business management plan for kempsey shire … by sgl consulting group australia pty ltd appendix a...

TRANSCRIPT

Prepared by SGL Consulting Group Australia Pty Ltd

www.sglgroup.net

Business Management Plan for Kempsey Shire Caravan Parks 2016 to 2021 Draft Report December 2015

APPENDIX A Page 1BMP - KSC CP

15DEC2015

SGL Consulting Group Australia Pty Ltd Adelaide 2a Mellor St West Beach SA 5024 Phone: +61 (08) 8235 0925 Fax: +61 (08) 8353 1067 Email: [email protected] Brisbane PO Box 713 Mount Gravatt Queensland 4122 Mobile: +61 (0) 416 235 235 Email: [email protected] Melbourne Level 6, 60 Albert Road South Melbourne VIC 3205 Phone: +61 (03) 9698 7300 Fax: +61 (03) 9698 7301 Email: [email protected] Perth 19 Clayton Street East Fremantle WA 6158 Phone: +61 (0) 8 9319-8991 Mobile: +61 (0) 407 901 636 Email: [email protected] Sydney 1/273 Alfred St Nth North Sydney NSW 2060 Mobile: +61 (04) 17 536 198 Email: [email protected]

SGL also has offices in: • Auckland • Christchurch • Wellington

APPENDIX A Page 2BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table of Contents

1 Background ......................................................................................................... 1 1.1 Project Overview ..................................................................................................... 1 1.2 Project Aims and Objectives .................................................................................. 1 1.3 Project Methodology ............................................................................................... 2 1.4 Kempsey Shire Area Overview ............................................................................... 3 1.5 Macleay Valley Coast Overview .............................................................................. 4 1.6 Tourism Profile ........................................................................................................ 4

1.6.1 Overview of Macleay Valley Coast Assets and Products ..................................... 5 1.6.2 Visitor Expenditure Trends ................................................................................... 6 1.6.3 MVC Visitation Trends ......................................................................................... 6 1.6.4 MVC Visitor Profiles ............................................................................................. 7

2 Review of Councils Caravan Parks ................................................................... 9 2.1 Introduction ............................................................................................................. 9 2.2 Historical Review of Council Caravan Parks ......................................................... 9

2.2.1 1988 Kempsey Shire Caravan Park Management Plan ....................................... 9 2.2.2 2005 Kempsey Shire Caravan Park Management Plans ................................... 10 2.2.3 Caravan Park Operational Changes and Improvements from 2005 ................... 11

2.3 Review of Kempsey Shire Holiday Parks ............................................................. 11 2.3.1 Crescent Head Holiday Park .............................................................................. 12 2.3.1.1 CH Holiday Park Cabin and Site Capacities .................................................... 13 2.3.1.2 CH Holiday Park Cabin Occupancy 2013/14 ................................................... 13 2.3.1.3 CH Holiday Park Tourist Site Occupancy 2013/14 .......................................... 13 2.3.1.4 CH Holiday Park Financial Trends 2011 to 2014 ............................................. 14 2.3.2 Hat Head Holiday Park ...................................................................................... 14 2.3.2.1 HH Holiday Park Cabin and Site Capacities .................................................... 14 2.3.2.2 HH Holiday Park Cabin Occupancy 2013/14 ................................................... 15 2.3.2.3 HH Holiday Park Tourist Site Occupancy 2013/14 .......................................... 16 2.3.2.4 HH Holiday Park Financial Trends 2011 to 2014 ............................................. 16 2.3.3 Horseshoe Bay Holiday Park ............................................................................. 16 2.3.3.1 HB Holiday Park Cabin and Site Capacities .................................................... 17 2.3.3.2 HB Holiday Park Cabin Occupancy 2013/14 ................................................... 17 2.3.3.3 HB Holiday Park Tourist Site Occupancy 2013/14 .......................................... 18 2.3.3.4 HB Holiday Park Financial Trends 2011 to 2014 ............................................. 18 2.3.4 Stuarts Point Holiday Park ................................................................................. 19 2.3.4.1 SP Holiday Park Cabin and Site Capacities .................................................... 19 2.3.4.2 SP Holiday Park Cabin Occupancy 2013/14 ................................................... 20 2.3.4.3 SP Holiday Park Tourist Site Occupancy 2013/14 .......................................... 20 2.3.4.4 SP Holiday Park Financial Trends 2011 to 2014 ............................................. 20 2.3.5 Grassy Head Holiday Park ................................................................................. 21 2.3.5.1 GH Holiday Park Cabin and Site Capacities ................................................... 21 2.3.5.2 GH Holiday Park Cabin Occupancy 2013/14 .................................................. 22 2.3.5.3 GH Holiday Park Tourist Site Occupancy 2013/14 .......................................... 22 2.3.5.4 GH Holiday Park Financial Trends 2011 to 2014 ............................................ 23

2.4 Combined MVC Holiday Parks Review ................................................................ 23 2.4.1.1 MVC Combined Holidays Park Cabin and Site Capacities .............................. 23 2.4.1.2 MVC Combined Holiday Parks Cabin Occupancy 2013/14 ............................. 24 2.4.1.3 MVC Combined Holiday Parks Tourist Site Occupancy 2013/14 .................... 25 2.4.1.4 MVC Combined Holiday Parks Financial Trends 2011 to 2014 ....................... 26 2.4.1.5 MVC Combined Holiday Parks Income Trends 2013/2014 ............................. 26 2.4.1.6 MVC Combined Holiday Parks Capital Improvements 2011 to 2014 ............... 27

APPENDIX A Page 3BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.5 MVC Holiday Parks Management Contract Review ............................................. 28

3 Caravan Park Research and Trends Review .................................................. 30 3.1 Introduction ........................................................................................................... 30 3.2 Review of Local Relevant Documents ................................................................. 30

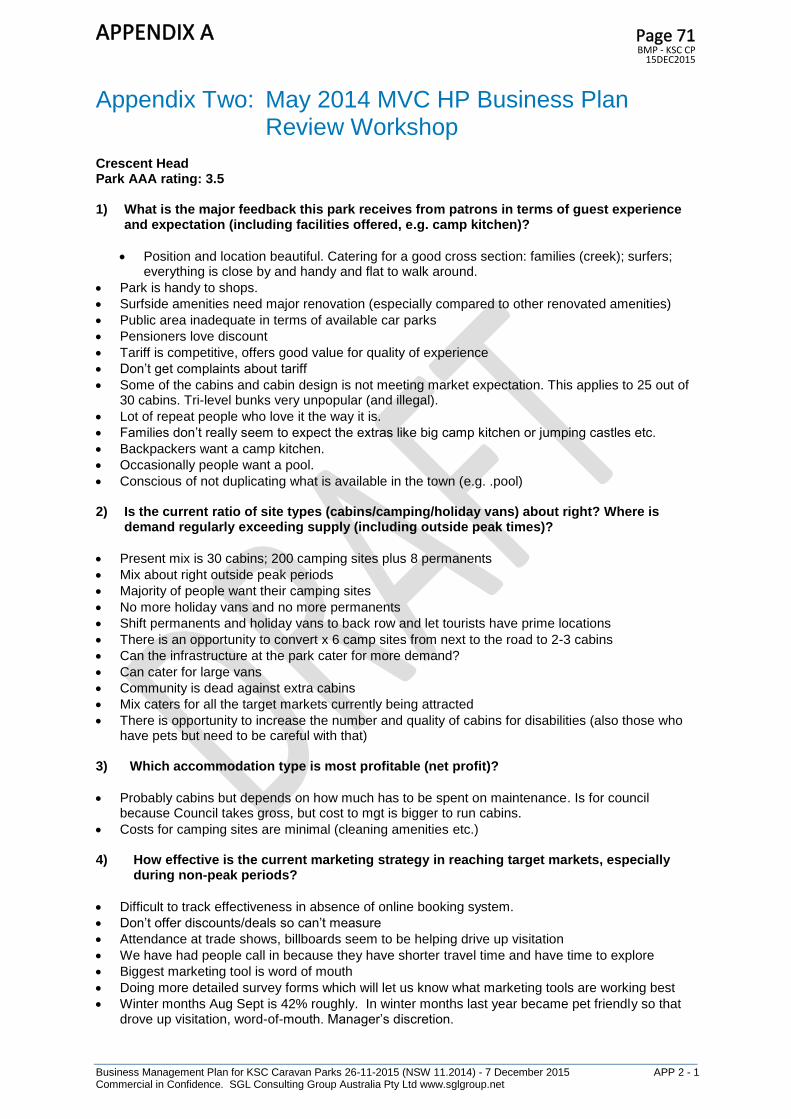

3.2.1 Holiday Park Cabins Structural Report 2014 ...................................................... 30 3.2.2 Macleay Valley Coastal Holiday Parks Marketing Plan ...................................... 31 3.2.3 MVC Holiday Parks Business Planning Workshop May 2014 ............................ 32

3.3 Caravan Parks Research and Industry Trends .................................................... 33 3.4 Local Area Caravan Park and Accommodation Review ..................................... 35

4 Future KSC Holiday Park Business Improvements ....................................... 36 4.1 Introduction ........................................................................................................... 36 4.2 MVC Holiday Park Review Key Findings ............................................................. 36

4.2.1 Historical Trends See Major Returns on Holiday Park Investment ..................... 36 4.2.2 Holiday Parks are a Major Outlet for Local Tourism Economic Growth .............. 37 4.2.3 Major Local Business that has Capacity for Increased Growth .......................... 37 4.2.4 Future MVC Holiday Park Business Impacts ...................................................... 38

4.3 Future HP Business Strategy 2016 to 2021 ......................................................... 38 4.3.1 New Holiday Park Market and Development Categories .................................... 38 4.3.2 Reducting Holiday Park Sites ............................................................................ 39 4.3.3 Continue to Improve High Yield Accommodation Opportunities ......................... 40 4.3.4 New/Redeveloped Facilities/Services To Increase Occupancy/Income ............. 40

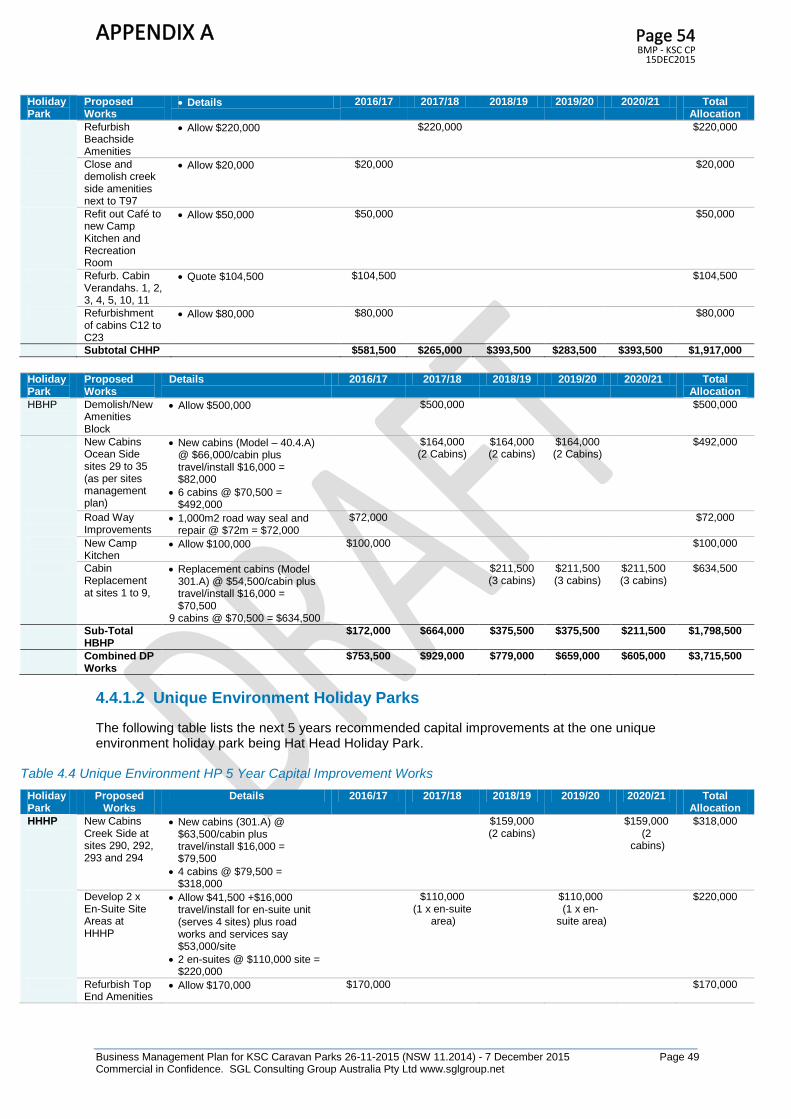

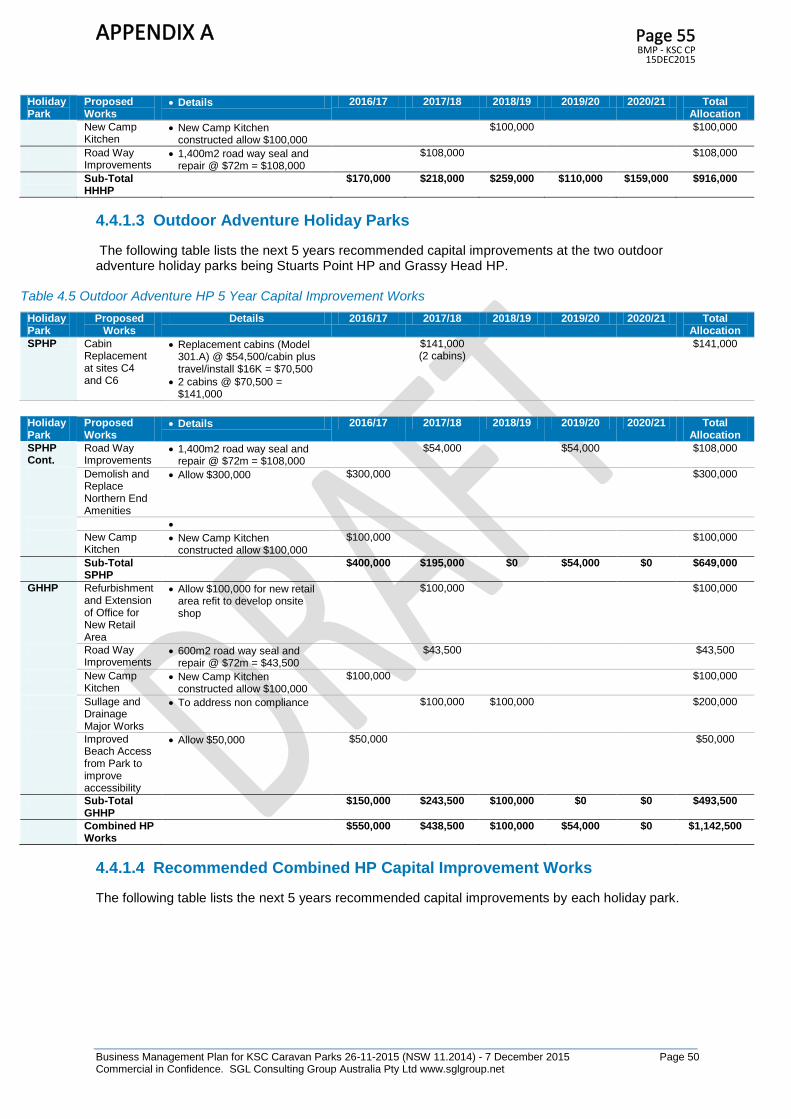

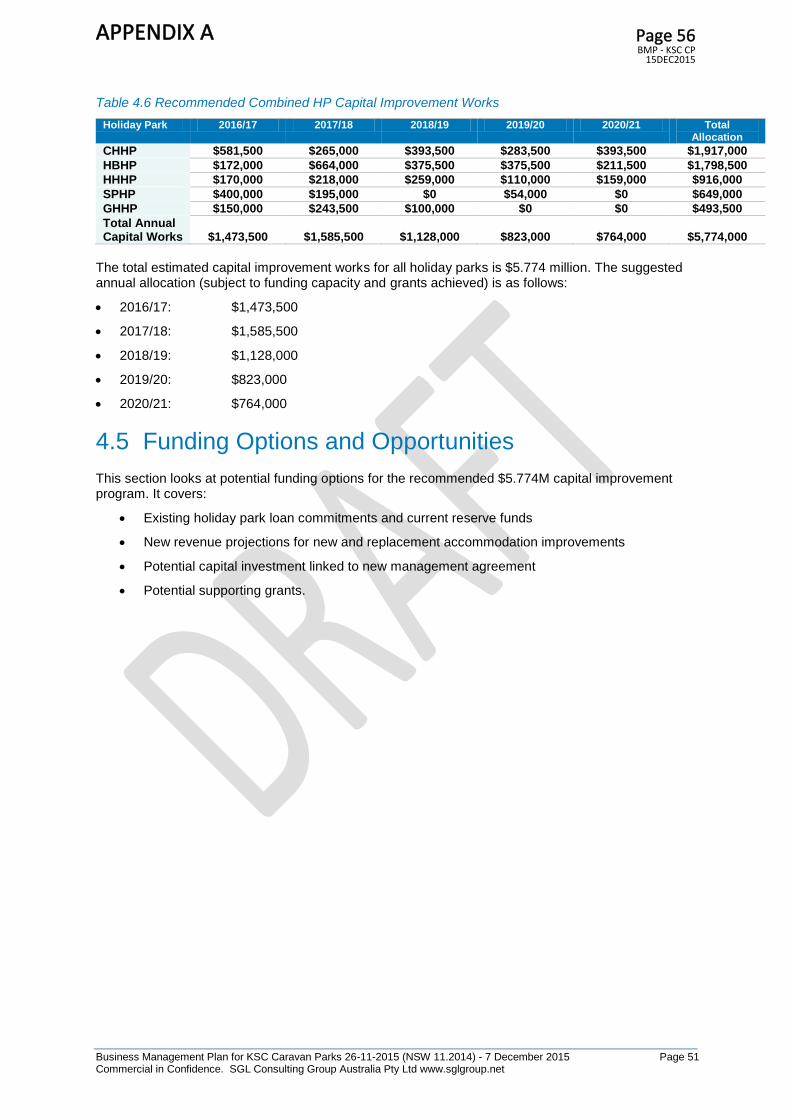

4.4 2016 to 2021 Capital Improvement Program ........................................................ 41 4.4.1 Future Park Improvements and Costs 5 Year Program ...................................... 48 4.4.1.1 Destination Holiday Parks ............................................................................... 48 4.4.1.2 Unique Environment Holiday Parks ................................................................. 49 4.4.1.3 Outdoor Adventure Holiday Parks ................................................................... 50 4.4.1.4 Recommended Combined HP Capital Improvement Works ............................ 50

4.5 Funding Options and Opportunities .................................................................... 51 4.5.1.1 Existing Holiday Park Loan Commitments ...................................................... 52 4.5.2 Current Reserve Funds ..................................................................................... 53 4.5.3 Revenue Projections from New Accommodation Investments ........................... 53 4.5.4 Revenue Projections for Site En-Suite Improvements ........................................ 55 4.5.5 Funding Opportunities and Options ................................................................... 55

4.6 Future Management Options and Opportunities ................................................. 56 4.6.1 Current Management Contract Financial Performance ...................................... 57 4.6.2 Current Management Contract Issues ............................................................... 57 4.6.3 Future Management Contract Opportunities ...................................................... 58 4.6.4 Future Business Direction Needs to Guide Future Management Model ............. 59 4.6.5 Recommended Future Management Model ....................................................... 59 4.6.6 Procuring New Management Deal ..................................................................... 60 4.6.7 What level of Business Improvement Does Council Want to Achieve? .............. 60

4.7 Project Recommendations ................................................................................... 61

Directory of Tables TABLE 1.1 PROJECT METHODOLOGY AND ASSOCIATED PHASES ............................................... 2 TABLE 1.2 KSC HOLIDAY PARK BEDS 2013 ....................................................................................... 5 TABLE 1.3 MVC VISITATION TRENDS BY VISITOR TYPE ................................................................. 6 TABLE 1.4 MVC KEY VISITOR CATEGORIES SUMMARY .................................................................. 7 TABLE 2.1 CRESCENT HEAD HOLIDAY PARK CABIN AND SITE CAPACITIES 2015 .................... 13 TABLE 2.2 CRESCENT HEAD HOLIDAY PARK CABIN OCCUPANCY 2013/14 ............................... 13 TABLE 2.3 CRESCENT HEAD HOLIDAY PARK TOURIST SITE OCCUPANCY 2013/14 ................. 13

APPENDIX A Page 4BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

TABLE 2.4 CRESCENT HEAD HOLIDAY PARK FINANCIAL TRENDS 2011 TO 2014 ..................... 14 TABLE 2.5 HAT HEAD HOLIDAY PARK CABIN AND SITE CAPACITIES 2015 ................................ 14 TABLE 2.6 HAT HEAD HOLIDAY PARK CABIN OCCUPANCY 2013/14 ........................................... 15 TABLE 2.7 HAT HEAD HOLIDAY PARK TOURIST SITE OCCUPANCY 2013/14.............................. 16 TABLE 2.8 HAT HEAD HOLIDAY PARK FINANCIAL TRENDS 2011 TO 2014 .................................. 16 TABLE 2.9 HORSESHOE BAY HOLIDAY PARK CABIN AND SITE CAPACITIES 2015 ................... 17 TABLE 2.10 HORSESHOE BAY HOLIDAY PARK CABIN OCCUPANCY 2013/14 ............................ 18 TABLE 2.11 HORSESHOE BAY HOLIDAY PARK TOURIST SITE OCCUPANCY 2013/14 .............. 18 TABLE 2.12 HORSESHOE BAY HOLIDAY PARK FINANCIAL TRENDS 2011 TO 2014 ................... 18 TABLE 2.13 STUARTS POINT HOLIDAY PARK CABIN AND SITE CAPACITIES 2015 .................... 19 TABLE 2.14 STUARTS POINT HOLIDAY PARK CABIN OCCUPANCY 2013/14 ............................... 20 TABLE 2.15 STUARTS POINT HOLIDAY PARK TOURIST SITE OCCUPANCY 2013/14 ................. 20 TABLE 2.16 STUARTS POINT HOLIDAY PARK FINANCIAL TRENDS 2011 TO 2014 ..................... 21 TABLE 2.17 GRASSY HEAD HOLIDAY PARK CABIN AND SITE CAPACITIES 2015....................... 21 TABLE 2.18 GRASSY HEAD HOLIDAY PARK CABIN OCCUPANCY 2013/14 .................................. 22 TABLE 2.19 GRASSY HEAD HOLIDAY PARK TOURIST SITE OCCUPANCY 2013/14 .................... 23 TABLE 2.20 GRASSY HEAD HOLIDAY PARK FINANCIAL TRENDS 2011 TO 2014 ........................ 23 TABLE 2.21 MVC COMBINED HOLIDAY PARK CABIN AND SITE CAPACITIES 2015 .................... 24 TABLE 2.22 MVC COMBINED HP CABIN/SITE CAPACITIES 1996/97 AND 2014/15 ....................... 24 TABLE 2.23 MVC COMBINED HOLIDAY PARKS CABIN OCCUPANCY 2013/14 ............................. 25 TABLE 2.24 MVC COMBINED HOLIDAY PARKS TOURIST SITE OCCUPANCY 2013/14 ............... 25 TABLE 2.25 MVC COMBINED HOLIDAY PARKS FINANCIAL TRENDS 2011 TO 2014 ................... 26 TABLE 2.26 MVC COMBINED HOLIDAY PARKS FINANCIAL TRENDS 2011 TO 2014 ................... 27 TABLE 2.27 MVC COMBINED HOLIDAY PARKS CAPITAL IMPROVEMENTS 2011 TO 2014 ........ 27 TABLE 2.28 MVC COMBINED HOLIDAY PARKS CAPITAL IMPROVEMENTS 2014/15 .................. 28 TABLE 4.1 MVC HOLIDAY PARKS CUSTOMER SELECTION CRITERIA REVIEW ......................... 41 TABLE 4.2 REVIEW OF MANUFACTURED CABINS SUITABLE FOR MVC HOLIDAY PARKS ....... 47 TABLE 4.3 DESTINATION HOLIDAY PARKS 5 YEAR CAPITAL IMPROVEMENT WORKS ............. 48 TABLE 4.4 UNIQUE ENVIRONMENT HP 5 YEAR CAPITAL IMPROVEMENT WORKS ................... 49 TABLE 4.5 OUTDOOR ADVENTURE HP 5 YEAR CAPITAL IMPROVEMENT WORKS ................... 50 TABLE 4.6 RECOMMENDED COMBINED HP CAPITAL IMPROVEMENT WORKS ......................... 51 TABLE 4.7 EXISTING HOLIDAY PARK LOAN COMMITMENTS ........................................................ 52 TABLE 4.8 NEW CABIN PROJECTED YEAR ONE REVENUE .......................................................... 53 TABLE 4.9 NEW CABIN PROJECTED YEAR ONE EXPENDITURE .................................................. 54 TABLE 4.10 NEW CABIN PROJECTED YEAR ONE REDUCED SITE INCOME REDUCTION ......... 54 TABLE 4.11 NEW CABIN ESTIMATED NEW OPERATING SURPLUS .............................................. 54 TABLE 4.12 NEW EN-SUITE PROJECTED YEAR ONE REVENUE .................................................. 55 TABLE 4.13 MVC HOLIDAY PARKS MANAGEMENT CONTRACT PAYMENTS 2011 TO 2014 ...... 57

Appendices APPENDIX ONE: 2005 Holiday Parks Management Plan Capital Improvement

Recommendations APPENDIX TWO: May 2013 MVC Holiday Parks Business Planning Forum APPENDIX THREE: Cabin Options Used for Capital Investment Modeling

APPENDIX A Page 5BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 1 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

1.1 Project Overview

Kempsey Shire Council is Reserve Trust Manager for five holiday parks located at popular holiday destinations on the Mid North Coast of NSW approximately mid-way between Brisbane and Sydney. Locations include Crescent Head, Hat Head, Horseshoe Bay, Grassy Head and Stuarts Point. The parks are operated by a private contractor and currently trade as Macleay Valley Coastal Holiday Parks. The project brief indicates the Macleay Valley Coast is popular holiday destination that has experienced strong growth of almost 10 per cent in its visitor economy over the past two years, rising $173M to $189M. This growth has seen the number of visitors to the Macleay rise from 489,000 to 554,000. While the biggest growth has been in the number of day visitors (now contributing $31M to the local economy), significant growth has also been experienced in the overnight visitor market, rising from 247,000 in 2011 to 269,000 for the year ended September 2013. Macleay Valley Coastal Holiday Parks are the single largest provider of accommodation beds in the Kempsey local government area, contributing approximately one-third (3571 of a total 10,764) of the Shire’s beds through a combination of cabins and campsites. All five parks are located in prime coastal locations, featuring pristine environmental surrounds, long stretches of sandy beaches, a sub-tropical climate and ideal conditions for surfing, fishing and other water-based recreational activities. The parks’ unique natural environs cannot, however, continue to be relied upon to attract new and returning visitors, particularly in what is becoming an increasingly sophisticated holiday park market. Recent visitor feedback suggests visitor expectations in relation to accommodation quality, public amenities, grounds, facilities and services are no longer being met. Council through this study is seeking to develop a comprehensive Plan of Management for the five holiday parks.

1.2 Project Aims and Objectives

The Plan of Management will provide Council with market analysis, a business plan (including cost-benefit analysis and fee modelling) and a budgeted capital works program that will be aimed at securing the parks’ long-term competitive advantage and commercial viability. This has involved:

Completing market analysis and a business plan to improve the parks’ long-term commercial viability, including identifying each park’s niche market strengths and opportunities.

Completing a full cost-benefit analysis for a range of capital upgrade options, including the type and style of accommodation offered, amenities, grounds, facilities and other value-add services aimed at enhancing the visitor experience.

1 Background

APPENDIX A Page 6BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 2 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Reviewing and recommending the most effective and efficient management model, including operational and reporting processes for day-to-day management.

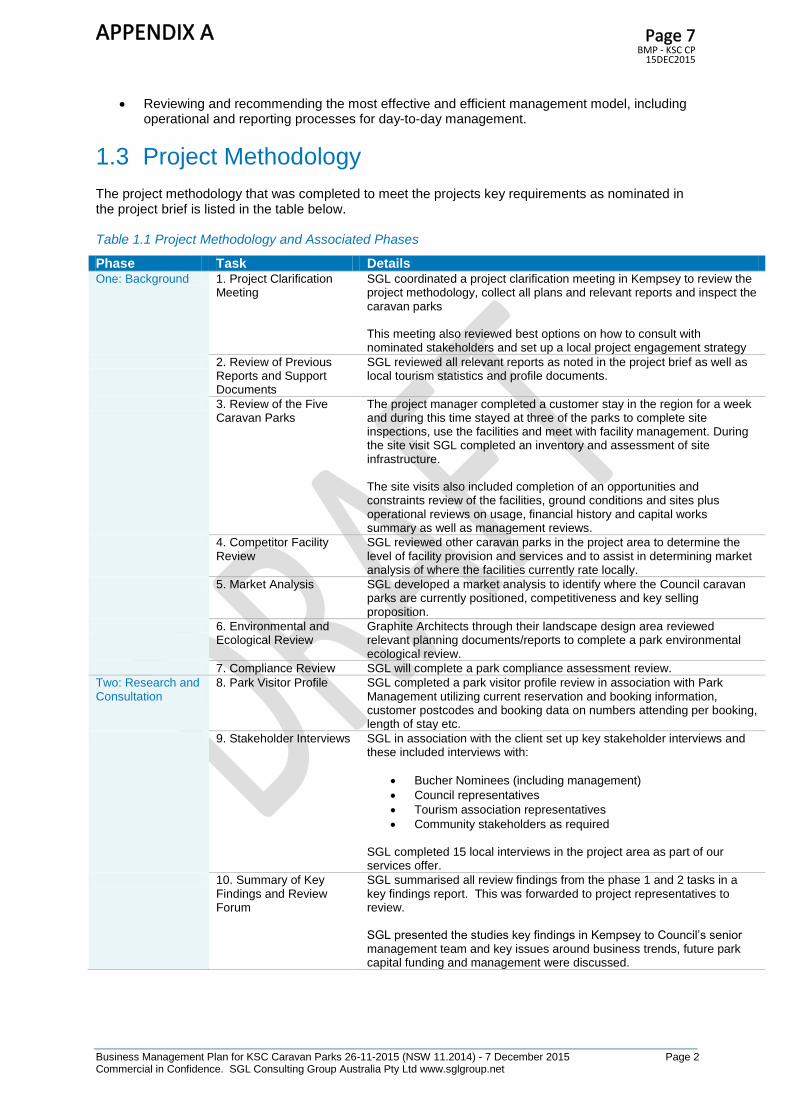

1.3 Project Methodology

The project methodology that was completed to meet the projects key requirements as nominated in the project brief is listed in the table below. Table 1.1 Project Methodology and Associated Phases

Phase Task Details One: Background 1. Project Clarification

Meeting SGL coordinated a project clarification meeting in Kempsey to review the project methodology, collect all plans and relevant reports and inspect the caravan parks This meeting also reviewed best options on how to consult with nominated stakeholders and set up a local project engagement strategy

2. Review of Previous Reports and Support Documents

SGL reviewed all relevant reports as noted in the project brief as well as local tourism statistics and profile documents.

3. Review of the Five Caravan Parks

The project manager completed a customer stay in the region for a week and during this time stayed at three of the parks to complete site inspections, use the facilities and meet with facility management. During the site visit SGL completed an inventory and assessment of site infrastructure. The site visits also included completion of an opportunities and constraints review of the facilities, ground conditions and sites plus operational reviews on usage, financial history and capital works summary as well as management reviews.

4. Competitor Facility Review

SGL reviewed other caravan parks in the project area to determine the level of facility provision and services and to assist in determining market analysis of where the facilities currently rate locally.

5. Market Analysis SGL developed a market analysis to identify where the Council caravan parks are currently positioned, competitiveness and key selling proposition.

6. Environmental and Ecological Review

Graphite Architects through their landscape design area reviewed relevant planning documents/reports to complete a park environmental ecological review.

7. Compliance Review SGL will complete a park compliance assessment review.

Two: Research and Consultation

8. Park Visitor Profile SGL completed a park visitor profile review in association with Park Management utilizing current reservation and booking information, customer postcodes and booking data on numbers attending per booking, length of stay etc.

9. Stakeholder Interviews SGL in association with the client set up key stakeholder interviews and these included interviews with:

Bucher Nominees (including management)

Council representatives

Tourism association representatives

Community stakeholders as required SGL completed 15 local interviews in the project area as part of our services offer.

10. Summary of Key Findings and Review Forum

SGL summarised all review findings from the phase 1 and 2 tasks in a key findings report. This was forwarded to project representatives to review. SGL presented the studies key findings in Kempsey to Council’s senior management team and key issues around business trends, future park capital funding and management were discussed.

APPENDIX A Page 7BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 3 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Phase Task Details Three: Options and Opportunities

11. Development Plan Key Directions

SGL developed up a future key directions report that highlighted future options and opportunities to guide the future management and development plan.

12. Priority Facility Components to Improve Commercial Viability.

Based on the study’s findings to date SGL developed a priority facility improvement component list for each park and summarise this into probable short, medium and long term options for further review and viability analysis. These works also took into account the unique ecological and environmental issues and constraints as well as compliance with relevant industry and WHS regulations.

13. Concept Design Plans

Graphite Architects used Councils base plans to develop a future improvement works for each park highlighting the proposed priority facility components. These took into account all previous draft and final master plans for each reserve.

14. Facility Development and Management Options Review Forum

SGL coordinated a review forum in Kempsey with Council project representatives to discuss options and confirm final option for each park based on the studies detailed development and assessment findings.

Four: Recommended Plan of Management

15. Detailing of Recommended Development

Graphite Architects completed final changes to the agreed concept designs and SGL used quantity surveyor advice to cost out proposed developments.

16. Financial Analysis SGL completed financial analysis of proposed development and also set up an agreed term capital works guide.

17. Final Draft Report SGL detailed up all findings in a final draft report.

18. Review of Final Draft Report

SGL forwarded the report to client representatives for review and feedback.

19. Final Report Following client feedback all required changes were completed and updated into a final report.

1.4 Kempsey Shire Area Overview

A review of Council’s website and Wikipedia indicates Kempsey Shire Council is a local government area covering an area of 3,375 km of prime coast and hinterland located on the Mid North Coast of NSW approximately mid-way between Sydney and Brisbane. Kempsey Shire was formed in 1976 by the amalgamation of the former Kempsey Municipality and the former Macleay Shire. Population data on Council’s website indicates at the collection of the 2011 Census, there were 28,134 people in the Kempsey Shire Local Government Area. Of these, 50.2% were male and 49.8% were female. A key demographic profile factor was that Aboriginal and Torres Strait Islander people made up 11.1% of the population, more than four times the national average. The median age of people in the Kempsey Shire was 45 years; some eight years older than the national median. Children aged 0 to 14 years made up 19.4% of the population and people aged 65 years and over made up 19.8% of the population. Population growth in the Kempsey Shire between the 2001 Census and the 2006 Census was 1.86%; and in the subsequent five years to the 2011 Census was 2.73%. When compared with total population growth of Australia for the same periods, being 5.78% and 8.32% respectively, population growth in the Kempsey Shire local government area was significantly lower than the national average. The median weekly income for residents within the Kempsey Shire was also significantly below the national average, being one of the factors that place parts of the Kempsey Shire in an area of social disadvantage. The Kempsey Shire Council Operating Plan 2013 to 14 identifies tourism as one of two key growth areas, alongside agriculture, capable of offering considerable return on investment from value adding.

APPENDIX A Page 8BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 4 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

1.5 Macleay Valley Coast Overview

Macleay Valley Coast (MVC) is the tourism brand of the Kempsey Shire LGA. The Macleay Valley Coast encompasses the main service town of Kempsey, popular tourist destinations South West Rocks and Crescent Head, and numerous smaller villages and holiday accommodation locations including the coastal areas of Grassy Head, Stuarts Point and Hat Head. The MVC 2014 to 2016 Destination Management Plan indicates that the “Macleay Valley Coast brand

pays tribute to the Macleay River, which features prominently in the local landscape as it flows through the valley from the hinterland to the coast.”

The map below highlights the Macleay Valley area take up and location in context to Brisbane (538kms away) to the north and both Sydney (428kms) and Newcastle (280kms) to the south.

Source: MVC: Destination Management Plan 2014 to 2016

The MVC Destination Management Plan 2014-2016 indicates there is a lot to see and do with a variety of experiences including “famous surfing hot-spots, to timeless forests and imposing mountain ranges, the Macleay Valley Coast is a popular destination for nature-lovers, adventurers, families, couples, fishers, diving enthusiasts, surfers and visitors seeking a peaceful holiday experience in an un-spoilt and relatively underdeveloped destination.”

1.6 Tourism Profile

The MVC Destination Management Plan 2014-2016 indicates the Macleay Valley’s tourism sector is a major contributor to the local economy, generating an estimated $173 million each year. It is also the region’s fourth largest employer, with 8.8 per cent of the local workforce employed in tourism-related businesses. Locally, tourism directly contributes to wages and jobs. Indirectly, it supports numerous local supply chains. Exports from tourism are also the region’s fourth highest, making up 4.9 per cent of all local exports. Kempsey Shire Council recognises the significant economic growth opportunities from growing and value adding to the local tourism industry and supports the State Government’s goal to double overnight expenditure by the year 2020.

APPENDIX A Page 9BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 5 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Council further recognises that the Visitor Economy is broader than holiday-makers, covering many other visitors to the Macleay Valley Coast for sport, business, events, culture and entertainment, or to visit friends and relatives.

The Kempsey Shire Council Operating Plan 2013/14 identifies tourism as one of two key growth areas, alongside agriculture, capable of considerable return on investment from value adding. The Macleay Valley Coast is an environmentally pristine coast and country destination that is popular among leisure-seekers and outdoor enthusiasts. Visitors are particularly attracted to the natural beauty of the Macleay Valley coastline. From gently rolling waves to pounding surf breaks, the variety and quality of local beaches make them some of Australia’s best, with surfers travelling from around the world to experience the breaks at Crescent Head Surfing Reserve. Within minutes of leaving the beach, visitors can also experience the Australian bush, complete with crystal clear creeks, rocky outcrops, towering eucalypts and good old- fashioned country hospitality. The Upper Macleay River offers some of Australia’s best bass fishing, while lovers of the great outdoors come to camp, bushwalk, explore the restored timber towns and soak up the natural beauty. Nature lovers enjoy mountain biking and bush walking trails, with access to 34 State forests, National Parks and reserves. Much of the Macleay Valley lifestyle is focused on the water, with plenty of locations and opportunities for boating, kayaking, paddle boarding and fishing. Diving is an international draw card, with the dives off South West Rocks some of the finest in the world. Known as ‘the divers dive’, the famous dive off Fish Rock features one of the only dive-through caves in Australia and is home to an abundance of temperate and subtropical marine life, including turtles, rays, eels and fish, as well as being a breeding ground for the rare Grey Nurse Shark. The Macleay is also home to a number of unique tourism icons, including historic Trial Bay Gaol, the most elevated lighthouse on the Australian East Coast, Smoky Cape Lighthouse, the famous Akubra hat and the original Slim Dusty Homestead.

1.6.1 Overview of Macleay Valley Coast Assets and Products The MVC Destination Management Plan 2014 to 2016 highlights a completed audit of tourism related assets and products in July 2013 and notes the following: 1. Accommodation There were 80 accommodation providers who collectively offered 2,703 rooms accounting for over 10,700 beds in Kempsey Shire. The largest concentration of accommodation providers was located at South West Rocks and Kempsey. The review saw the total beds at the 5 council holiday parks being: Table 1.2 KSC Holiday Park Beds 2013

Holiday Park Cabins/Beds Sites/Beds Total Beds

Crescent Head HP 30/150 206/1,030 1,180

Horseshoe Bay HP 12/52 152/600 652

Hat Head HP 10/40 269/1,000 1,040

Stuarts Point HP 13/51 143/272 323

Grassy Point HP 4/16 90/360 376

Total Beds 2,919

The review of Kempsey Shires five caravan parks indicates in the 2013 accommodation audit they account for a total of 2,919 beds. This represents 27% of the area’s accommodation beds. 2. Transport Commercial flights are available at the regional centres of Port Macquarie and Coffs Harbour with Kempsey Airport available for private charter.

APPENDIX A Page 10BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 6 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

The main access point for most visitors is the Pacific Highway, linking the major populations of Sydney/Newcastle and the Hunter Valley to the south and Brisbane/Gold Coast and Northern NSW to the north. 3. Restaurants and Cafes There were over 90 food and beverage outlets identified including:

45 restaurants

22 cafes

24 takeaway outlets

4. Attractions and Activities The MVC area is best known for its natural assets (over 100,000ha), which include National Parks, Walking Trails, State Forests and beaches. There are 14 key main made attractions in the Shire including Smoky Cape Lighthouse, Trial Bay Goal and Galleries. 5. Events The MVC hosts approximately 46 events throughout the year and the annual events calendar is increasing each year.

1.6.2 Visitor Expenditure Trends

The Visitor Economy is estimated to be worth $173 million to the Macleay Valley Coast. Domestic visitors represent 98.1% of travel within the Macleay, contributing $169 million to the local economy.

Domestic overnight visitors spend an average of $570 per visit, averaging $128 per night. International visitors represent 1.9% of travel within the region, contributing around $4 million to the local economy. The average spend per international visitor is $383, averaging $74 per night which is significantly less than domestic overnight visitors.

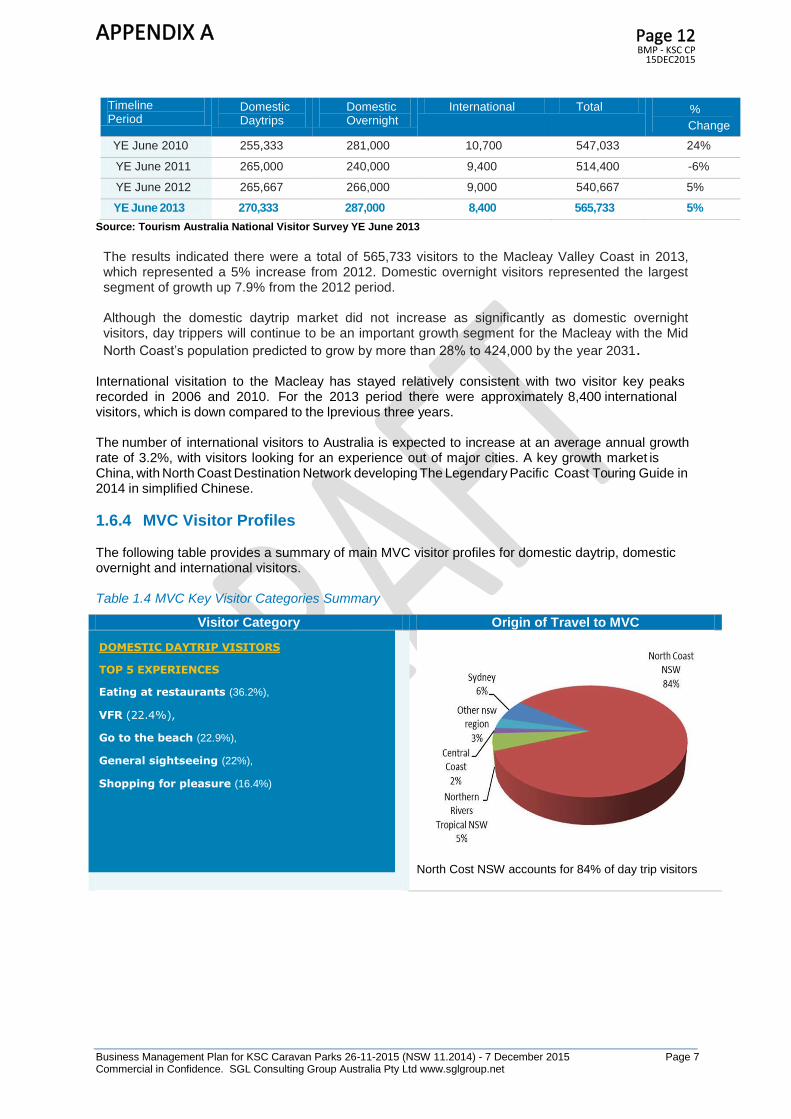

1.6.3 MVC Visitation Trends

The below table highlights the Macleay Valley Coast’s performance over the past 13 years, the statistics have been derived from the National Visitor Survey (NVS) and International Visitor Survey (IVS) – YE June 2013.

Table 1.3 MVC Visitation Trends By Visitor Type

Timeline Period

Domestic

Daytrips

Domestic

Overnight

International Total %

change

YE June 2000 - 291,000 8,000 299,000 -

YE June 2001 232,333 285,000 6,400 523,733 75%

YE June 2002 214,667 336,000 4,800 555,467 6%

YE June 2003 198,000 285,000 5,300 488,300 -12%

YE June 2004 181,000 298,000 5,100 484,100 -1%

YE June 2005 212,667 360,000 5,400 578,067 19%

YE June 2006 210,667 289,000 11,000 510,667 -12%

YE June 2007 235,333 307,000 8,200 550,533 8%

YE June 2008 213,333 247,000 9,200 469,533 -15%

YE June 2009 228,667 203,000 8,200 439,867 -6%

APPENDIX A Page 11BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 7 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Source: Tourism Australia National Visitor Survey YE June 2013

The results indicated there were a total of 565,733 visitors to the Macleay Valley Coast in 2013, which represented a 5% increase from 2012. Domestic overnight visitors represented the largest segment of growth up 7.9% from the 2012 period. Although the domestic daytrip market did not increase as significantly as domestic overnight visitors, day trippers will continue to be an important growth segment for the Macleay with the Mid

North Coast’s population predicted to grow by more than 28% to 424,000 by the year 2031.

International visitation to the Macleay has stayed relatively consistent with two visitor key peaks recorded in 2006 and 2010. For the 2013 period there were approximately 8,400 international visitors, which is down compared to the lprevious three years. The number of international visitors to Australia is expected to increase at an average annual growth rate of 3.2%, with visitors looking for an experience out of major cities. A key growth market is China, with North Coast Destination Network developing The Legendary Paci fi c Coast Touring Guide in 2014 in simpli fi ed Chinese.

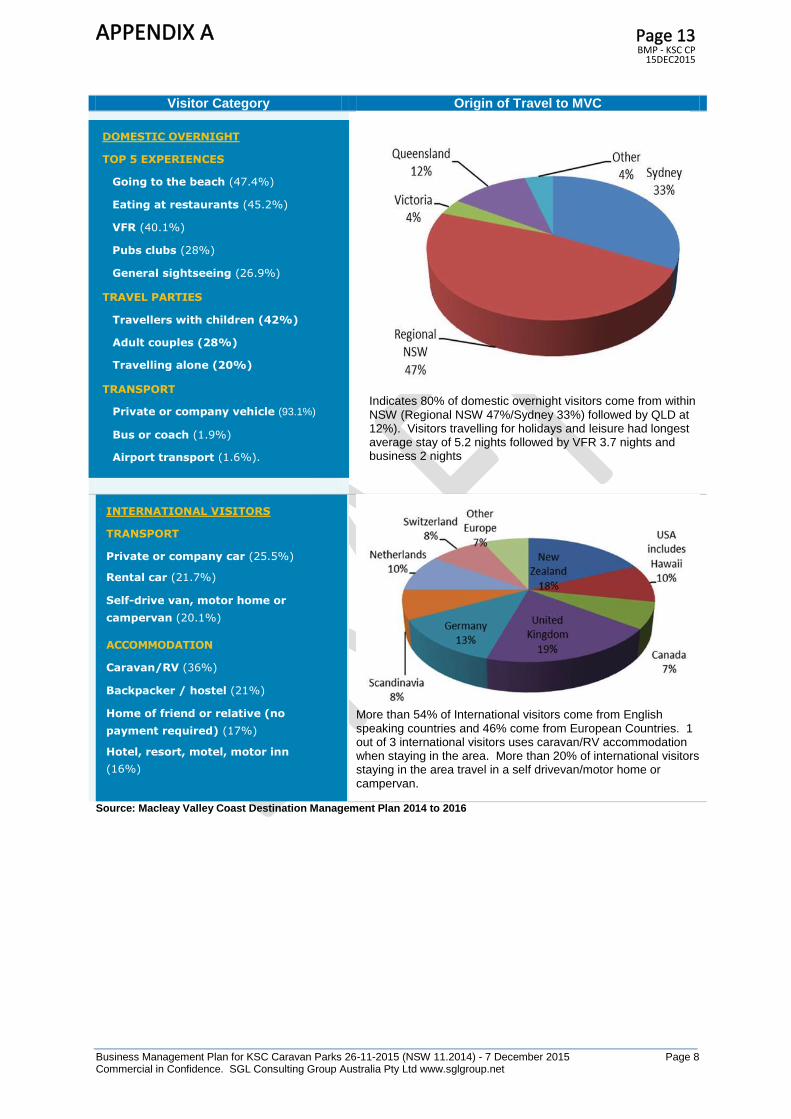

1.6.4 MVC Visitor Profiles The following table provides a summary of main MVC visitor profiles for domestic daytrip, domestic overnight and international visitors. Table 1.4 MVC Key Visitor Categories Summary

Visitor Category Origin of Travel to MVC

North Cost NSW accounts for 84% of day trip visitors

Timeline Period

Domestic Daytrips

Domestic Overnight

International Total %

Change

YE June 2010 255,333 281,000 10,700 547,033 24%

YE June 2011 265,000 240,000 9,400 514,400 -6%

YE June 2012 265,667 266,000 9,000 540,667 5%

YE June 2013 270,333 287,000 8,400 565,733 5%

DOMESTIC DAYTRIP VISITORS

TOP 5 EXPERIENCES

Eating at restaurants (36.2%),

VFR (22.4%),

Go to the beach (22.9%),

General sightseeing (22%),

Shopping for pleasure (16.4%)

APPENDIX A Page 12BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 8 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Visitor Category Origin of Travel to MVC

Indicates 80% of domestic overnight visitors come from within NSW (Regional NSW 47%/Sydney 33%) followed by QLD at 12%). Visitors travelling for holidays and leisure had longest average stay of 5.2 nights followed by VFR 3.7 nights and business 2 nights

More than 54% of International visitors come from English speaking countries and 46% come from European Countries. 1 out of 3 international visitors uses caravan/RV accommodation when staying in the area. More than 20% of international visitors staying in the area travel in a self drivevan/motor home or campervan.

Source: Macleay Valley Coast Destination Management Plan 2014 to 2016

INTERNATIONAL VISITORS

TRANSPORT

Private or company car (25.5%)

Rental car (21.7%)

Self-drive van, motor home or

campervan (20.1%)

ACCOMMODATION

Caravan/RV (36%)

Backpacker / hostel (21%)

Home of friend or relative (no

payment required) (17%)

Hotel, resort, motel, motor inn

(16%)

DOMESTIC OVERNIGHT

TOP 5 EXPERIENCES

Going to the beach (47.4%)

Eating at restaurants (45.2%)

VFR (40.1%)

Pubs clubs (28%)

General sightseeing (26.9%)

TRAVEL PARTIES

Travellers with children (42%)

Adult couples (28%)

Travelling alone (20%)

TRANSPORT

Private or company vehicle (93.1%)

Bus or coach (1.9%)

Airport transport (1.6%).

APPENDIX A Page 13BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 9 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.1 Introduction

This section of the report presents information on the five holiday parks in relation to their capacity, management, operational and business trends including:

History of the Council Parks

Individual and combined holiday park overview and capacity

Individual and combined holiday park past three years occupancy results

Individual and combined holiday park past three years operating income

Individual and combined holiday park past three years operating expenditure

Individual and combined holiday park past three years operating performance

Individual and combined holiday park past three years capital development funding

2.2 Historical Review of Council Caravan Parks

The five Kempsey Shire Caravan Parks have different historical and development history as well as being operated under different management and lease models. We have reviewed a range of documents to help summarise some of the available history of the caravan parks.

2.2.1 1988 Kempsey Shire Caravan Park Management Plan Reviews of the 1988 Kempsey Shire Caravan Park Management Plan indicated at this time Council managed four parks, each under separate management contracts being:

Crescent Head Caravan Park (253 sites)

Grassy Head Caravan Park (85 sites)

Hat Head Caravan Park (250 sites)

Stuarts Point Caravan Park (126 sites)

The review found the contracts were set up to provide caretakers for the parks and there were no incentives for management to improve the park’s assets, onsite accommodation or increase use and associated income. The report also noted:

The parks did not comply with regulatory standards and required significant upgrades and capital expenditure.

Were poorly presented and maintained.

The stock of available onsite accommodation was limited and mainly was low standard onsite caravans.

The tariff levels and charges were high for overnight and low for long-term users, so inappropriate for the use and also park amenities and services standard offered.

2 Review of Councils Caravan Parks

APPENDIX A Page 14BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 10 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

There were a large number of permanent users and long-term visitors paying low rates who believed they had ongoing rights to the sites.

The combined caravan park contracts were operating at an annual loss.

The 1988 management plan report recommended a large number of changes to management systems, operations and capital improvements.

2.2.2 2005 Kempsey Shire Caravan Park Management Plans This report was prepared by Integrated Site Design in June 2005 and covered the four caravan parks under direct Council control, being:

Crescent Head Caravan Park (16 cabins and 261 sites)

Grassy Head Caravan Park (2 cabins and 98 sites)

Hat Head Caravan Park (3 cabins and 301 sites)

Stuarts Point Caravan Park (6 cabins and 132 sites)

The report reviews the changes made from 1988 that, in summary, included:

Management was changed to link the parks under one contracted management model and management was paid a percentage of income.

Tariffs were reviewed and modified to reduce long-term use and attract higher revenue for short-term use.

New onsite units (cabins) were installed at the parks.

Capital works to improve regulatory services was commenced.

Many long-term sites were turned back to short-term sites over time.

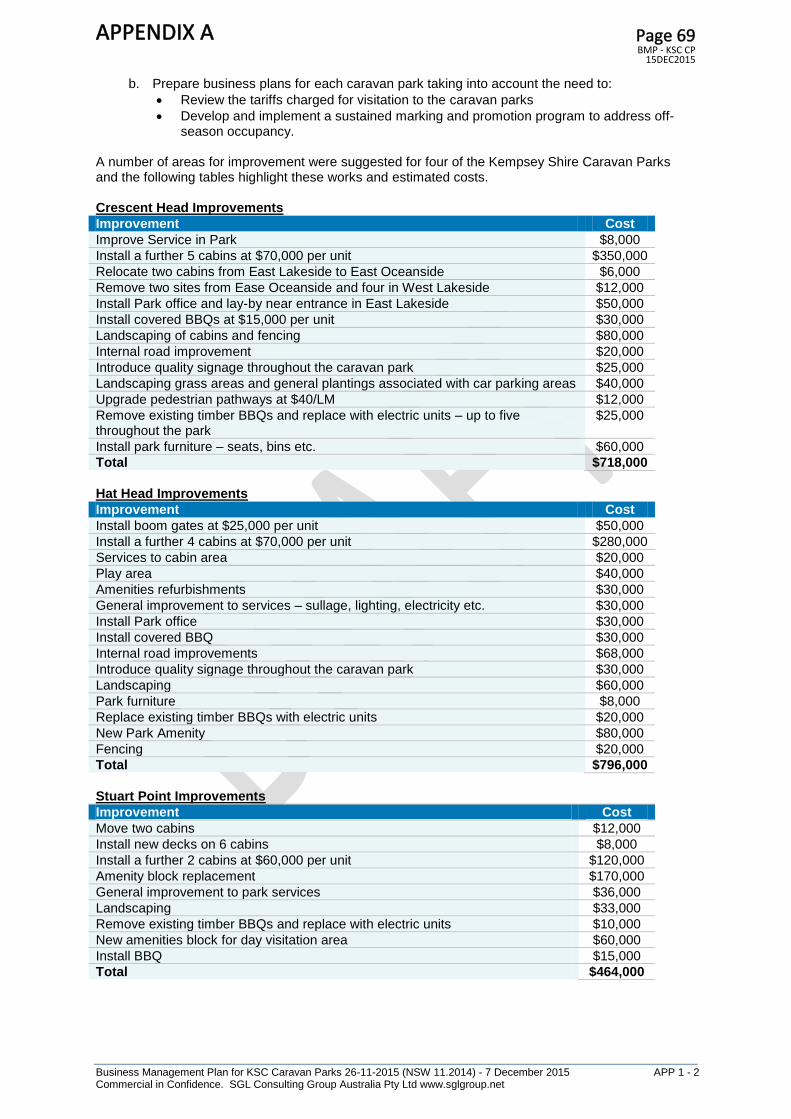

The report reviews the 1996/97 operating year as a period to review these changes some 8 years after the 1988 review. This showed the four parks had a total income of $1.362M with camping/site fees accounting for approx. 74% of income and onsite cabins accounting for 26% of income. The combined parks operating expenditure was estimated at $992,000. This saw a major turnaround in business performance from an operating loss in 1988 to an operating surplus (before capital investment) of $370,000. Council invested $316,194 in capital works (mix of loan funded and direct funded projects) in 1996/97 and this was able to be funded from operating surpluses. The report also reviewed the 2002/03 financial year results for the four combined caravan parks and noted annual income had increased to an estimated $1.900M ($600,000 increase in income). Annual operating expenditure was estimated at $1.288M, so the net operating surplus (before capital expenditure) had also increased considerably to $612,000 (increase of $242,000 on 1996/97 operating surplus). The 2005 report findings indicated Council had made significant improvements to the four caravan parks since 1988 and this investment was now showing positive results. The report presented a range of recommendations for each of the four parks and these are summarised in Appendix One of the report. The report made 7 key recommendations and estimated a total of $2.254M in capital works was required to be made by Council over the next 5 years:

Crescent Head CP: $718,000

Hat Head CP: $796,000

Stuart Point CP: $464,000

Grassy Head CP: $275,000

Total Recommended Works: $2,253,000

APPENDIX A Page 15BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 11 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.2.3 Caravan Park Operational Changes and Improvements from 2005 There has not been an updated plan of management for the combined parks since 2005 so SGL has not been able to obtain any detailed reports to track the completed improvement works, funding and specific business impacts from these changes. What is obvious is that the combined caravan park business has improved considerably since 2005, so this indicates many of the recommended changes have positively occurred. A key change that has impacted on the business not covered in the 2005 report is the Horseshoe Bay (Reserve) Holiday Park (previously referred to as South West Rocks Caravan Park) was taken back over by Council. This was added to the current management contract that took effect on the 30

th of

June 2011. This now saw five caravan parks linked in management under a common contract. Interviews with Council management and park management indicated the Horseshoe Bay CP was in poor condition at handover and this required increased capital investment over the past few years.

2.3 Review of Kempsey Shire Holiday Parks

Before future business and management plan improvements are researched, it is essential to gain a more detailed understanding of the current facilities, management, operations and services that make up Kempsey Shire Holiday Parks. A key change to the management and marketing of Council’s Holiday Parks came about with the new management contract and rebranding of the parks into Macleay Valley Coastal Holiday Parks in 2011. Macleay Valley Coastal Holiday Parks are now the single largest provider of accommodation beds in the Kempsey Shire local government area, contributing approximately one-third (3000 of a total 10,764) of the Shire’s beds through a combination of cabins and campsites. All five parks are located in prime coastal locations (see diagram below), featuring pristine environmental surrounds, long stretches of sandy beaches, a sub-tropical climate and ideal conditions for surfing, fishing and other water-based recreational activities.

Source: Macleay Valley Coast Map – Here and Now Advertising and Publications

APPENDIX A Page 16BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 12 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

The 5 parks’ unique natural environs cannot, however, continue to be relied upon to attract new and returning visitors, particularly in what is becoming an increasingly sophisticated holiday park market. Ongoing visitor feedback suggests visitor expectations in relation to accommodation quality, public amenities, grounds, facilities and services are not always being met. The following sections provide an overview of each of the parks:

Site/user capacities,

2013/14 cabin and site occupancies,

Past three years financial review

Past four years capital improvement budgets and key work areas

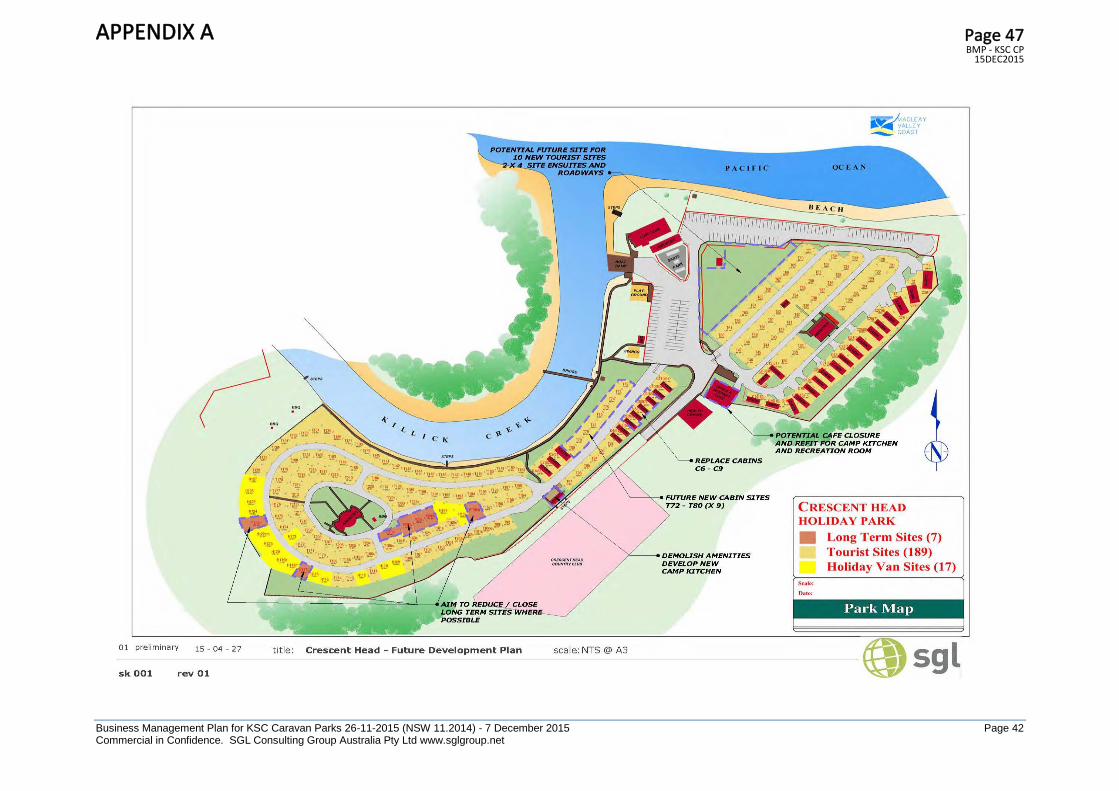

2.3.1 Crescent Head Holiday Park

The parks website notes “with its beachfront location and proximity to the many activities the area has to offer, Crescent Head Holiday Park is one of the best located parks on the Mid North Coast of NSW. Crescent Head has one of the best right hand point breaks in the world, and the village is one of the hot spots of national and international surfing”. The park is divided up into two key zones, being Oceanside or Creekside, and both areas have many sites with water views. A site layout plan is listed below.

APPENDIX A Page 17BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 13 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.3.1.1 CH Holiday Park Cabin and Site Capacities The following table lists the current (2015) Crescent Head Holiday Park cabin and site capacities. Table 2.1 Crescent Head Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Crescent Head

Holiday Park

30 7 189 17 0 0

Today’s cabin and site capacity is lower than the park originally had due to changes to the park’s layout, inclusion of more onsite accommodation and reduction of long term/holiday sites. In 1997/98 the park had the following provision of sites:

9 long term sites

200 vacant short term (tourist) sites

16 short term sites with park cabins

32 holiday vans on short term sites

20 camp sites

The comparison of the 1997/98 capacities indicates that in 2015 there are 14 more cabins, 2 less long-term sites, 11 less tourist sites, 15 less holiday van sites and no camping sites.

2.3.1.2 CH Holiday Park Cabin Occupancy 2013/14 The following table lists the Crescent Head Holiday Park Cabin Occupancy for 2013/14: Table 2.2 Crescent Head Holiday Park Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Crescent Head

Holiday Park

30 10,950 7,785 3,165 $1.141M $146 71%

The occupancy review for the 30 cabins indicates the park is preforming well above industry cabin occupancy averages at 71% with 7,785 days occupied out of a total of 10,950 possible hire days. The average revenue per day hired is also above industry standards at $146/day/cabin.

2.3.1.3 CH Holiday Park Tourist Site Occupancy 2013/14 The following table lists the Crescent Head Holiday Park tourist site occupancy for 2013/14: Table 2.3 Crescent Head Holiday Park Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Crescent Head

Holiday Park

189 68,985 35,964 33,021 $1,500M $41.70 52%

The occupancy review for the 189 tourist sites indicates the park is preforming well above industry tourist site occupancy averages at 52% with 35,964 days occupied out of a total of 68,985 possible site hire days. The average revenue per day hired is about on average for industry standards at $41.70/day/tourist site.

APPENDIX A Page 18BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 14 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.3.1.4 CH Holiday Park Financial Trends 2011 to 2014 The following table lists the Crescent Head Holiday Park financial trends between 2011 and 2014: Table 2.4 Crescent Head Holiday Park Financial Trends 2011 to 2014

Crescent Head HP 2011/12

(Actual)

2012/13

(Actual)

2013/14

(Actual)

Operating Income $2,255,782 $2,344,469 $2,607,576

Operating Expenditure $1,666,414 $1,772,747 $1,945,685

Net Operating Profit/(Loss) $589,368 $571,722 $661,891

Capital Expenditure $260,708 $241,478 $132,162

Loan Repayments $12,302 $12,534 $12,782

Note: Family Holiday Experience Settlement $29K

Depreciation $174K

Family Holiday Experience Settlement $81K

Depreciation $176K

Depreciation $202K

The financial review indicates:

Operating income has increased annually from $2.255M in 2011/12 to $2.607M in 2013/14. This was an increase of approx. $352,000 (+15.6%) or an average yearly increase on average of $176,000 (+7.8%).

Operating expenditure has also increased annually from $1.666M in 2011/12 to $1.945M in 2013/14. This was an increase of approx. $279,000 (16.7%) or an average yearly increase on average of $89,000 (+8.35%).

A net operating profit was recorded for each of the three years ranging from $589,000 in 2011/12 and increasing to $662,000 by 2013/14. In 2013/14 the net operating profit saw income as a percentage of expenditure being 134%.

Capital expenditure fluctuated over the three years with a high of $260,708 in 2011/12 and a low of $132,162 in 2013/14.

Annual loan repayments were low at approximately $12,000/year.

2.3.2 Hat Head Holiday Park

This Holiday Park surrounded by the grandeur of Hat Head National Park and the tranquil seaside village of Hat Head, offers the ultimate beachside escape for nature lovers. The rich aquatic environment of the continental shelf is just 5.25 nautical miles offshore. Hat Head Holiday Park is a great place for people looking to fish with a diverse range of ocean, river and creek fishing options. The park is also divided up into a number of key zones being ocean side or creek side divided by a public road that provides access to ocean and creek boat ramps and public parking and day areas. A site layout plan is listed on the next page.

2.3.2.1 HH Holiday Park Cabin and Site Capacities The following table lists the current (2015) Hat Head Holiday Park cabin and site capacities. Table 2.5 Hat Head Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Hat Head Holiday

Park

10 0 101 49 89 47

APPENDIX A Page 19BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 15 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Today’s cabin and site capacity is lower than the park originally had, due to changes to the park’s layout and inclusion of more onsite accommodation, and reduction of long term/holiday sites. In 1997/98, the park had the following provision of sites:

4 long term sites

102 vacant short term (tourist) sites

3 short term sites with park cabins

46 holiday vans on short term sites

149 camp sites

The comparison of the 1997/98 capacities indicates that in 2015 there are 7 more cabins, no long- term sites, 1 less tourist sites, 3 less holiday van sites and 60 less camping sites (though there are a large number of temporary/overflow camping sites still used at peak holiday periods).

2.3.2.2 HH Holiday Park Cabin Occupancy 2013/14 The following table lists the Hat Head Holiday Park Cabin Occupancy for 2013/14: Table 2.6 Hat Head Holiday Park Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Hat Head

Holiday Park

10 3,650 2,291 1,359 $266K $116 63%

The occupancy review for the 10 cabins indicates the park is preforming slightly above industry cabin occupancy averages at 63% with 2,291 days occupied out of a total of 3,650 possible hire days. The average revenue per day hired is also at average industry standards at $116/day/cabin.

APPENDIX A Page 20BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 16 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2.3.2.3 HH Holiday Park Tourist Site Occupancy 2013/14 The following table lists the Hat Head Holiday Park tourist site occupancy for 2013/14: Table 2.7 Hat Head Holiday Park Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Hat Head

Holiday Park

101 36,865 23,967 12,898 $952K $39.72 65%

The occupancy review for the 101 tourist sites indicates the park is preforming well above industry tourist site occupancy averages at 65% with 23,967 days occupied out of a total of 36,865 possible site hire days. The average revenue per day hired is higher than average for industry standards at $39.72/day/tourist site.

2.3.2.4 HH Holiday Park Financial Trends 2011 to 2014 The following table lists the Hat Head Holiday Park financial trends between 2011 and 2014: Table 2.8 Hat Head Holiday Park Financial Trends 2011 to 2014

Hat Head HP 2011/12

(Actual)

2012/13

(Actual)

2013/14

(Actual)

Operating Income $1,133,116 $1,151,338 $1,366,845

Operating Expenditure $891,522* $899,451* $1,001,075*

Net Operating Profit/(Loss) $241,594 $251,887 $365,770

Capital Expenditure $10,348 $180,702 $20,323

Loan Repayments $89,904 $90,027 $68,609

Note *: Family Holiday Experience Settlement $15K

Depreciation 93K

Family Holiday Experience Settlement $39K

Depreciation 93K

Depreciation 93K

The financial review indicates:

Operating income has increased annually from $1.133M in 2011/12 to $1.366M in 2013/14. This was an increase of approx. $233,000 (+20.5%) or an average yearly increase on average of $116,500 (+10.25%).

Operating expenditure has also increased annually from $0.891M in 2011/12 to $1.001M in 2013/14. This was an increase of approx. $110,000 (12.3%) or an average yearly increase on average of $55,000 (+6.15%).

A net operating profit was recorded for each of the three years ranging from $242,000 in 2011/12 and increasing to $366,000 by 2013/14. In 2013/14 the net operating profit saw income as a percentage of expenditure being 136%.

Capital expenditure fluctuated over the three years with a high of $180,702 in 2012/13 and a low of $10,348 in 2011/12.

Annual loan repayments fluctuated from $89,900 in 2011/12 to $68,609 in 2013/14.

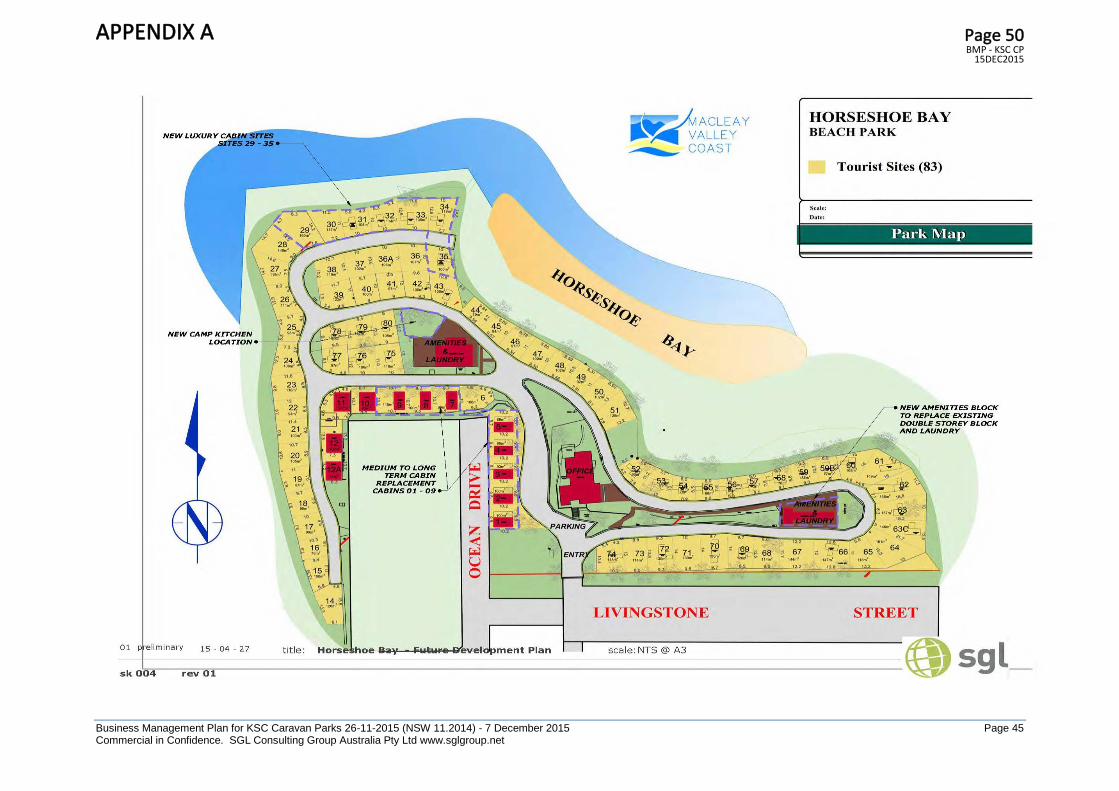

2.3.3 Horseshoe Bay Holiday Park

The MVC website indicates the park is in a unique and picturesque location on the NSW north coast, Horseshoe Bay Holiday Park is located on absolute beach frontage at South West Rocks and is nestled under shady pines with panoramic ocean, mountain and beach views. South West Rocks offers a selection of breathtaking beaches, rivers and National Parks and is perfect for family holidays, fishermen and those who want to explore or get away from it all.

APPENDIX A Page 21BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 17 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

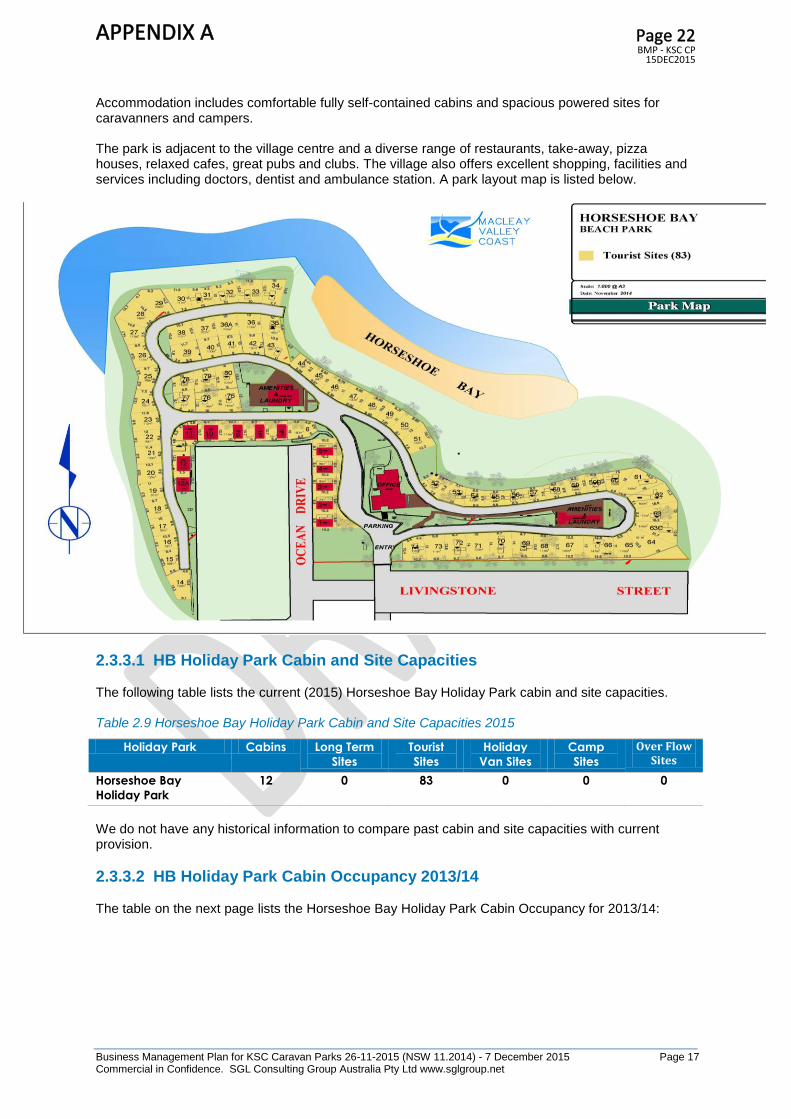

Accommodation includes comfortable fully self-contained cabins and spacious powered sites for caravanners and campers. The park is adjacent to the village centre and a diverse range of restaurants, take-away, pizza houses, relaxed cafes, great pubs and clubs. The village also offers excellent shopping, facilities and services including doctors, dentist and ambulance station. A park layout map is listed below.

2.3.3.1 HB Holiday Park Cabin and Site Capacities The following table lists the current (2015) Horseshoe Bay Holiday Park cabin and site capacities. Table 2.9 Horseshoe Bay Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Horseshoe Bay

Holiday Park

12 0 83 0 0 0

We do not have any historical information to compare past cabin and site capacities with current provision.

2.3.3.2 HB Holiday Park Cabin Occupancy 2013/14 The table on the next page lists the Horseshoe Bay Holiday Park Cabin Occupancy for 2013/14:

APPENDIX A Page 22BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 18 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 2.10 Horseshoe Bay Holiday Park Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Horseshoe Bay

Holiday Park

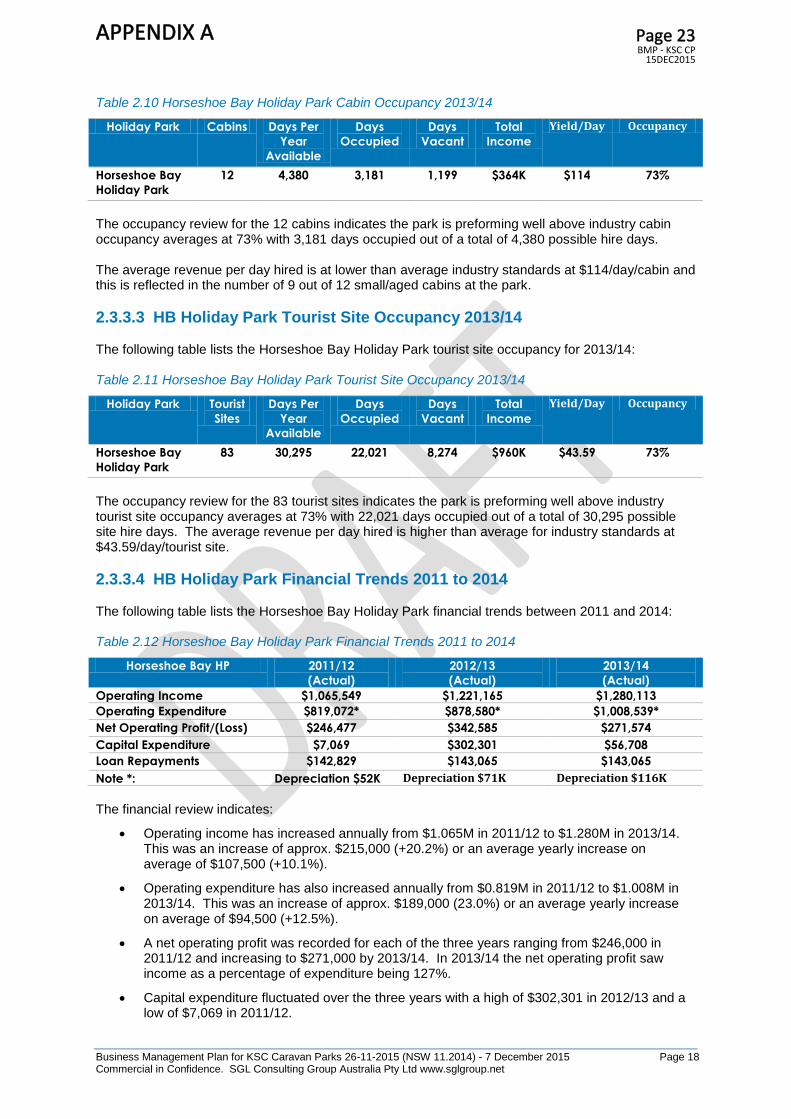

12 4,380 3,181 1,199 $364K $114 73%

The occupancy review for the 12 cabins indicates the park is preforming well above industry cabin occupancy averages at 73% with 3,181 days occupied out of a total of 4,380 possible hire days. The average revenue per day hired is at lower than average industry standards at $114/day/cabin and this is reflected in the number of 9 out of 12 small/aged cabins at the park.

2.3.3.3 HB Holiday Park Tourist Site Occupancy 2013/14 The following table lists the Horseshoe Bay Holiday Park tourist site occupancy for 2013/14: Table 2.11 Horseshoe Bay Holiday Park Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Horseshoe Bay

Holiday Park

83 30,295 22,021 8,274 $960K $43.59 73%

The occupancy review for the 83 tourist sites indicates the park is preforming well above industry tourist site occupancy averages at 73% with 22,021 days occupied out of a total of 30,295 possible site hire days. The average revenue per day hired is higher than average for industry standards at $43.59/day/tourist site.

2.3.3.4 HB Holiday Park Financial Trends 2011 to 2014 The following table lists the Horseshoe Bay Holiday Park financial trends between 2011 and 2014: Table 2.12 Horseshoe Bay Holiday Park Financial Trends 2011 to 2014

Horseshoe Bay HP 2011/12

(Actual)

2012/13

(Actual)

2013/14

(Actual)

Operating Income $1,065,549 $1,221,165 $1,280,113

Operating Expenditure $819,072* $878,580* $1,008,539*

Net Operating Profit/(Loss) $246,477 $342,585 $271,574

Capital Expenditure $7,069 $302,301 $56,708

Loan Repayments $142,829 $143,065 $143,065

Note *: Depreciation $52K Depreciation $71K Depreciation $116K

The financial review indicates:

Operating income has increased annually from $1.065M in 2011/12 to $1.280M in 2013/14. This was an increase of approx. $215,000 (+20.2%) or an average yearly increase on average of $107,500 (+10.1%).

Operating expenditure has also increased annually from $0.819M in 2011/12 to $1.008M in 2013/14. This was an increase of approx. $189,000 (23.0%) or an average yearly increase on average of $94,500 (+12.5%).

A net operating profit was recorded for each of the three years ranging from $246,000 in 2011/12 and increasing to $271,000 by 2013/14. In 2013/14 the net operating profit saw income as a percentage of expenditure being 127%.

Capital expenditure fluctuated over the three years with a high of $302,301 in 2012/13 and a low of $7,069 in 2011/12.

APPENDIX A Page 23BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 19 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Annual loan repayments were similar for all three years, being between $142,000 and $143,000.

2.3.4 Stuarts Point Holiday Park

The MVC website indicates this park is nestled on the banks of the Macleay River between vast golden beaches, the lush forests and rich pastures of the Macleay Valley. It is described as a secluded and serene riverside hideaway, offering a boat ramp and mooring, fish cleaning table and choice of beach, river or blue water fishing. Stuarts Point Holiday Park offers clean, well-equipped facilities and a playground and is situated close to local shops, a Tavern and a Workers Club. The park site plan is listed below.

2.3.4.1 SP Holiday Park Cabin and Site Capacities The following table lists the current (2015) Stuarts Point Holiday Park cabin and site capacities. Table 2.13 Stuarts Point Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Stuarts Point Holiday

Park

9 4 69 39 36 0

Today’s cabin and site capacity is lower than the park originally had due to changes to the park’s layout and inclusion of more onsite accommodation, and reduction of long term/holiday sites. In 1997/98 the park had the following provision of sites:

APPENDIX A Page 24BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 20 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

12 long term sites

65 vacant short term (tourist) sites

6 short term sites with park cabins

35 holiday vans on short term sites

20 camp sites

The comparison of the 1997/98 capacities indicates that in 2015 there are 3 more cabins, 8 less long- term sites, 4 more tourist sites, 4 more holiday van sites and 16 more camping sites.

2.3.4.2 SP Holiday Park Cabin Occupancy 2013/14 The following table lists the Stuarts Point Holiday Park Cabin Occupancy for 2013/14: Table 2.14 Stuarts Point Holiday Park Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Stuarts Point

Holiday Park

9 3,285 1,555 1,730 $156K $100 47%

The occupancy review for the 9 cabins indicates the park is preforming well below industry cabin occupancy averages at 47% with only 1,555 days occupied out of a total of 3,285 possible hire days. The average revenue per day hired is also below industry standards at $100/day/cabin. This is being influenced in part by two of the cabins not having en-suites and therefore recording low hire rates.

2.3.4.3 SP Holiday Park Tourist Site Occupancy 2013/14 The following table lists the Stuarts Point Holiday Park tourist site occupancy for 2013/14: Table 2.15 Stuarts Point Holiday Park Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Stuarts Point

Holiday Park

69 25,185 11,851 13,334 $357K $30.12 47%

The occupancy review for the 69 tourist sites indicates the park is preforming just below industry tourist site occupancy averages at 42% with 11,851 days occupied out of a total of 25,185 possible site hire days. The average revenue per day hired is below average for industry standards at $30.12/day/tourist site.

2.3.4.4 SP Holiday Park Financial Trends 2011 to 2014 The table on the next page lists the Stuarts Point Holiday Park financial trends between 2011 and 2014:

APPENDIX A Page 25BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 21 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 2.16 Stuarts Point Holiday Park Financial Trends 2011 to 2014

Stuarts Point HP 2011/12

(Actual)

2012/13

(Actual)

2013/14

(Actual)

Operating Income $512,346 $556,959 $635,072

Operating Expenditure $471,600* $491,178* $546,613*

Net Operating Profit/(Loss) $40,746 $65,781 $88,459

Capital Expenditure $6,050 $107,501 $281,201

Loan Repayments $140,002 $139,864 $139,978

Note *: Family Holiday Exp. Settlement $7K

Depreciation $52K

Family Holiday Exp. Settlement $19K

Depreciation $71K

Depreciation $116K

The financial review indicates:

Operating income has increased annually from $0.512M in 2011/12 to $0.635M in 2013/14. This was an increase of approx. $123,000 (+24%) or an average yearly increase on average of $61,500 (+12.0%).

Operating expenditure has also increased annually from $0.471M in 2011/12 to $0.546M in 2013/14. This was an increase of approx. $75,000 (16.0%) or an average yearly increase on average of $37,500 (+8.0%).

A net operating profit was recorded for each of the three years ranging from $40,000 in 2011/12 and increasing to $88,000 by 2013/14. In 2013/14 the net operating profit saw income as a percentage of expenditure being 116%.

Capital expenditure fluctuated over the three years with a high of $281,201 in 2013/14 and a low of $6,050 in 2011/12.

Annual loan repayments were similar at approximately $140,000/year.

2.3.5 Grassy Head Holiday Park

The MCV website indicates the park is tucked away amongst lush coastal forests and immaculate golden beaches and is one of the natural holiday parks of the Mid North Coast. The abundance of fish and birdlife combined with the beautiful bushland surrounds is a delight for nature lovers. The Park, nestled beneath a canopy of shady trees, is located just 200 metres from Grassy Head beach. Tranquil recreational activity opportunities include rainforest, beach and river walks, rock and beach fishing, swimming and surfing. A park site map is listed as follows on the next page.

2.3.5.1 GH Holiday Park Cabin and Site Capacities The following table lists the current (2015) Grassy Head Holiday Park cabin and site capacities. Table 2.17 Grassy Head Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Grassy Head Holiday

Park

4 0 43 29 24 0

Today’s cabin and site capacity is lower than the park originally had due to changes to the park’s layout and inclusion of more onsite accommodation and reduction of long term/holiday sites. In 1997/98 the park had the following provision of sites:

1 long term site

35 vacant short term (tourist) sites

APPENDIX A Page 26BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 22 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

2 short term sites with park cabins

32 holiday vans on short term sites

30 camp sites

The comparison of the 1997/98 capacities indicates that in 2015 there are 2 more cabins, no long- term sites, 8 more tourist sites, 3 less holiday van sites and 6 less camping sites.

2.3.5.2 GH Holiday Park Cabin Occupancy 2013/14 The following table lists the Grassy Head Holiday Park Cabin Occupancy for 2013/14: Table 2.18 Grassy Head Holiday Park Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Grassy Head

Holiday Park

4 1,460 629 831 $52K $83 43%

The occupancy review for the 4 cabins indicates the park is preforming well below industry cabin occupancy averages at 43% with 629 days occupied out of a total of 1,460 possible hire days. The average revenue per day hired is also well below industry standards at $83/day/cabin.

2.3.5.3 GH Holiday Park Tourist Site Occupancy 2013/14 The table on the next page lists the Grassy Head Holiday Park tourist site occupancy for 2013/14:

APPENDIX A Page 27BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 23 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 2.19 Grassy Head Holiday Park Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Grassy Head

Holiday Park

43 15,695 5,137 10,558 $170K $33.09 33%

The occupancy review for the 43 tourist sites indicates the park is preforming at well below industry tourist site occupancy averages at 33% with 5,137 days occupied out of a total of 15,695 possible site hire days. The average revenue per day hired is just below average for industry standards at $33.09/day/tourist site.

2.3.5.4 GH Holiday Park Financial Trends 2011 to 2014 The following table lists the Grassy Head Holiday Park financial trends between 2011 and 2014: Table 2.20 Grassy Head Holiday Park Financial Trends 2011 to 2014

Grassy Head HP 2011/12

(Actual)

2012/13

(Actual)

2013/14

(Actual)

Operating Income $254,945 $264,837 $282,030

Operating Expenditure $221,526* $227,974* $227,478*

Net Operating Profit/(Loss) $33,419 $36,863 $54,552

Capital Expenditure $3,708 $40,398 $15,574

Loan Repayments $0 $0 $0

Note *: Family Holiday Exp. Settlement $3K

Depreciation $27K

Family Holiday Exp. Settlement $9K

Depreciation $26K

Depreciation $33K

The financial review indicates:

Operating income has increased annually from $0.254M in 2011/12 to $0.282M in 2013/14. This was an increase of approx. $28,000 (+11.0%) or an average yearly increase on average of $14,000 (+5.5%).

Operating expenditure has also increased annually from $0.221M in 2011/12 to $0.227M in 2013/14. This was an increase of approx. $6,000 (3.0%) or an average yearly increase on average of $3,000 (+1.5%).

A net operating profit was recorded for each of the three years ranging from $33,000 in 2011/12 and increasing to $54,000 by 2013/14. In 2013/14 the net operating profit saw income as a percentage of expenditure being 123%.

Capital expenditure fluctuated over the three years with a high of $40,398 in 2012/13 and a low of $3,708 in 2011/12.

There was no annual loan repayments recorded for any of the review years at this holiday park.

2.4 Combined MVC Holiday Parks Review

Sections 2.3 provide comparative information on each of the Kempsey Shire Holiday Parks. This section draws this information together into a combined business to provide a guide to key trends to develop future business and management plans from.

2.4.1.1 MVC Combined Holidays Park Cabin and Site Capacities The table on the next page lists the current (2015) MVC Combined Holiday Parks cabin and site capacities.

APPENDIX A Page 28BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 24 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 2.21 MVC Combined Holiday Park Cabin and Site Capacities 2015

Holiday Park Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

Crescent Head

Holiday Park

30 7 189 17 0 0

Hat Head Holiday

Park

10 0 101 49 89 47

Horseshoe Bay

Holiday Park

12 0 83 0 0 0

Stuarts Point Holiday

Park

9 4 69 39 36 0

Grassy Head Holiday

Park

4 0 43 29 24 0

Macleay Valley

Holiday Parks

Total Capacity

65 11 485 134 149 47

The following table compares current cabin and site provision at the MVC Holiday Parks compared to what was identified provided at four of the five parks in 1996/1997 (excluding Horseshoe Bay HP that was not included in the review at that time). Table 2.22 MVC Combined HP Cabin/Site Capacities 1996/97 and 2014/15

Year Cabins Long Term

Sites

Tourist

Sites

Holiday

Van Sites

Camp

Sites

Over Flow Sites

1996/97 27 26 402 145 219 47

2014/15 (excl.) HBHP 53 11 402 134 149 47

2014/15 HBHP 12 0 83 0 0 0

Total Combined Parks

2014/15

65 11 485 134 149 47

Change Between

1996/97 and 2014/15

+38 -15 +83 -9 -70 0

The comparison of the 1997/98 four holiday park capacities indicates that in 2015, with 5 holiday parks, there are 38 more cabins, 15 less long- term sites, 83 more tourist sites, 9 less holiday van sites and 70 less camping sites. This indicates positive change with higher income earning cabin and tourist sites and less long-term low income earning camping, holiday van and long term sites.

2.4.1.2 MVC Combined Holiday Parks Cabin Occupancy 2013/14 The table on the next page lists the MVC Combined Holiday Parks Cabin Occupancy for 2013/14:

APPENDIX A Page 29BMP - KSC CP

15DEC2015

Business Management Plan for KSC Caravan Parks 26-11-2015 (NSW 11.2014) - 7 December 2015 Page 25 Commercial in Confidence. SGL Consulting Group Australia Pty Ltd www.sglgroup.net

Table 2.23 MVC Combined Holiday Parks Cabin Occupancy 2013/14

Holiday Park Cabins Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Crescent Head

Holiday Park

30 10,950 7,785 3,165 $1.141M $146 71%

Hat Head

Holiday Park

10 3,650 2,291 1,359 $266K $116 63%

Horseshoe Bay

Holiday Park

12 4,380 3,181 1,199 $364K $114 73%

Stuarts Point

Holiday Park

9 3,285 1,555 1,730 $156K $100 47%

Grassy Head

Holiday Park

4 1,460 629 831 $52K $83 43%

Total Macleay

Valley Holiday

Parks

65 23,725 15,441 8,284 $1.979M $128 N/A

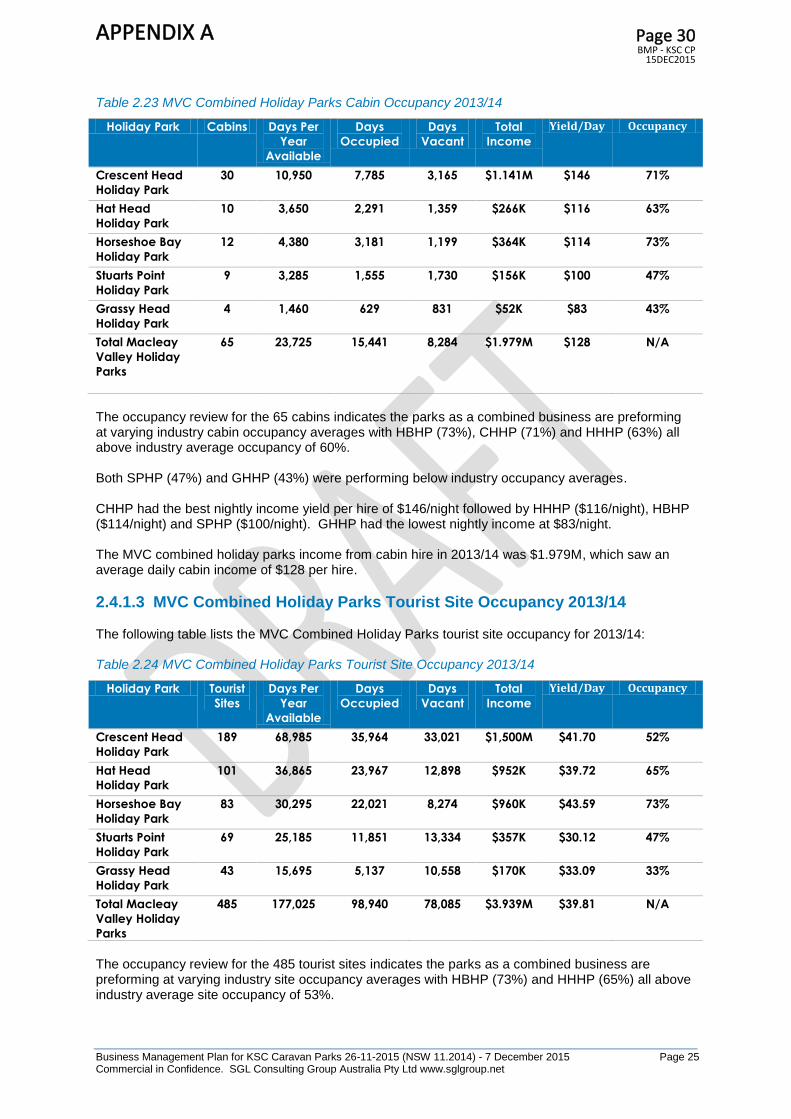

The occupancy review for the 65 cabins indicates the parks as a combined business are preforming at varying industry cabin occupancy averages with HBHP (73%), CHHP (71%) and HHHP (63%) all above industry average occupancy of 60%. Both SPHP (47%) and GHHP (43%) were performing below industry occupancy averages. CHHP had the best nightly income yield per hire of $146/night followed by HHHP ($116/night), HBHP ($114/night) and SPHP ($100/night). GHHP had the lowest nightly income at $83/night. The MVC combined holiday parks income from cabin hire in 2013/14 was $1.979M, which saw an average daily cabin income of $128 per hire.

2.4.1.3 MVC Combined Holiday Parks Tourist Site Occupancy 2013/14 The following table lists the MVC Combined Holiday Parks tourist site occupancy for 2013/14: Table 2.24 MVC Combined Holiday Parks Tourist Site Occupancy 2013/14

Holiday Park Tourist

Sites

Days Per

Year

Available

Days

Occupied

Days

Vacant

Total

Income

Yield/Day Occupancy

Crescent Head

Holiday Park

189 68,985 35,964 33,021 $1,500M $41.70 52%

Hat Head

Holiday Park

101 36,865 23,967 12,898 $952K $39.72 65%

Horseshoe Bay

Holiday Park

83 30,295 22,021 8,274 $960K $43.59 73%

Stuarts Point

Holiday Park

69 25,185 11,851 13,334 $357K $30.12 47%

Grassy Head

Holiday Park

43 15,695 5,137 10,558 $170K $33.09 33%