city of san buenaventura, california162.243.137.184/.../06/san-buenaventura-2017-tda-3... ·...

TRANSCRIPT

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3, Section 99234 Public Utilities Code

Financial Statements

Fiscal Years Ended June 30, 2017 and 2016

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3, Section 99234 Public Utilities Code

Fiscal Years Ended June 30, 2017 and 2016

TABLE OF CONTENTS

Page Independent Auditor’s Report 1 Financial Statements: Comparative Balance Sheet 4 Comparative Statement of Revenues, Expenditures and Changes in Fund Balance

5

Notes to Financial Statements General Information Summary of Significant Accounting Policies Cash and Investments Restrictions Contingencies Budgetary Data

6 6 8 8 9 9

Supplemental Data: Schedule of Revenues, Expenditures and Changes in Fund Balance – 2017 Budget and Actual Schedule of Revenues, Expenditures and Changes in Fund Balance – 2016 Budget and Actual

11

12 Schedule of Status of Funds by Project 13 Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards

14

__________________________________________________________________________________________________________________________________________________________________________________

23702 Birtcher Drive, Lake Forest, CA 92630 ■ T: (949) 552-7700 ■ www.conradllp.com

1

Board of Commissioners Ventura County Transportation Commission Ventura, California

INDEPENDENT AUDITOR’S REPORT We have audited the accompanying financial statements of the Transportation Development Act (“TDA”) Article 3 funds (“TDA Fund”) of the City of San Buenaventura, California (“City”), as of and for the fiscal years ended June 30, 2017 and 2016, and the related notes to the financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

Board of Commissioners Ventura County Transportation Commission Ventura, California

2

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Emphasis of Matters As discussed in Note 1, the financial statements present only the TDA Fund of the City and do not purport to, and do not present fairly, the financial position of the City as of June 30, 2017 and 2016, the changes in its financial position, or, where applicable, its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America. Our opinion is not modified with respect to this matter.

Opinion In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the TDA Fund of the City, as of June 30, 2017 and 2016, and the change in financial position of the TDA Fund of the City for the fiscal year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters Our audit was conducted for the purpose of forming opinions on financial statements of the TDA Fund of the City. The Schedule of Revenues, Expenditures and Changes in Fund Balances – Budget and Actual and the Schedule of Status of Funds by Project, listed as supplemental data in the table of contents, are presented for purposes of additional analysis and are not a required part of the financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements for the TDA Fund of the City. This supplemental data has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the information is fairly stated in all material respects in relation to the financial statements as a whole.

Board of Commissioners Ventura County Transportation Commission Ventura, California

3

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued a report dated November 20, 2017 on our consideration of the City’s internal control over financial reporting for the TDA Fund, and our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance, and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering City’s internal control over financial reporting and compliance.

Lake Forest, California November 20, 2017

2017 2016

Cash and investments (Note 3) 306,478$ 394,355$

Total assets 306,478$ 394,355$

Accounts payable -$ 40,191$

Total liabilities - 40,191

Fund balance - restricted 306,478 354,164

Total liabilities and fund balance 306,478$ 394,355$

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund

Article 3, Section 99234 Public Utilities Code

Assets

Liabilities and fund balance

Comparative Balance Sheet

June 30, 2017 and 2016

See accompanying notes to financial statements

4

2017 2016

Revenues:

Local transportation allocation Article 3 64,803$ 68,176$

Interest income 5,289 5,176

Total revenues 70,092 73,352

Expenditures:

Construction, maintenance, and engineering 117,778 75,251

Total expenditures 117,778 75,251

Net changes in fund balances (47,686) (1,899)

Fund balance at beginning of year 354,164 356,063

Fund balance at end of year 306,478$ 354,164$

and Changes in Fund Balance

Fiscal Years Ended June 30, 2017 and 2016

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund

Article 3, Section 99234 Public Utilities Code

Comparative Statement of Revenues, Expenditures

See accompanying notes to financial statements

5

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3, Section 99234 Public Utilities Code

Notes to Financial Statements

Fiscal Years Ended June 30, 2017 and 2016

6

(1) General Information

The financial statements are intended to reflect the financial position and changes in financial position for the Transportation Development Act Local Transportation Fund pursuant to Article 3 (“TDA Fund”) of the City of San Buenaventura, California (“City”) only. Pursuant to Section 99234 of the California Public Utilities Code, Article 3 monies may be used only for facilities provided for the exclusive use of pedestrians and bicycles, including the construction and related engineering expenses of those facilities, the maintenance of bicycle trails (which are closed to motorized traffic), and bicycle safety education programs. Facilities that provide for the use of bicycles may include projects that serve the needs of commuting bicyclists, including, but not limited to, new trails serving major transportation corridors, secure bicycle parking at employment centers, park and ride lots, and transit terminals where other funds are unavailable. Funding for this program was authorized by the Ventura County Transportation Commission (“VCTC”).

(2) Summary of Significant Accounting Policies

Fund Accounting The accounts of the City are organized on the basis of funds and account groups. A fund is defined as an independent fiscal and accounting entity wherein operations of each fund are accounted for in a separate set of self-balancing accounts that record resources, related liabilities, obligations, reserves, and equity segregated for the purpose of carrying out specific activities or attaining certain objectives in accordance with special regulations, restrictions, or limitations. The City accounts for the activity of the Article 3 funds in its TDA Fund, which is a Special Revenue Fund. Measurement Focus and Basis of Accounting Special Revenue Funds are accounted for using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collected within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, revenues are available if they are collected within 60 days of the end of the fiscal period. Expenditures generally are recorded when a liability is incurred.

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3. Section 99234 Public Utilities Code

Notes to Financial Statements

Fiscal Years Ended June 30, 2017 and 2016

7

(2) Summary of Significant Accounting Policies (Continued) Revenue Recognition Recognition of revenues arising from nonexchange transactions, which include revenues from taxes, certain grants, and contributions, is based on the primary characteristic from which the revenues are received by the City. For the City, funds received under TDA Article 3 possess the characteristic of a voluntary nonexchange transaction similar to a grant. Revenues under TDA Article 3 are recognized in the period when all eligibility requirements have been met. A deferred inflow of resources arises when potential revenues do not meet both the measurable and availability criteria for recognition in the current period. Deferred inflows of resources also arise when the City receives resources before it has a legal claim to them, as when grant monies are received prior to the incurrence of qualified expenditures. In subsequent periods, when both revenue recognition criteria are met, or when the City has a legal claim to the resources, the liability for deferred inflow of resources is removed from the balance sheet, and revenue is recognized. Fund Equity The components of the fund balances of governmental funds reflect the component classifications described below.

• Nonspendable Fund Balance – this includes amounts that cannot be spent because they are either (a) not in spendable form, or (b) legally or contractually required to be maintained intact.

• Restricted Fund Balance – this includes amounts that can be spent only for specific purposes stipulated by constitution, external resource providers, or through enabling legislation.

• Committed Fund Balance – includes amounts that can be used only for the specific purposes determined by a formal action of the City Council.

▪ Assigned Fund Balance – includes amounts that are intended to be used by the City for

specific purposes, but do not meet the criteria to be classified as restricted or committed.

▪ Unassigned Fund Balance – includes any deficit fund balance resulting from overspending for specific purposes for which amounts had been restricted, committed, or assigned.

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3, Section 99234 Public Utilities Code

Notes to Financial Statements

Fiscal Years Ended June 30, 2017 and 2016

8

(2) Summary of Significant Accounting Policies (Continued) It is the City’s policy that restricted resources will be applied first, followed by (in order of application) committed, assigned, and unassigned resources, in the absence of a formal policy adopted by the City Council. Use of Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect certain amounts and disclosures. Accordingly, actual results could differ from those estimates.

(3) Cash and Investments

The City has pooled its cash and investments in order to achieve a higher return on investments while facilitating management of cash. The balance in the pool account is available to meet current operating requirements. Cash in excess of current requirements is invested in various interest-bearing accounts and other investments for varying terms. The TDA Fund’s cash and investments as of June 30, 2017 and 2016 were $306,478 and $394,355, respectively. The TDA Fund’s cash is deposited in the City’s internal investment pool, which is reported at fair value. Interest income is allocated on the basis of average cash balances. Investment policies and associated risk factors applicable to the TDA Fund are those of the City and are included in the City’s basic financial statements. See the City’s basic financial statements for disclosures related to cash and investments including those disclosures relating to interest rate risk, credit rate risk, custodial credit risk, and concentration risk.

(4) Restrictions

Funds received pursuant to the California Public Utilities Code §99234 (TDA Article 3) may only be used for facilities provided for exclusive use by bicycle and pedestrian facilities or bicycle safety education programs.

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund Article 3. Section 99234 Public Utilities Code

Notes to Financial Statements

Fiscal Years Ended June 30, 2017 and 2016

9

(5) Contingencies See the City’s basic financial statements for disclosures related to contingencies including those relating to various legal actions, administrative proceedings, or claims in the ordinary course of operations.

(6) Budgetary Data

The City adopts an annual budget on a basis consistent with accounting principles generally accepted in the United States of America and utilizes an encumbrance system as a management control technique to assist in controlling expenditures and enforcing revenue provisions. Under this system, the current year expenditures are charged against appropriations. Accordingly, actual revenues and expenditures can be compared with related budget amounts without any significant reconciling items.

10

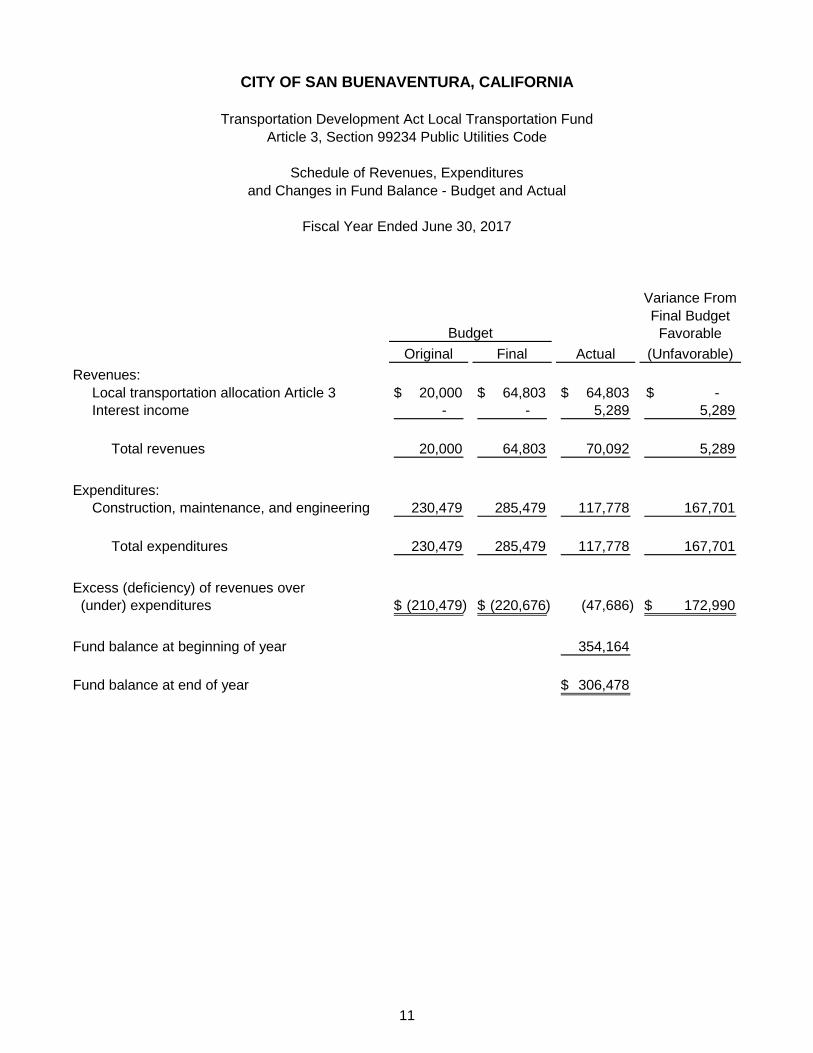

Supplemental Data

Variance From

Final Budget

Favorable

Original Final Actual (Unfavorable)

Revenues:

Local transportation allocation Article 3 20,000$ 64,803$ 64,803$ -$

Interest income - - 5,289 5,289

Total revenues 20,000 64,803 70,092 5,289

Expenditures:

Construction, maintenance, and engineering 230,479 285,479 117,778 167,701

Total expenditures 230,479 285,479 117,778 167,701

Excess (deficiency) of revenues over

(under) expenditures (210,479)$ (220,676)$ (47,686) 172,990$

Fund balance at beginning of year 354,164

Fund balance at end of year 306,478$

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund

Article 3, Section 99234 Public Utilities Code

Schedule of Revenues, Expenditures

Budget

and Changes in Fund Balance - Budget and Actual

Fiscal Year Ended June 30, 2017

11

Variance From

Final Budget

Favorable

Original Final Actual (Unfavorable)

Revenues:

Local transportation allocation Article 3 20,000$ 68,176$ 68,176$ -$

Interest income - - 5,176 5,176

Total revenues 20,000 68,176 73,352 5,176

Expenditures:

Construction, maintenance, and engineering 147,910 268,827 75,251 193,576

Total expenditures 147,910 268,827 75,251 193,576

Excess (deficiency) of revenues over

(under) expenditures (127,910)$ (200,651)$ (1,899) 198,752$

Fund balance at beginning of year 356,063

Fund balance at end of year 354,164$

Budget

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation Fund

Article 3, Section 99234 Public Utilities Code

Schedule of Revenues, Expenditures

and Changes in Fund Balance - Budget and Actual

Fiscal Year Ended June 30, 2016

12

ProgramYear

LTF Allocations

Required Local Match

Approved Transfer/ Accrued Interest Applied Note

LTF Allocations and

Local Match

Current Year LTF

Expenditures

Current Year Local Match Expenditures

Prior Years LTF

Expenditures

Prior Years Local Match Expenditures

Unexpended LTF

Allocations and City Match (2) Note

ProgramStatus

Access Ramps 2009-10 55,000$ 55,000$ 384$ (1) 110,384$ -$ -$ 55,383$ 55,000$ 1$ (3) ClosedBike Education Program 2011-12 40,000 40,000 885 (1) 80,885 441 441 4,765 4,765 70,473 OpenBicycle Path Maintenance- Class I 2012-13 21,591 - - 21,591 - - 21,591 - - ClosedFive Point Intersection Improvements 2012-13 100,000 100,000 1,560 (1) 201,560 3,300 3,300 44,729 44,729 105,502 OpenBicycle Path Maintenance- Class I 2013-14 20,723 - - 20,723 - - 20,723 - - ClosedSeaward Bike Safety Funds 2014-15 50,000 50,000 - 100,000 43,255 43,256 6,745 6,744 - OpenBicycle Path Maintenance- Class I 2014-15 13,411 - - 13,411 6,334 - 7,077 - - OpenBicycle Path Maintenance- Class I 2015-16 68,176 - - 68,176 17,451 - - - 50,725 OpenBicycle Path Maintenance- Class I 2016-17 64,803 - - 64,803 - - - - 64,803 Open

433,704$ 245,000$ 2,829$ 681,533$ 70,781$ 46,997$ 161,013$ 111,238$ 291,504$

Unexpended interest accumulated to date 15,350 GASB 31 Adjustment (376)

Fund balance at June 30, 2017 306,478$

Note: (1) These funds were transferred from accrued interest for project use as approved by VCTC on December 17, 2015.(2) The unexpended balance includes both LTF and City match, as the City recognizes match revenue when funds are received from VCTC. The city match included in the unexpended amount is approximately 30%.(3) The unexpended balance of $1 is LTF funds.

CITY OF SAN BUENAVENTURA, CALIFORNIA

Transportation Development Act Local Transportation FundArticle 3, Section 99234 Public Utilities Code

Schedule of Status of Funds by Project

Fiscal Year Ended June 30, 2017

13

14 __________________________________________________________________________________________________________________________________________________________________________________

23702 Birtcher Drive, Lake Forest, CA 92630 ■ T: (949) 552-7700 ■ www.conradllp.com

Board of Commissioners Ventura County Transportation Commission Ventura, California

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN

AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

We have audited, in accordance with the auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards issued by the Comptroller General of the United States, the Transportation Development Act Local Transportation Fund pursuant to Article 3 (“TDA Fund”) of the City of San Buenaventura, California (“City”), as of and for the fiscal years ended June 30, 2017 and 2016, and the related notes to the financial statements, which collectively comprise City’s TDA Fund financial statements, and have issued our report thereon dated November 20, 2017.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered the City’s internal control over financial reporting (internal control) to determine the audit procedures that are appropriate in the circumstances for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the City’s internal control. Accordingly, we do not express an opinion on the effectiveness of the City’s internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Our consideration of internal control was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control that might be material weaknesses or significant deficiencies. Given these limitations, during our audit we did not identify any deficiencies in internal control that we consider to be material weaknesses. However, material weaknesses may exist that have not been identified.

Board of Commissioners Ventura County Transportation Commission Ventura, California

15

Compliance and Other Matters As part of obtaining reasonable assurance about whether the financial statements of the TDA Fund of the City are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, including §6666 of Part 21 of the California Code of Regulations, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards, including §6666 of Part 21 of the California Code of Regulations.

Purpose of this Report The purpose of this report is solely to describe the scope of our testing of internal control and compliance and the results of that testing, and not to provide an opinion on the effectiveness of the entity’s internal control or on compliance. This report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the entity’s internal control and compliance. Accordingly, this communication is not suitable for any other purpose.

Lake Forest, California November 20, 2017