business partners, financing and the … partners, financing and the commercialization of inventions...

TRANSCRIPT

Business Partners, Financing and the Commercialization of Inventions

Thomas Åstebro, HEC Paris

Carlos J. Serrano University of Toronto and NBER

What is the Role of Business Partners?

• Start-up Founders often advised to from teams – Why?

• Business partners may provide either financing or skills or both

• But the founder has to share equity – Do business partners bring mostly financing or

mostly skills, or both? – Do business partners provide value added with

the skills they bring? – Do they release liquidity constraints?

Some definitions of Business Partners

• Business Partnerships are formally defined in the U.S. tax code as relationships between two or more persons who join to carry on a trade or business, with each person contributing money, property, labor or skill, and each expecting to share in the profits and losses of the business.

• We define business partners as those who join the original inventor to try and commercialize an invention, contributing either human, social, or financial capital to the venture. – Interviews with a few inventors indicated that the

questions most often reflect equity partnerships, and definitely not the decision to hire an employee, or to engage a consultant or other service provider for cash payment.

Selection Predictions

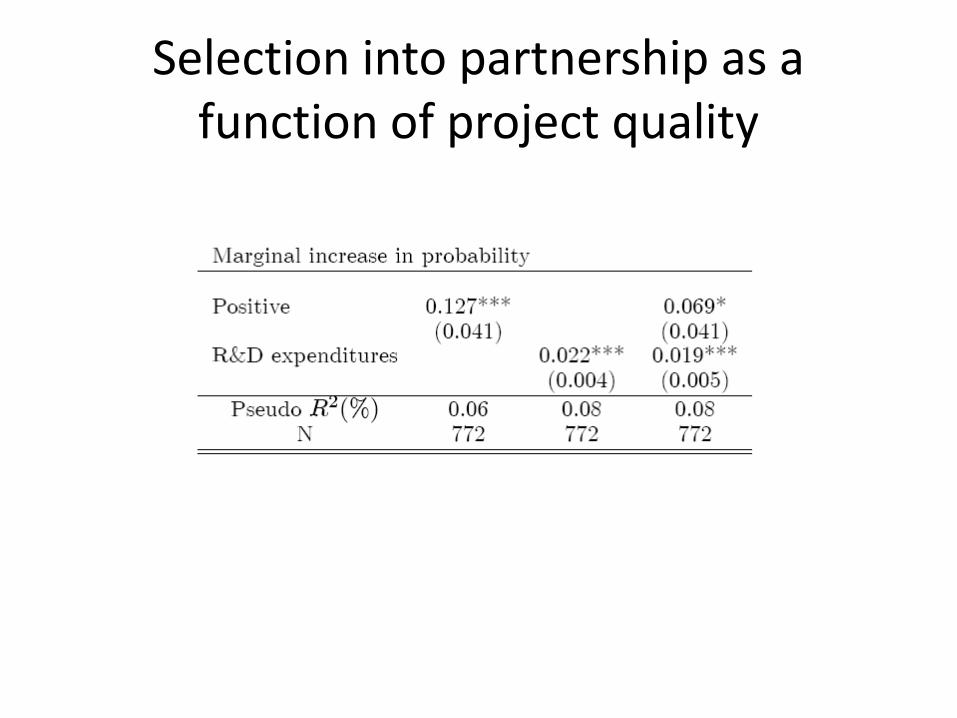

1. Higher project quality increases the probability of partnerships

– High Q allows partners to obtain higher return as compensation for their effort

2. Higher partner ability increases the probability of partnership – Better partners are more attractive to the inventor – There will be selection into partnerships based on partner ability

3. Higher Q implies greater likelihood of being liquidity constrained, inventor thus more likely to seek out partner with money – Implies selection based on demand for financing

• Once controlling for selection one should be able to identify the

marginal effect of human and social capital

Data : Survey of Canadian Inventors

• Inventors self-identified through their use of the services of the Canadian Innovation Center (CIC)

• Telephone survey responses from 772 inventor-invention pairs evaluated by CIC during 1994-2001

• Pre-team research expenditures, pre-team invention quality assessment (CIC), pre-revenue commercialization expenditures by inventor and external financiers, all commercialization revenues

• Partnership dummy; human capital, social capital and financing dummies

• Industry codes, year dummies, inventor characteristics

Selection into partnership as a function of project quality

Value Added Analysis

• Tobit analysis of partnership formation effect on commercialization success Yi*

• Yi* = αQi + βdi + γXi + δj + ηt + εi

Q invention quality di partnership dummy; β captures partner ability X includes financing amounts δ and η industry and year dummies we observe Yi = 0, or Yi = log revenues

Value Added Analysis

• Control for project quality • Control for endogeneity of partnership formation

to commercialization investment • Control for correlation with relaxation of liquidity

constraints • Control for observed inventor and invention

heterogeneity determining probability of partnership

• Analyze effect of unobservables on estimate of value added

Control for Project Quality

Endogeneity of Investment

Effect of Labor Input

Effect of External Financing

Observable inventor characteristics affecting partnership formation

Partnership to develop invention, gender, marital status, age, education, work experience, managerial experience, business experience, family business experience, years experience inventing, number of inventions, Invention stimulated at work, employment status. Positive, R&D, industry, year, fee sponsored.

Effect of unobservables

Interpretation of coefficients

• A partner that exclusively provides financing should not affect revenues in any other way than relaxing liquidity constraints – The estimate for P(no ability, with fin) -- (γ) should

be zero after controlling for the amount of investment

– The estimate for P(with ability) -- (β) should represent the partner’s value added

– If γ is positive (and significant) it therefore must indicate selection on unoberservables

Construct lower bound of value added

• Note that γ is estimated controlling for its covariance with β

• A lower bound of the estimated value added subtracts the effect of unobservables that is correlated with P(with ability, no fin) – Use cov(P(with ability;Q)<cov P(no ability, with fin;Q)

• We obtain βlow = βhat - 0.22*γ • Lower bound effect of value added is

approximately 0.06 increase on p(comm) and 38% increase in revenues at sample mean

Summary

• What is the role of business partners for startups? – Partnerships are five times more likely to be commercialized and

have ten times the commercialization revenues of solo-run projects

– Model shows how selection on quality and demand for financing can jointly arise to explain partnership formation

– Empirically show that there is strong selection on project quality and maybe less on demand for financing

• What is their added value? – Value added of human and social capital may represent

approximately 50% of the total partnership effect – Value added approximately doubles probability of

commercialization and increases expected revenues by 38%

Limitations and Conclusions

• Probably over-emphasize the value added of partners given the setting

• Do not count the number of partners, do not have data on non-realized partners’ skills, nor on skills of realized partners

• Do not examine contracts, teamwork efficiency, or revenue sharing

• For this sample, relaxing liquidity constraints seems the least important, while invention quality and partner value added seem the most important – Methods to produce / screen higher quality inventions useful – Policies to aid entrepreneurs finding business partners useful

extra

The Role of Patents

• Patent

• Commercialization

• Patentability

• Market Opp.

• Techn. Opp.

• Expected Comp.

Astebro, T. And K. Dahlin (2005) Opportunity Knocks, Research Policy, 34: 1404-18.

What is the Role of Business Partners?

• Approximately 10% of all U.S. businesses are partnerships

• 52% of start-ups are partnerships (Ruef et al., 2003)

• Why are there more partnerships for start-ups than on-going businesses? – Are they more likely to fail? – Are they especially valuable during start-up?

• What is their role and economic effects? – How do they help founders?

The Role of Informal VC • Do early-stage financers provide any value added?

– Value added of institutional venture capital hard to determine due to many confounding effects [Hellmann and Puri, 2000; 2002, Hochberg et al. 2007, Puri and Zarutski 2008]

• provide value added (advice, contacts, skills,...)

• reduce liquidity constraints

• screen for quality

– Entrepreneurs pay more for financing from highly reputed VCs suggesting value added [Meggison and Weiss, 1991, Hsu 2004, Sorensen 2008]

– Kerr, Lerner, Schoar,(2010) demonstrate a total positive effect of angel financing on business success using a regression discontinuity approach

• Control for project quality

• Informal venture capital sector becoming more important as formal VCs retract

• 5% of U.S. household are informal venture investors (Bygrave and Reynolds 2006)

Business Partners as Informal Investors

• Business partners may provide either financing or skills or both;

– Do business partners bring mostly financing or mostly skills, or both?

– Do business partners provide value added with the skills they bring?

– Do they release liquidity constraints?

Main Features of Paper

• Focus on inventors' choice between going solo and forming business partnership for invention commercialization

• Model shows selection on invention quality and demand for financing can jointly arise to explain team formation

• Empirically separate selection into partnership from value added of partners

Model Setup

• Entrepreneur-inventors have varying assets Z and hold inventions that vary in quality Q

• Entrepreneur meet potential partner with ability A(β) with positive probability

• Partners can invest $ to relax liquidity constraints and either, or in addition, provide ability to increase the marginal productivity of capital

• Forming a team involves a sunk costs τ • Entrepreneurs trade off the added value of partner

ability and the value of relaxing credit constraints against the cost of forming a partnership

Decision to form partnership

• Value of going solo

• VS = QKα + r(Z-K) – Constrained entrepreneur can borrow (λ-1)Z from

bank and invest up to K< λZ, λ>1, where λZ<=K* • Value of partnership

• VP = A(β)QKα + r(Z-K) – τ – Entrepreneur can borrow from bank and in addition

obtain capital from partner to reach K* – Partner add value by leveraging capital with ability A – A>=1; partners cannot reduce value

Selection Based on Quality and Partner Ability