auditor’s independency and responsibility: expectation gap …

TRANSCRIPT

AUDITOR’S INDEPENDENCY AND RESPONSIBILITY:

EXPECTATION GAP BETWEEN AUDITOR AND USER’S

PERCEPTION (CASE STUDY IN RSM INDONESIA)

SKRIPSI

By

Nopita Aulia Siregar

008201200137

Presented to the

Faculty of Business, President University

In partial fulfillment of the requirements

for

Bachelor Degree in Business, Major in Accounting

PRESIDENT UNIVERSITY

Cikarang Baru – Bekasi

Indonesia

2016

ii | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

PANEL OF EXAMINERS APPROVAL SHEET

Herewith, the Panel of Examiners declares that the skripsi entitled

“AUDITOR’S INDEPENDENCY AND RESPONSIBILITY:

EXPECTATION GAP BETWEEN AUDITOR AND USER’S

PERCEPTION (CASE STUDY IN RSM INDONESIA)” submitted by

Nopita Aulia Siregar, Accounting Study Program, Faculty of Business, has

been assessed and proved to pass the Oral Examination on 2nd

March 2016.

Chair, Panel of Examiner,

Monika Kussetya Ciptani M.Ak

Examiner 1

Dr. Sumarno Zain, SE, Ak., MBA

Examiner 2

Misbahul Munir, Ak., MBA, CPMA, CA

iii | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

RECOMMENDATION LETTER OF SKRIPSI ADVISOR

The thesis prepared and submitted by

Name : Nopita Aulia Siregar

Student ID : 008201200137

Faculty : Business

Study Program : Accounting

Skripsi Title : Auditor’s Independency and Responsibility: Expectation

Gap between Auditor and User’s Perception (Case Study in RSM

Indonesia)

Has been reviewed and found to have satisfied the necessities for Oral Defense as partial

fulfillment of the requirements for Bachelor Degree in Economics – Major in Accounting.

Cikarang, Indonesia, 25th

January 2016

Acknowledge, Skripsi Advisor,

Misbahul Munir, Ak., MBA, CPMA, CA Dr.Sumarno Zain, SE, Ak., MBA

Head of Accounting Study Program Skripsi Advisor

iv | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

DECLARATION OF ORIGINALITY

I hereby declare that the skripsi entitled “AUDITOR’S INDEPENDENCY AND

RESPONSIBILITY: EXPECTATION GAP BETWEEN AUDITOR AND USER’S

PERCEPTION (CASE STUDY IN RSM INDONESIA)” is originally written by

myself based on my own research and has never been used for any other purpose before.

I, therefore, request for Oral Defense of the skripsi.

Cikarang, Indonesia, 25th

January 2016

Author,

Nopita Aulia Siregar

008201200137

v | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

AUDITOR’S INDEPENDENCY AND RESPONSIBILITY:

EXPECTATION GAP BETWEEN AUDITOR AND USER’S

PERCEPTION (CASE STUDY IN RSM INDONESIA)

ABSTRACT

The purpose of this study was to determine whether the audit expectation gap

between auditors and user in RSM Indonesia did exist. In some ways, public and other

users of the financial statements expect of the auditor is not necessarily the same as the

law requires of him, or that which is realistically possible. The independent and

responsibility factor is the foundation of the public accounting profession.

Author has performed a qualitative study consisting of interviews with

representatives from auditor and user. The conclusions are based on the interviewees’

personal opinion, observation and based on literature review. However author believe

author have discovered certain important negative tendencies

The author comes to the conclusion that this kind of gap did exist between auditor

and user. Their different perceptions about responsibility and independency of auditor are

the key element of expectation gap in this research. The result shows that the expectation

gap did exist because of different concept from auditor ad user’s perceptions. Other

causes of expectation gap are misunderstanding from client about independency and

responsibility and lack of implementation in independency from client. The expectation

gap should be reduced by the auditor by improving audit responsibilities, educating

various users, and mandating new standards and the user by reducing the expectation and

increasing knowledge about auditing. Due to these causes auditors are not able to produce

a fair report. Therefore the auditor and user should understand each other’s responsibility

and independency.

Keywords: Auditors’ Responsibility, Auditors’ Independence and Expectation Gap

vi | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

ACKNOWLEDGMENT

First and foremost, I would like to thank to Allah S.W.T, for blessing me and

guide me so that I am able to accomplish this thesis entitled “Auditor’s Independency and

Responsibility: Expectation Gap between Auditor and User’s Perception” appropriately. It

would not have been possible to write this thesis without the help and support of around

me. I would like to deliver and express my highly appreciation to these people whose

contribution in assorted ways and gave me the possibility to complete this thesis.

1. To my beloved parents, M. Ridwan Siregar and Nur Mega Afni Pohan. Thank you

for your love, encouragement, moral support and faith in me and their endless

supports that made me possible to finish this study. To my beloved brothers and

sister, Viky Hari Chandra Siregar, Riky Afrizal Siregar and Yosi Hadijah Siregar

thank you for the contribution, endless support, and happiness.

2. My sincere thanks to Mr. Febrial Pratama as my thesis advisor who has given his

valuable time, knowledge, patience, guidance, encouragement, and correction from

the beginning up to the end of this thesis. I’m blessed to have the opportunity to

have an inspiring advisor and it’s an honor to do the research under his supervision.

3. My sincere thanks to Mr. Joseph Ginting for the guidance and give me the

opportunity to do the research under Mr. Febrial Pratama supervision.

4. My sincere thanks also go to Mr. Misbahul Munir (Dean of Faculty of Business) and

my entire lecture in President University for the contribution and support.

5. To the auditors at RSM Indonesia, kak agung, mba icha and pradyana for giving me

information to commence this thesis, to do necessary research work. Thanks for

your help and support.

vii | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

6. To my beloved friends, Melisa Anggreni, Sapphira Julia S., Febby Pricilla, Raymon

Yutto T., Adam Maulana A., Risky Dwi Y., Christian Heriyando, Defri Kurniawan,

Chandra Sentosa. Thank you for your help, encouragement, support, laugh and

smile.

7. To my beloved friends from senior high school, Yubi Hartland and Agata

Akasyahanda. Thanks for the help, contribution, encouragement and endless

support.

8. To my beloved roommates, Ekky Charlen, Farah Chinta Arin Ruswanti and Louise

Johanna Gloria Sirait. Thank you for your support and love. I am blessed to have

friends like you.

9. To my senior and manager in RSM Indonesia during my internship. Thank you for

taught me about the audit, inspiring me, and also the encouragement.

Finally, I would like to thank every single person who has been a part of my college

life that I could not mention personally. I might not be able to write this thesis without

amazing people around me. Thanks for everything and I apologize for all the mistakes I

made.

Nopita Aulia Siregar

viii | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

TABLE OF CONTENTS

PANEL OF EXAMINERS APPROVAL SHEET ........................................................ ii

RECOMMENDATION LETTER OF THESIS ADVISOR ........................................ iii

DECLARATION OF ORIGINALITY ........................................................................ iv

ABSTRACT .................................................................................................................. v

ACKNOWLEDMENT ................................................................................................ vi

TABLE OF CONTENTS ........................................................................................... viii

LIST OF TABLES ....................................................................................................... xi

LIST OF FIGURES ..................................................................................................... xi

CHAPTER

I. INTRODUCTION ........................................................................................... 1

1.1. Research Background ........................................................................... 1

1.2. Problem Identification and Statement ................................................... 4

1.3. Research Scope and Limitation ............................................................ 5

1.4. Research Objectives .............................................................................. 5

1.5. Research Benefit ................................................................................... 6

1.6. Research Method .................................................................................. 7

II. LITERATURE REVIEW .............................................................................. 8

2.1. Concept of Audit ................................................................................... 8

2.2. Auditor Responsibility and Independence Concept .............................. 9

2.3. Audit Quality ...................................................................................... 11

ix | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

2.4. Expectancy Theory ............................................................................. 12

2.5. Audit Expectation Gap ........................................................................ 14

2.6. Empirical Evidence on Expectation Gap ............................................ 17

III. METHOD OF DATA PROCESSING ...................................................... 19

3.1. Methodology Design ........................................................................... 19

3.2. Data Collecting and Processing .......................................................... 20

3.3. Data Collecting Category .................................................................... 20

3.3.1. Inquiry of Client ...................................................................... 20

3.3.2. Observation ............................................................................. 21

3.3.3. Documentation ........................................................................ 21

3.3.4. Literature Review .................................................................... 22

3.4. Company’s Existing Condition ........................................................... 22

3.4.1. RSM History ........................................................................... 22

3.4.2. Vision, Mission & Objective .................................................. 24

3.4.3. Governance of RSM Indonesia ............................................... 25

3.4.4. RSM Indonesia Business Fields .............................................. 26

IV. ANALYSIS AND EVALUATION ............................................................... 29

4.1. Interview Result .................................................................................. 29

4.1.1. Auditor's Perceptions Result ................................................... 30

4.1.2. User’s Perceptions Result ....................................................... 33

x | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

4.1. Research Findings ............................................................................... 35

4.2.1. Auditor's and User’s Perceptions about Concept of

Independency..... ..................................................................... 35

4.2.2. Users Misundertanding in Responsibility of Auditors Perceptions

Result ...................................................................................... 36

4.3. Research Analysis .............................................................................. 36

4.3.1. Is the Audit Indepedence Concept of User Different with

Auditors? ................................................................................ 36

4.3.2. Is the Audit Responsibility Concept of User Different with

Auditors ................................................................................... 38

4.3.3. What are the Causes of Expectation Gap between the Auditor and

User? ....................................................................................... 39

4.3.4. Is there Any Negative Impact of Audit Expectation Gap on User

and Auditor ............................................................................. 41

V. CONCLUSION AND RECOMMENDATION .......................................... 43

5.1. Conclusion .......................................................................................... 43

5.3. Recommendation ................................................................................ 44

REFERENCES ........................................................................................................... 46

APPENDICES ............................................................................................................ 49

xi | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

LIST OF TABLES

Table 3.1: Lines of Business and Its Services ............................................................. 27

Table 3.2: Divisons in RSM Indonesia ....................................................................... 28

LIST OF FIGURE

Figure 2.1: Expectation Gap Framework .................................................................... 16

Figure 3.1: STAR Value in RSM Indonesia ............................................................... 24

Figure 3.2: Governance of RSM Indonesia ................................................................ 26

Figure 3.3: RSM Indonesia Business Fields ............................................................... 26

1 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

CHAPTER I

INTRODUCTION

1.1. Research Background

The audit profession is one of the important professions for business in order to

make qualified corporation on market competition. Audit is concerned with the way an

organization performance has been reported. There are many elements in financial

society that play a part for business world, but only three elements that directly help

business world to keep sustaining. The three elements are external auditor, corporations

and user of audit report. The external auditor is a profession that makes a financial

report correctly and accurately for corporations in order to make user of audit report or

public trust to the corporation that being audited. Mautz and Sharaf (1986), define the

auditing in their study as being “…Concerned with the verification of accounting data,

with determining the accuracy and reliability of accounting statements and reports.”

Another definition of auditing by Arnes et al. (1997), they are including the “objectively

obtaining and evaluating evidence” and”competent independent person.” The meaning

is external auditor is a must to have an understanding in the criteria used and also

competent to know types and amounts of evidence to accumulate for examination to

reach proper conclusions on one hand and must possess an independent attitude to

objectively obtain and evaluate results without bias, or prejudice on the other. American

Accounting Association (AAA) (1973) also defined the auditing as a “systematic

process of objectively obtaining and evaluating evidence regarding assertions about

economic actions and events to ascertain the degree of correspondence between those

assertions, established criteria and communicating the results to related users

Therefore, external auditor should be professional, independence and reliable to

make the quality of audit report. Auditing is an independent function by means of an

ordered and structures series of steps, critically examining the assertions made by

2 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

individual or organization about economic activities and summarize the result in a

report to use by the public or users. For example, investors, management of a company,

creditors, analyst, or other individual or party that use the audit report in their activities,

they are main user of the audit report. They are requesting for the good quality of audit

report to make their decision confidently. They may rely upon audited financial

statement to obtain a view of the financial result as the guidance for their investment

decisions. Users of audit report or the management of a company will also need audited

financial statement, since the information in their audited financial statements is

important for the owner and/or board of directors to evaluate their performance. They

all should be able to rely on the information in audited reports in making their decisions.

To make a good quality of audit external auditors need to fulfill their responsibilities to

the public. There are also probabilities that an external auditor will report any

violations. For this reason, external auditors are perceived to be competent individuals

who play independence and objective role when auditing companies' financial

statements.

The responsibility of external auditor is impact to the quality of audit result, if

auditor couldn’t fulfill their responsibility or role, quality of audit will also decrease.

The external Auditor is obligate to give a high audit quality to public. It is auditor

responsible also to give the public high quality audit with reliable information. “Big

Four” accounting firms are in the high level of competency, they can manage to fulfill

all of their responsibilities to public with their competency. They have to perform

continuously in auditing process in terms of maintaining competence to public.

Auditor’s performance professionally will also create reliable opinion.

One of major responsibilities of external auditor is being independence. For all

profession independence is a critical issue, especially for auditor. This paper reviews

evidence related to the auditor independence and expectation gap between user and

external auditor. The expectation gap is occurring in concept independence of auditor.

Without independence the auditor report will not be reliable for the public.

“Independence is the main means by which the auditor demonstrates that he can

perform his task in an objective manner” (FEE, 1995). Independence is fundamental to

3 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

reliability of auditors’ report. The auditors will be called as a professional if they can

maintain their independences in order to create a good quality of audit. Perception from

public about the independence of auditor is important. There are several major causes

independence reduction of auditor. The causes are economic dependence of auditor on

the client; audit market competition; the provision of non-audit services.

However, external auditor and user or public hold different beliefs about the

auditors’ independence. Because of that phenomena the auditor is not always satisfied

the user’s demand of quality audit report. “Our findings indicate that expectation gap

exists; users have higher expectations for various facets and/or assurances of the audit

than do auditors in the following areas: disclosure, internal control, fraud, and illegal

operations” (John E. and Stanley C. 2001). Since there are some Scandals in national or

international, the reliable audit practice is decreasing. On the other hand, the expectation

from user or public is always increase, since the requirement of reliable audited

financial statement also increases daily. For example Arthur Anderson and Enron

Scandal, Arthur Andersen is an accounting and consulting service that operates

businesses throughout the US & world, on the other hand, Enron has been a client of

Andersen’s for 16 years up until Enron’s 2001 bankruptcy. Andersen hid millions of

dollars of debt from the public for Enron. In this scandal Arthur Andersen is not

independence with its work in auditing Enron Company. Since then, many of Arthur

Andersen’s auditing clients are choosing other accounting firms to perform auditing

work.

The term of “expectation gap” in auditing was first introduced to audit literature

by Liggio (1974). Since then, many researchers defined and analyze the expectation gap

of auditor. Liggio defined expectation gap as the differences between the levels of

expected performance “as envisioned by the independent accountant and by the user of

financial statements”. The expectation gap of independency of auditor exist when the

auditor and users hold different believe of concept of auditor’s independence. Koh and

woo extended this definition as “The existence of an audit expectation gap implies that

the role senders (auditees and audit beneficiaries) are dissatisfied with the performance

of auditors”(Koh and Woo, 1998). Monroe and woodliff (1993), defined the expectation

4 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

gap of auditing as the difference in beliefs between auditors and users or public about

the duties and responsibilities.

In general the auditor will be expected to give an accurate opinion that favorable

for a company. The opinion from auditor will affect the stakeholders in decision-making

related to the company performance. Therefore, the opinion from auditor is one of the

most important aspects to build a business. User of the audit report is expecting the

audit accounting firm to give the opinion with actual condition of the company in good

quality of audit. In other words the auditor should make an opinion independently,

accurately and professional.

In this context, the audit profession seek to shift the preferred meanings about the

nature, practice and/or outcomes of auditor’s responsibility and independence, in other

words leading to the varying definition and perception of the function and independency

of the auditor thereby resulting to a gap between the services received versus the

expected services provided by the auditors, which is generally termed the audit

expectation gap in the literature. Further, the empirical evidences on audit expectation

gap have revealed that one of the major reasons for audit expectation gap in many

countries is that there are differences in perceptions about the independence of auditors

with regard to accounting frauds. Auditor independence is a key element of the audit

expectation gap. Based on the elaboration of background of this study, the author

decides to discuss an issue with a title: “Auditor’s independence and Responsibility:

Expectation Gap between Auditor and User’s Perception”. In other word this study

will revisit the concept of expectation gap, auditors’ independence and the different

perception of user and auditor of audit quality.

1.2. Problem Identification and Statement

Based on the background above author can define statements of problem to be

observed. Statement of problem will be the main problem to discuss in this study. The

statements of problem of this study are:

5 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

1) Is the auditor’s independence concept of user different with auditors?

2) Is the auditor’s responsibility concept of user different with auditors?

3) What are the causes of the expectation gap between the auditor and user?

4) Is there any negative impact of audit expectation gap on user and auditor?

1.3. Research Scope and Limitation

The discussion is only focused on perception of auditor and user about auditor’s

independence. This research has short observation period and it is not possible to

interview more than four respondents; three auditors and one user. The conclusions of

this research are based on the answers received in the interviews; these are

interviewees’ personal opinions and should not be general perceptions in Indonesia.

1.4. Research Objectives

Based on the statement problem and introduction the author defines the objective of

this study. As the author mention above, this study is revisiting the concept of auditor’s

independency and responsibility, expectation gap and the different perception of user

and auditor about independency and responsibility of auditor. The purposes of this study

are:

1) To define the concept of auditor’s independence that users and auditors hold.

2) To define the concept of auditor’s responsibility that users and auditors hold.

3) To analyze the causes of the expectation gap between the auditor and the public

or user of audit report.

4) To analyze the influence or impact of audit expectation gap on user and auditor.

6 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

1.5. Research Benefits

As reported earlier, the objective of this study is revisiting concept of audit

independence, expectation gap and different perception of users and auditor of auditor’s

independence. It is also investigate the effect and causes of different beliefs that auditor

and users held about auditor’s roles and responsibilities of being independence, and it

will also affect the different perception of auditor’s independence. The different beliefs

from auditor and users is create an expectation gap that might be arises during decision

making. The motivation for undertaking this study is because to analyze expectation gap

theory or different perspective of auditor and users about auditor’s independence. The

author beliefs this study will have several benefits. The benefit of the study can be

summarized as follows:

1. For the business:

This research can be use as tools to analyze the independence of external

auditor in order to make the users increase their confident in decision making.

In addition, it will help the auditor and users have same opinion about

auditors’ independence, so they can avoid the expectation gap problem.

2. For author and other researcher:

The first benefit of this research is that it provides knowledge for the author

and other researcher about auditor’s independence from auditor and user

perception. Furthermore, this research gives the benefit for author and all

researchers about the knowledge of how to conduct a research.

3. For literature:

This research is to define the different perceptions of auditor’s independence

from auditor and users and the user’s expectation of auditor’s independence in

real business.

7 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

1.6. Research Method

This research is a qualitative research with types of verification approach. In gathering

and processing the data, the author will do two methods as follows:

1. Literature review

In this research the author gather the secondary data from literature review to get

references or relevant theories related to the topic discussed in this research. The

author will collect data by gathering all information from books, articles, and

journal.

2. Field research

In this research the author will get primary data by collecting and evaluating data

through inquiry, observation, and documentation.

Inquiry

The author will gather the data by doing an interview and discussion with

two people within two group; auditors and users in order to get the

information about each perception about auditor’s independence.

Observation

The author obtains the information from a specific observation in one of a

public accountant firm in Jakarta, Indonesia. The author observes the work

from auditor and also observes the opinion from users about auditors’

independence.

Documentation

Documents for this research examined by the author are the records of

interview result. Documentation is used to clarify the evidence of

information which is obtained by the author to analyze the research.

8 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

CHAPTER II

LITERATURE REVIEW

2.1. Concept of Audit

Audit is a requirement for every company to be trusted by the other party or the

public. The word of ‘audit is from Latin word ‘audire’, which means ‘to hear’. The

meaning of audit is a systematic process to obtaining evidence of the misstatement,

error or fraud of financial condition of a company. This definition also explain by ISO

19011, “Audit is a systematic, independent and documented process for obtaining audit

evidence and evaluating it objectively to determine the extent to which the audit criteria

are fulfilled” (ISO 19011). The function of auditor is to provide professional opinion in

the financial statement, in order to support their opinion the auditors must obtain

evidence.

Auditing refers to a systematic and independent examination of books, accounts,

documents and vouchers of an organization to ascertain how far the financial statements

present a true and fair view of the concern. “Auditing has become such an ubiquitous

phenomenon in the corporate and the public sector that academics started identifying an

‘Audit Society’.” (Michael, 1999).

The audit report is a connector between a corporation and stakeholder or other

party that engage to that company. It means the audit process is a must for every

company. According to Chow (1982), controlling the conflict of interests among firm

managers, shareholders and bondholders is a major reason for engaging auditors.

9 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

2.2. Auditor Responsibility and Independence Concept

Generally, Auditor’s role is to perform audit and be able to find reasonable

assurance about material misstatement in financial statement of a corporation. The audit

result is shown the information accurately and correctly about a corporation in order to

help the public and user of audit report confidently making economic decision. “The

auditor has a responsibility to plan and perform the audit to obtain reasonable assurance

about whether the financial statements are free of material misstatement, whether

caused by error or fraud” (Auditing Standards No. 82).

However, if the misstatements are not material the auditor is not obligate to

perform the audit procedure. After performing the audit procedures the auditor's

responsibility is to express an opinion on the financial statements. The auditors need to

make an opinion with professional and independent. The opinion from auditor will help

the user and also the corporation that being audit. The opinion are unqualified,

qualified, adverse and disclaimer. Unqualified opinion is the best possible opinion from

auditor, and this opinion is the most reported opinion by the auditor. The second

opinion is qualified opinion. “A qualified opinion means the auditor found the financial

reports essentially in conformance with Generally Accepted Accounting Principles,

except for one or a few areas where the auditor cannot, or does not want to, assert

conformance” (Marty Schmidt, 2004). Another opinion for audit report is adverse,

adverse opinion means that the auditor find some misstatement in client financial

statement, the auditor will give a suggestion to the client before the audit report is

publish. “An adverse opinion means the auditor has concluded that the audited financial

statements do not fairly represent the organization's financial position or financial

performance and that there are significant departures from GAAP” (Marty Schmidt,

2004). Another opinion that auditor can give to the client’s financial statement’s is

disclaimer, disclaimer means the auditor is not issue an opinion for a corporation.

“The auditor may issue a disclaimer of opinion, that is, publicly report that

the auditor has chosen not to issue an opinion. This may occur when

auditors decide they cannot be impartial or independent regarding the

10 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

company or organization audited, auditor's scope of coverage was

substantially limited and The auditor has significant uncertainties

regarding the appropriateness of parts or all of the financial reports”

(Marty Schmidt, 2004) .

In other word the auditor is responsible to perform audit and make an audit appropriate

report in circumstances when, in forming an opinion in accordance. The auditor is

obligate to perform the audit process in order to issue an opinion, in the process of audit

and issuing opinion to the public auditor should be professional and independence, the

independence is one of the responsibilities of auditor in performing audit.

Auditor independence is important to create good quality of audit. Users will

expect more from auditor to have independence in their performance. If the auditors

cannot fulfill their responsibility in being independence, it will impact to audit report,

the audit report will become a suspect and not reliable to use. In the research of

independence auditor by Gill and Cosserat (1996), they have emphasized that

“independence is the cornerstone of auditing profession, without independence the

auditor’s opinion is suspect.” Independence in generally is defined as freedom from

material conflicts of interest that threaten objectivity. According to ISB independence

can be defined as a “Freedom from those pressures and other factors that compromise,

or can reasonably be expected to compromise, an auditor ability to make unbiased audit

decisions” (ISB, 2000).

Mautz and Sharaf (1961) discuss independence and describe several meanings

of the concept. They note that Carey (1970) discusses two meanings of independence

for professional auditors. One he called “the self-reliance of any professional person”

and the other is described as the special kind of independence, an “honest

disinterestedness” in the results of his or her work that arises because of the public’s

reliance on an auditor’s work. Mautz and Sharaf note that they agree that a practitioner

should maintain an honest disinterestedness to promote unbiased judgments and

consideration of the facts as determinants of a final opinion. They also believe,

however, that in order for a practitioner to have this honest disinterestedness, he or she

must have a thorough understanding of the pressures and factors, “some of which may

11 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

be so subtle as to be scarcely recognizable,” that may color or influence that

disinterestedness. They suggest the recognition of programming independence (the

auditor has sole control over the nature of the audit program), investigative

independence (the auditor is free to collect and evaluate all the evidence deemed

necessary without interference), and reporting independence (the auditor is free to

report the results of the audit without interference) as concepts that will help a

practitioner achieve honest disinterestedness.

Another research by Geiger, Lowe, and Pany (2002), in their research they

examines about loan officers view and make decisions based on loan proposals within

the context of various relationships between the applicant, the auditor that performs the

external audit, and the auditor that performs the internal audit function, whether in-

house or outsourced to the applicant’s external auditor. The results support the position

that having outsourced internal audit services performed by the company’s external

auditor does not appear to negatively affect financial statement users’ perceptions of

auditor independence and other related decisions. The results also support the position

that if the external auditors are associated with internal audit activities, they should not

perform any management functions as part of the outsourced internal audit work. The

results also provide support for internal audit outsourcing if there is a requirement that

the engagement team for the external audit and internal audit activities remain separate.

More research is needed on issues related to independence and objectivity for internal

auditors and the internal audit function.

2.3. Audit Quality

Auditor independence is important because it has an impact on the audit quality.

The Audit Quality is the concept that already familiar, there are many definitions about

this concept. But the most commonly use in the research or study is the definition or the

concept of audit quality from De Angelo (1981), she stated that “the quality of audit

services is defined to be the market-assessed joint probability that a given auditor will

both (a) discover a breach in the client's accounting system, and (b) report the breach”,

as quite a number of other papers have cited that, or have similar implied definition

12 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

which would be discussed in the next section. Many researchers then used this double

approach to further define audit quality with details in competence and independence,

while others adopt it as a foundation to identify other audit quality attributes.

According to De Anglo’s (1981) definition, audit quality is an increasing function of

an auditor’s ability to detect accounting misstatements and auditor independence as

assessed by the market. De Angelo’s (1981) definition refers to “market assessed” or

perceived audit quality. When applying this definition to actual audit quality, there is an

underlying assumption that market perceived audit quality reflects actual audit quality.

However, many studies adopt this definition without addressing the distinction between

these two different concepts.

The quality of audit is depending on the auditor itself. If the auditor cannot fulfill

their responsibility, role and function, the business world cannot meet the high quality

of audit. Therefore, mostly the big companies use the auditor who already known as

their competency such as ‘Big Four’ accounting firms. The ‘Big Four’ accounting firm

is known as an accounting firms that have a high competency in doing audit procedure,

they already obtain the trust from the public and make the user confidently use their

audit report, for example investors will confidently make an economic decision-making.

2.4. Expectancy Theory

The Expectancy Theory of Motivation describes the behavioral process of

individuals including reasons why the individuals choose one behavioral option over

another. "The basic idea behind the theory is that people will be motivated because they

believe that their decision will lead to their desired outcome" (Redmond, 2009). The

theory explains that goals will impact to mental processes of individuals in choosing

behavioral option and they can be motivated towards goal if they believe in positive

aspect between efforts and performance. An individual is willing to work towards this

higher level of performance because of the perceived correlation between performance

and rewards. That is, that the level of performance is based on the strength of the

13 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

relationship between an employee's behaviors and the rewards that they can receive from

those actions. If working five extra hours a week will result in an eventual promotion, the

willingness to work those extra hours’ increases due to the employee's desire to be

awarded the promotion. Expectancy Theory of motivation first introduce by Victor

Vroom of the Yale School of Management in 1964. Victor Vroom’s study is one of the

most widely accepted theories of employee motivation.

"This theory emphasizes the needs for organizations to relate rewards directly

to performance and to ensure that the rewards provided are those rewards

deserved and wanted by the recipients." (Montana, Patrick J, Charnov & bruce

H, 2008)

According to his study, Victor H. Vroom (1964) defines motivation as a process

governing choices among alternative forms of voluntary activities, a process controlled

by the individual. The individual makes choices based on estimates of how well the

expected results of a given behavior are going to match up with or eventually lead to the

desired results. Motivation is a product of the individual’s expectancy that a certain

effort will lead to the intended performance, the instrumentality of this performance to

achieving a certain result, and the desirability of this result for the individual, known

as valence.

The Expectancy theory states that employee’s motivation is an outcome of how

much an individual wants a reward (Valence), the assessment that the likelihood that the

effort will lead to expected performance (Expectancy) and the belief that the

performance will lead to reward (Instrumentality). In short, Valence is the significance

associated by an individual about the expected outcome. It is an expected and not the

actual satisfaction that an employee expects to receive after achieving the

goals. Expectancy is the faith that better efforts will result in better performance.

Expectancy is influenced by factors such as possession of appropriate skills for

performing the job, availability of right resources, availability of crucial information

and getting the required support for completing the job.

14 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

Research of expectancy theory is also emphasized by Edward Tolman. He was a

cognitive behavioral psychologist who studied motivation and learning. The theory

from Edward Tolman describes learning with no obvious reward for the learner. Tolman

also began to develop the theory of behavior and motivation. He theorized that a motive

drives a person to behave a certain way until some intrinsic need is met. Until the need

is met the person will continue to behave in the same manner. This was the start of

motivation theories. Vroom would add to Tolman’s work with the Expectancy theory

later in history (VanderZwaag, 1998).

Another research of expectancy theory was emphasized by Miller and

Grush(1988). Their study in expectancy tested the hypotheses that the behavior of some

individuals is determined by personal expectancies while the behavior of other

individuals is determined by social norms. The author took two groups of people and

gave one group personal expectations about their behavior. The other group was given

information on what the social norms were for the time being. The author found that

strong expectancy behavior correspondence was given for those individuals who were

aware of personal expectancies but who were not knowledgeable about social norms.

For those individuals who were attuned to social norms, their behavior corresponded

with such (Miller & Grush, 1988).

2.5. Audit Expectation Gap Theory

The auditor’s responsibility is to provide ‘reasonable assurance’ that the

information in the financial statements accurately represents the financial position.

Auditor is required to reduce audit risk to an acceptably low level to attain reasonable

assurance. But what is reasonable? This can be different in the eyes of auditor and in the

eyes of users of financial statements and this creates expectation gap. Auditor is already

providing less than absolute assurance so he/she must not leave any effort undone to

maintain reasonable level of assurance by complying with the requirements of relevant

auditing standards. For example, proper planning, appropriate understanding of entity to

15 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

design further audit procedures, maintaining skeptic attitude, reducing sampling risk to

appropriate level etc.

However, that which the investor, public and other users of the financial

statements expect of the auditor is not necessarily the same as the law requires of him,

or that which is realistically possible. This difference of expectation is known as the

‘expectation gap’. There is concern that auditors and the public hold different beliefs

about the auditors’ duties and responsibilities, and the different beliefs that they have

create an expectation gap. When the users and the auditor hold different beliefs, the

expectation from the users will not match with the performance of the auditors and the

users will not really satisfied with the quality of the audit report that the auditors

performed. Expectation gap can also be explained as the difference between the

effectiveness of audit engagement what users believe and what auditor believes. It can

also refer to difference in understanding regarding nature of audit engagement i.e. what

users believe audit is and what audit actually is.

Audit Expectation gap is the term used to signify the difference in expectations of

users of financial statements and auditor’s expectation concerning audited financial

statements. Although it’s about expectations but still its scope and meanings have been

defined in number of ways. Difference in expectation can arise on the performance i.e.

the level of performance what users expect from auditor and how auditor actually

performed. An Expectation Gap also exists between the users of financial statements

and the auditors. No matter how many times the investing public is told that audits are

not designed to detect fraud, shareholders often believe that financial statement auditors

can and will find fraud in companies. Even those who should be savvy in financial

matters investing professionals, executives, and auditors themselves often do not

understand that traditional financial statements audits do not regularly detect fraud.

The term of “audit expectation gap” was first introduced to audit literature by

Liggio (1974). Liggio defines the Audit Expectation Gap as the difference between the

levels of expected performance as envisioned by users of a financial statement and the

independent accountant. After Liggio, there are also many opinions that arise from the

16 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

term of “expectation gap”. The Cohen Commission (1978) on auditor’s responsibility

extended this definition by considering whether a gap may exist between what the

public expects or needs and what auditors can and should reasonably expect to

accomplish.

Figure 2.1 Expectation Gap Frameworks

According to Guy and Sullivan (1988), there is a difference between what the

public and financial statement users believe accountants and auditors are responsible for

and what the accountants and auditors themselves believe they are responsible for.

Godsell (1992) described the expectation gap as “which is said to exist, when auditors

and the public hold different.” Monroe and Woodcliff (1993) define the audit

expectation gap as the difference in beliefs between auditors and the public about the

Auditor’s

Independence

and

Responsibility

Auditor’s Perception

1) Is the auditor’s

independence concept

of user different with

auditors?

2) Is the auditor’s

responsibility concept

of user different with

auditors?

3) What are the causes of

the expectation gap

between the auditor

and user?

4) Is there any negative

impact of audit

expectation gap on

user trust of the

auditor?

1)

User’s Perception

1) Is the auditor’s

independence concept

of user different with

auditors?

2) Is the auditor’s

responsibility concept

of user different with

auditors?

3) What are the causes of

the expectation gap

between the auditor

and user?

4) Is there any negative

impact of audit

expectation gap on

user trust of the

auditor?

Audit Expectation Gap

17 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

duties and responsibilities assumed by auditors and the messages conveyed by audit

reports. Porter (1993) did an empirical study of the audit expectation-performance gap.

In his study he defines the expectation gap as the gap between society’s expectations of

auditors and auditors’ performance, as perceived by society. In his study there are 2

components: a) reasonableness gap (that is, the gap between what society expects

auditors to achieve and what the auditors can reasonably be expected to accomplish);

and b) performance gap (that is, the gap between what society can reasonably expect

auditors to accomplish and what auditors are perceived to achieve).

2.6. Empirical Evidence on Expectation Gap

One of the previous research’s is from John E. McEnroe and Stanley C. they

extend their research by directly comparing audit partners’ and investors’ perceptions of

auditors’ responsibilities involving various dimensions of the attest function. They

conducted the study to determine if an expectation gap currently exists and they find

that it does; investors have higher expectations for various faces and/or assurances of

the audit than auditors. Their findings serve as evidence that the accounting profession

should engage in appropriate measures to reduce this expectation gap.

Rohalla G., Ali M. El Zolh, and Rasol M. Moghadam, in their study they use

statistical sample of their research included auditors and user, which were 2023, and

then final sample study was estimated by Cocaran formula at 260 people. However,

number of collected questionnaire was 217. Methodology of the research was

descriptive. Result of research indicated that there was no conflict about acceptable

report, report no comment, internal control, and ensure concept, importance concept

between producers and users, however, there was conflict between rejected and

conditional report and auditor independence. Furthermore producer had positive

perspective about acceptable and conditional report current research showed that

auditors do not have sufficient independence. Finally, 30% perspectives were different

and 70% were equal.

18 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

Humphrey (1991) investigated the expectation gap with reference to England is an

extension of first studies. The man conclusions on Humphrey’s study include

expectation gap in auditors’ role in fraud detection; the extent of auditor’s responsibility

to this party; the nature of balance sheet valuation; threats to auditors’ independence;

and auditors’ ability to cope up with risk and uncertainty. According to his study “If any

topic can be classified as going to the of the audit expectations debate, it is the issue of

auditor independence”. In his study Humphrey stated that the auditor independent is the

key elements in audit expectation gap. In 1992 the empirical study of expectation gap

by Humphrey and Garcia-Benau in both UK and Spain. They investigated the

expectation gap and asking the auditors, users, and finance directors whether audit firms

should not provide NAS to their audit clients. The result in both countries was close to

neutral. Their average response was close to neutral except for UK auditors who

expressed strong disagreement.

19 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

CHAPTER III

METHOD OF DATA PROCESSING AND

COMPANY’S EXISTING CONDITION

3.1. Methodology Design

This research is qualitative research since this research is defining a condition of

expectation gap between users and auditors. The qualitative research has its roots in

social science and is more concerned with understanding why people behave as they do,

this method will need more review concept and science for the research. The focus of

qualitative research tends to be on understanding the meaning imbedded in participant

experiences through an open-ended, unstructured and subjective approach (Lincoln &

Guba, 1985). The research is most often conducted in a naturalistic setting with a

purposive sample (Patton, 2002). The research tends to be holistic, descriptive and

focuses on the depth and details of experiences (Denzin & Lincoln, 1998). Data

collection methods include interviews, observations, field notes, and documents to name

a few (Wolcott, 1994). Data tend to be analyzed through an inductive, ongoing and

evolving process of identifying themes within a particular context (Miles & Huberman,

1994).

“Qualitative research is an inquiry process of understanding based on

distinct methodological traditions of inquiry that explore a social or human

problem. The researcher builds a complex, holistic picture, analyzes words,

reports detailed views of informants and conducts the study in a natural

setting.” (As Creswell, 1998)

The main reason to use this method in writing this research is because this

research tends to be on understanding the meaning imbedded in participant experiences.

20 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

The participants of respondent in this research need to give the details of their

perceptions related to the topic of this research. Since the topic of the research is about

perceptions of external auditors and users about auditor’s independence which is related

to ethic and behave of an auditor. To answer the statement problem of this research the

author needs auditors and users who have a lot of experience and competence.

3.2. Data Collecting and Processing

The author chooses qualitative method as the method in collecting data. The

most common sources of data collection in qualitative research are interviews,

observations, and review of documents. Author places the data-collecting procedures

into three categories: observations, interviews, documents and the data obtained in

this research are from:

1. First is primary data, advantages of using the primary data is that author are

collecting information directly and for the specific purposes of research. For this

reason, the data that collected by the author is reliable by directly collecting by

the author from the result of interviewed with the auditor at public accounting

firm, RSM Indonesia.

2. In this research the secondary data will obtain from the history of company,

related theories, relevant books, and internet sources.

3.3. Data Collection Category

3.3.1. Inquiry of client

Inquiry is to obtain information or data from knowledgeable persons in order to

obtain explanation efficiently. The author uses interview method because interview is

undoubtedly the most common source of data in qualitative research. The data is more

relevant and acceptable because interview will need to directly questioning the

respondent. Interviews range from the highly structured style, in which questions are

determined before the interview, to the open-ended, conversational format. In qualitative

research, the highly structured format is used primarily to gather information. These

21 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

interviews will be used as qualitative input. The following techniques of interview that is

used are:

1. Structured technique is approach to gather all information by the

structured/listed questions interview. Structured interviews can be conducted

efficiently by interviewers trained only to follow the instructions on the

interview guide. Structured interviews can produce consistent data.

2. Another technique of interview is semi structured technique. A semi-structured

interview will involve many open-ended questions, although they may also

contain some closed questions. The author will take the representative from

external auditor at RSM Indonesia and user. These technique will conducted

by the author to get perception from each representative. By using both

techniques the author will obtain some perceptions from each representative

and it will show the gap and problem arising in different perceptions of

auditor’s independence from each representative.

The author will obtain the data based on perceptions of auditor and user about the

auditor’s independency and responsibility. The data is related to non-financial data. The

interview will be conducted with author in public accounting firms in Indonesia especially

in Jakarta at RSM Indonesia. Other respondents are internal user of audit report this

research has been done the interview session on:

Date 14th

January 2016 (Auditors) and 16th

January 2016 (Internal User)

Time 7.00 PM

Duration 45 minutes

Place RSM Indonesia (south Jakarta) and Grand Indonesia (Central Jakarta)

Interviewee Auditors in RSM Indonesia and internal user of audit report

Topics Independency, Responsibility & Expectation Gap Experience

3.3.2. Observation

The author will obtain the primary data by conducting direct observation to the

public accounting firm, which is being object of the research in order to see the practice

and perception of auditor’s independence. By doing observation the author will able to

22 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

detect the findings and factors that caused the findings. This research did observation

starting 5th

January 2016 until 5th

April 2016.

3.3.3. Documentation

Documentation is used to clarify the evidence of information which is

obtained by the author to analyze the research. Documents for this research examined by

the author are the records of interview result. Other documentation took from list of

interview questions and letter of interview statement from RSM Indonesia. The function

of the records is to tracking down evidences either internal or external evidences of

activities being researched.

3.3.4. Literature review

The secondary data that used in this research is literature review. The data is

collected and observe by the author from the theory based on literatures, articles, journal,

and previous research. The literatures are not only focused on the book, the author also

collects the literatures data from the internet. The author uses library research to more

understand with the literature related to this study. The purpose of library research is to

support this study and make the author and reader more understand the literature of this

study or research.

3.4. Company’s Existing Condition

3.4.1. RSM History

a) RSM International

RSM International is one of the world’s leading audit, tax, and advisory networks

of independently owned and managed professional services firms. RSM and its

member firm are full members of the forum of firms. The forum of firms is an

association of international networks of accounting networks of accounting firms

that perform audits of financial statements that are may be used across national

borders. RSM established in 1964 and until now it has presence in 106 countries

in 700 offices throughout the world. The executive office is located in London,

and it is supported with regional office in Australia for Asia Pacific countries,

23 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

United Kingdom for Europeann countries, and Yemen for Middle East and North

African countries, and South Africa for African countries, and United States for

North American and Latin American countries.

RSM is a global network of independently owned and managed professional

services firms, united by a common desire to provide the highest quality of

services to their clients. The vison of RSM is to create member to be the provider

of choice to internationally active growing organizations who are looking for

accounting tax, consulting and specialist advisory services that will create lasting

success and help them reach their goals. Member firms of RSM International are

all independent operate in their home countries under their home countries under

their own firm names such as RSM AAJ Associates in Indonesia, RSM Nelson

Wheeler in Hong Kong, and RSM Chio Lim Stoner Forrest in Singapore. RSM

International was the initial of three original member firms of the organization

which are Robson Rhodes (England), Salustri Reydel (France), and McGladrey &

Pullen (America).

b) RSM AAJ Associates

RSM AAJ is a member firm RSM, a global organization of independent

professional services firms. RSM AAJ Associates is an international firm with

strong local presence in Indonesia that offers world-class services. The offices are

located in Jakarta and Surabaya. RSM AAJ is offers a group of auditing and

consulting services that provided excellent services with aim to add value for

clients. RSM AAJ Associates Established in 1985 by Amir Abadi Jusuf, with a

Registered Public Accountants as the flagship firm. It began to provide reliable

auditing and assurance services. At present, it have managed to develop and grew

into a large, reputable and integrated accounting and consulting professional

services, involves in wide array of services, from accounting services, to

consulting services in areas of risk management, taxation, finance, and

information technology. RSM AAJ Associates is become the 5th

largest accounting

and auditing practice in Indonesia. RSM AAJ consists of KAP Aryanto, Amir

Jusuf, Mawar & Saptoto; PT AAJ Bismatamma; PT AAJ Kapital; PT AAJ Mitra

24 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

Daya; PT AAJ MitraDana and other business units under which all under the RSM

AAJ Group and RSM AAJ Brand.

3.4.2.Vision, Mission& Objective

a) Vision

To be the right partner to its stakeholders

b) Mission

1. Support achievement of clients' excellence by rendering world class

professional services

2. Give contribution to the profession and to the Indonesian economy

3. Provide a rewarding and enjoyable professional working and learning

environment1

c) Objective

We are committed to provide services that will add value to our clients and will

aid to our clients' excellence. Values delivered to our clients will bring sustainable

growth for both RSM AAJ Associates and moreover to our valuable clients. For

that reason, we believe in implementing "STAR" value in each aspects of our

everyday activity.

d) STAR Value

RSM AAJ also has STAR value to guide the employees how to behave when they

doing their job. Below is the STAR value of RSM AAJ Associates that every

employee needs to understand:

Figure 3.1 STAR Value of RSM Indonesia

1 RSM AAJ Associates Employee Handbook Version 14.01

25 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

SMART – Work Smarter, not just harder

Do what human do, Think!, Not just do, but do the right thing, Know what you do, Learn

from others, Maintain professionalism skepticism, Initiate ideas, Think Outside of the

box, Master your emotion.

TRUST - Build Trust, and maintain

Practice what you preach, Earn your trust, maintain integrity, Confidentiality is a must,

always keep your promise, Live out unconditional responsibility, be a player not a victim,

Deficiency shows when you blame others.

ACTION - Commit, and make things happen

Committed and dedicated to your work, Consciously act and response to provide

solutions, Never satisfy with minimum effort and quality, Always be prudent and

meticulous, Eager to develop and increase competency, Communicate authentically and

constructively, Always consider budget in executing tasks, Contributes value to all,

Coordinate impeccably, and support your team and peers, Enjoy work, bring out the best.

RESPECT - Respect yourself, respect others

Have sense of ownership, Maintain positive attitude, be nice, hostility, won’t take you

anywhere, Appreciate differences, people take different roads seeking fulfillment,

Congratulate achievements, and don’t be selfish and envious.

3.4.3.Governance of RSM Indonesia

RSM AAJ’s management is oversight by the ‘Board of Partners’. The management

or executive role is performed by Chief Executive Partner that is assisted by Managing

Partners, Division Chief Operating Officers, Partners, Directors and other officers, which

collectively called ‘Board of Management’. Below is the organization structure of RSM

AAJ Associates:

26 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

Figure 3.2 Governance of RSM Indonesia

Sources: Employee Handbook RSM AAJ Associates version 14.01

3.4.4.RSM Indonesia Business Fields

RSM AAJ Services are managed under Line of Business (LOB). LOBs are services

that this firm performs for clients. It generally includes a concept, a set of offerings, a

methodology, a process, standard work plans and standard skill and standard resources.

Figure 3.3 RSM Indonesia Business Fields

Audit Asurance Outsourcing Tax

Transaction Support Governance,

Risk & Control

Sources: Employee Handbook RSM AAJ Associates version 14.01

1

2 3

4

5

27 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

Table 3.1 Lines of Business and its Services

No Line of Business Services Covered

1 Audit Assurance General Audit on Financial Statements

Financial Information review ( Review on

Historical Financial Information, Examination of

Prospective Financial Information, Agreed-Upon

Procedures on Financial Information)

IFRS

2 Tax and Outsourcing

Tax

Tax Litigation and tax Disputes, Transfer Pricing

Reviews & Documentation, International Tax

Structuring, Tax Compliance, Tax Audits, Tax

Consulting.

Outsourcing

Company Incorporation & Representative Office

Establishment, Corporate Secretarial, Executive

Research & recruitment, Accounting & Payroll.

3 Corporate Finance

and Transaction

Support

Financial forecast & Working Capital Review,

Due Diligence, Transaction Analyst, Post-Merger

Integration

Pre-IPO Preparation & Grooming, IPO Support,

Post-Ipo Advisory Services

Mergers & Acquisitions, Disposals

Deal Structuring & Origination, Business Planning

Governance Advisory & Assurance

Internal Audit (Co-sourced & Outsourced Internal

Audit, Audit Compliance, Performance Audit,

Internal Control testing, Quality Assurance

Review on Audit Activity).

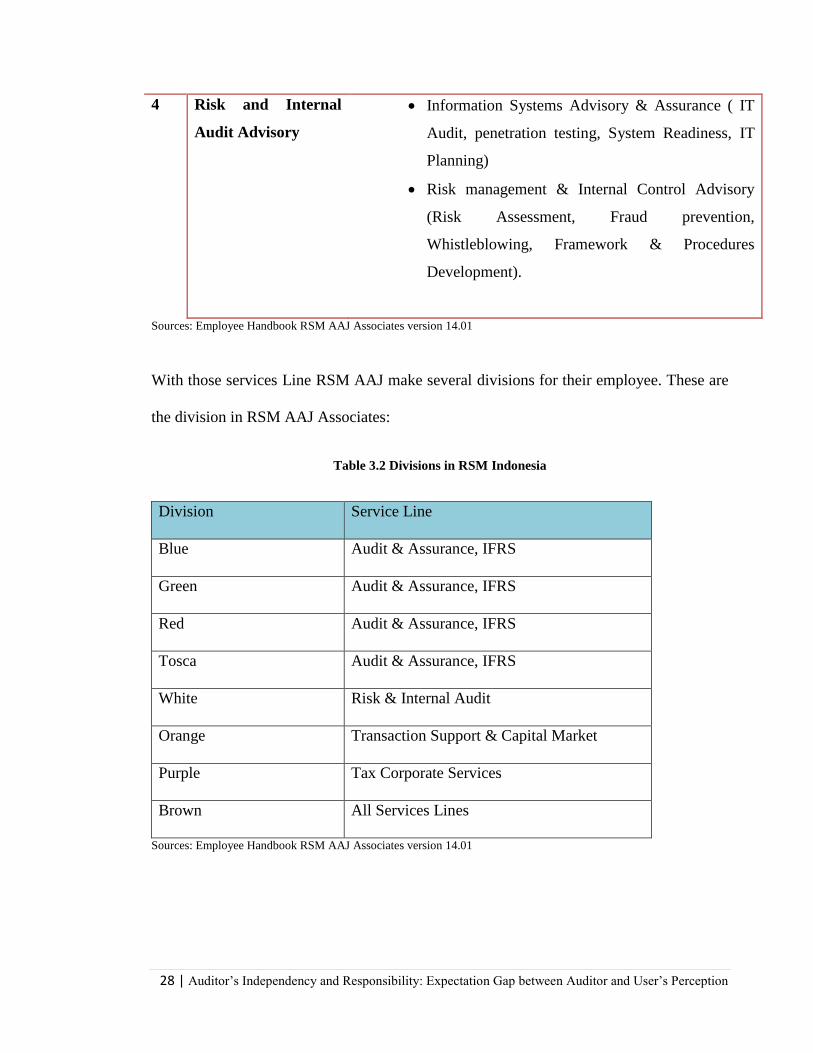

28 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

4 Risk and Internal

Audit Advisory

Information Systems Advisory & Assurance ( IT

Audit, penetration testing, System Readiness, IT

Planning)

Risk management & Internal Control Advisory

(Risk Assessment, Fraud prevention,

Whistleblowing, Framework & Procedures

Development).

Sources: Employee Handbook RSM AAJ Associates version 14.01

With those services Line RSM AAJ make several divisions for their employee. These are

the division in RSM AAJ Associates:

Table 3.2 Divisions in RSM Indonesia

Division Service Line

Blue Audit & Assurance, IFRS

Green Audit & Assurance, IFRS

Red Audit & Assurance, IFRS

Tosca Audit & Assurance, IFRS

White Risk & Internal Audit

Orange Transaction Support & Capital Market

Purple Tax Corporate Services

Brown All Services Lines

Sources: Employee Handbook RSM AAJ Associates version 14.01

29 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

CHAPTER IV

ANALYSIS AND EVALUATION

4.1. Interview Result

In this chapter, after author did the interview process with all respondents the

author will discuss the perceptions from auditors and users about auditor’s

independence and connecting perceptions from each interviewee to seek the gap and

findings arising in this topic by using interview result. The author also will compare the

perceptions of auditor’s independence from each interviewee with the theory literature

and condition that has been implemented by the auditor in RSM Indonesia.

First, the author will discuss the interview result from auditor, in order to know

the perceptions from auditor and observe the implementation of interview result in RSM

Indonesia. The author has worked as an external auditor RSM Indonesia to observe the

implementation. Second, the discussion continued with interview result from user. The

author will discuss perceptions from user of audit result about auditor independency.

Third, author will compare each perception and analyze the gap between user and

auditor about the independence external auditor.

This chapter will contain the result of interview with several interviewees which

author has done on January 14th

and January 16th

. From the interview result the author

can obtain perceptions from auditors and users about auditor’s independence, auditor’s

responsibility and their expectation to each other. Their explanation will be used as the

30 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

data for this chapter in order to analyze the expectation gap between auditor’s

independence and responsibility. The information from interview result as follows:

4.1.1. Auditor’s perceptions result

The first interviewees are auditors from RSM Indonesia. Based on the interview

result, the auditors explained briefly about the concept of auditor’s independence and

auditor’s responsibility and their implementation in their work. The result of interview

with auditors can be described as follow:

a) Auditor’s Independence

There is a possibility that auditor will face the client who wants him/her

to cover some materials amount from public. One of the interviewee had this

experience in one of the public accounting firms in Indonesia before he worked

in RSM Indonesia. In RSM Indonesia the independence of external auditor is

important because RSM Indonesia is also big accounting firm even if not

included in big 4 accounting firms. They explained that the probability to have

un-independence auditor in small accounting firms is higher than the big

accounting firms.

When the auditors get some benefit from client which outside from the

engagement letter in order to ask him to cover some weaknesses in client’s

company it will not really impact to all external auditor, it will only impact to

partner or manager that has authority to make opinion for audit results. In here

the author can conclude that the auditor’s perception of auditor’s independence

31 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

will only be needed for partner or manager because it will only impact to them

not all the external auditors.

From the result of interview, one of interviewee from auditor does not

really understand about auditor’s independence because the explanation is too

general. He explained that auditor’s independence is code of ethic. It means the

auditor need to holding on the code of ethic. Another interviewee explained that

auditor’s independence refers to an action that will not be affected by other

opinion and independence in auditors is the most important thing because

independence is something that will restrict the auditors and client’s company.

One of the auditor described independence is impartial action and not affected

by others in providing an opinion.

During the interview one of interviewee is the staff auditor in RSM

Indonesia. She described experience in un-independence action from client

when detected some findings which are really material around 1 billion. Her

client’s was mistaken in recording process. This client’s company is job-costing

industry and it is a small company if we compare to others client. The client asks

her to hide those findings from auditor’s manager, partner, and public to avoid

material losses in exchange she get some benefit from client. All of the

interviewees in RSM Indonesia are independence enough to their job.

b) Auditor’s Responsibility

From the result of interview with auditor, they believe that they have three main

responsibilities. The first responsibility is to reorganized financial statement of

client. Second, provide opinion for client’s financial statement in order to make

32 | Auditor’s Independency and Responsibility: Expectation Gap between Auditor and User’s Perception

their financial statement reliable to use by public or users. The third responsibility

is to check the internal control of a company, is there any accounting policy of a

company that is not relevant with PSAK. The responsibility of auditor is not to

find a mistake of a client, even if sometimes clients are miss-understanding with

auditor’s responsibility. The auditors stated that the clients sometimes not really

understand with auditor’s responsibility, clients believe that auditor’s

responsibility is to find a mistake of their company. On interview section, one of

the interviewee explained that he also has an experience in facing a conflict when

he tries to communicate with clients because they both have different perceptions

in several aspects and the communication with client is not always a good

conversation.

c) Expectations Gap Experience

The interviewees from auditor group have experience in facing the client

who has high expectation from the auditors. The result of interview can be

concluded that the client who has higher expectation is client who has been

audited by big 4 accounting firms. One of the interviewee has a client who expects

she/he will not be independent and cover their findings.

There are several clients who have high expectation from auditor. Their

client expects all of them to have equal experience even if the auditor is a junior