business index december 2015 - sensis® - marketing ... sensis business index december 2015 covers...

TRANSCRIPT

SensisBusiness Index December 2015A survey of confidence and behaviour of Australian small and medium businesses

Released 20 January 2016

OPEN

Join the conversation:

@sensis #SensisBiz

linkedin.com/company/sensis

www.sensis.com.au/SBI

Sensis Business Index | Small and medium businessesSensis Business Index | Small and medium businesses

Table of contentsIntroduction ...............................................................................................................................................................................................2

About the survey ........................................................................................................................................................................................................................................ 3

Foreword ......................................................................................................................................................................................................................................................4

Executive summary .................................................................................................................................................................................................................................... 5

SMB business cycle analysis .....................................................................................................................................................................................................................7

SBI snapshot ............................................................................................................................................................................................................................................... 8

Small and Medium Business Outlook – National Summary ................................................................................................................10

SMB confidence in their own business prospects over the next 12 months ....................................................................................................................................... 11

Confidence by state and territory, sector and size .................................................................................................................................................................................12

Perceptions of the economy ....................................................................................................................................................................................................................14

Expectations on key indicators for the next 12 months .......................................................................................................................................................................15

Concerns ....................................................................................................................................................................................................................................................16

Sales ...........................................................................................................................................................................................................................................................17

Employment ...............................................................................................................................................................................................................................................18

Wages bill ...................................................................................................................................................................................................................................................19

Prices .........................................................................................................................................................................................................................................................20

Capital expenditure ..................................................................................................................................................................................................................................21

Access to finance...................................................................................................................................................................................................................................... 22

Profitability................................................................................................................................................................................................................................................ 23

Exports ...................................................................................................................................................................................................................................................... 24

Government Policies ...............................................................................................................................................................................25

Government policies ................................................................................................................................................................................................................................ 26

Assessment of Federal Government policies ........................................................................................................................................................................................ 27

Assessment of state and territory government policies ......................................................................................................................................................................28

Small and Medium Business Outlook ...................................................................................................................................................29

National .....................................................................................................................................................................................................................................................30

New South Wales ......................................................................................................................................................................................................................................31

Victoria ...................................................................................................................................................................................................................................................... 32

Queensland ............................................................................................................................................................................................................................................... 33

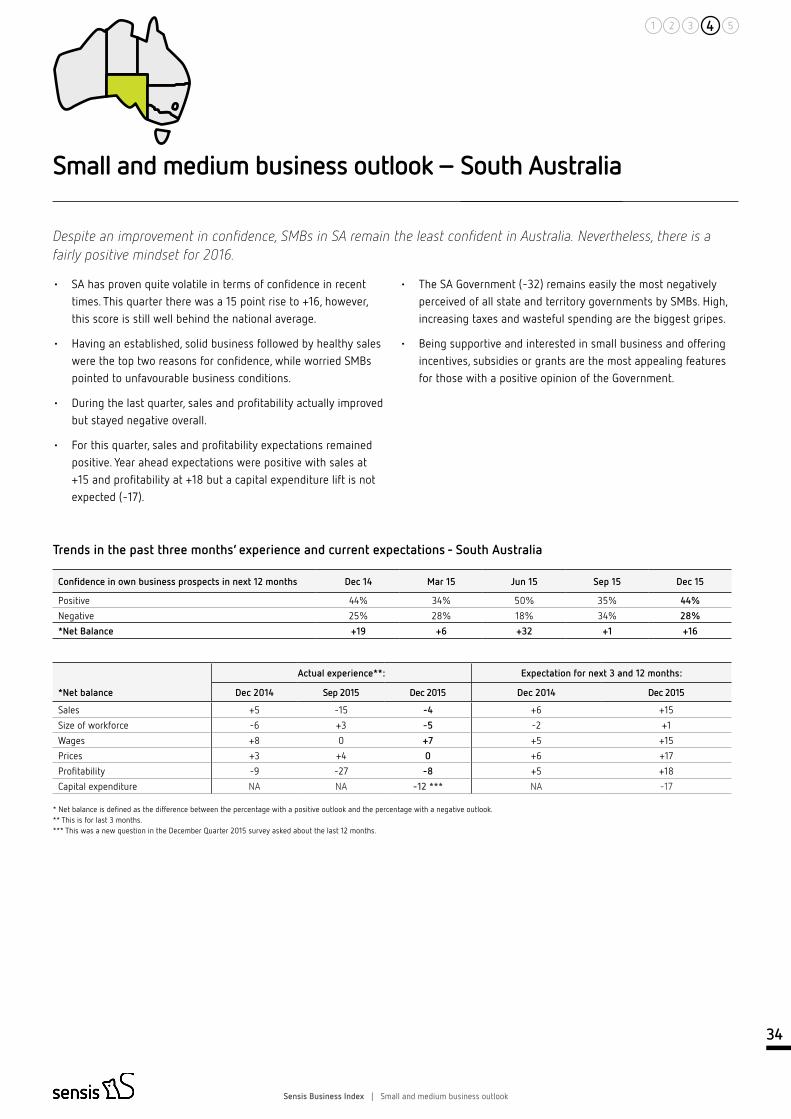

South Australia ......................................................................................................................................................................................................................................... 34

Western Australia ..................................................................................................................................................................................................................................... 35

Tasmania ................................................................................................................................................................................................................................................... 36

Northern Territory ..................................................................................................................................................................................................................................... 37

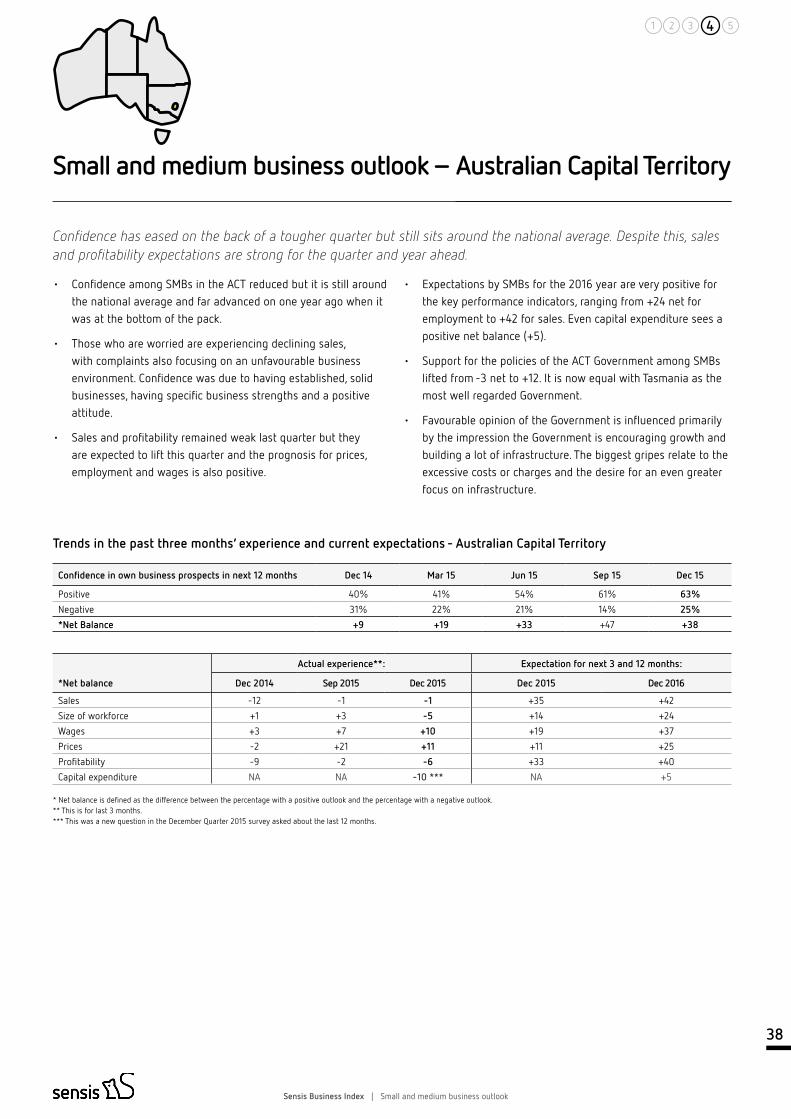

Australian Capital Territory ......................................................................................................................................................................................................................38

Industry Snapshots .................................................................................................................................................................................39

Manufacturing ..........................................................................................................................................................................................................................................40

Building and Construction .......................................................................................................................................................................................................................40

Wholesale Trade ........................................................................................................................................................................................................................................41

Retail Trade ................................................................................................................................................................................................................................................41

Transport and Storage ............................................................................................................................................................................................................................. 42

Communication, Property and Business Services ................................................................................................................................................................................. 42

Finance and Insurance ............................................................................................................................................................................................................................. 43

Health and Community Services ............................................................................................................................................................................................................. 43

Cultural, Recreational and Personal Services ........................................................................................................................................................................................ 44

Hospitality (Accommodation, Cafes and Restaurants) ......................................................................................................................................................................... 44

Sensis Business Index | Introduction

2

1 3 42 5

IntroductionThe Sensis Business Index is a quarterly survey of Australia’s small and medium businesses (SMBs) which commenced in 1993 to measure and track:

• SMB business activity over the previous quarter.

• Expectations for the current quarter.

• Overall confidence among SMBs.

The Sensis Business Index samples SMBs nationally, enabling broad scrutiny of this market and relevant trends and issues. It examines differences by location, business size and industry. The aim is to reflect the attitudes and behaviour of SMBs, which comprise some 99% of Australian businesses.

Results are based on the responses of SMBs surveyed and reported as a net balance, which represents total positive responses minus total negative responses.

The Sensis Business Index is an initiative of Sensis as part of its commitment to this vital business sector. As Australia’s #1 marketing services company, we’re here to engage consumers with Australian businesses. We make this happen through a number of leading brands - Yellow Pages, White Pages, TrueLocal, Whereis and Skip and our expert digital know-how. Our digital expertise is what sets us apart - we give businesses a competitive edge through websites, search engine marketing and optimisation, data, and through our digital advertising agency, Found.

Sensis Business Index | Introduction

3

1 3 42 5

The Sensis Business Index December 2015 covers the period October to December. It is based on 1,001 telephone interviews conducted with small and medium business proprietors or managers, respectively employing less than 20 and 20-199 people.

This sample is drawn from metropolitan and major non-metropolitan regions throughout Australia, with targets set for location and industry as shown opposite. Interviewing was conducted from October 19 to November 23, 2015. TKW is responsible for sampling and fieldwork and Di Marzio Research for analysis and reporting.

Results for each survey are weighted so the sample is reflective of the total SMB population. Prior to 2015 the weighting was by selected ANZSIC (industry sector) divisions within the metropolitan and non-metropolitan region of each state and territory as per the Australian Bureau of Statistics (ABS) Business Register of June 1998. Now the weighting is also by industry, location and business size but based on the most current ABS data contained in the publication 8165.0 - Counts of Australian Businesses, including Entries and Exits, Jun 2009 to Jun 2013. Some adjustments to this weighting data were also made by Sensis to exclude firms with a turnover of under $50,000 per annum. These are primarily non-operating and/or non-employing firms.

This report covers experiences over the last quarter and expectations for the current quarter. It also covers expectations for the year ahead, which are only asked in the December quarter survey.

About the survey

Total Metro Regional

New South Wales 170 110 60

Victoria 170 110 60

Queensland 170 90 80

South Australia 125 90 35

Western Australia 125 89 36

Tasmania 80 40 40

Northern Territory 81 40 41

Australian Capital Territory 80 80 -

Total 1,001 649 352

Location of business

Industry sector

Business location

65% Metro

35% Regional

Manufacturing 105

Building and Construction 155

Wholesale Trade 75

Retail Trade 135

Hospitality (Accommodation, Cafes and Restaurants) 57

Transport and Storage 74

Finance and Insurance 66

Communication, Property and Business Services 170

Health and Community Services 79

Cultural, Recreational and Personal Services 85

Total Businesses 1,001

90% Small

(1-19 employees)

10% Medium

(20-199 employees)

Business size

OPEN OPEN

Sensis Business Index | Introduction

4

1 3 42 5

After a fairly flat 2015, Australian businesses ended the year on a high, posting the highest net confidence score for almost five years.

Sensis spoke to 1,000 Australian small and medium businesses for the latest Sensis Business Index survey, with the results showing more than three times as many businesses are now confident, as those who are concerned. Confidence went up everywhere except the Australian Capital Territory, with businesses more optimistic thanks to their specific business strengths, as well as healthy sales.

This was the first survey to be taken since Malcolm Turnbull took over from Tony Abbott and it is clear the new Prime Minister has had a positive impact on perceptions of the Government, as well as a halo effect on business confidence.

Despite being more confident in their own business prospects, perceptions of the economy continue to be negative with 86 percent of businesses still thinking the economy is either slowing or standing still. Looking ahead, however, there was an 11 point improvement in the expectations for the economy in 12 months’ time, with the net balance entering positive territory for the first time since December 2014.

Not unexpectedly, support for the Federal Government went up six points, with eight percent of businesses pointing to the new Prime Minister as a reason for their positive perceptions.

In the last survey Tasmania was the only region where support for the Federal Government went up, but in this survey the reverse was true with all states registering a positive uplift bar one. South Australia is now the most supportive of the Federal Government’s policies, with only Western Australia posting a negative net balance.

In the December quarter we also examine year ahead expectations for a range of indicators. With the exception of capital expenditure all of the other indicators are looking positive. These include sales, employment, wages, prices and profitability.

As we enter 2016 SMBs primary concern remains a lack of work or sales. This is also a growing barrier to businesses taking on new staff. Another concern is finding and retaining suitable staff with the right skills and training.

In terms of exports there has been little change in this area for the last 12 months and exports haven’t grown now for three years. Eleven percent of SMBs are currently exporting and only one percent of those not exporting plan to do so in the year ahead.

Obviously this varies greatly across the industry sectors, with manufacturers and wholesalers much more export oriented. Looking at the sectors more generally, confidence again rose in health and community services this quarter for it to retain top spot, while poor sales saw manufacturing become the least confident sector.

I’d be keen to hear your thoughts on the issues you see impacting on small and medium businesses this year using #SensisBiz.

John Allan, Chief Executive Officer, Sensis

Foreword

Sensis Business Index | Introduction

5

1 3 42 5

Historical trends and overall SMB highlights

SMB confidence lifted strongly to reach levels last seen two years ago and the highest score since March 2011. Despite difficult business conditions, the economy is expected to improve and performance expectations are fairly positive for the quarter and year ahead. The new Prime Minister appears to have had some impact as views of the Federal Government have improved.

The key findings of the Sensis Business Index December 2015 are:

• SMB confidence jumped twelve points to net +39. This compares with +27 a year ago.

• Confidence rose in all locations except the ACT. The most confident State is now Tasmania (+64 net), which saw a major improvement of 46 points. Double figure rises were also noted in NSW, Queensland, SA and WA.

• Opinions of the current state of the economy improved marginally but remain negative. More SMBs still believe the economy is slowing (31%) rather than growing (14%). They are now more hopeful about the health of the economy in 12 months’ time however (up from -4 to +7).

• Last quarter, performance indicators were uninspiring with sales and profitability both slightly negative.

• This quarter, all indicators are expected to remain positive on balance but to a lesser degree than last time.

• In the December quarter we also measure key indicator expectations for the year ahead, including for capital expenditure. There is a fairly positive outlook on all indicators except capital expenditure (-6). Sales expectations registered a net balance of +34, while for profitability it is +28 with prices at +32, wages at +25 and employment at +11. Apart from prices, which were four points higher, the expectations for the other four indicators were two to six points lower than a year ago.

• Lack of work or sales remains the most mentioned barrier to

taking on staff, followed by difficulty in finding suitable staff.

• Last survey, opinions of the Federal Government had deteriorated but there has now been some improvement. Previously, the proportion of SMBs believing the Federal Government’s policies help small business almost equalled those with the opposite view but now the net balance is +7. The key drivers for this change are tax and incentive related but 8% spontaneously mentioned the new Prime Minister as a reason for regarding the Government favourably.

• Among state and territory governments, only Tasmania (+12), the ACT (+12) and NSW (+11) receive a positive score from SMBs. Perceptions of the ACT Government moved into positive territory (-3 to +12), while the NT Government went from a positive to negative assessment (+10 to -4). The majority of the State Governments remain unpopular, with the SA Government (-32) remaining the most poorly regarded by SMBs.

Executive summary

Sensis Business Index | Introduction

6

1 3 42 5

Metropolitan versus regional

Confidence lifted among both metropolitan and regional SMBs.

Key findings relating to metropolitan and regional businesses included:

• Confidence rose 15 points in metropolitan locations and four points among regional SMBs. The gap in confidence between metropolitan and regional SMBs increased from four to 15 points (+44 versus +29).

• Metropolitan and regional SMBs remain similarly pessimistic overall about the current state of the economy (-17 net in regional compared to -18). However, metropolitan SMBs have stronger expectations for the economy in a year’s time (+10 versus +3).

• There were no major differences between metropolitan and regional SMBs on key performance indicators in the past quarter, with those results generally soft.

• For the current quarter there are positive expectations for all indicators in both metropolitan and regional locations, with net balances slightly higher in metropolitan areas or equal. Sales (+16 and +15) and profitability (+13 and +7) forecasts are relatively modest in both segments.

• Year ahead expectations are quite solid on all key indicators except capital expenditure in both metropolitan and regional areas, although they are slightly more positive among metropolitan SMBs. The respective sales and profitability forecasts for 2016 are +38 and +28 for sales and +32 and +20 for profitability.

• Both metropolitan and regional SMBs are more positive towards the Federal Government’s policies. Their net balances are the same but a greater increase occurred in regional areas (from -3 to +7) compared to metropolitan areas (from +3 to +7).

Executive summary

Industry sector trends

Most sectors have found conditions challenging recently but all sectors have a positive outlook for 2016, especially health and community services.

• The health and community services sector again displayed the highest confidence level (+65) and is well ahead of all other sectors on this measure. Around the average are building and construction; cultural, recreation and other services; communication, property and business services; and finance and insurance. Retail trade; transport and storage and manufacturing were below the average.

• Sales performances last quarter ranged from modest to poor, with wholesale recording the highest net balance of +14 followed by +6 for cultural, recreation and other services. Transport and storage (-20) and retail (-13) battled the hardest.

• Negative profitability results were common last quarter with communication, property and business services the only positive performer (+10). Retailers (-23) struggled most on profitability followed by transport and storage (-14).

• For the current quarter, sales and profitability expectations are generally positive across the sectors with some variations. The best sales expectations are in retail and health and community services (+32 in each), while the lowest are in transport and storage (+2). On profitability, retail led with a +27 net balance, while hospitality was the weakest on -9.

• The net balances for year ahead sales expectations ranged from +24 in transport and storage to +53 in health and community services. For profitability, the same two sectors stood out at the top and bottom - health and community services with +40 and transport and storage with +13.

Sensis Business Index | Introduction

7

1 3 42 5

A challenging last quarter has dampened performance expectations however they remain positive. SMBs are more confident about the economy and their own business prospects in 2016.

Examining the latest key indicator results shown opposite provides a gauge on the potential direction of the Australian economy.

Performance indicator results last quarter were uninspiring, yet confidence about their own business prospects for the next 12 months has lifted sharply and SMB perceptions of the economy in 2016 are now also positive. The Federal Government is more favourably viewed, coinciding with the change in Prime Minister and this appears to have influenced assessments and expectations measured in this survey.

SMB business cycle analysis

Results for this quarter

Expectations for this quarter

Expectations for next 12 months

Business Confidence

NA NA Increased optimism

Economy NA NA Improved from pessimism to

optimism

Sales Flat Lower but positive Lower but still quite optimistic

Employment Flat Marginally lower but positive

Marginally lower but optimistic

Wages Lower but positive Lower but positive Lower but still quite optimistic

Prices Flat but positive Marginally lower but positive

Lower but still quite optimistic

Profitability Marginally up but negative

Lower but positive Lower but still quite optimistic

Capital Expenditure

NA NA Lower and now pessimistic

Sensis Business Index | Introduction

8

1 3 42 5

SBI snapshot

Tasmania +64 ( 46)

+39 net balance- =57% feel confident

Because of:•Specific business strengths•Established, solid business•Healthy, growing sales

18% feel worried

Because of: • Unfavourable business, economic or industry environment• Decreasing sales

Increased 12 points from last quarter

65%Metro

35%Regional

90%Small

10%Medium

SBI SnapshotThe Sensis Business Index has tracked the confidence and behaviourof Australia’s small and medium businesses (SMBs) since 1993.Here are some of the key findings of the latest report.

Who did we survey?

What did they tell us?

Region

SMBs feeling confident

Business size

OPENOPEN

Net confidence increased to

Up 12 points from last quarter

points+39SMB confidence by state

Western Australia +31 ( 13)

Queensland +35 ( 10)

Northern Territory +24 ( 2)

South Australia +16 ( 15)

New South Wales +46 ( 12)

National average +39 ( 12)

Australian Capital Territory +38 ( 9)

Victoria +38 ( 6)

1 3 42 5

Health and Community Services +65 ( 24)

Perceptions of the economy now

2 points higher than last quarter

Slowing+31%

Growth+14%

Standing Still+55%

Better+28%

Same+51%

Worse+21%

Perceptions of the economy a year from now

11 points higher than last quarter

SBI Snapshot

-17Net balance

+7Net balance

SMB confidence by sector

Cultural, Recreational and Personal Services +42 ( 20)

Hospitality (Accommodation, Cafes and Restaurants) +38 ( 14)

Building and Construction +47 ( 21)

Manufacturing +15 ( 2)

Retail Trade +19 ( 3)

Wholesale Trade +30 ( 28)

Communications, Property and Business Services +38 ( 2)

National average +39 ( 12)

Finance and Insurance +40 ( 2)

Transport and Storage +24 ( 6)

Experience and expectations on key business indicators

* Net balance is defined as the difference between the percentage reporting an increase and the percentage reporting a decrease.** Actual experience relates to last 3 months. *** Expectation is for next 12 months.

*Net Balance for Key Indicators Actual experience** Expectation for next 12 months***

Change in expectation for next 12 months

Sales -1 +34 ↓6

Size of workforce 0 +11 ↓2

Wages +6 +25 ↓5

Prices +9 +32 ↑4

Profitability -5 +28 ↓6

Capital expenditure NA -6 ↓15

10

1 3 42 5

10

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Small and Medium Business Outlook – National Summary

SMB confidence in their own business prospects over the next 12 months ............................................................................. 11

Confidence by state and territory, sector and size ..........................................................................................................................12

Perceptions of the economy .................................................................................................................................................................14

Expectations on key indicators for the next 12 months ................................................................................................................ 15

Concerns ................................................................................................................................................................................................. 16

Sales ...........................................................................................................................................................................................................17

Employment ............................................................................................................................................................................................ 18

Wages bill ................................................................................................................................................................................................. 19

Prices .......................................................................................................................................................................................................20

Capital expenditure ................................................................................................................................................................................21

Access to finance ..................................................................................................................................................................................22

Profitability ..............................................................................................................................................................................................23

Exports ....................................................................................................................................................................................................24

11

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

SMB confidence in their own business prospects over the next 12 months

Net confidence has lifted to the highest score since March 2011.

Key findings

The net confidence level of Australian SMBs rose this quarter to a level not seen since December 2013.

Last quarter (July - September)

The net balance figure was up 12 points to +39, with 57% of SMBs feeling confident about their prospects for the year ahead and 18% feeling worried. This represents a significant shift as the net balance had barely moved for the previous twelve months. The last time a similar net balance was observed was in the December quarter of 2013 when the score was +38.

Once more the leading factors generating confidence are specific strengths of the business, being an established, solid business and healthy, growing sales.

Lack of work or sales continues to be the prime cause of concern.

Small Business (up to 19

employees)

Medium Business (20 - 199

employees)

Total Small and Medium

Extremely confident 9 10 9

Fairly confident 48 44 48

Neutral 25 26 25

Fairly worried 13 13 13

Extremely worried 5 7 5

Total confident 57 54 57

Total worried 18 20 18

*Net Balance +39 +34 +39

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Confident 51% 49% 51% 50% 57%

Worried 24% 22% 20% 23% 18%

*Net Balance +27 +27 +31 +27 +39

Overall confidence - Dec 2015

Confidence trends - past five quarters

Thinking about the next 12 months, how confident do you feel about your business prospects?

100%

50%

0%

Confident Worried *Net balance

Long term trends in confidence

* Net balance is defined as the difference between the percentage who are confident and the percentage who are worried.

Note: rounding occurs

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

57%

+39

18%

12

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Confidence by state and territory, sector and size

Confidence was higher almost across the board and substantially so in some cases.

Key findings

Confidence lifted everywhere except the ACT. Queensland improved for a third consecutive quarter with double figure improvements also noted in NSW, SA, WA and Tasmania. In Tasmania the net balance for confidence more than tripled. In Victoria confidence resembles the national average. SA is still clearly bottom of the pack but positive overall. The NT improved by only two points.

Confidence lifted more in metropolitan than regional areas. The gap is now 15 points compared to four points last quarter. Most regional areas are far less confident than their metropolitan counterparts. Most sectors are clearly more confident but some large differences exist. Small firms are now more confident than medium firms.

Last quarter

Tasmania jumped into a clear leadership position on confidence, rising 46 points to +64 net. NSW improved 12 points to +46, Victoria by six points to +38 and Queensland by 10 points to +35. WA (+31) and SA (+16) lifted 13 and 15 points each but remain below average, as does the NT (up two points to +22). The only fall was recorded in the ACT (down 9 points to +38).

The most confident capital city is Hobart, followed by Sydney and Brisbane with others under the national average. Darwin is now the most negative capital city having overtaken Adelaide. Regionally, confidence was strongest in Tasmania with the NT and WA also clearly above average. Regional SMBs in SA and Queensland were the least positive.

Confidence was easily highest in the health and community services sector, with building and construction the only other industry noticeably above average. However, communications; property and business services; finance and insurance; cultural, recreational and personal services; and hospitality are around the national average. Confidence is positive but relatively low in manufacturing; retail, wholesale trade; transport and storage.

Last survey medium sized businesses were much more positive about their prospects than small businesses - by a gap of 28 points - but that is no longer true with their net balance now at +34 compared to +39 for small businesses. Previously their net balances were +54 and +26 respectively, hence there has been quite a fall in the confidence of medium firms and a sizeable rise for small businesses.

13

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Confidence by state and territory, sector and size

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

National +27 +27 +31 +27 +39

New South Wales +24 +38 +31 +34 +46

Victoria +38 +33 +42 +32 +38

Queensland +13 +10 +18 +25 +35

South Australia +19 +6 +32 +1 +16

Western Australia +38 +29 +28 +18 +31

Tasmania +38 +32 +39 +18 +64

Northern Territory +46 +35 +43 +22 +24

Australian Capital Territory +9 +19 +33 +47 +38

Metro Regional Total

National +44 +29 +39

New South Wales +56 +32 +46

Victoria +42 +29 +38

Queensland +55 +22 +35

South Australia +15 +20 +16

Western Australia +27 +41 +31

Tasmania +73 +60 +64

Northern Territory -3 +45 +24

Australian Capital Territory +38 NA +38

Trends by state - *net balance

Metro and regional confidence - *net balance

Confidence by business size

Confident Worried *Net Balance

Total 57% 18% +39

1-2 Employees 51% 17% +34

3-4 Employees 60% 22% +38

5-9 Employees 63% 15% +48

10-19 Employees 63% 22% +41

Total Small Business 57% 18% +39

20-99 Employees 56% 20% +36

100-199 Employees 42% 17% +25

Total Medium Business 54% 20% +34

Confidence by sector

Confident Worried *Net Balance

Manufacturing 48% 33% +15

Building/Construction 60% 13% +47

Wholesale Trade 56% 26% +30

Retail Trade 48% 29% +19

Transport/Storage 46% 22% +24

Communication Property & Business Services

55% 17% +38

Finance and Insurance 53% 13% +40

Health and Community Services 74% 9% +65

Cultural, Recreational and Personal Services

62% 20% +42

Hospitality (Accommodation, Cafes and Restaurants)

55% 17% +38

* Net balance is defined as the difference between the percentage of SMBs with a positive outlook and the percentage with a negative outlook.

Note: rounding occurs.

14

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

SMB expectations for the economy are improving.

Key findings

SMB assessments of the current state of the Australian economy are not quite as negative as last survey and their expectations for the next year have shifted into positive territory.

Last quarter (July - September)

There were one point improvements in the proportions believing the economy is growing or slowing down. This led to a net balance of -17 compared to -19 previously.

SMB perceptions of the current state of the economy stayed negative everywhere but Tasmania (+1). They remain lowest in SA (-32) and WA (-32), despite lifting 8 and 9 points respectively.

Regional SMBs (-17) are similar to those in metropolitan locations (-18) on this measure.

Views about the economy in a year’s time have improved by 11 points and are now positive on balance. The proportion expecting the economy to get better was up eight points from the prior survey with a three point drop in the proportion who feel the economy will be worse in a year’s time. As a result, the net balance was +7 compared to -4 last time, -2 previously and -9 before that. There had been positive net balances throughout 2014.

Expectations are now positive everywhere but SA (-5) and the NT (-8). There is a double figure net balance for year ahead expectations in NSW (+12), WA (+14), Tasmania (+22) and the ACT (+15).

There was a seven point gap between metropolitan (+10) and regional (+3) SMBs on this measure.

Perceptions of the economy

55+31+14+y 51+21+28+y Same

Worse

5128

21

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

The economy now

Growth 19% 12% 13% 13% 14%

Slowing 28% 35% 28% 32% 31%

*Net Balance -9 -23 -15 -19 -17

The economy a year from now

Better 28% 20% 18% 20% 28%

Worse 22% 29% 20% 24% 21%

*Net Balance +6 -9 -2 -4 +7

NSW VIC QLD SA WA TAS NT ACT

The economy now

Growth 18% 9% 17% 8% 8% 19% 13% 16%

Slowing 27% 36% 27% 40% 40% 18% 40% 22%

*Net Balance -9 -27 -10 -32 -32 +1 -27 -6

The economy a year from now

Better 33% 22% 27% 20% 36% 34% 24% 30%

Worse 21% 20% 24% 25% 22% 12% 32% 15%

*Net Balance +12 +2 +3 -5 +14 +22 -8 +15

Perceptions of the economy - trends

Perceptions of the economy by state

60

0

20

40

-20

-40

-60

-80

The economy now The economy a year from now

Perceptions of the economy Long term trends - *net balance

Dec 1

2

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

SlowingBetter

The economy now The economy a year from now

GrowthStanding

still

Dec 1

3

5531

14

Dec 1

4

Dec 1

5

+7

-17

15

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Almost all the year ahead indicators were positive while lower than this time last year.

Key findings

Five of the six year ahead business indicators were lower relative to the 2014 December quarter findings. SMBs are still more likely to be expecting increases in sales, employment, wages, prices and profitability than falls. The exception is capital expenditure.

Next 12 months (to December quarter 2016)

Forty seven percent expect an increase in sales over the next 12 months with 13% expecting a decline. The net balance of +34 is six points lower than the 2014 result. SMBs in all states and territories were again positive with respect to increased sales. The net balance varied from a low of +15 in SA to a high of +56 in Tasmania. The ACT (+42), Victoria (+40) and NSW (+37) exceeded the national average.

The health and community services sector is the most confident with a net +53 expecting better sales. The least optimistic sector is finance and insurance on net +22.

Employment expectations for 2016 eased two points to a net balance of +11. Around the nation Tasmania had the best results with a net balance of +24. The least optimistic SMBs are in SA (+1) and the NT (+5).

By industry the community, property and business services sector is the most bullish about employment results on +19, with retail the least positive on +3. Most of the other sectors resembled the national average in their year ahead employment expectations.

Wages and salary costs for the year ahead are anticipated to increase with a net balance result of +25. The strongest expectations for wages were recorded in Tasmania (+41) and the lowest in SA (+15). The wholesale sector is forecasting the biggest rise in wages over the next year (net balance of +39) followed by health and community services (+30). Retail stands out as the lowest on this measure (+13).

Selling price expectations for the year ahead were four points higher than in the December 2014 quarter, with 36% expecting an increase and just 4% a fall in the prices they charge. Those in NSW (+41) and in the wholesale sector (+46) are the most likely to be expecting increased prices.

Expectations on key indicators for the next 12 months

Profitability expectations were down six points to net +28 in the latest survey. Tasmania (+42) and the ACT (+40) recorded the strongest profit expectations for the year ahead. At an industry level the health and community services sector (+40) displayed the highest annual profit expectations.

Capital expenditure expectations for the year ahead were down 15 points to a net balance of -6. The only positive capital expenditure expectations for the next 12 months were recorded in Tasmania (+3) and the ACT (+5). By industry this was true only for health and community services (+3) and finance and insurance (0).

Expect an increase

Expect a decrease

*Net Balance

Value of sales 47% 13% +34

Size of workforce 19% 8% +11

Wages bill 35% 10% +25

Prices charged 36% 4% +32

Profitability 44% 16% +28

Capital expenditure 28% 34% -6

Dec 13

Dec 14

Dec 15

Value of sales +58 +40 +34

Size of workforce +19 +13 +11

Wages bill +42 +30 +25

Prices charged +34 +28 +32

Profitability +52 +34 +28

Capital expenditure +9 +9 -6

Expectations on key indicators over the next 12 months - Dec 2015

Expectations on key indicators - Trends in net balance over next 12 months

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

16

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Once more lack of work or sales is the most mentioned concern.

Key findings

A similar proportion of SMBs (41%) said they are facing no significant problems in their business as last time (39%). As discovered for many surveys now, lack of work or sales is cited above any other concern.

Last quarter

Nineteen percent nominated lack of work or sales revenue as the main issue impacting their business. This was up one point from last quarter. This concern stood out most in Queensland and SA at 24% each and least in Tasmania at 10%. In the finance and insurance sector only 9% worried about lack of work but this was 28% in manufacturing.

Spontaneous concern about the economic climate was mentioned by 11%, compared to 14% last time. Economic climate includes issues such as consumer confidence and spending levels, interest and exchange rates, concerns about the general economic climate, as well as global, state and regional economic concerns. This was most prominent in SA (20%) and WA (19%) as well as in the retail sector (17%).

Competition concerns registered 10% (previously 7%) with this figure at 11% in WA and 19% in the transport and storage sector.

Cash flow, bad debts or profitability, down three points, was mentioned by 7% overall, 11% in SA and by 11% of manufacturers.

All other issues were raised by fewer than 10% of SMBs and that has been a consistent situation for some time now.

Interestingly, 6% of SMBs mentioned difficulties in finding quality staff and when asked what specific problems they encountered the primary reasons given were lack of qualified or skilled staff (20%) and finding people who want to work (15%).

Concerns

As far as your business is concerned, what problems, if any, are you facing at the moment?

Prime concerns

Lack of work/sales

Economic climate

Competition

Cash flow/bad debts/profitability

Paperwork/bureaucracy

Finding/keeping staff

Costs/overheads

Employment costs and regulations

Taxes

No concerns = 41%

19%11%

10%7%7%

6%3%

2%2%

20%

25%

30%

15%

10%

5%

0%

Prime concerns - long term trends - lack of work or sales

Dec 1

2

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

3

Dec 1

4

Dec 1

5

19%

Prime concerns - long term trends - economic climate

15%

20%

25%

10%

5%

0%

Dec 1

2

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

3

Dec 1

4

Dec 1

5

11%

Prime concerns - long term trends - cash flow20%

5%

10%

15%

0%

Dec 1

2

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

3

Dec 1

4

Dec 1

5

7%

17

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Sales remain flat and expectations have reduced but remain optimistic.

Key findings

Overall, sales performance has continued to be weak despite expectations for the quarter ahead remaining optimistic.

Last quarter

Sales performance registered a net balance of -1, which was one point down on the previous quarter.

Sales performance was best in Tasmania (+17) followed by Victoria (+5). It was worst in WA (-19).

Across industry sectors, wholesale recorded the leading sales performance (+14) while the weakest was in transport and storage (-20). Retail was also a struggling sector (-13).

Current quarter

SMBs are expecting higher sales over the current quarter. Thirty two percent expect an increase in sales and 16% forecast a fall giving a net balance of +16, which is eight points lower than last time.

Sales expectations are positive in all locations except the NT where the net balance is -9. Tasmania and the ACT stood out with net balances of +46 and +35.

By industry, the expectations are best in the health and community services and retail sectors (+32 in each).

Next 12 months

Twelve month sales expectations were six points lower to net +34, with 47% expecting their sales to increase in the next 12 months and 13% expecting a decrease. This net balance score compares with +58 observed two years ago in December 2013.

Sales

50

40

30

20

10

0

-10

-20

-30

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last Quarter

Experienced increase 33% 30% 23% 29% 26%

No change 34% 37% 50% 41% 45%

Experienced decrease 31% 31% 25% 29% 27%

*Net Balance +2 -1 -2 0 -1

Current Quarter

Expect increase 34% 43% 31% 38% 32%

No change 43% 44% 55% 46% 49%

Expect decrease 20% 12% 13% 14% 16%

*Net Balance +14 +31 +18 +24 +16

Value of sales

Experience Expectations

Value of sales - trends in *net balance

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

+16

-1

Dec 1

5

18

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

A subdued employment situation perseveres.

Key findings

This indicator has not gained traction for quite some time.

Last quarter

Ten percent of SMBs increased employment and 10% reported a decrease creating a neutral net balance. The net balance range has been -4 to +1 for the last six quarters.

At a state level, the best result was in Queensland (+10). It was not positive anywhere else. WA and Tasmania were lowest with a net balance of -6.

The best performing sector was cultural, recreational and other personal services (+8), in stark contrast to transport and storage (-7).

Fifty-two percent reported barriers to taking on new employees (50% last survey). Lack of work or sales is again the dominant barrier, mentioned by 49% (42% last survey). Business growth remained the prime reason for boosting staff.

Current quarter

Minimal change was noted again with 12% forecasting an increase and 7% expecting to shed staff. The net balance of +5 is in line with the last five surveys.

Tasmania (+16) is the most optimistic, while SMBs in SA (-2) and the NT (-10) are in negative territory.

By sector, expectations are highest in cultural, recreational and personal services (+14) and lowest in hospitality (-2).

Next 12 months

Year ahead expectations are positive. Nineteen percent expect an increase and 8% a decrease. The net balance of +11 compares with +13 in 2014 and +17 in 2013.

Employment

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last QuarterExperienced increase 10% 11% 8% 12% 10%No change 79% 79% 81% 75% 80%Experienced decrease 12% 10% 11% 13% 10%*Net Balance -2 +1 -3 -1 0Current QuarterExpect increase 11% 14% 11% 13% 12%No change 83% 78% 83% 80% 79%Expect decrease 6% 7% 5% 6% 7%*Net Balance +5 +7 +6 +7 +5

Size of workforce

What are the barriers to taking on new employees?

Note: Base = those who believe barriers or impediments exist

(52% of all respondents).

All other responses less than 2%.

49%8%

Lack of work/sales

Finding suitable staff

Lack of funds

Cost of employing

Paperwork/administration

Economic climate

Employment conditions

Fluctuating workload

Too many changes/regulations/rules

Lack of cash flow

Cost of wages

Profitability/lack of profits

7%7%

4%4%

3%

2%2%

3%

3%2%

Why SMBs have increased employment - Dec 2015

Note: Base = SMBs that

have increased staff in

the past quarter (11%

of all respondents).

Business is growing

Economic conditions improving

Increasing staff from part time to full time

Replacing staff that left

Planning ahead for economic growth

Easier to find staff in current economic conditions

Other reason

47%17%

6%

12%

2%18%

10%

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

15

20

5

10

0

-5

-10

Experience Expectations

Size of workforce - trends in *net balance

+5

0

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

19

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Wages pressure has eased.

Key findings

Expectations for wages growth among SMBs were down on the prior survey.

Last quarter

Twenty-one percent indicated higher wages against a 15% fall. The net balance of +6 compares with +10 previously and +9 one year earlier.

Wages growth in the last quarter registered a net balance of +19 in Tasmania and between +7 and +12 in NSW, Queensland, the NT and the ACT. This was negative in WA (-7) and below average in Victoria (+4).

Sector-wise, retail recorded the greatest rise in wage costs on +16, followed by finance and insurance (+14). The transport and storage sector was easily lowest on this indicator (-11), with wholesale at +3.

Current quarter

In this quarter, 21% foresee increased wage costs while 10% expect a decrease. The net balance of +11 compares with +19 last quarter and +11 a year ago.

There is a positive net balance in all but two locations for wages expectations ranging from +5 in SA to +33 in Tasmania. The NT (-3) and WA (-1) are negative.

Expected wage growth is highest in wholesale and cultural, recreational and other services (+18 in each) and lowest in communications, property and business services (+2).

Next 12 months

Expectations for wages growth over the next year have slipped slightly relative to the previous survey. Thirty-five percent expect wages growth and just 10% expect a decline.

The net balance of +25 is five points lower than in 2014.

Wages bill

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last Quarter

Experienced increase 23% 25% 15% 25% 21%

No change 59% 56% 67% 57% 61%

Experienced decrease 14% 15% 14% 15% 15%

*Net Balance +9 +10 +1 +10 +6

Current Quarter

Expect increase 22% 24% 20% 26% 21%

No change 66% 67% 71% 65% 67%

Expect decrease 11% 8% 6% 7% 10%

*Net Balance +11 +16 +14 +19 +11

Wages bill

30

0

10

20

-10

-20

Experience Expectations

Wages bill - trends in *net balance

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

+11

+6

Dec 1

5

20

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Steady pricing behaviour with expectations still trending down.

Key findings

Overall prices have lifted quite consistently over the year while expectations have tempered.

Last quarter

There was no shift in the net balance of +9. Price increases were noted by 15% with 6% cutting prices.

Net price changes last quarter were in the range of 0 (SA) to +22 (Tasmania).

By sector we saw a well above average situation in wholesale (+26) followed by retail (+15), which was clearly higher than finance and insurance (+1), manufacturing (+3), health and community services (+3).

Current quarter

Expectations for price rises this quarter were two points lower, establishing a net balance of +14.

These expectations ranged from +6 in SA and WA to +17 in Victoria and +19 in Tasmania.

Expectations for increased pricing were strongest in manufacturing (+25), wholesale and retail (both +21). Lowest on this measure were SMBs in the finance and insurance sector (+3).

Next 12 months

At a net balance of +32, expectations for price rises in the year ahead were higher than one year earlier when it registered +28.

Over the year 36% expect a rise in the prices they charge with 4% predicting a fall.

Prices

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last Quarter

Experienced increase 17% 21% 16% 18% 15%

No change 70% 67% 73% 70% 76%

Experienced decrease 10% 10% 8% 9% 6%

*Net Balance +7 +11 +8 +9 +9

Current Quarter

Expect increase 17% 26% 20% 21% 17%

No change 77% 68% 75% 72% 78%

Expect decrease 5% 5% 2% 5% 3%

*Net Balance +12 +21 +18 +16 +14

Prices charged

30

40

0

10

20

-10

Experience Expectations

Prices charged - trends in *net balance

+14

+9

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

21

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Negative results expected to continue next year.

Key findings

More SMBs reported decreased capital expenditure over the last year than an increase. This also applies to expectations for next year.

Last 12 months

In the last year, 30% increased capital expenditure, whilst 34% reduced it. The net balance of -4 cannot be compared with another ‘last 12 months measure’ as this is a new question. However, in the December quarter of 2014 we did ask about capital expenditure for the last 3 months and that revealed a net balance of -9 suggesting there has been little improvement on this indicator for some time.

Only in NSW (+3) and the NT (+10) was there a positive net balance in this area. In other locations it ranged from 0 (Tasmania) to -12 (SA).

Capital expenditure last year also varied substantially across sectors, ranging from +15 in health and community services to -20 in transport and storage.

Next 12 months

There was a drop from net +9 to -6 in SMBs expecting to increase capital expenditure in the coming year.

Capital expenditure expectations in the next 12 months were highest in the ACT (+5) and Tasmania (+2) and negative elsewhere, especially in SA (-17). By sector, health and community services recorded a net balance of +3, while in finance and insurance it was +1. The scores were negative for the remaining sectors, with transport and storage again standing out on -21.

Capital expenditure

Dec 14

Dec 15

Over last 12 months spent

More than in previous 12 months NA 30%

Same as in previous 12 months NA 33%

Less than in previous 12 months NA 34%

*Net Balance NA -4

Over next 12 months expect to spend

More than this year 29% 28%

Same as this year 49% 35%

Less than this year 20% 34%

*Net Balance +9 -6

Capital expenditure - trends

NOTE: This question is only asked in the December quarter survey about the last 12 months and next 12 months. Capital expenditure refers to funds used by a company to acquire or upgrade physical assets such as property, industrial buildings or equipment. It is often used to undertake new projects or investments by the firm.

22

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Obtaining finance is still challenging for SMBs.

Key findings

SMBs’ ability to access finance is critical for capital expenditure and growth. Overall they are still not finding it easy to access finance.

Last quarter

Accessing finance continues to just hover in positive territory. The net score of +3 compares with +1 and +4 in the last two surveys and +2 one year ago.

SMBs in SA (-4) and WA (-5) battled to access finance most of all, while those in NSW were the most positive on this dimension (+5).

By sector, transport and storage (+17) stood out at the top end in contrast to manufacturing (-5), cultural, recreational and other personal services (-7).

Medium size firms (+16) found it easier than small firms (+2) to access finance. The gap last time was +27 in favour of medium businesses.

Sixteen percent of SMBs indicated an attempt to access finance, compared to 17% last quarter. However, of those, 73% had success in both surveys.

The highest incidence of seeking finance was in Tasmania (28%) followed by WA (22%). The lowest was in NSW (11%). SMBs in the transport and storage sector (30%) were the most likely to have sought finance.

Access to finance

84+16+y

73+24+3+y

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last QuarterRelatively easy 25% 24% 19% 23% 24%Average 52% 58% 66% 55% 56%Relatively hard 23% 18% 15% 22% 21%*Net Balance +2 +6 +4 +1 +3

Access to finance

Access to finance - trends in *net balance

Success in accessing finance

Have you tried to access finance for your business in the past quarter?

Were you successful?

Ease of accessing finance - by business size (Dec 2015)

Easy Difficult *Net Balance

Total 24% 21% +3

1-2 Employees 21% 21% 0

3-4 Employees 23% 23% 0

5-9 Employees 26% 18% +8

10-19 Employees 28% 21% +7

Total Small Business 23% 21% +2

20-99 Employees 31% 14% +17

100-199 Employees 25% 17% +8

Total Medium Business 30% 14% +16

No

Pending

Yes

No

Yes

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

Base: Those who had tried to access finance.

16

3

7324

+3

+21

+24

84

0

10

20

30

40

50

-30

-20

-10

-40

-50

Relatively easy Relatively hard *Net balance

Dec 1

3

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

23

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Profitability

Consistently negative profitability experiences are tempering expectations.

Key findings

Despite SMBs reporting negative profitability for some time, their expectations have been upbeat. However, expectations have fallen nine points this quarter.

Last quarter

Twenty-three percent reported a profit rise against a 28% fall. The net balance result of -5 compares with -7 last survey.

The last net positive profitability result recorded was in February 2008.

Profitability was negative everywhere but Tasmania (+17) and Victoria (+1). It was very weak in WA (-21) and the NT (-17).

Only in communications, property and business services (+10) was profitability positive. Retail (-23) and transport and storage (-14) ranked lowest on this measure.

Current quarter

Profitability expectations are the lowest they have been this year, now sitting on +10.

The expectations are well above average in Tasmania (+38) and the ACT (+33). The opposite is true for WA (-3) and the NT (-14). Other locations are positive overall ranging from +5 (SA) to +16 (Victoria).

The retail (+27) and cultural, recreational and personal services sectors (+25) are the most positive, with the weakest being hospitality (-9) and finance and insurance (-6).

Next 12 months

Expectations for the year ahead have decreased again. Forty-four percent expect increased profitability and 16% anticipate a decrease. The net balance of +28 compares with +34 in 2014 and +52 in 2013.

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

Last Quarter

Experienced increase 26% 24% 21% 24% 23%

No change 37% 40% 53% 43% 47%

Experienced decrease 34% 34% 24% 31% 28%

*Net Balance -8 -10 -3 -7 -5

Current Quarter

Expect increase 33% 44% 29% 35% 29%

No change 44% 41% 55% 47% 50%

Expect decrease 22% 13% 14% 16% 19%

*Net Balance +11 +31 +15 +19 +10

Profitability

50

0

10

20

30

40

-20

-10

-40

-30

Experience Expectations

Profitability - trends in *net balance

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

+10

-5

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

24

1 3 42 5

Sensis Business Index | Small and medium business outlook – national summary

Exports

Exports have not grown in three years.

Key findings

There has been no growth in the proportion of SMBs exporting over the last three years.

Last 12 months

Eleven percent of SMBs exported goods or services in the last year (12% in 2014 and 13% in 2013). SMBs in the ACT (17%) were most likely to export followed by NSW (14%), while those in the NT were the least likely (5%).

Metropolitan SMBs were more likely to export than their regional counterparts (14% compared to 6%). Manufacturers (29%) and wholesalers (26%) were again the most export-oriented. Least likely was the hospitality sector (1%).

New exporters

Only 1% of the SMBs not exporting in the last year expect to do so in the next 12 months. This intention ranges from 0% in WA to 3% in NSW and the ACT. By industry, wholesale stands out at 9% with the rest ranging from 0% to 3% on this measure.

Exporting and business growth

Elsewhere in this survey we discovered 43% of SMBs seeking growth for their business and 6% of those expect their growth will mainly come from exports. This represents under 3% of the total base.

Proportion of SMBs exporting in the last year

* Net balance is defined as the difference between the percentage with a positive outlook and the

percentage with a negative outlook.

National

New South Wales

Victoria

Queensland

South Australia

Western Australia

Tasmania

Northern Territory

Australian Capital Territory

11%14%

10%

10%

7%7%

5%17%

11%

25

21 543

Government policies ..............................................................................................................................................................................26

Assessment of Federal Government policies ................................................................................................................................... 27

Assessment of state and territory government policies ...............................................................................................................28

Government Policies

25

21 543

Sensis Business Index | Government policies

26

21 543

Sensis Business Index | Government policies

21 543

Government policies

The maps below show the net balance of attitudes to Federal, state and territory government policies. This is calculated from the proportion believing the government is supportive less the proportion believing it to be working against small business interests. Also displayed is the change in net balance compared with the previous quarter.

Attitudes to Federal Government policies

Attitudes to state and territory government policies

Western Australia

Northern Territory

South Australia New South

Wales

Victoria

Queensland

National

ACT

Tasmania

No change

14

30

2

7

1

1

1

6

18

5

14

15

-10

-4

+18

-32+11

+4

-17

+7

-15

+3

+12

+18

+12

1-5

5+14

7+13

6+3

Western Australia

Northern Territory

South Australia New South

Wales

Victoria

Queensland

ACT

Tasmania

27

21 543

Sensis Business Index | Government policies

SMBs view the Federal Government more favourably than last survey and this time one year ago.

Key findings

SMBs see the Federal Government in a more positive light than last survey and in the corresponding 2014 survey.

Last quarter

Twenty-seven percent now assess Federal Government policies as supportive of SMBs with 20% disagreeing. The net balance of +7 compares with the prior result of +1, which had fallen significantly from +18 in the June quarter following the Federal Budget. Year on year the net balances recorded have been +9 in the first post-election survey of December 2013, -4 last December quarter and +7 now.

The top three reasons for a favourable assessment of the Government are tax cuts (15%), tax incentives (11%) and other incentives, subsidies or grants (11%). However, 8% also spontaneously mentioned “a new Prime Minister”.

SMBs not keen about the Federal Government’s policies mostly cite excessive bureaucracy or red tape (26%) followed by a lack of incentives, support or financial assistance for small business (15%), high taxes (13%) and a focus on big business (13%).

Businesses in the NT (+14), Tasmania (+18) and SA (+18) are the most impressed with Federal Government support for small business. Only in WA (-5) are opinions unfavourable overall.

Conversely, the wholesale (-12), cultural, recreational and other personal services sectors (-8) are the only negative sectors on this measure. The building and construction (+14) and communications, property and business services sectors (+19) are the most positive about Federal Government support.

Assessment of Federal Government policies

Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

Supportive 22% 16% 30% 25% 27%

Work against 26% 24% 12% 24% 20%

No impact 52% 60% 58% 51% 53%

*Net Balance -4 -8 +18 +1 +7

Location Dec 14 Mar 15 Jun 15 Sep 15 Dec 15

National average -4 -8 +18 +1 +7

New South Wales +3 -7 +25 +6 +13

Victoria -6 -3 +13 +3 +4

Queensland -2 -8 +22 -3 +3

South Australia -22 -17 +25 -12 +18

Western Australia -19 -5 +10 -6 -5

Tasmania 17 -12 +8 +23 +18

Northern Territory -8 -1 +42 +9 +14

Australian Capital Territory -38 -33 +9 -15 +3

Attitudes to Federal Government policies - trends

Attitudes to Federal Government policies - by location

Thinking about the current Federal Government, do you believe that their policies are supportive of small business, work against small business or have no real impact either way?

Supportive Work against

Attitudes to Federal Government policies - long term trends

30%

40%

60%

50%

70%

20%

10%

0%

27%

20%

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

Dec 1

3

Dec 0

8

Dec 0

9

Dec 1

0

Dec 1

1

Dec 1

2

Dec 1

4

Dec 1

5

28

21 543

Sensis Business Index | Government policies

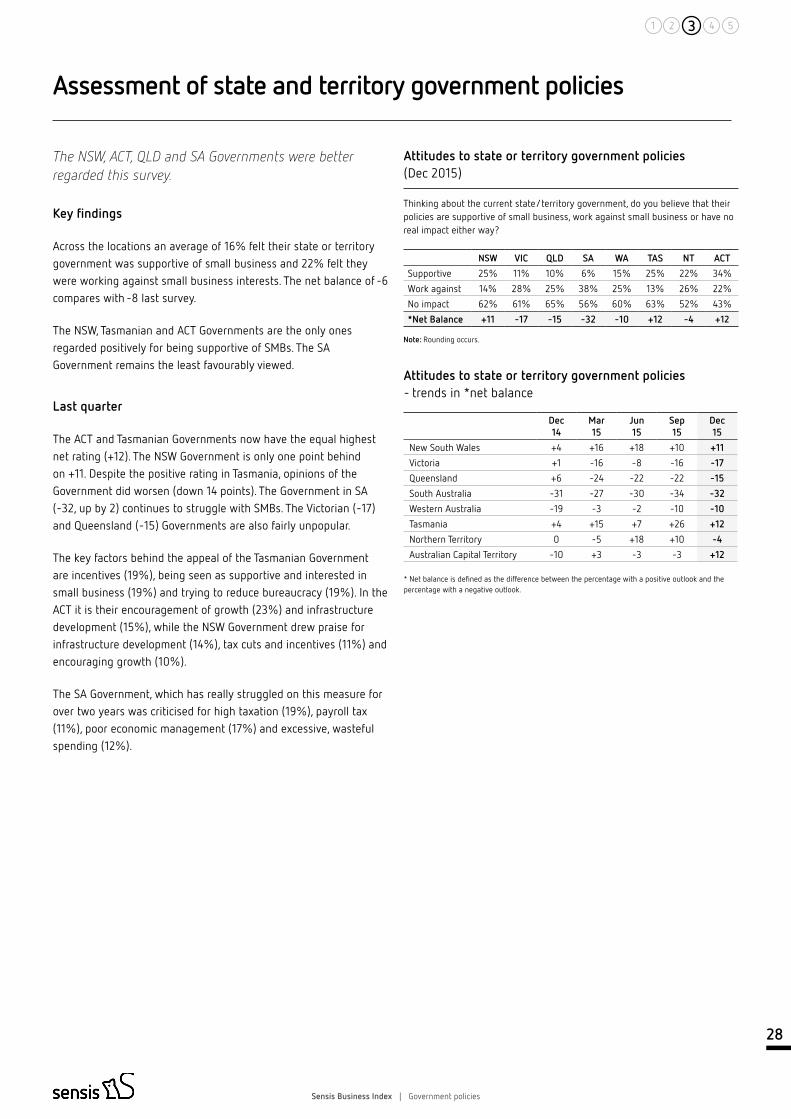

The NSW, ACT, QLD and SA Governments were better regarded this survey.

Key findings

Across the locations an average of 16% felt their state or territory government was supportive of small business and 22% felt they were working against small business interests. The net balance of -6 compares with -8 last survey.

The NSW, Tasmanian and ACT Governments are the only ones regarded positively for being supportive of SMBs. The SA Government remains the least favourably viewed.

Last quarter

The ACT and Tasmanian Governments now have the equal highest net rating (+12). The NSW Government is only one point behind on +11. Despite the positive rating in Tasmania, opinions of the Government did worsen (down 14 points). The Government in SA (-32, up by 2) continues to struggle with SMBs. The Victorian (-17) and Queensland (-15) Governments are also fairly unpopular.

The key factors behind the appeal of the Tasmanian Government are incentives (19%), being seen as supportive and interested in small business (19%) and trying to reduce bureaucracy (19%). In the ACT it is their encouragement of growth (23%) and infrastructure development (15%), while the NSW Government drew praise for infrastructure development (14%), tax cuts and incentives (11%) and encouraging growth (10%).

The SA Government, which has really struggled on this measure for over two years was criticised for high taxation (19%), payroll tax (11%), poor economic management (17%) and excessive, wasteful spending (12%).

Assessment of state and territory government policies

Attitudes to state or territory government policies (Dec 2015)

Dec 14

Mar 15

Jun 15

Sep 15

Dec 15

New South Wales +4 +16 +18 +10 +11

Victoria +1 -16 -8 -16 -17

Queensland +6 -24 -22 -22 -15

South Australia -31 -27 -30 -34 -32

Western Australia -19 -3 -2 -10 -10

Tasmania +4 +15 +7 +26 +12

Northern Territory 0 -5 +18 +10 -4

Australian Capital Territory -10 +3 -3 -3 +12

Attitudes to state or territory government policies - trends in *net balance

* Net balance is defined as the difference between the percentage with a positive outlook and the percentage with a negative outlook.

NSW VIC QLD SA WA TAS NT ACT

Supportive 25% 11% 10% 6% 15% 25% 22% 34%

Work against 14% 28% 25% 38% 25% 13% 26% 22%

No impact 62% 61% 65% 56% 60% 63% 52% 43%

*Net Balance +11 -17 -15 -32 -10 +12 -4 +12

Thinking about the current state/territory government, do you believe that their policies are supportive of small business, work against small business or have no real impact either way?

Note: Rounding occurs.

29

21 53 4

29

21 53 4

Sensis Business Index | Small and medium business outlook

National ....................................................................................................................................................................................................30

New South Wales ....................................................................................................................................................................................31

Victoria ......................................................................................................................................................................................................32

Queensland ..............................................................................................................................................................................................33

South Australia .......................................................................................................................................................................................34

Western Australia ...................................................................................................................................................................................35

Tasmania ..................................................................................................................................................................................................36

Northern Territory ................................................................................................................................................................................... 37

Australian Capital Territory ...................................................................................................................................................................38

Small and Medium Business Outlook

30

21 53 4

Sensis Business Index | Small and medium business outlook

Confidence jumps with SMBs also believing the economy will improve in 2016.

• Confidence was up 12 points this quarter (+39), generating the highest level observed since March 2011.

• Views of the current state of the economy were two points higher but still clearly negative overall (-17). However, expectations for the economy in a year’s time were 11 points higher, moving from -4 to +7 net balance.

• Sales and profitability results are again uninspiring with no employment growth indicated in the latest quarter. Some wages and price pressure was apparent.