david fin ass 1

TRANSCRIPT

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 1/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 I

Financial Ratio Analysis International College of Hotel Management

Student Name : Tan Wee Jian, David Chan,

Azry Rasyeqa Binti Mohd Rafflee

ID Number : 000865887, 000864839, 000865888

Subject : BBHM Managing Business Financial Performance

Subject Code : BBHM 301

Due Date : 26th

March 2012

Lecture : Donald Peter

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 2/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 II

Table of Contents

1.0. Financial Ratio Analysis ...................................................................................... 1

2.0. Liquidity ratios ..................................................................................................... 2

2.1. Current Ratio .................................................................................................... 2

2.2. Quick (Acid Test) Ratio ................................................................................... 2

3.0. Activity Ratio ....................................................................................................... 3

3.1. Inventory Turnover ........................................................................................... 3

3.2. Average Collection Period ................................................................................ 3

3.3. Average Payment Period .................................................................................. 3

3.4. Total Asset Turnover ........................................................................................ 4

4.0. Debt Ratio ............................................................................................................ 5

4.1. Times Interest Earned Ratio ............................................................................. 5

4.2. Earnings per Share ............................................................................................ 5

5.0. Analyzing Profitability ......................................................................................... 6

5.1. Gross Profit Margin .......................................................................................... 6

5.2. Operating Profit Margin ................................................................................... 6

5.3. Net Profit Margin.............................................................................................. 6

5.4. Return on Total Assets (ROA) ......................................................................... 6

5.5. Return on Equity (ROE) ................................................................................... 7

5.6. Earnings per Share ............................................................................................ 7

5.7. DuPont System of Analysis .............................................................................. 7

Conclusion ...................................................................................................................... 8

Reference ........................................................................................................................ 9

Appendix

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 3/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 1

1.0. Financial Ratio Analysis

All information obtained from financial statements is vital and from the statement,

the organization will do an analysis to determine financial ratios as each stakeholder

requires the information for monitoring and knowledge of company’s growth.

It is an amalgamation of financial and operating data from an organization to

provide basic information. It consists of 15 categories financial ratios found in the

company the authors choose which McDonalds is.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 4/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 2

2.0. Liquidity ratios

It is measured for short term obligations in assets which could be converted to cash

whenever necessary. Liquidity simply means to have cash in hand at all times, hence

when it is needed necessarily there is always cash prepared. (Pamela.P, 2012)

2.1. Current Ratio

From Appendix – E 1, the ratio improves from year 2009 to 2011 which proven that

McDonalds is not facing any financial difficulties and it has the ability to settle all

financial obligations. With this result, their profitability is secure as their target market is

high which makes their return of profit is high.

2.2. Quick (Acid Test) Ratio

From Appendix – E 2, inventory of the food items which is high in liquidity because their

inventory items perishability is high as the demand of fast food has grown all over the

world each year.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 5/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 3

3.0. Activity Ratio

3.1. Inventory Turnover

Inventory Turnover is a ratio of cost of goods sold to inventory that indicates how many

times inventory is created and sold during the period (Drake, 2012) According to the

turnover rate (Appendix – E3) of McDonald shows that over the three years it has an

increasing from 131 times to 139 times turnover that is 8 times on the year 2011. Based

on research, McDonald’s opens more stores by using cash on hand and increasing the

advertising budget and buying back shares to push on their sales, thus the inventory

turnover rate is increasing in stability (Kennon, 2012).

3.2. Average Collection Period

Average Collection Period (Accounts Receivable Turnover) is the ratio of net credit sales

to accounts receivable that indicates how many times in the daily period credit sales have

been created and collected (Gitman, Juchau & Flanagan, 2011). McDonald’s has an

increasing higher turnover on account receivable over the three years based on the

calculation (Appendix – E4). The author assumed that McDonald’s does not indicate a

not strong management on credit collection department thus caused the lengthened period

of the credit collection.

3.3. Average Payment Period

Average Payment Period is the average age of accounts payable that indicates how many

times in the daily period payments relate to the credit term extension of the firm (Gitman,

Juchau & Flanagan, 2011). Based on the equation (Appendix-E5), McDonald’s has an

frustrating figure on the ratio for credit terms, from ratio of 16.64 increased to 23.86 and

yet dropped to 21.50 on the year 2011, this could be assumed that the firms has been

paying attention and building a good relation with the suppliers so that the frustration of

credit term is flexible and under control based on the financial circumstances of the firm.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 6/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 4

3.4. Total Asset Turnover

The Total Asset Turnover indicates the efficiency with the uses all its assets to generate

sales. With the figure shows in the calculation for TAT (Appendix-E6), the frustration of

the turnover is basically has a poor productivity as on the year 2009, the asset turnover

was 6.66 times but on the year 2011 was a gap of 0.53 times, this proves that the amount

of assets that McDonald’s previously held was not been maximized to be productivity to

work out an increasing return of equity.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 7/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 5

4.0. Debt Ratio

The debt ratio is also called the debt (or liabilities)-to-assets ratio. This measures a

company’s use of leverage: It notifies you the percentage of liabilities compared to

financial assets. The more liabilities compared to assets a company has, the more

leveraged it is and the riskier it is considered to be. In Appendix equation no.7, the debt

ratio had increased over the three years from 53.6% to 56.4% in McDonald. This doesn’t

mean the business at risk as McDonald is a large and well-established fast-food company,

and they’re able to take more risks/debts without losing any investors.

4.1. Times Interest Earned Ratio

This calculation is formulated by taking McDonald’s earnings before interest and taxes

(EBIT) and dividing total interest. This will show and indicates how many timesMcDonald can cover its interest charges on a pre-tax basis. Referring to Appendix

equation no.8, the percentage had slightly increased over the three years, but there’s

possibility that McDonald is facing financial problems and unable to settle outstanding

interests.

4.2. Earnings per Share

EPS is calculated over a number of years indicates whether the earning power of the

company has improved or deteriorated. By calculating EPS, it can determine a company’sprofitability. From 2009 till 2011, in Appendix equation no.14, the EPS of McDonald has

steadily increased. An increase in EPS is an important measure because it reveals the

amount of profit that McDonald is generating for the shareholders. This will attract more

investors as they always look for companies with steadily increasing earnings per share.

The higher the earnings per share with all else equal, the higher each share should be

worth.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 8/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 6

5.0. Analyzing Profitability

The main purpose for McDonalds to have this information is too evaluating the earnings

gained from investment made and the earnings they made in the market as well as

generating financial return in terms of gaining back the assets invested in. (Spire Frame,

2012)

5.1. Gross Profit Margin

From Appendix – E 9, McDonalds gross profit margin are quite high and it increase

every year which concludes they made good profit and even after paid for their goods the

profit is up to 39 to 40% which is essential and excellent for the company.

5.2. Operating Profit Margin

It measures profit earn in sales before minus interest and taxes as shown in Appendix – E

10 the margin shows positive figures which is good for the organization as it proves that

their return rate is high and each cents spend on the company is worth it. They get to earn

their profit margin back in short period of time and it increases yearly.

5.3. Net Profit Margin

Is net profit gained after minus expenses and taxes, from Appendix – E 11 shows

increases from 20 % to 21% in year 2009 to 2010 however it decreases to 20% again in

2011 shows inconsistency for net profit gain. The impact on this situation will be

common as consumer’s preferences changes from time to time.

5.4. Return on Total Assets (ROA)

Simply means return on investment which measures the effectiveness in generating

profits which is shown in Appendix – E 12. For both years 2009 and 2010 was the same

rate but increases in 2011as economy downturn effects consumers from eating out

however once it is back on track they came back and demand for more.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 9/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 7

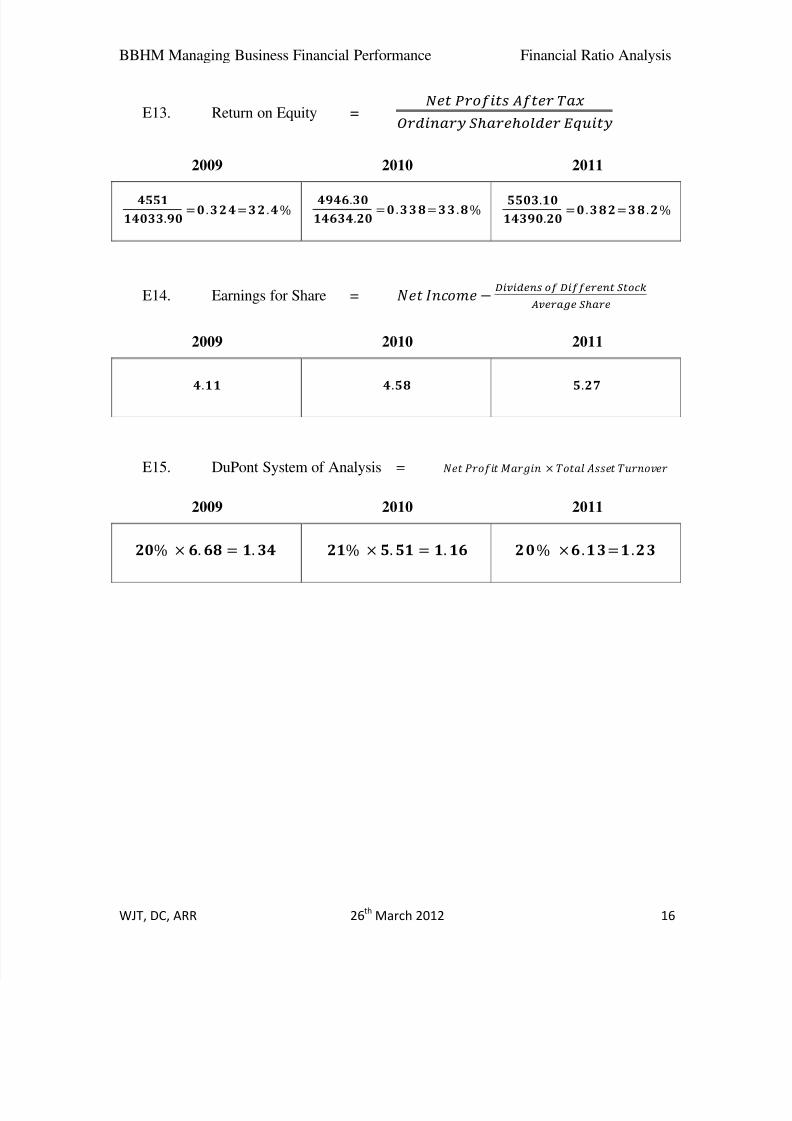

5.5. Return on Equity (ROE)

Measuring rate of return earned on shareholder’s investment for the organization as

shown in Appendix – E 13 it is calculated and result was positive. Each year, it increases

positively and the shareholders return earn is high and it definitely makes them feel worth

investing on McDonalds as the market segmentation is high and demand is there hence

each future year will be forecast high gaining as well.

5.6. Earnings per Share

EPS is calculated over a number of years indicates whether the earning power of the

company has improved or deteriorated. By calculating EPS, it can determine a company’s

profitability. From 2009 till 2011, in Appendix equation no.14, the EPS of McDonald has

steadily increased. An increase in EPS is an important measure because it reveals the

amount of profit that McDonald is generating for the shareholders. This will attract more

investors as they always look for companies with steadily increasing earnings per share.

The higher the earnings per share with all else equal, the higher each share should be

worth.

5.7. DuPont System of Analysis

The DuPont analysis system helps business owner’s to gain information about its

efficiency and how effective they are in utilising assets to generate revenue. To gain

higher return on assets requires business to boost its operating profit margin through

more efficient use of company assets, or to increase gross revenues through higher sales.

In McDonald’s case, base on Appendix equation no.15, we can determine that the

company isn’t really fully utilizing the assets as it declines from 1.34 in 2009 to 1.16 in

2010, but increased back to 1.26 in 2011.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 10/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 8

Conclusion

This assignment is all about the financial ratio analysis of McDonald’s Company and

making assumptions and seeks for facts regarding what are the causes based on the figure

of the ratio. The financial ratio can be obtained from McDonald annual financial report,

then calculate the ratio that includes from current ratio to quick ratio, debt ratio, and

DuPont analysis. Overall, McDonald’s Company is doing well due to high sales volume.

Although McDonald’s Company is well-established and stable, maybe the management

can look into financial control and reduce their expenses not only just focusing on

marketing side.

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 11/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 9

Reference

Zacks.com (2012), MCDONALDS CORP (NYSE) - Annual Income Statement,

viewed 20th

Macrh 2012, <http://www.zacks.com/research/report.php?type=ais&t=MCD >

Zacks.com (2012), MCDONALDS CORP (NYSE) - Annual Balance Sheet,

viewed 20th

Macrh 2012, <http://www.zacks.com/research/report.php?type=abs&t=mcd >

Joshua Kennon (2012), McDonald's vs. Wendy's - A Case Study In Inventory on the

Balance Sheet, viewed 20th

March 2012,

<http://beginnersinvest.about.com/od/analyzingabalancesheet/a/mcdonalds-vs-

wendys.htm>

Lawrence J. Gitman, Roger Juchau & Jack Flanagan (2011), Principle of Managerial

Finance 6 th

Edition, Financial statements and analysis – Activity Ratios, pg 55 - 57,

Pearson.

Pamela Peterson Drake, 2012, Financial Ratio Analysis, viewed 20th March 2012,

< http://educ.jmu.edu/~drakepp/principles/module2/fin_rat.pdf>

Spire Frame, 2012, Measuring Profitability, viewed 20th

March 2012,

<http://www.spireframe.com/articles/>

Time Interest Earned Ratio, viewed 21st March 2012,

<http://timesinterestearnedratio.info/>

Lister, J 2012, ‘ How The DuPoint System of Analysis Breaks Down Return on Assets’

Earnings Per Share (EPS), viewed 21st

March 2012,

<http://investing-school.com/definition/earnings-per-share-eps/>

Analysing Debt Ratios 2012, viewed 21st March 2012,

<http://www.aaii.com/computerized-investing/article/fundamental-focus-analyzing-debt-

ratios.mobile>

Kennon J 2012, About.com Guide, ‘ Return On Equity (ROE)’

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 12/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 10

Appendix

McDonald’s Annual Balance SheetFiscal Year End for MCDONALDS CORP falls in the month of December.All items in Millions except Per Share data.

12/31/11 12/31/10 12/31/09

Cash & Equivalents 2,335.70 2,387 1,796

Receivables 1,334.70 1,179.10 1,060.40

Notes Receivable 0 0 0

Inventories 116.80 109.90 106.20

Other Current Assets 615.80 692.50 453.70

Total Current Assets 4,403 4,368.50 3,416.30

Net Property & Equipment 22,834.50 22,060.60 21,531.50

Investments & Advances 1,427 1,335.30 1,212.70

Other Non-Current Assets 0 0 0

Deferred Charges 0 0 0

Intangibles 2,653.20 2,586.10 2,425.20

Deposits & Other Assets 1,672.20 1,624.70 1,639.20

Total Assets 32,989.90 31,975.20 30,224.90

Notes Payable 0 0 0

Accounts Payable 961.30 943.90 636

Current Portion Long-Term Debt 366.60 8.30 18.10

Current Portion Capital Leases 0 0 0

Accrued Expenses 1,581 1,585.60 1,854.80

Income Taxes Payable 600.30 386.90 479.80

Other Current Liabilities 0 0 0

Total Current Liabilities 3,509.20 2,924.70 2,988.70

Mortgages 0 0 0

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 13/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 11

Deferred Taxes/Income 1,344.10 1,332.40 1,278.90

Convertible Debt 0 0 0

Long-Term Debt 12,133.80 11,497 10,560.30

Non-Current Capital Leases 0 0 0

Other Non-Current Liabilities 1,612.60 1,586.90 1,363.10

Minority Interest (Liabilities) 0 0 0

Total Liabilities 18,599.70 17,341 16,191

Preferred Stock 0 0 0

Common Stock (Par) 16.60 16.60 16.60

Capital Surplus 5,487.30 5,196.40 4,853.90

Retained Earnings 36,707.50 33,811.70 31,270.80

Other Equity 449.70 752.90 747.40

Treasury Stock 28,270.90 25,143.40 22,854.80

Total Shareholder's Equity 14,390.20 14,634.20 14,033.90

Total Liabilities & Shareholder's Equity 32,989.90 31,975.20 30,224.90

Total Common Equity 14,390.20 14,634.20 14,033.90

Shares Outstanding 1,023.20 1,056.50 1,079.10

Book Value Per Share 14.06 13.85 13.01

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 14/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 12

Annual Income StatementFiscal Year End for MCDONALDS CORP falls in the month of december.All items in Millions except EPS data.

12/31/11 12/31/10 12/31/09

Sales 27,006 24,074.60 22,744.70

Cost Of Goods 16,319.40 14,437.30 13,952.90

Gross Profit 10,686.60 9,637.30 8,791.80

Selling & Adminstrative & Depr. & AmortExpenses

2,156.90 2,164.20 1,950.80

Income After Depreciation &Amortization

8,529.70 7,473.10 6,841

Non-Operating Income -24.70 -21.90 119.20

Interest Expense 492.80 450.90 473.20

Pretax Income 8,012.20 7,000.30 6,487

Income Taxes 2,509.10 2,054 1,936

Minority Interest 0 0 0

Investment Gains/Losses 0 0 0

Other Income/Charges 0 0 0

Income From Cont. Operations 5,503.10 4,946.30 4,551

Extras & Discontinued Operations 0 0 0

Net Income 5,503.10 4,946.30 4,551

Income Before Depreciation & Amortization 9,944.70 8,749.30 8,057.20

Depreciation & Amortization (Cash Flow) 1,415 1,276.20 1,216.20

Income After Depreciation &Amortization

8,529.70 7,473.10 6,841

Average Shares 1,044.90 1,080.30 1,107.40

Diluted EPS Before Non-Recurring Items 5.27 4.59 3.98

Diluted Net EPS 5.27 4.58 4.11

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 15/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 13

Equations * All items in Millions

E1. Current Ratio =

2009 2010 2011

E2. Quick Acid Test =

2009 2010 2011

E3. Inventory Turnover =

2009 2010 2011

E4. Average Collection Period =

2009 2010 2011

(

)

(

)

(

)

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 16/18

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 17/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 15

E9. Gross Profit Margin =

2009 2010 2011

E10. Operating Profit Margin =

2009 2010 2011

E11. Net Profit Margin =

2009 2010 2011

E12. Return on Total Assets =

2009 2010 2011

8/2/2019 David FIN Ass 1

http://slidepdf.com/reader/full/david-fin-ass-1 18/18

BBHM Managing Business Financial Performance Financial Ratio Analysis

WJT, DC, ARR 26th

March 2012 16

E13. Return on Equity =

2009 2010 2011

E14. Earnings for Share =

2009 2010 2011

E15. DuPont System of Analysis =

2009 2010 2011