document of the world bankdocuments.worldbank.org/curated/en/848751484661114608/pdf/icr3990... ·...

TRANSCRIPT

Document of The World Bank

Report No: ICR00003990

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IBRD-81640)

ON A

LOAN

IN THE AMOUNT OF US$2 BILLION

TO THE

REPUBLIC OF INDONESIA

FOR A

PROGRAM FOR ECONOMIC RESILIANCE, INVESTMENT AND SOCIAL ASSISTANCE IN INDONESIA

December 22, 2016

Macroeconomic and Fiscal Management Global Practice East Asia and Pacific Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective 22 December 2016)

Currency Unit = IDR 1.00 = US$ [ 0.0001 ] US$ 1.00 = [ 13,450.8 ]

FISCAL YEAR 2017

ABBREVIATIONS AND ACRONYMS

AAA Analytical and Advisory Activities Jamkesmas Jaminan Kesehatan Masyarakat (Health Insurance Reform Scheme)

ADB Asian Development Bank JBIC Japan Bank for International Cooperation

AusAID Australian Agency for International Development

JICA Japan International Cooperation Agency in Indonesia

Bappenas Badan Perencanaan Pembangunan Nasional (National Development Planning Agency)

KUR Kredit Usaha Rakyat (People’s Business Credit)

BCP Basel Core Principles LKPP Lembaga Kebijakan Pengadaan Barang/Jasa Pemerintah (National Public Procurement Office)

BI Bank Indonesia LPS Indonesia Deposit Insurance Corporation

BKPM Badan Koordinasi Penanaman Modal (Indonesia Investment Coordinating Board)

MDFTIC Multi-Donor Trust Fund for Trade and Investment Climate

BLT Bantuan Langsung Tunai (Cash Transfer)

MenPAN Kementrian Pemberdayaan Aparatur Negara (State Ministry of State Apparatus Reform)

BPK Badan Pemeriksa Keuangan (State Audit Agency)

MoF Ministry of Finance

BPKP Badan Pengawas Keuangan dan Pembangunan (Finance and Development Supervisory Agency)

MoT Ministry of Trade

BPN Badan Pertanahan Negara (National Land Authority)

MPW/MoPW Ministry of Public Works

BPS Badan Pusat Statistik (Central Bureau of Statistics)

MTEF Medium-Term Expenditure Framework

Bps Basis points NGO Non-Governmental Organizations

BSM Beasiswa untuk Siswa Miskin (Scholarship for Poor Students)

NPPO National Procurement Policy Office

CATS Customs Advanced Trade System NTS National Targeting System

CDD Community Driven Development OECD Organization for Economic Cooperation & Development

CMEA Coordinating Ministry of Economic Affairs

OJK Otoritas Jasa Keuangan (Indonesia Financial Services Authority)

CPI Consumer Price Index OP Operational Policy

CPS Country Partnership Strategy PEFA Public Expenditure and Financial Accountability

CY Calendar Year PERISAI Program for Economic Resilience, Investment and Social Assistance in Indonesia

DAK Dana Alokasi Khusus (Special Allocation Funds)

PER Public Expenditure Review

DAU Dana Alokasi Umum (General Allocation Funds)

PESF Public Expenditure Support Facility

DB Doing Business PFM Public Financial Management

DDO Deferred Drawdown Option PINTAR Project for Indonesian Tax Administration Reform

DG Directorate General PKH Program Keluaraga Harapan (Conditional Cash Transfer Program)

DJPU Direktorat Jenderal Pengelolaan Utang (Directorate General for Debt Management)

PNPM MandiriProgram Nasional Pemberdayaan Masyarakat (National Program for Community Empowerment)

DGH Directorate General of Highways in MoPW

PP Presidential Regulation

DGT Directorate General Tax PPP Public-Private Partnership

DIPA Budget Activity Lists RPJMN National Medium-Term Development Plan

DPL Development Policy Loan SAL Sisa Anggaran Lebih (Unspent Excess Budget)

DPR Dewan Perwakilan Rakyat (People’s Consultative Assembly)

Sakernas Survei Angkatan Kerja Nasional (National Labor Force Survey)

EAP East Asia Pacific SBI Sertifikat Bank Indonesia (Bank Indonesia Certificate)

FDI Foreign Direct Investment SME Small and Medium Enterprise FPO Fiscal Policy Office SOE State Owned Enterprises

FSAP Financial Sector Assessment Program SPAN Sistem Perbendaharaan dan Anggaran Negara (State Treasury and Budget System)

FSSC Financial System Stability Coordination

SOE State Owned Enterprise

FSSF Financial Sector Stability Forum SUN Surat Utang Negara (Government Debt Securities)

FSSN Financial System Safety Net Susenas Survei Sosial Ekonomi Nasional (National Household Socio-Economic Survey)

FY Fiscal Year TEPPA

Tim Evaluasi dan Pengawasan Pelaksanaan Anggaran (Budget Implementation Evaluation and Supervisory Team)

GDP Gross Domestic Product TNP2K

Tim Nasional Percepatan Penanggulangan Kemiskinan (National Team for Acceleration of Poverty Reduction)

GFMIS Government Financial Management Information System

TSA Treasury Single Account

GNI Gross National Income UKP4

Unit Kerja Presiden Bidang Pengawasan dan Pengendalian Pembangunan (Presidential Working Unit for Supervision and Management of Development)

GoI Government of Indonesia US$ United States Dollars

IBRD International Bank for Reconstruction and Development

USDRP Urban Sector Development and Reform Project

IDR Indonesian Rupiah VAT Value Added Tax IMF International Monetary Fund WB World Bank IT Information Technology WBG World Bank Group

Senior Global Practice Director: Carlos Felipe Jaramillo

Country Director: Sector Practice Manager:

Rodrigo Chaves Ndiame Diop

Project Team Leader: Hans Anand Beck

ICR Team Leader: Hans Anand Beck

REPUBLIC OF INDONESIA

PROGRAM FOR ECONOMIC RESILIANCE, INVESTMENT AND SOCIAL ASSISTANCE IN INDONESIA (P130048)

CONTENTS

ABBREVIATIONS AND ACRONYMS ....................................................................... ii DATA SHEET ................................................................................................................ ii 1. Program Context, Development Objectives and Design ............................................ 1

1.1 Context at Appraisal ............................................................................................. 1 1.2 Original Program Development Objectives (PDO) and Key Indicators (as approved) .................................................................................................................... 4 1.3 Revised PDO (as approved by original approving authority) and Key Indicators, and reasons/justification .............................................................................................. 4 1.4 Original Policy Areas Supported by the Program (as approved) .......................... 4 1.5 Revised Policy Areas (if applicable) ..................................................................... 5 1.6 Other significant changes ...................................................................................... 5

2. Key Factors Affecting Implementation and Outcomes .............................................. 5 2.1 Program Performance ........................................................................................... 5 2.2 Major Factors Affecting Implementation: ............................................................ 6 2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization: ... 10

3. Assessment of Outcomes .......................................................................................... 11 3.1 Relevance of Objectives, Design and Implementation ....................................... 11 3.2 Achievement of Program Development Objectives ........................................... 16 3.4 Justification of Overall Outcome Rating ............................................................ 21 3.5 Overarching Themes, Other Outcomes and Impacts .......................................... 21 3.6 Summary of Findings of Beneficiary Survey and/or Stakeholder Workshops ... 21

4. Assessment of Risk to Development Outcome ......................................................... 22 5. Assessment of Bank and Borrower Performance ..................................................... 22

5.1 Bank Performance ............................................................................................... 22 5.2 Borrower Performance ........................................................................................ 23

6. Lessons Learned........................................................................................................ 24 7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners ........... 26 Annex 1 Bank Lending and Implementation Support/Supervision Processes .............. 27 Annex 2. Beneficiary Survey Results ........................................................................... 28 Annex 3. Stakeholder Workshop Report and Results ................................................... 29 Annex 4. Summary of Borrower's ICR and/or Comments on Draft ICR ..................... 30 Annex 5. Comments of Co-financiers and Other Partners/Stakeholders ...................... 31 Annex 6. List of Supporting Documents ...................................................................... 32 MAP .............................................................................................................................. 33

i

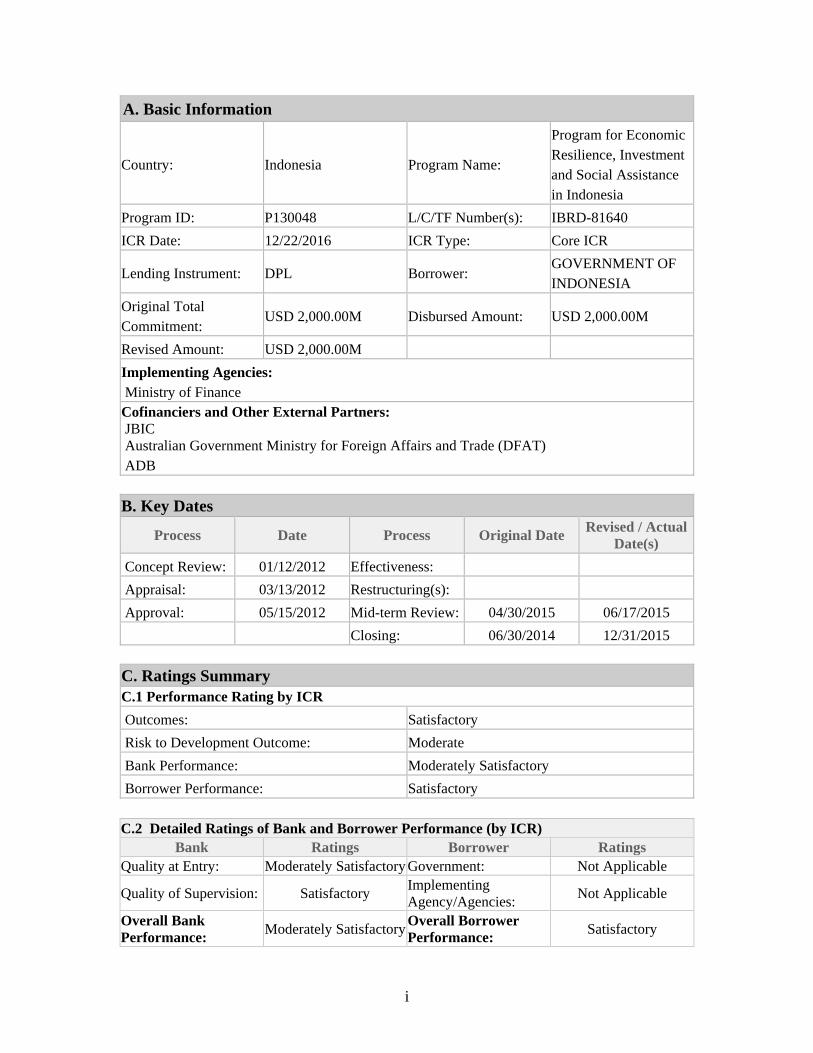

A. Basic Information

Country: Indonesia Program Name:

Program for Economic Resilience, Investment and Social Assistance in Indonesia

Program ID: P130048 L/C/TF Number(s): IBRD-81640

ICR Date: 12/22/2016 ICR Type: Core ICR

Lending Instrument: DPL Borrower: GOVERNMENT OF INDONESIA

Original Total Commitment:

USD 2,000.00M Disbursed Amount: USD 2,000.00M

Revised Amount: USD 2,000.00M

Implementing Agencies: Ministry of Finance Cofinanciers and Other External Partners: JBIC Australian Government Ministry for Foreign Affairs and Trade (DFAT) ADB B. Key Dates

Process Date Process Original Date Revised / Actual

Date(s)

Concept Review: 01/12/2012 Effectiveness:

Appraisal: 03/13/2012 Restructuring(s):

Approval: 05/15/2012 Mid-term Review: 04/30/2015 06/17/2015

Closing: 06/30/2014 12/31/2015 C. Ratings Summary C.1 Performance Rating by ICR

Outcomes: Satisfactory

Risk to Development Outcome: Moderate

Bank Performance: Moderately Satisfactory

Borrower Performance: Satisfactory

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR) Bank Ratings Borrower Ratings

Quality at Entry: Moderately Satisfactory Government: Not Applicable

Quality of Supervision: Satisfactory Implementing Agency/Agencies:

Not Applicable

Overall Bank Performance:

Moderately SatisfactoryOverall Borrower Performance:

Satisfactory

ii

C.3 Quality at Entry and Implementation Performance Indicators

Implementation Performance

Indicators QAG Assessments

(if any) Rating:

Potential Problem Program at any time (Yes/No):

No Quality at Entry (QEA):

None

Problem Program at any time (Yes/No):

No Quality of Supervision (QSA):

None

DO rating before Closing/Inactive status:

Moderately Satisfactory

D. Sector and Theme Codes

Original Actual

Sector Code (as % of total Bank financing)

Central Government (Central Agencies) 63 63

General finance sector 25 25

Other social services 12 12

Theme Code (as % of total Bank financing)

Economic statistics, modeling and forecasting 13 13

Public expenditure, financial management and procurement

37 37

Regulation and competition policy 37 37

Social Safety Nets/Social Assistance & Social Care Services

13 13

E. Bank Staff

Positions At ICR At Approval

Vice President: Victoria Kwakwa Pamela Cox

Country Director: Rodrigo A. Chaves Stefan G. Koeberle

Practice Manager/Manager:

Ndiame Diop Sudhir Shetty

Program Team Leader: Hans Anand Beck Enrique Blanco Armas

ICR Team Leader: Hans Anand Beck

ICR Primary Author: William E. Wallace

iii

F. Results Framework Analysis

Program Development Objectives (from Project Appraisal Document) Enhance the Government's crisis preparedness to address the potential adverse impact of ongoing volatility in financial markets on the Government's ability to meet its gross fiscal financing needs from markets Revised Program Development Objectives (if any, as approved by original approving authority) (a) PDO Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1 : N/A

Value (quantitative or Qualitative)

Date achieved Comments (incl. % achievement)

(b) Intermediate Outcome Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised

Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1 : Members of OJK Preparation Teams meet on a regular basis and develop joint reports on plans for establishment of new agency

Value (quantitative or Qualitative)

OJK preparation team not met

OJK now functioning as a fully fledged financial sector regulator

Date achieved 05/01/2012 12/31/2015 Comments Fully achieved, and sustained.

iv

(incl. % achievement)

Indicator 2 :

In the absence of a sudden capital outflow crisis (the 3rd risk scenario as articulated in the program document), the overall financial system remains stable as measured by the absence of a financial sector crisis.

Value (quantitative or Qualitative)

No financial crisis

No financial crisis

Date achieved 05/01/2012 12/31/2015 Comments (incl. % achievement)

Fully Achieved

Indicator 3 :

If there is a failure of a financial institution, the Financial Sector Stability Coordination Forum takes timely and appropriate measures to address it.

Value (quantitative or Qualitative)

N/A

There was no institutional failure. No financial crisis. However crisis simulations done quarterly.

Date achieved 05/01/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved

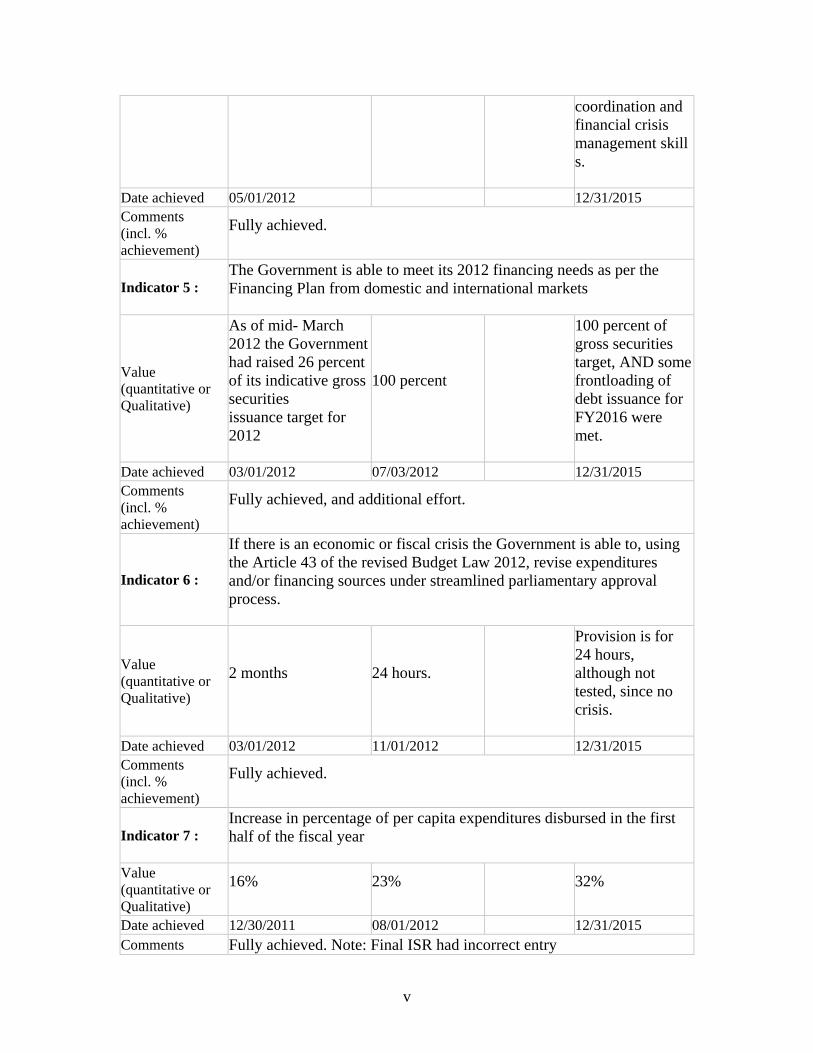

Indicator 4 :

Improved common understanding among the authorities (MoF, BI, LPS and OJK) of the definition of a systemic financial institution, and the policy options and measures that can be used in the event of a failure, which minimize losses in state funds

Value (quantitative or Qualitative)

No coordinated and commonly held understanding exists.

FKSSK taking leading role in coordination and decision making and leading medium-term work on important policy issues. FKSSK has taken efforts to strengthen interagency

v

coordination and financial crisis management skills.

Date achieved 05/01/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved.

Indicator 5 : The Government is able to meet its 2012 financing needs as per the Financing Plan from domestic and international markets

Value (quantitative or Qualitative)

As of mid- March 2012 the Government had raised 26 percent of its indicative gross securities issuance target for 2012

100 percent

100 percent of gross securities target, AND some frontloading of debt issuance for FY2016 were met.

Date achieved 03/01/2012 07/03/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved, and additional effort.

Indicator 6 :

If there is an economic or fiscal crisis the Government is able to, using the Article 43 of the revised Budget Law 2012, revise expenditures and/or financing sources under streamlined parliamentary approval process.

Value (quantitative or Qualitative)

2 months

24 hours.

Provision is for 24 hours, although not tested, since no crisis.

Date achieved 03/01/2012 11/01/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved.

Indicator 7 : Increase in percentage of per capita expenditures disbursed in the first half of the fiscal year

Value (quantitative or Qualitative)

16%

23%

32%

Date achieved 12/30/2011 08/01/2012 12/31/2015 Comments Fully achieved. Note: Final ISR had incorrect entry

vi

(incl. % achievement)

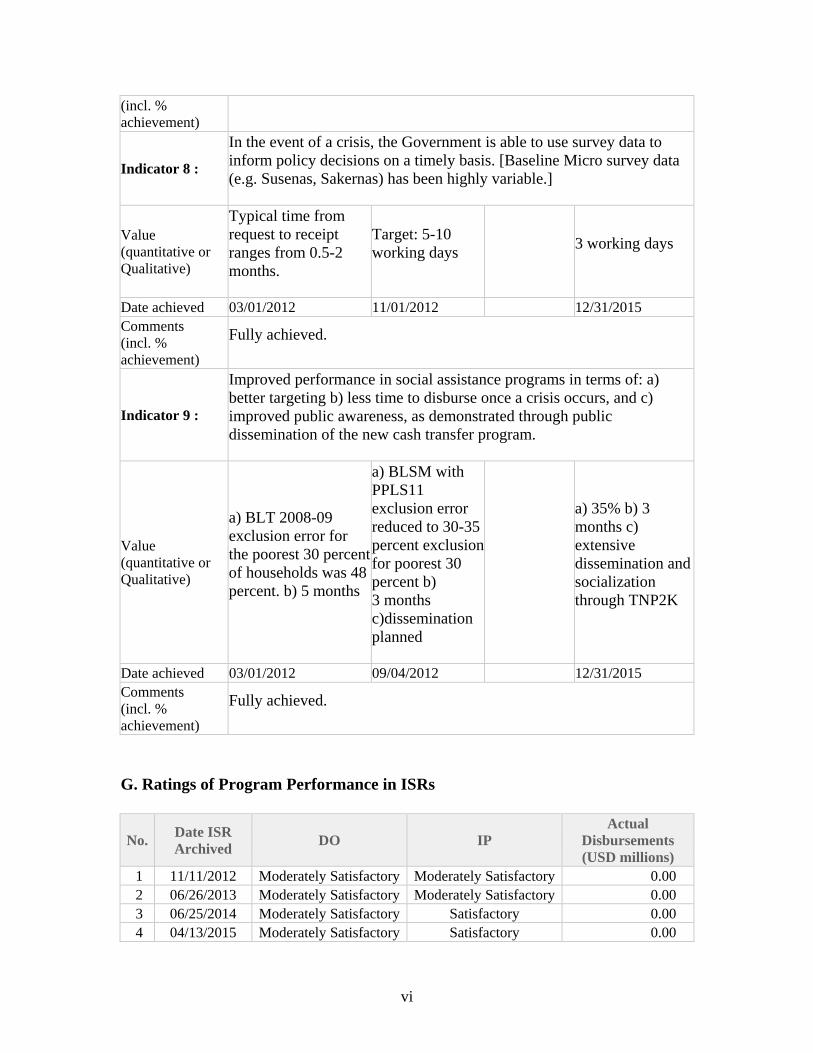

Indicator 8 :

In the event of a crisis, the Government is able to use survey data to inform policy decisions on a timely basis. [Baseline Micro survey data (e.g. Susenas, Sakernas) has been highly variable.]

Value (quantitative or Qualitative)

Typical time from request to receipt ranges from 0.5-2 months.

Target: 5-10 working days

3 working days

Date achieved 03/01/2012 11/01/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved.

Indicator 9 :

Improved performance in social assistance programs in terms of: a) better targeting b) less time to disburse once a crisis occurs, and c) improved public awareness, as demonstrated through public dissemination of the new cash transfer program.

Value (quantitative or Qualitative)

a) BLT 2008-09 exclusion error for the poorest 30 percent of households was 48 percent. b) 5 months

a) BLSM with PPLS11 exclusion error reduced to 30-35 percent exclusion for poorest 30 percent b) 3 months c)dissemination planned

a) 35% b) 3 months c) extensive dissemination and socialization through TNP2K

Date achieved 03/01/2012 09/04/2012 12/31/2015 Comments (incl. % achievement)

Fully achieved.

G. Ratings of Program Performance in ISRs

No. Date ISR Archived

DO IP Actual

Disbursements (USD millions)

1 11/11/2012 Moderately Satisfactory Moderately Satisfactory 0.00 2 06/26/2013 Moderately Satisfactory Moderately Satisfactory 0.00 3 06/25/2014 Moderately Satisfactory Satisfactory 0.00 4 04/13/2015 Moderately Satisfactory Satisfactory 0.00

vii

5 12/18/2015 Moderately Satisfactory Satisfactory 2000.00 H. Restructuring (if any) Not Applicable

1

1. Program Context, Development Objectives and Design The main objective of the Program for Economic Resilience, Investment and Social Assistance in Indonesia (known as PERISAI for its Indonesian Acronym) was to enhance the Government’s economic crisis preparedness (full Program Development Objective (PDO) in section 1.2). Learning the lessons from the Asian Financial Crisis of 1997/98 and more recently 2008/09, the Government wanted to ensure that essential public expenditures were maintained and, if necessary, augmented to provide economic stimulus during periods of stress. The operation included confidence-boosting policy measures and financing, with the option to defer withdrawal of the financing from the Bank and development partners until the government saw fit. The financing, a part of which was PERISAI, would help the Government meet its gross financing needs in the event that worsening global financial market conditions hindered Indonesia from accessing fiscal financing. PERISAI was thus designed as contingent financing or insurance on the basis of a government financing plan and confidence building measures, but in practice was available to the client upon a simple withdrawal request, subject to a general assessment that the program and macroeconomic environment was on track (see section 2.2, 3.1 and 4 for more detailed discussion). Upon the approval of the DPL, the government had put in place confidence boosting measures focused on maintaining financial sector stability, sustaining critical public expenditures and supporting the poor and vulnerable, that were sustained and strengthened over the period of the operation up to an beyond the withdrawal of the loan proceeds in September 2016.

1.1 Context at Appraisal By 2011 Indonesia had recovered from the 2008/2009 global financial crisis (GFC), supported by an effective policy response and high commodity prices. Growth had risen to 6.5 percent, the highest since before the Asian Financial Crisis (AFC) in 1997/98, supported by strong domestic consumption. The government debt to GDP ratio had fallen below 25 percent, fiscal deficits were running below 2 percent of GDP (less than 1 percent in 2010), and the primary balance had remained in surplus despite the GFC. On the external side, the current account was in surplus through the 3rd quarter (Q3) of 2011. Inflation was around 4 percent in the first half of 2012, low by Indonesian standards. Recognizing these fundamentals, Fitch (December 2011) and then Moody’s (January 2012) returned Indonesia to an investment grade rating. Despite the improved economic position, the authorities were concerned about vulnerability to volatile international financial markets and commodity price shocks. Indonesia has an open capital account, elevated levels of externally mobile capital, a large share of foreign holdings in government securities, and a legacy of risk aversion from the crisis in 1997/98. High bond yields in Indonesia combined with central bank liquidity injections in developed countries had generated strong portfolio flows increasing the sense of vulnerability.

2

This vulnerability was reinforced in the context of the turmoil around a possible Greece exit (‘Grexit’) from the Euro from August 2011 through October 2011. Grexit created turmoil in global markets with the MOVE (measuring volatility in global bond markets) and the VIX (measuring volatility in global equity markets) rising by over 100 percent and 33 percent respectively between the 2nd and 4th quarter of 2011 (see Table 1). In Indonesia the rupiah lost 4.5 percent, despite a drawdown of reserves of over US$10 billion (around 9 percent of total reserves), and Indonesia’s international bond spread (as measured by the Indonesia specific Emerging Markets Bond index, EMBI) rose by 80 basis points. In contrast, Indonesia’s domestic government bond market was stable, as Bank Indonesia, and to an extent the Ministry of Finance (MoF), bought back bonds in the secondary market. While temporarily stabilizing, the policy may have masked bond risks faced by investors and risked monetizing the fiscal deficit. Furthermore, sustained volatility remained a risk to the Government’s access to finance. Table 1 Key Economic Indicators between loan approval and disbursement

VIX MOVE EMBI Global

EM

Oil Price (Brent)

Exchange Rate

Yield 5 year

CPI Real GDP

Index Index Index

(last of month)

US$/barrel Avg percent percent

yoy percent

yoy

2011 Q1 101.7 18.8 116.0 8863.0 7.8 6.6 6.5

Q2 79.1 16.8 111.0 8569.3 6.9 5.5 6.3

Q3 91.1 23.8 104.8 8636.3 6.4 4.6 6.0

Q4 105.8 35.0 423.3 107.6 9024.3 5.7 3.8 5.9

2012 Q1 80.4 19.7 398.3 123.7 9088.3 4.9 3.9 6.1

Q2 75.4 19.6 373.0 92.5 9411.7 5.4 4.3 6.2

Q3 72.0 17.8 346.7 111.5 9544.3 5.5 3.8 5.9

Q4 61.1 16.3 297.0 110.6 9630.0 5.1 3.7 5.9

2013 Q1 59.8 15.4 275.0 109.5 9694.7 4.7 5.0 5.5

Q2 61.7 14.8 301.7 102.6 9817.7 5.2 5.4 5.6

Q3 98.8 15.4 357.0 109.0 10938.3 7.6 7.9 5.5

Q4 75.0 14.2 341.5 111.6 11800.0 7.7 8.1 5.6

2014 Q1 65.3 15.4 353.7 108.0 11754.7 8.0 7.3 5.1

Q2 59.5 12.6 313.7 113.5 11704.0 7.6 6.7 5.0

Q3 57.0 13.4 287.0 96.5 11840.0 7.9 4.5 5.0

Q4 66.8 15.0 333.0 57.3 12239.3 7.9 8.4 5.0

2015 Q1 82.9 17.8 420.3 55.6 12857.3 7.2 6.4 4.7

Q2 82.7 13.9 388.7 61.2 13160.0 7.9 7.3 4.7

Q3 84.9 19.9 409.7 47.6 14055.0 8.6 6.8 4.7

Q4 75.2 17.4 438.7 36.5 13758.0 8.7 3.4 5.0 Source: Bloomberg, CEIC, MOVE, VIX. Notes: MOVE is the Merrill Lynch Option Volatility Estimate. VIX is a measure of the implied volatility of S&P 500 index options, as calculated by the Chicago Board Options Exchange (CBOE).

3

The authorities’ other concern was around peaking commodity and oil prices, and the commensurate fuel subsidy bill, or the detrimental poverty impacts if fuel prices were increased. International commodity prices (as measured by Indonesia’s net trade commodity index) peaked in Q3 of 2011 and international oil prices (reached US$123 a barrel in Q1 of 2012). Higher commodity and oil prices increased government revenues (directly and indirectly) but, as Indonesia was a net oil & gas importer, they increased fuel subsidies even more. In fact, had oil prices remained at their level in Q2 of 2011, they would have pushed Indonesia’s deficit over 3 percent breaching the State Finance Law limit. Anticipating the need to raise fuel prices significantly, the authorities were exploring introducing an unconditional cash transfer to mitigate the impact on poverty rates. The Government requested the World Bank provide a contingent support operation as an element of a broader crisis support program, including adopting confidence boosting policy measures and conventional DPLs. The Government wanted to sustain public spending and resurgent growth, but worried that repeated episodes of financial volatility would jeopardize access to financing from the markets, with risks to spending, and increased poverty. In parallel, and to address longer term reform priorities, the government requested increased financing through several new series of Development Policy Loans (DPLs) in support of complementary reforms in the financial sector (a Financial Sector and Investment Climate Reform and Modernization DPL or FIRM), the public sector (an Institutional, Tax Administration, Social and Investment DPL or INSTANSI) and infrastructure (a Connectivity DPL). Rationale for Bank Assistance: Based on the positive experience with a contingent loan during the GFC from 2009 to 2011 (the World Bank led Public Expenditure Support Facility (PESF 1 ), the Government requested that the World Bank use its convening power to create a large program of contingent finance to be effective in the event of a significant economic shock. The Government requested preparation of US$2 billion through PERISAI and that this PERISAI support be augmented with additional contingent financing from the Asian Development Bank, and the Australian and Japanese Governments to a total of US$5 billion. This amount, which constituted 12 percent of a total US$40 billion gross financing needs in 2011, was thought to be sufficient in the event of a moderate shock. In addition, PERISAI’s innovative policy and insurance objectives, intended to protect and reinforce the World Bank’s long term support program for Indonesia in the event of a financial shock. As such PERISAI was designed to build on and protect the reforms supported by Development Policy Loans (DPLs 1-8)), the poverty and social lending through a community driven development program (Program Nasional Pemberdayaan Mandiri Peduli (PNPM)) and the rest of the Bank Program. As insurance

1 The PESF was a US$2 billion DPL-DDO approved by the World Bank Board of Executive Directors in March 2009 in the aftermath of the Global Financial Crisis. It was not disbursed before closing in December 2010

4

it would provide confidence to the markets, and hence allow the authorities to sustain borrowing at reasonable rates. While the CPS 2009 to 2012 did not explicitly envisage contingent support, the PERISAI’s policy reform agenda was consistent with the 2009-12 CPS. It aimed to improve the ability of key Indonesian institutions to address and manage risks related to international financial market crises. In particular, the PERISAI was fully in line with the CPS focus on Strengthening Indonesia’s Institutions. Further, the CPS Progress Report issued in February 2011 highlights the instrumentality of the previous PESF contingent financing operation in providing timely contingent financing support to the Government at a time of crisis, and how this instrument can be used in the face of economic uncertainty.

1.2 Original Program Development Objectives (PDO) and Key Indicators (as approved) The main objective of the operation was to enhance the Government’s crisis preparedness to address the potential adverse impact of ongoing volatility in financial markets on the Government’s ability to meet its gross fiscal financing needs from markets. The PERISAI supported the government’s reform program under three pillars (policy areas)

i) Maintaining financial system stability ii) Sustaining critical public expenditures iii) Supporting the poor and vulnerable during a crisis

The Key indicators, as presented in the PERISAI were: Policy Area 1. Maintaining financial system stability: Enhanced Government preparedness towards preventing a systemic financial system crisis, as demonstrated by improved systemic monitoring, regular inter-agency consultations and coordination, and establishment of information sharing mechanisms. Policy Area 2. Sustaining critical public expenditures: Enhanced Government ability to meet its financing needs and maintain critical public expenditures, as measured by its continued access to markets. Policy Area 3. Supporting the poor and vulnerable during a crisis: Enhanced Government preparedness to mitigate the potential adverse impact on the poor and vulnerable households, as demonstrated by an improved cash transfer program.

1.3 Revised PDO (as approved by original approving authority) and Key Indicators, and reasons/justification N/A

1.4 Original Policy Areas Supported by the Program (as approved) i. The policy reform areas being supported under the proposed PERISAI, and

described in section 1.2, are fully in line with the Government’s program for

5

developing crisis mitigation and institutional response capability in the aftermath of the global financial crisis. In particular, the Indonesian Government developed a crisis management protocol to deal with financial crises. The Government also established a team to intensively monitor budget execution to enhance the effectiveness of fiscal stimulus packages should the need arise. The government increased its flexibility to react to a rapidly deteriorating external environment by increasing or reallocating expenditures while maintaining fiscal prudence. The Government also prepared to swiftly implement emergency social assistance measures, and enhance their impact.

1.5 Revised Policy Areas (if applicable) N/A

1.6 Other significant changes N/A

2. Key Factors Affecting Implementation and Outcomes

2.1 Program Performance PERISAI was prepared in order to protect Indonesia against a potential global financial shock. The operation, modeled on the previous PESF operation, was prepared in 5 months from the time the concept note was reviewed in December 2011 to loan approval in May 2012. As all prior actions were met prior to the signing of the loan agreement, all conditions in the program document were fulfilled. The operation’s closing date was first extended from June 2014 to June 2015 following a request to all financing partners. It was renewed at the government’s request until end-December 2015, and was disbursed in September 2015. As captured in the five implementation status and results reports (ISRs), program implementation performance improved over the course of the operation as the government held regular quarterly program monitoring meetings and the Bank exerted intensive economic monitoring.

DPL-DDO-PD

List conditions from Legal Agreement/ Program Document Status

Policy Area 1: Maintaining Financial System Stability 1. Ministry of Finance and Bank Indonesia created Joint Financial Services

Authority (OJK) Preparation Team Done

2. The Government established the Financial Sector Stability Coordination Forum under the Financial Services Authority (OJK) Law

Done

3. The Ministry of Finance prepared a National Crisis Management Protocol that sets forth mechanisms for systemic monitoring, coordination and information sharing on the financial system among Ministry of Finance, Bank Indonesia, Deposit Insurance Corporation (LPS) and the Financial Services Authority (OJK)

Done

Policy Area 2: Sustaining Critical Public Expenditures

6

4. Ministry of Finance issued a Financing Plan for 2012 that specifies the terms and circumstances under which the Government would draw on financing support available from the PERISAI and from Indonesia’s development partners providing related support.

Done

5. The Budget Law 2012 provided flexibility to the Government of Indonesia to use fiscal policy to stimulate demand in the event of an economic or fiscal crisis.

Done

6. The President established the Budget Implementation Evaluation and Supervisory Team (TEPPA) led by the Presidential Working Unit for Supervision and Management and Development (UKP4)

Done

Policy Area: 3 Supporting the Poor and Vulnerable during a Crisis 7. Statistics Indonesia (BPS) established an improved and standardized

mechanism for processing and making available household socio-economic and labor force survey data.

Done

8. Government strengthened the cash transfer program to be used in the event of a crisis, through: (i) improved targeting of poor and vulnerable households; and (ii) better dissemination of the program among key stakeholders.

Done

2.2 Major Factors Affecting Implementation: The overall implementation of the PERISAI was adequate. Factors contributing to successful implementation included: the strength of underlying analytical work; learning lessons from the preceding PESF, notably on the scope of policy reforms and government ownership, and mitigating macro and institutional risks identified in the program document by government conducting quarterly financing partners meetings. However, greater clarity should have been achieved at the design stage on the role of the Financing Plan in the event of withdrawal of the proceeds of the loan. Adequacy of Government Commitment The government commitment to PERISAI, was strong, led by the Ministry of Finance, and intensified during periods of global financial volatility. The Ministry of Finance requested PERISAI based on their experience with PESF and as part of a proactive response to financial market volatility in late 2011, caused by fears of Greece leaving the Euro. Their engagement with development partners deepened at the time of the “taper tantrum” (May 2013) and prior to the PERISAI drawdown in September 2015 when China devalued the Yuan causing financial turmoil in the region. With occasional delays due to the government budget cycle, quarterly meetings were held with partners, financing plans completed and clauses added to the budget to provide crisis flexibility. The engagement of the ministries/agencies responsible for Pillars 1 (OJK, BI) and 3 (TNP2K) was supported by direct Bank dialogue, but could have been encouraged more through the quarterly MoF led coordination process. The quarterly meetings did not feature updates on the pillars of the program covering the financial sector and protection for the poor and vulnerable. The government had met the conditions for PERISAI before approval and the expectation was only that program reforms be sustained. To assess whether progress had been sustained, or whether there had been backsliding,

7

Bank staff monitored progress through existing engagements with these agencies and regular Bank operational reporting. In the event of a financial or economic crisis, the quarterly meetings would have been a useful coordinating mechanism for the fiscal and social assistance response, complementing the FKSSK for the financial sector. Soundness of the Background Analysis The PERISAI Operation was built on a strong program of ongoing support. The goal of the operation was to safeguard Indonesia’s public spending from an external financial shock and the broader economic risks that were well identified by the World Bank through previous DPL and DDO operations and AAA. PERISAI (and PESF) built on 8 core DPLs (2004-2011) and associated projects and technical assistance engagements on the investment climate, the financial sector, public financial management and poverty reduction. Trust Funded support to the Government, notably on macroeconomic management (SEMEFPA), Public Financial Management MDTF, and Multi-Donor Poverty Trust Fund provided analysis, technical assistance and capacity building that underpinned PERISAI prior actions. The Indonesia Economic Quarterly report, dating back to 2009 (created as part of PESF), provided the data and analytical underpinning for a thorough understanding of Indonesia’s macro economy and was a product of the Bank team also responsible for PERISAI. The Government’s request to develop DPLs to support public sector reform (INSTANSI) and financial sector reform (FIRM) would parallel and reinforce PERISAI. Of particular relevance was INSTANSI, focusing on improving spending, including budget execution and poverty measurement, targeting and programs. FIRM also included a focus on financial sector stability including support to OJK and associated financial sector oversight agencies. While not a programmatic series, the single loan PERISAI built directly on the very similar PESF contingent loan, promoting sequential reforms. The first two pillars in PERISAI (“Financial Stability” and Sustaining Spending”) directly extend the reforms in corresponding PESF pillars. The third pillar in PESF on investment climate and competitiveness was replaced by a pillar on “supporting the poor and the vulnerable during a crisis” that grew out of a prior action in the “sustaining spending” pillar of PESF (a Presidential decree on Coordination of National Poverty Reduction). Finally, important analysis, including an ICR for PESF, provided underlying analytical work in each program area.

PESF ICR. Lessons learned under PESF, but not fully applied for PERISAI in the case of conditions for withdrawal, included the potential value of the contingent finance mechanisms proposed for PERISAI, the need for a strong set of confidence building measures in the correct areas, the need for post-crisis follow-up, the importance of carefully defining the context and conditions for withdrawal during loan design, using the funds as insurance and/or financing and the need to improve understanding among stakeholders of how this instrument could work to those aims.

8

Maintaining Financial System Stability. In May 2011, a Financial Sector Assessment Program (FSAP) was completed (this had also been an element of the PESF Program design). The FSAP laid out the vulnerabilities in the financial sector and provided the under-pining for the financial sector stability pillar of the operation. It was supplemented with work on risks in the banking sector, domestic and international demand for Indonesian bonds, and a crisis simulation exercises (these also continued during and beyond the operation).

Sustaining Critical Expenditures: The analytical underpinnings here are drawn from a Public Expenditure Review (PER) in 2009 (Towards 2015 – Spending for Indonesia’s Development) and a 2012 Public Expenditure and Financial Accountability (PEFA) report. The PEFA notes, among other things, weak and end-loaded budget execution particularly for capital, reflecting an excessive focus on ex-ante controls and compliance rather than delivery and performance.

Supporting the Poor and Vulnerable during a Crisis: This area also built on a rich stream of material starting from “Making the New Indonesia work for the Poor” in 2006 updated in “Protecting Poor and Vulnerable Households in Indonesia” (2012) and “Targeting Poor and Vulnerable Households in Indonesia” also 2012. Particularly useful to this operation, was the 2010 study on how crisis support had worked during the GFC in “Crisis Monitoring and Response System” (CMRS) from September 2010.

Assessment of the Project Design Indonesia’s macro-fiscal vulnerabilities were well known to the World Bank at the time of the design of the PERISAI operation. There had been a great deal of scrutiny, including by the World Bank the IMF and others, of the devastating impact on Indonesia of the Asian Financial Crisis in 1997/98. Similar attention was paid to Indonesia’s strong macro-fiscal response to the Global Fiscal Crisis in 2008/2009, in part due to World Bank led contingent support provided through the PESF program. Thus, PERISAI, correctly, started from PESF in proposing contingent financing support and a complementary set of “confidence building” measures. PERISAI also inherited advantages from PESF, simplifying the design and the mechanism for joint participation of development partner financiers, all of whom had been involved in the previous operation. The annual financing plan and the quarterly meetings to assess market conditions and performance against the financing plan were derived from PESF and contributed to creating and sustaining a common understanding. The program under PERISAI had only 8 relatively easily verified conditions in three pillars. In this regard it was simpler than PESF which had 11 conditions. The prior actions in PERISAI largely built on those in PESF, thus contributing to continuity and sustainability of reforms. The government agencies involved had relatively strong implementation capacity. The Ministry of Finance, in particular the Director General for Budget Financing and Risk Management and the Fiscal Policy Agency were very capable organizations. By 2012 the

9

Budget Finance and Risk Management DG had been managing Indonesia’s financing for over ten years including through a number of domestic and global shocks. The Fiscal Policy Agency, while newer, had developed quickly, including through World Bank support provided through SEMEFPA linked to the PESF operation. However, PERISAI inherited ambiguities from PESF that could have been clarified during design of PERISAI. PESF was a very innovative design, developed in the middle of the worst global financial crisis since the Great Depression. The speed of PESF’s design had left several unresolved ambiguities that affected PERISAI’s implementation. One such ambiguity was the potential for different interpretations of the trade-off between providing insurance and regular deficit financing. This ambiguity would affect the perception of how to best set thresholds and whether these thresholds should be limited to exogenous shocks. It also affected perceptions, especially among co-financing partners, of the broader contingent financing support and of how binding the Financing Plan was for loan disbursement under that arrangement, and hence required careful management of the relationship with those partners. Clarifying these ambiguities would have helped to smooth implementation. Assessment and Mitigation of Risk Several relevant risks were outlined in the PERISAI operation and were in effect mitigated by actions on the part of the Bank team and counterparts or did not materialize. These included: the complexity of the institutional arrangements in the financial sector; the possibility that financial support provided by PERISAI (and others) might not be sufficient in the event the crisis was severe; policy reversals; the impact of high oil prices and related subsidies on the government budget deficit; unfinished reforms in public financial management; and changes in the government’s borrowing strategy. The main risk involved the possibility of the program’s financial support being overwhelmed by the scale of a financial market shock. The risk of such a shock taking the Bank by surprise, was mitigated by the strength of the Bank team and their on-going macro-fiscal assessment (that forms a part of every DPL-DDO). In the event of an overwhelming shock, PERISAI would have been a valuable addition to a larger rescue effort. There was also a risk of back-sliding on the prior actions as “confidence boosting” measures. The quarterly meeting and the regular meetings of the FKSSK mitigated this risk. The government counterpart, augmented by Bank staff working in the financial area including on FIRM, were on top of the institutional developments linked into developments in the financial sector. The World Bank SEMFPA and Poverty teams were working closely in each of their areas, including on the INSTANSI DPL. The quarterly meeting provided a mechanism to raise risks of backsliding if needed. The Program Document identifies volatile (high at the time) oil prices and the corresponding high fiscal burden of subsidies as a risk, especially absent political consensus to raise fuel prices. If oil prices had remained well above US$100 a barrel,

10

Indonesia would have risked breeching the 3 percent of GDP fiscal deficit limit set in the State Finance Law. The risk here, not explicitly stated in the Program Document, was that the need for financing of the growing subsidy bill would have increased pressure to draw PERISAI. This risk was mitigated by the financing plan, the macro monitoring, and Indonesia’s reputation for addressing fuel subsidies when they became too large. Ironically, the risk of a sudden drop in oil prices and related fiscal revenues, and the commensurate pressure to draw PERISAI to cover the resulting financing gap, were not explicitly identified in the Program Document. When this drop in oil prices occurred, it resulted in a widening fiscal deficit and financing needs. Risks from unfinished PFM reforms including the delayed completion of SPAN are flagged and mitigated by the INSTANSI DPL and GFMRAP, TA and intensive policy dialogue. The policy dialogue through: complementary DPLs; a multi-donor trust funded PFM technical assistance program; and a, albeit delayed, PEFA assessment in 2012 all contributed to mitigating PFM risks identified at design. Social and environmental risks issues were negligible, and fiduciary, political and debt strategy risks were the same as in other parallel DPLs, so well understood. The social protection pillar directly contributed to mitigating poverty and vulnerability in the face of shocks. The intensive monitoring of implementation built into the program, and leverage of dialogue through other DPLs, combined to mitigate the political risks of policy reversal. This dialogue and the strength of the broader client relationship also allowed early assessment that the government’s overall official borrowing strategy would remain unchanged. Similarly, risks that a new elected government would reverse good policy implementation or overly expand the fiscal stance, were tackled across the Indonesia country program portfolio through formal policy engagement with all policy stakeholders during the transition period.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization: M&E Design: M&E design was appropriate and aided by the simplicity of the Policy Matrix. There were relatively few and simple prior actions and key indicators, and the latter were linked well to the PERISAI program.The results framework intermediate outcomes cover the program well. There is a good mix of qualitative and quantitative results indicators in the results framework. Qualitative indicators were for instance used in pillar 1 where institutions such as the financial services authority (OJK) was established. The M&E framework could adequately capture the creation and operation of institutions. Questions of attribution made it difficult to measure the impact of those institutions on financial sector stability. Quantitative indicators were appropriately used when measuring response times, disbursement and fiscal financing rates in pillars 2 and 3. One specific question relates to the choice of capital spending in the first half of the year as a share of budget as a results indicator. Improvements in the indicator might have included tracking not just progress on capital spending but also progress on budgeting reforms. An indicator of capital spending in relation to previous years’ outturn may have been more appropriate.

11

M&E Implementation: The M&E strategy was implemented in two main parts: firstly economic monitoring and the quarterly meetings, and secondly biannual monitoring of the DPL results indicators complemented by linked DPLs and Trust Funded engagements. The quarterly meetings of the Development Partners (The World Bank, ADB, Japan and Australia) with the Government to discuss macro-fiscal developments and program progress was critical and supported strong program monitoring and implementation. The financing plan was an integral element of these discussions. The quarterly meeting focused on the macro and financing picture. This focus was augmented by the PERISAI team’s general engagement, and the intensive monitoring of results indicators reflected in the preparation of thorough ISRs, in coordination with associated Bank teams responsible for engagements on the Financial Sector and for support for the Poor and Vulnerable. M&E Utilization: For intensive Economic Monitoring, based in part on the financial sector and fiscal stability indicators in the results framework, the PERISAI team, building on PESF, could tap support provided by the World Bank to the Fiscal Policy Agency (FPA) on macroeconomic capacity building through the SEMEFPA program. This provided the Bank insight and information on developing fiscal issues while building capacity within the FPA around the vulnerabilities identified in PERISAI. The Indonesia Economic Quarterly with its associated analytical foundations would also provide a strong foundation for understanding events as they played out in Indonesia. This intensive economic monitoring provided for strong assessments of macro performance and risks during program implementation, and in particularly at the time of disbursement. The information gathered through economic monitoring, in part based on the results framework, also informed the dialogue with government and among financing partners during quarterly PERISAI meetings. 2.4 Expected Next Phase/Follow-up Operation (if any): At the time this ICR is being written there is no request for a follow-on deferred drawdown loan. Nevertheless, literally everyone the ICR mission spoke with suggested that the kind of “insurance” PERISAI provides was valuable, although usually with some modification. One constraint identified was that the PERISAI loan, even if not disbursed, counts 100 percent against an increasingly narrow World Bank global lending headroom, and the borrowing limit for Indonesia, suggesting that alternative methods of contingent support could be considered.

3. Assessment of Outcomes

3.1 Relevance of Objectives, Design and Implementation2

2 As per the advice of CMU in review of 21 December 2016, this section follows the IEG rating scale (High, Substantial, Modest, Negligible)

12

Overall rating: Substantial Relevance of Objectives Rating: High The overall objectives of the program were, and remain, highly relevant. The reforms supported by the program, to enhance the government’s capacity to meet its financing needs while shielding capital and social spending, remain relevant today. Furthermore, contingent finance was and is a relevant loan modality to Indonesia given vulnerabilities to a global shock and rapid capital outflow. Indonesia remains at risk to global financial shocks through its open capital account, high levels of portfolio flows and risk aversion left from the Asian Financial Crisis. Shocks have been transmitted through a rapid pull-back in foreign portfolio investment (primarily government debt, and equity), severe depreciations in the rupiah, reductions in reserves and a spike in government interest rates. This played out most dramatically at the time of the GFC, when the rupiah depreciated by over 20 percent between the 3rd and 4th quarter of 2008, and interest rates (5-year government bond) rose to over 15 percent. Thus, the PDO remains relevant under both the FY13-15 CPS and the FY16-20 CPF. In the case of the latter, which aligns with the government’s own 2015-2019 development strategy, the PDO contributes to the achievement of CPF outcomes by preserving macro-economic stability for growth, and through Beam 1 (Leveraging the Private Sector: Investment, Business Climate and Functioning of Markets). PERISAI was aimed at enhancing the government’s crisis preparedness in the event of a shock to the financial sector that constrained spending and hurt the poor and vulnerable. It did this by: a) supporting the government on implementing confidence building measures to improve market confidence, and b) by leveraging Bank support with other development partners as insurance for budget finance to crowd in private support. The existence, and possible use, of such a program, safeguards the Bank- supported reform efforts across the portfolio. Relevance of Design Rating: Substantial While the policy content, as reflected in the designed policy matrix was relevant, there was too much space left at design for interpretation among financing partners of the loan disbursement criteria. A strength of the PERISAI operation is the relevance of the policy areas and prior actions to the program’s stated objectives. Any shock would have played itself out by risking financial sector stability and the ability to sustain spending and would have impacted on the needs of the poor and vulnerable. Thus pillars and actions in these areas represented appropriate choices on where the PERISAI, complemented by other Bank programs and working with other development partners, could assist Indonesia to avert shocks or better respond if they happened.

13

The financial sector conditions and the focus on capital spending proved particularly prescient, while the social assistance pillar, while relevant, faced a traditional challenge of targeting the near poor. Ramping up social spending, also critical for human development in general, may have been more appropriate than capital spending in response to a severe shock, given the lead times to putting ‘shovel-ready’ development projects in place. Nevertheless, capital spending was an area of long-standing weakness in the budget, with low execution rates, and an impact on aggregate demand and potential growth. More importantly, capital spending was most often the area cut during shocks in order to reduce financing needs, given its flexibility. The policy actions on improved data availability in the pillar on support for the poor and vulnerable seem relatively weak given the vulnerability of the poor and near poor and size of the operation. Essentially the action requires the statistics agency to make available data they already have, to other government agencies, within a week. Like capital spending, the policy action targeting improving the quality of social assistance (reducing inclusion and exclusion errors) was focused on existing programs of support for the poor. These programs could and were appropriately used when shocks occurred. However, a challenge faced by this and more targeted support to shock mitigation programs is how to address a shock where large numbers of (non-poor) were laid off, as these new beneficiaries would not have been detectable and hence targeted through existing systems. The exclusion of trade and investment, a policy pillar in PESF, is a design weakness. By 2012 Indonesia had relatively strong GDP and investment growth but export growth had turned negative (year on year) as had the current account balance. The current account deficit continued to increase and averaged over 3 percent of GDP in 2013 and 2014. This increasing current account deficit was offset by increasing portfolio flows from low-return advanced economies. This amplified the existing high risks of portfolio outflows. In addition, there was an explosion of trade and investment restrictions during this period. For example, the number of tariff lines subject to non-tariff measures (NTMs) on imports grew from 42 percent in 2009 to 51 percent in 2015 with many lines subject to multiple measures.3 While the PESF operation had explicitly targeted trade and investment reforms, PERISAI was prepared at a time where there was no strong government program of reform in these areas. However, the incoming government of President Jokowi focused on trade issues once again in 2015. Thus, with the benefit of hindsight, PERISAI could have helped avoid trade-restricting behavior, and bridged to the new government’s relative trade openness. The main design flaw was the failure to address the ambiguities inherited from PESF. While PERISAI is formally a stand-alone operation, in a real sense it was the second in a series. This simplified the design in many ways (PERISAI had similar pillars and the same partners as PESF for instance) but also meant problems in the PESF design were inherited.

3 Marks, S., “Non-Tariff Trade Regulations in Indonesia: Nominal and Effective Rates of Protection”, Bulletin of Indonesian Economic Studies, September 2016, pg. 1.

14

At design, there was a common understanding among the development partners and many in government that PERISAI was to be used as insurance against an exogenous shock, defined in a financing plan. In the spirit of the operation, described in the Program Document, the drawdown of PERISAI, like PESF, was to be triggered by a domestic interest rate rise above an agreed domestic bond yield threshold. While there was a general agreement on this principle, different co-financing partners had discretion to have different tolerances for the level of shock needed to make drawing the loan occur. The resulting financing plan constituted a consensus but this tension inherited from PESF persisted into PERISAI. In addition, the Government had a crisis management protocol that included but was not limited to the financing plan. Based on PESF, the government had introduced two clauses into the budget law. The first clause defined what constituted a crisis. The second clause indicated the measures the government could take. These clauses changed over time but at the time of PERISAI’s approval, the definition of a crisis was that: an “… emergency situation included (i) growth a minimum of 1 percent lower than the Budget assumption and deviation of other macro assumptions by a minimum of 10 percent, or 5 percent for crude oil lifting, which would lead to lower revenues and/or increased expenditures; (ii) systemic crisis in the domestic financial and banking system requiring additional funds for guaranteeing deposits for financial and non-financial institutions; (iii) a significant increase of financing costs, i.e. a rise in government bond yields.” A crisis, in the government definition, for any of these reasons would create pressure to request the financial support in PERISAI without the requisite breach of the thresholds in the Financing Plan. However, it can safely be said that if these crisis indicators occurred, then the bond-yield criteria in the financing plan were, as correlates, very likely also to be breached. The Government requested that the Bank take the lead in developing PERISAI but the partnership with the financing partners was never made formal. The government, learning from PESF, felt that markets believed that the World Bank had a strong grasp on Indonesia’s macroeconomic fundamentals and this would reinforce the Government’s access to market credit in a shock. Development partners were urged to join to achieve a program of sufficient size to be credible as insurance. However, inherited from PESF, development partners operated on different time frames, including for loan program preparation and extensions, and with different systems and disbursement mechanisms, making it problematic and unlikely that the full set of funds would be available, or available at the same time, in a crisis. In theory the only thing in common for the participating financing partners was the shared view of the Financing Plan. The Financing Plan was a government decree, but the plan’s role in the event of disbursement was not clear at the outset. To implement the insurance concept and reassure financing partners (with possibly different risk tolerances), PESF and then PERISAI introduced a financing plan. In the event of a moderate shock the design was for development partners, either in proportion or in sequence, to provide finance to make up the shortfall in government financing for a given maturity (for example 5 year bonds) at a given yield that was made explicit in the financing plan. This understanding was entered into with the government, and captured in the first financing plan of the operation, namely

15

the 2012 financing plan, and included as a prior action in the Loan Agreement. The initial logic in PERISAI was that the financing plan, as part of the program, could be changed when requested, in discussion with other development partners, but in the absence of such an agreement the Government would be out of compliance with the plan and could (or would) not draw. That strictness reflected the government’s own explicit approach to ‘tie-its hands’ regarding the circumstances under which it would seek to draw down the loan. This is not standard DPL DDO practice. Pursuant to OP 8.60, a regular DDO allows a country to postpone drawing down a Bank loan for a defined period after the loan has been declared effective. During this time the country must continue to implement the program being supported in accordance with its Letter of Development Policy and must maintain an adequate macroeconomic policy framework. The drawdown is available upon the country’s request, as applied in the case of PERISAI. The connection between the Government’s financing plan and the World Bank disbursement, was clarified in April 2014, but the Government chose to defer drawing down on the loan for nearly another year and half. The World Bank clarified to the government, and co-financing partners, that the Government can draw the funds if the program is on track and the macro situation satisfactory. However, in the spirit of PERISAI the government opted for the insurance value and extended the loan for one year, to the end of June 2015. It then requested all financiers to renew it to the end of December 2015, choosing to withdraw only in September 2015. Interviews with new representatives of donor financing partners at the time of writing the ICR indicated that they perceived the disbursement criteria to be more harmonized. Relevance of Implementation The Bank’s implementation support was responsive to changing needs and the operation remained important to achieving the country and program’s development objective. The continuous engagement through quarterly meetings was very effective. The quarterly meetings, linked closely to the financing plan and involving all the stakeholders made for a strong, and well appreciated, system including for monitoring and evaluation. This was augmented by the Bank’s engagement through SEMEFPA with the Fiscal Policy Agency and through the series of DPLs (especially FIRM and INSTANSI), GFMRAP and Trust Funded support on Poverty Reduction. Flexibility on the financing plan was good. Inevitably, given the variables and changing situations, the financing plan would need to be revised at least once each year and probably more often. The design allowed for this and the Bank team worked with government partners as situations evolved. The drawdown decision, while complex, was in the spirit of PERISAI. The key implementation issues around the drawdown decision were the design ambiguities, described above and the misunderstandings created.

16

The shock that triggered the loan withdrawal reflected domestic revenue shortfalls against an ambitious target for 2015, as commodity prices, and commodity revenues also fell. The first budget of President Jokowi and his administration reflected the need to dramatically step up capital and social spending, funded by a cut to fuel subsidies as fuel prices were raised, and complemented by a program of cash transfers to the poor and vulnerable. This fiscal and social assistance response was fully consistent with PERISAI’s objectives. The drawback was that the decline in oil prices (to roughly US$50 per barrel) that made the fuel price reform politically feasible also eliminated the fiscal space envisioned for the increased capital spending, as natural resource revenues declined with prices (see also section 2.2 on assessment of risk). The Government then adopted what proved to be ambitious estimates on tax and non-tax revenue. By mid-2015 the revenue shortfall was clear and the deficit was widening rapidly. This cash flow challenge became the domestic policy driver for disbursement. This is coupled with an external driver as financial markets were unsettled by volatility in the Chinese currency and stock markets. The international shock from global financial market volatility spilling in from China’s devaluation of the Renminbi, dramatically amplified risks arising from the domestic fiscal deterioration. The rupiah devalued (by over 6 percent in Q2 of 2015 alone), and government interest rates, proxied by the 5-year bond, approached the threshold in the financing plan in early September. The exchange rate rose to over 14,000 rupiah/US$ with market rumors of impending financing difficulties for stretched commodity linked corporates. The government foresaw challenges to finance the growing deficit and was fearful of crowding out private investment and pushing domestic interest rates significantly higher. Net foreign reserves at the central bank position declined towards US$100 billion, although this still constituted a comfortable buffer for imports at the time. The Ministry of Finance acted to safeguard capital and social spending by allowing the deficit to rise and drawing PERISAI. In 2015, the government for the first time in years was able to accelerate capital spending to support growth, fully in line with the new government plan to accelerate infrastructure and social spending. PERISAI financing was important to sustaining the momentum. The loan, once drawn, was deposited in Bank Indonesia and converted to Rupiah. Bank Indonesia appears to have had the added benefit of making the reserves available to the public reducing the mounting pressure on the rupiah. In sum while the macroeconomic uncertainty at the time of disbursement had a self-inflicted component as revenues were overestimated, there was also a severe external shock. The combination caused circumstances which the government deemed to warrant drawn down of the loan, and the funds to be used to maintain essential capital and social spending, fully in line with PERISAI’s Program Development objective.

3.2 Achievement of Program Development Objectives Overall Rating: Substantial4

4 As per the advice of CMU in review of 21 December 2016, this section follows the IEG rating scale (High, Substantial, Modest, Negligible)

17

Policy Area 1: Maintaining Financial System Stability Rating: High While difficult to attribute successes in the financial sector directly to PERISAI, prior actions and results were achieved, and built upon. There has been no backsliding and the institutional structure around financial sector oversight has improved significantly including the recent passage of a Financial Safety Net Law in 2016. The financial system has remained stable. The financial sector has been at the heart of Indonesia’s economic vulnerability reflected in several episodes after the global financial crisis that were transmitted to Indonesia. PERISAI was designed to support public spending in the event of an international financial shock that hindered the government’s access to fiscal financing in the markets. Such a shock occurred in the fourth quarter of 2011, less than a year after PERISAI’s predecessor support loan, PESF, had expired, contributing to the Government’s request to put a new operation in place. This episode was followed by additional shocks in the 3rd quarter of 2013 (the Taper Tantrum) and in the 3rd quarter of 2015 (Renminbi devaluation) when PERISAI was drawn. The PERISAI operation, through Policy Pillar 1, successfully supported the institutional framework for financial sector oversight, with results indicators 1-4 fully achieved and even extended with the Landmark Financial Safety Net Law in 2016. This framework included an integrated financial sector supervisor (the FSA, known by its Indonesian acronym of OJK) and the institutional base for coordinating institutions (a Financial Stability Forum, FKSSK) with oversight responsibility for the financial sector (Bank Indonesia, the Deposit Insurance Agency and the Ministry of Finance in addition to the FSA). During PERISAI the creation and integration of bank and non-bank supervision at the FSA went well (results indicator 1). Non-bank supervision moved to the FSA in 2013 and Bank Supervision in 2014. There is more to be done to reduce silos and improve supervision including across bank and non-bank entities within conglomerates but progress continues to be good, including through an FSAP now being undertaken. The Financial Stability Forum was established, procedures and responsibilities laid out, expertise on resolving bank crises improved and numerous crisis simulations held, including most recently simulations created and directed by the Indonesian authorities themselves. The financial sector performed well during PERISAI (results indicators 2-4, and additional evidence). Indicators for the Banking sector including Non-Performing Loans and Capital Adequacy remained strong. There were no major Bank failures. The new government agencies ran simulations of bank failures (systemic and not) multiple times. In fact, over the period the financial system deepened marginally, with for example M2/GDP, improving from 38 percent in 2011 to over 40 percent in 2015, although this remains low for a country at Indonesia’s level of development. Policy Area 2: Sustaining Critical Public Expenditures Rating: Substantial

18

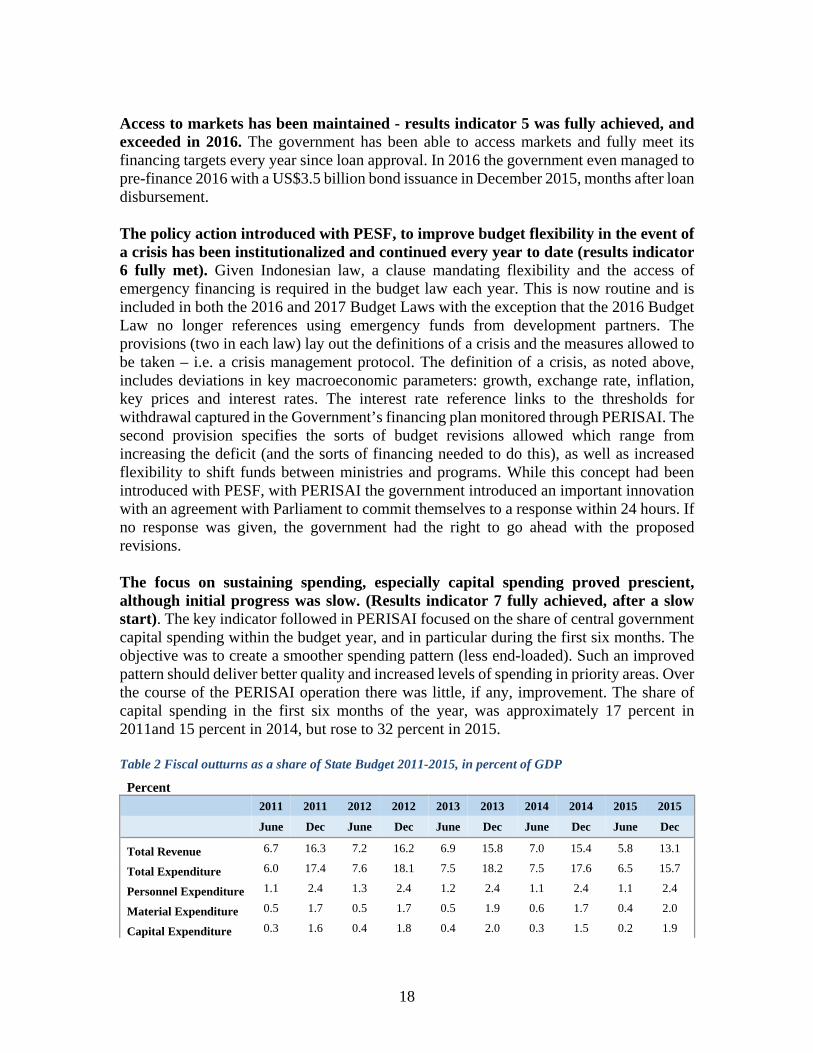

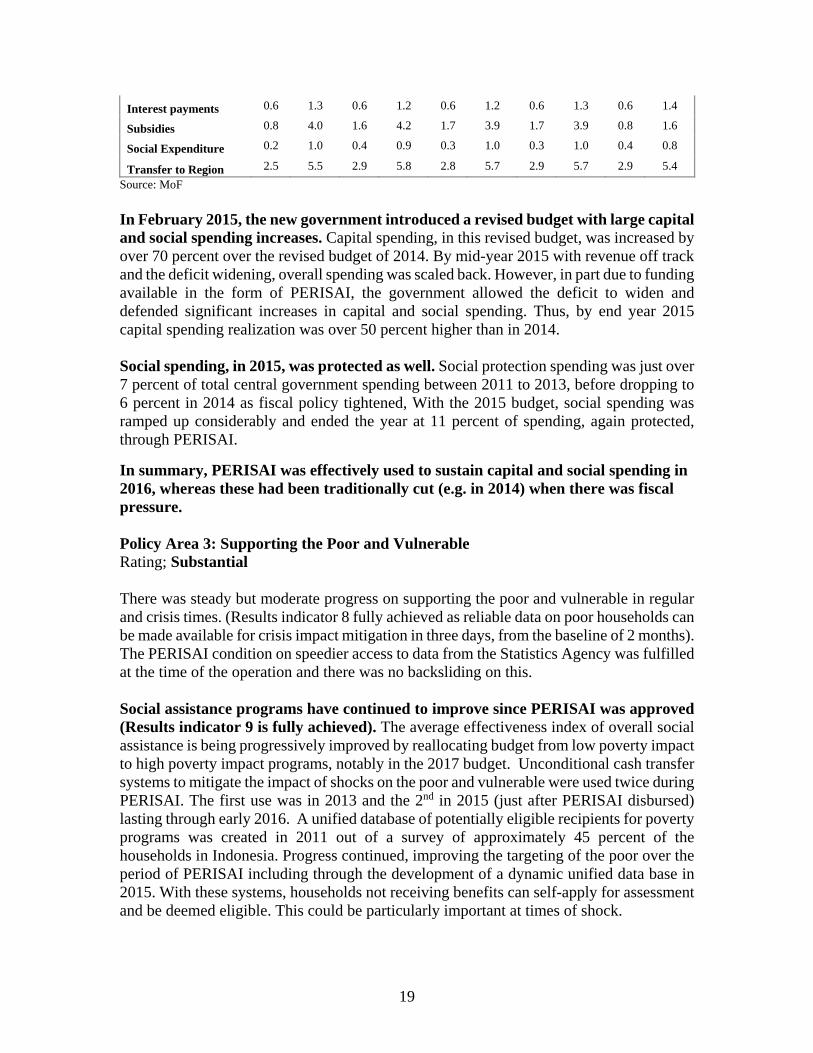

Access to markets has been maintained - results indicator 5 was fully achieved, and exceeded in 2016. The government has been able to access markets and fully meet its financing targets every year since loan approval. In 2016 the government even managed to pre-finance 2016 with a US$3.5 billion bond issuance in December 2015, months after loan disbursement. The policy action introduced with PESF, to improve budget flexibility in the event of a crisis has been institutionalized and continued every year to date (results indicator 6 fully met). Given Indonesian law, a clause mandating flexibility and the access of emergency financing is required in the budget law each year. This is now routine and is included in both the 2016 and 2017 Budget Laws with the exception that the 2016 Budget Law no longer references using emergency funds from development partners. The provisions (two in each law) lay out the definitions of a crisis and the measures allowed to be taken – i.e. a crisis management protocol. The definition of a crisis, as noted above, includes deviations in key macroeconomic parameters: growth, exchange rate, inflation, key prices and interest rates. The interest rate reference links to the thresholds for withdrawal captured in the Government’s financing plan monitored through PERISAI. The second provision specifies the sorts of budget revisions allowed which range from increasing the deficit (and the sorts of financing needed to do this), as well as increased flexibility to shift funds between ministries and programs. While this concept had been introduced with PESF, with PERISAI the government introduced an important innovation with an agreement with Parliament to commit themselves to a response within 24 hours. If no response was given, the government had the right to go ahead with the proposed revisions. The focus on sustaining spending, especially capital spending proved prescient, although initial progress was slow. (Results indicator 7 fully achieved, after a slow start). The key indicator followed in PERISAI focused on the share of central government capital spending within the budget year, and in particular during the first six months. The objective was to create a smoother spending pattern (less end-loaded). Such an improved pattern should deliver better quality and increased levels of spending in priority areas. Over the course of the PERISAI operation there was little, if any, improvement. The share of capital spending in the first six months of the year, was approximately 17 percent in 2011and 15 percent in 2014, but rose to 32 percent in 2015. Table 2 Fiscal outturns as a share of State Budget 2011-2015, in percent of GDP

Percent

2011 2011 2012 2012 2013 2013 2014 2014 2015 2015

June Dec June Dec June Dec June Dec June Dec

Total Revenue 6.7 16.3 7.2 16.2 6.9 15.8 7.0 15.4 5.8 13.1

Total Expenditure 6.0 17.4 7.6 18.1 7.5 18.2 7.5 17.6 6.5 15.7

Personnel Expenditure 1.1 2.4 1.3 2.4 1.2 2.4 1.1 2.4 1.1 2.4

Material Expenditure 0.5 1.7 0.5 1.7 0.5 1.9 0.6 1.7 0.4 2.0

Capital Expenditure 0.3 1.6 0.4 1.8 0.4 2.0 0.3 1.5 0.2 1.9

19

Interest payments 0.6 1.3 0.6 1.2 0.6 1.2 0.6 1.3 0.6 1.4

Subsidies 0.8 4.0 1.6 4.2 1.7 3.9 1.7 3.9 0.8 1.6

Social Expenditure 0.2 1.0 0.4 0.9 0.3 1.0 0.3 1.0 0.4 0.8

Transfer to Region 2.5 5.5 2.9 5.8 2.8 5.7 2.9 5.7 2.9 5.4

Source: MoF

In February 2015, the new government introduced a revised budget with large capital and social spending increases. Capital spending, in this revised budget, was increased by over 70 percent over the revised budget of 2014. By mid-year 2015 with revenue off track and the deficit widening, overall spending was scaled back. However, in part due to funding available in the form of PERISAI, the government allowed the deficit to widen and defended significant increases in capital and social spending. Thus, by end year 2015 capital spending realization was over 50 percent higher than in 2014. Social spending, in 2015, was protected as well. Social protection spending was just over 7 percent of total central government spending between 2011 to 2013, before dropping to 6 percent in 2014 as fiscal policy tightened, With the 2015 budget, social spending was ramped up considerably and ended the year at 11 percent of spending, again protected, through PERISAI.

In summary, PERISAI was effectively used to sustain capital and social spending in 2016, whereas these had been traditionally cut (e.g. in 2014) when there was fiscal pressure. Policy Area 3: Supporting the Poor and Vulnerable Rating; Substantial There was steady but moderate progress on supporting the poor and vulnerable in regular and crisis times. (Results indicator 8 fully achieved as reliable data on poor households can be made available for crisis impact mitigation in three days, from the baseline of 2 months). The PERISAI condition on speedier access to data from the Statistics Agency was fulfilled at the time of the operation and there was no backsliding on this. Social assistance programs have continued to improve since PERISAI was approved (Results indicator 9 is fully achieved). The average effectiveness index of overall social assistance is being progressively improved by reallocating budget from low poverty impact to high poverty impact programs, notably in the 2017 budget. Unconditional cash transfer systems to mitigate the impact of shocks on the poor and vulnerable were used twice during PERISAI. The first use was in 2013 and the 2nd in 2015 (just after PERISAI disbursed) lasting through early 2016. A unified database of potentially eligible recipients for poverty programs was created in 2011 out of a survey of approximately 45 percent of the households in Indonesia. Progress continued, improving the targeting of the poor over the period of PERISAI including through the development of a dynamic unified data base in 2015. With these systems, households not receiving benefits can self-apply for assessment and be deemed eligible. This could be particularly important at times of shock.

20

Information dissemination and the handling of complaints and grievances for excluded households, has improved. Prior to the cash transfer program in 2013, there had been very limited information campaigns. In 2013, TNP2K improved information dissemination and monitoring and evaluation, not only for the cash transfer program but also other programs using the unified data base. Brochures on programs including the rice transfer program and scholarships (how to claim, benefits for instance) were distributed to local governments and households via the post office. Information was also provided online and through call centers. The implementation was accompanied by complaint handling mechanisms via direct complaint report to special post at the village and district levels as well as online (website, call, text message). Progress on improving the targeting of poverty programs is good, and would be helpful in a crisis. Work is also ongoing to improve the government’s capability to mitigate a shock to those above the poverty line for whom Indonesia has no formal safety net or automatic stabilizers. The Proxy Means Test used to determine eligibility for poverty programs is currently good for determining long-term poverty and vulnerability but not for sudden decreases in individual welfare.

21

3.4 Justification of Overall Outcome Rating Rating: Satisfactory

Evidence demonstrates that all results indicators were achieved, and in certain cases exceeded by the close of the program, justifying a strong overall outcome rating. However, some indicators started slow (e.g. indicator 7 on accelerating public capital spending in the first half of the year), and hence bring this rating to Satisfactory.