cb property insights q1 2015

DESCRIPTION

market trendsTRANSCRIPT

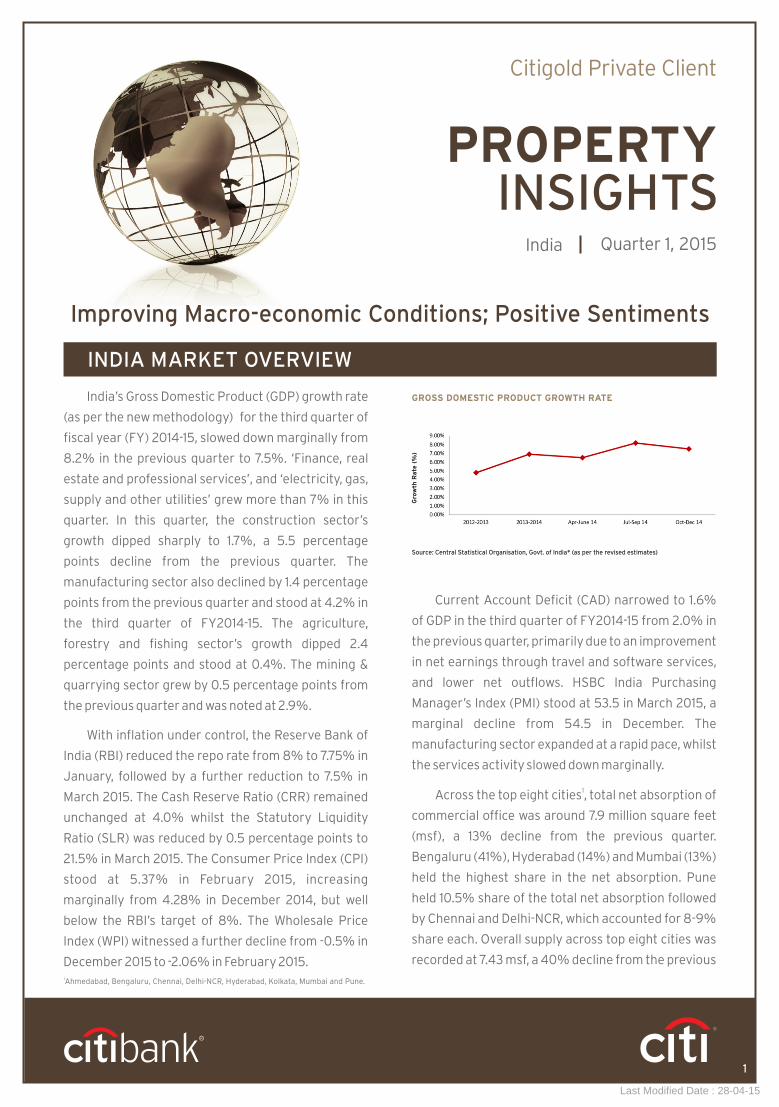

India’s Gross Domestic Product (GDP) growth rate

(as per the new methodology) for the third quarter of

fiscal year (FY) 2014-15, slowed down marginally from

8.2% in the previous quarter to 7.5%. ‘Finance, real

estate and professional services’, and ‘electricity, gas,

supply and other utilities’ grew more than 7% in this

quarter. In this quarter, the construction sector’s

growth dipped sharply to 1.7%, a 5.5 percentage

points decline from the previous quarter. The

manufacturing sector also declined by 1.4 percentage

points from the previous quarter and stood at 4.2% in

the third quarter of FY2014-15. The agriculture,

forestry and fishing sector’s growth dipped 2.4

percentage points and stood at 0.4%. The mining &

quarrying sector grew by 0.5 percentage points from

the previous quarter and was noted at 2.9%.

With inflation under control, the Reserve Bank of

India (RBI) reduced the repo rate from 8% to 7.75% in

January, followed by a further reduction to 7.5% in

March 2015. The Cash Reserve Ratio (CRR) remained

unchanged at 4.0% whilst the Statutory Liquidity

Ratio (SLR) was reduced by 0.5 percentage points to

21.5% in March 2015. The Consumer Price Index (CPI)

stood at 5.37% in February 2015, increasing

marginally from 4.28% in December 2014, but well

below the RBI’s target of 8%. The Wholesale Price

Index (WPI) witnessed a further decline from -0.5% in

December 2015 to -2.06% in February 2015.

Current Account Deficit (CAD) narrowed to 1.6%

of GDP in the third quarter of FY2014-15 from 2.0% in

the previous quarter, primarily due to an improvement

in net earnings through travel and software services,

and lower net outflows. HSBC India Purchasing

Manager’s Index (PMI) stood at 53.5 in March 2015, a

marginal decline from 54.5 in December. The

manufacturing sector expanded at a rapid pace, whilst

the services activity slowed down marginally.

1Across the top eight cities , total net absorption of

commercial office was around 7.9 million square feet

(msf), a 13% decline from the previous quarter.

Bengaluru (41%), Hyderabad (14%) and Mumbai (13%)

held the highest share in the net absorption. Pune

held 10.5% share of the total net absorption followed

by Chennai and Delhi-NCR, which accounted for 8-9%

share each. Overall supply across top eight cities was

recorded at 7.43 msf, a 40% decline from the previous

INDIA MARKET OVERVIEW

Citigold Private Client

PROPERTY INSIGHTS

India Quarter 1, 2015

Improving Macro-economic Conditions; Positive Sentiments

1

GROSS DOMESTIC PRODUCT GROWTH RATE

Gro

wth

Rate

(%

)

Source: Central Statistical Organisation, Govt. of India* (as per the revised estimates)

1Ahmedabad, Bengaluru, Chennai, Delhi-NCR, Hyderabad, Kolkata, Mumbai and Pune.

Last Modified Date : 28-04-15

quarter. Due to healthy leasing, the overall vacancy

levels across these eight cities dropped by 0.5

percentage points from the previous quarter, and was

noted at 18.3% in the first quarter of 2015.

In the retail sector, across the top eight cities, only

Bengaluru witnessed new mall supply of 0.2 msf. A few

malls have deferred their completion timelines due to

construction delays and in some cases, due to delay in

obtaining required approvals. In the wake of low new

supply, the overall mall vacancies across the top eight

cities remained largely stable at 14.7%

In the residential sector, approximately 24,600

units were launched across the top eight cities in this

quarter, a 21% decline from the previous quarter.

Bengaluru had a major share of these unit launches at

17%, closely followed by Mumbai contributing 16% to

the total unit launches. Capital values remained

largely stable in both high-end and mid segment units

of five cities including Ahmedabad, Delhi-NCR, Mumbai,

Kolkata and Pune, primarily due to existing high unsold

inventory. Bengaluru and Chennai witnessed a 5-7%

capital value appreciation in the mid segment due to an

increase in demand. In Hyderabad, limited availability in

the high-end segment resulted in 3-6% capital value

appreciation in select submarkets. With downward

revision of repo rates and reduction in home loan

interest rates, housing demand is likely to increase in

the coming quarters.

The Consumer Price Index (CPI) increased

marginally from 5.19% in January to 5.37% in

February 2015, however the inflation largely seemed

to be under control. In order to revive the economic

growth, the RBI reduced its benchmark lending rate -

the repo rate - twice (0.50 basis points in total) in the

first quarter of 2015, to 7.5%. The Cash Reserve

Ratio (CRR) remained unchanged at 4.0%. However,

the Statutory Liquidity Ratio (SLR) was reduced by

0.5 percentage point from December 2014 to 22.5%

in March 2015. The Wholesale Price Index (WPI) continued to

witness a decline for the last four months, and was

noted at -2.06% in February 2015 from -0.5% in

December 2015, due to a decline in the prices of food

products, manufactured goods, fuel and power. In

February 2015, food inflation was noted at 7.74%.

Although this was a marginal decline from January, it

registered a 2.79 percentage points increase from

December 2014. The fuel and power inflation stood at -

14.72% a further decline from -7.82% recorded in

December. Inflation for manufactured goods dropped

by 1.11 percentage points to 0.33% in February 2015.

Economic Trends

Trends & Updates

2

EXCHANGE RATE MOVEMENT (INR/USD)

Source: RBI

INR

/US

D

FDI INFLOW IN HOUSING AND REAL ESTATE SECTOR

INR

Cro

re

Source: Dept. of Industrial Policy & Promotion, Govt, of India

Last Modified Date : 28-04-15

India’s GDP is projected to attain 7.4% growth at

the end of FY2014-15. With the government’s agenda

to boost infrastructure investments, and improve

the business environment, private investments are

anticipated to increase in the future periods. This quarter witnessed an improvement in the

Indian Rupee from INR 63.6 in December 2014 to INR

62.5 in March 2015, as against the US Dollar. The

rupee strengthened in this quarter primarily due to

increased inflows from Foreign Institutional

Investors (FIIs).

The total FDI inflows in India were INR 155,489

crore during April 2014 – January 2015, of which

2.8% came in the construction development sector

(comprising townships, housing, bui lt-up

infrastructure), which was around INR 4,359 crores.

FDI doubled in January 2015 in comparison to the

same month last year, making it the highest inflow in

the past 29 months.

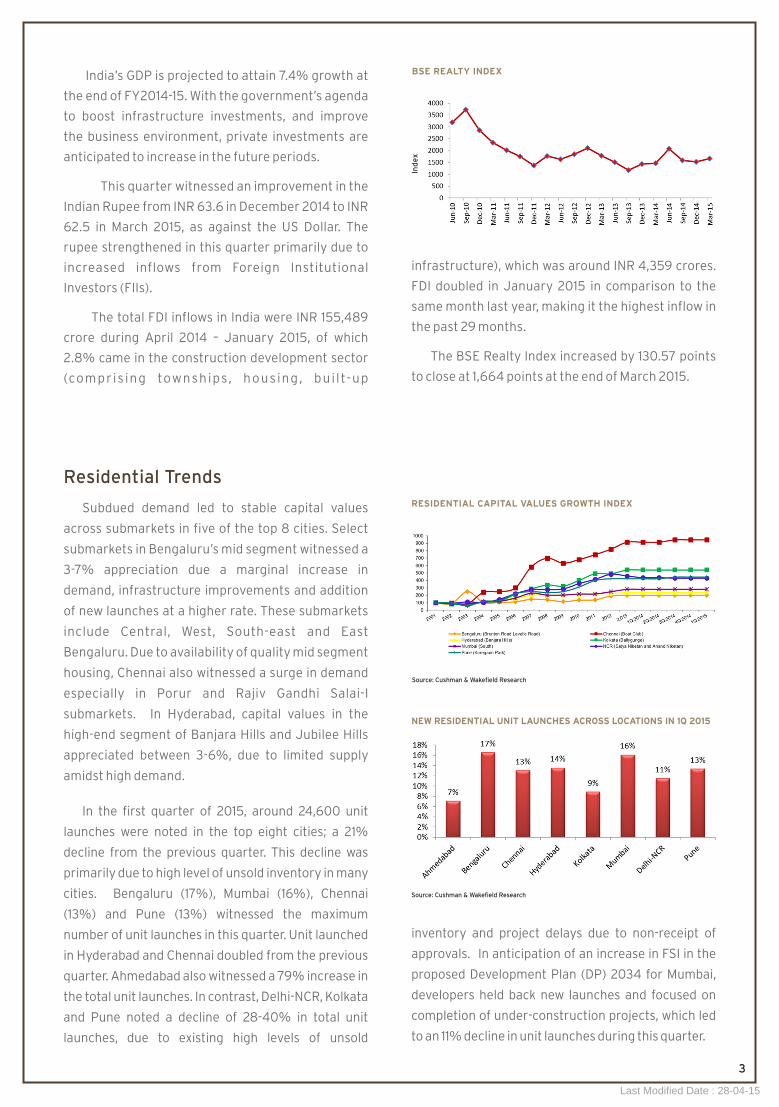

The BSE Realty Index increased by 130.57 points

to close at 1,664 points at the end of March 2015.

3

Subdued demand led to stable capital values

across submarkets in five of the top 8 cities. Select

submarkets in Bengaluru’s mid segment witnessed a

3-7% appreciation due a marginal increase in

demand, infrastructure improvements and addition

of new launches at a higher rate. These submarkets

include Central, West, South-east and East

Bengaluru. Due to availability of quality mid segment

housing, Chennai also witnessed a surge in demand

especially in Porur and Rajiv Gandhi Salai-I

submarkets. In Hyderabad, capital values in the

high-end segment of Banjara Hills and Jubilee Hills

appreciated between 3-6%, due to limited supply

amidst high demand.

In the first quarter of 2015, around 24,600 unit

launches were noted in the top eight cities; a 21%

decline from the previous quarter. This decline was

primarily due to high level of unsold inventory in many

cities. Bengaluru (17%), Mumbai (16%), Chennai

(13%) and Pune (13%) witnessed the maximum

number of unit launches in this quarter. Unit launched

in Hyderabad and Chennai doubled from the previous

quarter. Ahmedabad also witnessed a 79% increase in

the total unit launches. In contrast, Delhi-NCR, Kolkata

and Pune noted a decline of 28-40% in total unit

launches, due to existing high levels of unsold

inventory and project delays due to non-receipt of

approvals. In anticipation of an increase in FSI in the

proposed Development Plan (DP) 2034 for Mumbai,

developers held back new launches and focused on

completion of under-construction projects, which led

to an 11% decline in unit launches during this quarter.

Residential Trends

BSE REALTY INDEX

Ind

ex

RESIDENTIAL CAPITAL VALUES GROWTH INDEX

Source: Cushman & Wakefield Research

NEW RESIDENTIAL UNIT LAUNCHES ACROSS LOCATIONS IN 1Q 2015

Source: Cushman & Wakefield Research

Last Modified Date : 28-04-15

4

Index

Ahmedabad................................................................................... 5

Bengaluru...................................................................................... 8

Chandigarh.................................................................................... 12

Chennai.......................................................................................... 14

Delhi - National Capital Region (NCR) .................................... 19

Jaipur ............................................................................................ 27

Hyderabad..................................................................................... 23

Kolkata.......................................................................................... 30

Mumbai........................................................................................... 35

Pune............................................................................................... 39

Last Modified Date : 28-04-15

Ahmedabad

Market Overview

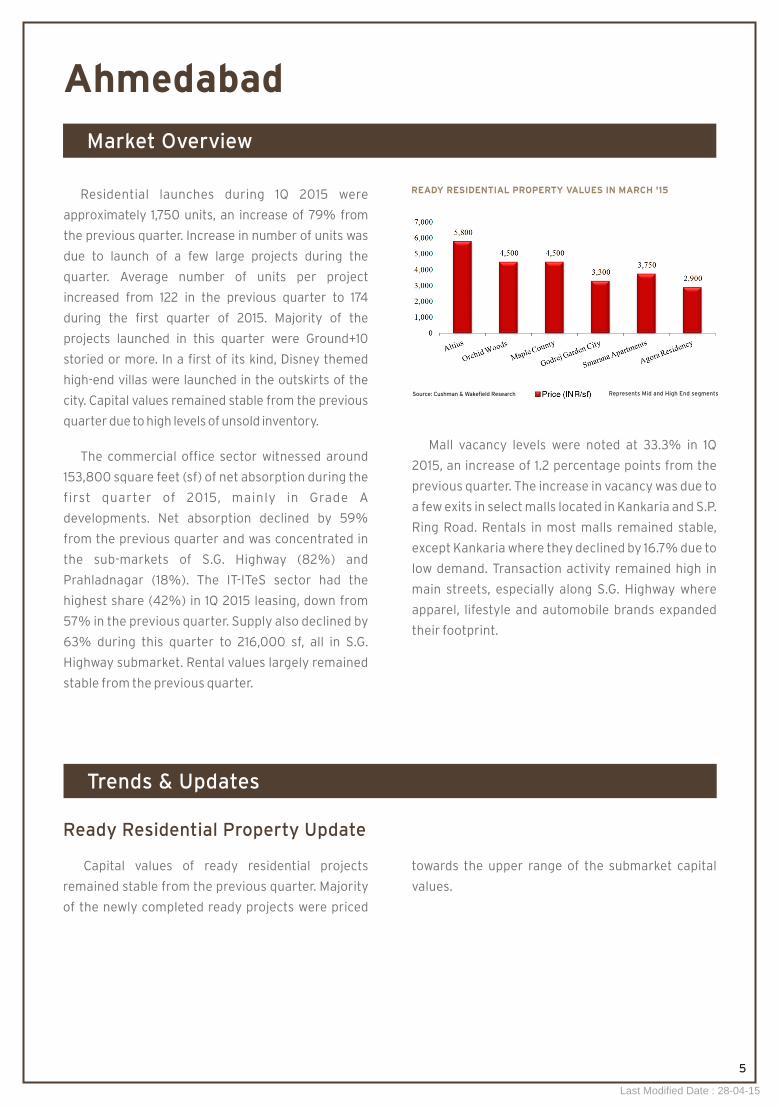

Residential launches during 1Q 2015 were

approximately 1,750 units, an increase of 79% from

the previous quarter. Increase in number of units was

due to launch of a few large projects during the

quarter. Average number of units per project

increased from 122 in the previous quarter to 174

during the first quarter of 2015. Majority of the

projects launched in this quarter were Ground+10

storied or more. In a first of its kind, Disney themed

high-end villas were launched in the outskirts of the

city. Capital values remained stable from the previous

quarter due to high levels of unsold inventory.

The commercial office sector witnessed around

153,800 square feet (sf) of net absorption during the

first quarter of 2015, mainly in Grade A

developments. Net absorption declined by 59%

from the previous quarter and was concentrated in

the sub-markets of S.G. Highway (82%) and

Prahladnagar (18%). The IT-ITeS sector had the

highest share (42%) in 1Q 2015 leasing, down from

57% in the previous quarter. Supply also declined by

63% during this quarter to 216,000 sf, all in S.G.

Highway submarket. Rental values largely remained

stable from the previous quarter.

Mall vacancy levels were noted at 33.3% in 1Q

2015, an increase of 1.2 percentage points from the

previous quarter. The increase in vacancy was due to

a few exits in select malls located in Kankaria and S.P.

Ring Road. Rentals in most malls remained stable,

except Kankaria where they declined by 16.7% due to

low demand. Transaction activity remained high in

main streets, especially along S.G. Highway where

apparel, lifestyle and automobile brands expanded

their footprint.

Capital values of ready residential projects

remained stable from the previous quarter. Majority

of the newly completed ready projects were priced

Trends & Updates

Ready Residential Property Update

towards the upper range of the submarket capital

values.

5

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

Last Modified Date : 28-04-15

New unit launches declined by 79% from the

previous quarter and around 1,750 units were

launched in 1Q 2015. Average project size also

increased from 122 units in the previous quarter to

174 units in this quarter. Around 65% of units

launched in this quarter catered to the mid segment

New Residential Launches

whilst 33% to the high-end segment. Western

peripheral locations such as Bopal, South Bopal and

Ambli dominated the launch activity with a 47%

share. 3 BHK configurations had the maximum

contribution to new launches with a 43% share

followed by 2 BHKs (28%) and 4 BHKs (22%).

Average Capital Values – High-end Segment (INR '000/sf)

Satellite

Vastrapur

S.G.Highway

Prahlad Nagar

Location

4.0 - 4.8

3.7 - 4.0

3.7 - 4.3

4.2 - 5.3

2010

4.3 - 6.0

3.7 - 5.0

3.7 - 4.5

4.2 - 6.0

2011

4.3 - 6.0

3.7 - 5.0

3.7 - 4.5

4.2 - 6.0

2012

4.3 - 6.0

3.7 - 5.0

3.7 - 4.5

4.2 - 6.2

2013

4.3 - 6.0

3.7 - 5.0

3.7 - 5.0

4.2 - 6.2

1Q 2015

4.3 - 6.0

3.7 - 5.0

3.7 - 5.0

4.2 - 6.2

2014

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 2,000-4,000 sf

Average Capital Values – Mid Segment (INR ‘000/sf)

#Satellite

Vastrapur#

S.G.Highway

Prahlad Nagar

Location

Project Name Developer Location Number of Units* Type Area of Units (sf)

Aaryan Gloria 560 Apartments 2 BHK: 999 to 1,4353 BHK:1,440

Aaryan Builders Bopal

Upland Villas 280 Villas 4 BHK: 2,925 to 3,8705 BHK: 4,950 to 6,0756 BHK: 9,900

Arvind

Infrastructure

Nasmed

Gala Eternia 216 Apartments 3 BHK: 1,385 to 1,745Gala

Infrastructure

Thaltej

Savvy Swaraaj 208 Apartments 2.5 BHK: 1,3803 BHK: 1,730

Savvy

Infrastructure

S.G. Highway

Binori Grandeur 152 Apartments 4 BHK: 2,995Binori Buildcon Ambli

Binori Gracia 102 Apartments 3 BHK: 1,435Binori Buildcon South Bopal

Binori Mable 52 Apartments 3 BHK: 1,965Binori Buildcon Prahladnagar

Dev Atelier 50 Apartments 3 BHK: 2,164Dev Group Prahladnagar

Setu Scarlet 36 Apartments 3 BHK: 2,070Setu Infracon Motera

Indraprasth Kadamb 42 Apartments 4 BHK: 3,000Deep Group,

Vedant Developers

Prahladnagar

Sepal Elegant 2 42 Apartments 1 BHK: 7562 BHK: 1,008 to 1,026

Swetalee

Developers

& Sepal Buildcon

Chandkheda

2.8 - 3.8

2.6 - 3.5

3.0 - 3.8

2.8 - 3.6

2010

2.8 - 4.3

2.6 - 3.8

3.3 - 4.3

3.2 - 4.2

2011

2.8 - 4.3

2.6 - 3.8

3.3 - 4.3

3.2 - 4.2

2012

2.8 - 4.3

2.6 - 3.9

3.0 - 4.3

3.2 - 4.3

2013

2.8 - 4.3

2.6 - 3.9

3.0 - 4.3

3.2 - 4.3

1Q 2015

2.8 - 4.3

2.6 - 3.9

3.0 - 4.3

3.2 - 4.3

2014

Source: Cushman and Wakefield Research

Note: The above values for mid segment typically include units of 1,200-1,800 sf#Limited availability at quoted values

6

Last Modified Date : 28-04-15

Commercial Office Sector

Ahmedabad witnessed 242,000 sf of supply

during this quarter, primarily in the S.G. Highway

sub-market. Leasing of 153,800 sf was noted during

the quarter with the IT-ITeS sector having the

highest share at 42%, followed by the chemicals

sector at 34%. Transaction activity in the form of

outright purchases by local traders was also

prominent during the quarter. Continued

transaction activity led to a quarterly decline in

Grade A vacancy levels by 1.7 percentage points and

was noted at 33.4%. Rental values remained stable

from the previous quarter.

7

Retail Sector

Low transaction activity led to an increase in mall

vacancy levels, which were noted at 33.3% in 1Q

2015. Lack of quality spaces and upkeep in certain

malls led to a few exits. Rentals remained stable from

the previous quarter across malls and main streets.

However, enquiries for prime main streets increased

due to which transaction activity may improve in the

coming year. Quick Service Restaurants (QSRs) such

as Starbucks and Burger King are looking to open

their first stores in the city whilst Dunkin Donuts

opened its first store in the city during this quarter.

Outlook

Residential launches in the upcoming quarter are

likely to remain at par with 1Q 2015, considering the

high levels of unsold inventory. Capital values are

also likely to remain stable across submarkets in the

upcoming quarter.

110,000 sf of office supply is expected to become

operational in Prahladnagar during the next quarter.

Although the under construction pipeline has

declined, high vacancy levels due to subdued

demand may lead to a downward pressure on rental

values in the upcoming quarter.

Mall rentals in the S.G. Highway sub-market may

decline in the upcoming quarter due to persistently

high vacancy levels. However, rentals in Vastrapur

may appreciated due to healthy demand and low

vacancy levels. Rentals in the main streets of C.G.

Road and Prahladnagar may appreciate, considering

the high levels of enquiries from F&B and lifestyle

brands. Rentals are likely to remain stable in all other

main streets in the next quarter.

Under Construction Residential Property Update

Peripheral locations along S.G. Highway and Bopal

and areas in north Ahmedabad such as Chandkheda,

Motera, etc. witnessed significant construction

activity during the quarter. Capital values across most

submarkets remained stable from the previous

quarter.

Last Modified Date : 28-04-15

Bengaluru

Market Overview

Ready Residential Property Update

Trends & Updates

Capital values improved in select submarkets from

the previous quarter. Mid segment rentals in the Central

and the Western quadrant appreciated by 7% from the

previous quarter. Whilst limited supply amidst launches

at a higher rate prompted an increase in the Central

submarket, enhanced metro connectivity and

developing social infrastructure caused a demand spur

in the Western submarket. Capital values of high-end

segment of the North submarket; and mid segment of

the South-east and East submarket also appreciated by

3-7%, due to sustained end-user demand. Rental values

across all submarkets remained stable from the

previous quarter.

About 4,000 units were launched in the first

quarter of 2015, a 28% decline from the previous

quarter. Mid segment dominated with about 91%

share of the total unit launches. Maximum unit

launches were in South-east submarket (41%),

followed by the North Submarket (25%). Strong-end

user demand, especially from IT-ITeS working

professionals and ease of connectivity to various

parts of the city drove new launches in these

submarket.

In the first quarter of 2015, approximately 1.96

msf supply was added. Whilst new supply was less

than half the previous quarter’s addition, leasing

remained strong at 3.89 msf. New supply comprised

only of Grade A developments, of which 42% came

in the Suburban South submarket, followed by 35%

in the Outer Ring Road submarket. In this quarter, IT-

SEZ developments accounted for more than half

(52%) of the total supply.

In the retail sector, a new mall supply of 200,000

sf in Tumkur Road was added in this quarter. The

overall mall vacancy dipped by 0.6 percentage

points and was recorded at 8.8%, due to healthy

leasing along Thanisandra Road and Tumkur Road.

Malls and main street rentals largely remained

stable from the previous quarter.

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

8

Last Modified Date : 28-04-15

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 2,000-4,000 sf.

Location

Central

South

Off-Central

East

North

Average Capital Values – High-end Segment (INR’000/sf)

2009

12.0 - 14.5

6.0 - 8.5

5.0 - 6.8

5.6 - 7.0

5.5 - 7.0

2010

13.5 - 17.5

6.0 - 9.5

5.0 - 7.0

6.5 - 7.5

5.5 - 7.0

2011

14.0 - 18.0

6.5 - 10.0

6.0 - 8.5

6.8 - 8.0

6.5 - 8.0

2012

18.0 - 28.0

6.5 - 10.0

7.0 - 9.0

6.5 - 9.0

6.5 - 8.2

1Q 2015

18.0 - 30.0

7.0 - 10.5

8.0 - 11.0

6.5 - 10.0

7.0 - 11.0

2014

18.0 - 30.0

7.0 - 10.3

8.0 - 11.0

6.5 - 10.0

7.0 - 9.8

2013

18.0 - 30.0

6.8 - 10.3

8.0 - 11.0

6.5 - 10.0

7.0 - 9.5

2008

14.0 - 18.0

7.0 - 9.0

6.5 - 7.5

6.5 - 9.0

6.0 - 8.0

Key to locations:

High-end Segment

Central: Lavelle Road, Off Palace Road, Off Cunnigham

Road, Ulsoor Road, Richmond Road

South: Koramangala, Outer Ring Road, Bannerghatta

Road, JP Nagar

Off-Central: Frazer Town, Benson Town, Richards Town,

Dollars Colony

East: Whitefield (villas)

North: Hebbal, Yelahanka, Jakkur, Devanahalli

Mid Segment

Central: Brunton Road, Artillery Road, Ali Askar Road,

Cunningham Road

East: Marathalli, Whitefield, Old Airport Road

South-East: Sarjapur Road, Outer Ring Road, HSR

Layout

South: Kormangala, Jakkasandra

South-West: Jayanagar, J P Nagar, Kanakpura Road,

Bannerghatta Road, BTM Layout

North: Hebbal, Bellary Road, Yelahanka, Dodballapur

Road, Jalahalli

Off-Central*: Vasanth Nagar, Richmond Town and

Indiranagar

Off-Central**: Cox Town, Frazer Town, HRBR, Benson

Town, etc.

North-West: Malleshwaram, Rajajinagar

9

Source: Cushman and Wakefield Research

Note: The above values for mid segment typically include units of 1,600-2,000 sf.

Average Capital Values – (INR’000/sf)Mid Segment

Location

Central

East

South-East

North

South-West

Off-Central*

Off-Central**

North-West

South

2008

5.8 - 7.0

2.7 - 3.1

2.9 - 4.0

5.0 - 6.5

2.8 - 4.2

3.5 - 6.0

4.0 - 6.0

4.2 - 5.8

3.0 - 4.0

2009

5.0 - 6.0

2.4 - 2.7

2.5 - 3.2

2.8 - 4.0

2.7 - 3.9

3.3 - 5.7

3.7 - 5.7

3.5 - 5.2

4.6 - 5.7

2010

5.5 - 7.0

2.7 - 3.1

2.8 - 4.0

2.8 - 4.4

3.2 - 4.5

4.0 - 6.2

3.8 - 6.2

3.8 - 5.6

4.8 - 6.0

2011

6.0 - 7.5

3.2 - 3.8

3.4 - 5.0

3.0 - 4.8

3.6 - 5.0

4.5 - 6.7

4.3 - 6.7

4.3 - 6.2

5.0 - 6.5

2012

6.0 - 8.0

3.8 - 4.8

4.0 - 5.5

6.0 - 9.0

4.0 - 5.5

5.0 - 7.5

5.0 - 7.0

4.5 - 6.5

3.5 - 5.5

2013

9.0 - 12.0

4.0 - 5.5

4.5 - 5.9

4.5 - 6.5

7.0 - 10.0

6.0 - 8.0

5.5 - 6.5

3.5 - 5.5

6.0 - 9.0

2014

9.0 - 12.0

4.0 - 5.5

4.5 - 6.0

4.5 - 6.5

7.0 - 10.0

6.5 - 8.5

6.0 - 6.8

4.0 - 5.5

6.0 - 9.0

1Q 2015

9.5 - 13.0

4.3 - 5.7

4.5 - 6.3

4.5 - 6.5

7.0 - 10.0

6.5 - 8.5

6.0 - 6.8

4.0 - 6.5

7.0 - 10.0

Last Modified Date : 28-04-15

New Residential Launches

In the first quarter of 2015, approximately 4,000

units were launched, of which 76% were from units

pre-launched in the previous quarters. Whilst total

unit launches declined by 28% from the previous

quarter, mid segment’s share remained strong at

91%. 41% of total unit launches came in Sarjapur and

Hosur Road in the South-east submarket.

Additionally, 25% of the unit launches came in

Yelahanka and Kogilu areas in the North submarket.

Several villa plot launches were also noted in this

quarter, especially in Southern and Northern

quadrants of the city.

Location Number of Units* Type Area of Units (in sf)Project Name Developer

Sobha Silicon Oasis Sobha Developers Hosur Road 918 Apartments 2 BHK: 1,3503 BHK: 1,675

Brigade Northridge Brigade Group Kogilu Main Road 600 Apartments 2 BHK: 1,2503 BHK: 2,000

SNN Raj Etternia SNN Builders Haralur Road 576 Apartments 1 BHK: 5602 BHK: 1,2703 BHK: 1,670

The Tree Provident Housing Off Magadi Road 560 Apartments 1 BHK: 6052 BHK: 1,0003 BHK: 1,256

Salarpuria SattvaLaurel Heights

Salarpuria SattvaGroup

Tumkur Road 438 Apartments 2 BHK: 9922.5 BHK: 1,2403 BHK: 1,416

Edge Waters Bren Corporation Sarjapur Road 191 Apartments 2 BHK: 1,0403 BHK: 1,418

Shrinikethan RNS InfrastructuresLimited

Yeshwantpur 186 Apartments 3 BHK: 3,0504 BHK: 3,390

RMZ Azure RMZ Bellary Road 182 Apartments 2 BHK: 1,6023 BHK: 2,100

After the rain Total Environment Yelahanka 127 Villas 4 BHK: 3,090

Green Aspire Tetra Grand Off ThanisandraRoad

120 Apartments 2 BHK: 8663 BHK: 1,453

ATZ Estrella ATZ Properties Varthur Road 110 Apartments 2 BHK: 1,3023 BHK: 1,780

The Urban Forest Alchemy Real Estate Whitefield 75 Apartments 2 BHK: 1,3143 BHK: 1,826

10

* Estimated and as per market information

Under Construction Residential Property Update

Around 168,000 residential units are under

construction across various submarkets, with mid

segment accounting for about 56%, followed by 26

% in the affordable segment. Capital values of under

construction residential projects remained mostly

stable from the previous quarter. A few projects

nearing completion include Vaswani Reserve in

Marathahalli, Sunrise Towers in Whitefield and HM

Grandeur in Frazer Town.

Last Modified Date : 28-04-15

11

Retail Sector

Rentals remained stable from the previous

quarter in malls as well as main streets of most sub-

markets. During this quarter, a few F&B, electronics,

footwear and apparel retailers leased spaces in malls

located along Thanisandra Road and Tumkur Road.

In the main streets, Brigade Road rentals dipped by

3.2% from the previous quarter due to a preferential

shift of the tenants towards other locations such as

Indiranagar and Koramangala. Benefitting from the

spill over demand from nearby saturated locations,

Koramangala 80 Feet Road witnessed a 4.3% rental

appreciation from the previous quarter.

Commercial Office Sector

Net absorption of around 3.3 msf was recorded in

Grade A developments during the first quarter of

2015; a 7% increase from the previous quarter.

Leasing of 3.89 msf was noted in this quarter, 33% of

which was in the Outer Ring Road submarket. IT-ITeS

sector dominated leasing and had a 68% in the total

transactions. Further, pre-commitments of

approximately 0.85 msf were noted in this quarter.

Office rentals also appreciated in select submarkets.

Sustained demand and limited availability of quality

spaces resulted in Grade A weighted average rental

appreciation along the Outer Ring Road, Peripheral

East and Peripheral North submarkets by 6.7%, 4.2%

and 6.0% respectively. In contrast to these, the

Suburban South and Suburban East submarkets

witnessed a decline of 4.4% and 9.3% respectively.

Whilst rental correction in a few buildings caused this

dip in the Suburban South, low demand led to a decline

in the Suburban East. Overall Grade A vacancy levels

decreased by 1.6 percentage points due to healthy

transactions and was noted at 8.0%.

Given the significantly high number of pre-

launches (around 13,000), residential unit launches

in the subsequent quarters are expected to be

strong. Rental and Capital values are likely to hold

steady as the existing supply presently exceeds the

demand.

Around 7.3 msf of office space supply is expected

to be added in the next quarter, most of which is

likely to be in Grade A developments. Given the

strong demand, transaction activity may remain

high in the upcoming quarters. Rentals may

Outlook

appreciate in select submarkets such as the Outer

Ring Road and Peripheral East due to a sustained

demand.

Rentals in most malls and main streets are likely

to remain stable in the next quarter. New BEL Road

and Kamanahalli Main Road are fetching increased

enquiries from international brands, amidst limited

space availability. However, rentals are expected to

gain traction in the coming quarters.

Last Modified Date : 28-04-15

Market Overview

Chandigarh

In the first quarter of 2015, approximately 700

units were launched in the Tri-City region. New

launches were primarily in the outskirts in

submarkets of Zirakpur, Mullanpur and Mohali. The

high-end segment witnessed improvement in

transaction activity during the quarter; however, the

capital values remained stable from the previous

quarter. Capital values in the mid segment too

remained stable across submarkets. With improved

connectivity to Mullanpur, this submarket witnessed

an increased interest from the homebuyers.

Approximately 650,000 sf of office space was

added to the Tri-City during the first quarter of 2015,

primarily in Mohali. Demand for office space

improved during the quarter with significant space

take-up from companies in BFSI, construction and

automobile sectors. Grade A office rentals softened

during the quarter, as investors agreed to lease out

their spaces at lower rentals considering the

prevailing subdued demand conditions.

No new mall space was added to the Tri-City

region in the first quarter of 2015. Vacancy levels

during the quarter declined as retailers of

accessories and apparels took up space across the

region. Demand continued to be tepid in the main

streets. Rentals remained stable for both malls and

main streets across Chandigarh

Trends & Updates

Capital values remained stable across all locations,

from the previous quarter. Transaction activity in the

high-end segment improved during the quarter with

availability of good deals at competitive prices. Capital

values in Mohali and Zirakpur hardened during the

quarter with continued interest from end-users but

remained stable amidst reduced investor demand.

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

12

Ready Residential Property Update

Last Modified Date : 28-04-15

Location

Chandigarh Sector: 2-11

Chandigarh Sector: 28

Panchkula

Manimajra

4Q 2013

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

1Q 2014

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

1Q 2015

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

4Q 2014

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

3Q 2014

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

2Q 2014

155,000 - 170,000/sqyd

140,000 - 160,000/sqyd

110,000 - 145,000/sqyd

14,000/sf

Average Capital Values – High-end Segment (INR)

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 2,000-4,000 sf, both apartments and villa *sqyd: Square Yard

Mid Segment:

Mohali: Sectors - 114, 115, 127

Panchkula: Sector - 20

High-end Segment:

Panchkula: Sectors - 2, 4, 6, 7, 8, 9, 15

Key to Locations:

Location

Zirakpur

Mohali

Dera Bassi

Panchkula

4Q 2013

2,800 - 3,600

3,200 - 4,000

3,000 - 3,200

2,800 - 3,500

1Q 2014

2,800 - 3,400

3,000 - 3,800

2,800 - 3,200

2,800 - 3,400

1Q 2015

2,800 - 3,600

3,200 - 4,200

2,700 - 3,500

2,900 - 3,500

4Q 2014

2,800 - 3,600

3,200 - 4,200

2,700 - 3,500

2,900 - 3,500

3Q 2014

2,800 - 3,500

3,200 - 4,000

2,800 - 3,500

2,900 - 3,500

2Q 2014

2,800 - 3,400

3,200 - 3,800

2,800 - 3,400

2,800 - 3,400

Average Capital Values – Mid Segment (INR/sf )

Source: Cushman and Wakefield Research

Note: The above values for mid segment apartments typically include units of 1,600-2,000 sf

The Tri-City region witnessed launch of around

700 units in the first quarter of 2015. With basic prices

in the range of INR 3,200-5,000/sf, new launches were

primarily in the northern and southern regions such

as Mullanpur, Zirakpur and Mohali.

New Residential Launches

Project Name Developer Location Number of Units* Type Area of Units (sf)

GBP Centrum 300 IndependentFloors

1 BHK: 475 to 491GBP Builders Zirakpur

Central Greens 280 Apartments 3 BHK: 1,460Preet Land Promoters and Developers

Sector 86, Mohali

Celestia Grand 60 IndependentFloors

3 BHK: 1,415Omaxe Mullanpur

Golden Oak SanskritiHomes

54 Apartments 3 BHK: 2,000Golden OakEstates

Mullanpur

13

Last Modified Date : 28-04-15

Commercial Office Sector

In 1Q 2015, BFSI, construction and automobile

sector companies had a major share in office space

take-up. Quoted rentals of IT Parks and SEZs were

around INR 50-60/sf/month and commercial spaces

were at INR 70-95/sf/month.

In 1Q 2015, capital values of under construction

projects increased by 2-3% across locations in

Mullanpur as developers revised basic selling prices

due to improved infrastructure in the region.

Approximately 450 units across several projects in

Zirakpur, Panchkula and Mohali are expected to be

ready for possession in the next quarter.

Under Construction Residential Property Update

The first quarter of 2015 witnessed retailer activity

primarily from accessories’ brands in mall locations

across the Tri-City region with brands such as Da

Milano and Inglot taking up spaces. Demand in main

street locations remained tepid during the quarter

Retail Sector

with footwear and apparel retailers such as Geox and

Levis taking up space in prominent locations. Rentals

across malls and main street locations remained

stable from the previous quarter.

Capital values are likely to remain stable in the

high-end segment despite improvement in

transaction activity, considering that there exists

significant unsold inventory. New launch activity is

likely to pick up in the northern submarket of

Mullanpur. Panchkula is expected to witness

softening of mid segment capital values due to

significant availability of ready to move projects.

No new office supply is likely to be added in the

next quarter. Demand may remain moderate and

Outlook

rentals are expected to remain stable over the next

quarter, considering the prevailing high vacancies.

Approximately 350,000 sf of mall space is

scheduled for completion in the second quarter of

2015, which is likely to increase vacancy levels in

Mohali submarket. Mall rentals are likely to remain

stable in Chandigarh city whilst they may soften

marginally in the peripheral submarkets.

14

Last Modified Date : 28-04-15

Chennai

Market Overview

During the first quarter of 2015, new residential

unit launches were nearly double the previous

quarter, and stood at 3,200 units. In the festival

season during this quarter, developers launched new

projects. Developers continued to focus on the mid

segment as is evident by the same accounting for

more than 96% of the total unit launches during the

quarter. Due to proximity to IT and manufacturing

hubs, Suburban (South) (32%) and Grand Southern

Trunk (GST) Road (27%) accounted for a major share

of new launches in the quarter. The high-end

segment had a 3% share in the total launches, most

of which was concentrated in Nungambakkam and

Off-Central I.

With only 75,400 sf office space becoming

operational during this quarter, Chennai witnessed

pre-commitments of nearly 547,000 sf from

occupiers looking to commence operations in

premium Grade A spaces in IT parks or IT-SEZs. Whilst

the entire new supply comprised of commercial

spaces, Grade A developments had a 27% share, all of

which was added in South-west. Driven by robust

occupier demand, gross absorption stood at 1.3 msf, of

which 62% was in Grade A developments. Strong

demand led to a 1.2 percentage points dip in Grade A

vacancy levels, which stood at 14.5% at the end of

this quarter.

Chennai did not witness any new mall supply

addition for the fifth consecutive quarter and

completion timelines for more than 3 msf under

construction mall spaces are staggered across the

next three years. Supply deficiency for new malls

coupled with limited churn led to a 0.12 percentage

points quarterly dip in mall vacancy levels and it

stood at 6.50% at the end of this quarter.

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

Trends & Updates

Ready Residential Property Update

At 2,500, new residential units that became

available for possession remained at par with the

previous quarter. This was primarily due to slow

construction pace of large township projects in the

peripheral submarkets. Of all the completed units,

77% belonged to the mid segment followed by 22% in

the high-end segment. GST Road (24%), Mogappair

(10%) and Velachery (8%) witnessed the maximum

number of unit completions during this quarter.

Nearly 35 projects were completed and developers

such as Newry Properties, Ruby Builders, Marutham

Group and Jains Housing & Constructions delivered

units in this quarter. Whilst rental values largely

remained stable, capital values appreciated by 5-13%

from the previous quarter in certain submarkets such

as Off-Central I, Porur and Rajiv Gandhi Salai-I, due to

increased demand.

15

Last Modified Date : 28-04-15

Source: Cushman & Wakefield Research

Note: The above values for mid segment typically include units of 1,000-2,000 sf

The time series have been adjusted to reflect the updated values

Average Capital Values – Mid Segment (INR ’000/sf)

Location

Adyar

Rajiv Gandhi

Salai (Perungudi)

Velachery

T. Nagar

Mylapore

Mogappair

Kilpauk

2009

4.5 - 6.5

2.5 - 2.8

3.5 - 4.0

4.0 - 6.5

NA

NA

4.5 - 6.0

2008

4.5 - 6.5

2.5 - 3.6

3.8 - 4.2

4.0 - 6.5

NA

NA

4.5 - 6.0

2010

6.0 - 8.5

3.5 - 4.5

3.5 - 5.0

7.5 - 10.5

NA

NA

6.0 - 8.0

2011

8.0 - 11.0

4.0 - 5.5

3.5 - 5.5

8.5 - 11.5

8.0 - 12.5

5.0 - 5.5

7.5 - 9.5

2012

9.0 - 13.0

5.0 - 6.3

4.5 - 6.5

8.5 - 14.0

10.0 - 15.0

5.0 - 6.5

9.0 - 12.0

10.0 - 14.0

5.0 - 6.3

6.0 - 8.0

10.0 - 17.0

12.0 - 17.0

5.0 - 7.5

2014

No availability

No availability

12.0 - 15.0

5.0 - 7.0

6.0 - 8.0

10.0 - 17.0

12.0 - 17.0

5.0 - 7.5

1Q 2015

10.0 - 14.0

5.0 - 6.3

6.0 - 8.0

10.0 - 16.0

12.0 - 17.0

5.0 - 7.5

9.0 - 12.0

2013

Source: Cushman & Wakefield Research

Note: The above values for high-end segment typically include units of 1,800-4,000 sf

The time series have been adjusted to reflect the updated values

*RA Puram also includes Alwarpet and Abhiramapuram

**Poes Garden also includes Venus Colony and Kasturi Rangan Road

Location 2008

18.0-24.0

13.0-15.0

NA

NA

5.5-10.0

14.5-20.0

13.0-16.0

6.0-9.0

4.0-8.0

Boat Club

R.A Puram*

Besant Nagar

Kotturpuram

Adyar

Poes Garden**

Nungambakkam

Anna Nagar

Kilpauk

2010

18.0-23.0

13.0-16.5

NA

NA

8.0-12.0

14.5-20.0

13.0-16.5

7.5-10.5

8.0-12.0

2009

18.0-20.0

13.0-15.0

NA

NA

5.5-9.5

14.5-18.0

13.0-16.0

6.0-9.0

4.0-8.0

2011

20.0-25.0

14.0-17.0

12.5-13.5

12.0-14.0

11.5 - 13.5

17.5-24.5

13.0-17.0

8.0-11.5

9.0-15.0

2012

23.0-27.0

15.0-19.0

13.0-14.5

14.0-16.0

13.0-14.5

18.5-25.0

17.0-20.0

12.0-14.0

12.0-15.0

Average Capital Values – High-end Segment (INR ‘000/sf)

2013

23.0-33.0

17.0-23.0

13.5-15.0

14.0-20.0

14.0-17.5

20.5-28.0

14.0-25.0

12.0-17.0

12.0-16.0

2014

23.0-35.0

17.0-23.0

13.5-15.0

14.0-20.0

14.0-17.5

20.5-33.0

14.0-25.0

12.0-17.0

12.0-16.0

1Q 2015

23.0-35.0

17.0-25.0

13.5-15.0

14.0-20.0

16.0-17.5

20.5-33.0

14.0-25.0

12.0-17.0

12.0-16.0

New Residential Launches

At 3,200, unit launches nearly doubled from the

previous quarter as many developers launched new

projects during the first quarter, to coincide with the

auspicious Pongal festival. New unit launches in the

mid segment continued to dominate and witnessed

more than 220% quarterly increase, as developers

focused on introducing products in this segment

that matched the homebuyers’ affordability.

Locations along the IT corridor of Rajiv Gandhi Salai

such as Sholinganallur, Siruseri as well as Suburban

(South) locations such as 200 Feet Pallavaram

T h o ra i p a k ka m Ro a d , M e d a va k ka m a n d

Perumbakkam witnessed significant new launches

due to their proximity to IT parks and IT-SEZs. New

launches in the high-end segment declined by 70%

over the previous quarter with launches largely

concentrated in Nungambakkam, Kotturpuram and

Off-Central I.

16

Last Modified Date : 28-04-15

Project Name Developer Location Number of Units* Type Area of Units (in sf)

S.I.S Queenstown South India Shelters

India Pvt. Ltd.Guduvanchery 424 Apartments 2 BHK: 623 to 1,226

2.5 BHK: 1,263 to 1,304

3 BHK: 1,373 to 1,508

Pinnacle Crest Baashyam

ConstructionsSholinganallur 421 Apartments 1 BHK: 579 to 607

2 BHK: 1,109 to 1,186

2.5 BHK: 1,336 to 1,357

3 BHK: 1,582 to 1,592

Temple Waves Amarprakash

DevelopersChrompet 405 Apartments 2 BHK: 616 to 918

3 BHK: 980

Casa Grande Cherry Pick

Casa Grande Pvt. Ltd. Perumbakkam 380 Apartments 1 BHK: 590 to 701

2 BHK: 1,199 to 1,354

2.5 BHK: 1,186 to 1,433

3 BHK: 1,379 to 1,624

3.5 BHK: 1,546 to 1,768

Real ValuePadmalaya Grand –Tower P,Q,E,F

Real Value Promoters Siruseri 288 Apartments 2 BHK: 942 to 1,060

3 BHK: 1,380 to 1,454

SkyPod Residences Vishwakarma Properties 200 Ft Pallavaram

Thoraipakkam Road280 Apartments 2 BHK:1,111

3 BHK: 1,363

S&P Essence - Phase I S&P Living Spaces Ayanambakkam 200 Apartments 1.5 BHK: 560 to 566

2 BHK: 952 to 953

3 BHK: 1,746 to 1,761

Urban Tree Wow Urban Tree Infrastructure Medavakkam 169 Apartments 2 BHK: 926 to 1,177

3 BHK: 1,428

Jamals Caladium Jamals Enterprises Velappanchavadi 158 Apartments 2 BHK: 955 to 1,105

3 BHK: 1,280 to 1,385

Silver Crest Rajkham Builders Madurapakkam 116 Apartments 2 BHK: 1,002 to 1,072

2.5 BHK: 1,271

3 BHK: 1,258 to 1,400

Vrindavan Enclave Amaar Foundations &

PropertiesVirugambakkam 64 Apartments 2 BHK: 972 to 1,110

3 BHK: 1,200 to 1,838

Color County Color Homes Iyappanthangal 60 Apartments 2 BHK: 884 to 974

3 BHK: 1,124 to 1,177

Tower of Adyar Nahar Group Adyar 56 Apartments 3 BHK: 2,113

4 BHK: 2,384 to 2,420

Shrayans Cara Properties Nungambakkam

High Road47 Apartments 4 BHK: 4,000 to 5,000

Hamlin AKB Developers Pallavaram 45 Apartments 2 BHK: 783 to 1,033

3 BHK: 1,265

GVSPL Raksha Green Valley Shelters

Pvt. Ltd.Valasaravakkam 35 Apartments 2 BHK: 1,145 to 1,165

2 BHK: 1,570 to 1,860

Green Crest Green Valley Shelters

Pvt. Ltd.Anna Nagar 28 Apartments 3 BHK: 1,260 to 1,345

Navin's Skanda Navin Housing Chrompet 16 Apartments 2 BHK: 1,032

3 BHK: 1,180

Sri Lakshmivilas Altis Properties Kotturpuram 11 Apartments 3 BHK: 2,392

4 BHK: 2,692

Aise Devinrayan Housing Nandanam 5 Apartments 4 BHK: 2,462

Sree Sarada Nivas Devinarayan Housing Mandaveli 4 Apartments 3 BHK: 2,494

Aquarelle Devinarayan Housing Kanathur 4 Apartments 3 BHK: 5,850 to 5,968

Sangeeth Arihant Foundations Shanthi Colony 3 Apartments 3 BHK: 2,000

* Estimated and as per market information 17

Last Modified Date : 28-04-15

Commercial Office Sector

Despite the improving occupier demand, Grade A

net absorption levels dipped by 19% from the

previous quarter and stood at 495,000 sf at the end

of the first quarter of 2015. This decline was

primarily due to change in employee to space ratio

requirements of a few major IT-ITeS companies. The

IT corridor of Suburban South (64%) and Peripheral

South (32%) witnessed maximum net absorption of

Grade A spaces. IT-ITeS sector was the major

demand driver and accounted for nearly 95% of

total gross absorption during the quarter. Rentals

largely remained stable in all sub markets, as

compared to the previous quarter.

Outlook

Whilst more than 4,300 residential units remain in

soft launch stages, the number of new unit launches

during the next quarter may remain at par with 1Q

2015, as developers may channelize larger efforts

towards completion of under construction units.

In the next quarter, nearly 1.5 msf of new office

supply is expected be added. Of the total new supply,

65% is expected to constitute Grade A spaces, all of

which will become operational in Suburban South.

Whilst leasing may strengthen, overall vacancy

levels may increase in the next quarter due to this

substantial new supply addition.

As no new mall supply is likely to be added in the

next quarter, mall vacancy levels may decline further

as prevalent demand for mall spaces from footwear,

F&B and apparel retailers remains strong. Anna

Nagar - 2nd Avenue and Pondy Bazar may witness

rental appreciation due to healthy demand and

limited options for prime retail spaces.

Retail Sector

Established main streets such as Anna Nagar 2nd

Avenue witnessed a steep rental escalation of 15%

compared to the last quarter as strengthening

demand and entry of new retailers prompted owners

(not affected by ongoing infrastructure upgrades) to

charge higher rentals. Purusawakam High Road too

witnessed a 4% rental rise due to higher demand

from footwear and apparel retailers.

As of 1Q 2015, under construction units across

various segments were around 33,600. As per

current estimates, these units are likely to complete

by the end of 2015. More than 90% of these units are

apartment projects and the remaining are villas, row

Under Construction Residential Property Update

houses and duplexes. Nearly one-third of these units

consist of new phases in existing township

developments in peripheral locations such as

Chrompet, Oragadam, Vandalur-Kelambakkam

Road, Perambur and Siruseri.

18

Last Modified Date : 28-04-15

Delhi - National Capital Region (NCR)

Market Overview

With around 2,800 new unit launches, Delhi-NCR

witnessed a decline of approximately 68% during

the first quarter of 2015, as compared to the

previous quarter. The decline in new launches was

primarily due to increasing unsold inventory, forcing

developers to restrict new launches. Capital values

remained stable from the previous quarter across all

submarkets in Delhi-NCR. With stable demand,

rentals also remained stable during the quarter

across most submarkets.

With Grade A office supply addition of about 2.1

msf in the first quarter of 2015, a marginal decline of

around 2.9% was noted from the previous quarter.

This quarter witnessed net absorption of more than

0.6 msf in Grade A developments, a 58% decline

from the previous quarter. No pre-commitments

were noted during the first quarter of 2015. Rental

values firmed up significantly in Gurgaon CBD, due

to limited availability and significant demand.

No new mall supply was added in the first quarter

of 2015, resulting in overall mall vacancy declining by

0.5 percentage points to 14.4%. Demand remained

high for mall spaces in Ghaziabad, Gurgaon and

South Delhi. Rental values in malls remained stable

from the previous quarter. Main street locations

across Greater Kailash, Lajpat Nagar and Green Park

witnessed healthy space take-up during the quarter.

Trends & Updates

Ready Residential Property Update

Due to subdued transaction activity, capital

values across all segments of various submarkets

remained stable from the previous quarter.

Transaction activity in the luxury segment seems to

be recovering with availability of several value deals

in this segment. Although the market remains buyer

friendly, capital values continued to remain stable

due to existing high unsold inventory.

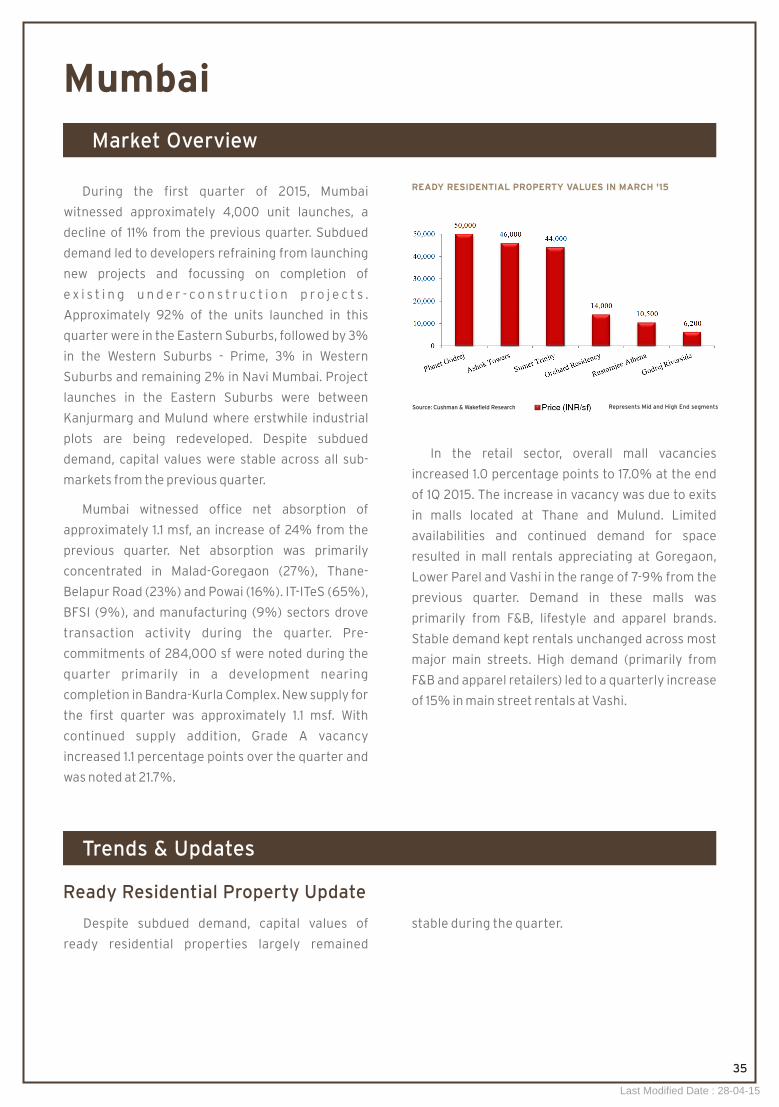

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

19

Last Modified Date : 28-04-15

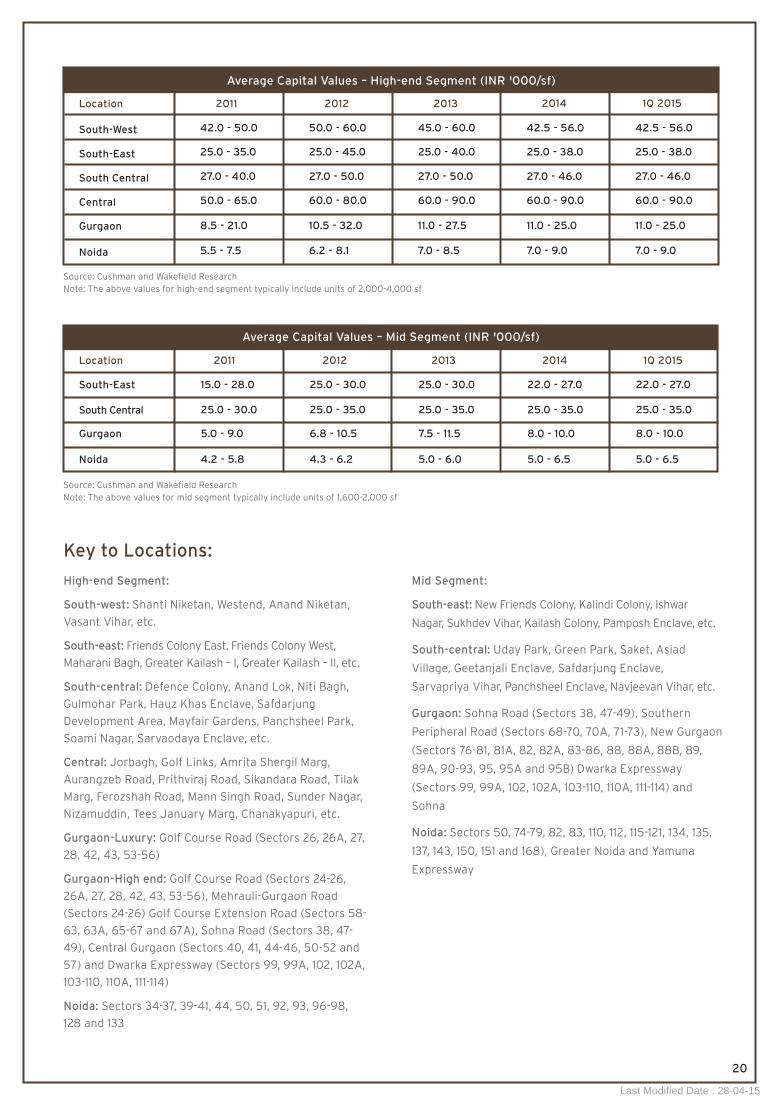

High-end Segment:

South-west: Shanti Niketan, Westend, Anand Niketan,

Vasant Vihar, etc.

South-east: Friends Colony East, Friends Colony West,

Maharani Bagh, Greater Kailash – I, Greater Kailash – II, etc.

South-central: Defence Colony, Anand Lok, Niti Bagh,

Gulmohar Park, Hauz Khas Enclave, Safdarjung

Development Area, Mayfair Gardens, Panchsheel Park,

Soami Nagar, Sarvaodaya Enclave, etc.

Central: Jorbagh, Golf Links, Amrita Shergil Marg,

Aurangzeb Road, Prithviraj Road, Sikandara Road, Tilak

Marg, Ferozshah Road, Mann Singh Road, Sunder Nagar,

Nizamuddin, Tees January Marg, Chanakyapuri, etc.

Gurgaon-Luxury: Golf Course Road (Sectors 26, 26A, 27,

28, 42, 43, 53-56)

Gurgaon-High end: Golf Course Road (Sectors 24-26,

26A, 27, 28, 42, 43, 53-56), Mehrauli-Gurgaon Road

(Sectors 24-26) Golf Course Extension Road (Sectors 58-

63, 63A, 65-67 and 67A), Sohna Road (Sectors 38, 47-

49), Central Gurgaon (Sectors 40, 41, 44-46, 50-52 and

57) and Dwarka Expressway (Sectors 99, 99A, 102, 102A,

103-110, 110A, 111-114)

Noida: Sectors 34-37, 39-41, 44, 50, 51, 92, 93, 96-98,

128 and 133

Mid Segment:

South-east: New Friends Colony, Kalindi Colony, Ishwar

Nagar, Sukhdev Vihar, Kailash Colony, Pamposh Enclave, etc.

South-central: Uday Park, Green Park, Saket, Asiad

Village, Geetanjali Enclave, Safdarjung Enclave,

Sarvapriya Vihar, Panchsheel Enclave, Navjeevan Vihar, etc.

Gurgaon: Sohna Road (Sectors 38, 47-49), Southern

Peripheral Road (Sectors 68-70, 70A, 71-73), New Gurgaon

(Sectors 76-81, 81A, 82, 82A, 83-86, 88, 88A, 88B, 89,

89A, 90-93, 95, 95A and 95B) Dwarka Expressway

(Sectors 99, 99A, 102, 102A, 103-110, 110A, 111-114) and

Sohna

Noida: Sectors 50, 74-79, 82, 83, 110, 112, 115-121, 134, 135,

137, 143, 150, 151 and 168), Greater Noida and Yamuna

Expressway

Key to Locations:

Average Capital Values – High-end Segment (INR '000/sf)

Location

South-West

South-East

South Central

Central

Gurgaon

Noida

42.0 - 50.0

25.0 - 35.0

27.0 - 40.0

50.0 - 65.0

8.5 - 21.0

5.5 - 7.5

2011

50.0 - 60.0

25.0 - 45.0

27.0 - 50.0

60.0 - 80.0

10.5 - 32.0

6.2 - 8.1

2012

45.0 - 60.0

25.0 - 40.0

27.0 - 50.0

60.0 - 90.0

11.0 - 27.5

7.0 - 8.5

2013

42.5 - 56.0

25.0 - 38.0

27.0 - 46.0

60.0 - 90.0

11.0 - 25.0

7.0 - 9.0

2014

42.5 - 56.0

25.0 - 38.0

27.0 - 46.0

60.0 - 90.0

11.0 - 25.0

7.0 - 9.0

1Q 2015

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 2,000-4,000 sf

Source: Cushman and Wakefield Research

Note: The above values for mid segment typically include units of 1,600-2,000 sf

Average Capital Values – Mid Segment (INR '000/sf)

South-East

South Central

Gurgaon

Noida

Location

15.0 - 28.0

25.0 - 30.0

5.0 - 9.0

4.2 - 5.8

2011

25.0 - 30.0

25.0 - 35.0

6.8 - 10.5

4.3 - 6.2

2012

25.0 - 30.0

25.0 - 35.0

7.5 - 11.5

5.0 - 6.0

2013

22.0 - 27.0

25.0 - 35.0

8.0 - 10.0

5.0 - 6.5

2014

22.0 - 27.0

25.0 - 35.0

8.0 - 10.0

5.0 - 6.5

1Q 2015

20

Last Modified Date : 28-04-15

21

Amrapali Enchante ApartmentsAmrapali Sector 16B, Greater

Noida (West)

650 2 BHK: 850 to 900

3 BHK: 1,050 to 1,150

Familia ApartmentsNimai Group Sector 7, Sohna 650 2 BHK: 1,150

3 BHK: 1,450

Sports Home ApartmentsDevsai Construction Sector 1, Greater

Noida (West)

366 2 BHK: 1,140

4 BHK: 3,210

Bollywood Towers ApartmentsAmrapali Sector 1, Greater

Noida (West)

360 2 BHK: 975 to 1,100

Omaxe Riyasat ApartmentsOmaxe Sector 93B, Noida 276 2 BHK: 1,225

3 BHK: 1,675

The Crest ApartmentsDLF DLF Phase V, Gurgaon 250 4 BHK: 3,081 to 3,497

Mahagun Villaments ApartmentsMahagun Group Sector 10, Greater

Noida (West)

104 3 BHK: 2,600

4 BHK: 2,950

Ayana Independent

FloorsRaheja Sector 79B, Gurgaon 96 3 BHK: 1,800 to 2,430

4 BHK: 2,564

Aspire Independent

FloorsAce Developers Sector 1, Greater Noida

(West)

72 2 BHK: 1,160

3 BHK: 1,365

4 BHK: 1,595

Project Name Developer Location Number of Units* Type Area of Units (in sf)

* Estimated and as per market information

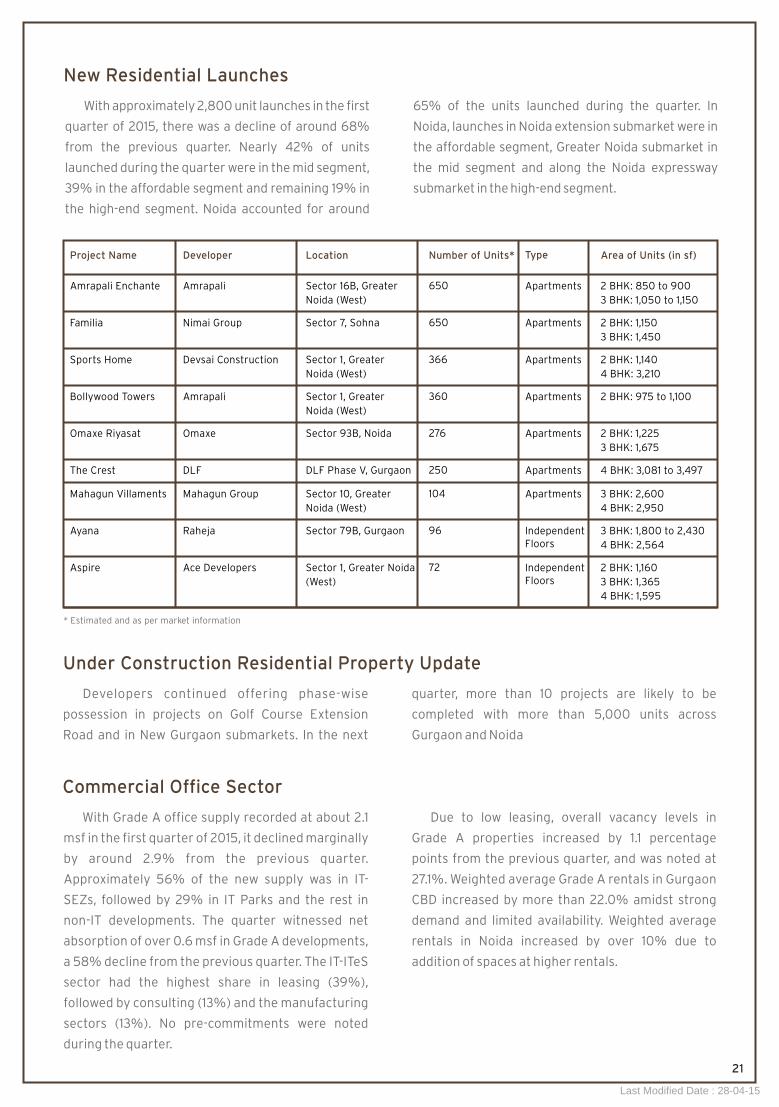

With approximately 2,800 unit launches in the first

quarter of 2015, there was a decline of around 68%

from the previous quarter. Nearly 42% of units

launched during the quarter were in the mid segment,

39% in the affordable segment and remaining 19% in

the high-end segment. Noida accounted for around

New Residential Launches

65% of the units launched during the quarter. In

Noida, launches in Noida extension submarket were in

the affordable segment, Greater Noida submarket in

the mid segment and along the Noida expressway

submarket in the high-end segment.

Developers continued offering phase-wise

possession in projects on Golf Course Extension

Road and in New Gurgaon submarkets. In the next

Under Construction Residential Property Update

quarter, more than 10 projects are likely to be

completed with more than 5,000 units across

Gurgaon and Noida

Commercial Office Sector

With Grade A office supply recorded at about 2.1

msf in the first quarter of 2015, it declined marginally

by around 2.9% from the previous quarter.

Approximately 56% of the new supply was in IT-

SEZs, followed by 29% in IT Parks and the rest in

non-IT developments. The quarter witnessed net

absorption of over 0.6 msf in Grade A developments,

a 58% decline from the previous quarter. The IT-ITeS

sector had the highest share in leasing (39%),

followed by consulting (13%) and the manufacturing

sectors (13%). No pre-commitments were noted

during the quarter.

Due to low leasing, overall vacancy levels in

Grade A properties increased by 1.1 percentage

points from the previous quarter, and was noted at

27.1%. Weighted average Grade A rentals in Gurgaon

CBD increased by more than 22.0% amidst strong

demand and limited availability. Weighted average

rentals in Noida increased by over 10% due to

addition of spaces at higher rentals.

Last Modified Date : 28-04-15

22

Mall vacancy levels were recorded at 14.4%, a 0.5

percentage points decline from the previous quarter.

Demand for mall spaces was driven mainly by

retailers of accessories and apparel such as Carat

Lane, Fossil, Nappadori, etc. Robust demand and

limited availability led to a quarterly rental increase

Retail Sector

of 7.1% in DLF Galleria, Gurgaon. Rentals in other

main street locations maintained status quo during

the quarter. F&B and jewellery retailers were the key

demand generators across main streets with brands

such as Subway, The Backyard and Senco Gold,

expanding their presence in the city.

Developers are likely to focus on completing

under construction projects rather than launching

new projects in the short term. As a result, new

launch activity may remain subdued in the next

quarter. In the absence of significant triggers for

demand improvement, capital values in Delhi and

Gurgaon may remain stable in the next quarter.

However, capital values in Noida may strengthen in

the next quarter due to continued end-user demand.

Approximately 3.9 msf of office space is likely to

be added in the next quarter. Although some of this

may be deferred, vacancy levels are likely to

increase, as net absorption is not likely to keep pace

with the supply.

Outlook

Nearly 1.9 msf of new mall supply is scheduled for

completion in the next quarter across Ghaziabad,

South Delhi and West Delhi. With tepid demand,

rental values are expected to remain stable. In

addition, infusion of new supply would lead to an

increase in vacancy levels in select submarkets.

Rentals across most main street locations are

expected to remain stable. Prominent main street

locations such as Connaught Place, Lajpat Nagar

and Greater Kailash II are expected to witness

continued retailer interest.

Last Modified Date : 28-04-15

Market Overview

Hyderabad

Hyderabad residential segment witnessed

launch of nearly 3,300 residential units during the

first quarter of 2015, nearly thrice the previous

quarter. About 98% of new unit launches were in the

north-west quadrant of the city, mainly Madhapur

and Gachibowli. This quadrant remained most active

in terms of new unit launches and construction

activity. As compared to the previous quarter, rental

and capital values largely remained stable across

submarkets. However, high-end segment capital

values in Banjara Hills and Jubilee Hills appreciated

by 3% and 6%, respectively, from the previous

quarter, due to limited availability amidst high

demand. Mid segment capital values in Jubilee Hills,

Madhapur and Gachibowli also appreciated

marginally by 1-2%, due to continued demand

emanating from IT-ITeS professionals employed in

the nearby office hubs.

The commercial real estate market witnessed an

influx of 1 msf of office space in 1Q 2015, of which

65% was in Grade A developments. Grade A net

absorption declined by 36% to around 0.6 msf at the

end of this quarter. Whilst overall vacancy for the

quarter declined by 0.6 percentage points to 17.6%,

Grade A vacancy in Suburban Madhapur submarket

increased marginally by 0.5 percentage points and

was noted at 5.4%.

SLN Lumbini mall, measuring 150,000 sf, is

currently undergoing fit-outs by tenants and is

expected to commence operations in the third quarter

of 2015. This quarter also witnessed limited

transactions and hence, mall rentals remained stable

across all sub-markets and overall mall vacancy levels

remained stable at 7%. Limited availability of quality

spaces in malls led to spill-over of demand to main

streets and subsequently healthy leasing activity was

noted in main streets such as Jubilee Hills, Kukatpally

and Chandanagar. The demand primarily emanated

from apparels and F&B retailers. Despite healthy

leasing, main street rentals remained stable from the

previous quarter, across the city.

Trends & Updates

Ready Residential Property Update

The first quarter of 2015 witnessed moderate

enquiries for ready residential properties. Mid

segment capital values in Jubilee Hills and

Madhapur-Gachibowli appreciated by 1% and 2%,

respectively, from the previous quarter, primarily

due to a healthy demand amidst limited supply of

quality projects. Around 320 units were completed

in the first quarter of 2015.

23

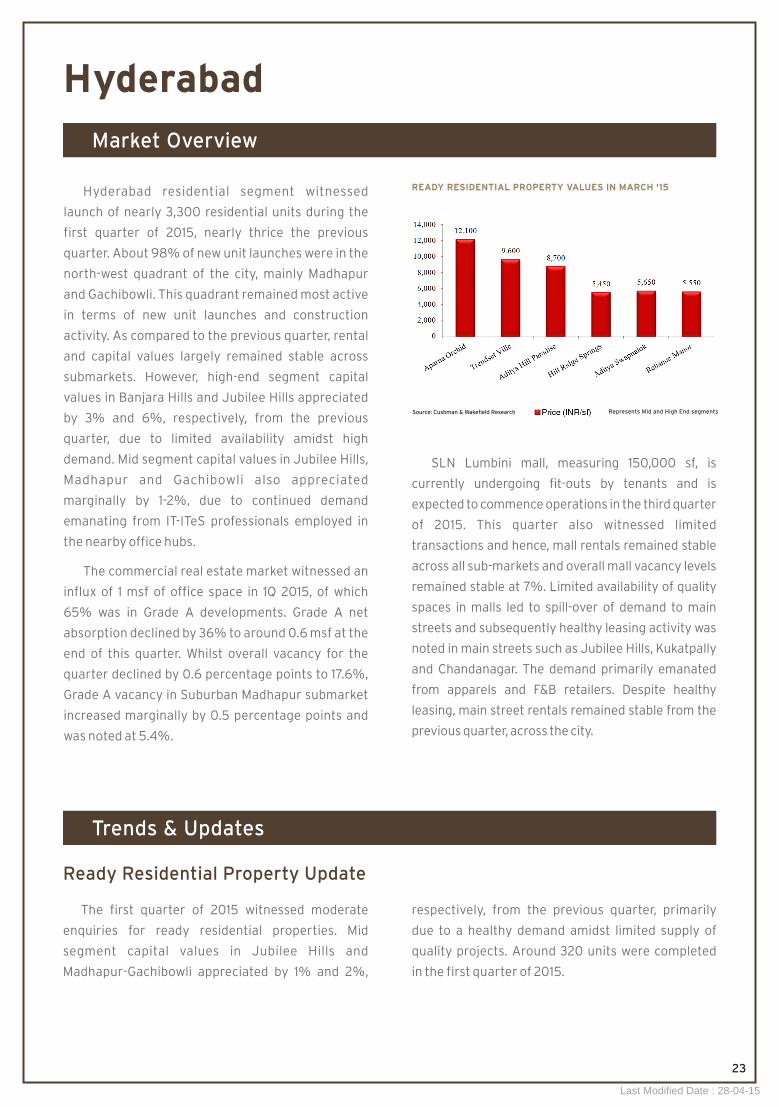

Source: Cushman & Wakefield Research Represents Mid and High End segments

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Last Modified Date : 28-04-15

New Residential Launches

The first quarter of 2015 witnessed three times

residential unit launches compared to the previous

quarter. Approximately 3,300 units were launched in

this quarter, all in the high-end segment. New

projects were launched primarily in Madhapur and

Gachibowli.

24

Project Name Developer Location Number of Units* Type Area of Units (in sf)

Highfields Prestige Constructions Gachibowli 2,240 Apartments 2 BHK: 1,283

2.5 BHK: 1,410 to 1,492

3 BHK: 1,742

3.5 BHK: 1,919 to 1,993

4 BHK: 2,713 to 2,848

3 BHK+Home Theatre: 4,070

Etania Lansum Gachibowli 552 Apartments 3 BHK: 1,895 to 3,255

4 BHK: 4,085

Ivy League Prestige Constructions Madhapur 349 Apartments 2 BHK: 1,327 to 1,355

3 BHK: 1,738 to 2,051

4 BHK: 3,031 to 3,498

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 1,600-4,000 sf

Banjara Hills

Jubilee Hills

Himayatnagar

West & East Marredpally

Begumpet, Somajiguda

Madhapur, Gachibowli

Kukatpally

Miyapur, Nizampet

Location 2009

3.3 - 4.0

2.6 - 3.3

5.8 - 6.5

5.5 - 6.3

3.3 - 4.0

3.3 - 3.8

3.9 - 4.5

3.5 - 4.3

2010

3.5 - 4.5

2.7 - 3.4

6.0 - 7.2

6.0 - 7.0

3.7 - 4.0

3.5 - 4.0

4.1 - 4.5

3.8 - 4.9

2011

3.8 - 5.1

2.8 - 3.5

6.4 - 7.5

6.2 - 7.2

3.7 - 4.2

3.6 - 4.3

4.3 - 4.8

3.9 - 5.3

2012

3.8 - 5.1

2.9 - 3.5

6.5 - 7.5

6.1 - 7.2

3.6 - 4.2

3.6 - 4.3

4.3 - 4.7

4.1 - 5.3

2013

4.0 - 6.0

2.9 - 3.5

7.0 - 9.5

6.5 - 9.5

4.0 - 5.5

4.0 - 5.5

4.5 - 5.5

4.5 - 6.0

2014

4.0 - 6.0

2.9 - 3.5

7.0 - 9.5

6.5 - 9.5

4.0 - 5.5

4.0 - 5.5

4.5 - 5.5

4.5 - 6.0

4.0 - 6.0

2.9 - 3.5

7.0 - 10.0

7.0 - 10.0

4.0 - 5.5

4.0 - 5.5

4.5 - 5.5

4.5 - 6.0

1Q 2015

Average Capital Values – High-end Segment (INR ‘000/sf)

Source: Cushman and Wakefield Research

Note: The above values for mid segment typically include units of 1,200-1,600 sf

Banjara Hills

Jubilee Hills

Himayatnagar

West & East Marredpally

Begumpet, Somajiguda

Madhapur, Gachibowli

Kukatpally

Miyapur, Nizampet

Location

2.4 - 2.9

1.8 - 2.5

3.6 - 4.2

3.5 - 4.0

2.7 - 3.0

2.5 - 2.8

2.6 - 3.1

2.5 - 3.1

2009

3.6 - 4.5

3.7 - 4.0

2.7 - 3.5

2.7 - 3.2

1.8 - 2.5

2.7 - 3.0

2.8 - 3.5

2.6 - 3.4

2010

2.9 - 3.5

2.4 - 3.0

3.8 - 4.6

4.0 - 4.2

2.7 - 3.7

2.8 - 3.2

2.9 - 3.6

2.8 - 3.5

2011

2.9 - 3.6

2.2 - 3.4

3.8 - 4.8

4.0 - 4.2

2.8 - 3.6

2.7 - 3.2

2.8 - 3.6

3.0 - 3.8

2012

3.1 - 4.0

2.7 - 3.4

4.0 - 5.0

3.8 - 4.4

3.0 - 3.8

3.0 - 3.5

3.0 - 4.0

3.5 - 4.2

2013

3.3 - 4.0

2.8 - 3.6

4.0 - 5.2

3.8 - 4.4

3.0 - 3.8

3.0 - 3.5

3.2 - 4.0

3.6 - 4.5

2014

3.3 - 4.0

2.9 - 3.6

4.0 - 5.2

3.8 - 4.5

3.0 - 3.8

3.0 - 3.5

3.2 - 4.0

3.8 - 4.6

1Q 2015

Average Capital Values - Mid Segment (INR ‘000/sf)

Last Modified Date : 28-04-15

25

Under Construction Residential Property Update

The North-West quadrant continued to witness

robust construction activities. Capital values of high-

end segment projects at Banjara Hills and Jubilee Hills

appreciated by 3% and 6%, respectively, from the

previous quarter due to limited availability amidst

high demand. Capital values of mid segment projects

at Jubilee Hills, Madhapur and Gachibowli too

appreciated marginally by 1-2% from the previous

quarter, due to sustained demand driven by IT-ITeS

professionals, coupled with availability of good

offerings at competitive prices.

Project Name Developer Location Number of Units* Type Area of Units (in sf)

Northstar District 1 Northstar Homes Gachibowli 151 Apartments 3BHK: 1,600 to 2,400

Fortune Galaxy Fortune Developers Banjara Hills 55 Apartments 3 BHK: 1,445 to 2,400

Studio: 500 to 900

* Estimated and as per market information

In the commercial office sector, majority of the

supply was concentrated in the suburban locations

of Madhapur (65%) and Gachibowli (21%). Although

IT-ITeS sector dominated leasing activity with a 65%

share, majority of the space (53%) was leased in

non-IT buildings. Grade A net absorption for the

quarter was 0.6 msf, recording a 36% quarterly

decline. Whilst overall vacancy declined by 0.6

percentage points (to 17.6%), low absorption

Commercial Office Sector

coupled with high supply addition in Grade A

developments in Suburban Madhapur submarket

resulted in a 0.5 percentage point increase in

vacancy. Rentals continued to remain nearly stable

across all submarkets, except the Prime Suburban

submarket where the weighted average rental

values declined by 6% due to an increase in vacant

spaces amidst high supply.

SLN Lumbini mall, measuring 150,000 sf, is

currently undergoing fit-outs by tenants and is

expected to commence operations in the third

quarter of 2015. This quarter witnessed limited

transactions and hence, mall rentals remained

stable across all sub-markets. Overall mall vacancy

levels remained stable from the previous quarter

Retail Sector

and were noted at 7%. Healthy leasing activity was

noted in main streets such as Jubilee Hills,

Kukatpally and Chandanagar. Demand primarily

emanated from apparel & F&B retailers. Despite

healthy leasing, main street rentals remained stable

across the city.

Last Modified Date : 28-04-15

26

High-end segment capital values may appreciate

marginally in Banjara Hills and Jubilee Hills in the

next quarter. Mid segment capital values in

submarkets such as Banjara Hills, Jubilee Hills,

Madhapur and Gachibowli may witness marginal

appreciation due to sustained demand and

availability of good offerings at competitive prices.

Nearly 2.6 msf of supply infusion is expected in

the upcoming quarter. Rental values in Suburban

Gachibowli submarket may appreciate marginally in

the next quarter as upcoming supply is likely to be

introduced at higher rentals. Limited availability of

Outlook

quality office spaces in Madhapur may result in

heightened demand in Gachibowli.

With no new supply addition and limited

availability in existing malls, rentals are likely to

remain stable in the next quarter. Rentals across

most main streets are expected to remain stable in

the upcoming quarter as leasing is expected to

remain steady. However, access related issues in

specific micro-markets such as Raj Bhavan Road /

Somajiguda may be a reason for waning retailers’

interest, which may lead to lower demand and

subsequently lower rentals.

Last Modified Date : 28-04-15

Market Overview

Jaipur

Approximately 1,200 units were launched in

Jaipur during the first quarter of 2015, a 44%

decline from the previous quarter. The quarter

witnessed unti launches primarily in the mid

segment. Locations across Mansarovar witnessed

the highest number of new unit launches followed by

Sirsi Road and Vaishali Nagar. Capital Values

appreciated marginally (around 1-3%) in both mid

and high-end segment.

No new office supply was added in the first

quarter of 2015. Transaction activity remained

stable during the quarter with demand primarily

from IT-ITeS and manufacturing companies. Rentals

maintained status quo from the previous quarter,

across all submarkets.

No new mall supply was added during the first

quarter of 2015. Healthy transaction activity was

noted in the main street locations of Mirza Ismail

(M.I.) Road and Malviya Nagar. During the quarter,

demand for mall spaces arose from large apparel,

lifestyle and F&B retailers. Rentals across malls and

main street locations maintained status quo during

the quarter.

Trends & Updates

Ready Residential Property Update

Capital values increased in the range of 1-2%

across high-end and mid segment properties during

the first quarter of 2015, due to stable demand from

end-users. In the high-end segment, whilst capital

values remained stable in Bapu Nagar, C-Scheme

witnessed the highest increase of 2.1% followed by

Civil Lines (1.4%) and Malviya Nagar (1.3%).

READY RESIDENTIAL PROPERTY VALUES IN MARCH '15

Source: Cushman & Wakefield Research Represents Mid and High End segments

27

Last Modified Date : 28-04-15

New Residential Launches

In the first quarter of 2015, new project launches

were primarily in the Western peripheries of the city.

Nearly 1,200 units were launched, of which 39%

were in Mansarovar followed by 34% in Sirsi Road,

17% in Vaishali Nagar and remaining in Jagatpura.

The quarter witnessed launches only in the mid

segment. The Basic Sale Price (BSP) of the new

launches ranged from INR 2,400-3,500/sf.

Project Name Developer Location Number of Units* Type Area of Units (in sf)

Terraza Greens Shivank Group Mansarovar 380 Apartments 2 BHK: 1,257 to 1,390

3 BHK: 1,321 to 1,782

Ozone SNG Group Sirsi Road 312 Apartments 2 BHK: 950 to 1,509

3 BHK: 1,200 to 2,000

The Horizon Vardhman Group Vaishali Nagar 204 Apartments 2 BHK: 900 to 1,200

3 BHK: 1,420 to 1,545

Bhavyaa Green Aradhana Buildtech Jagatpura 108 Apartments 2 BHK: 1,050 to 1,310

3 BHK: 1,560 to 1,580

Atelier Erica Apeksha Group Sirsi Road 98 Apartments 2 BHK: 980

3 BHK: 1,300 to 1,450

The Trump IPG Group Mansarovar 90 Apartments 2 BHK: 952 to 1,300

3 BHK: 1,300

28

Source: Cushman and Wakefield Research

Note: The above values for high-end segment typically include units of 2,000-4,000 sf, both apartments and villas

*sqyd: Square Yard

Average Capital Values – High End (INR ‘000/sf)

Location

C- Scheme

Bapu Nagar

Civil Lines

Malviya Nagar

1Q 2014

8,000-10,500/sf

7,000-9,000/sf

80,000-100,000/sqyd

75,000-95,000/sqyd

3Q 2014

8,000-11,000/sf

7,000-9,000/sf

80,000-110,000/sqyd

75,000-100,000/sqyd

2Q 2014

8,000-10,500/sf

7,000-9,000/sf

80,000-100,000/sqyd

75,000-95,000/sqyd

Average Capital Values – High-end Segment (INR)

1Q 2015

8,200-11,200/sf

7,000-9,000/sf

82,500-115,000/sqyd

77,500-105,000/sqyd

4Q 2014

8,000-11,000/sf

7,000-9,000/sf

80,000-115,000/sqyd

75,000-105,000/sqyd

Source: Cushman and Wakefield Research

Note: The above values for mid segment apartments typically include units of 1,600-2,000 sf, both apartments and villas

*sqyd: Square Yard

Average Capital Values – High End (INR ‘000/sf)

Location

Malviya Nagar

Vaishali Nagar

Mansarovar

Jagatpura

3Q 2014

60,000-75,000/sqyd

2,900-3,600/sf

2,800-3,800/sf

2,900-3,400/sf

1Q 2015

65,000-77,500/sqyd

3,000-3,600/sf

2,800-3,850/sf

2,900-3,500/sf

4Q 2014

65,000-75,000/sqyd

2,900-3,600/sf

2,800-3,850/sf

2,900-3,500/sf

2Q 2014

60,000-75,000/sqyd

2,900-3,400/sf

3,000-3,500/sf

2,900-3,300/sf

1Q 2014

60,000-75,000/sqyd

2,900-3,300/sf

3,000-3,400/sf

2,900-3,200/sf

Average Capital Values – Mid Segment (INR)

* Estimated and as per market information

Last Modified Date : 28-04-15

Commercial Office Sector

No new office supply was added in the first quarter

of 2015. Rental values in the Central Business District

(CBD) of MI Road and C-Scheme remained stable at

INR 65/sf/month and that for Secondary Business

District (SBD) at INR 35-50/sf/month. IT-ITeS and

manufacturing companies had a majority share in

office space take-up during the quarter.

No new mall supply was added during the first

quarter of 2015. Demand for mall spaces was primarily

from large lifestyle and apparel brands such as Marks

& Spencer and Shoppers Stop. Main street locations of

MI Road and Malviya Nagar witnessed interest from

Retail Sector

apparels and F&B retailers such as Van Heusen, Allen

Solly and Dunkin Donuts. Rentals remained stable

from the previous quarter across malls and main

street locations.

Capital values in the residential sector are likely

to remain stable in the short term with marginal

improvement in submarkets of C-scheme and Sirsi

Road, due to bettering infrastructure. Considering

that only a few projects are currently in the pre-

launch stages, number of new launches are likely to

decline in the future periods.

New office space measuring 80,000 sf is

expected to be added during the next quarter. Rental

Outlook

values are expected to remain stable with stagnant

demand for office space.

No new mall supply is expected to be added in the

next quarter. Rentals are expected to remain stable