chiquita brands south pacific limited annual report2002

TRANSCRIPT

Chiquita Brands South Pacific Limited

Annual Report 2002

1

Contents

Chairman’s Report 2

CEO’s Report 2002 4

Highlights 8

Five Year Financial Summary 9

Directors’ Report 10

Financials 17

Directors’ Declaration 58

Independent Audit Report 59

Corporate Governance Statement 60

Shareholder Information 62

Chairman’s Report

2002 was a year of consolidation and transformation

for Chiquita Brands South Pacific (Chiquita) which places

the Company in a sound financial position for 2003.

In May 2002, shareholders endorsed a $25.6 million

recapitalisation of the Company. They also agreed to

the appointment of Mr Mano Babiolakis as CEO and

Managing Director, and Mr Frank Costa and Mr Carl

Schokman to the Board of Directors. These three

men are well credentialed in the fresh produce industry

and bring to the Board a wealth of knowledge and

perspective.

At the board meeting immediately following the AGM,

Mr Babiolakis presented the Board with his strategy to

transform and re-invigorate the Company. At its simplest

level the plan involved the restructuring of the Company

into autonomous and accountable Strategic Business

Units (SBUs), each with their own focus, direction and

targets. The strategy also included the divestment

and rationalisation of non-performing assets.

This strategy presented the Board with some very

tough decisions about the structure of the Company.

The decision to post an abnormal charge for restructuring

costs of $27.4 million followed lengthy and vigorous

debate by the Board and Chiquita executive management.

Since resolving to undertake this restructure, Chiquita

management has remained dedicated to refocusing and

restructuring the business to bring about consolidation

and improvement of previously under-performing

business units.

The cost base of all business units was reviewed and

non-performing assets divested. The areas principally

affected by this strategic review include the banana

farming operations, the market and trading businesses,

and corporate Head Office.

2

3

The banana farming operations have made significant

losses over a number of years. The restructure, now

completed, was a major process with all facets of the

business analysed and assessed to determine continued

investment. As a result, the Company divested non-

profitable farming and packing operations. The Board

is confident that Chiquita’s banana farming operations

are well placed to deliver positive returns going forward.

The rationalisation of the market and trading operations,

including its assets, equipment, warehousing and

staffing, is well underway. Assets have been sold or

written down to their realisable value and non

performing facilities closed or sold. The restructured

and revised cost base of this business unit will ensure

a competitive advantage and leave it better positioned

to service its customer base.

Our strategy to move to autonomous SBUs has

necessitated downsizing the corporate Head Office

whereby redundant services have been eliminated.

The devolvement of responsibility back to the business

units from Head Office did not result in an increase in

administrative or financial personnel within the SBUs.

Following the restructure it is pleasing to note that

operating results excluding abnormal charges have

improved significantly, with the Group posting an

EBIT of $10.4 million for the year. Positive operating

cash flows of $10.0 million, after one-off charges

of $5.0 million, were a marked improvement over the

previous year and have been enhanced as a direct

result of stringent working capital management.

The refocus and rationalisation have given substantive

impetus to Chiquita’s vision to be the dominant player

in the production, processing and marketing of

horticultural products in its chosen categories and

markets. Our vision supports our goal to deliver

consistent after tax returns on shareholder funds

greater than 15% and increasing to 20% over the

next three years.

Throughout the consolidation and transformation

process, Chiquita has appreciated the support given

by its two major shareholders, Chiquita Brands

International (CBII) and the Costa’s Group. They have

added intellectual rigour to the strategic plan and the

vision and direction of the Company.

I believe that under Mr Babiolakis and his Executive

Team, Chiquita is on a solid footing for the future.

The emphasis of the business is very much on gaining

maximum returns and synergies from the existing

business units while focusing on shareholder return,

cash generation and the attainment of further

opportunities in line with Chiquita’s vision.

I would like to acknowledge the contribution and

dedication of all the Chiquita staff in what has been

a year of significant change.

Anthony G. Hartnell

Chairman

Chairman’s Report 2002 continued

As we enter 2003, I want to take the opportunity

to restate our operating model and financial goals.

Our operating model is based on being the dominant

player in the production, processing and marketing

of horticultural products in our chosen categories

and markets. Dominant is in respect to market share,

degree of pricing power, competitive advantage and

where there are barriers to entry. By executing against

this model, we believe that we will achieve our overall

financial goal of delivering consistent improvement

in after tax returns to shareholders of 15% initially,

growing to 20% over the next three years.

In line with the Group’s vision and strategic plan,

a number of objectives were set following Chiquita’s

successful capital raising in May 2002. These were

aimed at stemming losses, restructuring the balance

sheet and attaining a solid platform on which to build.

The establishment of clearly autonomous Strategic

Business Units (SBUs) became the overriding objective.

This now provides each of Chiquita’s businesses with

a clearly defined focus and fiscal accountability, while at

the same time, strengthening communication within the

businesses and within the Company as a whole.

The key to any successful business is the calibre,

dedication and enthusiasm of its people. In order to

harness the power of Chiquita’s people, the Executive

Team was restructured to include the General Manager

of each SBU and our Chief Financial Officer.

The Executive Team are highly committed and competent

individuals, each focused on achieving Chiquita’s clearly

defined objectives and demonstrating credibility by

doing and delivering what we have committed to do

and deliver. Throughout the organisation, building trust

and teamwork, with an emphasis on maximising returns,

remains crucial to our overall success.

CEO’s Report 2002

4

5

Our strategy has already begun to deliver value.

Chiquita’s performance highlights the strong turnaround

over the previous year with earnings before interest,

tax and one-off charges increasing from $2.2 million

in 2001 to $10.4 million in 2002.

It is pleasing to note there was a significant improvement

in underlying cash from trading. The cash generated,

excluding cash outflows for restructuring costs, increased

from $4.5 million to $14.7 million.

Our financial discipline and focus on restructuring

our balance sheet has resulted in reduced investment

in working capital down from $21.0 million (December

2001) to $15.9 million (December 2002). We have

set strict performance measures for managing the

investment in working capital for each SBU. This will

result in improved cash flow in 2003 and reduced

reliance on external seasonal debt.

The improved profitability and cash flow, together

with the capital raising, have translated into a stronger

balance sheet, with Chiquita’s overall debt down from

$88.0 million in December 2001 to $56.0 million in

December 2002. Net debt to shareholders funds at

31 December 2002 was 78%, down from 134% at the

same time last year.

With the establishment of autonomous SBUs, Head

Office has been systematically reduced with significant

cost savings flowing through in the final quarter of 2002.

In conjunction with the Board, the focus of Head Office

is now to provide Chiquita’s strategic direction, allocate

and measure its resources and give strong corporate

governance through effective policy, reinforced by a

robust internal control environment. To this end, an

internal audit function for both Finance and Occupational

Health & Safety, is currently being implemented and

should be in place by the second quarter of 2003.

The SBUs fall into three operational segments:–

- Farming operations which include Chiquita Mushrooms,

Blueberry Farms of Australia and Chiquita Bananas

North Queensland.

- Trading operations which comprise Chiquita Trading,

Chiquita Export and Chiquita Nibbles.

- Processing operations which include Kangara Foods

and Angas Park Fruit Company.

For the purpose of the financial segmental analysis,

it is difficult to draw comparisons to previous years

due to the significant restructuring implemented

during 2002. Going forward, comparisons obviously

will become more meaningful.

FARMING OPERATIONS

Blueberry Farms of Australia (BFA)

BFA enjoyed an exceptional year with earnings well

ahead of forecast. While the drought impacted on both

the size and overall yield of the fruit, this was more than

offset by a very high quality product and strong sales

prices, particularly in our export markets. BFA ended

the year on a high note, culminating in recognition as

winner of the 2002 Premier’s NSW Regional Exporter

of the Year award.

Comprising 530 acres of blueberries, BFA is one

of the largest operations of its kind in the Southern

Hemisphere. Furthermore, additional land, adjacent to

the Corindi Farm, has been purchased and earmarked

for further expansion.

In order to capitalise on BFA’s reputation in the berry

category, BFA also has a substantial raspberry operation.

Whilst production suffered materially from the drought,

the end result, driven primarily from stronger sales prices,

was exceptionally positive. Continued research and

development into out of season raspberries has been

made. We believe this development will provide additional

financial benefits and we have committed to expand.

CEO’s Report 2002 continued

CEO’s Report 2002 continued

Chiquita Mushrooms

The Chiquita Mushroom business has improved

its quality and yields, resulting in an increase in

market share. Importantly in 2002 we have seen the

establishment of a strong, cohesive management

team that has contributed greatly to improving and

strengthening employee relations, an area of concern

for a number of years. Aligned with this building of

internal confidence, management have also placed

a much stronger focus upon the health and safety

aspects of the business. During 2003, these initiatives

should result in improved productivity and translate

into improved return on funds employed.

Chiquita Mushroom’s operations are at Mernda,

Yarrambat and Nagambie in Victoria, and Casuarina

in Western Australia. Overall we produced about 280

tonnes per week, making Chiquita the largest single

producer of mushrooms in Australia. We are committed

to expanding our mushroom business. This expansion

will come through maximising efficiencies, acquisition

and green field development.

Chiquita Bananas North Queensland

A key objective in 2002 was the restructure of the

banana farming operations, which in recent years

have been a significant drain on Chiquita’s resources.

Now completed, the restructure involved a change

of management, the divestment of two loss-making

packing operations, the sale of one farm and the exit

of a leased farm.

In addition, a regeneration program has been implemented.

This will result in the average age of the plantations falling

in line with international farming practices over the next

three years. The implementation of post-harvest technology

late in 2002 has resulted in better returns to the farms due

to a strong and immediate effect on farm yield, quality and

pack-out of fruit. The financial impact of the restructure

forecasts the operations will break-even in this fiscal year

and return to profitability thereafter.

TRADING OPERATIONS

Chiquita Trading

During the year, all markets, logistics and sales operations

have been combined nationally to form Chiquita Trading.

Operations, in each of the major cities, give a national focus

to our marketing and trading of produce and make Chiquita

Trading one of the only such operations in Australia.

Previously, under the category management system,

the markets and logistics formed part of each of the

individual categories. This approach proved difficult to

effectively operate as lines of ownership, accountability

and control crossed organisational boundaries and

impacted negatively on both return and profitability.

The restructure has focused on eliminating duplication

in terms of warehousing and infrastructure, administration,

procurement and sales.

To date, much of the planning has been achieved, with

implementation some 60% of the way through. It is

anticipated that by June 2003, the entire exercise will

be complete, with some $2.5 million of annual savings

expected to be realised in 2003. Clear accountability

under the restructured unit now gives the appropriate

focus and direction to deliver a positive result in 2003.

Chiquita Nibbles

Directly involved in the processing, packing and marketing

of dried fruit and nut products, Chiquita Nibbles has

had a very good year. This has been underpinned by

the introduction of the pre-pack and punnet ranges,

which resulted in a substantial increase on prior year sales.

A key focus has been new product development and

packaging design.

The challenge for this SBU, in the medium term is to

efficiently manage the logistics and supply chain elements

of its business to support growth expectations. Additional

plans include the broadening of distribution into new

markets.

Brian LeckieGeneral ManagerKangara Foods & Angas Park

David GreenChief Financial Officer & Company Secretary

Executive Team

Peter McPhersonGeneral ManagerBlueberry Farms of Australia & Chiquita Export

Stephen LittleGeneral ManagerChiquita Mushrooms

Ray TantiGeneral ManagerChiquita Nibbles & Banana Farms

6

7

PROCESSING OPERATIONS

Kangara Foods & Angas Park

Kangara Foods has had a mixed year. The returns

from vine fruit exceeded expectations. However, a very

poor citrus season combined with delays in carrot

planting in newly acquired lands, directly caused by

delays in capital spending during the first half of the

year, have diminished financial returns.

During the year, much of the focus has been on

infrastructural development and ensuring that the

required asset base can deliver the expected returns.

To date, a large portion of this work has been

completed. Kangara Foods is a large-scale primary

agricultural business that has exposure to adverse

weather conditions. If the drought, currently being

experienced throughout Australia, continues to affect

the South Australian Riverland, returns from Kangara

for the forthcoming year will be impacted.

Going forward, the focus of the business is very

much to reduce and diversify that risk. Key in that

process is the increased emphasis on new and existing

value-added products that Kangara currently produces.

During the last quarter of the year, Angas Park was

merged with Kangara Foods. Synergies between

these businesses have been exploited particularly in

areas of procurement, rationalisation of product lines,

warehousing and processing facilities, sales and

administration. Strategically, the merger has added

critical mass to this SBU. Enormous focus has been

placed on working capital management and changing

the nature of the business from a production driven

entity to a market driven one, with particular focus on

customer requirements.

Overall, the merged entity performed below anticipated

targets. However, given the magnitude of change,

particularly at Angas Park, the overall result has been

a positive one and although much structural work is

still required, the platform to go forward is very solid.

The accolade Kangara received on being awarded

the 2002 Premier’s South Australia Food Award, is clear

recognition of this business’ position of excellence in

the food industry.

OUTLOOKThe restructuring process is substantially complete.

As Chiquita moves into 2003, each SBU has clearly

defined financial and operational goals aligned with

overall Group targets. In line with our vision, we will

continue to grow and expand our SBUs, and further

focus on areas where we can value-add to our

products and services.

We will continue to extract synergies between business

units. This has particular relevance for Kangara Foods

and Angas Park, and also for Chiquita Trading and its

trading relationships with banana farms, BFA and

Chiquita Mushrooms. The benefits of this integration

have already started to flow through in the improved

Group earnings for 2002, with the full annualised benefit

anticipated in 2003. The growth of our export business,

currently responsible for approximately 15% of the

Group’s turnover, is an area of significant opportunity

and focus.

The fresh produce industry in Australia is valued at

approximately $4.5 billion and remains fragmented

in many areas. Chiquita accounts for only 6.5% of this

industry sector. However, as one of Australia’s largest

producing and marketing horticultural businesses,

Chiquita is well positioned to involve itself in the

rationalisation and consolidation of the industry as a

whole. Our focus is to continually look for opportunities

in the market to further consolidate our position within

given sectors or that vertically integrate with our existing

businesses, that allows Chiquita to maximise returns

to shareholders. This will further cement Chiquita’s

position as one of Australia’s largest and most successful

suppliers in the fresh produce industry.

CEO’s Report 2002 continued

Mark RobinsonGeneral ManagerChiquita Trading

2002 Highlights

0

2

4

6

8

10

12

2002

EBIT (before significant items)

2001 2000 1999 19980

2

4

6

8

10

-2

Net Cash Flows from operations

2002 2001 2000 1999 1998

Gearing (net debt to shareholders' equity) (%)

2002 2001 2000 1999 19980

50

100

150

200

Mill

ions

Mill

ions

Earnings before interest and tax up 378% to $10.4 million

Injection of fresh talent to the Board with the appointments of Mano Babiolakis as Managing Director, Frank Costa and Carl Schokman as non executive directors.Collectively 80 years of experience in the fresh produce industry.

Cash from operating activities up 123% to $10.0 million.

Successful restructure of the banana assets in Far North Queensland, stemming losses and establishing a viable, quality focused farming operation.

Debt reduction through improved trading cash flow and $25.6 million capital raising.

Stage one of the Chiquita Trading rationalisation complete resulting in significant cost savings.

Significant improvement in debt to equity ratio down to 78% from 134% in 2001.

Downsizing of Head Office with staff members reduced to 14 from 39 with no increasein corresponding head count at the SBU’s

Profit after tax excluding significant items of $4.7 million up from a loss of $3.0 million in 2001.

Five Year Financial Summary

8

9

$'000

For years ended 31 December 2002 2001 2000 1999 1998

PROFITABILITYNet Sales 304,135 303,230 241,145 202,944 148,025

EBITDA Earnings before interest, tax,depreciation and amortisation (before significant items) 16,080 9,639 13,404 15,569 7,515

Depreciation and amortisation 5,724 7,474 6,142 6,878 5,090

EBIT Earnings before Interest and tax 10,356 2,165 7,262 8,691 2,425

Net interest (Cr)/Dr 5,739 5,719 3,012 2,491 1,944

Earnings before tax and significant items 4,617 (3,554) 4,250 6,200 481

Net profit after tax (before significant items) 4,674 (3,023) 3,850 3,811 212

Net profit after tax (after significant items) (18,511) (12,209) 3,272 3,609 514

BALANCE SHEETCapital employed 127,865 153,676 160,331 72,098 75,458

Net debt 56,178 87,881 88,890 30,720 49,040

Shareholder funds 71,687 65,795 71,441 41,378 26,418

CASH FLOWNet Cash Flows from operations 9,982 4,486 7,426 9,775 (2,069)

Capital expenditure and acquisitions 8,861 9,556 64,426 7,138 32,979

FINANCIAL RATIOSBasic EPS (cents) (17.32) (18.10) 6.65 11.63 2.28

Basic EPS before significant items (cents) 4.37 (4.48) 7.82 12.28 0.94

Return on average shareholders' equity (%) (1) 6.80% (4.41%) 6.83% 11.24% 1.60%

Net tangible asset backing per share (cents) 0.42 0.79 0.81 1.06 0.92

Net interest cover (times) 1.8 0.4 2.4 3.5 1.2

Gearing (net debt to shareholders' equity) (%) 78% 134% 124% 74% 186%

OTHERFully paid shares ('000) 144,048 68,032 66,214 35,421 23,746

Convertible securities - number of shares ('000) (2) 6,100 6,100 6,100 6,100 6,100

Share price

- year low ($) $0.30 $0.32 $0.78 $0.95 $0.70

- year high ($) $0.50 $0.90 $1.30 $1.12 $1.20

- close ($) $0.47 $0.45 $0.85 $1.01 $1.20

Market capitalisation $'000 67,703 30,614 56,282 35,775 28,495

Number of shareholders 1,464 1,457 1,201 878 634

(1) Based on net operating profit before significant items(2) Repaid via intercompany funding on 15 January 2003

Directors’ Report

Your directors submit their report for the year ended 31 December 2002.

DIRECTORSThe names of the Directors of the Company in office during the financial year and until the date of this report are:

Anthony G. Hartnell Dennis M. Doyle

Mano D. Babiolakis Craig A. Stephen

Bruce W. Kemp Francis A. Costa

Carl C. Schokman Donald J. Taig

Donald J. Taig resigned from the Board on 29 May 2002

Mano D. Babiolakis was appointed to the Board, effective 12 April 2002

Francis A. Costa and Carl C. Schokman were appointed to the Board, effective 29 May 2002

The details of the Directors of the Company in office at the date of this report are:

Anthony Geoffrey Hartnell – Chairman

Solicitor B.Ec (ANU); LLB (Hons)(ANU); LLM (Highest Hons.)(George Washington University) A.M.

Appointed Chairman 1985. Board member since 1984. Former Chairman of the Australian Securities Commission and

National Companies & Securities Commission. Serves and has served on boards of both public (including listed) and

private companies. Directorships currently held include Chairman of BT Australian Equity Management Ltd, BT Global

Asset Management Ltd, BT Resources Management Ltd, Television & Media Services Ltd, KAZ Computer Services

Ltd, NSW Thoroughbred Racing Board, and ANU Endowment for excellence.

Dennis Michael Doyle

Solicitor. B.S. (Xavier University); J.D. (University of Cincinnati) Order of the Coif.

Appointed to the Board on 15 January 1998. Former Chairman of the International Banana Association. In 1984

was appointed Vice President, General Counsel and Secretary of Chiquita Brands International, Inc. Presently serves

as Executive Vice President – Regulatory Affairs.

Bruce William Kemp

Dip. Mech. Eng., Dip. Ind. Eng.

Appointed to the Board 24 February 2000. Former Chief Executive of Southcorp Wines. Presently Chief Executive

of Global Wine Advice. Directorships include Anthony Smith Australasia Pty Ltd, Pipers Brook Vineyards Limited and

Rabobank Advisory Board.

Craig Allan Stephen

CPA. B.S. (University of Cincinnati)

Appointed to the Board on 15 January 1998. Has several years experience consulting to large public clients whilst

with Ernst & Young. Joined Chiquita Brands International, Inc. in 1990 as a Corporate Planner. Currently serves as

President & Chief Operating Officer, Chiquita Banana – Far and Middle East, Austral/Asia Region.

Anthony Hartnell – Chairman Dennis Doyle Bruce Kemp

10

11

Francis Aloysius Costa

OAM

Appointed to the Board on 29 May 2002. Director of Costa Bros. Annuities Pty Ltd and Managing Director and

CEO of Costa’s Pty Ltd. President of the Geelong Football Club. Honoured with an Order of Australia Medal for

services to youth and the community.

Carl Christopher Schokman

B. Com. (Deakin University); FCPA; FAICD; FTIA

Appointed to the Board on 29 May 2002. Presently the Chief Financial Officer of Costa Bros. Annuities Pty Ltd and

Group General Manager Commercial of Costa’s Pty Ltd. Has several years experience in public accounting with an

emphasis on business advisory services. Is a Fellow of the Institute of Company Directors and the Taxation Institute

of Australia.

Manoussos Diogenis Babiolakis – Managing Director

B. Com. (Rhodes University South Africa)

Appointed to the Board on 12 April 2002. Former CEO of Interfresh Limited, the largest horticultural concern

in Zimbabwe. Presently CEO and Managing Director of CBSP and Director of Zymex Holdings Pty Ltd.

Has 17 years experience in the agricultural sector.

Directors were in office from the beginning of the financial year until the date of this report, unless otherwise stated.

INTEREST IN THE SHARES OF THE COMPANYThe relevant interests of each of the directors in the shares and options issued by the companies within the

consolidated entity as notified by the directors to the Australian Stock Exchange in accordance with S205G(1)

of the Corporations Act 2001, at the date of this report are as follows:

Directors Ordinary Shares Exchange Quoted Options Executive Options

Anthony Hartnell 548,185 Nil Nil

Dennis Doyle Nil Nil Nil

Bruce Kemp 174,999 Nil Nil

Mano Babiolakis 5,400,000 Nil 1,000,000

Francis Costa 37,175,221 Nil Nil

Carl Schokman 350,000 Nil Nil

Craig Stephen 390,000 Nil Nil

Directors’ Report continued

Craig Stephen Francis Costa Carl Schokman Mano Babiolakis – Managing Director

(1)

(1) As trustee for the CBSP Employee Share Plan.

Directors’ Report continued

PRINCIPAL ACTIVITIESThe principal activities of entities within the consolidated entity during the year were:

- The manufacturing, marketing and distribution of fruit, vegetables and dried fruit and nuts within Australia and to

export markets; and

- The growing of bananas, mushrooms, blueberries, raspberries, carrots, grapes, citrus and other fruits, in Australia.

EARNINGS PER SHAREBasic earnings per share, was a loss of 17.32 cents per share. Diluted earnings per share, was a loss of

17.25 cents per share.

DIVIDENDS PAID OR RECOMMENDEDNo dividend will be paid in respect of the year ended 31 December 2002. A final dividend for 31 December 2000

(3 cents per share fully franked) of $1.986 million was paid during 2001. No dividends were paid in respect of the

year ended 31 December 2001.

REVIEW AND RESULTS OF OPERATIONSRefer to the Chairman’s Report and CEO’s Report in the front section of this Annual Report.

SIGNIFICANT CHANGES IN THE STATE OF AFFAIRSIn the opinion of the directors there were no significant changes in the state of affairs of the consolidated entity that

occurred during the financial year under review not otherwise disclosed in this report or the financial statements.

LIKELY DEVELOPMENTS AND RESULTSRefer to the Chairman’s Report and CEO’s Report in the front section of this Annual Report.

ENVIRONMENTAL REGULATIONS AND PERFORMANCEChiquita Brands South Pacific Limited and all of its subsidiaries are committed to conducting all business

activities having proper respect for the environment while continuing to meet other expectations of shareholders,

employees, customers and suppliers.

All group companies are subject to environmental regulations under various Federal, State and local laws relating

predominantly to air, noise and water emission levels, and the Directors are not aware of any non-compliance

with these regulations.

The consolidated entity is committed to achieving a level of environmental performance that meets or exceeds

Commonwealth, State and local, requirements, and improves its use of natural resources and minimises waste.

Chiquita Mushrooms Pty Ltd is participating in an initiative of the Victorian State Government to establish World’s

Best Environmental Practice for Victoria’s Food Industry.

Chiquita Mushrooms Pty Ltd and Angas Park Fruit Company Pty Ltd have entered into the Greenhouse Challenge,

a Commonwealth Government initiative designed to reduce greenhouse gas emissions while improving performance.

SHARE OPTIONSAs at the date of this report, there were 2,583,425 unissued Ordinary Shares in the Company under options.

During the financial year, the Company issued 1,000,000 executive options to the Managing Director. Since the end of

the financial year the Company has issued a further 1,050,000 executive options to the Chiquita Executive, excluding

the Managing Director. The executive options were issued in four tranches in amounts, exercise prices per ordinary

share and expiry dates as set out in the table below.

No options were exercised during the financial year.

12

13

As at the date of this report, the following options were on issue:

Details Number of Exercise Options Price

Employee options expiring 27 March 2003 111,000 $1.00

Employee options expiring 12 February 2004 142,000 $1.00

Employee options expiring 29 December 2004 20,000 $1.00

Employee options expiring 27 March 2005 260,425 $1.154

Executive options expiring 29 May 2004 400,000 $0.435

Executive options expiring 29 May 2005 750,000 (a)

Executive options expiring 29 May 2006 600,000 (a)

Executive options expiring 29 May 2007 300,000 (a)

Total options on issue at balance date 2,583,425

(a) Options expiring 29 May 2005, 29 May 2006 and 29 May 2007 have an exercise price based on the weighted

average price of Ordinary Shares of Chiquita Brands South Pacific Limited on the 20 business days immediately

prior to 29 May 2003, 2004 and 2005 respectively.

INDEMNIFICATION AND INSURANCE OF DIRECTORS AND OFFICERSThe Company has not, during or since the reporting period, in respect of any person who is or has been an officer

of the Company:

– Indemnified or made any relevant agreement for indemnifying against a liability incurred as an officer, including

costs and expenses in successfully defending legal proceedings; or

– Paid or agreed to pay a premium in respect of a contract insuring against a liability incurred as an officer for the

costs or expenses to defend legal proceedings;

with the exception of the following matters:

During the financial year the Company paid premiums to insure all of the directors and officers against liabilities

for costs incurred by them in defending proceedings for conduct involving any actual or alleged error, mis-statement,

misleading statement, omission, neglect or breaches of duties and wrongful acts resulting in loss arising from

discharge of pollutants. Disclosure of the total amount of the premiums paid under this renewed insurance policy

is prohibited under the provisions of the insurance contract.

DIRECTORS’ AND OTHER OFFICERS’ EMOLUMENTSThe Remuneration Committee of the Board of Directors is responsible for determining and reviewing compensation

arrangements for the Managing Director and management team and determining and reviewing the annual bonus

system for employees. The Committee is also responsible for recommending a total of Directors’ remuneration to

be approved by resolution of shareholders at the Annual General Meeting of the Company.

Directors’ Report continued

Directors’ Report continued

The appropriateness of the nature and amount of emoluments is reviewed on a periodic basis by reference to the

relevant employment market conditions with the overall objective of ensuring maximum shareholder benefit from the

retention of a high quality Board and management team. The Managing Director and management team are given

the opportunity to receive their base emolument in a variety of forms including cash and fringe benefits such as

motor vehicles and expense payment plans. It is intended that the manner of payment chosen will be optimal for

the recipient without creating undue cost for the Company.

To assist in achieving these objectives, the nature and amount of the Managing Directors’ and management team

members’ emoluments are linked to the Company’s financial and operational performance. All senior executives have

the opportunity to participate in the annual bonus system which currently provides cash and share option incentives

where specified criteria are met including criteria relating to profitability, cash flow, share price growth and individual

performance targets.

Details of the nature and amount of each element of the emolument of each director of the Company and each of the

five executive officers of the Company and the consolidated entity receiving the highest emolument for the financial

year are as follows:

Emoluments of directors of Chiquita Brands South Pacific Limited

Annual Long Term Emoluments Emoluments

Base Fee Bonus Other Termination Super TotalPayments -annuation

$ $ $ $ $ $

A.G. Hartnell 52,000 - - - - 52,000

D.M. Doyle - - - - - -

M.D. Babiolakis* 326,826 - 33,054 - 23,710 383,590Managing Directorand CEO appointed29 May 2002

D.J. Taig** 194,697 - 18,602 1,522,840 14,458 1,750,597

F.A. Costa - - - - - -

C.C. Schokman - - - - - -

C.A. Stephen - - - - - -

B.W. Kemp 30,000 - - - 2,550 32,550

* During the year 1,000,000 options were issued to Mr Babiolakis, the terms and conditions are included in the share options section of this

Annual Report.

** 1,000,000 options issued to Mr Taig in 2001 were cancelled in 2002 following the termination of his contract with the Company.

14

15

Emoluments of the five most highly paid executive officers of the Company and the consolidated entity

Annual Long Term Emoluments Emoluments

Base Fee Bonus Other Termination Super TotalPayments -annuation

$ $ $ $ $ $

D.K. Green 115,108 - 18,825 - 7,460 141,393CFO and CompanySecretary appointed5 July 2002

S. Little 149,000 20,000 25,216 - 9,661 203,877General ManagerChiquita Mushrooms

P. McPherson 132,911 20,000 26,164 - 19,218 198,293General ManagerBFA & Chiquita Export

R.Tanti 123,644 30,000* 23,245 - 20,370 197,259General ManagerChiquita Nibbles & Banana Farms

M. Robinson 132,154 15,000 37,654 - 10,260 195,068General ManagerChiquita Trading

*Includes hardship allowance of $20,000 for relocating to Far North Queensland during the rationalisation of the Banana farms.

The elements of emoluments have been determined having regard to the cost to the Company and the consolidated

entity. Executives are those directly accountable and responsible for the operational management and strategic

direction of the Company and the consolidated entity. The category ‘Other’ includes the value of any non-cash

benefits provided. No value has been included in emoluments in respect of employee or executive options, as all

options were issued at exercise prices greater than the market value of ordinary shares as at 31 December 2002.

Bonuses paid in 2003 relate to the 2002 year performance and were only made where business unit performance

exceeded original budget estimates.

Options granted to directors and any of the five most highly paid officers

In addition to those options granted to the Managing Director Mr. Babiolakis, detailed above, the Remuneration

Committee resolved in January 2003 to issue each member of the Chiquita Executive, excluding Mr Babiolakis,

options over unissued shares in Chiquita Brands South Pacific Limited. The terms and conditions of these options

are included in the notes to the Financial Statements.

Directors’ Report continued

Directors’ Report continued

MEETINGS OF DIRECTORSThe number of meetings of directors (including meetings of committees of directors) held during the year and the

number of meetings attended by each director were as follows:

Director Board of Directors Remuneration Committee Audit Committee Meetings Meetings Meetings

Eligible Number Eligible Number Eligible Numberto attend attended to attend attended to attend attended

A.G. Hartnell 13 13 3 3 Nil Nil

D.M. Doyle 13 13 3 3 Nil Nil

M.D. Babiolakis* 8 8 Nil Nil Nil 1

D.J. Taig* 7 7 Nil Nil Nil 1

F.A. Costa 6 6 2 2 Nil Nil

C.C. Schokman 6 6 Nil Nil 1 1

C.A. Stephen 13 13 Nil Nil 2 2

B.W. Kemp 13 13 Nil Nil 2 2

At the date of this report, the Company had an Audit Committee and a Remuneration Committee of the

Board of Directors.

The members of the Audit Committee during the year were C. A. Stephen (Chairman), B. W. Kemp and

C. C. Schokman. *The Managing Director and CEO is an ex officio member of the Audit Committee.

The members of the Remuneration Committee are A. G. Hartnell (Chairman), D. M. Doyle and F. A. Costa.

ROUNDINGThe amounts contained in this report and in the financial statements have been rounded off under the option available

to the Company under ASIC Class Order 98/100. The Company is an entity to which the Class Order applies.

The numbers have been rounded to the nearest thousand dollars.

SIGNIFICANT EVENTS AFTER BALANCE DATENo matters or circumstances have arisen since the end of the financial year which significantly affected or may

significantly affect the operations of the consolidated entity, the results of those operations or the state of affairs

of the consolidated entity in future financial years.

CORPORATE GOVERNANCEIn recognising the need for the highest standards of corporate behaviour and accountability, the Directors of Chiquita

Brands South Pacific Ltd support and adhere to the principles of corporate governance. The Company’s corporate

governance statement is contained within this Annual Report.

Signed in accordance with a resolution of the Board of Directors,

Anthony G. Hartnell

Chairman

25 February 2003

16

17

Financials 2002

Statement of Financial PerformanceFor the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

Revenues from ordinary activities 2 312,359 311,592 16,723 19,604 Other expenses from ordinary activities, excluding borrowing costs 3 (329,494) (319,902) (33,456) (33,956)Borrowing costs 4 (5,739) (5,719) (1,275) (1,802)

Loss from ordinary activities before income tax expense 4 (22,874) (14,029) (18,008) (16,154)Income tax expense/(benefit) relating to ordinary activities 6 (4,363) (1,820) 470 94

Loss attributable to members of Chiquita Brands South Pacific Ltd 20 (18,511) (12,209) (18,478) (16,248)

Non-owner transaction changes in equityIncrease in retained profits on adoption of revised accounting standards:

Self-Generating & Regenerating Assets - AASB 1037 1,13 - 7,404 - 9,474

Total revenues, expenses and valuation adjustments attributable to members of Chiquita Brands South Pacific Limited and recognised directly into equity - 7,404 - 9,474

Total changes in equity from non-owner transactions attributable to members of Chiquita Brands South Pacific Limited (18,511) (4,805) (18,478) (6,774)

Basic earnings per share (cents per share) 26 (17.32) (18.10)Diluted earnings per share (cents per share) 26 (17.25) (18.10)Franked dividends per share (cents per share) 7 - 3.00

The accompanying notes form part of these financial statements.

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

CURRENT ASSETSCash assets - 1,009 - 1 Receivables 8 22,845 28,438 2,486 2,139 Inventories 9 23,807 21,631 1,339 801 Self-generating and regenerating assets 13 4,718 2,379 - - Current tax assets 6 1,921 1,900 - - Other 10 2,188 1,885 78 38

TOTAL CURRENT ASSETS 55,479 57,242 3,903 2,979

NON-CURRENT ASSETSReceivables 8 605 345 45,339 33,287 Other financial assets 11 409 409 12,248 20,616 Property, plant and equipment 12 68,657 72,633 9,804 9,046 Self-generating and regenerating assets 13 33,114 47,923 9,318 13,059 Intangible assets 14 10,877 12,020 555 589 Deferred tax assets 6 5,312 3,291 177 108 Other 10 - 139 - 63

TOTAL NON-CURRENT ASSETS 118,974 136,760 77,441 76,768

TOTAL ASSETS 174,453 194,002 81,344 79,747

CURRENT LIABILITIESPayables 15 32,712 27,198 1,844 1,929 Interest-bearing liabilities 16 15,471 21,494 6,858 4,536 Current tax liabilities 6 - - 180 284 Provisions 17 9,646 4,058 140 231 Other liabilities 18 47 - - -

TOTAL CURRENT LIABILITIES 57,876 52,750 9,022 6,980

NON-CURRENT LIABILITIESPayables 15 108 105 66 - Interest-bearing liabilities 16 40,707 67,396 288 6,854 Deferred tax liabilities 6 2,967 5,191 195 72 Provisions 17 1,108 2,765 87 80

TOTAL NON-CURRENT LIABILITIES 44,890 75,457 636 7,006

TOTAL LIABILITIES 102,766 128,207 9,658 13,986

NET ASSETS 71,687 65,795 71,686 65,761

EQUITYContributed equity 19 92,895 68,492 92,895 68,492 Accumulated losses 20 (21,208) (2,697) (21,209) (2,731)

TOTAL EQUITY 71,687 65,795 71,686 65,761

The accompanying notes form part of these financial statements.

Statement of Financial PositionAs at 31 December 2002

18

19

Statement of Cash FlowsFor the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

CASH FLOWS FROM OPERATING ACTIVITIESCash receipts in the course of operations 309,628 301,333 15,128 18,282 Cash payments in the course of operations (294,325) (290,241) (13,972) (16,546)Dividends received 20 18 - - Interest received 72 90 560 540 Borrowing costs paid (5,510) (6,329) (1,248) (1,809)Income taxes paid 97 (385) (89) (133)

NET OPERATING CASH FLOWS 21 9,982 4,486 379 334

CASH FLOWS FROM INVESTING ACTIVITIESPurchase of property, plant and equipment (8,861) (9,556) (1,135) (396)Proceeds from sale of property, plant and equipment 5,414 5,681 209 - Advances to related parties - - - 1,509 Repayment of advance to other persons 411 414 - 173Purchase of controlled entities - - (172) (1,004)

NET INVESTING CASH FLOWS (3,036) (3,461) (1,098) 282

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from issue of ordinary shares 25,606 - 25,606 -Share issue costs (1,203) - (1,203) - Repayment of borrowings - other loans (50,911) (10,000) (4,787) - Repayment of borrowings - related parties (4,161) - (19,129) -Proceeds from borrowings 21,615 12,499 - 214 Dividends paid - (830) - (830)Finance lease and hire purchase borrowings 711 - 361 -Finance lease and hire purchase payments (406) - (130) -

NET FINANCING CASH FLOWS (8,749) 1,669 718 (616)

NET INCREASE/(DECREASE) IN CASH HELD (1,803) 2,694 (1) -

Cash at the beginning of the financial year 1,009 (1,685) 1 1

CASH AT THE END OF THE FINANCIAL YEAR 21 (794) 1,009 - 1

The accompanying notes form part of these financial statements.

The financial report is a general purpose financial report,which has been prepared in accordance with the requirementsof the Corporations Act 2001, which includes applicableAccounting Standards. Other mandatory professional reportingrequirements (Urgent Issues Group Consensus Views) have also been complied with.

The financial report has been prepared in accordance with the historical cost convention, except for self-generating and regenerating assets measured at net market value.

Changes in accounting policiesThe accounting policies adopted are consistent with those of the previous year.

Principles of consolidationThe consolidated financial statements are those of the consolidated entity, Chiquita Brands South Pacific Limited,and all entities that Chiquita Brands South Pacific Limited controlled from time to time during the year and at balance date.

Information from the financial statements of subsidiaries is included from the date the parent company obtains controluntil such time as control ceases. Where there is a loss of control of a subsidiary, the consolidated financial statementsinclude the results for the part of the reporting period duringwhich the parent company has control.

Subsidiary acquisitions are accounted for using the purchasemethod of accounting.

The financial statements of subsidiaries are prepared for thesame reporting period as the parent company, using consistentaccounting policies.

All intercompany balances and transactions, including unrealised profits arising from intra-group transactions,have been eliminated in full.

Cash and cash equivalentsCash on hand and in banks are stated at nominal value.

For the purposes of the Statement of Cash Flows, cash includescash on hand and in banks, and money market investmentsreadily convertible to cash within two working days, net of outstanding bank overdrafts.

Bank overdrafts are carried at the principal amount.Interest is charged as an expense as it accrues.

ReceivablesTrade receivables are recognised and carried at original invoice amount less a provision for any uncollectable debts.An estimate for doubtful debts is made when collection of thefull amount is no longer probable. Bad debts are written-off as incurred.

Receivables from related parties are recognised and carried at the nominal amount due. Interest is taken up as income on an accruals basis.

InventoriesRaw material and stores

Raw material and stores are valued at the lower of cost andnet realisable value. Costs incurred in bringing each product to its present location and condition are accounted for on afirst-in first-out basis.

Finished goods and work in progress

Finished goods and work in progress are valued at the lower of cost and net realisable value. Costs incurred in bringing eachproduct to its present location and condition are accounted forusing average cost.

Self-generating and Regenerating Assets (SGARAs)Self-generating and regenerating assets are measured at theirnet market value at each reporting date. The net market valueis determined, in the absence of an active and liquid market inthe Group’s growing assets, as the net present value of cashflows expected to be generated by these crops (discounted at a risk adjusted interest rate).

Net increments or decrements in the market value of the cropsare recognised as revenues or expenses in the profit or loss,determined as:

(i) The difference between the total net market value ofthe crops recognised at the beginning of the financialyear and the total net market value of the crops recognised at the reporting date, less

(ii) Costs incurred during the financial year to acquire and plant the crops.

Costs incurred in maintaining or enhancing crops and plants are recognised as expenses when incurred.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

20

21

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

The market value of produce picked during the year and recognised as revenue is determined as the net market value of the crops immediately after picking, less the cost of picking.

Short lived crops such as mushrooms and carrots are accountedfor on a cost basis because cost is considered more relevantand reliable.

All non-current SGARA values have been determined in accordance with a directors’ valuation at each reporting date.In determining the market value the following factors havebeen taken into account:

(a) The productive life of the SGARA;

(b) The period over which the SGARA will mature;

(c) The expected future sale prices;

(d) The cost expected to arise throughout the life of the SGARA; and

(e) Net cash flows are discounted at a pre-tax averagereal rate of 15% per annum and it is assumed thatinflation will continue at the current rate.

Cash flows are gross of income tax and are expressed in real terms.

Expected future sale prices for all SGARAs, except vines,is constant in real terms, based on average prices throughoutthe current year. Vine sale prices are expected to decline overthe next 5 years. Costs, expected to arise throughout the life ofthe SGARAs, are constant in real terms, based on average coststhroughout the year. Details of plantings are outlined in Note 13.

Mushrooms and carrots (being short lived growing crops) have been valued on a cost basis and are disclosed as current SGARAs.

InvestmentsInvestments are brought to account at cost. The carryingamount of investments is reviewed annually by Directors to ensure it is not in excess of the recoverable amount of the investments. The recoverable amount is assessed from the underlying net assets in the particular entities.Dividends are brought to account in the profit and loss when received.

Property, Plant and EquipmentCost and valuation

Property, plant and equipment are brought to account at cost, less where applicable, any accumulated depreciation or amortisation. The carrying amount of property, plant and equipment is reviewed by Directors to ensure it is not in excess of the recoverable amount.

Depreciation and amortisation

The depreciable amounts of all fixed assets including buildingsand capitalised leased assets, but excluding freehold land aredepreciated over their useful lives commencing from the timethe asset is held ready for use.

Depreciation is provided on a straight line basis on all property,plant and equipment other than freehold land and water rights.

Major depreciation periods are:

- Freehold buildings 33 years

- Leasehold improvements 5 years

- Plant and equipment 5 to 20 years

- Market lease premiums 20 years

LeasesLeases are classified at inception as either operating or finance leases based on the economic substance of the agreement so as to reflect the risks and benefits incidental to ownership.

Operating leases

The minimum lease payments of operating leases, where the lessor effectively retains substantially all of the risks andbenefits of ownership of the leased item, are recognised as an expense on a straight line basis.

Finance leases

Leases of fixed assets where substantially all the risks and benefits incidental to the ownership of the asset, but not the legal ownership, are transferred to the Company are classified as finance leases. Finance leases are capitalised,recording an asset and a liability equal to the present value of the minimum lease payments, including any guaranteedresidual values. Leased assets are amortised over their estimated useful lives. Lease payments are allocated betweenthe reduction of the lease liability and the lease interestexpense for the period. Lease payments for operating leases,where substantially all the risk and benefits remain with thelessor, are charged as expenses in the periods in which they are incurred.

Costs of improvements to or on leasehold property is capitalised, disclosed as leasehold improvements, and amortised over the unexpired period of the lease or the estimated useful lives of the improvements, whichever is the shorter.

IntangiblesShare issue expenses

Costs associated with the public issue of shares and the listingof the Company on the Australian Stock Exchange incurredprior to 1999 are being written off over a period of twentyyears. Costs incurred from 1999 onwards have been written off against the proceeds of the share issues.

Acquisition costs

Professional costs associated with the listing of Chiquita and the associated acquisition, have been capitalised in these accounts and are being written off over a period of twenty years from the completion date of 15th January,1998. Costs associated with all acquisitions by Chiquita are also capitalised and written off over 20 years.

Goodwill

Goodwill is amortised using the straight line method over the period during which benefits are expected to be received,which is assumed to be twenty years.

Brand Names

The value of brand names has been supported by an external valuation. Brand names are recorded in the financial statementsat cost. No amortisation is provided against the carrying value of these brand names on the basis that their lives are consideredto be very long (in excess of 50 years) and that their terminalvalue approximates their carrying value.

Recoverable AmountNon-current assets are not carried at an amount above theirrecoverable amount, and where carrying values exceed thisrecoverable amount assets are written down. In determiningrecoverable amount, the expected net cash flows have been discounted to their present value using a market determined discount rate.

PayablesLiabilities for trade creditors and other amounts are carried at cost which is the fair value of the consideration to be paid in the future for goods and services received, whether or notbilled to the consolidated entity.

Payables to related parties are carried at the principal amount.Interest, when charged by the lender, is recognised as anexpense on an accruals basis.

Employee EntitlementsProvision is made for employee entitlement benefits accumulated as a result of employees rendering services up tothe reporting date. These benefits include wages and salaries,annual leave and long service leave. Liabilities arising inrespect of wages and salaries, annual leave and any other

employee entitlements expected to be settled within twelvemonths of the reporting date have been measured at theirnominal amount. All other employee entitlement liabilities are measured at the present value of estimated future cash outflows to be made in respect of services provided by employees up to the reporting date.

Employee entitlement expenses arising in respect of the following categories:

- Wages and salaries, non-monetary benefits, annualleave, long service leave, sick leave and other leave entitlements: and

- Other types of employee entitlements are chargedagainst profits on a net basis in their respective categories.

The employee share plans described in Note 24 do not result inany values being charged as an employee entitlement expense.

Interest-bearing liabilitiesAll loans (including commercial bills and convertible notes) are measured at the principal amount. Interest is charged as an expense as it accrues.

The finance lease liabilities are as determined in accordancewith the requirements of AASB 1008 “Leases“.

Contributed EquityIssued and paid-up capital is recognised at the fair value of the consideration received by the Company.

Any transaction costs arising on the issue of ordinary sharesare recognised directly in equity as a reduction of the shareproceeds received.

Revenue RecognitionRevenue is recognised to the extent that it is probable that the economic benefits will flow to the entity and the revenuecan be reliably measured. The following specific recognitioncriteria must also be met before revenue is recognised:

Sale of Goods:

Control of goods has passed to the buyer.

Rendering of Services:

Revenue from rendering services is recognised in the period in which the service is provided.

Interest:

Control of a right to receive consideration for the provision of, or investment in, assets has been attained.

Dividends:

Control of a right to receive consideration for the investment in assets is attained, usually evidenced by approval of the dividend at a meeting of shareholders.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

22

23

TaxesIncome Tax

Tax-effect accounting is applied using the liability methodwhereby income tax is regarded as an expense and is calculated on the accounting profit after allowing for permanent differences. The extent to which timing differencesoccur between the time items are recognised in the accountsand when items are taken into account in determining taxableincome, the net related taxation benefit or liability calculated at current rates is disclosed as a future income tax benefit or a provision for deferred income tax. The net future income tax benefit relating to tax losses and timing differences is not carried forward as an asset unless the benefit is virtually certain of being realised.

Goods and Services Tax (GST)

Revenue, expenses and assets are recognised net of theamount of GST except:

- Where the GST incurred on a purchase of goods andservices is not recoverable from the taxation authority,in which case the GST is recognised as part of the costof acquisition of the asset or as part of the expenseitem as applicable; and

- Receivables and payables are stated with the amountof GST included.

The net amount of GST recoverable from the taxation authorityis included as part of receivables in the Statement of FinancialPosition.

Cash flows are included in the Statement of Cash Flows on agross basis and the GST component of cash flows arising frominvesting and financing activities, which is recoverable from,payable to, the taxation authority are classified as operatingcash flows.

Foreign CurrenciesTransactions in foreign currencies of entities within the consolidated entity are converted to local currency at the rate of exchange ruling at the date of the transaction.

Amounts payable to and by the entities within the consolidatedentity that are outstanding at the balance date and are denominated in foreign currencies have been converted to local currency using rates of exchange ruling at the end of the financial year.

All resulting exchange differences arising on settlement or re-statement are brought to account in determining the profitor loss for the financial year, and transaction costs, premiumsand discounts on forward currency contracts are deferred and amortised over the life of the contract.

The Company does not enter into speculative forwardexchange contracts.

Earnings per Share (EPS)Basic EPS is calculated as net profit attributable to members,adjusted to exclude costs of servicing (other than dividends)and preference share dividends, divided by the weighted average number of ordinary shares, adjusted for any bonus element.

Diluted EPS is calculated as the net profit attributable to members, adjusted for:

- Cost of servicing equity (other than dividends) and preference share dividends;

- The after tax effect of dividends and interest associatedwith the dilutive potential ordinary shares that havebeen recognised as expenses; and

- Other non-discretionary changes in revenue or expenses during the period that would result from the dilution of potential ordinary shares;

divided by the weighted average number of ordinary sharesand dilutive potential ordinary shares, adjusted for any bonuselement.

ComparativesWhere necessary, comparatives have been reclassified for consistency with current year disclosures as a result of the firstapplication of revised Accounting Standard AASB 1005“Segment Reporting”.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

2. REVENUE FROM ORDINARY ACTIVITIESRevenues from operating activitiesRevenue from sales of goods 229,843 237,555 8,453 9,585 Revenue from services 4,077 4,724 234 394 Net market value of growing crops harvested 68,715 59,433 6,923 7,072 Net increment/(decrement) in market value of plant and growing crops 1,500 1,518 246 (91)

Total revenues from operating activities 304,135 303,230 15,856 16,960

Revenues from non-operating activitiesDividends and distributions

Wholly owned controlled entities - - - 1,900 Other persons / corporations 20 19 - -

Total dividends and distributions 20 19 - 1,900

Interest Wholly owned controlled entities - - 540 540 Other persons / corporations 72 91 20 -

Total interest 72 91 560 540

Proceeds on sale of non-current assets 5,414 5,681 209 - Rent 139 119 - - Other revenue 2,579 2,452 98 204

Total revenues from non-operating activities 8,224 8,362 867 2,644

Total revenues from ordinary activities 312,359 311,592 16,723 19,604

3. EXPENSES FROM ORDINARY ACTIVITIES(EXCLUDING BORROWING COSTS)

Cost of Goods Sold 253,455 252,707 9,983 12,213 Farming and production costs 21,943 15,818 3,921 1,212 Marketing, selling and distribution expenses 16,734 15,322 - 40 Administration costs 9,301 10,655 364 433 Other expenses from ordinary activities 570 14,925 - 858Significant items 5 27,491 10,475 19,188 19,200

Total expenses from ordinary operations (excluding borrowing costs) 329,494 319,902 33,456 33,956

24

25

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

4. PROFIT FROM ORDINARY ACTIVITIES BEFORE INCOME TAX EXPENSE

Profit and loss from ordinary activities before income tax has been arrived at after charging/(crediting) the following items:

ExpensesDepreciation of non-current assets

Buildings and improvements 1,160 1,175 37 5 Plant and equipment 3,815 4,996 54 412

Total depreciation of non-current assets 4,975 6,171 91 417

Amortisation of non-current assetsGoodwill 536 770 35 - Market lease premiums 149 189 - - Plant and equipment under lease 64 227 53 - Option premiums - 76 - - Acquisition costs - 41 - 41

Total amortisation of non-current assets 749 1,303 88 41

Total depreciation and amortisation expenses 5,724 7,474 179 458

Borrowing costs expensedOther related parties 469 632 1,243 1,802 Finance lease costs 70 96 27 - Other persons / corporations 5,200 4,991 5 -

Total borrowing costs expensed 5,739 5,719 1,275 1,802

Net foreign currency (gain)/loss 119 270 (1) - Bad and doubtful debts - trade debtors 351 1,425 - 3 Provision for employee entitlements 4,160 3,148 179 112 Operating lease rentals 6,957 6,272 99 138 Superannuation contributions 3,769 3,684 537 526 Net loss /(gain) on disposal of property, plant and equipment 764 395 (25) -

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

5. INDIVIDUALLY SIGNIFICANT ITEMS CHARGED IN OPERATING PROFIT FROM ORDINARY ACTIVITIES BEFORE INCOME TAX EXPENSE

Restructuring provision 10,186 1,018 - - Write-down of market lease premiums 1,407 - - - Write-down of plant and equipment 4,596 1,852 - - Write-down of land and buildings 5,568 580 - - Loss on sale of property, plant and equipment 1,077 - - - SGARA write-down 3,294 - 3,294 - Debtor provisioning 756 1,425 - - Write-down of carrying value of goodwill 607 5,600 - - Provision for diminution in value of investment in controlled entities - - 8,540 19,200 Provision for diminution in value of receivables from controlled entities - - 6,660 -

27,491 10,475 18,494 19,200

26

27

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

6. INCOME TAX

Prima facie tax on profit/(loss) from ordinary activities differs from the income tax provided in the financial statements as follows:

Loss from ordinary activities before income tax (22,874) (14,029) (18,008) (16,154)

Income tax expense calculated on profit/(loss) from ordinary activities at 30% (2001: 30%) (6,862) (4,209) (5,402) (4,846)Tax effect of permanent differences

Rebateable dividends - - - (570)SGARA adjustment 988 - 988 -Amortisation of intangible assets 226 114 10 - Other items (net) (866) (266) (230) (46)Write-down of intangible assets 565 1,680 - - Write-down of land & buildings 1,757 - - - Provision for diminution in value of investments and receivables - - 4,560 5,759 Tax losses not carried forward as future income tax benefits - 1,070 - -

Under/(over) provision of previous year (171) (209) 84 (203)

Income tax (benefit)/expense relating to profit from ordinary activities (4,363) (1,820) 470 94

Deferred tax assets and liabilitiesCurrent tax payable - - 180 284 Provision for deferred income tax - non-current 2,967 5,191 195 72 Future income tax benefit - current 1,921 1,900 - - Future income tax benefit - non-current 5,312 3,291 177 108

Income tax losses recognisedFuture income tax benefit arising from tax losses included in future income tax benefit 1,921 2,265 - -

Income tax losses not recognisedFuture income tax benefit arising from tax losses of a controlledentity not brought to account at balance date as realisation of thebenefit is not regarded as virtually certain 1,070 1,070 - -

The future tax benefit will only be obtained if:

(a) Future assessable income is derived of a nature and an amount sufficient to enable the benefit to be realised;

(b) The conditions of deductibility imposed by income tax legislation continue to be complied with; and

(c) No changes in income tax legislation adversely affect the consolidated entity in realising the benefit.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

28

29

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

7. DIVIDENDS PAID OR PROVIDED FOR

(a) Dividends paid during the yearCurrent year interimFranked dividends (2001: 3.0 cents per share) - 1,986 - 1,986

- 1,986 - 1,986

The rate at which dividends have or will be franked is 30% (2001:30%).(b) Franking credit balance

The amount of franking credits available for the subsequent financial year are:

Franking credit balance at the end of the financial year 137 137

Franking credits available within the group 2,378 2,441

Total franking credits 2,515 2,578

8. RECEIVABLES

CurrentTrade debtors 8(a),(b),(c) 21,972 27,512 2,400 1,987 Provision for doubtful debts (1,105) (1,665) - -

20,867 25,847 2,400 1,987 Sundry loans 8(c) 451 872 - - Other debtors 8(c) 1,513 1,715 75 148 Amounts other than trade debts receivable from related parties:

Employees 8(c) 14 4 11 4

22,845 28,438 2,486 2,139

Non-CurrentTrade debtors 264 - - - Deposits 119 120 - - Sundry loans 8(c) 222 225 222 224 Amounts other than trade debts receivable from:

Wholly owned controlled entities 8(c),31 - - 51,777 33,063 Provision for diminution in value of receivables from wholly controlled entities - - (6,660) -

605 345 45,339 33,287

(a) Related party trade receivablesTrade debtors include the following amounts receivable from related parties:

Wholly owned controlled entities - - 1,035 1,173

(b) Australian dollar equivalents Australian dollar equivalent of amounts receivable in foreign currency not effectively hedged:

- United States Dollar 642 - - -- New Zealand Dollar 87 - - -- Japanese Yen 276 - - -

1,005 - - -

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

8. RECEIVABLES continued

(c) Terms and conditionsTerms and conditions relating to the above financial instruments(i) Trade debtors are non-interest bearing and credit sales terms vary from 14 to 30 days depending

on the individual terms negotiated with customers.

(ii) Sundry loans are to unrelated suppliers of produce to the group and have an average maturity of four years.Interest is charged at rates specified in the loan agreements.

(iii) Employee loans are unsecured and bear interest at the rate necessary to avoid incurrance of Fringe Benefit Tax.They represent temporary advances repayable over ten years.

(iv) Detail of the terms and conditions of related party receivables are set out in Note 31.

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

9. INVENTORIESCurrentRaw materials and stores - at cost 3,604 2,920 324 324 Work in progress - at cost 1,699 8,885 - - Work in progress - at net realisable value 7,639 - - -Finished goods - at cost 10,865 9,826 1,015 477

23,807 21,631 1,339 801

10. OTHER ASSETSCurrentPrepayments 2,188 1,885 78 38

Non-CurrentOther - 139 - 63

11. OTHER FINANCIAL ASSETSNon-CurrentInvestments comprise:

Unlisted Shares - at cost 409 409 32 32 Unlisted shares in controlled entities - at cost - - 39,956 39,784 Provision for diminution in value of unlisted shares in controlled entities - - (27,740) (19,200)

409 409 12,248 20,616

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Chiquita BrandsSouth Pacific Ltd2002 2001$'000 $'000

11. OTHER FINANCIAL ASSETS continuedInvestments in controlled entities comprises:

Beneficial percentage held 2002 2001

Name % %

Angas Park Fruit Company Pty Ltd 100 100 19,548 19,420

CBSP Pty Ltd 100 100 18,290 18,290

Chiquita Brands Brisbane Pty Ltd* 100 100 - -

Chiquita Brands Melbourne Pty Ltd* 100 100 - -

Chiquita Nibbles Pty Ltd (formerly Chiquita Brands Sydney Pty Ltd)* 100 100 - -

Chiquita Foods Pty Ltd* 100 100 - -

Chiquita Mushrooms Holdings Pty Ltd 100 100 - -

Chiquita Mushrooms Pty Ltd 100 100 - -

Chiquita North Queensland Pty Ltd* 100 100 - -

Chiquita Plantations Innisfail Pty Ltd* 100 100 - -

Fruitexpress Pty Ltd* 100 100 - -

Chiquita Export (Australia) Pty Ltd (formerly Golden Goodness Fresh Pty Ltd)* 100 100 - -

Kangara Foods Pty Ltd 100 100 2,118 2,074

Loxton Fruit Processors Pty Ltd 100 100 - -

39,956 39,784

* Wholly owned subsidiaries of CBSP Pty Ltd

All controlled entities are incorporated in Australia.

30

31

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

12. PROPERTY, PLANT AND EQUIPMENTLand and Buildings:

At cost 38,295 49,863 6,960 7,065 Provision for depreciation (12,640) (11,392) (277) (240)

Total land and buildings 12(c) 25,655 38,471 6,683 6,825

Plant and equipmentAt cost 61,082 58,867 4,765 4,136 Provision for depreciation (25,012) (33,037) (2,137) (2,153)

12(c) 36,070 25,830 2,628 1,983

Plant and equipment under leaseAt cost 2,258 2,242 546 238 Provision for amortisation (908) (1,048) (53) -

12(c) 1,350 1,194 493 238

Total plant and equipment 37,420 27,024 3,121 2,221

Market lease premiumsAt cost 1,159 4,143 - - Provision for amortisation (559) (1,987) - -

12(c) 600 2,156 - -

Water RightsAt cost 4,982 4,982 - - Provision for amortisation - - - -

12(c) 4,982 4,982 - -

Total property, plant and equipmentAt cost 107,776 120,097 12,271 11,439 Provision for depreciation and amortisation (39,119) (47,464) (2,467) (2,393)

Total written down amount 68,657 72,633 9,804 9,046

(a) Assets pledged as securityAll freehold land and buildings are secured by mortgage debenture which has been granted as security over bank loans (see Note 16). Assets under lease are pledged as security for the associated lease liabilities.

(b) ValuationsAll freehold land and buildings were independently valued by Mason Green, during June 2000, on the basis of estimates of theamounts for which the assets could be exchanged between a knowledgeable willing buyer and a knowledgeable willing seller inan arm’s length transaction at valuation date. The total valuation for freehold land and buildings was $39.034 million.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

12. PROPERTY, PLANT AND EQUIPMENT continued(c) ReconciliationsLand and Buildings:

Carrying amount at beginning of year 38,471 39,164 6,825 5,937 Additions 310 709 128 - Disposals (6,398) (74) (233) - Transfer from plant and equipment - 427 - 893 Depreciation expense (1,160) (1,175) (37) (5)Write-down of land and buildings (5,568) (580) - -

25,655 38,471 6,683 6,825

Plant and Equipment at cost

Carrying amount at beginning of year 25,830 32,474 1,983 3,131 Additions 8,243 8,609 699 158 Disposals (769) (5,932) - - Transfer from /(to) SGARA 11,177 (3,129) - (894)Depreciation expense (3,815) (4,996) (54) (412)Write-down of plant and equipment (4,596) (1,196) - -

36,070 25,830 2,628 1,983

Plant and Equipment under lease

Carrying amount at beginning of year 1,194 1,262 238 - Additions 308 238 308 238 Disposals (88) (80) (1) - Depreciation expense (64) (226) (52) -

1,350 1,194 493 238

Market lease premiums

Carrying amount at beginning of year 2,156 2,346 - - Write-down of market lease premiums (1,407) - - - Depreciation expense (149) (190) - -

600 2,156 - -

Water Rights

Carrying amount at beginning of year 4,982 4,982 - -

4,982 4,982 - -

Total written-down amount 68,657 72,633 9,804 9,046

32

33

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

13. SELF-GENERATING AND REGENERATING ASSETSCurrentVines - at net market value 1,850 - - - Vegetables - at cost 2,868 2,379 - -

4,718 2,379 - -

Non-CurrentVines - at net market value 11,874 26,420 - - Fruit - at net market value 21,240 21,503 9,318 13,059

33,114 47,923 9,318 13,059

The SGARA valuations are based on the following plantings:

SGARAs Hectares Location Growing crop Productive life Non-matureplanted (approx) plant maturity

Vines 430 ha South Australia Primarily Shiraz In excess of 25 yrs Between now& Cabernet grapes and 2006

Fruit

Citrus 320 ha South Australia Primarily oranges In excess of 40 yrs Between nowand 2014

Blueberries 210 ha New South Wales Blueberries Between 1 & 11 yrs Between nowand 2006

Bananas* 315 ha Queensland Bananas Up to 9 yrs N/A

Other 77 ha South Australia Prunes & Apricots Between 5 & 10 yrs N/A

Vegetables

Mushrooms N/A Victoria Mushrooms Less than 1 yr N/A

Carrots 171 ha South Australia Carrots Less than 1 yr N/A

* The net market value of bananas has been assessed as nil (2001:Nil) at 31 December 2002.

Notes to the Financial StatementsFinancial Statements for the year ended 31 December 2002

Consolidated Chiquita BrandsSouth Pacific Ltd

2002 2001 2002 2001Note $'000 $'000 $'000 $'000

14. INTANGIBLE ASSETSGoodwill 7,420 10,683 - - Provision for amortisation (1,114) (3,268) - -

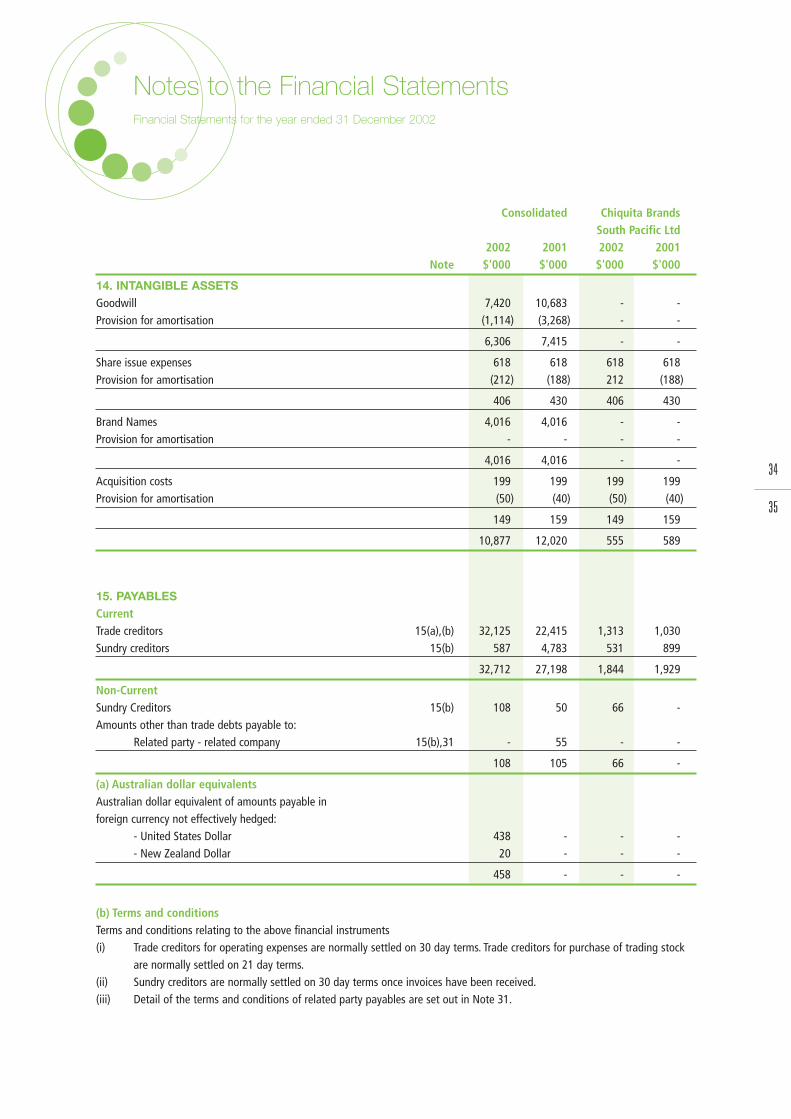

6,306 7,415 - -

Share issue expenses 618 618 618 618 Provision for amortisation (212) (188) 212 (188)

406 430 406 430

Brand Names 4,016 4,016 - - Provision for amortisation - - - -

4,016 4,016 - -

Acquisition costs 199 199 199 199 Provision for amortisation (50) (40) (50) (40)

149 159 149 159

10,877 12,020 555 589

15. PAYABLESCurrentTrade creditors 15(a),(b) 32,125 22,415 1,313 1,030 Sundry creditors 15(b) 587 4,783 531 899

32,712 27,198 1,844 1,929

Non-CurrentSundry Creditors 15(b) 108 50 66 - Amounts other than trade debts payable to:

Related party - related company 15(b),31 - 55 - -

108 105 66 -

(a) Australian dollar equivalents Australian dollar equivalent of amounts payable inforeign currency not effectively hedged:

- United States Dollar 438 - - -- New Zealand Dollar 20 - - -

458 - - -

(b) Terms and conditionsTerms and conditions relating to the above financial instruments(i) Trade creditors for operating expenses are normally settled on 30 day terms. Trade creditors for purchase of trading stock