 e.g., GM

Bolt, Renault (Zoe), Hyundai (Ioniq), in which case LG Chem could enjoy high volumes translating into lower fixed

costs per unit, likely improving profitability from 2H16. Also, we see potential upside for LG Chem in the Chinese

market assuming no further regulatory headwinds as its NCM batteries have significantly higher energy density and

require much advanced technology compared to LFP (Lithium Iron Phosphate) batteries that are currently prevalent in

China. While Chinese players are actively trying to catch up with EV battery technology, it will likely take time to build

track record in energy density/safety/cost, which supports why major automakers such as SAIC or Geely use LG

Chem’s batteries. We believe LG Chem’s EV battery revenue will grow on average 48% for 2016/17/18E, and expect its

EV battery business to pass breakeven point in 2017E. We see its risk-reward as attractive as Chemicals (92% of 2015

EBIT) should benefit from favorable product exposure while the share price already implies a negative value for EV-

battery. In line with this, and given its 40% upside to our 12m target price, we reiterate CL-Buy on LG Chem.

Catalysts

1. Launch of EVs with LG Chem batteries in 2H16 – We expect EV battery sales to pick up from 3Q given planned EV

launches from GM (Bolt), Renault (Zoe), Hyundai (Ioniq) and Chinese passenger car makers in 2H16. We expect

revenue recognition to start from August for GM/Renault (new car launch in October). Higher volumes also

translate to lower fixed costs per unit, likely improving profitability from 3Q16 for LG Chem’s(LGC) EV-battery

segment.

2. Strong core chemical earnings; gradual turnaround in other segments – We believe LG Chem’s core chemicals

earnings will stay strong in 3Q, despite some moderation from 2Q highs, as improving SAP profitability partly

offsets blended spreads decline. Combined with a turnaround in the non-chemicals business, (stronger EV-battery

performance, small battery expansion), we expect LG Chem to continue its strong earnings sequentially in 3Q16.

Valuation

Our 12-m SOTP-based target price of W335K is unchanged. Our calculations indicate that LGC’s SOTP valuation may

rise by 10% vs. our base case if the company’s guidance on EV battery revenues is achieved (54% sales CAGR in 2016-

20 vs. GSe base case 30%). However, market is pricing in a negative value for the EV battery business, implying a

favorable risk reward.

Key risks

Slower-than-expected turnaround of EV and small battery businesses, lower-than-expected chemical margins, CROCI-

dilutive M&A.

INVESTMENT LIST MEMBERSHIP

Asia Pacific Buy listAsia Pacific Conviction Buy list

Coverage View: Neutral

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

LG Chem (051910.KS)

Asia Pacific Chemicals Peer Group Average

Key data Current

Price (W) 238,500

12 month price target (W) 335,000

Market cap (W bn / US$ mn) 17,538.0 / 15,896.7

Foreign ownership (%) --

12/15 12/16E 12/17E 12/18E

EPS (W) 18,410 21,431 23,254 24,317