directors & officers bootcamp basics of duties & liabilities rian jorgensenadrian atilano...

TRANSCRIPT

Directors & Officers BootcampBasics of Duties & Liabilities

Rian Jorgensen Adrian AtilanoSenior Vice President Vice PresidentFINPRO FINPROSan Francisco, CA San Diego, CA

January 26, 2007

2

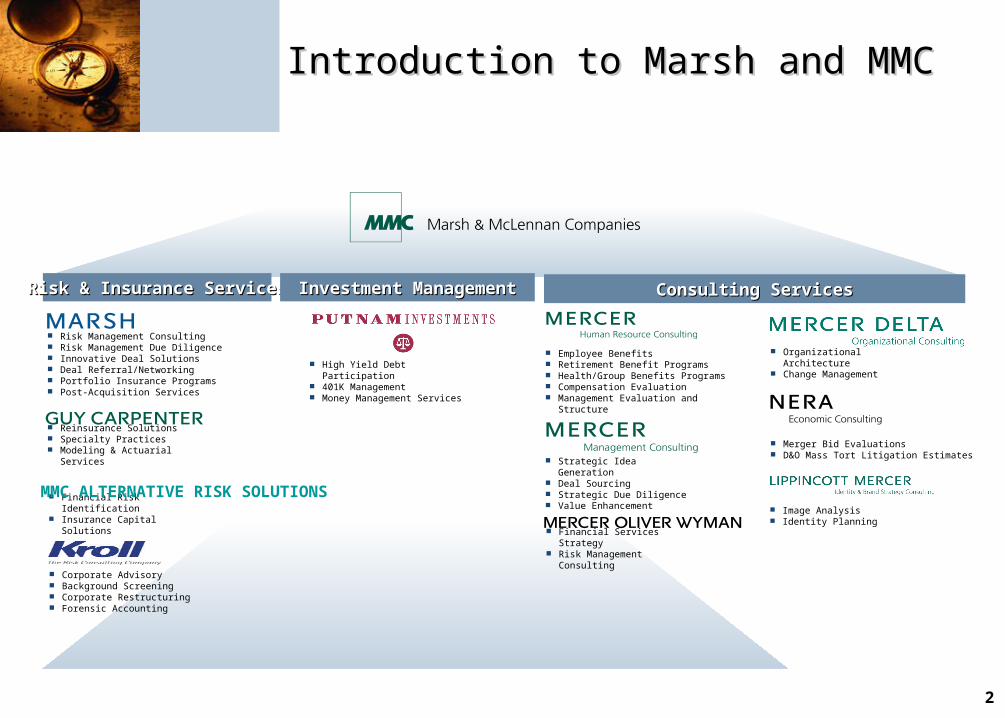

Introduction to Marsh and MMCIntroduction to Marsh and MMC

Merger Bid Evaluations D&O Mass Tort Litigation Estimates

Consulting ServicesConsulting Services

Risk Management Consulting Risk Management Due Diligence Innovative Deal Solutions Deal Referral/Networking Portfolio Insurance Programs Post-Acquisition Services

Employee Benefits Retirement Benefit Programs Health/Group Benefits Programs Compensation Evaluation Management Evaluation and Structure

High Yield Debt Participation 401K Management Money Management Services

Strategic Idea Generation Deal Sourcing Strategic Due Diligence Value Enhancement

Financial Risk Identification Insurance Capital Solutions

Organizational Architecture Change Management

Image Analysis Identity Planning

Reinsurance Solutions Specialty Practices Modeling & Actuarial Services

Risk & Insurance ServicesRisk & Insurance Services Investment ManagementInvestment Management

Corporate Advisory Background Screening Corporate Restructuring Forensic Accounting

Financial Services Strategy Risk Management Consulting

MMC ALTERNATIVE RISK SOLUTIONS

3

1995 PSLRA: Be Careful What You Wish For

Rise of the institutional investors (who were not as benign as the law’s drafters had hoped)

Number and severity of suits continued unabated

4

Enron, WorldCom and Tyco

Massive frauds

Personal liability (triggered much concern, for the most part, overblown, particularly for outside directors)

5

2002 SOX

Expanded statute of limitations (from 1/3 to 2/5)

Increased criminal penalties and enforcement Boost in the SEC’s enforcement division’s funding

6

NERA and Cornerstone Results

Why the drop in number of suits? Steady bull market of last few years Turmoil among the plaintiffs attorneys Less fraud due to fear of criminal prosecution

Not all good news – Many new routes to courthouse besides class actions (Opt-outs, serious derivative litigation, SEC/DOJ)

Stock option backdating cases – directors investigating (and spending the company’s money on legal fees) at the drop of a hat

7

What Does The Future Hold?

More invasive personal underwriting for D&O coverage

More uninsured legal costs for investigations (challenge for the insurance industry to address)

Movement afoot to “loosen up” SOX

Conflicts between interests of companies and their D’s and O’s to become more pronounced (broad indemnification, A-side to the extreme…)

D&O Indemnification Trends and Implications

9

How are Personal Assets of Directors and How are Personal Assets of Directors and Officers Protected?Officers Protected?

IndemnificationIndemnificationIndemnificationIndemnification InsuranceInsuranceInsuranceInsuranceBBOOTTHH

10

Indemnification

Indemnification Authorization (DE & CA)

Corporate Charter Corporate Bylaws Indemnification Contract

11

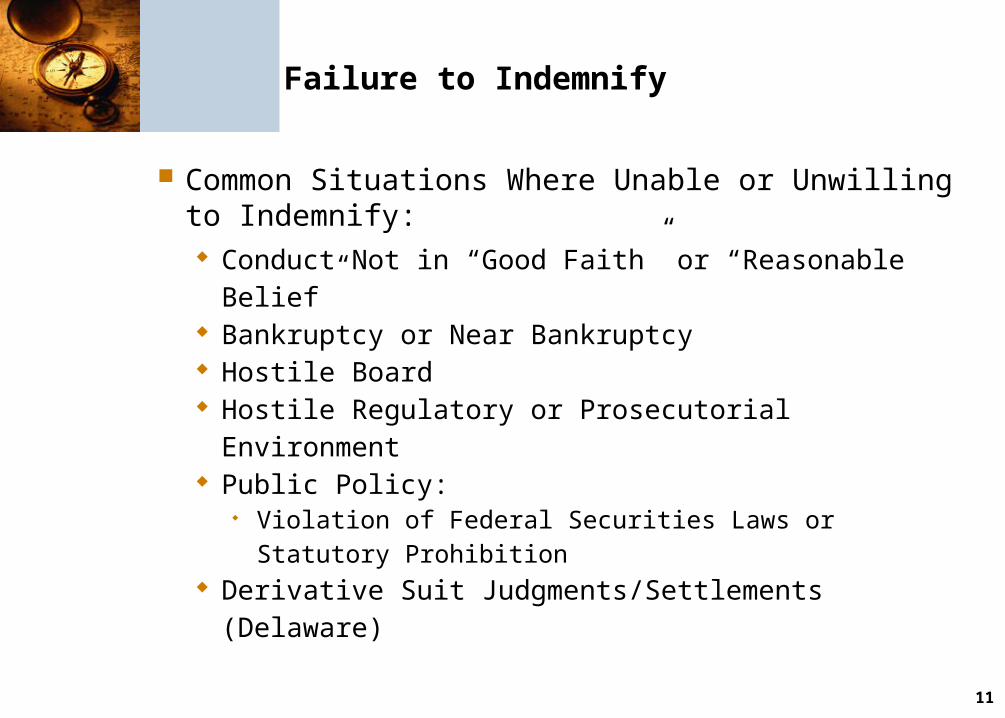

Failure to Indemnify

Common Situations Where Unable or Unwilling to Indemnify:

Conduct Not in “Good Faith” or “Reasonable Belief” Bankruptcy or Near Bankruptcy Hostile Board Hostile Regulatory or Prosecutorial Environment Public Policy:

Violation of Federal Securities Laws or Statutory Prohibition

Derivative Suit Judgments/Settlements (Delaware)

D&O Insurance Trends & Implications

13

Directors’ & Officers’ Liability InsuranceDirectors’ & Officers’ Liability Insurance

Covered Claim Against

Directors & Officers

Covered Claim Against

Directors & Officers

NoNo

Insureds -Directors & Officers

Insureds -Directors & Officers

Personal AssetsPersonal Assets

D&O InsuranceInsuring Agreement A:

Personal Liability

D&O InsuranceInsuring Agreement A:

Personal Liability

““PERSONAL ASSETS PERSONAL ASSETS PROTECTION”PROTECTION”

INDEMNIFICATION?INDEMNIFICATION?

YesYes

Insured -Corporate Balance Sheet

Insured -Corporate Balance Sheet

Corporate AssetsCorporate Assets

D&O InsuranceInsuring Agreement B:

Corporate Reimbursement

D&O InsuranceInsuring Agreement B:

Corporate Reimbursement

““CORPORATE RISK CORPORATE RISK TRANSFER”TRANSFER”

Covered Sec. Claim Against

Corporate Entity

Covered Sec. Claim Against

Corporate Entity

Insured -Corporate Entity as a

Defendant in Sec. Claims only

Insured -Corporate Entity as a

Defendant in Sec. Claims only

Corporate AssetsCorporate Assets

D&O InsuranceInsuring Agreement C:

Corporate Entity Coverage for SEC Claims

D&O InsuranceInsuring Agreement C:

Corporate Entity Coverage for SEC Claims

““SIGNIFICANT DEFENDANT SIGNIFICANT DEFENDANT ALLOCATION COVERAGE”ALLOCATION COVERAGE”

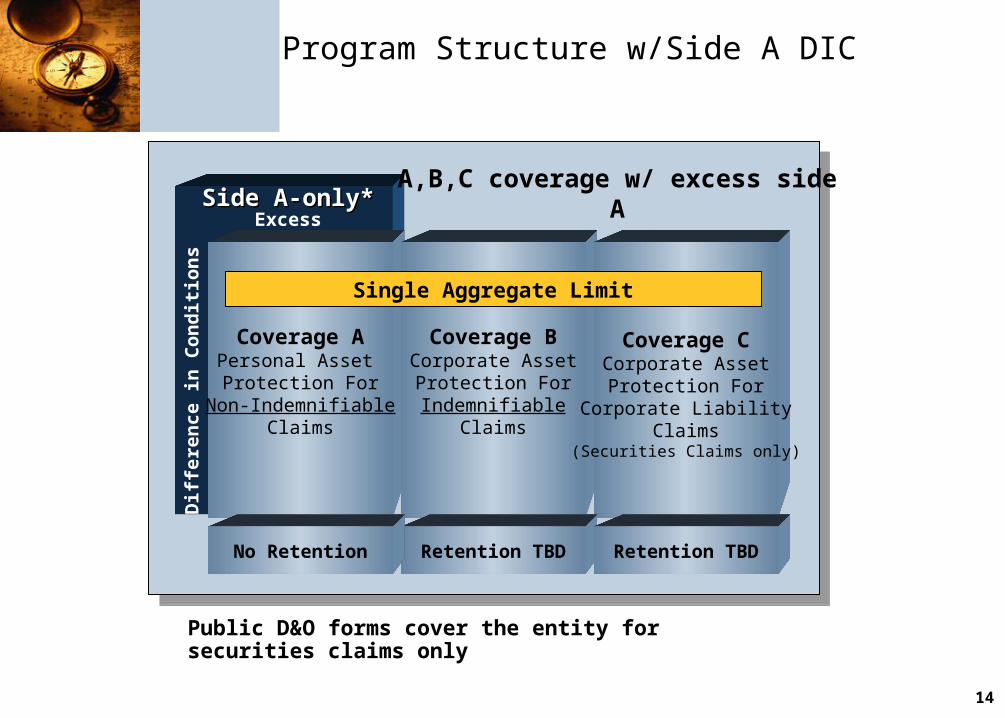

Side A Side B Side C

14

Coverage APersonal Asset Protection For

Non-IndemnifiableClaims

Coverage BCorporate AssetProtection ForIndemnifiable

Claims

Coverage CCorporate AssetProtection For

Corporate LiabilityClaims

(Securities Claims only)

Side A-only*Side A-only*Excess

Dif

fere

nce

in

Co

nd

itio

ns

Single Aggregate Limit

Retention TBDNo Retention Retention TBD

A,B,C coverage w/ excess side A

Program Structure w/Side A DIC

Public D&O forms cover the entity for securities claims only

15

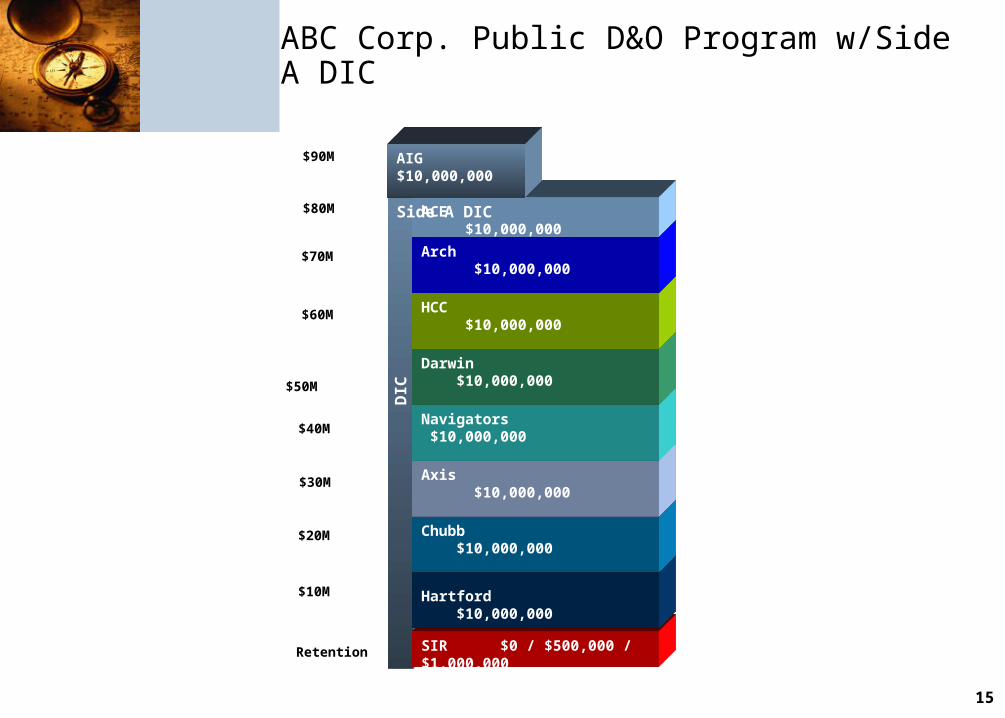

ABC Corp. Public D&O Program w/Side A DIC

SIR $0 / $500,000 / $1,000,000

Hartford $10,000,000

Chubb $10,000,000

Axis $10,000,000

$10M

$20M

$30M

Retention

Navigators $10,000,000

$40M

Darwin $10,000,000

HCC $10,000,000

$60M

Arch $10,000,000

$70M

ACE $10,000,000

$80M

$90M

$50M

DIC

AIG $10,000,000 Side A DIC

16

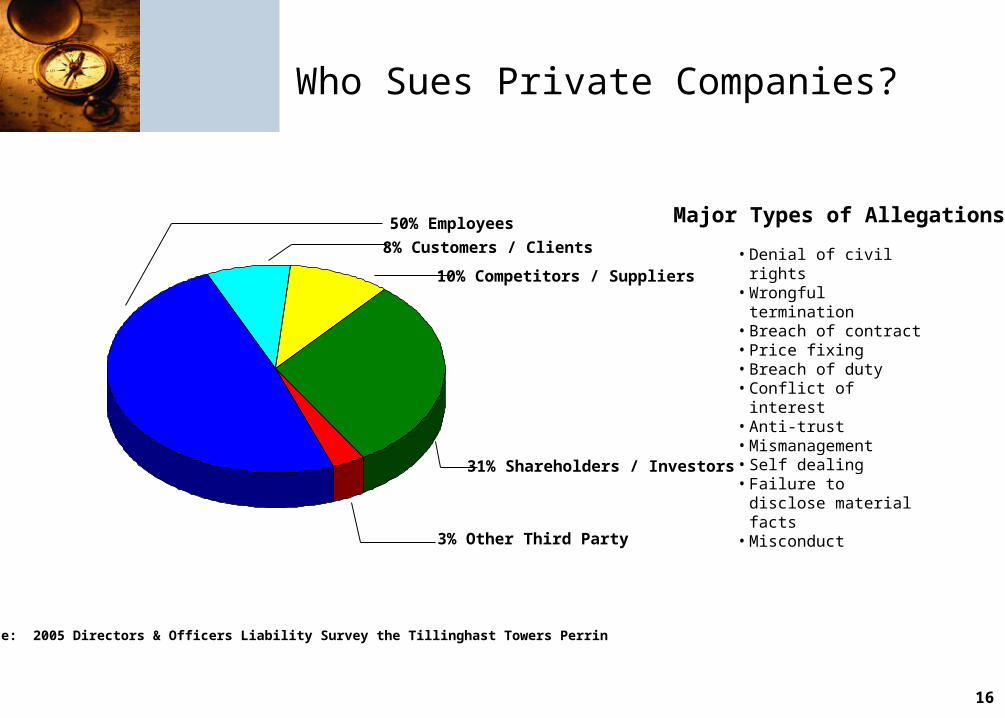

50% Employees

8% Customers / Clients

10% Competitors / Suppliers

31% Shareholders / Investors

3% Other Third Party

Source: 2005 Directors & Officers Liability Survey the Tillinghast Towers Perrin

Major Types of Allegations

• Denial of civil rights• Wrongful termination• Breach of contract• Price fixing• Breach of duty• Conflict of interest• Anti-trust• Mismanagement• Self dealing• Failure to disclose

material facts• Misconduct

Who Sues Private Companies?

17

Preparing to go public – Form Changes

Private to Public Form Changes

Add SEC coverage for individuals and Entity (securities only ) Understand severability provisions and fraud exclusions Continuity with side A and side B insuring clauses Address Employment Practices Liability exposures (separate policy) Securities Act of 1933 coverage

section 11 (material misrepresentation) section 12 (misrepresentation in prospectus or oral

communication) Securities Act of 1934 coverage

18

FAQs

Do I have to pay a retention/deductible if I am sued?

What happens if I am accused of fraudulent conduct?

Will I be covered by the D&O Insurance if someone else commits fraud?

Will I be covered by the insurance contract if someone else makes misrepresentations in the application to the D&O Insurers or if the company has to restate its financials?

Will the D&O Insurance protect me if the SEC pursues a formal investigation against me?

If the company is sued as well as directors and officers, how does the policy respond?

If the company declares bankruptcy, will the D&O policy cover me?

May I have choice of counsel?

19

Shopping For D&O Coverage

Choosing a broker:

Expertise and Service Proactive solutions Relationships with markets and leveraging power Claims advocacy and Governance consulting Global presence

Choosing a underwriter/carrier

Policy language, Pricing, Deductibles Financial Strength/Surplus Global presence Internal and Experienced Claims Adjusters Consistency

Coverage

Policy language Who’s the buyer? Board? Officers? Limits Benchmarking – Peers or Market Cap

20

QUESTIONS???