clw pitch-vlinkedin-20160328

TRANSCRIPT

1

Clearwater Paper Corporation (CLW)

Recommendation (Buy)

Xiaoshuang Zha and Hongyuan Wang

The 360 Huntington Fund

Sector: MaterialsIndustry (GICS): Paper and ForestIndustry (Fidelity): Paper & Forest Products

2

Disclosure Statement• I have no positions in any stocks mentioned, and

no plans to initiate any positions within the next 72 hours.

3

Business Description & Market Profile• Market Profile

– Market cap (Small-821.76M)– Primary market (U.S.)

• Business Description– Clearwater Paper manufactures quality consumer

tissue, away-from-home (AFH) tissue, parent roll tissue, bleached paperboard, used by quality-conscious printers and packaging converters, and pulp at manufacturing facilities across the nation.

– Pulp and paperboard: 45% of 2015 net sales;– Consumer products: 55% of 2015 net sales.

4

LARGEST NORTH AMERICANMANUFACTURERS OF PRIVATE LABEL TISSUE

5

LEADING MANUFACTURER OF Solid Bleach Sulfate paperboard used in packaging of premium consumer goods, pharmaceuticals, food and liquid, and food service plates, cups and folding cartons.

Solid Bleach Sulfate paperboard

6

• The cost structure;• The realization of operating efficiencies,

as well as the company overall. It started with the sale of our specialty mills at the end of 2014 with a plan to reinvest the proceeds of that sale into strategic capital investments.

The cost structure improvement from 2014 to 2015

7

Industry Analysis• SWOT

Strengths:Leading private label tissue manufacturer with a broad U.S. footprint.High quality brand-equivalent tissue and other products to meet retailers' private label strategies.High quality paperboard.Long-standing customer relationships.Strategically positioned facilities.

Weaknesses:-Tax structure-Competitive market

Opportunities:-New acquisitions-Growth rates and profitability-New technology-Cost efficiency improvement

Threats:-Increase in labor costs-Price changes-Tax changes-Government regulations-Financial capacity

8

Porter’s Five Forces• Competitive Rivalry

– High exit barriers; highly competitive market• Buyer Power

– Low buyer price sensitivity; customer concentration• Supplier Power

– Partial self supply; low bargaining costs• Threat of New Entry

– Capital intensive; expensive facility; loyal customers• Threat of Substitution

– Limited number of substitutes

9

Industry Analysis• Pros: • The stable U.S. economy stimulates the consumption demand • Packaging segment is growing increasingly due to the boom of

online shopping and the large production of consumer nondurable;

• Demand of tissue tend to grow with the economy and the expansion of middle class; (in 2015 tissue industry grew 1%)

• Lower oil price reduces paper production cost;• Pulp price will rise due to capacity closure and China’s robust

demand;• The introduction of this industry can further diversify our

portfolio because no such equity has been included. (Beta of CLW is 0.67)

10

Industry Analysis• Cons: • The declining print market due to expanding

electronic communications• The rising debt due to more capital spending

11

Catalysts• New Coating: • CLW announced the introduction of a modified

clay coating formulation on Feb 15, 2016.• The modification will result in a 10 to 15 point

improvement in paperboard gloss. • This change will be effective with mid-April

production.

12

Catalysts• Sale of Specialty Mills:• CLW sold its specialty products business and

mills to Dunn Paper on December 30, 2014. • The company intends to sharpen Consumer

Products Division’s focus on the core retail business and improve efficiency.

• The capital projects in which they invest the proceeds are expected to yield a 300 to 400 bp improvement in Consumer Product Division’s EBITDA margins over the next three years.

13

Catalysts• Vertical Integration• The company produces pulp, which is the raw

material for paperboard and other consumer products that the company makes. Almost all the pulp is for internal use (81% Paperboard+19% Tissue).

• Supply Chain Management: a secure pulp supply and a steady demand source; transportation and drying cost savings; reduction of bargaining cost and input cost volatility

14

Catalysts• Revenue Drivers: • Consumer Products division had two big wins in 2015:

selected as a sole supplier to a new grocery chain in the east; secured incremental new business with a big box retailer in the Midwest.

• Pulp digester and optimization project: core engineering design and planning phase were completed in 2015 and all environmental permits were secured with some attractive local tax incentives.

• Warehouse automation project: laser-guided vehicles and related equipment are being installed in various mills, will start up soon.

• Lean Six Sigma and TPM projects: help reduce waste and improve efficiency rate.

15

Catalysts• Unique Role:• The only producer that does not convert SBS

paperboard into end products among the five largest producers.

• It is not simultaneously a supplier of and a competitor to its customers. When market supply of paperboard decreases, the company will not divert production to internal use.

• Resulted in customer loyalty. Average tenure of top 10 tissue customers is 13 years; of top 10 paperboard customers is 31 years.

16

Catalysts• Unique Role:• The only coated SBS paperboard (folding carton,

plates, cup and liquid packaging) mill in the western U.S..

• Reduce transaction costs to customers in western U.S. and Asia (esp. Japan); be able to compete on a cost-advantaged basis relative to East Coast competitors.

• Logistics planning: reduced miles traveled per customer shipment by 2% in 2015.

17

ComparablesCLW NP (Neenah Paper) GLT (Glatfelter) UFS (Domtar)

Current Current Current Current52W Range $32.00-$67.99 $52.70-$69.63 $14.09-$27.58 $29.88-$47.00

Market Cap 841.48M 1048.2M 839.30M 2343.4M

Beta 0.668 0.954 0.995 1.074

Current 3 Yr Avg

Current 3 Yr Avg Current 3 Yr Avg Current 3 Yr Avg

ROA 3.60 3.26 6.92 8.27 4.21 4.36 2.40 3.59

ROE 11.51 9.92 16.69 21.08 9.84 10.40 5.12 7.85

ROIC 7.43 6.75 14.08 14.03 6.75 7.27 4.57 6.28

Gross Margin 13.67 12.79 21.66 20.65 12.18 12.61 19.51 15.81

Operating Margin

7.06 5.46 11.16 10.55 5.78 5.56 5.47 5.00

Debt to Equity 119.82 114.27 73.62 77.29 54.86 60.61 47.51 49.84

P/E 14.70 14.74 16.88 16.61 13.17 16.22 11.24 13.51

P/B 1.81 2.08 3.63 3.37 1.26 1.55 0.89 0.95

PEG 2.51 3.18 1.49 1.53 1.25 1.41 4.17 4.07

Dividend Yield 0.00 0.00 1.91 1.75 2.43 1.92 3.48 3.24

18

Valuation (Why mispriced)• Market overreaction (oversold) to 2014 negative

earnings

19

Income Tax

20

Why Mispriced

21

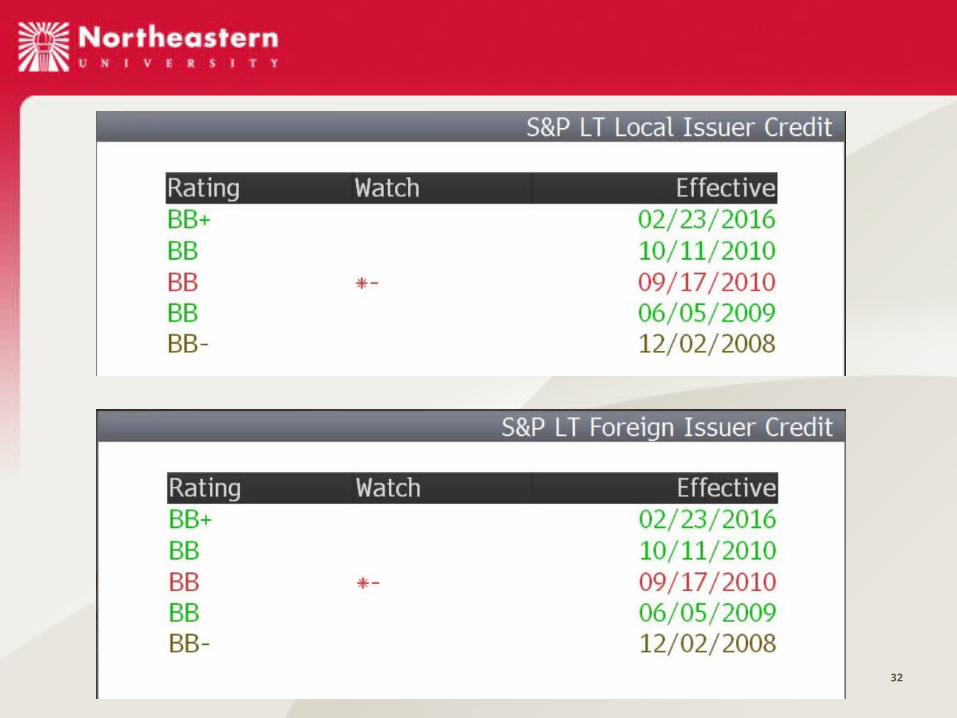

Risks• Market risks

– Interest rate risk– Currency risk– Oil price

• Industry risks– Regulatory risks: environmental regulations

• Company specific risks– Labor contract negotiation– Concentrated customers– 2013 Notes contain restriction covenants

22

Price Graph• CLW vs. Russell 3000 (IWV) and peer group.

23

Target Price

24

Q&A

25

Discussion

• Why do we buy back this company after 3 months?

(Background: 360 Huntington Fund sold it at the end of 2015, 3 month ago.)

26

Model Comparison

Difference The Model of December Our ModelWeights 40% P/E – 30% P/S – 30%

P/B 70% FCFF -- 30% P/E

NI growth forecast

2015 forecast: -1058.39% 2015 real: 2518%

Comparables Compared to IP and KS Compared to GLT and UFSRevenue of Tissue

Limited growth;sale of specialty business and mills

Limited growth is true;Gross margin: 13.1%--13.7%Operating margin: 4.1%--7.1%

27

28

Catalysts• Unique Role:• The only tissue manufacturer that solely produces

quality private label tissue for large retail trade channels.

• Other producers manufacture only branded products or both branded and private label products. Generally they manufacture private label products at a lower quality grade than their branded products so as not to impair sales of branded products.

• CLW is able to offer brand-equivalent quality products but at lower prices.

29

Supplements

30

GDP 2016 Forecast• http://

cn.knoema.com/qhswwkc/us-gdp-growth-forecast-2015-2019-and-up-to-2060-data-and-charts

• http://www.indexmundi.com/commodities/?commodity=crude-oil&months=12

GDP Crude Oil Price

• http://www.midlandpaper.com/clearwater-paper-announces-pending-coating-modification/

31

32