currency wars triple dips and politics to dominate 2013

TRANSCRIPT

Currency Wars, Triple‐Dips & Politics to Dominate in the Year of the Snake

13 March 2013

Richard Ramsey Chief Economist Northern Ireland

Slide 2

Depending

on who you talk to things may not that bad…

Source:

The Economist

Muhammed Saeed al-Sahafaka ‘Comical Ali’

Iraqi Information Minister 2003

Slide 3

Global output growth continues…

Global Output - PMI

25

30

35

40

45

50

55

60

65

Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13

Total Manufacturing Services

Source: Markit Economics

ExpansionC

ontraction

Slide 4

US remains the best performer relative to China, UK & EZ

Composite PMIs (Manufacturing & Services ** Excludes Construction**)

35

40

45

50

55

60

65

Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13

Eurozone US (ISM) China UK

Source: Markit Economics

ExpansionC

ontraction

Slide 5March 14, 2013 – Page 5 © Ulster Bank

The biggest threat to growth & financial markets is / was….sovereign debt dominos….

?

Slide 6

Investor sentiment in sovereign debt markets has improved since Draghi’s

‘Whatever it takes’

8-Yr Govt Bond Yields

2

4

6

8

10

12

14

16

18

Dec-09

Mar-10

Jun-1

0Sep

-10Dec

-10Mar-

11Ju

n-11

Sep-11

Dec-11

Mar-12

Jun-1

2Sep

-12Dec

-12Mar-

13%

Source: Bloomberg

Slide 7

Debt Mountain still has to be conquered and that applies to the US too

Source:

The Economist

Slide 8

The fiscal challenges in the Eurozone remain…

Euro Area Budget Balances 2012,% of GDP

-9-8-7-6-5-4-3-2-1

-

German

yFinl

and

Estonia

Luxe

mbourg

Malta

Italy

Austria

Belgium

Netherl

ands

Sloven

iaFran

ceCyp

rus

Slovak

Rep

ublic

Portug

alSpa

inGree

ceIre

land

Source: IMF, Dept of Finance

Euro Area Debt Levels 2012,% of GDP

-20406080

100120140160180

Greece Italy

Portug

alIre

land

Belgium

Spain

France

Cyprus

German

yAus

triaMalt

aNeth

erlan

dsSlov

enia

Finlan

d

Slovak

Rep

ublic

Luxe

mbourg

Estonia

Source: IMF, Dept of Finance

Slide 9

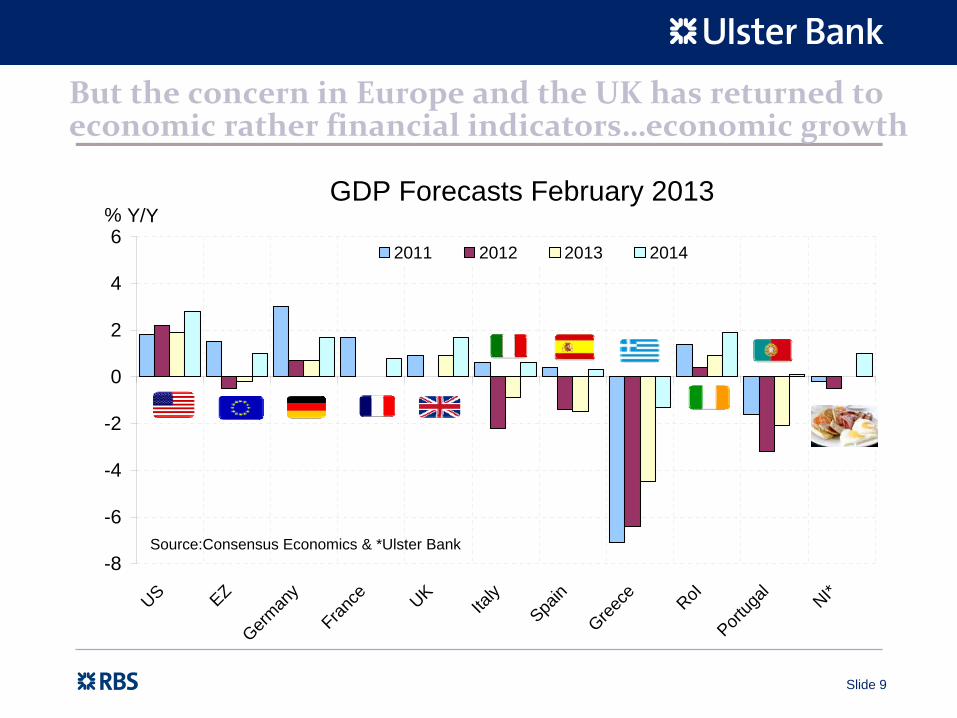

But the concern in Europe and the UK has returned to economic rather financial indicators…economic growth

GDP Forecasts February 2013

-8

-6

-4

-2

0

2

4

6

US EZGerm

any

France UK

Italy

Spain

Greece RoI

Portug

al NI*

% Y/Y

2011 2012 2013 2014

Source:Consensus Economics & *Ulster Bank

Slide 10

Recovery well under way in some economies –

focus on levels of GDP

not just growth rates

Recession & Recoveries (% GDP Change Since Pre-Recession Peak as of Q4 2012*)

+2.4%

-3.0%

-3.3%

-7.7% or -9.5% using GNP

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21Time in Quarters, Pre-Recession GDP Peak = 0

US EZ UK RoI

Source: Bloomberg, *RoI as of Q3 2012

Slide 11

Last year saw Portugal, Italy, Spain & Greece continue to contract at a rapid rate

Recession & Recoveries (% GDP Change Since Pre-Recession Peak as of Q4 2012)

-6.7%

-7.7%

-6.6%

-1.1%

-7.7%

+1.4%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Time in Quarters, Pre-Recession GDP Peak = 0

Portugal Ireland Italy Spain Germany France

Source: Bloomberg & UB Calculations @ -20%

Slide 12

The 2nd, 3rd

& 4th

largest economies within the eurozone are contracting at a rapid rate in 2013

Composite PMIs (Manufacturing & Services ** Excludes Construction**)

30

35

40

45

50

55

60

65

Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13

Source: Markit Economics PMIs

Contraction

Expansion

Slide 13

After Greece, France & Italy post steepest falls in manufacturing output. Denmark posts strongest gain

PMIs: Manufacturing Output February 2013

35 40 45 50 55 60 65

GreeceFrance

ItalyIsrael**

AustraliaSpain

EZJapan

EUSingapore

AustriaPoland

VietnamUK

S.KoreaCzech

IndonesiaNetherlands

TaiwanGermany

ChinaIreland

CanadaGlobal

South AfricaNI

RussiaTurkey

BrazilMexico

IndiaSwitzerland

USN.Zealand*

Denmark

Source: Markit Economics Output Indices, * January, **December

NI, RoI & UK

Slide 14

It’s a similar story when it comes to services

PMIs: Services Output February 2013

40 45 50 55 60

ItalyFranceSpain

NIEZ

AustraliaEU

JapanUK

ChinaBrazil

Emerging MarketsGlobalIreland

IndiaGermany

RussiaUS*

Source: Markit Economics Output Indices, * US Non-manufacturing which is wider than services

€

March / April 2012

‘The Psycho-Dwarf’’

April / May 2012 November 2012

France hitting the headlines for the wrong reasons

Slide 16

Les Misérable economy needs an economic revolution

•

U‐Rate 10.6% Q4 2012 (7.5% Q1 2008)

•

<25yrs U‐Rate 25.2% Q4 2012 (17.2% Q1 2008 & 5.9% Q1 1975)

•

Employment Rate 51.1% (Male 56% & Female 46.6%)

•

Corporation tax rate 33.3% (EU average 20.5%)

Key Facts

Starring Francois Hollande

Slide 17

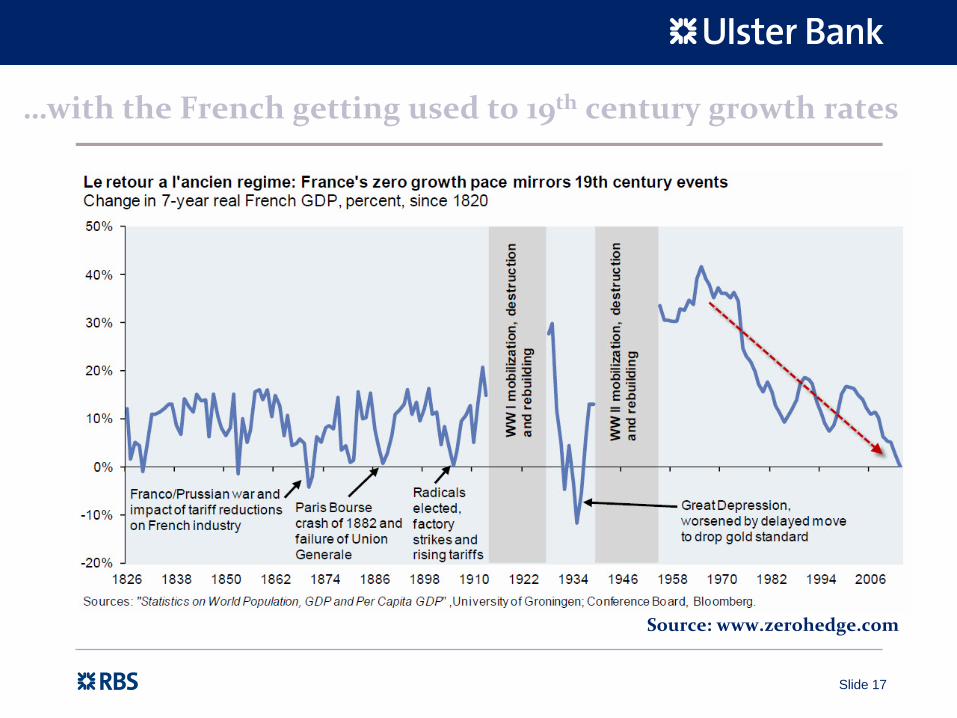

…with the French getting used to 19th

century growth rates

Source: www.zerohedge.com

Slide 18Slide 18

‘The Grizz’ blasts French work ethic

Maurice ‘The Grizz’

Taylor

Chairman of Titan International, a US tyre giant asked by the French government to take over a Goodyear

plant in France.

“The French worker can be as productive as anyone else when he

works, but he is not working”

“The French workers are paid high wages but only work three

hours….they get one hour for breaks & lunch, talk for three hours and

work for three”.

“In five years, Michelin won’t be producing tyres in France. You can

keep your so‐called workers”.

Comments made February 2013

Slide 19

Hollande must turn right and left!

Source: The Economist, 16 February 2013Source: The Economist, 16 February 2013

The Self Preservation Society or Grand Coalition?The Self Preservation Society or a Grand Coalition?

€ € €€

‘Rigor Montis’

the Technocrat

The Comedian‘Dead man talking’

‘The Psycho-Dwarf’’

Slide 21

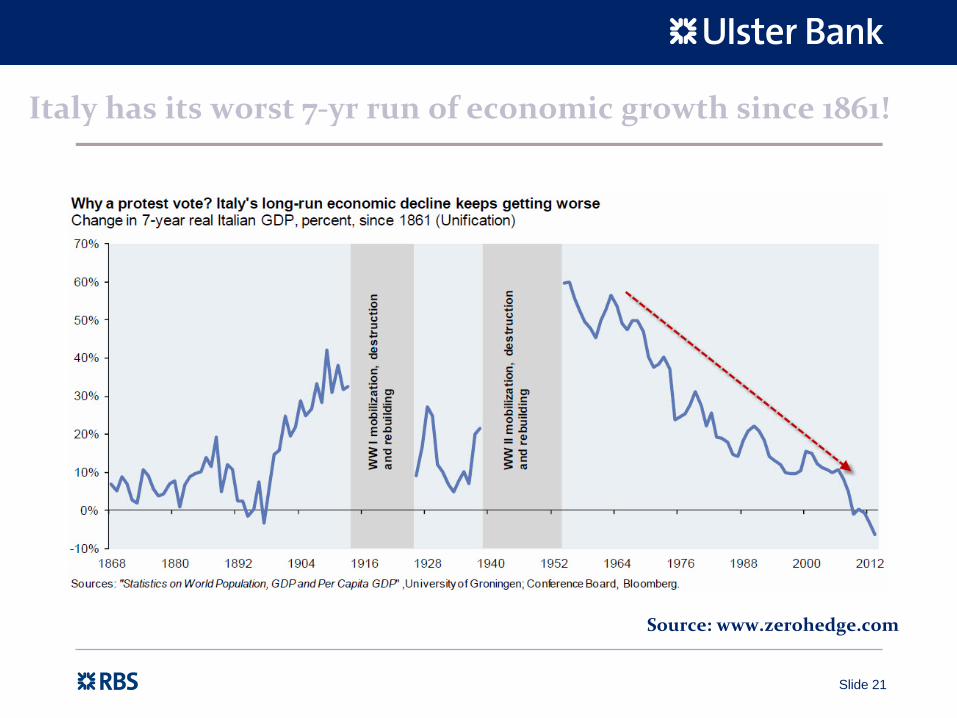

Italy has its worst 7‐yr run of economic growth since 1861!

Source: www.zerohedge.com

Slide 22

Italy not in great shape either, particularly the labour market

•

U‐Rate 11.7% Jan‐2013 (5.8% Apr‐07)

•

<25yrs U‐Rate 38.7% Jan‐2013 (17.2% Q1 2008 & 5.9% Q1 1975)

•

Employment Rate 51.1% (Male 56% & Female 46.6%)

•

Corporation tax rate 31.4% (EU average 20.5%)

Key Facts

Big political risk for Eurozone as a whole

Slide 23

Italy has overtaken Portugal and its Youth unemployment is where Greece was 2 years ago

€€

Source: www.zerohedge.com

Slide 24Slide 24

No quick‐fix – the ‘Juncker Conundrum’

“We all know what we need to do, we just don’t know how to get re‐elected after doing it”

Jean‐Claude Juncker – Former President of the Euro Group (January 2005 – January

2013)

& current Luxembourg Prime Minister. Quote November 2012.

Slide 25

Italy has overtaken Portugal and its Youth unemployment is where Greece was 2 years ago

€€

Source: www.zerohedge.com

Slide 26

The eurozone is also at a distinct advantage with its currency & outbreak of currency wars

Euro / Yen Exchange Rate

80

100

120

140

160

180

Mar-07 Nov-07 Jul-08 Mar-09 Nov-09 Jul-10 Mar-11 Nov-11 Jul-12 Mar-13

Yen per

Source: Bloomberg

€

Yen weakening / Euro strengthening

Yen strengthening / Euro weakening

Sterling / Euro Exchange Rate

1.1434

1.0

1.1

1.2

1.3

1.4

1.5

1.6

Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

€

Source: Bloomberg

2009/10€1.13

2008/09€1.20

2007/08€1.41

2010/11€1.18

2011/12 €1.16 (86.3p)

Slide 27

German & South Korean brands have gained market share since 2007. But so too have brands built in the UK

Change (PP) in Market Share in EU New Car Sales* 2007-2012

-3 -2 -1 +0 +1 +2 +3

VolkswagenNissan

HyundaiAudi

KiaDaciaBMW

SkodaMini

Land RoverVolvo

MercedesChevrolet

Alfa RomeoSeat

PeugeotFord

CitroenSuzukiMazdaHonda

RenaultFiat

Opel (GM)Toyota

Percentage Point Change

Source: ACEA, *flags denote nationality of manufacturer

Land Rover, Mini & Nissan are built in the

UK so +ve for UK economy

Seat's dominance in Spanish market, & severe downturn in

Spain explains brands declining

market share

Slide 28

French & Italian brands losing significant market share in 2012 as their domestic economies battle recession

Change (PP) in Market Share in EU New Car Sales* 2011-2012

-1.5 -1.0 -0.5 +0.0 +0.5 +1.0

AudiHyundai

KiaVW

BMWSkoda

MercedesLand Rover

ToyotaChevrolet

NissanDaciaJeepMini

HondaJaguarLexus

GM (US)Lancia/Chrysler

SmartVolvo

MazdaSuzuki

SeatMitsubishi

Alfa RomeoCitroen

PeugeotFiat

FordOpel / Vauxhall

Renault

Percentage Point Change

Source: ACEA, *flags denote nationality of manufacturer

Jaguar, Land Rover, Mini & Nissan are built in the UK so +ve for

UK economy

French, Spanish (Seat German owned) & Italian brands suffering as their

domestic economies battle with recession

Slide 29Slide 29

UK Economy…from Triple A to Triple‐Dip?

Source: Financial Times 12th

March 2013

Slide 30

UK composite PMI suggests Q1 2013 GDP growth will be marginal at best

UK GDP versus UK Composite PMI

25

30

35

40

45

50

55

60

65

2007 Q1 2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1*

PMI Index

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5GDP Q/Q

GDP Q/Q PMI PMI No Change

Source: ONS & Markit Economics, * refers to January & February

Slide 31

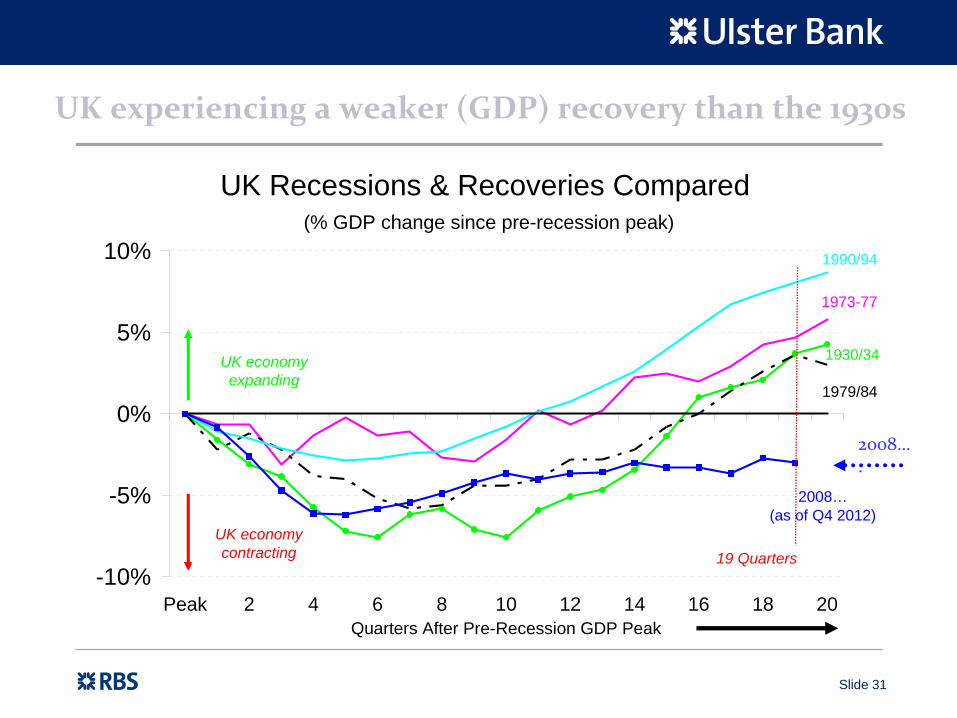

UK experiencing a weaker (GDP) recovery than the 1930s

UK Recessions & Recoveries Compared (% GDP change since pre-recession peak)

1930/34

1973-77

1979/84

1990/94

2008… (as of Q4 2012)

-10%

-5%

0%

5%

10%

Peak 2 4 6 8 10 12 14 16 18 20Quarters After Pre-Recession GDP Peak

UK economy contracting 19 Quarters

UK economy expanding

2008…

.

Slide 32

A lack of a consumer recovery explains the UK’s poor performance…

UK GDP by Expenditure Category(% Change Since Pre-Recession Peak Q1 2008)

-3.6%

+0.8%

+4.7%

-12%-10%-8%-6%-4%-2%0%2%4%6%8%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19Time in Quarters, Pre-Recession GDP Peak = 0

Household Final ConsumptionExports (Goods & Services)General Government Consumption Expenditure

Slide 33

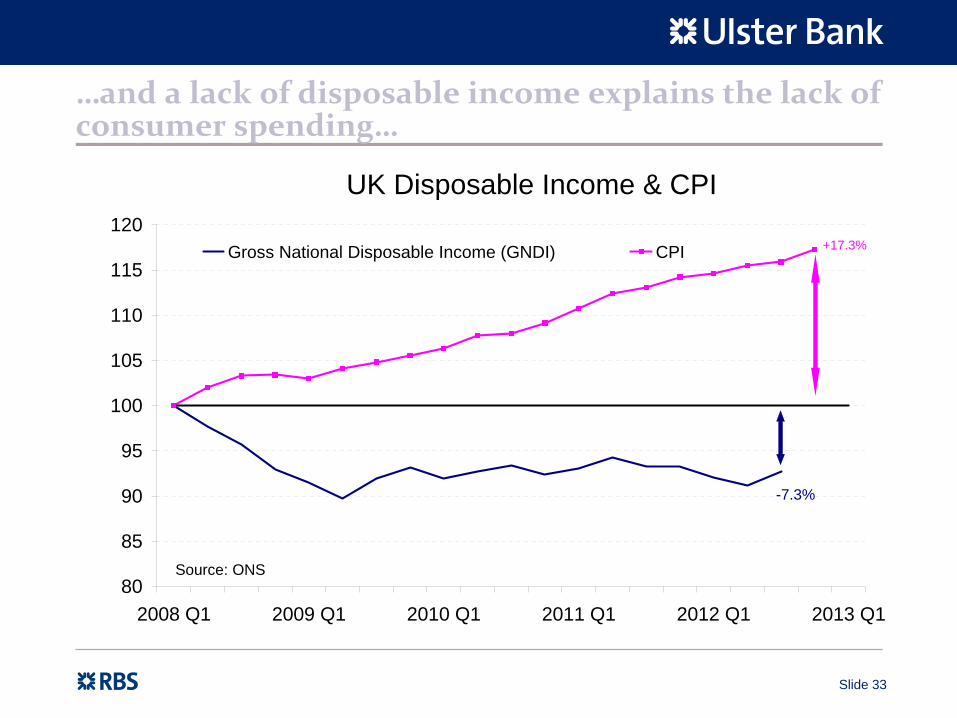

…and a lack of disposable income explains the lack of consumer spending…

UK Disposable Income & CPI

-7.3%

+17.3%

80

85

90

95

100

105

110

115

120

2008 Q1 2009 Q1 2010 Q1 2011 Q1 2012 Q1 2013 Q1

Gross National Disposable Income (GNDI) CPI

Source: ONS

Slide 34

With inflation set to go higher, UK consumer likely to remain on strike…UK CPI (annual average) above 2% for 10 years!!

CPI inflation projection based on market interest rate expectations & £375 billion asset purchases

3 years of an overshoot

Source: BoE QIR February 2013

CPI inflation projection based on market interest rate expectations & £375 billion asset purchases

3 years of an overshoot

Source: BoE QIR February 2013

CPI inflation projection based on market interest rate expectations & £375 billion asset purchases

3 years of an overshoot

Source: BoE QIR February 2013

Slide 35

Weak sterling good for exports but UK struggling from weak demand in core export markets

UK Exports of Goods*

12% below pre-downturn high

44% above 2009 low & 22% below

pre-downturn level

80

90

100

110

120

130

140

2006 Q4 2007 Q4 2008 Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q4

Index 2009 = 100

EU Non-EU Total

Source: ONS,Excludes Oil & Erratics

Slide 36

Contrast UK performance with the RoI. Consumer downturn not as bad but export recovery not as good…

RoI GNP by Expenditure Category(% Change Since Pre-Recession GNP Peak Q1 2007)

-6.3%

+9.8%

-18%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

0 2 4 6 8 10 12 14 16 18 20

22

Time in Quarters, Pre-Recession GDP Peak = 0

Personal Consumption ExpenditureExports (Goods & Services)General Government Consumption Expenditure

Slide 37

Ireland is a small & extremely open economy…

Ireland UK Germany US Port Greece Spain

Consumption 53 66 58 71 68 70 57Govt Spending 17 23 20 20 21 20 21Investment 12 15 17 12 19 16 24Exports 101 29 49 13 33 21 23Imports 82 33 43 17 41 27 26GDP 100 100 100 100 100 100 100

GDP Breakdown, % of Total

Slide 38Slide 38

UK loses ‘Triple‐A’

rating….So what?

10-Yr Government Bond Yields

0

1

2

3

4

5

6

Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13

Interest Rate %

Reflects the cost (interest rate) of Government borrowing

Source:Bloomberg

Moody's downgrade

Slide 39

UK recovery more evident within the labour market

UK Workforce Jobs

31.945

32.083

30.8

31

31.2

31.4

31.6

31.8

32

32.2

Sep-05 Sep-06 Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12

Millions

Source: ONS

After 2.6% PTT fall employment

0.4% below peak

UK, NI & RoI Unemployment Rates

NI & UK 7.8%

14.1%

3%

5%

7%

9%

11%

13%

15%

Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

NI UK RoI

Source: ONS, Labour Force Survey & CSO Live Register

Slide 40Slide 40

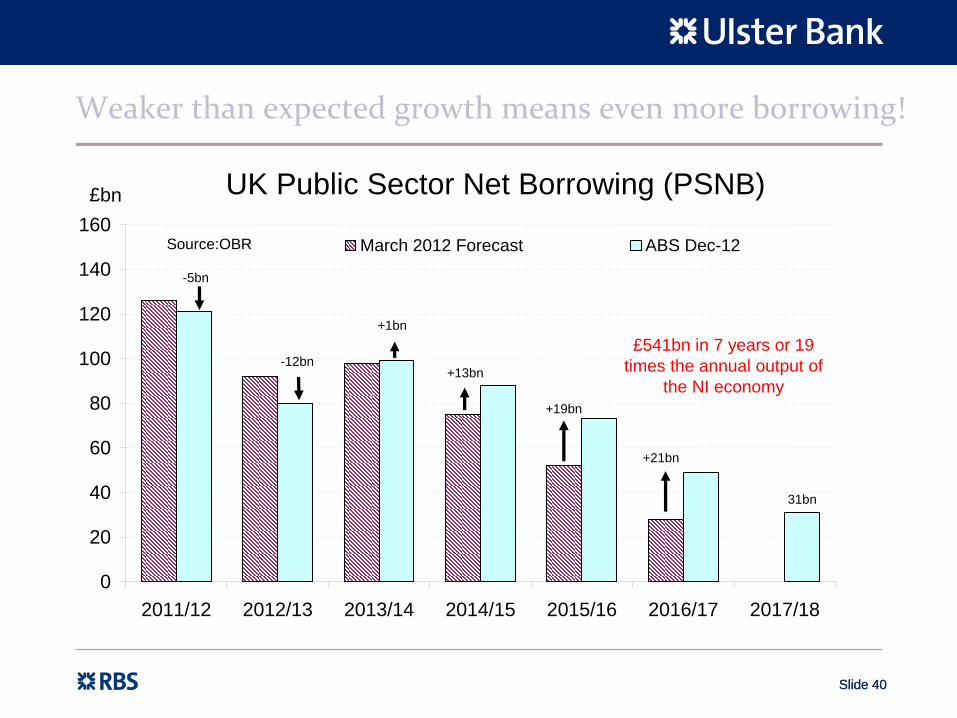

Weaker than expected growth means even more borrowing!

UK Public Sector Net Borrowing (PSNB)

31bn

+21bn

+19bn

+13bn

+1bn

-12bn

-5bn

0

20

40

60

80

100

120

140

160

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

£bn

March 2012 Forecast ABS Dec-12Source:OBR

£541bn in 7 years or 19 times the annual output of

the NI economy

Slide 41Slide 41

Almost £170bn more than what UK Government first expected

UK Public Sector Net Borrowing (PSNB)

+5bn

-9bn

+39bn

+51bn

+28bn+53bn

0

20

40

60

80

100

120

140

160

2011/12 2012/13 2013/14 2014/15 2015/16 2016/17 2017/18

£bn

June 2010 Forecast ABS Dec-12Source:OBR

£169bn additional borrowing required over 6 years or £198bn over 7 years

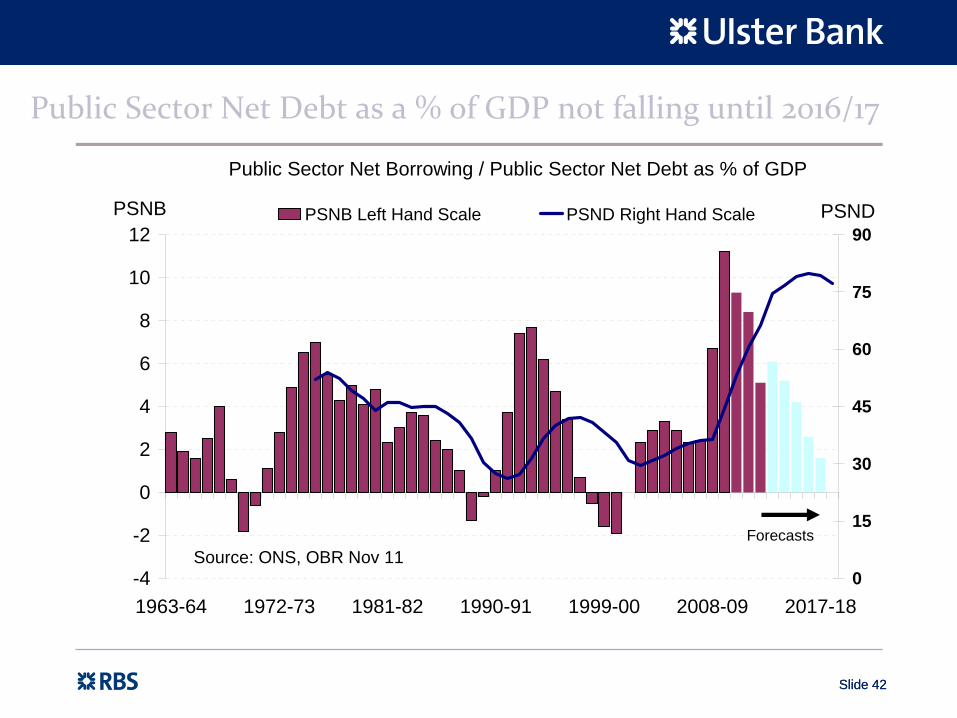

Slide 42Slide 42

Public Sector Net Debt as a % of GDP not falling until 2016/17

Public Sector Net Borrowing / Public Sector Net Debt as % of GDP

-4

-2

0

2

4

6

8

10

12

1963-64 1972-73 1981-82 1990-91 1999-00 2008-09 2017-18

PSNB

0

15

30

45

60

75

90PSNDPSNB Left Hand Scale PSND Right Hand Scale

ForecastsSource: ONS, OBR Nov 11

Slide 43Slide 43

Meanwhile 12‐yr public spending feast followed by 7‐year famine

UK Public Spending Growth in Real Terms (excluding Debt Interest & Social Security)

-10%

-5%

0%

5%

10%

15%

1951-52 1962-63 1973-74 1984-85 1995-96 2006-07 2017-18

Y/Y

Source: IFS February 2013

We are here

17% cut in 7yrs over 60% of Departmental cuts have been made

Slide 44Slide 44

And how is the Northern Ireland economy doing….

N.Ireland downturn by numbers 10 Facts1.

Unemployment (claimant count) up 41,500 (Jan 2013)

2.

Workforce jobs have fallen by almost 55,000 in 4 yrs to June 2012

3.

Personal insolvencies have doubled since 2007 & still rising

4.

Corporate insolvencies have doubled since 2007 & still rising

5.

House prices down 56% from peak (by Q4 2012)

6.

House completions down 66% from 2006 peak & still falling

7.

Mortgages for home movers at lowest level since 1974

8.

Almost 1 in 4 retail outlets are vacant in Belfast

9.

New car sales have fallen by one third relative to 2007

10.

Consumer prices (UK CPI) up 19% since August 2007

Slide 46Slide 46

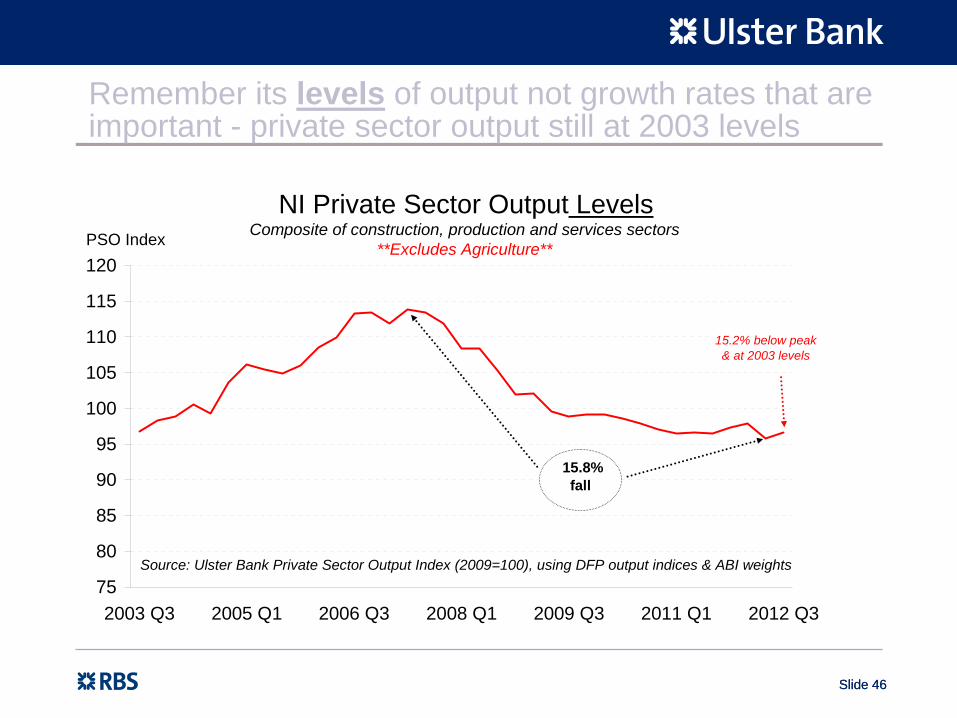

Remember its levels of output not growth rates that are important - private sector output still at 2003 levels

NI Private Sector Output LevelsComposite of construction, production and services sectors

**Excludes Agriculture**

75

80

85

90

95

100

105

110

115

120

2003 Q3 2005 Q1 2006 Q3 2008 Q1 2009 Q3 2011 Q1 2012 Q3

PSO Index

Source: Ulster Bank Private Sector Output Index (2009=100), using DFP output indices & ABI weights

15.8%fall

15.2% below peak & at 2003 levels

Slide 47

Services sector output has now been below its pre- downturn peak for 24 quarters or 6 years

NI Private Sector Output Relative to Pre-Recession PeaksAs of Q3 2012 (Peak = 0)

-15.2%

-11.8%-13.6%

-42.3%

-50%

-40%

-30%

-20%

-10%

0%

10%

0 2 4 6 8 10 12 14 16 18 20 22 24Time in Quarters Since Pre-Recession Output Peak

Total Private Sector Output Private Sector Services Industrial Production Construction

Slide 48

‘Winners’ during the downturn…

Slide 48

Industrial Group % Change

Recession Winners ↑↑↑

Other Services 50.0%

Chemicals & Pharmaceutical Products 26.8%

Utilities (Electricity & Gas) 10.1%

Transport, Storage & Communications 7.3%

Food, Drink & Tobacco 5.8%

Wholesale & Retail Distribution, Accommodation & Food Service 1.2%

Agriculture (Gross annual output in real terms 2007‐11) 0.5%

Source: DFP Indices of Production, Services and Construction, DARD & Ulster Bank calculations

Change in NI Private Sector OutputQ2 2007 ‐ Q3 2012

Slide 49

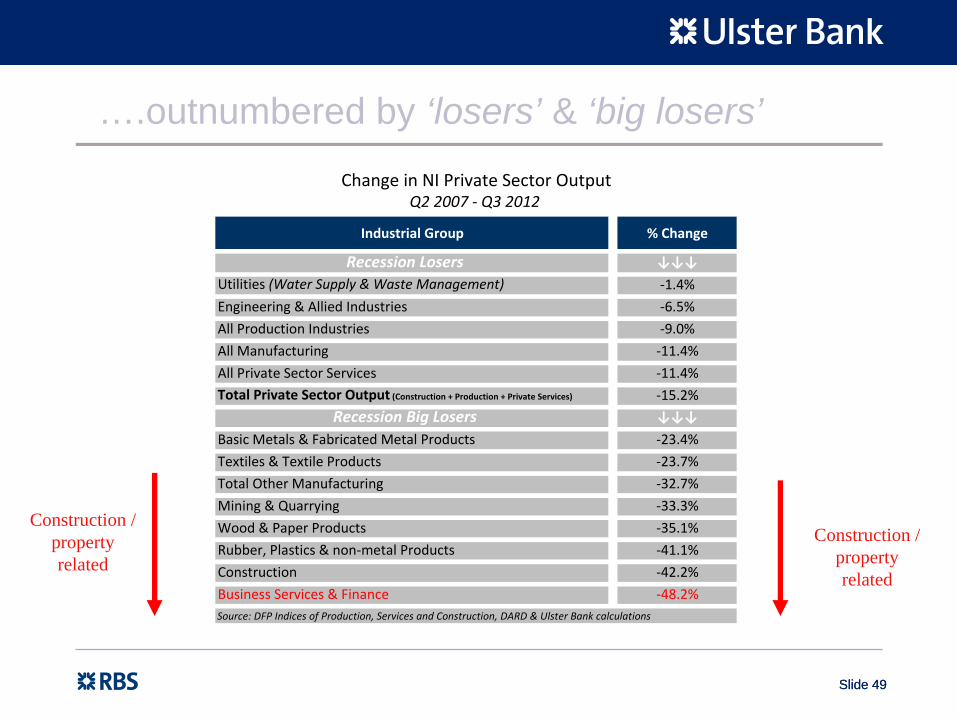

….outnumbered by ‘losers’ & ‘big losers’

Slide 49

Construction / property related

Construction / property related

Industrial Group % Change

Recession Losers ↓↓↓Utilities (Water Supply & Waste Management) ‐1.4%

Engineering & Allied Industries ‐6.5%

All Production Industries ‐9.0%

All Manufacturing ‐11.4%

All Private Sector Services ‐11.4%Total Private Sector Output (Construction + Production + Private Services) ‐15.2%

Recession Big Losers ↓↓↓

Basic Metals & Fabricated Metal Products ‐23.4%

Textiles & Textile Products ‐23.7%

Total Other Manufacturing ‐32.7%

Mining & Quarrying ‐33.3%

Wood & Paper Products ‐35.1%

Rubber, Plastics & non‐metal Products ‐41.1%

Construction ‐42.2%

Business Services & Finance ‐48.2%Source: DFP Indices of Production, Services and Construction, DARD & Ulster Bank calculations

Change in NI Private Sector OutputQ2 2007 ‐ Q3 2012

Slide 50Slide 50

Recent investments in 2011/12 – dominated by ‘the worst performing sector’

business services & finance

Source: Invest NI

Jobs Areas

501 IT Development, FX securities/settlement, Legal & Compliance

106 Marketing

317 HR, Finance, Legal

359 FS IT Development, Service Delivery, Project Management

90 FS IT Development, Project Management

242 R&D Product Development, Sales, Marketing

45 HR Consulting, Risk and Actuarial – Pensions management

50 IT Development

104 IT Development, Product Development, Engineering

85 IT Development, Project Management

297 Call Centre, Customer Service and Management

109 IT Development, Product Development, Sales

130 R&D Product Development, Engineering

102 Legal

Jobs Areas

501 IT Development, FX securities/settlement, Legal & Compliance

106 Marketing

317 HR, Finance, Legal

359 FS IT Development, Service Delivery, Project Management

90 FS IT Development, Project Management

242 R&D Product Development, Sales, Marketing

45 HR Consulting, Risk and Actuarial – Pensions management

50 IT Development

104 IT Development, Product Development, Engineering

85 IT Development, Project Management

297 Call Centre, Customer Service and Management

109 IT Development, Product Development, Sales

130 R&D Product Development, Engineering

102 Legal

In the last 10 years

78% of new FDI jobs

have been in

business & financial

services and

software

Slide 51

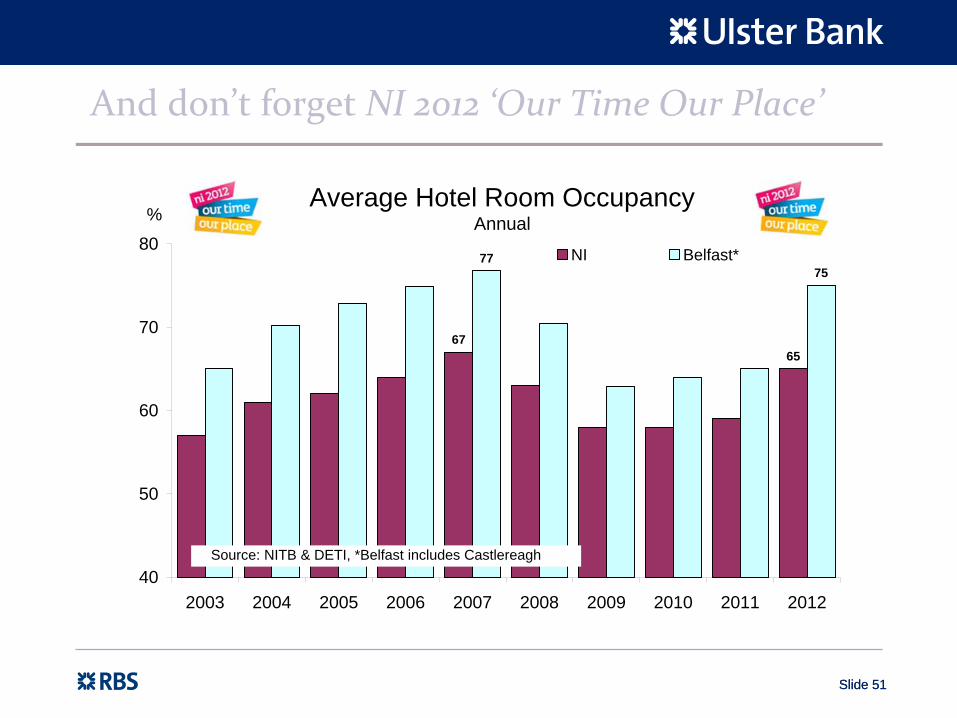

And don’t forget NI 2012 ‘Our Time Our Place’

Slide 51

Average Hotel Room Occupancy Annual

6765

7775

40

50

60

70

80

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

%

NI Belfast*

Source: NITB & DETI, *Belfast includes Castlereagh

Slide 52

UK workforce jobs are just 0.5% below their June 2008 peak whereas NI has not recouped any of its job losses

NI & UK Workforce Jobs (as of June 2012)

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

June 2008 Peak to Trough Recovery from Trough Net Position Relative toJune 2008 Peak

NI UK

Source: DFP & NOMIS, June annual figures

Slide 53

Apart from manufacturing, NI’s job losses have been more severe than in the UK

Employee Jobs Q3 2012 relative to recent peaks

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Construction Manufacturing Services Total

NI UK NI Peak Q4 2007

NI Peak Q2 2007

NI Peak Q2 2008 NI Peak Q2 2008

Source: DFP & NOMIS

Slide 54

No meaningful jobs recovery outside of manufacturing

Northern Ireland Employment (Employee Jobs)

-40%

-30%

-20%

-10%

0%

10%

All Sectors Services Manufacturing Construction

Peak to Trough Recovery from Trough Q3 2012 Relative to Peak

Source: DFP, QES

Slide 55

Demand in NI remains weak in 2013 but pace of decline has eased…

Private Sector Business Activity - PMIs

30

35

40

45

50

55

60

65

Feb-04 Aug-05 Feb-07 Aug-08 Feb-10 Aug-11 Feb-13

NI UK RoI

Source: Markit & Ulster Bank NI PMI: 50 = threshold between expansion / contraction

Expansion

Contraction

**PMI Surveys Exclude Agriculture & Public Sector**

Slide 56

… lack of demand still a problem for jobs

NI PMI - Employment Index 3 month moving average

25

30

35

40

45

50

55

60

65

Feb-04 Feb-05 Feb-06 Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13

Manufacturing Services Construction

Source: Markit Economics & Ulster Bank NI PMI

Job Gains

Job Losses

Slide 57

NI enjoyed Southern Comfort through the Celtic Tiger years

WealthTrade Tourism Investment WealthWealthTradeTrade TourismTourism InvestmentInvestment

Slide 58

Eurozone’s

fastest growing economy was on NI’s doorstep. But what went up ……

•

ISEQ +101% & +231% (5yr/10yr prior to Feb‐2007 peak)

•

House Completions +68% / +162% (5yr/10yr prior to 2006 peak)

•

Unemployment rate 4.6%

(average 1998‐2007)

& 33% rise in employment

(Q3 1998 – Q3 2007)

•

Annual GDP growth 6.7% (1998‐2007; averaged 5% 2002‐2007)

•

House prices +269% (10 years prior to Sep‐2007 peak)

•

NI manufacturing exports to RoI +81% (6 years to 2007/08)

Slide 59

TradeTourism Wealth

InvestmentTradeTrade

TourismTourism WealthWealthInvestmentInvestment

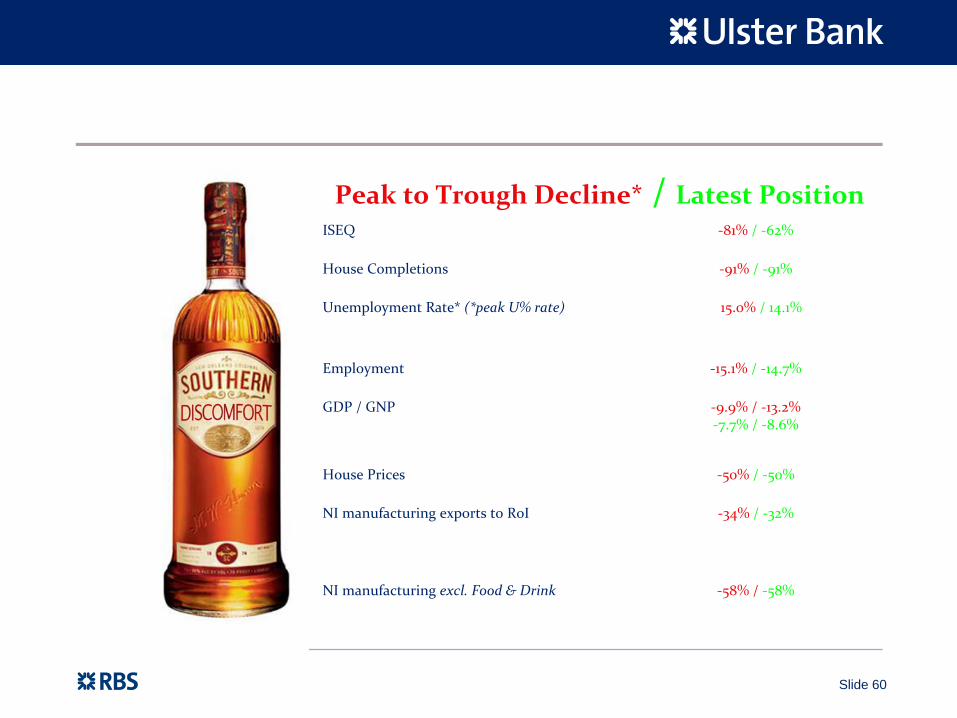

Slide 60

ISEQ ‐81% / ‐62%

House Completions ‐91% / ‐91%

Unemployment Rate* (*peak U% rate) 15.0% / 14.1%

Employment ‐15.1% / ‐14.7%

GDP / GNP ‐9.9% / ‐13.2%

‐7.7% / ‐8.6%

House Prices ‐50% / ‐50%

NI manufacturing exports to RoI ‐34% / ‐32%

NI manufacturing excl. Food & Drink ‐58% / ‐58%

Peak to Trough Decline*

/ Latest Position

Slide 61

Inflationary Pressures & Declining Disposable Incomes

Challenge

Slide 62

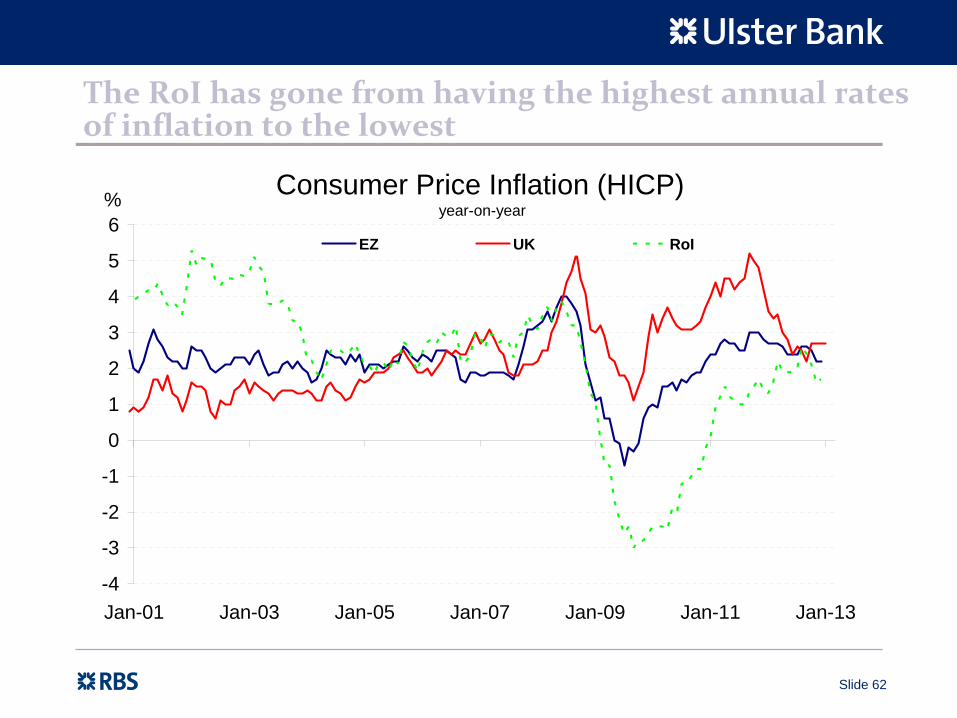

The RoI has gone from having the highest annual rates of inflation to the lowest

Consumer Price Inflation (HICP) year-on-year

-4

-3

-2

-1

0

1

2

3

4

5

6

Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13

%

EZ UK RoI

Slide 63

Ireland has become the poster child of low inflation with the UK experiencing the highest rises outside of Eastern Europe

EU-27 Cumulative % Rise in Consumer Prices (HICP) August 2007 to December 2012 / January 2013*

0% 5% 10% 15% 20% 25% 30% 35% 40%

Romania Hungary

Lithuania Estonia

Latvia Bulgaria Poland

UK Greece Finland

Slovakia Italy

Slovenia Cyprus

LuxembourgEU 27 Spain

Belgium Czech Republic

Austria Denmark

MaltaNetherlands

SwedenEZ

Portugal France

Germany Ireland

Source: ONS, CSO, *January 2013 only for EZ & UK, all others December

€

Slide 64

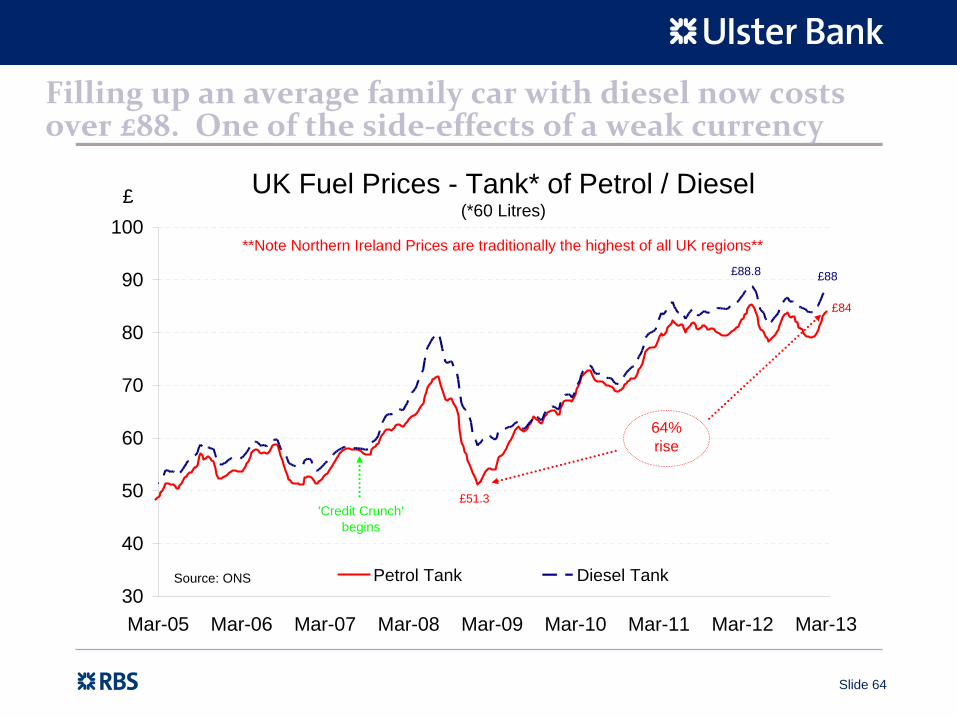

Filling up an average family car with diesel now costs over £88. One of the side‐effects of a weak currency

UK Fuel Prices - Tank* of Petrol / Diesel (*60 Litres)

£51.3

£84

£88.8 £88

30

40

50

60

70

80

90

100

Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13

£

Petrol Tank Diesel Tank

64% rise

Source: ONS

**Note Northern Ireland Prices are traditionally the highest of all UK regions**

'Credit Crunch' begins

Slide 65

Drinking, smoking & eating have become expensive pastimes particularly after duty rises – past, present & future

UK v RoI Cumulative % Change in Consumer Prices since 'Credit Crunch' began (Aug 2007 to January 2013)

18.8%

0%

10%

20%

30%

40%

50%

60%

Food & Non-Alcoholic

Beverages

Food ElectricityGas & Other

Fuels

TransportFuels &

Lubricants

TransportServices

All CPI

UK RoISource: ONS & Eurostat

Slide 66

EU 27 Cumulative % Rise in Food & Drink Prices August 2007 to December 2012 (HICP)

0% 5% 10% 15% 20% 25% 30% 35% 40%

HungaryUK

MaltaLatvia

LithuaniaEstonia

RomaniaPoland

BulgariaFinland

Czech RepublicSloveniaDenmark

CyprusSlovakia

AustriaBelgium

EU 27Luxembourg

SwedenGermany

NetherlandsItalyEZ

GreeceFranceSpain

PortugalIreland Source: ONS, CSO & Eurostat

€

After Hungary, the UK has posted the largest rise in food & drink prices (& the RoI the least)

within the EU‐27 since Aug‐07

Slide 67

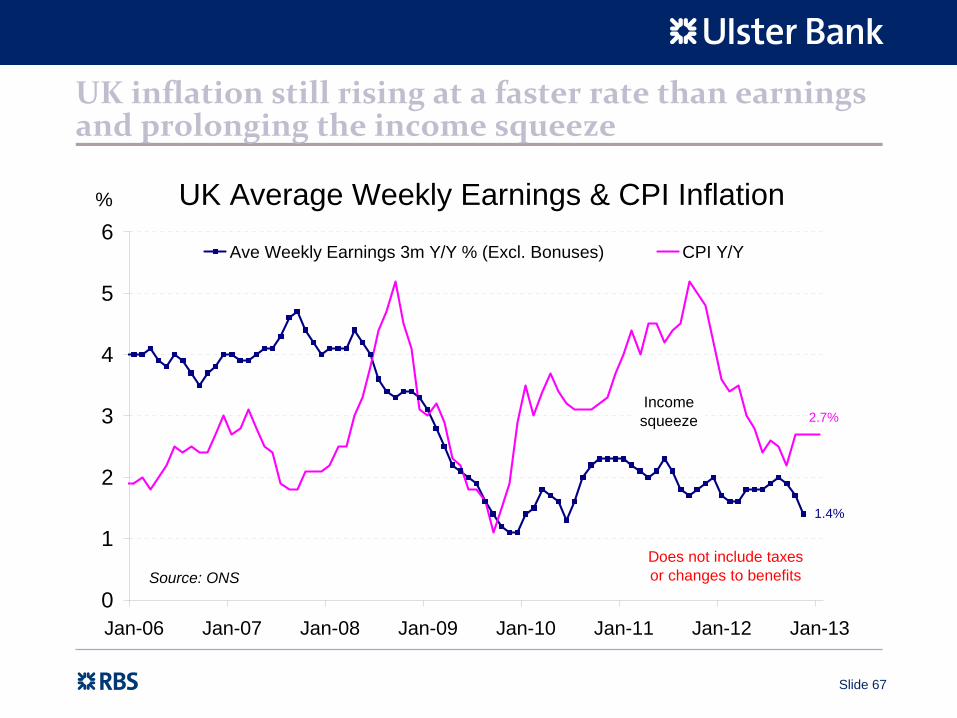

UK inflation still rising at a faster rate than earnings and prolonging the income squeeze

UK Average Weekly Earnings & CPI Inflation

1.4%

2.7%

0

1

2

3

4

5

6

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

%

Ave Weekly Earnings 3m Y/Y % (Excl. Bonuses) CPI Y/Y

Source: ONS

Income squeeze

Does not include taxes or changes to benefits

Slide 68

Discretionary spending hit with consumer confidence also very weak…

21,200 fewer NI new car sales relative to 2007 peak 12 Month Rolling Sum

57,170

47,580 47,532

68,708

30,000

40,000

50,000

60,000

70,000

80,000

Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12 Feb-13

Sales now 31% below

peak

Source: SMMT

Temporary reduction in VAT rate to 15% & 'Cash for Clunkers'

Slide 69

….. following rise in dole queue & job insecurity

Slide 69

NI Unemployment Claimant Count Levels

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Dec-85 Dec-88 Dec-91 Dec-94 Dec-97 Dec-00 Dec-03 Dec-06 Dec-09 Dec-12

Source: DFP

Dec 2012 65,200 highest levels

since April 1997

Record low Aug 0723,500

Good Friday Agreement signed

April 199857,900

Slide 70

NI has posted steepest decline in UK but new car sales in RoI remain 60% below peak…

New Car RegistrationsIndexed 2007 =100

-31%

-8.5%

-18%-14%

-60%

0

20

40

60

80

100

120

Dec-07 Sep-08 Jun-09 Mar-10 Dec-10 Sep-11 Jun-12 Mar-13

NI Scotland Wales UK RoI

Source: SMMT & SIMI

Slide 71

Kia car sales more than treble, Hyundai up 58% & Skoda up 13%. All post new record sales in 2012

Growth in NI New Car Registrations by Manufacturer 2007-2012

0% 50% 100% 150% 200% 250%

Kia

Hyundai

Chevrolet

Nissan

Skoda Source: SMMT

Slide 72

Brands gaining NI market share 2007‐2012

Cool? Seriously

Cool? Sub‐Zero?

Value for Money?

Slide 73

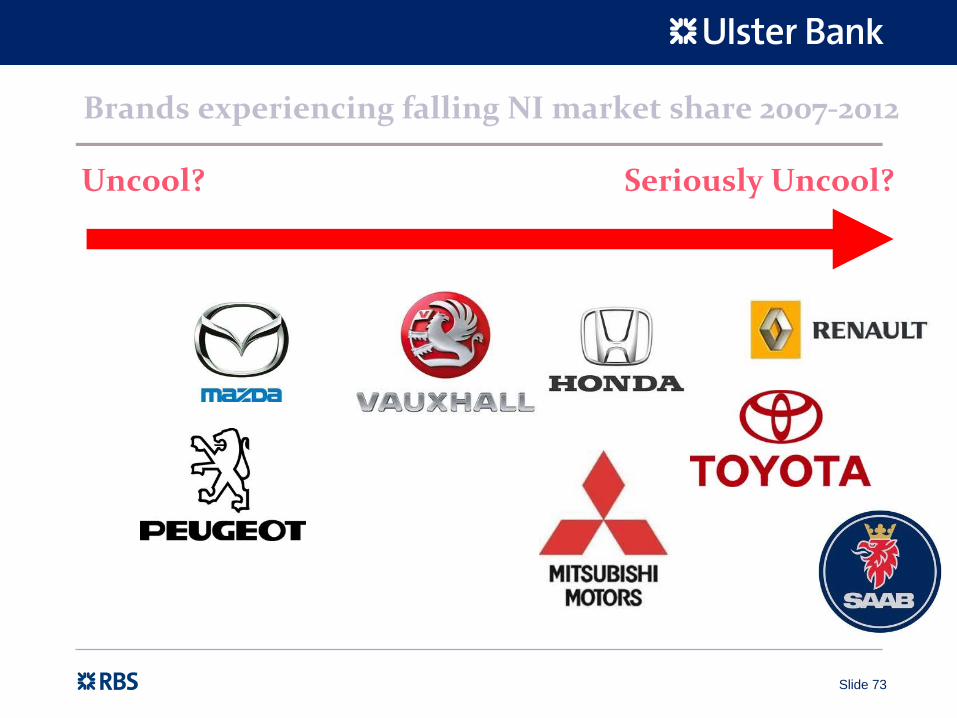

Brands experiencing falling NI market share 2007‐2012

Uncool? Seriously Uncool?

Slide 74

N. Ireland premium brand new car sales have taken a hit

2007 (house price peak)

2012

12

45

02 11190

29 218 4 2 14 238

167

Slide 76

UK high street hit by changing consumer trends

UK Internet Sales as a % of Total Retail Sales* Not Seasonally Adjusted

10.4%

0

2

4

6

8

10

12

2006 Q4 2007 Q4 2008 Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q4

%

Source: ONS, * Excluding Automotive Fuel

Slide 77

The Changing Face of the UK High Street 2012

Winners Payday Loans +20.0%

Pawnbrokers +13.2%

Poundshops +13.0%

Supermarkets +3.6%

Coffee Shops +3.4%

Betting Shops +3.3%

Charity Shops +2.7%

Losers

Net change in units in 2012. Source: Local Data Company

Computer Games ‐45.0%

Health Food ‐24.7%

Card Shops ‐23.4%

Recruitment ‐15.1%

General Clothes ‐8.7%

Women’s Clothes ‐7.2%

Banks / Financial ‐2.9%

Slide 78

Input cost inflation eases in February (but up over last 3 months)

with output prices and charges still falling

NI Private Sector Profit Squeeze3 Month Moving Average

30

40

50

60

70

80

Feb-04 Aug-05 Feb-07 Aug-08 Feb-10 Aug-11 Feb-13

Output Prices Input Prices No Change

InflationD

eflation

Source: Markit Economics & Ulster Bank NI PMI

Profits squeeze

Price of goods & services falling

Slide 79

Unemployment a major problem within the <25s

Slide 79

NI Youth Claimant Count Levels<25 years of age

17,876

Nov 07 low 7,050

0

5,000

10,000

15,000

20,000

25,000

Nov-96 Nov-98 Nov-00 Nov-02 Nov-04 Nov-06 Nov-08 Nov-10 Nov-12

Source: DFP

19,551 Highest level since October

1996

GFAApril 1998

14,145

Slide 80

Public sector employment boom has been & gone. A sustained period of job losses is anticipated going forward

NI Public Sector Employee Jobs Levels

213,480

Pre-recession peak Q4 2005221,050

Good Friday Agreement Signed April 1998

195,120 Q2 98209,480

180,000

190,000

200,000

210,000

220,000

230,000

Q3 1994 Q3 1997 Q3 2000 Q3 2003 Q3 2006 Q3 2009 Q3 2012

Public Unadjusted Public Adjusted* (excl. financial institutions)

Source: DFP, * UB estimates

Public sector employment boosted by @5k in Q4 2008 as

part-nationalised financial institutions reclassified as

public sector. Public sector jobs (excl. financial institutions) now estimated at @209.5k or

Q4 2002 levels.

+26,000 jobs (13%) in 7yrs

post GFA

Slide 81

Decade

ahead will HURT

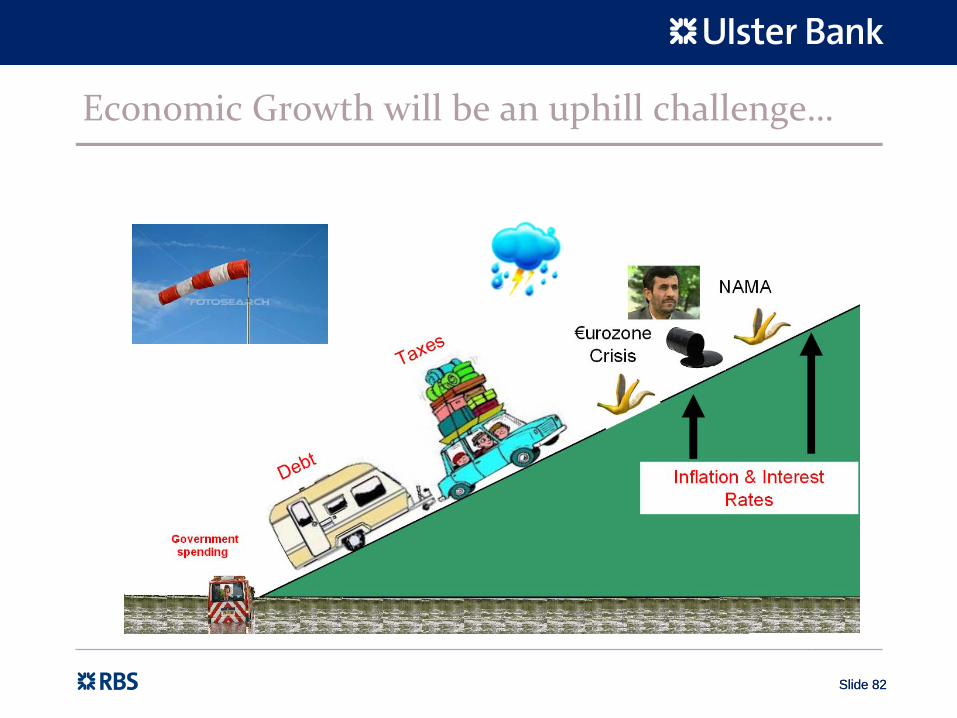

Downside risks to NI growth (EZ crisis linked to EZ politics)

Unemployment to stay higher for longer…. a lost decade for the under 25’s?

Households face devaluation in S.O.L, debt de-leverage

Factors present in ‘NICE’ era have gone into reverse - Next decade ahead will HURT – Higher Unemployment Rising Taxes / Tariffs

Fiscal austerity in NI – it hasn’t really started yet!

Key labour market trends: part-time v full-time, working longer, multi-job careers v job for life, demand for jobs with no skills falling

Slide 82Slide 82

Economic Growth will be an uphill challenge…

Source:

The Economist

Slide 83Slide 83

…with a ‘spreadsheet recovery’

Source:

The Economist

Computer says Yes. But consumer says No!

Slide 84Slide 84

In UK & NI we too face the ‘Juncker Conundrum’

“We all know what we need to do, we just don’t know how to get re‐elected after doing it”

Jean‐Claude Juncker – Former President of the Euro Group (January 2005 – January

2013)

& current Luxembourg Prime Minister. Quote November 2012.

Slide 85

Any Questions

?

Slide 86Slide 86

But NI is still better when I left school!

Laganside

1994 Source: Invest NI

Slide 87Slide 87

Laganside today

Source: Invest NI

Titanic QuarterTitanic Quarter

Slide 88

Website

www.ulsterbankcapitalmarkets.comContact me (to be added to distribution lists)

Tel .no. 02890 276354

Slide 89Slide 89

DisclaimerThis document is issued for information purposes only for clients of Ulster Bank Group who are eligible counterparties or professional customers, and does not constitute an offer or invitation to purchase or sell any instrument or to provide any service in any jurisdiction where the required authorisation is not held. Ulster Bank and/or its associates and/or its employees may have a position or engage in transactions in any of the instruments mentioned.

The information including any opinions expressed and the pricing given, is indicative, and constitute our judgement at time of publication and are subject to change without notice. The information contained herein should not be construed as advice, and is not intended to be construed as such. This publication provides only a brief review of the complex issues discussed and readers should not rely on information contained here without seeking specific advice on matters that concern them. Ulster Bank make no representations or warranties with respect to the information and disclaim all liability for use the recipient or their advisors make of the information. Over-the-counter (OTC) derivates can involve a number of significant and complex risks which are dependent on the terms of the particular transaction and your circumstances. In the event the market has moved against the transaction you have undertaken, you may incur substantial costs if you wish to close out your position.

Ulster Bank Limited Registered Number R733 Northern Ireland. Registered Office 11-16 Donegal Square East, Belfast, BT1 5UB. Authorised and regulated by the Financial Services Authority. Member of The Royal Bank of Scotland Group.

Ulster Bank Ireland Limited, a private company limited by shares, trading as Ulster Bank, Ulster Bank Group and Bank Uladh. Registered No. 25766. Registered Office Ulster Bank Group Centre, George’s Quay, Dublin 2. Ulster Bank Ireland Limited is regulated by the Financial Regulator. Member of The Royal Bank of Scotland Group.

Calls may be recorded.