building customer trust to drive your kpis

TRANSCRIPT

WHAT DRIVES TRUST IN ONE BRAND, DOESN'T DO ANYTHING FOR THE OTHER

This publication and all its contents are copyright mext 2016

PROACTIVE STUDY INTO CUSTOMER TRUST AND LOYALTY IN TELCOS AND HEALTH FUNDS.

November 2016

2

Having worked globally with telecommunications and health-related companies, as well as government organisations in insight, brand, experience and sales & service training, we conducted a small-scale proactive study with 300 telco customers and non-customers in november 1016.

We explore trust in telstra, vodafone and optus, and what drives their trust best. We look at a number of health funds to examine their levels of trust and loyalty, as well as what drives them.

These study findings are to be used to understand the principles, impact and operationalisation of trust – and as a good indication and hypothesis only

Additionally, in this study, we looked into customer perception of efficient delivery and the impact of issues concerning trust and loyalty.

UNDERSTANDING TRUST

TRUST DRIVES 85% OF YOUR NPSAND 75% OF YOUR CUSTOMER LOYALTY.

3

CONTENT

Executive summary

The effect of trust on organisational performance and KPIs

How trust works – the science of trust

Telecommunicaton

Telstra & competitor HuTrust® Equity Analysis - what telcos are trusted for, and how strongly

Telstra’s trust is driven differently from competitors – HuTrust® Driver Analysis

The attributes that drive Telstra trust are surprising – HuTrust® Attribute Analysis

How to operationalise ‘trust’

Health insurance

Average loyalty and trust scoresHuTrust® Profile

- what PHIs are trusted for, and how strongly

HuTrust® Driver Analysis

4

5

7

9

15

17

20

23

26

28

8

21

4

EXECUTIVE SUMMARY

Performance is a question of trust

Trust is not the same for each brand

{

Trust – the robust kind

PWC calls trust the ‘forgotten asset’. They urge you to view trust not as an insurance, but as your greatest growth opportunity, and advise boards and managements to adopt a trust strategy.

Ours and others’ international studies show that trust drives the vast majority of all organisational KPIs, the top and bottom line.

For 14 years we have specialised in the psychology of trust and developed robust frameworks to analyse, build and track trust to help organisations improve their performance, both internally and externally.

Every little bit of trust, added or lost, makes a huge impact on sales, loyalty and advocacy

Competence and Benefit trust drive well over 1/3 of Telstra’s total trust. Competence trust is driven by your network quality and understanding of your long-term in-vestment, such as e-health.Your benefit trust, by a big margin, is driven by Telstra’s foresight in its CEO succession.Optus’ and Vodafone’s trust are driven by total-ly different trust dimensions.

Trust is about ‘what you can and want to trust for’; In the 3 telcos reviewed, it is totally different from one brand to the other. To effectively build trust, one needs to know ‘what trust’ to build.

What drives trust for particular health insurers is very different from one company to the next.

Our approach, HuTrust®, is a practical, robust and scientifically proven methodology that analyses and builds trust through all functions.

5

TRUST DRIVES THE VAST MAJORITY OF YOUR KPIs

Trust is the root cause of your customer’s attitudes and behaviours.

If trust is the key driver, can you improve your kpis effectively, without understanding it?

6

TRUST: EVERY LITTLE BIT COUNTS

Investor behaviour

Every little bit of trust, added or lost, makes a huge impact on acquistion and retention.

Just 20% more trust with a customer results in an improved attitude and behaviour by 400%

People behaviour

Customer behaviour

7

Working with psychologists and psychology professor w. Salber in 2003, we found that trust consists of 6 distinct categories.

These 6 categories of trust drive over 86% of trust – which, in statistical terms, is pretty much all of it.

The 6 categories of trust in the HuTrust® model are also proven to drive the vast majority of all key customer attitudes and behaviours.

The 6 HuTrust® dimensions are proven to be the drivers of trust and thus your other KPIs.

HUTRUST®: THE SCIENTIFICALLY SOUND AND PRACTICALLY PROVEN WAY TO MEASURE AND BUILD TRUST

HuTrust® makes trust, the key driver of attitudes and behaviours towards you, workable.

The program encompasses measurement, trust driver development and training, and workshop programs that empower your teams to build more and more trust in all functions.

8

UNDERSTANDING TRUST

TRUST & LOYALTY IN

TELCOS

These study findings are to be used to understand the principles, impact and operationalisation of trust – but only as a good indication and hypothesis

9

HUTRUST® EQUITY ANALYSIS

In this study, telstra’s and optus’ customer trust sits at just below the trust threshold.

From our other studies, we would expect this to be a bit higher in your own studies.

Total sample = 300Q: I am loyal to this brand // I trust this brand

YOU ARE HERE

10

LOYALTY & TRUST DISTRIBUTION – TELCO PROVIDER

Other telcos we worked with achieved up to 25% of customers giving them a 10/10 on trust.

Total sample = 300Q: I am loyal to this brand // I trust this brand

I am loyal to this brand

I trust this brand

These customers would be a prime opportunity to shift into 9/10 or 10/10. That’s not done by eliminating pain points and more ‘getting what I want when I want’.

11

‘Why didn’t we do this years ago?’Global Managing Partner, Legal Firm

WHAT YOUR TRUST IS MADE OF…

12

HUTRUST® EQUITY ANALYSIS

The HuTrust® equity analysis shows how strongly you and your competitors are trusted in each of the 6 trust categories.

This is what enables organisations to do something about trust.

Telstra’s own customers appear to trust Telstra less in Relationship, Benefit, Competence and Vision trust than the customers of the other telcos.

Total sample = 300

Customers

Telstra

Optus

Vodafone

13

HUTRUST® EQUITY ANALYSIS

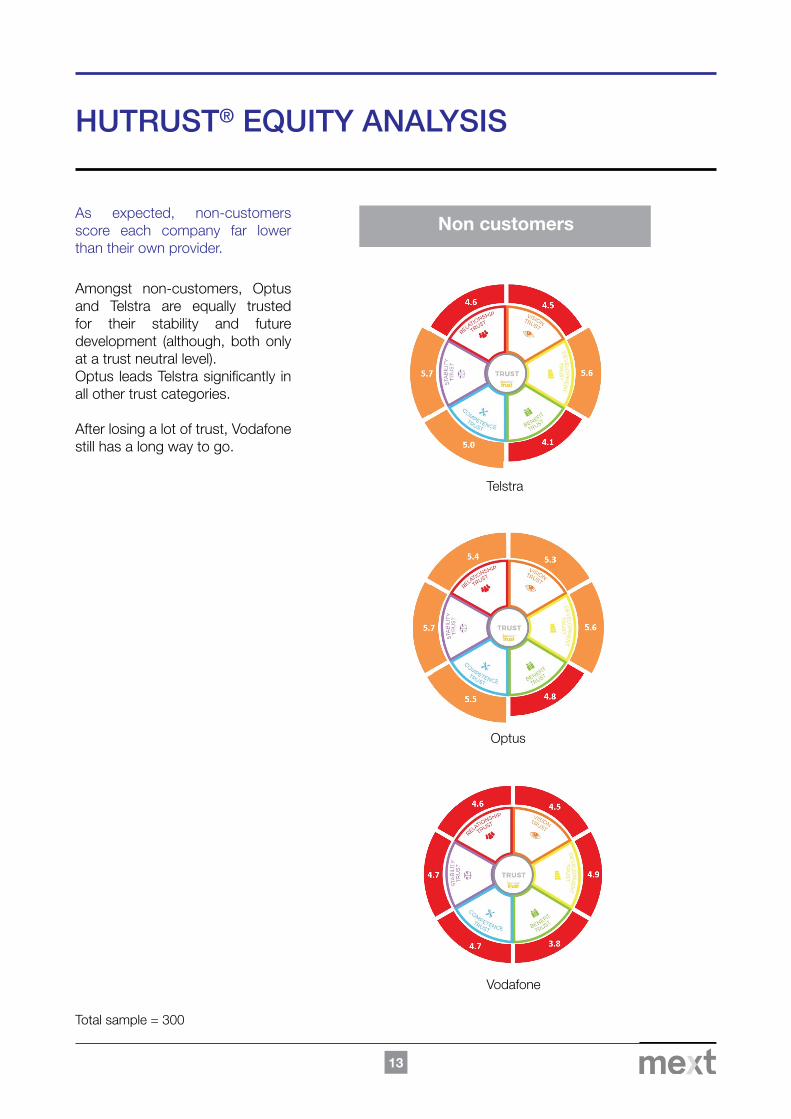

As expected, non-customers score each company far lower than their own provider.

Amongst non-customers, Optus and Telstra are equally trusted for their stability and future development (although, both only at a trust neutral level).Optus leads Telstra significantly in all other trust categories.

After losing a lot of trust, Vodafone still has a long way to go.

Total sample = 300

Non customers

Telstra

Optus

Vodafone

14

WHAT DRIVES YOUR TRUST

15

HUTRUST® DRIVER ANALYSIS – OWN CUSTOMERS

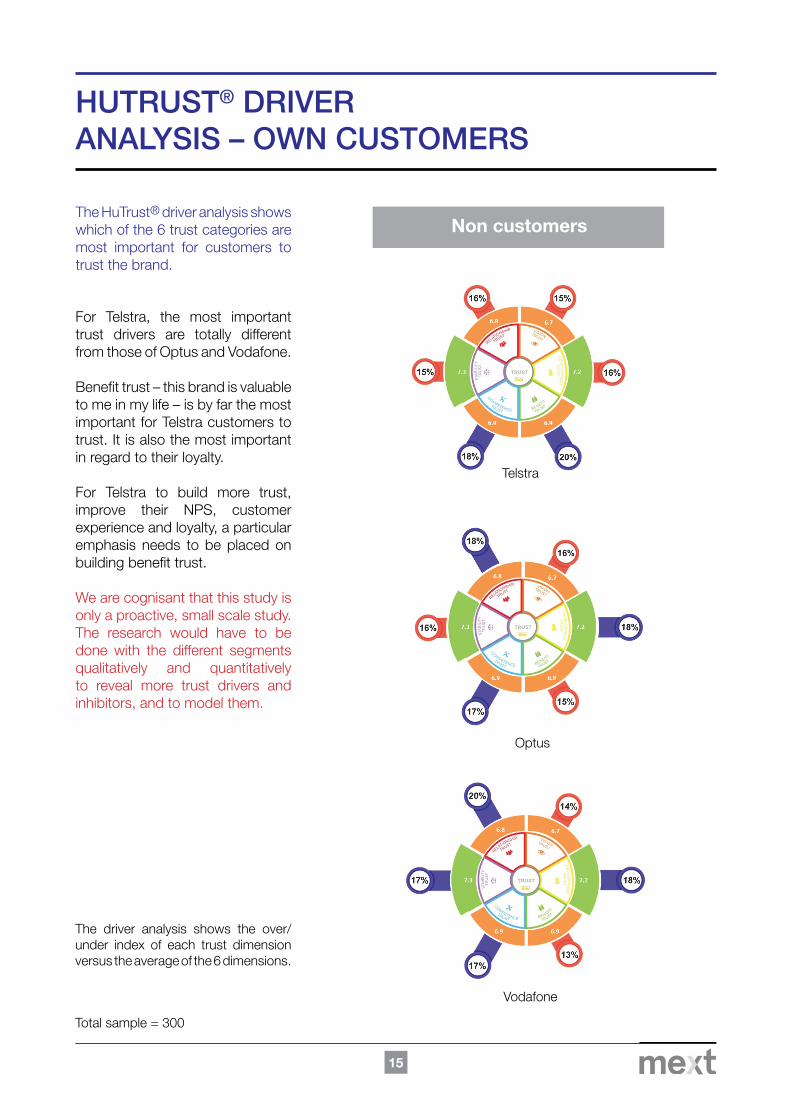

The HuTrust® driver analysis shows which of the 6 trust categories are most important for customers to trust the brand.

For Telstra, the most important trust drivers are totally different from those of Optus and Vodafone.

Benefit trust – this brand is valuable to me in my life – is by far the most important for Telstra customers to trust. It is also the most important in regard to their loyalty.

For Telstra to build more trust, improve their NPS, customer experience and loyalty, a particular emphasis needs to be placed on building benefit trust.

We are cognisant that this study is only a proactive, small scale study. The research would have to be done with the different segments qualitatively and quantitatively to reveal more trust drivers and inhibitors, and to model them.

Non customers

Total sample = 300

Telstra

Optus

Vodafone

The driver analysis shows the over/under index of each trust dimension versus the average of the 6 dimensions.

16

HUTRUST® DRIVER ANALYSIS – OWN CUSTOMERS

Here, we also checked what drives customer loyalty, as it is telstra’s key focus.

Benefit trust shows to be even more important to loyalty than it is for trust.

Customer retention is obviously critical. Loyalty means higher lifetime value, higher degree of product holding, less price sensitivity and lower cost to serve.

For Optus, it becomes clear that development trust is key.For Vodafone it is stability, development and relationship trust.

Customer loyalty drivers

Telstra

Optus

Vodafone

Total sample = 300

17

WHAT FILLS YOUR KEY TRUST BUCKETS BEST

HUTRUST® ATTRIBUTE ANALYSIS –OWN CUSTOMERS

‘It’s not training. It’s not a lecture.

It’s playing to learn how to play better.’Senior executive participant

18

HUTRUST® ATTRIBUTE ANALYSIS – TELSTRA’S OWN CUSTOMERS

THE HUTRUST ATTRIBUTE ANALYSIS TELLS YOU HOW TO BEST BUILD THE FOCUS TRUST.

We are happy to discuss the full set.

We included 61 attribute statements.These were split into: — Business-generic attributes—attributes that relate to an organisation being well run.

— Category-generic attributes—attributes that relate to category product and service factors

— Brand attributes—attributes and values that are brand unique, or could be (in this study we included a number of attributes we know from our qualitative research. It is not a list of your internally agreed values and attributes.

In addition, they broadly covered all 6 HuTrust® categories.

Business-generic attributes Category-generic attributes

Brand attributes

Is well managed

The management is stable

They have been around for a long time

They innovate continuously

They think about innovation beyond product and technology – more about me

I know what they currently do that will benefit me in the future

They understand how I want to contact them

...

They are one of the largest

They have their own network

They have been around for a long time

I know how they will improve/develop their network in the future

They proactively let me know what happens with the NBN

They have access to the best brands and products

They think beyond TELCO, including watches and virtual reality

...

After the government sell-off, Telstra has shown long-term foresight in their choice and smooth transition of management teams and styles by first using an outsider to shake the organisation up, then making the hard and big decisions regarding the network and technology. Further, by using David Thodey to lead a customer-focused change in culture and now Andy Penn, who worked with David as CFO, to continue that path and lay out a clear succession plan.

Telstra were founded to look after our telecommunication needs. And though now privatised, they still regard this foundation as important.

Telstra understand how telecommunications can change our lives and, therefore, invest into the future with telehealth and education.

At Telstra all staff, including IT and finance, regularly have to spend time with customers or join the call centre to ensure they understand customers and what impacts them. So, you may have their CEO listen to your next call and view your next chat.

Telstra has a clear, long-term investment plan, continuing to offer their customers the best option in telecommunications.

...

19

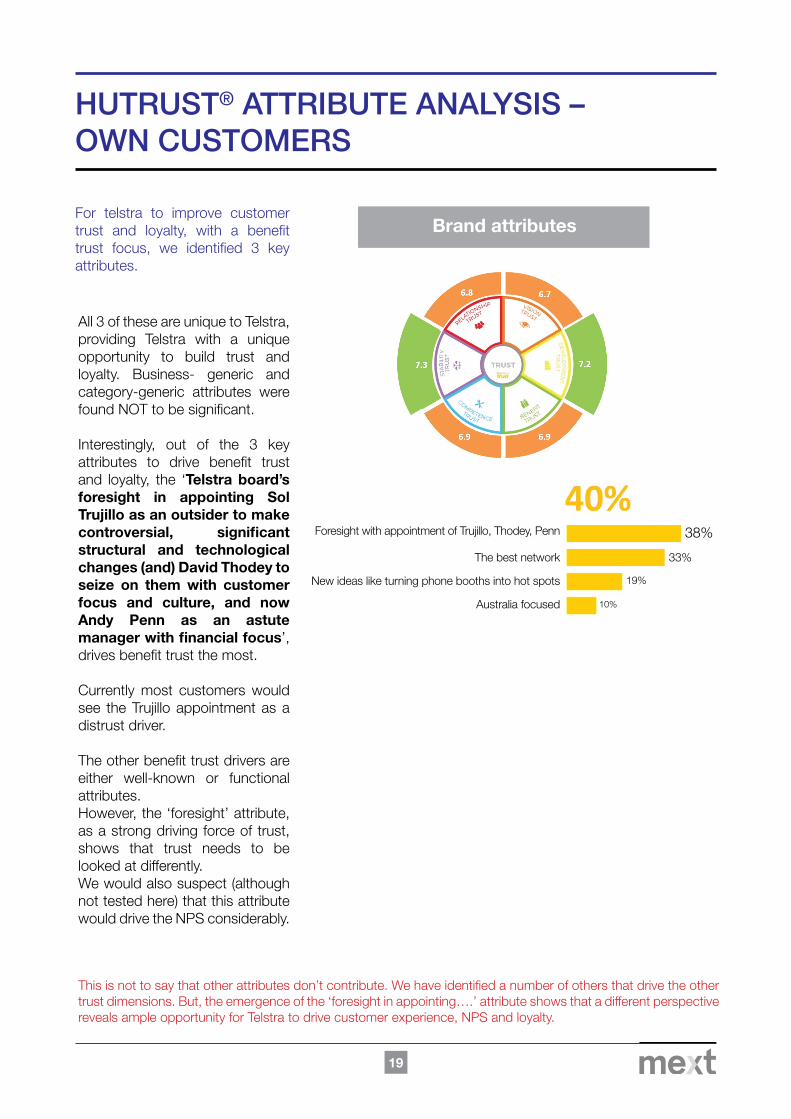

HUTRUST® ATTRIBUTE ANALYSIS – OWN CUSTOMERS

For telstra to improve customer trust and loyalty, with a benefit trust focus, we identified 3 key attributes.

All 3 of these are unique to Telstra, providing Telstra with a unique opportunity to build trust and loyalty. Business- generic and category-generic attributes were found NOT to be significant.

Interestingly, out of the 3 key attributes to drive benefit trust and loyalty, the ‘Telstra board’s foresight in appointing Sol Trujillo as an outsider to make controversial, significant structural and technological changes (and) David Thodey to seize on them with customer focus and culture, and now Andy Penn as an astute manager with financial focus’, drives benefit trust the most.

Currently most customers would see the Trujillo appointment as a distrust driver.

The other benefit trust drivers are either well-known or functional attributes. However, the ‘foresight’ attribute, as a strong driving force of trust, shows that trust needs to be looked at differently. We would also suspect (although not tested here) that this attribute would drive the NPS considerably.

This is not to say that other attributes don’t contribute. We have identified a number of others that drive the other trust dimensions. But, the emergence of the ‘foresight in appointing….’ attribute shows that a different perspective reveals ample opportunity for Telstra to drive customer experience, NPS and loyalty.

Brand attributes

Foresight with appointment of Trujillo, Thodey, Penn

The best network

38%

33%

19%

10%Australia focused

New ideas like turning phone booths into hot spots

20

HUTRUST® ATTRIBUTE OPERATIONALISATION

The attributes identified can be implemented through the best suited channels.

The attribute most effective in improving customer trust and loyalty is also the easiest and least cost and time intensive to implement.

In our work, we continuously find our clients don’t make effective use of their existing trust equity in channels like marketing, sales and service.

Trust and Loyalty driver

Status Action Best channels

Foresight with appointment of Trujillo, Thodey, Penn…..

Unknown, in fact, currently negatively perceived.

The best network Well known. Reminding from time to time. Possibly with localised info.

New ideas, like turning phone booths into hot spots

Well known, but remind and look at fresh, often small, ideas to introduce.

Australia focused Customers are not sure about this. Even the SEA investment doesn’t take this away. Investment into e- health, etc., would support this further.

FOR ILLUSTRATION ONLY

21

UNDERSTANDING TRUST

TRUST & LOYALTY

IN HEALTH FUNDS

These study findings are to be used to understand the principles, impact and operationalisation of trust – but only as a good indication and hypothesis.

22

EXECUTIVE SUMMARY

Trust and Loyalty.

Navy Health garners the highest level of loyalty with 28% of customers scoring them 10/10.For others, the loyalty levels are far lower.

Medibank’s stability trust is clearly impacted by recent issues.But, customers’ trust in Medibank to successfully develop is equal to other providers, indicating a trust in Medibank to overcome the issues.

Customers give their providers the same scores on trust.This is not surprising, because the more we trust, the more loyal we become.

Knowing what drives trust the strongest in one’s brand enables us to focus on and explore how to best build or rebuild it.

In Private Health Insurance, this can be done in a unique and differentiated manner.

What drives trust in each brand is very different.

23

LOYALTY & TRUST SCORES

Total sample = 300Q: I am loyal to this brand // I trust this brand

Medibank, bupa and navy health trust sit just above the trust threshold in the “low trust” category. Gmhba on average sits below the others in “neutral trust”.

Loyalty scores for each company are in line with their trust scores.

I trust this brand

I am loyal to this brand

24

LOYALTY DISTRIBUTION

In this study, navy health garners an impressive 28% of 10/10 in loyalty.

Overall loyalty is not high.

Total sample = 300Q: I am loyal to this brand // I trust this brand

I am loyal to this brand

25

The trust distribution shows the high level of correlation.

This is not surprising. The more we trust someone, the more loyal we are.

Total sample = 300Q: I am loyal to this brand // I trust this brand

I trust this brand

LOYALTY & TRUST DISTRIBUTION – HEALTH PROVIDER

26

HUTRUST® PROFILE – HEALTH PROVIDER

The privatisation and recent issues have had a significant impact on what medibank is trusted for.

All but development trust are affected, indicating that customers trust medibank to overcome the issues.

Navy health score consistently high in all HuTrust® dimensions – but specifically in competence trust.

Total sample = 300Q: Please tell us your level of agreement to the following statements....HuTrust®

Medibank

GMHBA

Bupa

Navy Health

Customers

27

Interestingly, non-customers score all other providers at almost identical levels.

They score other providers very low on trust – a benefit to the particular provider – and, on average, they don’t trust other providers.

Total sample = 300Q: Please tell us your level of agreement to the following statements....HuTrust®

LOYALTY & TRUST DISTRIBUTION – HEALTH PROVIDER

Non customers

Medibank

Bupa

GMHBA

Navy Health

28

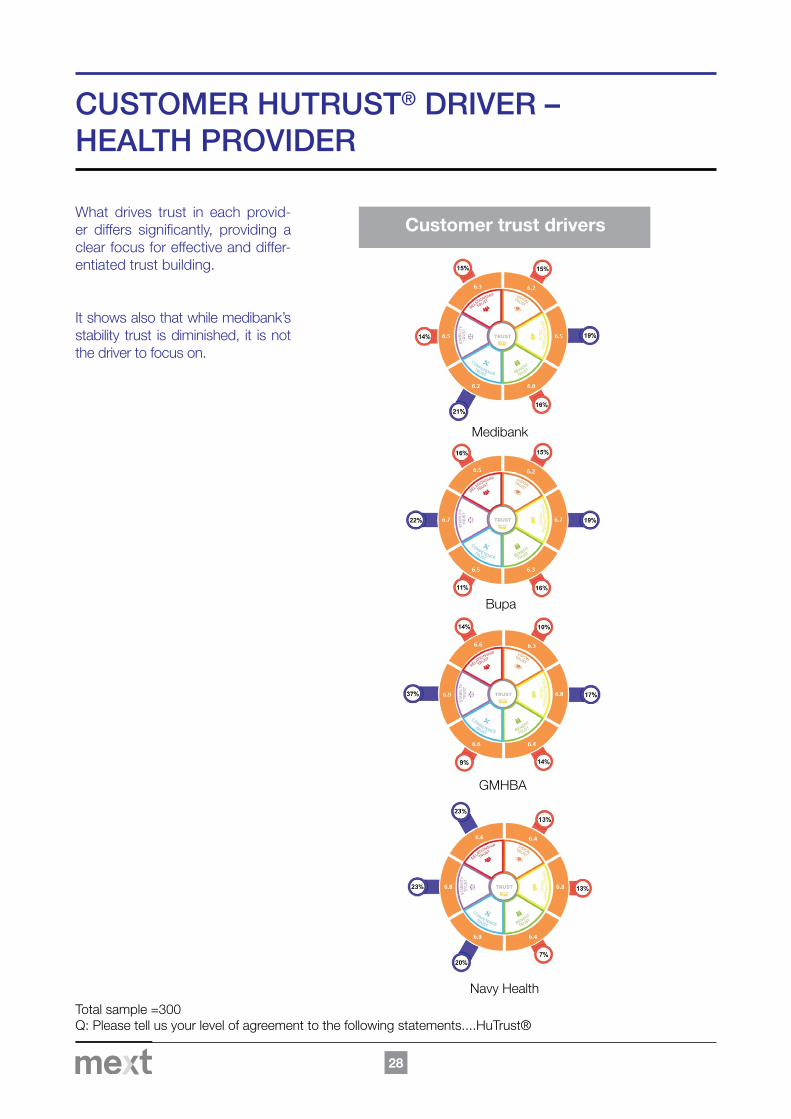

CUSTOMER HUTRUST® DRIVER – HEALTH PROVIDER

What drives trust in each provid-er differs significantly, providing a clear focus for effective and differ-entiated trust building.

It shows also that while medibank’s stability trust is diminished, it is not the driver to focus on.

Total sample =300Q: Please tell us your level of agreement to the following statements....HuTrust®

Medibank

Bupa

GMHBA

Navy Health

Customer trust drivers

29

The loyalty driver analysis polaris-es this further. For medibank, the focus needs to be on rebuilding competence trust.

Total sample =300Q: Please tell us your level of agreement to the following statements....HuTrust®

Customer loyalty drivers

Medibank

Bupa

GMHBA

Navy Health

CUSTOMER HUTRUST® DRIVER – HEALTH PROVIDER

Grow withvision, precision

& certainty®