comprehensive national industrial strategy and...

TRANSCRIPT

COMPREHENSIVE NATIONAL

INDUSTRIAL STRATEGY AND

INDUSTRY ROADMAPS

Employers’ Sectoral Consultation27 May 2016, Makati City

Securing the Future of Industries

Presentation OutlineI. Macroeconomic Performance, Opportunities

and ChallengesII. New Industrial Policy: Structural Transformation for

Inclusive & Sustainable Growth Address unemployment and poverty Attract more investments Global value chains

III. PH Manufacturing Resurgence Program Industry Roadmaps

IV. Comprehensive National Industrial Strategy (CNIS) Manufacturing, Agriculture, Services

2

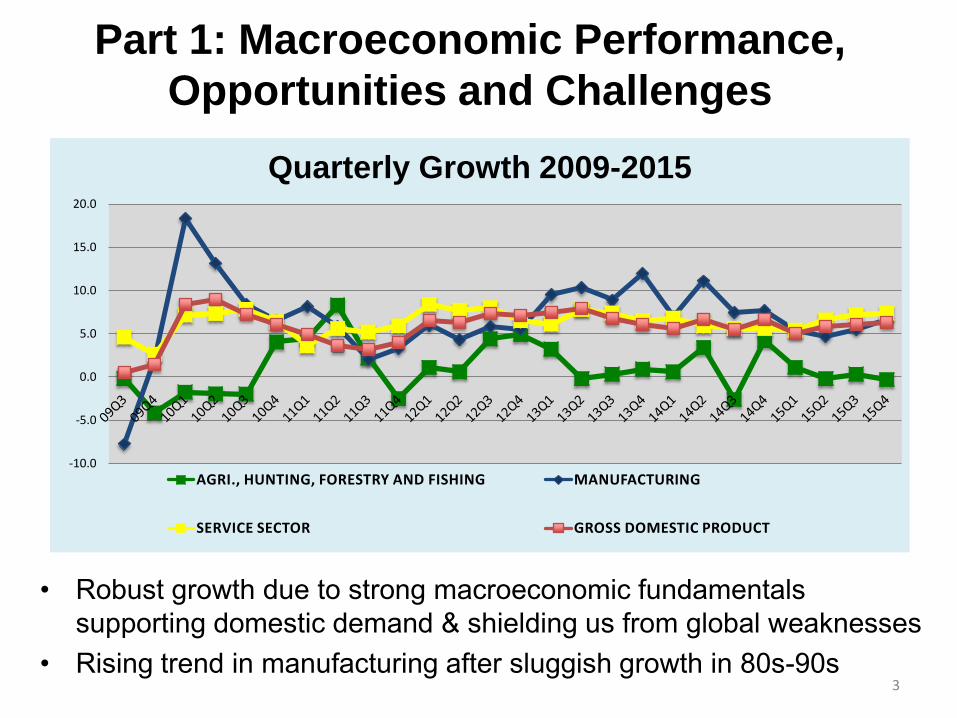

Part 1: Macroeconomic Performance,

Opportunities and Challenges

• Robust growth due to strong macroeconomic fundamentals supporting domestic demand & shielding us from global weaknesses

• Rising trend in manufacturing after sluggish growth in 80s-90s

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Quarterly Growth 2009-2015

AGRI., HUNTING, FORESTRY AND FISHING MANUFACTURING

SERVICE SECTOR GROSS DOMESTIC PRODUCT

3

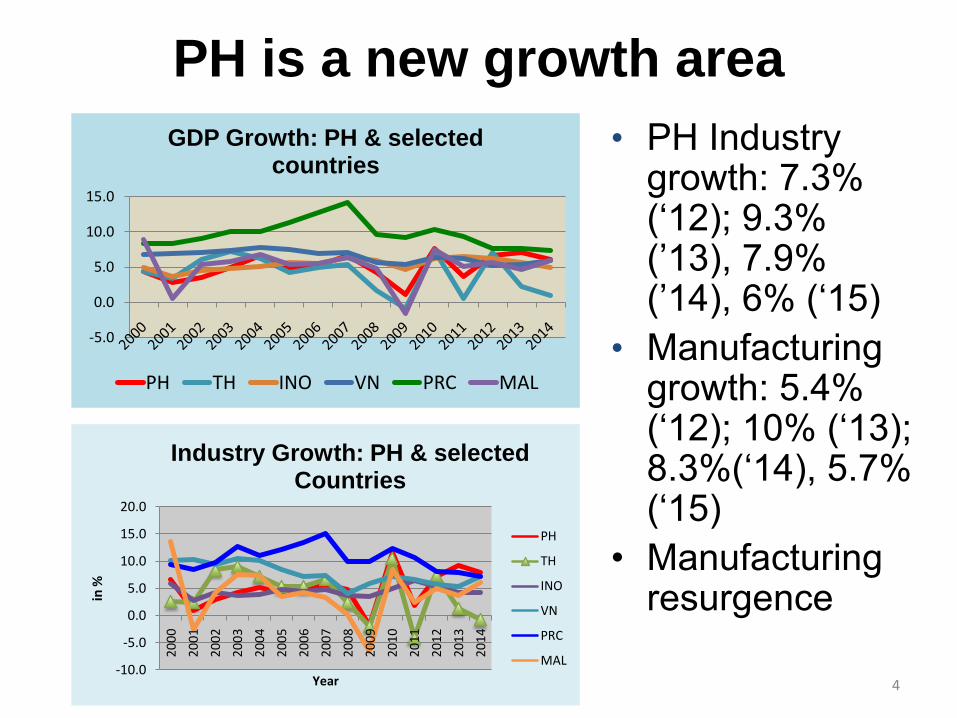

PH is a new growth area

• PH Industry growth: 7.3% (‘12); 9.3% (’13), 7.9% (’14), 6% (‘15)

• Manufacturing growth: 5.4% (‘12); 10% (‘13); 8.3%(‘14), 5.7% (‘15)

• Manufacturing resurgence

-5.0

0.0

5.0

10.0

15.0

GDP Growth: PH & selected countries

PH TH INO VN PRC MAL

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

in %

Year

Industry Growth: PH & selected Countries

PH

TH

INO

VN

PRC

MAL

4

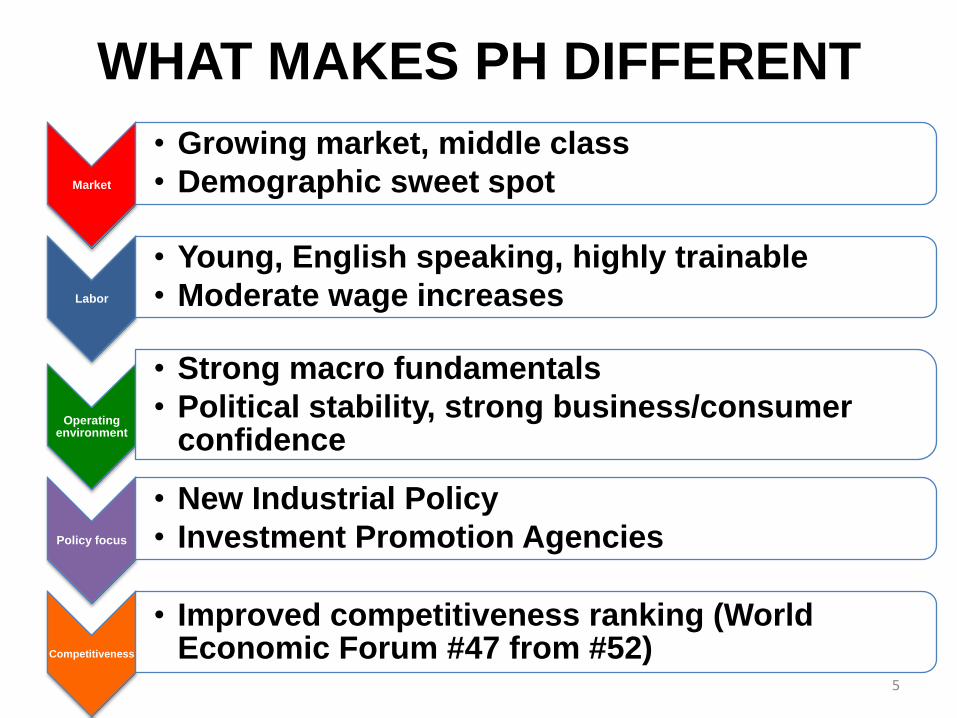

WHAT MAKES PH DIFFERENT

Market

• Growing market, middle class

• Demographic sweet spot

Labor

• Young, English speaking, highly trainable

• Moderate wage increases

Operating environment

• Strong macro fundamentals

• Political stability, strong business/consumer confidence

Policy focus

• New Industrial Policy

• Investment Promotion Agencies

Competitiveness

• Improved competitiveness ranking (World Economic Forum #47 from #52)

5

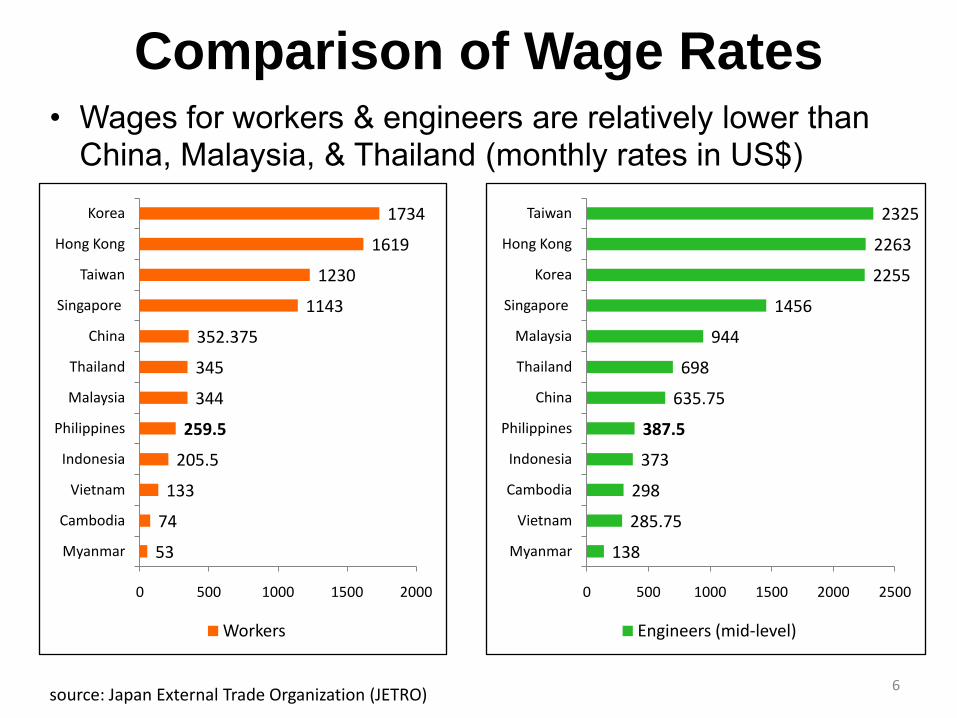

Comparison of Wage Rates

53

74

133

205.5

259.5

344

345

352.375

1143

1230

1619

1734

0 500 1000 1500 2000

Myanmar

Cambodia

Vietnam

Indonesia

Philippines

Malaysia

Thailand

China

Singapore

Taiwan

Hong Kong

Korea

Workers

source: Japan External Trade Organization (JETRO)

138

285.75

298

373

387.5

635.75

698

944

1456

2255

2263

2325

0 500 1000 1500 2000 2500

Myanmar

Vietnam

Cambodia

Indonesia

Philippines

China

Thailand

Malaysia

Singapore

Korea

Hong Kong

Taiwan

Engineers (mid-level)

• Wages for workers & engineers are relatively lower than China, Malaysia, & Thailand (monthly rates in US$)

6

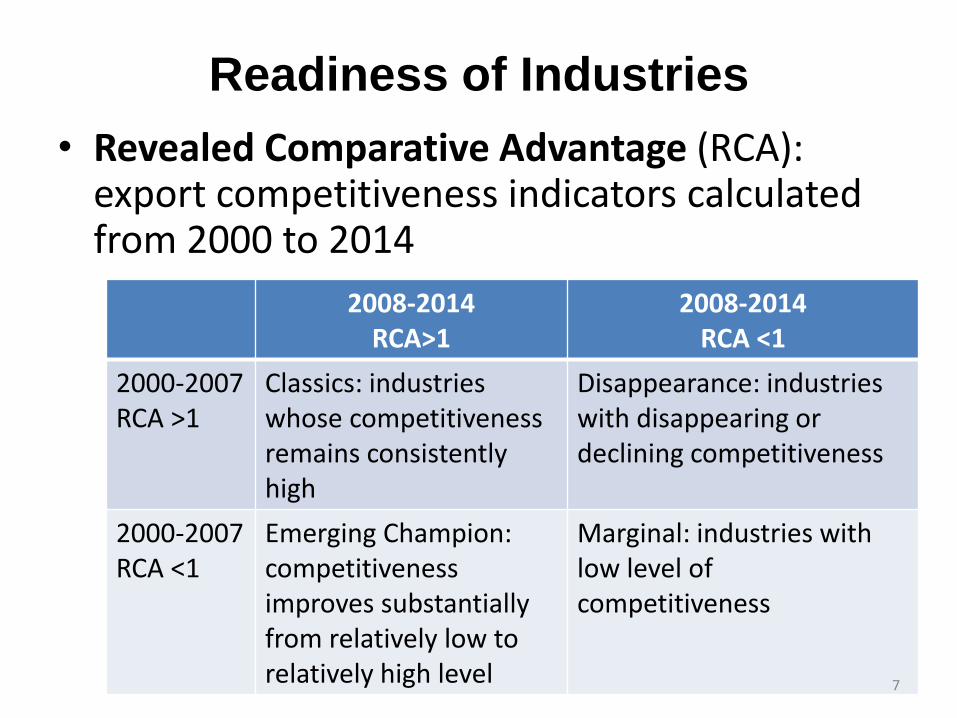

Readiness of Industries

• Revealed Comparative Advantage (RCA): export competitiveness indicators calculated from 2000 to 2014

2008-2014RCA>1

2008-2014RCA <1

2000-2007 RCA >1

Classics: industrieswhose competitivenessremains consistently high

Disappearance: industries with disappearing or declining competitiveness

2000-2007 RCA <1

Emerging Champion: competitiveness improves substantially from relatively low to relatively high level

Marginal: industries with low level of competitiveness

7

CODE PRODUCT DESCRIPTION611 Sugars, beet and cane, raw, solid

2659 Vegetable textile fibres, nes, and waste4243 Coconut (copra) oil541 Potatoes, fresh or chilled, excluding sweet potatoes

8745 Measuring, controlling and scientific instruments, nes7621 Radio receivers for motor-vehicles573 Banana, plantain, fresh or dried

7591 Parts, nes of & accessories for machines of headings 7511 or 75187722 Printed circuits, and parts thereof, nes8432 Women’s, girls’, infants’ outerwear, textile, not knitted or crocheted

7763 Diodes, transistors, photocells, etc585 Fruit or vegetable juices589 Fruit prepared or preserved, nes

8811 Photographic cameras, flashlight apparatus, parts, accessories, nes

7764 Electronic microcircuits615 Molasses371 Fish, prepared or preserved, nes577 Nuts edible, fresh or dried

Classics

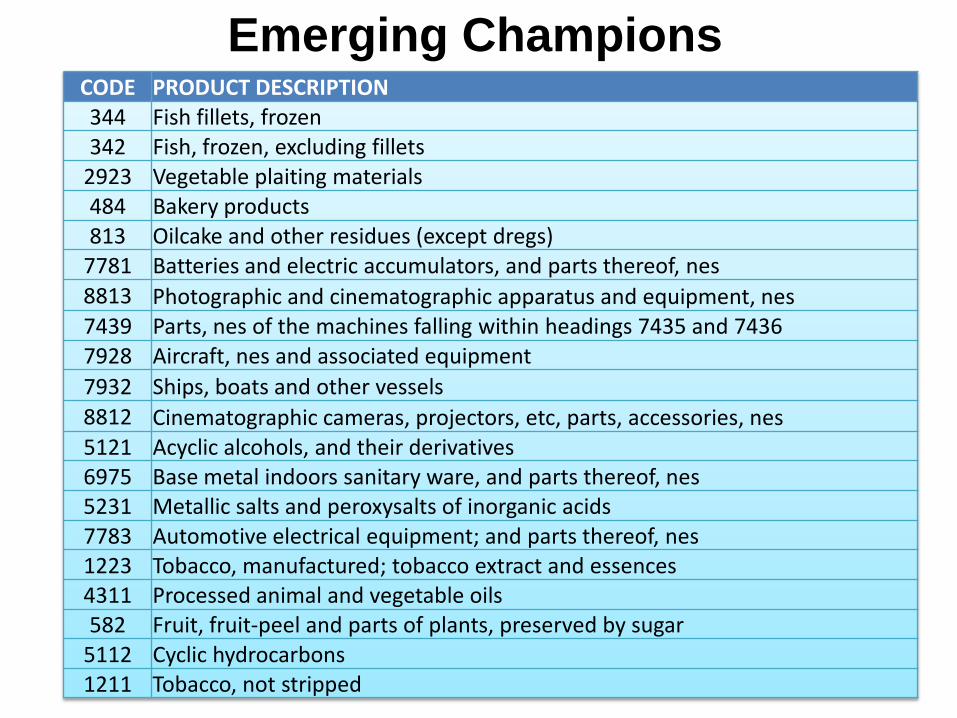

CODE PRODUCT DESCRIPTION344 Fish fillets, frozen342 Fish, frozen, excluding fillets

2923 Vegetable plaiting materials484 Bakery products813 Oilcake and other residues (except dregs)

7781 Batteries and electric accumulators, and parts thereof, nes

8813 Photographic and cinematographic apparatus and equipment, nes7439 Parts, nes of the machines falling within headings 7435 and 74367928 Aircraft, nes and associated equipment

7932 Ships, boats and other vessels

8812 Cinematographic cameras, projectors, etc, parts, accessories, nes5121 Acyclic alcohols, and their derivatives6975 Base metal indoors sanitary ware, and parts thereof, nes5231 Metallic salts and peroxysalts of inorganic acids7783 Automotive electrical equipment; and parts thereof, nes1223 Tobacco, manufactured; tobacco extract and essences4311 Processed animal and vegetable oils582 Fruit, fruit-peel and parts of plants, preserved by sugar

5112 Cyclic hydrocarbons1211 Tobacco, not stripped

Emerging Champions

CODE PRODUCT DESCRIPTION

612 Refined sugar etc712 Coffee extracts, essences or concentrates711 Coffee green, roasted; coffee substitutes containing coffee723 Cocoa butter and paste730 Chocolate and other preparations containing cocoa, nes721 Cocoa beans, raw, roasted752 Spices, except pepper and pimento2331 Synthetic rubber, latex; factice derived from oils421 Rice in the husk or husked, but not farther prepared422 Rice, semi-milled or wholly milled440 Maize, unmilled4242 Palm oil4244 Palm kernel oil4249 Fixed vegetable oils, nes6639 Articles of ceramic materials, nes7851 Motorcycles, auto-cycles; side-cars of all kind, etc5530 Perfumery, cosmetics, toilet preparations, etc224 Milk and cream, preserved, concentrated or sweetened2882 Other non-ferrous base metal waste and scrap, nes

Marginals

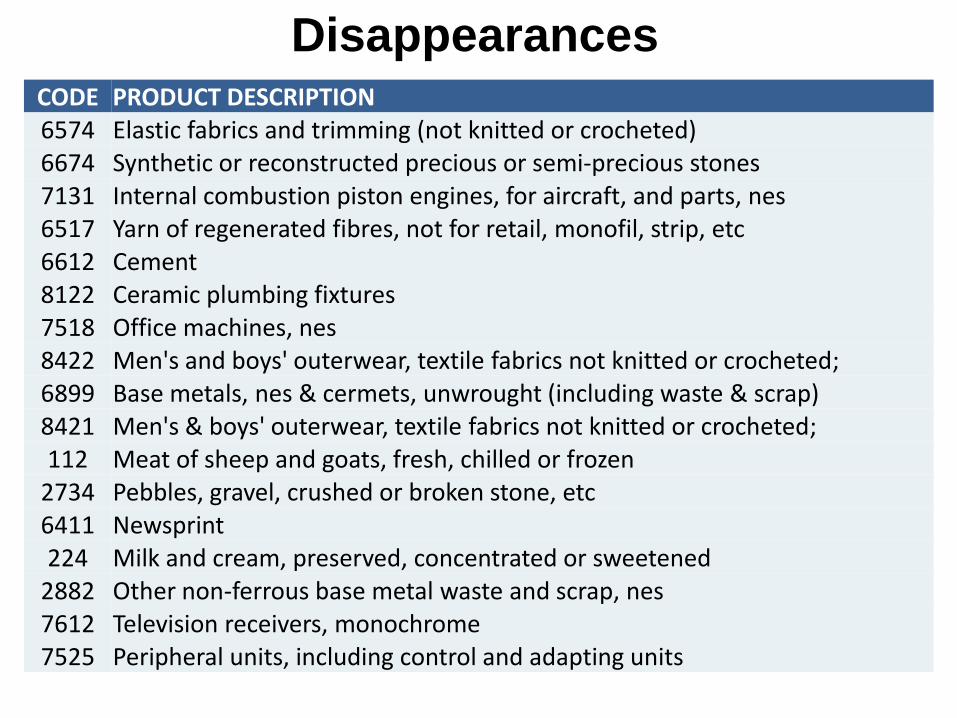

CODE PRODUCT DESCRIPTION6574 Elastic fabrics and trimming (not knitted or crocheted)6674 Synthetic or reconstructed precious or semi-precious stones7131 Internal combustion piston engines, for aircraft, and parts, nes6517 Yarn of regenerated fibres, not for retail, monofil, strip, etc6612 Cement8122 Ceramic plumbing fixtures7518 Office machines, nes8422 Men's and boys' outerwear, textile fabrics not knitted or crocheted;6899 Base metals, nes & cermets, unwrought (including waste & scrap)8421 Men's & boys' outerwear, textile fabrics not knitted or crocheted;112 Meat of sheep and goats, fresh, chilled or frozen

2734 Pebbles, gravel, crushed or broken stone, etc6411 Newsprint224 Milk and cream, preserved, concentrated or sweetened

2882 Other non-ferrous base metal waste and scrap, nes7612 Television receivers, monochrome7525 Peripheral units, including control and adapting units

Disappearances

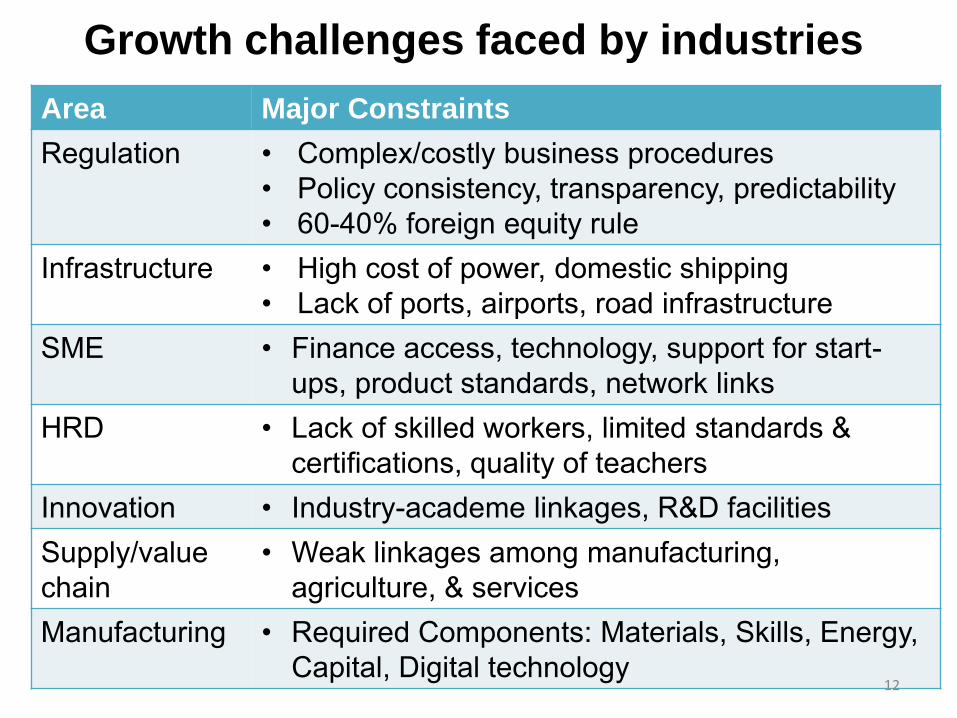

Growth challenges faced by industries

Area Major Constraints

Regulation • Complex/costly business procedures • Policy consistency, transparency, predictability • 60-40% foreign equity rule

Infrastructure • High cost of power, domestic shipping• Lack of ports, airports, road infrastructure

SME • Finance access, technology, support for start-ups, product standards, network links

HRD • Lack of skilled workers, limited standards & certifications, quality of teachers

Innovation • Industry-academe linkages, R&D facilitiesSupply/value chain

• Weak linkages among manufacturing, agriculture, & services

Manufacturing • Required Components: Materials, Skills, Energy, Capital, Digital technology

12

Part 2: Government Strategy

New Industrial Policy

Inclusive growth

Regional economic

integration, FTAs

Jobs,

Competitive-

ness

Competitiveness - crucial in upgrading, rising regional integration & global value chains

Industrial policy -best way to create jobs, reduce poverty, & achieve inclusive growth

13

• Upgrade industries

• Remove growth obstacles

GOAL: Improve Competitiveness

• Create proper environment for private sector development

• Private sector: proximate source of growth

Government as Facilitator

• How to plug in regional production networks

• Move up the value chain

• Build strong regional economies

GVC-focused,

Cluster-based

Strategic Industrial Policy

14

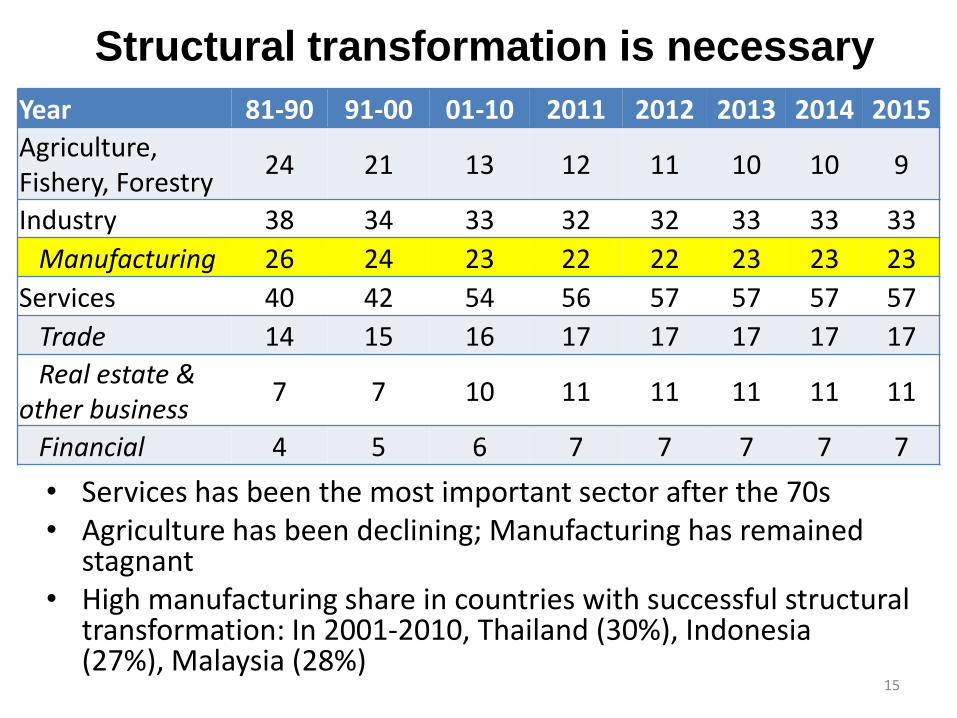

Structural transformation is necessary

• Services has been the most important sector after the 70s• Agriculture has been declining; Manufacturing has remained

stagnant• High manufacturing share in countries with successful structural

transformation: In 2001-2010, Thailand (30%), Indonesia (27%), Malaysia (28%)

Year 81-90 91-00 01-10 2011 2012 2013 2014 2015

Agriculture, Fishery, Forestry

24 21 13 12 11 10 10 9

Industry 38 34 33 32 32 33 33 33

Manufacturing 26 24 23 22 22 23 23 23

Services 40 42 54 56 57 57 57 57

Trade 14 15 16 17 17 17 17 17

Real estate & other business

7 7 10 11 11 11 11 11

Financial 4 5 6 7 7 7 7 7

15

Regional Economic Transformation is crucialSuccessful structural change relies on the strength of regional economies

• Imbalances: NCR, Calabarzon, Central Luzon: largest share of GDP; highest manufacturing share to GRDP, highest unemployment

• ARMM, CARAGA, IVB, V, IX: poverty incidence persistently high • Industrial policy efforts in the regions: improve productivity in

agriculture where half of the poor are, agribusiness

NCR

CAR

ILOCOSCAGAYAN VALLEY

CENTRAL LUZON

CALABARZON

MIMAROPA BICOL

WESTERN VISAYAS

CENTRAL VISAYAS

EASTERN VISAYAS

ZAMBOANGA PENINSULA

NORTHERN MINDANAO

DAVAO REGION SOCCSKSARGEN

CARAGAARMM

-10%

0%

10%

20%

30%

40%

50%

60%

70%

-5% 0% 5% 10% 15% 20%

Average Growth Rate (’12-’14)

Man

ufa

ctu

rin

g as

% o

f G

RD

P

16

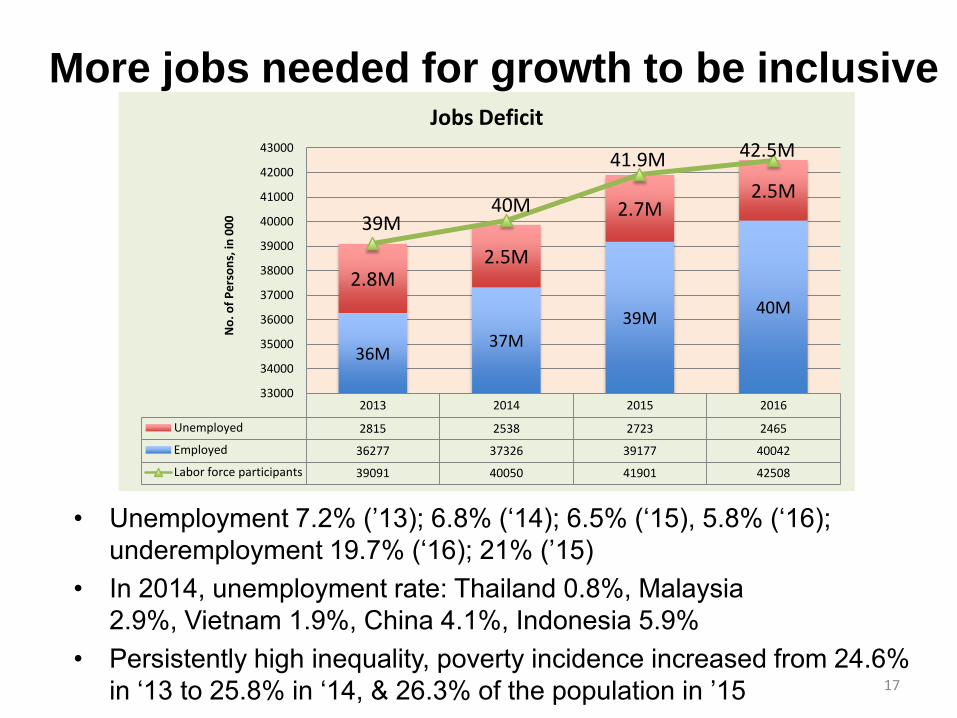

More jobs needed for growth to be inclusive

• Unemployment 7.2% (’13); 6.8% (‘14); 6.5% (‘15), 5.8% (‘16); underemployment 19.7% (‘16); 21% (’15)

• In 2014, unemployment rate: Thailand 0.8%, Malaysia 2.9%, Vietnam 1.9%, China 4.1%, Indonesia 5.9%

• Persistently high inequality, poverty incidence increased from 24.6% in ‘13 to 25.8% in ‘14, & 26.3% of the population in ’15

2013 2014 2015 2016

Unemployed 2815 2538 2723 2465

Employed 36277 37326 39177 40042

Labor force participants 39091 40050 41901 42508

36M37M

39M40M

2.8M2.5M

2.7M2.5M

39M40M

41.9M 42.5M

33000

34000

35000

36000

37000

38000

39000

40000

41000

42000

43000

No

. of

Pe

rso

ns,

in 0

00

Jobs Deficit

17

Need to attract more FDIs

• 2013-2014: PH ($3.9B; 6.2B) still lags behind Indonesia ($18B; 25.9), Malaysia ($12.3; 10.6B), Thailand ($12.9B; 12.7B), Singapore ($63.8B; 67B ), & Vietnam ($8.9B

• aggressive marketing/promotion program to attract FDI esp. technology intensive, target companies to fit our IP strategy

-10000

0

10000

20000

30000

40000

50000

60000

70000

FDI Inflows, annual 1970-2013 (million US$)

Brunei Darussalam

Cambodia

Indonesia (…2002)

Lao People's Dem. Rep.

Malaysia

Myanmar

Philippines

Singapore

Thailand

Viet Nam

18

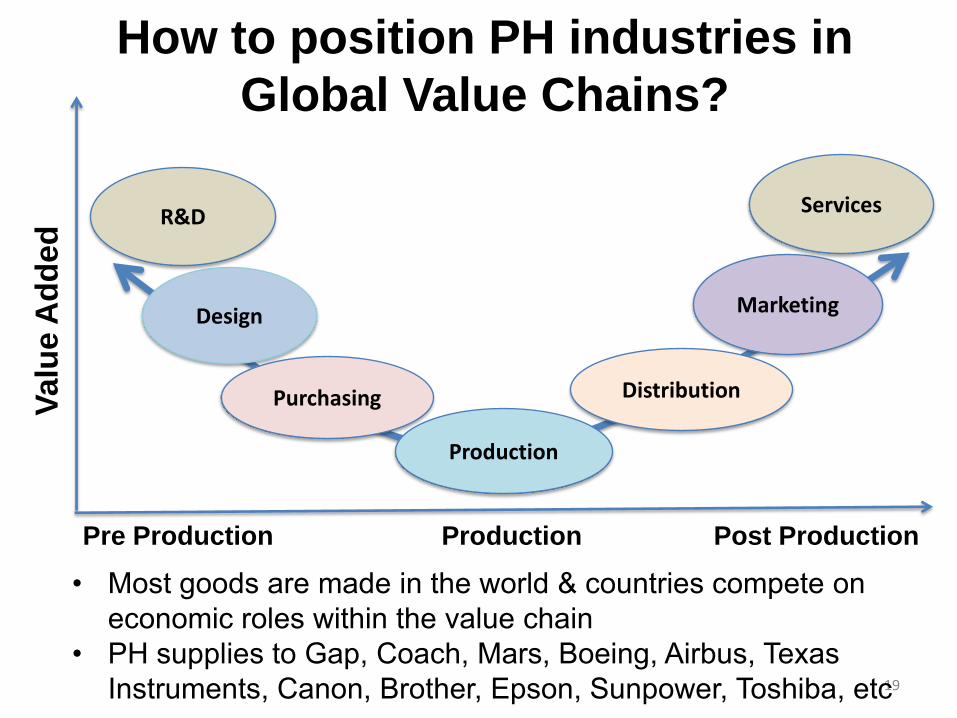

How to position PH industries in

Global Value Chains?V

alu

e A

dd

ed

19

Design

Purchasing

Production

Distribution

Marketing

Services

Pre Production Production Post Production

• Most goods are made in the world & countries compete on economic roles within the value chain

• PH supplies to Gap, Coach, Mars, Boeing, Airbus, Texas Instruments, Canon, Brother, Epson, Sunpower, Toshiba, etc

R&D

Part 3: Manufacturing Resurgence

Program (MRP)

Enhance manufacturing competitiveness • Lead Implementing Agency: DTI• Participating Agencies: DTI, DOST, DOLE, DOLE-

TESDA, CHED, DOE, DA, NPC, NEA, PCA

Targets by 2025: 30% share of manufacturing to GDP; 15% share to Total Employment

Industry Development Program DTI-BOI’s contributory program to MRP Comprehensive Automotive Resurgence Strategy

(CARS) Program – E.O. 182

20

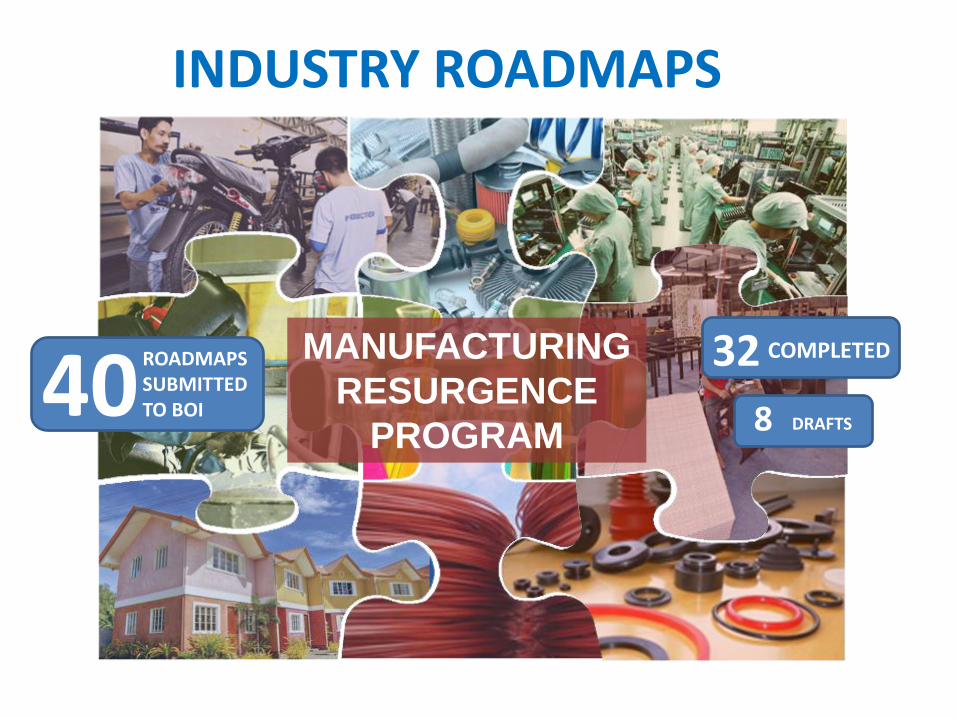

INDUSTRY ROADMAPS

MANUFACTURING

RESURGENCE

PROGRAM40

ROADMAPS SUBMITTEDTO BOI

32 COMPLETED

8 DRAFTS

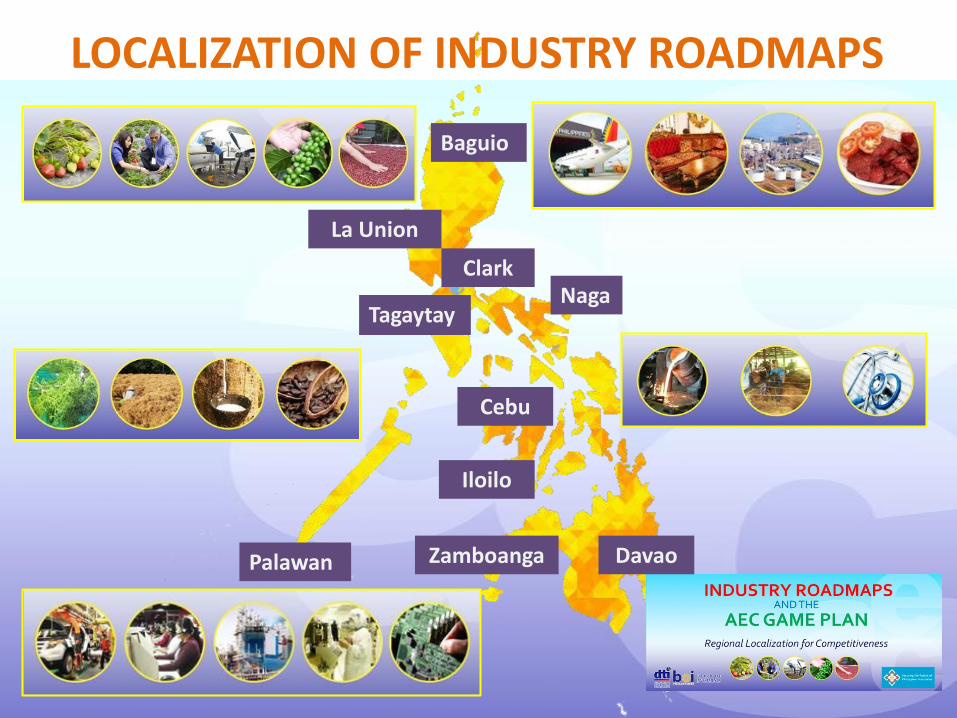

LOCALIZATION OF INDUSTRY ROADMAPS

Baguio

Clark

Palawan

TagaytayNaga

Iloilo

Zamboanga Davao

Cebu

La Union

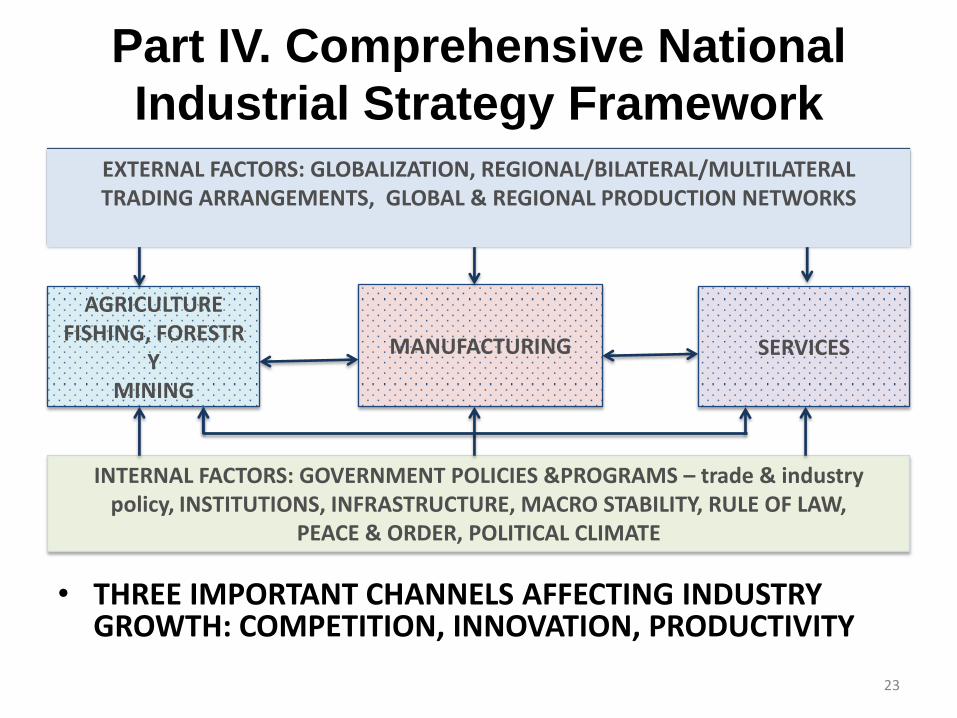

Part IV. Comprehensive National

Industrial Strategy Framework

• THREE IMPORTANT CHANNELS AFFECTING INDUSTRY GROWTH: COMPETITION, INNOVATION, PRODUCTIVITY

23

MANUFACTURING SERVICES

AGRICULTURE FISHING, FORESTR

YMINING

INTERNAL FACTORS: GOVERNMENT POLICIES &PROGRAMS – trade & industry policy, INSTITUTIONS, INFRASTRUCTURE, MACRO STABILITY, RULE OF LAW,

PEACE & ORDER, POLITICAL CLIMATE

EXTERNAL FACTORS: GLOBALIZATION, REGIONAL/BILATERAL/MULTILATERAL TRADING ARRANGEMENTS, GLOBAL & REGIONAL PRODUCTION NETWORKS

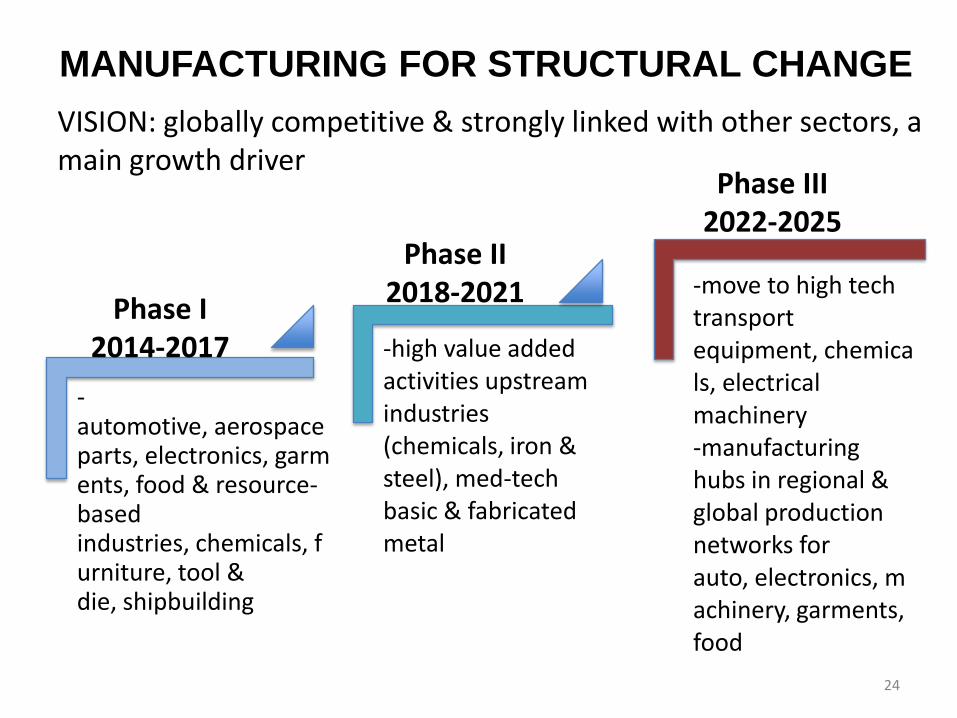

MANUFACTURING FOR STRUCTURAL CHANGE

-automotive, aerospace parts, electronics, garments, food & resource-based industries, chemicals, furniture, tool & die, shipbuilding

-move to high tech transport equipment, chemicals, electrical machinery-manufacturing hubs in regional & global production networks for auto, electronics, machinery, garments, food

-high value added activities upstream industries (chemicals, iron & steel), med-tech basic & fabricated metal

Phase I 2014-2017

Phase II 2018-2021

Phase III 2022-2025

VISION: globally competitive & strongly linked with other sectors, a main growth driver

24

AGRIBUSINESS: CATALYST TO DRIVE

REGIONAL ECONOMIC TRANSFORMATIONTransform & upgrade agriculture from traditional farming to a globally competitive agribusiness sector

-rubber, coconut, mangoes, coffee, cacao,banana, palm oil & other high value crops; supply chain gaps: strengthen agro-processing & its linkages to production

-deepen participation in GVC -PH as agribusiness regional hub

- strengthen supply chains, upgrade commodity clusters; R&D, access to technologies, finance; regulatory & certification system

Phase I 2014-2017

Phase II 2018-2021

Phase III 2022-2025

25

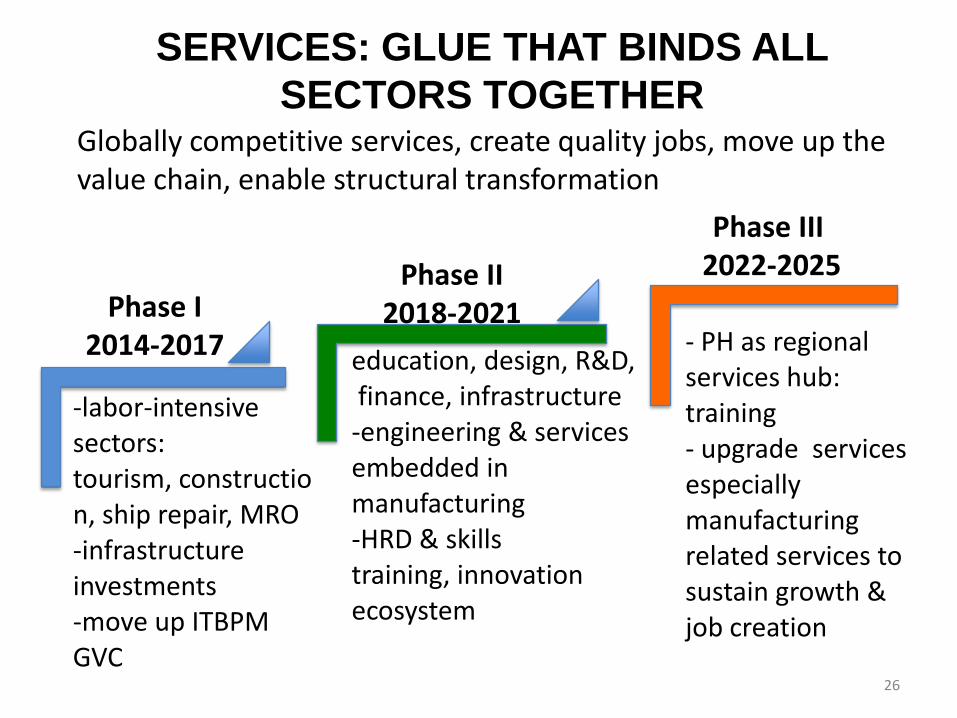

SERVICES: GLUE THAT BINDS ALL

SECTORS TOGETHER

-labor-intensive sectors: tourism, construction, ship repair, MRO-infrastructure investments -move up ITBPM GVC

- PH as regional services hub: training - upgrade services especially manufacturing related services to sustain growth & job creation

education, design, R&D,finance, infrastructure-engineering & services embedded in manufacturing-HRD & skills training, innovation ecosystem

Phase I 2014-2017

Phase II 2018-2021

Phase III2022-2025

Globally competitive services, create quality jobs, move up the value chain, enable structural transformation

26

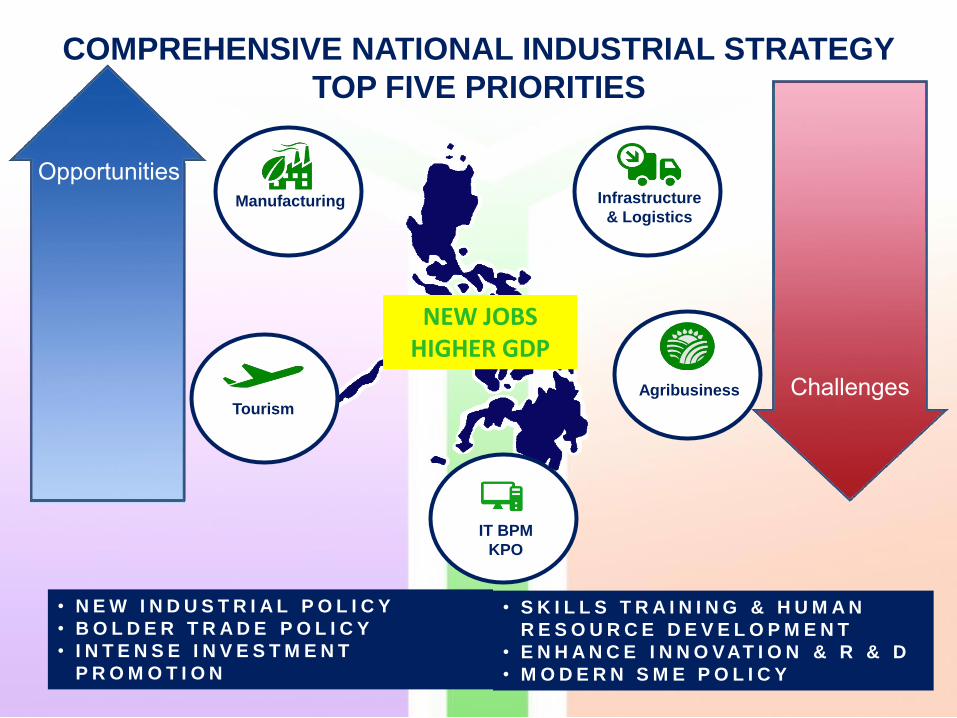

COMPREHENSIVE NATIONAL INDUSTRIAL STRATEGY

TOP FIVE PRIORITIES

Opportunities

Challenges

Manufacturing

Tourism

IT BPM

KPO

Agribusiness

Infrastructure

& Logistics

NEW JOBSHIGHER GDP

• N E W I N D U S T R I A L P O L I C Y

• B O L D E R T R A D E P O L I C Y

• I N T E N S E I N V E S T M E N T

P R O M O T I O N

• S K I L L S T R A I N I N G & H U M A N

R E S O U R C E D E V E L O P M E N T

• E N H A N C E I N N O VAT I O N & R & D

• M O D E R N S M E P O L I C Y

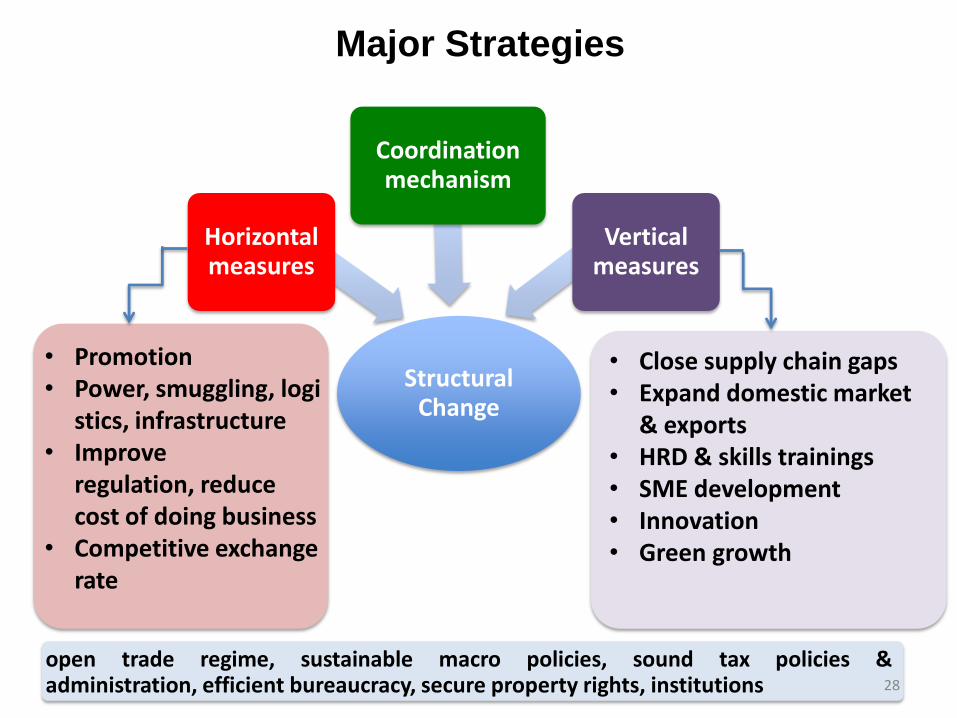

Major Strategies

Structural Change

Horizontal measures

Coordination mechanism

Vertical measures

• Close supply chain gaps• Expand domestic market

& exports• HRD & skills trainings• SME development• Innovation • Green growth

• Promotion• Power, smuggling, logi

stics, infrastructure• Improve

regulation, reduce cost of doing business

• Competitive exchange rate

open trade regime, sustainable macro policies, sound tax policies &administration, efficient bureaucracy, secure property rights, institutions 28