de la rue plcinvestors.delarue.com/.../prelim-presentation-2012.pdf2009 2010 2011 2012f (bn) paper...

TRANSCRIPT

© De La Rue 2012

Full Year Results

29 May 2012

De La Rue plc

© De La Rue 2012

Agenda

Group Headlines

Financial Results

Business and Markets

Delivering the Improvement Plan

Outlook

2

© De La Rue 2012

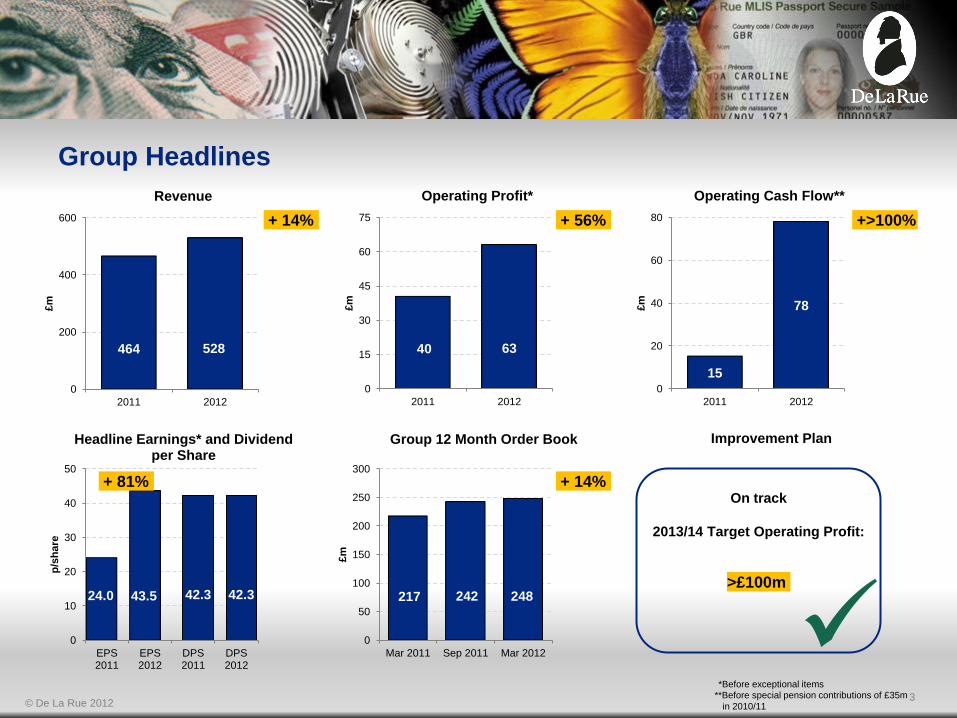

24.0 43.5 42.3 42.3

0

10

20

30

40

50

EPS 2011

EPS 2012

DPS 2011

DPS 2012

p/s

hare

Headline Earnings* and Dividend per Share

Group Headlines

15

78

0

20

40

60

80

2011 2012

£m

Operating Cash Flow**

217 242 248

0

50

100

150

200

250

300

Mar 2011 Sep 2011 Mar 2012

£m

Group 12 Month Order Book

40 63

0

15

30

45

60

75

2011 2012

£m

Operating Profit*

464 528

0

200

400

600

2011 2012

£m

Revenue

**Before special pension contributions of £35m

in 2010/11

*Before exceptional items

+ 14% + 56% +>100%

On track

2013/14 Target Operating Profit:

+ 81% + 14%

Improvement Plan

>£100m

3

© De La Rue 2012

Financial Results

Colin Child

Group Finance Director

© De La Rue 2012

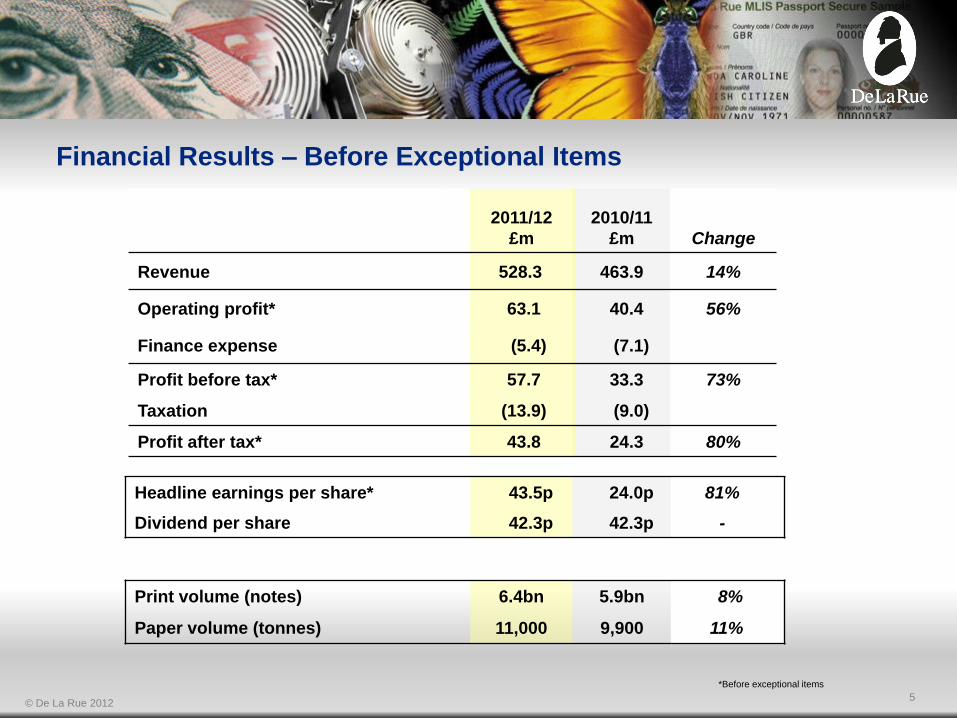

Print volume (notes) 6.4bn 5.9bn 8%

Paper volume (tonnes) 11,000 9,900 11%

Headline earnings per share* 43.5p 24.0p 81%

Dividend per share 42.3p 42.3p -

2011/12

£m

2010/11

£m Change

Revenue 528.3 463.9 14%

Operating profit* 63.1 40.4 56%

Finance expense (5.4) (7.1)

Profit before tax* 57.7 33.3 73%

Taxation (13.9) (9.0)

Profit after tax* 43.8 24.3 80%

Financial Results – Before Exceptional Items

5

*Before exceptional items

© De La Rue 2012

2011/12

£m

2010/11

£m

Improvement plan (24.1) -

Curtailment gain on closure of defined benefit pension

scheme - 16.0

Paper production quality issues (0.7) (29.0)

Corporate costs - (2.6)

Profit on sale of Camelot investment - 55.1

Total exceptional items (24.8) 39.5

Tax credit on exceptional items 13.2 3.6

Exceptional Items

6

© De La Rue 2012

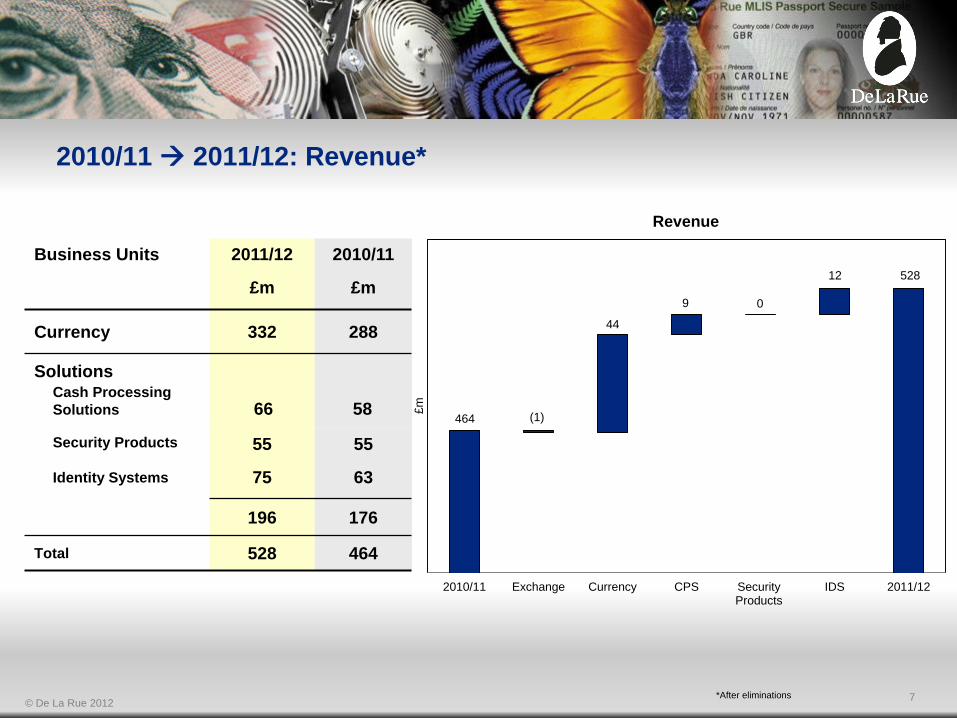

Business Units 2011/12

£m

2010/11

£m

Currency 332 288

Solutions Cash Processing

Solutions

Security Products

Identity Systems

55

75

55

63

196 176

Total 528 464

2010/11 Exchange Currency CPS Security Products

IDS 2011/12

£m

(1)

2010/11 2011/12: Revenue*

Revenue

464

44

9 0

12 528

7 *After eliminations

66 58

© De La Rue 2012

Business Units 2011/12

£m

2010/11

£m

Currency 45 28

Solutions Cash Processing

Solutions

Security Products

Identity Systems

7

9

9

3

18 12

Total 63 40

2010/11 Cotton Price

Exchange Improvement Plan

IDS Mix/Volume Other 2011/12

£m

2010/11 2011/12: Operating Profit*

Operating Profit*

40 (9)

(1)

5

8

(3)

63

23

8 *Before exceptional items

2 -

© De La Rue 2012

2011/12

£m

2010/11

£m

Operating profit before exceptional items 63.1 40.4

Depreciation 26.6 24.4

Working capital 11.9 (14.4)

Pension fund contributions (23.1) (7.5)

Other 3.6 (1.7)

Operating cash flow before special pension

contribution & operating exceptional items 82.1 41.2

Special pension fund contribution - (35.0)

Cash costs of exceptional items (3.7) (26.5)

Cash flow from operating activities 78.4 (20.3)

Operating Cash Flow

9

© De La Rue 2012

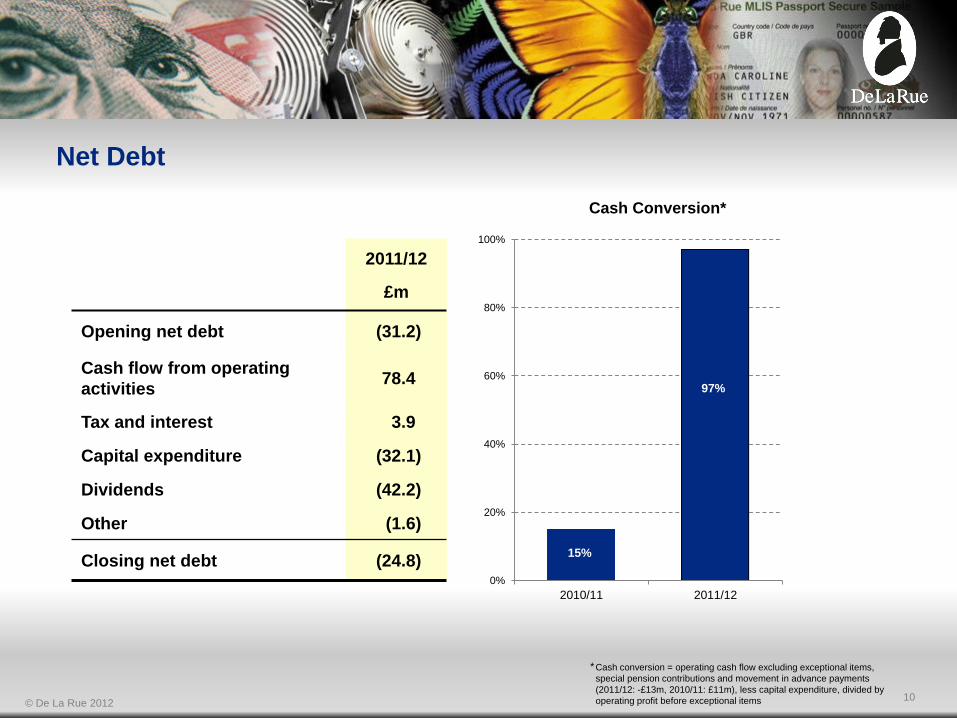

2011/12

£m

Opening net debt (31.2)

Cash flow from operating

activities 78.4

Tax and interest 3.9

Capital expenditure (32.1)

Dividends (42.2)

Other (1.6)

Closing net debt (24.8)

Net Debt

Cash conversion = operating cash flow excluding exceptional items,

special pension contributions and movement in advance payments

(2011/12: -£13m, 2010/11: £11m), less capital expenditure, divided by

operating profit before exceptional items

94%

15% 0%

20%

40%

60%

80%

100%

2010/11 2011/12

Cash Conversion*

97%

15%

*

10

© De La Rue 2012

Business and Markets

Tim Cobbold

Chief Executive

© De La Rue 2012

De La Rue Business Overview

Banknote substrates and security features

Design, origination and printing

High speed cash sorting and inspection

equipment

Service, maintenance and spares

Cash management solutions

Design, origination and printing of secure

products

Tax stamp and authentication solutions

Currency

Proportion of

Group 2011/12

63% 72%

12% 3%

11% 12%

14% 13%

Revenue Operating

Profit

So

luti

on

s

Cash

Processing

Solutions

Security

Products

Identity

Systems

Design, origination and printing of identity

documents

Personalisation solutions

12

© De La Rue 2012

0

40

80

120

160

200

2009 2010 2011 2012F 2015F

Ban

kn

ote

s (

bn

)

Global Banknote Issuance** - CAGR 4%

100

200

300

400

500

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Ind

ex

Value of Cash in Circulation*

Currency Market – Robust Long Term Growth

supply

cash issued

withdrawn

cash

Destruction

Banknote

Supplier

Central

Bank

Stock

Cash Cycle

Cash

Centre

Nigeria

US

Brazil

UK

Global Banknote Issuance has 4% CAGR over the

past 20 years**

Malaysia

CAGR

13

17%

15%

5%

6%

9%

**Source: Estimates De La Rue

*Source: IMF, May 2012

© De La Rue 2012

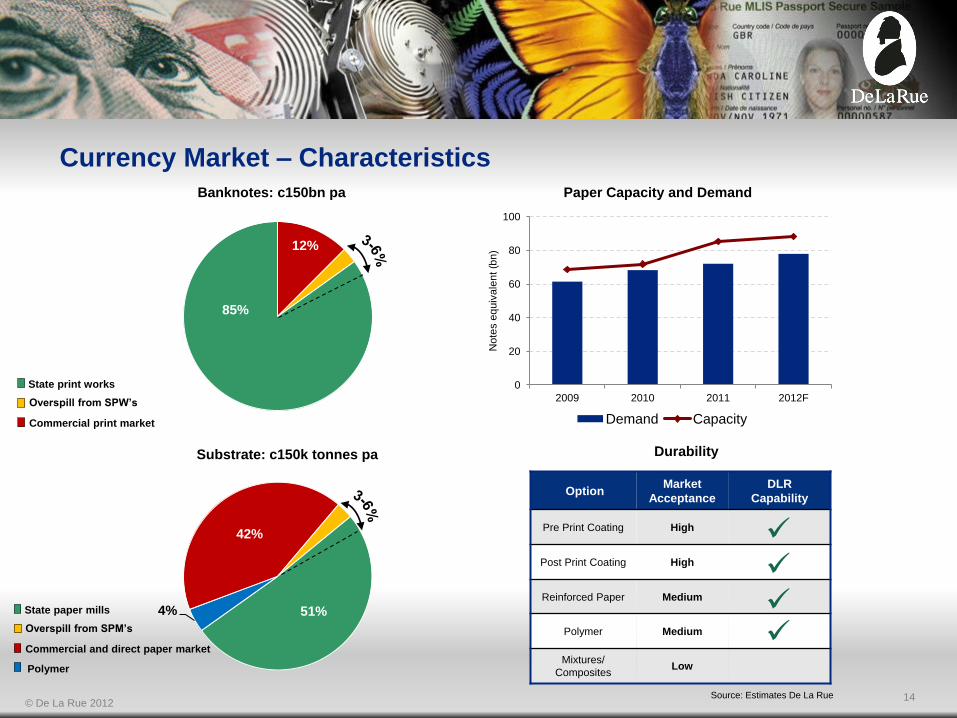

12%

85%

Banknotes: c150bn pa

42%

51% 4%

Substrate: c150k tonnes pa Durability

0

20

40

60

80

100

2009 2010 2011 2012F

No

tes e

quiv

ale

nt

(bn)

Paper Capacity and Demand

Demand Capacity

Currency Market – Characteristics

Option Market

Acceptance

DLR

Capability

Pre Print Coating High

Post Print Coating High

Reinforced Paper Medium

Polymer Medium

Mixtures/

Composites Low

Commercial print market

Overspill from SPW’s

State print works

Commercial and direct paper market

Overspill from SPM’s

State paper mills

Polymer

14 Source: Estimates De La Rue

© De La Rue 2012 Source: Estimates De La Rue

15

Integrated Presence – Print and Substrate

De La Rue

Oberthur

Other

De La Rue Distribution of

Currency Sales

UK & Ireland Central

&South

America

De La Rue

G&D

Arjo

Crane

Securency

Fabriano

Other

Print : Available Market Share

Middle East

Africa

Rest of

the World

Far East

& Asia

Substrate : Available Market Share

G&D

© De La Rue 2012

Integrated Presence – Technology & Design

Technology – Providing Security

Depth™ Thread

Holographic

Stripe

StarChrome®

colourshift

thread (red)

StarChrome®

colourshift thread

(green)

Watermark

Intaglio

Invisible

Fluorescent

Thread

backlit

Micro-printing

Design – Reflecting National Identity

De La Rue customer banknotes

have won every major industry

design award in the past five years.

16

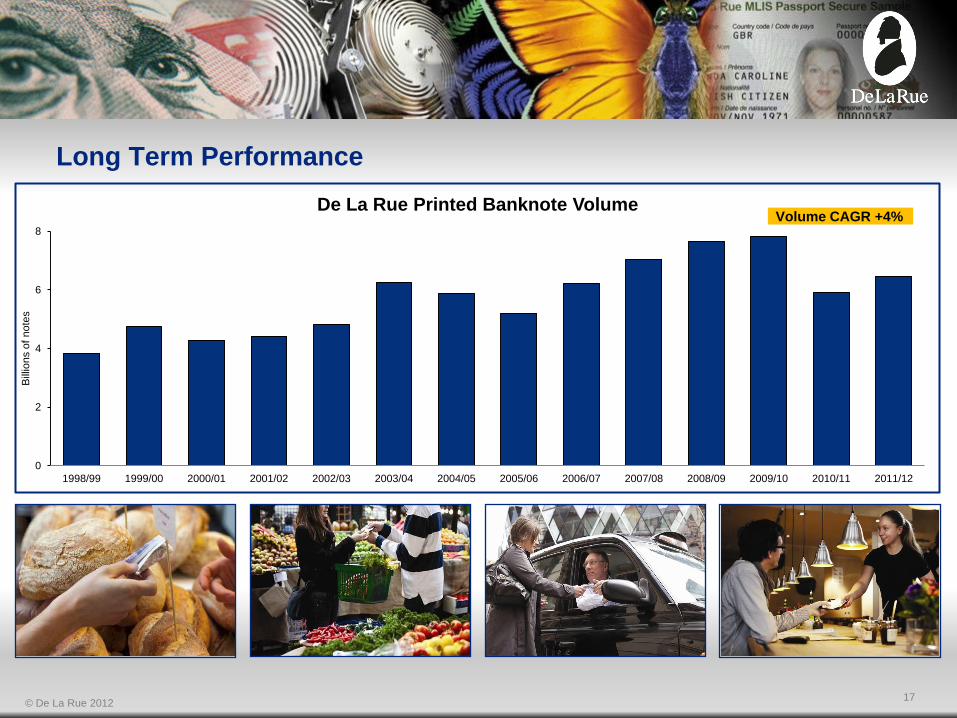

© De La Rue 2012

0

2

4

6

8

1998/99 1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

Bill

ions o

f note

s

De La Rue Printed Banknote Volume

Long Term Performance

Volume CAGR +4%

17

© De La Rue 2012

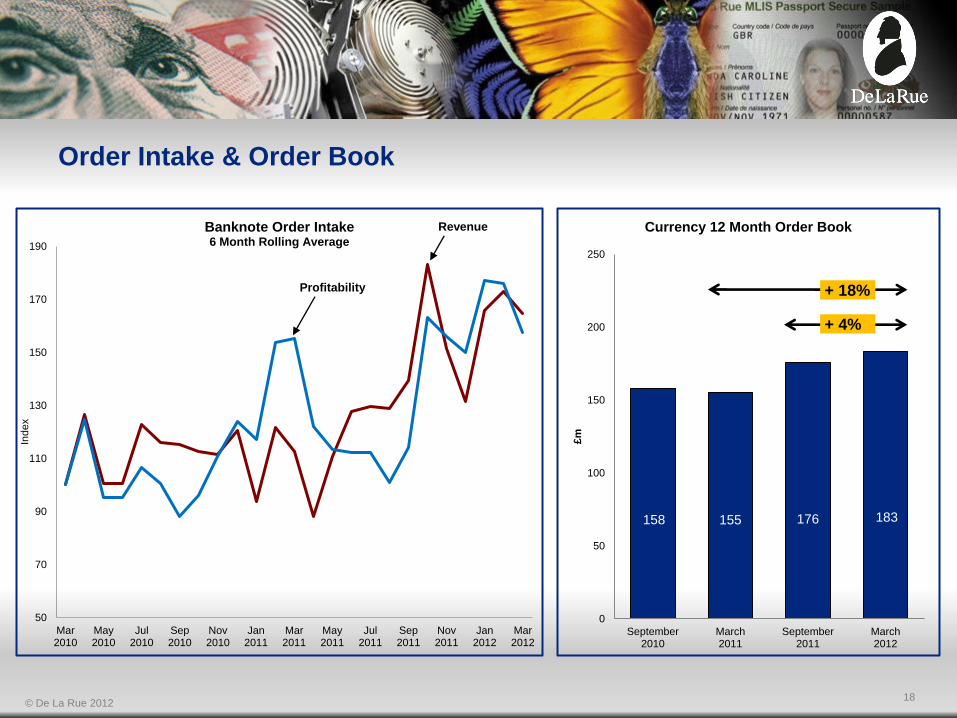

Order Intake & Order Book

50

70

90

110

130

150

170

190

Mar 2010

May 2010

Jul 2010

Sep 2010

Nov 2010

Jan 2011

Mar 2011

May 2011

Jul 2011

Sep 2011

Nov 2011

Jan 2012

Mar 2012

Ind

ex

Banknote Order Intake 6 Month Rolling Average

158 155 176 183

0

50

100

150

200

250

September 2010

March 2011

September 2011

March 2012

£m

Currency 12 Month Order Book

+ 18%

+ 4%

Revenue

Profitability

18

© De La Rue 2012

Solutions – Moving Forward

Pe

rfo

rman

ce

Ca

se S

tud

y

Cash Processing Solutions

40

50

60

70

2011 2012

£m

Revenue

0

5

10

2011 2012

£m

Operating Profit*

Security Products

50

55

60

2011 2012 £

m

Revenue

0

5

10

2011 2012

£m

Operating Profit*

50

60

70

80

2011 2012

£m

Revenue

Identity Systems

0

10

20

2011 2012

£m

Operating Profit*

Vaultex UK Ltd Long term partnership approach

Equipment & Business Intelligence

Software Solutions

UK Passport £400m contract over 10 years

Over 7 million books produced

Demanding service levels

Sh

are

d

Infr

as

tru

ctu

re

Sales & Pipeline Management

Solution Design & Project Management

Commercial Marketing

Finance

Service

Cameroon Tax Stamps Tobacco and Alcohol labels launched

Pharmaceutical labels to follow

Track and Trace system in final phase

Training of enforcement officers underway

*Before exceptional items

19

© De La Rue 2012

Delivering the Improvement Plan

Tim Cobbold

Chief Executive

© De La Rue 2012

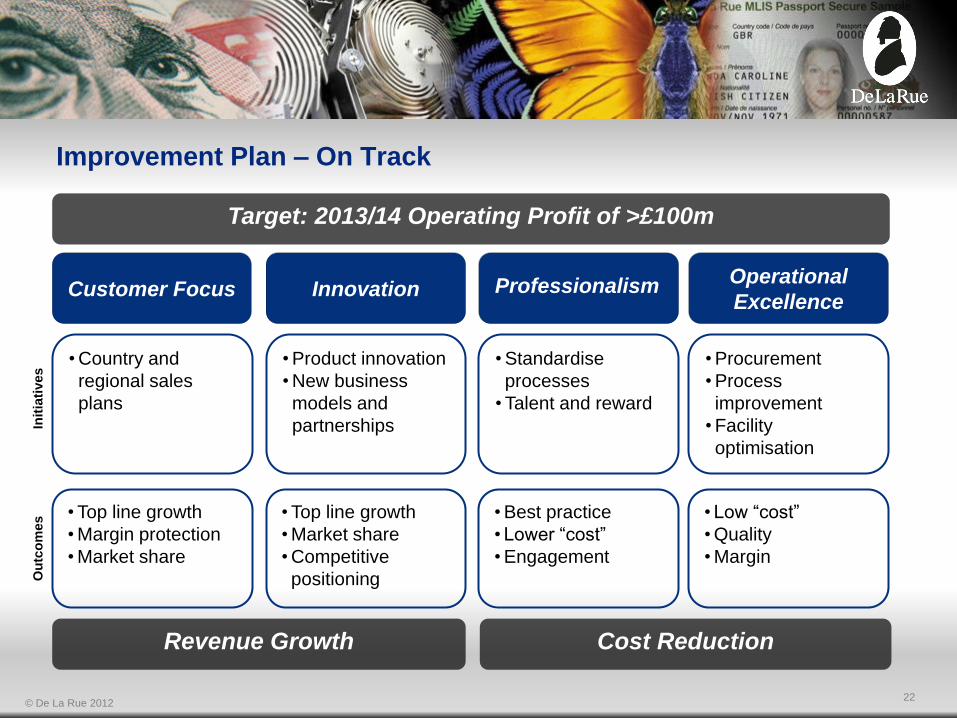

Improvement Plan

Target: 2013/14 Operating Profit of >£100m

Opportunities Fundamental Strengths

Brand and reputation

Long standing customer relationships

Strong integrated competitive position

Record of innovation

High margin, cash generative model

Focus, focus, focus

Deepen and broaden „One De La Rue‟

Improve sales and marketing

effectiveness

Maximise technological capability

Develop supply chain

21

© De La Rue 2012

Improvement Plan – On Track

Revenue Growth

Innovation Operational

Excellence Customer Focus

• Product innovation

• New business

models and

partnerships

• Top line growth

• Market share

• Competitive

positioning

• Standardise

processes

• Talent and reward

• Best practice

• Lower “cost”

• Engagement

• Low “cost”

• Quality

• Margin

• Country and

regional sales

plans

• Top line growth

• Margin protection

• Market share

Init

iati

ve

s

Ou

tco

me

s

Cost Reduction

Target: 2013/14 Operating Profit of >£100m

Professionalism

• Procurement

• Process

improvement

• Facility

optimisation

22

© De La Rue 2012

New Structure & Organisation – Operational

Currency

£332m

Solutions

£196m

Currency

£332m

Cash Processing

Solutions £66m

Security Products

£55m

Identity Systems

£75m

Legal & Company

Secretarial

Finance

Human Resources

Currency

Solutions

Strategy & Business

Development

Business

Transformation Supply Chain

Customer Focus Innovation Professionalism

23

Operational

Excellence

© De La Rue 2012

Full Potential Country Plan

Stage III

Actions

identified and in

process

Stage I

Identify

opportunities

Customer Focus – Country Plans – Identifying Opportunities

Stage II

Set vision and

targets

„One De La Rue‟ approach

Technology led

Focus on partnerships

„Out of the box‟ thinking

Added value service and support COMPLETE

>40 Countries

COMPLETE

>40 Countries

COMPLETE

13 Countries

24

„A‟

„To partner with the

government for the supply

of high profile national

security documents;

passports, banknote paper,

sorters and tax stamp

solutions.’

<£1m pa <£4m pa

£20m pa £8m pa

‘To be the partner of choice

for the production of secure

documents and their

authentication solutions as

well as to develop access

to the commercial market

for sorting machines and

software.’

Country

Strategic

vision

Sales last

5 years

Full

potential

„B‟

© De La Rue 2012

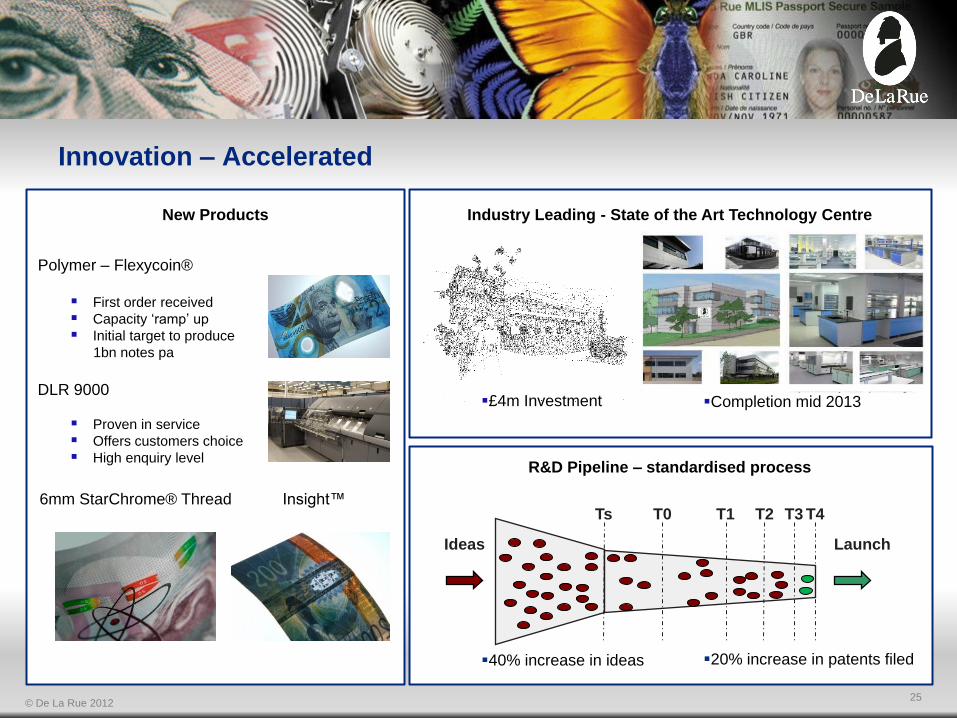

Innovation – Accelerated

New Products

Polymer – Flexycoin®

First order received

Capacity „ramp‟ up

Initial target to produce

1bn notes pa

DLR 9000

Proven in service

Offers customers choice

High enquiry level

Industry Leading - State of the Art Technology Centre

£4m Investment

Ideas Launch

Ts T0 T1 T2 T4 T3

Completion mid 2013

R&D Pipeline – standardised process

40% increase in ideas 20% increase in patents filed

6mm StarChrome® Thread Insight™

25

© De La Rue 2012

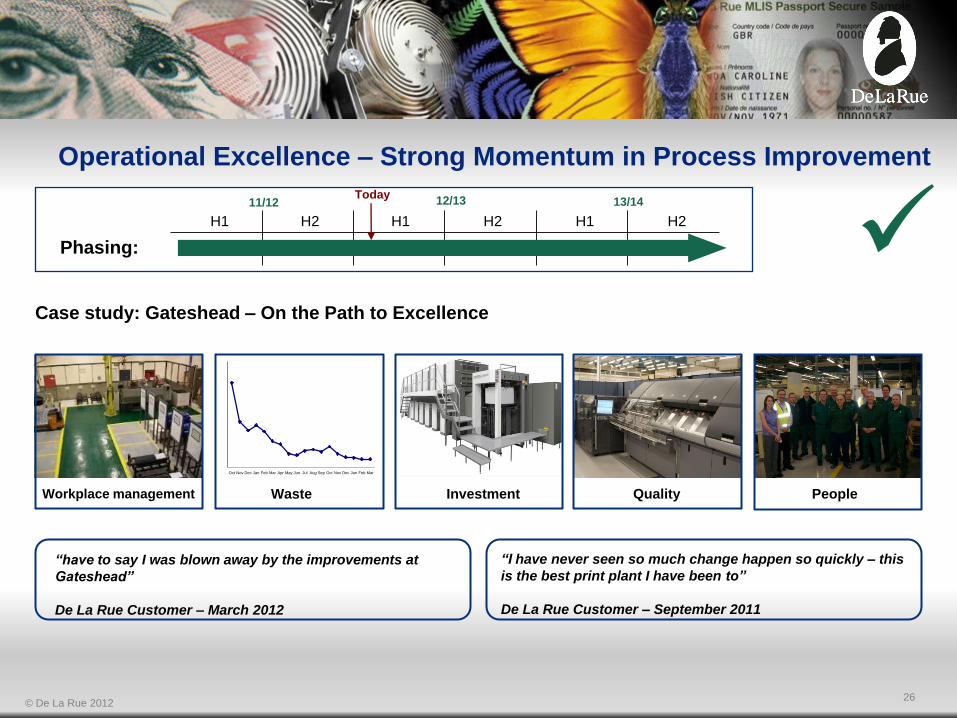

Operational Excellence – Strong Momentum in Process Improvement

0%

5%

10%

15%

20%

25%

30%

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Workplace management Waste Investment Quality People

Phasing:

13/14 11/12 12/13 Today

H2 H1 H2 H1 H2 H1

Case study: Gateshead – On the Path to Excellence

“I have never seen so much change happen so quickly – this

is the best print plant I have been to”

De La Rue Customer – September 2011

“have to say I was blown away by the improvements at

Gateshead”

De La Rue Customer – March 2012

26

© De La Rue 2012

Phase

Targeted/

Negotiated

Savings

I 4

II 6

III 2

Total 12

Cumulative Delivered

Savings

2011/12

£m pa

2012/13 E.

£m pa

5 10

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Apr 2009

Sep 2009

Feb 2009

Jul 2010

Dec 2010

May 2011

Oct 2011

Mar 2012

$ p

er

to

nn

e

Operational Excellence – Procurement Delivering

13/14 11/12 12/13

Phasing:

H2 H1 H2 H1 H2 H1

I III II IV Phase I to III: Consolidation of Supply Base

Phase IV: Key Supplier Management – Accelerated Top 25 suppliers

Supplier manual

Cotton (Comber) Market Prices

Supplier audit

QCD and security performance analysis

27

Today

£m pa

© De La Rue 2012

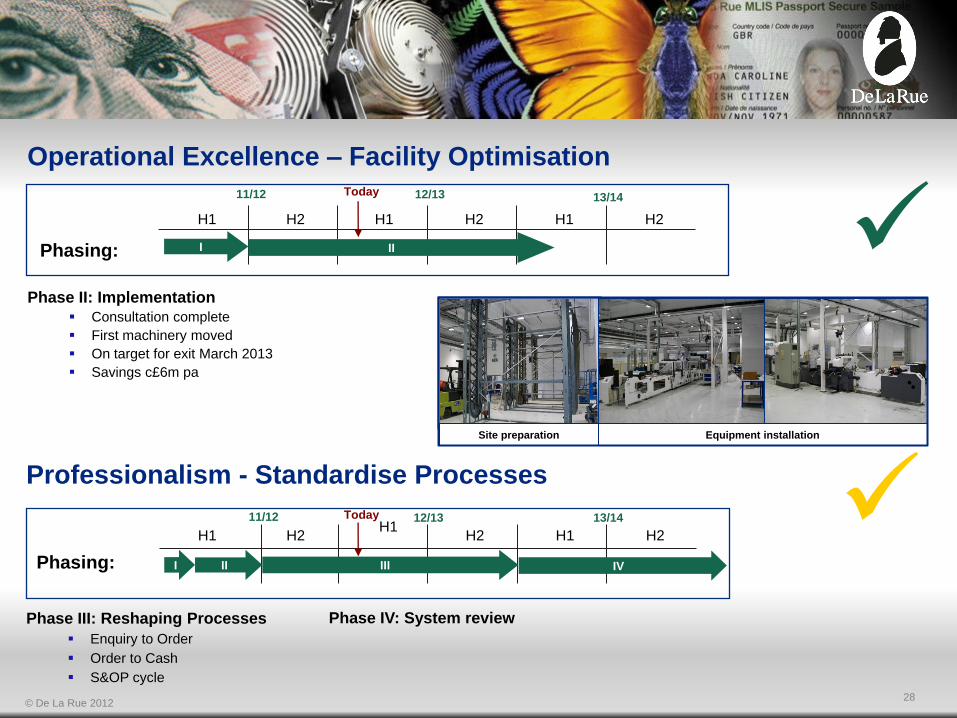

Professionalism - Standardise Processes

Phase III: Reshaping Processes

Enquiry to Order

Order to Cash

S&OP cycle

H2 H1

Phasing:

13/14 11/12 12/13

H2 H1 H2 H1

I III II IV

Phase II: Implementation

Consultation complete

First machinery moved

On target for exit March 2013

Savings c£6m pa

13/14 11/12 12/13

Phasing:

H2 H1 H2 H1 H2 H1

I II

Site preparation Equipment installation

Phase IV: System review

Operational Excellence – Facility Optimisation

28

Today

Today

© De La Rue 2012

Improvement Plan Generating Value for Shareholders

Target Historic revenue growth 4%

Cost reduction £30m

2013/14 Operating profit in excess of £100m

Investment Exceptional costs up to £35m

Capital expenditure phased towards

second and third years ~ £20m

Confidence in delivery

29

© De La Rue 2012

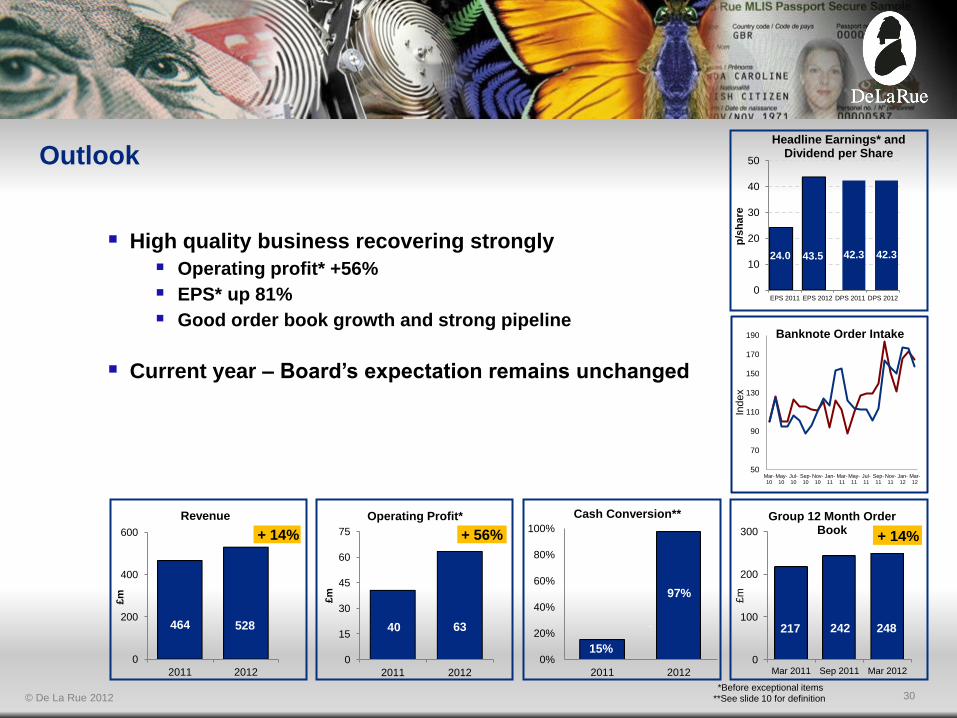

High quality business recovering strongly

Operating profit* +56%

EPS* up 81%

Good order book growth and strong pipeline

Current year – Board’s expectation remains unchanged

217 242 248

0

100

200

300

Mar 2011 Sep 2011 Mar 2012

£m

Group 12 Month Order Book

15%

97%

0%

20%

40%

60%

80%

100%

2011 2012

Cash Conversion**

9464 528

0

200

400

600

2011 2012

£m

Revenue

40 63

0

15

30

45

60

75

2011 2012

£m

Operating Profit*

+ 14% + 56% + 14%

50

70

90

110

130

150

170

190

Mar-10

May-10

Jul-10

Sep-10

Nov-10

Jan-11

Mar-11

May-11

Jul-11

Sep-11

Nov-11

Jan-12

Mar-12

Ind

ex

Banknote Order Intake

30

Outlook

24.0 43.5 42.3 42.3

0

10

20

30

40

50

EPS 2011 EPS 2012 DPS 2011 DPS 2012

p/s

hare

Headline Earnings* and Dividend per Share

**See slide 10 for definition

*Before exceptional items

© De La Rue 2012 31