drake drake university fin 284 bond mathematics finance 298 analysis of fixed income securities

Post on 20-Dec-2015

221 views

TRANSCRIPT

DrakeDRAKE UNIVERSITY

Fin 284

Bond Mathematics

Finance 298Analysis of Fixed Income

Securities

DrakeDrake University

Fin 284A General Valuation Model

The basic components of valuing any asset are:

An estimate of the future cash flow stream from owning the assetThe required rate of return for each period based upon the riskiness of the asset

The value is then found by discounting each cash flow by its respective discount rate and then summing the PV’s (Basically the PV of an Uneven Cash Flow Stream)

DrakeDrake University

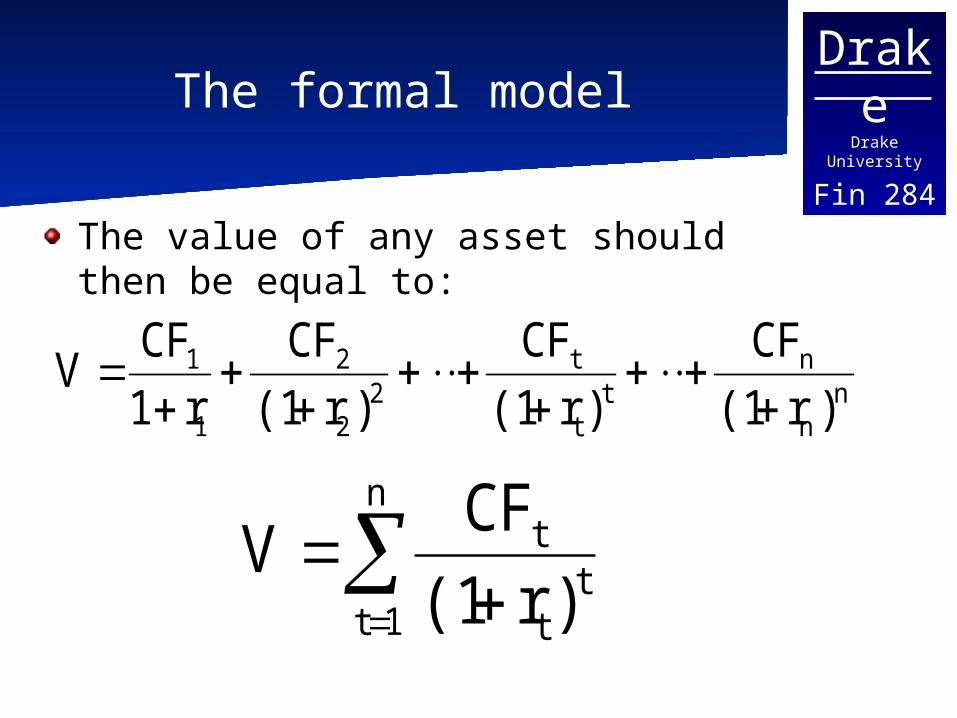

Fin 284The formal model

The value of any asset should then be equal to:

nn

nt

t

t2

2

2

1

1

)r(1

CF

)r(1

CF

)r(1

CF

r1

CFV

n

1tt

t

t

)r(1

CFV

DrakeDrake University

Fin 284 A Basic Bond

A bond is basically a debt contract issued by a corporation or government entity.The buyer is lending the issuer an amount of money (the par value). The issue agrees to pay interest at specified intervals (coupon payments) to the buyer, and return the par value at the end of the contract (the maturity date).

DrakeDrake University

Fin 284

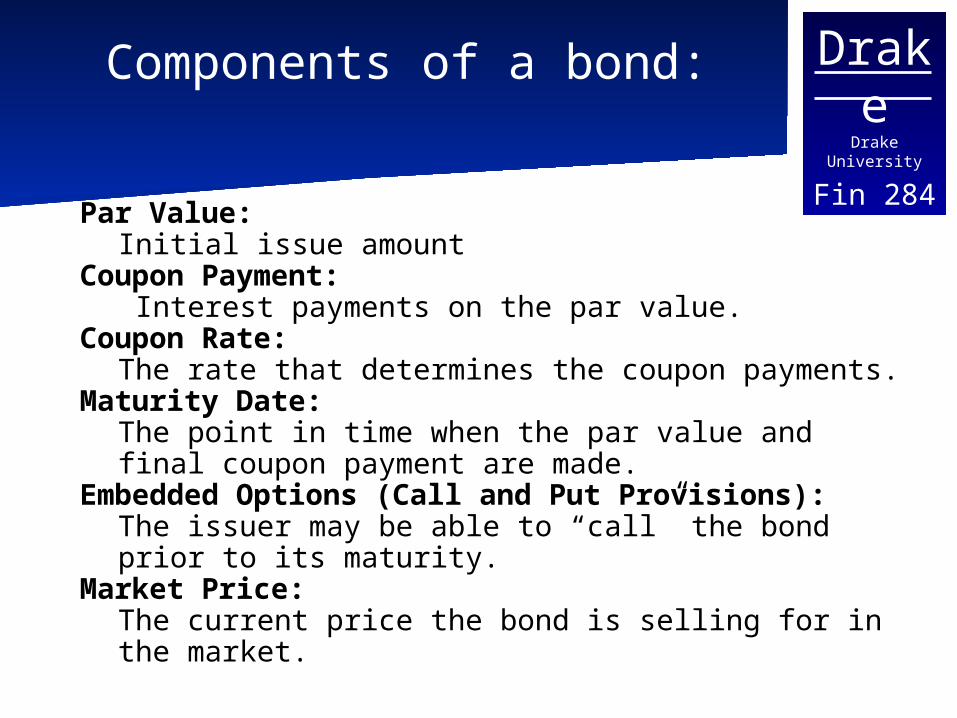

Components of a bond:

Par Value: Initial issue amount

Coupon Payment: Interest payments on the par value.

Coupon Rate: The rate that determines the coupon payments.

Maturity Date: The point in time when the par value and final

coupon payment are made. Embedded Options (Call and Put Provisions):

The issuer may be able to “call” the bond prior to its maturity.

Market Price: The current price the bond is selling for in the

market.

DrakeDrake University

Fin 284

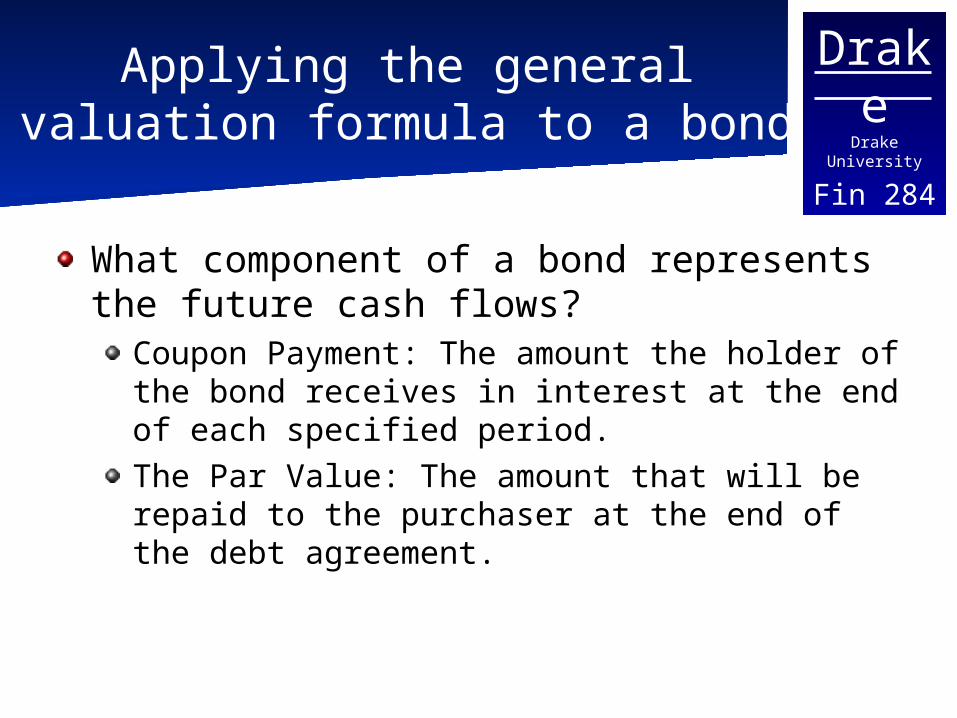

Applying the general valuation formula to a bond

What component of a bond represents the future cash flows?

Coupon Payment: The amount the holder of the bond receives in interest at the end of each specified period.The Par Value: The amount that will be repaid to the purchaser at the end of the debt agreement.

DrakeDrake University

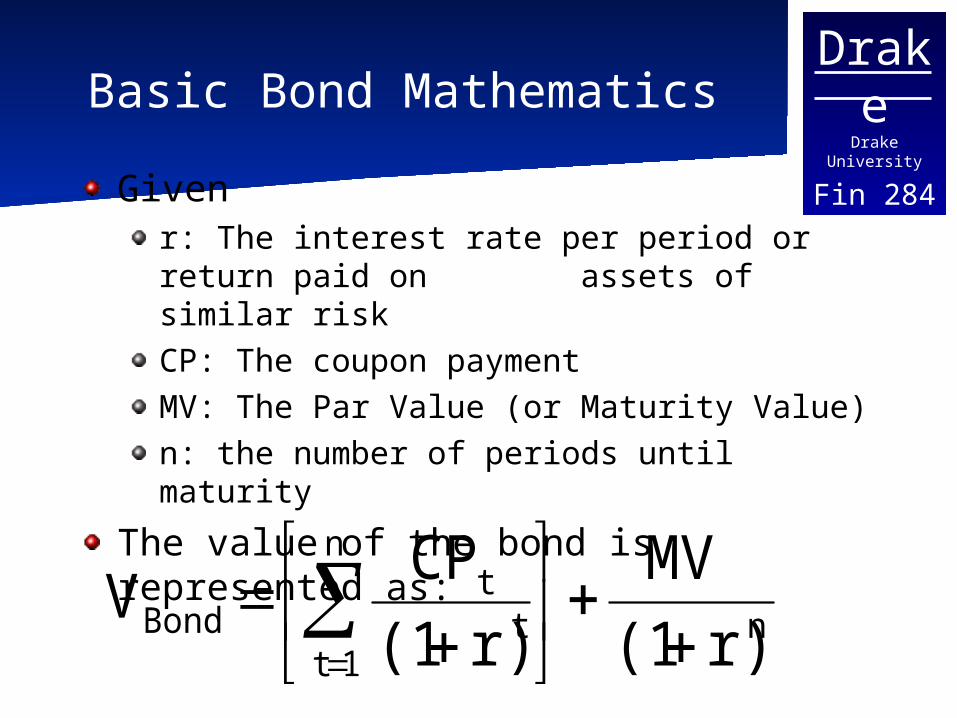

Fin 284Basic Bond Mathematics

Givenr: The interest rate per period or return paid on assets of similar riskCP: The coupon paymentMV: The Par Value (or Maturity Value)n: the number of periods until maturity

The value of the bond is represented as:

n

n

1tt

tBond r)(1

MV

r)(1

CPV

DrakeDrake University

Fin 284

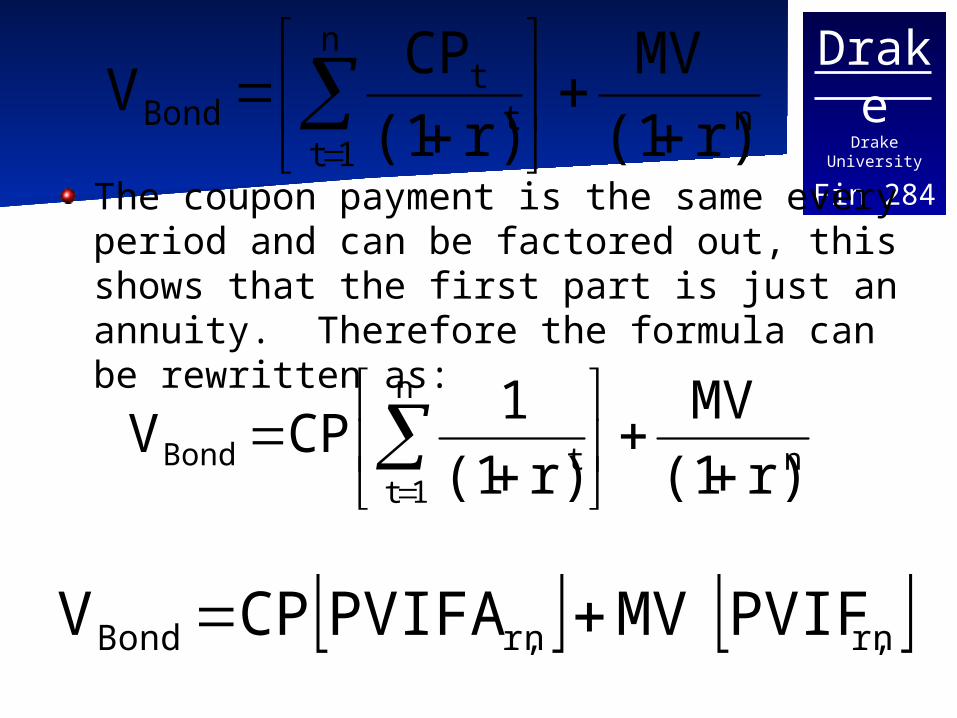

The coupon payment is the same every period and can be factored out, this shows that the first part is just an annuity. Therefore the formula can be rewritten as:

n

n

1tt

tBond r)(1

MV

r)(1

CPV

n

n

1ttBond r)(1

MV

r)(1

1CPV

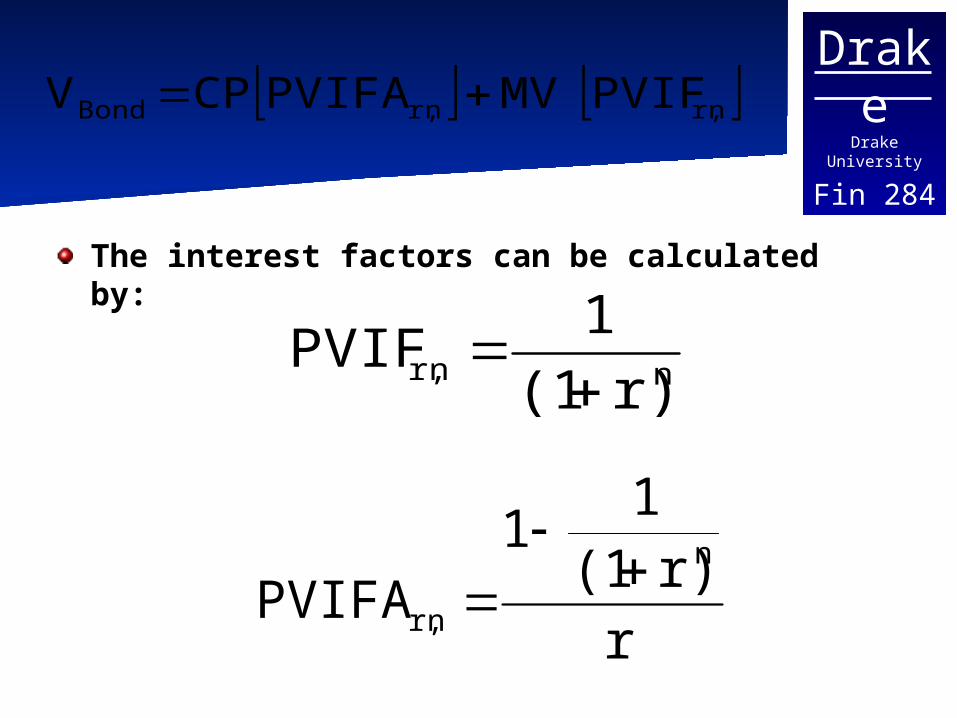

nr,nr,Bond PVIFMVPVIFACPV

DrakeDrake University

Fin 284 nr,nr,Bond PVIFMVPVIFACPV

The interest factors can be calculated by:

nnr, r)(1

1PVIF

rr)(1

11

PVIFAn

nr,

DrakeDrake University

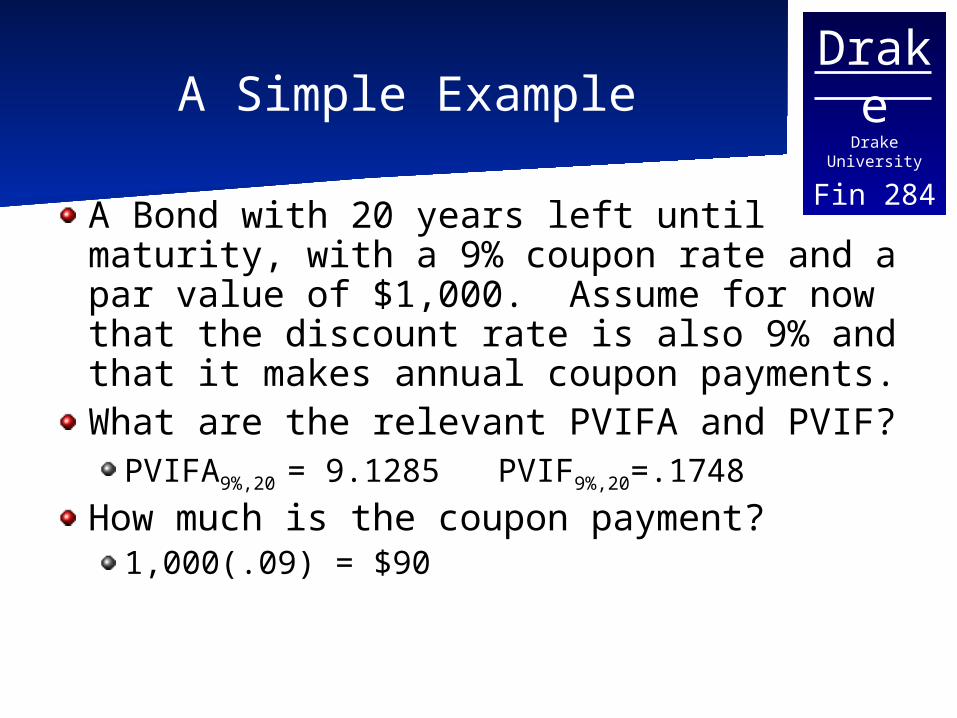

Fin 284A Simple Example

A Bond with 20 years left until maturity, with a 9% coupon rate and a par value of $1,000. Assume for now that the discount rate is also 9% and that it makes annual coupon payments.What are the relevant PVIFA and PVIF?

PVIFA9%,20 = 9.1285 PVIF9%,20=.1748

How much is the coupon payment?1,000(.09) = $90

DrakeDrake University

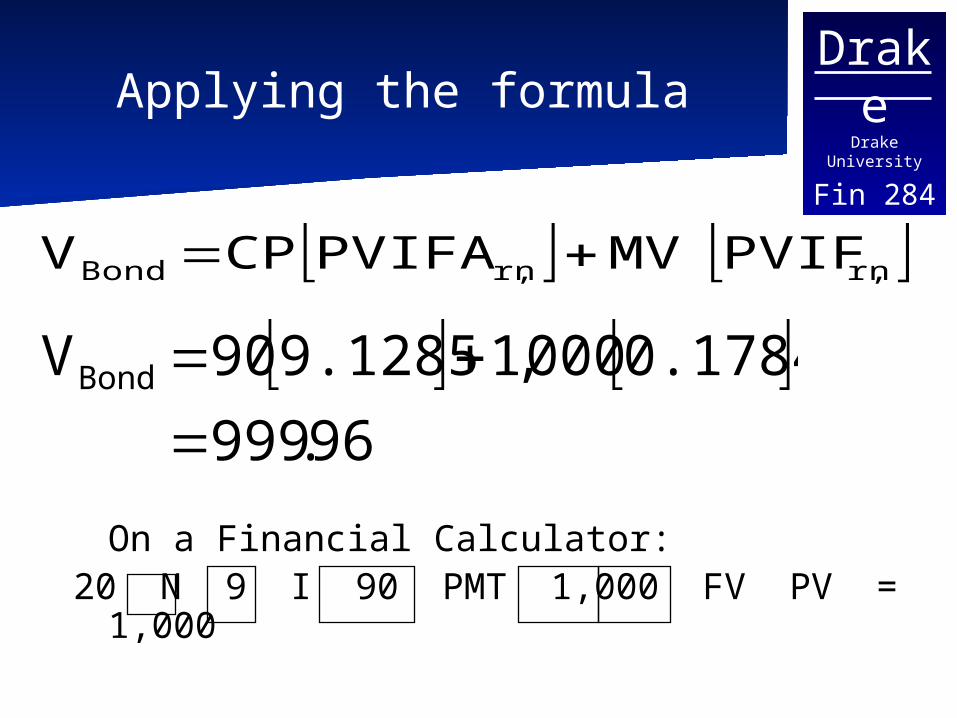

Fin 284Applying the formula

On a Financial Calculator:20 N 9 I 90 PMT 1,000 FV PV = 1,000

nr,nr,Bond PVIFMVPVIFACPV

96.999

0.1784000,19.128590VBond

DrakeDrake University

Fin 284The Discount Rate

So far we assumed that the interest rate is the same as the coupon rate. When this is true the value of the bond equals the par value.Are the two usually the same?

No, the discount rate should represent the current required return on assets of similar risk. This changes as the level of interest rates in the economy changes

DrakeDrake University

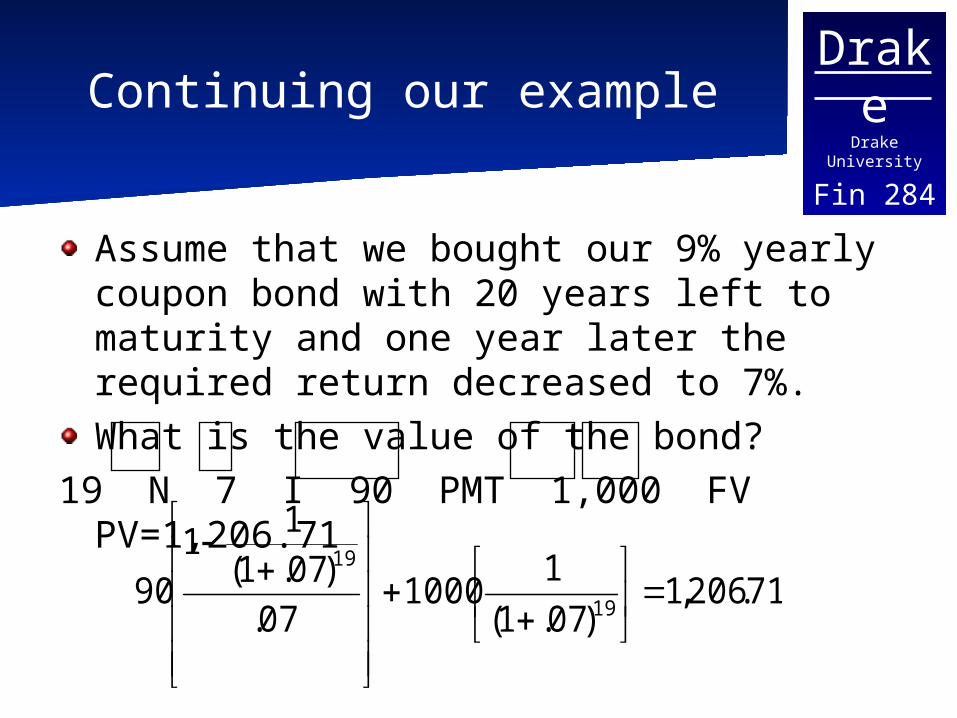

Fin 284Continuing our example

Assume that we bought our 9% yearly coupon bond with 20 years left to maturity and one year later the required return decreased to 7%.What is the value of the bond?

19 N 7 I 90 PMT 1,000 FV PV=1,206.71

71.206,1)07.1(

11000

07.)07.1(

11

9019

19

DrakeDrake University

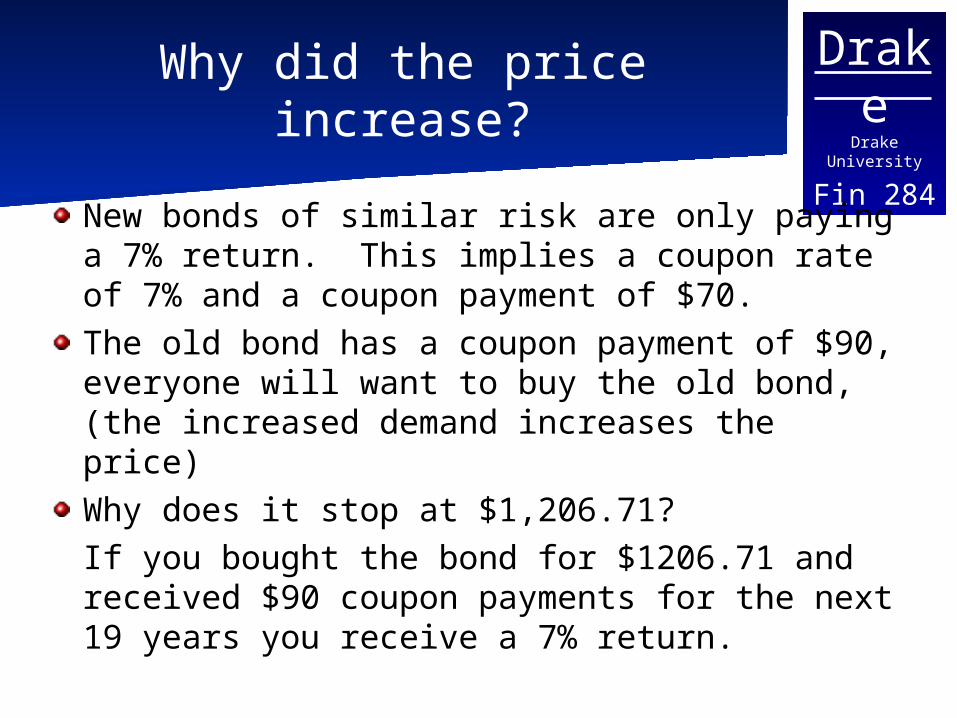

Fin 284Why did the price increase?

New bonds of similar risk are only paying a 7% return. This implies a coupon rate of 7% and a coupon payment of $70.The old bond has a coupon payment of $90, everyone will want to buy the old bond, (the increased demand increases the price)Why does it stop at $1,206.71?

If you bought the bond for $1206.71 and received $90 coupon payments for the next 19 years you receive a 7% return.

DrakeDrake University

Fin 284

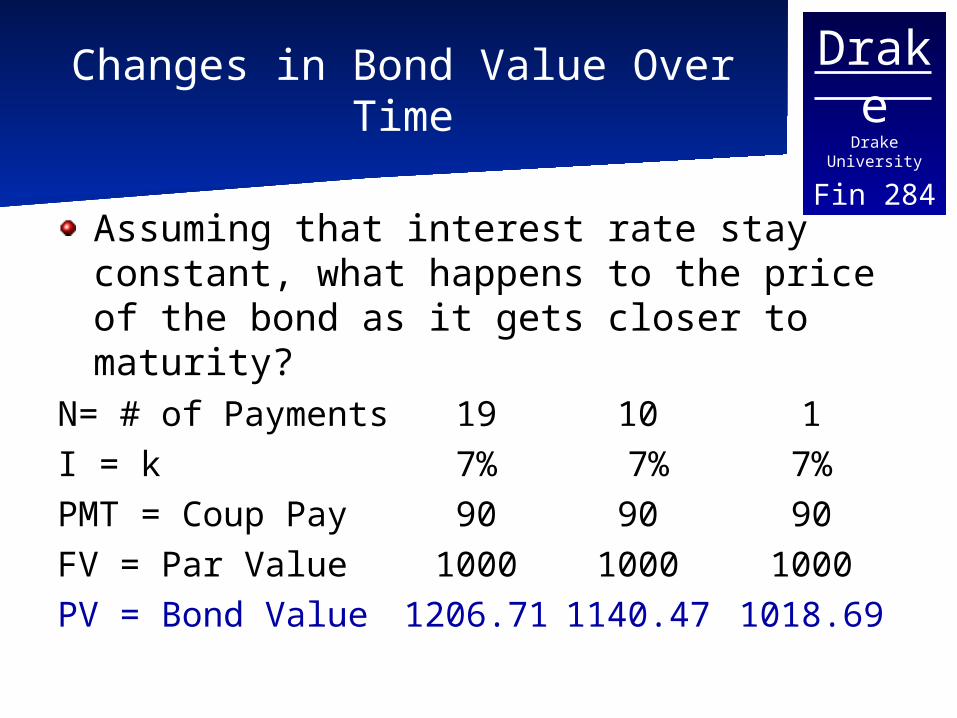

Changes in Bond Value Over Time

Assuming that interest rate stay constant, what happens to the price of the bond as it gets closer to maturity?

N= # of Payments 19 10 1I = k 7% 7% 7%PMT = Coup Pay 90 90 90FV = Par Value 1000 1000 1000PV = Bond Value 1206.71 1140.47 1018.69

DrakeDrake University

Fin 284Calculating Return

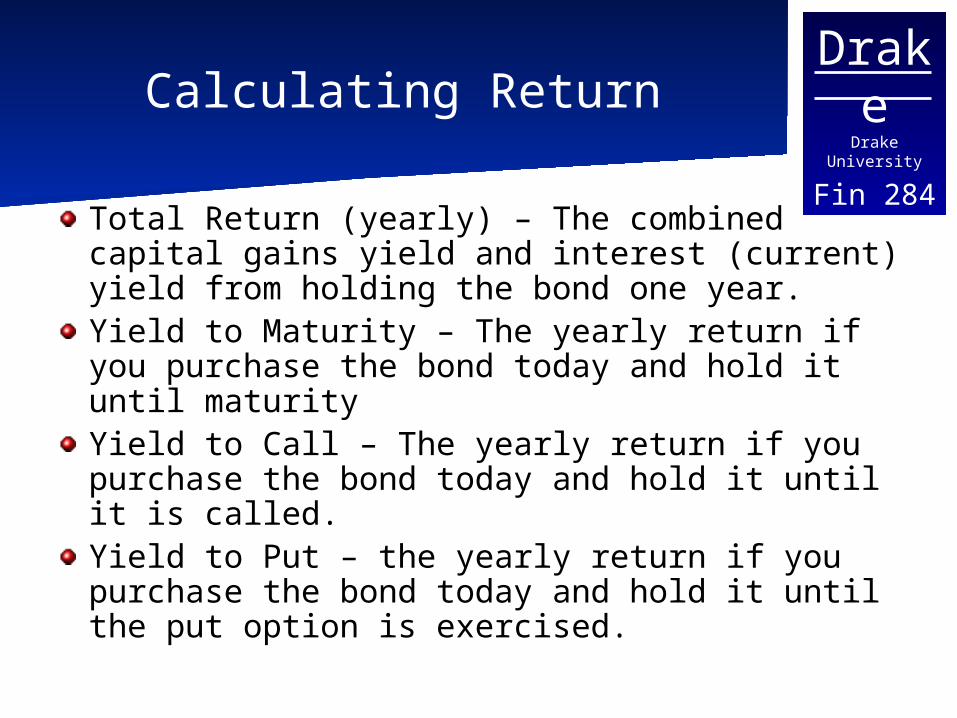

Total Return (yearly) – The combined capital gains yield and interest (current) yield from holding the bond one year.Yield to Maturity – The yearly return if you purchase the bond today and hold it until maturityYield to Call – The yearly return if you purchase the bond today and hold it until it is called.Yield to Put – the yearly return if you purchase the bond today and hold it until the put option is exercised.

DrakeDrake University

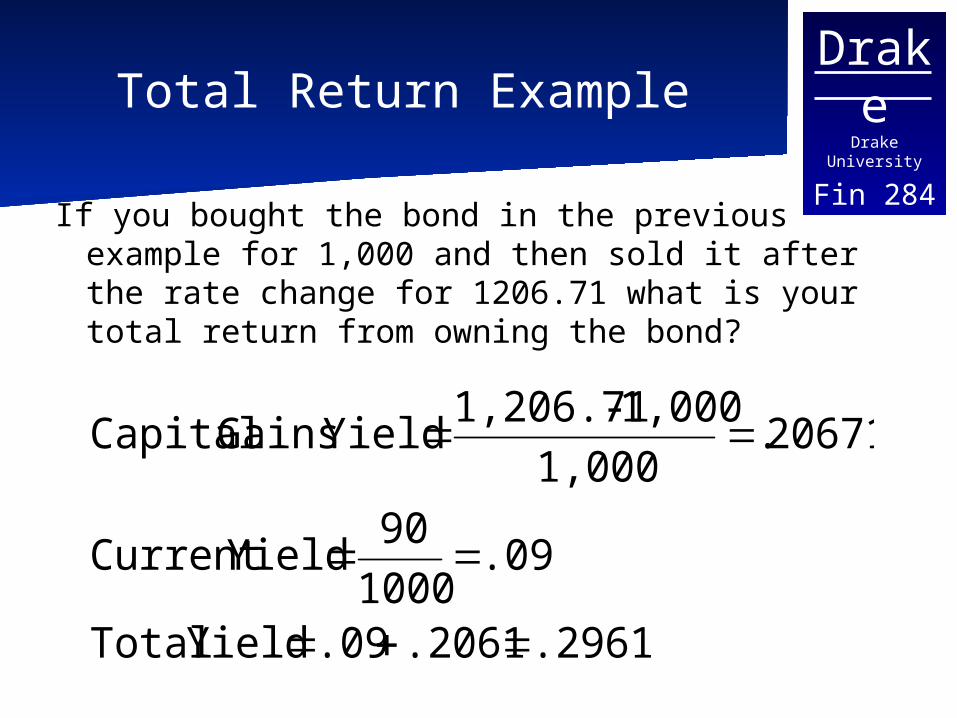

Fin 284Total Return Example

If you bought the bond in the previous example for 1,000 and then sold it after the rate change for 1206.71 what is your total return from owning the bond?

.2961 .2061 .09 Yield Total

.09 1000

90 YieldCurrent

20671.1,000

1,000 - 1,206.71 Yield Gains Capital

DrakeDrake University

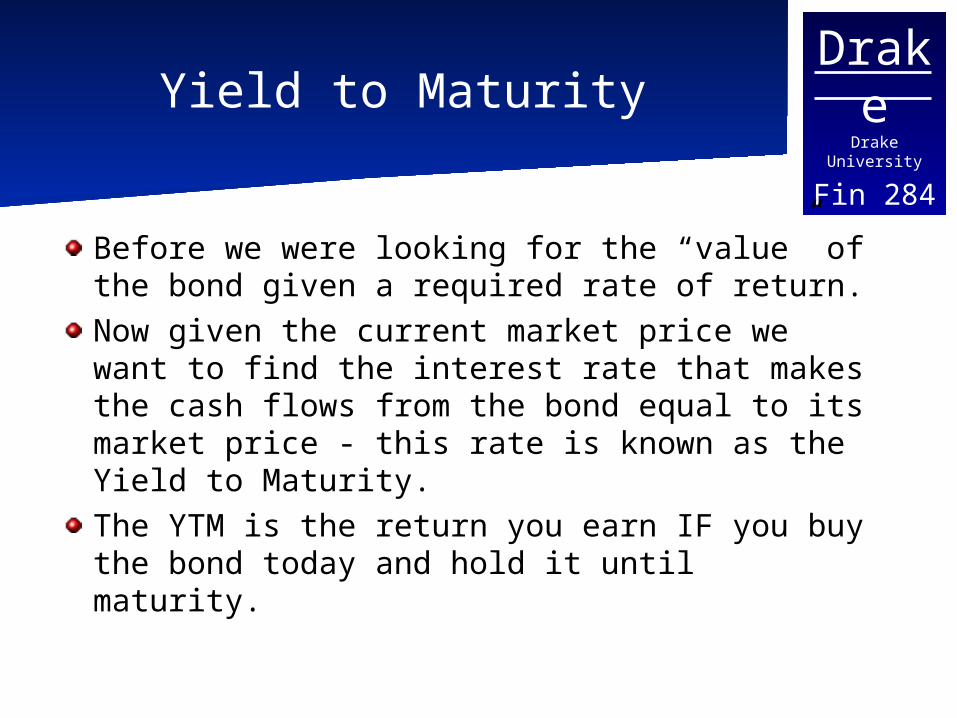

Fin 284Yield to Maturity

Before we were looking for the “value” of the bond given a required rate of return.Now given the current market price we want to find the interest rate that makes the cash flows from the bond equal to its market price - this rate is known as the Yield to Maturity.The YTM is the return you earn IF you buy the bond today and hold it until maturity.

DrakeDrake University

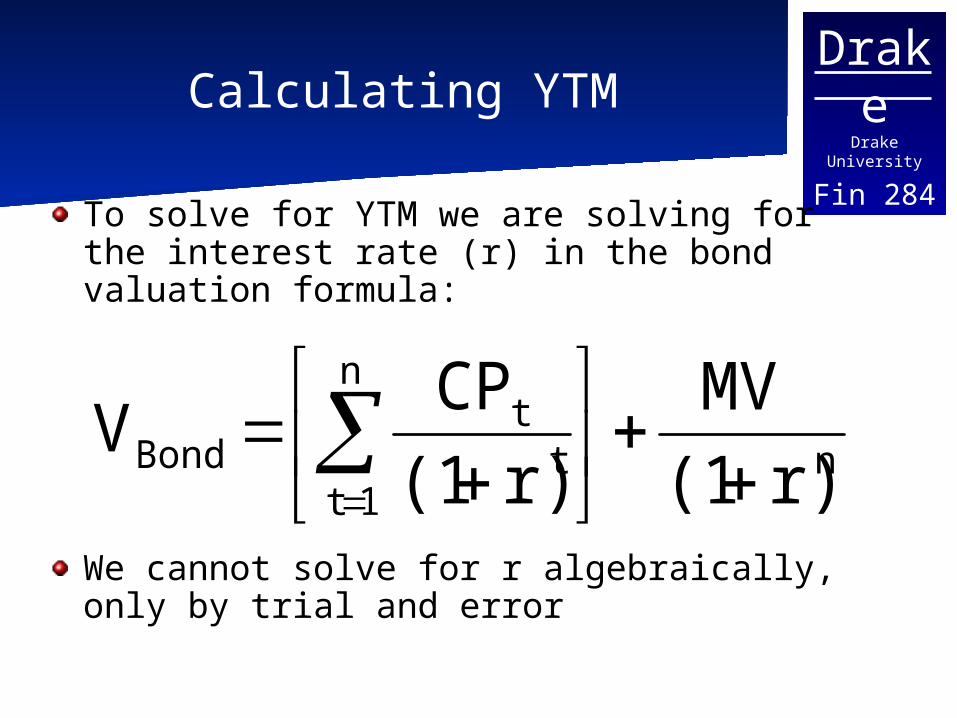

Fin 284Calculating YTM

To solve for YTM we are solving for the interest rate (r) in the bond valuation formula:

We cannot solve for r algebraically, only by trial and error

n

n

1tt

tBond r)(1

MV

r)(1

CPV

DrakeDrake University

Fin 284Calculating YTM

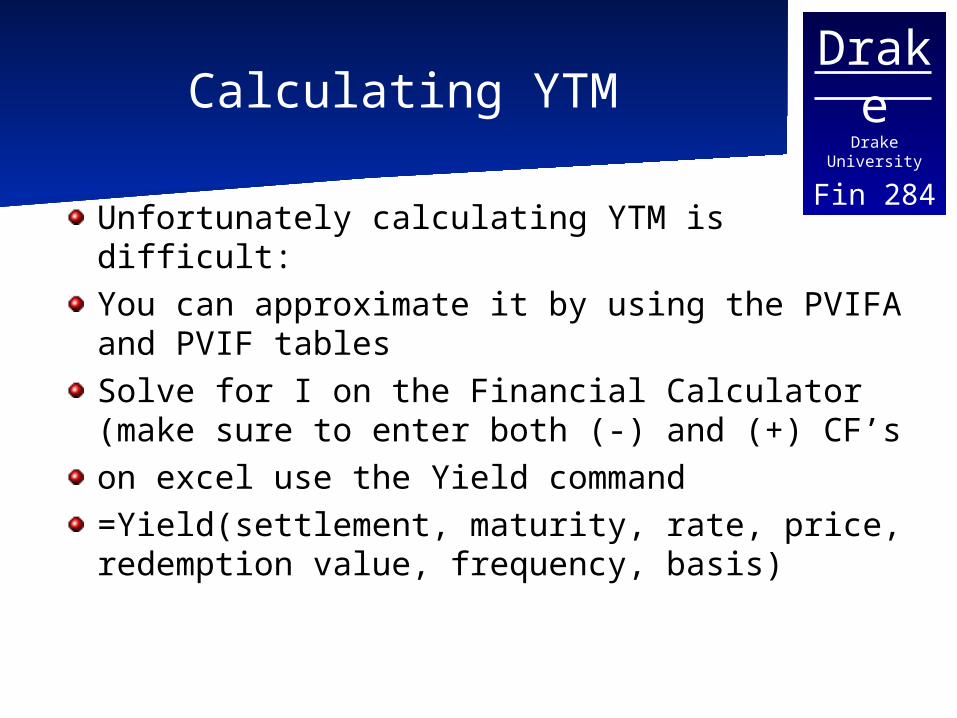

Unfortunately calculating YTM is difficult:You can approximate it by using the PVIFA and PVIF tablesSolve for I on the Financial Calculator (make sure to enter both (-) and (+) CF’son excel use the Yield command=Yield(settlement, maturity, rate, price, redemption value, frequency, basis)

DrakeDrake University

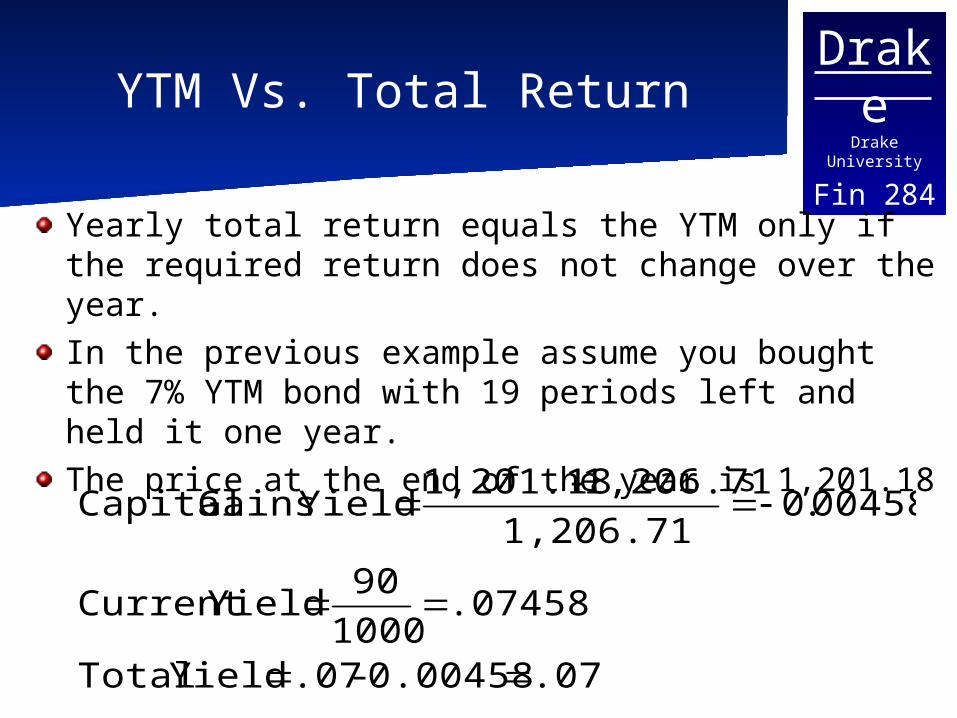

Fin 284YTM Vs. Total Return

Yearly total return equals the YTM only if the required return does not change over the year.In the previous example assume you bought the 7% YTM bond with 19 periods left and held it one year.The price at the end of the year is 1,201.18

.07 0.00458 - .07 Yield Total

.07458 1000

90 YieldCurrent

00458.01,206.71

1,206.71 - 1,201.18 Yield Gains Capital

DrakeDrake University

Fin 284YTM and Risk

The YTM will change as the level of interest rates in the economy change and as the risk associated with the firm and its projects change.The YTM is a representation of the probability of default and the current level of interest rates in the economy.

DrakeDrake University

Fin 284

Promised or Expected Return

You will earn the YTM if the bond does not default and you hold it to maturity. The expected return should encompass the chance of default, probability the bond is called or a put option is exercised, and the possibility of interest rate fluctuations.The YTM is only the expected return if the prob. of default is zero, the prob. of call or put is zero, and interest rates remain unchanged.

DrakeDrake University

Fin 284Yield to Call

The yield to call is the yield paid on the bond assuming that a call option is exercised, given the current market price.It represents the yield you would earn if you bought the bond today and held it until the call option was exercised.

DrakeDrake University

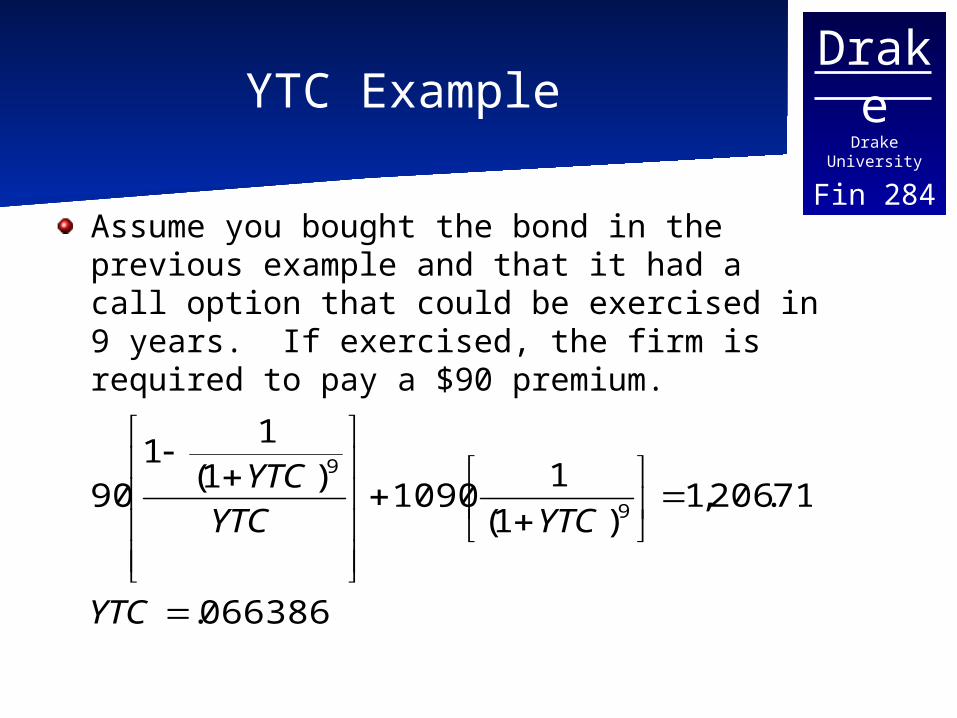

Fin 284YTC Example

Assume you bought the bond in the previous example and that it had a call option that could be exercised in 9 years. If exercised, the firm is required to pay a $90 premium.

066386.

71.206,1)1(

11090

)1(1

190

9

9

YTC

YTCYTCYTC

DrakeDrake University

Fin 284Yield to Worst

After calculating all the possible Yields (yield to call, yield to put) the one with the lowest return is the termed the yield to worst.

DrakeDrake University

Fin 284Quick Facts

1) If the level of interest rates in the economy increases the bond price decreases and vice versa.

2) If r>Coupon rate the price of the bond is below the par value - it is selling at a discount.

3) If r<Coupon rate the price of the bond is above the par value - it is selling at a premium.

4) Keeping everything constant the value of the bond will move toward par value as it gets closer to maturity.

DrakeDrake University

Fin 284Complications

Most bonds make payments every six months instead of each year.We have assumed that the next coupon payment is exactly 6 months away, often that is not the case. When the time frame is less than 6 months you need to account for interest over the shortened period.We have assumed that the interest rate is constant, some bonds pay a floating rate of interest.

DrakeDrake University

Fin 284Semiannual Compounding

Most bonds make coupon payments twice a year, to account for this:Divide the annual coupon interest payment by 2.Multiply the number of periods by 2. Divide the annual interest rate by 2

DrakeDrake University

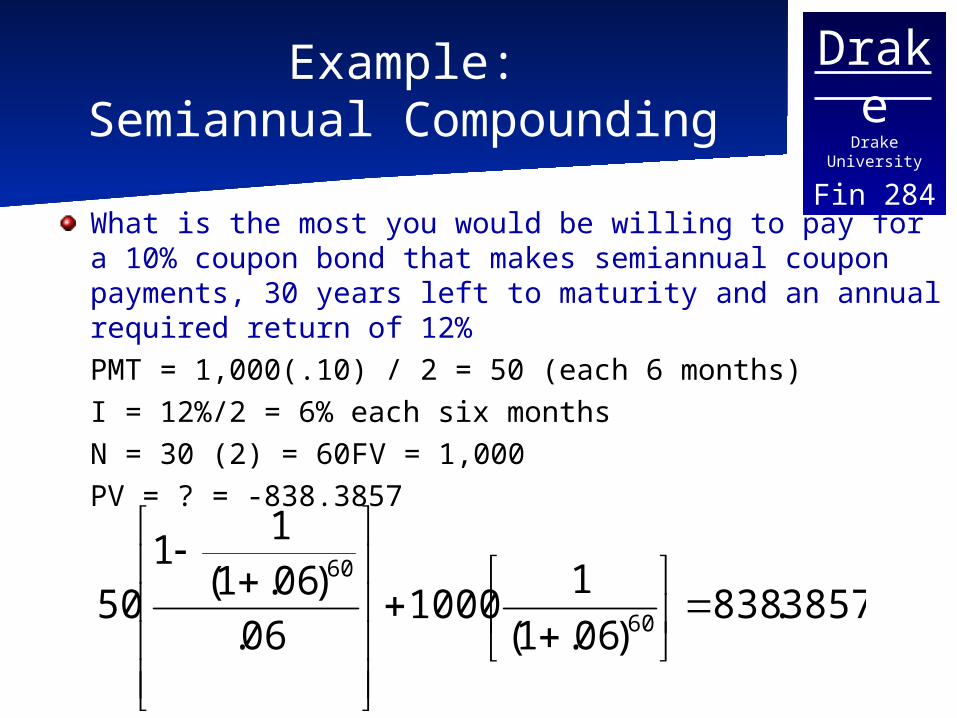

Fin 284

Example:Semiannual Compounding

What is the most you would be willing to pay for a 10% coupon bond that makes semiannual coupon payments, 30 years left to maturity and an annual required return of 12%

PMT = 1,000(.10) / 2 = 50 (each 6 months) I = 12%/2 = 6% each six months N = 30 (2) = 60 FV = 1,000 PV = ? = -838.3857

3857.838)06.1(

11000

06.)06.1(

11

5060

60

DrakeDrake University

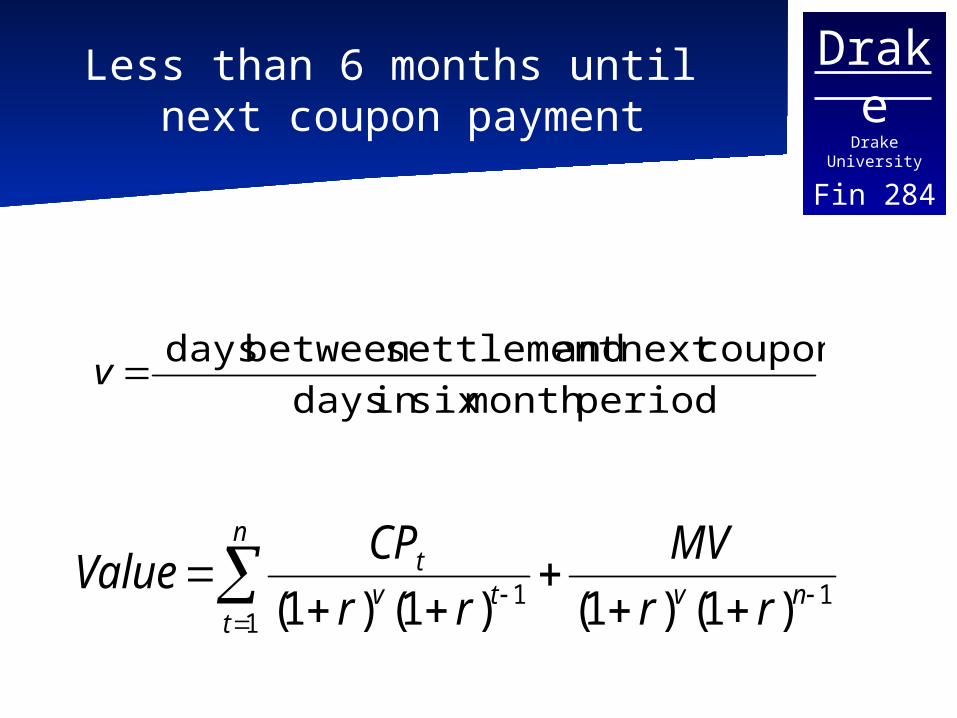

Fin 284

Less than 6 months until next coupon payment

11

1 )1()1()1()1(

nv

n

ttv

t

rr

MV

rr

CPValue

periodmonth six in days

couponnext and settlementbetween days v

DrakeDrake University

Fin 284Floating Interest Rates

A useful measure is the effective margin (Or spread compared to a base rate). Use the spread to calculate a value and compare that to the current price. If the two are different then there should be a change to the margin. You then develop an estimate of the margin the market is currently using to price the bond.

DrakeDrake University

Fin 284Bond Price Volatility

Assuming an option free bond, we have shown that the price and yield move in an opposite direction, however there are some important details:

Given similar bonds that differ only in maturity or coupon rate, The % price change associated with the same size change in yield will differ.For a given bond the % price change associated with a small change in yield is the same regardless of whether the yield increases or decreases.

DrakeDrake University

Fin 284

Bond Price Volatility continued

For a given bondthe % price change associated with a large increase in yield will not be the same as the % price change associated with the same size decrease in yieldFor a large change in yield the % price increase is greater than the % change decrease associated with the same size yield change.

DrakeDrake University

Fin 284Different Coupons

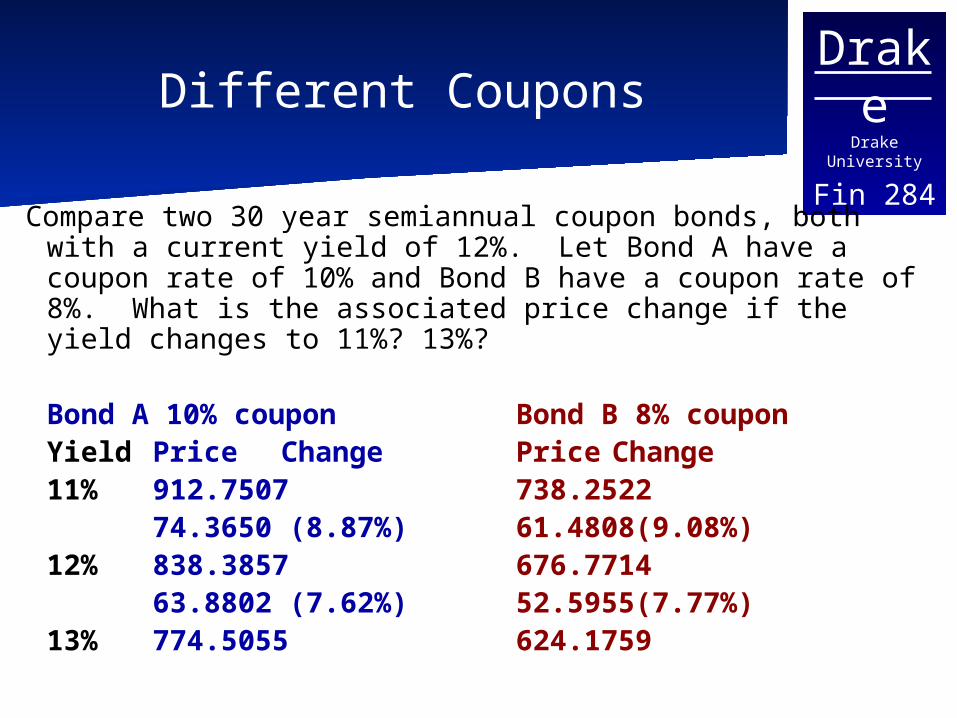

Compare two 30 year semiannual coupon bonds, both with a current yield of 12%. Let Bond A have a coupon rate of 10% and Bond B have a coupon rate of 8%. What is the associated price change if the yield changes to 11%? 13%?

Bond A 10% coupon Bond B 8%

couponYield Price Change Price Change

11% 912.7507 738.2522 74.3650 (8.87%) 61.4808(9.08%) 12% 838.3857 676.7714 63.8802 (7.62%) 52.5955(7.77%) 13% 774.5055 624.1759

DrakeDrake University

Fin 284Impact of Maturity

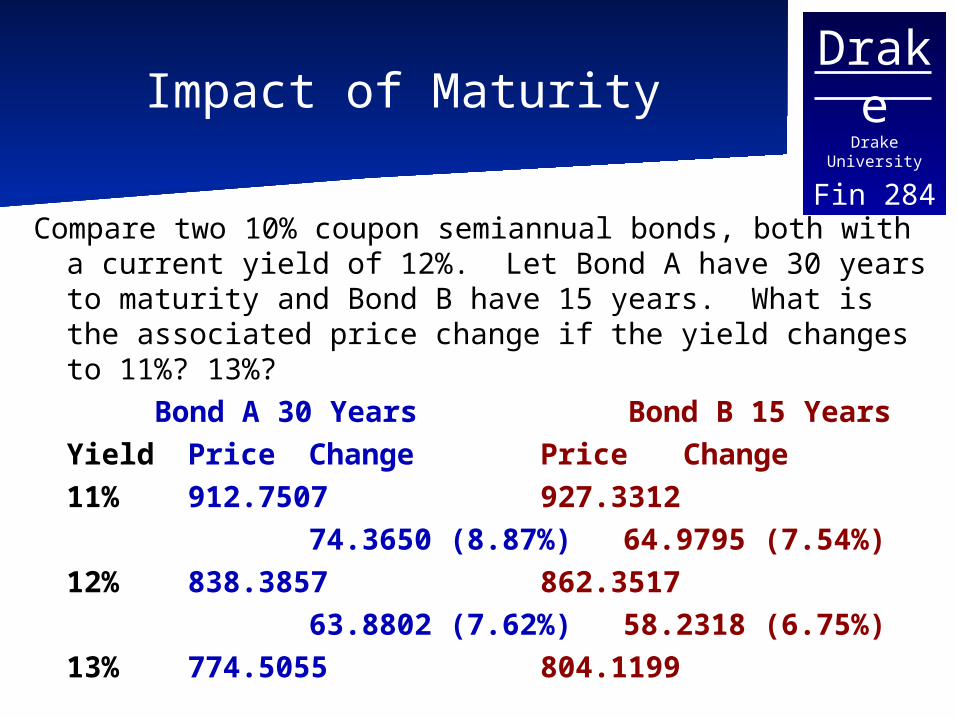

Compare two 10% coupon semiannual bonds, both with a current yield of 12%. Let Bond A have 30 years to maturity and Bond B have 15 years. What is the associated price change if the yield changes to 11%? 13%?

Bond A 30 Years Bond B 15 YearsYield Price Change Price Change

11% 912.7507 927.3312 74.3650 (8.87%) 64.9795 (7.54%) 12% 838.3857 862.3517 63.8802 (7.62%) 58.2318 (6.75%) 13% 774.5055 804.1199

DrakeDrake University

Fin 284

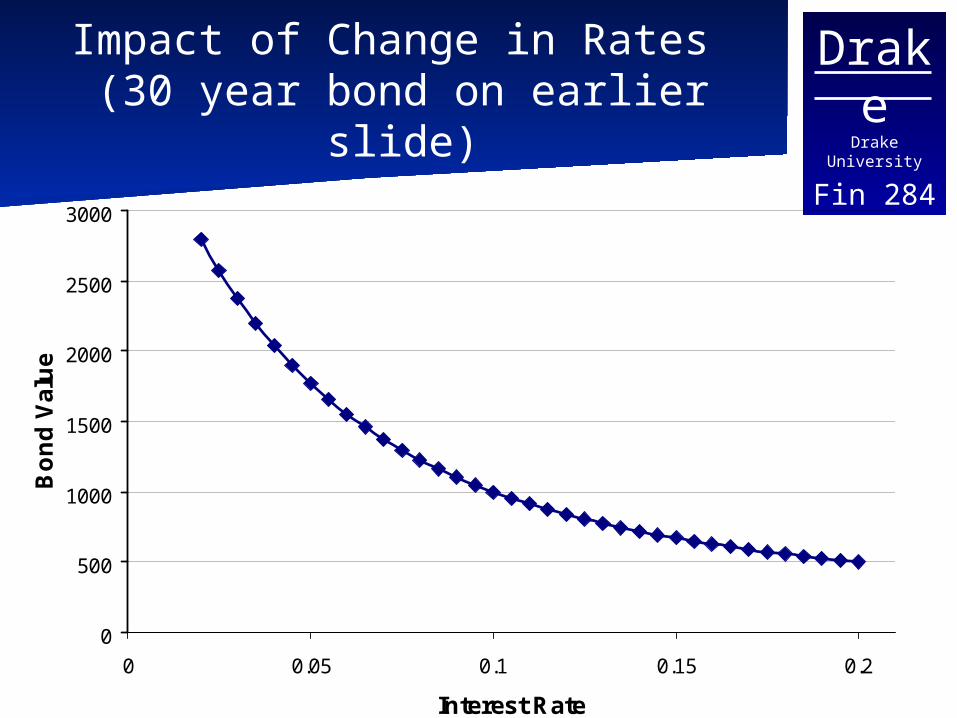

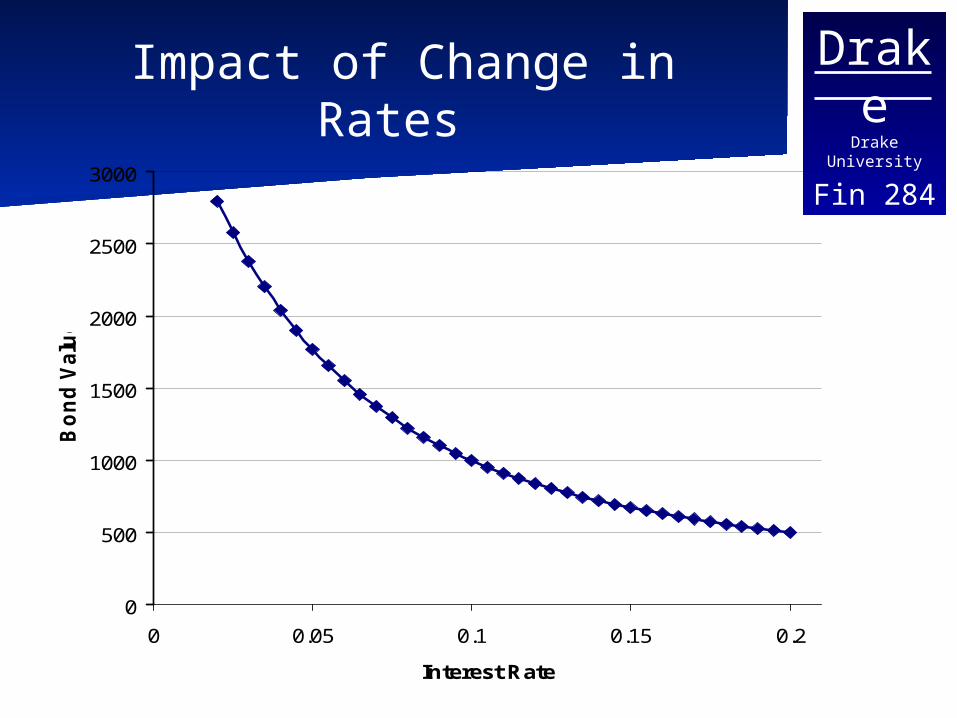

Impact of Change in Rates (30 year bond on earlier slide)

0

500

1000

1500

2000

2500

3000

0 0.05 0.1 0.15 0.2

Interest Rate

Bo

nd

Val

ue

DrakeDrake University

Fin 284

Measuring Bond Price Volatility

Price value of a basis pointMeasures the price change for a one basis point (.0001 or.01%) change in the yield of the bond.

Yield value of a basis pointMeasures the change in the yield of the bond for a given price change.

DurationMeasures the price elasticity of the bond.

DrakeDrake University

Fin 284

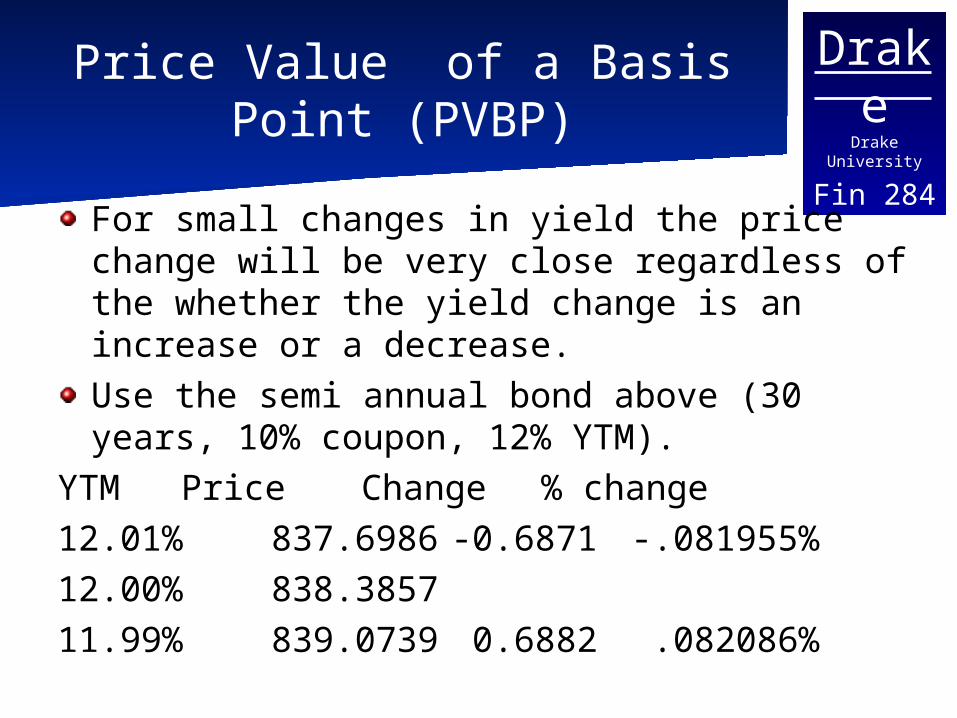

Price Value of a Basis Point (PVBP)

For small changes in yield the price change will be very close regardless of the whether the yield change is an increase or a decrease.Use the semi annual bond above (30 years, 10% coupon, 12% YTM).

YTM Price Change % change12.01% 837.6986 -0.6871 -.081955%12.00% 838.385711.99% 839.0739 0.6882 .082086%

DrakeDrake University

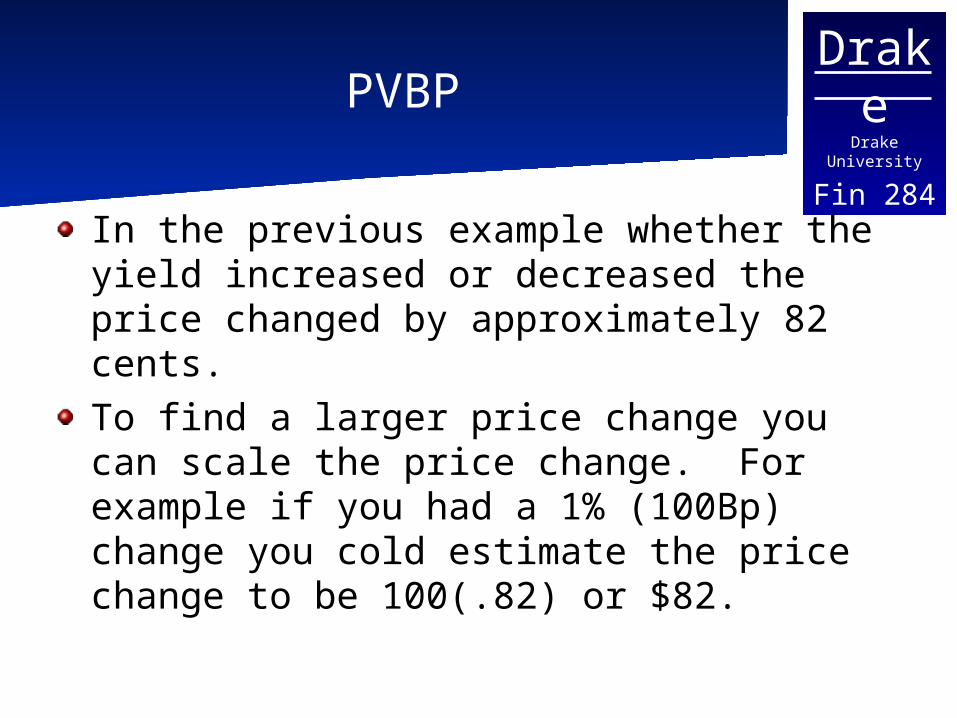

Fin 284PVBP

In the previous example whether the yield increased or decreased the price changed by approximately 82 cents.To find a larger price change you can scale the price change. For example if you had a 1% (100Bp) change you cold estimate the price change to be 100(.82) or $82.

DrakeDrake University

Fin 284

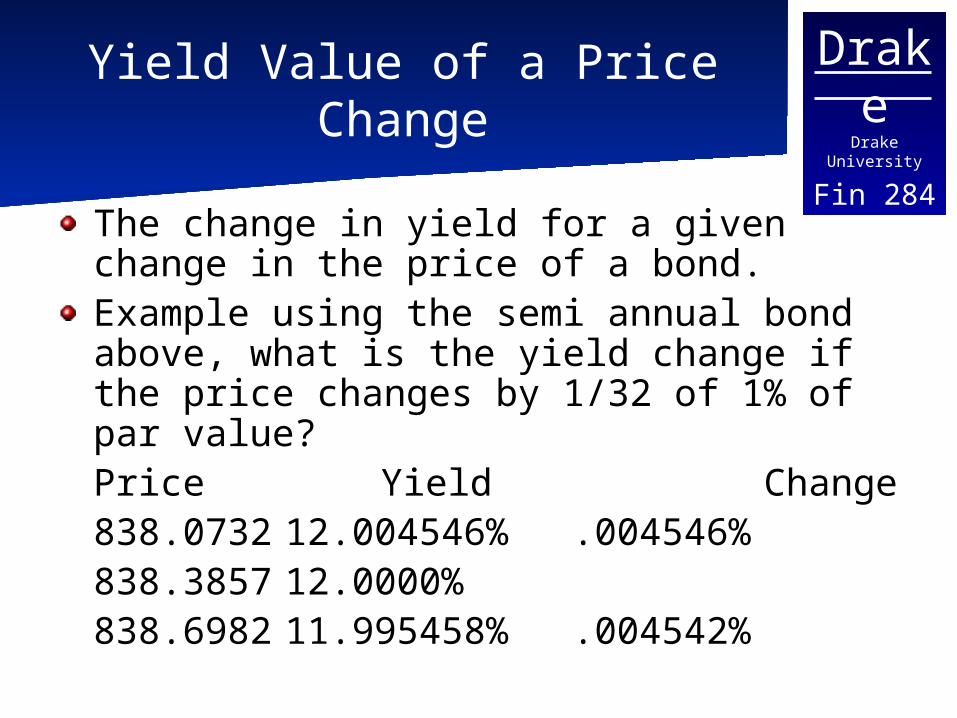

Yield Value of a Price Change

The change in yield for a given change in the price of a bond.Example using the semi annual bond above, what is the yield change if the price changes by 1/32 of 1% of par value?Price Yield Change838.0732 12.004546% .004546%838.3857 12.0000%838.6982 11.995458% .004542%

DrakeDrake University

Fin 284Duration: The Big Picture

Duration: Measures the sensitivity of the PV of a cash flow stream to a change in the discount rate.Keeping everything else constant the change in PV is greater:

The longer the time prior to receiving the cash flowThe larger the cash flow(we just showed both of these)

DrakeDrake University

Fin 284Duration: The Big Picture

Calculation: Given the PV relationships, we need to weight the Cash Flows based on the time until they are received. In other words we are looking for a weighted maturity of the cash flows where the weight is a combination of timing and magnitude of the cash flows

DrakeDrake University

Fin 284Calculating Duration

One way to measure the sensitivity of the price to a change in discount rate would be finding the price elasticity of the bond (the % change in price for a % change in the discount rate)

DrakeDrake University

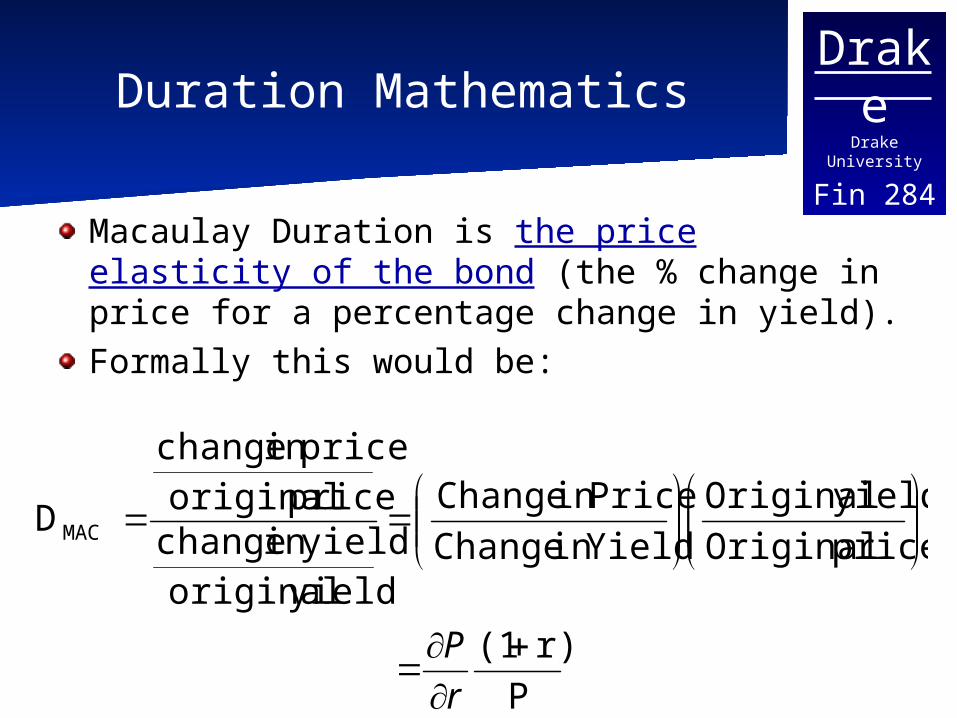

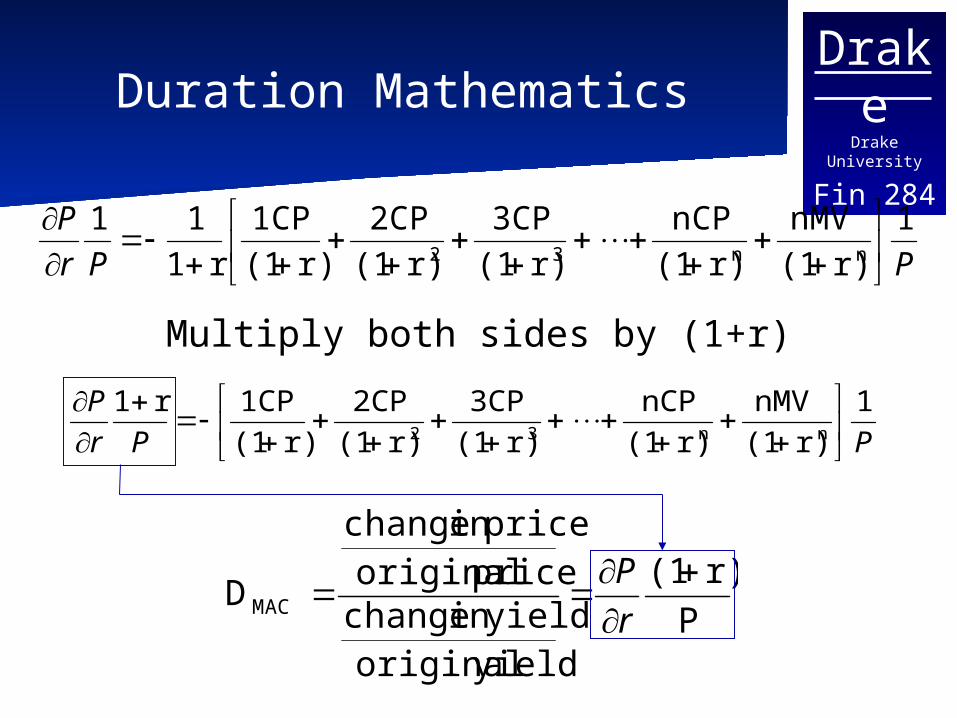

Fin 284Duration Mathematics

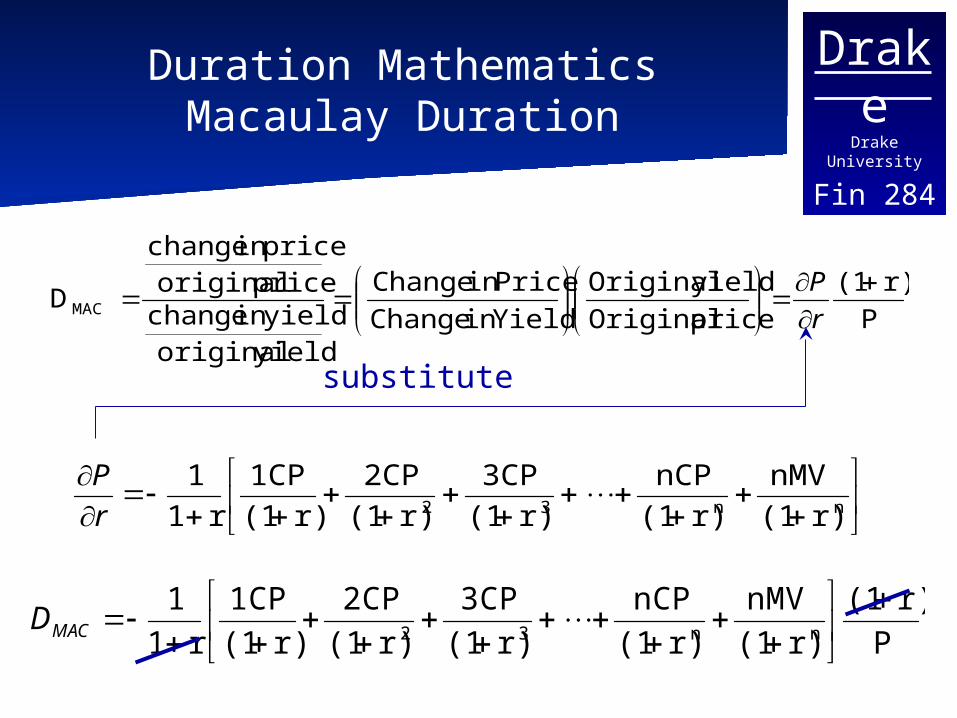

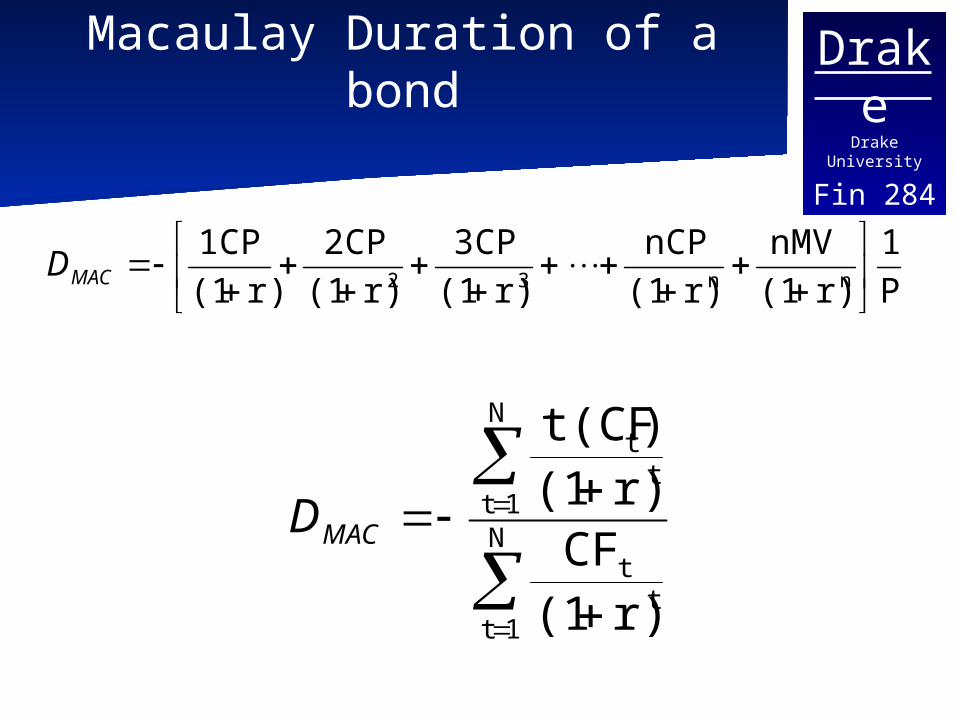

Macaulay Duration is the price elasticity of the bond (the % change in price for a percentage change in yield).Formally this would be:

P

r)(1

price Original

yield Original

Yieldin Change

Pricein Change

yield originalyieldin change

price originalpricein change

DMAC

r

P

DrakeDrake University

Fin 284Estimating Duration

There are multiple methods for estimating the duration of a bond we will look at three different approaches.

Weighted Discounted Cash Flows (Macaulay)Modified DurationAveraging the price change

DrakeDrake University

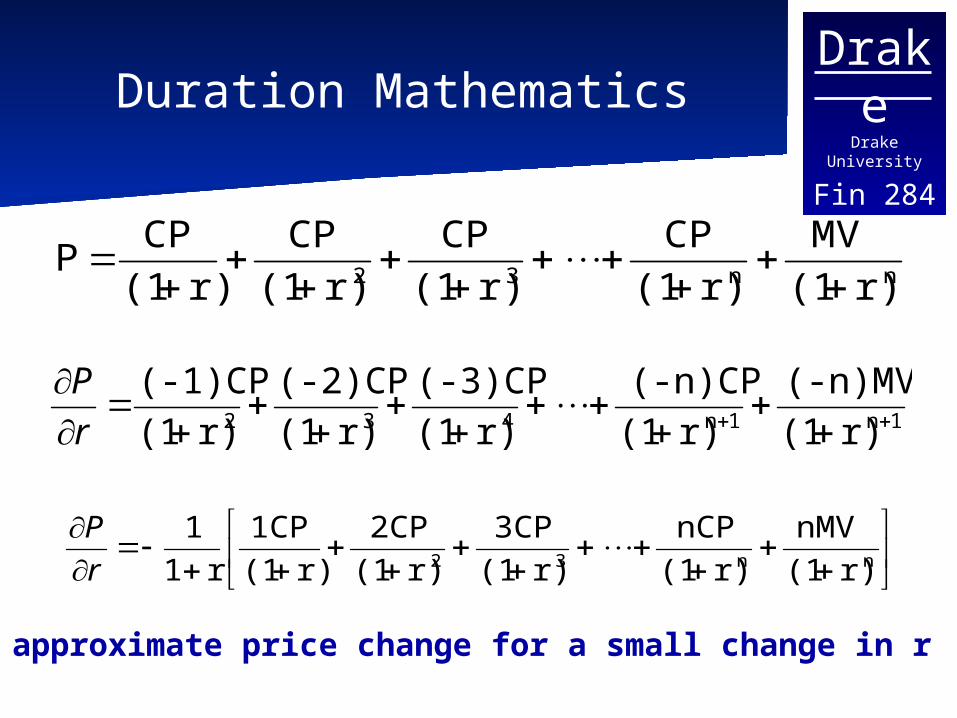

Fin 284Duration Mathematics

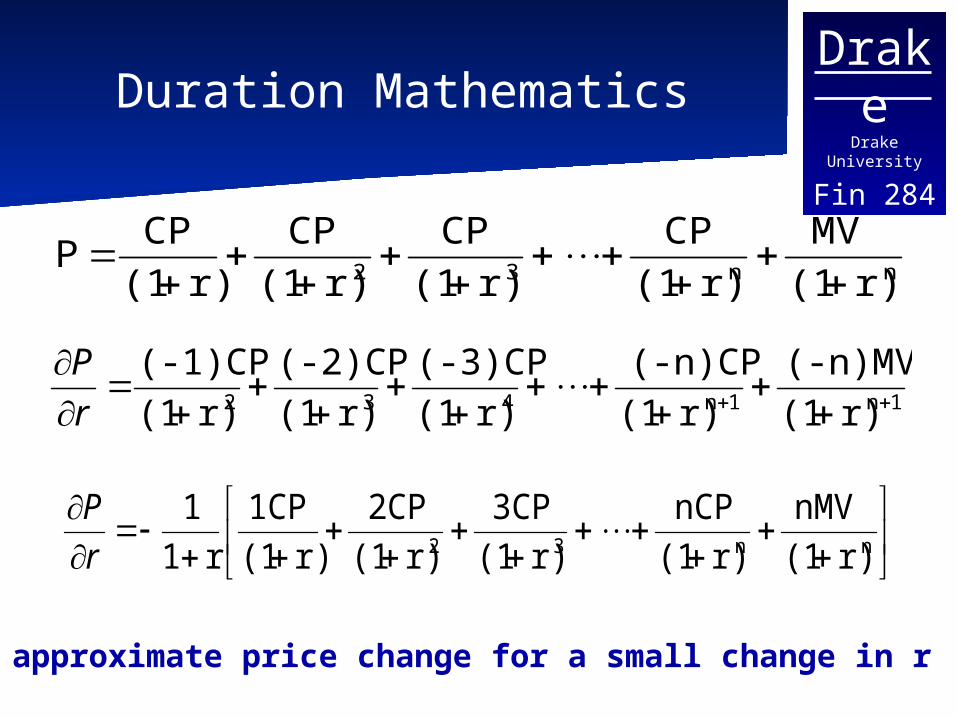

Taking the first derivative of the bond value equation with respect to the yield will produce the approximate price change for a small change in yield.

DrakeDrake University

Fin 284Duration Mathematics

1n1n432 r)(1

(-n)MV

r)(1

(-n)CP

r)(1

(-3)CP

r)(1

(-2)CP

r)(1

(-1)CP

r

P

nn32 r)(1

MV

r)(1

CP

r)(1

CP

r)(1

CP

r)(1

CPP

nn32 r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

1

r

P

The approximate price change for a small change in r

DrakeDrake University

Fin 284

Duration MathematicsMacaulay Duration

P

r)(1

price Original

yield Original

Yieldin Change

Pricein Change

yield originalyieldin change

price originalpricein change

DMAC

r

P

nn32 r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

1

r

P

substitute

P

r)(1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

1nn32

MACD

DrakeDrake University

Fin 284

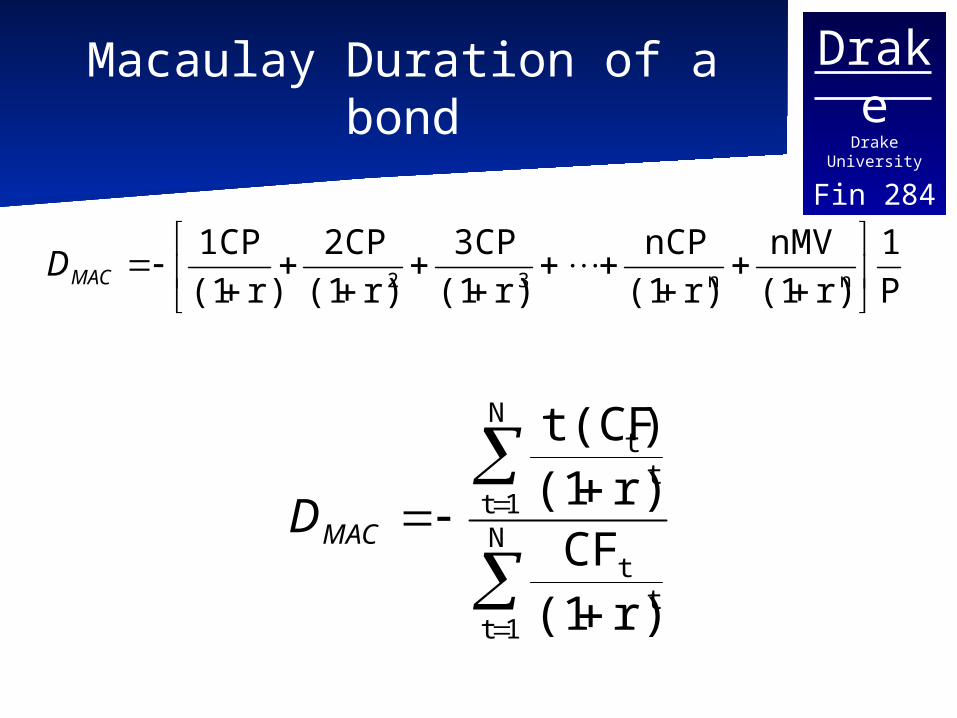

Macaulay Duration of a bond

N

1tt

t

N

1tt

t

r)(1CF

r)(1)t(CF

MACD

P

1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CPnn32

MACD

DrakeDrake University

Fin 284

Duration Mathematics (2nd derivation)

Taking the first derivative of the bond value equation with respect to the yield will produce the approximate price change for a small change in yield.

DrakeDrake University

Fin 284Duration Mathematics

1n1n432 r)(1

(-n)MV

r)(1

(-n)CP

r)(1

(-3)CP

r)(1

(-2)CP

r)(1

(-1)CP

r

P

nn32 r)(1

MV

r)(1

CP

r)(1

CP

r)(1

CP

r)(1

CPP

nn32 r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

1

r

P

The approximate price change for a small change in r

DrakeDrake University

Fin 284Duration Mathematics

nn32 r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

1

r

P

Divide both sides by the original price to get the % change in price associated with a given change in r

PPr

P 1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

11nn32

DrakeDrake University

Fin 284Duration Mathematics

PPr

P 1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CP

r1

11nn32

PPr

P 1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CPr1nn32

Multiply both sides by (1+r)

P

r)(1

yield originalyieldin change

price originalpricein change

DMAC

r

P

DrakeDrake University

Fin 284

Macaulay Duration of a bond

N

1tt

t

N

1tt

t

r)(1CF

r)(1)t(CF

MACD

P

1

r)(1

nMV

r)(1

nCP

r)(1

3CP

r)(1

2CP

r)(1

1CPnn32

MACD

DrakeDrake University

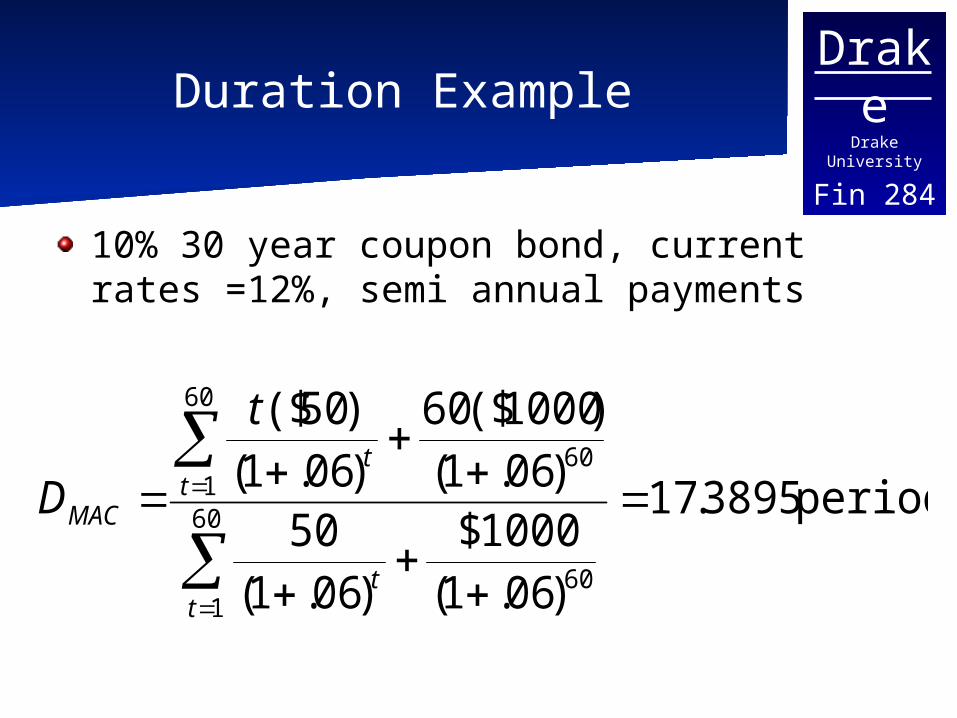

Fin 284Duration Example

10% 30 year coupon bond, current rates =12%, semi annual payments

periods 3895.17

)06.1(1000$

)06.1(50

)06.1()1000($60

)06.1()50($

60

160

60

160

tt

tt

MAC

t

D

DrakeDrake University

Fin 284Example continued

Since the bond makes semi annual coupon payments, the duration of 17.389455 periods must be divided by 2 to find the number of years.17.389455 / 2 = 8.6947277 yearsAnother interpretation of duration is shown here: Duration indicates the average time taken by the bond, on a discounted basis, to pay back the original investment.

DrakeDrake University

Fin 284

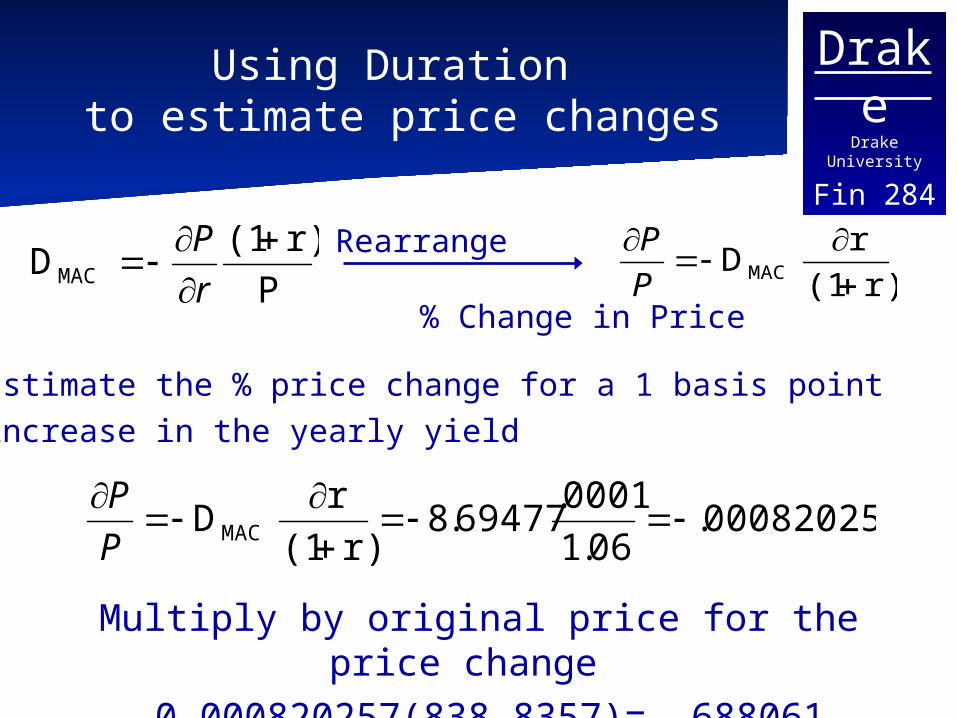

Using Duration to estimate price changes

P

r)(1DMAC

r

Pr)(1

rDMAC

P

PRearrange

% Change in Price

Estimate the % price change for a 1 basis point increase in the yearly yield

000820257.06.1

0001.69477.8

r)(1

rDMAC

P

P

Multiply by original price for the price change

-0.000820257(838.8357)=-.688061

DrakeDrake University

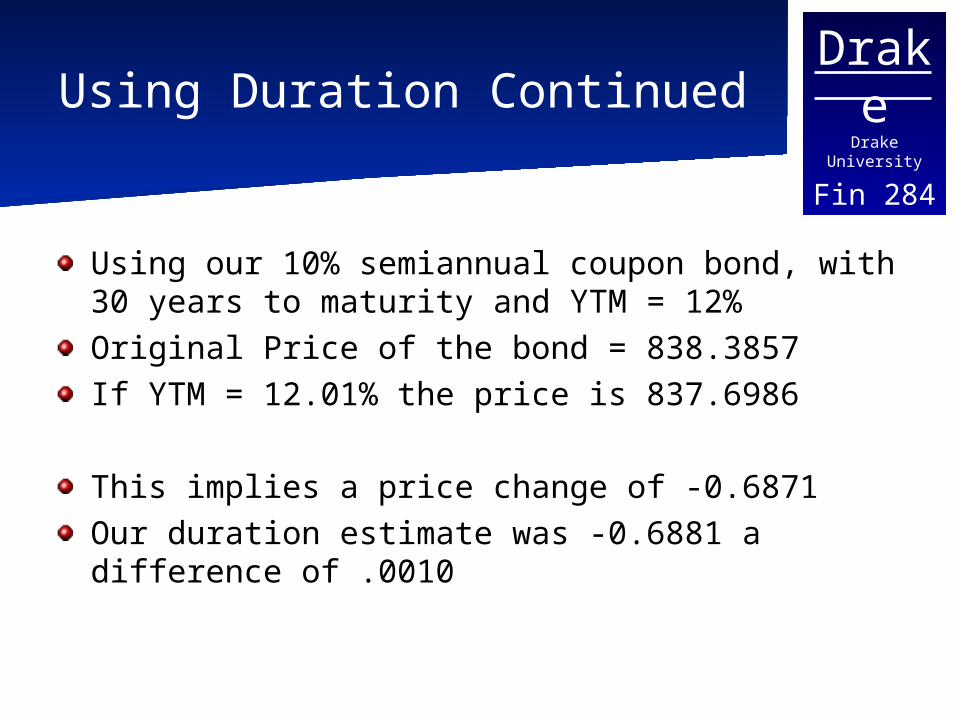

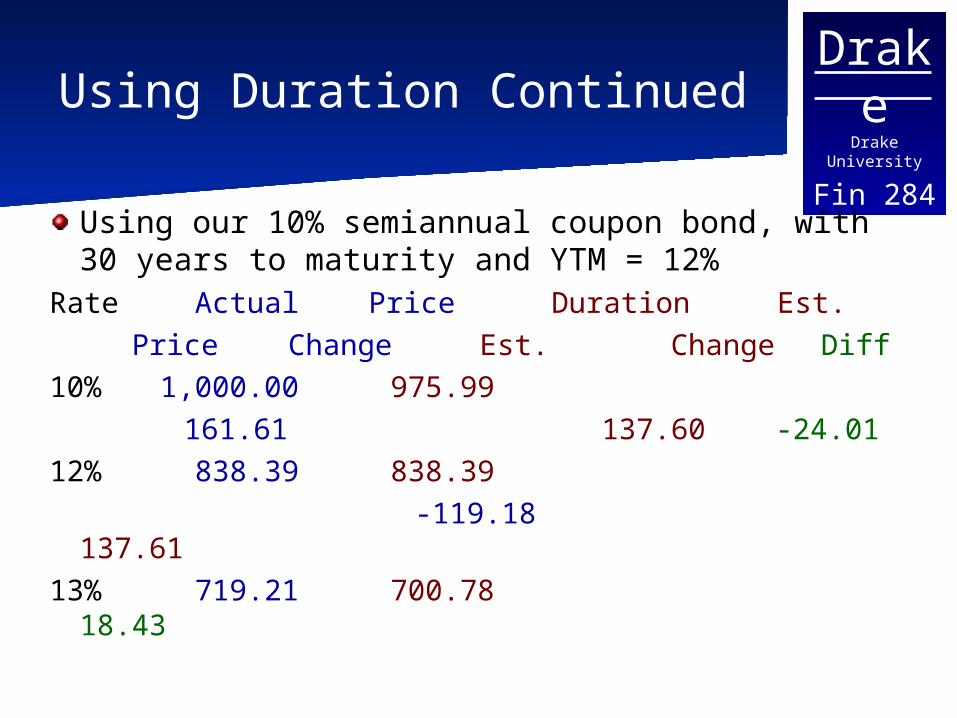

Fin 284Using Duration Continued

Using our 10% semiannual coupon bond, with 30 years to maturity and YTM = 12%Original Price of the bond = 838.3857If YTM = 12.01% the price is 837.6986

This implies a price change of -0.6871Our duration estimate was -0.6881 a difference of .0010

DrakeDrake University

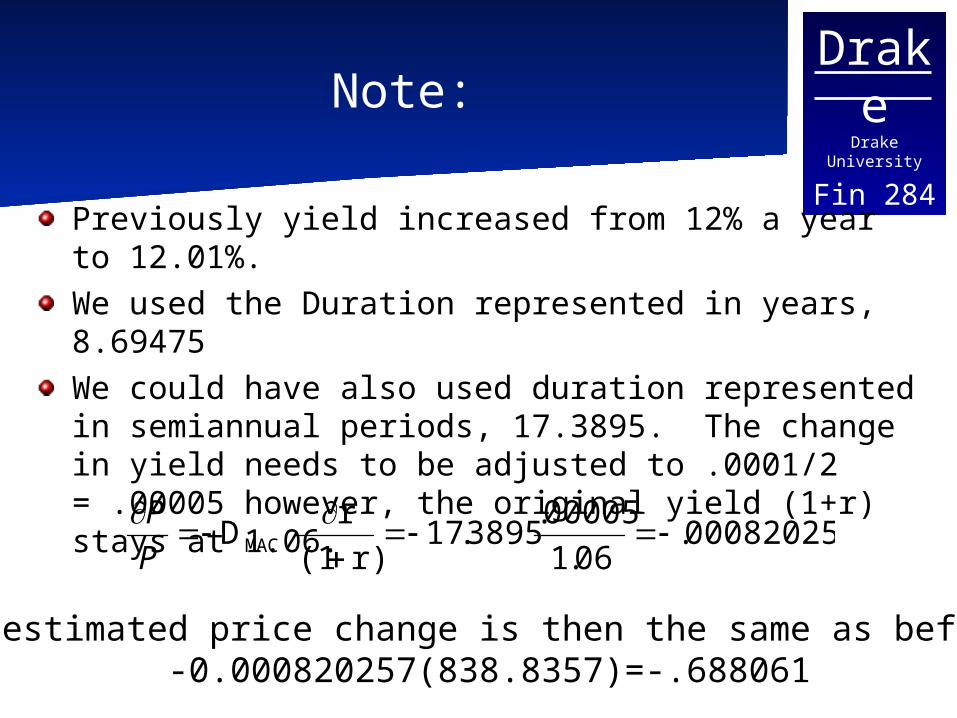

Fin 284Note:

Previously yield increased from 12% a year to 12.01%.We used the Duration represented in years, 8.69475We could have also used duration represented in semiannual periods, 17.3895. The change in yield needs to be adjusted to .0001/2 = .00005 however, the original yield (1+r) stays at 1.06.

000820257.06.1

00005.3895.17

r)(1

rDMAC

P

P

The estimated price change is then the same as before: -0.000820257(838.8357)=-.688061

DrakeDrake University

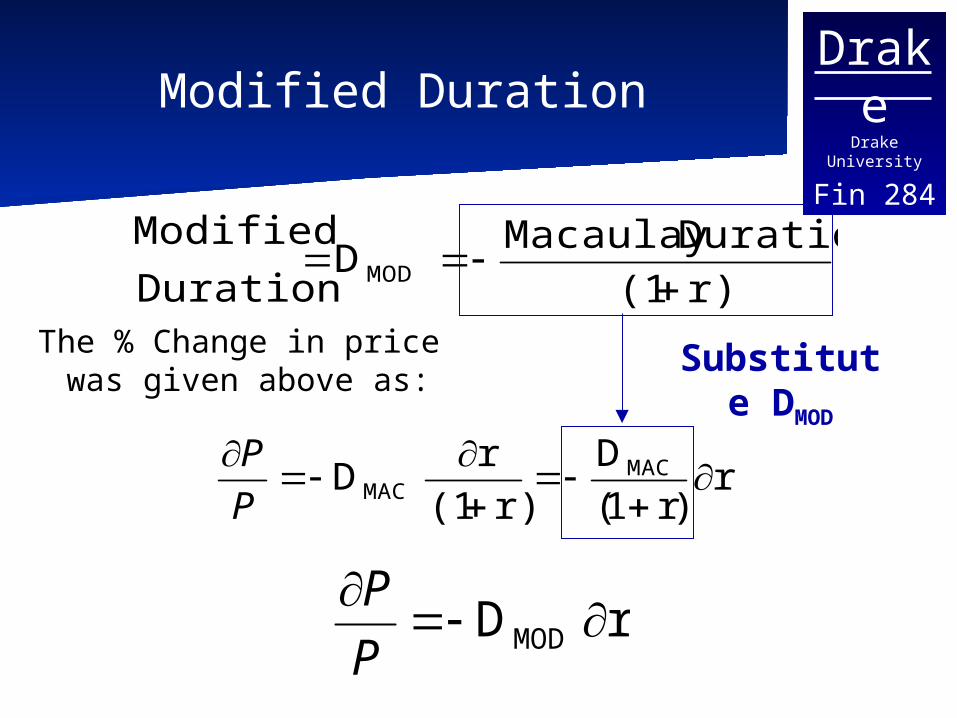

Fin 284Modified Duration

r)(1

DurationMacaulay D

Duration

ModifiedMOD

r)r1(

D

r)(1

rD MAC

MAC

P

P

Substitute DMOD

The % Change in price was given above as:

rDMODP

P

DrakeDrake University

Fin 284

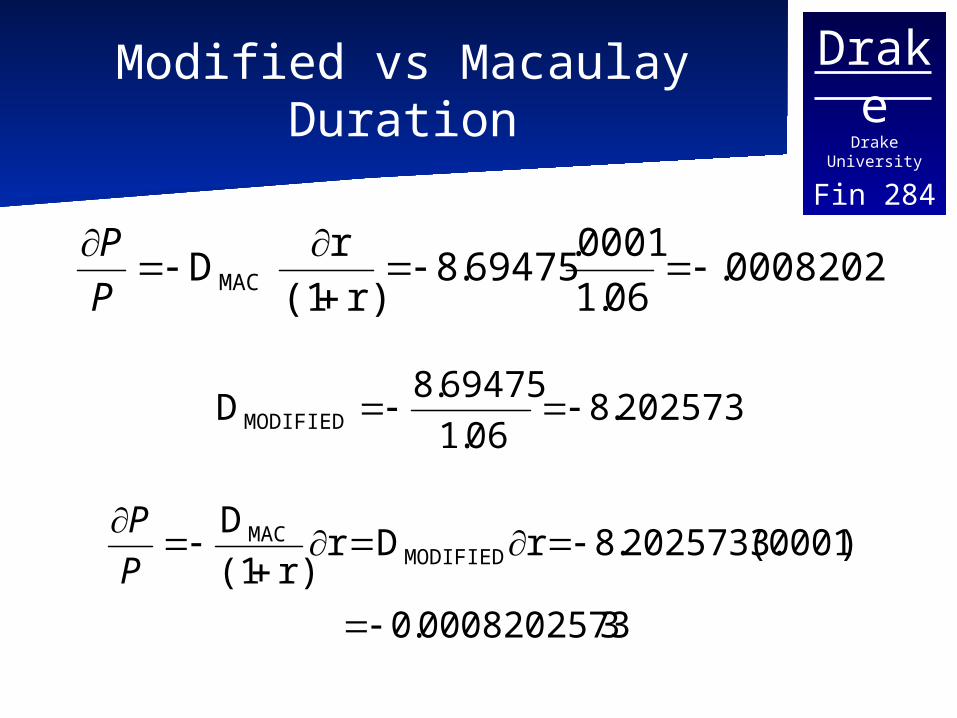

Modified vs Macaulay Duration

2025733.806.1

69475.8DMODIFIED

00082025.06.1

0001.69475.8

r)(1

rDMAC

P

P

30008202573.0

)0001(.2025733.8r Drr)(1

DMODIFIED

MAC

P

P

DrakeDrake University

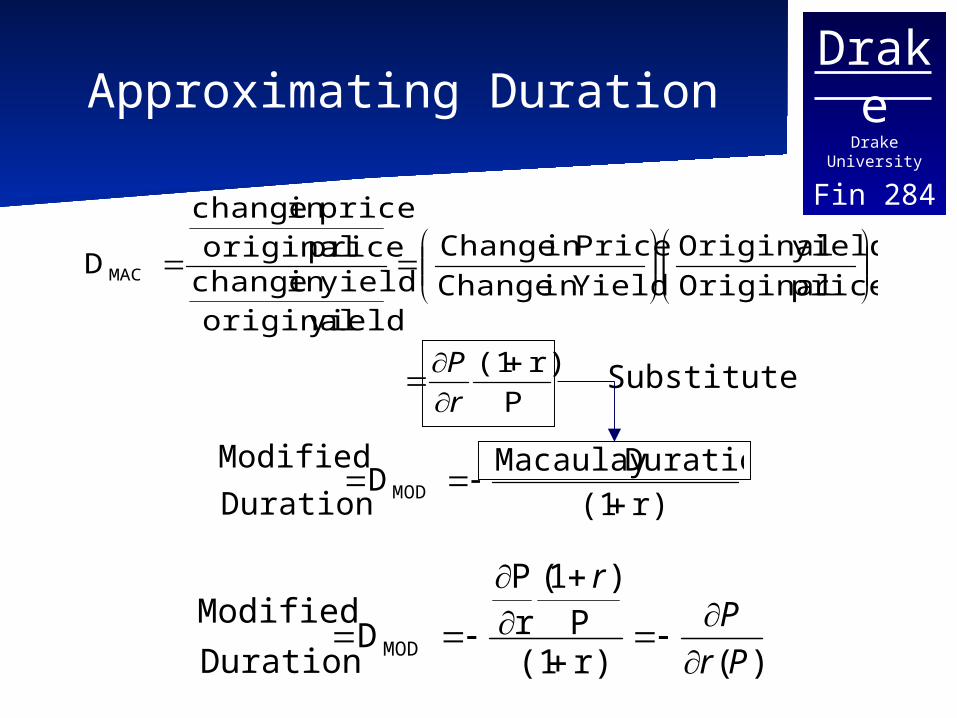

Fin 284Approximating Duration

P

r)(1

price Original

yield Original

Yieldin Change

Pricein Change

yield originalyieldin change

price originalpricein change

DMAC

r

P

r)(1

DurationMacaulay D

Duration

ModifiedMOD

)(r)(1P

)1(rP

DDuration

ModifiedMOD Pr

Pr

Substitute

DrakeDrake University

Fin 284

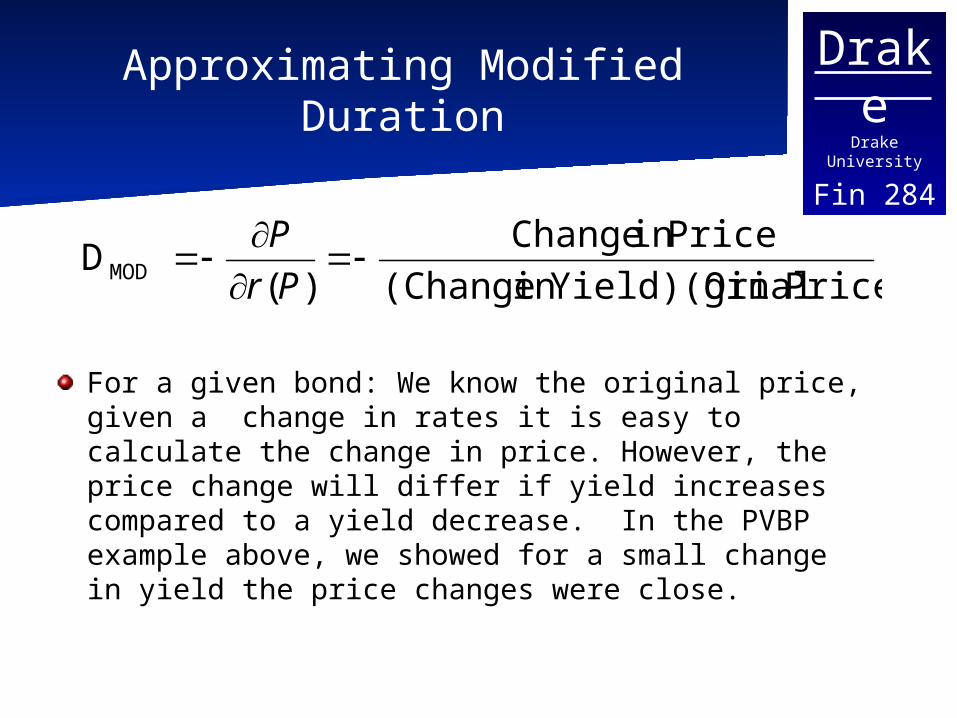

Approximating Modified Duration

For a given bond: We know the original price, given a change in rates it is easy to calculate the change in price. However, the price change will differ if yield increases compared to a yield decrease. In the PVBP example above, we showed for a small change in yield the price changes were close.

Price) ginalYield)(Oriin (Change

Pricein Change

)(DMOD

Pr

P

DrakeDrake University

Fin 284Approximating Duration

We can use the fact that the price change associated with a small yield change will be very close regardless of whether the yield increases or decreases. To get an approximation of the price change you can average the two price changes associated with a change in yield.

DrakeDrake University

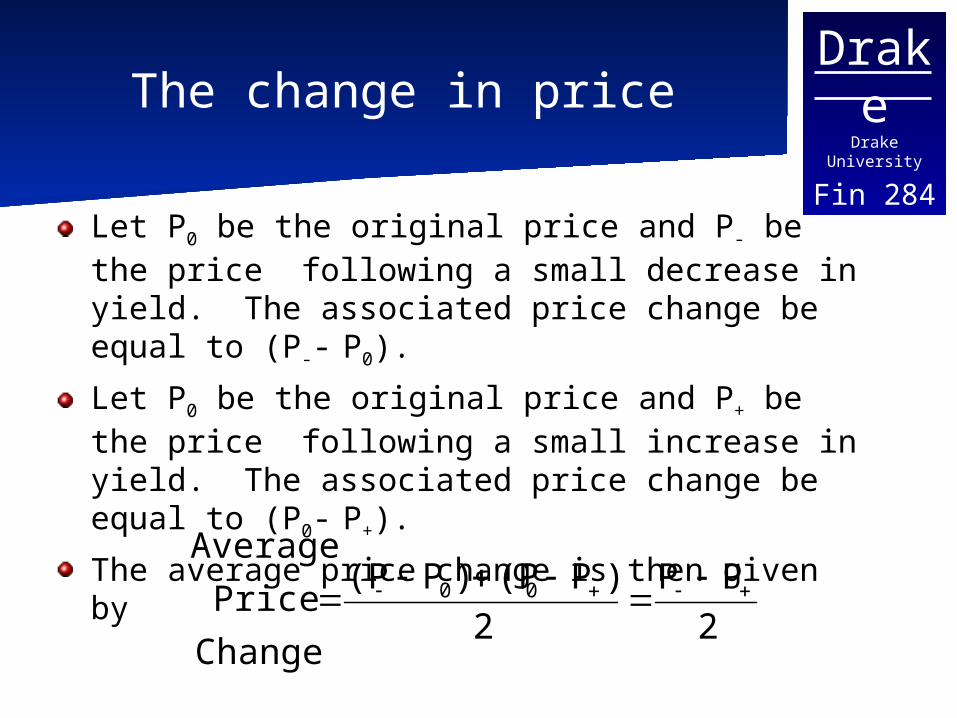

Fin 284The change in price

Let P0 be the original price and P- be the price following a small decrease in yield. The associated price change be equal to (P-- P0).

Let P0 be the original price and P+ be the price following a small increase in yield. The associated price change be equal to (P0- P+).

The average price change is then given by

2

PP

2

)P(P)P(P

Change

Price

Average00

DrakeDrake University

Fin 284

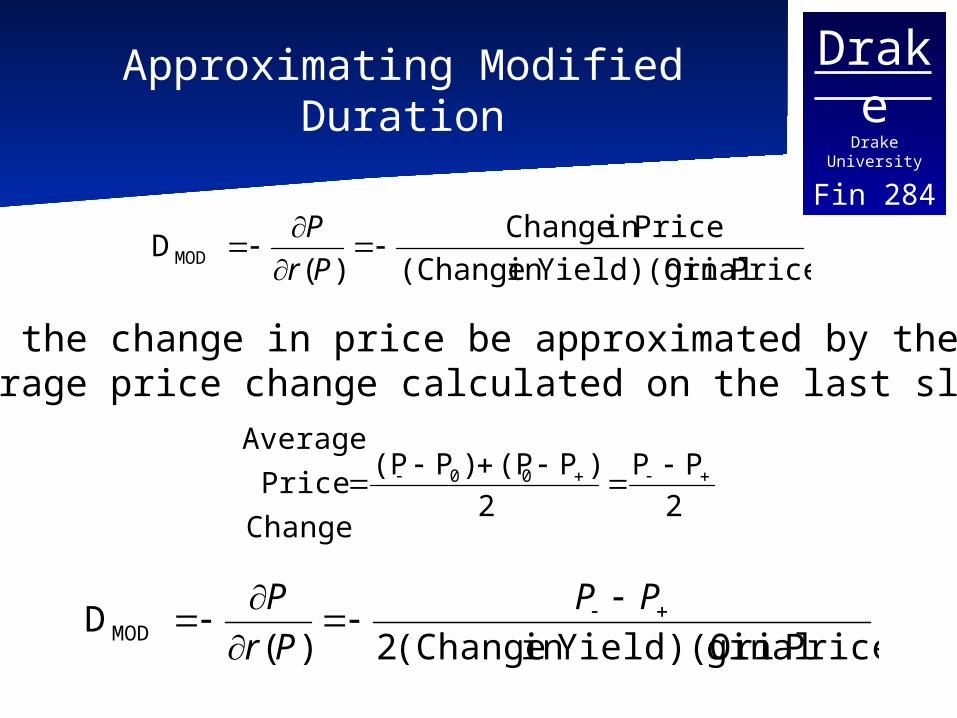

Approximating Modified Duration

Price) ginalYield)(Oriin (Change

Pricein Change

)(DMOD

Pr

P

2

PP

2

)P(P)P(P

Change

Price

Average00

Let the change in price be approximated by the average price change calculated on the last slide

Price) ginalYield)(Oriin (Change2)(DMOD

PP

Pr

P

DrakeDrake University

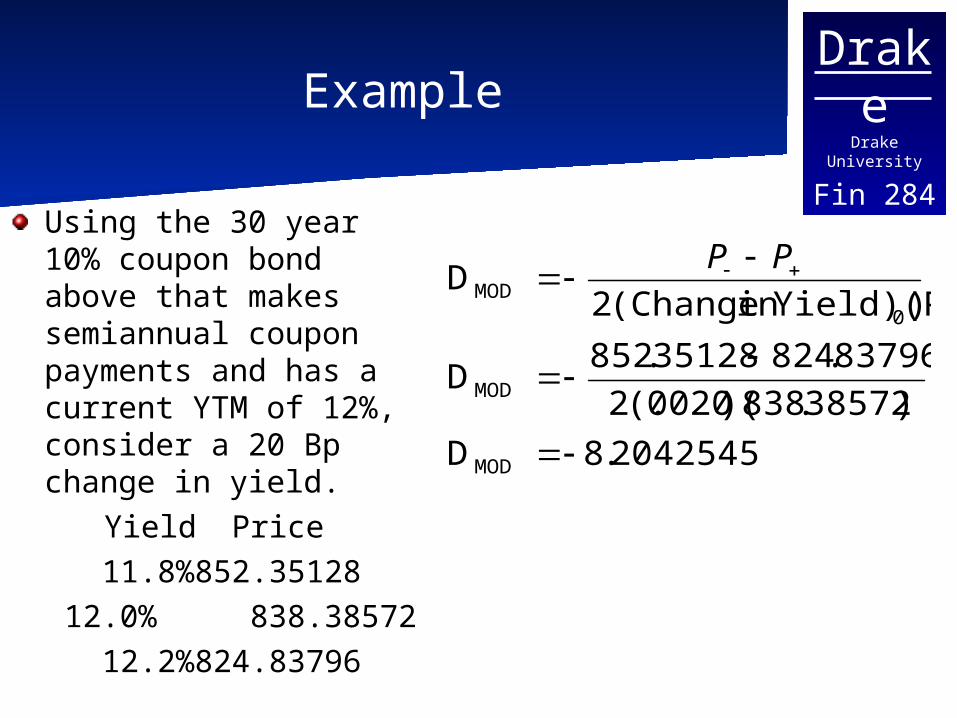

Fin 284Example

Using the 30 year 10% coupon bond above that makes semiannual coupon payments and has a current YTM of 12%, consider a 20 Bp change in yield.

Yield Price11.8% 852.35128 12.0% 838.3857212.2% 824.83796

2042545.8D

)38572.838)(0020(.2

83796.82435128.852D

)Yield)(Pin (Change2D

MOD

MOD

0MOD

PP

DrakeDrake University

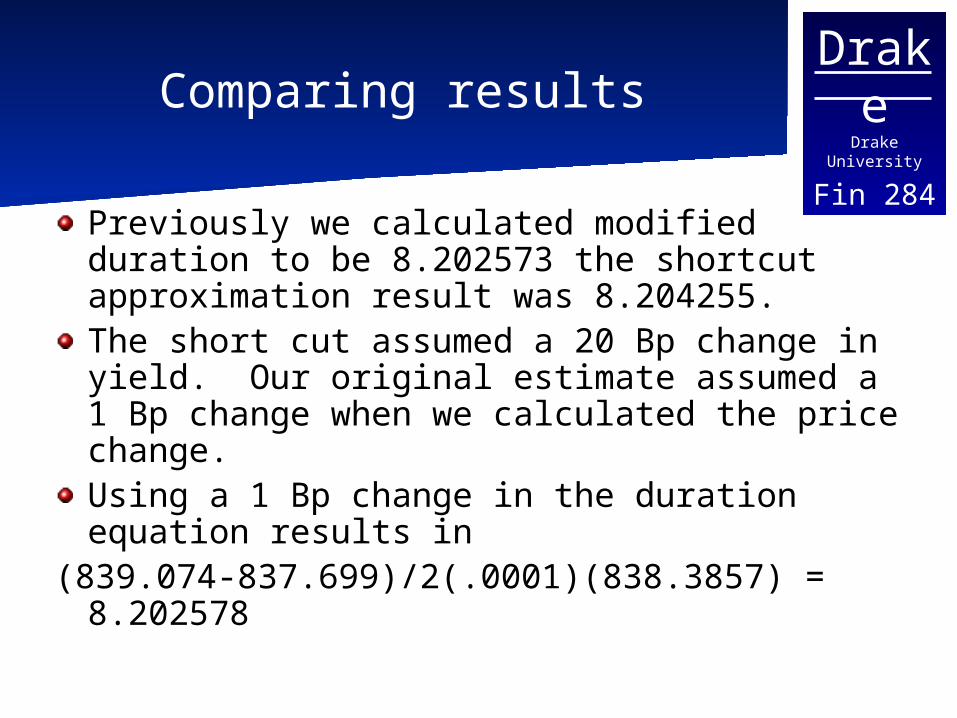

Fin 284Comparing results

Previously we calculated modified duration to be 8.202573 the shortcut approximation result was 8.204255. The short cut assumed a 20 Bp change in yield. Our original estimate assumed a 1 Bp change when we calculated the price change.Using a 1 Bp change in the duration equation results in

(839.074-837.699)/2(.0001)(838.3857) = 8.202578

DrakeDrake University

Fin 284

How much does the size of Bp change matter?

What is the duration if we had assumed a 50 Bp change? Or a 100 Bp Change? Generally with a shorter maturity bond, the duration estimates will be very close, but for longer maturity bonds the duration estimates may differ by a small amount.

DrakeDrake University

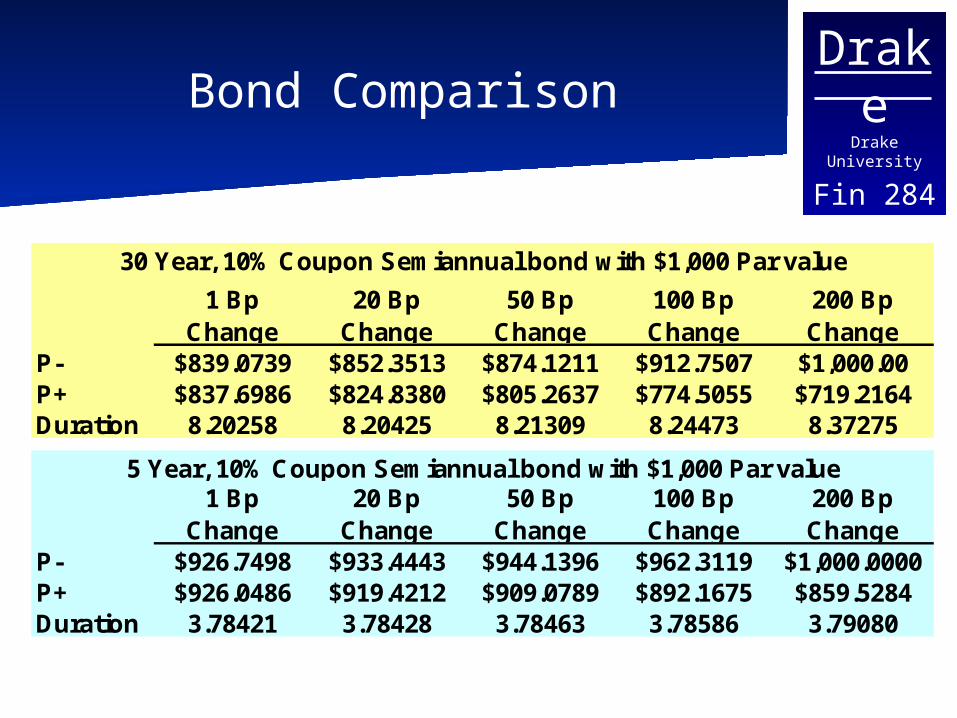

Fin 284Bond Comparison

1 Bp Change

20 Bp Change

50 Bp Change

100 Bp Change

200 Bp Change

P- $839.0739 $852.3513 $874.1211 $912.7507 $1,000.00P+ $837.6986 $824.8380 $805.2637 $774.5055 $719.2164Duration 8.20258 8.20425 8.21309 8.24473 8.37275

1 Bp Change

20 Bp Change

50 Bp Change

100 Bp Change

200 Bp Change

P- $926.7498 $933.4443 $944.1396 $962.3119 $1,000.0000P+ $926.0486 $919.4212 $909.0789 $892.1675 $859.5284Duration 3.78421 3.78428 3.78463 3.78586 3.79080

30 Year, 10% Coupon Semiannual bond with $1,000 Par value

5 Year, 10% Coupon Semiannual bond with $1,000 Par value

DrakeDrake University

Fin 284Duration Characteristics

Keeping other factors constant the duration of a bond will:Increase with the maturity of the bondDecrease with the coupon rate of the bondWill decrease if the interest rate is floating making the bond less sensitive to interest rate changes

DrakeDrake University

Fin 284

Effective Duration vs. Other Definitions

Macaulay Duration and the most frequently used definition of modified duration assume that the cash flows do not change as the discount rate (yield) changes.Effective Duration accounts for an associated change in the cash flow, for example if a bond is called, or if mortgages are prepaid early.The linear approximation of Duration also implicitly assumes that cash flows can change. The value of the security should include any changes in the cash flows.

DrakeDrake University

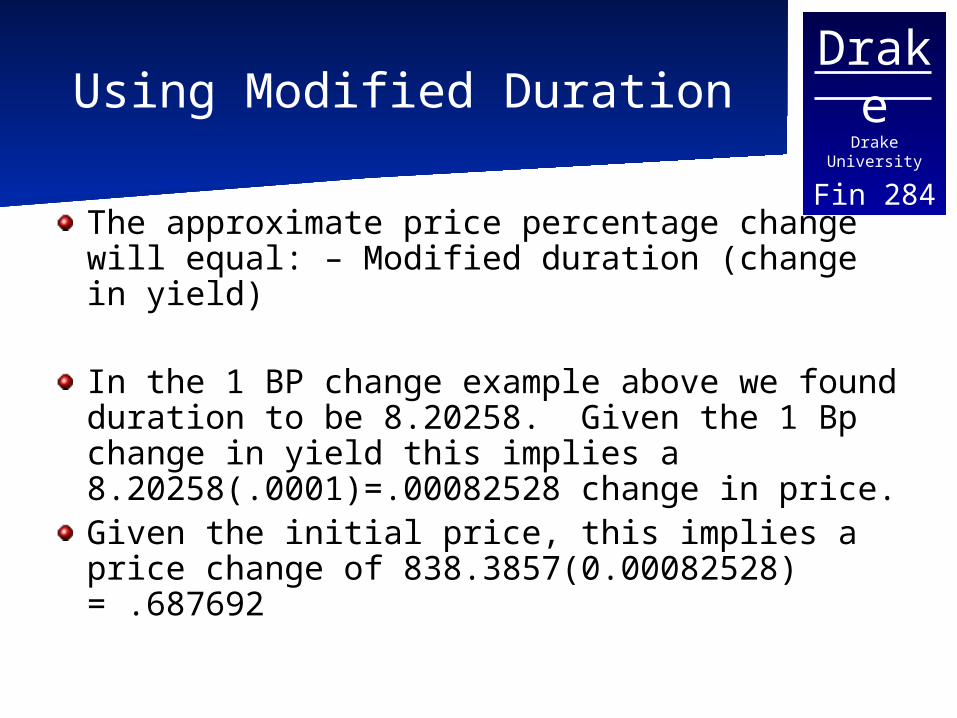

Fin 284Using Modified Duration

The approximate price percentage change will equal: – Modified duration (change in yield)

In the 1 BP change example above we found duration to be 8.20258. Given the 1 Bp change in yield this implies a 8.20258(.0001)=.00082528 change in price.Given the initial price, this implies a price change of 838.3857(0.00082528) = .687692

DrakeDrake University

Fin 284Using duration continued

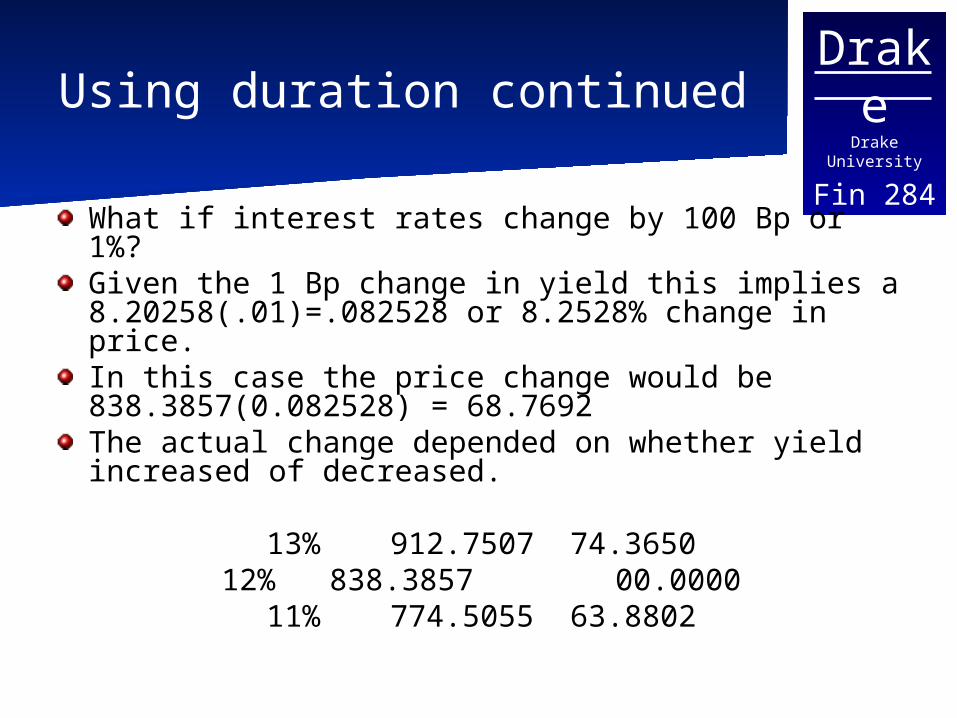

What if interest rates change by 100 Bp or 1%?Given the 1 Bp change in yield this implies a 8.20258(.01)=.082528 or 8.2528% change in price.In this case the price change would be 838.3857(0.082528) = 68.7692The actual change depended on whether yield increased of decreased.

13% 912.7507 74.365012% 838.3857 00.000011% 774.5055 63.8802

DrakeDrake University

Fin 284Duration Intuition

The previous slide provides a good explanation of the intuition underlying duration. The duration of 8.20258 was shown to create an approximate price change of 8.25258% for a 100 Bp change in yield. However, the actual price change was not equal to the approximation in either case due to the shape of the price yield relationship.

DrakeDrake University

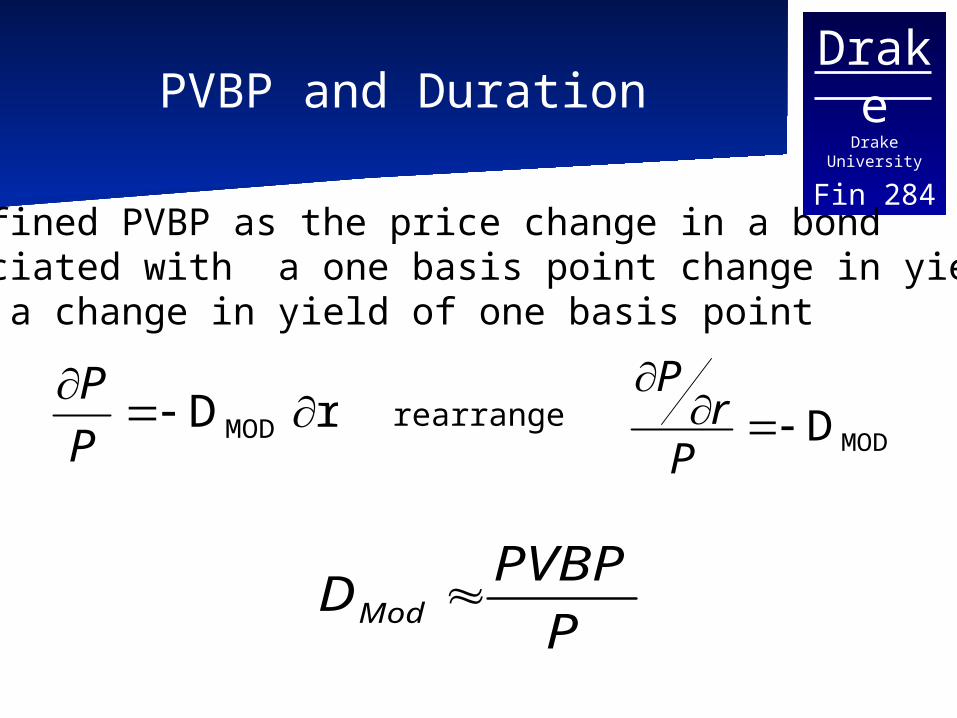

Fin 284PVBP and Duration

rDMODP

P

P

PVBPDMod

We defined PVBP as the price change in a bond associated with a one basis point change in yield. Using a change in yield of one basis point

MODD

Pr

Prearrange

DrakeDrake University

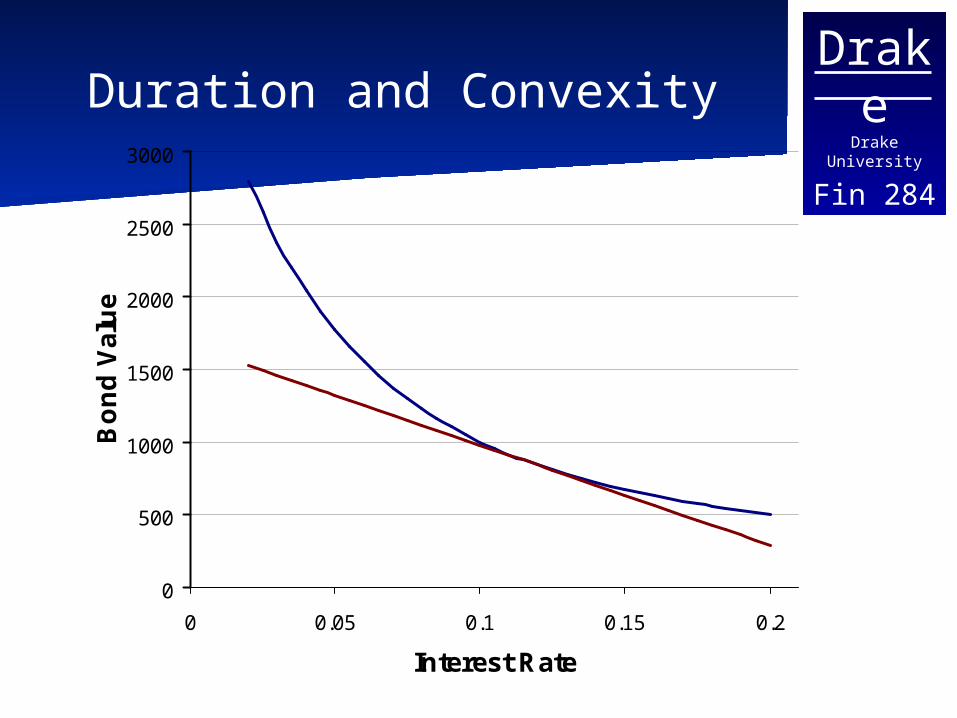

Fin 284Duration and Convexity

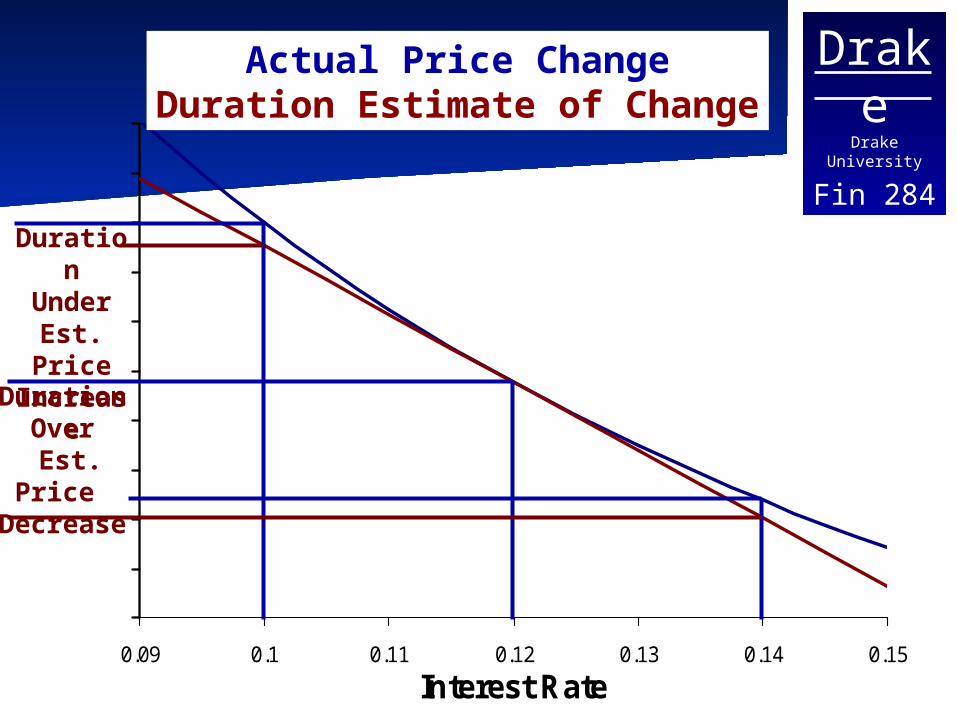

Using duration to estimate the price change implies that the change in price is the same size regardless of whether the price increased or decreased.The price yield relationship shows that this is not true.

DrakeDrake University

Fin 284Impact of Change in Rates

0

500

1000

1500

2000

2500

3000

0 0.05 0.1 0.15 0.2

Interest Rate

Bo

nd

Valu

e

DrakeDrake University

Fin 284Duration

Duration provides a linear approximation of the price change, the actual relationship is convex

DrakeDrake University

Fin 284Duration and Convexity

0

500

1000

1500

2000

2500

3000

0 0.05 0.1 0.15 0.2

Interest Rate

Bo

nd

Val

ue

DrakeDrake University

Fin 284Using Duration Continued

Using our 10% semiannual coupon bond, with 30 years to maturity and YTM = 12%

Rate Actual Price Duration Est. Price Change Est. Change Diff

10% 1,000.00 975.99 161.61 137.60 -24.01

12% 838.39 838.39 -119.18 137.6113% 719.21 700.78 18.43

DrakeDrake University

Fin 284

0.09 0.1 0.11 0.12 0.13 0.14 0.15

Interest Rate

Duration Over

Est. Price Decrease

DurationUnderEst.

PriceIncrease

Actual Price ChangeDuration Estimate of Change

DrakeDrake University

Fin 284Convexity

The amount of curvature in the yield price relationship is often referred to as the convexity.The curvature is measuring the change in the duration for a given change in yield (return).

DrakeDrake University

Fin 284Positive Convexity

Generally: as the yield of the bond increases, the convexity of the bond decreases (positive convexity) This implies

As Yield increases, each successive price decline is less (there is a decline in the duration of the bond)As Yield decreases, each successive price increase is greater (there is an increase in the duration of the bond)

DrakeDrake University

Fin 284Convexity

Generally the following can also be said:For a given return and maturity, the lower the coupon the greater the convexityFor a given return and modified duration, the lower the coupon the lower the convexity