chapter 8 capital budgeting techniques © 2005 thomson/south-western

TRANSCRIPT

Chapter 8

Capital BudgetingTechniques

© 2005 Thomson/South-Western

2

What is Capital Budgeting?

The process of planning and evaluating expenditures on assets whose cash flows are expected to extend beyond one yearAnalysis of potential additions to fixed assets

Long-term decisions; involve large expenditures

Very important to firm’s future

3

Generating Ideas for Capital Projects

A firm’s growth and its ability to remain competitive depend on a constant flow of ideas for new products, ways to make existing products better, and ways to produce output at a lower cost.

Procedures must be established for evaluating the worth of such projects.

4

Project Classifications Replacement Decisions:Replacement Decisions: whether to

purchase capital assets to take the place of existing assets to maintain or improve existing operations

Expansion Decisions:Expansion Decisions: whether to purchase capital projects and add them to existing assets to increase existing operations

Independent Projects:Independent Projects: Projects whose cash flows are not affected by decisions made about other projects

Mutually Exclusive Projects:Mutually Exclusive Projects: A set of projects where the acceptance of one project means the others cannot be accepted

5

Similarities between Capital Budgeting and Asset Valuation

Uses same steps as in general asset valuation1. Determine the cost, or purchase price, of the asset.

2. Estimate the cash flows expected from the project.

3. Assess the riskiness of cash flows. [Note that we will

explicitly address the risk issue in the next chapter. For

now, risk is taken as given.]

4. Compute the present value of the expected cash flows to

obtain as estimate of the asset’s value to the firm.

5. Compare the present value of the future expected cash

flows with the initial investment.

6

Net Cash Flows for Project S and Project L

1,5001,200

800300

400900

1,3001,500

^Net Cash Flows, CFt

r e dp AEx cte fte -Tax

Year (T) Project S Project L0a $(3,000) $(3,000)1234

7

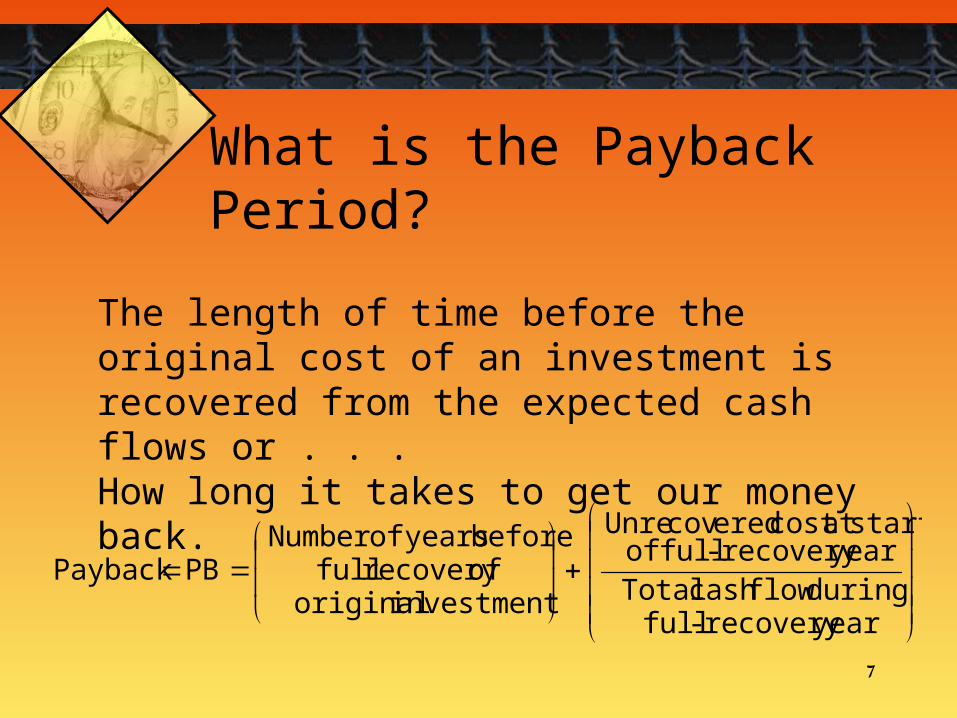

What is the Payback Period?

The length of time before the original cost of an investment is recovered from the expected cash flows or . . . How long it takes to get our money back.

yearrecovery -fullduring flowcash Total

yearrecovery -full ofstartat cost eredcovUnre

investment originalofrecovery fullbefore years of Number

PBPayback

8

Payback Period for Project S

=PaybackS 2 + 300/800 = 2.375 years

Net Cash Flow

Cumulative Net CF

1,500

-1,500

800

500

1,200

-300

-3,000

-3,000

300

800

PBS0 1 2 3 4

9

=PaybackL 3 + 400/1,500 = 3.3 years

Net Cash Flow

Cumulative Net CF

400

- 2,600

1,300

- 400

900

- 1,700

- 3,000

- 3,000

1,500

1,100

PBL0 1 2 3 4

Payback Period for Project L

10

Strengths of Payback:Strengths of Payback:• Provides an indication of a

project’s risk and liquidity• Easy to calculate and understand

Weaknesses of Payback:Weaknesses of Payback: • Ignores TVM• Ignores CFs occurring after the

payback period

Strengths and Weaknesses of Payback:

11

Net Present Value: Sum of the PVs of Inflows and Outflows

Cost is CF0 and is generally negative.

NPV

CF

kt

nt

t 0 1

.^

NPV

CF

kCF

t

nt

t

0

01

.^

^

12

What is Project S’s NPV?k = 10%

1,500 8001,200(3,000)

1,363.64

991.74

601.05

204.90

161.33

300

0 1 2 3 4

NPVS =

13

What is Project L’s NPV?

k = 10%

400 1300900(3,000)

363.64

743.80

976.71

1024.52

108.67

1500

0 1 2 3 4

NPVL =

14

Calculator Solution, NPV for L :

NPVL = 108.67 = NPVL

Enter in CF for L:

I

-3,000

400

900

1,300

1,500

10%

CF0

CF1

CF2

CF3

CF4

15

Rationale for the NPV method:

NPV = PV inflows - Cost= Net gain in wealth.

Accept project if NPV > 0.

Choose between mutually exclusive projects on basis of higher NPV. Which adds most value?

16

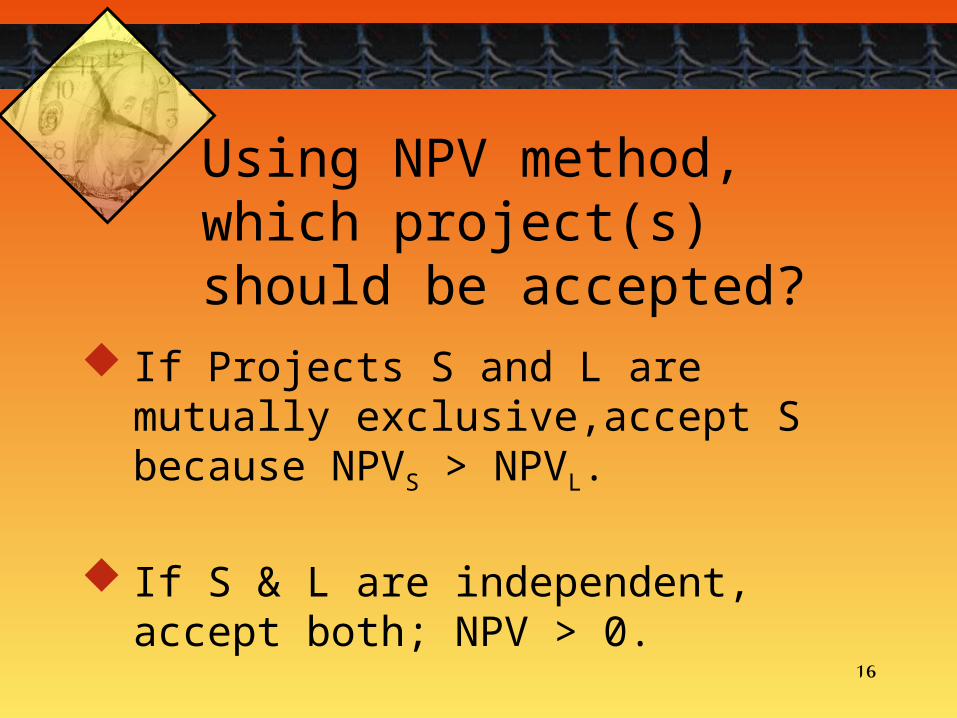

Using NPV method, which project(s) should be accepted?

If Projects S and L are mutually exclusive,accept S because NPVS > NPVL.

If S & L are independent, accept both; NPV > 0.

17

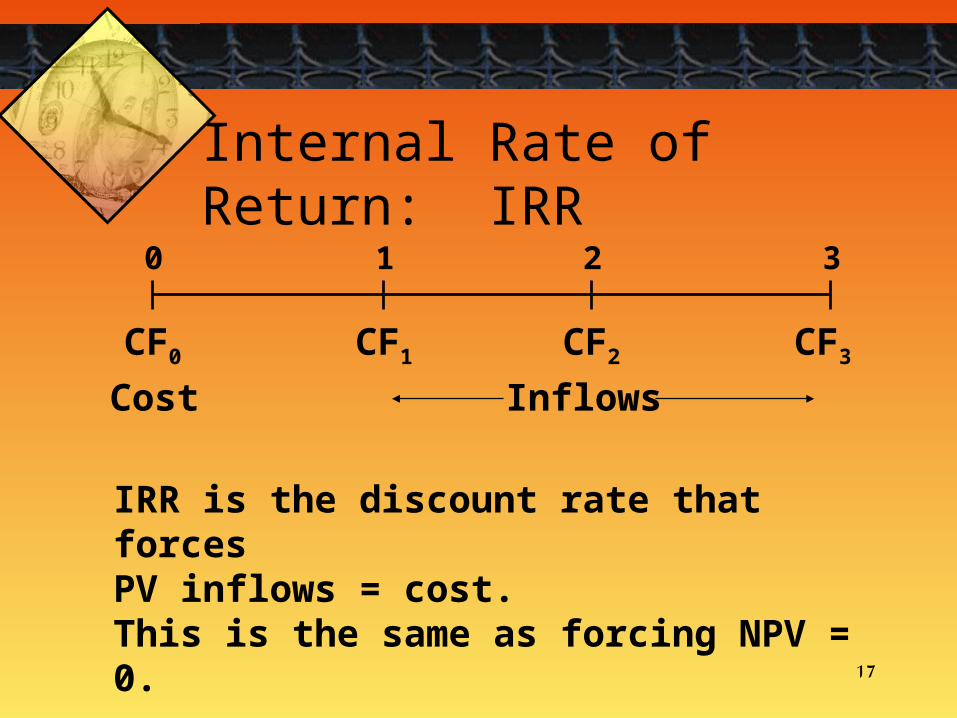

Internal Rate of Return: IRR

0 1 2 3

CF0 CF1 CF2 CF3

Cost Inflows

IRR is the discount rate that forces PV inflows = cost. This is the same as forcing NPV = 0.

18

t

nt

t

CF

kNPV

0 1.

t

nt

t

CF

IRR

0 10.

NPV: Enter k, solve for NPV.

IRR: Enter NPV = 0, solve for IRR.

Calculating IRR

19

What is Project S’s IRR?

NPVS = IRRS = 13.1%Enter CFs in CF register, thenpress IRR:0

(3,000)

IRR = ?0 1 2 3 4

Sum of PVs for CF1-4 = 3,000

1,500 8001,200 300

20

What is Project L’s IRR?

NPVL =Enter CFs in CF register, thenpress IRR: IRRL = 11.4%0

IRR = ?

400 1300900 1500

0 1 2 3 4

Sum of PVs for CF1-4 = 3,000

(3,000)

21

How is a Project’s IRRRelated to a Bond’s YTM?

They are the same thing.A bond’s YTM is the IRRif you invest in the bond.

90 109090

0 1 2 10IRR = ?

-1134.20

IRR = 7.08% (use TVM or CF register)

22

Rationale for the IRR Method:

If IRR (project’s rate of return) > the firm’s required rate of return, k, then some return is left over to boost stockholders’ returns.

Example: k = 10%,IRR = 15%. Profitable.

23

IRR acceptance criteria:

If IRR > k, accept project.

If IRR < k, reject project.

24

Decisions on Projects S and L per IRR

If S and L are independent, accept both. IRRs > k = 10%.

If S and L are mutually exclusive, accept S because IRRS > IRRL .

25

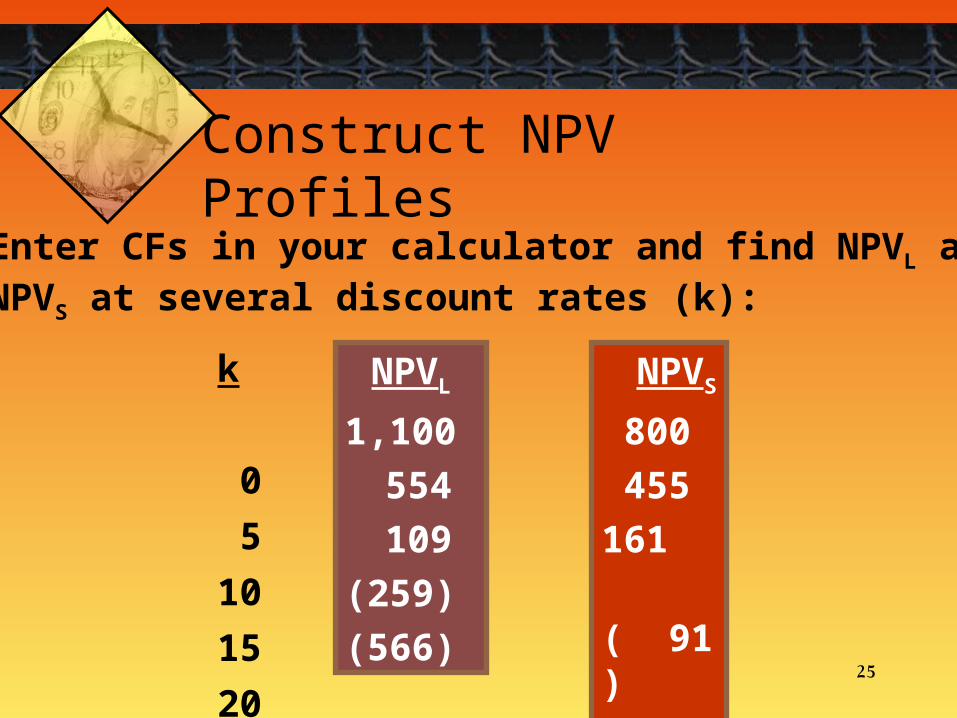

Construct NPV ProfilesEnter CFs in your calculator and find NPVL andNPVS at several discount rates (k):

k

0

5

10

15

20

NPVL

1,100

554

109

(259)

(566)

NPVS

800

455

161

( 91)

(309)

26

IRRL = 11.4%

IRRS = 13.1%

Crossover Point = 8.1%

k

0

5

10

15

20

NPVL

1,100

554

109

(259)

(566)

NPVS

800

455

161

( 91)

(309)

NPV Profiles for Project S and Project L

(800)

(600)

(400)

(200)

0

200

400

600

800

1,000

1,200

0 2 4 6 8 10 12 14 16 18 20

Project L

Project S

27

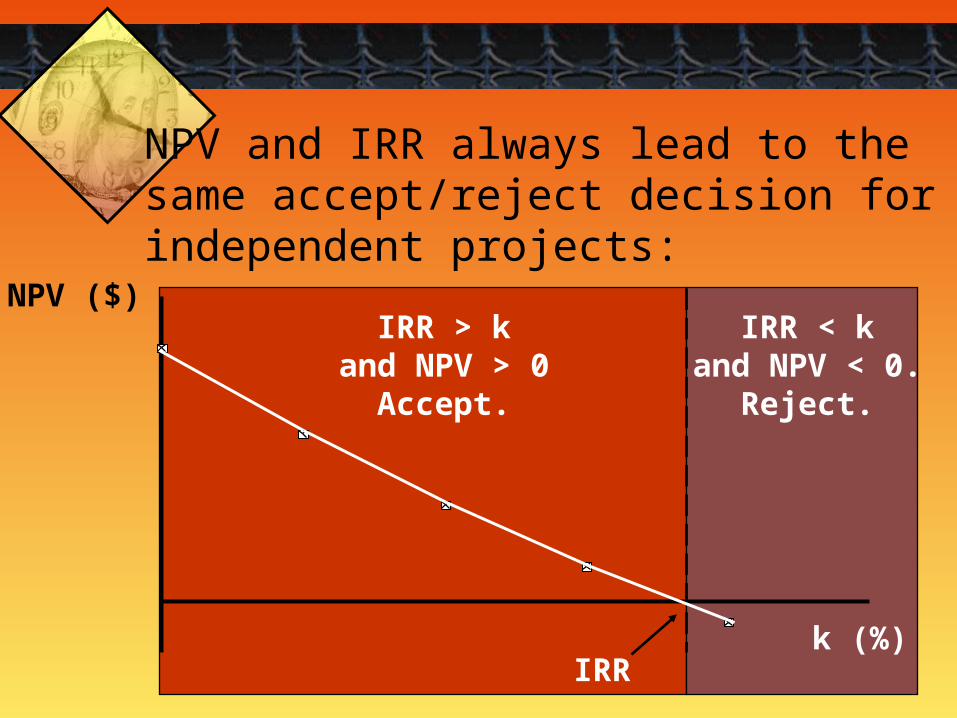

NPV and IRR always lead to thesame accept/reject decision forindependent projects:

IRR < kand NPV < 0.

Reject.

NPV ($)

k (%)IRR

IRR > kand NPV > 0

Accept.

28

Mutually Exclusive Projects

k< 8.1: NPVL> NPVS , IRRL < IRRS

CONFLICT

k> 8.1: NPVS> NPVL , IRRS > IRRL

NO CONFLICT

8.1

NPV

%

IRRs

IRRL

S

L

29

To Find the Crossover Rate:

1. Find cash flow differences between the projects. See data at beginning of the case.

2. Enter these differences in CF register, then press IRR. Crossover rate = 8.11, rounded to 8.1%.

3. Can subtract S from L or vice versa.

4. If profiles don’t cross, one project dominates the other.

30

Two Reasons NPV Profiles Cross:

1) Size (scale) differences.1) Size (scale) differences. Smaller project frees up funds at t = 0 for investment. The higher the opportunity cost, the more valuable these funds, so high k favors small projects.

2) Timing differences.2) Timing differences. Project with faster payback provides more CF in early years for reinvestment. If k is high, early CF especially good, NPVS> NPVL.

31

Reinvestment Rate Assumptions

NPV assumes reinvest at k.

IRR assumes reinvest at IRR.

Reinvest at opportunity cost, k, is more realistic, so NPV method is best. NPV should be used to choose between mutually exclusive projects.

32

End of Chapter 6

Capital Budgeting Techniques