chapter 1 indroduction

TRANSCRIPT

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 1

CHAPTER 1

INDRODUCTION

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 2

INTRODUCTION

“Microfinance” as a branch of economic development for those who lack access to

resources has garnered considerably recognition over the last several years, much of it due to

the 2006 awarding of the Nobel Peace Prise to Professor Mohammed Yunus, a US trained,

Bangladeshi economist who serves as the global figurehead for the microfinance movement.

The committee has recognized microfinance as “an important liberating force” and “ever

more important instrument in the struggle against poverty”.

Microfinance is a financial service of small quantity provided by Financial Institutions

to the poor. These financial services may include savings, credit, insurance, leasing, money

transfer, etc. That is any type of financial services, provided to customers to meet their

normal financial needs: life cycle, economic opportunity and emergency with the only

qualification that transaction value is small and customers are poor.

As point out by the former UN secretary General Kofi Annan during the launch of

the International Year of Micro Credit (2005), “sustainable access to Microfinance helps

alleviate poverty by generating income, creating jobs, allowing children to go to school,

enabling families to obtain health care, and empowering people to make the choices that best

serve their needs.

The microfinance was prompted in India to overcome poverty, increase income and

enhance well being of the poor. But most of the Indian Microfinance Institutions only focus

on microcredit and their high lending rate and loan shark type behaviour credited problems.

An alternative to the commercial model of Microfinance is the Kudumbashree

programme initiated in 1998 by the Government of Kerala. It focuses for overall development

of the family

In the words of the former Prime minister ShriAtalBehariBajpai, “group savings and

group action can remove the curse of money lenders. Since the whole system is organized

transparently, the thrift and savings can become informal banks for the poor and of the poor”.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 3

STATEMENT OF THE PROBLEM

Microfinance became a leading and effective strategy for poverty alleviation with the

potential for far reaching impact in transforming the lives of poor people. Microfinance can

facilitate the achievement of the national policies that target poverty reduction, empowerment

of women, assisting vulnerable groups and improving standards of living.

Studies have been shown that Microfinance plays critical role in development. It enables

the very poor households to meet their most basic needs and protect against risks. It is

associated with improvements in households’ economic participation, it helps to empower

women and promote gender equity.

It is available from past studies that, Kudumbashree is an effective MFI to support

economic development. So the poor people can become more empowered especially women

by joining Kudumbashree programme. It points out that the need of the Kudumbashree units

in the area where the poor people are reported lower.

So far no systematic studies are available in the area of Microfinance generated through

Kudumbashree units in Malappuram District. Hence the present study address these issues

like to know the impact of Microfinance through Kudumbashree and problems related with

Kudumbashree Units in Areekode Panchayath.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 4

SCOPE OF THE STUDY

Women empowerment is considered as an important responsibility of every government.

Till recently very little attention has been given to empowerment and sustainability issues.

Women’s access to savings and credit gives them greater economic role in decision making,

thereby optimising their own and households welfare. It is available from past studies

that;kudumbashree is an effective MFI to support economic development. So the poor people

can become more empowered especially women by joining kudumbashree programme. It

points out that the need of the kudumbashree units in the area where the poor people are

reported lower.

The study related to performance of Kudumbashree units in Areekode Panchayath, role

of Government for their improvement and level of problems in their units help to find out the

key factor which enhance this field and give suggestions for betterment.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 5

OBJECTIVES OF THE STUDY

➢ To study the impact of microfinance on women empowerment through kudumbashree

unit.

➢ To analyze the role of government agencies in the promotion of kudumbashree units.

➢ To study the purpose of obtaining microfinance by members in kudumbashree units.

➢ To identify problems and constraints of kudumbashree units.

➢ To give further suggestions for the empowerment of women through kudumbashree

units.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 6

RESEARCH METHODOLOGY

The study is designed on a descriptive study conducted in AreekodePanchayath based on

both secondary and primary data.

SOURCE OF DATA

SOURCE OF PRIMARY DATA

Primary data collected from members of the Kudumbashree units in Areekode Panchayath

SOURCE OF SECONDARY DATA

Secondary data collected from published books, magazines, journals, websites, reports

and periodicals of Kudumbashree units, etc.

Journals:-

• A study on Kudumbashree Project Sponsored by Planning Commission of India.

• Federal Reserve Bank of ST.Locus review.

• Indian Journal Marketing.

• International Journal Finance.

• International Journal of Microfinance.

• International Journal of Rural Management.

• Journal of South Asian Development.

• Kerala’s Kudumbashree working Paper 17.

Reports and periodicals:-

• Status of Microfinance in India 2011-12, by NABARD.

• Rural Monthly Report July 2012 by KDS District Mission Malappuram.

Books:-

• Microcredit, poverty And Empowerment Linking The Triad, edited by NeeraBulra

Joy Deshmukh, Ranadeve, Ranjani k, Murthy, published by SAGE Publications.

• Microfinance Case Studies, edited by S.Rajagopalan, published by ICFAI University

Press.

• Praveshika, by National Rural Livelihood Mission.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 7

• Rural Finance Sector, edited by Tamal Data Chaudhuri, published by ICFAI

University Press.

Websites:-

• www.google.com.

• www.kudumbashree.org.

• www.nabard.org.

• www.pondiuni.edu.in.

• www.researchersworld.com.

• www.sjsry-kudumbashree.org.

.

SAMPLING SIZE

Altogether 282 NHGs are working in Areekode Panchayath. Out of 282 NHGs, 100

units were selected at random and one respondent from each 100 units were selected to know

the impact of microfinance.

SAMPLING METHOD

The method of sampling used is random sampling. The units are respondent in each

unit has been selected by drawing lot.

TOOLS AND TECHNIQUES

TOOLS OF DATA COLLECTION

The required data for the study has been collected through questionnaire and

structured interview schedule.

TOOLS USED FOR DATA PRESENTATION

Tables, graphs and charts are used to present the data.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 8

TOOLS USED FOR DATA ANALYSIS

The following tools have been used to analyze and interpret the data.

✓ Z test.

✓ Weighted Average and Rank.

✓ Karl Pearson’s Correlation coefficient.

✓ Percentage analysis.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 9

LIMITATIONS OF THE STUDY

➢ The study is based on sampling techniques, so there is a chance of sampling error.

➢ The study was conducted and data collected within a short period which may affect in

getting the reliable data.

➢ There is a chance of exaggerated information provided by the respondents.

➢ The study covered only in small geographical area.

➢ Sample is limited to 100 respondents in the Areekode panchayath.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 10

HYPOTHESIS

Hypothesis 1

H0: There is no significant improvement in the indebtedness of members from money lenders

and chitties through the intervention of Microfinance programme.

H1: There is a significant improvement in the indebtedness of members from money lenders

and chitties through the intervention of microfinance programme.

Hypothesis 2

H0: There is no significant improvement in the indebtedness of members from religious

organization through the intervention of Microfinance programme.

H1: There is a significant improvement in the indebtedness of members from religious

organization through the intervention of microfinance programme.

Hypothesis 3

H0: There is no significant improvement in the indebtedness of members from loan taken

from government and funding agencies through the intervention of Microfinance programme.

H1: There is a significant improvement in the indebtedness of members from loan taken from

government and funding agencies through the intervention of Microfinance programme.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 11

CHAPTER PLAN

The study contains 5 chapters. The first chapter deals with introduction, statement of the

problem, objectives, scope, methodology, limitations, etc.

The second chapter deals with review of literature of the study.

The Third chapter contains microfinance, profile and details of kudumbashree.

The fourth chapter includes the analysis and interpretation of data collected from

sample units and members.

The Fifth chapter contains summary, findings, suggestions and conclusion.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 12

CHAPTER 2

REVIEW OF LITERATURE

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 13

LITERATURE REVIEW

Kudumbashree is a unique poverty eradication mission of the state of Kerala. Many

studies have so far conducted in relation with Kudumbashree and self-help groups in different

parts of our country. A brief view of the studies so far conducted is given below.

Kenneth Kalyani, Seena P.C (2012) reveals that economic development is the base

for other development. Collective effort has been recognized as tenets of women

empowerment. Through women empowerment leads to sustainable social development.

Economic development of women leads to better living status in the family, educational,

nutritional, and the health needs of the children were well satisfied. Economic independence

through Kudumbashree improved the social participation of its members and the

Kudumbashree NHG movement is supporting for social empowerment of poor women flock.

Minimol M. C and Makesh K. G (2012) in their study identified that Intellectual

empowerment is considered more important, or at least equally important to social, economic

or financial empowerment. The concept of personal empowerment often fails to encompass

intellectual empowerment. The objective intended to be achieved is that the members become

more capacitated to think and act better from blunt in thinking to sharp; and from thick in

action to fine. According to them the concept of SHGs for rural women empowerment has

not yet run its full course in attaining its objective.

Sanjay Kanti Das (2012) in his study indicated that SHG-Bank Linkage of micro

finance programme has a profound influence on the economic status, decision making power,

knowledge and self worthiness of women participants of SHG linkage programme in Assam.

Sri.V.P.Ragavan (2009), in his article stated that the poor women of the State have

become active participants in the planning and implementation process of various ant-poverty

programmes. By participating in various incomes generating –cum-developmental activities,

the morale and confidence of women became very high. Capacity of the poor women of the

State in several areas has gone up considerably. Status of women in families and community

has also improved. Kudumbashree has gained national and international acclaim as an ideal

and workable model of participatory development for eradicating poverty. He further stated

that women empowerment is the best strategy for poverty eradication.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 14

J. Bhagyalakshmi (2004) , in the article, “Women’s Empowerment - Miles to Go”,

points out that India as a signatory to the UN Convention has taken several measures to

ensure full development and advancement of women. The women specific programmes are

showing positive results in empowering women, until now, one feels, there are miles to go

and promises to keep. All forms of violence against women, physical and mental, whether at

familial or communal level shall be dealt with great care. She states that all forms of

discrimination against girl child and violation of her rights shall be eliminated by undertaking

strong measures both preventive and disciplinary within and outside the family. Though

women play a major role in agriculture and allied sectors, their contribution is hardly

recognized. Intensive efforts are needed to ensure that benefits of training, extension and

various programmes will reach them to make them more effective in their own area of

operation.

MeenakshiMalhotra (2004) , in her work entitled, “Empowerment of Women” (in 3

volumes), deals with the issues leading to empowerment of women with particular reference

to rural women. Volume one deals with issues like gender inequalities in labour market and

in entrepreneurship. Volume two focuses on micro finance options for women empowerment.

It looks into micro credit schemes for rural women and micro finance movement in India.

Third volume describes the various programmes introduced to empower women and bring

them into the orbit of development network.

Jaya S. Anand (2002), in her discussion paper titled “Self-Help Groups in

Empowering Women: Case Study of Selected SHGs and NHGs”, gives a review of progress

of Self Help Groups. She has attempted to examine the performance of selected SHGs and

NHGs and to assess its impact, especially the impact of micro credit programme on

empowering women. It has been clearly established that delivering credit alone may not

produce the desired impact. The supporting services and structures through which credit is

delivered, ranging from group formation and training to awareness-raising and a wide range

of other supporting measures are critical to make the impact of group activity strong and

sustainable.

Puhazhendhi and Satyasai (2001) in their study attempted to evaluate the

performance of SHGs with special reference to social and economic empowerment. Primary

data collected with the help of structured questionnaire from 560 sample households in 223

SHGs functioning in 11 states representing four different regions across the country have

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 15

formed the basis of the study. The findings of the study reveal that the SHGs as institutional

arrangement could positively contribute to the economic and social empowerment of rural

poor. The impact on the later is more pronounced than on the former. Though there has been

no specific pattern in the performance of SHGs among different regions, the southern region

could edge out other regions. The SHGs programme has been found more popular in the

southern region and its progress in other regions is quite low, thus signifying an uneven

achievement among the regions. Older groups had relatively more positive features like better

performance than younger groups.

SakuntalaNarasimhan (2001) , focuses specifically on rural Scheduled Caste and

Scheduled Tribe women, who are disadvantaged as women, as members of the rural section

of the laypeople and because of their low caste status. The book compares the effectiveness

of State initiatives with the motivation - and conscientisation strategy advocated by Action

for Welfare and Awakening in Rural Environment (AWARE), a non-governmental

development organization working in 6000 villages spread over 7 States in India. It analyses

the success of AWARE’s work among women through various case studies and concludes

that, besides monetary resources, it is the mindset of the policy makers, bureaucrats and

particularly the women concerned that must change in order to assist the empowerment of

women.

Gurumoorthy (2000) reveals that empowering women contributes to social

development. Economic progress in any country whether developed or underdeveloped could

be achieved through social development. The self-help group disburses micro-credit to the

rural women for the purpose of making them enterprising women and encouraging them to

enter into entrepreneurial activities. Credit needs of the rural women are fulfilled totally

through the self-help groups. SHGs enhance equality of status of women as participants,

decision makers and beneficiaries in the democratic economic, social and cultural spheres of

life. SHGs also encourage women to take active part in socio-economic progress of our

nation.

Dr.Muralidhar A. Lokhande conducted a case study of

MahilaArthikVikasMahamandal in Maharashtra, founded micro financing helps the

development of unprivileged people. His study is based on following expansion of business

activities, gainful employment, increased income, regular savings, awareness regarding

financial matters, increased social relation, feeling of social security, etc. The study

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 16

conducted by Amith Roy and Dr.SamanashDutta in Assam founded the SHG members earn

high income from microenterprises, but low scale of operation, lack of job training, need for

the strengthening of SHG- Project Market Linkage, etc create barriers.

Now it is apparent that a number of studies are conducted on SHG groups and

Kudumbashree and its role on empowerment of women. The researcher is intended to study

to know to what extend Kudumbashree programme in Kerala has influenced the rural women

for their empowerment.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 17

CHAPTER 3

CONCEPTUAL FRAMEWORK

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 18

INTRODUCTION

The history of micro financing can be traced back to early 1700s when Jonathan Swift, an

Irishmen had the idea to create the banking system that would reach the poor. He creates the

Irish loan fund, which gave small short loan to the poorest people in Ireland who were not

being served by commercial banks. In the 1800s similar banking systems showed up all

across Europe targeting the rural and urban poor. Friedrich Wilhelm Raiffeisen of Germany

realized that the poor people were being taken advantage of by loan sharks. He acknowledged

that under the current lending system, the poor would never be able to create wealth. He

founded the first rural Credit Union in 1864 to break this trend. The idea of Credit Union

spread globally and by the end of the 1800s.

The pioneering of modern microfinance is often credited to Dr. Mohammed Yunus ,

who begun experimenting by lending to poor women in the village of Jobra, Bangladesh,

during his tenure as a professor of economics at Chittagong University in 1970s.

In recent time the World Bank estimates that about more than 160 billion people in

developing countries are served by microfinance. Microfinance is being practiced as a tool

for socio-economic development.

Government of India and RBI has taken several initiatives to expand access to

financial systems to the poor. Some of the measures are nationalization of banks, prescription

of priority sector lending, differential interest rate schemes for the weaker sections, and

development of credit institution like RRB.

The provision of comprehensive financial services in rural areas encompassing

savings, credit remittance, insurance, and pension products and establishing linkages between

banks and external entities based on two broad models namely Business Facilitator model

and Business Correspondent model.

Under Business Facilitator model the banks may use a wide array of Civil Service

Organization and others for providing facilitation services. Under Business Correspondent

model, it is envisaged that institutional agents, other external entities would act as Business

Correspondent for extending financial services.

In India, there are two model of microfinance based on these two models, SHG –

Bank Linkage Programme (SBLP) and MFI model.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 19

MFI model comprising various entities such as Non Banking Financial Companies,

Non Governmental Organizations, trusts, Co-operatives etc.

NABARD defined the term the “microfinance” as “provision of thrift, credit and other

financial services and products of very small amounts the poor in rural, semi urban to urban

areas, for enabling them to raise their income level and improve living status”.

SHG is a group with an average size of about 15 people from a homogeneous class.

They come together for addressing their common problems. They are encouraged to make

voluntary thrift on a regular basis. They use this pooled resource to make small interest

bearing loans to their members, the balance is maintained in the saving accounts with the

banks. Once the group shows the mature financial behaviour, banks are encouraged to make

loans to the SHG in certain multiple of the accumulated savings of the SHG. The bank loans

are given without any collateral and at market interest rate.

As per the latest estimate, SHG –Bank Linkage Programme enabled 103 million poor

households access to sustainable financial service from the banking system and has an

outstanding institutional credit exceeding Rs.36340 cores as at the end March 2012. The

balance in the saving accounts of the bank as at end of March 2012 stood at Rs.6551.41

crores.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 20

KUDUMBASHREE- A MICROFINANCE PROGRAMME IN KERALA

The kudumbashree is a comprehensive poverty alleviation programme in Kerala

focuses primarily on microfinance and micro enterprises. These poor women oriented Self

Help Group programme is a unique one. The spark of the community based, women oriented,

participatory approach to poverty eradication occurred in Alappuzha Municipality in 1993

through Urban Based Self-Employment Programme (UBSP) with the assistance of UNISEF.

The same model was experimented in the entire district of Malappuram also with a unique

poverty alleviation programme called Community Based Nutrition Programme and Poverty

Alleviation Project (CBNP-PA). The success CDS system of Alappuzha town and

Malappuram district promoted the State Government to accept the CDS of poor women as a

meaningful strategy.

In 1998 State Government with the support of Central Government and NABARD set

up an establishment called State Poverty Eradication Mission or Kudumbashree. The Prime

Minister Shri A.B Vajpayee inaugurates the programme in Malappuram.

The Kudumbashree Programme was extended through three stages (2000 June, 2001

September, 2002 March), on the basis of this Kudumbashree CDS was launched in all

gramaPanchayath. At last in 2010 Kudumbashree was launched in Edamalakudi Tribal

Panchayath.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 21

The slogan of the mission is “Reaching out to families through women and reaching

out to communities through families”. Microfinance is the essence of rural areas which

ultimately result the rural development. The development must require the social justice and

equal opportunity to realize the great potential for the poorest of the poor and Kudumbashree

is doing the same. The mission statement of Kudumbashree is “To eradicate absolute poverty

through concerted community action under the leadership of local governments, by

facilitating organization of the poor for combining self-help with demand-led convergence of

available services and resources to tackle the multiple dimensions and manifestations of

poverty, holistically.

As on 2012, Kudumbashree has covered 3,653,655 families through 211,578 NHGs,

18,183 ADSs and 1,061 CDSs in Kerala. Kudumbashree provided 4,956.11 cores as internal

loan and the balance of thrift savings is 1,666 cores. The Kudumbashree used 1,399 cores as

linkage loan.

In Malappuram District, Kudumbashree covered 373,937 families through 19,931

NHGs, 2,081 ADSs and 110 CDSs. The Kudumbashree have an internal loan of

2,743,233,969 cores, thrift savings of 1,329,125,647 cores and linkage loan of 398,044,699

cores.

In Areekode Panchayath Kudumbashree covered 4,890 families through 282 NHGs,

22 ADSs, 3,03,11,420 cores internal loan, 1,98,71,262 cores thrift savings and 41,05,000 lakh

linkage loan.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 22

STRUCTURE OF KUDUMBASHREE

Kudumbashree follows a three tier Community Based Organization (CBO).

Figure: 3.1

Structure of CBOs in Kudumbashree

NEIGHBOURHOOD GROUP (NHG)

The lowest tier constitutes the Neighbourhood Group consisting of 10-20 women members

selected from the poor families and the women of families are part of the meetings. The

main objective of Neighbourhood Group is to collect micro deposits and distribute the loan

among members. In each Neighbourhood Groups 5 volunteers are selected from among them.

NHG 5 Member Volunteer

Team

ADS 7 Member Leadership

CDS General Body

Monitoring & Advisory

Committee

Governing Body-9

Member Committee

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 23

Table: 3.1

Salient Features of Neighbourhood Groups

Salient Features of the NHG

Membership Women 18 years of age and above from

economically weaker families from the

area covered by the group;

Membership limited to one from a family,

but other women family members can take

part in discussions and activities,

All members of the NHG from the General

Body Special NHG for ST Communities

Executive

Committee =5

Members

President, Secretary, Income Generation

Volunteer, Health & Education Volunteer,

Basic Infrastructure Volunteer

Affiliation with

CDS

To be renewed every year

Election of

Executive

Committee

Once in three years; At the special meeting

of the NHG convened for the purpose, as

part of the general election process in the

CDS; Either the President or Secretary

should be from a BPL family; Same person

can be President or Secretary only for two

consecutive terms

Fund Fund of the NHG made up of membership

fees, interest and penal interest earned

from lending to members, donations,

receipts from activities etc.

Thrift and credit Collection of thrift on a regular basis and

its accounting; Managing thrift account

with local bank; Lending to members from

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 24

AREA DEVELOPMENT SOCIETY (ADS)

The second tier of the organizational structure known as Area Development Society.

It is formed at ward level of Panchayath/municipality by federating 10-15 NHGs. Area

Development Society functions through General body and Governing body.

➢ General body: - consisting of the president, secretary and 3 sect oral volunteers such

as Health, Income Generation and Infra structure Volunteers of federated NHGs.

➢ Governing body: - constitutes President, Secretary and 5 members elected from

among the General body.

An important feature of ADS is its linkage with local Government. Records maintained

by ADS include Minutes Book, Notice Book, General Body-Executive Committee

thrift funds based on terms developed by

the group

Bank Linkage Obtain grading as per NABARD grading

norms Bank Linkage for graded groups

Activity Groups Members from the NHG along with

members of other NHGs form activity

groups for micro enterprises, joint liability

groups, etc.

Records maintained

by NHG

Minutes book, Membership Register,

Thrift Register, Loan Register, Monthly

Report of Thrift and Credit, Membership

fees and penalty register, Assets register,

Revolving Fund-Grants-Aid register,

Affiliation file, Micro Enterprise Register,

Bank Pass Book, Annual Receipts and

Payment Statement and Audited accounts

Audit Accounts of the NHG are audited by the

Kudumbashree Accounting and Auditing

Service Society(KAASS); Internal audit is

taken up by the NHG

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 25

membership register, Affiliation Register, Cash Book, General Ledger, Stock register, Micro

Enterprise Register, Bank Pass Book, Annual Receipts and payment Statement and Audited

accounts, Monthly report of thrift and credit activities of NHGs, and NREGS works in its

area. The election is conducted once in every 3 year per the General Election Process.

Accounts of the ADS are audited by the Kudumbashree Accounting and Auditing Service

Society (KAASS); internal audit is taken up by the ADS.

COMMUNITY DEVELOPMENT SOCIETY (CDS)

Community Development Society, a registered body under the Charitable Society

Act is formed by various ADSs at the Panchayath/municipality level. As in the case of ADS,

the CDS has also a General body and Governing body.

➢ General body: - consists of all the chair persons and Governing body members of

ADS along with Resource persons and officers of local body who are involved in

implementing various poverty alleviation and women empowerment.

➢ Governing body: - consists of President, Member Secretary and 5 selected Committee

members.

Accounts of the CDS are audited by a Chartered Accountant (with support of KAASS);

internal audit is taken up by the CDS. The role of CDS includes Local Self Government

liaison, Linkage Banking co-ordination, information dissemination, community network

strengthening activity, facilitating income generating activity, facilitation of Centrally

Sponsored Scheme, etc.

MAJOR ACTIVITIES OF KUDUMBASHREE

PROGRAMME

MICROFINANCE

Microfinance is the most grassroots level activity of Kudumbashree. It is the binding

force of NHGs. Each NHG has operational flexibility in respect of its microfinance

operations. Formation of informal banks of poor women in every locality of the state with

regular and continuous thrift and credit operations and setting up of micro enterprises are

major activities.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 26

The various activities under microfinance by Kudumbashree are:

Thrift and Credit

Each NHG act as a Thrift and Credit Society and facilitates the poor to save and to

provide them cost effective and easy credit. A member can avail loan up to a maximum of 4

times of his savings without any collateral security. The repayment of the loan is collected

weekly. The interest income from thrift can also be used for loans. The main feature of

Kudumbashree Programme is the facility for poor women to save and borrow from their own

pooled savings.

Bank Linkage Programme

Banks are advised through RBI guidelines lo lend up to 5 lakh to SHGs without any

collateral securities. In addition to the loan from their own savings, NHGs are facilitated to

avail loan from bank through Bank Linkage Programme.

NABARD has developed the following 15 point index for rating NHGs on the basis

of which they will be allowed to link with various banks under the Linkage Banking

Programme.

1. Structure of SHG.

2. Period of operation.

3. Number of meeting held.

4. Attendance in meeting.

5. Recording of minutes.

6. Participation in discussion.

7. Promotion of thrift.

8. Thrift accounting.

9. Decision making.

10. Loan sanctioning procedure.

11. Rate of interest changed.

12. Velocity of lending.

13. Percentage of repayment.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 27

14. Maintenance of records and Registers.

15. Bye law.

The fund can be utilized by the groups for internal lending and setting up of micro

enterprises.

Matching Grant

Matching grand is an incentive provided to NHGs. This grant linked to the amount of

thrift mobilized, performance of NHG in the grading and loan availed from banks. An

amount of 10% of the savings of NHG subject to maximum of Rs.5000 is provided as

matching grant to each NHG. The grant is released based on their assessment rated using a 15

point grading criteria developed by NABARD. In order to avail matching grand NHG must

have passed the grading.

Interest Subsidy

As per the scheme, all commercial and cooperative banks that are prepared to lend to

Kudumbashree NHGs under the linkage banking programme at 9% or below, will be the

participants in the scheme. The 5%will be paid by Government through Kudumbashree.

MICRO ENTERPRISES

Micro enterprises development is a means for economic empowerment by providing

gainful employment to the people below poverty line and thereby improving their income and

living standards. These micro enterprises posses certain criteria like:

➢ The capital of Rs.5000-Rs.500000.

➢ Enterprise should have a potential to generate at least Rs.1500 per month either by

way of wage or profit or both together.

➢ Enterprise fully owned, managed and operated by members themselves.

➢ Minimum turnover of Rs. 500000.

➢ It can be started as group enterprise or individual enterprise.

A special employment programme launched by the State Government to support the

educated youth was assigned to Kudumbashree which is known as Yuvashree.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 28

50K Programme was to identify the innovative areas to set up micro enterprises for the

youth. Under this programme male groups are allowed to enter in this scheme through the

support of female kudumbashree member in their family.

HOUSING

Currently there are two housing programme namely Bavanashree and VAMBAY.

Bavanashree is the programme which facilitates to get loans to the homeless people

for the construction of houses from the Banks.

ValmikiAmbedkarAwasYojana is a newly formulated centrally sponsored scheme for

the benefit of the slum dwellers. The scheme mainly aims at ameliorating the housing

problems of the slum dwellers living below poverty lines in different towns.

AGRICULTURE

For agricultural purposes Kudumbashree introduce Lease Land Group Farming or

Harithashree. Lease Land Farming aims at helping both the landless poor women of

Kudumbashree NHGs and the landowners who are not interested in farming.

REHABILITATION OF DESTITUTE PROGRAMME

Asraya is the programme which implemented in order to identify and rehabilitate the

poorest among poor families. Those identified under the project are provided with livelihood

necessities such as food, clothing, health coverage, pension, education; basic necessities like

house, water, sanitation facilities, and development needs like vocational training, personality

development trainings, care services like counselling and other training programmes.

EDUCATION AND CHILDREN WELFARE

Buds Special School is an innovative model developed by the Kudumbashree Mission for the

development and protection of mentally challenged children to enable them to access to

education and training within their community. The experimental project was launched in

2004 at Venganoor with the ownership of GramaPanchayath. The success of the model was

appreciated and the Government of Kerala sought the model to be replicated with the

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 29

guidance and support of Kudumbashree. Balasabhas are groups of children at the grass root

level. Balasabhas, organized in line with the CBO network of the mission, aim at the capacity

and confidence building of BPL children through a variety of initiatives and activities,

orchestrated for their creative, emotional, educational, and intellectual development.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 30

CHAPTER 4

DATA ANALYSIS AND INTERPRETATION

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 31

DATA ANALYSIS AND INTERPRETATION OF MICROFINANCE THROUGH

KUDUMBASHREE UNITS

This chapter deals with analysis and interpretation of data collected with the help of

questionnaire and interview schedule. The present study is intended to analyze the impact of

microfinance through kudumbashree and problems related with kudumbashree unit in

Areekode panchayath. The data is analyzed and presented in the form of table with necessary

interpretation along side. Various type of statistical methods are used for analysis of data.

This analysis is supplemented by explanation, tables, and diagrams.

The data analyzed and interpreted on the basis of:

• Socio- economic profile of the sample members.

• Overall performance of kudumbashree.

• Impact of microfinance.

• Purpose of obtaining microfinance by members.

• Problems of kudumbashree units.

OVERALL PERFOMANCE OF KUDUMBASHREE

This section analysis the data collected through interview schedule to study the overall

perfomance of kudumbashree units in Areekode panchayath on the basis of following factors.

• Accumulated savings

• Internal loan allowed

• Matching grant received

• Number of members in the unit

• Subsidy received

• Number of meeting per month

• Hours of meeting

• Average attendance of meeting

• Participation level of members in the unit

• Savings collection within the group per month

• Utlisation of savings amount

• Status of loan recovery

• Participation of unit in government offered programmes

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 32

ACCUMULATED SAVINGS (YEARLY)

Here,the units are classified on the basis of thrift collected by them.The accumulated

savings are categorised in the study as:

25000-50000, 50000-75000,75000-100000,morethan100000.

Table:4.1

Accumulated savings in kudumbashree units

Accumulated savings Number of KDS units Percentage

25000-50000 15 15

50000-75000 10 10

75000-100000 20 20

Morethan100000 55 55

Total 100 100

Source: primary data

Interpretation:

From the above table 55% of sample units have morethan 100000 accumulated

savings which means they are in a good position. 20% of sample units are in satisfactory

position.15% of sample units are in unsatisfactory position.The same data furnished below as

a picture. Figure:4.1

Accumulated savings in kudumbashree units

0

10

20

30

40

50

60

25000-50000 50000-75000 75000-100000 Morethan100000

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 33

INTERNAL LOAN ALLOWED (YEARLY)

The units are studied on the basis of credit allowed from their own accumulated

savings.

Table: 4.2

Internal loans allowed by KDS units

Internal loan allowed Number of KDS units Percentage

Less than 25% of

accumulated savings

15 15

25-50% of accumulated

savings

30 30

More than 50% of

accumulated savings

55 55

Total 100 100

Source: primary data

Interpretation:

The above table shows 15% of units uses more than 50% of accumulated savings as

internal loan and are in very good region. 30% of units are satisfactory.majority of thr units

are in unsatisfactory region ie, 55%. Figure 4.2

Internal loans allowed by KDS units

15%

30%55%

Number of KDS Units

Less than 25%of accumulatedsavings

More than 50%of accumulatedsaving

25%-50%of accumulated savings

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 34

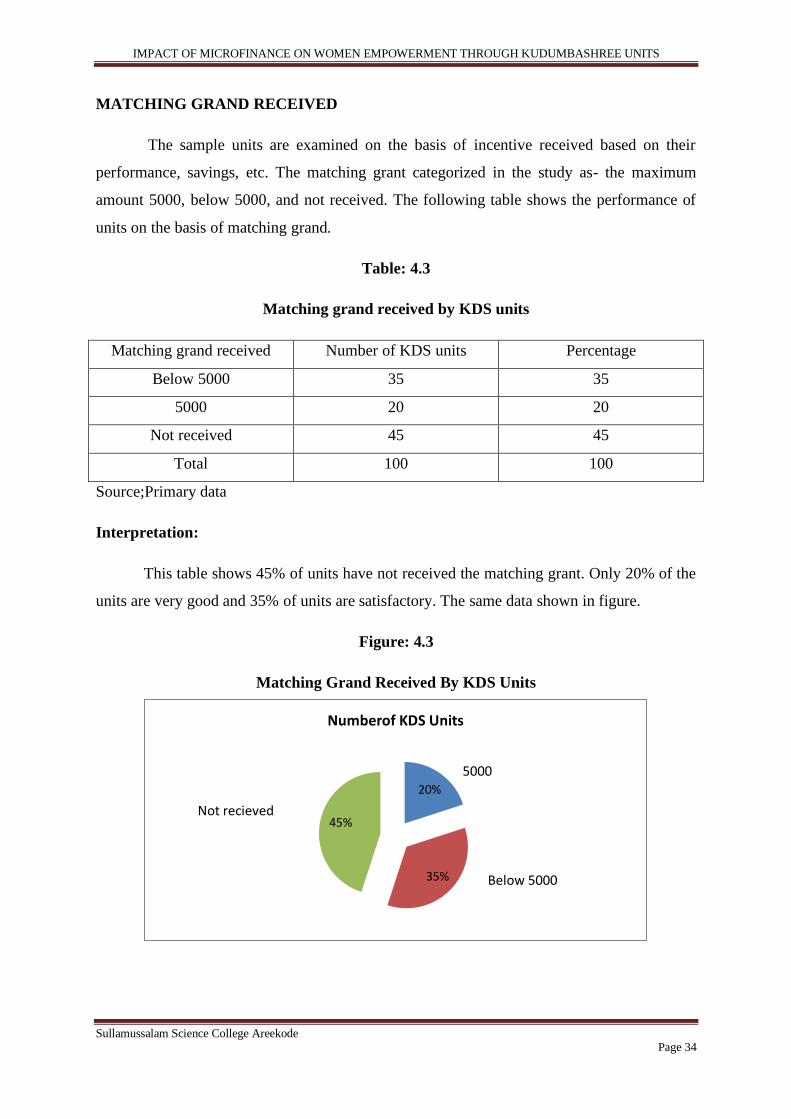

MATCHING GRAND RECEIVED

The sample units are examined on the basis of incentive received based on their

performance, savings, etc. The matching grant categorized in the study as- the maximum

amount 5000, below 5000, and not received. The following table shows the performance of

units on the basis of matching grand.

Table: 4.3

Matching grand received by KDS units

Matching grand received Number of KDS units Percentage

Below 5000 35 35

5000 20 20

Not received 45 45

Total 100 100

Source;Primary data

Interpretation:

This table shows 45% of units have not received the matching grant. Only 20% of the

units are very good and 35% of units are satisfactory. The same data shown in figure.

Figure: 4.3

Matching Grand Received By KDS Units

20%

35%

45%

Numberof KDS Units

5000

Not recieved

Below 5000

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 35

NUMBER OF MEMBERS IN THE UNIT

In the study numbers of members are categorized as below 10 members,10-15

members,15-20 members,more than 20 members. The following table shows the details

regarding number of member in the units.

Table: 4.4

Number of Members in the units

Number of members in the

unit

Number of KDS units Percentage

Below 10 members 20 20

10-15 members 35 35

15-20 members 30 30

More than 20 members 15 15

Total 100 100

Source:primary data

Interpretation:

Based on the above table 20% of units are included below 10 members.But,majority

35% units are include 10-15 members.

Figure:4.4

Number of members in the unit

Below 10 members

10-15 members

15-20 members

More than 20 members

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 36

SUBSIDY RECEIVED

For studying about subsidy received, the sample units are categorized in the study as,

1 or 2 times, more than 2 times, and not received. The table 4.5 shows the classification of

sample units on the basis of subsidy received.

Table 4.5

Distributions of Sample Units on the Basis of Subsidy Received

Subsidy received Number of KDS Units Percentage

1 or 2 times 25 25

More than 2 times 15 15

Not received 60 60

Total 100 100

Source: primary data

Interpretation:

It is clear from the above table that majority 60% of units are not received the subsidy

and are unsatisfactory. Only 15% of units have received subsidy for more than 2 times. 25%

units have received subsidy for 1 or 2 times. The 4.6 show the same data.

Figure 4.5

Distributions of Sample Units on the Basis of Subsidy Received

0

10

20

30

40

50

60

1 or 2 times More than 2times

Not received

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 37

NUMBER OF MEETINGS PER MONTH

The sample units are studied on the basis of number of meeting conducted by the

units in a month. For this the units are classified on the basis of following. Less than 2

meeting,2-3 meeting,more than 3 meeting The following table shows the distribution of units

on the basis of number of meetings conducted.

Table: 4.6

Number of meetings per months in KDS

Number of meeting per

month

Number of KDS units Percentage

Below 2 meeting 10 10

2-3 meetings 30 30

More than 3 meeting 60 60

Total 100 100

Source: primary data

Interpretation:Based on Table: 4.6, 60% of units conduct more than 3 meetings in a month.

30% units are conduct 2-3 meetings in a month. Only 10% units are in unsatisfactory

category.The figure: 4.6show the diagrammatic presentation.

Figure 4.6 Number of meetings per month in KDS

0

10

20

30

40

50

60

Below 2 meeting 2-3 meetings More than 3meeting

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 38

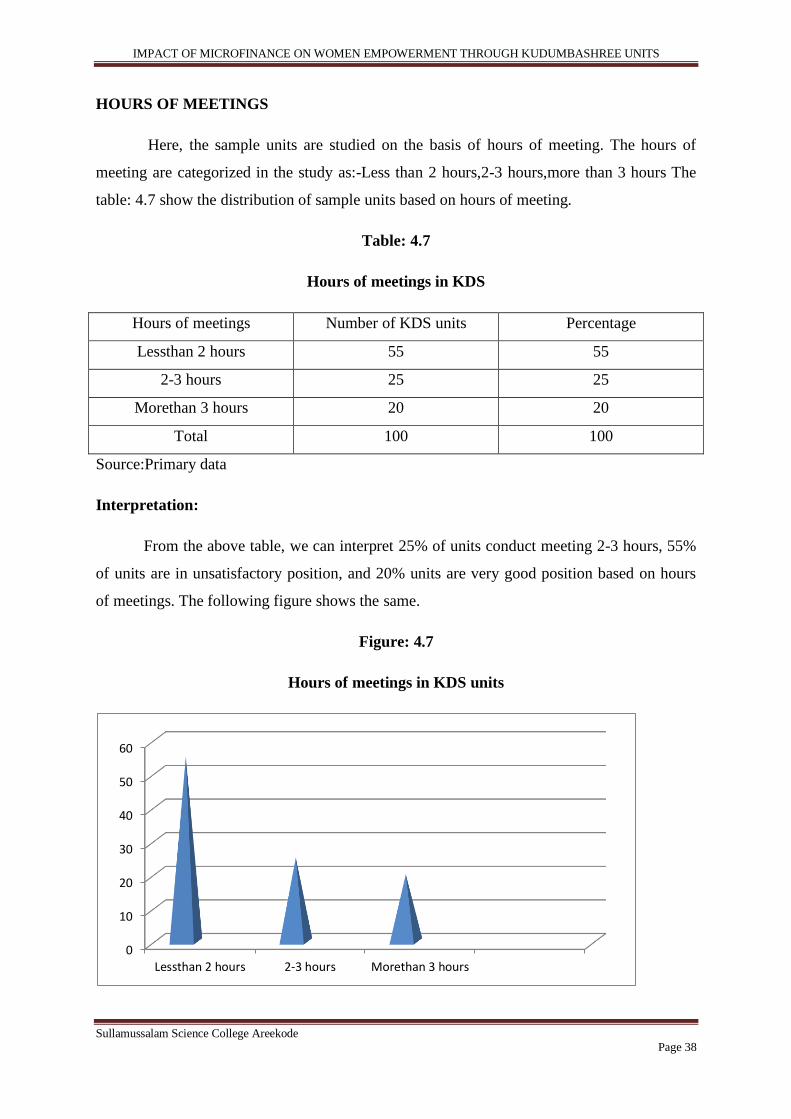

HOURS OF MEETINGS

Here, the sample units are studied on the basis of hours of meeting. The hours of

meeting are categorized in the study as:-Less than 2 hours,2-3 hours,more than 3 hours The

table: 4.7 show the distribution of sample units based on hours of meeting.

Table: 4.7

Hours of meetings in KDS

Hours of meetings Number of KDS units Percentage

Lessthan 2 hours 55 55

2-3 hours 25 25

Morethan 3 hours 20 20

Total 100 100

Source:Primary data

Interpretation:

From the above table, we can interpret 25% of units conduct meeting 2-3 hours, 55%

of units are in unsatisfactory position, and 20% units are very good position based on hours

of meetings. The following figure shows the same.

Figure: 4.7

Hours of meetings in KDS units

0

10

20

30

40

50

60

Lessthan 2 hours 2-3 hours Morethan 3 hours

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 39

AVERAGE ATTENDANCE IN THE MEETING

For studying the attendance level of members in the meeting the sample units are

categorized as :-Less than 50%,50-70%,70-90%,more than 90%. The table: 4.9 gives the

details about the sample units based on average attendance of members in the meeting.

Table: 4.8

Attendance levels of members in the meeting

Average attendance of

meetings

Number of KDS units Percentage

lessthan 50% 10 10

50%-70% 15 15

70%-90 20 20

Morethan 90% 55 55

Total 100 100

Source: primary data

Interpretation: From the above table, it is clear that 55% of units have morethan 90%

attendance (very good position), 20% of units have 70%-90% attendance (good position), 20

% of units have 70%-90% of attendance (satisfactory position) and 15% of units have50%-

70% of attendance (unsatisfactory position) .The following figure shows the same data.

Figure: 4.8: Attendance levels of members in the meeting

lessthan 50%

50%-70%

70%-90

Morethan 90%

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 40

PARTICIPATION LEVEL OF MEMBERS IN THE MEETINGS

The participation level of members is categorized in the study as:-very low,Low,

medium,High,Very high. The following table shows the details.

Table: 4.9

Participation levels of members in the meeting

Participation level of

members in the meeting

Number of KDS units Percentage

Very low 10 10

low 15 15

medium 25 25

High 20 20

Very high 30 30

Total 100 100

Source:Primary data

Interpretation:

From the above table, we can interpret 30% of have very high participation level of

members in the meeting and very good position in this regards. 25% of units are good. Only

10% units are unsatisfactory. The following figure shows the graphical presentation of the

same data.

Figure: 4.9

Participation levels of members in the meeting

0

5

10

15

20

25

30

35

very low low medium high very high

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 41

COLLECTION OF SAVINGS WITHIN THE UNIT PER MONTH

The sample units are studied on the basis of savings collected within the group per

month. In this study savings collection are categorized as less than 2 times in a month, 2 -3

times in a month, and more than 3 times. The following table shows the classification in this

regard.

Table: 4.10

Collections of savings within the units

Collection of savings Number of KDS units Percentage

Lessthan 2 times 10 10

2 -3 times 30 30

More than 3 times 60 60

Total 100 100

Source:Primary data

Interpretation:

From the above table, 60% of units collect the savings more than 3 times in a month,

30% of units collect their savings 2-3 times in a month. The remaining 10% collect the

savings lessthan 2 times. The same data shows as picture below.

Figure: 4.10

Collections of savings within the units

number of KDS units

Lessthan 2 times

2 -3 times

More than 3 times

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 42

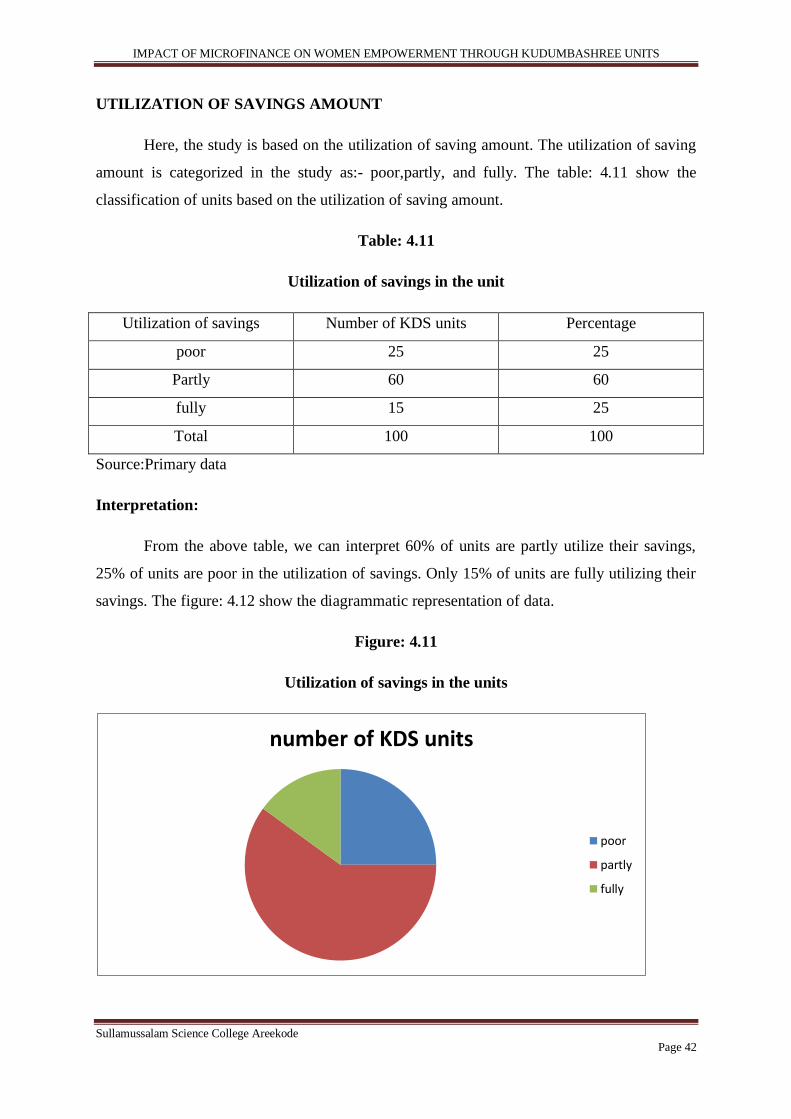

UTILIZATION OF SAVINGS AMOUNT

Here, the study is based on the utilization of saving amount. The utilization of saving

amount is categorized in the study as:- poor,partly, and fully. The table: 4.11 show the

classification of units based on the utilization of saving amount.

Table: 4.11

Utilization of savings in the unit

Utilization of savings Number of KDS units Percentage

poor 25 25

Partly 60 60

fully 15 25

Total 100 100

Source:Primary data

Interpretation:

From the above table, we can interpret 60% of units are partly utilize their savings,

25% of units are poor in the utilization of savings. Only 15% of units are fully utilizing their

savings. The figure: 4.12 show the diagrammatic representation of data.

Figure: 4.11

Utilization of savings in the units

number of KDS units

poor

partly

fully

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 43

STATUS OF LOAN RECOVERY

Here, the sample units are studied on the basis of status of loan recovery. The status of

loan recovery categorized the study as:-Less than25%,25-50%,50-70%,70-90%,more than

90%. The following table shows the status of loan recovery in KDS unit.

Table: 4.12

Status of loan recovery

Status of loan recovery Number of KDS units Percentage

less than 25% 2 2

25%-50% 3 3

50%-70% 10 10

70%-90% 30 30

More than 90% 55 55

Total 100 100

Source:Primary data

Interpretation:

From the above table, 55% of units are very good in status of loan recovery; they

recovered more than 90% of loan. 30% of units are in good position, they recovered 70%-

90% loan amount. The remaining 15% of units are unsatisfactory. The figure: 4.1 show the

data are graph.

Figure: 4.12

Status of loan recovery

less than 25%

25%-50%

50%-70%

70%-90%

More than 90%

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 44

PARTICIPATION OF UNITS IN GOVERNMENT OFFERED PROGRAMMES

The participation level is categorized in the study as:-Very

low,Low,Medium,High,Very high. The table: 4.13 show the classification of units on the

basis of participation of government offered programmes.

Table: 4.13

Participation of units in government offered programmes

Participation level Number of units Percentage

Very low 2 2

Low 10 10

medium 13 13

High 25 25

Very high 50 50

Total 100 100

Source:Primary data

Interpretation:

From the above table, 50% of units are very high participation in government offered

programmes. 25% of units are high participation in government offered programmes. The

10% units are low participation. The figure: 4.13show the same data.

Figure: 4.13

Participation of units in government offered programmes

0

20

40

60

Very low low medium high Very high

number of KDS units

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 45

ROLE OF GOVERNMENT AGENCIES FOR THE PROMOTION OF

KUDUMBASHREE

One of the objectives is to study the role of government agencies for the promotion of

KDS, for this purpose question number 29 of the questionnaire is analyzed. The five variables

are studied under this section; that are generation of employment, granding financial

assistance, eradication of poverty, improve the status of women, and setting up of training

programme. The table: 4.14 Show the members responses.

Table: 4.14

Role of Government Agencies in KDS

Variables Likert scale Frequency Likert score Percentage

Generation of

employment

Always 11 55 11

Frequently 35 140 35

Occasionally 37 111 37

Rarely 17 34 17

Never - - -

Total 100 340 100

Average 3.40

Granting

financial

assistance

Always - - -

Frequently 13 52 13

Occasionally 45 135 45

Rarely 42 84 42

Never - - -

Total 100 271 100

Average 2.71

Eradication of

poverty

Always - - -

Frequently 11 44 11

Occasionally 34 102 34

Rarely 52 104 52

Never 3 3 3

Total 100 253 100

Average 2.53

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 46

Improve the

status of women

Always 9 45 9

Frequently 45 180 45

Occasionally 41 123 41

Rarely 5 10 5

Never - - -

Total 100 358 100

Average 3.58

Setting up of

training

programmes

Always - - -

Frequently 33 132 33

Occasionally 48 144 48

Rarely 19 38 19

Never - - -

Total 100 314 100

Average 3.14

Interpretation:

From the table: 4.14, 37% of sample members say the role of Government Agencies

in generation of employment is medium. 45% of sample members denote the role of

Government Agencies in grating financial assistance is medium. 52% of members say role of

Government Agencies in eradication of poverty is unsatisfactory. 45% of members are

satisfied with role of Government Agencies in improving status of women. The majority 48%

of members are less satisfied with the role of Government Agencies in setting up of training

programme.

The table shows the high weighted average 3.58 in the variable “improve the status of

women” and low weighted average 2.53 in the variable “eradication of poverty”. So we can

interpret, from the five variables members are highly satisfied with the role of Government

Agencies in improving the status of women and satisfaction level is very poor in eradication

of poverty.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 47

IMPACT OF MICROFINANCE

Microfinance is the provision of financial services to low income people. The goal of

microfinance is to give low income people an opportunity to become self sufficient by

providing a means of saving money and borrowing money. Another aim of microfinance is to

empower women economically, socially, and psychologically. The impact of microfinance is

studied through the members of kudumbashree units on the basis of followings:

• Change in the level of indebtedness from money lenders/chitties.

• Changes of indebtedness from religious organizations.

• Changes of indebtedness from loan taken from government & funding agencies.

CHANGE IN THE LEVEL OF INDEBTEDNESS OF MEMBERS

In this section, question number 10 of the questionnaire is analyzed regarding the

change in the level of indebtedness of members. The members who have debts from the

informal sources were categorized into loans availed from moneylenders and chitties,

religious organizations and from government and other funding agencies. The contribution of

microfinance programme in the reduction of outside loan among the KDS members was

tested by applying “Z test” to test the proportions of increase during pre-KDS and post-KDS

period.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 48

CHANGES OF INDEBTEDNESS FROM MONEYLENDERS/CHITTIES

H0: There is no significant improvement in the indebtedness of members from money lenders

and chitties through the intervention of microfinance programme.

Table 4.15

Change of Indebtedness from Moneylenders/chitties

Total number

of

respondents

Pre KDS Post KDS

Number of

respondents

taking loan

Proportion(P1) Number of

respondents taken

loan

Proportion

(P2)

100 30 0.30 10 0.10

Z=P1-P2/SE

=0.30-0.10/0.0458

=4.366

Interpretation:

The calculated value 4.366 is greater than the table value (2.326) at level of

significance =1% and degree of freedom=infinity.

Therefore the null hypothesis is rejected and there is significant improvement in the

indebtedness of members from moneylenders through the intervention of microfinance

programme.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 49

CHANGES OF INDEBTEDNESS FROM RELIGIOUS ORGANIZATION

H0: There is no significant improvement in the indebtedness of member from religious

organizations through the intervention of microfinance programme.

Table: 4.15A

Changes in indebtedness from religious organizations

Total number of

respondents

Pre KDS Post KDS

Number of

respondents

taken loan

Proportion (P1) Number of

respondents

taken loan

Proportion (P2)

100 25 0.25 15 0.15

Z= P1-P2/SE

=0.25-0.15/0.0433

=2.309

Interpretation:

The calculated value 2.309 is less than the table value (2.326) at level of

significance=1% and degree of freedom = infinity.

Therefore the H0 is accepted. We can interpret that there is no significant

improvement in the indebtedness of members from religious organizations through the

intervention of microfinance programme.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 50

CHANGES OF INDEBTEDNESS FROM LOAN TAKEN FROM GOVERNMENT &

FUNDING AGENCIES

H0: There is no significant improvement in the indebtedness of members from loan taken

from government and funding agencies through the intervention of microfinance programme.

Table: 4.16

Changes of Indebtedness from Loan Taken from Government/funding agencies

Total Number of

respondents

Pre KDS Post KDS

Number of

respondents

taken loan

Proportion(P1) Number of

respondents

taken loan

Proportion(P2)

100 45 0.45 20 0.20

Z=P1-P2/SE

=0.45-0.20/0.0494

=5.0301

Interpretation:

The calculated value 5.0301 is greater than the table value (2.326) at level of

significance=1% and degree of freedom=infinity.

Therefore the H0is rejected. We can interpret that there is significant improvement in

the indebted.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 51

PURPOSE OF OBTAINING MICROFINANCE BY RESPONDENTS

This part analyzes the question number 28 of the questionnaire to know the purpose of

obtaining loan by the members from kudumbashree units. The following table shows

preference of members for obtaining loan in various purposes. The weighted average is used

to rank the purpose.

Table: 4.16A

Purpose of obtaining microfinance by members

Sl.

No

Purpose Alw

ays

(5)

Freque

ntly

(4)

Occasi

onally

(3)

Rare

ly

(2)

Never

(1)

Scor

e

Weight

ed

average

Ran

k

1 Day to day

expenditure

- 4 8 17 71 145 1.45 VII

2 Children’s

education &

welfare

7 36 23 18 16 300 3 I

3 Medical

expenditure

4 21 48 19 8 294 2.94 II

4 Children’s marriage - - - 18 82 118 1.18 IX

5 Housing - 8 32 54 6 242 2.42 III

6 Promote/ start

business

- 5 26 9 60 176 1.76 VI

7 Providing

electricity, drinking

water, sanitation

facility, etc

- 7 34 46 13 235 2.35 IV

8 Repayment of loan - - - 18 82 118 1.18 IX

9 Purchase of house

hold items

- - 18 75 7 211 2.11 V

10 Others - - 3 18 79 124 1.24 VIII

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 52

Interpretation:

Table: 4.18 shows responses of sample members with regards to various purposes of

obtaining loan. From the above table we can interpret that majority of the members are taking

loan for children’s education and welfare (Rank I, weighted average 3). The next purpose of

obtaining loan is for medical expenditure (Rank II, weighted average 2.94). the least

preference for obtaining loan is for children’s marriage.

RESPONDENTS EDUCATION QUALIFICATION AND OBTAINING

MICROFINANCE FOR CHILDRENS EDUCATION AND WELFARE

To know the association between respondents’ education qualification and obtaining

microfinance for children’s education and welfare, karlpeasons coefficient of correlation is

used.

Table: 4.16B

Correlation between educational qualification and obtaining microfinance for

children’s education and welfare

Educational qualification No. Of

respondents

on the basis

of education

qualification

(X)

No. Of respondents obtaining

microfinance for children’s education

and welfare

Weig

hted

avera

ge

(Y)

Alwa

ys (5)

Freque

ntly (4)

Occasi

onally

(3)

Rare

ly

(2)

Nev

er

(1)

Read and write 16 - - 6 1 9 1.93

Completed high school 43 - 9 11 20 3 7.46

SSLC & +2 33 6 16 6 2 3 7.93

Degree and above 8 3 5 - - - 2.33

Total 100 19.65

Source: primary data

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 53

Coefficient of correlation (r)=∑dxdy/√∑dx²∑dy²

= 140.74/√758*31.15

=140.74/153.66

=0.91

Interpretation:

The correlation coefficient is 0.91 i.e., there is good positive correlation between

education qualification and obtaining microfinance for children’s education and welfare.

PROBLEMS IN KUDUMBASHREE UNITS

In this section question number 30 is analyzed to know about problems in

kudumbashree units. Weighted average is used to rank the problems. The table: 4.34 shows

the problems in kudumbashree with corresponding rank based on members responses.

Table: 4.17

Problems in kudumbashree units

Sl

.n

o

Variables Alw

ays

(5)

Freq

uentl

y (4)

Occas

ionall

y (3)

Rar

ely

(2)

Nev

er

(1)

Scor

e

Weight

ed

average

Ra

nk

1 Lack of capital 9 14 32 23 22 265 2.65 I

2 Non availability of loan - - - 13 87 113 1.13 VII

3 Lack of basic book keeping

and accounting skill

- - - 28 72 128 1.28 VI

4 Limited awareness - - - 11 89 133 1.33 V

5 Time allocation of members - - - 9 91 109 1.09 IX

6 Caste/ethic barriers - - - 13 87 113 1.33 V

7 Poor management - - - 7 93 107 1.07 VII

I

8 Highly competition - - - 13 87 113 1.13 VII

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 54

9 Insufficient government

support/poor relation with

local government

- - 9 32 59 150 1.50 II

10 Conflict between members

of the unit

- - 3 42 55 148 1.48 III

11 Miscellaneous problems - - 2 34 64 138 1.38 IV

Sours: primary data

Interpretation:

As per the above table majority of the units faces the problem of lack of capital (rank

I). The least problem in the units is time allocation of members.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 55

CHAPTER 5

SUMMARY, FINDINGS, SUGGESTIONS, AND CONCLUSION

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 56

SUMMARY

Microfinance has emerged as a very important sector in India. Microfinance

interventions are well recognized world over as an effective tool for poverty alleviation and

improving socio-economic status of poor people. Most effective and efficient MFI is the

kudumbashree programme initiated by the Kerala government. Microfinance through

kudumbashree considered as the tool for rural development by empowering poor women and

improving living status of the poor.

The area where the poor people living lot needs the more kudumbashree units for their

development and well being. The kudumbashree rural-monthly report July 12 point out the

insufficiency of kudumbashree units in Areekode panchayath. This study intended to know

about the impact of microfinance through existing kudumbashree units in Areekode

panchayath and their performance and problems in their units. The study is presented through

5thchapter: introduction (statement of the problem, objectives, scope, methodology,

limitations etc.)Review of literature and conceptual frame work of microfinance

(history,present status, structure, and major activities of kudumbashree) kudumbashree- a

microfinance programme in Kerala, data analysis and interpretation of the study of

microfinance through kudumbashree units in Areekode panchayath, and summary, findings,

suggestions and conclusions.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 57

FINDINGS

➢ The study founded that the intervention of microfinance programme reduces

indebtedness of members only from religious organizations, and no changes in money

lenders/chittiesand other funding agencies.

➢ Mainstream of members are obtained microfinance for the purpose of children’s

education and welfare.

➢ Educated members have mostly taken microfinance for the purpose of children’s

education and welfare.

➢ The members are highly satisfied with the role of Government Agencies in setting up

of training programme and less satisfied with the role of Government Agencies in

eradication of poverty.

➢ The study founded that lack of capital is the main problem in most of the unit.

➢ 45% of KDS unit in Areekode panchayath doesn’t receive the matching grand.

➢ The study founded that 65% of unit have more than 100000 accumulated savings in a

year.

➢ In Areekode panchayath, 60% of the unit doesn’t receive the subsidy.

➢ The majority 55% of the unit have more than 90% of loan recovery.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 58

SUGGESTIONS

➢ A sincere effort should be made by kudumbashree mission and local government to

extend expertise in identification of income generating activities suitable to the local

conditions and allocate more resources to such activities.

➢ The kudumbashree mission must consider microenterprise as the most important

instrument for creating employment and income to the poor women.

➢ There is a need for promotion of modern microenterprise like clinical laboratory,

computer centre, etc.

➢ Close monitoring and follow up on the effective utilization micro credit.

➢ More awareness campaigns can be conducted for micro credit, micro thrift, micro

insurance and other product on a wide base.

➢ Innovative steps can be promoted by the kudumbashree with the help of government

to reach the unreached poor.

➢ Government, RBI, NABARD can come out with more effective subsidy schemes for

borrowing groups.

➢ The product of kudumbashree units needed to be competitive in the market.

➢ The government can provide market for kudumbashree s product.

➢ The government departments and public sectors undertaking should be made to

considerable purchasing their requirements from enterprise owned by women.

➢ More research activities are needed to be carried out to assess the impact of

microfinance through kudumbashree to enable the policy makers and programme

implementers to formulate an universal approach to empower the women.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 59

CONCLUSION

Microfinance acts as a catalyst in the lives of the poor and kudumbashree became the

lifeline to many of the poor women. In the present study, an attempt has been made to

analyze the performance of KDS units in Areekode panchayath, impact of microfinance,

purpose of obtaining microfinance, role of government, and problems of KDS units.

The performance of KDS unit in areacodepanchayath is satisfactory but there is

necessity to take some measures to reach the unreached poor and efficient performance of

kudumbashree units.

The microfinance helps the members to come out of the indebtedness from outside

loan, increase the living status through increased income and increased savings, and

empowered by engaged in income generating activities. Micro enterprise under

kudumbashree helps in developing and entrepreneurial culture in society and increasing

better living capacity of the poor.

In the study area the members manly adopt microfinance for the purpose of

children’s education and medical expenditure. The government must play eventually role for

the promotion of kudumbashree units. Lack of sufficient capital is the main problem in KDS

units.

Thus, there is an urgent need to widen the scope and financial services to cover the

unreached population.

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 60

BIBILIOGRAPHY

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 61

Journals:-

➢ Biju BL,Abhilash kumar K G(2013),-class femininism:The kudumbashree Agitation

in kerala, Economic and political weekly,Vol.XLVIII,No.9,march 2,mumbai.pg22-26.

➢ Kudumbashree(2011),-kudumbashree mission Hope,Thiruvananthapuram, kerala-

india

➢ Kamdar Sangita(2009),-microfinance-self employment and poverty

Alleviation,himalaya publication,Mumbai.

➢ Government of kerala(2009),-Kudumbashree mission,state poverty eradication

mission of kerala,Department of local self-Government,Hand book for resource

persons,(Malayalam)Thiruvananthapuram.

➢ Bassu priya(2008),-A financial System for India’s poor in Karmak K G,-Microfinance

in india(ed) (2008),sage publication,Newdelhi.

➢ Misra kamal K,Jannet Huber Lowry(2007),-Reasoned studies on Indian women

Empirical work of Social Scientists,Rawat Publications,Newdelhi,pg.302-323.

➢ Robinson M (2001)- The Microfinance Revollusion:Sustainable Finance for the

poor,World bank.

Reports and periodicals:-

• Status of microfinance in india 2011-12,by NABARD

• Rural Monthly Report july 2012 by KDS District Mission,Malappuram.

Books:-

• Microcredit,poverty and empowerment Linking the Triad,edited by NeeraBulra joy

Deshmukh,Ranadeve,Ranjani k,Murthy, published by SAGE publications.

• Microfinance Case studies,edited by S.Rajagopalan,published by ICFAI University

press.

• Praveshika,by National Rural Livelihood Mission.

• Rural finance sector,edited by Tamal Data Chaudhuri,published by ICFAI university

press.

Websites:-

• www.google.com.

• www.kudumbashree.org.

• www.nabard.org.

• www.researchersworld.com

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 62

APPENDIX

IMPACT OF MICROFINANCE ON WOMEN EMPOWERMENT THROUGH KUDUMBASHREE UNITS

Sullamussalam Science College Areekode Page 63

QUESTIONNAIRE

1.Name of the unit :.............................

2.Accumulated savings:

(a)250000-50000 (b)50000-750000

(c)75000-100000 (d)more than 100000

3.Internal loan allowed (yearly)

(a)Less than 25% of accumulated savings.

(b)25%-50% of accumulated savings.

(c)More than 50% of accumulated savings.

4.Matching grand received:

(a)Less than 5000 (b)5000 (c)Not received

5.Number of Members in the unit:

(a)below 10 members (b)10-15 members

(c)15-20 members (d)more than 20 members

6. Subsidy received:

(a)1 or 2 times (b)more than 2 times (c)Not received

7.Number of meetings per month:

(a)Less than 2 meeting (b)2-3 meeting (c)more than 3meeting

8.Hours of meeting

(a)Less than 2 hours (b)2-3 hour (c)more than 3 hours

9.Average attendance of meeting:

(a)Less than 50% (b)between 50%-70%