data center security products -...

TRANSCRIPT

Data Center Security –The Increasing Requirements for Data Center-Class Performance

Data Center Security ProductsBiannual Worldwide and Regional Market Share, Size, and Forecasts: Excerpts

1

WHITE PAPER: AGILE NETWORK SECURITY IN THE AWS ENVIRONMENT

Data centers have increasingly distinct security and performance requirements from traditional enterprise fi rewalls

and edge security use cases. Fortinet’s unique strengths based on ASIC-driven hardware acceleration and

consolidated security architectures have led to industry-leading capabilities in performance and throughput,

scalability, high-speed ports and port density, including the release of the world’s fi rst device to exceed 1 Tbps

of fi rewall throughput. This leadership has resulted in rapid growth to becoming a leading vendor for data center-

class appliances from the enterprise to leading telecommunications and service providers.

In the following report from Infonetics Research, Principal Analyst Jeff Wilson discusses the data center market

and adoption drivers for fi rewalls, integrated security, and other appliances. Wilson introduces criteria for data-

center class capabilities, and discusses the leading vendors who are poised to deliver on the new requirements.

Data Center Security – The Increasing Requirements for Data Center-Class Performance

As organizations shift to becoming increasingly knowledge-driven businesses, the data center continues to grow in size and importance, accelerated by initiatives such as cloud, big data and SaaS. This is leading to rapid increases in network bandwidth and refresh of networking and fi rewall hardware.

As organizations shift to becoming increasingly knowledge-driven businesses, the data center continues to grow in size and importance, accelerated by initiatives such as cloud, big data and SaaS. This is leading to rapid increases in network bandwidth and refresh of networking and fi rewall hardware.

www.fortinet.com/solutions/data-center-fi rewalls.html

695 C ampbe l l Techno lo gy Pa rkway • Sui t e 200 • Ca mpbe l l • C a l i fo r n ia • 95008 • t 408. 583 .0011 • f 408 . 583 . 0031

www. i nf one t i c s . com • S i l ic o n Val le y, CA • Bos ton, MA • London, UK

Data Center Security Products Biannual Worldwide and Regional Market Share, Size, and Forecasts: 2nd Edition

Report Excerpts

December 2014

By Analyst Jeff Wilson

INFONETICS RESEARCH REPORT EXCERPTS

Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

Table of Contents

TOP TAKEAWAYS 1

DATA CENTER SECURITY APPLIANCES 1

Overall Market: 2014 Strong for Data Center Appliances 1

Manufacturers and Market Share Analysis: Cisco Continues to Lead, but There Are Many Challengers 3

DATA CENTER SECURITY APPLIANCE ROADMAP 5

DATA CENTER SECURITY PRODUCT DRIVERS 6

Service Provider Survey Results 7

REPORT AUTHOR 8

ABOUT INFONETICS RESEARCH 8

REPORT REPRINTS AND CUSTOM RESEARCH 8

List of Exhibits

Exhibit 1 Data Center Security Appliance Revenue by Category 2

Exhibit 2 Data Center Security Appliance Market Share 4

Exhibit 3 Data Center Security Product Roadmap 5

1 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

TOP TAKEAWAYS

Enterprises and service providers are upgrading data centers to support huge increases in traffic and handle the massive waves of attacks they face every day; they’re investing in data center security solutions now because they need to increase overall security throughput, increase their ability to handle sessions/connections, and add new threat protection capabilities.

Key data points from this edition:

● Revenue for data center security appliances was up 5% in 2Q14 from 1Q14, rising to $599M, and it will hit $2.7B by CY18, a 5-year CAGR of 4%; 2Q14 revenue was up 14% from 2Q13. Revenue for data center security appliances was up 6% in CY13, rising to $2.2B from CY12, and is expected to increase 12% to $2.5B in CY14.

● Market share for security appliances in the data center fairly closely mirrors overall market share for security solutions, with Cisco leading in 2Q14, followed by Fortinet, Juniper, Check Point, and McAfee. In CY13, Cisco lead, followed by Fortinet, Juniper, Check Point, and McAfee.

DATA CENTER SECURITY APPLIANCES

Overall Market: 2014 Strong for Data Center Appliances

Revenue for data center security appliances was up 5% sequentially in 2Q14, rising to $599M, and it will hit $2.7B by CY18, a 5-year CAGR of 4%. 2Q14 revenue was up 14% YoY, and looking at the annual data 2013 revenue was up 6% from 2012, hitting $2.2B, and 2014 will be up 12% from 2013. The market will continue strong through 2014, but transformation in data center infrastructure will start to cause tectonic shifts in the revenue makeup for data center security.

The data center security appliance data presented in this report covers security products deployed in data center environments, including integrated security appliances, secure routers, IPS appliances, web and mail security gateways, and DDoS prevention systems. The products in this service tend to be higher-end, but not all data center security appliances are large $100K+ devices; there are small and mid-sized data centers that use lower-end gear than someone like an Amazon or Google, there are many commercial hosting environments with colocation facilities or per-customer appliances. Roughly 60-70% of the revenue for integrated appliances tracked here are what the industry would consider data center class ($30K and up, 40G+ aggregate throughput, etc.). DDoS shows the most growth but is also the smallest segment by far. The following table summarizes actual data and historical data.

2 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

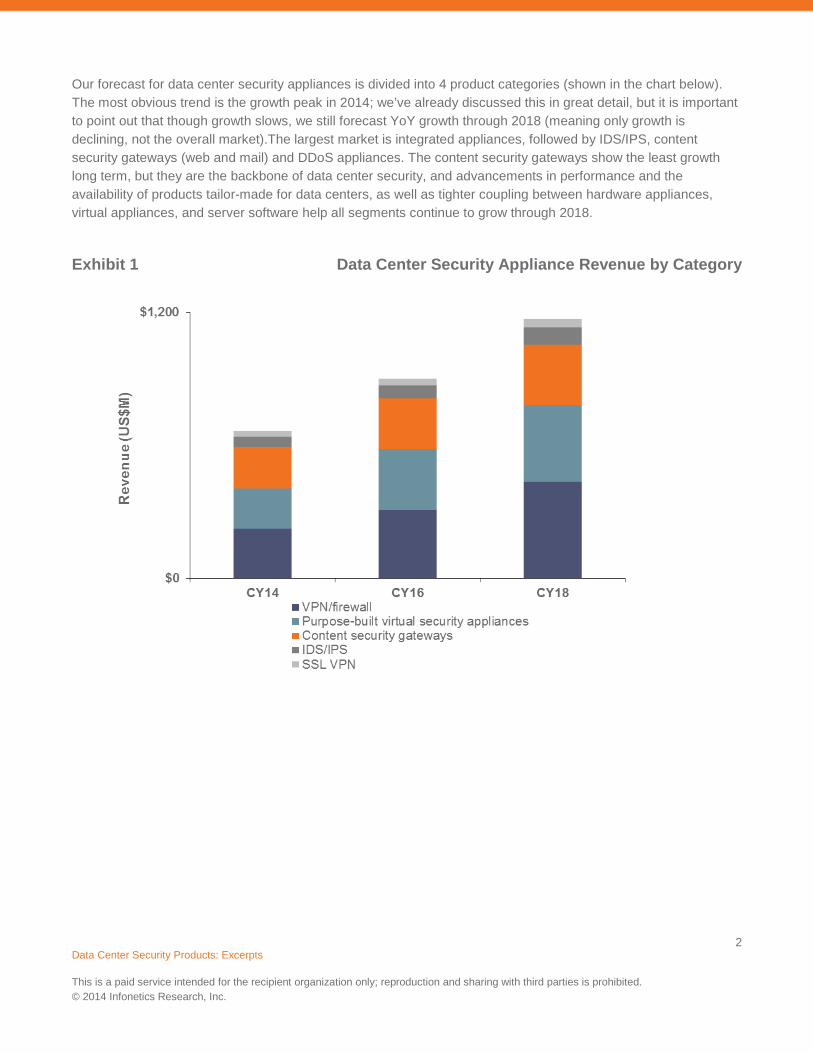

Our forecast for data center security appliances is divided into 4 product categories (shown in the chart below). The most obvious trend is the growth peak in 2014; we’ve already discussed this in great detail, but it is important to point out that though growth slows, we still forecast YoY growth through 2018 (meaning only growth is declining, not the overall market).The largest market is integrated appliances, followed by IDS/IPS, content security gateways (web and mail) and DDoS appliances. The content security gateways show the least growth long term, but they are the backbone of data center security, and advancements in performance and the availability of products tailor-made for data centers, as well as tighter coupling between hardware appliances, virtual appliances, and server software help all segments continue to grow through 2018.

Exhibit 1 Data Center Security Appliance Revenue by Category

3 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

The key drivers for data center security appliances are:

● The need to upgrade hardware appliances to new physical interfaces (10G, 40G, 100G)

● The need for higher aggregate throughput (40G and up, but in some cases approaching 1 terabit)

● The need for massive performance increases in connection rate and concurrent connections for key web/data center protocols (like TCP); in many cases, data centers’ connection performance needs have increased 10x in the last 2 to 3 years, and their firewalls are having a hard time keeping up

● A growing need for lower-latency data center security solutions in latency-sensitive environments, like financial data centers, and any data center serving real-time communications applications

● The need to integrate some security functions at high speeds in small to medium-sized data centers (consolidating firewall, IPS, and DDoS in a platform that supports 5G to 10G aggregate throughput)

● Deployment of high-end appliance solutions that are aware of or can interface with virtualized security solutions and/or SDNs/NFV

● Availability of new products that are specifically focused on data center security (like F5’s data center firewall solution) or offer significantly better performance than previous generations of products

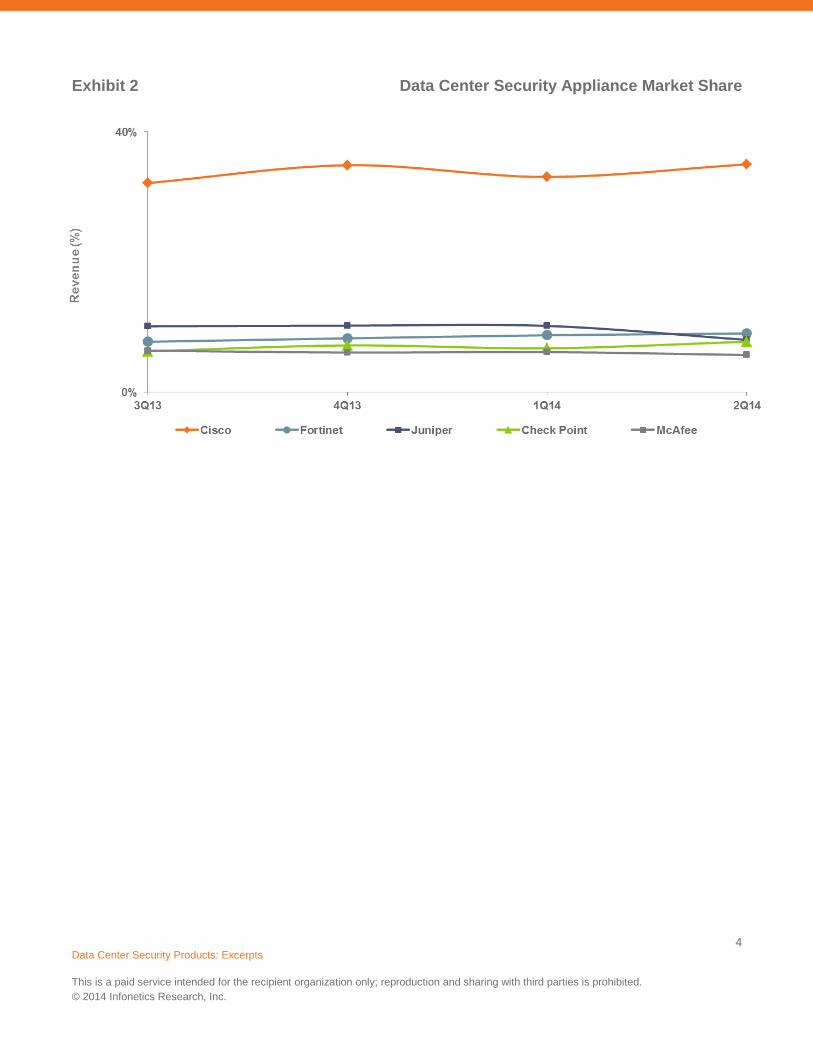

Manufacturers and Market Share Analysis: Cisco Continues to Lead, but There Are Many Challengers

Market share for security appliances in the data center fairly closely mirrors overall market share for security solutions. Cisco has a broad product portfolio (selling integrated appliances, IPS, and content security) and has the sales and support infrastructure (as well as a deep interest in data center business outside of security) to serve data center customers well. Over a year ago Cisco announced a bevy of new data center security solutions, and they closed the Sourcefire acquisition, which will give them a full line of next generation firewall and IPS hardware, which they will aim directly at the data center as well.

Cisco led data center security appliance revenue market share in 2Q14. Fortinet moved up to second place, followed by Juniper in the third spot, Check Point in fourth, and McAfee in fifth.

Fortinet moves past Juniper into second due to its strong position in many mid-sized data centers and strong price/performance position (their 3700D has been wildly successful in some high profile data center deals), and its launch of the 3810D (300G throughput and 100G interfaces) should help it gain some ground at the very high end of the market.

4 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

Exhibit 2 Data Center Security Appliance Market Share

5 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

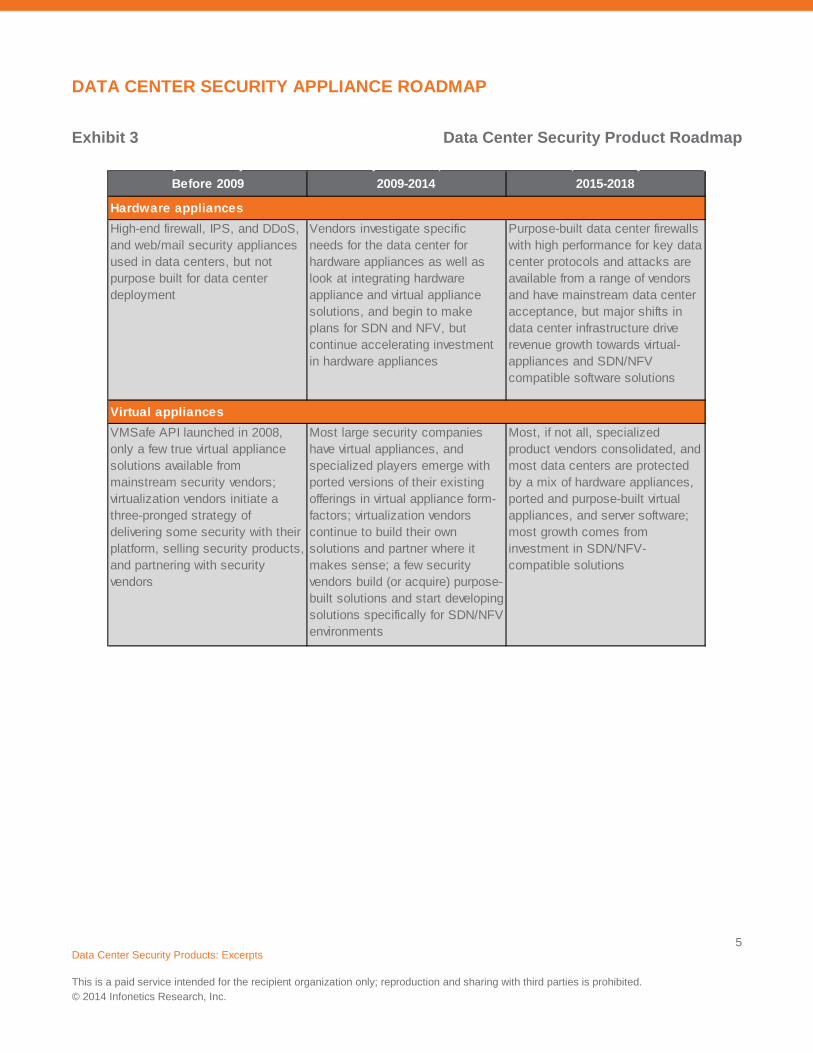

DATA CENTER SECURITY APPLIANCE ROADMAP

Exhibit 3 Data Center Security Product Roadmap

Virtual appliances

Purpose-built data center firewalls with high performance for key data center protocols and attacks are available from a range of vendors and have mainstream data center acceptance, but major shifts in data center infrastructure drive revenue growth towards virtual-appliances and SDN/NFV compatible software solutions

High-end firewall, IPS, and DDoS, and web/mail security appliances used in data centers, but not purpose built for data center deployment

Vendors investigate specific needs for the data center for hardware appliances as well as look at integrating hardware appliance and virtual appliance solutions, and begin to make plans for SDN and NFV, but continue accelerating investment in hardware appliances

Before 2009 2009-2014 2015-2018

Hardware appliances

VMSafe API launched in 2008, only a few true virtual appliance solutions available from mainstream security vendors; virtualization vendors initiate a three-pronged strategy of delivering some security with their platform, selling security products, and partnering with security vendors

Most large security companies have virtual appliances, and specialized players emerge with ported versions of their existing offerings in virtual appliance form-factors; virtualization vendors continue to build their own solutions and partner where it makes sense; a few security vendors build (or acquire) purpose-built solutions and start developing solutions specifically for SDN/NFV environments

Most, if not all, specialized product vendors consolidated, and most data centers are protected by a mix of hardware appliances, ported and purpose-built virtual appliances, and server software; most growth comes from investment in SDN/NFV-compatible solutions

6 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

DATA CENTER SECURITY PRODUCT DRIVERS

To generate the forecast for virtual security appliances we went through our standard process for sizing and forecasting a product market (detailed in the Methodology section of the Excel size/forecast file for this report); we gathered actual data where available from vendors through 2Q14. This is a new market though, and most vendors aren’t directly forthcoming with their shipment data, so we built a model for both forecasting and verifying actuals through 2Q14; this model factors in:

● Deployment of server virtualization technology through 2Q14 by region

● Estimated penetration of security (by technology) into the virtual server market

● Total market size for the corresponding non-virtual appliance and software market (total IDS/IPS market size, total SSL VPN market size)

● Size of the virtual market relative to the total market by technology, divided into products ported from existing solutions, and products built from the ground up to operate in virtualized environments

● Historical growth rates of the corresponding traditional appliance and software market

● Forecasted growth of server virtualization and traditional security appliances and software

● Feedback from vendors on the portion of their total security product revenue made up by virtual appliance sales

● Adoption of public and private cloud services, and growth in cloud infrastructure rollouts

To generate the size, forecast, and share data for data center security appliances, we start with the base of our security appliance data, and based on discussions with enterprises, service providers, the channel, and the financial community, we estimate by vendor/region/product category the percentage of revenue and units for data center deployments of hardware security appliances.

We used the following Infonetics Research services to build the model for the forecasts we present in this service:

● Network Security Appliances and Software, August 2014

● Content Security Gateway Appliances, Software, and SaaS, August 2014

● DDoS Prevention Appliance, June 2014

7 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

Service Provider Survey Results

In December 2013, we published a report based on interviews with 24 of the largest and most influential cloud/hosting providers around the globe, titled Data Center Security Strategies and Vendor Leadership: Global Service Provider Survey. Key findings that were directly applied to the market sizing and forecast in this service include:

● 96% of respondents are driven to deploy new solutions by the need to upgrade to high speed network interfaces on their security appliances to match the upgrades that have happened in their switching infrastructure, and 100% are driven by the need for security solutions with aggregate performance that matches their data center network performance; 100% also need new solutions for DDoS.

● Even more than their enterprise counterparts, service provider respondents favor a multi-layered model for deploying security in the data center; over 70% of respondents are already using hardware appliances, virtual appliances, and server software.

● Respondents deploying virtual security appliances what to have equal levels of security in physical and virtual environments, and are looking for new layers of security to protect against new types of threats.

8 Data Center Security Products: Excerpts This is a paid service intended for the recipient organization only; reproduction and sharing with third parties is prohibited. © 2014 Infonetics Research, Inc.

REPORT AUTHOR

Jeff Wilson

Principal Analyst, Security

Infonetics Research

+1 408.583.3337 | [email protected]

Twitter: @securityjeff

ABOUT INFONETICS RESEARCH

Infonetics Research is an international market research and consulting analyst firm serving the communications industry since 1990. A leader in defining and tracking emerging and established technologies in all world regions, Infonetics helps clients plan, strategize, and compete more effectively.

REPORT REPRINTS AND CUSTOM RESEARCH

To learn about distributing excerpts from Infonetics reports or custom research, please contact:

North America (West) and Asia Pacific Larry Howard, Vice President, [email protected], +1 408.583.3335 North America (East, Midwest, Texas), Latin America, and EMEA Scott Coyne, Senior Account Director, [email protected], +1 408.583.3395 Greater China, Southeast Asia, and India 大中华区及东南亚地区 Jeffrey Song, Market Analyst 市场分析师及客户经理 [email protected], +86 21.3919.8505