discussion materials for: dallas cpa society may 26, 2011 raising capital in today’s market

TRANSCRIPT

Discussion Materials for:

Dallas CPA Society

May 26, 2011

Raising Capital in Today’s Market

2

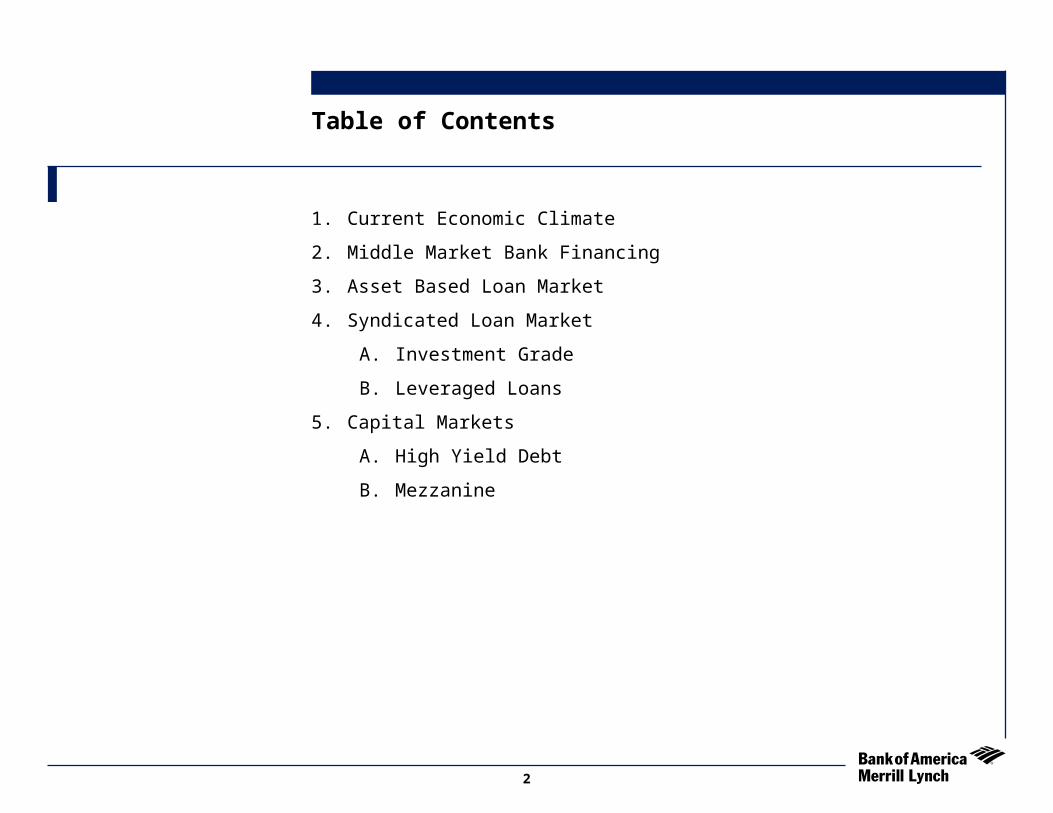

1. Current Economic Climate

2. Middle Market Bank Financing

3. Asset Based Loan Market

4. Syndicated Loan Market

A. Investment Grade

B. Leveraged Loans

5. Capital Markets

A. High Yield Debt

B. Mezzanine

Table of Contents

Current Economic Climate

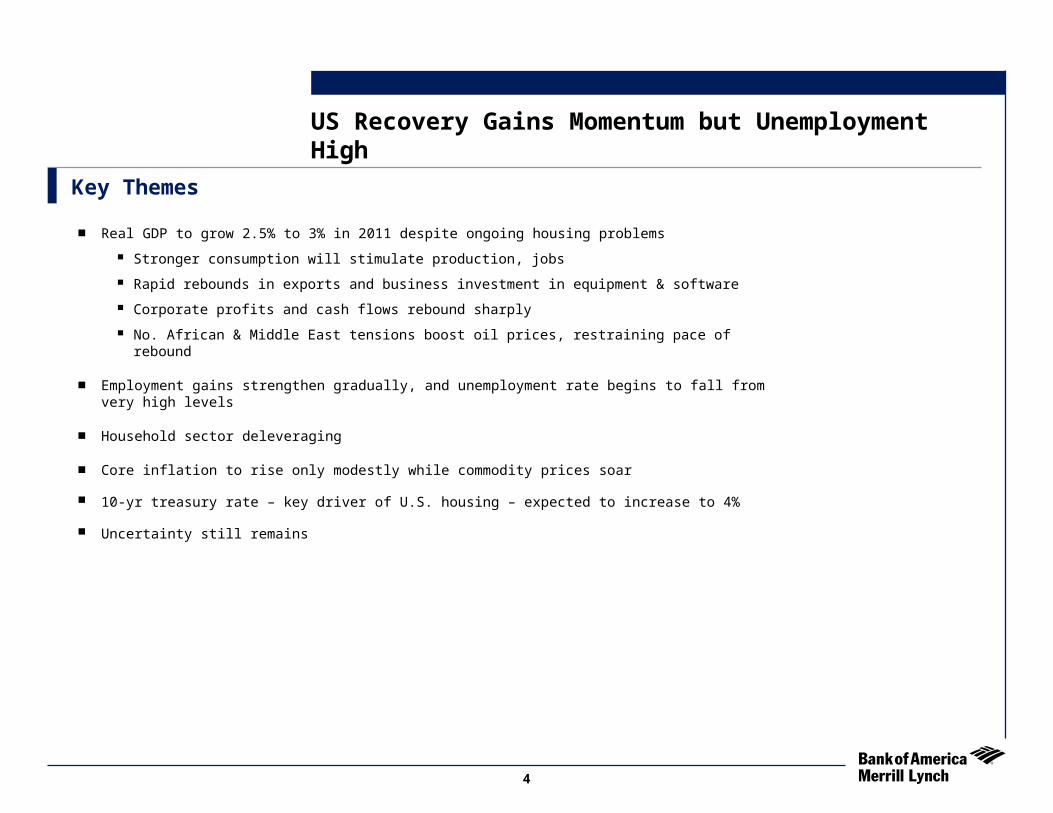

US Recovery Gains Momentum but Unemployment High

■ Real GDP to grow 2.5% to 3% in 2011 despite ongoing housing problems

Stronger consumption will stimulate production, jobs

Rapid rebounds in exports and business investment in equipment & software

Corporate profits and cash flows rebound sharply

No. African & Middle East tensions boost oil prices, restraining pace of rebound

■ Employment gains strengthen gradually, and unemployment rate begins to fall from very high levels

■ Household sector deleveraging

■ Core inflation to rise only modestly while commodity prices soar

10-yr treasury rate – key driver of U.S. housing – expected to increase to 4%

Uncertainty still remains

Key Themes

4

U.S. Macroeconomic Outlook

U.S. Consumer Update

An Improving U.S. Economic Outlook For 2011

3.0%2.5%

3.1%3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

2011

2.9%

2012

3.1%

U.S. GDP

Consensus:

Consumer Credit(2)

$2.44$2.45

$2.56

$2.52

$2.30

$2.40

$2.50

$2.60($tn)

2007

2008

2009

2010

____________________Source: Bloomberg and BofAML Economic Research as of April 15, 2011.Note: Old estimates as of January 28, 2011.(1) Source: University of Michigan Consumer Sentiment survey.(2) Dollars in trillions. Per Federal Reserve statistical release dated February 7, 2011. Includes revolving credit such as credit cards and nonrevolving credit such as

loans for automobiles and education. Excludes loans secured by real estate.

Consumer Sentiment(1)

50

60

70

80

90

100

Jan-07 May-08 Sep-09 Feb-11

72.0

77.5

Avg

Personal Savings

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Jan-07 May-08 Sep-09 Jan-11

4.5%

5.8%

Avg

(% disp. income)

Inflation Outlook

Consensus:

3.1%

1.6%

1.6%1.1%

0.0%

1.0%

2.0%

3.0%

4.0%

2011

2.6%

2012

2.0%

U.S. Unemployment

Consensus:

OldNew

8.6%

7.9%

9.4%8.9%

6.0%

7.5%

9.0%

10.5%

2011

8.7%

2012

8.2%

5

Unemployment Remains High

An Improving U.S. Economic Outlook For 2011

Civilian Unemployment Rate: 16 yr +

SA, %

100500959085807570Source: Bureau of Labor Statistics /Haver Analytics 03/04/11

12

10

8

6

4

2

12

10

8

6

4

2

6

Housing Activity Remains Weak & Inventory Lingers

An Improving U.S. Economic Outlook For 2011

Housing StartsSAAR, Thous.Units

NAR Single Fam Homes Avail for Sale at End of Period, United StatesUnits,NSA

100908070605040302010099989796Sources: CENSUS, REALTOR /Haver 01/14/11

2400

2000

1600

1200

800

400

4000000

3500000

3000000

2500000

2000000

1500000

7

Distressed Mortgages

An Improving U.S. Economic Outlook For 2011

8

Middle Market Bank Financing

Bank of America Offers Financing of Long-term Assets such as Fixed Assets, Permanent Working Capital and Business Expansion and Acquisition on a Structured Payment Schedule

Bank Financing – Term Loans

■ Features

Predetermined payment schedule for your cash flow planning

Repayment schedule matched to the estimated depreciated life of the asset financed

Alternative fixed-rate pricing

■ Benefits

Allows you to retain your operating cash flow

Leverages your capital for expansion and acquisitions

Eliminates the guesswork around cash needed for repayment

10

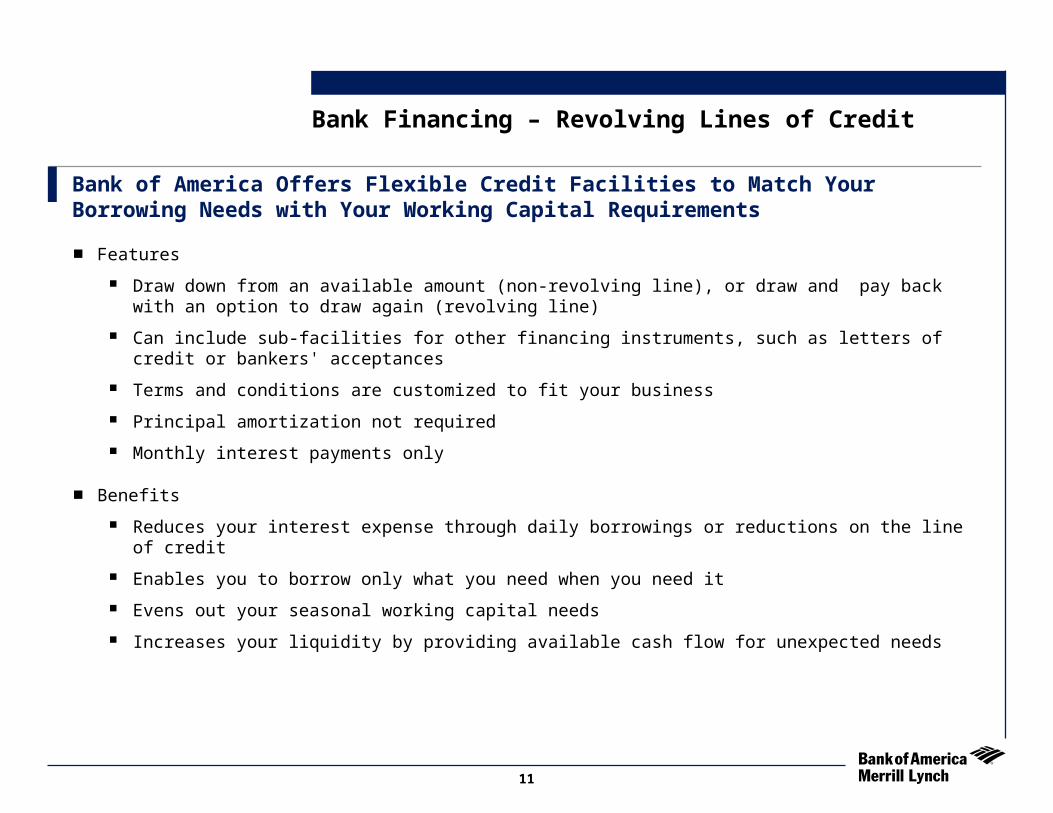

Bank of America Offers Flexible Credit Facilities to Match Your Borrowing Needs with Your Working Capital Requirements

Bank Financing – Revolving Lines of Credit

■ Features

Draw down from an available amount (non-revolving line), or draw and pay back with an option to draw again (revolving line)

Can include sub-facilities for other financing instruments, such as letters of credit or bankers' acceptances

Terms and conditions are customized to fit your business

Principal amortization not required

Monthly interest payments only

■ Benefits

Reduces your interest expense through daily borrowings or reductions on the line of credit

Enables you to borrow only what you need when you need it

Evens out your seasonal working capital needs

Increases your liquidity by providing available cash flow for unexpected needs

11

Asset Based Loan Market

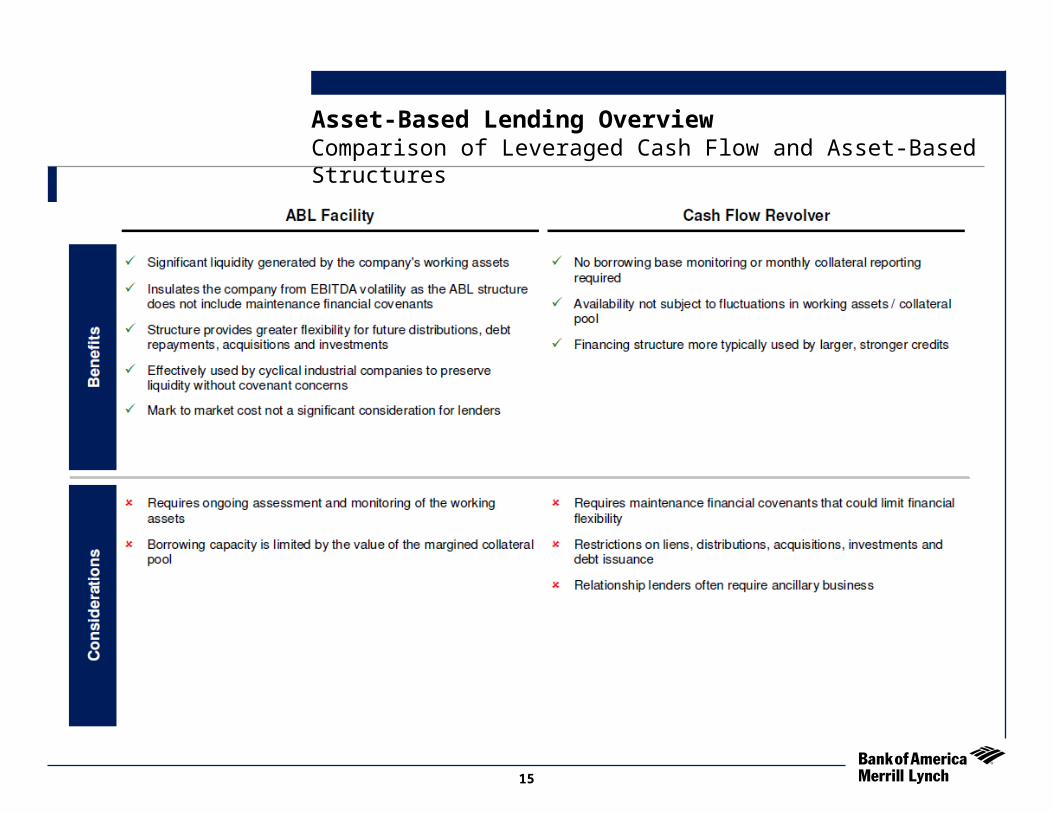

Asset-Based Lending OverviewComparison of Leveraged Cash Flow and Asset-Based Structures

13

Asset-Based Lending OverviewComparison of Leveraged Cash Flow and Asset-Based Structures

14

Asset-Based Lending OverviewComparison of Leveraged Cash Flow and Asset-Based Structures

15

Based on current deals in-market and the slate of forward calendar transactions, BofAML anticipates average LIBOR spreads will trend to the 225-250 bps area, with unused fees ranging from 37.5 bps – 50.0 bps Refinancing

Investors remain focused on structure:

5 year tenors have become the standard

Cash dominion typically triggered at 12.5% – 15.0% availability

Appraisal and field exam frequency (1-2 times per year, with a trigger to 1 additional)

Financial covenant generally springs at 12.5% availability

Restricted payments generally allowed with 17.5% - 20.0% availability and 1.1x pro forma fixed charge coverage

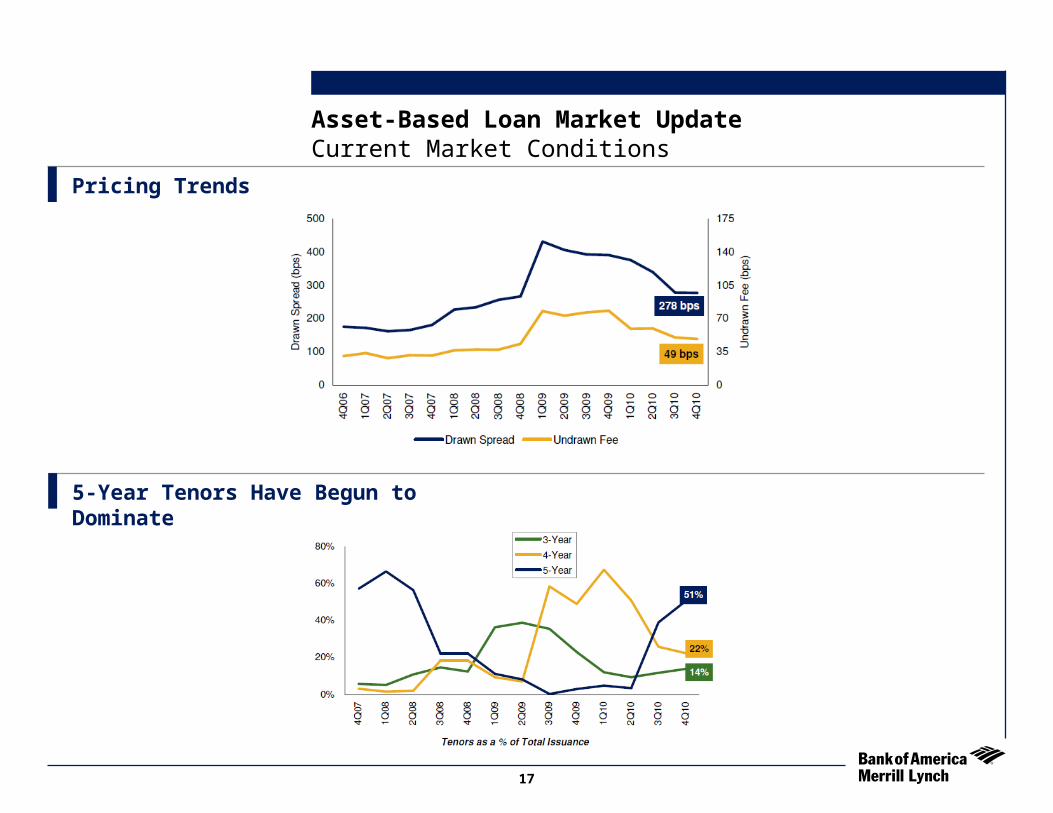

Asset-Based Loan Market UpdateCurrent Market Conditions

Pricing and Structure Continue to Tighten

16

Asset-Based Loan Market UpdateCurrent Market Conditions

Pricing Trends

5-Year Tenors Have Begun to Dominate

17

Syndicated Loan MarketInvestment GradeLeveraged Finance

Investment Grade Market

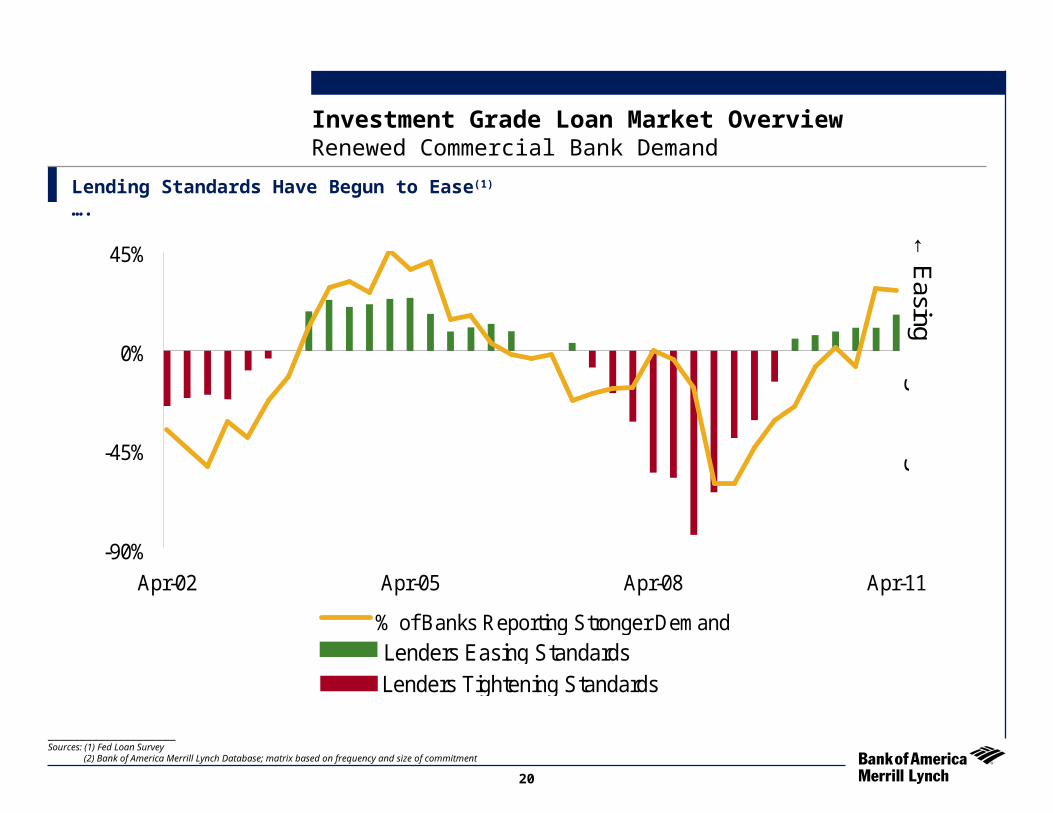

Renewed Commercial Bank Demand

Lending Standards Have Begun to Ease(1)….

Investment Grade Loan Market Overview

____________________Sources: (1) Fed Loan Survey (2) Bank of America Merrill Lynch Database; matrix based on frequency and size of commitment

20

Lenders Tightening Standards

-90%

-45%

0%

45%

Apr-02 Apr-05 Apr-08 Apr-11

% of Banks Reporting Stronger Demand

←E

asing T

ightening→

Lenders Easing Standards

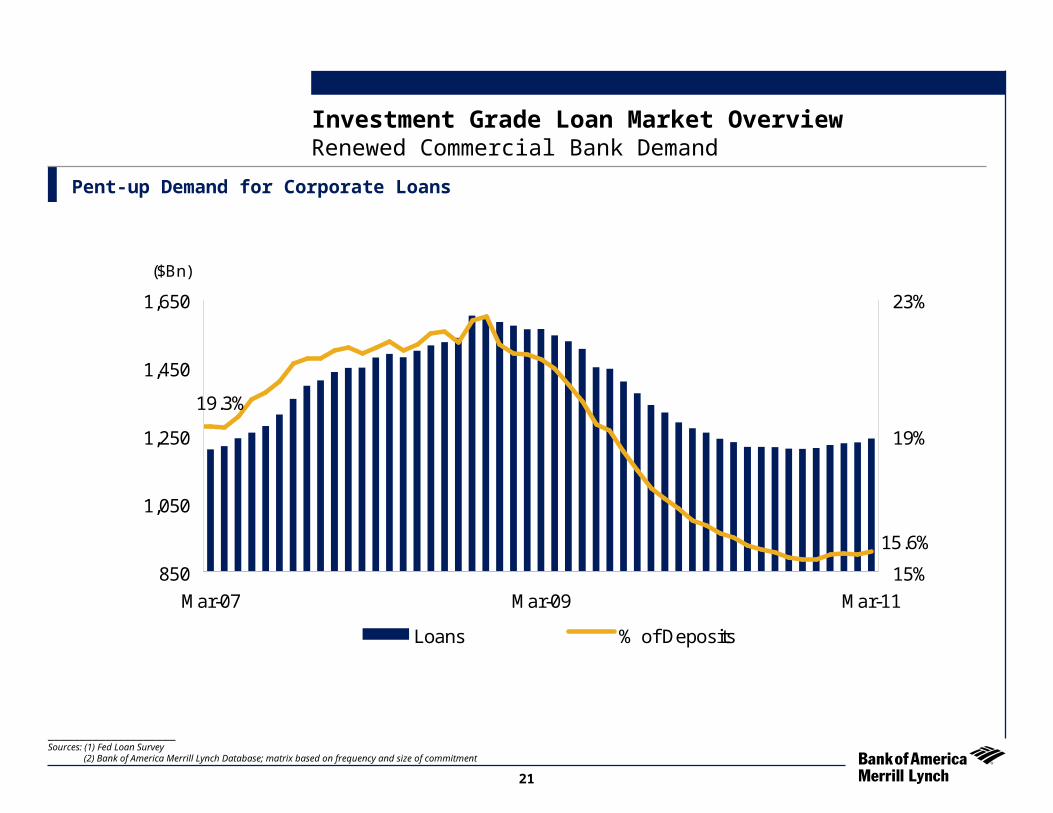

Renewed Commercial Bank Demand

Pent-up Demand for Corporate Loans

Investment Grade Loan Market Overview

____________________Sources: (1) Fed Loan Survey (2) Bank of America Merrill Lynch Database; matrix based on frequency and size of commitment

15.6%

19.3%

850

1,050

1,250

1,450

1,650

Mar-07 Mar-09 Mar-11

15%

19%

23%

Loans % of Deposits

($Bn)

21

…As the Markets Recovered, IG Loan Volume Was Strong Across All Sectors

____________________Sources: Bloomberg and Bank of America Merrill Lynch Database

Capital Markets RecoveryInvestment Grade Loan Market Overview

IG Loan Volume Rebounds Alongside Solid Bond Issuance

LTM Investment Grade Loan Volume: $538.5

$114.5

$93.7

$104.6 $105.2

$51.8

$64.0

Fin

anci

alIn

stitu

tions

En

ergy

&P

ow

er

Te

ch,

Med

ia,

Te

leco

m

Gen

era

lIn

dust

ries

Hea

lthca

re

Con

sum

erR

etai

l

$689

$879 $9

60

$748

$1,0

12

$737

$855

$539

$638 $6

77

$606

$283

$21

6

$376

2005 2006 2007 2008 2009 2010 LTM

IG Bonds IG Loans

$Bn

22

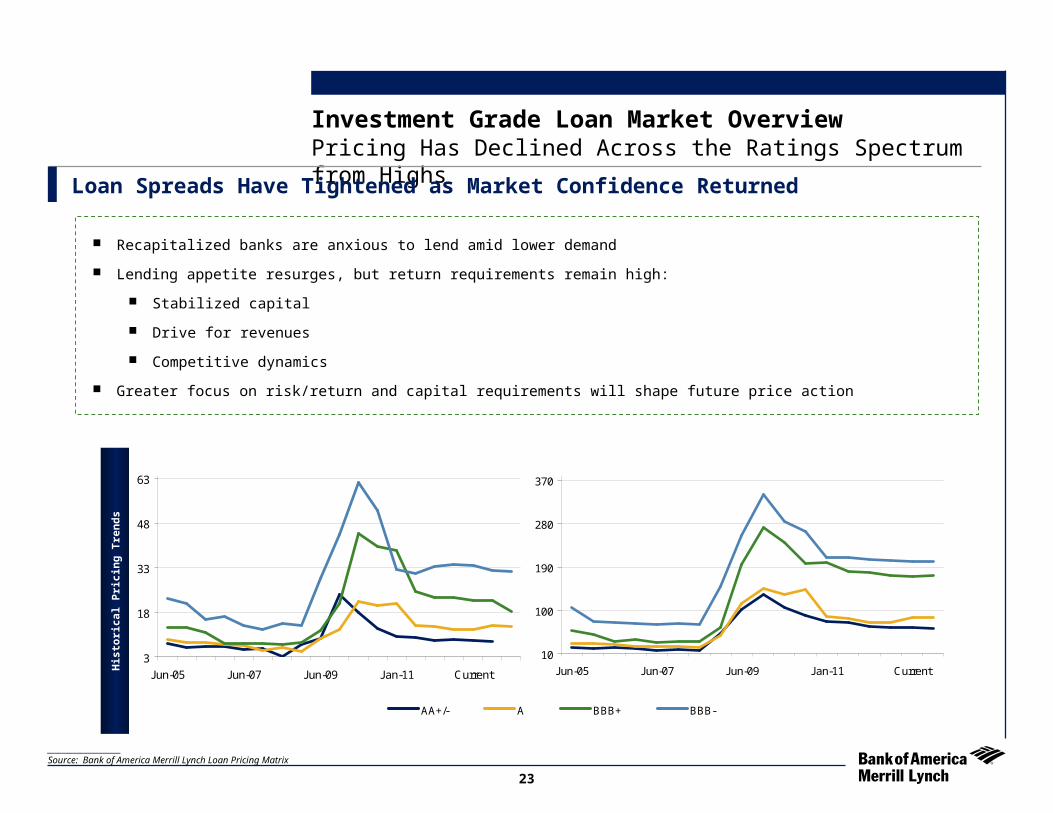

Recapitalized banks are anxious to lend amid lower demand

Lending appetite resurges, but return requirements remain high:

Stabilized capital

Drive for revenues

Competitive dynamics

Greater focus on risk/return and capital requirements will shape future price action

Pricing Has Declined Across the Ratings Spectrum from HighsLoan Spreads Have Tightened as Market Confidence Returned

____________________Source: Bank of America Merrill Lynch Loan Pricing Matrix

Investment Grade Loan Market OverviewH

isto

rica

l P

rici

ng

Tre

nd

s

10

100

190

280

370

Dec-03 Jun-05 Dec-06 Jun-08 Dec-09 Current

AA+/- A BBB+ BBB-

3

18

33

48

63

Jun-05 Jun-07 Jun-09 Jan-11 Current

(Undrawn bps)

10

100

190

280

370

Jun-05 Jun-07 Jun-09 Jan-11 Current

AA+/- A BBB+ BBB-

(L+bps Drawn)

3

18

33

48

63

Jun-05 Jun-07 Jun-09 Jan-11 Current

(Undrawn bps)

23

Pricing Expectations

3 Month LIBOR Expectations Remain Subdued

Investment Grade Loan Market Overview

0.0%

1.0%

2.0%

3.0%

4.0%

2011 2012 2013 2014

2Q11 3Q11 4Q11 1Q12 2Q12

BofAMLResearch 0.30% 0.30% 0.35% 0.45% 0.60%

BloombergConsensus 0.32% 0.38% 0.52% 0.79% 1.16%

ForwardCurve 0.26% 0.28% 0.37% 0.48% 0.66%

24

Renewed Commercial Bank Demand

Most Active Lenders(1)

Investment Grade Loan Market Overview

____________________Sources: (1) Bank of America Merrill Lynch Database; matrix based on frequency and size of commitment

Rank Rank Lender

1 Bank of America 9 Crédit Suisse

2 JP Morgan Chase 10 Morgan Stanley

3 Wells Fargo 11 Deutsche Bank

4 Citigroup 12 BNP Paribas

5 Barclays 13 Goldman Sachs

6 Royal Bank of Scotland 14 HSBC

7 US Bank 15 Bank of Nova Scotia

8 Mitsubishi UFJ 16 Bank of New York

Lender

25

____________________Source: Bank of America Merrill Lynch Database

The tenor distribution in the high grade loan market tilts toward longer maturities

More than 63% of forward calendar volume is multi-year

Nearly 75% of closed LTM volume is multi-year

Increasingly, there is a willingness to structure facilities with 4- and 5-year maturities

The maturity schedule is manageable given current market conditions and lender demand in the market

Investment Grade Loan Market OverviewMulti-Year Facilities Dominate the Market

Forward Calendar Volume Illustrates a Shift Toward Longer Maturities (1)

$134

$79$90

$169$158

$448

$502$515

$2$14

$38

$219

$390$390

$160

$230

$99

2005 2006 2007 2008 2009 1H'09 2H'09 1H'10 2H'10 1H'11 2H'11 2011 2012 2013 201620152014 2017

Forward Calendar Mix Investment Grade Loan Maturity Wall Through 2017

5+ Years45%

3+ to 4 Years12%

3 Years7%

364 days36%

1 to < 3 Years0%

26

Leveraged Loan Market

Robust Volume in 2011

Current Leveraged Loan Market ConditionsLeveraged Loan Market Overview

____________________Source: S&P/LCD

$33.3$35.4$35.1

$67.1

$29.8

$18.1

$27.5

$21.0

$31.4

$8.5$13.1

Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11Institutional Pro Rata

YTD Volume: $200.7 Bn YTD Volume: $200.7 Bn

Market Conditions Strong

The technical position in the leveraged finance market remains attractive as demand continues to outweigh supply, however heavy volumes are beginning to balance the technical picture

Despite equity and commodity volatility, and the large primary calendar, overall tone is solid

A recent wave of jumbo leveraged loan executions has tested market capacity, proving demand limits

28

Inflows Remain Positive

Current Leveraged Loan Market ConditionsLeveraged Loan Market Overview

____________________Source: S&P/LCD

Technical Position

Leveraged loan mutual fund inflows total $22.6 Bn over the LTM (46 consecutive weeks)

LTM flows: $22.6 Bn with 46 consecutive inflows

LTM flows: $22.6 Bn with 46 consecutive inflows

$532

$937

$604

$419

$597

$708

$569

$721$627

$381

$639$686

$1,053

$927$941

$1,048

$206

$848

$951

$482

$890

$417

$609

$897

$707

$804

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11

Loan Weekly Flows 3 Week Moving Average

29

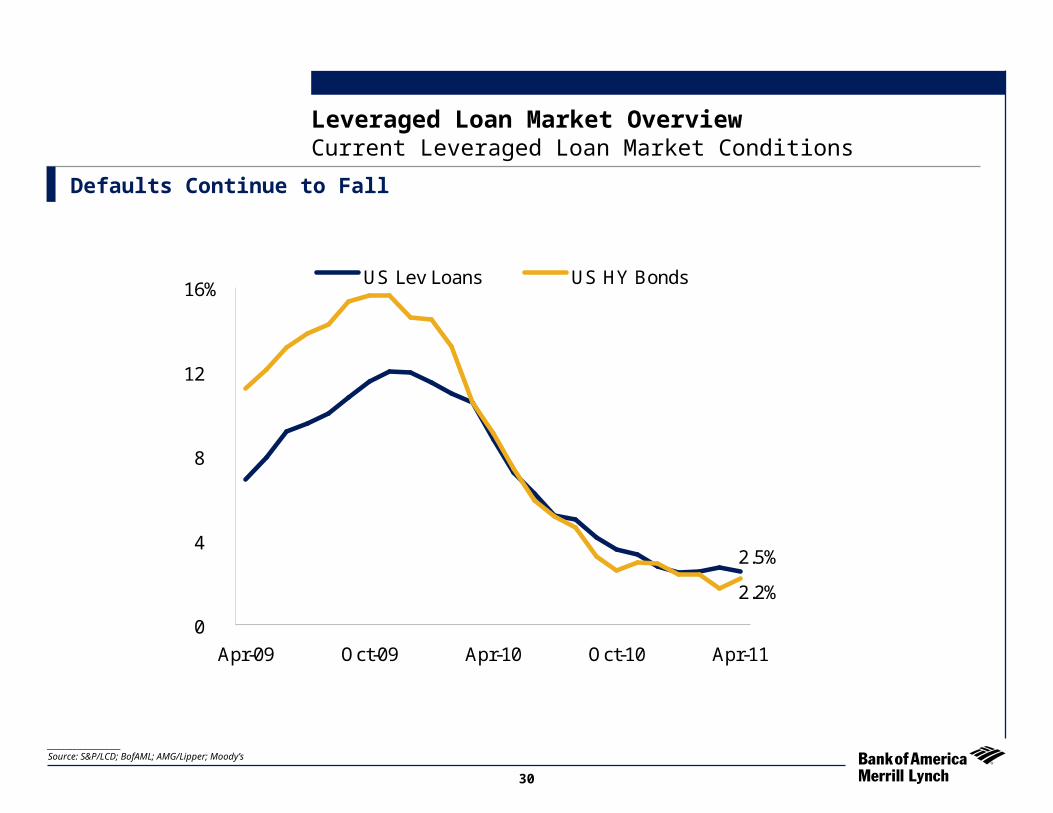

Defaults Continue to Fall

Leveraged Loan Market OverviewCurrent Leveraged Loan Market Conditions

____________________Source: S&P/LCD; BofAML; AMG/Lipper; Moody’s

2.5%

2.2%

0

4

8

12

16%

Apr-09 Oct-09 Apr-10 Oct-10 Apr-11

US Lev Loans US HY Bonds

30

4.46%

2.50%3.22%

3.83%

0.92%

0.26%

0%

6%

Jun-11 Jan-12 Aug-12 Feb-13 Sep-13 Mar-14

10 Yr UST 3 Mo LIBOR

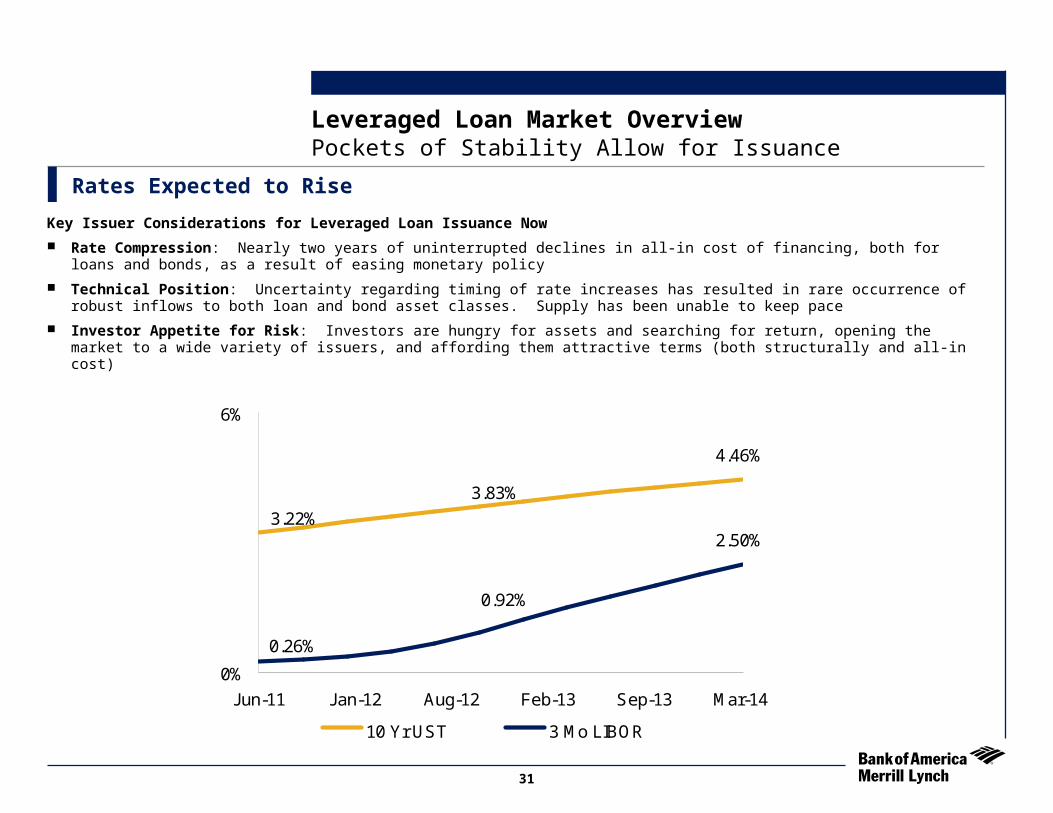

Leveraged Loan Market OverviewPockets of Stability Allow for Issuance

Rates Expected to Rise

Key Issuer Considerations for Leveraged Loan Issuance Now

Rate Compression: Nearly two years of uninterrupted declines in all-in cost of financing, both for loans and bonds, as a result of easing monetary policy

Technical Position: Uncertainty regarding timing of rate increases has resulted in rare occurrence of robust inflows to both loan and bond asset classes. Supply has been unable to keep pace

Investor Appetite for Risk: Investors are hungry for assets and searching for return, opening the market to a wide variety of issuers, and affording them attractive terms (both structurally and all-in cost)

31

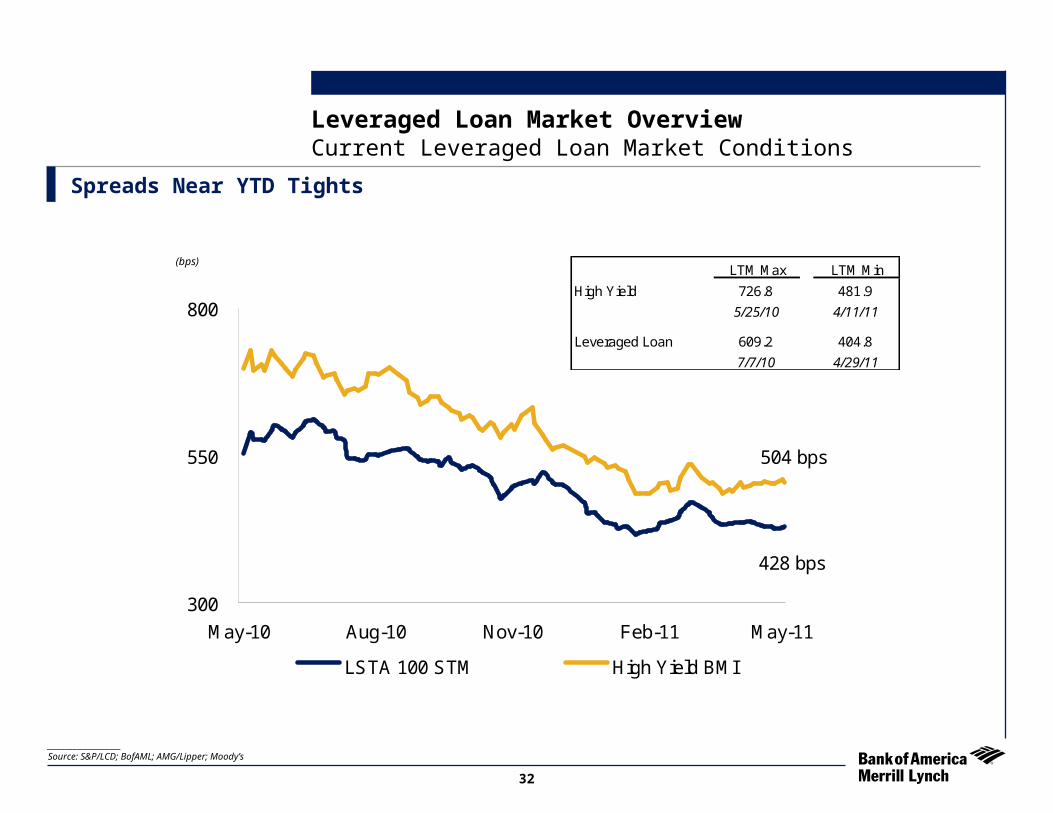

Spreads Near YTD Tights

Leveraged Loan Market OverviewCurrent Leveraged Loan Market Conditions

____________________Source: S&P/LCD; BofAML; AMG/Lipper; Moody’s

LTM Max LTM Min

High Yield 726.8 481.9

5/25/10 4/11/11

Leveraged Loan 609.2 404.8

7/7/10 4/29/11

428 bps

504 bps

300

550

800

May-10 Aug-10 Nov-10 Feb-11 May-11

LSTA 100 STM High Yield BMI

(bps)

32

____________________Source: Moody’s Investor Service, LCD, BofAML Research

Leveraged Loan Market Overview

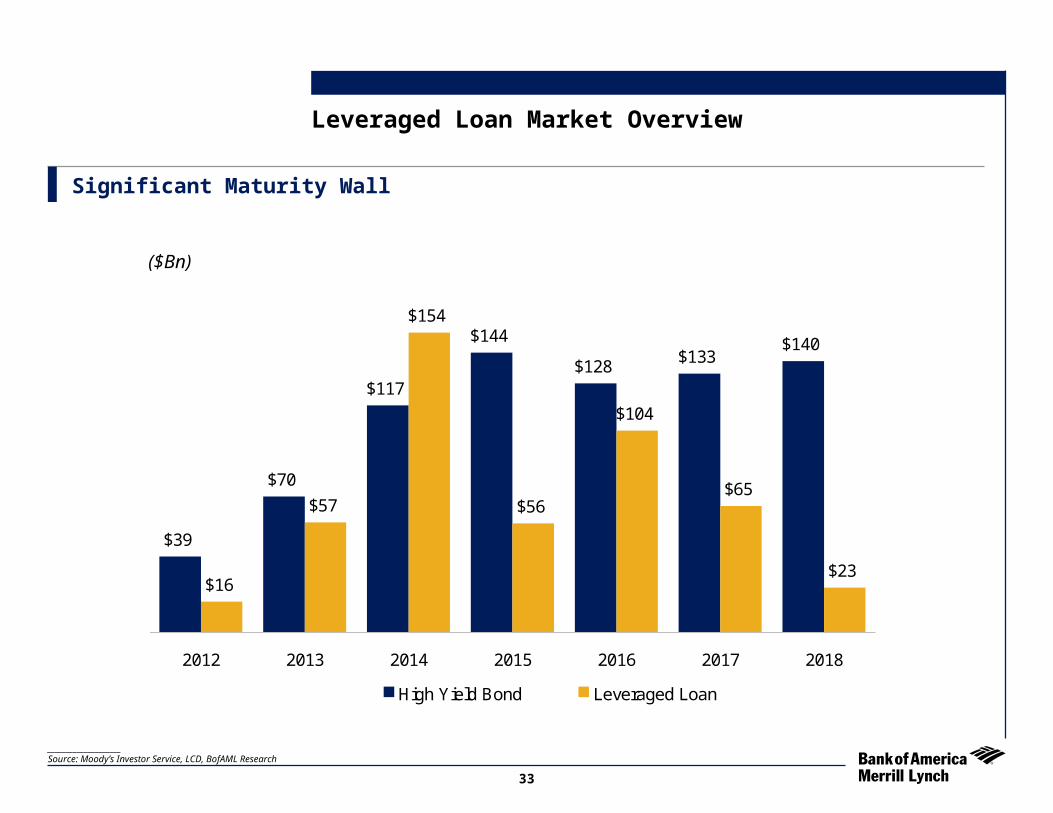

Significant Maturity Wall

($Bn)

$39

$70

$117

$144

$128$133

$140

$16

$56

$154

$23

$65

$104

$57

2012 2013 2014 2015 2016 2017 2018

High Yield Bond Leveraged Loan

33

Recent Use of Proceeds

Current Leveraged Loan Market ConditionsLeveraged Loan Market Overview

____________________Source: S&P/LCD

LBO12%

Dividend19%

M&A6%

Refi63%

34

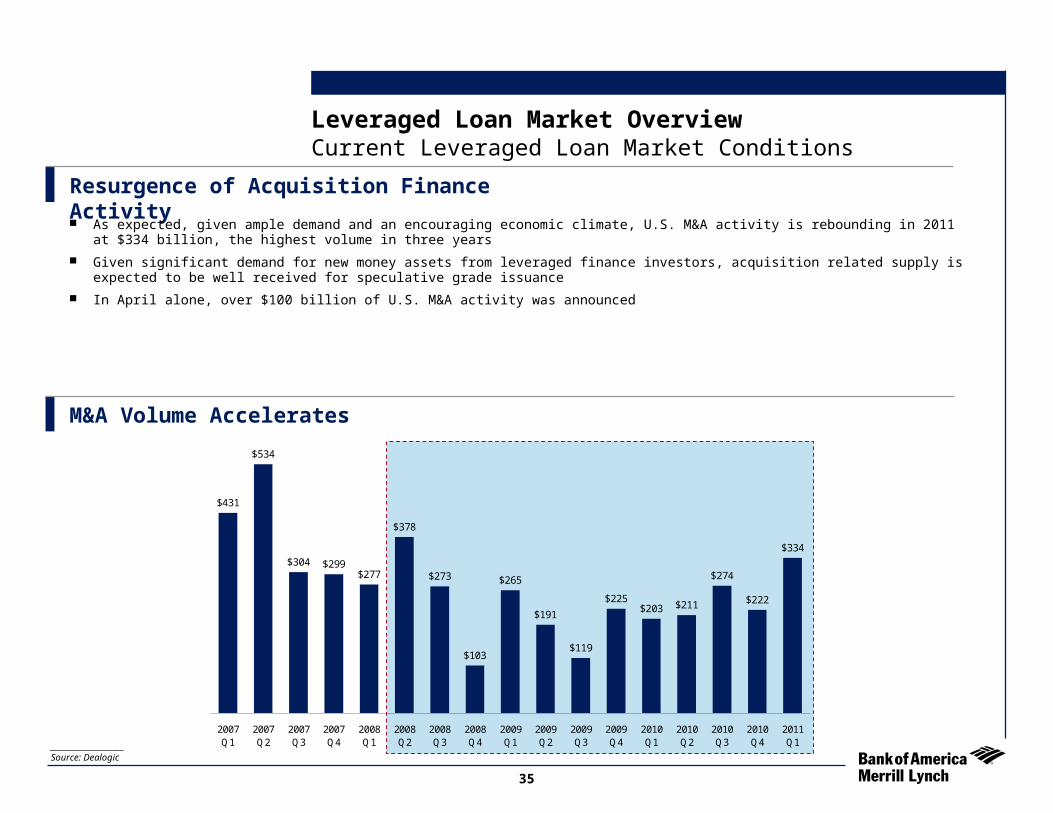

Resurgence of Acquisition Finance Activity As expected, given ample demand and an encouraging economic climate, U.S. M&A activity is rebounding in 2011 at $334 billion,

the highest volume in three years

Given significant demand for new money assets from leveraged finance investors, acquisition related supply is expected to be well received for speculative grade issuance

In April alone, over $100 billion of U.S. M&A activity was announced

Current Leveraged Loan Market Conditions

M&A Volume Accelerates

$431

$534

$304 $299$277

$378

$273

$103

$265

$191

$119

$225$203 $211

$274

$222

$334

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1____________________

Source: Dealogic

Leveraged Loan Market Overview

35

Strong Secondary Market

Current Leveraged Loan Market ConditionsLeveraged Loan Market Overview

____________________Source: S&P/LCD

95.59

428 bps

90

97

May-11Mar-11Jan-11Nov-10

410

540

LSTA 100 Bid LSTA 100 STM

36

Forward Calendar Builds

Current Leveraged Loan Market ConditionsLeveraged Loan Market Overview

____________________Source: S&P/LCD

$41$41$40$41$39

$29

$23$22

$16

$25

$51

$31

$25

18-May4-May20-Apr6-Apr23-Mar9-Mar23-Feb

($ Bn)

37

Capital MarketsHigh YieldMezzanine

High Yield Market

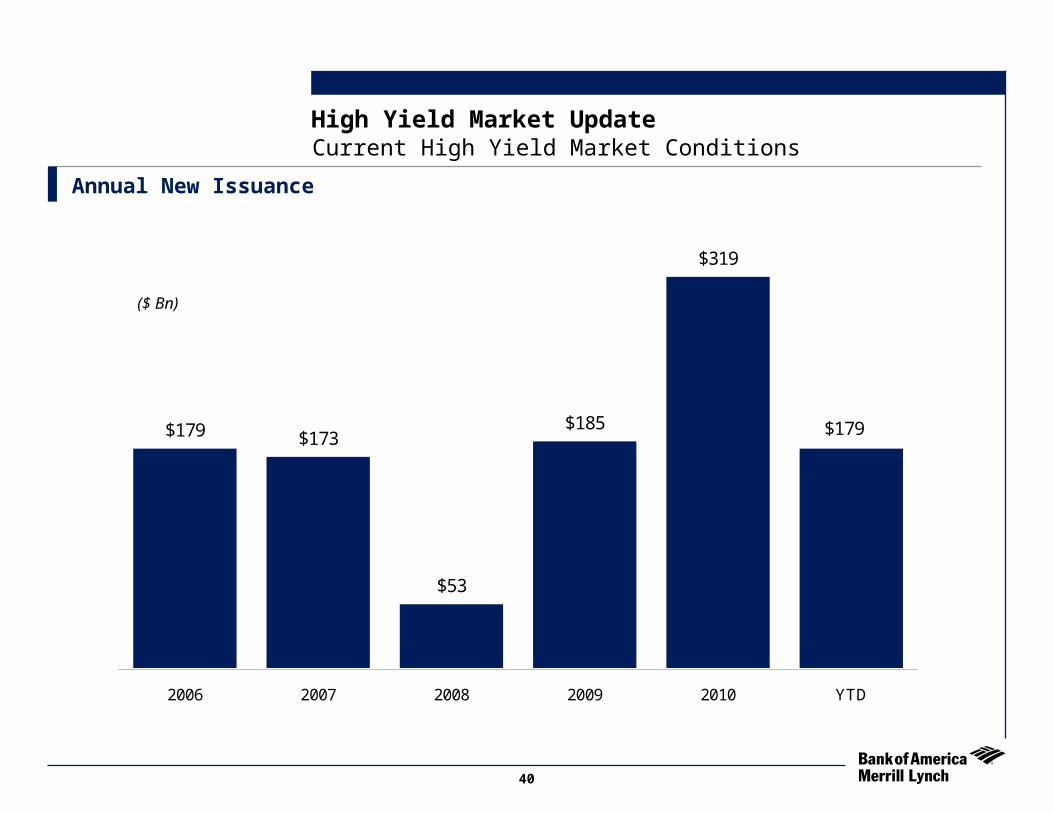

Current High Yield Market ConditionsHigh Yield Market Update

Annual New Issuance

$179 $173

$53

$185

$319

$179

2006 2007 2008 2009 2010 YTD

40

($ Bn)

New Issue Volume at Record Breaking Pace in 2011

Current High Yield Bond Market ConditionsHigh Yield Market Update

____________________Source: S&P/LCD.

Historical Market Perspective

$17.8

$10.2

$40.9 $38.9 $38.9

$49.1

$37.9$34.0

$22.8$25.9

$18.5$22.2 $22.1

$27.1

$19.3$22.6

$15.1

$35.3

$7.7 $9.7

$20.2$24.8

$39.0

$23.7

$35.5

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

Jan-10

Feb-10

Mar-10

Apr-10

May-10

Jun-10

Jul-10

Aug-10

Sep-10

Oct-10

Nov-10

Dec-10

Jan-11

Feb-11

Mar-11

Apr-11

May-11

Year-to-Date: $179.3 BnYear-to-Date: $179.3 Bn

$13

$83$61

$115

$179$157$140

$43 $67$37 $43 $60

$101$138

$101

$48

$173

$53

$185

$319

$179

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

YT

D

41

($ Bn)

($ Bn)

Current High Yield Market ConditionsHigh Yield Market Update

High Yield Mutual Funds Flow

($186)

$1,037

($471)

$1,290

$375

$739

$439

($1,154)

$492

$967

$196$403

$1,037

$315$421

$510

($87)

$373$574

$131

($4)

$466

$743

$234

($677)

$358

Nov-10 Dec-10 Jan-11 Feb-11 Mar-11 Apr-11 May-11

HY Weekly Flows 3 Week Moving Average

42

($ MM)

Refinancing Activity Continues to Dominate

Structures and Uses of Proceeds have Evolved Since the Credit Crisis

High Yield Market Update

35%

20%25%

45%

57%

61%

43%

52%42%

39%27%33%

33%

23%

23%

24%

15% 19%

29%

31%

37%29%

15%

15%

13%

8%

16%

75%

75%

36%

17%

16%

0

55

110

Q4-07 Q1-08 Q2-08 Q3-08 Q4-08 Q1-09 Q2-09 Q3-09 Q4-09 Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11

Vol

ume

($ B

illio

ns)

20,000

40,000

60,000

$80,000

Q1 2007 Q2 2007 Q3 2007 Q4 2007 Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 - YTD2009

Bank Refi Bond Redemptions GCP Cap Ex M&A Dividend

42%

57%

17%

2007

2008 2009 2010 2011

43

Refinancing Activity Continues to Dominate

Current High Yield Bond Market ConditionsHigh Yield Market Update

____________________Source: S&P/LCD.

Use of HY Proceeds – 2011 YTD

Bank Refi34%

M&A16%

Dividend7%

Cap Ex2%

GCP15%

Bond Redemptions

26%

44

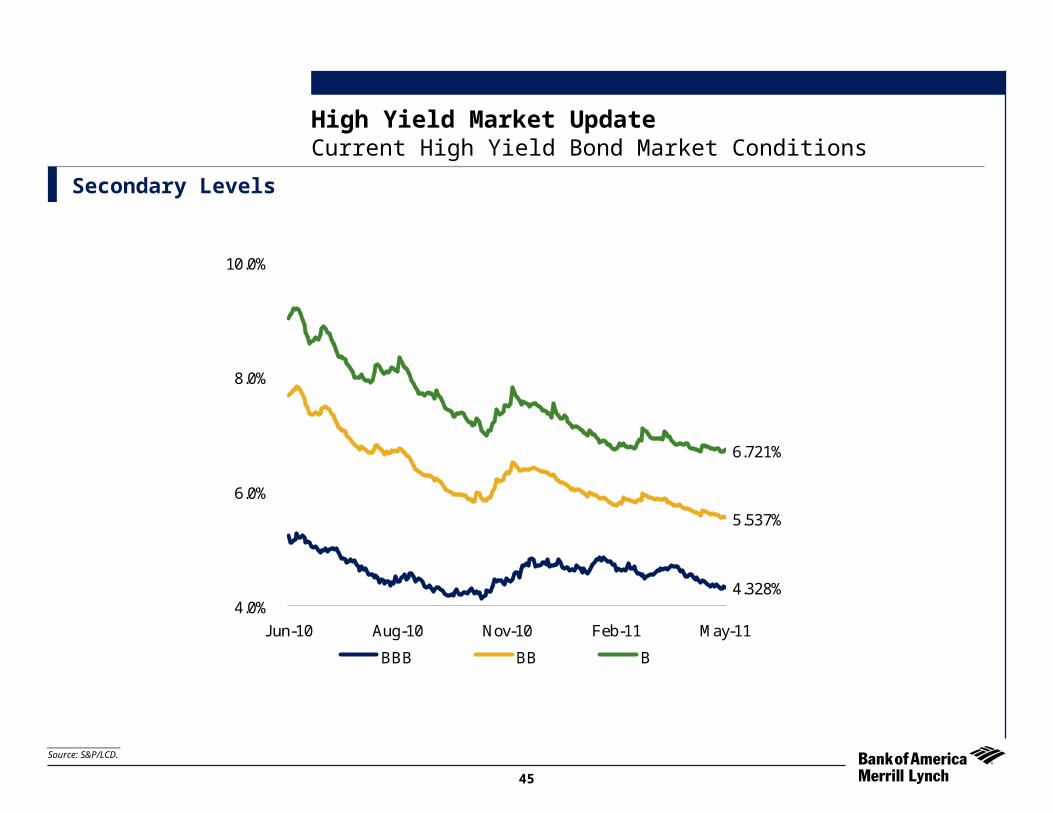

Secondary Levels

Current High Yield Bond Market ConditionsHigh Yield Market Update

____________________Source: S&P/LCD.

4.328%

5.537%

6.721%

4.0%

6.0%

8.0%

10.0%

Jun-10 Aug-10 Nov-10 Feb-11 May-11

BBB BB B

45

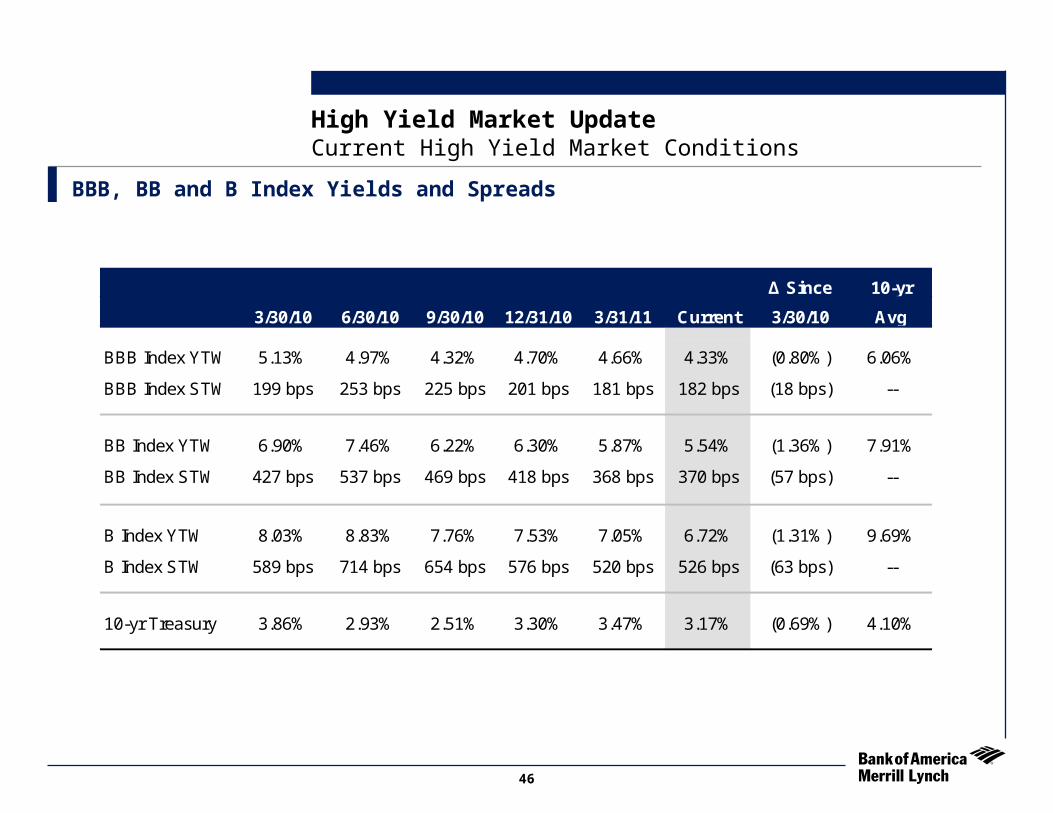

High Yield Market UpdateCurrent High Yield Market Conditions

BBB, BB and B Index Yields and Spreads

Δ Since 10-yr

3/30/10 6/30/10 9/30/10 12/31/10 3/31/11 Current 3/30/10 Avg

BBB Index YTW 5.13% 4.97% 4.32% 4.70% 4.66% 4.33% (0.80%) 6.06%

BBB Index STW 199 bps 253 bps 225 bps 201 bps 181 bps 182 bps (18 bps) --

BB Index YTW 6.90% 7.46% 6.22% 6.30% 5.87% 5.54% (1.36%) 7.91%

BB Index STW 427 bps 537 bps 469 bps 418 bps 368 bps 370 bps (57 bps) --

B Index YTW 8.03% 8.83% 7.76% 7.53% 7.05% 6.72% (1.31%) 9.69%

B Index STW 589 bps 714 bps 654 bps 576 bps 520 bps 526 bps (63 bps) --

10-yr Treasury 3.86% 2.93% 2.51% 3.30% 3.47% 3.17% (0.69%) 4.10%

46

Mezzanine

Creates financial flexibility by increasing senior debt capacity and preserving bank facilities for future needs

Adds a layer of long-term capital which will be viewed by banking institutions as equity-like capital

Creates minimal equity dilution, when compared to an equity offering

Mezzanine Capital Benefits

Typical Issuer Profile

Mezzanine

EBITDAEBITDA Generally $5 million or greater

Typical LeverageTypical Leverage Total Debt : EBITDA less than 4.0x to 4.5x

SituationsSituations Expansion / growth capital

Acquisition capital

Buy-out / ownership change

Restructuring / recapitalization

48

Typical Offering Parameters

Mezzanine

CompaniesCompanies

IssueIssue Subordinated debt

Security InterestSecurity Interest Typically Unsecured

Occasionally requires second lien

MaturityMaturity Typically 6 – 8 Years

PricingPricing 12-14% cash pay coupon

1-2% payment in kind

Issue SizeIssue Size > $5MM

WarrantsWarrants Generally required

49

Typical Offering Parameters

Mezzanine

Financial CovenantsFinancial Covenants Typically maintenance based (coverages)

Generally more lenient than senior debt

RatingsRatings Credit ratings are not required to complete a financing

RedemptionRedemption Optional Redemption: At anytime with scaling premium

Mandatory Redemption: Usually bullet maturities, sometimes amortizing

Target ReturnsTarget Returns 15-17% (including Warrants)

Board SeatBoard Seat Negotiable

Observation rights

50

“Bank of America Merrill Lynch” is the marketing name for the global banking and global markets businesses of Bank of America Corporation. Lending, derivatives, and other commercial banking activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., member FDIC. Securities, strategic advisory, and other investment banking activities are performed globally by investment banking affiliates of Bank of America Corporation (“Investment Banking Affiliates”), including, in the United States, Merrill Lynch, Pierce, Fenner & Smith Incorporated and Merrill Lynch Professional Clearing Corp., all of which are registered broker dealers and members of FINRA and SIPC, and, in other jurisdictions, by locally registered entities.

Investment products offered by Investment Banking Affiliates: Are Not FDIC Insured * May Lose Value * Are Not Bank Guaranteed.

These materials have been prepared by one or more subsidiaries of Bank of America Corporation for the client or potential client to whom such materials are directly addressed and delivered (the "Company") in connection with an actual or potential mandate or engagement and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with us. These materials are based on information provided by or on behalf of the Company and/or other potential transaction participants, from public sources or otherwise reviewed by us. We assume no responsibility for independent investigation or verification of such information (including, without limitation, data from third party suppliers) and have relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the managements of the Company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such managements (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). No representation or warranty, express or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. These materials were designed for use by specific persons familiar with the business and affairs of the Company and are being furnished and should be considered only in connection with other information, oral or written, being provided by us in connection herewith. These materials are not intended to provide the sole basis for evaluating, and should not be considered a recommendation with respect to, any transaction or other matter. These materials do not constitute an offer or solicitation to sell or purchase any securities and are not a commitment by Bank of America Corporation or any of its affiliates to provide or arrange any financing for any transaction or to purchase any security in connection therewith. These materials are for discussion purposes only and are subject to our review and assessment from a legal, compliance, accounting policy and risk perspective, as appropriate, following our discussion with the Company. We assume no obligation to update or otherwise revise these materials. These materials have not been prepared with a view toward public disclosure under applicable securities laws or otherwise, are intended for the benefit and use of the Company, and may not be reproduced, disseminated, quoted or referred to, in whole or in part, without our prior written consent. These materials may not reflect information known to other professionals in other business areas of Bank of America Corporation and its affiliates.

Bank of America Corporation and its affiliates (collectively, the "BAC Group") comprise a full service securities firm and commercial bank engaged in securities, commodities and derivatives trading, foreign exchange and other brokerage activities, and principal investing as well as providing investment, corporate and private banking, asset and investment management, financing and strategic advisory services and other commercial services and products to a wide range of corporations, governments and individuals, domestically and offshore, from which conflicting interests or duties, or a perception thereof, may arise. In the ordinary course of these activities, parts of the BAC Group at any time may invest on a principal basis or manage funds that invest, make or hold long or short positions, finance positions or trade or otherwise effect transactions, for their own accounts or the accounts of customers, in debt, equity or other securities or financial instruments (including derivatives, bank loans or other obligations) of the Company, potential counterparties or any other company that may be involved in a transaction. Products and services that may be referenced in the accompanying materials may be provided through one or more affiliates of Bank of America Corporation. We have adopted policies and guidelines designed to preserve the independence of our research analysts. These policies prohibit employees from offering research coverage, a favorable research rating or a specific price target or offering to change a research rating or price target as consideration for or an inducement to obtain business or other compensation. We are required to obtain, verify and record certain information that identifies the Company, which information includes the name and address of the Company and other information that will allow us to identify the Company in accordance, as applicable, with the USA Patriot Act (Title III of Pub. L. 107-56 (signed into law October 26, 2001)) and such other laws, rules and regulations as applicable within and outside the United States.

We do not provide legal, compliance, tax or accounting advice. Accordingly, any statements contained herein as to tax matters were neither written nor intended by us to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. If any person uses or refers to any such tax statement in promoting, marketing or recommending a partnership or other entity, investment plan or arrangement to any taxpayer, then the statement expressed herein is being delivered to support the promotion or marketing of the transaction or matter addressed and the recipient should seek advice based on its particular circumstances from an independent tax advisor. Notwithstanding anything that may appear herein or in other materials to the contrary, the Company shall be permitted to disclose the tax treatment and tax structure of a transaction (including any materials, opinions or analyses relating to such tax treatment or tax structure, but without disclosure of identifying information or, except to the extent relating to such tax structure or tax treatment, any nonpublic commercial or financial information) on and after the earliest to occur of the date of (i) public announcement of discussions relating to such transaction, (ii) public announcement of such transaction or (iii) execution of a definitive agreement (with or without conditions) to enter into such transaction; provided, however, that if such transaction is not consummated for any reason, the provisions of this sentence shall cease to apply. ©2011 Bank of America Corporation.

Notice to RecipientConfidential

51