dynamic correlation analysis of us financial crisis and ... · goldfajn, 1999) focuses on providing...

TRANSCRIPT

OC12062

1

Dynamic Correlation Analysis of US Financial Crisis and Contagion:

Evidence from Four OECD countries

Hong-Ghi Mina

Department of Management Science, Korea Advanced Institute of Science and Technology,

and

Young-Soon Hwang

Busan Development Institute

This version: 9 September 2011

________________________________________________________________ a

Correspondence: E-mail: [email protected] Tel:+82-42-350-6305, Fax:+82-42-350-6339.

OC12062

2

Dynamic Correlation Analysis of US Financial Crisis and Contagion:

Evidence from Four OECD countries

This version: 9 September 2011

Abstract

By analyzing the dynamic conditional correlations (DCC) of the daily stock returns of four OECD countries with that of the US for the period of 2006-2010, we could find a process of increasing correlations (contagion) in the first phase of the US financial crisis and an additional increase of correlations (herding) during the second phase of the US financial crisis for the UK, Australia, and Switzerland. However, the impact of the US financial crisis on Japan was limited to the increase in correlation volatilities in the first phase. We also propose a new approach (DCCX-MGARCH) that allows simultaneous estimation of the DCC and their determinants, which can be used to identify channels of contagion. It is shown that an increase in VIX stock market index increases conditional correlations but an increase in the TED spread and relative stock market capitalization decrease conditional correlations of stock returns between four OECD countries and the US.

JEL classification: F31, G15

Keywords: DCCX-MGARCH, Dynamic conditional correlations, contagion, US financial

crisis, VIX index, TED spread.

OC12062

3

I. Introduction

At the beginning of the US financial crisis, which began with the failure of Lehmann

Brothers in September 2008, some economists expected that the decoupling of financial

markets could isolate the adverse impact of the US recession on the rest of the world.

However, many studies report contagion of emerging markets (Beirne et al., 2008; Dooley

and Hutchison, 2009; Kim and Kim, 2011) and advanced markets (Boyson et al., 2010;

Christensen and Ronaldo, 2010; Chudick and Fratzscher, 2011) from the US financial crisis.

Even though identifying the nature of financial market contagion is extremely

important, previous studies failed to reach a consensus on the existence of contagion with the

earlier financial crisis episodes. Forbes and Rigobon (2002) argue that most of previous

evidence of contagion (King and Wadhwani, 1990; Lee and Kim, 1993; Calvo and Reinhart,

1996) disappears when unconditional cross-market correlation coefficients are corrected for

bias. However, Corsetti et al. (2005) show that Forbes and Rigobon’s test is biased towards

the null hypothesis of no contagion and report “some contagion, some interdependence.” In

other words, for proper investigation of stock market comovement (contagion), we need to

consider heteroscedasticity and the dynamic nature of the correlations.

In this paper, we investigate the transmission of the recent US financial crisis to stock

markets in four OECD countries. In particular, we are interested in (i) finding empirical

evidence of contagion from the US stock market to those of the four OECD countries and (ii)

analyzing two phases of crisis transmission, i.e., contagion and herding. Most importantly, we

are interested in finding the channels of the transmission mechanism. To answer the first two

questions, we use Engle’s (2002) dynamic conditional correlation multivariate GARCH

(DCC-MGARCH) model. To answer the third question, we propose a new DCC-MGARCH

type model with exogenous variables (DCCX-MGARCH). This methodology can estimate

OC12062

4

both the dynamic conditional correlation and the impact of explanatory variables

simultaneously in one framework. The DCCX-MGARCH method can be useful in

identifying the channels of contagion in the stock returns of four OECD countries (United

Kingdom, Japan, Switzerland, and Australia) and that of the US. In other words, our DCCX-

MGARCH model is different from previous models in that ours can directly estimate the

effects of exogenous variables on the conditional correlations.

A number of variables can be considered important for the determination of dynamic

conditional correlations of stock returns. We include the daily sovereign CDS spread, the

VIX index, the relative stock market capitalization to the US, and the TED spread. We

include the CDS spread as a measure of the sovereign risk of each country. The VIX implied

volatility is a proxy for stock market uncertainty (Connolly et al., 2005), and it is a widely

used measure of investor fear. The TED spread is the difference between the three-month

LIBOR and the yield on the US Treasury bills with the same maturity. The TED spread is

used as a measure for the level of financial stress in the interbank market. Brunnermeier

(2009) shows that the TED spread provides a useful basis for gauging the severity of the

liquidity crisis. Finally, the ratio of stock market capitalization relative to the US is included

in the analysis as a measure of the financial independence from the US.

This paper is organized as follows. Section II reviews previous literature related to our

research questions. In Section III, we estimate the dynamic conditional correlations of four

OECD countries’ stock return with the US stock return and provide empirical evidence of

two phases (contagion and herding) of the US financial crisis on the conditional correlations

of four OECD countries. Section IV investigates the determinants of conditional correlations

using the DCCX-MGARCH model, and Section V concludes the paper.

OC12062

5

II. Literature

Studies on stock market comovement (contagion) can be grouped into three different

groups. The first group of studies (King and Wadhwani, 1990; Lee and Kim, 1993; Baig and

Goldfajn, 1999) focuses on providing evidence of a significant increase in cross-country

unconditional correlations of stock returns by employing a subsample analysis for a structural

break, with a known structural break date. However, several studies (Forbes and Rigobon,

2002; Bordo and Murshid, 2001; Basu, 2002) argue that there is no significant increase in

stock return correlations when they account for heteroscedasticity. Corsetti et al. (2005),

Froot et al. (2001) and Basu (2002) confirm the existence of the contagion effect, making the

evidence on the financial contagion inconclusive.

The second group of studies (Hamao et al., 1990; Kanas, 1998; Kim et al., 2006; Chiang

et al., 2007; Ng, 2000, Beirne et al., 2008; Frank and Hesse, 2009) utilizes a multivariate

GARCH model to account for heteroscedasticity and the dynamic nature of the correlations.

First of all, Hamao et al. (1990) utilizes the ARCH family of statistical models and report a

price volatility spillover effect among three major international stock markets. In a similar

vein, Kanas (1998), using the EGARCH model, shows reciprocal spillover effects in the

European equity markets, and Ng (2000), using multivariate GARCH model, shows that

Pacific-Basin stock markets are driven by a regional shock from Japan and a global shock

from the US. On the other hand, Connolly et al. (2005) and Kim et al. (2006) investigate the

international stock-bond return relation and report that stock market uncertainty has

important cross-market pricing influences. Furthermore, Chiang et al. (2007) investigate the

financial contagion of Asian markets during the Asian financial crisis using dynamic

correlations analysis and report evidence of contagion in this area. Finally, Frank and Hesse

(2009) use a multivariate GARCH model to investigate the extent of comovements of

OC12062

6

financial variables across markets and report that inter-linkages between funding stress and

equity markets in advanced economies and emerging market financial indicators increase

sharply during specific crisis moments. Our methodology can be classified into this second

group since we use the multivariate GARCH model to estimate dynamic conditional

correlations between the stock returns of the four OECD countries with that of the US.

The third group of studies (Bracker et al., 1999; Johnson and Soenen, 2003; Connoly et

al., 2007; Baele et al., 2009; Norden and Weber, 2009) have tried to find determinants of

stock market comovements. While Bracker et al. (1999) show that measures of bilateral

import dependence and the size deferential across markets are important determinants of

stock market integration, Johnson and Soenen (2003) report that a high share of trade with the

US has a strong positive impact on stock market comovements but that increased bilateral

exchange rate volatility and a higher ratio of stock market capitalization relative to US

contribute to lower comovement in Americas. On the other hand, Connolly et al. (2007) find

that cross-country stock return comovements tend to be stronger following high implied

volatility days. Finally, Norden and Weber (2009) investigate the comovement of credit-

default swap, bond and stock markets during 2000-2002 and they report that stock returns

lead CDS and positive stock returns are associated with negative CDS spread changes. While

the third group of studies identified a number of fundamentals that determine the

comovements of stock markets, they failed to establish a relationship between dynamic

conditional correlations and those fundamentals.

In our analysis of the DCCX-MGARCH model, we simultaneously estimate dynamic

conditional correlations and the impact of exogenous variables over time, which can be used

to identify channels of contagion.

III. The dynamic conditional correlation model

OC12062

7

3.1. The DCC-MGARCH Model

We use the dynamic conditional correlation (DCC) estimator proposed by Engle (2002).

The DCC model is a flexible yet parsimonious parametric model that has been widely

employed.

Let 1, 2,[ ]'t t ty s s= ∆ ∆ be a 2× 1 vector of the log of stock market index (si,t) in a conditional

mean equation. A VAR representation of the conditional mean equation can be written as in

Equation (1):

( ) , (0, ) 1,..... (1),t t t tA L y e where e N H t T= ∀ =�

where ( )A L is a polynomial matrix in the lag operator L and '

1 , 2[ ]t t t

e ε ε= is a vector of

innovations with a conditional variance-covariance matrix { } 1 2.t i tH h i and= ∀ = The

GARCH component of the framework can be rewritten as t t t tH D R D=,

where

, ,( )t i i t

D diag h= ,

and { }t ij tR ρ= is the time-varying correlation matrix containing

conditional correlation coefficients. The elements in tD follow the univariate GARCH (P,

Q) processes in the following manner:

2

, , ,

1 1

1, 2 (2).i iP Q

i t i ip i t p iq i t q

p q

h h iω α ε β− −= =

= + + ∀ =∑ ∑

The second component of the framework consists of a specific DCC(M, N) structure, which

can be expressed as:

( )* 1 * 1 3 ,t t t t

R Q Q Q− −=

where 1 1 1 1

(1 ) ( ' )M N M N

t m n m t m t m n t n

m n m n

Q Q Qα β α ε ε β− − −= = = =

= − − + +∑ ∑ ∑ ∑ ,

Q is the unconditional correlation matrix of ,i tε and ,j tε , *

,{ }t i i

Q diag q= is a 2 2×

diagonal matrix containing the square root of diagonal elements in tQ , and α and β are

OC12062

8

nonnegative scalars that satisfy 1α β+ p .

In this paper, our key element of interest in tR is 1,2, 1,2, 1,1, 2,2,/t t t t

q q qρ = , which

represents the conditional correlation between US stock returns and other OECD countries’

stock returns. The log-likelihood function for this model can be expressed as follows:

2 ' 2 ' 1 '

1 1

[ 1/ 2 ( log(2 ) log )] [ 1/ 2 (log )]T T

t t t t t t t t t t

t t

L n D D R Rπ ε ε ε ε ε ε− −

= =

= − + + + − + +∑ ∑. (4)

Engle (2002) proposes a two-step approach for estimating the DCC model.

3.2. Estimation of the DCC-MGARCH model

3.2.1. Data and summary statistics

We collected daily stock market indices, the TED spread1, the stock market volatility

index (VIX), and stock market capitalization from DataStream. CDS spreads were from

Bloomberg, Inc. To investigate the dynamic correlation coefficient of four OECD countries

during the US financial crisis, our sample covers from the 1st of September 2006 to the 22nd

of July 2010. Table 1 shows the summary statistics for stock market returns of four OECD

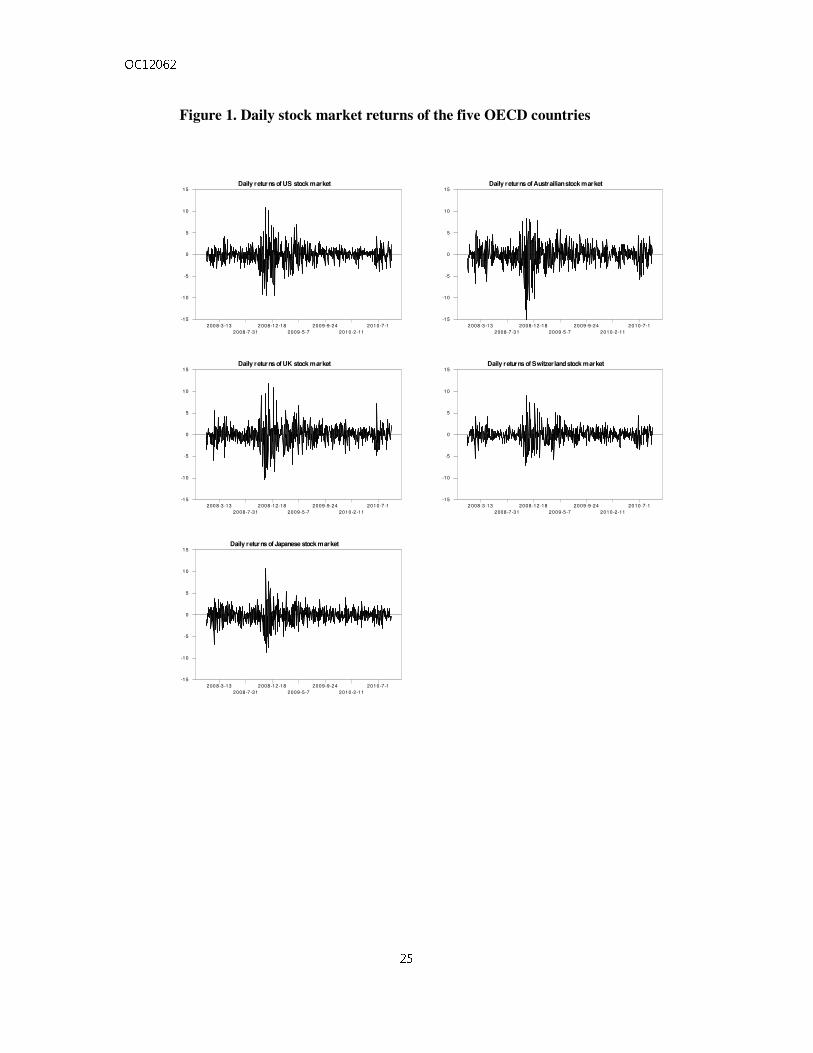

countries, and Figure 1 plots the daily stock return of the five countries.

[Table 1 about here]

From the first panel of Table 1, we can see that the average daily stock market returns

are negative for all the countries for the whole sample period (before the US financial crisis

and thereafter). The UK recorded the largest average negative return (loss) of 0.069% while

Switzerland recorded the smallest average daily loss of 0.0365%. From the JB statistics, we

can reject that all daily return series have normal distributions. In addition to this, ARCH (5)

test statistics reject the null hypnosis of homoscedasticity for all countries, and Ljung-Box Q 1 The data appendix has the detailed definitions and sources of each time series.

OC12062

9

test statistics reject the null hypothesis of no serial correlation for the United Kingdom, Japan,

and Australia.

Figure 1 shows the daily stock market returns of the five OECD countries. From Figure

1,

[Figure 1 about here]

we can see that stock return volatility is highest in Australia (standard error of 2.548) and

lowest in Switzerland (standard error of 1.675) and that all five countries’ stock return

volatility increase significantly after Lehmann Brothers’ failure. Table 2 reports the summary

statistics for the conditional correlation coefficients estimated by DCC-GARCH model

defined in

[Table 2 about here]

Equation (2). From Table 2, we can see that the mean value of DCC is highest in the United

Kingdom (as high as 0.5481) and lowest in Japan (as low as -0.0007).

3.3.2. Estimates of the DCC-GARCH model

Table 3 reports the estimates of the return and conditional variance equations. From

[Table 3 about here]

Table 3, we can see that the AR(1) term in the mean equation is significantly negative for all

five countries, and this is consistent with Antoniou et al. (2005) in terms of the presence of

positive feedback trading in advanced markets. The effects of the US stock returns on OECD

stock returns are highly significant, positive, and consistently large in magnitude, ranging

from 0.371 (Switzerland) to 0.826 (Australia). The coefficients for the lagged variance and

shock-squared terms in the variance equation are significant, and this is consistent with time-

varying volatility and confirms the appropriateness of the GARCH (1,1) specification. Note

OC12062

10

that the sum of the estimated coefficients (a+b) is quite close to unity, implying that the

volatility displays a highly persistent fashion. One advantage of using the model is the fact

that four possible pair-wise correlation coefficients for the five index returns in the sample

can be estimated in a single system equation. From Table 3, we can see that the hypothesis

that all estimated coefficients of the US return ( 2γ) are zero in the mean equation and all

estimated coefficients of the US volatility (b) in the variance equation are zero can be rejected,

and this validates our GARCH (1,1) model specifications.

3.3.3. Estimates of DCC for stock return data

Figure 2 shows estimates of DCC between the stock returns of the US and those of the

United Kingdom, Japan, Australia, and Switzerland during the period of September 2006 -

July 2010. First of all, we can see that DCCs increase sharply after Lehmann Brothers’

failures (third quarter of 2008) and reach their highest level at the end of 2008. Even though

the United Kingdom, Australia, and Switzerland were hit hard, recording large and positive

correlations, the stock returns of Japan show very low correlations with the US before the

crisis (as low as -0.07). After Lehmann Brothers’ failure, the correlations became

significantly higher and persisted at higher levels for the UK, Australia, and Switzerland,

ranging from 0.35 to 0.62. Those estimates of stock return correlations are much higher than

the estimates of Asian markets (Chiang et al., 2007).

However, the correlations of Japan increased as high as 0.217 after the crisis, but

decayed thereafter. Our study provides evidence of contagion 2 effects in OECD stock

markets in the early phase of the recent US financial crisis and then herding behavior in the

latter phase. However, the impact of the US financial crisis has had a limited impact on Japan, 2 Contagion describes the spread of shocks from one market to another with a significant increase in correlations between markets while herding is the simultaneous behavior of investors across different markets with high correlation coefficients in all markets.

OC12062

11

i.e., the US financial crisis has increased the stock return correlations of Japan, but this has

been a temporary impact.

3.3.4. Two phases of the US financial crisis

As shown in Figure 2, the pair-wise conditional correlation coefficients between the stock

returns of OECD countries are persistently higher and more volatile after Lehmann Brothers’

failure (September 15th, 2008). At the same time, it seems clear that conditional correlation

coefficients of Japan returned to the pre-crisis level after almost a year. For this reason, we

want to look into the time series behavior of correlation coefficients and identify the impact

of external shocks on their movements and volatility. We use two dummy variables for

different sub-samples to investigate the dynamic patterns of correlation coefficients.

The model is given as follows:

2

, , , ,

1 1

p

ij t p ij t p k k t ij t

p k

DM eρ φ ρ α−= =

= + +∑ ∑ , (7)

where ,ij tρ is the pair-wise correlation coefficient between the stock returns of the US and

those of the UK, Japan, Australia, and Switzerland. The lag length in Equation (7) is

determined by the AIC criterion. DM1 is a dummy for the first phase of the crisis period

(9/15/2008-9/14/2009), and DM2 is a dummy for the second phase of the crisis period

(9/15/2009-7/21/2010). Since our pre-tests using ARCH-LM statistics (Table 1) find

significant heteroscedasticity in all cases, the conditional variance equation is assumed to

follow a GARCH (1,1) specification with two dummy variables:

,

22

, 0 1 , 1 1 ,

1ij tij t ij t k k t

k

h C A h B e d DM−=

= + + +∑ . (8)

As the model implies, the significance of the estimated coefficients of the dummy variables

OC12062

12

indicates structural changes in the mean and/or variance shifts of the correlation coefficients

due to external shocks during the different phases of the crisis. The maximum likelihood

estimation of Models (7) and (8) are reported in Table 4.

[Table 4 about here]

To verify the validity of our model, we tested whether or not the estimated coefficients of

dummy variables are zero in the mean and variance equations using the likelihood ratio tests,

and we can reject the hypotheses of zero restrictions on dummy variables in the mean and

variance equations. From Table 4, we can see that all estimates of DM1,t and DM2,t in the

mean equation are significant and positive, except for Japan. This implies that the correlation

during the early phase of the crisis is significantly higher than that of the pre-crisis period,

and there are additional increases in correlations during the second phase of the crisis. This

finding is consistent with the comovement paths shown in Figure 2 and support the herding

behavior hypothesis in the early and second phase of the crisis. The herding phenomenon will

nullify the benefit of holding a diversified international portfolio in the region. All of the

lagged variance and shock-squared terms are highly significant, displaying a clustering

phenomenon. From the lower part of Table 4, the coefficients for DM1,t are positive for all

four countries while the coefficients for DM2,t are significant only for the United Kingdom.

This evidence suggests that the correlation coefficients can vary greatly, and this variability

could last for a prolonged period time for the United Kingdom but only a certain period of

time for Australia, Japan, and Switzerland. It is interesting that correlation coefficients for

Japan do not show any structural break during the different phases of crisis, but Japan only

show increased correlation variability during the first phase of the crisis.

IV. Determinants of DCC for stock market returns

4.1. The DCCX-MGARCH Model

OC12062

13

We propose a DCCX-MGARCH type model, where the conditional correlation

coefficient is determined by exogenous variables.

12, 1,1, 2,2,( )t t t th X h hρ=, (5)

where 1 ( ) 1tXρ− p p is a monotonic increasing function of tX , a 1K × vector of

economic fundamental variables that affects the size of the conditional correlation. This

approach is useful for identifying the propagation channel of stock returns comovements. We

propose the following parameterization for such a conditional correlation function:

exp ( ' )( ) 2 1,

1 exp( ' )t

t

t

XX

X

θρ

θ

= −

+ (6)

where 1 2 1 2[ , ,..., ] ' [ , ,...., ] '.k t kand X x x xθ θ θ θ= =

For exogenous variables that are supposed to determine the dynamic conditional

correlations, we include the daily sovereign CDS spread, the VIX index, relative stock market

capitalization to the US, and the TED spread. We include CDS spreads since Jorion and

Zhang (2007) show that credit event information is captured in CDS spread and Bystrom

(2005) and Norden and Weber (2009) find that positive stock returns are negatively

associated with CDS spread changes. The VIX index is included since Giot (2005) showed

that the VIX index and stock return have negative relationship. While Andersson et al. (2007)

suggest that periods of elevated stock market uncertainty lead to decoupling between stock

and bond prices, Cai et al. (2009) show that higher correlations emerge between countries

when both countries experience higher stock market volatility. We include the TED spread

since Brunnermeier (2009) shows that the TED spread provides a useful basis for gauging the

severity of the liquidity crisis. Finally, we include the ratio of stock market capitalization

relative to the US since Johnson and Soenen (2003) show that a higher ratio of stock market

capitalization relative to the US contributes to lower comovement.

OC12062

14

4.3. Estimation

The estimation results for Equation 6 are reported in Table 5. First, it is shown that

increased

[Table 5 about here]

TED spread decreases conditional correlations for all four countries under consideration.

Increased TED spread implies a worsened liquidity situation or “fear” (Lashgari, 2000:

Cheung et al., 2010) in the world capital market, and this, in turn, decreases the comovements

of stock returns among four OECD countries and that of the US. Second, it is shown that the

VIX index of a sovereign country has a significant positive effect on the conditional

correlations for three countries under investigation. This implies that uncertainty in one

countries’ stock market may spread to the US or vice versa. This is consistent with Cai et al.

(2009) and previous estimates of conditional variance function in Table 3. In Table 3, all

estimates of b in variance equations are positive and significant, implying that there are

significant volatility spillover effects in those countries. Third, the estimated coefficient of the

ratio of stock market capitalization to the US is negative and significant for all four countries,

and this finding is consistent with Johnson and Soenen (2003). A higher ratio of stock market

capitalization relative to the US implies a higher level of independence from the US stock

market, and this can decrease the conditional correlations of stock returns.

Finally, increased sovereign risk measured by the CDS spread increases the conditional

correlations for the UK and Australia. This finding is consistent with Bystrom (2005), who

found that an increase in stock price volatility is positively correlated with the CDS spread. In

other words, increased CDS spread increases stock price volatility, and this increased stock

return volatility in the UK and Australia can increase stock return correlations. However,

estimated coefficient of CDS spread for Switzerland has an unexpected negative sign.

OC12062

15

We can see that most of dummy variables are significant in Table 5 (dummy variables

are not included for Switzerland since its CDS spread data does not cover a whole range of

analysis). While dummy variables for both phases are significant and positive for the United

Kingdom and Australia, it is shown that those of Japan are negative and significant only for

the second phase of the crisis.

V. Conclusions

This paper investigated the relationship between the stock returns of four OECD markets

and that of the US. To examine stock market contagion and herding behavior, we employed

dynamic multivariate GARCH model to estimate dynamic conditional correlations using the

daily stock return data for the 2006-2010 period. Based on the estimated dynamic

conditional correlations between four OECD countries and the US, we analyzed the dynamic

behavior of stock market interactions by dividing the whole sample period into three sub-

sample periods (pre-crisis, first phase of the crisis, and second phase of the crisis). During the

first phase of the crisis, we identified a process of increasing correlations and an additional

increase of correlations during the second phase caused by herding behavior in the United

Kingdom, Australia, and Switzerland. However, the impact of the US financial crisis on

Japan was limited to the increase in correlation volatilities in the first phase, and this

disappeared during the second phase of the crisis, leaving the correlations of the Japan pre-

crisis level. Finally, we proposed a new approach that allows simultaneous estimation of the

conditional correlation coefficients and determinants of conditional correlations over time

and that can be used to identify channels of contagion. It is shown that an increase in the VIX

stock market index increases conditional correlations while increases in TED spreads and

relative stock market capitalization decrease the conditional correlations of the four OECD

countries with the US.

OC12062

16

References

Andersson, M., Krylova, E., Vahamaa, S., 2007. "Why does the correlation between stock

and bond returns vary over time?" Applied Financial Economics 18(2), 139-151.

Antoniou, A., Koutmos, G., Pericli, A., 2005. "Index futures and positive feedback trading:

Evidence from major stock exchanges." Journal of Empirical Finance 12, 219-238.

Baig, T., Goldfajn, I., 1999. "Financial market contagion in the asian crisis." IMF Staff Papers,

46, 167-195.

Basu, R., 2002. "Financial contagion and investor "learning": An empirical investigation."

IMF Working Paper 1-36.

Beirne, J., Caporale, G.M., Schulze-Ghattas, M., Spagnolo, N., 2009. "Volatility spillovers

and contagion from mature to emerging stock markets." Brunel University Working

Paper No.09-05.

Boyson, N.M., Stahel, C.W., Stulz, R.M., 2010. "Hedge fund contagion and liquidity shocks."

Journal of Finance, 65, 1789-1816.

Bracker, K., Docking, D.S., Koch, P.D., 1999. "Economic determinants of evolution in

international stock market integration." Journal of Empirical Finance, 6, 1-27.

Brunnermeier, M.K., Pedersen, L.H., 2009. "Market liquidity and funding liquidity." Review

of Financial Studies, 22, 2201-2238.

Bystrom, H., 2005. "Credit default swapss and equity prices: The itraxx cds market index."

Financial Analysts Journal, 62, 65-76.

Cai, Y., Chou, R., Li, D., "Explaining international stock correlations with CPI fluctuations

and market volatility." Journal of Banking and Finance, 2009, 33, 2026-2035.

Calvo, S., Reihart, C., 1996, "Capital flows to Latin America: Is there evidence of contagion

effect?" In. Calvo, G., Goldstein, M., Hochreiter, E., esd. Private capital flows to

emerging markets after the Mexican Crisis, Institute of International Economics.

Cheung, W., Fung, S., Tsai, S.C., 2010. "Global capital market interdependence and spillover

effect of credit risk: Evidence from the 2007-2009 global financial crisis." Applied

Financial Economics, 20, 85-103.

Chiang, T.C., Jeon, B.N., Li, H.M., 2007. "Dynamic correlation analysis of financial

contagion: Evidence from asian markets." Journal of International Money and Finance,

26, 1206-1228.

Chudick, A., Fratzscher, M., 2011, "Identifying the global transmission of the 2007-2009

OC12062

17

fiancial crisis in a GVAR model." European Economic Review, 55, 325-339.

Christiasen, C., Ranaldo, A., Soderlind, P., 2011. "The time-varying systematic risk of carry

trade strategies." Journal of Financial and Quantitative Analysis, forthcoming.

Connolly, R., Stivers, C., Sun, L.C., 2005. "Stock market uncertainty and the stock-bond

return relation." Journal of Financial and Quantitative Analysis, 40, 161-194.

Connolly, R.A., Stivers, C., Sun, L.C., 2007. "Commonality in the time-variation of stock-

stock and stock-bond return comovements." Journal of Financial Markets, 10, 192-

218.

Corsetti, G., Pericoli, M., Sbracia, M., 2005. "'Some contagion, some interdependence: More

pitfalls in tests of financial contagion." Journal of International Money and Finance,

24, 1177-1199.

Dooley, M and Hutchison, M., 2009, "Transmission of the US Subprime crisis to emerging

markets: Evidence on the decoupling o-recoupling hypothesis," Journal of

International Money and Finance, 28, 1331-1349.

Engle, R., 2002. "Dynamic conditional correlation." Journal of Business and Economic

Statistics, 20, 339-350.

Forbes, K.J., Rigobon, R., 2002. "No contagion, only interdependence: Measuring stock

market comovements." Journal of Finance, 57, 2223-2261.

Frank, N., Hesse, H., 2009. "Financial spillovers to emerging markets during the global

financial crisis. Finance a Uver-Czech." Journal of Economics and Finance, 59, 507-

521.

Froot, K., O'Connell, P., Seasholes, M.,2001. "The portfolio flows of international invesotrs,

Journal of Financial economics." 59, 151-193.

Giot, P., 2005. "Relationships between implied volatility indexes and stock index returns - are

implied volatility indexes leading indicators?" Journal of Portfolio Management, 31,

92-100.

Hamao, Y., Masulis, R.W., Ng, V., 1990. "Correlations in price changes and volatility across

international stock markets." Review of Financial Studies, 3, 281-307.

Johnson, R., Soenen, L., 2003. "Economic integration and stock market comovement in the

americas." Journal of Multinational Financial Management, 13, 85-100.

Jorion, P., Zhang, G.Y., 2007. "Good and bad credit contagion: Evidence from credit default

swaps." Journal of Financial Economics, 84, 860-883.

OC12062

18

Kanas, A., 1998. "Volatility spillovers across equity markets: European evidence." Applied

Financial Economics, 8, 245-256.

Kim, S., Moshirian, F., Wu, E., 2006, "Evolution of international stock and bond market

integration:Influence of the European Monetary Union." Journal of Banking and

Finance, 30, 1507-1534.

Kim, H., Kim, B., 2010. "Spillover effects of the US financial crisis on financial markets in

emerging Asian countries." Auburn Economics Working Paper Series, 1-39.

King, M., Wadhwani, S., 1990. "Transmission of volatility between stock markets." Review

of Financial Studies, 3, 5-33.

Lashgari, M., 2000. "The role of ted spread and confidence index in explaining behavior of

stock prices." American Business Review, 18(2), 9-11.

Lee, S., Kim, K., 1993. "Does the october 1987 crash strengthen the co-movements among

national stock markets?" Review of Financial Economics, 3, 89-102.

Ng, A., 2000. "Volatility spillover effects from japan and the us to the pacific-basin." Journal

of International Money and Finance, 19, 207-233.

Norden, L., Weber, M., 2009. "The co-movement of credit default swap, bond and stock

markets: An empirical analysis." European Financial Management, 15, 529-562.

OC12062

19

Data Appendix

Stock Index

Item Description Datastream Code

US Index S&P 500 Composit S&PCOMP(PI) UK Index UK-DS Market TOTMUK$(PI) Swiss Index Swiss-DS Market TOTMKSW(PI) Australia Index Australia-DS Market TOTMAU$(PI) Japan Index Japan-DS Market TOTMJP$(PI)

Volatility Index

Item Description Bloomberg Source

US Volatility Index for S&P 500 VIX UK Volatility Index for FTSE 100 VFTSE Swiss Volatility Index for SMI VSMI Australia Volatility Index for S&P/ASX SPAVIX Japan Volatility Index for Nikkei225 VXJ

TED Spread

Item Description Datastream Code

TED US LIBOR – US Treasury Bill 3M BOELI3M – FRTBS3M TED UK LIBOR – UK Interbank 3M BOELI3M – LDNIB3M TED Swiss LIBOR – Swiss Interbank 3M BOELI3M – SWIBK3M TED Australia LIBOR – Australian Deposit 3M BOELI3M – GSAUD3M TED Japan LIBOR – Japan Interbank 3M BOELI3M – JPIBO3M

CDS Spread

Item Description Bloomberg Source

CDS US US CDS Spread CMA New York CDS UK UK CDS Spread CMA New York CDS Swiss Swiss CDS Spread CMA New York CDS Australia Australia CDS Spread CMA New York CDS Japan Japan CDS Spread CMA New York

OC12062

20

Table 1. Descriptive statistics for stock market returns (2006/09/01-2010/07/21)

A.Entire Period

US UK Japan Australia Switzerland

Daily stock market returns ( ,i ts∆ ) Mean -0.0441 -0.069 -0.0559 -0.0584 -0.0365

Std. Error 1.9838 2.2531 1.7939 2.5481 1.6751

Normality Test

Skewness -0.1375 0.0205 -0.0074 -0.821** 0.173**

Kurtosis 5.336** 4.616** 3.8664** 4.8765** 3.715**

JB statistic 811.53** 605.68** 424.82** 752.34** 6982.6**

Heteroscedasticity test

ARCH(5) LM test

161.29** 191.393** 116.792** 307.490** 120.752**

Autocorrelations test Ljung-Box Q 68.53** 52.620** 55.611** 23.219 65.720**

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) at 5% critical level respectively.

B.Pre-Crisis Period

US UK Japan Australia Switzerland

Daily stock market returns ( ,i ts∆ ) Mean -0.0167 -0.03478 -0.0424 0.005498 -0.003388

Std. Error 1.0874 1.3116 1.3115 1.6685 0.9917

Normality Test

Skewness -0.382** -0.1804 -0.347** -0.377** -0.221*

Kurtosis 2.0656** 2.2960 ** 1.801** 2.243** 3.117**

Jarque-Bera 107.510** 119.739** 82.563** 124.108** 219.687**

Heteroscedasticity test

ARCH(5) LM test

7.39** 14.92** 14.09** 19.80** 12.69**

Autocorrelations test Ljung-Box Q 37.05* 30.16 37.28* 10.59 22.90

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) at 5% critical level respectively.

C.Post-Crisis Period

US UK Japan Australia Switzerland

Daily stock market returns ( ,i ts∆ ) Mean -0.01795 -0.02381 -0.02948 -0.000634 -0.0070

Std. Error 2.1920 2.4634 1.8482 2.7278 1.8272

Normality Test

Skewness -0.153 -0.0269 0.050 -0.973** 10.149

Kurtosis 4.696** 4.200** 4.649** 5.098** 3.242**

Jarque-Bera statistic

445.775** 335.135** 435.143** 599.137** 213.303**

Heteroscedasticity test

ARCH(5) LM test

24.71** 26.33** 39.58** 50.96** 20.47**

Autocorrelations test Ljung-Box Q 44.00** 43.41** 42.28** 20.98 55.92**

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) at 5% critical level respectively.

OC12062

21

Table 2: Summary statistics of estimated DCCs of 5 OECD countries: Equation (5)

, ,

, ,

, , , ,

i j t

i j t

i i t j j t

q

q qρ =

Entire Period US-UK US-Japan US-Australia US-Switzerland

Mean 0.5481 -0.0007 0.2707 0.4813

Std. Error 0.0259 0.0369 0.0368 0.0383

Skewness 1.0437 ** 2.174 ** 0.6241 ** 1.8894 **

Kurtosis 2.5225 ** 5.6123 ** 0.3809 ** 4.7100 **

Jarque-Bera statistic 304.65 ** 1432.31 ** 48.4007 ** 1036.197 **

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) denote significance at 5% critical level.

Pre-Crisis Period

US-UK US-Japan US-Australia US-Switzerland

Mean 0.5298 -0.02491 0.2260 0.4605

Std. Error 0.01618 0.02469 0.02162 0.01815

Skewness -1.6699** 0.4548** -0.1471 -0.6070**

Kurtosis 4.9780** 3.6973** 0.8967** 0.4881*

Jarque-Bera statistic 796.5491** 227.2236** 19.7411** 37.9653**

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) denote significance at 5% critical level.

Post-Crisis Period

US-UK US-Japan US-Australia US-Switzerland

Mean 0.5638 -0.004604 0.2848 0.4981

Std. Error 0.02990 0.05496 0.04221 0.04897

Skewness 1.2510** 1.7403** 0.7839** 1.3541**

Kurtosis 2.2670** 3.0890** -0.08467 2.9252**

Jarque-Bera statistic 229.4058** 435.8264** 49.6082** 319.8108**

Note: Double asterisks (**) denote significance at 1% critical level and single asterisk (*) denote significance at 5% critical level.

OC12062

22

Table 3: Estimation results from the DCC-GARCH model (2006/09/01-2010/07/21)

UK Japan Australia Switzerland US

Return equation: , ,0 ,1 , 1 2 , 1 ,i t i i i t US t i ts s sγ γ γ ε− −∆ = + ∆ + ∆ +

0γ 0.077* (0.037) -.0001* (0.029) 0.128* (0.037) 0.070* (0.037) 0.072* (0.037)

1γ -0.230* (0.020) -0.134* (0.021) -0.157* (0.021) -.197* (0.019) -.089* (0.031)

2γ 0.497* (0.033) 0.462* (0.025) 0.826* (0.035) 0.371* (0.022) -- --

Variance equation: , 1

2

, , 1 i tij t i i ij t ih c a h b ε−−= + +

c 0.029** (0.006) 0.046* (0.014) 0.137* (0.044) 0.096* (0.022) 0.022** (0.005)

a

0.929** (0.001 0.891* (0.014) 0.843* (0.019) 0.927* (0.010) 0.899* (0.012)

b

0.063** (0.007) 0.087* (0.011) 0.139* (0.019) 0.063* (0.011) 0.093* (0.011)

-Log Likelihood 7454.53

LR-test ( 2 0γ = for all countries) Chi-squared (4) = 708.94***

LR-test (b = 0 for all countries) Chi-squared (5) = 36935.3***

LR-test (b = 2 0γ = for all countries) Chi-squared (9) = 40849.54***

Notes: Values in parentheses are standard errors. Double asterisks (**) and single asterisk (*) indicate significance at the 1% and 5% critical levels, respectively.

OC12062

23

Table 4: Test of changes in DCC during different phases of US financial crisis

UK Japan Australia Switzerland

Mean equation: 2

, , , ,

1 1

p

ij t p ij t p k k t ij t

p k

DM eρ φ ρ α−= =

= + +∑ ∑

Con. 0.071** (.0001) -0.002** (.0003) .0121** (.0001) 0.0313** (0.001)

1tρ − 0.869** (.0002) 0.908** (.0104) 0.946** (.0007) 0.932** (.0005)

DM1,t 0.005** (.0005) 0.0004 (.0009) 0.004** (.0009) 0.0002* (.0009)

DM2,t 0.001** (.0004) 0.0004 (.0006) 0.001** (.0001) .0012** (.0005)

-----------------------------------------------------------------------------------------------------------------

Variance equation: ,

22

, 0 1 , 1 1 ,

1ij tij t ij t k k t

k

h C A h B e d DM−=

= + + +∑

___________________________________________________________________________

0C 1.34e-6** (2.24e-7) 2.22e-6**

4.76e-7 1.12e-6**

3.26e-7 4.77e-6**

5.69e-7

1th − 0.679** (0.018) .824** (.010) 0.783** (0.008) 0.734** (0.019)

2

1tε − 0.377** (0.022) .182** (0.013) 0.287** (0.003) 0.210** (0.025)

DM1,t 9.88e-6** (3.36e-6) 1.2e-5**

(1.7e-6) 1.18e-5**

(3.6e-6) 2.68e-5**

(6.6e-6)

DM2,t 4.16e-6** (1.18e-6) 1.16e-6 (9.83e-7)

-3.78e-7 (4.81e-7)

1.54e-7 (8.55e-7)

LR test H0 : DM1=DM2=0 in mean equation, Chi-squared (8)=71.71*** H0 : DM1=DM2=0 in variance equation, Chi-squared (8)=19019782.54*** H0 : DM1=DM2=0 in mean and variance equation, Chi-squared (16)=43866124.01***

Notes: Values in parentheses are standard errors. Double asterisks (**) and single asterisk (*) indicate significance at the 1% and 5% critical levels, respectively.

OC12062

24

Table 5: Estimation of DCCX

0 1 2 3 4

exp ( ' )( ) 2 1, [ , , , , ] '

1 exp ( ' )t

t

t

XX

X

θρ θ θ θ θ θ θ

θ

= − =

+

UK Japan Australia Switzerland

Coef. S.E. Coef. S.E. Coef. S.E. Coef. S.E.

0θ 1.298** (.087) 0.131** (0.044) 0.027 (0.079) 1.211** (0.028)

1θ 0.004** (.0001) 0.0004 (.0001) 0.0015** (.0002) -.0001 (.0008)

2θ -.037** (0.005) -0.019** (0.003) -0.141** (0.009) 1.992** (0.668)

3θ -0.829* (0.333) -.3633* (0.161) -0.351 (0.765) -.012 (0.009)

4θ 0.005** (.0006) 0.0028** (.0003) 0.0012* (.0006) 0.004** (.0006)

DM1 0.268** (.0006) -0.012 (0.012) 0.437** (0.017) --3 --

DM2 0.306** (0.019) -0.135** (0.015) 0.317** (0.022) --3 --

Log Likelihood 923.12 1018.62 597.11 600.01

Notes: 1. Values in parentheses are standard errors. Double asterisks (**) and single asterisk (*) indicate significance at the 1% and 5% critical levels, respectively. 2. X0 is a constant, X1 is the CDS spread, X2 is the TED spread, X3 is the relative stock market capitalization of four OECD countries relative to US and X4 is the VIX index for stock market. 3. Switzerland does not have sufficient observations of CDS spread data to utilize dummy variables.

OC12062

25

Figure 1. Daily stock market returns of the five OECD countries

Daily returns of US stock market

200 8-3-13

2008-7-31

2 008-12-18

2009-5-7

2009-9-24

2010-2-11

2010-7-1

-15

-10

-5

0

5

10

15

Daily returns of UK stock market

200 8-3-13

2008-7-31

2 008-12-18

2009-5-7

2009-9-24

2010-2-11

2010-7-1

-15

-10

-5

0

5

10

15

Daily returns of Japanese stock market

200 8-3-13

2008-7-31

2 008-12-18

2009-5-7

2009-9-24

2010-2-11

2010-7-1

-15

-10

-5

0

5

10

15

Daily returns of Austrailian stock market

2 008-3-13

2008-7-31

2008-12-18

2009-5-7

2009-9-24

2010-2-11

2010-7-1

-15

-10

-5

0

5

10

15

Daily returns of Switzerland stock market

2 008-3-13

2008-7-31

2008-12-18

2009-5-7

2009-9-24

2010-2-11

2010-7-1

-15

-10

-5

0

5

10

15

OC12062

26

Figure 2. Estimates of DCCs among US and four OECD countries

DCC of US with OECD countries

2008-3-13 2008-7-31 2008-12-18 2009-5-7 2009-9-24 2010-2-11 2010-7-1

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

USUK

USJP

USAT

USSW