beyond 2010 - ppc ltd. interim results 31 march 2009...1 pretoria portland cement company limited...

TRANSCRIPT

1

Pretoria Portland Cement Company Limited

Beyond 2010Unaudited interim results

for the half-year ended 31 March 2009

2

2009 – A TALE OF 2 HALVES

1ST HALF 2009

Picture

• Group financial overview• Cement

• Market• Production and costs• Capital projects

• Lime and aggregates

Precast Yard for the Gautrain

3

H1 2009 - Financial Highlights

• Revenue R3.26bn 12% [R2.92bn]

• EBITDA* R1.24bn 5% [R1.18bn]

• EBITDA margin* 38.2% [40.5%]

• Cash generated from operations R1.03bn (7%) [R1.11bn]

• Operating profit* R1.10bn 2% [R1.08bn]

• Interim dividend 45 cps [45 cps]

* Excluding impact of the BBBEE IFRS 2 charges

4

H1 2009 – Summary Income Statement

2009R million

2008R million

% Change

Revenue 3 261 2 919 12

EBITDA 1 245 1 181 5

Depreciation and amortisation (145) (104) 38

BBBEE IFRS 2 charges (487) -

Operating profit 613 1 077 (43)

Finance costs (180) (57) (216)

Investment income 39 59 (34)

Profit before exceptional items 472 1 079 (56)

Exceptional items - 1

Share of associate’s retained profit 4 7

Taxation (363) (413) (12)

Profit for the period 113 674 (83)

HEPS (cents) (excluding BBBEE IFRS 2 charges) 105.4 125.6 (16)

CASH EARNINGS PER SHARE (cents) (excl. BBBEE IFRS 2 charges) 101.4 104.3 (3)

DPS (cents) 45 45 -

5

H1 2009 – Summary Balance Sheet

ASSETS2009

R million2008

R million

Non-current assetsProperty, plant and equipment 3 114 2 487Other 384 398

Current assets Inventories 482 336Trade and other receivables 857 756Cash and cash equivalents 374 468

TOTAL ASSETS 5 211 4 445EQUITY AND LIABILITIES Capital and reserves 166 1 298

Non-current liabilities

Long-term borrowings 2 627 68

Deferred taxation 340 165

Provisions and other non-current liabilities 207 127

Current liabilities Short-term borrowings 1 237 2 161

Trade and other payables 634 626TOTAL EQUITY AND LIABILITIES 5 211 4 445

6

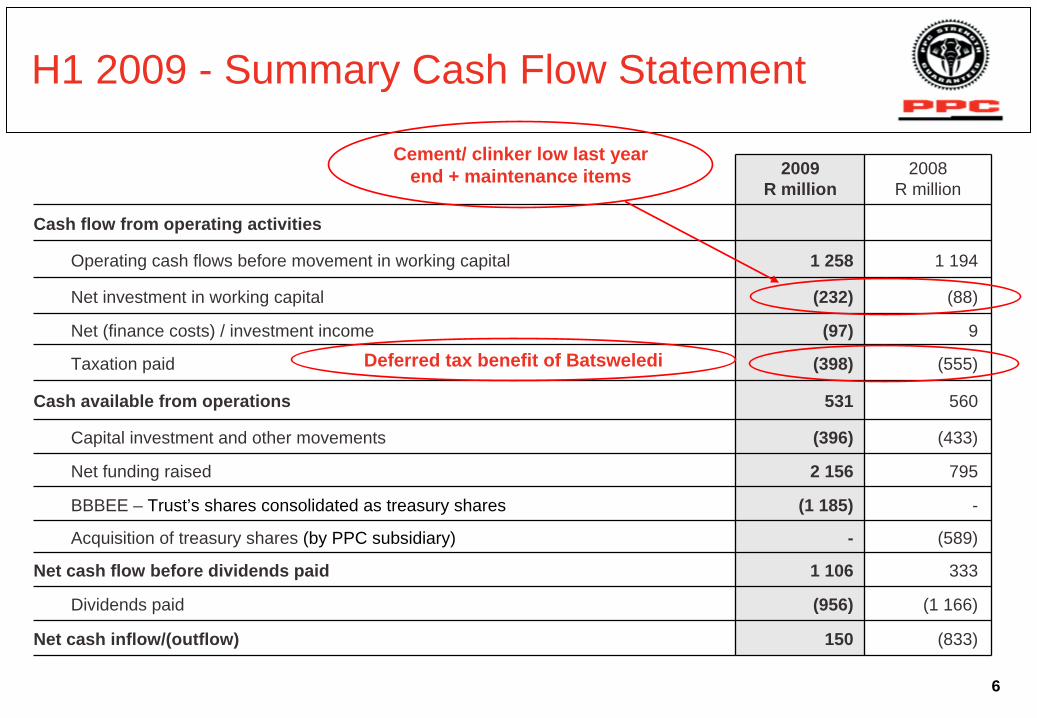

H1 2009 - Summary Cash Flow Statement

2009R million

2008R million

Cash flow from operating activities

Operating cash flows before movement in working capital 1 258 1 194

Net investment in working capital (232) (88)

Net (finance costs) / investment income (97) 9

Taxation paid (398) (555)

Cash available from operations 531 560

Capital investment and other movements (396) (433)

Net funding raised 2 156 795

BBBEE – Trust’s shares consolidated as treasury shares (1 185) -

Acquisition of treasury shares (by PPC subsidiary) - (589)

Net cash flow before dividends paid 1 106 333

Dividends paid (956) (1 166)

Net cash inflow/(outflow) 150 (833)

Deferred tax benefit of Batsweledi

Cement/ clinker low last year end + maintenance items

7

• HEPS -16% (excl. BEE charges)

• Sales volumes• Regional cement sales -6%• Lime burnt product -36% and Operating Profit down 60%

• Input cost pressures peaked• Cement R/t delivered cost ~24% Y-on-Y (but moving down)

• Operations• Dwaalboom kiln2 performing - 3 old inland kilns shut-down to match demand

• Cash finance charges/ investment income (net):• R97m on increased borrowings – mainly expansion projects related

H1 2009 – Financial Overview

• Continued strong cash generation• Cash generated from operations and EBITDA +5%

8

H1 2009 - Segmental Analysis*

n.b. Dwaalboom K2 depreciation R32m 2009R million

2008R million

% change 2008Year

Cement

EBITDA 1 168 1 056 10.6% 2 281

EBITDA margin 40.3% 42.0% -1.7% pts 42.5%

Operating profit 1 043 970 +7.5% 2 100

Lime

EBITDA 46 90 -48.9% 167

EBITDA margin 19.2% 31.4% -12.2% pts 27.9%

Operating profit 31 77 -60% 141

Aggregates

EBITDA 31 35 -11.4% 93

EBITDA margin 25.0% 28.9% -3.9% pts 33.1%

Operating profit 26 30 -13% 82

GROUP

EBITDA 1 245 1 181 +5.4% 2 541

EBITDA margin 38.2% 40.5% -2.3% pts 40.7%

Operating profit 1 100 1 077 +2.1% 2 323

* Excluding impact of BBBEE IFRS 2 charges

9

H1 2009 - Cement – Industry Regional Sales

• Regional industry cement volumes for the 6 months down 7.5%

• Mpumalanga +8.6%, Botswana +14.2%

• Gauteng -15.5%, Western Cape -21.0%

• Construction sector +12% indicating demand from infrastructure projects

• Number of infrastructure projects now taking cement

• Medupi power station & area (H1 ~50 000 tons), Gauteng, Mpumalanga & Limpopo road upgrades

• Major projects recently started

• Kusile power station, Ingula pumped storage

• Industry clinker and cement imports down to almost nothing

10

H1 2009 - Cement – Industry Imports

Cement and Clinker Imports

20

40

60

80

100

120

140

160

180

Mar-07

May-07

Jul-07

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

kt

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%Clinker

Cement

% of Regional Sales

700kt less imports in period under review = 11% of regional sales

11

H1 2009 - Cement – PPC Regional Sales

• PPC Regional sales -6%

• Preferred supplier to most major infrastructure projects

• Re-entered some exports markets – but Rand strength making it less profitable

• Partially offset decline in the coastal markets

• Sold 23 000 tons clinker

• Dwaalboom kiln 2 production allowed the planned shutdown of 3 older kilns

• Jupiter, Hercules kilns 4 & 5

• average 39 yrs old

• De Hoek kiln 5 running intermittently – lower demand in Western Cape

12

H1 2009 – PPC - Cement - Input Cost Increases

Ranked in order of total impact –Rand/ ton cement

% change vs H1 ‘08

Road distribution costs 24%

(Diesel) 13%

Coal (delivered) 63%

Maintenance 28%

Packaging 25%

ESKOM/ Municipal Power 39%

13

H1 2009 – Cement – Distribution cost increase

• Complex logistics in Q1 –• Market tightness generally made optimisation difficult• Transported cement from the W. Cape when inland competitor shortage developed

in Nov & Dec’08

• Excess dedicated transport fleet – has been downsized to match demand• Some diesel reduction has been gained since January/ February• Market transport rates have recently been trending softer (other than diesel

costs)

14

H1 2009 - Dwaalboom Kiln 2 Progress

• Finished cost will be within budget• Regularly achieves daily output above

design capacity • To April kiln has produced 400 000t of

clinker (500 000 tons cement equivalent)

• Achieved 83% availability in April• Cash cost benefits exciting! Covered

on slide 22

Dwaalboom Kiln 2

15

H1 2009 - Capital Projects Progress

• Ntšhafatso (Hercules) mill upgrade• 330 kt/yr additional capacity• Construction delays• Output now only expected FY10• Capex increase of R95 m -

• Geotechnical/ piling problems• Major escalations in contracts• Clinker silo/ congested area delays• Some increased scope

• Se Kïka (Riebeeck West) new 1,25mt/yr factory

• Nett additional capacity 700 kt/yr• EIA report submitted, approvals

awaited• Limited Capex likely in 2010

New Vertical Roller Mill – Hercules

16

H1 2009 - Lime and Aggregates

• Burnt product sales -36% due to lower demand from steel• Q1 worst affected in line with lowest steel producing quarter• Improvement expected in H2 09 as destocking cycle concludes• World Steel Association predicting 2009 global demand decline at -14.9%

• Recent significant energy cost increases being recovered through long term supply contracts price adjustments

• Aggregate volumes -10%• Reduced demand for metallurgical stone from steel industry• Tighter market in Gauteng partially offset by demand from road construction• Strong demand experienced in Botswana partially off-setting Gauteng decline

17

2009 – A TALE OF 2 HALVES

2nd HALF 2009 Prospects

• Financial overview• Cement

• Market• Production and costs• Capital projects

• Lime and aggregates

• Dividends and gearing

Nelson Mandela Stadium – Port Elizabeth

18

2009 - Prospects – Regional Cement Demand

• Civil Construction• R787bn Government infrastructure spend over next 3 years• New regime must now deliver on housing and services

• Tokyo Sexwale appointment to head up Dept. of Human Settlement• Housing Development Agency created and funded to acquire land

• Major infrastructure projects in progress or about to start

• Building - Residential• Interest rates 3.5 percentage points off peak, still very high real interest rates and encouraging

carry trade funds creating Rand strength• Further interest rate cuts inevitable? Or exports and especially mining will continue to shrink• SARB concerned about debt stressed consumers

• Building – Non residential • Hotels (10 City Lodges for 2010 World Cup, 3 hotels for Langa Sun Resort Hotels)• Mixed use developments incl. residential (Cradle City R35bn over 7 years)• New & upgraded retail developments

19

2009 - Prospects – Industry Cement Regional Sales/Day to April 2009

Industry Regional Sales Per Day

40

45

50

55

60

65

70

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

kt

2007 2008 2009

PPC Regional Daily Sales - April 2008

5

10

15

20

25

01-Apr

03-Apr

05-Apr

07-Apr

09-Apr

11-Apr

13-Apr

15-Apr

17-Apr

19-Apr

21-Apr

23-Apr

25-Apr

27-Apr

29-Apr

Public Holidays

We anticipate Regional Industry Cement sales won’t

decline by more than 10% this financial year compared to

2008.

20

2009 - Prospects – Market Intelligence

Building Plans Passed 2008Category Sub Category Value (R m)

% Value Cement*

Cement (000 tons)**

Residential

Dwelling-houses < 80 square metres 2 775 6.1 169

Dwelling-houses >= 80 square metres 19 902 5.9 1 174

Flats and townhouses 12 883 1.1 142

Other residential buildings 1 527 2.6 40

Non-residential

Office and banking space 4 669 2.4 110

Shopping space 5 650 1.6 90

Industrial and warehouse space 6 562 2.6 171

Other non-residential buildings 1 145 2.2 25

Additions &Alterations

Dwelling-houses 14 287 2.6 371

Other buildings 7 670 2.6 199

Total 77 069 2 491

Total SA Cement Consumed 13 472

Cement in Building Plans Passed as % of total SA cement sales 18%

* University of the Witwatersrand Study 2006 and 2008

** Calculated using a weighted average selling price of bags and bulk, delivered and through retail outlets

21

2009 - Prospects - Supply and Demand

10

12

14

16

18

20

22

2006 2007 2008 2009 2010 2011

Mt

Growth 7.4% -3.9% -10%? 0%? 6%?

PPC 1.25Mt/yr, Cimpor 0.6Mt/Yr: (2009)Lafarge 1Mt/yr (2010)

PPC Mill 0.3Mt/yr (2010)

Contracted / Building

Completed

Industry DemandIndustry Maximum Capacity- - - (Old PPC Kilns Retired)

Latest Revision : May 2009

Imports 92% Utilisation

22

2009 - Prospects – Cement – Costs/ Margins

• Potential cement cash cost savings in H2• Dwaalboom

• coal and electricity energy efficiency improvements between 20 – 25% vs the 3 kilns shut- down

• kiln total cash cost saving could benefit cement annual EBITDA % margin by the equivalent of 0.7 to 0.9 percentage points (pp)

• Balance of cement production• Distribution costs, mining diesel, coal savings and reduced maintenance load in H2 after

completing most annual shut-downs in H1• could add a further 1.2 to 1.6 pp to cement annual EBITDA % margin

• Focus is on extracting all possible savings no matter how small• Should the strong Rand continue throughout H2 further cost savings could arise, but we

should be cautious

23

2009 - Prospects – Cement Costs/ Margins cont.

• Further meaningful cost reductions can be expected in 2010 and especially from falling coal prices and transport costs

• The benefit of the lower Dwaalboom cash cost will be in for a full year

• Cement prices• Whereas only Q2 had the benefit of the January ~15% cost recovery price increase,

H2 will have the benefit for rest of year

• In view of expected cost reductions and the current economic situation, it is possible that the normal mid year selling price increase may be deferred

24

• Lime sales to the steel industry should improve in H2 and early signs have been seen. It will be sometime before they get back to early 2008 levels

• Lime January price adjustments will be in for the half

• Aggregates should maintain a steady performance

2009 - Prospects – Lime and Aggregates

25

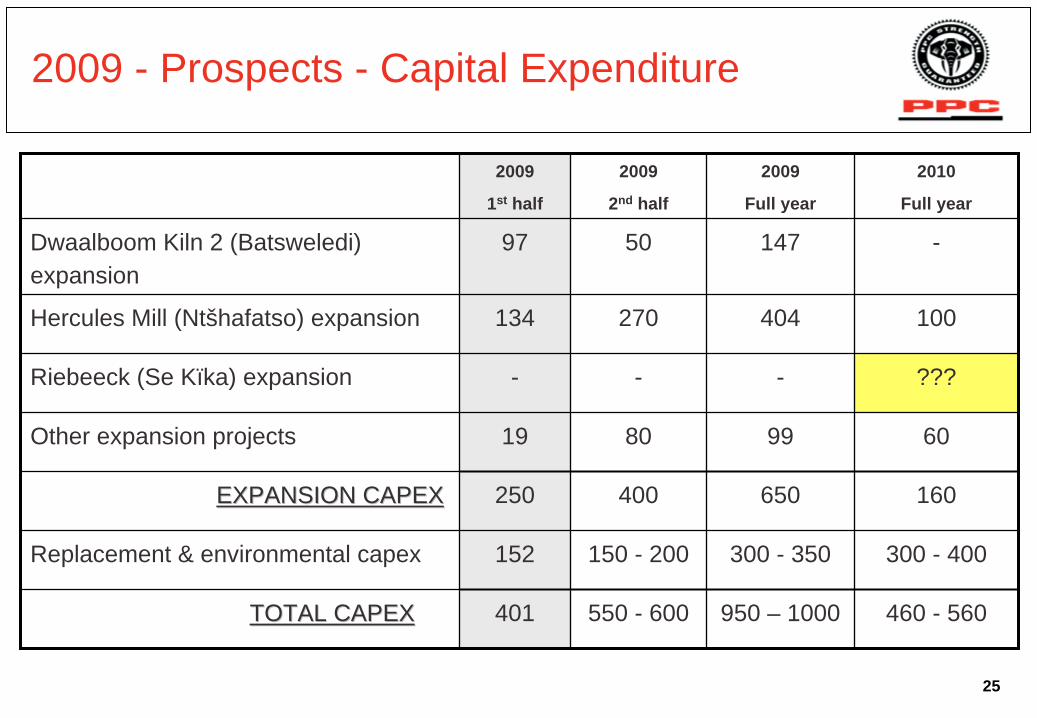

2009 - Prospects - Capital Expenditure

2009

1st half

2009

2nd half

2009

Full year

2010

Full year

Dwaalboom Kiln 2 (Batsweledi) expansion

97 50 147 -

Hercules Mill (Ntšhafatso) expansion 134 270 404 100

Riebeeck (Se Kïka) expansion - - - ???

Other expansion projects 19 80 99 60

EXPANSION CAPEXEXPANSION CAPEX 250 400 650 160

Replacement & environmental capex 152 150 - 200 300 - 350 300 - 400

TOTAL CAPEXTOTAL CAPEX 401 550 - 600 950 – 1000 460 - 560

26

2009 - Prospects – Gearing and Dividends

• Future expansionary capital expenditure will continue to be funded through borrowings

• Current gross debt to EBITDA cover of 1.4 times is well within the stated target of 2 to 3 times cover

• Dividend cover will remain in the target range of 1.2 to 1.5 x earnings before non-cash IFRS 2 charges of R404 million

• Will consider the distribution of excess cash if and when this arises

• Level of shareholders’ equity and reserves will be the ultimate limiting factor – until reserves increase (through issue of shares etc.)

27

THANK YOUTHANK YOU

QUESTION TIME

28

ANNEXURES

PPC 2009 Interim ResultsPPC 2009 Interim Results

29

BBBEE transaction

• R2.7bn broad-based black ownership initiative - effected 15 December 2008

• Combination of strategic black partners, PPC employees, communities, construction and related industry associations

• 15.29% of increased issued share capital, 15.1% black owned

R75320 140

R1 19037 991

R548 558

R millions

000’s Shares• Impact on issued share capital

• New shares issued to strategic black partners, at par, with full economic and voting rights. ITO accounting treated as a separate class of shares for the calculation of EPS and HEPS

• Shares bought back by BEE Trusts in terms of Scheme of Arrangement @ R31.32/ share - consolidated as treasury shares

• Impact of new BEE shares issued was reduced by PPC 2008 buy- backs by a wholly-owned subsidiary - treated as treasury shares

Effective dilution is ONLY 5.3%

30

BBBEE transaction (continued)

• Impact on statement of comprehensive income• Variable interest rates were swopped for fixed interest rates to reduce interest rate

exposure• Dividends paid to certain internal trusts treated as an expense

• Impact on statement of financial position• Pretoria Portland Cement Company Limited guaranteed part of the funding required

for some of the Trust financing in the transaction• Have to consolidate that part of the funding structure as a result of residual risk• R1 190 million shares treated as treasury shares, including consolidated trusts• Related funding raised as liabilities• Total borrowings including BEE transaction still leave plenty of room for further

gearing to the targeted level if necessary

31

Detail of Borrowings & Gearing

31 March ’09*

R million

8-year bullet loan (reduced short-term borrowings already in place) 1 517

Redeemable preference shares issued in wholly-owned subsidiary 168

BBBEE SPV / Trusts redeemable preference shares and loans consolidated 939

Total funding raised with the BBBEE transaction 2 624

Other borrowings 1 240

Total borrowings 3 864

Included in long-term borrowings 2 627

Included in short-term borrowings 1 237

Annual gross debt to EBITDA (excluding IFRS 2 charges) of 1.4 tiAnnual gross debt to EBITDA (excluding IFRS 2 charges) of 1.4 times are well within the targeted mes are well within the targeted level of 2 to 3 times EBITDAlevel of 2 to 3 times EBITDA

* Total balance outstanding at 31 March 2009, net of costs

32

H1 2009 – Safety Statistics

Group Lost Time Injuries and Lost Time Injury Frequency Rate

0

1

2

3

4

5

6O

ct-0

6

Dec

-06

Feb-

07

Apr

-07

Jun-

07

Aug

-07

Oct

-07

Dec

-07

Feb-

08

Apr

-08

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-

09

0.00

0.10

0.20

0.30

0.40

0.50

0.60

LTIs (LHS) LTIFR (RHS)

H1 2009 11

H1 2008 10

33

Contacts

John Gomersall Chief Executive OfficerPeter Esterhuysen Chief Financial OfficerOrrie Fenn Chief Operating Officer

Kevin Odendaal Investor Relations

www.ppc.co.zaTel. 011 386 9000

34

Disclaimer

This document including, without limitation, those statements concerning the demand outlook, PPC¹s expansion projects and its capital resources and expenditure, contain certain forward-looking views. By their nature, forward- looking statements involve risk and uncertainty and although PPC believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward- looking statements as a result of, among other factors, changes in economic and market conditions, success of business and operating initiatives, changes in the regulatory environment and other government action and business and operational risk management.

While PPC takes reasonable care to ensure the accuracy of the information presented, PPC accepts no responsibility for any consequential, indirect, special or incidental damages, whether foreseeable or unforeseeable, based on claims arising out of misrepresentation or negligence arising in connection with a forward-looking statement. This document is not intended to contain any profit forecasts or profit estimates, and the information published in this document is unaudited.