city of missoula, montana audit exit conference year ended june 30, 2009 presented january 20, 2010

TRANSCRIPT

CITY OF MISSOULA, MONTANA

Audit Exit ConferenceYear Ended June 30, 2009Presented January 20, 2010

Presentation Outline

• Acknowledgements• Scope of Audit• Summary of Audit Results• Financial Statement Highlights• Internal Controls and Compliance• Management Comments• Audit Committee Communications• Component Units• Looking Forward

Audit Scope

• U.S. Generally Accepted Auditing Standards• Government Auditing Standards• Single Audit Act/OMB Circular A-133• All City Funds• Component Units – Missoula Parking Commission– Missoula Redevelopment Agency– Business Improvement District

Summary of Audit Results

• Clean opinion on financial statements

• Two internal control findings considered to be material weaknesses over financial reporting

• No internal control or compliance findings related to major federal programs

Financial Statement Highlights

• Government-Wide Net Assets• Governmental Funds Fund Balances• Revenues• Expenses• Mill Levies• Taxable Values• Debt Margin

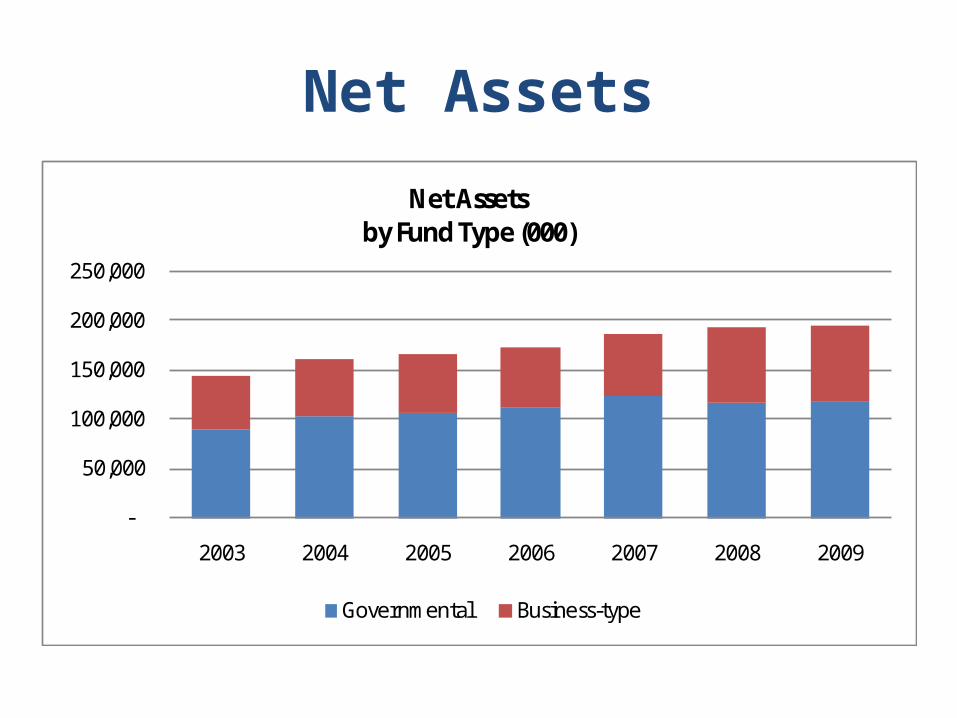

Net Assets

-

50,000

100,000

150,000

200,000

250,000

2003 2004 2005 2006 2007 2008 2009

Net Assetsby Fund Type (000)

Governmental Business-type

Net Assets

-

50,000

100,000

150,000

200,000

250,000

2003 2004 2005 2006 2007 2008 2009

Net Assets by Category (000)

Investment in Fixed Assets Restricted Unrestricted

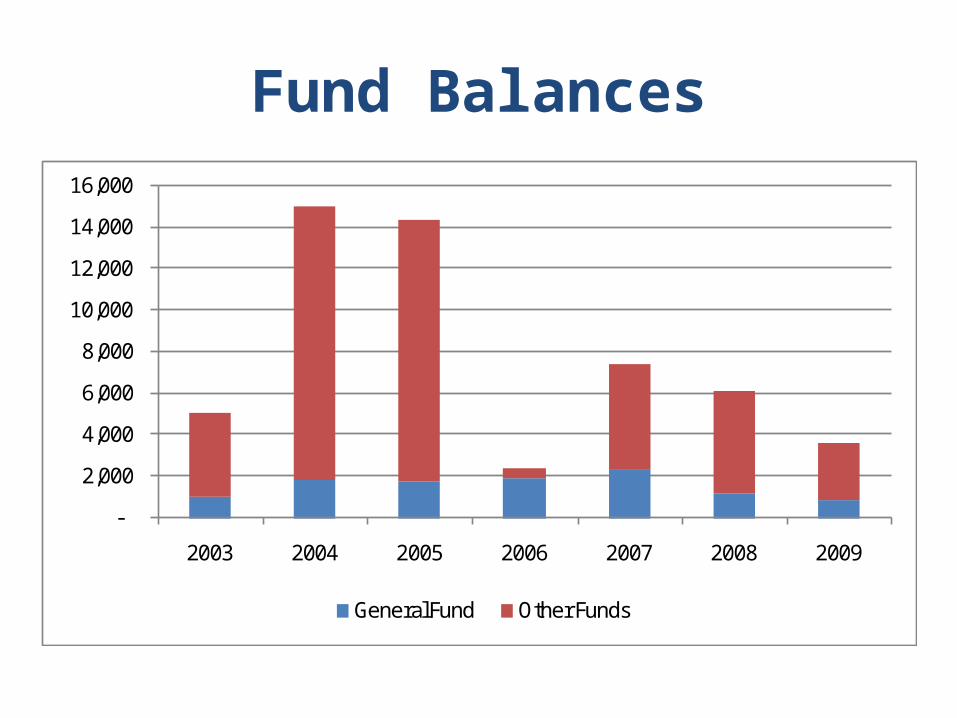

Fund Balances

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2003 2004 2005 2006 2007 2008 2009

General Fund Other Funds

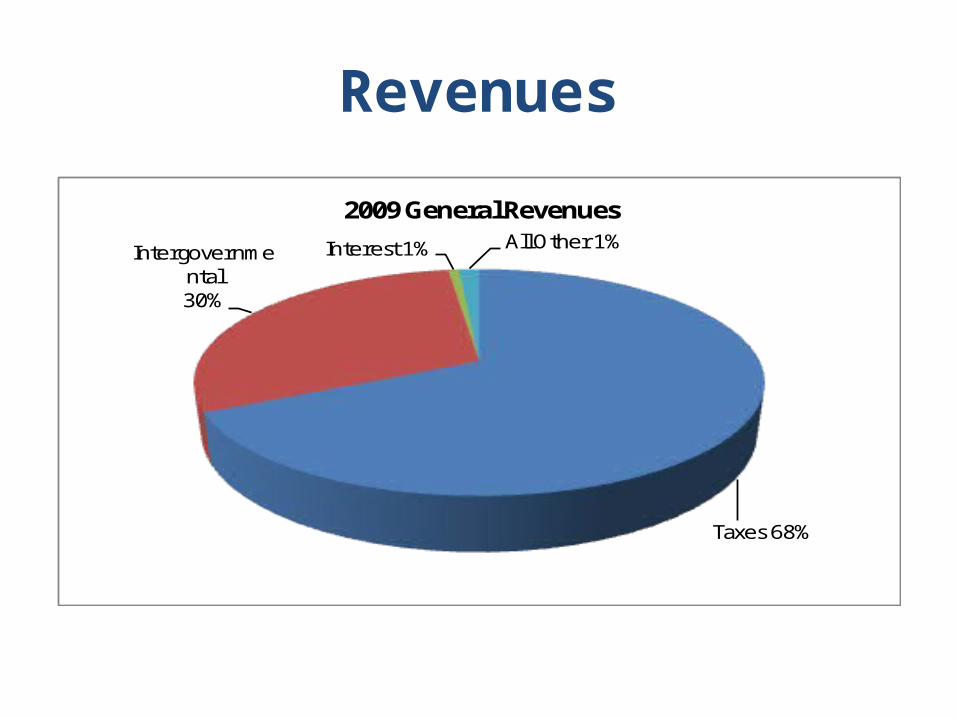

Revenues

-5,000

10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

2003 2004 2005 2006 2007 2008 2009

General Revenues by Source (000)

Taxes Intergovernmental Interest Annexation/Devel Contribs All Other

Revenues

Taxes 68%

Intergovernmental 30%

Interest 1% All Other 1%

2009 General Revenues

Revenues

-

5,000

10,000

15,000

20,000

2003 2004 2005 2006 2007 2008 2009

Program Revenues (000)

Charges for Services Operating Grants Capital Grants

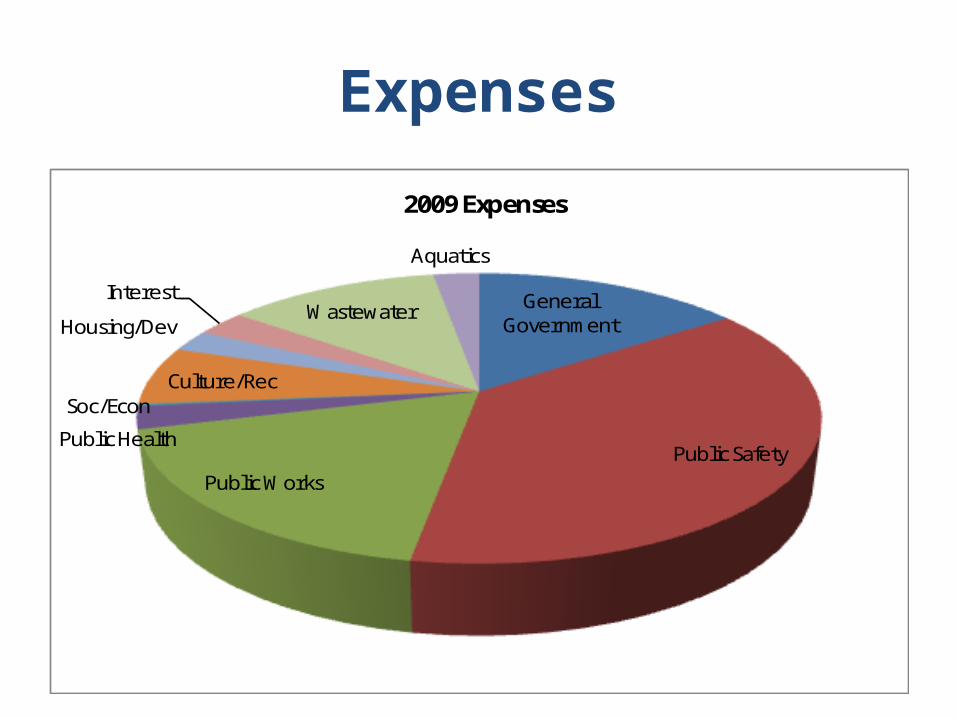

Expenses

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2003 2004 2005 2006 2007 2008 2009

Expenses (000)

Gen Gov't Safety Works Health Soc/Econ Culture/Rec

Housing/Dev Interest Other Wastewater Aquatics

Expenses

General Government

Public SafetyPublic Works

Public Health

Soc/EconCulture/Rec

Housing/Dev

InterestWastewater

Aquatics

2009 Expenses

Mill Levies

-

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

2003 2004 2005 2006 2007 2008 2009

Tax Levies

City County Schools State Urban Trans

Taxable Values

-

20,000

40,000

60,000

80,000

100,000

120,000

2003 2004 2005 2006 2007 2008 2009

Taxable Values (000)

City w/o Increment Tax Increment

Debt Margin

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2003 2004 2005 2006 2007 2008 2009

Debt Margin (000)

Other Post-Employment Benefits

• Accounting and disclosure requirements implemented in 2009 (see Note G-3)

• Relates to health benefits provided to retirees and the implied premium subsidy

• Net OPEB obligation was $499,000 for 2009• Actuarial valuation of unfunded OPEB liability

is $5.4 million

Internal Controls & Compliance

• Financial Statement Level– Two material weakness findings related to taxes

receivable and capital assets– No material noncompliance

• Major Programs– No significant deficiencies or material weaknesses– No material noncompliance

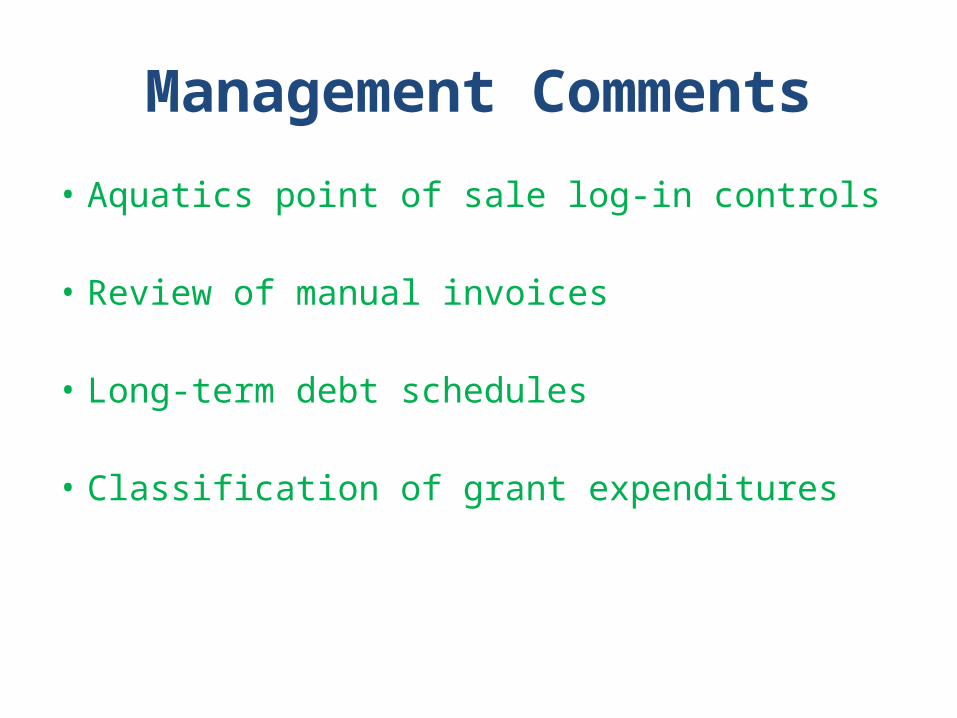

Management Comments

• Aquatics point of sale log-in controls

• Review of manual invoices

• Long-term debt schedules

• Classification of grant expenditures

Governance Communications

• Auditor Responsibilities• Planned Scope and Timing• Accounting Policies• Significant Audit Findings• Difficulties in Performing the Audit• Corrected and Uncorrected Misstatements• Other Information in the CAFR• Disagreements with Management• Management Representations• Consultations with Other Accountants

Component Units

• Missoula Redevelopment Agency– Clean opinion on financial statements– No internal control or compliance findings

• Missoula Parking Commission– Clean opinion on financial statements– No internal control or compliance findings

Component Units

• Business Improvement District– Included in CAFR as a discretely-presented

component unit– No separate report issued– No material internal control or compliance

findings – Prior year management letter comments were

implemented

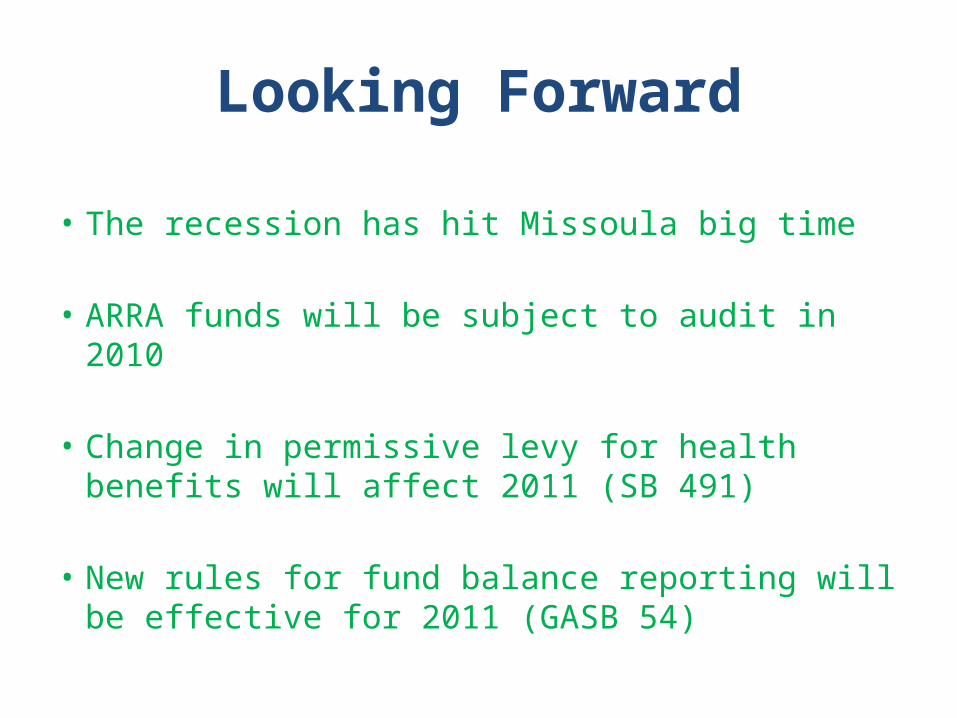

Looking Forward

• The recession has hit Missoula big time

• ARRA funds will be subject to audit in 2010

• Change in permissive levy for health benefits will affect 2011 (SB 491)

• New rules for fund balance reporting will be effective for 2011 (GASB 54)

QUESTIONS?