breakout is an epi-v initiative, delivered by transitions. dynamic financial analysis shai vyakarnam...

TRANSCRIPT

Breakout is an Epi-V initiative, delivered by Transitions.

Dynamic Financial Analysis

Shai Vyakarnam and Simon Pratten

What to Measure?

• Building KPIs• Lead/lag indicators• Business• Liquidity (risk)• Shareholder returns

Business

SalesProfitsProduct profitabilitySales per employeeMetersTonnesOutputs from the factoryAsset utilisationAbsolutePercentage changesOver timeCumulativeRolling annual

Time

Shareholders

• Level of profit shared out among shareholders (dividends)

• Value of shares – profits and adjusted for risks and future earnings

• Level of debt against the level of shareholders money injected in the business (gearing)

Liquidity (cash)

• Amount of stock (inventory)

• Amount of money owed by customers (debtors)

• Amount of cash in the bank

• Money you owe to the tax man

• Money owed to suppliers (creditors)

• Level of overdraft

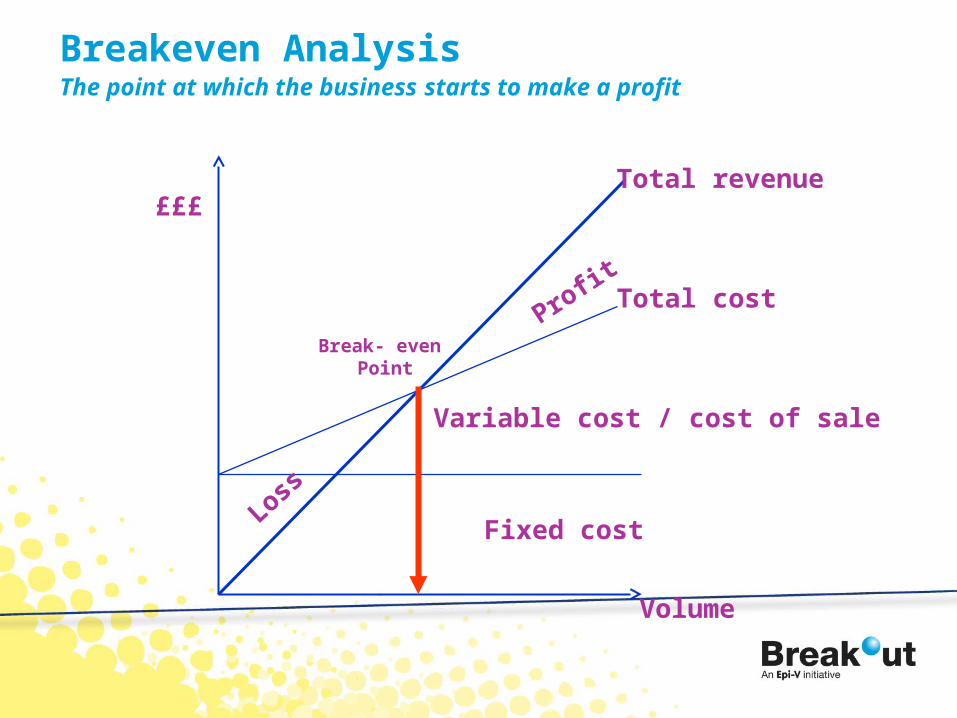

Breakeven AnalysisThe point at which the business starts to make a profit

Volume

Fixed cost

Variable cost / cost of sale

Total cost

Total revenue

Loss

Profit

£££

Break- even Point

How to use Breakeven

• Dynamic

• Calculate what-if

• Help with decisions

• Need to have gross profit figure

• Forces the right disciplines into business

• Most people can understand it in the business!

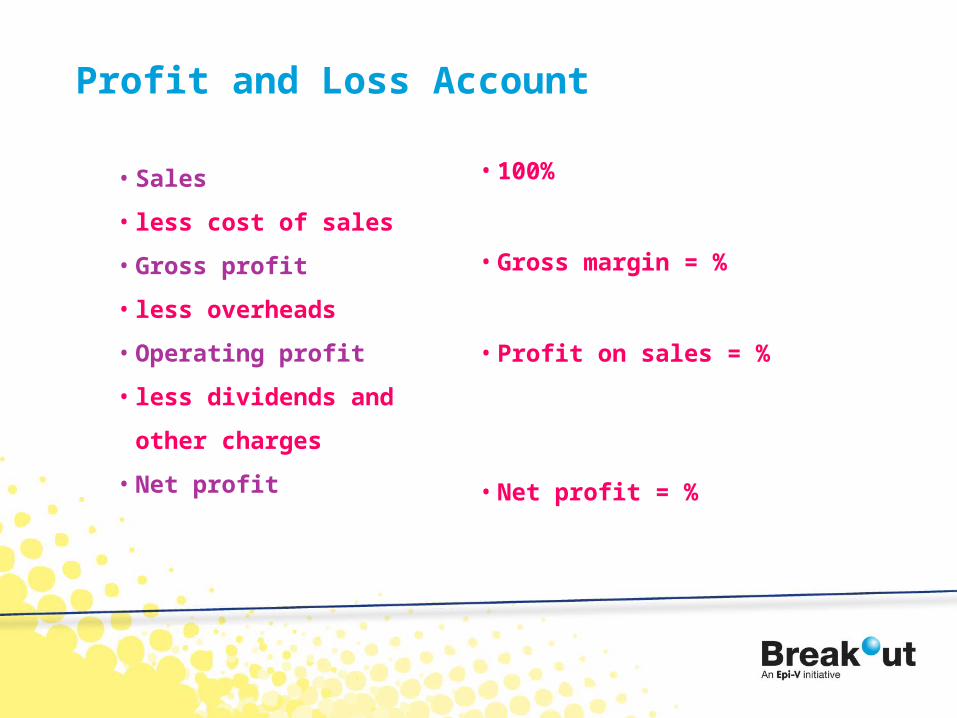

Profit and Loss Account

• Sales

• less cost of sales

• Gross profit

• less overheads

• Operating profit

• less dividends and

other charges

• Net profit

• 100%

• Gross margin = %

• Profit on sales = %

• Net profit = %

Gross (Profit) Margin

• The gap between sales and variable costs

• The real income of the business

• Expressed as a percentage of sales (Gross Margin %)

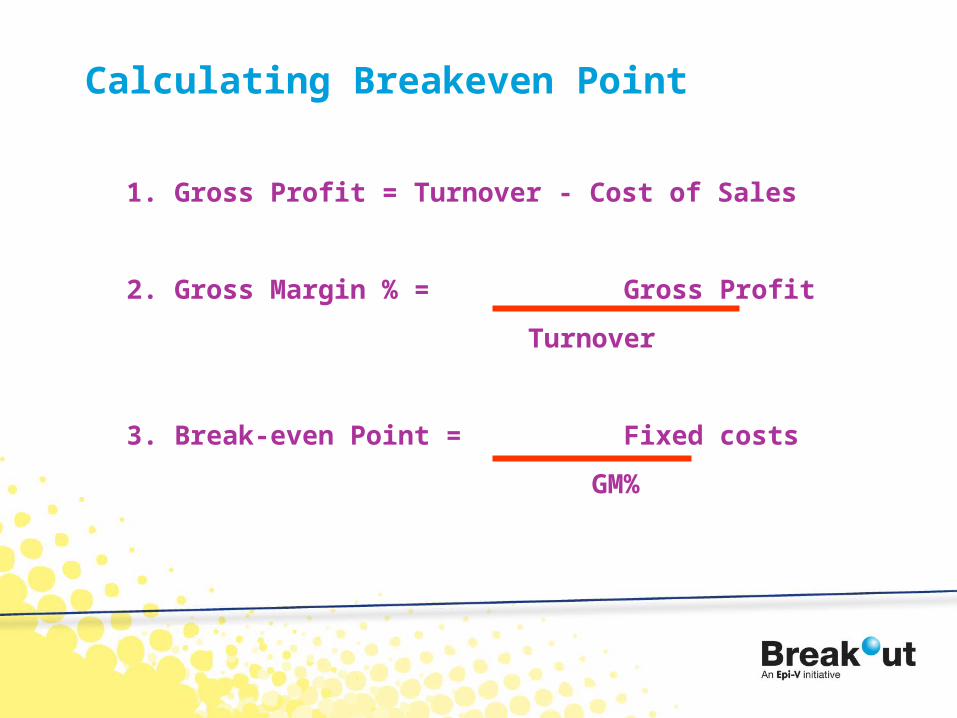

Calculating Breakeven Point

1. Gross Profit = Turnover - Cost of Sales

2. Gross Margin % = Gross Profit

Turnover

3. Break-even Point = Fixed costs

GM%

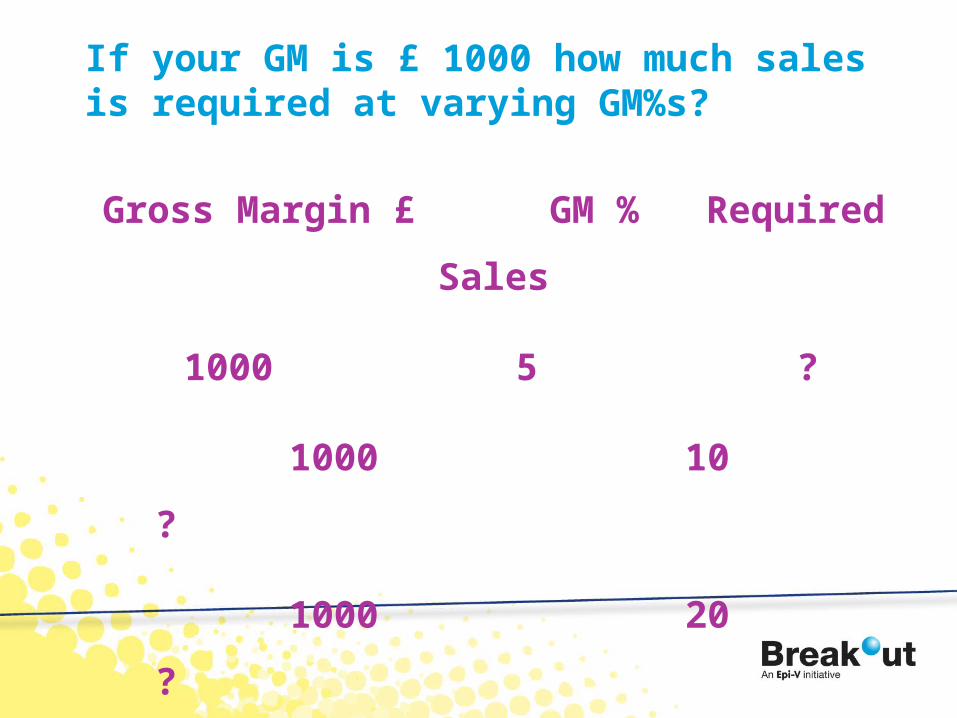

If your GM is £ 1000 how much sales is required at varying GM%s?

Gross Margin £ GM % Required Sales

1000 5 ?

1000 10 ?

1000 20 ?

1000 40 ?

Your Accounts

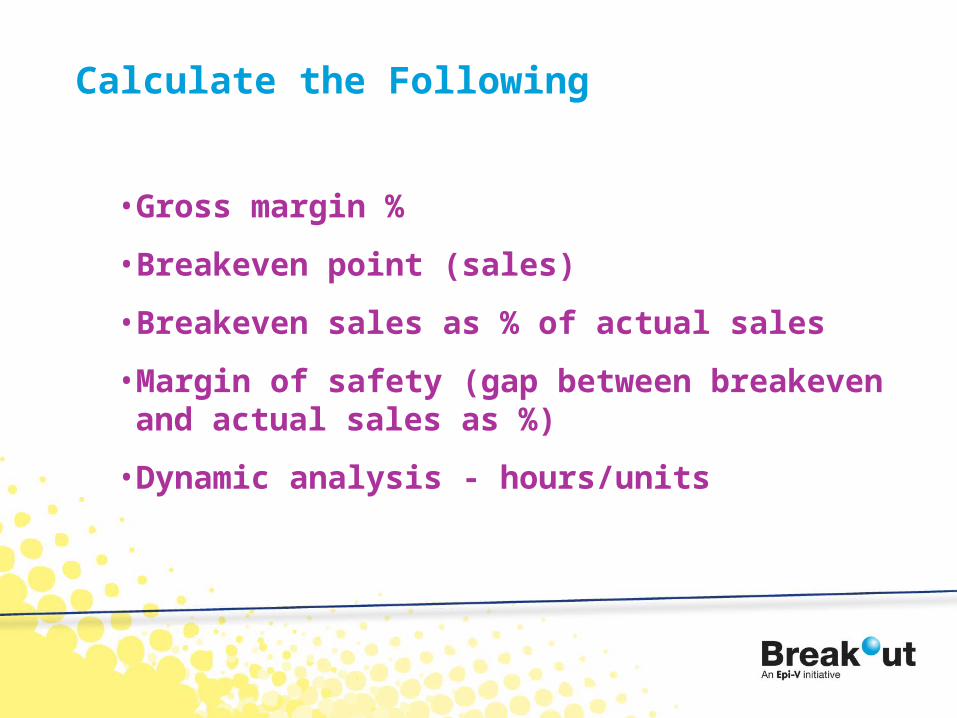

Calculate the Following

• Gross margin %

• Breakeven point (sales)

• Breakeven sales as % of actual sales

• Margin of safety (gap between breakeven and actual sales as %)

• Dynamic analysis - hours/units

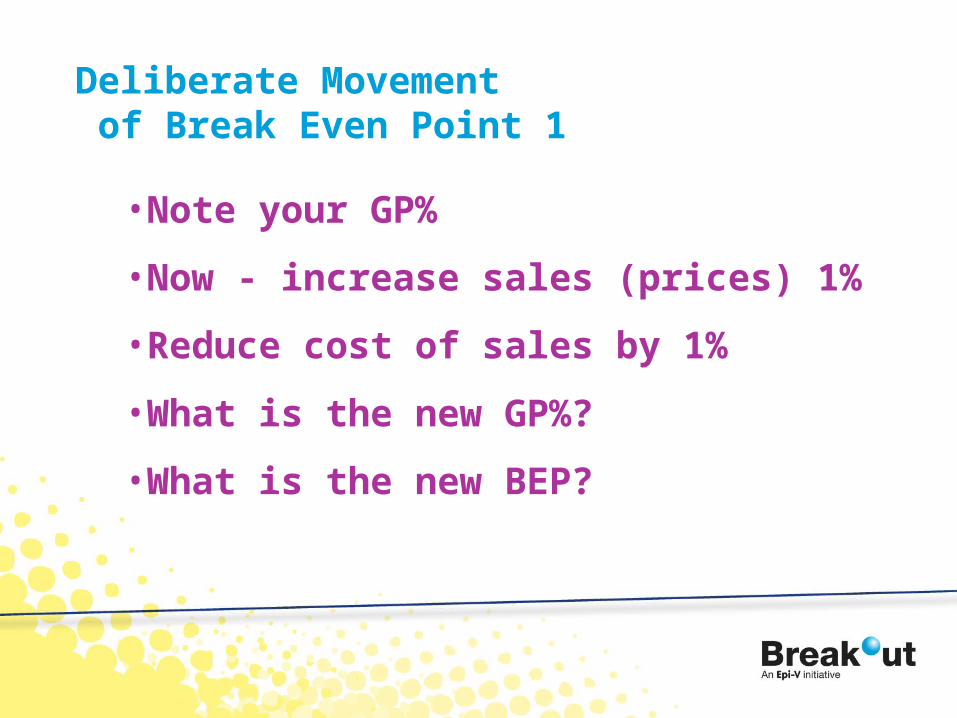

Deliberate Movement of Break Even Point 1

• Note your GP%

• Now - increase sales (prices) 1%

• Reduce cost of sales by 1%

• What is the new GP%?

• What is the new BEP?

Movement of Break Even Point 2

• Reduce your fixed costs by 1%• Having increased sales price and reduced

both cost of sales and fixed costs what is the new NET PROFIT?

• What is the % increase in net profit?• You have just seen the magic of 1%• Suppose you can change these by more

than 1%?!

Controlling costs

• Building on the impact of flexing your breakeven point

• have a first cut at shedding costs

Cash flow

• Short term future plans and the impact on cash flow estimates

• Activity Ratios: How well do you manage your cash in the business?

Gearing and Capital Structure

• How much ‘cover’ is there in the business to meet the needs of the bank?

And

• Is there enough equity in the business to ensure the bank feels comfortable with the amount being lent?

Solvency and Liquidity

• Is there enough ‘liquidity’ in the business to meet day to day obligations?

• Are the assets of the business really being ‘sweated’?

• Can the business demonstrate that the ration of current assets and inventory to short term creditors is strong enough?

Conclusions

• What have been the key take home messages for you?

• What needs to be changed?

• What are your action points and how will you prioritise them?