credit suisse 2014 energy summit - seadrill · credit suisse 2014 energy summit ceo – per wullf...

TRANSCRIPT

Credit Suisse 2014 Energy SummitCEO – Per Wullf

Vail, Colorado, February 2014

Forward Looking Statements

The statements described in this presentation that are not historical facts are forward-looking statements

within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of

1934. Forward-looking statements which could be made include, but are not limited to, statements involving

prospects for the Company, expected revenues, capital expenditures, costs and results of operations and

contingencies and other factors discussed in the Company's most recent annual report on the Form 20-F for the year

ended December 31, 2012 and in the Company's other filings with the SEC, which are available free of charge on the

SEC's website at www.sec.gov. Should one or more of these risks or uncertainties materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those indicated. All subsequent written and oral

forward-looking statements attributable to the Company or to persons acting on our behalf are expressly qualified in

their entirety by reference to these risks and uncertainties. You should not place undue reliance on forward-looking

statements. Each forward-looking statement speaks only as of the date of the particular statement, and we undertake

no obligation to publicly update or revise any forward-looking statements. All non-GAAP financial measure

reconciliations to the most comparative GAAP measure are displayed in quantitative schedules on the company’s

web site at seadrill.com.

2

Seadrill Limited Overview

• Most modern fleet of all the major offshore drillers

• Diverse asset base of 69(1) units

– 34 drillships & semi-submersibles(11 Under Construction)

– 32 jack-up rigs (9 Under Construction)

– 3 tender rigs

• Global reach including harsh environment

• Current market capitalization ~ US$17 bn

• Broad customer base with contract backlog ~ US$20 bn

• Dividend annualized ~ US$1.8 bn

Market Leading Track Record of Value Creation

(1) Includes rigs contributed to Seadrill Partners.3

$0

$4

$8

$12

$16

$20

EquityIssuance

Dividends CurrentMarket Cap

ValueCreation

4

Establishing Vehicles to Offer Exposure to Key Themes

Demonstrated Access to Capital Markets

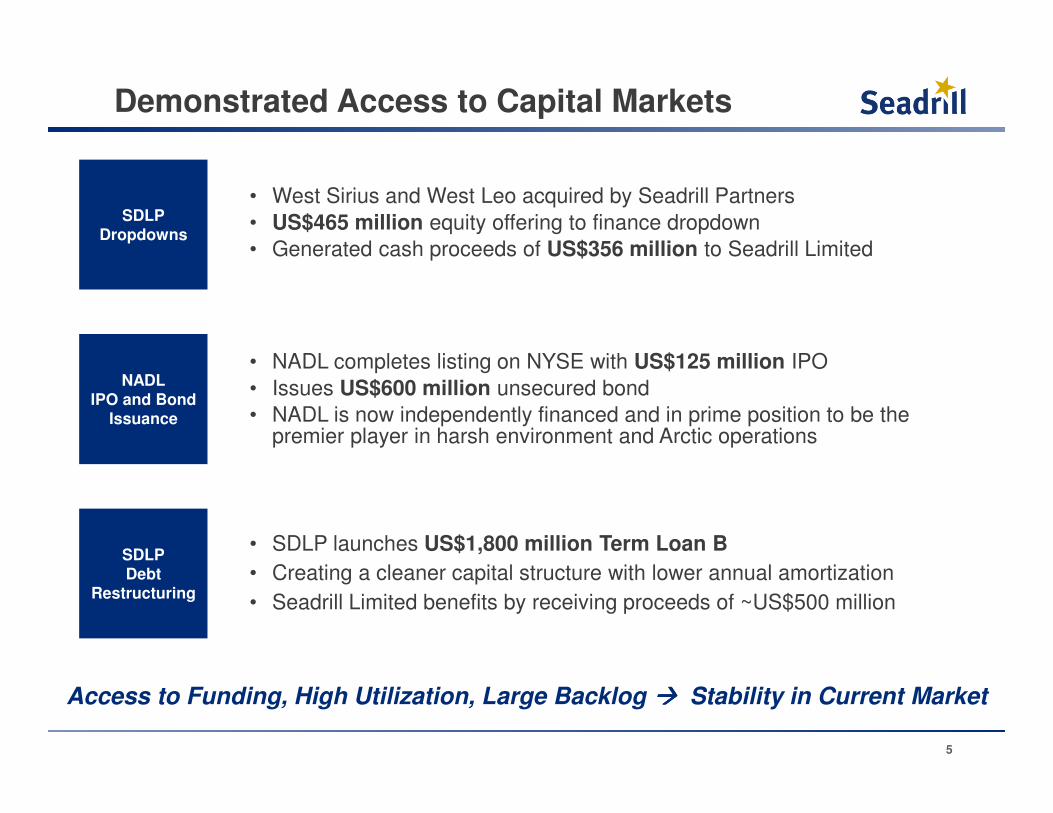

SDLPDropdowns

• West Sirius and West Leo acquired by Seadrill Partners

• US$465 million equity offering to finance dropdown

• Generated cash proceeds of US$356 million to Seadrill Limited

NADLIPO and Bond

Issuance

• NADL completes listing on NYSE with US$125 million IPO

• Issues US$600 million unsecured bond

• NADL is now independently financed and in prime position to be the premier player in harsh environment and Arctic operations

SDLPDebt

Restructuring

• SDLP launches US$1,800 million Term Loan B

• Creating a cleaner capital structure with lower annual amortization

• Seadrill Limited benefits by receiving proceeds of ~US$500 million

Access to Funding, High Utilization, Large Backlog ���� Stability in Current Market

5

Key Investment Highlights

6

Key Investment Highlights

� Significant Contracted Backlog Providing Dividend Visibility

� Innovative Capital Structure and Funding Strategy

Modern Fleet with Exposure to Premium Segments�

� Dividend Growth a Priority… While Maintaining Earnings Growth Profile

7

Global Operational Footprint�

8

Global Operational Footprint

Presence in all important oil and gas regions

Newbuilds 20 units

- 8 Drillships

- 3 Semis

- 1 HE jack-up

- 8 BE jack-ups

Americas12 units

- 4 Drillships

- 2 Semis

- 1 Semi-tender

- 8 Jack-ups

Africa –Middle East15 units

Brazil

North Atlantic

West Africa

Middle East

Asia Pacific

Gulf of Mexico

- 2 Tender rigs

- 8 Jack-ups

Asia Pacific10 units

- 4 HE Semis

- 2 HE Jack-ups

- 1 Drillship

North Atlantic7 units

London

- 2 Drillships- 5 Semis - 5 jack-up

- 5 Semis

Brazil5 units

Strategic Focus on Premium Asset Classes

…with a Modern Fleet…One of the largest Offshore Drillers…

Ultra-Deepwater Units Average Floater Age

Average Jack-Up AgeJack-Up Units

…and Exposure to Premium Segments

% of Jack-Up fleet >350’ Water Depth

% o

f T

ota

l Flo

ate

rs%

of

To

tal F

loa

ters

Nu

mb

er

of

un

its

Nu

mb

er

of

un

its

% Ultra-Deepwater of Total Floaters

Source: ODS Petrodata. 9

Longstanding Relationships with Leading Oil & Gas Companies

Current backlogUS$ Millions

2.9

5.6

4.1

3.2

4.7

1.4

10

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2014 2015 2016 Remaining

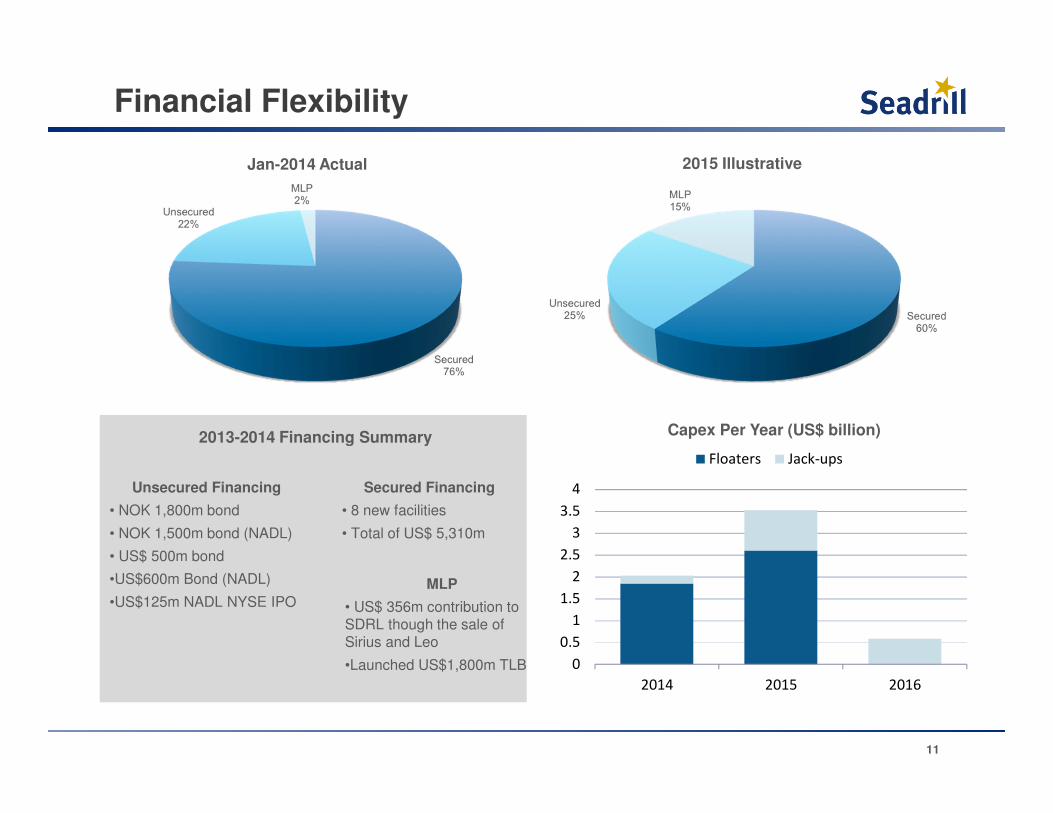

Financial Flexibility

Jan-2014 Actual 2015 Illustrative

11

0

0.5

1

1.5

2

2.5

3

3.5

4

2014 2015 2016

Floaters Jack-ups

Capex Per Year (US$ billion)2013-2014 Financing Summary

Secured Financing

• 8 new facilities

• Total of US$ 5,310m

Unsecured Financing

• NOK 1,800m bond

• NOK 1,500m bond (NADL)

• US$ 500m bond

•US$600m Bond (NADL)

•US$125m NADL NYSE IPOMLP

• US$ 356m contribution to SDRL though the sale of Sirius and Leo

•Launched US$1,800m TLB

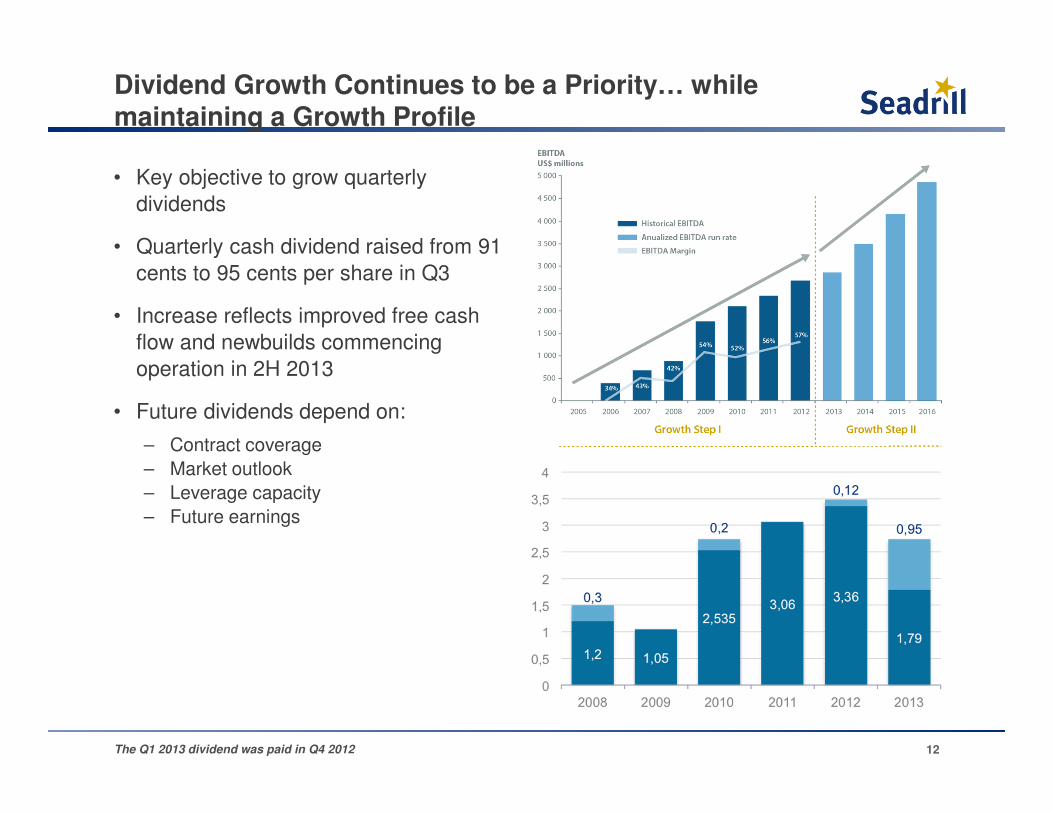

Dividend Growth Continues to be a Priority… while maintaining a Growth Profile

• Key objective to grow quarterly

dividends

• Quarterly cash dividend raised from 91

cents to 95 cents per share in Q3

• Increase reflects improved free cash

flow and newbuilds commencing

operation in 2H 2013

• Future dividends depend on:

– Contract coverage

– Market outlook

– Leverage capacity

– Future earnings

The Q1 2013 dividend was paid in Q4 2012 12

Market Outlook

Upstream Market Outlook

13

Source: IEA, IHS, Wood Mackenzie, EIA, ODS Petrodata.

Increased Service Intensity

400

500

600

700

22

23

24

25

2005 2006 2007 2008 2009 2010 2011 2012 2013

Num

ber

of

Rig

s C

ontr

acte

d

Mill

ion B

arr

els

per

Day

Total Offshore Production Total Offshore Rigs

14

More Rigs Working, but Declining Oil Production

Resources discovered and produced 2000-2012 (Billion boe)

-

20

40

60

80

100

120

140

1980 1985 1990 1995 2000 2005 2013

Shelf Deep Water Ultra deepwater

Discovered resources 1980 to 2013 (Billion boe)

Source: Rystad Energy research and analysis; UCube

Recent Discoveries to Become Produced Volumes

15

Ultra-Deepwater Production Growth Accelerating

16

Global liquids production, by land and water depth

Offshore ultra deep

Onshore

Million bbl/d 2012-2030CAGR = 1.3%

19%

2%

0%

1%

2012-2020CAGR

Source: Rystad Energy

30 mbbl/d

Thousand boe/d

Global offshore productionby water depth 1960 - 2040

16.4

2.5

0.5

0.9

Rep

lacem

en

t R

ati

o

0

10000

20000

30000

40000

50000

60000

70000

80000

1960 1970 1980 1990 2000 2010 2020 2030 2040

Shelf (to 400 ft) Deep water (400-5000 ft) Ultra deepwater (5000+ ft)

30 mbbl/d

16 mbbl/d

5 mbbl/d

16

Near Term Outlook

X-axis: total liquids production mbpd; Y-axis: avg Brent equivalent breakdown price, $/bblSource: Morgan Stanley and Rystad Energy

1

1

2014 Projects Pushed to 2015

• Block 32 � Total – Angola• Mad Dog 2� BP – Gulf of Mexico• Stampede � Hess – Gulf of Mexico• Chevron Indonesia� Chevron – Indonesia • Bonga� 2 rigs - Nigeria

17

Drilling Market Outlook

18

256316

455

60 (50)

189

0

50

100

150

200

250

300

350

400

450

500

Global Rig Supply & Demand Imbalance Favors Contractors

Significant Newbuilds Required to Bridge Expected Demand Gap

Newbuilds2014 - 2016

Current Floater Fleet

PotentialSupply

2020 DemandPossible Retirements

Additional Rig Requirements1

SupplyDemand

1 Includes Brazil rigsSource: Rystad Energy, DNB

3

0 1

8

21 21

28

17 18

2523

12

0

5

10

15

20

25

30

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Ultra-Deep Water Deliveries

19

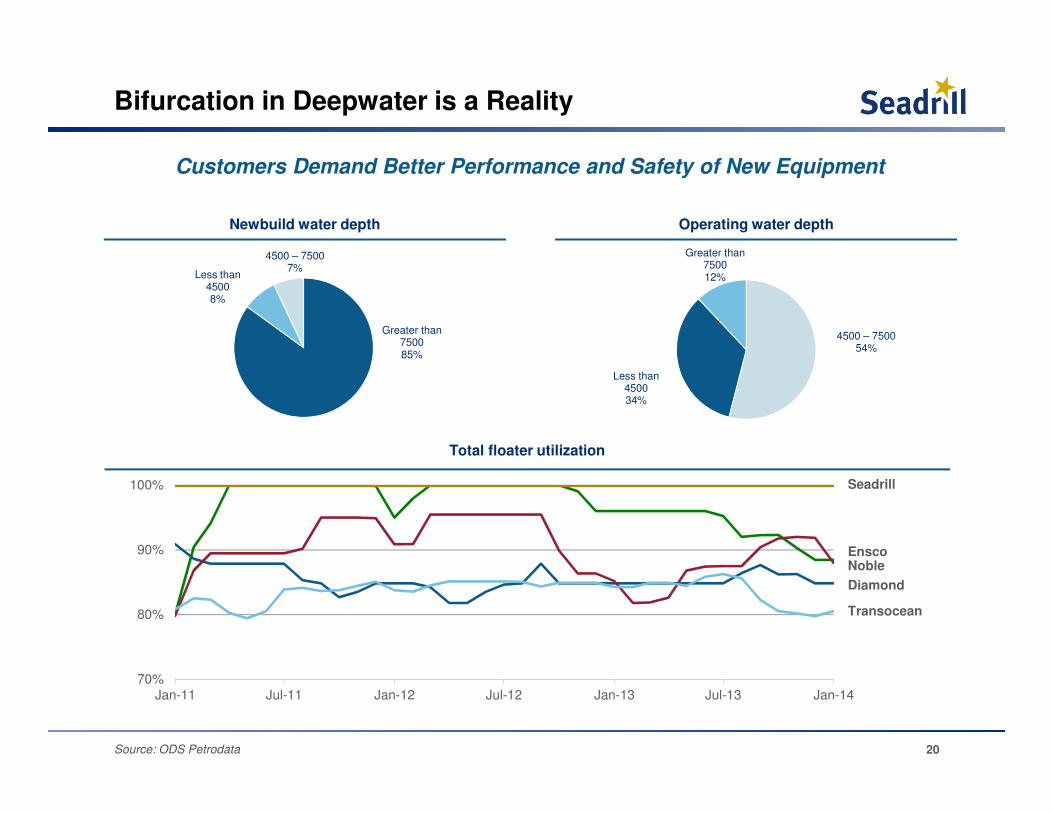

70%

80%

90%

100%

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14

Newbuild water depth Operating water depth

Greater than 750085%

Less than 45008%

4500 – 75007%

Total floater utilization

Seadrill

NobleEnsco

Diamond

Transocean

4500 – 750054%

Less than 450034%

Greater than 750012%

Source: ODS Petrodata

Bifurcation in Deepwater is a Reality

Customers Demand Better Performance and Safety of New Equipment

20

Robust Jack-up Fundamentals

• In 2015 more than 220 of the currently contracted Jack-up fleet will be more than 30 years old

• 90 of the units will be more than 35 years old

• Scrapping & Conversion of older units increased in 2011 and 2012 with trend expected to continue

Age Development of Contracted Jack-up Fleet Jack-ups Removed from the Market

21

1017

26

90

51

67

90

220208

215 220232

0

50

100

150

200

250

2013 2014E 2015E 2020E

40 years or more 35 years or more 30 years or more

# of rigs

1

2

3

6

8

7

10

6

12

2

11

9

8

3

4

2

1 1 1

4

1 1 1 1

4

1

12

15

2

0

2

4

6

8

10

12

14

16

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

# of rigs

Source: Pareto

Conclusion

22

23

Well Positioned to Weather the Storm…..

West Tellus

World oil demand and oil price* by scenario

Illustrative daily liquidity cushion

Floater supply and demand

(1) Based on LTM average for the West Sirius, West Leo, West Aquarius and West Capella(2) Assuming $1,700 million of debt @4.25%(3) Assuming 5% amortization per year(4) Based on average contrat dayrates for West Sirius, West Leo, West Aquarius and West Capella, assumes 95% utilization and 4.25% tax on revenuesSource: Morgan Stanley and Rystad Energy

Seadrill UDW Coverage 2014

(1) (2) (3) (4)(1)

• 32 Ultra-deepwater units built after 2000

• 2 Midwater semi-submersible rigs

• 29 High-specification jack-up rigs built after 2005

• 3 Harsh environment Jack-ups

• 3 Tender Rigs

Core Assets

Financial Investments

12% of SapuraKencana –

Market Value ~US$960mm

50.11% of Sevan Drilling –

Market Value ~US$200mm

39.9% of Archer –

Market Value ~US$245mm

24