beyond the outsourcing angst: making america more

TRANSCRIPT

VOL. 1, NO. 2FEBRUARY 2006 EconomicLetter

Beyond the Outsourcing Angst:Making America More Productiveby Thomas F. Siems

Insights from theF E D E R A L R E S E R V E B A N K O F D A L L A S

Outsourcing is not new. For years, American companies have

focused on core competencies and contracted out activities that could be

accomplished better, faster and cheaper by outside, specialized providers.

These vendors may be across town, elsewhere in the country or on the far

side of the world.

The motive has always been to remain competitive. In today’s busi-

ness environment, profit and even survival depend on making constant

improvements throughout supply chains by lowering costs and improving

quality, designs, cycle times and processes. Through specialization and

trade, businesses develop important competitive advantages that help them

become more flexible and innovative in rapidly changing markets.

The best companies

keep costs low and

boost productivity

by doing what

they do best and

outsourcing the rest.

2

Indeed, the best companies keepcosts low and boost productivity by doingwhat they do best and outsourcing therest.1

Even when it involves foreign work-ers, outsourcing benefits individual com-panies. Many Americans, however,express a deep unease over reports offirms’ “exporting jobs” and displacingdomestic workers by moving jobs toIndia, China or other up-and-comingnations.

The concern is understandable. Joblosses are painful, especially when theyare related to global economic forcesbeyond individual workers’ control. Asreports of outsourcing grow, manyAmericans are advocating policiesdesigned to preserve existing jobs andindustries. But many economists—includ-ing such notables as Milton Friedmanand Jagdish Bhagwati—discourage theseefforts as harmful to the overall econo-my.2 They argue that outsourcing increas-es efficiency and productivity and leadsto competitiveness, innovation and ever-larger market opportunities.

Knowledge Workers at RiskOne reason today’s overseas out-

sourcing generates heat is the widerswath of occupations being performedoffshore. Computers, software, theInternet and fiber-optic cables form aninfrastructure that allows businesses tobreak apart activities and redistributethem elsewhere—increasingly toknowledge workers all over the world.Digital technologies and inexpensivetelecommunications have created anefficient and effective informationsuperhighway: Strings of zeroes andones can be moved to Bangalore,Beijing or just about anyplace in seconds.

White-collar activities such as pro-cessing accounting data, performingstandard financial analyses, writing rou-tine software and maintaining call cen-ters are no longer exempt from interna-tional competition. With an Internet con-nection and specialized skills, individualsand companies in the remotest ends ofthe earth are able to compete and col-laborate in today’s global economy.

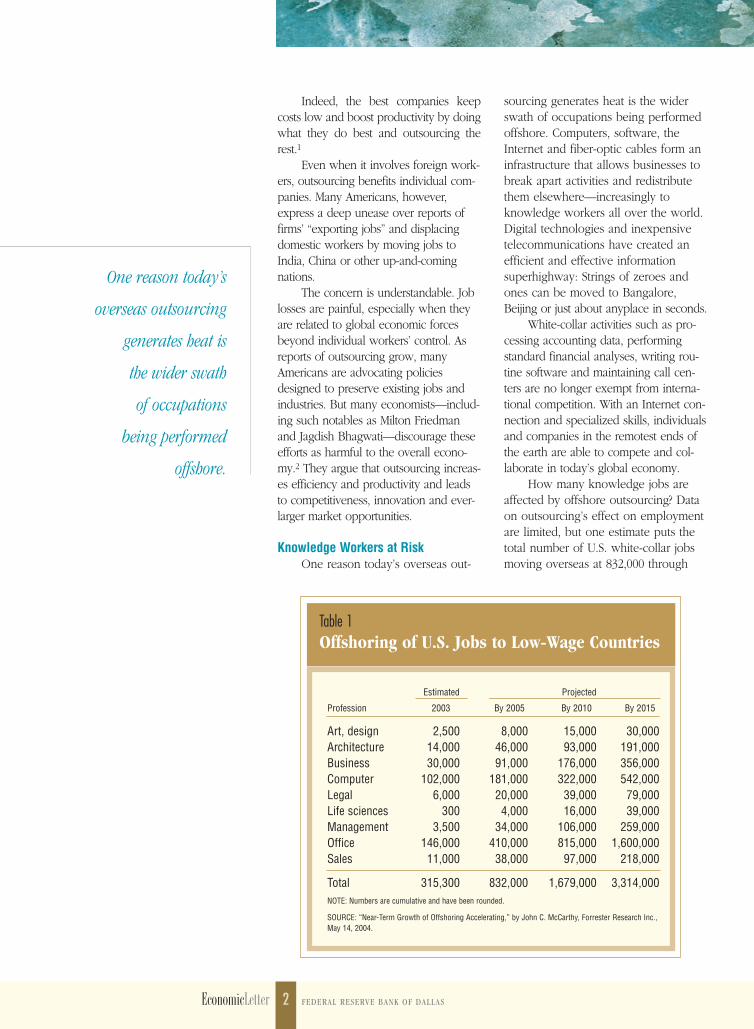

How many knowledge jobs areaffected by offshore outsourcing? Dataon outsourcing’s effect on employmentare limited, but one estimate puts thetotal number of U.S. white-collar jobsmoving overseas at 832,000 through

One reason today’s

overseas outsourcing

generates heat is

the wider swath

of occupations

being performed

offshore.

EconomicLetter FEDERAL RESERVE BANK OF DALLAS

Table 1Offshoring of U.S. Jobs to Low-Wage Countries

NOTE: Numbers are cumulative and have been rounded.

SOURCE: “Near-Term Growth of Offshoring Accelerating,” by John C. McCarthy, Forrester Research Inc.,May 14, 2004.

Estimated Projected

Profession 2003 By 2005 By 2010 By 2015

Art, design 2,500 8,000 15,000 30,000Architecture 14,000 46,000 93,000 191,000Business 30,000 91,000 176,000 356,000Computer 102,000 181,000 322,000 542,000Legal 6,000 20,000 39,000 79,000Life sciences 300 4,000 16,000 39,000Management 3,500 34,000 106,000 259,000Office 146,000 410,000 815,000 1,600,000Sales 11,000 38,000 97,000 218,000

Total 315,300 832,000 1,679,000 3,314,000

3

2005, nearly triple the figure through2003 (Table 1). In another five years,the total could rise to 1.7 million; in adecade, to 3.3 million. We should keepin mind, however, that the U.S. hasadded 18 million jobs in the past 10years. Total employment rose to nearly135 million workers in early 2006, sothe offshore outsourcing estimates rep-resent a relatively small part of a grow-ing economy.

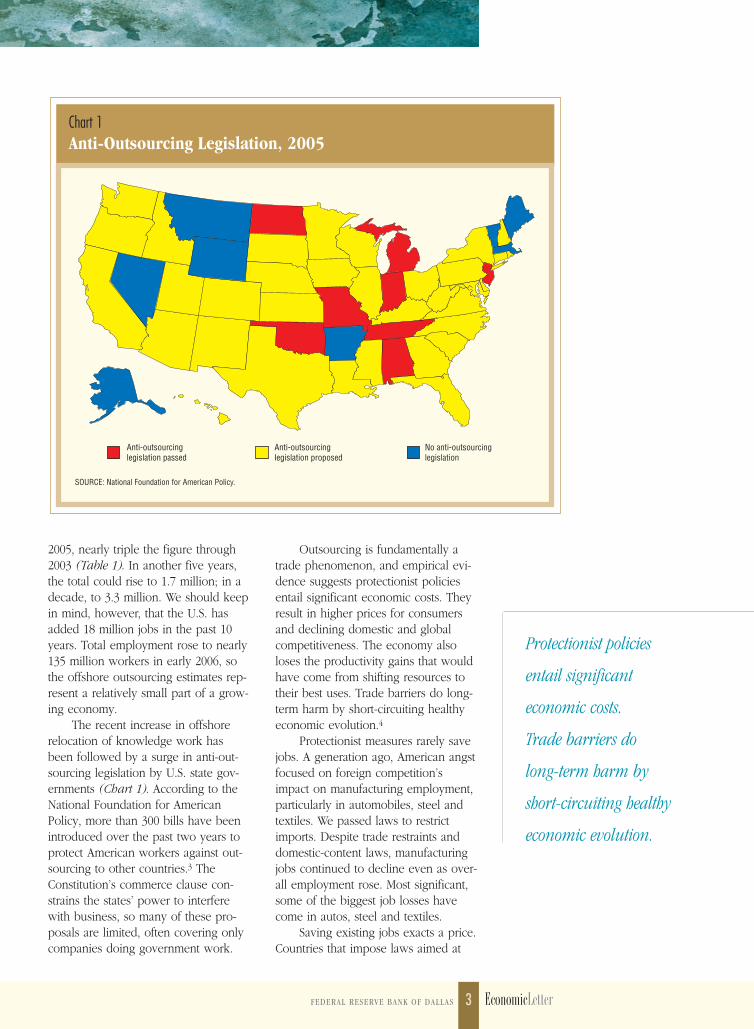

The recent increase in offshorerelocation of knowledge work hasbeen followed by a surge in anti-out-sourcing legislation by U.S. state gov-ernments (Chart 1). According to theNational Foundation for AmericanPolicy, more than 300 bills have beenintroduced over the past two years toprotect American workers against out-sourcing to other countries.3 TheConstitution’s commerce clause con-strains the states’ power to interferewith business, so many of these pro-posals are limited, often covering onlycompanies doing government work.

Outsourcing is fundamentally atrade phenomenon, and empirical evi-dence suggests protectionist policiesentail significant economic costs. Theyresult in higher prices for consumersand declining domestic and globalcompetitiveness. The economy alsoloses the productivity gains that wouldhave come from shifting resources totheir best uses. Trade barriers do long-term harm by short-circuiting healthyeconomic evolution.4

Protectionist measures rarely savejobs. A generation ago, American angstfocused on foreign competition’simpact on manufacturing employment,particularly in automobiles, steel andtextiles. We passed laws to restrictimports. Despite trade restraints anddomestic-content laws, manufacturingjobs continued to decline even as over-all employment rose. Most significant,some of the biggest job losses havecome in autos, steel and textiles.

Saving existing jobs exacts a price.Countries that impose laws aimed at

FEDERAL RESERVE BANK OF DALLAS EconomicLetter

Protectionist policies

entail significant

economic costs.

Trade barriers do

long-term harm by

short-circuiting healthy

economic evolution.

Chart 1Anti-Outsourcing Legislation, 2005

Anti-outsourcinglegislation passed

Anti-outsourcinglegislation proposed

No anti-outsourcing legislation

SOURCE: National Foundation for American Policy.

Outsourcing often

creates employment

uncertainties because it’s

not always immediately

apparent where the new jobs

will materialize. History

tells us, however, that

job creation outpaces job

destruction in the long run.

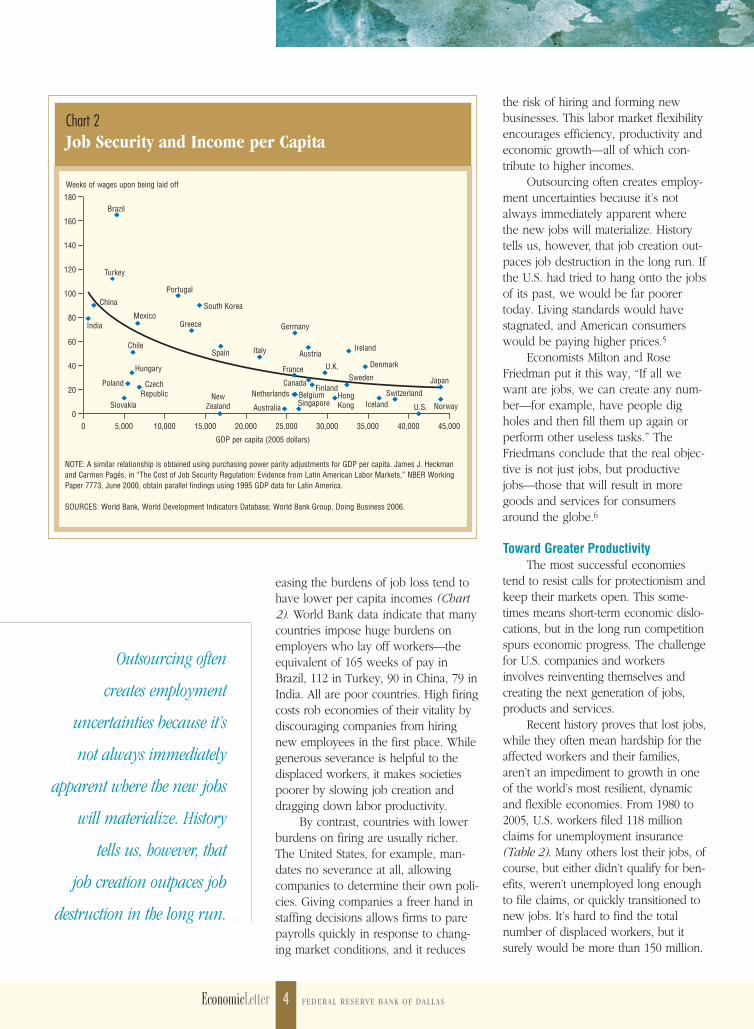

easing the burdens of job loss tend tohave lower per capita incomes (Chart2). World Bank data indicate that manycountries impose huge burdens onemployers who lay off workers—theequivalent of 165 weeks of pay inBrazil, 112 in Turkey, 90 in China, 79 inIndia. All are poor countries. High firingcosts rob economies of their vitality bydiscouraging companies from hiringnew employees in the first place. Whilegenerous severance is helpful to thedisplaced workers, it makes societiespoorer by slowing job creation anddragging down labor productivity.

By contrast, countries with lowerburdens on firing are usually richer.The United States, for example, man-dates no severance at all, allowingcompanies to determine their own poli-cies. Giving companies a freer hand instaffing decisions allows firms to parepayrolls quickly in response to chang-ing market conditions, and it reduces

the risk of hiring and forming newbusinesses. This labor market flexibilityencourages efficiency, productivity andeconomic growth—all of which con-tribute to higher incomes.

Outsourcing often creates employ-ment uncertainties because it’s notalways immediately apparent wherethe new jobs will materialize. Historytells us, however, that job creation out-paces job destruction in the long run. Ifthe U.S. had tried to hang onto the jobsof its past, we would be far poorertoday. Living standards would havestagnated, and American consumerswould be paying higher prices.5

Economists Milton and RoseFriedman put it this way, “If all wewant are jobs, we can create any num-ber—for example, have people digholes and then fill them up again orperform other useless tasks.” TheFriedmans conclude that the real objec-tive is not just jobs, but productivejobs—those that will result in moregoods and services for consumersaround the globe.6

Toward Greater ProductivityThe most successful economies

tend to resist calls for protectionism andkeep their markets open. This some-times means short-term economic dislo-cations, but in the long run competitionspurs economic progress. The challengefor U.S. companies and workersinvolves reinventing themselves andcreating the next generation of jobs,products and services.

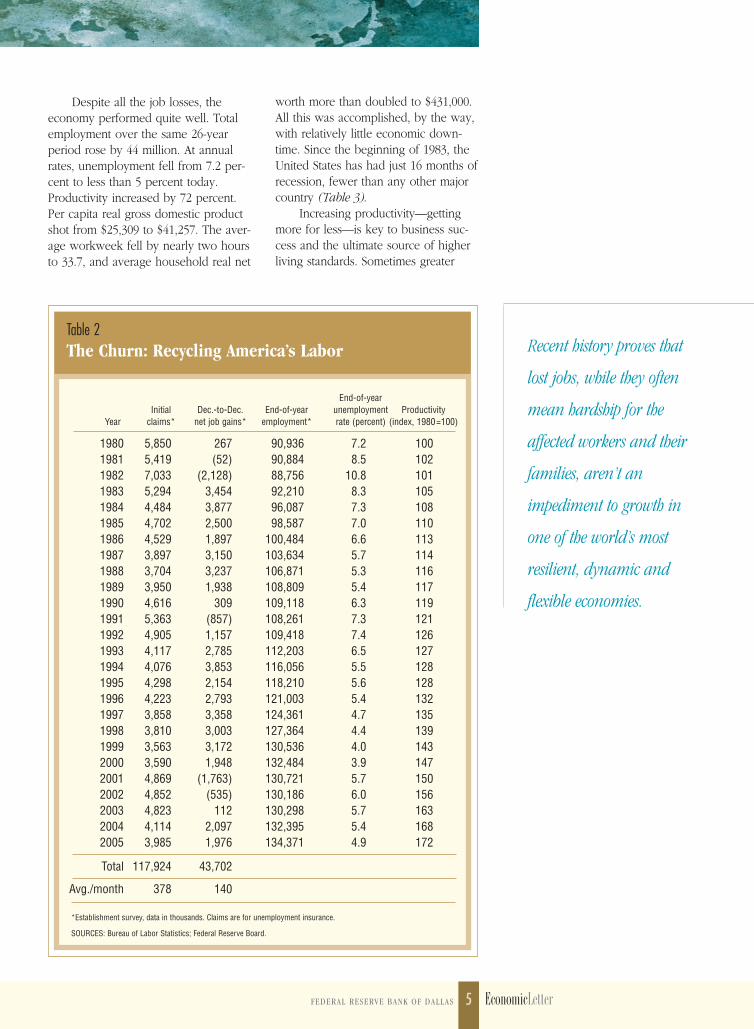

Recent history proves that lost jobs,while they often mean hardship for theaffected workers and their families,aren’t an impediment to growth in oneof the world’s most resilient, dynamicand flexible economies. From 1980 to2005, U.S. workers filed 118 millionclaims for unemployment insurance(Table 2). Many others lost their jobs, ofcourse, but either didn’t qualify for ben-efits, weren’t unemployed long enoughto file claims, or quickly transitioned tonew jobs. It’s hard to find the totalnumber of displaced workers, but itsurely would be more than 150 million.

4EconomicLetter FEDERAL RESERVE BANK OF DALLAS

NOTE: A similar relationship is obtained using purchasing power parity adjustments for GDP per capita. James J. Heckmanand Carmen Pagés, in “The Cost of Job Security Regulation: Evidence from Latin American Labor Markets,” NBER WorkingPaper 7773, June 2000, obtain parallel findings using 1995 GDP data for Latin America.

SOURCES: World Bank, World Development Indicators Database; World Bank Group, Doing Business 2006.

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,0000

20

40

60

80

100

120

140

160

180Brazil

Turkey

China

India

Portugal

MexicoSouth Korea

Greece

ItalySpain

Germany

Japan

Norway

SwitzerlandIceland

Denmark

IrelandAustria

U.K.Sweden

HongKongAustralia

NewZealand

CanadaNetherlands

France

Chile

Hungary

CzechRepublic

Slovakia

Poland

Singapore U.S.

FinlandBelgium

GDP per capita (2005 dollars)

Chart 2Job Security and Income per Capita

Weeks of wages upon being laid off

Despite all the job losses, theeconomy performed quite well. Totalemployment over the same 26-yearperiod rose by 44 million. At annualrates, unemployment fell from 7.2 per-cent to less than 5 percent today.Productivity increased by 72 percent.Per capita real gross domestic productshot from $25,309 to $41,257. The aver-age workweek fell by nearly two hoursto 33.7, and average household real net

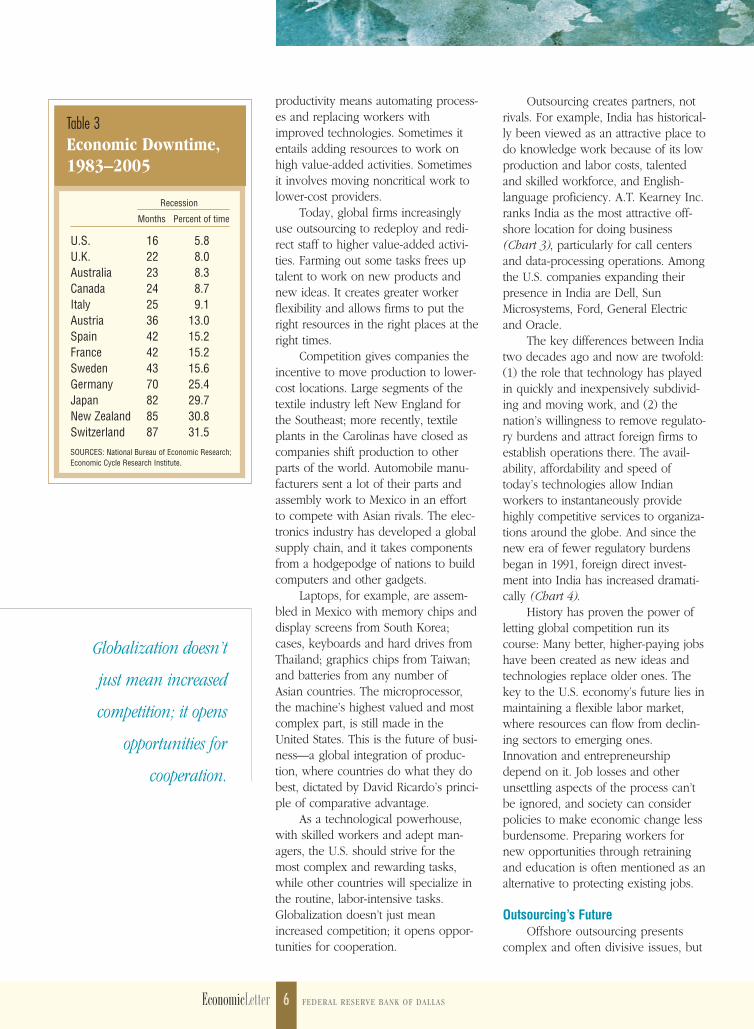

worth more than doubled to $431,000.All this was accomplished, by the way,with relatively little economic down-time. Since the beginning of 1983, theUnited States has had just 16 months ofrecession, fewer than any other majorcountry (Table 3).

Increasing productivity—gettingmore for less—is key to business suc-cess and the ultimate source of higherliving standards. Sometimes greater

5FEDERAL RESERVE BANK OF DALLAS EconomicLetter

Table 2The Churn: Recycling America’s Labor

*Establishment survey, data in thousands. Claims are for unemployment insurance.

SOURCES: Bureau of Labor Statistics; Federal Reserve Board.

End-of-year Initial Dec.-to-Dec. End-of-year unemployment Productivity

Year claims* net job gains* employment* rate (percent) (index, 1980=100)

1980 5,850 267 90,936 7.2 1001981 5,419 (52) 90,884 8.5 1021982 7,033 (2,128) 88,756 10.8 1011983 5,294 3,454 92,210 8.3 1051984 4,484 3,877 96,087 7.3 1081985 4,702 2,500 98,587 7.0 1101986 4,529 1,897 100,484 6.6 1131987 3,897 3,150 103,634 5.7 1141988 3,704 3,237 106,871 5.3 1161989 3,950 1,938 108,809 5.4 1171990 4,616 309 109,118 6.3 1191991 5,363 (857) 108,261 7.3 1211992 4,905 1,157 109,418 7.4 1261993 4,117 2,785 112,203 6.5 1271994 4,076 3,853 116,056 5.5 1281995 4,298 2,154 118,210 5.6 1281996 4,223 2,793 121,003 5.4 1321997 3,858 3,358 124,361 4.7 1351998 3,810 3,003 127,364 4.4 1391999 3,563 3,172 130,536 4.0 1432000 3,590 1,948 132,484 3.9 1472001 4,869 (1,763) 130,721 5.7 1502002 4,852 (535) 130,186 6.0 1562003 4,823 112 130,298 5.7 1632004 4,114 2,097 132,395 5.4 1682005 3,985 1,976 134,371 4.9 172

Total 117,924 43,702

Avg./month 378 140

Recent history proves that

lost jobs, while they often

mean hardship for the

affected workers and their

families, aren’t an

impediment to growth in

one of the world’s most

resilient, dynamic and

flexible economies.

productivity means automating process-es and replacing workers withimproved technologies. Sometimes itentails adding resources to work onhigh value-added activities. Sometimesit involves moving noncritical work tolower-cost providers.

Today, global firms increasinglyuse outsourcing to redeploy and redi-rect staff to higher value-added activi-ties. Farming out some tasks frees uptalent to work on new products andnew ideas. It creates greater workerflexibility and allows firms to put theright resources in the right places at theright times.

Competition gives companies theincentive to move production to lower-cost locations. Large segments of thetextile industry left New England forthe Southeast; more recently, textileplants in the Carolinas have closed ascompanies shift production to otherparts of the world. Automobile manu-facturers sent a lot of their parts andassembly work to Mexico in an effortto compete with Asian rivals. The elec-tronics industry has developed a globalsupply chain, and it takes componentsfrom a hodgepodge of nations to buildcomputers and other gadgets.

Laptops, for example, are assem-bled in Mexico with memory chips anddisplay screens from South Korea;cases, keyboards and hard drives fromThailand; graphics chips from Taiwan;and batteries from any number ofAsian countries. The microprocessor,the machine’s highest valued and mostcomplex part, is still made in theUnited States. This is the future of busi-ness—a global integration of produc-tion, where countries do what they dobest, dictated by David Ricardo’s princi-ple of comparative advantage.

As a technological powerhouse,with skilled workers and adept man-agers, the U.S. should strive for themost complex and rewarding tasks,while other countries will specialize inthe routine, labor-intensive tasks.Globalization doesn’t just meanincreased competition; it opens oppor-tunities for cooperation.

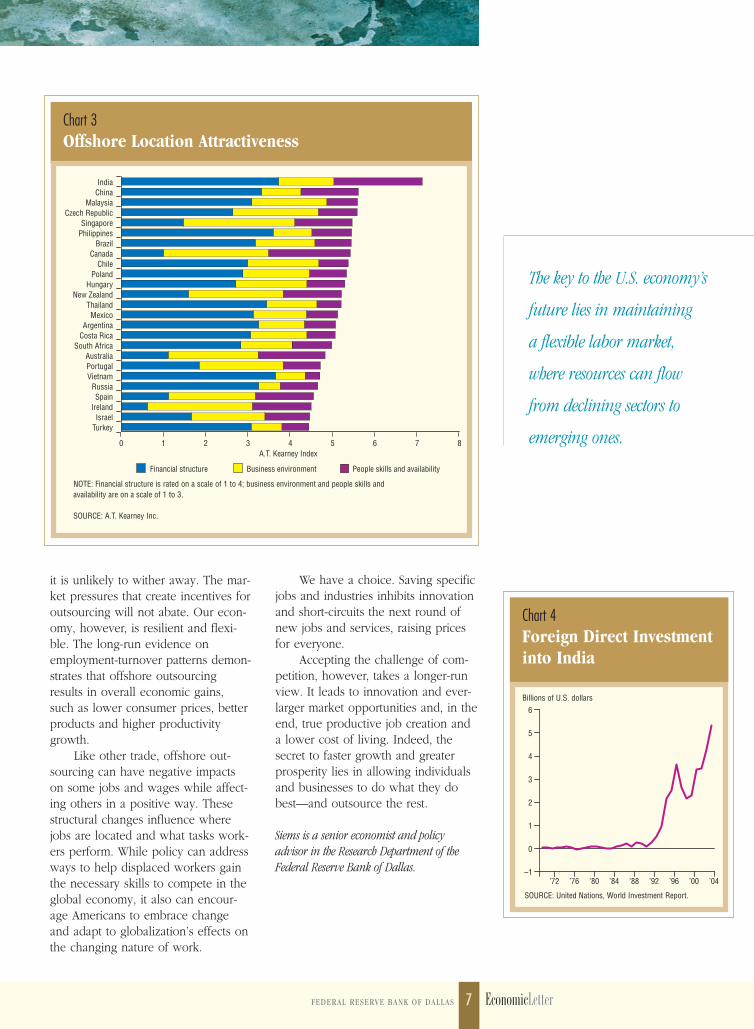

Outsourcing creates partners, notrivals. For example, India has historical-ly been viewed as an attractive place todo knowledge work because of its lowproduction and labor costs, talentedand skilled workforce, and English-language proficiency. A.T. Kearney Inc.ranks India as the most attractive off-shore location for doing business(Chart 3), particularly for call centersand data-processing operations. Amongthe U.S. companies expanding theirpresence in India are Dell, SunMicrosystems, Ford, General Electricand Oracle.

The key differences between Indiatwo decades ago and now are twofold:(1) the role that technology has playedin quickly and inexpensively subdivid-ing and moving work, and (2) thenation’s willingness to remove regulato-ry burdens and attract foreign firms toestablish operations there. The avail-ability, affordability and speed oftoday’s technologies allow Indianworkers to instantaneously providehighly competitive services to organiza-tions around the globe. And since thenew era of fewer regulatory burdensbegan in 1991, foreign direct invest-ment into India has increased dramati-cally (Chart 4).

History has proven the power ofletting global competition run itscourse: Many better, higher-paying jobshave been created as new ideas andtechnologies replace older ones. Thekey to the U.S. economy’s future lies inmaintaining a flexible labor market,where resources can flow from declin-ing sectors to emerging ones.Innovation and entrepreneurshipdepend on it. Job losses and otherunsettling aspects of the process can’tbe ignored, and society can considerpolicies to make economic change lessburdensome. Preparing workers fornew opportunities through retrainingand education is often mentioned as analternative to protecting existing jobs.

Outsourcing’s FutureOffshore outsourcing presents

complex and often divisive issues, but

Globalization doesn’t

just mean increased

competition; it opens

opportunities for

cooperation.

6EconomicLetter FEDERAL RESERVE BANK OF DALLAS

SOURCES: National Bureau of Economic Research; Economic Cycle Research Institute.

Recession

Months Percent of time

U.S. 16 5.8U.K. 22 8.0Australia 23 8.3Canada 24 8.7Italy 25 9.1Austria 36 13.0Spain 42 15.2France 42 15.2Sweden 43 15.6Germany 70 25.4Japan 82 29.7New Zealand 85 30.8Switzerland 87 31.5

Table 3Economic Downtime, 1983–2005

it is unlikely to wither away. The mar-ket pressures that create incentives foroutsourcing will not abate. Our econ-omy, however, is resilient and flexi-ble. The long-run evidence onemployment-turnover patterns demon-strates that offshore outsourcingresults in overall economic gains,such as lower consumer prices, betterproducts and higher productivitygrowth.

Like other trade, offshore out-sourcing can have negative impactson some jobs and wages while affect-ing others in a positive way. Thesestructural changes influence wherejobs are located and what tasks work-ers perform. While policy can addressways to help displaced workers gainthe necessary skills to compete in theglobal economy, it also can encour-age Americans to embrace changeand adapt to globalization’s effects onthe changing nature of work.

The key to the U.S. economy’s

future lies in maintaining

a flexible labor market,

where resources can flow

from declining sectors to

emerging ones.

7FEDERAL RESERVE BANK OF DALLAS EconomicLetter

SOURCE: United Nations, World Investment Report.

–1

0

1

2

3

4

5

6

’04’00’96’92’88’84’80’76’72

We have a choice. Saving specificjobs and industries inhibits innovationand short-circuits the next round ofnew jobs and services, raising pricesfor everyone.

Accepting the challenge of com-petition, however, takes a longer-runview. It leads to innovation and ever-larger market opportunities and, in theend, true productive job creation anda lower cost of living. Indeed, thesecret to faster growth and greaterprosperity lies in allowing individualsand businesses to do what they dobest—and outsource the rest.

Siems is a senior economist and policy advisor in the Research Department of theFederal Reserve Bank of Dallas.

Chart 4Foreign Direct Investment into India

Billions of U.S. dollars

Chart 3Offshore Location Attractiveness

NOTE: Financial structure is rated on a scale of 1 to 4; business environment and people skills andavailability are on a scale of 1 to 3.

SOURCE: A.T. Kearney Inc.

0 1 2 3 4 5 6 7 8

TurkeyIsrael

IrelandSpain

RussiaVietnamPortugalAustralia

South AfricaCosta RicaArgentina

MexicoThailand

New ZealandHungary

PolandChile

CanadaBrazil

PhilippinesSingapore

Czech RepublicMalaysia

ChinaIndia

Financial structure Business environment People skills and availability

A.T. Kearney Index

ISSUE 1

JANUARY/FEBRUARY 2006

F E D E R A L R E S E RV E B A N K O F D A L L A S

SouthwestEconomy

In Th i s I s sue

Texas Economy Shifts

into Higher Gear

U.S., Mexico Deepen

Economic Ties

Spotlight: Texas Exports

On the Record:

Harvey Rosenblum

Regional Information You Can Use!In the January/February 2006 issue:

• Texas Economy Shifts into Higher Gear• Spotlight on Texas Exports• U.S., Mexico Deepen Economic Ties• Harvey Rosenblum on the Fed’s Changing of the Guard

To subscribe, call 214-922-5254 or visit our web site at www.dallasfed.org.

SouthwestEconomy

NotesThe author thanks Julia Carter and Timothy J.Schaaf for assistance in research.1 A prelude to this article is “Do What You DoBest, Outsource the Rest?” by Thomas F. Siemsand Adam S. Ratner, Federal Reserve Bank ofDallas Southwest Economy, November/Decem-ber 2003, pp. 13–14.2 The debate over outsourcing is clearly framedin “The Muddles over Outsourcing,” by JagdishBhagwati, Arvind Panagariya and T.N. Srinivasan,Journal of Economic Perspectives, vol. 18, no. 4,Fall 2004, pp. 93–114.3 “Outsourcing Saves Money,” by Stuart Ander-son, State Legislatures Magazine, June 2005,

FEDERAL RESERVE BANK OF DALLAS2200 N. PEARL ST.DALLAS, TX 75201

EconomicLetter is published monthlyby the Federal Reserve Bank of Dallas. The viewsexpressed are those of the authors and should not beattributed to the Federal Reserve Bank of Dallas or theFederal Reserve System.

Articles may be reprinted on the condition thatthe source is credited and a copy is provided to theResearch Department of the Federal Reserve Bank ofDallas.

Economic Letter is available free of charge bywriting the Public Affairs Department, Federal ReserveBank of Dallas, P.O. Box 655906, Dallas, TX 75265-5906; by fax at 214-922-5268; or by telephone at 214-922-5254. This publication is available on the DallasFed web site, www.dallasfed.org.

Richard W. FisherPresident and Chief Executive Officer

Helen E. HolcombFirst Vice President and Chief Operating Officer

Harvey RosenblumExecutive Vice President and Director of Research

W. Michael CoxSenior Vice President and Chief Economist

Robert D. HankinsSenior Vice President, Banking Supervision

Executive EditorW. Michael Cox

EditorRichard Alm

Associate EditorKay Champagne

Graphic DesignerGene Autry

and “Outsourcing Attacks Not Over,” by StuartAnderson, National Review, February 11, 2005.4 Interested readers are directed to In Defense ofGlobalization, by Jagdish Bhagwati, New York:Oxford University Press, 2004.5 Job anxieties brought on by offshore outsourc-ing highlight the tension between efficiency anddistributional concerns. See “A Specific-FactorsView on Outsourcing,” by Wilhelm Kohler, NorthAmerican Journal of Economics and Finance,vol.12, issue 1, 2001, pp. 31–53, and “WhatDoes Evidence Tell Us About Fragmentation andOutsourcing?” by Ronald Jones, HenrykKierzkowski and Chen Lurong, InternationalReview of Economics and Finance, vol. 14, 2005,pp. 305–16.6 “The Case for Free Trade,” by Milton Friedmanand Rose Friedman, Hoover Digest, no. 4, 1997.

Beyond the Outsourcing Angst(continued from page 7)