dcf pemex outlook 060102 i - political-analysis.com · dcf, january 2, 2006 5 pemex is the 9th...

TRANSCRIPT

DCF, January 2, 20061

PEMEX Outlook

January, 2006

DCF, January 2, 20062

• This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in our periodic reports to the Mexican Banking and Securities Commission and theU.S. Securities and Exchange Commission (SEC), in our annual report, in our proxy statements, in our offering circulars and prospectuses, in press releases and other written materials and in oral statements made by our officers, directors or employees to third parties

• Statements that are not historical facts, including statements about our beliefs and expectations, are forward looking-statements. These are good faith statements based on current plans, estimates and projections and therefore you should not place undue reliance onthem. Forward-looking statements speak only as of the date they were made, and we undertake no obligation to update publicly any of them in light of new information or future events

• Forward-looking statements involve inherent risks and uncertainties. We caution you that a number of important factors could cause actual results to differ materially from those contained in any forward-looking statement

Forward-looking Statement

DCF, January 2, 20063

• The U.S. Securities and Exchange Commission (SEC) permits oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production orconclusive formation tests to be economically and legally producible under existing economic and operating conditions. We use certain terms in this document, such as total reserves, probable reserves and possible reserves, that the SEC's guidelines strictly prohibit us from including in filings with the SEC. Investors are urged to consider closely the disclosure in our Form 20-F, available from us at www.pemex.com or Marina Nacional 329 Floor 38 Col. Huasteca, Mexico City 11311 or at (52 55) 1944 9700. You can also obtain this Form from the SEC by calling 1-800-SEC-0330

• EBITDA, free cash-flow and discretionary cash-flow are non-GAAP measures. They are presented because PEMEX believes that they are useful for financial analysis

• The total debt calculation includes, in addition to documented debt, the items that are usually considered as debt by the financial markets

Cautionary Note

DCF, January 2, 20064

Agenda

PEMEX Highlights

Lines of Business

CAPEX and Financing Program

New Fiscal Regime

Looking Forward

DCF, January 2, 20065

PEMEX is the 9th Largest Integrated Oil Company in the World

Third largest producer of crude oil in the world(1)

Ninth largest integrated oil company in the world(1)

Proved reserves equivalent to 11 years of production(2)

Low cost producer vs. market average

Key supplier of crude oil to the US market

Mexico’s largest company with 2004 revenues of 69 billion dollars

Sole producer of crude oil, natural gas and refined products in Mexico

Sole marketer of refined products in Mexico

1) Based on PIW 2004 Rankings, December 2005, Petroleum Intelligence Weekly2) 2004 production levels and proved reserves in accordance with the definition under Rule 4.10(a) of

Regulation S-X under the U.S. Securities Act of 1933

DCF, January 2, 20066

Integrated Oil Majors

1

2

3

4

5

6

7

8

9

9

Source: PIW 2004 Rankings, December 2005, Petroleum Intelligence Weekly

Place Company Country Crude GasReserves

Crude GasProduction

Sales

Saudi Aramco

Exxon Mobil

PDVSA

NIOC

BP

RD Shell

Total

Chevron

PEMEX

PetroChina

Saudi Arabia

USA

Venezuela

Iran

UK

Netherlands and UK

France

USA

Mexico

China

1

13

5

2

18

25

22

19

10

14

4

13

5

2

15

17

21

24

29

16

1

5

4

2

6

8

15

11

3

9

7

2

11

5

4

3

9

12

14

19

9

1

8

12

3

2

6

4

14

13

CapacityRefining

9

1

3

14

5

2

6

10

13

12

DCF, January 2, 20067

Crude Oil and Natural Gas Reserves

• Long life of proved reserves of 11 years and 3P life of 29 years based on 2004 production(3)

• Reserves figures are certified by third parties

Reserves as of December 31, 2004MMMboe

1) In accordance with the definition of proved reserves under Rule 4.10(a) of Regulation S-X under the U.S. Securities Act of 1933. Probable and possible reserves were obtained through the difference between 3P reserves and proved reserves

2) The figure does not total due to rounding3) Reserves as of December 31, 2004 and based on 2004 production (average production of 4.4 MMboed)

17.6

15.8 46.9

13.4

Proved Probable Possible 3P(1) (2)

DCF, January 2, 20068

Production Profile

Crude oil production (MMbd)

Natural gas production (MMMcfd)

Refined products (MMbd)

• Crude oil production has grown steadily since 1999

• Refined products production has grown moderately

• The decreasing trend of natural gas production was reversed in 2003

3.02 3.01 3.13 3.18 3.37 3.38 3.402.913.07

3.48

1997 1998 1999 2000 2001 2002 2003 2004 2005E 2006E

5.24.8 4.8 4.94.64.54.44.54.74.5

1997 1998 1999 2000 2001 2002 2003 2004 2005E 2006E

1.61.5 1.5 1.61.61.61.51.51.41.5

1997 1998 1999 2000 2001 2002 2003 2004 2005E 2006E

DCF, January 2, 20069

Lifting Cost

Source: 2004 Annual Reports and 2004 20-F’s, (excluding PEMEX)

2004 Lifting CostUS$/boe

5.4 5.34.6

4.3 4.0 3.83.5 3.4

2.6

ChevronTexaco

ConocoPhillips

ExxonMobil

Petrobras RD Shell Statoil BP Total

DCF, January 2, 200610

Important Supplier of Crude Oil to the U.S.

(2) Source: Energy Information Administration (EIA)(1) Source: PEMEX

PEMEX’s exports by region 2004(1)

U.S. Importsby region 2004(2)

100% = 1.9 MMbd 100% = 10.0 MMbd

Saudi Arabia

Europe

Other Non-OPEC

VenezuelaOther OPEC

MexicoCanada

Rest of America

Far East USA 15%

16%

13%

16%

18%

22%

10%

2%9%

79%

DCF, January 2, 200611

EBITDA(1) of the Major Integrated Oil Companies

EBITDA 2004

MMMUS$

(1) Earnings before interests, taxes, depreciation and amortization.Source: Bloomberg, excluding PEMEX

45.6 45.0

32.629.6

25.2

19.517.0

13.4 13.3

ExxonMobil

BP Total RD Shell ChevronTexaco

ConocoPhillips

Statoil Petrobras

DCF, January 2, 200612

PEMEX EBITDA 2004

MMMUS$

(1) Special tax on production and services(2) Depreciation and amortization(3) Cost of the reserve for retirement payments, pensions and indemnities

Total sales

Total sales net of IEPS

Costs and expenses

Operating income net

of IEPS

Other revenues

D&A(2) EBITDACost of the reserve(3)

IEPS(1)

3.7

28.34.8

45.0

4.7

1.035.6

63.968.7

DCF, January 2, 200613

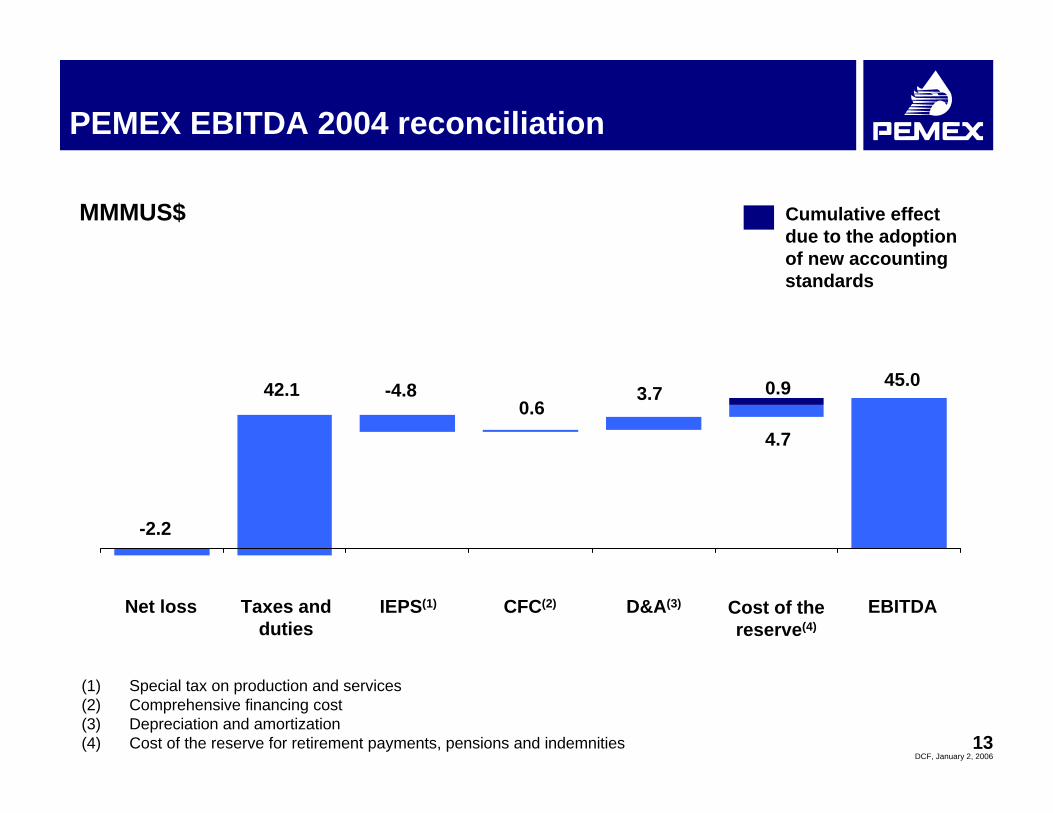

PEMEX EBITDA 2004 reconciliation

MMMUS$

(1) Special tax on production and services(2) Comprehensive financing cost(3) Depreciation and amortization(4) Cost of the reserve for retirement payments, pensions and indemnities

Net loss Taxes and duties

IEPS(1) CFC(2) D&A(3) EBITDACost of the reserve(4)

42.1 3.745.0

-2.2

-4.80.6

4.7

0.9

Cumulative effect due to the adoption of new accounting standards

DCF, January 2, 200614

Agenda

PEMEX Highlights

Lines of Business

CAPEX and Financing Program

New Fiscal Regime

Looking Forward

DCF, January 2, 200615

Untapped Exploration Potential

BasinsPEMEX has studied approximately 26% of Mexico’s prospective area

Approx. 55% of the prospective resources is found in the deep waters of the Gulf of Mexico

Approx. 33% of the prospective resources is found in southeast Mexico, where PEMEX currently holds a large amount of its operations

Mexico’shydrocarbons potential(MMMboe)

3P Reserves:

Total prospective resources(1) (mean):

Total remaining production potential in Mexico:

46.9

53.8

100.7

Prospective resources(MMMboe)

As a % of total prospective resources

Sabinas 1%0.3

Burgos 6%3.1

Tampico – Misantla 3%1.6

Veracruz 2%0.8

Sureste 33%17.7Golfo de México Profundo 55%29.3

Plataforma de Yucatán 1%0.3

(1) As of December 31, 2004. Stochastic addition, results may vary from an algebraic addition.

DCF, January 2, 200616

E&P Projects (1/2)

Reserves Development

(1) Proved and probable reserves as of December 31, 2004(2) Forecast based on portfolio 5.2E (3) Strategic Gas Program

OffshoreOnshore

1

43

7 2

5 6

1. Amatitlán (Chicontepec)2. Crudo Ligero Marino (SGP)(3)

3. Agua Fría (Chicontepec)4. Ayín-Alux5. San Manuel (SGP)(3)

6. Ixtal-Manik (SGP)(3)

7. Burgos

Project

Oil reserves(1)

(MMb)

Gas reserves(1)

(MMMcf)

1,740766357299214184

98

2,338906637

671,084

993,006

393230173

741155

-

202920072012201420062008

-

Oil peakproduction(2)

(Mbd) Year

Gas peakproduction(2)

(MMcfd) Year

439641191

19214

631,260

2029200720122014200620082009

DCF, January 2, 200617

E&P Projects (2/2)

OffshoreOnshore

9

11

8

10

8. Cantarell9. Ku-Maloob-Zaap10. Antonio J. Bermúdez11. Jujo-Tecominoacán12. Poza Rica13. Bellota Chinchorro14. Cactus Sitio Grande

Project

Oil reserves(1)

(MMb)

Gas reserves(1)

(MMMcf)

8,8844,3522,207

923670334308

2,3121,0482,4951,110

791532507

1,996794161

88515327

2006201020082008201120082010

Oil peakproduction(2)

(Mbd) Year

Gas peakproduction(2)

(MMcfd) Year

727324282

80567073

2006201020082008201120082010

Injection

N2N2N2N2

H2OPP(3)

PP(3)

(1) Proved and probable reserves as of December 31, 2004(2) Forecast based on portfolio 5.2E (3) Pneumatic pumping

12

13 14

Secondary / Enhanced Recovery

DCF, January 2, 200618

Refining System

Salamanca• 245 Mbd• 1,929 KEDC, C.I. = 8.8• Supplies fuels for central

and western areas• Base lubricant production

Madero• 195 Mbd• 2,996 KEDC, C.I. = 15.8• Supplies fuels for

Central and Gulf Areas

Tula• 320 Mbd• 3,408 KEDC, C.I. = 11.0• Supplies fuels for

MCMA(2), Morelos and Guerrero

Salina Cruz• 330 Mbd• 2,869 KEDC, C.I. = 8.8• Supplies fuels for Pacific Coast

Cadereyta• 275 Mbd• 3,313 KEDC, C.I. = 13.1• Supplies fuels for northern area

Refining System • KEDC(1): 2,675• Complexity Index (C.I.): 11.3

(1) K=1,000; EDC=Equivalent Distillation Capacity(2) MCMA = Mexico City’s Metropolitan Area

Salamanca

Madero

Tula

Salina Cruz

Cadereyta

Minatitlán

Minatitlán• 200 Mbd• 1,538 KEDC, C.I. = 7.7• Supplies fuels for southern

area and Yucatán Peninsula

DCF, January 2, 200619

Refining

Modernization of the refining system

Increase in heavy crude processing capacity

Raise output of high value added refined products

Meet international standards of quality in gasolines and diesel

Real time monitoring of the pipeline system

Main projects

Distribution (SCADA, maritime terminals modernization)Production facilities (Minatitlán revamping, residual conversion in Tula and Salamanca)Gasolines and diesel (improvements in quality by lower sulfur content)

Minatitlán refinery revamping is expected to be finished in 2009– Total estimated CAPEX:

MMMUS$2.4– Expected incremental production of

gasolines: 86 Mbd– Expected incremental production of

intermediate distillates: 47 Mbd

DCF, January 2, 200620

Natural Gas

Increase processing capacity

Enhance flexibility of the transportation system

Raise import-export capacity (currently, there are ten interconnections with the U.S.)

Capacity expansion of the processing system in northern Mexico to capture natural gas liquids (6 cryogenic plants: 2 started operations in 2004, 2 are under construction and 2 more are expected to be constructed in the following years)

New compression stations to increase the transport capacity in the Central and South Western Regions of Mexico

Step up processing and improve transportation

Main projects

Gas processing centers

Pipelines (km): 9,109Sweetening plantscapacity(1) (MMcfd): 4,503Liquids recovery plantscapacity(1) (MMcfd): 5,546

(1) 92% of the sweetening capacity and 69% of the liquids recovery capacity is located in Cd. Pemex, Cactus and Nuevo Pemex

nReynosa

n

Poza RicaCd Pemex

Nuevo PemexCactus

Matapionchenn

nn n

n

La VentanBurgosnArenque

Coatzacoalcos area(Cangrejera, Morelos, Pajaritos)

DCF, January 2, 200621

Petrochemicals

Invest in profitable petrochemical chains

Possible joint ventures with private sector in minority role companies to integrate the value chains

Capacity expansions on the ethane chain and the aromatic chain in order to meet domestic demand and reduce imports

Seize opportunities

Main projects

5

5

5

5

55

Camargo

Tula

San Martín Texmelucan

Pajaritos

Cosoleacaque Cangrejera

Morelos5

5

Escolín

Petrochemical centers

On September 15, 2004, a resolution was published in the Official Gazette of the Federation (Diario Oficial de la Federación) authorizing the Ministry of Energy to carry out the merger of the seven subsidiaries of Pemex-Petrochemicals. On September 15, 2005, the Ministry of Energy requested a 6 months extension

Pemex-Petrochemicals’ subsidiary companies consolidation

DCF, January 2, 200622

Agenda

PEMEX Highlights

Lines of Business

CAPEX and Financing Program

New Fiscal Regime

Looking Forward

DCF, January 2, 200623

SGP(2) (8%)

Burgos (10%)

KMZ(1) (6%)

A. J. Bermúdez (2%)

Cantarell (26%)

Others (28%)

CAPEX 2001-2005100% = MMMUS$ 40.5

Oil productionMbd

0

1,000

2,000

3,000

4,000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Chuc, Jujo yEl Golpe (4%)

Exploration (16%)

Natural gas productionMMcfd

0100020003000400050006000700080009000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Forecast

Forecast

Oil and Gas Production and E&P CAPEX

(1) Ku-Maloob-Zaap(2) Strategic Gas Program

DCF, January 2, 200624

Historical and Projected CAPEX

6.4 5.8

8.3

3.12.0 1.6 1.0 1.1 1.8 1.6 1.9 2.5 2.8 3.0

2.1 2.03.1 3.6 3.1 2.6 3.0 3.0 2.2 1.7 1.1 1.8

0.6 2.0 2.9

4.5 3.9 5.68.4 9.8

9.9

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05E

MMMUS$ PIDIREGAS

Non - PIDIREGAS

PIDIREGAS: Long-term productive infrastructure projects(1) Authorized by the Ministry of Finance on May 20, 2005 (Adecuado III)

5.15.5

7.56.9

7.8

10.110.9

4.2

11.7

(1)

DCF, January 2, 200625

CAPEX 2005

11.7Total

0.1Others

0.2Petrochemicals

0.4Gas and Basic Petrochemicals

1.2Refining

9.8Exploration and Production

2005E (1) CAPEX 2005E100% = MMM US$11.7 (1)

(1) Authorized by the Ministry of Finance on May 20, 2005 (Adecuado III)

10%2%

84%

1% 3%

CAPEXMMM US$

DCF, January 2, 200626

EBITDA and Interest Coverage

15.9x15.2x

2003 2004

33.2

45.0

2003 2004

EBITDA / InterestEBITDA

Note: EBITDA net of sales taxes (IEPS). Interest expense does not include capitalized interest

MMMUS$ Times

DCF, January 2, 200627

Debt-to-Reserves Ratio vs. Peers

Source: Companies’ 2004 Annual Reports, 2004 20-F’s, 2004 Financial Results1) Audited financial statements and proved reserves data as of December 31, 2004. Debt is the sum of documented debt, notes

payable to contractors and sale of future account receivable

Debt / Proved reservesUS$ / boe

2.5

2.0 1.9 1.8

1.41.2

1.0 1.0

0.4

ConocoPhillips

BP Petrobras Stat Oil RD Shell Total ChevronTexaco

ExxonMobil

(1)

DCF, January 2, 200628

Credit Profile Relative to Integrated Majors

Source: Companies’ 2004 Annual Reports, 2004 20-F’s, 2004 Financial Results1) Data as of December 31, 2004, PEMEX’s proved reserves in accordance with the definition of proved reserves

under Rule 4.10(a) of Regulation S-X under the U.S. Securities Act of 1933

Senior Unsecured RatingsS&PMoody´sFitch

Operating DataProved Reserves (MMMboe) (1)

Production (MMboed)Proved Reserves Life (years)CAPEX (MMMUS$)

Exxon Mobil

BBBBaa1BBB-

17.64.4

11.010.9

Aa1

11.93.8

8.613.6

AA+Aa1AA+

14.64.0

10.014.5

AAAAaaAAA

22.04.2

14.314.9

AAAa2AA

11.12.6

11.811.8

AAAa2AA

11.32.5

12.38.3

A-A3A-

7.61.6

13.09.5

RD Shell

Total BP Chevron Texaco

ConocoPhillips

Ba1BB-

11.81.5

21.77.4

Petrobras

AAA2

4.31.1

10.67.0

Statoil(2)

DCF, January 2, 200629

Agenda

PEMEX Highlights

Lines of Business

CAPEX and Financing Program

New Fiscal Regime

Looking Forward

DCF, January 2, 200630

PEMEX’s New Fiscal Regime: Introduction

• The purpose of the new fiscal regime is to strengthen PEMEX’s competitiveness and contribute to improving its financial position

• The new fiscal regime is in effect since January 1, 2006

• On December 21, 2005, PEMEX’s new fiscal regime was published in the Official Gazette of the Federation (Diario Oficial de la Federación)

• Under the new structure, taxes and duties for E&P are established in the “LeyFederal de Derechos”. Taxes and duties for the rest of the subsidiary entities remain included in the “Ley de Ingresos de la Federación”(oil income tax)

DCF, January 2, 200631

Agenda

PEMEX Highlights

Lines of Business

CAPEX and Financing Program

New Fiscal Regime

Looking Forward

DCF, January 2, 200632

Looking Forward

• Implementing value management oriented to efficiency

• Implement corporate governance best practices

Looking forward

DCF, January 2, 200633

Implementing Value Management Oriented to Efficiency

• Process reengineering

• Implementing best practices in projects management

• Optimization of plants and pipelines

• Optimization of the procurement process

• Value management for corporate services (medical and telecom)

• Implementing compensation according to performance

DCF, January 2, 200634

Implement Corporate Governance Best Practices

• Lack of transparency and accountability of the management process

• PEMEX budget part of the federal budget

• Overburden and inefficient audit system

• Legal restrictions for joint ventures

• These “problems” are means of controls over the administration

• All firms face the problem of the separation of ownership from management

• The solution to this problem is “Best Practices”- Corporate Governance

DCF, January 2, 200635

Modernization of PEMEX

• New fiscal regime• Independence from the federal

budget• Issuance of quasi-shares

Financial flexibility

• More efficient audit system• New procurement laws• Joint ventures

Operational flexibility

• New corporate governance creates accountability and transparency

• Continue to incorporate best practices:– Independent board members– Board Committees– Prompt disclosure of

information– Compensation based on

performance– Clear mandate to create

value– OECD guidelines on the

corporate governance of state-owned enterprises

DCF, January 2, 200636

www.pemex.com

Contact information:

Investor Relations(52 55) 1944 9700