dnb investor meeting, london march 6, 2012

TRANSCRIPT

DNB Investor Meeting, London March 6, 2012

Per Sagbakken,

Head of Investor Relations, Long-term Funding

Harald Serck-Hanssen

Global Head of Shipping, Offshore and Logistics

Agenda

2

A 2011 DNB summary DNB’s shipping activities

Full year 2011

3

Pre-tax operating profit before write-downs in NOK billion

21.8 (21.1)

Cost/income ratio in per cent

47.1 (47.6)

Return on equity in per cent

11.4 (13.6)

Proposed dividend in NOK

2 (4)

Key figures for the last three years

4

Earnings per share (NOK)

Return on equity (Per cent)

Cost/income ratio (Per cent)

Ratio of deposits to lending (Per cent)

10.6

13.6

11.4

2009 2010 2011

48.147.6

47.1

2009 2010 2011

53.054.8

57.8

2009 2010 2011

•

1.75

4.00

2.00

2009 2010 2011

Earnings per share Dividends/proposed dividend

8.66

6.43

7.98

Business areas

5

Net non-performing and net doubtful commitments 1)

6

4.2

11.9

19.1

21.8 21.4 20.8

18.4 18.9

16.114.5

19.5

0.42

0.99

1.711.88 1.81 1.77

1.55 1.56

1.311.14

1.50

0.35

0.73

1.051.22 1.14

1.040.88 0.93

0.69 0.63

1.10

31 Dec.2007

31 Dec.2008

31 Dec.2009

31March

30June

30Sept.

31Dec.

31March

30June

30Sept.

31Dec.

2010 2011

DNB Baltics and Poland

DNB Group excl. DNB Baltics and Poland

As a percentage of net lending

As a percentage of net lending excl. DNB Baltics and Poland

Per cent

NOK billion

1) Includes non-performing commitments and commitments subject toindividual write-downs. Accumulated individual write-downs are deducted.

Write-downs on loans and guarantees

7

Full year Full year

Amounts in NOK million 4Q11 3Q11 2Q11 1Q11 4Q10 2011 2010

Individual write-downs:

Retail Banking

- Private Customer Divisions 78 38 58 13 132 186 286

- SME Divisions 233 128 (45) 96 182 411 356

- DNB Finans 1) 29 106 97 138 49 370 582

Large Corporates and International

- Nordic Corporates Division 144 (3) 145 120 4 406 28

- International Corporates and

Institutions Division 29 110 (10) 273 196 402 249

- Shipping, Offshore and Logistics Division 143 17 (13) 13 3 160 219

- Energy Division 1 2 (11) 0 (10) (8) 88

- Other units 1 (1) 3 (4) (1) (1) 4

DNB excl. former DnB NORD 657 397 223 649 553 1 926 1 811

Former DnB NORD

- DNB Baltics and Poland 237 494 169 202 319 1 103 1 719

- Other units 126 28 15 19 88 188 543

Total individual write-downs 1 020 919 408 870 961 3 217 4 074

Collective write-downs:

DNB excl. DNB Baltics and Poland (44) 43 54 29 (329) 82 (628)

DNB Baltics and Poland (50) 208 (4) (8) (103) 146 (449)

Total collective write-downs on loans (94) 251 50 21 (432) 227 (1 077)

Write-downs on loans and guarantees 926 1 170 457 892 529 3 445 2 997

1) Includes leasing, factoring and credit card and consumer financing

Stable access to long-term funding

2012

2011

2010

NOK billion Maturity

Covered bonds 84.4 7.5 49

Senior bonds 32.3 7.3 84

Total 116.6 7.5 59 bp

Spread

3-month Euribor

NOK billion Maturity

Covered bonds 98.3 6.5 53

Senior bonds 27.8 8.8 108

Total 126.1 7.0 65 bp

In addition: LTRO funding 15.7 3.0 n.a.

Spread

3-month Euribor

Spread

NOK billion Maturity

Covered bonds 18.5 5.5 83

Senior bonds 22.7 7.9 196

Total 41.2 6.8 146 bp

Lower Tier 2 5.8 10nc5 340

Total 47.0

In addition: LTRO2 funding 9.0 3.0 n.a.

3-month Euribor

Equity Tier 1 Capital according to Nordic rules

Reported capital adequacy Pro forma full IRB IRB with "Nordic" risk weight

Adjusted for Nordic risk weight for credit cards

Adjusted for Nordic risk weight for corporates

Adjusted for Swedish risk weight for mortgage loans

Adjusted for full IRB

DNB risk weights

9.4

10.8

14.2

EquityTier 1 capital as at 31 December 2011 (CET 1)

Per cent

Agenda

10

DNB’s strategy and position

The shipping markets and the Norwegian

maritime industry

Special focus on the dry bulk, tanker and

container segments

The DNB shipping portfolio

DNB’s shipping activities

In shipping, the supply of new vessels remains a challenge in some segments.

The orderbook is, however, much lower than in 2008. ”Slippage” continues.

%

Source: Clarkson

Orderbook within the major shipping segments as a % of the existing fleet

Source: Clarkson

200

400

600

800

1000

1200

1400

1600

1800

2003 2005 2007 2009 2011 2013 2015

Million dwt

LPG carriers

Chemical tankers

Product tankers

Crude oil tankers

Dry bulk carriers

Containerships

Expected Worldwide Shipping Demand

Seaborne trade is expected to grow steadily within all sectors.

Source: Lorentzen & Stemoco

Shipping consists of many segments, with different drivers.

Our largest segment is offshore, where market conditions are positive.

Bulk Carrier/Dry Cargo

UltraLargeOreCarrier,

Cape Size, Panamax,

Handymax, Handysize

Crude Oil/Product

ULCC , VLCC, Suezmax,

Aframax, Panamax,

Product (LR1/LR2/MR)

Chemical Tankers

Container Vessel

Post Panamax,

Panamax, Sub

Panamax, Handy

Feedermax, Feeder

Liquid Natural

Gas (LNG)

Supply

vessels

PSV, AHTS,

Reefer vessel

Refrigerated cargo

RoRo / PCTC /

PCC

Cruise /

Passenger vessel

13

14

Norway is the world’s 5th largest shipping nation

Norwegian maritime insurance has a world market

share of 15-20%

Within ship classification, the market share is +15%

OSE is a leading shipping and offshore exchange

World leading within shipbroking, legal and finance

Active Government involvement through GIEK, etc

Specialized yards, and professional R&D

environments at university levels

Norway is a major shipping nation with a unique maritime cluster

Shipowners

Finance

Ship-brokers

Legal

services

Education Insurance

R&D

Yards

etc

Class

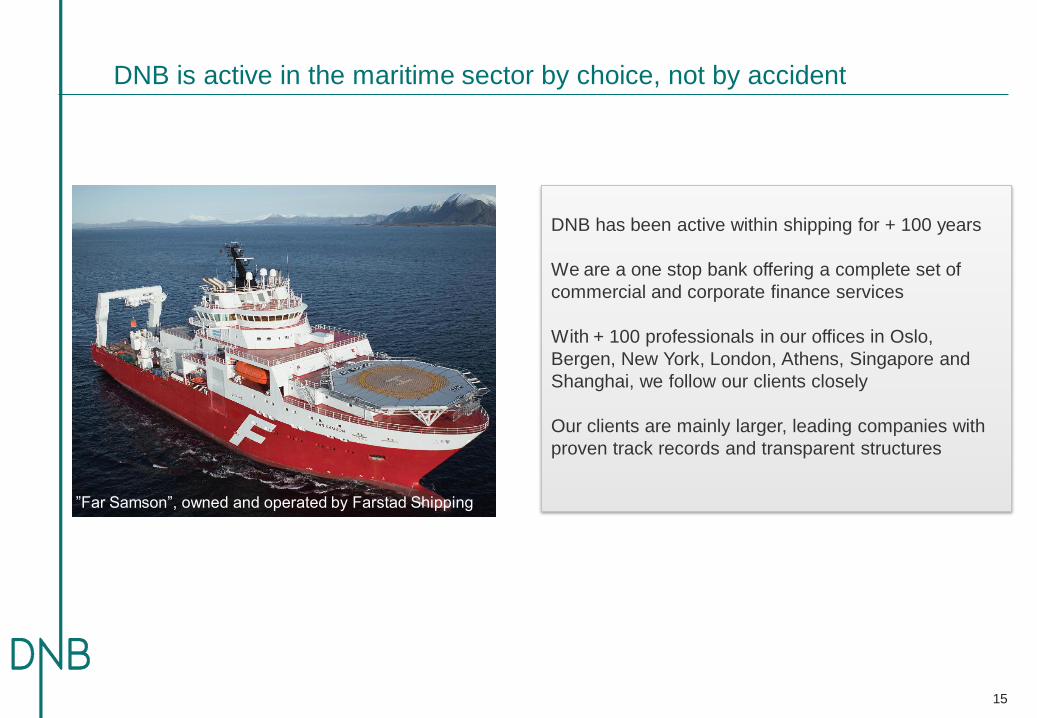

DNB is active in the maritime sector by choice, not by accident

15

DNB has been active within shipping for + 100 years

We are a one stop bank offering a complete set of

commercial and corporate finance services

With + 100 professionals in our offices in Oslo,

Bergen, New York, London, Athens, Singapore and

Shanghai, we follow our clients closely

Our clients are mainly larger, leading companies with

proven track records and transparent structures

”Far Samson”, owned and operated by Farstad Shipping

We are long term and relationship driven

16

• Our core clients are typically leading integrated shipping companies

• We prioritize clients where we have a good and close dialogue and

who use a broad range of DNB products

• We aim to keep a good credit quality, our credit guidelines being

based upon the “4 Cs”:

Client

Collateral

Cash flow

Covenants

The 4 C’s in the Credit Guidelines

DNB is maintaining a diversified portfolio within shipping and offshore

17

Offshore is the largest single segment with

27%. It is comprised of drilling rigs, support-

and specialized vessels

Industrial shipping, such as gas, ro/ro,

chemical and cruise totals 23%

Within tankers, dry bulk and container the

share is 14%, 12% and 11% respectively.

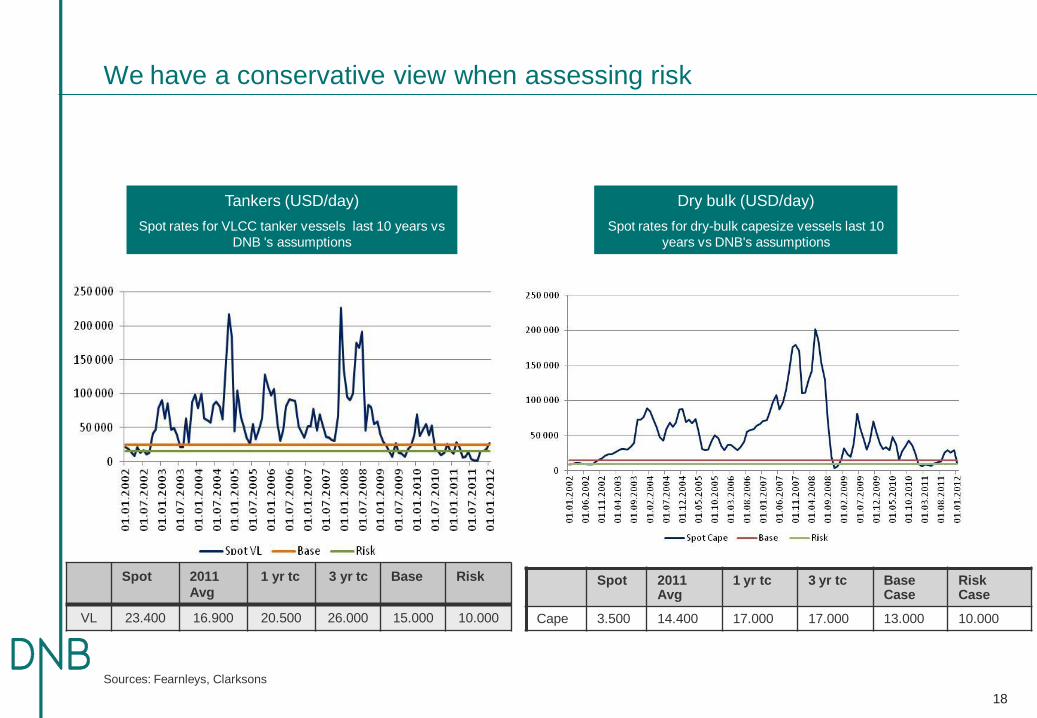

Dry bulk (USD/day)

Spot rates for dry-bulk capesize vessels last 10

years vs DNB's assumptions

Tankers (USD/day)

Spot rates for VLCC tanker vessels last 10 years vs

DNB 's assumptions

We have a conservative view when assessing risk

Sources: Fearnleys, Clarksons

18

Spot 2011 Avg

1 yr tc 3 yr tc Base Case

Risk Case

Cape 3.500 14.400 17.000 17.000 13.000 10.000

Spot 2011

Avg

1 yr tc 3 yr tc Base Risk

VL 23.400 16.900 20.500 26.000 15.000 10.000

19

In Offshore the activity is high, and the outlook positive

The sentiment is positive due to the high oil

price and increasing energy demand.

Especially the deep water drilling market is

seeing close to 100% utilization

Again, from the bank’s point of view, selecting

the right clients in a growing industry is key.

Sources: IHC Petrodata, Reuters

Sources: Clarkson, Galbraiths

Spot 2011 Avg

1 yr tc 3 yr tc Base Case

Risk Case

Cape 3.500 14.400 17.000 17.000 13.000 10.000

Panmx 5.400 11.340 11.250 11.600 12.000 8.000

Handy 5.700 10.900 7.250 10.000 12.000 8.000

Dry bulk: Lower spot rates, as expected. Some t/c activity at higher levels

The cape market experienced a strong 2nd half

2011, but the spot rates are now very low.

Currently, there are low spot rates in all

segments.

Somewhat higher forward rates.

Tanker markets are so far better than expected.

Spot 2011

Avg

1 yr tc 3 yr tc Base Risk

VL 23.400 16.900 20.500 26.000 15.000 10.000

Suez 21.600 19.200 16.000 20.000 15.000 10.000

Afra 12.700 13.500 13.750 16.000 14.000 8.000

Tanker spot rates have been increasing since

September 2011

Forward rates are lower, but at fairly acceptable

levels

Source: Clarkson

The 2nd hand values dropped substantially and rapidly in 2009. The reduction

has continued especially for older vessels, but at a slower pace.

VLCC 2012 values, vs the peak in 2008 and the

record low levels in 2002.

USD mill.

Source: Clarkson

Containers: Supply of new vessels is expected to increase more than

demand in 2012 and 2013. Rates appear to have bottomed out.

23

Rate developments 2009 - 2012

Source: Alphaliner

The shipping portfolio has been reduced since 2008, both in absolute numbers

and as a share of DNB’s total portfolio

EaD NOK bill.

The shipping exposure has been reduced since

2008, especially within Dry Bulk.

The portfolio is around 7% of the

bank’s total portfolio vs. 10% in 2008

24

Including Dry

Bulk and Tankers

NOK bill.

25

The total Division

The tanker segment The Dry Bulk segment

The container segment

Increasing PD levels in the division, especially within dry bulk, as expected.

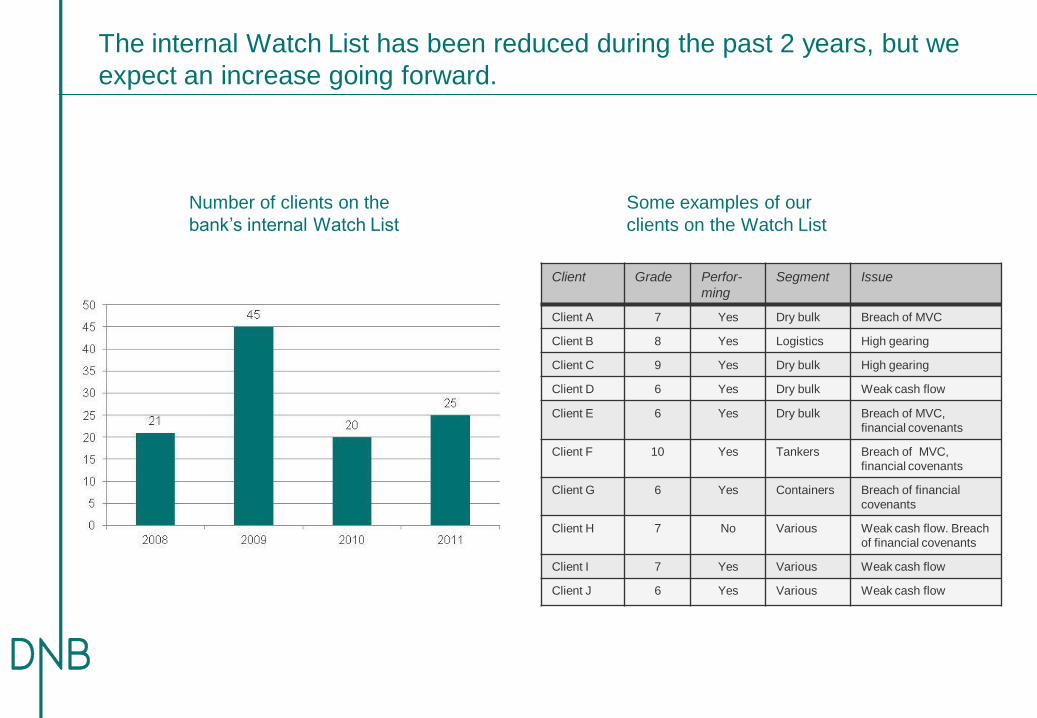

NOK bill.

Client Grade Perfor-

ming

Segment Issue

Client A 7 Yes Dry bulk Breach of MVC

Client B 8 Yes Logistics High gearing

Client C 9 Yes Dry bulk High gearing

Client D 6 Yes Dry bulk Weak cash flow

Client E 6 Yes Dry bulk Breach of MVC,

financial covenants

Client F 10 Yes Tankers Breach of MVC,

financial covenants

Client G 6 Yes Containers Breach of financial

covenants

Client H 7 No Various Weak cash flow. Breach

of financial covenants

Client I 7 Yes Various Weak cash flow

Client J 6 Yes Various Weak cash flow

The internal Watch List has been reduced during the past 2 years, but we

expect an increase going forward.

Number of clients on the

bank’s internal Watch List

Some examples of our

clients on the Watch List

27

DNB reports the aggregate of Non-performing and Net doubtful commitments.

The aggregate of the Non-performing and Net

doubtful commitments for the DNB group totalled

NOK 19.5 billion at year end 2011.

The shipping share was 22% and was more than

75% performing.

The shipping companies and the banks usually find ways to solve

challenging situations. In very few cases, the bank becomes a shipowner

28

• Providing additional guarantees or

security

• Raising additional capital

• Reducing or stopping dividends

• Cancelling or postponing newbuildings

• Scrapping vessels

• Selling assets

• Cutting costs

• Modifying, postponing or waiving

covenants

• Moratorium, stretching the repayment

schedule

• "Bridge loans" - solving temporary

liquidity challenges

• Restructuring – in several ways

Bank Contribution Shipowner Contribution

ILLUSTRATIVE CASE: 70% Financing of a USD 1 bill. acquisition.

Values drop by 50% whereas the loan loss is 1% of the original loan amount.

29

2006: Our well established client acquires a fleet of modern

vessels. A bankgroup led by DNB provides 70% financing

based upon 1st pr. mortgages and a set of covenants. DNB’s

share of the loan is 30%. It is a 7 year facility with a 15 year

profile.

2008: Values are down 30%, the client cuts costs and stops

dividends. Expect satisfactory EBITDA next 2 years due to

contract coverage. The bank group reduces the min. value

clause (MVC) to 100% for 2 years.

2010: Values drop a further 15%, and the cash flow is

weak. The company attracts some new hybrid capital, the

banks agree to reduce the MVC for a further year and forego

installments.

2012: Values drop a further 15%. In a theoretical WORST

CASE scenario the Client gives up, and the banks sell the

assets, realizing a loss of MUSD 7, ie 1% of the original loan

amount. DNB’s share of the loss is MUSD 2.4.

70% financing of a USD 1.000 mill. investment

• Valued are provided by recognized brokers. We finance mostly

standard vessels

• We complete detailed cash flow analysis of our clients based

upon base- and risk case assumptions

MUSD

30

Writedowns: Shipping has a good track record

The accumulated specified SOL writedowns

during the past 3 years have been NOK 850

mill, ie. 0,15% p.a. of the portfolio

The shipping write-downs have been between 5%

and 9% of DNB’s total writedowns last 3 years

DNB maintains its position as a leading shipping, offshore and logistics bank,

delivering strong results each year

The Shipping division’s financial

performance, 2009 - 2011

Top maritime bookrunners according to Deallogic

NOK mill.

31

In Summary...

32

1. DNB is the leading bank in Norway with strong earnings and a sound capital base

2. DNB has a proven track record within shipping, delivering strong results each year

3. By concentrating on the larger and leading companies within each segment the risk

is acceptable, and these companies have a high demand for non-lending products

4. We are experiencing a challenging year, but we have substantial loss absorbing

capacity and are therefore confident that 2012 will be profitable for the division