axis bank -...

TRANSCRIPT

Axis Bank

Gradual strengthening of balance sheet continues

January 23, 2018

Prabhudas Lilladher Pvt. Ltd. and/or its associates (the 'Firm') does and/or seeks to do business with companies covered in its research reports. As a result investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of the report. Investors should consider this report as only a single factor in making their investment decision.

Please refer to important disclosures and disclaimers at the end of the report

Q3FY18 Result Update

R Sreesankar [email protected] / +91‐22‐66322214

Pritesh Bumb [email protected] / +91‐22‐66322232

Vidhi Shah [email protected] / +91‐22‐66322258

Rating BUY

Price Rs611

Target Price Rs651

Implied Upside 6.5%

Sensex 35,798

Nifty 10,966

(Prices as on January 22, 2018)

Trading data

Market Cap. (Rs bn) 1,570.5

Shares o/s (m) 2,570.2

3M Avg. Daily value (Rs m) 4800.1

Major shareholders

Promoters 28.04%

Foreign 48.06%

Domestic Inst. 14.33%

Public & Other 9.57%

Stock Performance

(%) 1M 6M 12M

Absolute 10.4 13.1 35.6

Relative 4.9 1.3 3.2

How we differ from Consensus

EPS (Rs) PL Cons. % Diff.

2019 31.4 32.8 ‐4.3

2020 44.7 47.1 ‐5.0

Price Performance (RIC: AXBK.BO, BB: AXSB IN)

Source: Bloomberg

0

100

200

300

400

500

600

700

Jan‐17

Mar‐17

May‐17

Jul‐17

Sep‐17

Nov‐17

(Rs)

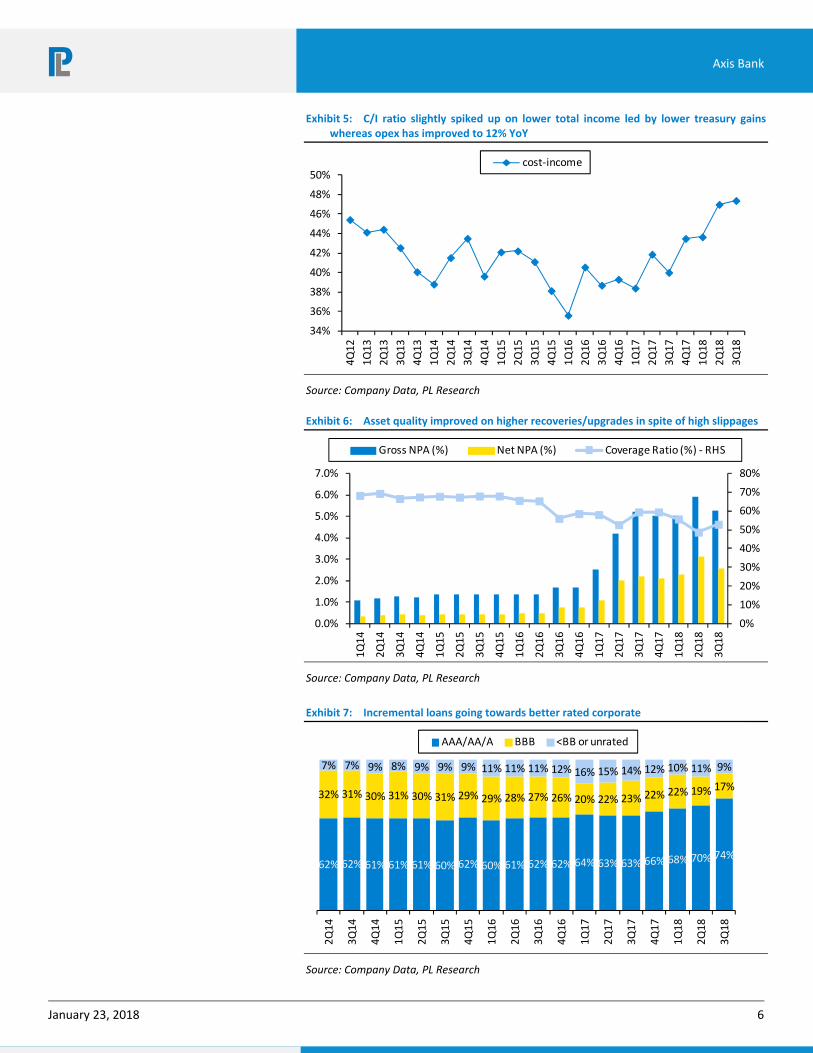

Axis Bank earnings were slightly below estimates on the back of higher provisions, though higher provisions helped improve PCR (calc) by 490bps to 58%. Asset quality improved despite relatively higher slippages of Rs44.3bn on large upgrade/recoveries of Rs40.1bn from the divergence related NPAs in Q2FY18 and also partly due to high write‐offs. Key positives for the bank continues to be strong CASA, improving retail/SME/better rated corporate and control on opex. We believe NIM pressure should bottom out and stabilize going ahead with tailwinds if MCLR increase from here on, while we see slippages & provisions gradually trending downwards in FY19 & FY20 helping improvement in return ratios, which makes us retain our positive stance intact directionally since our upgrade last month. The stock has run up sharply and hence leaves limited upside in the near term with PT of Rs651 based on 2.3x Sep‐19 ABV.

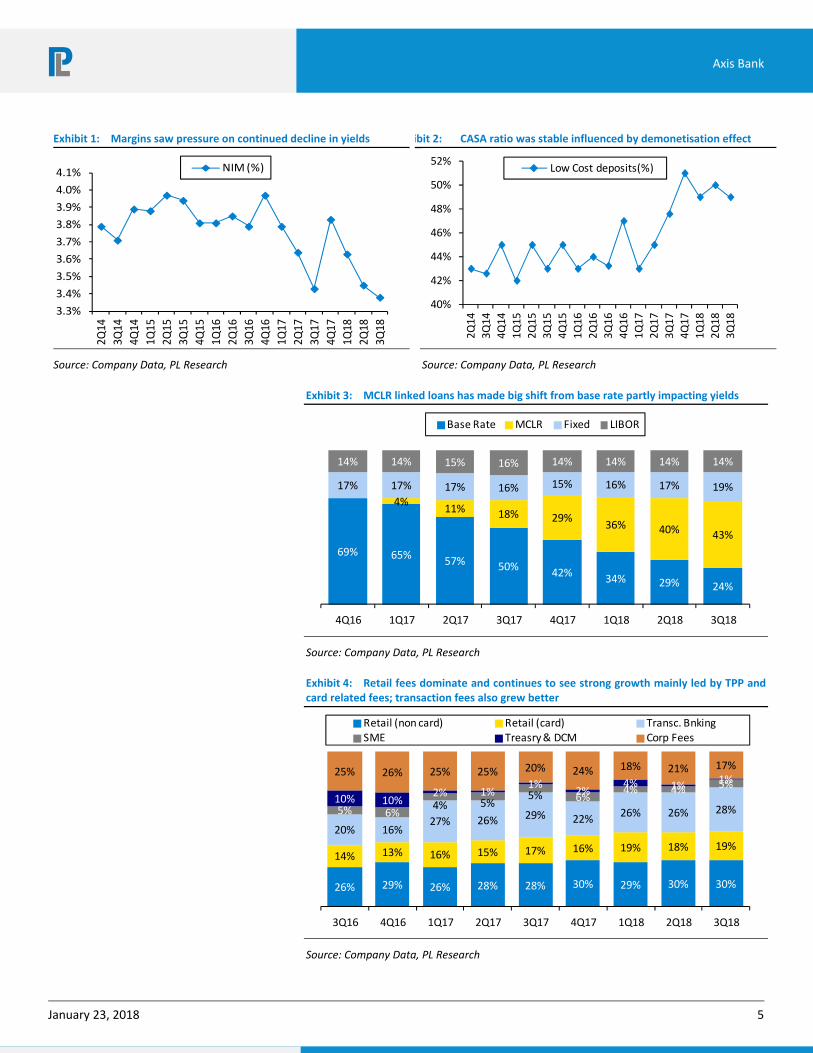

Ex‐treasury PPOP better: Core PPOP growth of ~17% YoY was better with decent NII growth of 9% YoY and strong fee income of 25% YoY (partly on lower base). Margins were lower by 7bps at 3.3% as pressure on yields continued but bank expect margin to have bottomed out and retained guidance of 20bps decline from FY17 exit of 3.67% which currently has declined by 19bps for 9MFY18. We believe NIM pressure to subside in near term and should improve slightly in next few quarters.

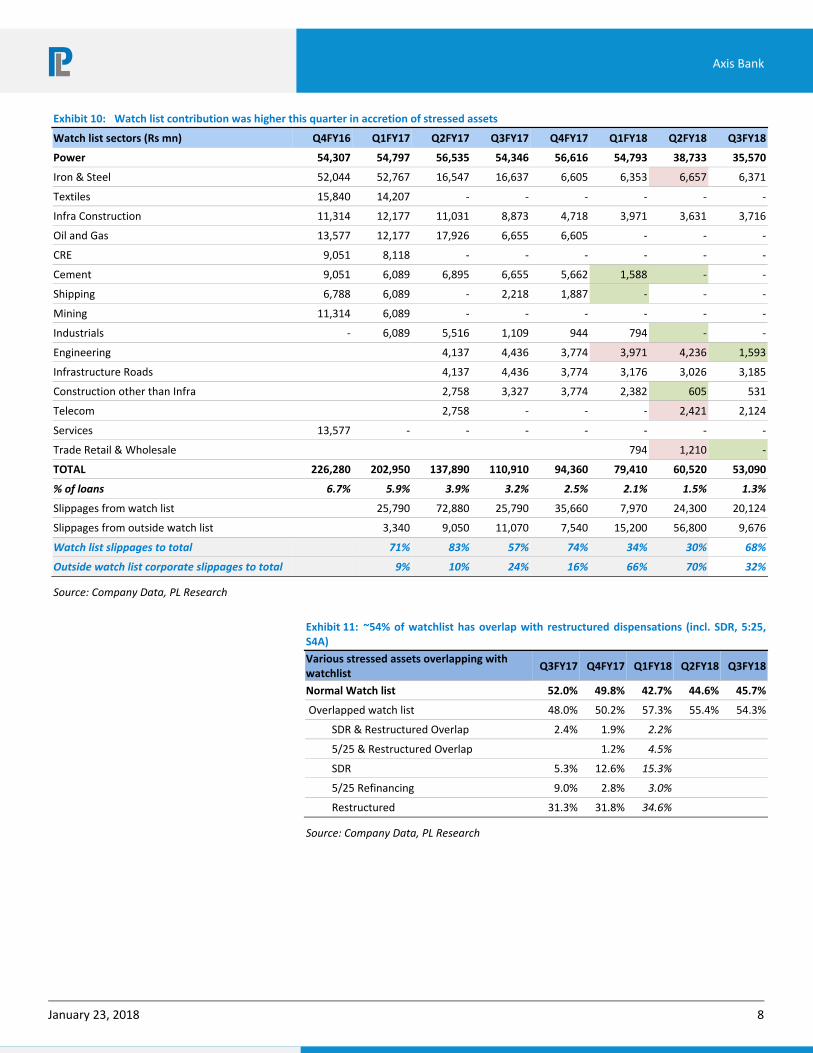

Slippages high but stronger recovery/upgrades: Bank continued to report relatively higher slippages of Rs44.3bn mainly from corporate book and within that from the “BB & below” rated pool. But asset quality improved as bank witnessed Rs40.1bn of recovery/upgrade on large upgrade in one steel a/c, recovery in one IT a/c related from the RBI divergent NPAs in Q2FY18 and one NPA a/c part of NCLT was sold to non‐ARC on cash basis with 40% haircut. “BB & Below” rated exposure which remains key a monitorable for asset quality increased QoQ to Rs161.2bn (3.8% of loans) from Rs158.2bn with overlap of restructuring dispensations & watchlist. Bank maintained its credit cost guidance of 220‐260bps with suitable PCR of 60‐65%.

Loan book growth strong; slippages to subside gradually: Loan book growth was strong at 21% YoY mainly contributed by strong SME/Retail (+27% each) growth and working capital loans in corporate book (49% growth). Bank continues to focus on retail/SME/Working capital and better rated corporate exposures helping improve overall asset quality of bank and in‐turn would help reduce slippages going ahead.

.

Key financials ( Y/e March) 2017 2018E 2019E 2020E

Net interest income 180,931 190,274 232,272 275,556

Growth (%) 7.5 5.2 22.1 18.6

Operating profit 175,845 165,333 202,785 242,812

PAT 36,793 36,577 81,412 117,040

EPS (Rs) 15.4 14.7 31.4 44.7

Growth (%) (55.5) (4.3) 113.1 42.5

Net DPS (Rs) 4.7 5.3 6.4 8.0

Profitability & Valuation 2017 2018E 2019E 2020E

NIM (%) 3.17 2.97 3.21 3.37

RoAE (%) 6.8 6.0 11.4 14.6

RoAA (%) 0.64 0.57 1.12 1.43

P / BV (x) 2.6 2.4 2.1 1.9

P / ABV (x) 3.0 2.7 2.4 2.0

PE (x) 39.7 41.5 19.5 13.7

Net dividend yield (%) 0.8 0.9 1.1 1.3

Source: Company Data; PL Research

January 23, 2018 2

Axis Bank

Exhibit 1: Q3FY18 Financials –Core performance was better; asset quality improves

(Rs m) Q3FY18 Q3FY17 YoY gr. (%) Q2FY18 QoQ gr. (%)

Interest Income 1,17,216 1,11,010 5.6 1,12,351 4.3

Interest Expenses 69,900 67,673 3.3 66,955 4.4

Net interest income (NII) 47,315 43,337 9.2 45,396 4.2

Other income 25,931 34,002 (23.7) 25,855 0.3

Total income 73,246 77,339 (5.3) 71,252 2.8

Operating expenses 34,708 30,937 12.2 33,478 3.7

‐Staff expenses 10,629 9,919 7.2 10,828 (1.8)

‐Other expenses 24,079 21,018 14.6 22,650 6.3

Operating profit 38,538 46,402 (16.9) 37,773 2.0

Core operating profit 36,538 31,148 17.3 34,003 7.5

Total provisions 28,110 37,958 (25.9) 31,404 (10.5)

Profit before tax 10,428 8,444 23.5 6,369 63.7

Tax 3,163 2,649 19.4 2,045 54.7

Profit after tax 7,264 5,796 25.3 4,324 68.0

Balance sheet (Rs m)

Deposits 40,89,667 37,07,901 10.3 41,64,306 (1.8)

Advances 42,09,227 34,71,747 21.2 41,01,708 2.6

Ratios (%)

Profitability ratios

RoaA 0.4 0.4 5 0.3 17

NIM 3.4 3.4 (5) 3.5 (7)

Cost of Funds 5.1 5.5 (43) 5.2 (10)

Asset Quality

Gross NPL 2,50,005 2,04,668 22.2 2,74,023 (8.8)

Net NPL 1,17,695 82,948 41.9 1,40,523 (16.2)

Restructured Assets (Rs m)

Gross NPL ratio 5.28 5.2 6 5.9 (62)

Net NPL ratio 2.56 2.2 38 3.1 (56)

Coverage ratio (Calc) 52.9 59.5 (655) 48.7 420

Rest. assets/ Total adv.

Business & Other Ratios

Low‐cost deposit mix 49.0 47.6 141 50.0 (100)

Cost‐income ratio 47.4 40.0 738 47.0 40

Non int. inc / total income 35.4 44.0 (856) 36.3 (89)

Credit deposit ratio 102.9 93.6 929 98.5 443

CAR 18.0 16.6 141 16.3 168

Tier‐I 14.1 13.0 114 12.4 177

Source: Company Data, PL Research

NII was decent at 9% YoY growth led by

strong growth in advances; however, yields

declined as more portion of book is linked

to MCLR (43%)

Core fee income was better at 24.5% YoY

growth mainly led by retail and transaction

fees. Within retail, card fees grew strong

Provisions were higher than our

expectations as bank strengthens the

balance sheet and improves PCR by 420bps

QoQ

Advances saw better growth at 21% YoY

led by retail and SME book

NIMs came off further on continued

pressure on yields side and slightly

increased cost of funds (calc).

Asset quality improved as bank saw huge

recoveries/upgrades including 2 A/cs which

fell in Q2FY18 due to RBS; however

slippages were slightly higher than our

expectations

CRAR improved significantly due to raising

of equity capital and AT1 Bonds

January 23, 2018 3

Axis Bank

Key Q3FY18 conference call highlights:

Balance sheet growth & outlook:

Loan book – Advances grew by 21% YoY as SME and retail book grew strong

while corporate loan growth was mainly working capital led.

Retail loan book – Book has become more diversified growing at 29% YoY led

by auto (33% YoY) and personal loans (36% YoY). Bank continues to see strong

traction in growth (smaller base) in credit cards, small business banking and

education loans segments. Retail book has become more granulized and

mainly growth is coming from existing customers.

Corporate loan book – Continue to grow robust at 49% YoY in working capital loans, whereas term loans were flat YoY. Focus is on moving to deeper

corporate bond market, better rated corporate, reduce risk by concentration

and improve transaction banking.

SME loan book – Book has grown at 27% YoY led by both working capital and

term loans and the growth momentum continues to be the same from hereon.

Liabilities: CASA Ratio stands at 49% for Q3FY18 mainly led by SA deposits. Daily

avg CASA continues show strong growth.

NIMs:

Margins came off further by 7bps QoQ to 3.38% mainly on increase in cost of

funds and yields on advances were flat sequentially. Outlook – Continue to

maintain compression of ~20bps in range of 3.4‐3.5% (19bps in 9MFY18) over

the FY from exit at 3.67% in FY17.

Fees:

Fee – Fees growth was driven by retail which constitutes 49% of fees and grew

by 35% YoY and transaction fees which now constitute 28% of fees grew by 23%

YoY. Within retail, card fees continue to show strong traction.

Asset Quality:

Stressed asset accretion – Bank witnessed Rs44.3bn of slippages of which 67%

came from corporate book of Rs29.3bn of which ~68% of slippages belonged to

watchlist & 93% from the BB & below pool. Retail slippages were slightly higher

on some seasonality. Bank witnessed cash recovery from IT/ITES A/c and one

steel A/c got upgraded during the quarter which was recognized as NPA as per

RBI divergence in Q2FY18. Bank also sold one NPA a/c from the NCLT list to non‐

ARC on cash basis with 40% haircut.

Watch list Details – Watch list has reduced from 1.5% to 1.3% of loan book

(2.5% as on FY17). Rs20bn slippages were seen from the watch list and the

funded watch list currently stands at Rs53bn. Power sector continues to

dominates the watch list with 67% share. Non Fund watch list stands at Rs8.1bn.

January 23, 2018 4

Axis Bank

BB & Below book – Exposure slightly increased to Rs161.2bn from Rs158.2bn in

Q2FY18 which is funded exposure and ~Rs50.0bn of non‐funded exposure. This

includes 100% of watch list and ~35% of Restructured Dispensations (incl SDR,

5:25 & S4A). Top 3 sectors that constitute 60% of this stressed asset book are

Power (35%), Infra Construction (30‐35%), and Iron and Steel. Bank has been

seeing as a trend of Rs20‐30bn down‐gradation to BB & Below since past 5

quarters

Power exposure has reduced to Rs160bn of which 36% is in BB & below category

and 30% is in BBB Category.

Credit Cost – Bank has done incremental provisioning of Rs2.4bn on the IBC

accounts taking PCR on IBC accounts to 68%. Bank continues to expect LGD to

remain elevated in this cycle and could be around 65%. Bank has no contingent

provisions. Outlook & guidance – Bank maintains the credit cost guidance at

220‐260bps for FY18 and expect it to improve in the latter half of FY19.

Others:

Bank has raised Rs86.8bn equity capital and Rs35bn AT1 bonds thus improving

Tier 1 Ratio to 14.13% from 12.36% in Q2FY18.

The warrants issued at Rs565 in Q3FY18 have validity of 18 months and the

same will expire on June, 2019.

The management expects the credit costs to start moving towards the

normalised levels by the second half of FY19.

Exhibit 2: Growth is led by retail mainly from Auto and unsecured segments and SME; while corporate book growth also picked up with demand in working capital

(Rs m) Q3FY18 Q3FY17 YoY gr. (%) Q2FY18 QoQ gr. (%)

Large & mid‐corporate 17,27,430 15,44,290 11.9 17,31,970 (0.3)

SME Advances 5,48,840 4,32,080 27.0 5,27,180 4.1

Retail 19,32,960 14,95,380 29.3 18,42,560 4.9

‐ Housing Loans & LAP 8,11,843 7,02,829 15.5 7,92,301 2.5

‐ Personal loans 1,93,296 1,79,446 7.7 1,65,830 16.6

‐ Auto loans 1,93,296 1,49,538 29.3 1,84,256 4.9

Source: Company Data, PL Research

January 23, 2018 5

Axis Bank

Exhibit 1: Margins saw pressure on continued decline in yields

3.3%

3.4%

3.5%

3.6%

3.7%

3.8%

3.9%

4.0%

4.1%

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

NIM (%)

Source: Company Data, PL Research

ibit 2: CASA ratio was stable influenced by demonetisation effect

40%

42%

44%

46%

48%

50%

52%

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

Low Cost deposits(%)

Source: Company Data, PL Research

Exhibit 3: MCLR linked loans has made big shift from base rate partly impacting yields

69% 65%57% 50%

42%34% 29% 24%

4%11% 18% 29%

36% 40% 43%

17% 17% 17% 16% 15% 16% 17% 19%

14% 14% 15% 16% 14% 14% 14% 14%

4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Base Rate MCLR Fixed LIBOR

Source: Company Data, PL Research

Exhibit 4: Retail fees dominate and continues to see strong growth mainly led by TPP and card related fees; transaction fees also grew better

26% 29% 26% 28% 28% 30% 29% 30% 30%

14% 13% 16% 15% 17% 16% 19% 18% 19%

20% 16%27% 26% 29% 22%

26% 26% 28%5% 6%4% 5%

5% 6%4% 4% 5%

10% 10%2% 1%

1%2%

4% 1%1%

25% 26% 25% 25% 20% 24% 18% 21% 17%

3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Retail (non card) Retail (card) Transc. BnkingSME Treasry & DCM Corp Fees

Source: Company Data, PL Research

January 23, 2018 6

Axis Bank

Exhibit 5: C/I ratio slightly spiked up on lower total income led by lower treasury gains whereas opex has improved to 12% YoY

34%

36%

38%

40%

42%

44%

46%

48%

50%

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

cost‐income

Source: Company Data, PL Research

Exhibit 6: Asset quality improved on higher recoveries/upgrades in spite of high slippages

0%

10%

20%

30%

40%

50%

60%

70%

80%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

Gross NPA (%) Net NPA (%) Coverage Ratio (%) ‐ RHS

Source: Company Data, PL Research

Exhibit 7: Incremental loans going towards better rated corporate

62% 62% 61% 61% 61% 60% 62% 60% 61% 62% 62% 64% 63% 63% 66% 68% 70% 74%

32% 31% 30% 31% 30% 31% 29% 29% 28% 27% 26% 20% 22% 23% 22% 22% 19% 17%

7% 7% 9% 8% 9% 9% 9% 11% 11% 11% 12% 16% 15% 14% 12% 10% 11% 9%

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

AAA/AA/A BBB <BB or unrated

Source: Company Data, PL Research

January 23, 2018 7

Axis Bank

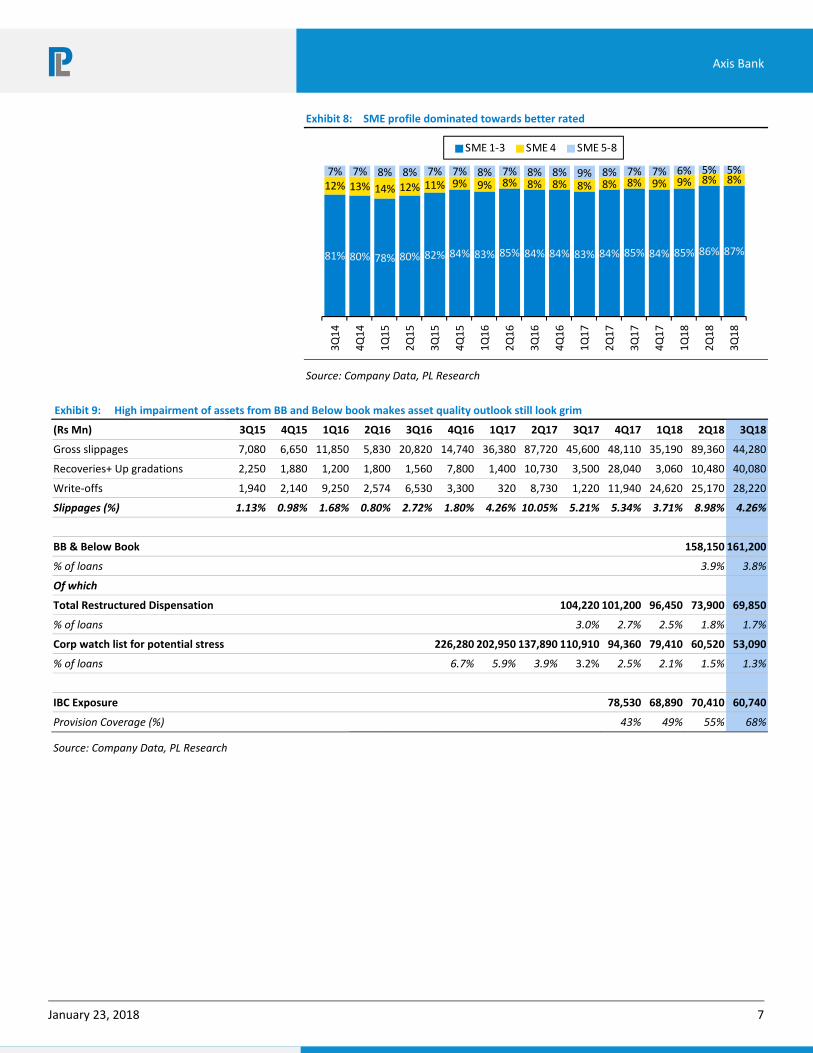

Exhibit 8: SME profile dominated towards better rated

81% 80% 78% 80% 82% 84% 83% 85% 84% 84% 83% 84% 85% 84% 85% 86% 87%

12% 13% 14% 12% 11% 9% 9% 8% 8% 8% 8% 8% 8% 9% 9% 8% 8%7% 7% 8% 8% 7% 7% 8% 7% 8% 8% 9% 8% 7% 7% 6% 5% 5%

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

4Q16

1Q17

2Q17

3Q17

4Q17

1Q18

2Q18

3Q18

SME 1‐3 SME 4 SME 5‐8

Source: Company Data, PL Research

Exhibit 9: High impairment of assets from BB and Below book makes asset quality outlook still look grim

(Rs Mn) 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18

Gross slippages 7,080 6,650 11,850 5,830 20,820 14,740 36,380 87,720 45,600 48,110 35,190 89,360 44,280

Recoveries+ Up gradations 2,250 1,880 1,200 1,800 1,560 7,800 1,400 10,730 3,500 28,040 3,060 10,480 40,080

Write‐offs 1,940 2,140 9,250 2,574 6,530 3,300 320 8,730 1,220 11,940 24,620 25,170 28,220

Slippages (%) 1.13% 0.98% 1.68% 0.80% 2.72% 1.80% 4.26% 10.05% 5.21% 5.34% 3.71% 8.98% 4.26%

BB & Below Book 158,150 161,200

% of loans 3.9% 3.8%

Of which

Total Restructured Dispensation 104,220 101,200 96,450 73,900 69,850

% of loans 3.0% 2.7% 2.5% 1.8% 1.7%

Corp watch list for potential stress 226,280 202,950 137,890 110,910 94,360 79,410 60,520 53,090

% of loans 6.7% 5.9% 3.9% 3.2% 2.5% 2.1% 1.5% 1.3%

IBC Exposure 78,530 68,890 70,410 60,740

Provision Coverage (%) 43% 49% 55% 68%

Source: Company Data, PL Research

January 23, 2018 8

Axis Bank

Exhibit 10: Watch list contribution was higher this quarter in accretion of stressed assets

Watch list sectors (Rs mn) Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18

Power 54,307 54,797 56,535 54,346 56,616 54,793 38,733 35,570

Iron & Steel 52,044 52,767 16,547 16,637 6,605 6,353 6,657 6,371

Textiles 15,840 14,207 ‐ ‐ ‐ ‐ ‐ ‐

Infra Construction 11,314 12,177 11,031 8,873 4,718 3,971 3,631 3,716

Oil and Gas 13,577 12,177 17,926 6,655 6,605 ‐ ‐ ‐

CRE 9,051 8,118 ‐ ‐ ‐ ‐ ‐ ‐

Cement 9,051 6,089 6,895 6,655 5,662 1,588 ‐ ‐

Shipping 6,788 6,089 ‐ 2,218 1,887 ‐ ‐ ‐

Mining 11,314 6,089 ‐ ‐ ‐ ‐ ‐ ‐

Industrials ‐ 6,089 5,516 1,109 944 794 ‐ ‐

Engineering 4,137 4,436 3,774 3,971 4,236 1,593

Infrastructure Roads 4,137 4,436 3,774 3,176 3,026 3,185

Construction other than Infra 2,758 3,327 3,774 2,382 605 531

Telecom 2,758 ‐ ‐ ‐ 2,421 2,124

Services 13,577 ‐ ‐ ‐ ‐ ‐ ‐ ‐

Trade Retail & Wholesale 794 1,210 ‐

TOTAL 226,280 202,950 137,890 110,910 94,360 79,410 60,520 53,090

% of loans 6.7% 5.9% 3.9% 3.2% 2.5% 2.1% 1.5% 1.3%

Slippages from watch list 25,790 72,880 25,790 35,660 7,970 24,300 20,124

Slippages from outside watch list 3,340 9,050 11,070 7,540 15,200 56,800 9,676

Watch list slippages to total 71% 83% 57% 74% 34% 30% 68%

Outside watch list corporate slippages to total 9% 10% 24% 16% 66% 70% 32%

Source: Company Data, PL Research

Exhibit 11: ~54% of watchlist has overlap with restructured dispensations (incl. SDR, 5:25, S4A)

Various stressed assets overlapping with watchlist

Q3FY17 Q4FY17 Q1FY18 Q2FY18 Q3FY18

Normal Watch list 52.0% 49.8% 42.7% 44.6% 45.7%

Overlapped watch list 48.0% 50.2% 57.3% 55.4% 54.3%

SDR & Restructured Overlap 2.4% 1.9% 2.2%

5/25 & Restructured Overlap 1.2% 4.5%

SDR 5.3% 12.6% 15.3%

5/25 Refinancing 9.0% 2.8% 3.0%

Restructured 31.3% 31.8% 34.6%

Source: Company Data, PL Research

January 23, 2018 9

Axis Bank

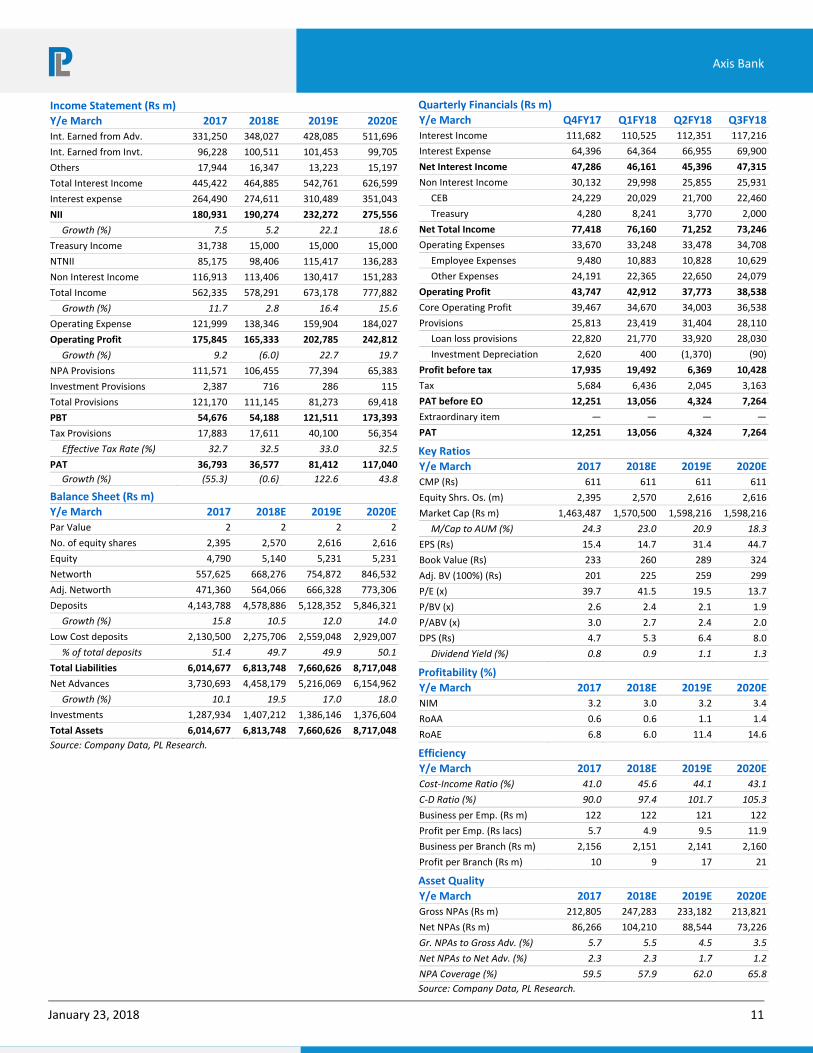

Exhibit 12: Slippages have mainly come from watchlist for this quarter

Sectoral Distribution of Corporate Slippages (Rs mn) Q2FY18 Q3FY18 % Mix

Total Corporate Slippages 81,100 29,800 100%

Power Gen & Distribution 23,519 7,450 25%

Iron & Steel 15,409 5,960 20%

IT & ITES 11,354 ‐

Engineering & Electronics 5,677 4,470 15%

Infrastructure Cons. & Roads 4,055 3,874 13%

Chemicals & Chemical Products 4,055 ‐

Cement & Cement Products 4,055 ‐

Sugar 3,244 596 2%

Shipping Transportation ‐ 1,192 4%

Trade ‐ 1,192 4%

Real Estate 2,433 1,192 4%

Paper & Paper Products 2,433 ‐

Food Processing 1,622 1,788 6%

Mining and Mining Products ‐ 596 2%

Entertainment & Media ‐ 596 2%

Source: Company Data, PL Research

Exhibit 13: Change in estimates table – We slightly tweak our estimates on yields and treasury gains

(Rs mn) Old Revised % Change

FY18E FY19E FY20E FY18E FY19E FY20E FY18E FY19E FY20E

Net interest income 1,98,370 2,31,023 2,75,656 1,90,274 2,32,272 2,75,556 (4.1) 0.5 (0.0)

Operating profit 1,92,589 2,23,703 2,66,632 1,65,333 2,02,785 2,42,812 (14.2) (9.4) (8.9)

Net profit 49,360 92,346 1,29,882 36,577 81,413 1,17,041 (25.9) (11.8) (9.9)

EPS (Rs) 19.9 35.6 49.7 14.7 31.4 44.7 (25.9) (11.8) (9.9)

ABVPS (Rs) 221.8 262.7 306.5 225.0 259.0 298.7 1.5 (1.4) (2.5)

Price target (Rs) 654 651 (0.5)

Recommendation BUY BUY

Source: Company Data, PL Research

January 23, 2018 10

Axis Bank

Exhibit 14: We maintain our BUY stance with TP of Rs651 (fromRs654) based on 2.3x Sep‐19 ABV

PT calculation and upside

Fair price ‐ EVA 643

Fair price ‐ P/ABV 659

Average of the two 651

Target P/ABV 2.3

Target P/E 17.1

Current price, Rs 612

Upside (%) 6%

Dividend yield (%) 1%

Total return (%) 8%

Source: Company Data, PL Research

Exhibit 15: AXSB’s historical P/ABV trends – Trading at mean levels

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan‐12

Apr‐12

Jul‐12

Oct‐12

Jan‐13

Apr‐13

Jul‐13

Oct‐13

Jan‐14

Apr‐14

Jul‐14

Oct‐14

Jan‐15

Apr‐15

Jul‐15

Oct‐15

Jan‐16

Apr‐16

Jul‐16

Oct‐16

Jan‐17

Apr‐17

Jul‐17

Oct‐17

Jan‐18

P/ABV 3 yr avg. avg. + 1 SD avg. ‐ 1 SD

Source: Company Data, PL Research

January 23, 2018 11

Axis Bank

Income Statement (Rs m)

Y/e March 2017 2018E 2019E 2020E

Int. Earned from Adv. 331,250 348,027 428,085 511,696

Int. Earned from Invt. 96,228 100,511 101,453 99,705

Others 17,944 16,347 13,223 15,197

Total Interest Income 445,422 464,885 542,761 626,599

Interest expense 264,490 274,611 310,489 351,043

NII 180,931 190,274 232,272 275,556

Growth (%) 7.5 5.2 22.1 18.6

Treasury Income 31,738 15,000 15,000 15,000

NTNII 85,175 98,406 115,417 136,283

Non Interest Income 116,913 113,406 130,417 151,283

Total Income 562,335 578,291 673,178 777,882

Growth (%) 11.7 2.8 16.4 15.6

Operating Expense 121,999 138,346 159,904 184,027

Operating Profit 175,845 165,333 202,785 242,812

Growth (%) 9.2 (6.0) 22.7 19.7

NPA Provisions 111,571 106,455 77,394 65,383

Investment Provisions 2,387 716 286 115

Total Provisions 121,170 111,145 81,273 69,418

PBT 54,676 54,188 121,511 173,393

Tax Provisions 17,883 17,611 40,100 56,354

Effective Tax Rate (%) 32.7 32.5 33.0 32.5

PAT 36,793 36,577 81,412 117,040

Growth (%) (55.3) (0.6) 122.6 43.8

Balance Sheet (Rs m)

Y/e March 2017 2018E 2019E 2020E

Par Value 2 2 2 2

No. of equity shares 2,395 2,570 2,616 2,616

Equity 4,790 5,140 5,231 5,231

Networth 557,625 668,276 754,872 846,532

Adj. Networth 471,360 564,066 666,328 773,306

Deposits 4,143,788 4,578,886 5,128,352 5,846,321

Growth (%) 15.8 10.5 12.0 14.0

Low Cost deposits 2,130,500 2,275,706 2,559,048 2,929,007

% of total deposits 51.4 49.7 49.9 50.1

Total Liabilities 6,014,677 6,813,748 7,660,626 8,717,048

Net Advances 3,730,693 4,458,179 5,216,069 6,154,962

Growth (%) 10.1 19.5 17.0 18.0

Investments 1,287,934 1,407,212 1,386,146 1,376,604

Total Assets 6,014,677 6,813,748 7,660,626 8,717,048

Source: Company Data, PL Research.

Quarterly Financials (Rs m)

Y/e March Q4FY17 Q1FY18 Q2FY18 Q3FY18

Interest Income 111,682 110,525 112,351 117,216

Interest Expense 64,396 64,364 66,955 69,900

Net Interest Income 47,286 46,161 45,396 47,315

Non Interest Income 30,132 29,998 25,855 25,931

CEB 24,229 20,029 21,700 22,460

Treasury 4,280 8,241 3,770 2,000

Net Total Income 77,418 76,160 71,252 73,246

Operating Expenses 33,670 33,248 33,478 34,708

Employee Expenses 9,480 10,883 10,828 10,629

Other Expenses 24,191 22,365 22,650 24,079

Operating Profit 43,747 42,912 37,773 38,538

Core Operating Profit 39,467 34,670 34,003 36,538

Provisions 25,813 23,419 31,404 28,110

Loan loss provisions 22,820 21,770 33,920 28,030

Investment Depreciation 2,620 400 (1,370) (90)

Profit before tax 17,935 19,492 6,369 10,428

Tax 5,684 6,436 2,045 3,163

PAT before EO 12,251 13,056 4,324 7,264

Extraordinary item — — — —

PAT 12,251 13,056 4,324 7,264

Key Ratios

Y/e March 2017 2018E 2019E 2020E

CMP (Rs) 611 611 611 611

Equity Shrs. Os. (m) 2,395 2,570 2,616 2,616

Market Cap (Rs m) 1,463,487 1,570,500 1,598,216 1,598,216

M/Cap to AUM (%) 24.3 23.0 20.9 18.3

EPS (Rs) 15.4 14.7 31.4 44.7

Book Value (Rs) 233 260 289 324

Adj. BV (100%) (Rs) 201 225 259 299

P/E (x) 39.7 41.5 19.5 13.7

P/BV (x) 2.6 2.4 2.1 1.9

P/ABV (x) 3.0 2.7 2.4 2.0

DPS (Rs) 4.7 5.3 6.4 8.0

Dividend Yield (%) 0.8 0.9 1.1 1.3

Profitability (%)

Y/e March 2017 2018E 2019E 2020E

NIM 3.2 3.0 3.2 3.4

RoAA 0.6 0.6 1.1 1.4

RoAE 6.8 6.0 11.4 14.6

Efficiency

Y/e March 2017 2018E 2019E 2020E

Cost‐Income Ratio (%) 41.0 45.6 44.1 43.1

C‐D Ratio (%) 90.0 97.4 101.7 105.3

Business per Emp. (Rs m) 122 122 121 122

Profit per Emp. (Rs lacs) 5.7 4.9 9.5 11.9

Business per Branch (Rs m) 2,156 2,151 2,141 2,160

Profit per Branch (Rs m) 10 9 17 21

Asset Quality

Y/e March 2017 2018E 2019E 2020E

Gross NPAs (Rs m) 212,805 247,283 233,182 213,821

Net NPAs (Rs m) 86,266 104,210 88,544 73,226

Gr. NPAs to Gross Adv. (%) 5.7 5.5 4.5 3.5

Net NPAs to Net Adv. (%) 2.3 2.3 1.7 1.2

NPA Coverage (%) 59.5 57.9 62.0 65.8

Source: Company Data, PL Research.

January 23, 2018 12

Axis Bank

Prabhudas Lilladher Pvt. Ltd.

3rd Floor, Sadhana House, 570, P. B. Marg, Worli, Mumbai‐400 018, India

Tel: (91 22) 6632 2222 Fax: (91 22) 6632 2209

Rating Distribution of Research Coverage PL’s Recommendation Nomenclature

43.4% 44.2%

12.4%

0.0%0%

10%

20%

30%

40%

50%

BUY Accumulate Reduce Sell

% of Total Coverage

BUY : Over 15% Outperformance to Sensex over 12‐months

Accumulate : Outperformance to Sensex over 12‐months

Reduce : Underperformance to Sensex over 12‐months

Sell : Over 15% underperformance to Sensex over 12‐months

Trading Buy : Over 10% absolute upside in 1‐month

Trading Sell : Over 10% absolute decline in 1‐month

Not Rated (NR) : No specific call on the stock

Under Review (UR) : Rating likely to change shortly

DISCLAIMER/DISCLOSURES

ANALYST CERTIFICATION

We/I, Mr. R Sreesankar (B.Sc ), Mr. Pritesh Bumb (MBA, M.com), Ms. Vidhi Shah (CA), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

Prabhudas Lilladher Pvt. Ltd, Mumbai, India (hereinafter referred to as “PL”) is engaged in the business of Stock Broking, Portfolio Manager, Depository Participant and distribution for third party financial products. PL is a subsidiary of Prabhudas Lilladher Advisory Services Pvt Ltd. which has its various subsidiaries engaged in business of commodity broking, investment banking, financial services (margin funding) and distribution of third party financial/other products, details in respect of which are available at www.plindia.com

This document has been prepared by the Research Division of PL and is meant for use by the recipient only as information and is not for circulation. This document is not to be reported or copied or made available to others without prior permission of PL. It should not be considered or taken as an offer to sell or a solicitation to buy or sell any security.

The information contained in this report has been obtained from sources that are considered to be reliable. However, PL has not independently verified the accuracy or completeness of the same. Neither PL nor any of its affiliates, its directors or its employees accepts any responsibility of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The suitability or otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt, advice should be sought from an independent expert/advisor.

Either PL or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market, act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior to publication.

PL may from time to time solicit or perform investment banking or other services for any company mentioned in this document.

PL is in the process of applying for certificate of registration as Research Analyst under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

PL submits that no material disciplinary action has been taken on us by any Regulatory Authority impacting Equity Research Analysis activities.

PL or its research analysts or its associates or his relatives do not have any financial interest in the subject company.

PL or its research analysts or its associates or his relatives do not have actual/beneficial ownership of one per cent or more securities of the subject company at the end of the month immediately preceding the date of publication of the research report.

PL or its research analysts or its associates or his relatives do not have any material conflict of interest at the time of publication of the research report.

PL or its associates might have received compensation from the subject company in the past twelve months.

PL or its associates might have managed or co‐managed public offering of securities for the subject company in the past twelve months or mandated by the subject company for any other assignment in the past twelve months.

PL or its associates might have received any compensation for investment banking or merchant banking or brokerage services from the subject company in the past twelve months.

PL or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past twelve months

PL or its associates might have received any compensation or other benefits from the subject company or third party in connection with the research report.

PL encourages independence in research report preparation and strives to minimize conflict in preparation of research report. PL or its analysts did not receive any compensation or other benefits from the subject Company or third party in connection with the preparation of the research report. PL or its Research Analysts do not have any material conflict of interest at the time of publication of this report.

It is confirmed that Mr. R Sreesankar (B.Sc ), Mr. Pritesh Bumb (MBA, M.com), Ms. Vidhi Shah (CA), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

The Research analysts for this report certifies that all of the views expressed in this report accurately reflect his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report.

The research analysts for this report has not served as an officer, director or employee of the subject company PL or its research analysts have not engaged in market making activity for the subject company

Our sales people, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all o the foregoing, among other things, may give rise to real or potential conflicts of interest.

PL and its associates, their directors and employees may (a) from time to time, have a long or short position in, and buy or sell the securities of the subject company or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the subject company or act as an advisor or lender/borrower to the subject company or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.

DISCLAIMER/DISCLOSURES (FOR US CLIENTS)

ANALYST CERTIFICATION

The research analysts, with respect to each issuer and its securities covered by them in this research report, certify that: All of the views expressed in this research report accurately reflect his or her or their personal views about all of the issuers and their securities; and No part of his or her or their compensation was, is or will be directly related to the specific recommendation or views expressed in this research report

Terms & conditions and other disclosures:

This research report is a product of Prabhudas Lilladher Pvt. Ltd., which is the employer of the research analyst(s) who has prepared the research report. The research analyst(s) preparing the research report is/are resident outside the United States (U.S.) and are not associated persons of any U.S. regulated broker‐dealer and therefore the analyst(s) is/are not subject to supervision by a U.S. broker‐dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

This report is intended for distribution by Prabhudas Lilladher Pvt. Ltd. only to "Major Institutional Investors" as defined by Rule 15a‐6(b)(4) of the U.S. Securities and Exchange Act, 1934 (the Exchange Act) and interpretations thereof by U.S. Securities and Exchange Commission (SEC) in reliance on Rule 15a 6(a)(2). If the recipient of this report is not a Major Institutional Investor as specified above, then it should not act upon this report and return the same to the sender. Further, this report may not be copied, duplicated and/or transmitted onward to any U.S. person, which is not the Major Institutional Investor.

In reliance on the exemption from registration provided by Rule 15a‐6 of the Exchange Act and interpretations thereof by the SEC in order to conduct certain business with Major Institutional Investors, Prabhudas Lilladher Pvt. Ltd. has entered into an agreement with a U.S. registered broker‐dealer, Marco Polo Securities Inc. ("Marco Polo").

Transactions in securities discussed in this research report should be effected through Marco Polo or another U.S. registered broker dealer.