city annual financial report fye 6-30-2013

DESCRIPTION

City of Carmel-by-the-SeaTRANSCRIPT

CITY OF CARMEL-BY-THE-SEA, CALIFORNIA

ANNUAL FINANCIAL REPORT

FOR THE FISCAL YEAR ENDED

JUNE 30, 2013

Prepared by:

Paul Wood Finance Director

This page intentionally left blank.

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Table of Contents

i

Page

Table of Contents .................................................................................................................................. i Organization Chart ........................................................................................................................... iii List of Officials ………………………………………………………………………………………iv

Independent Auditors’ Report ........................................................................................................... 1

Management’s Discussion and Analysis (Required Supplementary Information) ....................... 3

Basic Financial Statements:

Government-Wide Financial Statements: Statement of Net Position ........................................................................................................ 15 Statement of Activities ............................................................................................................ 16

Fund Financial Statements:

Governmental Funds: Balance Sheet ................................................................................................................................ 20 Reconciliation of Governmental Funds Balance Sheet to the Statement of Net Position ........................................................................................................ 22 Reconciliation of Fund Basis Balance Sheet to Government-wide Statement of Net Position – Governmental Activities ............................................................. 23 Statement of Revenues, Expenditures, and Changes

in Fund Balances – Governmental Funds ................................................................................ 24 Reconciliation of Fund Basis Statements to Government-wide Statement of Activities ............................................................................................................ 26 Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities ............................... 27

Statement of Revenues, Expenditures, and Changes in Fund Balances - Budget to Actual – General Fund and Major Special Revenue Funds ................................................................................................. 28

FINANCIAL SECTION

INTRODUCTORY SECTION

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Table of Contents, Continued

ii

Page Basic Financial Statements, Continued:

Notes to Basic Financial Statements .......................................................................................... 33

Other Supplemental Information:

Required Supplementary Information: Other Postemployment Benefits – Schedule of Funding Progress ................................................ 61

Combining and Individual Fund Financial Statements and Schedules:

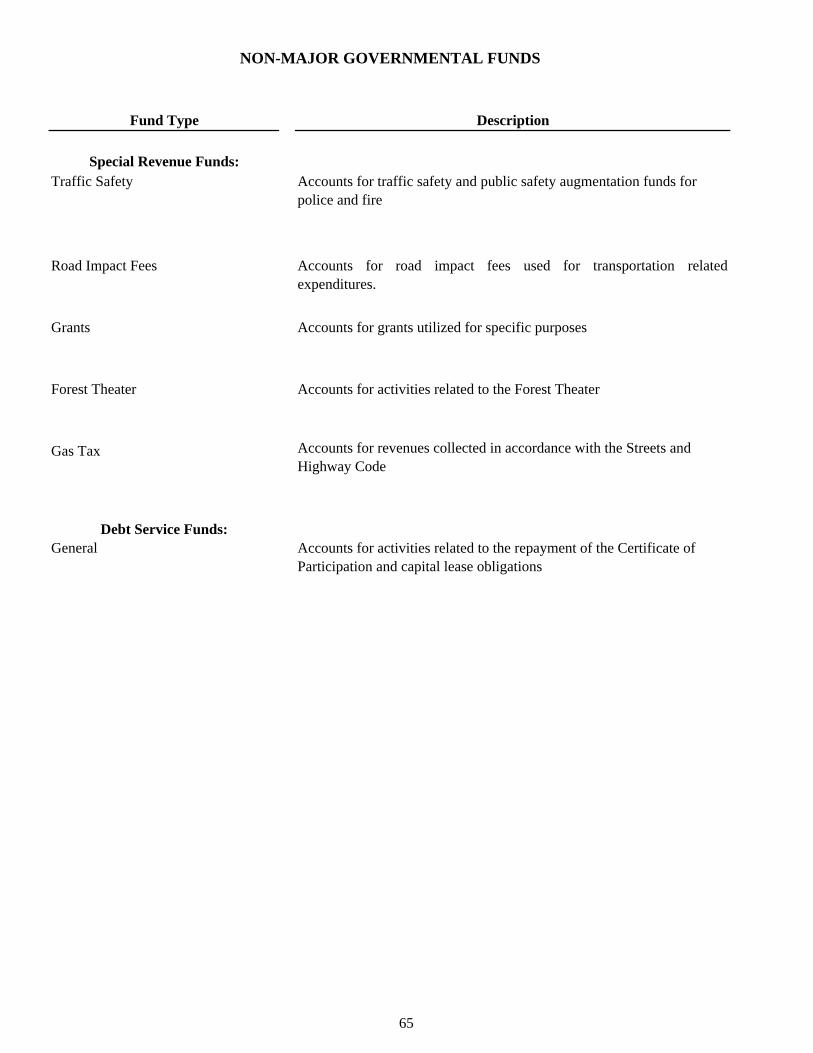

Nonmajor Governmental Funds: Combining Balance Sheet ............................................................................................................. 66 Combining Statement of Revenues, Expenditures, and Changes

in Fund Balances ............................................................................................................... 68

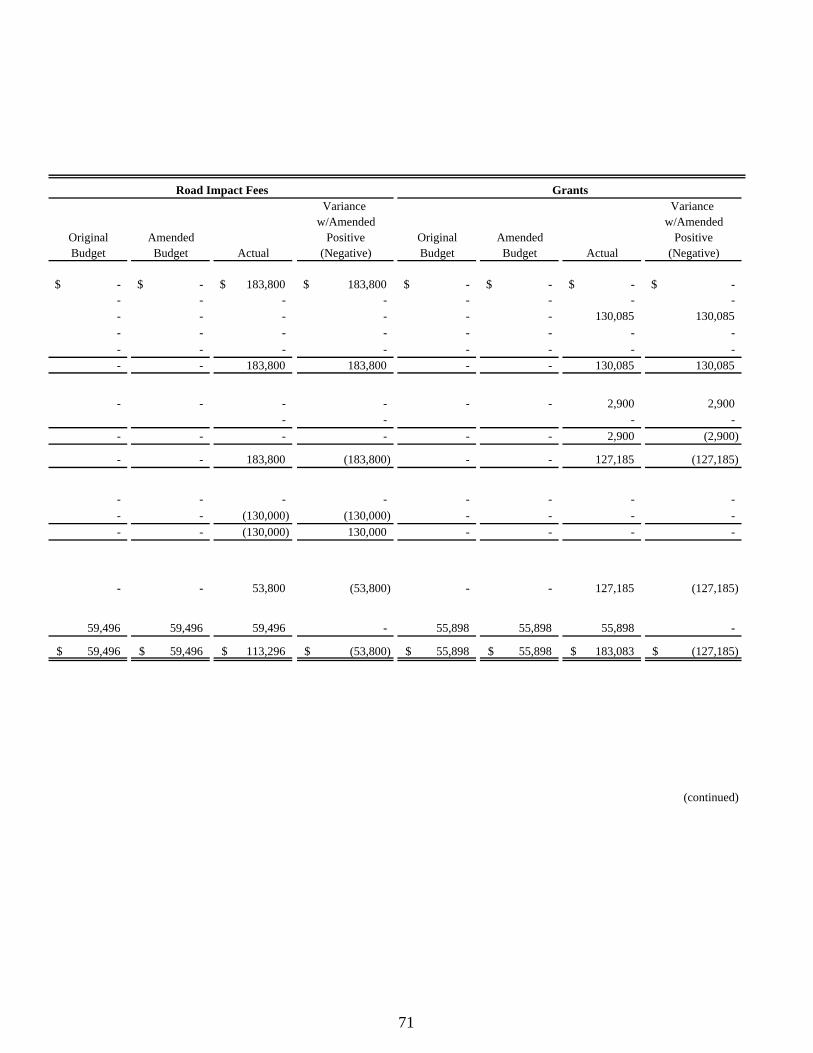

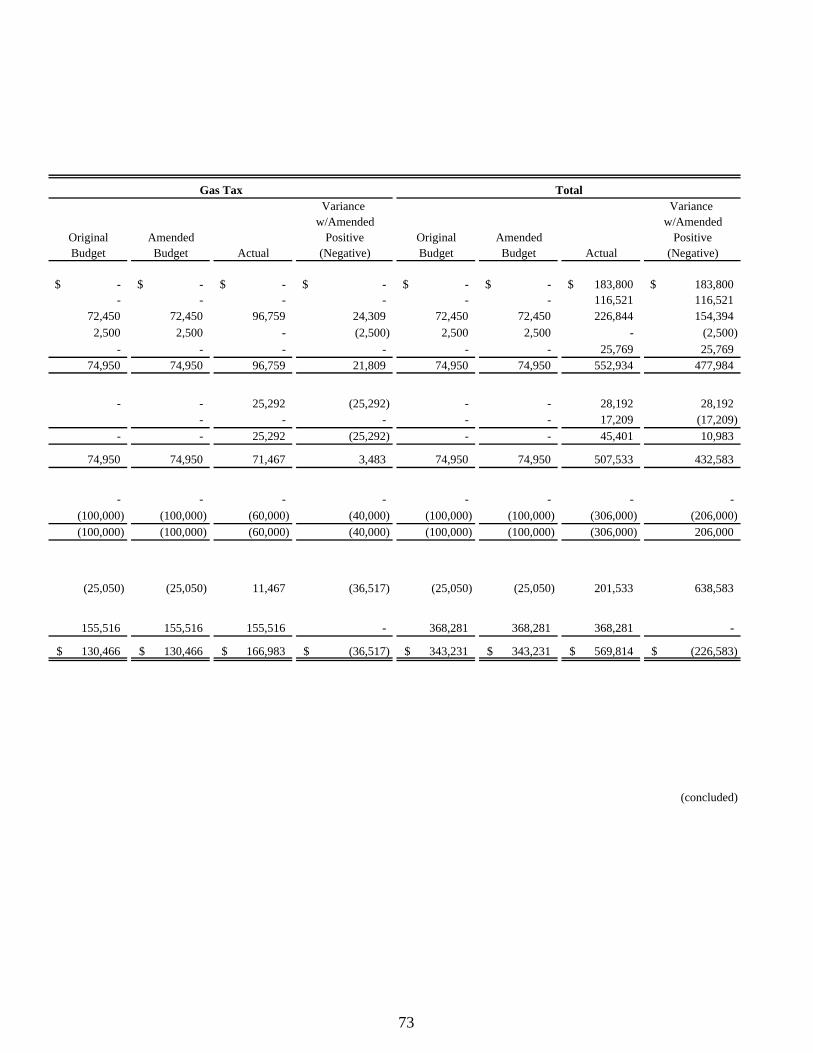

Nonmajor Special Revenue Funds: Schedule of Revenues, Expenditures, and Changes in Fund Balances – Budget to Actual ............................................................................................................... 70

Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in

Accordance With Government Auditing Standard .................................................................. 75

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Organization Chart

iii

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 List of Officials

iv

Jason Burnett, Mayor Ken Talmage, Vice Mayor Victoria Beach, Councilmember Carrie Theis, Councilmember Steve Hillyard, Councilmember

Jason Stilwell, City Administrator

Don Freeman, City Attorney

Susan Paul, Administrative Services Director

James Emery, City Treasurer

Sherman Low, City Engineer

CITY OFFICIALS

CITY COUNCIL

7080 Donlon Way, Suite 204, Dublin, CA 94568 ● phone (925) 556-6200 ● fax: (510) 217-5930 www.jjacpa.com

INDEPENDENT AUDITOR’S REPORT To the Honorable Mayor and City Council of the City of Carmel-by-the-Sea Carmel-by-the-Sea, California

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund, the aggregate remaining fund information, and the budgetary comparison information of the City of Carmel-by-the-Sea, California (City), as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise the City’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City, as of June 30, 2013, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

To the Honorable Mayor and City Council of the City of Carmel-by-the-Sea Carmel-by-the-Sea, California Page 2

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the Management’s Discussion and Analysis and budgetary comparison information and other information listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City’s basic financial statements. The combining and individual nonmajor fund financial statements and the introductory sections are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The combining and individual nonmajor fund financial statements and the introductory sections are the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual nonmajor fund financial statements and the introductory sections are fairly stated, in all material respects, in relation to the basic financial statements as a whole.

The combining and individual nonmajor fund financial statements and the introductory sections has not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on it.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated January 31, 2014 on our consideration of the City's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering City’s internal control over financial reporting and compliance.

]]TVcT? \ÇvA January 31, 2014 JJACPA, INC. Dublin, CA

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis

3

This section provides a narrative overview and analysis of the financial activities of the City of Carmel-by-the-Sea (City) for the fiscal year ended June 30, 2013. It should be read in conjunction with the accompanying transmittal letter and basic financial statements. FINANCIAL HIGHLIGHTS ♦ As of June 30, 2013, total assets of the City exceeded its liabilities by $32,377,893 (net position).

The portion of net position that may be used to meet the government’s ongoing obligations to citizens and creditors (unrestricted net position) is $2,205,463. The portion of net position that is restricted and may only be used for specific purposes is $566,992. The remaining $29,605,438 is invested in capital assets.

♦ As of June 30, 2013, the City’s governmental funds reported combined ending fund balances of

$10,558,901. Approximately .4% of this total amount ($46,747) is non-spendable to indicate that it is not available because it represents amounts that are more long-term in nature or will never be converted to cash. Of the remaining balance, $566,992 is restricted because it represents resources that are required to be spent for specific purposes as provided by an external source. The committed balance of $2,898,615 represents a Council commitment for economic uncertainties and anticipated future short-term structural deficits. The assigned fund balances in Special Revenue Funds amounted to $1,793,249 and represented Library, Parking and Ambulance Fund items. The remaining fund balance is unassigned.

♦ Capital assets, net of depreciation, decreased to $37,285,185 from $39,349,535, due to depreciation

and adjustments of ($1,256,304) and net capital asset retirements and adjustments of ($808,046).

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

4

OVERVIEW OF THE ANNUAL FINANCIAL REPORT This Annual Financial Report is in two major parts: 1) Introductory section, which includes the Transmittal Letter and general information; 2) Financial section, which includes the Management’s Discussion and Analysis (this part), the Basic

Financial Statements, which include the Government-wide and the Fund Financial Statements along with the notes to these financial statements and Combining and Individual Fund Financial Statements and Schedules.

The Basic Financial Statements The Basic Financial Statements are comprised of the Government-wide Financial Statements and the Fund Financial Statements; these two sets of financial statements provide two different views of the City’s financial activities and financial position. The Government-wide Financial Statements The Government-wide Financial Statements provide a broad overview of the City’s activities as a whole and comprise the Statement of Net Position and the Statement of Activities. The Statement of Net Position provides information about the financial position of the City as a whole, including all its capital assets and long-term liabilities on the full accrual basis, similar to that used by corporations. The Statement of Activities provides information about all the City’s revenues and all its expenses, also on the full accrual basis, with the emphasis on measuring net revenues or expenses of each the City’s programs. The Statement of Activities explains in detail the change in Net Position for the year. All of the City’s activities are grouped into Governmental Activities, as explained below. ♦ Governmental activities – All of the City’s basic services are considered to be governmental

activities, including general government, community development, economic development, public safety, animal control, engineering, community events, public improvements, planning and zoning, building inspections, and general administration. These services are supported by general City revenues such as taxes and by specific program revenues such as developer fees.

Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the City can be divided into two categories: governmental funds and proprietary funds.

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

5

OVERVIEW OF THE ANNUAL FINANCIAL REPORT, Continued Fund Financial Statements, continued Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the Government-wide Financial Statements. However, unlike the Government-wide Financial Statements, Governmental Fund Financial Statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements. Because the focus of the Governmental Fund Financial Statements is narrower than that of the Government-wide Financial Statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the Government-wide Financial Statement. By doing so, readers may better understand the long-term impact of the government’s near-term financial decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. The Governmental Fund Financial Statements provide detailed information about each of the City’s most significant funds, called major funds. The concept of major funds, and the determination of which are major funds, was established by GASB Statement 34 and replaces the concept of combining like funds and presenting them as one total. Instead, each major fund is presented individually, with all non-major funds summarized and presented only in a single column. Subordinate schedules present the detail of these non-major funds. Major funds present the major activities of the City for the year, and may change from year to year as a result of changes in the pattern of the City’s activities. For the fiscal year ended June 30, 2013, the City’s major funds are as follows: GOVERNMENTAL FUNDS:

General Fund Harrison Memorial Library Special Revenue Fund Parking Special Revenue Fund Ambulance Special Revenue Fund

Notes to the Basic Financial Statements The notes provide additional information that is essential to a full understanding of the data provided in the Government-wide and Fund Financial Statements. The notes to the basic financial statements can be found on pages 33-60 of this report. Required Supplementary Information follows the notes on page 61. Combining and Individual Fund Financial Statements and Schedules The combining statements referred to earlier in connection with non-major governmental funds are presented immediately following the notes to the financial statements. Combining and individual fund statements can be found on pages 63-73 of this report.

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

6

GOVERNMENT-WIDE FINANCIAL ANALYSIS As noted earlier, net position may serve over time as a useful indicator of a government’s financial position. In the case of the City, assets exceeded liabilities by $32,377,893 as of June 30, 2013. The Summary of Net Position as of June 30, 2013, and 2012, follows:

2013 2012Govern- Govern-mental mental

Activities Activities Changes

Current and other assets 12,042,025$ 11,027,118$ 1,014,907$ Noncurrent assets 37,285,185 39,349,535 (2,064,350)

Total assets 49,327,210 50,376,653 (1,049,443)

Current and other liabilities 2,440,181 1,812,246 627,935 Long-term liabilities 14,509,136 9,226,006 5,283,130

Total liabilities 16,949,317 11,038,252 5,911,065

Net position:Net invested in capital assets 29,605,438 31,374,354 (1,768,916)

Restricted 566,992 555,524 11,468 Unrestricted 2,205,463 7,408,523 (5,203,060)

Total net position 32,377,893$ 39,338,401$ (6,960,508)$

Summary of Net Position

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

7

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued The change in net position for the fiscal years ended June 30, 2013, and 2012, follows:

2013 2012Govern- Govern-mental mental

Activities Activities Changes

Revenues:Program revenues:

Charges for services 702,381$ 493,248$ 209,133$ Grants and contributions:

Operating 1,474,331 871,230 603,101 General revenues:

Property taxesand assessments 4,652,176 4,571,481 80,695

Transient occupancy taxes 4,615,598 4,179,900 435,698 Sales tax 2,760,414 1,743,748 1,016,666 Franchises 981,831 491,674 490,157 Business licenses 577,364 532,019 45,345 Use of money and property 69,735 55,995 13,740

Other general revenues 98,331 276,751 (178,420) Total revenues 15,932,161 13,216,046 2,716,115

Expenses:Governmental activities:

Administration 9,481,135 2,904,382 6,576,753 Building maintenance 3,763,094 2,718,581 1,044,513 Public safety 4,193,157 4,694,672 (501,515) Public works 1,896,305 1,790,684 105,621 Forest, parks and beaches 472,123 1,578,381 (1,106,258) Culture and recreation 2,405,481 1,314,073 1,091,408 Economic development 304,587 361,458 (56,871) Interest and fiscal charges 376,787 194,153 182,634

Total expenses 22,892,669 15,556,384 7,336,285

Excess (Deficiency) of revenues overexpenditures before transfers (6,960,508) (2,340,338) (4,620,170)

Transfers - - -

Special Item:Infrastructure capitalization - 13,760,000 (13,760,000)

Change in net position (6,960,508) 11,419,662 (4,620,170)

Net position:Beginning of year 39,338,401 27,918,739 11,419,662 End of year 32,377,893$ 39,338,401$ 6,799,492$

Changes in Net Position

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

8

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued Revenues The City’s total revenues for governmental were $15,932,161 for the fiscal year ended June 30, 2013. Approximately 75% of the City’s key revenues are generated from three major sources. The following discusses variances in key revenues from the prior fiscal year:

1. Property Taxes. Property taxes increased 1.77% over last year reflecting a continuing strengthening real estate market over the past year.

2. Transient occupancy taxes. Hostelry taxes increased 10.42% reflecting a continuing growth in tourism and potential benefit from citywide and individual marketing efforts.

3. Sales Tax. Annual receipts increased 4.8%. This increase is attributed to increases in

building and construction (+21%) and hotels and restaurants (+8%) offset by decreases in general consumer goods (-1%) and business and industry (-34%). We anticipate that sales tax revenue will continue to rebound next fiscal year at about a 4% rate. Beginning in April, 2013, the City started collecting an additional 1% use tax pursuant to the passage of Measure D in the November, 2012 election. Receipts for the three months ended June 30, 2013 were in excess of $682,000.

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

9

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued Expenses Governmental activity expenses of the City for the year totaled $22,892,669. Public Safety costs represented 18.32% of total governmental activities expenses and represented the largest single expense for governmental activities. Governmental Activities The following table shows the cost of each of the City’s major programs and the net cost of the programs. Net cost is the total cost less fees and other direct revenue generated by the activities. The net cost reflects the financial burden that was placed on the City’s taxpayers by each of the programs. The total cost of services and the net cost of services for the fiscal years ended June 30, 2013, and 2012, are as follows:

Total Cost Net Cost Total Cost Net Costof Services of Services of Services of Services

Administration 9,481,135$ 9,461,314$ 2,904,382$ 2,899,647$ Building maintenance 3,763,094 3,763,094 2,718,581 2,718,581 Public safety 4,193,157 3,250,139 4,694,672 4,065,576 Public works 1,896,305 1,118,292 1,790,684 1,096,067 Forest, parks and beaches 472,123 472,123 1,578,381 1,578,381 Culture and recreation 2,405,481 1,969,621 1,314,073 1,278,043 Economic development 304,587 304,587 361,458 361,458 Interest and fiscal charges 376,787 376,787 194,153 194,153

Total 22,892,669$ 20,715,957$ 15,556,384$ 14,191,906$

2013 2012

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

10

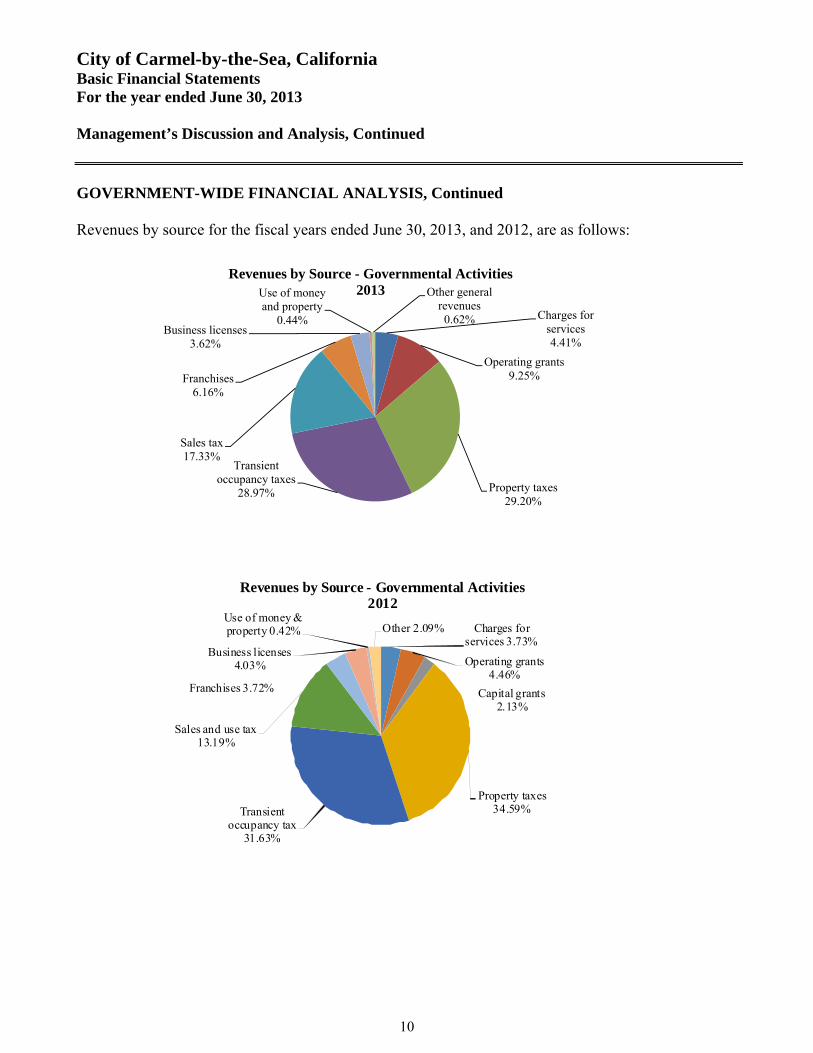

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued Revenues by source for the fiscal years ended June 30, 2013, and 2012, are as follows:

Charges for services4.41%

Operating grants9.25%

Property taxes29.20%

Transient occupancy taxes

28.97%

Sales tax17.33%

Franchises6.16%

Business licenses3.62%

Use of money and property

0.44%

Other general revenues0.62%

Revenues by Source - Governmental Activities 2013

Charges for services 3.73%

Operating grants 4.46%

Capital grants 2.13%

Property taxes 34.59%Transient

occupancy tax 31.63%

Sales and use tax 13.19%

Franchises 3.72%

Business licenses 4.03%

Use of money & property 0.42% Other 2.09%

Revenues by Source - Governmental Activities2012

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

11

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued

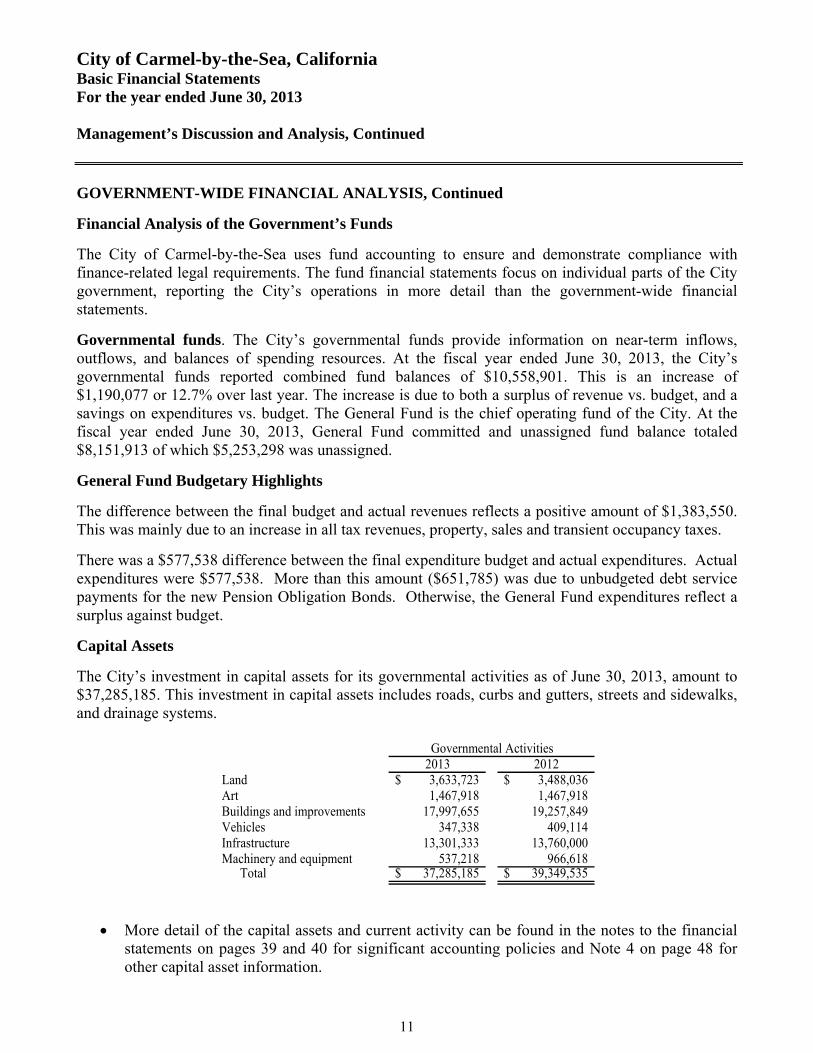

Financial Analysis of the Government’s Funds

The City of Carmel-by-the-Sea uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. The fund financial statements focus on individual parts of the City government, reporting the City’s operations in more detail than the government-wide financial statements.

Governmental funds. The City’s governmental funds provide information on near-term inflows, outflows, and balances of spending resources. At the fiscal year ended June 30, 2013, the City’s governmental funds reported combined fund balances of $10,558,901. This is an increase of $1,190,077 or 12.7% over last year. The increase is due to both a surplus of revenue vs. budget, and a savings on expenditures vs. budget. The General Fund is the chief operating fund of the City. At the fiscal year ended June 30, 2013, General Fund committed and unassigned fund balance totaled $8,151,913 of which $5,253,298 was unassigned.

General Fund Budgetary Highlights

The difference between the final budget and actual revenues reflects a positive amount of $1,383,550. This was mainly due to an increase in all tax revenues, property, sales and transient occupancy taxes.

There was a $577,538 difference between the final expenditure budget and actual expenditures. Actual expenditures were $577,538. More than this amount ($651,785) was due to unbudgeted debt service payments for the new Pension Obligation Bonds. Otherwise, the General Fund expenditures reflect a surplus against budget.

Capital Assets

The City’s investment in capital assets for its governmental activities as of June 30, 2013, amount to $37,285,185. This investment in capital assets includes roads, curbs and gutters, streets and sidewalks, and drainage systems.

2013 2012Land 3,633,723$ 3,488,036$ Art 1,467,918 1,467,918 Buildings and improvements 17,997,655 19,257,849 Vehicles 347,338 409,114 Infrastructure 13,301,333 13,760,000 Machinery and equipment 537,218 966,618

Total 37,285,185$ 39,349,535$

Governmental Activities

More detail of the capital assets and current activity can be found in the notes to the financial statements on pages 39 and 40 for significant accounting policies and Note 4 on page 48 for other capital asset information.

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Management’s Discussion and Analysis, Continued

12

GOVERNMENT-WIDE FINANCIAL ANALYSIS, Continued Debt Administration Debt, considered a liability of governmental activities, increased by $5,869,566, reflecting the pay down of the Sunset bond and lease obligations, offset by an increase in the OPEB obligation, and the issuance of the new Pension Obligation Bonds, see Note 6 on page 49. Compensated absences decreased by $79,995 to $458,376 of which $273,981 is considered a current liability.

Economic Outlook

Fiscal year 2013-2014 will continue to be another “hard to forecast” year. While consumer spending continues to rise at a modest pace, still assisted by an extraordinarily simulative Federal Reserve, it is hard to predict what consumers will do when the Fed takes its foot off the gas pedal. The State of California has seen larger than expected revenue surpluses brought about by Proposition 30’s personal income tax rates for high-income taxpayers and healthy local property tax growth, but the state’s Legislative Analyst’s Office (LAO) expresses cautious optimism due to economic and political uncertainty. On issues that relate to us more locally, Wells Fargo’s “California Economic Outlook” states that California tourism continues to rebound with hotel occupancy and ADR (average daily room rate). Average daily rates in the San Francisco and San Jose areas are up roughly 8 to 10 percent year to date. From our records, we confirm the trend with Carmel’s YOY (year over year) ADR increasing 8%. Somewhat promising, recent unemployment figures for the Monterey Region have fallen to 10.9 percent from over 12 percent last year. Additionally, home prices are rising in the coastal region, and are adding to local coffers in property taxes. These factors and the many unanswered questions concerning political, fiscal, including international monetary outcomes, will likely result in a relatively weak economic period ahead.

The City’s major General Fund revenue sources are property tax, hostelry tax and sales tax. All of these revenue sources are rising currently, but with the economy in such slow recovery, and for such unsustainable reasons, we must prepare ourselves for an economic slowdown. We are estimating an increase for sales tax revenue in fiscal year 2013–2014 of 3-4%. Also, in fiscal year 2013–2014, we are estimating property taxes to increase 4-5%.

The City maintains a multi-year forecasting model to project anticipated revenues and expenditures. The model projects continued increased revenues through fiscal year 2017-18, along with increased investments in infrastructure maintenance, capital outlay and IT backbone and infrastructure. If the national economy reverses, there will be a correlated reduction in this capital spending.

Requests for Information

This Annual Financial Report is intended to provide citizens, taxpayers, investors, and creditors with a general overview of the City’s finances. If you have any questions about this report, need additional financial information, or would like to obtain component unit financial statements, contact the City of Carmel-by-the-Sea Finance Department, PO Box CC, Carmel-by-the-Sea, CA 93921, or visit the City’s web page at ci.carmel.ca.us/carmel/.

BASIC FINANCIAL STATEMENTS

13

This page intentionally left blank.

14

City of Carmel-by-the-Sea, CaliforniaStatement of Net Position

June 30, 2013

Governmental Activities

ASSETSCurrent assets:

Cash and investments 9,012,438$ Cash and investments with fiscal agents 400,008 Receivables:

Accounts receivable 809,875 Intergovernmental receivable 929,066 Other receivables 890,638 Total current assets 12,042,025

Noncurrent assets:Capital assets:

Nondepreciable 5,101,641 Depreciable 32,183,544 Total noncurrent assets 37,285,185

Total assets 49,327,210

LIABILITIESCurrent liabilities:

Accounts payable and accrued liabilities 562,889 Deposits payable 460,235 Interest payable 47,793 Compensated absences - current portion 273,981 Due within one year 1,095,283

Total current liabilities 2,440,181 Noncurrent liabilities:

Long-term liabilities:Claims liabilities 460,000 Compensated absences 184,395 Due after one year 12,749,464 Net OPEB obligation 1,115,277 Total noncurrent liabilities 14,509,136

Total liabilities 16,949,317

NET POSITIONNet invested in capital assets 29,605,438 Restricted 566,992 Unrestricted 2,205,463

Total net position 32,377,893$

Total liabilities and net position 49,327,210$

The accompanying notes are an integral part of these basic financial statements.

15

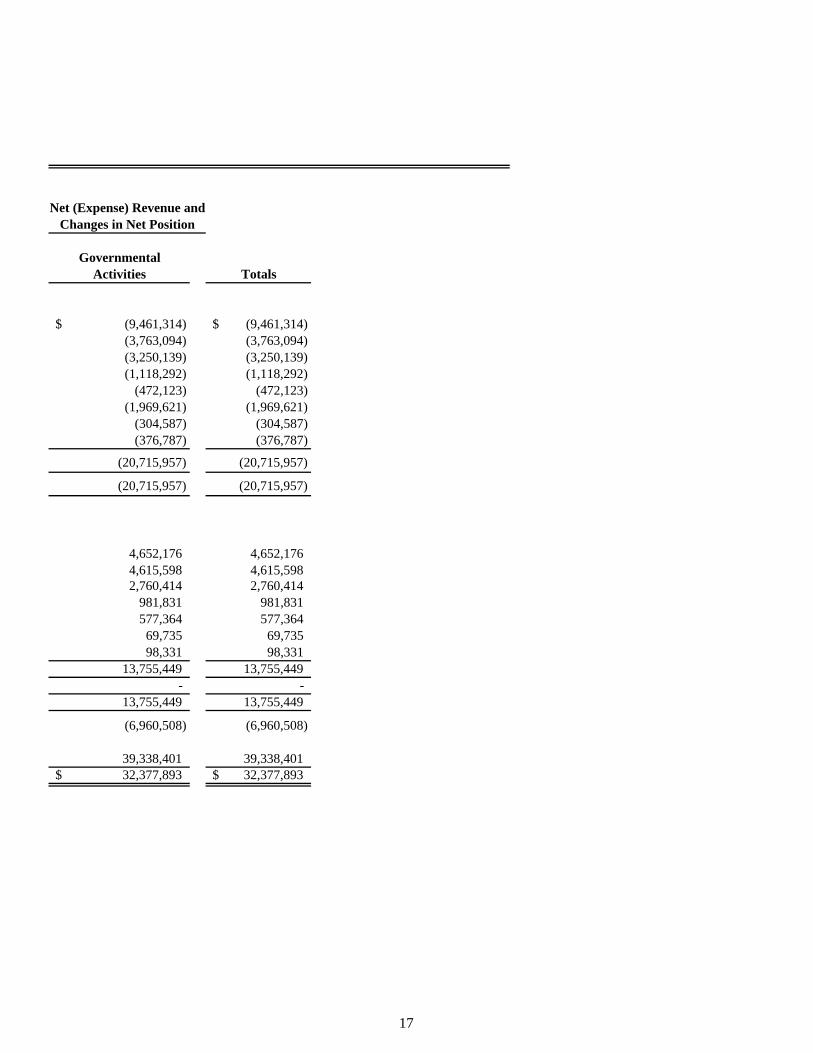

City of Carmel-by-the-Sea, CaliforniaStatement of Activities

For the year ended June 30, 2013

OperatingCharges for Grants and

Functions/Programs Expenses Services ContributionsPrimary government:Governmental activities:

Administration 9,481,135$ 19,821$ -$ Building maintenance 3,763,094 - - Public safety 4,193,157 167,723 775,295Public works 1,896,305 433,928 344,085Forest, parks and beaches 472,123 - - Culture and recreation 2,405,481 80,909 354,951Economic development 304,587 - - Interest and fiscal charges 376,787 - -

Total governmental activities 22,892,669 702,381 1,474,331

Total primary government 22,892,669$ 702,381$ 1,474,331$

General revenues: Taxes:

Property taxes, levied for general purposesTransient occupancy tax, levied for general purposesSales and use tax

FranchisesBusiness licensesUse of money and propertyOther general revenues

Total general revenuesTransfers

Total general revenues and transfers

Change in net positionNet position:

Beginning of yearNet position - Ending

Program Revenues

The accompanying notes are an integral part of these basic financial statements.

16

GovernmentalActivities Totals

(9,461,314)$ (9,461,314)$ (3,763,094) (3,763,094) (3,250,139) (3,250,139) (1,118,292) (1,118,292)

(472,123) (472,123) (1,969,621) (1,969,621)

(304,587) (304,587) (376,787) (376,787)

(20,715,957) (20,715,957)

(20,715,957) (20,715,957)

4,652,176 4,652,176 4,615,598 4,615,598 2,760,414 2,760,414

981,831 981,831 577,364 577,364

69,735 69,735 98,331 98,331

13,755,449 13,755,449 - -

13,755,449 13,755,449

(6,960,508) (6,960,508)

39,338,401 39,338,401 32,377,893$ 32,377,893$

Net (Expense) Revenue andChanges in Net Position

17

This page intentionally left blank.

18

Fund

Governmental Funds:

General Fund

Harrison Memorial Library Special Revenue Fund

Parking Special Revenue Fund

Ambulance Special Revenue Fund Accounts for activities associated with ambulance service billings,which have been outsourced to a third party.

FUND FINANCIAL STATEMENTS

Description

MAJOR FUNDS

The Fund Financial Statements present only individual major fiunds, while non-major funds are combined in a single column. Major funds are defined as having significant activities or balances in the current year.

Accounts for activities associated with the Harrison Memorial Library

Accounts for activities associated with parking in-lieu fees.

Primary operating fund of the City; accounts for all activities except those legally or administratively required to be accounted for in other funds.

19

City of Carmel-by-the-Sea, CaliforniaBalance Sheet

Governmental Funds

June 30, 2013

General Harrison MemorialFund Library Parking

ASSETS

Cash and investments 7,165,306$ 614,752$ 698,086$ Cash and investments with fiscal agents - - - Receivables:

Accounts 146,812 - - Intergovernmental 892,080 - - Other receivable 890,638 - -

Due from other funds 452,477 - -

Total assets 9,547,313$ 614,752$ 698,086$

LIABILITIES AND FUND BALANCES

Liabilities:Accounts payable and accrued liabilities 475,165$ -$ -$ Deposits payable 460,235 - - Due to other funds - - - Claims liabilities 460,000 - -

Total liabilities 1,395,400 - -

Fund balances:Nonspendable:

Endowments - 46,747 - Restricted reported in:

Special revenue funds - - Committed 2,898,615 - - Assigned reported in:

Special revenue funds - 568,005 698,086Unassigned (deficit), reported in:

General Fund 5,253,298 - -

Total fund balances 8,151,913 614,752 698,086

Total liabilities and fund balances 9,547,313$ 614,752$ 698,086$

Major Funds

The accompanying notes are an integral part of these basic financial statements.

Special Revenue Funds

20

NonmajorGovernmental

Ambulance Funds Totals

-$ 534,294$ 9,012,438$ 400,008 400,008

663,063 - 809,875 - 36,986 929,066 - - 890,638 - - 452,477

663,063$ 971,288$ 12,494,502$

86,259$ 1,465$ 562,889$ - - 460,235

452,477 - 452,477 - - 460,000

538,736 1,465 1,935,601

- - 46,747

- 566,992 566,992 - - 2,898,615

124,327 402,831 1,793,249

- - 5,253,298

124,327 969,823 10,558,901

663,063$ 971,288$ 12,494,502$

21

City of Carmel-by-the-Sea, CaliforniaReconciliation of the Governmental Funds Balance Sheet

to the Statement of Net Position

June 30, 2013

Total fund balances - total governmental funds 10,558,901$

37,285,185

Compensated absences (458,376)$ Long-term liabilities (13,844,747) Net OPEB obligation (1,115,277) (15,418,400)

(47,793)

Net position of governmental activities 32,377,893$

The accompanying notes are an integral part of these basic financial statements.

Amounts reported for governmental activities in the Statement of Net Position aredifferent because:

Long-term liabilities are not due and payable in the current period and,therefore, are not reported in the governmental funds balance sheet.

Capital assets used in governmental activities are not current financialresources and, therefore, are not reported in the governmental funds balancesheet.

Interest payable on long-term debt does not require the use of current financial resources and, therefore, is not reported in the governmental funds.

22

City of Carmel-by-the-Sea, CaliforniaReconciliation of Fund Basis Balance Sheet to Government-wide Statement of Net Position

Governmental Activities

June 30, 2013

Governmental Funds Changes Statement of

Balance Sheet Reclassifications in GAAP Net PositionASSETS

Current assets:Cash and investments 9,012,438$ -$ -$ 9,012,438$ Cash and investments with fiscal agents 400,008 400,008 Receivables:

Accounts receivable 809,875 - - 809,875 Intergovernmental receivable 929,066 - - 929,066 Other receivable 890,638 - - 890,638

Due from other funds 452,477 (452,477) - - Total current assets 12,494,502 (452,477) - 12,042,025

Noncurrent assets:Capital assets, net - - 37,285,185 37,285,185

Total noncurrent assets - - 37,285,185 37,285,185 Total assets 12,494,502$ (452,477)$ 37,285,185$ 49,327,210$

LIABILITIESCurrent liabilities:

Accounts payable and accrued liabilities 562,889$ -$ -$ 562,889$ Deposits payable 460,235 - - 460,235 Due to other funds 452,477 (452,477) - - Interest payable - - 47,793 47,793 Compensated absences - current - - 273,981 273,981 Due within one year 1,095,283 1,095,283

Total current liabilities 1,475,601 (452,477) 1,417,057 2,440,181 Noncurrent liabilities:

Long-term liabilities:Claims liabilities 460,000 - - 460,000 Compensated absences - - 184,395 184,395 Due after one year - 12,749,464 12,749,464 Net OPEB obligation - - 1,115,277 1,115,277 Total noncurrent liabilities 460,000 - 14,049,136 14,509,136 Total liabilities 1,935,601 (452,477) 15,466,193 16,949,317

FUND BALANCES/NET POSITIONFund balances:Nonspendable:

Endowments 46,747 (46,747) - - Restricted reported in:

Special revenue funds 566,992 (566,992) - - Assigned reported in:

Special revenue funds 1,793,249 (1,793,249) - - Capital projects funds - - - -

Unassigned (deficit), reported in:General Fund 5,253,298 (5,253,298) Special revenue funds - - - -

Net position:Net invested in capital assets - - 29,605,438 29,605,438 Restricted - - 566,992 566,992 Unrestricted - 10,558,901 (8,353,438) 2,205,463

Total fund balances/ net position 10,558,901 - 21,818,992 32,377,893 Total liabilities and net position 12,494,502$ (452,477)$ 37,285,185$ 49,327,210$

The accompanying notes are an integral part of these basic financial statements.

23

City of Carmel-by-the-Sea, CaliforniaStatement of Revenues, Expenditures, and Changes in Fund Balances

Governmental Funds

For the year ended June 30, 2013

General Harrison MemorialFund Library Parking

REVENUES:Taxes and assessments 12,505,034$ -$ -$ Licenses and permits 1,011,292 - - Fines and forfeitures 16,647 - - Intergovernmental 378,410 4,050 - Use of money and property 283,233 1,273 - Charges for services 88,200 18,098 - Contributions 3,884 350,901 - Other revenues 109,392 - -

Total revenues 14,396,092 374,322 -

EXPENDITURES:Current:

Administration 3,029,816 - - Building maintenance 2,263,763 - - Public safety 3,114,048 - - Public works 1,313,412 - - Forest, parks and beaches 466,021 - - Culture and recreation 673,022 1,227,965 - Economic development 304,587 - -

Capital outlay 651,785 - - Debt service:

Principal 410,434 - - Interest and fiscal charges 216,284 - -

Total expenditures 12,443,172 1,227,965 -

REVENUES OVER (UNDER)EXPENDITURES 1,952,920 (853,643) -

OTHER FINANCING SOURCES (USES):Proceeds from sales of assets 2,346 - - Transfers in 4,924,039 945,455 - Transfers out (5,986,953) - - Proceeds from bond issuance 6,280,000 - - Retirement of PERS side fund (6,280,000) - -

Total other financing sources (uses) (1,060,568) 945,455 -

Net change in fund balances 892,352 91,812 -

FUND BALANCES:Beginning of year 7,259,561 522,940 698,086

End of year 8,151,913$ 614,752$ 698,086$

Major Funds

The accompanying notes are an integral part of these basic financial statements.

Special Revenue Funds

24

OtherGovernmental

Ambulance Funds Totals

-$ -$ 12,505,034$ - 183,800 1,195,092 - 116,521 133,168 - 226,844 609,304

168 - 284,674 606,299 25,769 738,366

- - 354,785 - - 109,392

606,467 552,934 15,929,815

- - 3,029,816 - - 2,263,763

912,836 - 4,026,884 - 28,192 1,341,604 - - 466,021 - 17,209 1,918,196 - - 304,587 - - 651,785

- - 410,434 - 112,710 328,994

912,836 158,111 14,742,084

(306,369) 394,823 1,187,731

- - 2,346 310,748 121,747 6,301,989

- (315,036) (6,301,989) - - 6,280,000 - - (6,280,000)

310,748 (193,289) 2,346

4,379 201,534 1,190,077

119,948 768,289 9,368,824

124,327$ 969,823$ 10,558,901$

25

City of Carmel-by-the-Sea, CaliforniaReconciliation of Fund Basis Statements to Government-wide Statement of Activities

For the year ended June 30, 2013

Capital

Asset Government-

Fund Based Debt Compensated (Additions)/ OPEB wide

Functions/Programs Totals Service Absences Depreciation Retirements Obligation Adjustment Totals

Governmental activities:

Administration 3,029,816$ 6,280,000$ (79,995)$ 2,055$ -$ 248,871$ 388$ 9,481,135$

Infrastructure capitalization - - - - - - -

Building maintenance 2,263,763 - - 39,888 1,459,443 - 3,763,094

Public safety 4,026,884 - - 166,273 - - - 4,193,157

Public works 1,341,604 - - 554,701 - - - 1,896,305

Forest, parks and beaches 466,021 - - 6,102 - - - 472,123

Culture and recreation 1,918,196 - - 487,285 - - 2,405,481

Economic development 304,587 - - - - - 304,587

Capital outlay 651,785 (651,397) - (388) -

Debt service/Interest 739,428 (362,641) - - - - - 376,787

Total governmental activities 14,742,084$ 5,917,359$ (79,995)$ 1,256,304$ 808,046$ 248,871$ -$ 22,892,669$

The accompanying notes are an integral part of these basic financial statements.

26

City of Carmel-by-the-Sea, CaliforniaReconciliation of the Statement of Revenues, Expenditures, and Changes in

Fund Balances of Governmental Funds to the Statement of Activities

For the year ended June 30, 2013

Net change in fund balances - total governmental funds 1,190,077$

Capital asset purchases capitalized 651,397$ Capital asset retirements (1,459,443) Depreciation expense (1,256,304) (2,064,350)

410,434

Change in interest payable (47,793) Change in compensated absences 79,995 32,202

The issuance of long-term debt (e.g., bonds, leases) provides current financial resources to governmental funds, while the repayment of the principal of long-term debt consumes the current financial resources of governmental funds. Neither transaction, however, has any effect on net position. Also, governmental funds report the effect of issuance costs, premiums, discounts, and similar items when debt is first issued, whereas these amounts are deferred and amortized in the statement of activities. This amount is the net effect of these differences in the treatment of long-term debt and related items.

Bond issuance (6,280,000)

Net OPEB obligation (248,871)

Change in net position of governmental activities (6,960,508)$

Amounts reported for governmental activities in the Statement of Activities aredifferent because:

Governmental funds report capital outlays as expenditures whilegovernmental activities report depreciation expense to allocate thoseexpenditures over the life of the assets:

Some expenses reported in the Statement of Activities do not require theuse of current financial resources and, therefore, are not reported asexpenditures in governmental funds:

The accompanying notes are an integral part of these basic financial statements.

Certain employee benefit obligations are recorded on a pay-as-you-gobasis in the governmental funds, but are accrued as liabilities in the

Repayment of debt principal is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in the Statement of Net Position

27

City of Carmel-by-the-Sea, CaliforniaStatement of Revenues, Expenditures, and Changes in Fund Balances

Budget to Actual - General Fund and Major Special Revenue Funds

For the year ended June 30, 2013

PositiveOriginal Final Actual (Negative)

REVENUES:Taxes and assessments 11,373,698 11,484,861 12,505,034$ 1,020,173$ Licenses and permits 895,000 895,000 1,011,292 116,292 Fines and forfeitures 195,200 195,200 16,647 (178,553) Intergovernmental 86,700 158,715 378,410 219,695 Use of money and property 59,300 59,300 283,233 223,933 Charges for services 90,700 94,200 88,200 (6,000) Contributions - - 3,884 3,884 Other revenues 125,266 125,266 109,392 (15,874)

Total revenues 12,825,864 13,012,542 14,396,092 1,383,550

EXPENDITURES:Current:

Administration 3,118,986 3,087,145 3,029,816 57,329 Building maintenance 2,358,243 2,367,575 2,263,763 103,812 Public safety 3,368,141 3,139,902 3,114,048 25,854 Public works 1,205,221 1,169,912 1,313,412 (143,500) Forest, parks and beaches 518,567 535,636 466,021 69,615 Culture and recreation 722,670 711,756 673,022 38,734 Economic development 306,735 306,735 304,587 2,148

Capital outlay - - 651,785 (651,785) Debt service:

Principal 285,000 285,000 410,434 (125,434) Interest and fiscal charges 252,200 252,200 216,284 35,916

Total expenditures 12,135,763 11,855,861 12,443,172 (587,311)

REVENUES OVER (UNDER)EXPENDITURES 690,101 1,156,681 1,952,920 796,239

OTHER FINANCING SOURCES (USES):Proceeds from sales of assets - - 2,346 2,346 Transfers in 575,002 585,002 4,924,039 4,339,037 Transfers out - - (5,986,953) (5,986,953) Proceeds from bond issuance - 6,280,000 Retirement of PERS side fund - (6,280,000)

Total other financing sources (uses) 575,002 585,002 (1,060,568) (1,645,570)

Net change in fund balances 1,265,103 1,741,683 892,352 (849,331)

FUND BALANCES:Beginning of year 7,259,561 7,259,561 7,259,561 -

End of year 8,524,664$ 9,001,244$ 8,151,913$ (849,331)$

General Fund

The accompanying notes are an integral part of these basic financial statements.

Budgeted AmountsVariance w/Final

28

Positive PositiveOriginal Final Actual (Negative) Original Final Actual (Negative)

-$ -$ -$ -$ -$ -$ -$ -$ - - - - - - - - - - - - - - - - - - 4,050 4,050 - - - -

1,000 1,000 1,273 273 - - - - 19,000 19,000 18,098 (902) - - - -

300,200 300,200 350,901 50,701 - - - - - - - - - - - -

320,200 320,200 374,322 54,122 - - - -

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

1,309,176 1,276,828 1,227,965 48,863 - - - - - - - - - - - -

- - - - - - - - - - - - -

1,309,176 1,276,828 1,227,965 48,863 - - - -

(988,976) (956,628) (853,643) 102,985 - - - -

- - - - - - - - - - 945,455 945,455 - - - - - - - - - - - -

- - 945,455 945,455 - - - -

(988,976) (956,628) 91,812 1,048,440 - - - -

522,940 522,940 522,940 - 698,086 698,086 698,086 -

(466,036)$ (433,688)$ 614,752$ 1,048,440$ 698,086$ 698,086$ 698,086$ -$

(continued)

Harrison Memorial Library Parking

Budgeted Amounts Budgeted AmountsVariance w/Final Variance w/Final

29

City of Carmel-by-the-Sea, CaliforniaStatement of Revenues, Expenditures, and Changes in Fund Balances

Budget to Actual - General Fund and Major Special Revenue Funds, Continued

For the year ended June 30, 2013

PositiveOriginal Final Actual (Negative)

REVENUES:Taxes and assessments -$ -$ -$ -$ Licenses and permits - - - - Fines and forfeitures - - - - Intergovernmental - - - - Use of money and property - - 168 168 Charges for services 370,000 370,000 606,299 236,299 Contributions - - - - Other revenues - - - -

Total revenues 370,000 370,000 606,467 236,467

EXPENDITURES:Current:

Administration - - - - Building maintenance - - - - Public safety 803,179 782,576 912,836 (130,260) Public works - - - - Forest, parks and beaches - - - - Culture and recreation - - - - Economic development - - - -

Debt service:Principal - Interest and fiscal charges - - - -

Total expenditures 803,179 782,576 912,836 (130,260)

REVENUES OVER (UNDER)EXPENDITURES (433,179) (412,576) (306,369) 106,207

OTHER FINANCING SOURCES (USES):Proceeds from sales of assets - - - - Transfers in - - 310,748 310,748 Transfers out - - - -

Total other financing sources (uses) - - 310,748 310,748

Net change in fund balances (433,179) (412,576) 4,379 416,955

FUND BALANCES:Beginning of year 119,948 119,948 119,948 -

End of year (313,231)$ (292,628)$ 124,327$ 416,955$

(concluded)

Budgeted Amounts

AmbulanceVariance w/Final

The accompanying notes are an integral part of these basic financial statements.

30

31

NOTES TO BASIC FINANCIAL STATEMENTS

City of Carmel-by-the-Sea, California Basic Financial Statements For the year ended June 30, 2013 Index to Notes to Basic Financial Statements

32

Page Note 1 - Summary of Significant Accounting Policies .................................................................... 33

Financial Reporting Entity ............................................................................................................. 33 Basis of Presentation ...................................................................................................................... 35 Measurement Focus ....................................................................................................................... 37 Basis of Accounting ....................................................................................................................... 37 Assets, Liabilities, and Equity ....................................................................................................... 38 Revenues, Expenditures, and Expenses ......................................................................................... 43 Budgetary Accounting ................................................................................................................... 44

Note 2 – Cash and Investments ......................................................................................................... 45 Note 3 – Accounts Receivable ........................................................................................................... 48 Note 4 – Capital Assets ...................................................................................................................... 48 Note 5 – Accounts Payable and Accrued Liabilities ....................................................................... 49 Note 6 – Long-term Liabilities .......................................................................................................... 49 Note 7 – Net Position/ Fund Balances .............................................................................................. 52 Note 8 – Interfund Transactions ...................................................................................................... 54 Note 9 – Risk Management ............................................................................................................... 55 Note 10 – Public Employee’s Retirement System ........................................................................... 56

Plan Description ............................................................................................................................. 56 Funding Policy ............................................................................................................................... 56

Note 11 – Other Post-Employment Benefits .................................................................................... 56 Note 12 – Commitments and Contingencies .................................................................................... 59 Note 13 – New Accounting Pronouncements ................................................................................... 59

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements For the year ended June 30, 2013

33

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The City of Carmel-by-the-Sea (City) was incorporated on November, 1956, under the laws and regulations of the State of California (State). The City operates under a City Council/Manager form of government and provides the following services: public works, planning and building, general administrative services, public safety (County Sheriff), fire suppression and prevention services, and sewage treatment services. The financial statements of the City have been prepared in accordance with accounting principles generally accepted in the United States of America (GAAP) as applied to governmental units. The Governmental Accounting Standards Board (GASB) is the standard-setting body for governmental accounting and financial reporting. On June 15, 1987, GASB issued a codification of the existing Governmental Accounting and Financial Reporting Standards which, along with subsequent GASB pronouncements (Statements and Interpretations), constitutes GAAP for governmental units. The City applies all GASB pronouncements to its activities. In addition, the City applies all Financial Accounting Standards Board (FASB) Statements and Interpretations, Accounting Principles Board (APB) Opinions, and Accounting Research Bulletins (ARB) issued after November 30, 1989, unless they conflict with or contradict GASB pronouncements. The more significant of these accounting policies are described below and, where appropriate, subsequent pronouncements will be referenced. Financial Reporting Entity The City operates as a self-governing local government unit within the State. It has limited authority to levy taxes and has the authority to determine user fees for the services that it provides. The City’s main funding sources include sales taxes, other intergovernmental revenue from state and federal sources, user fees, and federal and state financial assistance. All property taxes are paid to San Mateo County (County) as part of the revenue neutrality payment obligation. The financial statements do not reflect the amounts received on behalf of the City and retained by the County. The financial reporting entity consists of (a) the primary government, the City, (b) organizations for which the primary government is financially accountable, and (c) other organizations for which the primary government is not accountable, but for which the nature and significance of their relationship with the primary government are such that exclusion would cause the reporting entity’s financial statements to be misleading or incomplete. Financial accountability is defined as the appointment of a voting majority of the component unit’s board, and either (a) the City has the ability to impose its will on the organization, or (b) there is a potential for the organization to provide a financial benefit to or impose a financial burden on the City.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

34

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Financial Reporting Entity, Continued As required by GAAP, these financial statements present the government and its component units, entities for which the government is considered to be financially accountable. These component units are reported on a blended basis. Blended component units, although legally separate entities, are, in substance, part of the government’s operations and so data from these units are combined with data of the primary government. The financial statements of the individual component units, if applicable as indicated below, may be obtained by writing to the City of Carmel-by-the-Sea, Finance Department, Post Office Box CC, Carmel-by-the-Sea, CA 93921. The City’s reporting entity includes the following blended component units:

Carmel Public Improvement Authority Harrison Memorial Library

The above component units are included in the City’s basic financial statements using the blended method. There are no component units of the City that meet the criteria for discrete presentation.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

35

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Basis of Presentation Government-Wide Financial Statements The statement of Net Position and statement of activities display information about the reporting government as a whole. They include all funds of the reporting entity except for fiduciary funds. The statements distinguish between governmental and business-type activities. Governmental activities generally are financed through taxes, intergovernmental revenues, and other nonexchange revenues. Amounts reported as program revenues include 1) charges to customers or applicants for goods, services, or privileges provided by a given function or segment, 2) operating grants and contributions, and 3) capital grants and contributions restricted to the operating or capital requirements of a specific function or segment. All taxes and internally dedicated resources are reported as general revenues rather than program revenues. Fund Financial Statements Fund financial statements of the reporting entity are organized into funds, each of which is considered to be a separate accounting entity. Each fund is accounted for by providing a separate set of self-balancing accounts, which constitute its assets, liabilities, fund equity, revenues, and expenditures/expenses. Funds are organized into three major categories: governmental, proprietary, and fiduciary. An emphasis is placed on major funds within the governmental and proprietary categories. A fund is considered major if it is the primary operating fund of the City or meets the following criteria:

a. Total assets, liabilities, revenues, or expenditures/expenses of that individual governmental fund are at least ten percent of the corresponding total for all funds of that category or type; and,

b. Total assets, liabilities, revenues, or expenditures/expenses of the individual

governmental fund are at least five percent of the corresponding total for all governmental funds combined.

The City reports the following major funds:

General Fund Harrison Memorial Library Special Revenue Fund Parking Special Revenue Fund Ambulance Special Revenue Fund

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

36

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Basis of Presentation, Continued Descriptions of these funds are included on the divider page preceding the Governmental Funds Balance Sheet. The funds of the financial reporting entity are described below: Governmental Funds General Fund The General Fund is used to account for resources traditionally associated with the City which are not required legally or by sound financial management to be accounted for in another fund. From this fund are paid the City’s general operating expenditures, the fixed charges, and the capital costs that are not paid through other funds. Special Revenue Funds The Special Revenue Funds are used to account for specific revenues that are legally or otherwise restricted to expenditures for particular purposes. Debt Service Fund The Debt Service Fund is used to account for financial resources used for the repayment of debt.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

37

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Measurement Focus Measurement focus is a term used to describe which transactions are recorded within the various financial statements. On the government-wide Statement of Net Position and the Statement of Activities, governmental and business-type activities are presented using the economic resources measurement focus. The accounting objectives of this measurement focus are the determination of net income, financial position, and cash flows. All assets and liabilities (whether current or noncurrent) associated with their activities are reported. Fund equity is classified as net position, which serves as an indicator of financial position. In the fund financial statements, the “current financial resources” measurement focus is used for governmental funds. Only current financial assets and liabilities are generally included on their balance sheets. Their operating statements present sources and uses of available spendable financial resources during a given period. These funds use fund balance as their measure of available spendable financial resources at the end of the period. Basis of Accounting

In the government-wide Statement of Net Position and Statement of Activities, governmental and business-type activities are presented using the accrual basis of accounting. Under the accrual basis of accounting, revenues are recognized when earned and expenses are recorded when the liability is incurred or economic asset used. Revenues, expenses, gains, losses, assets, and liabilities resulting from exchange and exchange-like transactions are recognized when the exchange takes place. In the fund financial statements, governmental funds are presented on the modified accrual basis of accounting. Under this modified accrual basis of accounting, revenues are recognized when “measurable and available.” Measurable means knowing or being able to reasonably estimate the amount. Available means the amount is collectible within the current period or soon enough thereafter to pay current liabilities. The City considers all revenues reported in the governmental funds to be available if the revenues are collected within 60 days after year end, with the exception of grant revenues and ambulance billing revenues. Grant revenues and ambulance billing revenues are considered to be available if collected within 180 days of the end of the current fiscal period.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

38

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Basis of Accounting, Continued Property taxes, transient occupancy taxes, franchise taxes, licenses, and interest associated with the current fiscal period are all considered to be susceptible to accrual and so have been recognized as revenues of the current fiscal year. All other revenue items are considered to be measurable and available only when cash is received by the government. Expenditures (including capital outlay) are recorded when the related fund liability is incurred. Assets, Liabilities, and Equity Cash Deposits and Investments The City’s cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition. The City pools cash and investments from all funds for the purpose of increasing income through investment activities. Highly liquid money market investments with maturities of one year or less at time of purchase are stated at amortized cost. All other investments are stated at fair value in accordance with GASB Statement No. 31, Accounting and Financial Reporting for Certain Investments and for External Investment Pools. Market value is used as fair value for those securities for which market quotations are readily available. Interfund Receivables and Payables During the course of operations, numerous transactions occur between individual funds that may result in amounts owed between funds. Those related to goods and services type transactions are classified as “due to and from other funds.” Long-term interfund loans (noncurrent portion) are reported as “advances from and to other funds.” Interfund receivables and payables between funds within governmental activities are eliminated in the Statement of Net Position. See Note 9 for details of interfund transactions, including receivables and payables at year-end.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

39

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Assets, Liabilities, and Equity, Continued Receivables In the government-wide statements, receivables consist of all revenues earned at year-end and not yet received. Major receivable balances for the governmental activities include property taxes, sales and use taxes, utility user taxes, intergovernmental subventions, interest earnings, and expense reimbursements. In the fund financial statements, material receivables in governmental funds include revenue accruals such as property tax, sales tax, utility user tax, and intergovernmental subventions since they are usually both measurable and available. Non-exchange transactions collectible but not available, such as property tax, are deferred in the fund financial statements in accordance with the modified accrual basis, but not deferred in the government-wide financial statements in accordance with the accrual basis. Interest and investment earnings are recorded when earned only if paid within 60 days since they would be considered both measurable and available. The loans receivable are recorded in the fund statements, but are deferred to indicate they do not represent current financial resources. The loans are recognized when advanced in the government-wide statements. The City’s experience is that all accounts receivable are collectible; therefore an allowance for doubtful accounts is unnecessary. Prepaid Items Certain payments to vendors reflect costs applicable to future accounting periods and are recorded as prepaid items in both government-wide and fund financial statements. In the governmental fund financial statements, prepaid items are offset with a reservation of fund balance for long-term assets to indicate they do not constitute current resources available for appropriation. Capital Assets The City's assets are capitalized at historical cost or estimated historical cost, if actual is unavailable, except for donated Capital Assets which are recorded at their estimated fair value at the date of donation. Policy has set the capitalization threshold for reporting at $5,000 for non-infrastructure capital assets and $25,000 for infrastructure capital assets.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

40

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Assets, Liabilities, and Equity, Continued Capital Assets, Continued Government-Wide Statements Public domain (infrastructure) capital assets include roads, bridges, curbs and gutters, streets, sidewalks, drainage systems, and lighting systems. The accounting treatment of property, plant and equipment (capital assets) depends on whether the assets are used in governmental fund operations or proprietary fund operations and whether they are reported in the government-wide or fund financial statements. Prior to July 1, 2003, governmental funds’ infrastructure assets were not capitalized, since then these assets have been valued at estimated historical cost. Depreciation of all exhaustible capital assets is recorded as an allocated expense in the Statement of Activities, with accumulated depreciation reflected in the Statement of Net Position. Depreciation is provided over the assets’ estimated useful lives using the straight-line method of depreciation. No depreciation is recorded in the year of acquisition or in the year of disposition. The range of estimated useful lives by type of asset is as follows:

Buildings and improvements 20 – 50 years Sewer Lines 30 years Machinery and equipment 5 - 20 years Computer Software 10 years

Fund Financial Statements In the fund financial statements, capital assets used in governmental fund operations are accounted for as capital outlay expenditures of the governmental fund upon acquisition. Capital assets used in proprietary fund operations are accounted for the same way as in the government-wide statements.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

41

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Assets, Liabilities, and Equity, Continued Compensated Absences Employees accrue vacation, sick, holiday, and compensatory time off benefits. City employees have vested interests in the amount of accrued time off, with the exception of sick time, and are paid on termination. Also, annually an employee may elect to be compensated for up to 40 hours of unused annual leave. However, this is contingent upon the employee using at least 40 hours during the previous year and, the employee having a minimum balance of 80 annual leave hours after the payment. All vacation pay is accrued when incurred in the government-wide and proprietary financial statements. A liability for these amounts is reported in the governmental funds only if they have matured, for example, as a result of employee resignations or retirements and is currently payable. The City had no employee resignations or retirements for which compensated absences should be accrued in governmental funds at year-end. The general fund is typically used to liquidate compensated absences. Equity Classification Government-Wide Statements Equity is classified as net position and is displayed in three components:

a. Net invested in capital assets – consists of capital assets, including restricted capital assets, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowings that are attributable to the acquisition, construction, or improvement of those assets.

b. Restricted net position – consists of net position with constraints placed on the use by

external groups such as creditors, grantors, contributors, or by laws or regulations of other governments or law through constitutional provisions or enabling legislation.

c. Unrestricted net position – all other net position that do not meet the definition of

“restricted” or “net invested in capital assets”.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

42

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Equity Classification, Continued Fund Financial Statements Governmental fund equity is classified as fund balance. Fund balance is classified as nonspendable, restricted, committed, assigned, or unassigned. Proprietary fund equity is classified the same as in the government-wide statements. The classifications for governmental funds are defined as follows for the City: Nonspendable Fund Balance –

Assets that will never convert to cash (prepaid items, inventory). Assets that will not convert to cash soon enough to affect the current period (long-term notes or

loans receivable). Resources that must be maintained intact pursuant to legal or contractual requirements (the

principal of an endowment). Restricted Fund Balance –

Resources that are subject to externally enforceable legal restrictions imposed by parties altogether outside the government (creditors, grantors, contributors and other governments).

Resources that are subject to limitations imposed by law through constitutional provisions or enabling legislation (e.g., Gas Tax).

Committed Fund Balance –

Self imposed limitations set in place prior to the end of the period (encumbrances, economic contingencies and uncertainties).

Limitation at the highest level of decision-making (Council) that requires formal action at the same level to remove.

Assigned Fund Balance –

Amounts in excess of nonspendable, restricted, and committed fund balance in funds other than the general fund automatically are reported as assigned fund balance.

Unassigned Fund Balance –

Residual net resources. Total fund balance in the general fund in excess of nonspendable, restricted, committed and

assigned fund balance (surplus). Excess of nonspendable, restricted, and committed fund balance over total fund balance

(deficit).

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

43

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES, Continued Revenues, Expenditures, and Expenses Property Tax The County of Monterey (County) is responsible for the collection and allocation of property taxes. Under California law, property taxes are assessed and collected by the County up to 1% of the full cash value of taxable property, plus other increases approved by the voters and distributed in accordance with statutory formulas. The City recognizes property taxes when the individual installments are due, provided they are collected within 60 days after year-end. Secured property taxes are levied on or before the first day of September of each year. They become a lien on real property on March 1 preceding the fiscal year for which taxes are levied. These taxes are paid in two equal installments; the first is due November 1 and delinquent with penalties after December 10; the second is due February 1 and delinquent with penalties after April 10. Secured property taxes, which are delinquent and unpaid as of June 30, are declared to be tax defaulted and are subject to redemption penalties, cost, and interest when paid. If the delinquent taxes are not paid at the end of five years, the property is sold at public auction and the proceeds are used to pay the delinquent amounts due. Any excess is remitted, if claimed, to the taxpayer. Additional tax liens are created when there is a change in ownership of property or upon completion of new construction. Tax bills for these new tax liens are issued throughout the fiscal year and contain various payments and delinquent dates, but are generally due within one year. If the new tax liens are lower, the taxpayer receives a tax refund rather than a tax bill. Unsecured personal property taxes are not a lien against real property. These taxes are due on March 1, and become delinquent, if unpaid on August 31. The City participates in an alternative method of distribution of property tax levies and assessments known as the “Teeter Plan.” The State Revenue and Taxation Code allow counties to distribute secured real property, assessment, and supplemental property taxes on an accrual basis resulting in full payment to cities each fiscal year. Any subsequent delinquent payments and penalties and interest during a fiscal year will revert to Monterey County.

City of Carmel-by-the-Sea, California Notes to Basic Financial Statements, Continued For the year ended June 30, 2013

44