drake drake university fin 284 futures markets fin 284 fixed income analysis

Post on 21-Dec-2015

229 views

TRANSCRIPT

DrakeDRAKE UNIVERSITY

Fin 284

Futures Markets

Fin 284Fixed Income Analysis

DrakeDrake University

Fin 284Derivatives

Basic DefinitionAny Asset whose value is based upon (or derived from) an underlying asset.The performance of the derivative is dependent upon the performance of the underlying asset.

Risk ManagementSince a derivatives performance is based on an underlying asset they can often be used to decrease the risk associated with changes in the spot price of an asset.

DrakeDrake University

Fin 284

Basic Types of Derivative Contracts

Forward ContractsAgreement between two parties to purchase or sell something at a later date at a prie agreed upon today

Futures ContractSame idea as a forward, but the contract trades on an exchange and the counter party is not set.

DrakeDrake University

Fin 284

Brief History of Derivatives Markets

1100’s Forward contracts were used by Flemish traders who gathered -- a letter de faire- forward contract specifying delivery at a later date 1600’s

Japan -- Cho-ai-mai (Rice Trade on Book) Essentially futures contracts on rice designed to manage the volatility in rice prices caused by weather, warfare and other risks.Netherlands -- formal futures markets developed to trade tulip bulbs in 1636Options also appeared in Amsterdam during the 1600’s

1863 -- Confederacy issued 20 year bonds denominated in French francs and convertible to cotton (a dual currency cotton indexed bond)

DrakeDrake University

Fin 284Brief History Continued.

Organized Exchanges in USChicago Board of TradeEstablished in 1848 to bring farmers and merchants together. Futures Contracts were first traded on the CBOT1865. Developed the first standard contract Chicago Mercantile ExchangeStarted as the Chicago Produce Exchange in 1874 for trade in perishable agricultural products. In 1919 it became the Chicago Mercantile Exchange (CME). Introduced a contract for S&P 500 futures in 1982. NYMEX 1872 KCBOT 1876

DrakeDrake University

Fin 284Other US Exchanges

NYBOTCoffee Sugar and Cocca ExchangeNew York Futures Exchange

Minneapolis Grain ExchangePhiladelphia Board of Trade

DrakeDrake University

Fin 284Payoff on Forward Contracts

Long PositionAgreeing to buy a specified amount (The Contract Size) of a given commodity or asset at a set point in time in the future (The Delivery Date) at a set price (The Delivery Price)

PayoffThe payoff will depend upon the spot price at the delivery date.Payoff = Spot Price – Delivery Price

DrakeDrake University

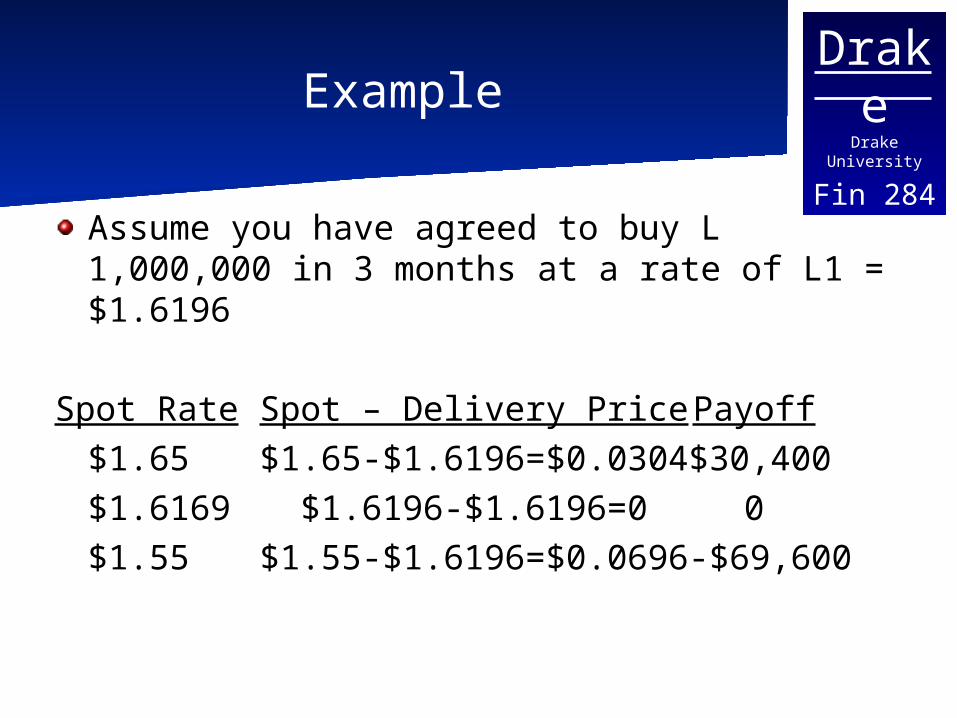

Fin 284Example

Assume you have agreed to buy L 1,000,000 in 3 months at a rate of L1 = $1.6196

Spot Rate Spot – Delivery Price Payoff$1.65 $1.65-$1.6196=$0.0304$30,400

$1.6169 $1.6196-$1.6196=0 0$1.55 $1.55-$1.6196=$0.0696-$69,600

DrakeDrake University

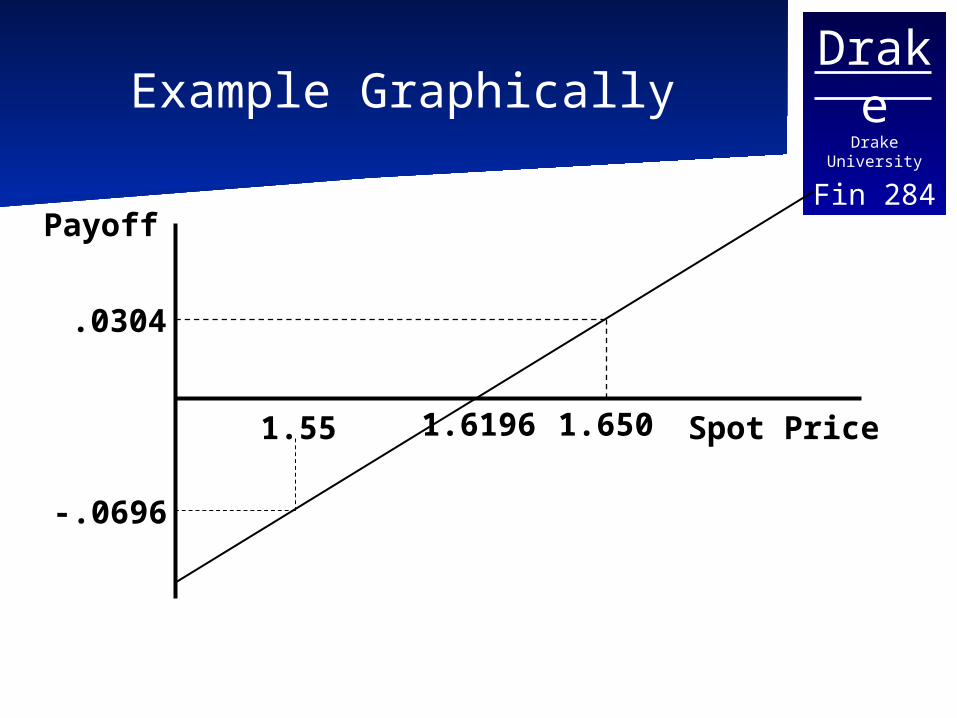

Fin 284Example Graphically

Spot Price

Payoff

1.55 1.6196 1.650

.0304

-.0696

DrakeDrake University

Fin 284Payoff: Short Position

Agreeing to sell a specified amount (The Contract Size) of a given commodity or asset at a point of time in the future (The Delivery Date) at a set price (The Delivery Price).Payoff on Short position

Since the position is profitable when the price declines the payoff becomes:Payoff = The Delivery Price – The Spot Price

DrakeDrake University

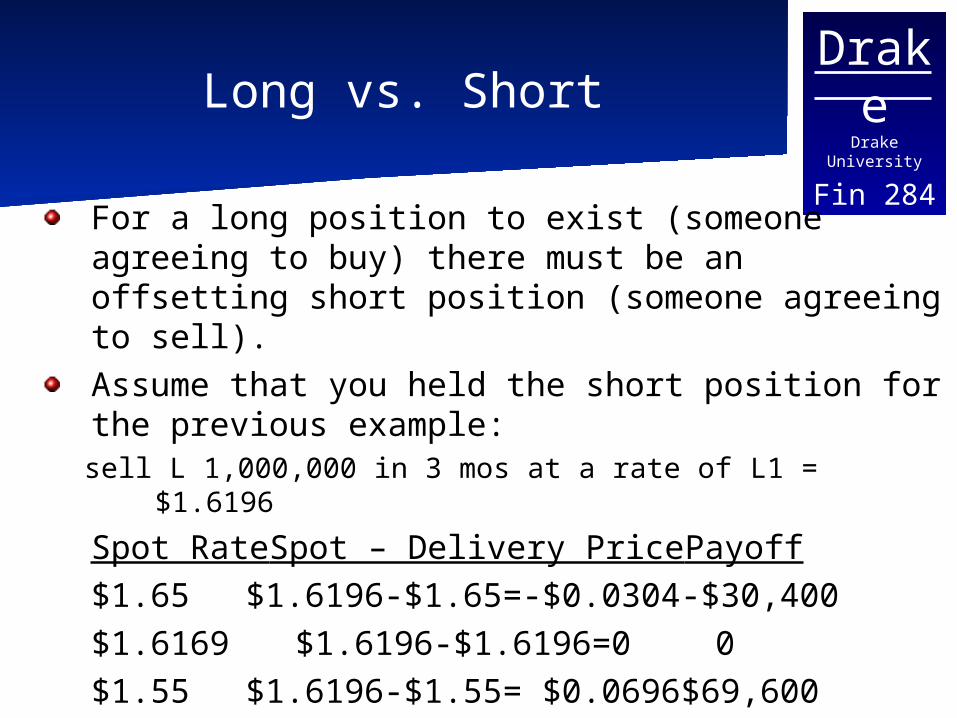

Fin 284Long vs. Short

For a long position to exist (someone agreeing to buy) there must be an offsetting short position (someone agreeing to sell).Assume that you held the short position for the previous example:sell L 1,000,000 in 3 mos at a rate of L1 = $1.6196

Spot Rate Spot – Delivery Price Payoff$1.65 $1.6196-$1.65=-$0.0304-$30,400$1.6169 $1.6196-$1.6196=0 0$1.55 $1.6196-$1.55= $0.0696$69,600

DrakeDrake University

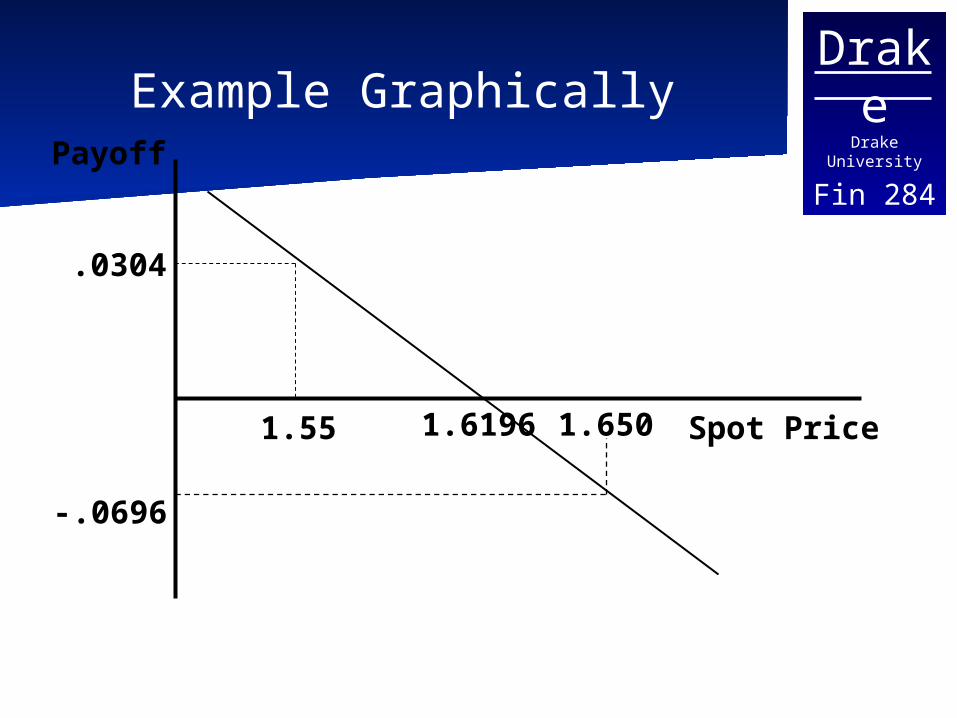

Fin 284Example Graphically

Spot Price

Payoff

1.55 1.6196 1.650

.0304

-.0696

DrakeDrake University

Fin 284Contract Goals

The goal of the contract is to decrease risk, assume that you had to pay L1,000,000 in 3 months for the shipment of an input. You are afraid that the $ price will increase and you will pay a higher price. Similarly the other party may be afraid that the $ price will decrease (maybe they are receiving a payment in 3 months)

DrakeDrake University

Fin 284

Determining the delivery price

The delivery price will be determined by the participants expectations about the future price and their willingness to enter into the contract. (Today’s spot price most likely does not equal the delivery price). What else should be considered?

They should both also consider the time value of money

DrakeDrake University

Fin 284

Future and Forward contracts

Both Futures and Forward contracts are contracts entered into by two parties who agree to buy and sell a given commodity or asset (for example a T- Bill) at a specified point of time in the future at a set price.

DrakeDrake University

Fin 284Futures vs. Forwards

Future contracts are traded on an exchange, Forward contracts are privately negotiated over-the-counter arrangements between two parties.Both set a price to be paid in the future for a specified contract.Forward Contracts are subject to counter party default risk, The futures exchange attempts to limit or eliminate the amount of counter party default risk.

DrakeDrake University

Fin 284

Other Forward Contract Risks

One goal of the negotiation is to specify exactly the type, quantity, and means of delivery of the underlying asset. The chance that an asset different than anticipated might be delivered should be eliminated by the contract.Futures contracts attempt to account for this problem via standardization of the contract.

DrakeDrake University

Fin 284Futures Contracts

Long Position: Agreeing to purchase a specified amount of a given commodity or asset at a point in time in the future at a set price (the futures price)Short Position: Agreeing to sell a specified amount of a given commodity or asset at a point of time in the future for a set price (the futures price).

DrakeDrake University

Fin 284

Standardization of Futures Contracts

To promote confidence in the system and eliminate counter party default risk, future contracts are highly standardized.

DrakeDrake University

Fin 284

Specifications of Futures Contract

The AssetThe Contract SizeDelivery ArrangementsDelivery MonthsPrice QuotesPrice LimitsPosition Limits

DrakeDrake University

Fin 284Contract Specifications

AssetQuality and type of asset are specified to guarantee specific product is delivered.

Contract SizeThe amount of asset that is to be delivered for one contract

Delivery ArrangementsMore important for commodities than financial assets. Specify how delivery occurs and location.

DrakeDrake University

Fin 284Contract Specifications

Delivery MonthsWhen delivery will occur (and during what part of the month delivery can occur)

Price QuotesContract must specify the units for the price quote (1/32 of a dollar etc) Also implicitly establishes the minimum fluctuation for the price of the contract.

DrakeDrake University

Fin 284Contract Specifications

Price LimitsDesigned to add stability to the market, limits on the maximum fluctuation in price that can occur during a trading day.

Position LimitsLimits the number of contracts that can be entered into by a speculator.

Speculator –attempting to profit from a movement in the marketHedger – attempting to offset an underlying spot position.

DrakeDrake University

Fin 284

Does Delivery need to take place?

No – most contracts will be closed out.Closing out a contract is simply taking the opposite (short if you are long or vice versa) position. The change in the futures price will be your gain or loss.With a futures contract your counter party does not remain the same. It does not matter who takes the opposite position. This is not the case for a forward contract.

DrakeDrake University

Fin 284

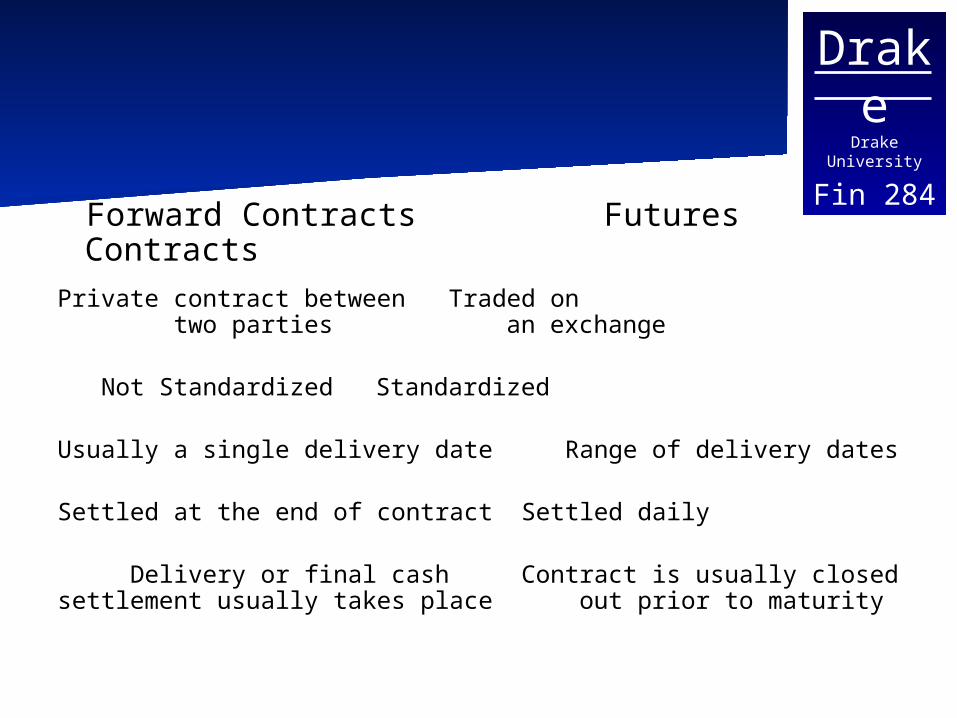

Forward Contracts Futures ContractsPrivate contract between Traded on two parties an exchange

Not Standardized Standardized

Usually a single delivery date Range of delivery dates

Settled at the end of contract Settled daily

Delivery or final cash Contract is usually closedsettlement usually takes place out prior to maturity

DrakeDrake University

Fin 284Important Terminology

Open InterestThe number of contracts that are currently open (both a short and long position exist).

What happens to open interest if a new long position is taken out?

It could IncreaseIt could decreaseIt might not change.The answer depends on whether both the long and short positions are new, or closing out or one of each.

DrakeDrake University

Fin 284Margin Requirements

To limit counter party default risk, the futures exchange requires participants to place funds in a margin account when the contract is taken out.Some Terminology:

Initial Margin: The original amount deposited in the margin accountMaintenance margin: The amount that must remain in the margin accountMargin call – Notice that the margin account has dropped below the maintenance margin, more money must be added to the account

DrakeDrake University

Fin 284Margin Example

Example:An investor has taken a long position in gold (agreed to buy gold at some date in the future).Assume that the agreement is for 2 gold contracts each contract consists of 100 ounces of gold. The futures price is $400 per ounce. This implies that the participant would need 200*400 = $80,000 to purchase gold at the expiration of the contract.

DrakeDrake University

Fin 284Margin Example

If the futures price for gold decreases to $398, the investor would suffer a loss if the contract is closed out. The loss would total (400 - 398)200 = $400. The fear is that if at the expiration of the contract the price is 398, the participant will not honor the contract since it would result in a loss of $400.

DrakeDrake University

Fin 284Margin Example

To counteract this the investor is ask to put a sum of money into a margin account lets assume $2,000 per contract or $4000 total. When the futures price declines the loss of $400 is taken from the margin account of the investor and given to a participant that took a short position.

DrakeDrake University

Fin 284Margin Example

The value of the contract is marked to market each day, and the margin account is adjusted. The margin is effectively guaranteeing that the position is covered.If the level of the account falls below the maintenance margin the investor is required to put more funds into the account this is known as a margin call. The extra funds provided are the variation margin, if they are not provided the broker will close out the account.

DrakeDrake University

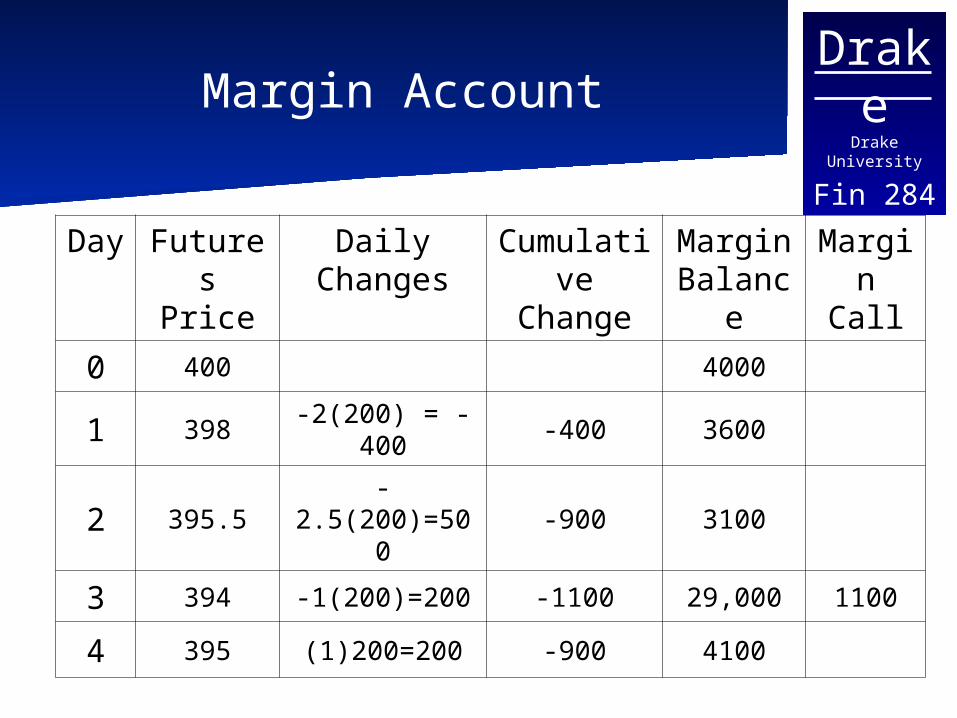

Fin 284Margin Account

Day

Futures Price

Daily Changes

Cumulative

Change

Margin Balanc

e

Margin Call

0 400 4000

1 398-2(200) = -

400-400 3600

2 395.5-

2.5(200)=500-900 3100

3 394 -1(200)=200 -1100 29,000 1100

4 395 (1)200=200 -900 4100

DrakeDrake University

Fin 284Note:

You can withdraw any amount above the initial marginMost accounts pay a money market rate of interestSome accounts allow deposit of securities, but valued at less than face value. (treasures valued at 90% other at 50%)

DrakeDrake University

Fin 284Role of Clearinghouse

The clearinghouse serves as an intermediary that guarantees the contract. The clearinghouse is an independent corporation whose shareholders are comprised of its member firms. Each member firm maintains a margin account (similar to the traders) with the clearinghouse. In essence the clearinghouse guarantees the long and the short trader that the other side will honor the contract

DrakeDrake University

Fin 284Patterns of Futures Prices

Basis = Spot Price – Futures PriceThe Basis moves toward zero as the spot price matures.This eliminates arbitrage possibilities.If futures is greater than spot, you could enter short in the futures market and make a profit by buying in the spot and then delivering in futuresSince everyone will attempt this demand for short positions increases and futures price decreases, also spot price would increase….

DrakeDrake University

Fin 284Other patterns

Normal Market: The futures price increase as the time to maturity increasesInverted Market: the futures price is a decreasing function of the time to maturityComparing the futures price to the expected future spot price.Normal Backwardation: The futures price is below the expected future spot price.Contango: The futures price is above the expected futures price.

DrakeDrake University

Fin 284Other Patterns

The Futures Price over timeNormal Market: The futures price increase as the time to maturity increasesInverted Market: the futures price is a decreasing function of the time to maturity

Comparing the futures price to the expected future spot price.

Normal Backwardation: The futures price is below the expected future spot price.Contango: The futures price is above the expected futures price.

DrakeDrake University

Fin 284

Theoretical Explanations of Backwardation

Keynes and Hicks-- Speculators will only enter the market if they expect to have a positive profit. If more speculators are holding a long position, it implies that the futures price is less than the expected spot price

A second explanation can be found by looking at the relationship between risk and return in the market. If thee is systematic risk involved with holding the security then the investor should be compensated for accepting the risk (nonsystematic risk can be diversified away).

DrakeDrake University

Fin 284

Theoretical Pricing of Futures Contracts

The theoretical price Is based upon the elimination of arbitrage opportunities.Start with a simple example:

Assume transaction costs are zeroAssume that storage costs are zero

You have a choice today of purchasing or selling a given asset or entering into a contract to buy or sell it in the future.

DrakeDrake University

Fin 284Theoretical Price

Assume you want to own the asset at a given point in time in the future, You can enter into a long futures position or buy the asset today and hold on to it. If you enter into the futures contract you can invest your cash today and earn interest ( r)

DrakeDrake University

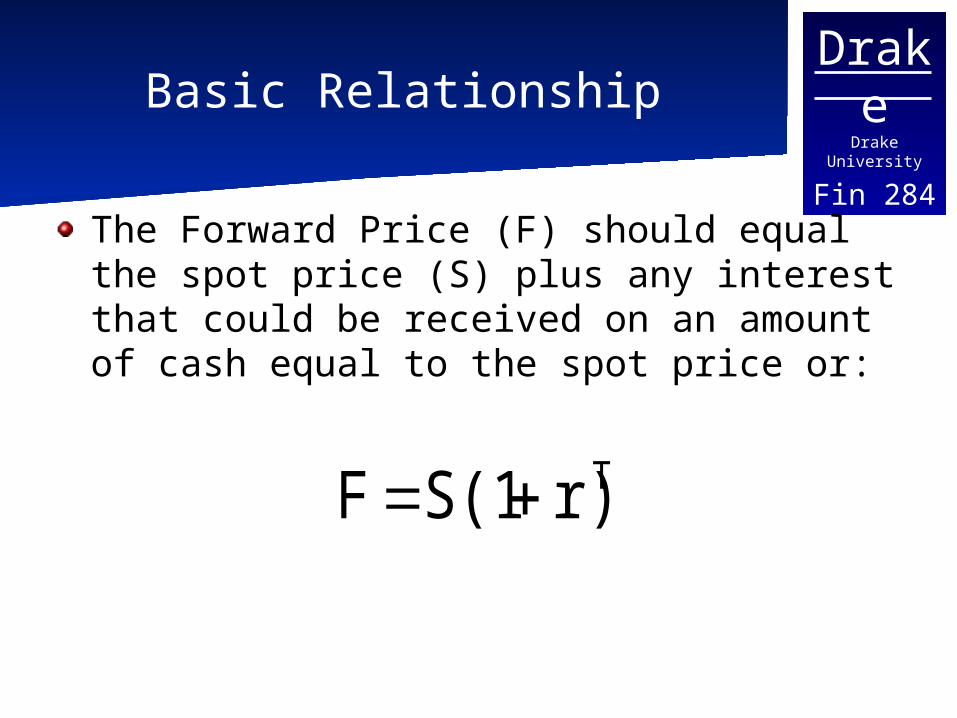

Fin 284Basic Relationship

The Forward Price (F) should equal the spot price (S) plus any interest that could be received on an amount of cash equal to the spot price or:

Tr)S(1F

DrakeDrake University

Fin 284Eliminating Arbitrage

If the forward price is greater than the spot plus interest an arbitrage opportunity exists.

Borrow to buy the underlying asset in the spot market and take a short position in the futures contract.

Tr)S(1F

DrakeDrake University

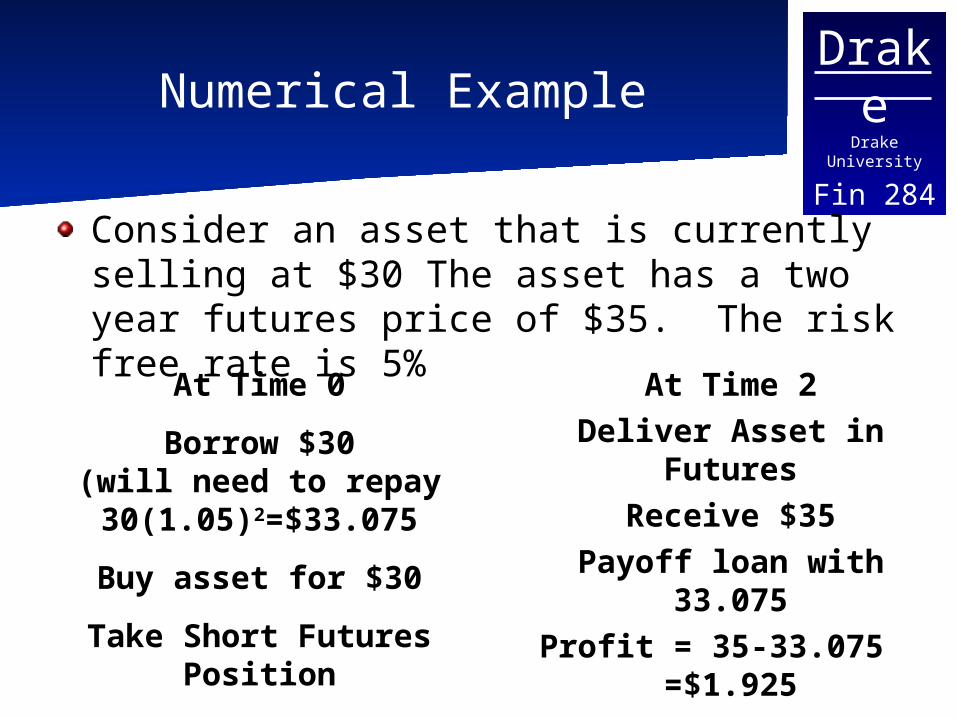

Fin 284Numerical Example

Consider an asset that is currently selling at $30 The asset has a two year futures price of $35. The risk free rate is 5%

At Time 0

Borrow $30(will need to repay 30(1.05)2=$33.075

Buy asset for $30

Take Short Futures Position

At Time 2Deliver Asset in Futures

Receive $35Payoff loan with 33.075

Profit = 35-33.075 =$1.925

DrakeDrake University

Fin 284Example con’t

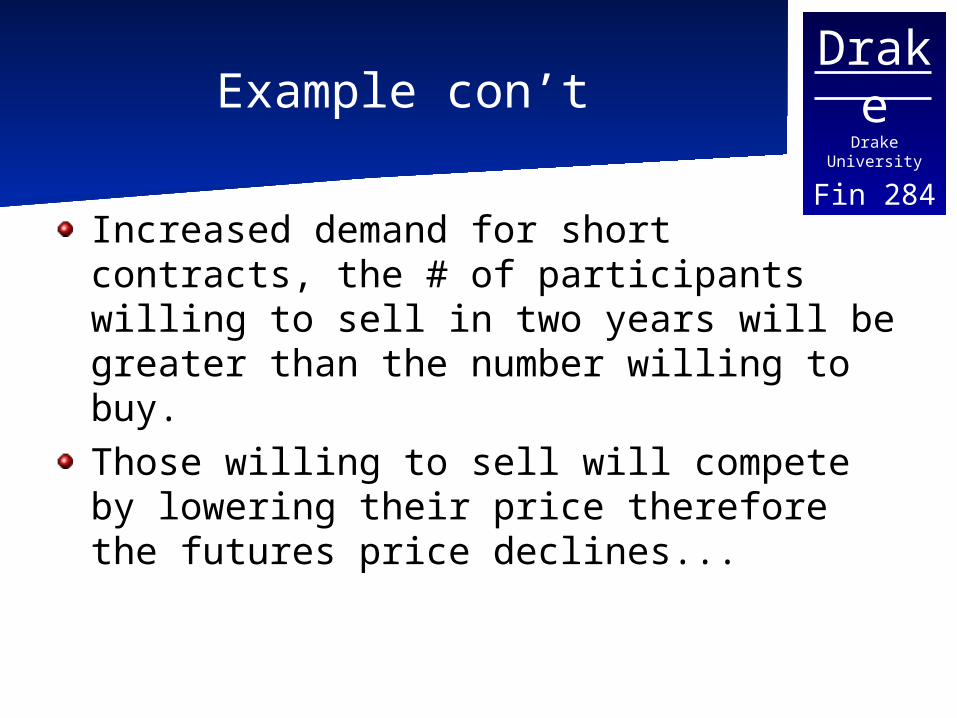

Increased demand for short contracts, the # of participants willing to sell in two years will be greater than the number willing to buy. Those willing to sell will compete by lowering their price therefore the futures price declines...

DrakeDrake University

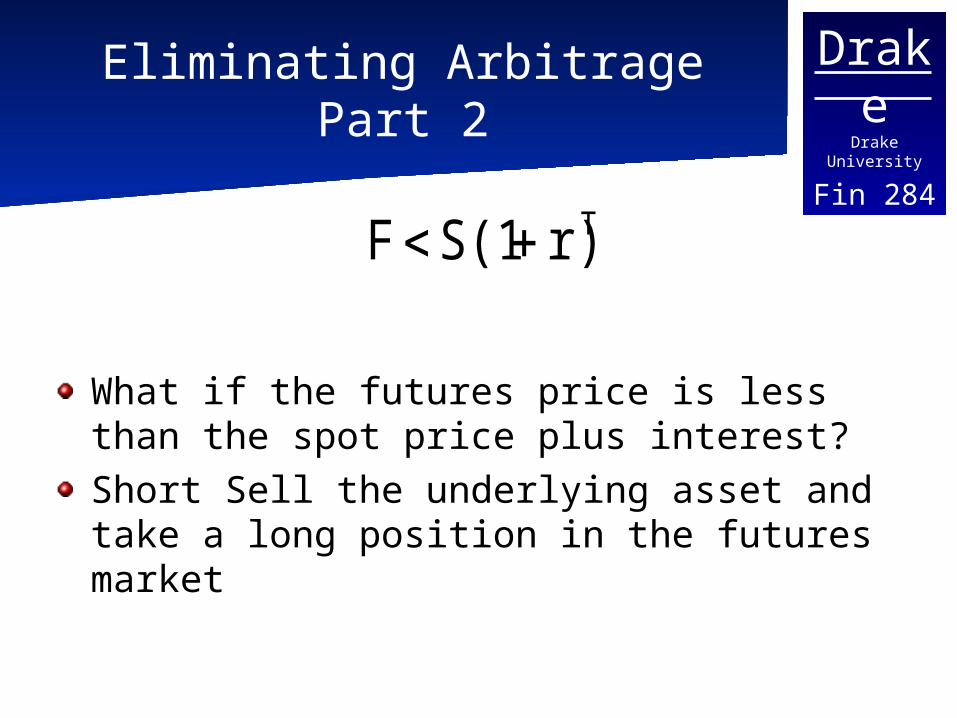

Fin 284Eliminating Arbitrage Part 2

What if the futures price is less than the spot price plus interest?Short Sell the underlying asset and take a long position in the futures market

Tr)S(1F

DrakeDrake University

Fin 284Numerical example

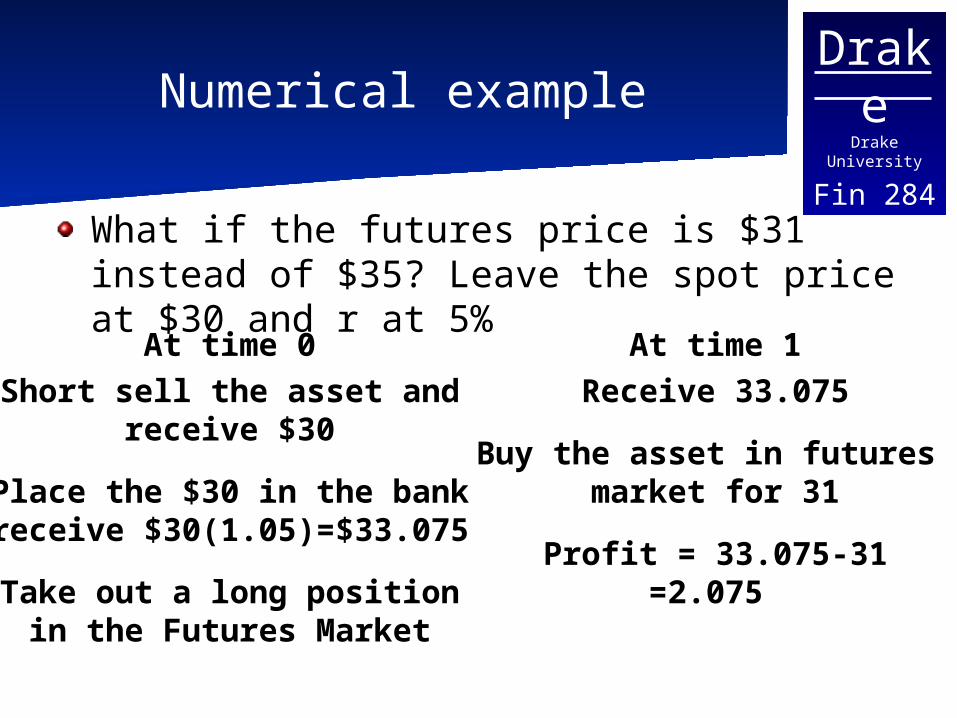

What if the futures price is $31 instead of $35? Leave the spot price at $30 and r at 5%

At time 0Short sell the asset and

receive $30

Place the $30 in the bankreceive $30(1.05)=$33.075

Take out a long positionin the Futures Market

At time 1Receive 33.075

Buy the asset in futures market for 31

Profit = 33.075-31=2.075

DrakeDrake University

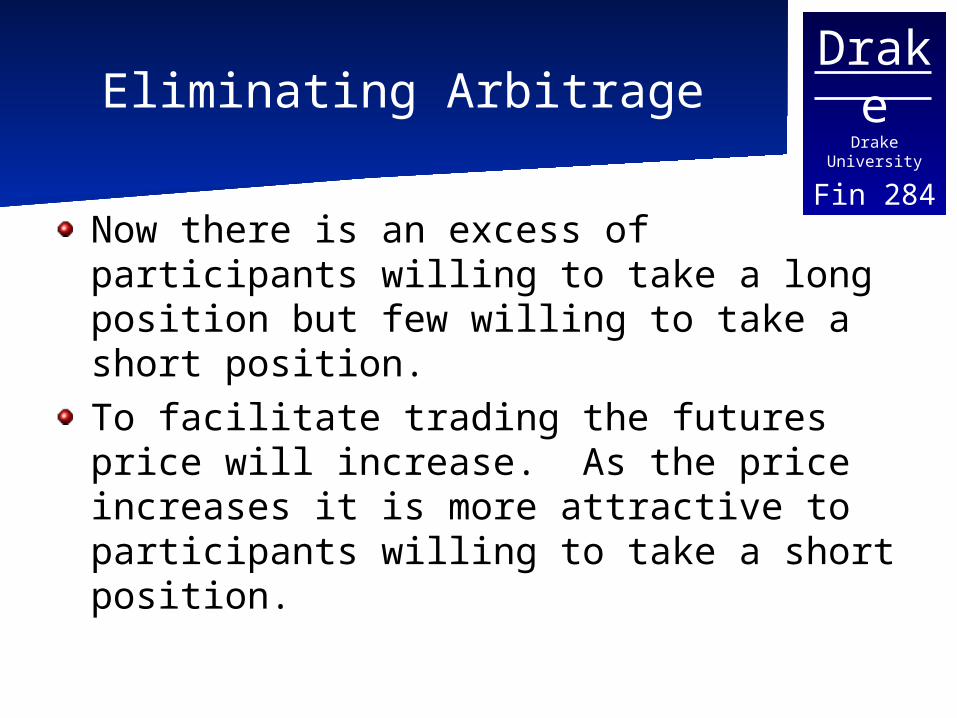

Fin 284Eliminating Arbitrage

Now there is an excess of participants willing to take a long position but few willing to take a short position. To facilitate trading the futures price will increase. As the price increases it is more attractive to participants willing to take a short position.

DrakeDrake University

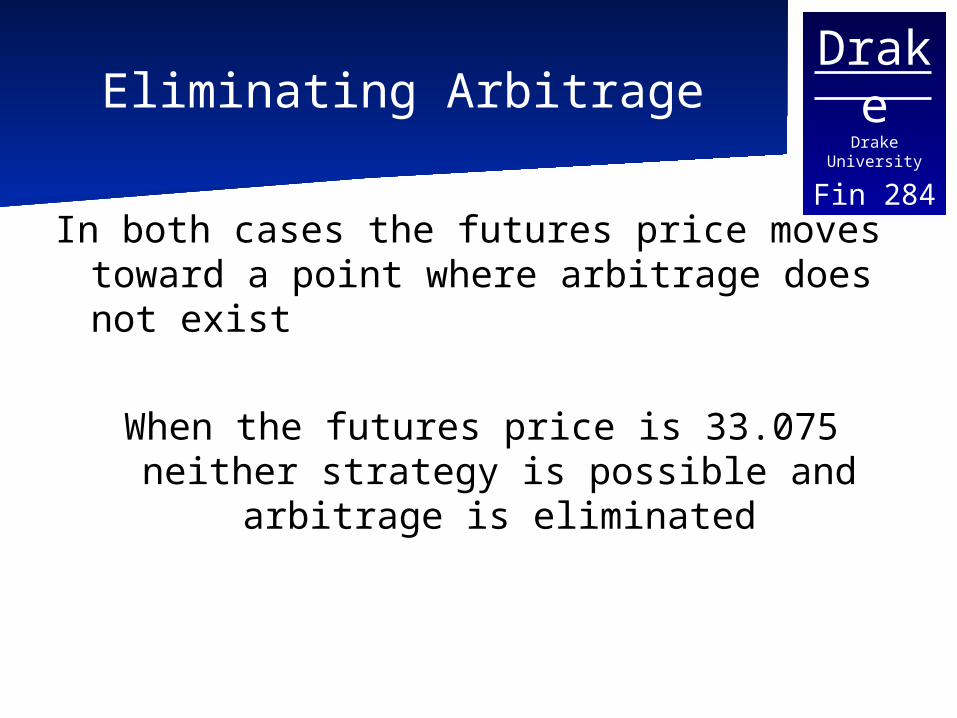

Fin 284Eliminating Arbitrage

In both cases the futures price moves toward a point where arbitrage does not exist

When the futures price is 33.075 neither strategy is possible and arbitrage is

eliminated

DrakeDrake University

Fin 284

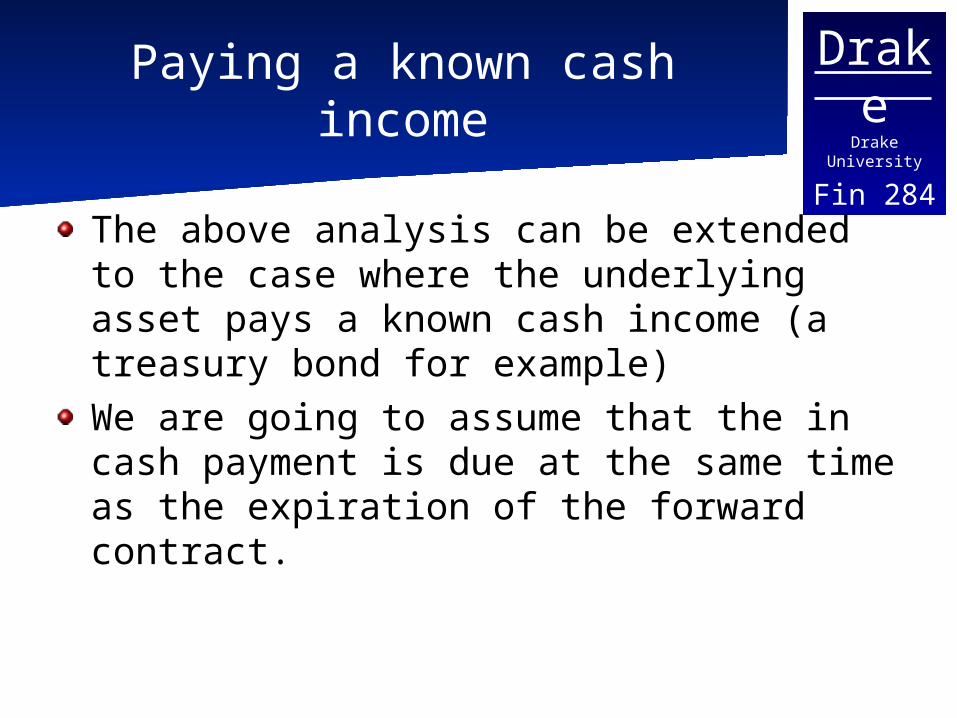

Paying a known cash income

The above analysis can be extended to the case where the underlying asset pays a known cash income (a treasury bond for example)We are going to assume that the in cash payment is due at the same time as the expiration of the forward contract.

DrakeDrake University

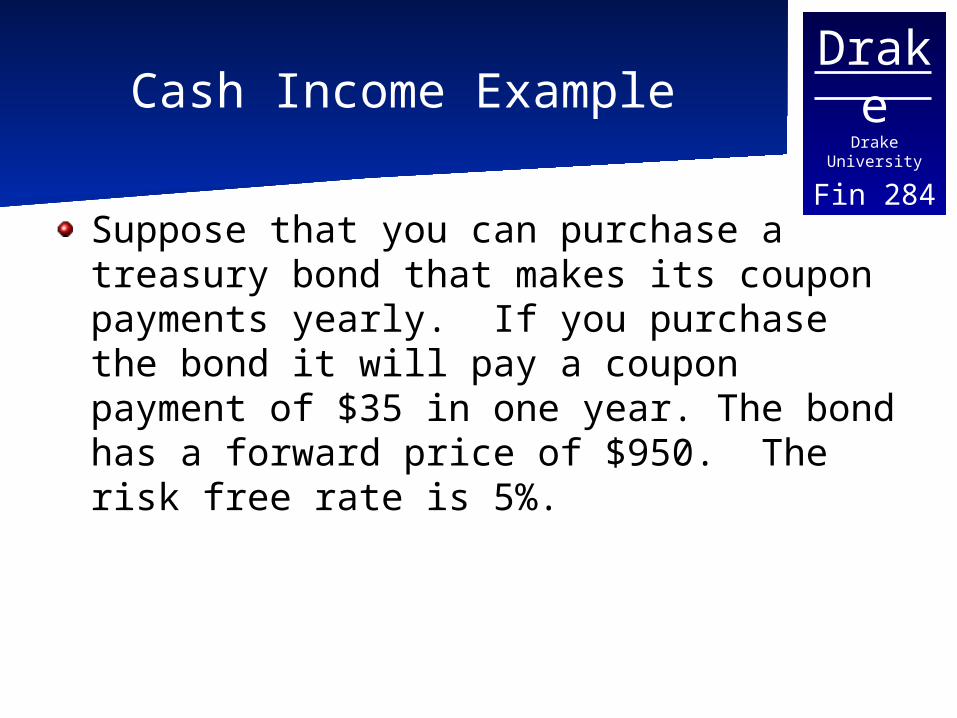

Fin 284Cash Income Example

Suppose that you can purchase a treasury bond that makes its coupon payments yearly. If you purchase the bond it will pay a coupon payment of $35 in one year. The bond has a forward price of $950. The risk free rate is 5%.

DrakeDrake University

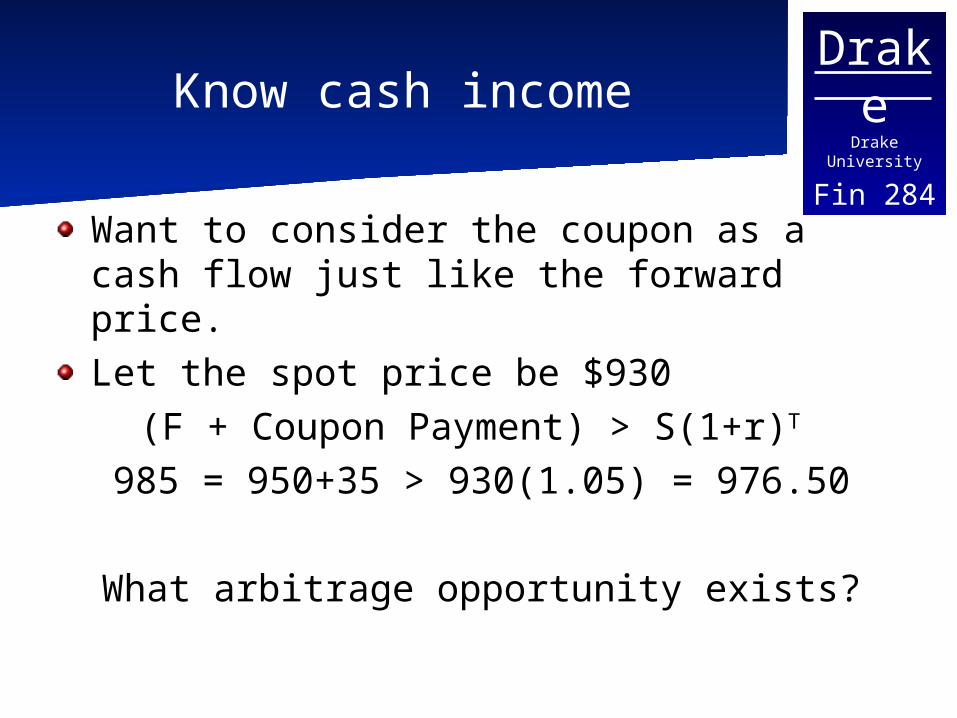

Fin 284Know cash income

Want to consider the coupon as a cash flow just like the forward price.Let the spot price be $930

(F + Coupon Payment) > S(1+r)T 985 = 950+35 > 930(1.05) = 976.50

What arbitrage opportunity exists?

DrakeDrake University

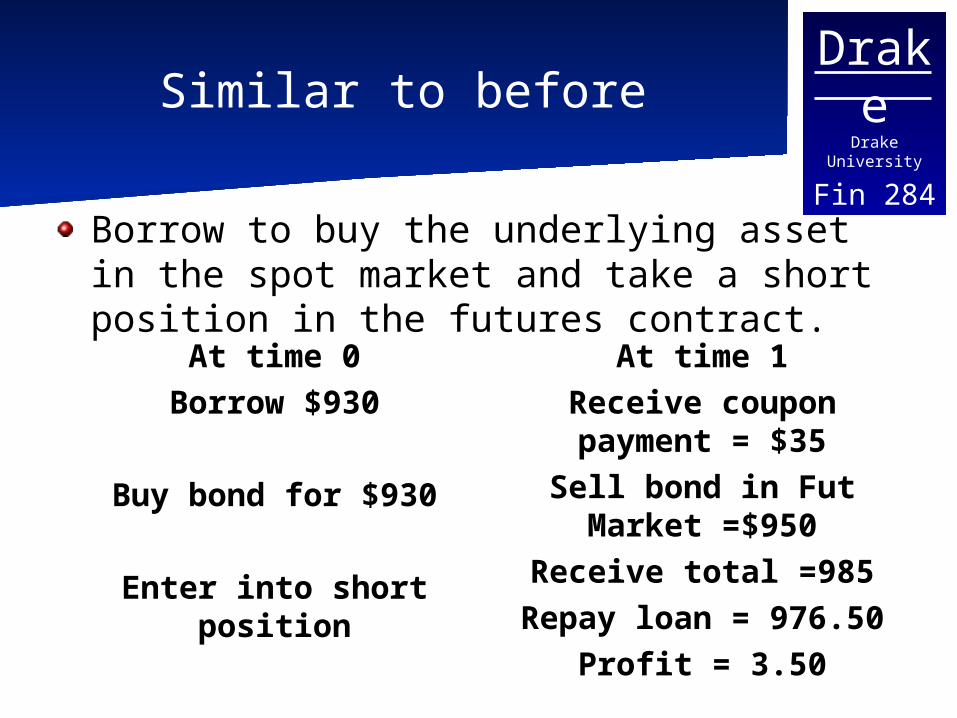

Fin 284Similar to before

Borrow to buy the underlying asset in the spot market and take a short position in the futures contract.

At time 0Borrow $930

Buy bond for $930

Enter into short position

At time 1Receive coupon payment = $35Sell bond in Fut Market =$950

Receive total =985Repay loan = 976.50

Profit = 3.50

DrakeDrake University

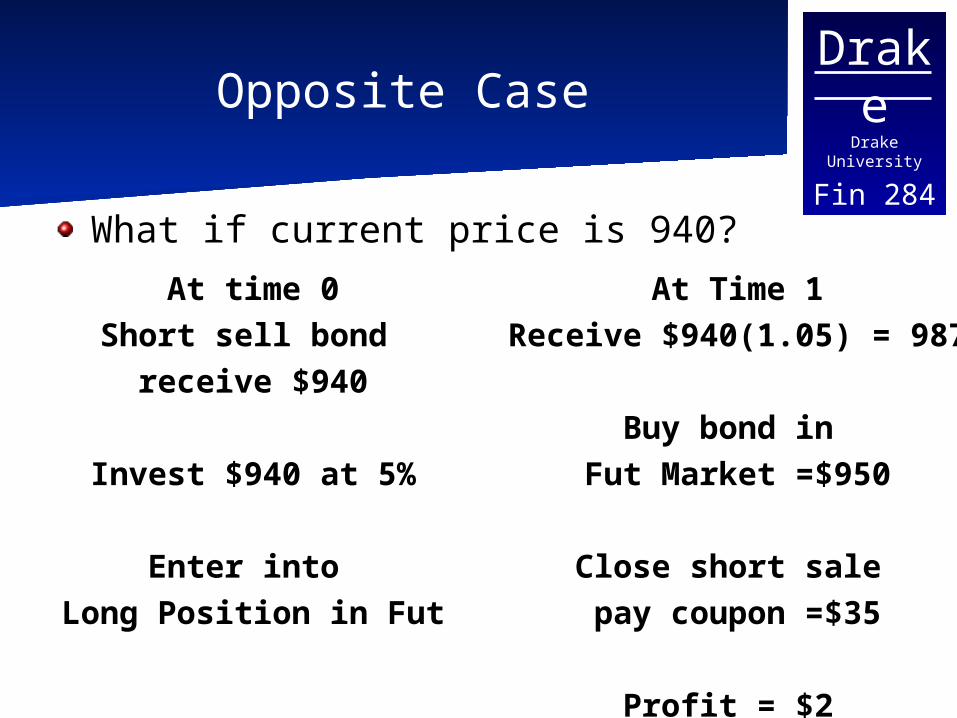

Fin 284Opposite Case

What if current price is 940?

At time 0Short sell bond

receive $940

Invest $940 at 5%

Enter into Long Position in Fut

At Time 1Receive $940(1.05) = 987

Buy bond in Fut Market =$950

Close short sale pay coupon =$35

Profit = $2

DrakeDrake University

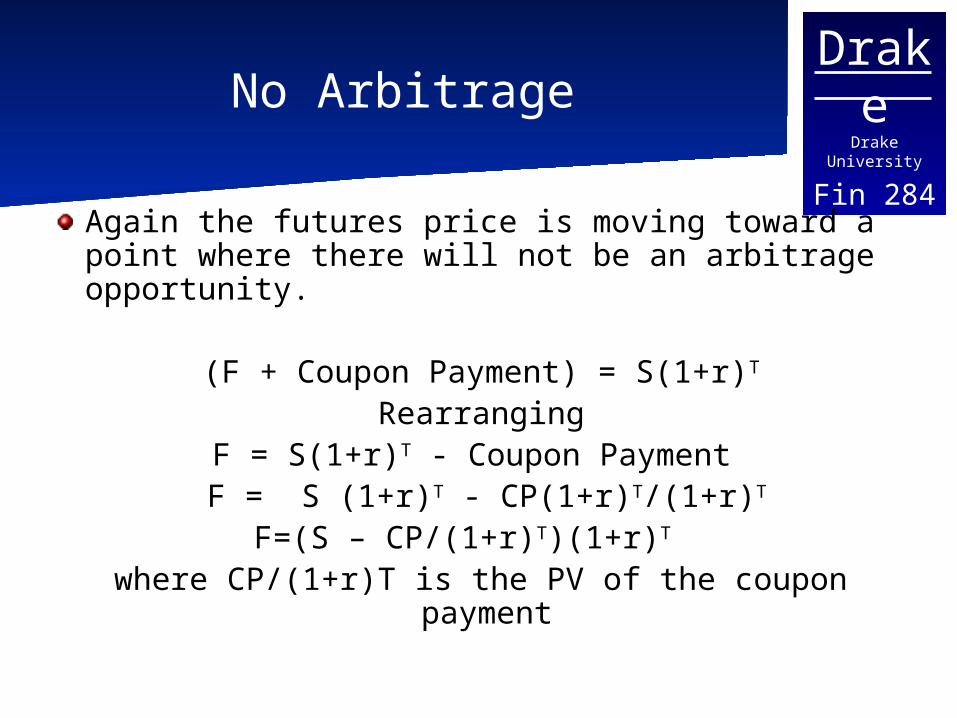

Fin 284No Arbitrage

Again the futures price is moving toward a point where there will not be an arbitrage opportunity.

(F + Coupon Payment) = S(1+r)T

RearrangingF = S(1+r)T - Coupon Payment F = S (1+r)T - CP(1+r)T/(1+r)T

F=(S – CP/(1+r)T)(1+r)T where CP/(1+r)T is the PV of the coupon payment

DrakeDrake University

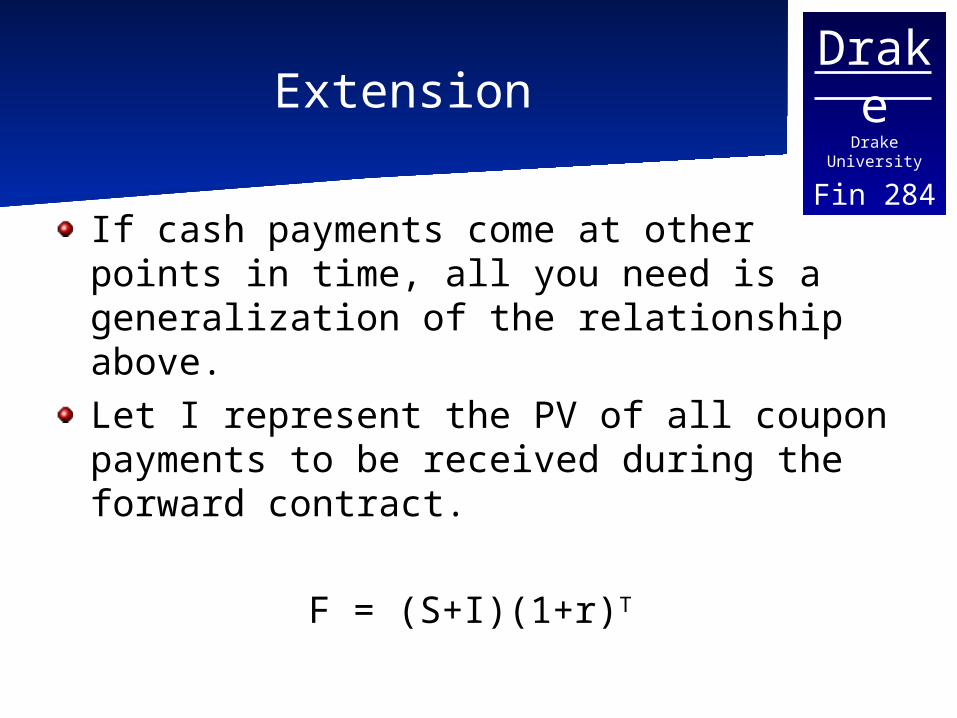

Fin 284Extension

If cash payments come at other points in time, all you need is a generalization of the relationship above.Let I represent the PV of all coupon payments to be received during the forward contract.

F = (S+I)(1+r)T

DrakeDrake University

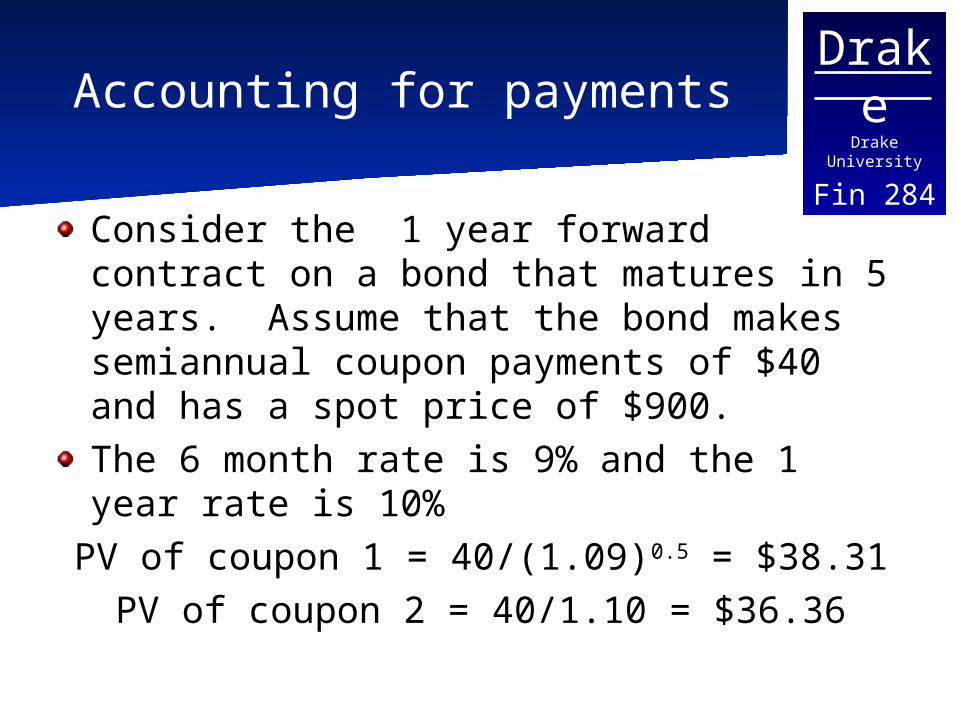

Fin 284Accounting for payments

Consider the 1 year forward contract on a bond that matures in 5 years. Assume that the bond makes semiannual coupon payments of $40 and has a spot price of $900.The 6 month rate is 9% and the 1 year rate is 10%

PV of coupon 1 = 40/(1.09)0.5 = $38.31PV of coupon 2 = 40/1.10 = $36.36

DrakeDrake University

Fin 284

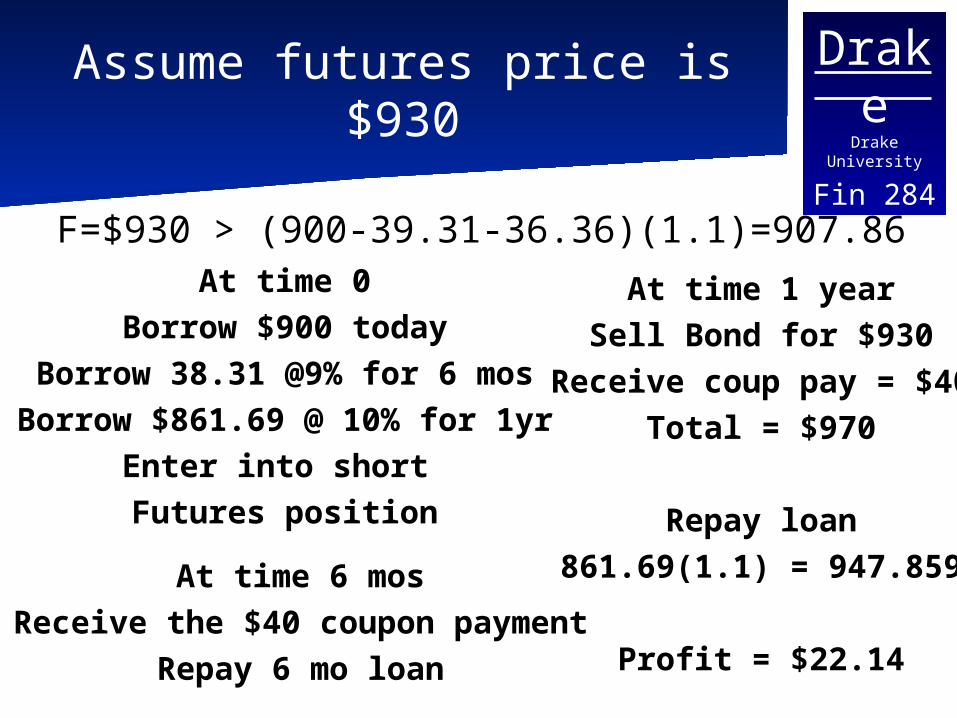

Assume futures price is $930

F=$930 > (900-39.31-36.36)(1.1)=907.86At time 0

Borrow $900 todayBorrow 38.31 @9% for 6 mos

Borrow $861.69 @ 10% for 1yrEnter into short Futures position

At time 6 mosReceive the $40 coupon payment

Repay 6 mo loan

At time 1 yearSell Bond for $930

Receive coup pay = $40Total = $970

Repay loan861.69(1.1) = 947.859

Profit = $22.14

DrakeDrake University

Fin 284Extensions

If the futures price was less than the spot minus the PV of the coupons carried forward an argument similar to the earlier ones could have also been madeA final case is if the income stream pays a known dividend income.

DrakeDrake University

Fin 284Dividend income

Assume that the asset pays a return of q in the future based on the current price of the asset. The equilibrium is then

F = S(1+r)T/(1+q)T

DrakeDrake University

Fin 284Storage Costs?

If the asset has a storage cost (more important for commodities than financial assets), it can be viewed as a negative cash income, the no arbitrage condition would be:

F = (S+U)(1+r)T

Where U represents the present value of all costs.

DrakeDrake University

Fin 284Generalization

Thank of the net amount of any of the possible costs, income received, and interest as the cost of carrying the spot position to the future. It is the cost of holding the spot position instead of the future position.The equilibrium condition is then simply

F = (S+C)(1+rc)T

C is any cash income / costs and rc is net interest expense

DrakeDrake University

Fin 284Treasury Bond Future Contracts

Traded on the CBOT10 year Treasury note future

Delivers 6.5 to 10 year maturity treasury notes (maturity form the first day of the delivery month).

DrakeDrake University

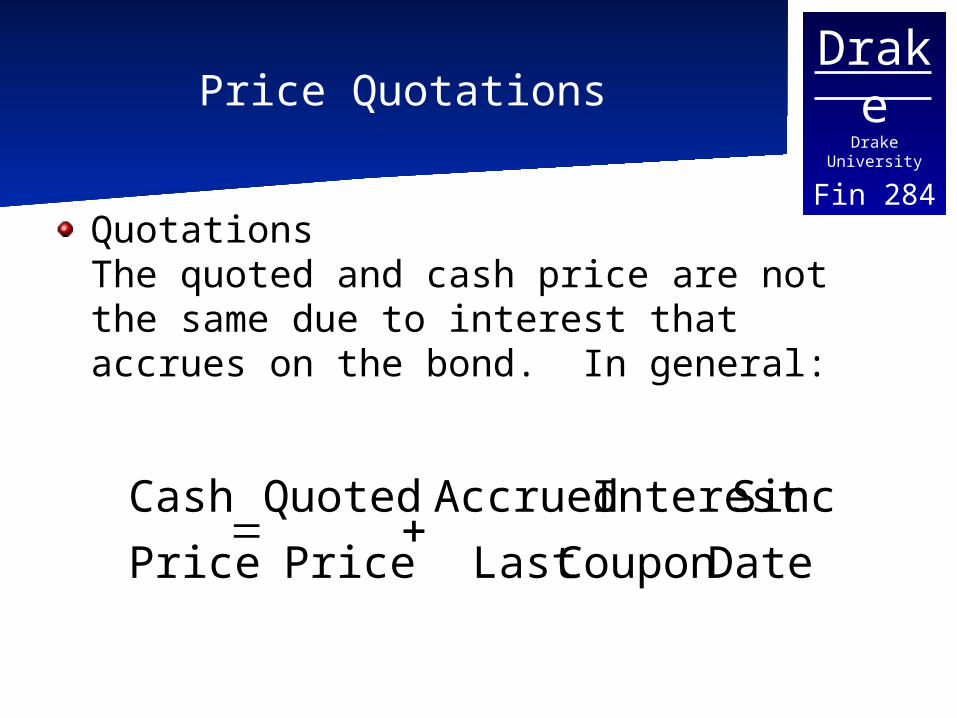

Fin 284Price Quotations

QuotationsThe quoted and cash price are not the same due to interest that accrues on the bond. In general:

DateCoupon Last

SinceInterest Accrued

Price

Quoted

Price

Cash

DrakeDrake University

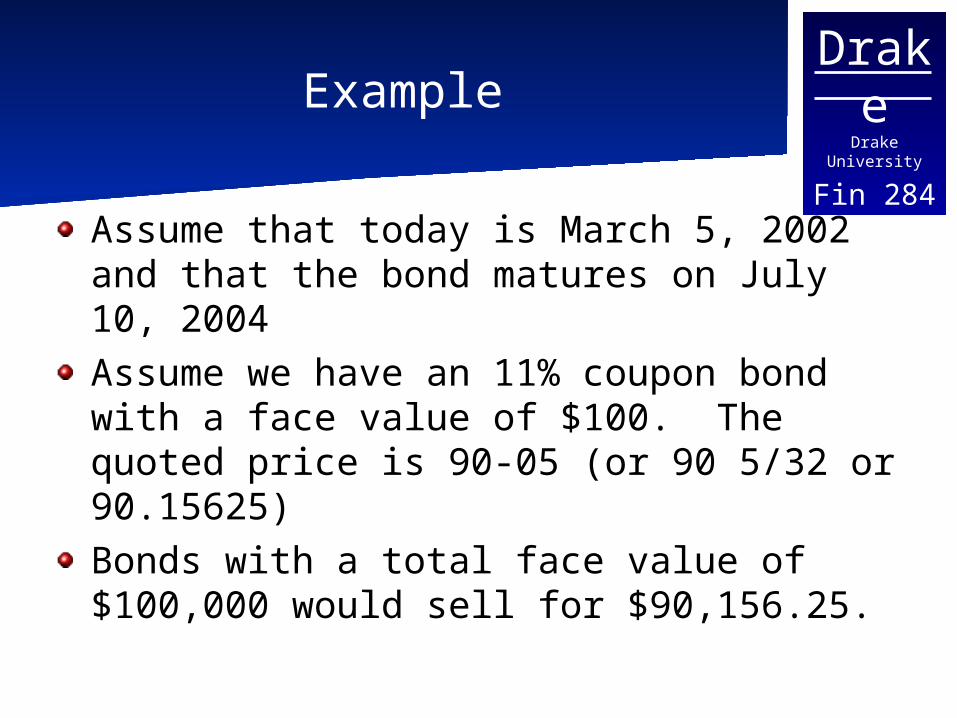

Fin 284Example

Assume that today is March 5, 2002 and that the bond matures on July 10, 2004 Assume we have an 11% coupon bond with a face value of $100. The quoted price is 90-05 (or 90 5/32 or 90.15625)Bonds with a total face value of $100,000 would sell for $90,156.25.

DrakeDrake University

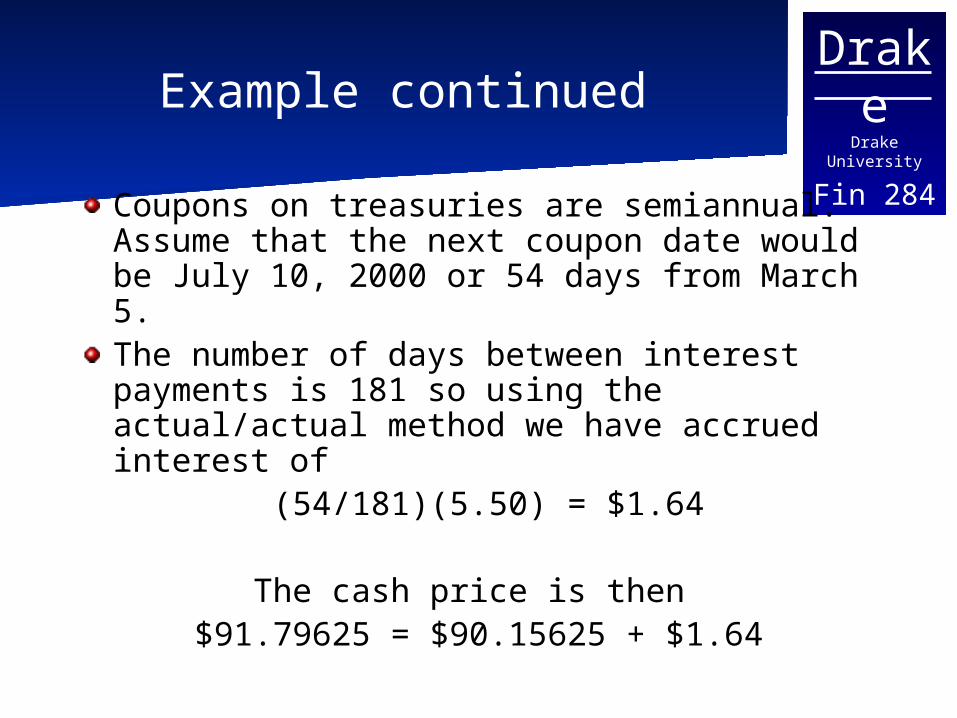

Fin 284Example continued

Coupons on treasuries are semiannual. Assume that the next coupon date would be July 10, 2000 or 54 days from March 5.The number of days between interest payments is 181 so using the actual/actual method we have accrued interest of

(54/181)(5.50) = $1.64

The cash price is then $91.79625 = $90.15625 + $1.64

DrakeDrake University

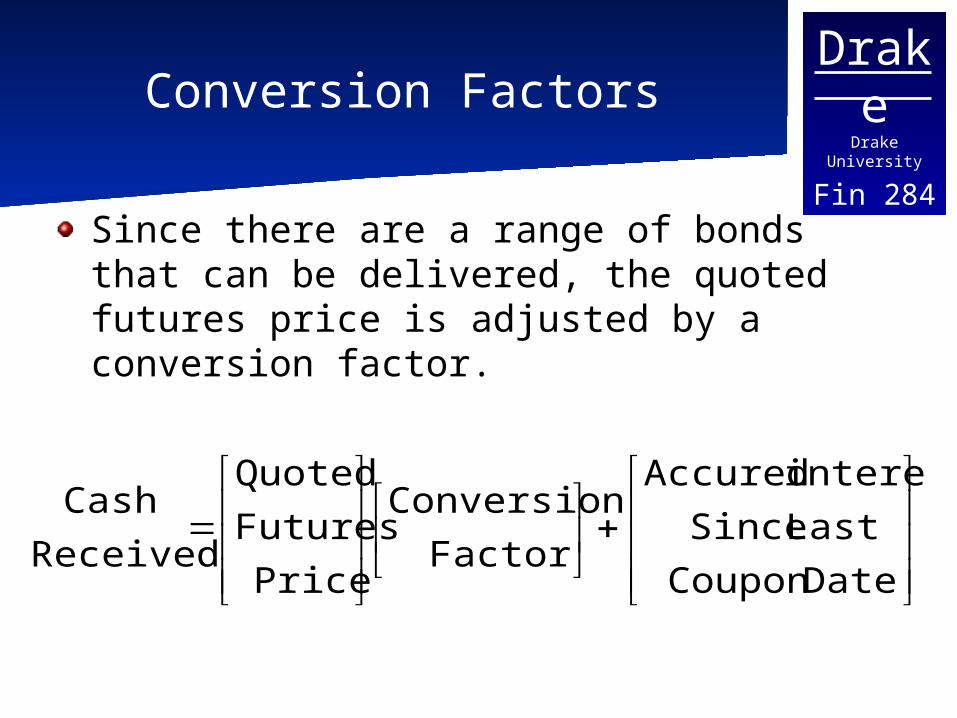

Fin 284Conversion Factors

Since there are a range of bonds that can be delivered, the quoted futures price is adjusted by a conversion factor.

DateCoupon

Last Since

interest Accured

Factor

Conversion

Price

Futures

Quoted

Received

Cash

DrakeDrake University

Fin 284Price based upon 6% YTM

The conversion factor is based off an assumption of a flat yield curve of 6% (that interest rates for all maturities equals 6%). By comparing the value of the bond to the face value, the CBOT produces a table of conversion factors.

DrakeDrake University

Fin 284

Conversion Factor Continued

The maturity of the bond is rounded down to the nearest three months.If the bond lasts for a period divisible by 6 months the first coupon payment is assumed to be paid in six months. (A bond with 10 years and 2 months would be assumed to have 10 years left to maturity)

DrakeDrake University

Fin 284Conversion Factor continued

If the bond does not round to an exact six months the first coupon is assumed to be paid in three months and accrued interest is subtracted. A bond with 14 years and 4 months to maturity would be treated as if it had 14 years and three months left to maturity

DrakeDrake University

Fin 284Example 1

14% coupon bond with 20 years and two months to maturityAssuming a 100 face value the value of the bond would equal the price valued at 6%:

The conversion factor is then 1.92459/100 = 1.92459

192.459 )03.(1

100

)03.(1

17 V

40

40

1ttBond

DrakeDrake University

Fin 284Example 2

What if the bond had 18 years and four months left to maturity? The bond would be considered to have 18 years and three months left to maturity with the first payment due in three months.Finding the value of the bond three months from today

329.187 )03.(1

100

)03.(1

17 V 36

36

1ttBond

DrakeDrake University

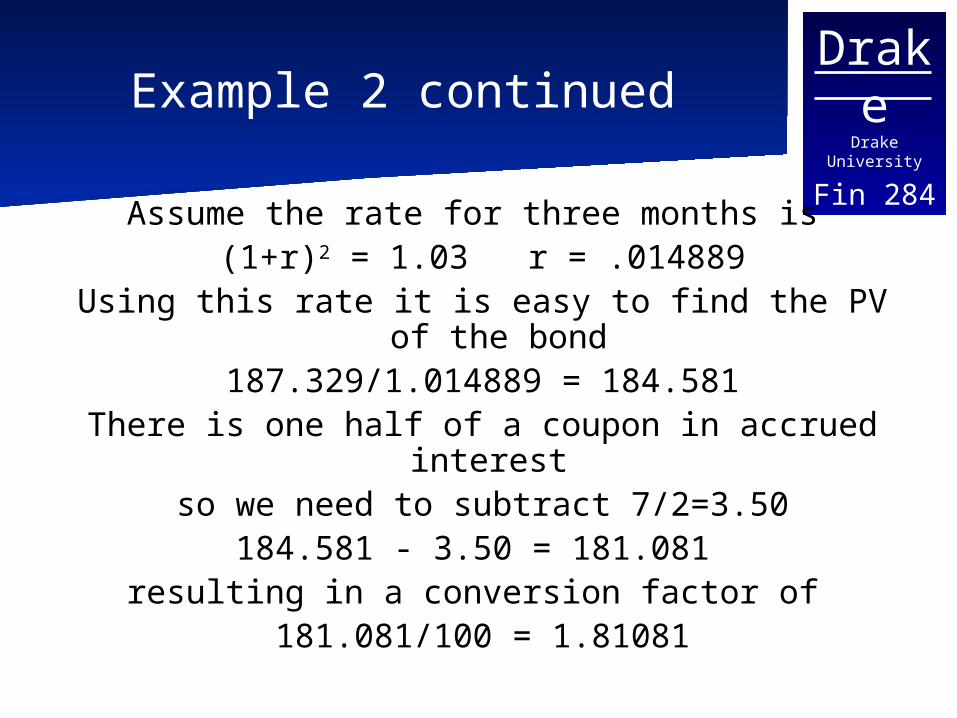

Fin 284Example 2 continued

Assume the rate for three months is (1+r)2 = 1.03 r = .014889

Using this rate it is easy to find the PV of the bond

187.329/1.014889 = 184.581There is one half of a coupon in accrued interest

so we need to subtract 7/2=3.50184.581 - 3.50 = 181.081

resulting in a conversion factor of 181.081/100 = 1.81081

DrakeDrake University

Fin 284Price Quote on T-Bills

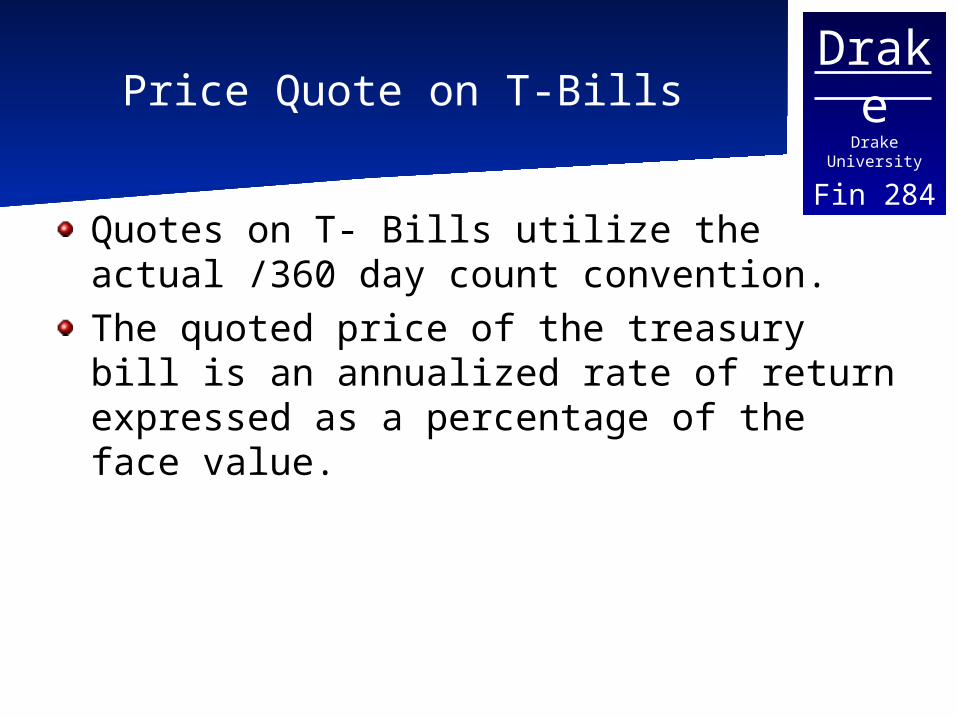

Quotes on T- Bills utilize the actual /360 day count convention. The quoted price of the treasury bill is an annualized rate of return expressed as a percentage of the face value.

DrakeDrake University

Fin 284T- Bills continued

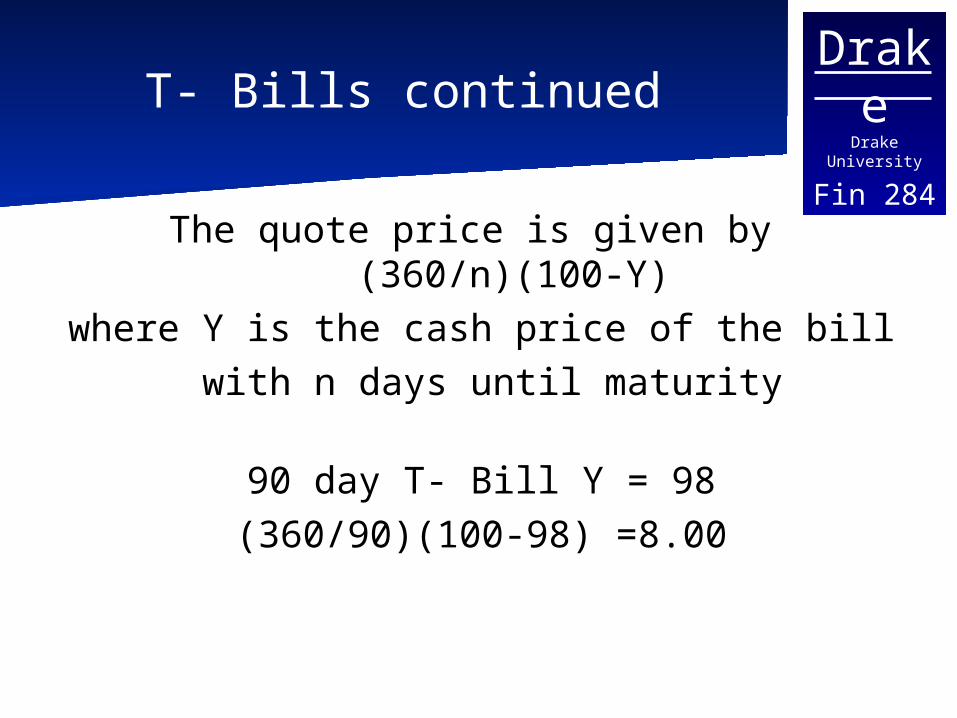

The quote price is given by (360/n)(100-Y)

where Y is the cash price of the bill with n days until maturity

90 day T- Bill Y = 98(360/90)(100-98) =8.00

DrakeDrake University

Fin 284Rate of Return

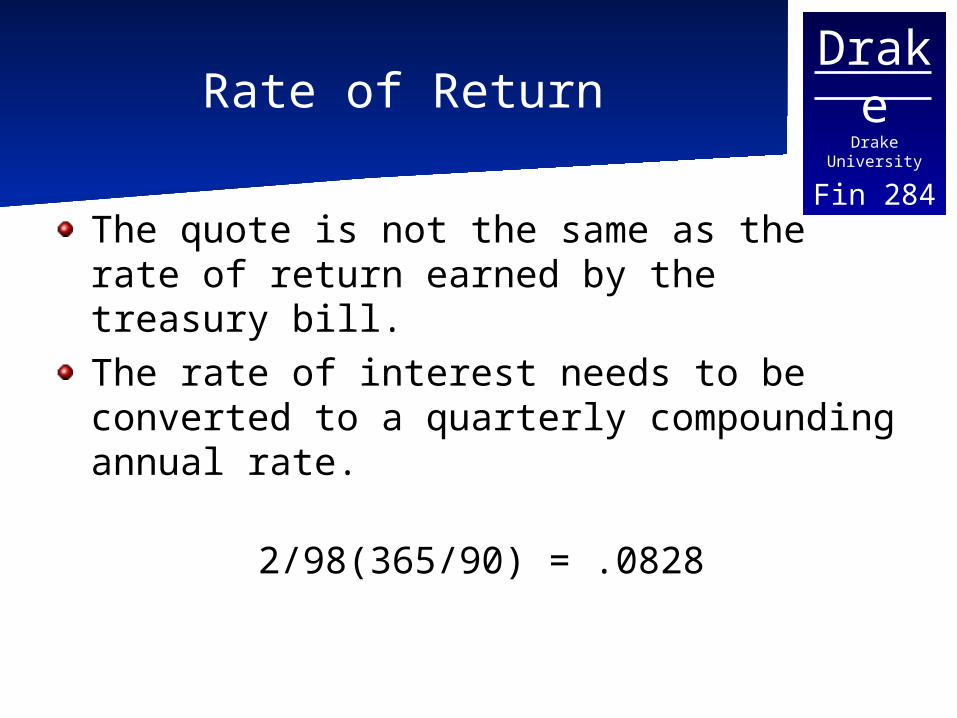

The quote is not the same as the rate of return earned by the treasury bill.The rate of interest needs to be converted to a quarterly compounding annual rate.

2/98(365/90) = .0828

DrakeDrake University

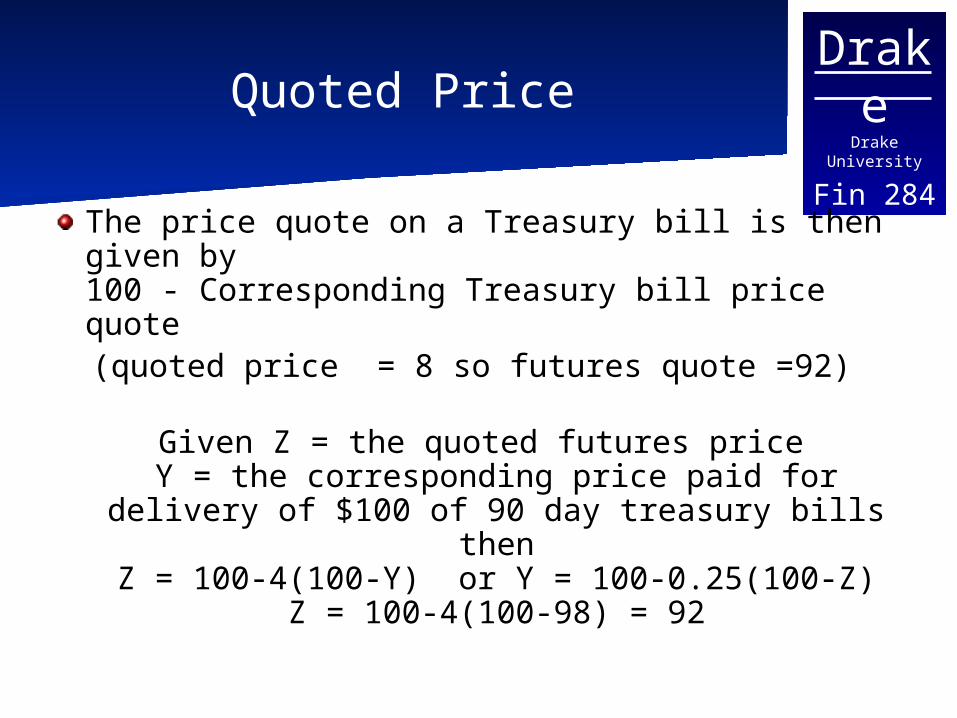

Fin 284Quoted Price

The price quote on a Treasury bill is then given by 100 - Corresponding Treasury bill price quote

(quoted price = 8 so futures quote =92)

Given Z = the quoted futures priceY = the corresponding price paid for delivery

of $100 of 90 day treasury bills thenZ = 100-4(100-Y) or Y = 100-0.25(100-

Z)Z = 100-4(100-98) = 92

DrakeDrake University

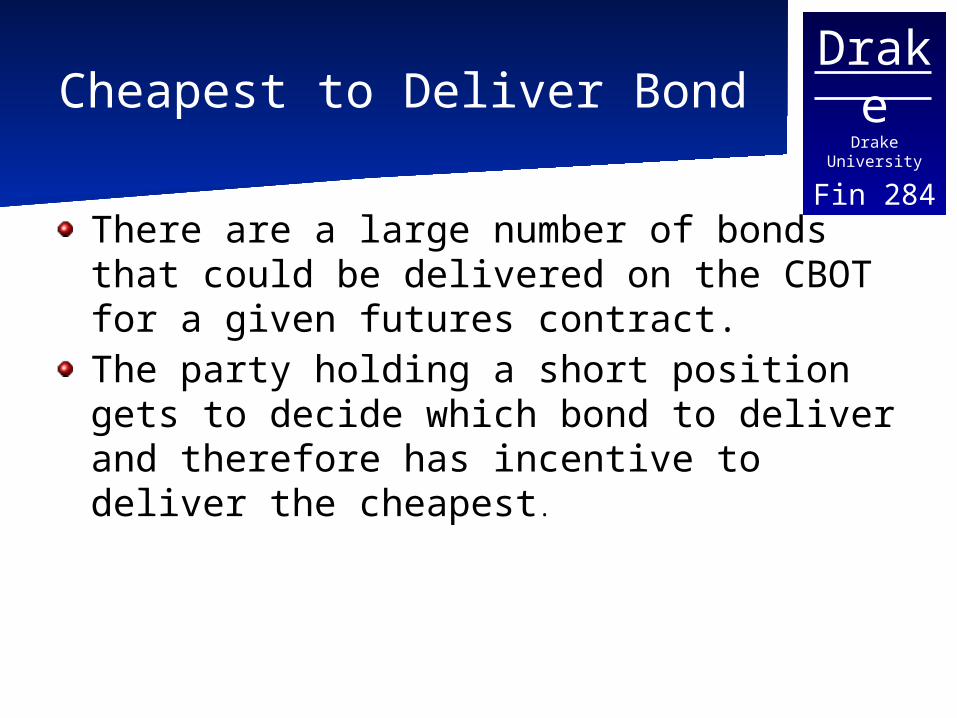

Fin 284Cheapest to Deliver Bond

There are a large number of bonds that could be delivered on the CBOT for a given futures contract. The party holding a short position gets to decide which bond to deliver and therefore has incentive to deliver the cheapest.

DrakeDrake University

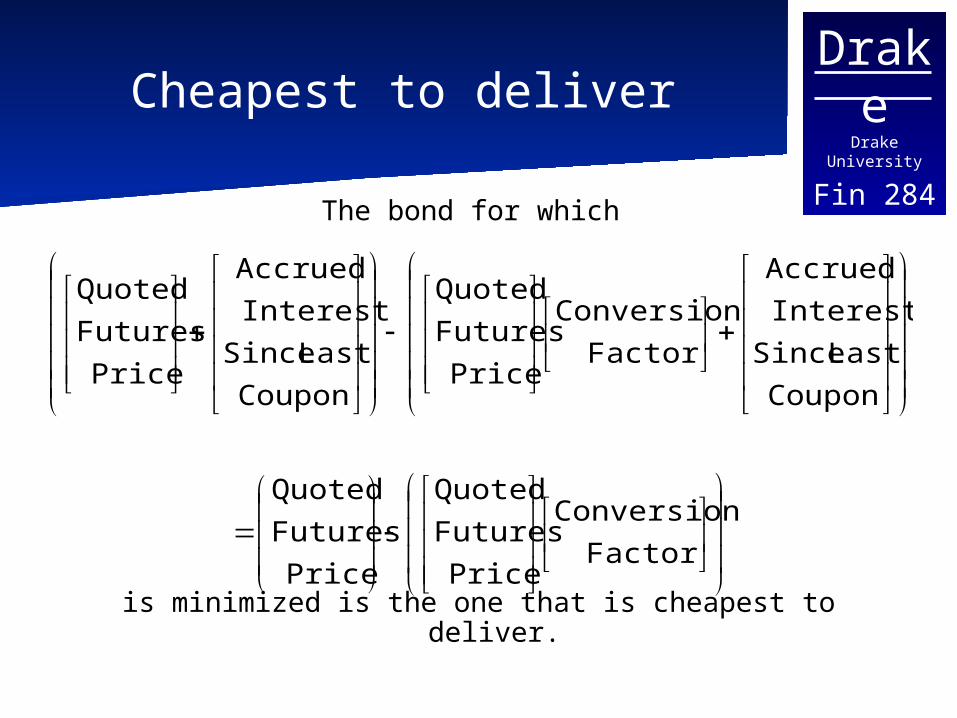

Fin 284Cheapest to Deliver

Upon delivery the short position receives

The cost of purchasing a bond isQuoted price + accrued interest

By minimizing the difference between the cost and the amount received, the party effectively delivers the cheapest bond:

DateCoupon

Last Since

interest Accured

Factor

Conversion

Price

Futures

Quoted

Received

Cash

DrakeDrake University

Fin 284Cheapest to deliver

The bond for which

is minimized is the one that is cheapest to deliver.

Factor

Conversion

Price

Futures

Quoted

Price

Futures

Quoted

Coupon

Last Since

Interest

Accrued

Factor

Conversion

Price

Futures

Quoted

Coupon

Last Since

Interest

Accrued

Price

Futures

Quoted

DrakeDrake University

Fin 284

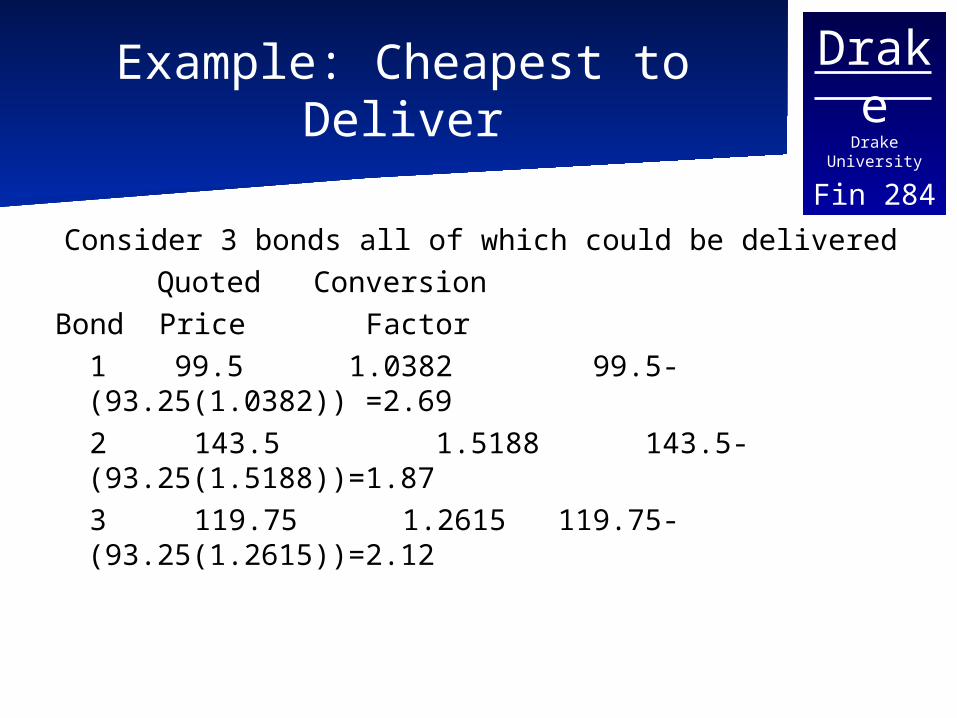

Example: Cheapest to Deliver

Consider 3 bonds all of which could be delivered Quoted Conversion

Bond Price Factor 1 99.5 1.0382 99.5-(93.25(1.0382))

=2.69 2 143.5 1.5188 143.5-

(93.25(1.5188))=1.87 3 119.75 1.2615 119.75-

(93.25(1.2615))=2.12

DrakeDrake University

Fin 284

Impact of yield changes on CTD

As yield increases bonds with a low coupons and longer maturities become relatively cheaper to deliver. As rates increase all bond prices decrease, but the price decrease for the longer maturity bonds is greaterAs yields decrease high coupon, short maturity bonds become relatively cheaper to deliver.

DrakeDrake University

Fin 284Wild Card Play

Trading at the CBOT closes at 2p.m. however treasury bonds continue to trade until 4:00pm and a party with a short position has until 8pm to file a notice of intention to deliver. Since the price is calculated on the closing price in the CBOT the party with a short position sometimes has the opportunity to profit from price movements after the closing of the CBOT.If the Bond Prices decrease after 2 pm it improves the short position.

DrakeDrake University

Fin 284Hedge Terminology

Short HedgeA short hedge occurs when the hedger already owns an asset or will own an asset soon and expects to sell it at some date in the future. In this case the hedger will take a short position in the futures market, guaranteeing the price in the future at which the asset can be sold.

DrakeDrake University

Fin 284Hedge Terminology

Long HedgeA long hedge occurs when the hedger knows that it will be necessary to purchase a given asset at a point in the future and wants to lock in the future price today. The alternatives to the hedge are buying the asset in the future at the market price or purchasing it today and holding onto it until the asset is needed in the future.

DrakeDrake University

Fin 284Simple Hedge Example

Assume you know that you will owe at rate equal to the LIBOR + 100 basis points in three months on a notional amount of $100 Million. The interest expenses will be set at the LIBOR rate in three months.Current three month LIBOR is 7%, Eurodollar futures contract is selling at 92.90.

DrakeDrake University

Fin 284Simple Hedge Example

100 - 92.90 = 7.10The futures contract is paying 7.10%

Assume the interest rate may either increase to 8% or decrease to 6%

DrakeDrake University

Fin 284A Short Hedge

Agree to sell 10 Eurodollar future contracts (each with an underlying value of $1 Million).We want to look at two results the spot market and the futures market. Assume you close out the futures position and that the futures price will converge to the spot at the end of the three months.

DrakeDrake University

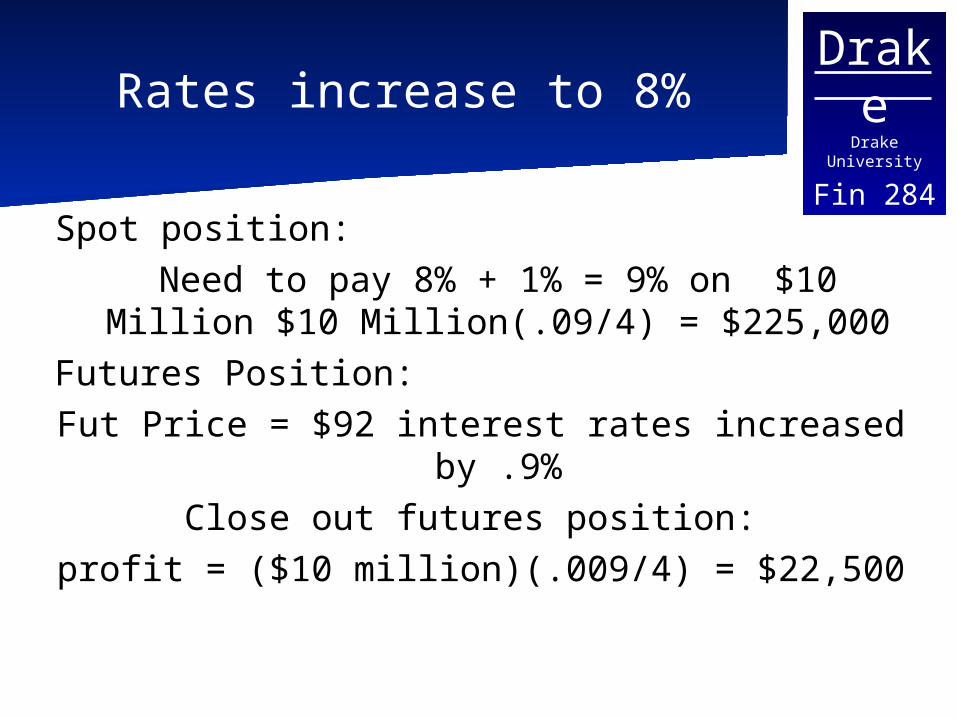

Fin 284Rates increase to 8%

Spot position:Need to pay 8% + 1% = 9% on $10 Million

$10 Million(.09/4) = $225,000Futures Position:

Fut Price = $92 interest rates increased by .9%

Close out futures position: profit = ($10 million)(.009/4) = $22,500

DrakeDrake University

Fin 284Rates Increase to 8%

Net interest paid$225,000 - $22,500 = $202,500

$10 million(.0810/4) = $202,500

DrakeDrake University

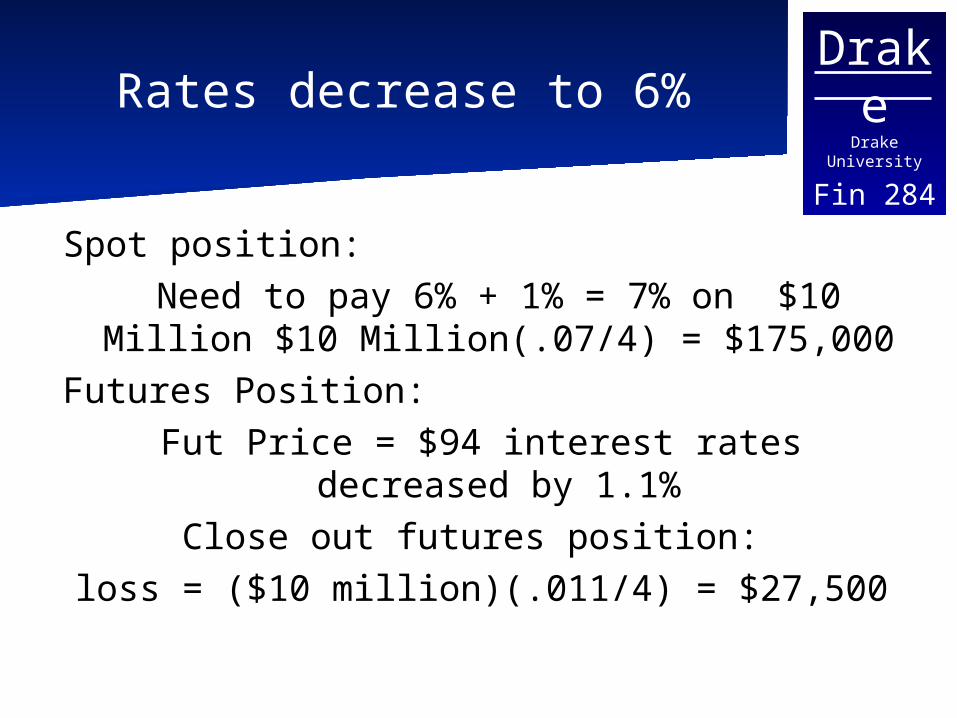

Fin 284Rates decrease to 6%

Spot position:Need to pay 6% + 1% = 7% on $10 Million $10 Million(.07/4) = $175,000

Futures Position:Fut Price = $94 interest rates decreased by

1.1%Close out futures position:

loss = ($10 million)(.011/4) = $27,500

DrakeDrake University

Fin 284Rates Decrease to 8%

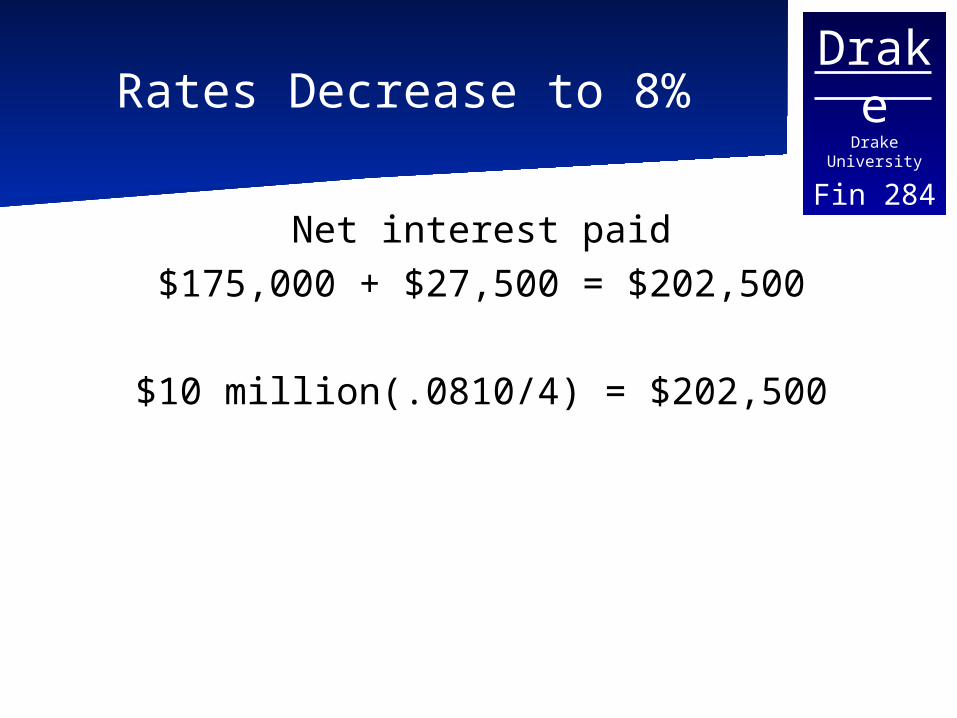

Net interest paid$175,000 + $27,500 = $202,500

$10 million(.0810/4) = $202,500

DrakeDrake University

Fin 284Results of Hedge

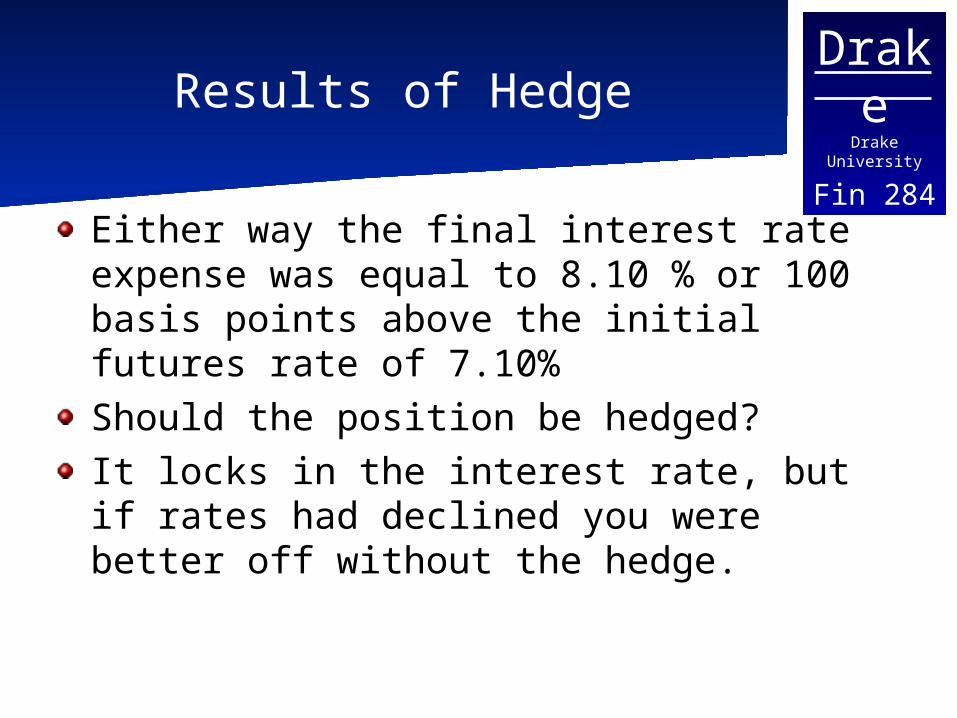

Either way the final interest rate expense was equal to 8.10 % or 100 basis points above the initial futures rate of 7.10%Should the position be hedged?It locks in the interest rate, but if rates had declined you were better off without the hedge.

DrakeDrake University

Fin 284Simple Example 2

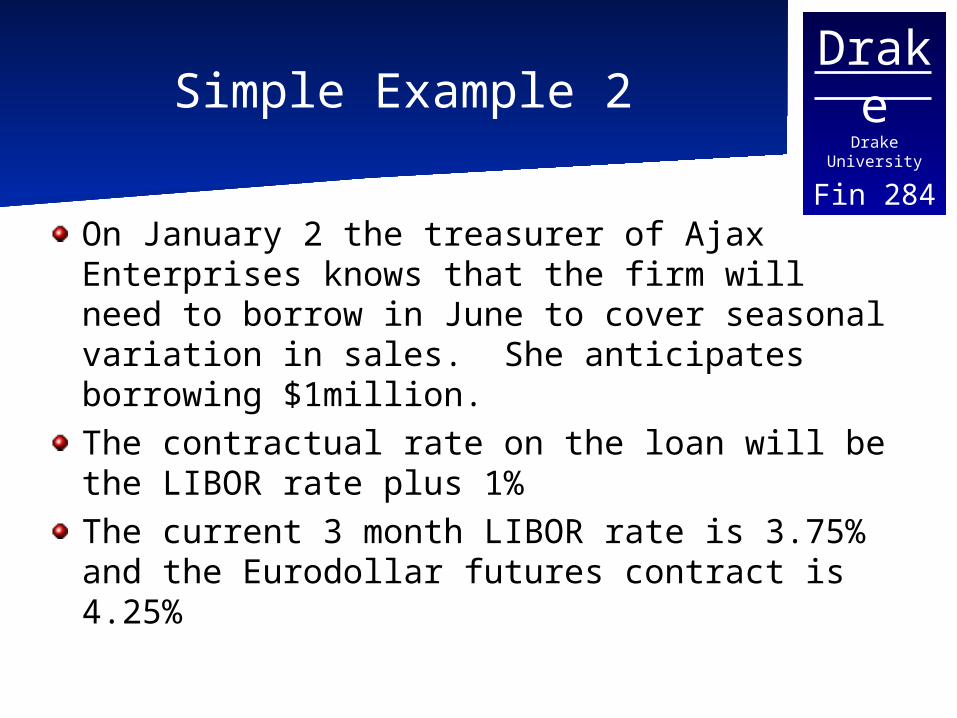

On January 2 the treasurer of Ajax Enterprises knows that the firm will need to borrow in June to cover seasonal variation in sales. She anticipates borrowing $1million.The contractual rate on the loan will be the LIBOR rate plus 1%The current 3 month LIBOR rate is 3.75% and the Eurodollar futures contract is 4.25%

DrakeDrake University

Fin 284

Simple Example 2 Continued

To hedge the position assume the treasurer sells one June futures contract. Assume interest rates increase to 5.5% on June 13.Assume that the expiration of the contract is June 13, the same day that the loan will be taken out. The futures price will be

100-5.50 = 94.50

DrakeDrake University

Fin 284Rates increase to 5.5%

Spot position:Need to pay 5.5%+1%= 6.5% on $1 Million $1 Million(.065/4) = $16,250

Futures Position:Fut Price = $94.50 interest rates

increased by 1.25%Close out futures position:

profit = ($1million)(.0125/4) = $3,125

DrakeDrake University

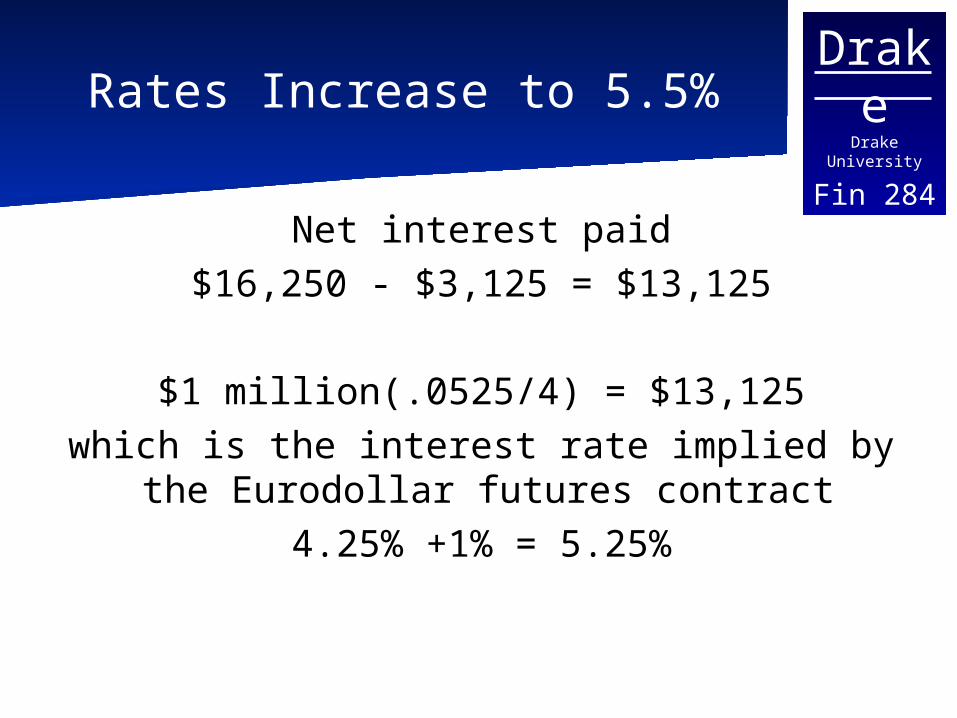

Fin 284Rates Increase to 5.5%

Net interest paid$16,250 - $3,125 = $13,125

$1 million(.0525/4) = $13,125which is the interest rate implied by the

Eurodollar futures contract 4.25% +1% = 5.25%

DrakeDrake University

Fin 284Assumptions

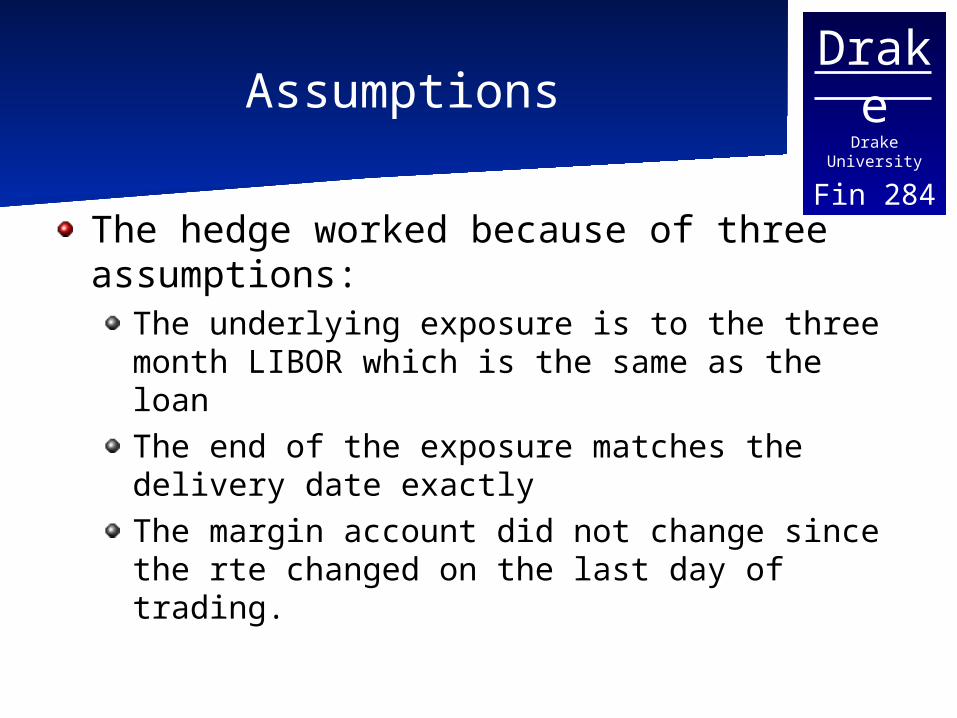

The hedge worked because of three assumptions:

The underlying exposure is to the three month LIBOR which is the same as the loanThe end of the exposure matches the delivery date exactlyThe margin account did not change since the rte changed on the last day of trading.

DrakeDrake University

Fin 284Basis Risk

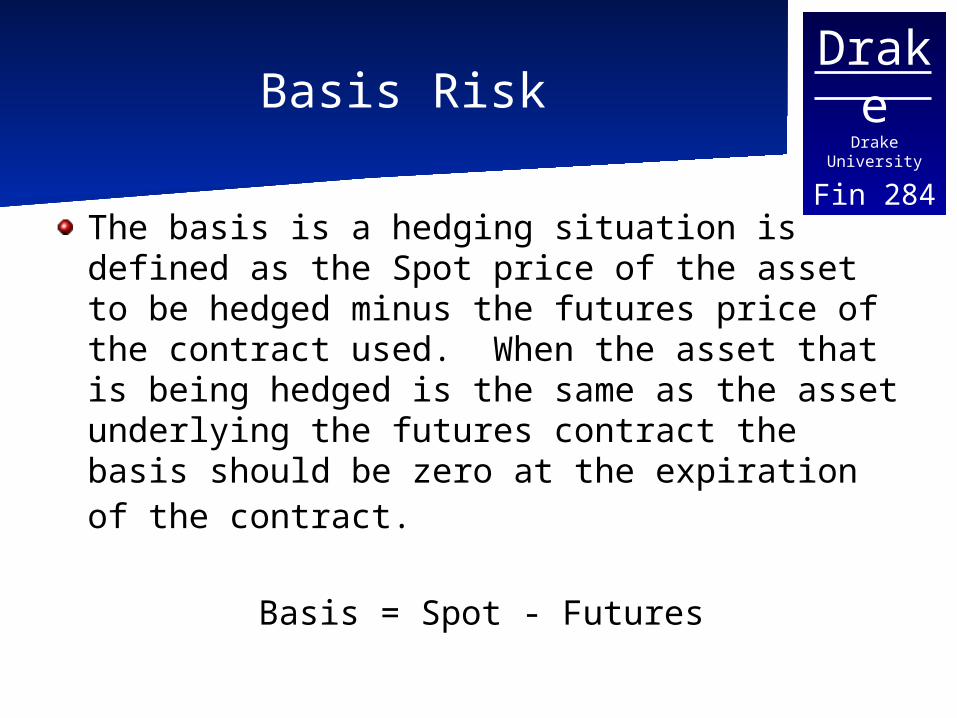

The basis is a hedging situation is defined as the Spot price of the asset to be hedged minus the futures price of the contract used. When the asset that is being hedged is the same as the asset underlying the futures contract the basis should be zero at the expiration of the contract.

Basis = Spot - Futures

DrakeDrake University

Fin 284Basis Risk

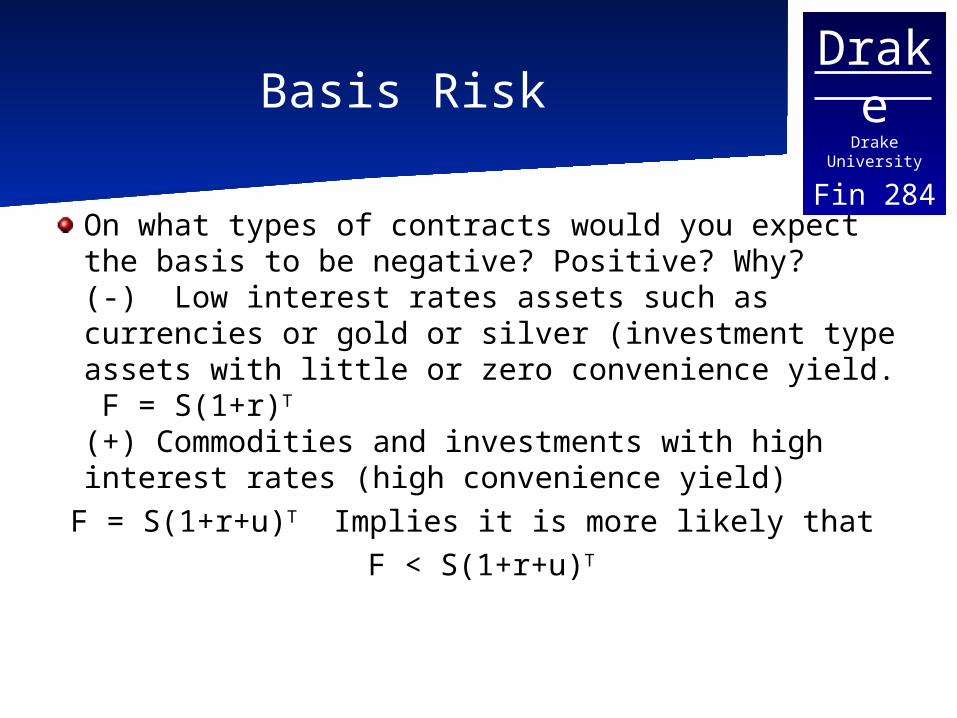

On what types of contracts would you expect the basis to be negative? Positive? Why?(-) Low interest rates assets such as currencies or gold or silver (investment type assets with little or zero convenience yield. F = S(1+r)T

(+) Commodities and investments with high interest rates (high convenience yield)F = S(1+r+u)T Implies it is more likely that

F < S(1+r+u)T

DrakeDrake University

Fin 284Basis Risk

The easiest way to illustrate the basis risk is with an example:

Let: St represent the spot price at time tFt represent the futures price at time tbt represent the basis at time t

DrakeDrake University

Fin 284Basis Risk Illustration

Assume we enter into a short hedge at time t = 1 and close out the hedge at time t = 2.

The profit on the futures position will equal F1- F2

The total price paid from the hedge is then S2 + F1 - F2

By definition:b1 = S1-F1 and b2 = S2-F2

DrakeDrake University

Fin 284Basis Risk

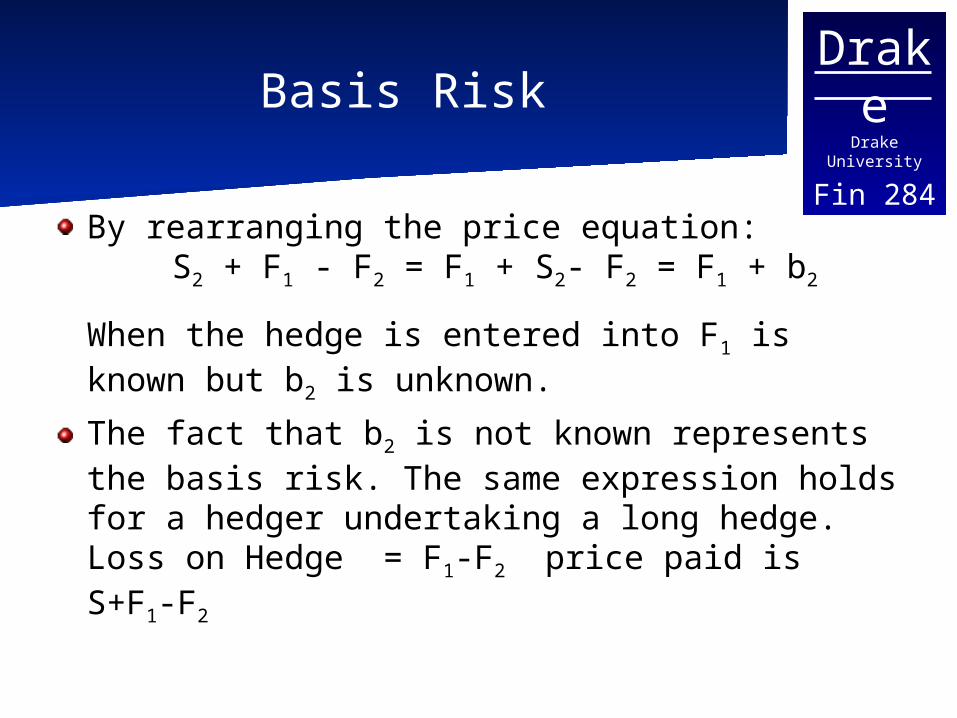

By rearranging the price equation:S2 + F1 - F2 = F1 + S2- F2 = F1 + b2

When the hedge is entered into F1 is known but b2 is unknown.

The fact that b2 is not known represents the basis risk. The same expression holds for a hedger undertaking a long hedge.Loss on Hedge = F1-F2 price paid is S+F1-F2

DrakeDrake University

Fin 284Mismatch of Maturities 1

Assume that the maturity of the contract does not match the timing of the underlying commitment.Assume that the loan is anticipated to be needed on June 1 instead of June 13.

DrakeDrake University

Fin 284Simple Example Redone

On January 2 the treasurer of Ajax Enterprises knows that the firm will need to borrow in June to cover seasonal variation in sales. She anticipates borrowing $1million.The contractual rate on the loan will be the LIBOR rate plus 1%The current 3 month LIBOR rate is 3.75% and the Eurodollar futures contract is 4.25%

DrakeDrake University

Fin 284

Simple Example 2 Continued

To hedge the position assume the treasurer sells one June futures contract. Assume interest rates increase to 5.5% on June 1.Assume that the futures price has decreased to 94.75 (before it had decreased to 94.50) implying a 5.25% rate (a 25 bp basis)

DrakeDrake University

Fin 284Rates increase to 5.5%

Spot position:Need to pay 5.5%+1%= 6.5% on $1 Million $1 Million(.065/4) = $16,250

Futures Position:Fut Price = $94.75 interest rates

increased by 1.00%Close out futures position:

profit = ($1million)(.0100/4) = $2,500

DrakeDrake University

Fin 284Rates Increase to 5.5%

Net interest paid$16,250 - $2,500 = $13,750

$1 million(.055/4) = $13,750which is more than the interest rate implied

by the Eurodollar futures contract 4.25% +1% = 5.25%

DrakeDrake University

Fin 284Minimizing Basis Risk

Given that the actual timing of the loan may also be uncertain the standard practice is to use a futures contract slightly longer than the anticipated spot position. The futures price is often more volatile during the delivery month also increasing the uncertainty of the hedge Also the short hedger could be forced to accept delivery instead of closing out.

DrakeDrake University

Fin 284Mismatch in Maturities 2

Assume that instead of our original problem the treasurer is faced with a stream of expected borrowing.Anticipated borrowing at 3 month LIBOR

Date AmountMach 1 $15 MillionJune 1 $45 MillionSeptember 1 $20 millionDecember 1 $10 Million

DrakeDrake University

Fin 284Strip Hedge

To hedge this risk, it to hedge each position individually.On January 1 the firm should:

enter into 15 short March contractsenter into 45 short June contractsenter into 20 short Sept contractsenter into 10 short December contracts

DrakeDrake University

Fin 284Strip Hedge continued

On each borrowing date the respective hedge should be closed out. The effectiveness of the hedge will depend upon the basis at the time each contract is closed out.

DrakeDrake University

Fin 284Rolling Hedge

Another possibility is to Roll the Hedge:January 2 enter into 90 short March contractsMarch 1 enter into 90 long March contracts

enter into 75 short June contractsJune 1 enter into 75 long June contracts

enter into 30 short Sept contractsSept 1 enter into 30 long Sept contracts

enter into 10 short Dec contractsDec 1 enter into 10 long Dec contracts

DrakeDrake University

Fin 284Rolling the Hedge

Again the effectiveness of the hedge will depend upon the basis at each point in time that the contracts are rolled over.This opens the from to risk from the resulting rollover basis.

DrakeDrake University

Fin 284Cross Hedging

So far we have assumed that the underlying asset is an exact match for the spot position to be hedged. Often this is not the case.Two questions

What futures contract should be used?How many contracts should be taken out?

DrakeDrake University

Fin 284Hedge Ratio

The hedge ratio is the ratio of the size of the position in the futures market to the size of the spot exposure being hedged. In our examples so far we have utilized a hedge ratio equal to one. In other words the size of the futures position was the same as the size of the position in the underlying asset.

DrakeDrake University

Fin 284

Minimum Variance Hedge Ratio

The ideal hedge ratio should be the one that minimizes the variance of the value of the hedged position.

DrakeDrake University

Fin 284

Minimum Variance Hedge Ratio

S be the change in the spot price S during a period of time equal to the life of the project

F be the change in the futures price F during a period of time equal to the life of the project

S be the standard deviation of S

F be the standard deviation of F be the coefficient of correlation between S and

Fh be the hedge ratio

DrakeDrake University

Fin 284Hedge positions

The change in the short hedgers position is

the change in the long hedgers position is

FS h

S-F h

DrakeDrake University

Fin 284Min Variance Hedge

The variance of the hedge position is

Taking the first derivative of the variance and setting it to zero produces the hedge ratio

FSFS hhv 2222

F

S

FSF

h

hh

v

022 2

DrakeDrake University

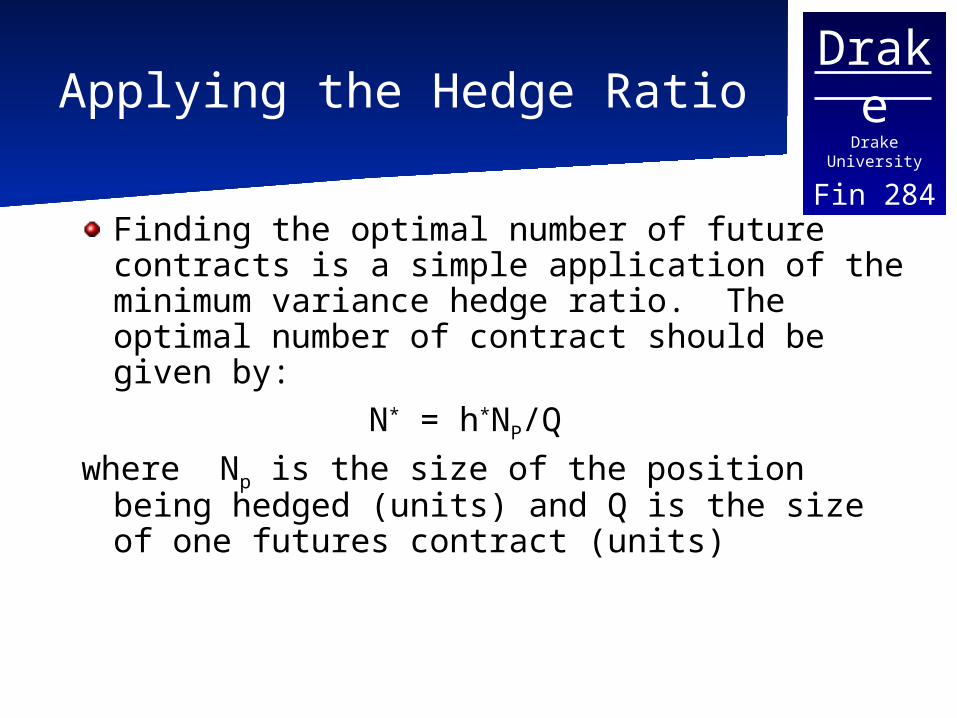

Fin 284Applying the Hedge Ratio

Finding the optimal number of future contracts is a simple application of the minimum variance hedge ratio. The optimal number of contract should be given by:

N* = h*NP/Q

where Np is the size of the position being hedged (units) and Q is the size of one futures contract (units)

DrakeDrake University

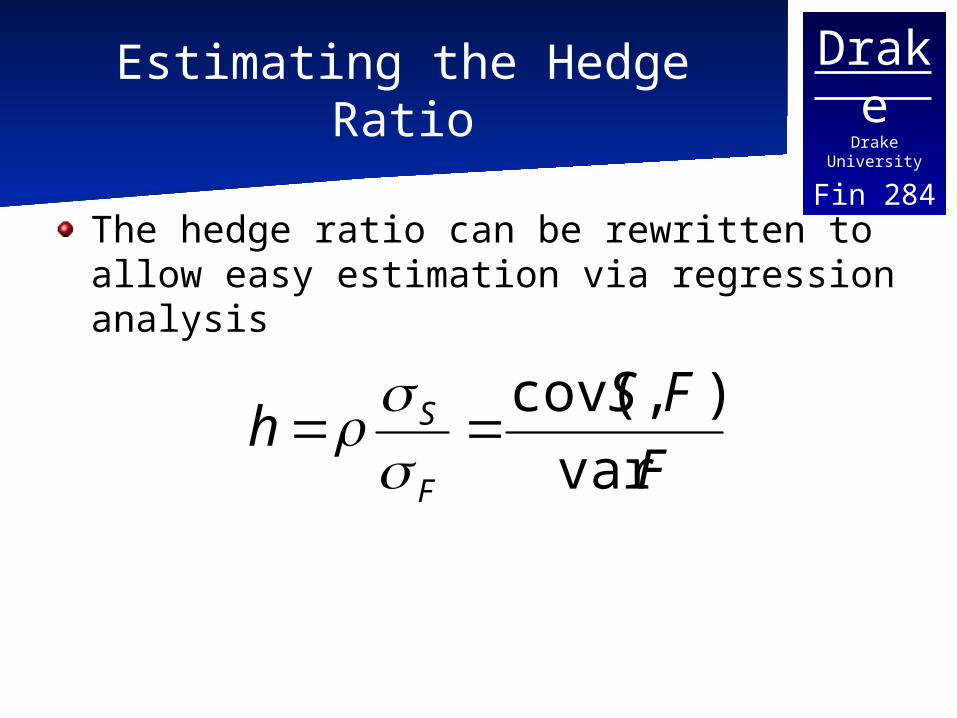

Fin 284Estimating the Hedge Ratio

The hedge ratio can be rewritten to allow easy estimation via regression analysis

F

FSh

F

S

var

),cov(

DrakeDrake University

Fin 284Regression Review

Equation of a line: Y = a + bXGraphing combinations of X and Y form a line.X is the independent variable and placed on the horizontal axis. Y the dependent variable and placed on the vertical axis (The value of Y depends upon X)a is the Y intercept and b the slope of the line.

DrakeDrake University

Fin 284

We can observe observations of X,Y and plot

them

DrakeDrake University

Fin 284

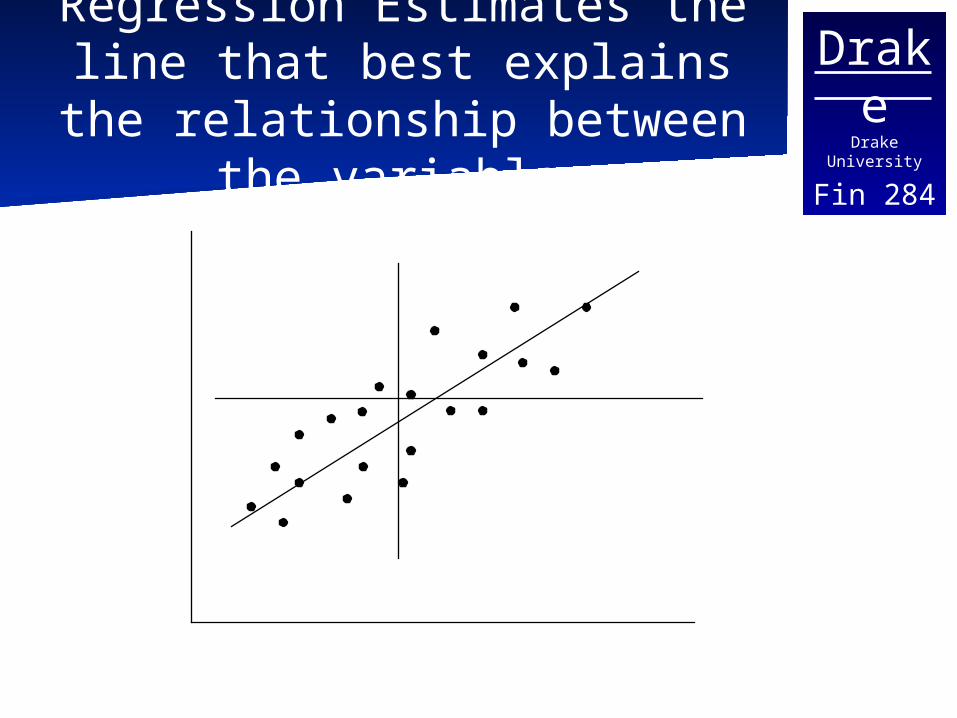

Regression Estimates the line that best explains the relationship between the

variables

DrakeDrake University

Fin 284

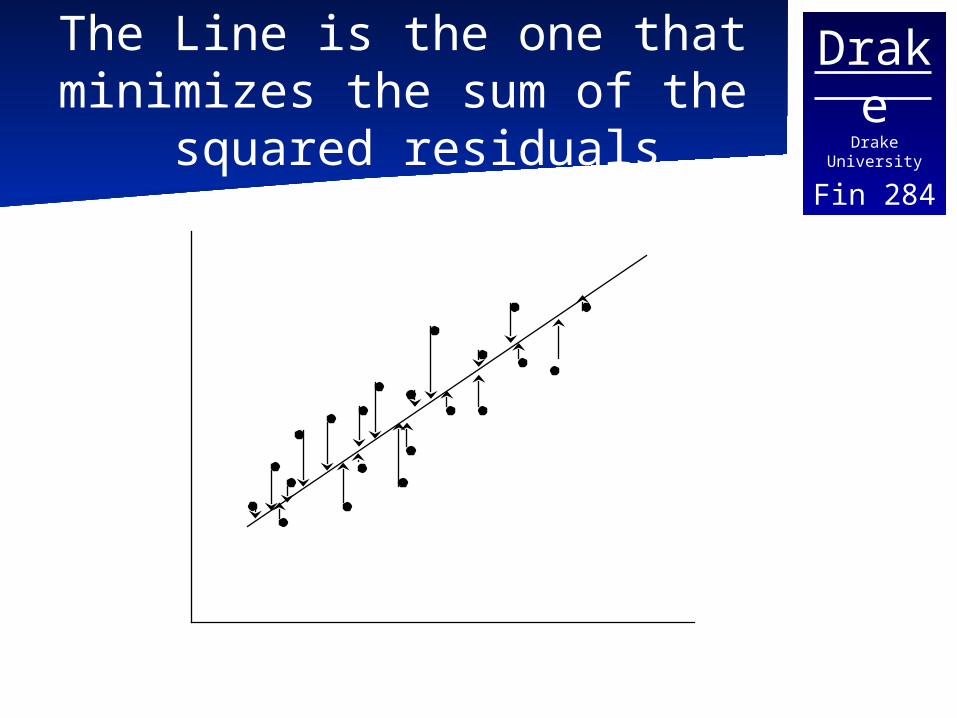

The Line is the one that minimizes the sum of the

squared residuals

DrakeDrake University

Fin 284Estimating the Regression

The slope of the line is then equal to

The Intercept is:XVariance

y)Cov(x,

)( XY AverageslopeAverage

DrakeDrake University

Fin 284

Applying the Regression to the Hedge Ratio

The minimum variance hedge ratio could be estimated by in the regression.

(St) = + (Ft) + t

DrakeDrake University

Fin 284Example

Now assume that the treasury has decided to borrow it the commercial paper market instead of from a financial institution.There is not a commercial paper futures contract so it must be decided what contract to use to hedge the possible interest rate change in the commercial paper market.Assume that the treasure wants to borrow $36 million in June with a one month commercial paper issue.

DrakeDrake University

Fin 284Number of contracts part 1

You must choose what underlying contract best matches the 30 day commercial paper return.90 Day T-Bill. 90 day LIBOR Eurodollar, 10 year treasury bond. Assume 90 day LIBOR Eurodollar has the highest correlation so it is chosen.Assume now that the treasurer for Ajax has ran the regression and that the beta is .75

DrakeDrake University

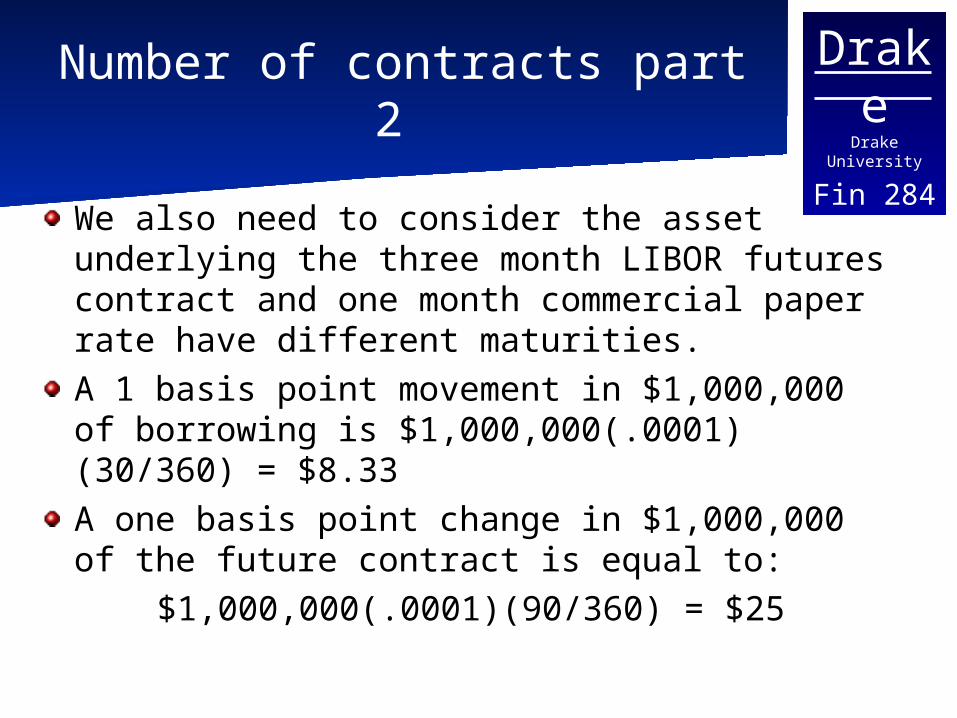

Fin 284Number of contracts part 2

We also need to consider the asset underlying the three month LIBOR futures contract and one month commercial paper rate have different maturities.A 1 basis point movement in $1,000,000 of borrowing is $1,000,000(.0001)(30/360) = $8.33A one basis point change in $1,000,000 of the future contract is equal to:

$1,000,000(.0001)(90/360) = $25

DrakeDrake University

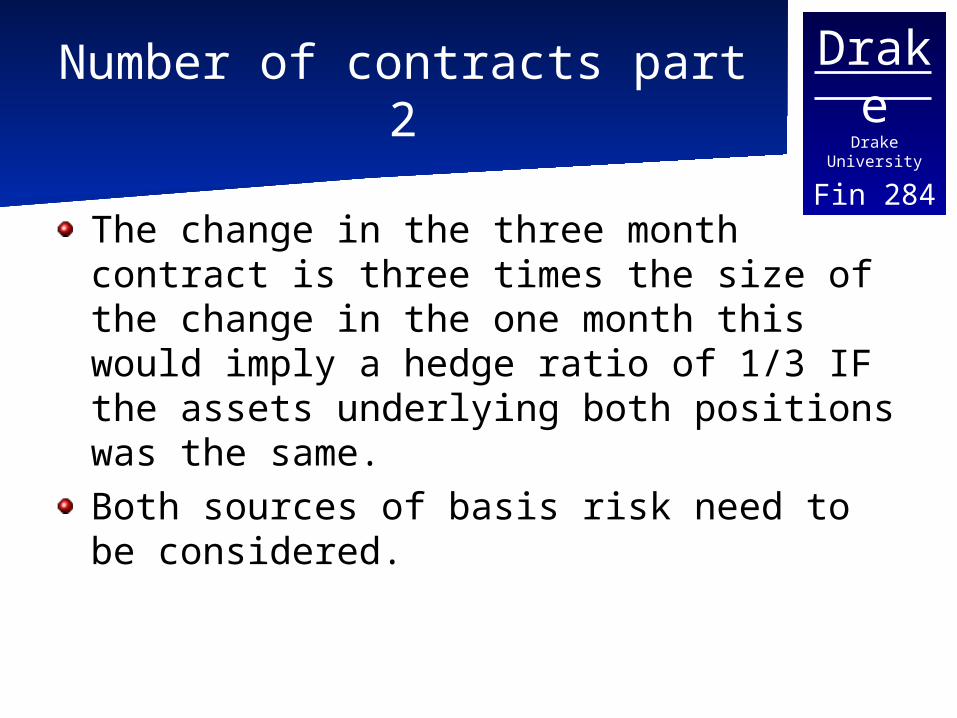

Fin 284Number of contracts part 2

The change in the three month contract is three times the size of the change in the one month this would imply a hedge ratio of 1/3 IF the assets underlying both positions was the same.Both sources of basis risk need to be considered.

DrakeDrake University

Fin 284Number of Contracts

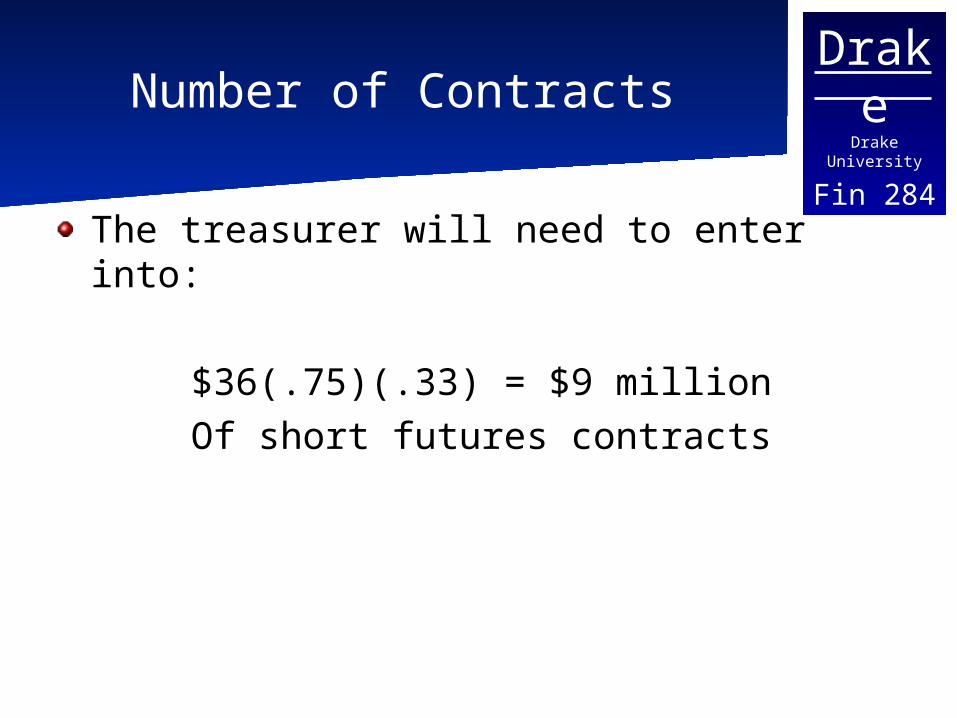

The treasurer will need to enter into:

$36(.75)(.33) = $9 millionOf short futures contracts

DrakeDrake University

Fin 284The Cross Hedge

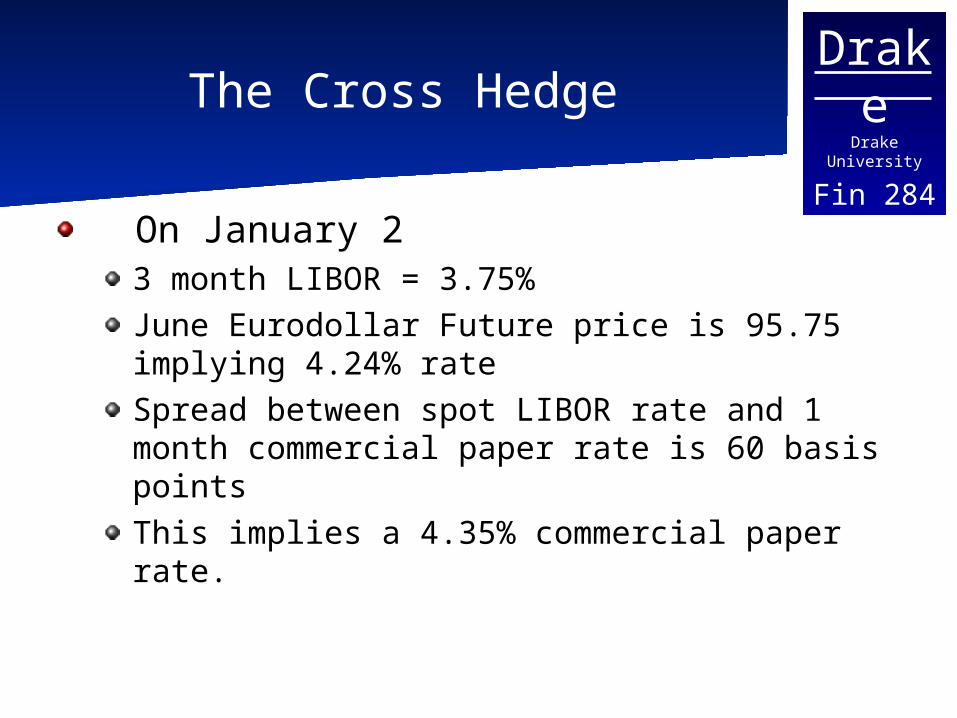

On January 23 month LIBOR = 3.75%June Eurodollar Future price is 95.75 implying 4.24% rateSpread between spot LIBOR rate and 1 month commercial paper rate is 60 basis pointsThis implies a 4.35% commercial paper rate.

DrakeDrake University

Fin 284Expectations

Previously Ajax hoped to lock in a 4.25% 3 month LIBOR rate or an increase of 50 basis points form the current 3.75%Keeping the 50 basis point increase constant and using our hedge ratio of .75 the goal becomes locking in a .75 (50) = 37.5 basis point increase in the commercial paper rate.This implies a one month rate of 4.35% + 37.5BP = 4.725%

DrakeDrake University

Fin 284Results Futures

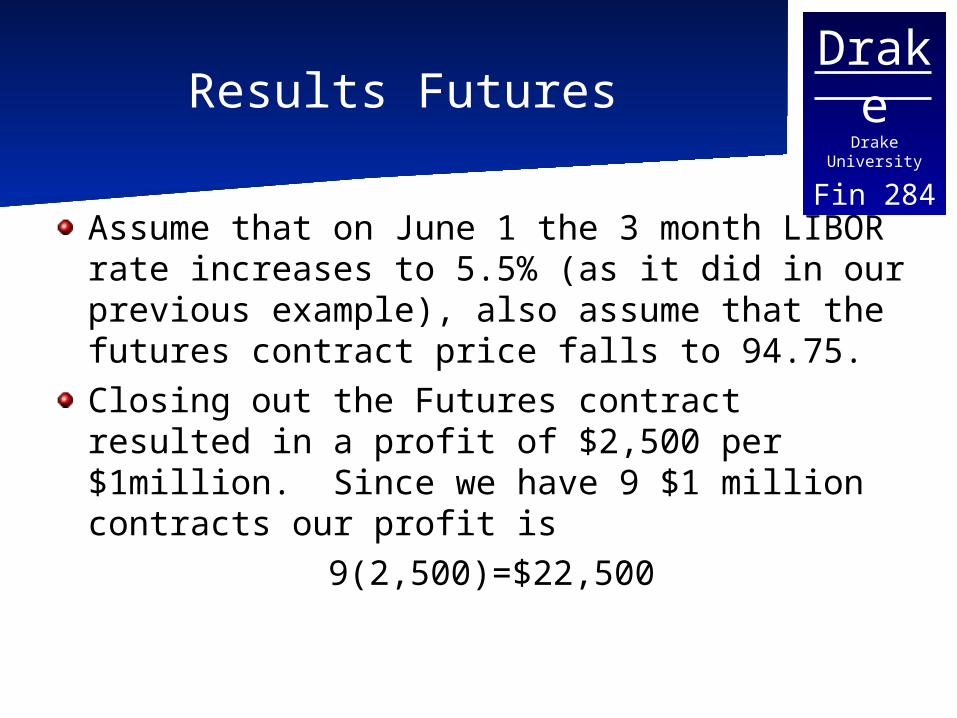

Assume that on June 1 the 3 month LIBOR rate increases to 5.5% (as it did in our previous example), also assume that the futures contract price falls to 94.75.Closing out the Futures contract resulted in a profit of $2,500 per $1million. Since we have 9 $1 million contracts our profit is

9(2,500)=$22,500

DrakeDrake University

Fin 284Results Spot

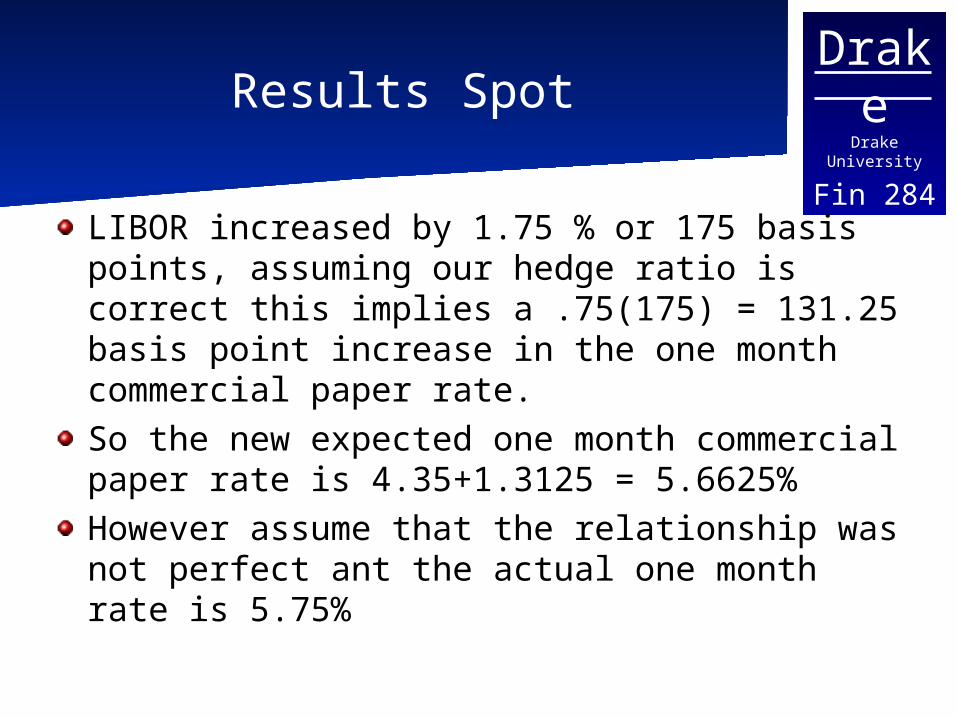

LIBOR increased by 1.75 % or 175 basis points, assuming our hedge ratio is correct this implies a .75(175) = 131.25 basis point increase in the one month commercial paper rate.So the new expected one month commercial paper rate is 4.35+1.3125 = 5.6625%However assume that the relationship was not perfect ant the actual one month rate is 5.75%

DrakeDrake University

Fin 284Results

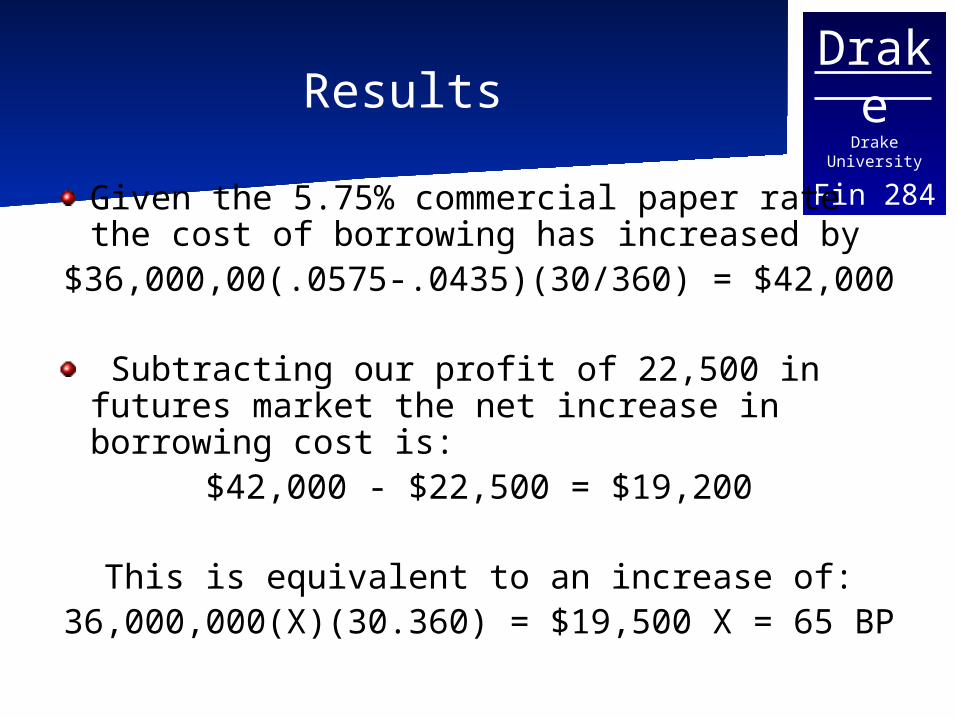

Given the 5.75% commercial paper rate the cost of borrowing has increased by

$36,000,00(.0575-.0435)(30/360) = $42,000

Subtracting our profit of 22,500 in futures market the net increase in borrowing cost is:

$42,000 - $22,500 = $19,200

This is equivalent to an increase of:36,000,000(X)(30.360) = $19,500 X = 65 BP

DrakeDrake University

Fin 284Results

Using the 65 BP increase Ajax ended up paying 5% for its borrowing.The treasurer was attempting to lock in 4.725% or 27.5BP less than what she ended up paying.The 27.5 BP difference is the result of basis risk.

DrakeDrake University

Fin 284Basis Risk

Source 1June 1 spot LIBOR was 5.5% the LIBOR rate implied by the futures contract was 5.25% a 25 BP differenceGiven the hedge ratio of .75 this should be a 25(.75) = 18.75 BP difference for commercial paper

Source 2Expected 1 month commercial paper rte is 5.6625%, actual is 5.75% a 8.75 BP difference

DrakeDrake University

Fin 284Basis Risk

The result of the two sources of risk:

18.75 + 8.75 = 27.5 basis points

DrakeDrake University

Fin 284Tailing the Hedge

Adjustments to the margin account will also impact the hedge and need to be made.The idea is to make the PV of the hedge equal the underlying exposure to adjust for any interest and reinvestment in the margin account.For N contracts this becomes Ne-rT contracts where r is the risk free rate and T is the time to maturity.

DrakeDrake University

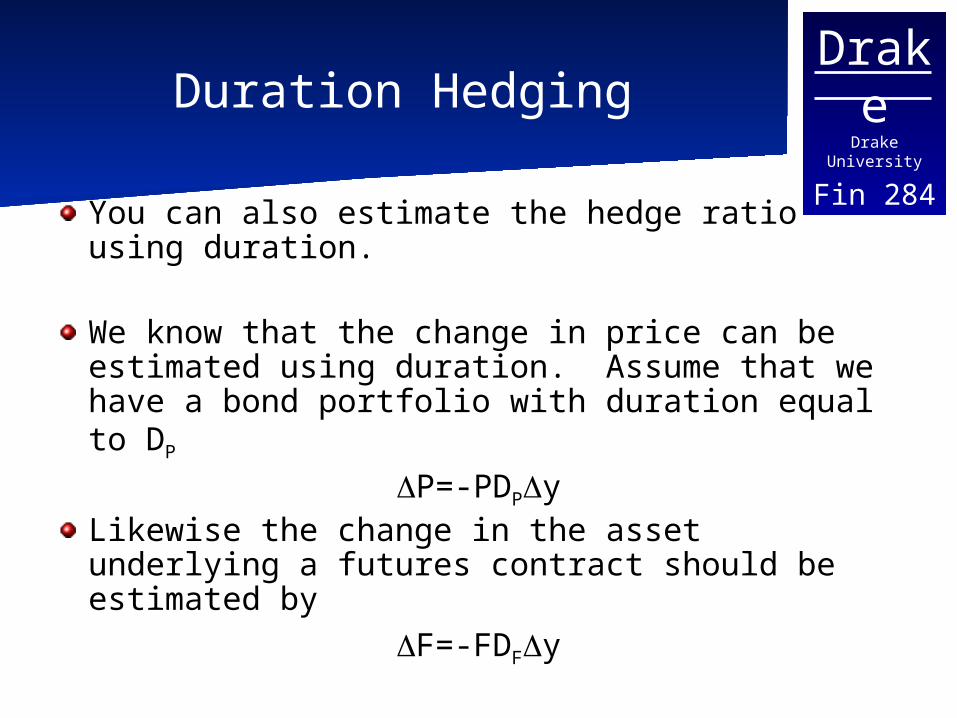

Fin 284Duration Hedging

You can also estimate the hedge ratio using duration.

We know that the change in price can be estimated using duration. Assume that we have a bond portfolio with duration equal to DP

P=-PDPyLikewise the change in the asset underlying a futures contract should be estimated by

F=-FDFy

DrakeDrake University

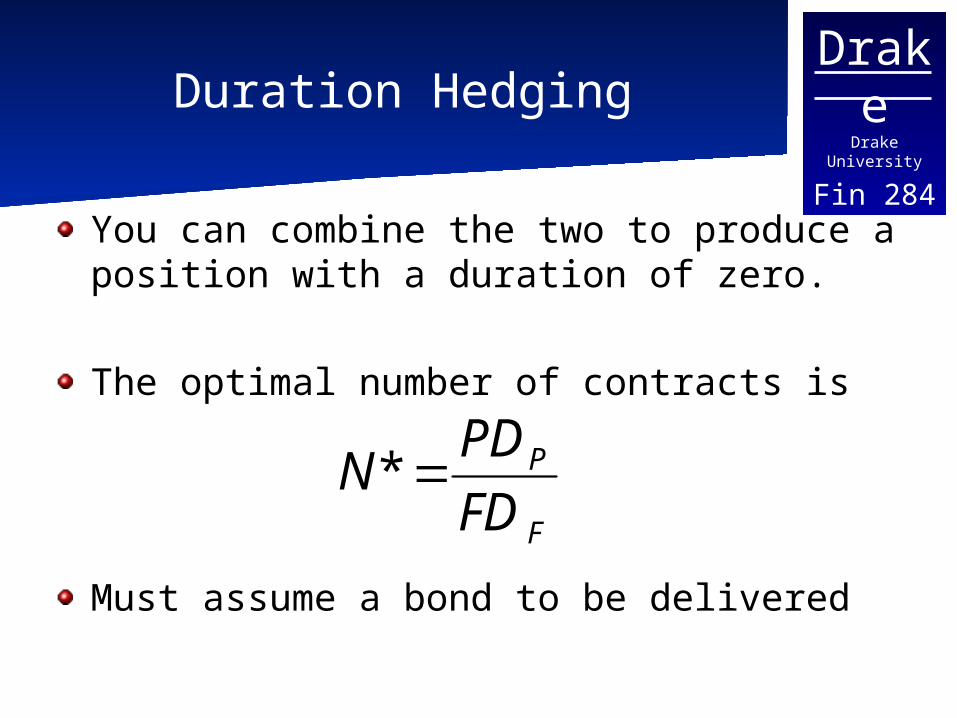

Fin 284Duration Hedging

You can combine the two to produce a position with a duration of zero.

The optimal number of contracts is

Must assume a bond to be delivered

F

P

FD

PDN *