ENGM 745 Forecasting for Business & Technology

Paula Jensen

South Dakota School of Mines and Technology, Rapid City

3rd Session 2/01/12: Chapter 3 Moving Averages and Exponential Smoothing

Agenda & New Assignment

ch3(1,5,8,11) Business Forecasting 6th Edition

J. Holton Wilson & Barry KeatingMcGraw-Hill

Moving Averages & Exponential Smoothing All basic methods based on

smoothing 1. Moving averages 2. Simple exponential smoothing 3. Holt's exponential smoothing 4. Winters' exponential smoothing 5. Adaptive-response-rate single

exponential smoothing

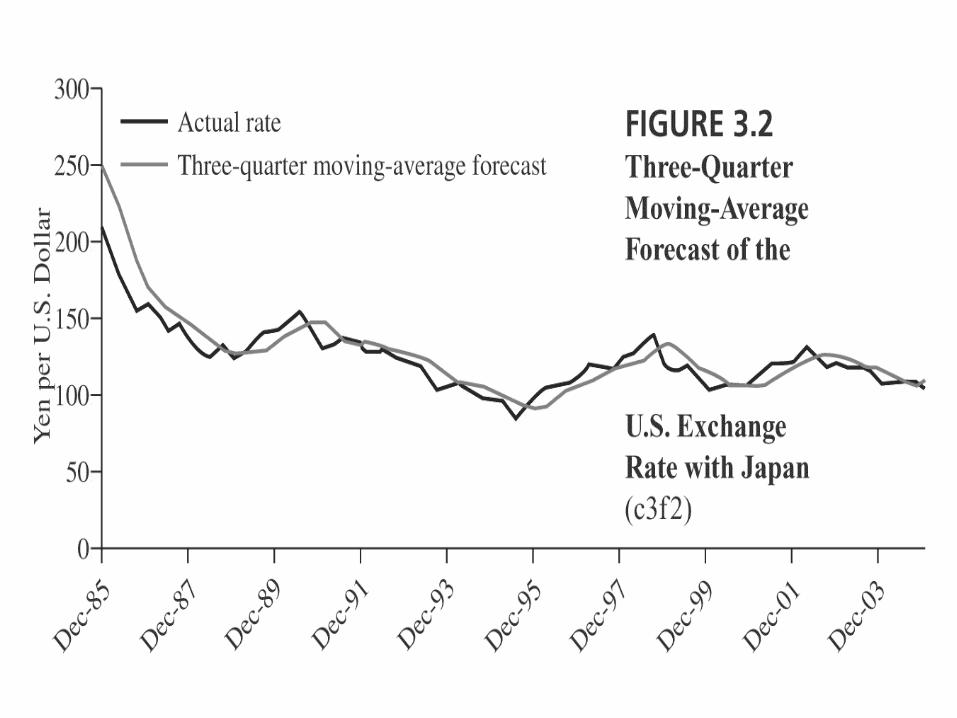

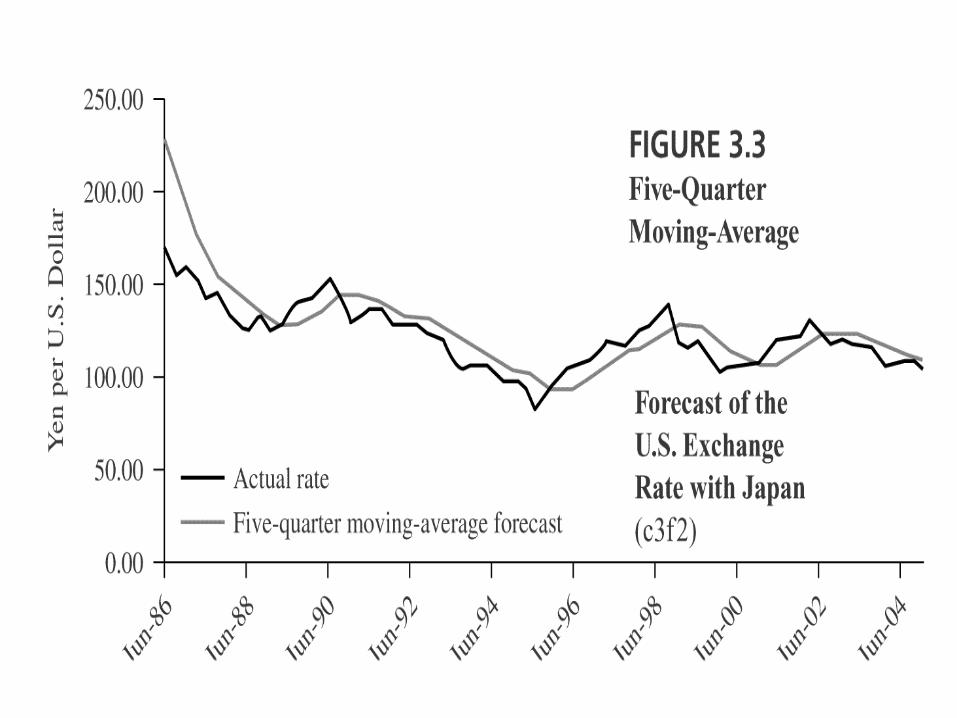

Moving Averages Ex. “Three Quarter Moving Average”

(1999Q1+1999Q2+1999Q3)/3 =Forecast for 1999Q4

Slutsky-Yule effect: Any moving average could appear to be acycle, because it is a serially correlated set of random numbers.

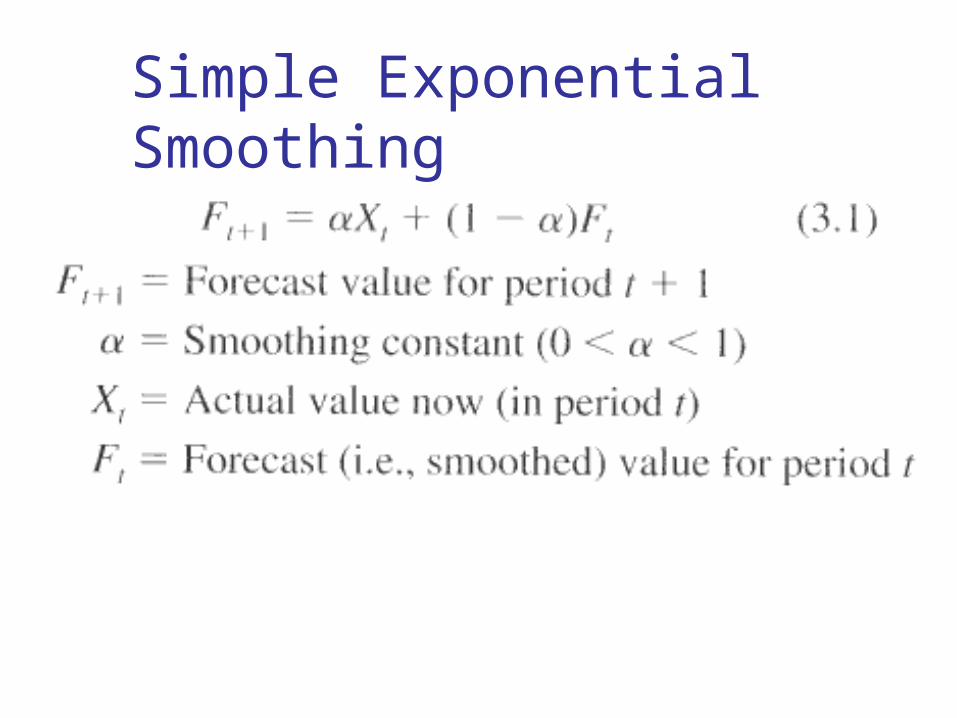

Simple Exponential Smoothing

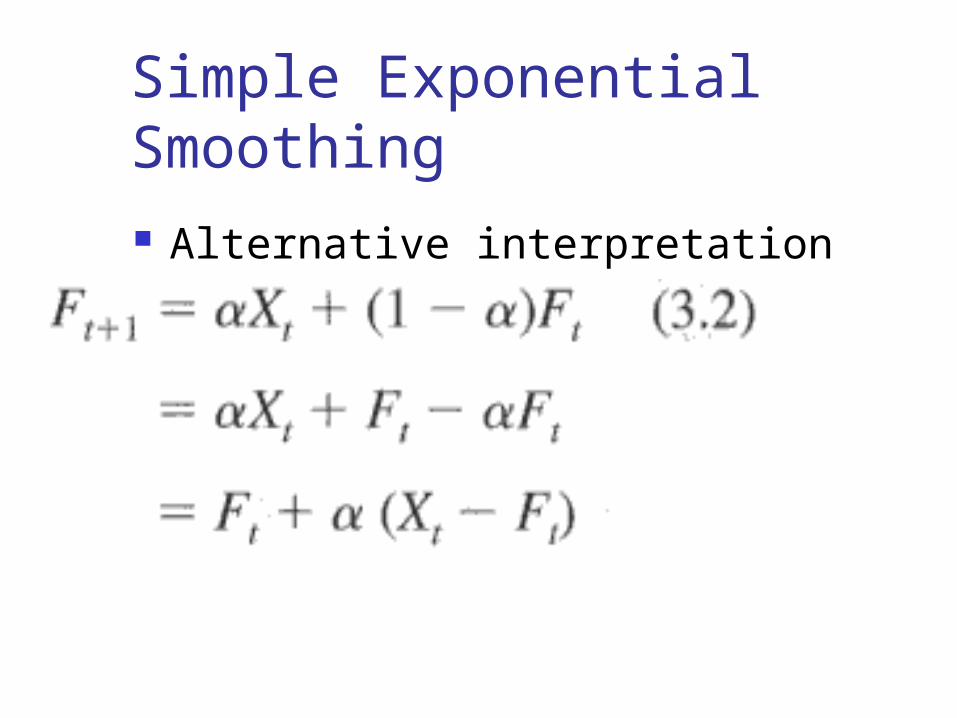

Simple Exponential Smoothing Alternative interpretation

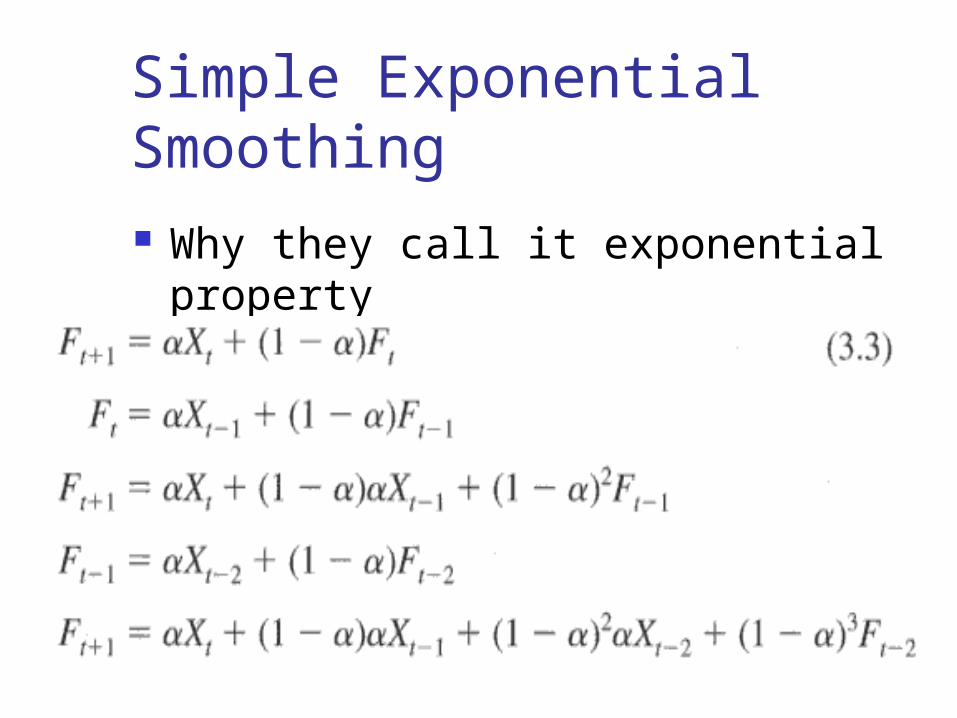

Simple Exponential Smoothing Why they call it exponential

property

Simple Exponential Smoothing Advantages

Simpler than other forms Requires limited data

Disdvantages Lags behind actual data No trend or seasonality

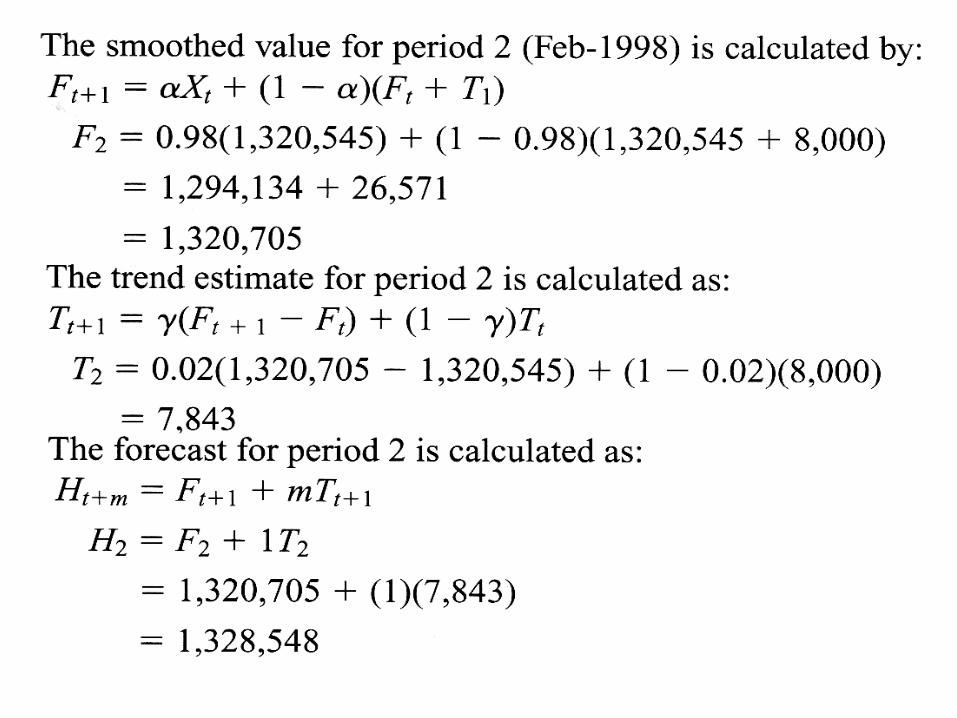

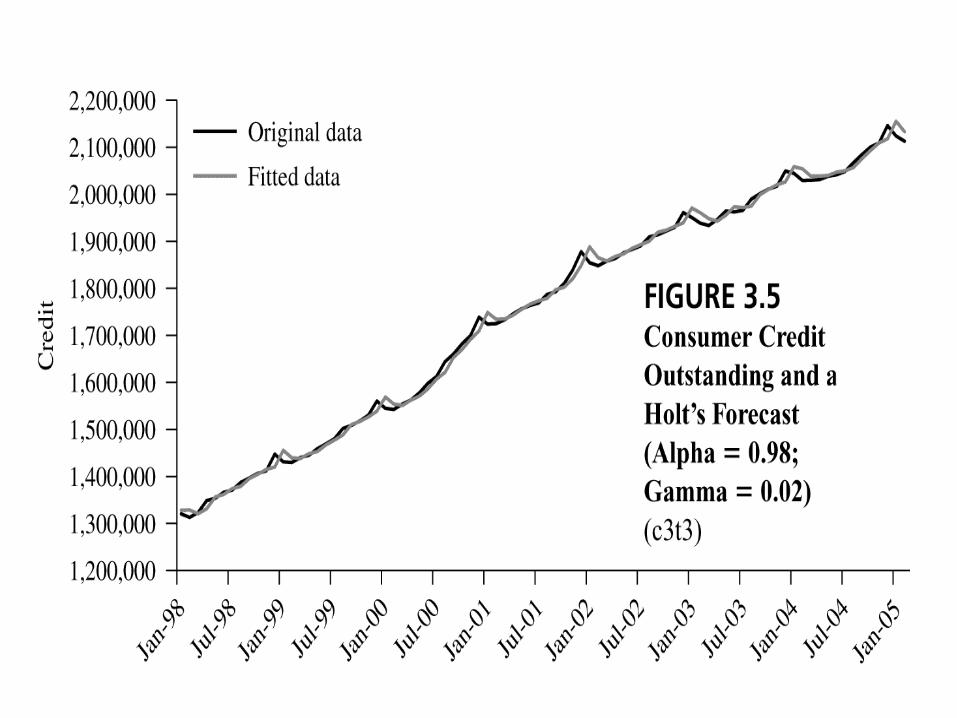

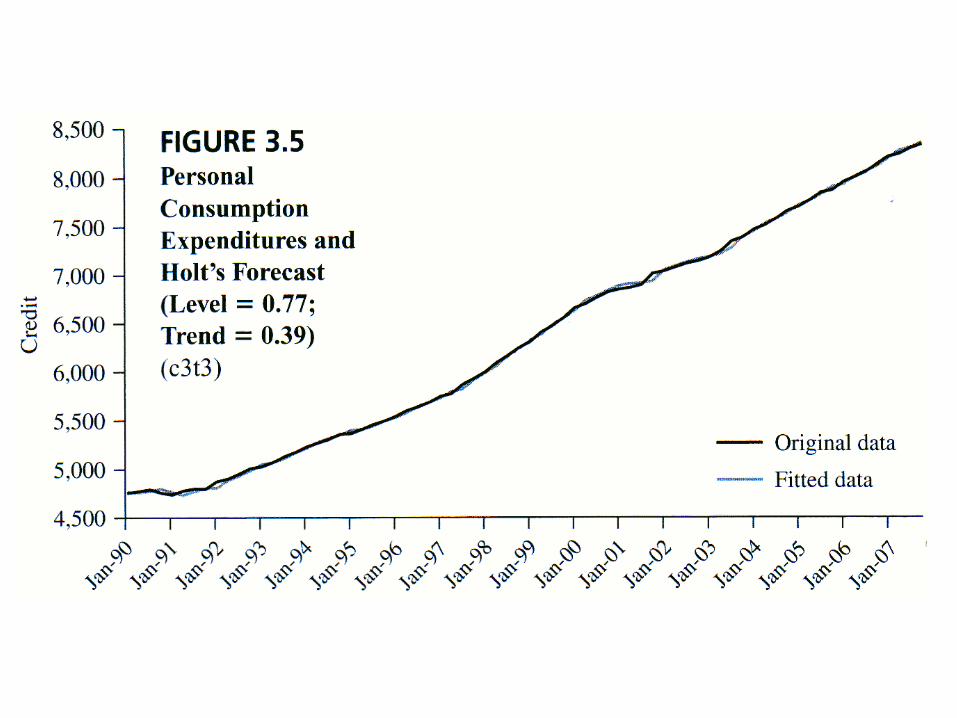

Holt's Exponential Smoothing(Double Holt in ForecastXTM)

ForecastXTM Conventions forSmoothing Constants

Alpha () =the simple smoothing constant

Gamma () =the trend smoothing constant

Beta () =the seasonality smoothing constant

Holt's Exponential Smoothing ForecastX will pick the smoothing

constants to minimize RMSE Some trend, but no seasonality Call it linear trend smoothing

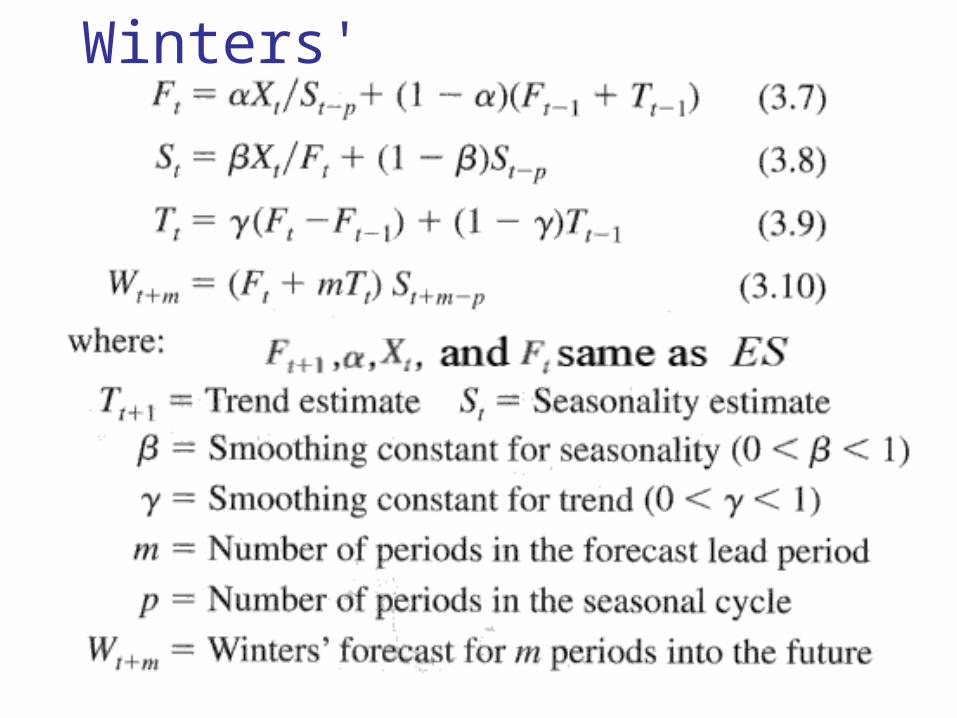

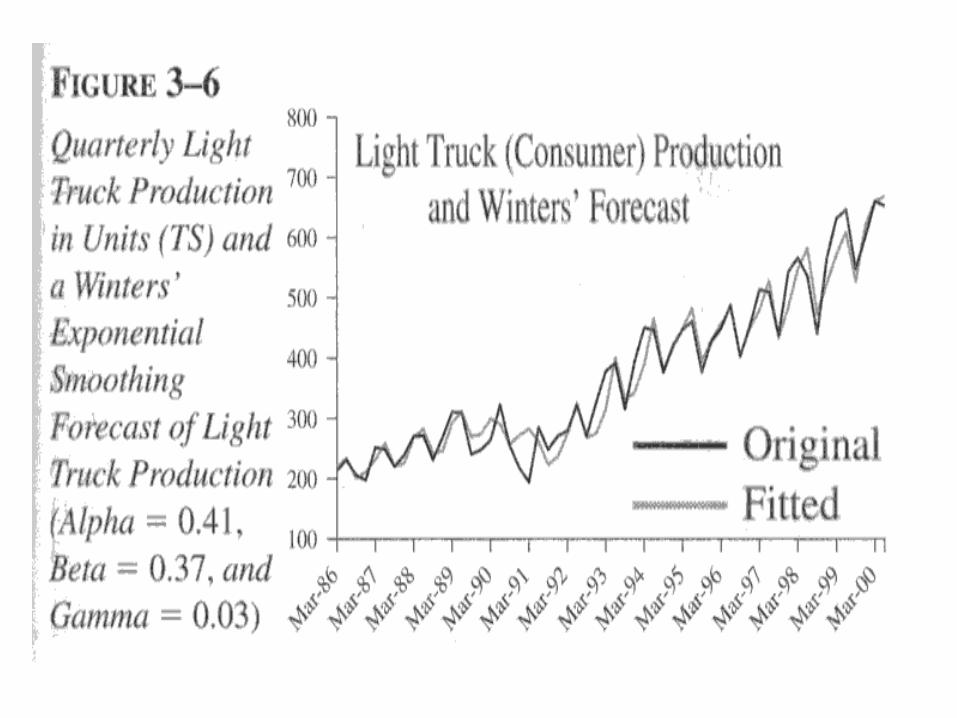

Winters'

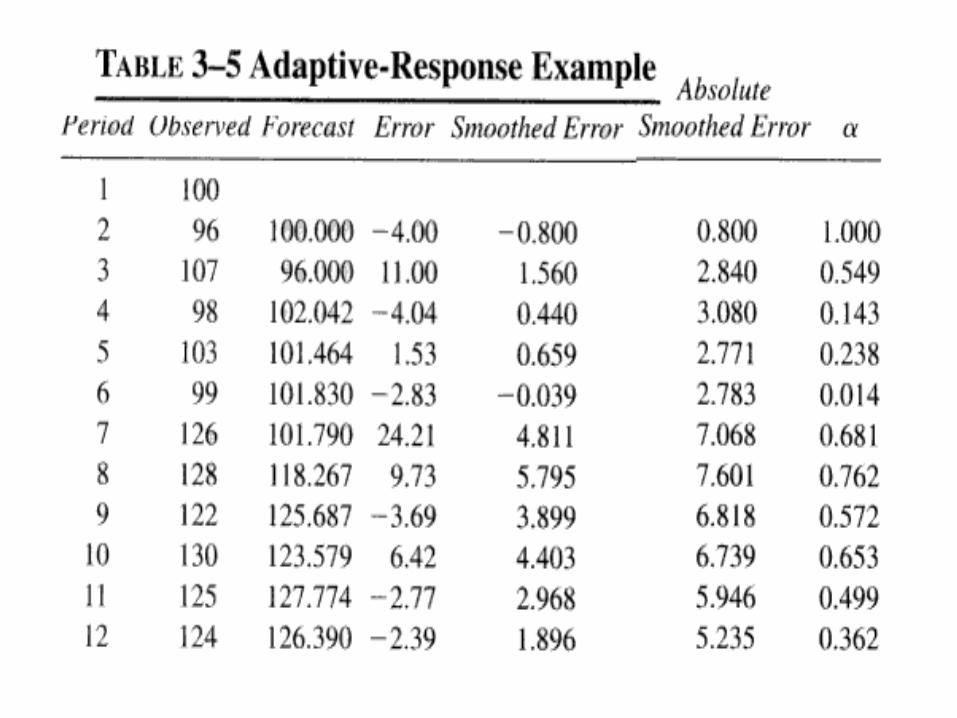

Adaptive-Response-Rate Single Exponential Smoothing

Adaptive-Response-Rate Single Exponential Smoothing Adaptive is a clue to how it works No direct way of handling

seasonality Does not handle trends ForecastX has different algorithm

Using Single, Holt's, or ADRES Smoothing to Forecast a Seasonal Data Series

1. Calculate seasonal indices for the series. Done in HOLT WINTERS ForecastX™.

2. Deseasonalize the original data by dividing each value by its corresponding seasonal index.

Using Single, Holt's, or ADRES Smoothing to Forecast a Seasonal Data Series

3. Apply a forecasting method (such as ES, Holt's, or ADRES) to the deseasonalized series to produce an intermediate forecast of the deseasonalized data.

4. Reseasonalize the series by multiplying each deseasonalized forecast by its corresponding seasonal index.

Conclusion Cover Single Exponential, Holt’s,

Winters, ADRES I will be sending an e-mail with a

link to get onto the Harvard link for a case study.

Take the quiz online to brush up on Statistic skills.